TeamLease Services: India's Labor Arbitrage Platform & The Quest for Margins

I. Introduction & Episode Roadmap

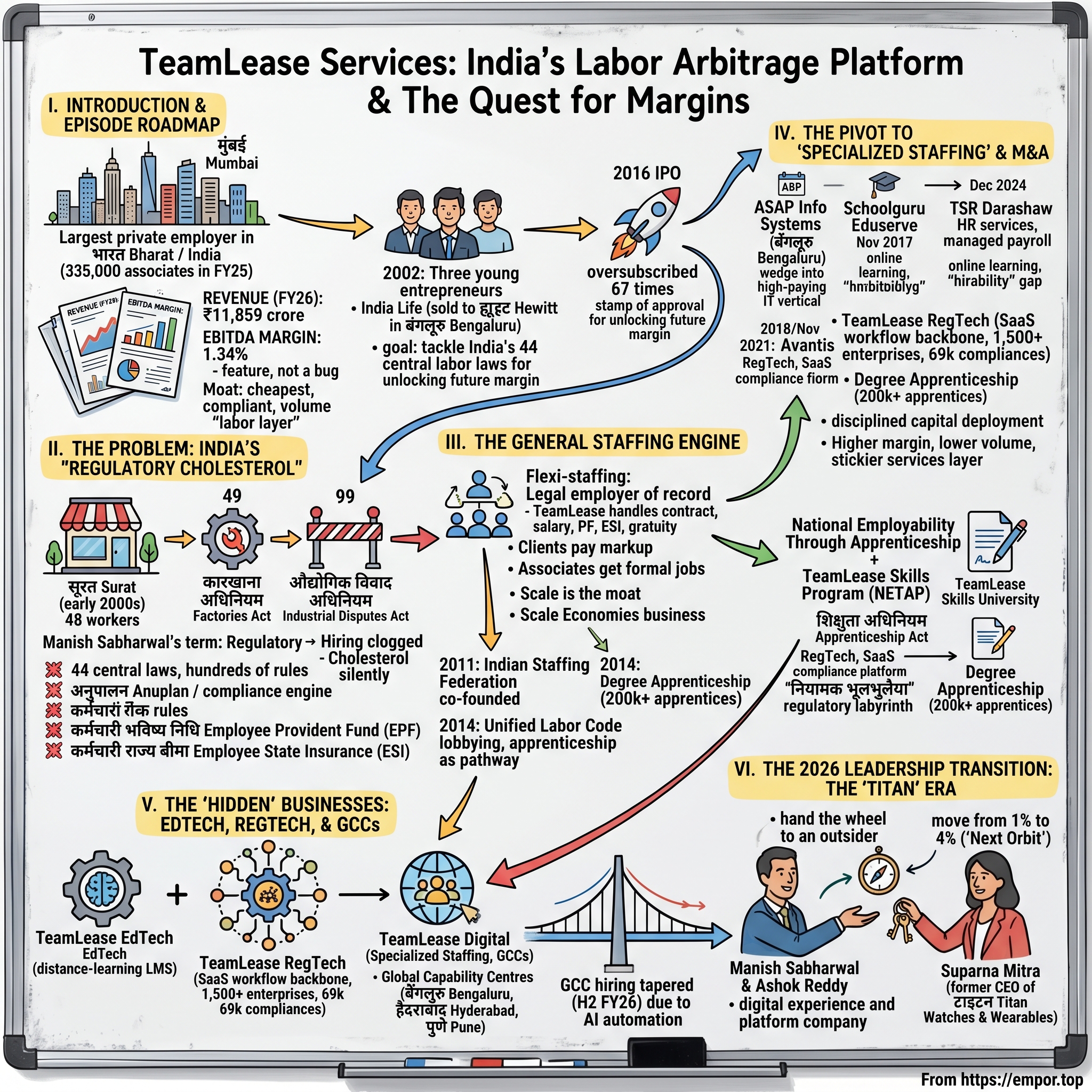

There is a quiet, almost invisible joke that runs through the financial press in मुंबई Mumbai: TeamLease Services Limited is the largest private-sector employer in भारत Bharat / India that almost nobody outside of HR circles has ever heard of. Walk into a Reliance Retail store, a Bajaj Allianz back office, an Amazon fulfilment centre, or the warehouse of a quick-commerce darling, and there is a non-trivial probability that the person scanning the barcode, ringing the till or driving the forklift is on TeamLease's payroll—not the brand-name company's. By the end of FY2025, the company carried roughly 335,000 associates on its books1, which would make it more populous than the city of पणजी Panaji, the capital of गोवा Goa. If "headcount carried" were a stock-market metric, TeamLease would be a mega-cap.

And yet, walk through the income statement, and the most striking number is the one you don't see: margin. For the full year FY2026, the company reported revenue of roughly ₹11,859 crore and EBITDA of ₹158 crore—an EBITDA margin of 1.34%2. One-point-three-four percent. Most listed Indian companies bin a press release that thin. TeamLease sells it as a feature. Because that is the whole game: in a country where formal employment has been a structural blind spot for two generations, being the cheapest, most compliant, highest-volume "labour layer" between the employer and the worker is the moat. The arithmetic is brutal, but the customer can never replicate it in-house.

This is the story of how three young entrepreneurs, fresh from selling an HR outsourcing business to ह्यूइट Hewitt Associates in बंगलूरु Bengaluru, looked at India's tangle of 44 central labour laws, hundreds of state rules and an informal-sector economy that absorbed eight of every ten workers, and decided to build a अनुपालन Anuplan / compliance engine the size of a small army. It is the story of the 2016 IPO that the market oversubscribed 67 times3—a stamp of approval not for the margin, but for what the margin would unlock. It is the story of careful, almost stingy capital allocation through ASAP Info Systems, Schoolguru, Avantis and TSR Darashaw—each tuck-in benchmarked against the parent business and squeezed for what little EBITDA juice the market would allow. And it is the story of February 2026, when the founders—Manish Sabharwal and Ashok Reddy—did something rare in Indian mid-cap promoter families: they handed the wheel to an outsider, सुपर्णा मित्रा Suparna Mitra, the former CEO of टाइटन Titan Watches & Wearables, and told her to "move from 1% to 4%."4

Over the next two hours, we will dig into how a company that begins each fiscal year owing wages to a third of a small city manages to also run a SaaS compliance platform serving over 1,500 enterprises, an EdTech subsidiary running degree-apprenticeship programs with universities, and a Specialized Staffing arm now leveraged to the Global Capability Centre boom that has put Bengaluru, हैदराबाद Hyderabad and पुणे Pune on the global engineering map. We will war-game it against क्वेस Quess Corp, hold its margins up against Adecco and Randstad, and try to understand what exactly the new CEO has been hired to do. Because the bull case and the bear case both hinge on one thing: whether TeamLease can finally, after twenty-four years, escape the gravity of two percent.

II. The Problem: India's "Regulatory Cholesterol"

To understand TeamLease, you first have to understand the problem the founders looked at in 2002 and decided was an opportunity rather than a deterrent. Picture a small-business owner in सूरत Surat in the early 2000s. She runs a textile workshop with forty-eight workers. If she hires the forty-ninth, the कारखाना अधिनियम Factories Act kicks in. If she hires the ninety-ninth, the औद्योगिक विवाद अधिनियम Industrial Disputes Act makes it nearly impossible to ever lay anyone off without state government permission. Each new employee triggers obligations under the कर्मचारी भविष्य निधि Employee Provident Fund (EPF) Act of 1952, the कर्मचारी राज्य बीमा Employee State Insurance (ESI) Act of 1948, the Payment of Gratuity Act, the Payment of Bonus Act, the Minimum Wages Act—each with its own returns, registers, inspections and pre-2016 paper-based interface with a different government department. Manish Sabharwal had a name for this stack: "regulatory cholesterol." It clogged hiring the way actual cholesterol clogs arteries—silently, expensively, and almost always until something burst.

The thesis that animated TeamLease was a contrarian one. The dominant narrative in India in the early 2000s was that the country had a "jobs problem." Sabharwal argued, in interview after interview and op-ed after op-ed, that India did not have a jobs problem—it had a wages problem, a productivity problem, and above all a formalization problem. Nine out of ten workers in India were in the informal sector with no PF, no ESI, no written contract, no recourse. The plumbing that connected an employer who wanted to hire with a worker who wanted to be hired was broken. A company that could rebuild that plumbing—legally, at scale, with margin-thin honesty—would own one of the largest infrastructure businesses in the country.

Before TeamLease there was India Life. Sabharwal, Ashok Reddy and a small team founded the HR outsourcing business in the late 1990s and sold it to Hewitt Associates in 2002, with Sabharwal staying on for two years as CEO of Hewitt Outsourcing (Asia) out of Singapore5. When the non-poach window expired, twenty-seven people from the old India Life team walked back across the line, joining Sabharwal and Reddy to start TeamLease in Bengaluru. Mohit Gupta rounded out the founding trio. The team had institutional muscle memory of payroll, compliance and back-office HR built up over six years, but no longer the encumbrance of the Hewitt mothership pulling them toward enterprise consulting.

The vehicle they chose was deceptively simple: temporary staffing, or "flexi-staffing" as the industry would come to call it. TeamLease would be the legal employer of record. The associate would physically work at a client site—a bank branch, a retail store, a factory—but the contract, the salary, the PF deposit, the ESI contribution, the gratuity accrual, the tax deduction, the bonus calculation, all of it ran through TeamLease's systems. The client paid a markup over the cost-to-company. For the client, the headache went away. For the associate, in many cases, a formal job with statutory benefits appeared where none had existed. For TeamLease, the markup was painfully thin, but the volumes—if the model worked—would be enormous.

It was an unsexy business with one beautiful property: the more associates you carried, the more you spread the fixed cost of your compliance back-office across, and the cheaper your per-associate cost became. Scale was the moat, but scale could only be earned the hard way—one client logo, one statutory filing, one state-level inspector at a time. The roadmap from "small Bengaluru outsourcing shop" to the largest private employer in the country would have to run through the bureaucracy itself.

III. The General Staffing Engine

By the early 2010s, the staffing engine had begun to hum. The model was clear to anyone who cared to look: a roughly 1.5–2.0% EBITDA margin on associate revenue, but with associate counts growing at double digits and a back office whose marginal cost of onboarding the next associate trended toward zero. It was an extreme version of a scale-economies business—closer in spirit to a logistics operator like a third-party courier than to a traditional services firm. Each new client wasn't a fresh consulting engagement; it was a recurring annuity that grew with the client's own headcount expansion.

A defining moment came in 2011, when TeamLease helped co-found the Indian Staffing Federation. On paper, an industry body. In practice, a political project. India's labour laws had been written for a 1950s economy of permanent factory employment; the staffing industry was treated, at best, as a tolerated workaround and, at worst, as something to be regulated out of existence. By 2014, the staffing federation, with TeamLease as one of its loudest voices, was pressing the Modi government for a unified labour code, recognition of the apprenticeship as a legitimate first-job pathway, and an end to the patchwork of state-level rules that made hiring across state borders a paperwork nightmare. The lobbying was patient, often unglamorous, but it materially shaped the way the four labour codes—on wages, industrial relations, social security and occupational safety—were eventually drafted later that decade.

Then came February 2016. TeamLease went public with an issue priced in a band of ₹785–₹850 per share, raising roughly ₹423 crore3. The book was oversubscribed 67 times—the second-highest oversubscription for any IPO in India in the eight years prior6. Goldman Sachs and Merrill Lynch were among the anchor investors. The market was not, fundamentally, paying for the 1.7% EBITDA margin it could see. It was paying for the unit it could not yet quantify: the long-tail formalization of the Indian labour force, supercharged in the following years by the Goods and Services Tax rollout in 2017 and demonetisation in late 2016, both of which forced thousands of mid-sized businesses out of the cash-based informal economy and into the GST-compliant, payroll-on-the-books world that TeamLease was designed to serve. For every small enterprise that had to suddenly produce a digital invoice trail, the staffing-as-a-service model became cheaper than building an in-house HR department from scratch.

The sleeper inside General Staffing was the National Employability Through Apprenticeship Program—NETAP. Launched in 2014 as a public–private partnership with the Ministry of Skill Development, the All India Council for Technical Education, the National Skill Development Corporation and TeamLease Skills University, NETAP rode on top of the rejuvenated शिक्षुता अधिनियम Apprenticeship Act[^7]. The trick was elegant. Under the Apprenticeship Act as amended, a trainee was not an "employee" in the strict sense, which meant a different—and lighter—compliance footprint, while still receiving a stipend at or above minimum wage and access to a structured 200-hour soft-skills, English and computer module. For employers, the apprenticeship slot was a low-friction way to test and convert young workers; for TeamLease, it was a parallel pipeline of associates that could be plugged into the same back-office. By the early 2020s, the program—since rebranded as TeamLease Degree Apprenticeship—had enrolled more than 200,000 apprentices across 700-plus employers, 40 sectors and 150 job roles[^7], building what was effectively the world's largest privately-run apprenticeship platform.

By FY2025, General Staffing had become a different kind of beast: in a year when staffing margins everywhere in the world were getting compressed by wage inflation, TeamLease still added roughly 25,000 net associates in general staffing despite second-half headwinds in certain sectors7. The dot was clear. General Staffing was the chassis. The engine the founders wanted to bolt onto it, however, was somewhere else entirely.

IV. The Pivot to "Specialized Staffing" & M&A

If General Staffing was the volume play, Specialized Staffing was always meant to be the margin play—and the way TeamLease got there reads like a master class in disciplined capital deployment. The first move came in July 2016, just five months after the IPO, when TeamLease's wholly owned subsidiary signed a definitive agreement to acquire बेंगलूरु Bengaluru-based ASAP Info Systems for approximately ₹67 crore8. ASAP had around 1,000 IT-staffing associates and 171 core employees serving multinational and domestic IT clients, with annual sales of roughly ₹63 crore. The economics were striking: roughly 1.1x revenue, a multiple any reasonable financial buyer would have killed for in a sector starting to wake up to India's IT services boom. Almost simultaneously, the company picked up Nichepro, a similar specialised IT staffing player.

The strategic logic was the Trojan horse. TeamLease had spent a decade-and-a-half placing security guards, retail associates and warehouse workers into India's largest IT services companies and multinationals; the same procurement teams that signed off on a thousand admin staff would happily sign off on a hundred Python developers if the same vendor could do the contracting, payroll and compliance. ASAP was the wedge into the highest-paying labour vertical in India. Within a few years, the unit—rebranded TeamLease Digital—would become the home of TeamLease's Specialized Staffing business and the platform onto which the GCC story would later be loaded.

A year later, in November 2017, came the second tuck-in: a 40% stake in Schoolguru Eduserve, an online learning company that worked with eighteen universities, for ₹13.53 crore9. This was a stranger, more long-horizon bet. Schoolguru was not a staffing business at all; it was an academic services player providing the technology backbone for university distance-learning programs. The thesis, as the founders explained at the time, was that India's "hireability" gap—the canyon between freshly graduated CVs and what employers actually wanted—was a structural drag on the entire staffing market. If TeamLease could plug a degree-issuing university into a TeamLease-built work-integrated curriculum, sit an apprentice in a TeamLease-staffed factory, and graduate them three years later with both a degree and a job, the company would own the entire ramp from school to formal employment. Crucially, they did not overpay. Forty percent of a then-tiny EdTech business for ₹13 crore was a startup-style call option, sized so it would not move the consolidated needle if it failed. It didn't. By September 2020, TeamLease was confident enough to pick up an additional 37.14% for ₹43.4 million, taking the holding past 78%10.

Then came the SaaS bet. Avantis, founded in 2015 to digitise India's mountain of अनुपालन Anuplan / compliance paperwork, took TeamLease as a strategic and equity partner in 2018. In November 2021, TeamLease topped up its stake to 61.5% and rebranded the unit TeamLease RegTech11. The numbers attached to the platform were arresting on their own: 1,500-plus legal entities, more than 69,000 compliances tracked, 6,700-plus filings, 3,500-plus annual regulatory changes monitored. This was India's नियामक भूलभुलैया regulatory labyrinth, but as a software product. Crucially, it was sold in two flavours: do-it-yourself for in-house corporate compliance teams, and do-it-for-me for the chartered accountants, company secretaries and labour consultants who serviced the long tail of mid-sized clients. For a company whose core business carried 2% margins, RegTech was the first glimpse of what SaaS-style retention and gross margins might do to the consolidated picture.

The most aggressive—and most debated—deployment came right at the end of 2024. On December 20, 2024, TeamLease signed a share purchase agreement to acquire a 90% stake in TSR Darashaw, a venerable HR services and payroll-processing house, for approximately ₹17.6 crore, with the remaining 10% to follow12. TSR Darashaw, with revenue of around ₹9.22 crore in FY2024 and a managed-payroll base of 165,000 employees, came in at roughly 1.9x revenue. That looked rich next to ASAP's 1.1x in 2016, but the underlying business was structurally different: payroll-as-a-service is a recurring, sticky engagement closer in spirit to a B2B SaaS contract than to a transactional staffing relationship. The bull case for the deal was straightforward arithmetic—payroll processing earns 17–20% PBT margins versus the 2% the parent earns on associate revenue, and once a 50,000-employee enterprise integrates TSR Darashaw into its monthly cut-over, switching vendors is a procurement project nobody wants to own. The bear case was that, at 1.9x revenue for a small business, TeamLease was paying a SaaS multiple for a service offering whose tech-platform leverage still had to be proved. Watch the gross margin trajectory of the HR services segment over the next eight quarters; that is where this debate gets settled.

Each of these four acquisitions—ASAP, Schoolguru, Avantis and TSR Darashaw—was small relative to the consolidated balance sheet. None of them turned TeamLease into an M&A roll-up story. But cumulatively, they built the second pillar of the business: the higher-margin, lower-volume, stickier services layer that sat on top of the staffing chassis. Which brings us to the businesses most public investors still under-appreciate.

V. The "Hidden" Businesses: EdTech, RegTech, and GCCs

Walk into the offices of any large Indian university running a distance-learning MBA in 2026, and there is a reasonable chance the learning management system, the proctoring engine, the analytics dashboard and the back-office academic services are being delivered by what used to be called Schoolguru—now wrapped inside TeamLease EdTech. The business has quietly grown into one of the country's larger work-integrated learning platforms, and it solves a problem the founders have been talking about for two decades: the "hirability" gap. An employer can pay TeamLease to place a fresher; that fresher can simultaneously be enrolled in a TeamLease EdTech degree-apprenticeship program running on Schoolguru's stack at a partner university. The dot-connecting between staffing, apprenticeship and EdTech is the closest thing in the industry to a true "human capital supply chain." For investors, the metric to watch is not the EdTech segment's standalone revenue line—it is the conversion rate of EdTech learners into TeamLease-placed apprentices and full-time hires, because that is the proof that the cross-sell is real and not just a PowerPoint synergy.

TeamLease RegTech is the businesses' SaaS conscience. The platform is now the workflow backbone for the in-house compliance teams of more than 1,500 enterprises across 45 industries11, tracking the stock-and-flow of Indian employer obligations as they mutate with each state-level amendment and central notification. In a country where the केंद्रीय बजट Union Budget and every state budget add to the regulatory backlog every February, having a software vendor monitor the changes on your behalf turns from a "nice-to-have" to a "cannot-live-without" within roughly three audit cycles. That is what high switching costs look like in regulated services. For management, the temptation must be considerable to break this out as a standalone listed entity—the SaaS multiples available in Indian public markets in 2026 would, in theory, surface value that the consolidated 2% EBITDA margin currently buries. The company has so far resisted the urge, perhaps for the simple reason that the cross-sell between RegTech and the staffing customer base is most valuable when the two live inside the same income statement.

The third hidden engine is the Global Capability Centres boom, and it has rerated the case for Specialized Staffing inside TeamLease in a way the founders could not have anticipated when they bought ASAP for ₹67 crore in 2016. India hosted more than 1,800 GCCs by FY2025, employing roughly 1.9 million professionals and generating roughly $64.6 billion in export revenue13. By 2030, that footprint is widely expected to scale to over 2,400 centres employing as many as 4 million people. TeamLease Digital, the home of Specialized Staffing, has become a primary supplier of contract engineers, data scientists, cloud architects and cybersecurity specialists to this base. By FY2026, the GCC segment was contributing more than 67% of Specialized Staffing's revenue, with Specialized Staffing growing gross revenue 13% year-on-year and EBITDA 15% on a full-year basis—well ahead of the General Staffing pace2.

The catch is the cyclicality. In the back half of FY2026, GCC hiring tapered as captives absorbed AI-led productivity gains and trimmed near-term recruitment budgets14. The pinch was visible in Q4 FY26, where overall EBITDA margin slipped to 1.5% from 1.7% a year earlier, partly because Specialized Staffing's mix of higher-paying GCC roles slowed temporarily. For investors, the lesson is twofold: yes, GCCs are the structural tailwind; yes, the very same offshoring 2.0 wave that drives them is also automating the more routine roles in the same companies. Which is why management has spent the last two years pushing harder into harder-to-automate disciplines—AI/ML, cloud, data engineering, cybersecurity—and pushing the EdTech and apprenticeship pipeline to produce more of them. The "hidden" businesses are the option value. The staffing chassis is the base case. Both arguments compound on the decision the board took in December 2025.

VI. The 2026 Leadership Transition: The "Titan" Era

The announcement landed on December 4, 2025, with the kind of restrained one-page board release that disguises a generational change. Effective February 2, 2026, Suparna Mitra would take over as Managing Director and Chief Executive Officer of TeamLease Services Limited, succeeding Ashok Reddy4. Manish Sabharwal would step down from his executive responsibilities and continue only as a Non-Executive Non-Independent Director. Ashok Reddy would move into an Executive Vice Chairman role, focused on long-term strategy, horizontal projects and adjacencies. Narayan Ramachandran would continue as Chairman. The founders had not exited; they had handed the operating keys to a complete outsider.

To understand why this was a shock, consider Indian mid-cap promoter culture. The default playbook is for founders to remain Executive Chairmen well into their seventies, with succession either internal (a son or daughter) or, in the more enlightened cases, an internal C-suite veteran groomed for a decade. Bringing in an outside CEO with no staffing-industry background is rare. Bringing in one from a luxury-goods business is rarer still. And bringing in someone whose résumé reads "former CEO of टाइटन Titan Watches & Wearables Division" to run India's largest private-sector employer of blue-collar associates is, by the standards of the Indian mid-cap universe, almost without precedent.

Suparna Mitra came to TeamLease with a profile that read more like a consumer brand veteran than a B2B services operator. An electrical engineering graduate from जादवपुर विश्वविद्यालय Jadavpur University and an MBA from IIM Calcutta, she began her career as a management trainee at Hindustan Lever before joining the Titan Company. At Titan's Watches & Wearables division, she presided over a doubling of revenue in three years to roughly ₹4,500 crore in FY2024-25, defended market leadership through premiumisation, and built a category-defining wearables business from the ground up4. Translation: she knows how to take a legacy, lower-margin product business and stretch its margin profile through brand, premium-mix and digital experience. Which is, almost word for word, the playbook the board is asking her to apply to TeamLease.

The thesis, never spelled out quite this bluntly in the official release but obvious from the strategy decks of the last two annual reports, is to push the consolidated EBITDA margin from the 1.3–2.0% range it has occupied for most of the public-company era toward 4–5%. That doubling-or-more of margin is what management has internally been calling "Next Orbit." The route runs through three things: HR services and RegTech revenue scaling fast enough to mix-shift the consolidated P&L; Specialized Staffing pricing power improving as the GCC mix richens; and General Staffing itself adopting more variable engagement models, where the client takes more of the wage risk and TeamLease takes more of a service-fee economics. By Q4 FY2026, more than 70% of new general-staffing logos were already being onboarded under variable engagement structures2—a quiet pre-positioning for the strategy the new CEO would inherit.

Incentives are aligned through the ESOP scheme rolled out in 2024, designed to vest only as Next Orbit margin milestones are met. The board's bet, in effect, is that a CEO who has built consumer-brand businesses can take a B2B sales organisation and turn it into a "digital experience and platform" company—standardising the buying flow, putting more of the customer relationship onto a self-serve interface, and selling RegTech and EdTech as products rather than as add-ons to staffing deals. The promoters, who collectively hold roughly 31.1% of the equity as of mid-202615, are not exiting either economically or governance-wise; their long-term incentive is to see the share count concentrated and the margin profile lifted. The ₹238-crore buyback approved alongside the FY26 results, at ₹1,600 per share, was a small but unmistakable signal that capital returned would tighten the per-share economics while Mitra's operating thesis plays out2.

The transition itself is being executed deliberately. Ashok Reddy's twelve-month role as Executive Vice Chairman gives the new CEO an institutional bridge into the customer base, the regulator relationships in नई दिल्ली New Delhi and the network with the state labour departments that the founders spent twenty years building. Manish Sabharwal's continuing board seat keeps the philosophical compass calibrated. But operating control, P&L authority and brand voice now sit elsewhere. For long-term investors, this is the most important strategic event in the company's history since the IPO.

VII. Hamilton's 7 Powers & Porter's 5 Forces

Step back from the news flow and look at TeamLease through the disciplined lenses of competitive strategy, and the picture sharpens considerably. Hamilton Helmer's 7 Powers framework names seven structural sources of durable advantage: Scale Economies, Network Economies, Counter-Positioning, Switching Costs, Branding, Cornered Resource and Process Power. TeamLease's General Staffing engine is a textbook study in Scale Economies. The marginal cost of onboarding the next associate, computing the next payroll, depositing the next PF contribution and filing the next state-level return falls as headcount grows, because the underlying compliance back office is a fixed-cost machine. Quess, FirstMeridian and a long tail of regional players all face the same arithmetic; only the top three meaningfully spread the fixed cost across enough associates to make the unit economics work. The three largest staffing firms captured roughly 23% of the total Indian staffing market by FY202516, and that share has been concentrating, not fragmenting.

Switching Costs are where the picture forks. In General Staffing, switching costs are real but modest; a corporate client unhappy with one staffing vendor can usually transition associates over to another vendor within a quarter, sometimes by simply having the new vendor pick up the same workers under a new contract. In Specialized Staffing, switching costs are higher because clients tend to embed contractors deeply into project teams and replacing them mid-project carries real productivity costs. In RegTech, switching costs become genuinely punishing—once an enterprise has loaded years of compliance history, regulatory mappings and workflow customisations into the platform, ripping it out is closer to a system migration than a vendor change. And in EdTech, the switching cost runs through the university partner more than the corporate client, but the same logic applies. TeamLease's strategic challenge is to mix-shift the consolidated revenue base toward the higher-switching-cost segments without losing the scale lever in the chassis.

The Cornered Resource is less obvious but real: TeamLease's proprietary database of more than two million job seekers, accumulated through twenty-plus years of associate placements, apprenticeships and EdTech enrolments. In a country whose labour-market data is famously patchy, owning a granular, wage-tagged, geography-tagged record of who took what job at what salary in which year is itself a strategic asset—particularly when the buyer of staffing services is increasingly procurement-driven and price-aware. The company's annual "Employment Outlook Report" and salary-trend publications are not just marketing; they are evidence that the data asset has a public face.

Porter's 5 Forces puts a sharper edge on the industry context. The rivalry leg is dominated by क्वेस Quess Corp, India's largest staffing firm with reported Indian staffing revenue of ₹17,000 crore in 2024 and a strategy of relentless diversification into facility management, security and IT services16. Quess has used its broader services basket to bundle staffing into integrated outsourcing deals, putting price pressure on the pure-play staffing flank. FirstMeridian, a private competitor, plays a similar bundling game. The bargaining power of customers is high on the General Staffing side—large customers like the टाटा Tata group, रिलायंस Reliance, Amazon India, Flipkart, the major Indian banks and the GCCs negotiate markups down to a few hundred basis points and consolidate vendors aggressively. The bargaining power of suppliers—in this business, the associates themselves—has been historically low but is rising as minimum-wage notifications tick up and the broader Indian labour market tightens in formal-sector occupations. The threat of substitutes lives in two places: gig platforms for blue-collar work (where players like Apna and Urban Company have nibbled at the edges) and AI-driven automation for white-collar work (where TeamLease's GCC exposure makes it a direct beneficiary today and potentially a direct casualty in the medium term). The threat of new entrants is high in geography-specific staffing niches but low in compliance-heavy national staffing, because the regulatory cost of building a credible nationwide payroll back office is genuinely a moat.

Net of all five forces, TeamLease sits in a defensible but not dominant position in its core market, and a structurally advantaged position in its emerging adjacencies—exactly the configuration that justifies why the board hired a brand-and-margin operator rather than a staffing veteran for the next chapter.

VIII. Playbook: Business & Investing Lessons

Three lessons travel out of the TeamLease story with portable value for investors and operators looking at any emerging-market formal-services business.

The first is that compliance is a moat in markets where rules are dense and informally enforced. In the United States or Western Europe, "we are good at filing your paperwork" is not a business; it is a feature of being a real company. In India—and by extension in much of Southeast Asia, Latin America and the Middle East—the cost of being "clean" in a "grey" industry is high enough that scale players who can absorb it become structurally cheaper to do business with than the alternative. TeamLease is what that looks like at maturity. The lesson is to look for businesses whose unit economics improve as the regulatory perimeter widens, not narrows—because every new rule the government adds is a fixed cost the scale incumbent spreads across a base its sub-scale competitors cannot match.

The second is the Trojan horse strategy of layering high-margin services on top of a low-margin volume business. TeamLease's playbook—use staffing as the wedge into the customer's HR workflow, then upsell RegTech, EdTech and managed payroll—is essentially the same playbook अमेज़न Amazon used with logistics to seed AWS, or that Indian banks have tried (with mixed success) by using current accounts to cross-sell wealth and credit. The discipline that distinguishes the winners is the willingness to keep the wedge product priced for volume even after the higher-margin tail starts to scale. If TeamLease ever decides to optimise General Staffing for margin rather than reach, it risks losing the very customer relationship that lets RegTech and EdTech sell themselves. So far, management has resisted that temptation. Whether the new leadership keeps the discipline is the central question of the next five years.

The third lesson is about founder humility. The decision by Manish Sabharwal and Ashok Reddy to hand operating control to Suparna Mitra is the kind of move that almost never happens in Indian mid-cap promoter families, because it requires the founders to admit that the skill set needed to take the company from ₹12,000 crore in revenue to ₹25,000 crore at meaningfully higher margins is not the skill set that built the company from ₹0 to ₹12,000 crore. That is a hard psychological pivot. The historical batting average of founders who make it is much higher than that of founders who refuse to. A राष्ट्र निर्माण Nation-Building mission—which is how Sabharwal has framed the company's purpose for two decades—is bigger than any one founder's ego, and the board's December 2025 decision is the public proof. For investors, transitions like this can compress two or three years of corporate development into a single fiscal year, in either direction. They need to be watched closely.

A second-layer diligence aside worth noting: the company's working-capital profile is structurally heavy because associate wages are paid before client invoices clear. Any disruption to receivables—a large client defaulting, or a regulatory change extending the EPF deposit timeline—shows up immediately in operating cash flow. The credit-rating profile has remained investment-grade through cycles, but this is a permanent feature of the model rather than a bug to be engineered away. Investors should track the trade receivables days line every quarter; it is the single best leading indicator of underlying business health that the consolidated EBITDA margin does not capture.

IX. Analysis & Bear vs. Bull Case

The bull case for TeamLease in mid-2026 is essentially a mix-shift case. If HR Services, RegTech, EdTech and managed payroll grow faster than General Staffing for four or five consecutive years—plausible given starting bases of 5–10% of revenue and reported growth rates well above the staffing chassis—then consolidated EBITDA margin can grind from the 1.3% it printed in FY2026 to something closer to 3–4%, which on a flat revenue base would more than double EBITDA in absolute terms. Layer onto that the GCC tailwind in Specialized Staffing, the buyback shrinking the share count, and a new CEO whose mandate is explicitly margin expansion, and the operating leverage story becomes the dominant narrative. The bull also gets to point to the Indian formalization trend—the four labour codes finally getting implemented across the major states, GST 2.0 broadening the formal-economy net further, and the structural tightening of blue-collar wages making "TeamLease as compliance partner" more, not less, valuable.

The bear case has three legs. The first is that GCCs—now the single most important growth driver of Specialized Staffing—are also, ironically, the most aggressive deployers of generative AI internally. As captives automate routine engineering and back-office roles, the demand for staffed contract headcount may grow slower than current models assume. The early FY2026 deceleration in GCC hiring is at least a yellow flag here14. The second is wage inflation in formal-sector India, which compresses the staffing markup directly; for a business at 1.3% EBITDA margin, the gap between 6% wage growth and 7% wage growth is the difference between profit growth and profit decline. The third is execution risk on the leadership transition itself. New CEOs from outside the industry have historically taken twelve to twenty-four months to fully calibrate; in a business with this thin a margin and this high a working-capital footprint, even a single quarter of mis-steered priorities can produce a meaningful earnings air-pocket.

Benchmarked against the global flexi-staffing majors, the picture is uncomfortable in some ways and flattering in others. Adecco and Randstad operate at consolidated EBITDA margins typically in the 3.5–4.5% range, with revenue growth in low single digits and far more mature regulatory environments. TeamLease earns roughly a third of those margins but grows revenue at three to four times the pace, and its underlying labour market is decades from the saturation those firms face in their core European geographies. The right way to think about TeamLease is not as a worse-margin Adecco; it is as an earlier-stage Adecco operating in a much larger and faster-growing demographic. Whether that justifies the trailing earnings multiple at which the stock trades is a judgement each investor has to make, but the comparison frames the long-duration optionality.

Three KPIs deserve permanent attention from a long-term fundamental investor. First, the consolidated EBITDA margin trajectory—not the quarterly print, but the rolling-four-quarter direction. The Next Orbit thesis lives or dies on this single line. Second, the Specialized Staffing revenue mix as a share of consolidated revenue; this is the proxy for the high-margin, GCC-leveraged growth engine. Third, the associate count net adds in General Staffing each quarter—if this line stops growing, the scale-economies moat in the chassis starts to erode and the entire mix-shift premise rests on a shrinking foundation. Everything else is colour. Those three numbers tell you whether the next decade looks like the last one or like something materially different.

There is also a useful "myth versus reality" check worth running. The common myth is that TeamLease is fundamentally a low-margin commodity body-shop and that low-margin commodity body-shops do not become attractive long-term investments. The reality is that TeamLease has spent the last decade quietly building a portfolio of compliance, education and payroll businesses whose economics are not body-shop economics at all, while keeping a body-shop in the basement to absorb the regulatory fixed cost and act as a customer-acquisition engine. The investor question is not "is the body-shop fundamentally cheap or fundamentally great?"—it is "will the rest of the building eventually be larger than the basement?" The answer to that question is what the next five fiscal years will resolve.

X. Epilogue

In the end, the most useful frame for thinking about TeamLease Services is probably the most prosaic one. It is the infrastructure of the Indian labour market. Not the glamour layer—not the LinkedIn profiles, the venture-funded gig platforms, the unicorn IPO prospectuses. The plumbing underneath, where 335,000 people get paid on time every month, where PF deposits land at the right account number, where ESI contributions show up on the right registers, where state labour departments in seventeen jurisdictions all receive the right returns by the right deadlines, and where the entire apparatus runs at a margin so thin it would offend a wholesale grocer.

For a country with the labour-force demographics India has between now and 2050—roughly twelve million young people entering the workforce every year for the next two decades—infrastructure of this kind is not optional. Someone has to be the boring layer between the employer and the worker, and the boring layer has scale economics. The question this episode has tried to frame is whether TeamLease, under a leader who has spent twenty years building consumer brands rather than HR back offices, can take that infrastructure and stretch it into something more profitable than infrastructure has historically been allowed to be in India. There is a path. It runs through RegTech, through EdTech, through GCC-driven specialised staffing, and through the kind of digital-experience layer that makes a B2B services company feel, to its customer, like a B2C product.

If that path works, the story of the company stops being a 2% EBITDA story and starts being a 4-to-5% EBITDA story with a much richer composition. If it doesn't, the chassis continues to grind out volume in a country that desperately needs more formal employment, and the patient holder is left with what they bought: a stake in राष्ट्र निर्माण Nation Building through formal employment, valued at whatever multiple of book the public market is in the mood to pay. Both outcomes coexist, in different probabilities, in the same stock today. The next four fiscal quarters are the ones in which Suparna Mitra will start to tell us which one is winning.

References

References

-

TeamLease ranked among India's largest staffing firms — Staffing Industry Analysts, 2025 ↩

-

TeamLease Services Q4 FY26 results and ₹238 crore buyback — Business Standard, 2026-05-20 ↩↩↩↩

-

TeamLease Rs 423-crore IPO oversubscribed — Business Standard, 2016-02-04 ↩↩

-

Suparna Mitra to Join as MD & CEO of TeamLease — TeamLease Press Release, 2025-12-04 ↩↩↩

-

TeamLease's Manish Sabharwal on Fixing India's People Supply Chain — Knowledge at Wharton ↩

-

TeamLease IPO oversubscribed 65 times, second-highest in eight years — DealStreetAsia, 2016 ↩

-

TeamLease Q4 revenue improves 17%, profits rally — Staffing Industry Analysts, 2025 ↩

-

Team Lease Services to acquire ASAP Info Systems — Business Standard, 2016-07-04 ↩

-

TeamLease acquires 40% stake in Schoolguru for Rs 13 crore — Business Standard, 2017-11-08 ↩

-

TeamLease Services Limited acquired an additional 37.14% stake in Schoolguru Eduserve — MarketScreener, 2020-09-08 ↩

-

TeamLease Services raises stake in Avantis Regtech; renames it as TeamLease Regtech — Business Standard, 2021-11-02 ↩↩

-

TeamLease acquires TSR Darashaw, takes minority stake in Crystal HR — Staffing Industry Analysts, 2024-12-24 ↩

-

Global Firms Double Down On India's Talent Infrastructure With 2,400 Global Capability Centers Expected By 2030 — Allwork, 2025-11 ↩

-

Staffing Firms Cut Growth Projections as Global Capability Centres Trim Recruitment Amid Automation — The Wire ↩↩

-

TeamLease Services Latest Shareholding Pattern — Trendlyne, 2026 ↩

-

Quess, TeamLease, FirstMeridian dominate India's staffing sector — Staffing Industry Analysts, 2025 ↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube