TBO Tek: Building the Global Travel Distribution Platform

I. Introduction & Episode Roadmap

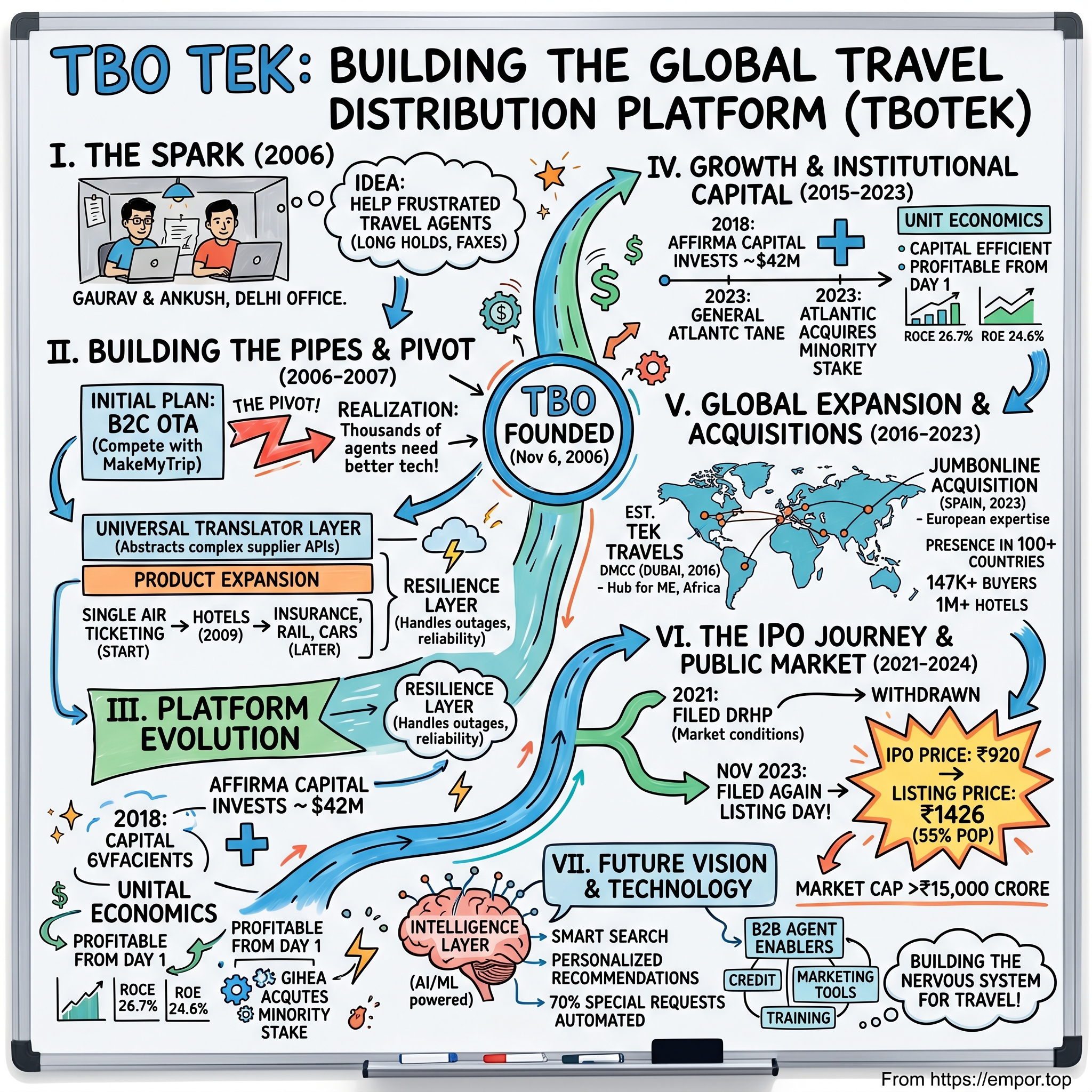

Picture this: It's 2006, and two entrepreneurs are hunched over laptops in a cramped Delhi office, watching travel agents struggle with antiquated booking systems. One agent calls, frustrated—he's been on hold with an airline for 45 minutes just to confirm a single ticket. Another faxes (yes, faxes) a hotel reservation request that will take days to confirm. Gaurav Bhatnagar and Ankush Nijhawan exchange glances. This is it—the moment they've been waiting for. The global travel industry, worth trillions, is still running on technology from the disco era.

Fast forward to 2024: Their company, TBO Tek, rings the bell at the National Stock Exchange. The IPO price of ₹920 soars to ₹1,426 on listing day—a 55% pop that values the company at over ₹15,000 crore. From that cramped office to connecting 147,000 buyers and suppliers across 100+ countries, processing billions in gross transaction value. The central question isn't just how they built this platform—it's how they managed to wedge themselves between century-old global distribution systems and modern tech giants, all while bootstrapping from India. This episode isn't just about how two guys built a unicorn—it's about understanding the architecture of modern intermediation. How do you create value in the age of direct-to-consumer? Why do B2B platforms sometimes outlast their B2C counterparts? And perhaps most intriguingly: In a world where everyone predicted disintermediation, why are the intermediaries getting stronger?

We'll trace this journey from Gaurav's one-way flight from Seattle to Delhi on Halloween 2004, leaving his prestigious Microsoft job with a promise to himself to build his own company, to the IPO listing at ₹1,426, delivering a 55% gain over the offer price of ₹920. Along the way, we'll unpack the strategic decisions, market dynamics, and sheer execution that transformed a simple insight—travel agents need better tools—into a platform processing billions in transactions.

What makes TBO's story particularly compelling isn't just the outcome—it's the path. While competitors raised hundreds of millions burning cash for consumer acquisition, TBO quietly built infrastructure. While others chased headlines, they chased unit economics. And while the market obsessed over B2C plays, they bet that B2B would be the real endgame. They were right. Let's understand why.

II. The Pre-Internet Travel Distribution Era

Imagine walking into a travel agency in 1999. The walls are plastered with faded posters of exotic destinations—pyramids, beaches, the Eiffel Tower. Behind the desk sits an agent, phone wedged between shoulder and ear, flipping through a three-inch-thick book of airline schedules. On hold with Air India for the third time today. A customer walks in wanting to book a Mumbai-to-London flight with a Bangkok stopover. The agent sighs. This will take hours.

This was the reality of travel distribution before the internet revolution. The industry operated on three archaic pillars: telephone lines that were perpetually busy, fax machines that jammed at crucial moments, and those infamous GDS terminals—green-screen monstrosities that required months of training to operate. Amadeus, Sabre, and Travelport had carved up the global market, charging airlines hefty fees (often 2-3% of ticket value) just to display inventory. Travel agents paid thousands of dollars monthly just to access these systems. Small wonder that only the largest agencies could afford them.

The inefficiencies were staggering. A hotel in Jaipur wanting to sell rooms to international tourists had to work through multiple layers—local agents, consolidators, tour operators, each taking their cut. By the time a room reached the end consumer, markups could exceed 40%. Confirmations took days. Changes required starting from scratch. And forget about real-time availability—you booked first and prayed later. In India, the context was even more dramatic. After an economic downturn in 1991, the Indian government began opening up markets and launched an economic liberalization program, unleashing forces that would transform the nation. In the early 2000s, air travel in India was a luxury, only accessible to the affluent few. The aviation sector had just been deregulated—Air India and Indian Airlines were the only two airlines operating until 1994, when Jet Airways and Air Sahara started operations, followed by Air Deccan, the first low cost carrier, in August 2003.

Meanwhile, India's middle class was exploding. The heterogenous and diverse middle class in India significantly expanded since the 2000s, creating millions of new travelers—businesspeople flying to meetings, families visiting relatives, young professionals exploring the world. But here's the paradox: just as technology should have eliminated middlemen, the complexity of global travel was actually increasing. More airlines meant more choices. More hotels meant more confusion. More options meant more friction.

The traditional GDS players—built for a world of travel agents with specialized training—couldn't adapt to this new reality. Their systems required IATA licenses, expensive hardware, months of training. A small travel agent in Jaipur or a startup in Bangalore couldn't access global inventory without massive upfront investment. The market was fragmenting at precisely the moment it needed to consolidate. Someone needed to build the pipes for this new world. The stage was set for disruption, but it would require a unique combination of technical expertise and deep understanding of travel distribution. Enter our protagonists.

III. The Founding Story: Gaurav & Ankush (2006)

Twenty years ago, on Halloween, Gaurav Bhatnagar took a one-way flight from Seattle to Delhi. In 2004, it was quite unconventional for a middle-class professional to leave a prestigious job at Microsoft to return to India, but he was determined to fulfill a promise he'd made to himself. Going to the US after graduation was never part of his initial plan. He had witnessed the first dot-com boom of 1999-2000 and was already set on building his own company. However, the Microsoft offer came along and it was too good to pass up. Back then, taking a job in the US often felt like a one-way commitment, but he promised himself that he would return after two years.

True to his word, Gaurav landed in Delhi with savings, Seattle rain still fresh in his memory, and a burning question: what problem was big enough to build a company around? A computer science graduate from IIT Delhi who had been working at Microsoft, Gaurav returned to India to pursue his entrepreneurial dreams. With his vision that travel would be one of the first sectors to move online due to minimal logistics needs, he wanted to create an online travel platform. At that point, he was running a software services company called Tekriti Software.

Meanwhile, across the city, Ankush Nijhawan was running his own battle. Initially, it was a B2B offline travel company operating in North and some parts of East India. By 2005, with the internet making strong inroads into the travel industry, Ankush saw both a challenge and an opportunity, as companies like MakeMyTrip and Yatra were quickly adapting to online models. His family travel business, Travel Boutique, was bleeding clients to these new online players. But Ankush saw something others missed—the travel agents weren't disappearing; they were desperate for tools to compete.

"I was sold on building an e-commerce platform for offering travel services and checking out TCS and Wipro when someone connected me to Gaurav Bhatnagar," says Ankush. Gaurav who was with Microsoft had returned to India and was evaluating the travel tech space. Both joined hands to build a B2C OTA christened Travel Boutique Online (TBO), leveraging the goodwill of the existing brand.

The initial plan seemed straightforward—compete with MakeMyTrip and Yatra in the B2C space. But then came the pivot that would define their future. "The swing from B2C to B2B was overnight," remembers Ankush. "Someone questioned us why B2C when there are already three players there and they have even raised capital. It was a moment of brutal clarity. Why fight in a crowded B2C market when thousands of travel agents were desperately seeking the same technology access that the big players had?

"Gaurav and I met in 2005, he started writing code in 2006 and in January 2007 the first ticket was printed from the TBO platform," shares Ankush. Initially the travel partner ecosystem was very skeptical, even assuming it was online fraud. But Ankush's tenacity and trade relationships curated over the years paid off in the end. With OTAs bursting on to the travel scene in 2005, TBO was at the right place at the right time offering global airline inventory on real-time basis to brick and mortar agents.

TBO Tek was founded on November 6, 2006. Gaurav Bhatnagar and Ankush Nijhawan are the co-founders and joint managing directors of TBO Tek. But founding was just the beginning. The real challenge was convincing travel agents—many of whom still used paper ledgers—to trust an online platform with their business. Ankush would personally visit agents, laptop in hand, demonstrating how they could book an international flight in minutes instead of hours. Gaurav, meanwhile, was architecting a platform that could handle the complexity of global travel distribution while being simple enough for a small-town agent to use.

The early days were brutal. Servers crashed during peak booking hours. Airlines questioned their legitimacy. Banks refused to process their payments. But they persisted, iterating rapidly, learning from each failure. Incorporated in 2006, TBO has revolutionized the B2B online travel space and grossed $1.2 billion last fiscal, of which, India pulled in 65 per cent—though this success was still years away.

What set them apart wasn't just technical capability—it was empathy for the travel agent. While competitors saw agents as obsolete middlemen to be eliminated, Gaurav and Ankush saw them as entrepreneurs who needed better tools. They didn't just build a booking platform; they built a business enablement system. Training programs, credit facilities, marketing support—everything an agent needed to compete in the digital age. The foundation was set. Now came the hard part: scaling a two-sided marketplace in one of the world's most complex industries.

IV. Building the Platform: From Air to Everything (2006–2015)

The conference room in TBO's Gurgaon office, 2008. Gaurav stands before a whiteboard covered in arrows and boxes—a sprawling diagram of the global travel ecosystem. "Look," he says to his team of twelve engineers, "we're not just building a booking engine. We're building the nervous system for travel distribution." The challenge was immense: connect hundreds of airlines, each with different APIs and booking protocols, to thousands of travel agents, each with unique needs and technical capabilities.

They started with air tickets because that's where the pain was most acute. TBO has evolved from a single-product air ticketing company into a leading Top 5 global travel distribution platform. But the journey from point A to point B was anything but linear. The first major technical challenge came in 2007 when they tried to integrate with Amadeus. The GDS giant's documentation was thousands of pages long, written for Fortune 500 companies with dedicated integration teams. TBO had three engineers and a deadline.

Gaurav's solution was elegant: instead of building direct integrations with every supplier, they created an abstraction layer—a universal translator that could speak every dialect of the travel industry. Hotel XML on one side, airline EDI on another, old-school GDS commands in between. Their platform became a Rosetta Stone for travel technology, allowing a small agent in Kochi to access the same global inventory as a major corporate travel management company.

The product expansion followed a careful sequence. Hotels came next, in 2009. But unlike aggregators who simply scraped rates, TBO built direct relationships with properties. TBO offers airline tickets, hotel rooms, foreign exchange, rail, car rentals and insurance. Each vertical wasn't just bolted on—it was integrated into a unified platform where booking a flight could trigger hotel recommendations, where a hotel booking could suggest local transfers.

By 2010, they faced a crisis that would define their approach to platform building. A major airline changed its API without warning, breaking thousands of bookings in process. Agents were furious. Customers were stranded. The easy solution would have been to blame the airline. Instead, TBO built what they called the "resilience layer"—automatic failovers, cached inventory, predictive issue detection. They turned a disaster into a competitive advantage: TBO became known as the platform that never went down. Operating Travelboutiqueonline.com (TBO) in B2B segment as an IATA registered ticketing agency required more than just technical capability—it required building trust in a market scarred by fly-by-night operators. The company's approach to network effects was counterintuitive. Instead of subsidizing transactions to boost volume, they focused on what they called "quality density"—ensuring that every agent who joined was successful, creating organic word-of-mouth growth.

The numbers tell the story: Monthly transacting buyers rose from 10,401 in fiscal 2021 to 24,530 in fiscal 2023. But more impressive was the retention—agents who joined TBO rarely left. The platform's reliability became its moat. In an industry where a single failed booking could destroy an agent's reputation, TBO's 99.7% uptime became legendary.

By 2015, they had built something unique: a platform that wasn't just processing transactions but orchestrating the entire travel value chain. Agents could book a complex multi-city itinerary involving flights from different alliances, hotels from independent chains, and ground transport from local providers—all in a single workflow, with unified payment and instant confirmation. The foundation was set for the next phase: institutional capital and global expansion.

V. The Funding Journey & Institutional Capital (2015–2023)

The boardroom at TBO's headquarters, 2017. Gaurav and Ankush sit across from representatives of Naspers, the South African media giant that had backed Tencent and Flipkart. The question on the table: why hadn't TBO raised institutional capital for eleven years? Ankush's answer was simple: "We didn't need it until now. But to go global, to build the infrastructure for the next billion travelers, we need partners who understand platforms."

The bootstrapping years from 2006 to 2017 were a masterclass in capital efficiency. While competitors burned through venture funding acquiring customers, TBO built a profitable business from day one. They reinvested every rupee into platform development and market expansion. No fancy offices, no PR campaigns, no growth hacking—just relentless focus on unit economics.

But by 2017, the landscape was shifting. International expansion required local presence, regulatory compliance, multi-currency settlement systems. The capital requirements were beyond what organic growth could fund. After Naspers' initial interest, the real breakthrough came in 2018, when Affirma Capital invested around $42 million to acquire a 46% stake in TBO Tek. This wasn't just capital—it was validation from one of Asia's most sophisticated PE firms.

"Since our investment in 2018, we have witnessed TBO's transformational journey to becoming one of the leading travel technology platforms globally, creating meaningful value for its shareholders along the way, as has been crystallised in Affirma Capital's multi-fold return on investment," Udai Dhawan, founding partner at Affirma Capital, would later reflect. The partnership was transformative, providing not just capital but strategic guidance through the treacherous COVID years.

In 2018, Affirma Capital had invested around $42 million to acquire a 46% stake in TBO Tek, witnessing TBO's transformational journey to becoming one of the leading travel technology platforms globally, creating meaningful value for its shareholders along the way, as has been crystallised in Affirma Capital's multi-fold return on investment as part of this transaction.

TBO raised total funding of $61M over 3 rounds, with latest PE round on Sep 01, 2018 for $50M. But the numbers don't tell the full story. Unlike the typical VC playbook of raising rounds every 18 months, TBO waited five years before their next major transaction. During this time, they weren't standing still—they were building the infrastructure for global scale while maintaining profitability.

Then came October 2023, the pivotal moment: General Atlantic acquired a minority stake in TBO from Affirma Capital. General Atlantic entered into an agreement with entities held by Affirma Capital to acquire a minority stake in TBO Tek Ltd, with Affirma Capital continuing to remain invested in the Company subsequent to this transaction. This wasn't just another funding round—it was a carefully orchestrated transition, with Affirma reportedly achieving a 9x multiple on invested capital through this partial exit.

"Gaurav, Ankush and the entire TBO team have pursued a clear mission to simplify travel sales in a growing and increasingly diverse traveler environment. They have been focused on building a unique technology platform that is able to deliver discovery, trust, payments and services to its Suppliers and Buyers. We see immense potential in the path ahead for TBO, including global expansion opportunities," said Shantanu Rastogi, Managing Director at General Atlantic.

What made TBO attractive to institutional investors wasn't just growth—it was the quality of that growth. In an era of blitzscaling, TBO had built a capital-efficient machine. They generated cash, not just revenue. They had network effects, not just user growth. They had built infrastructure, not just an app. The institutional capital wasn't funding losses; it was accelerating an already profitable playbook into new markets.

VI. Global Expansion & Market Penetration (2016–2023)

Dubai International Airport, 2016. Ankush walks through Terminal 3, the world's busiest international hub, watching the river of humanity flow between continents. The Middle East wasn't just a market—it was a crossroads. If TBO could crack Dubai, they could reach Africa, Europe, and Asia simultaneously. The decision to establish Tek Travels DMCC in Dubai wasn't about following the money; it was about following the network effects.

The global expansion strategy was surgical. Rather than the spray-and-pray approach of opening offices everywhere, TBO identified nodes in the global travel network. Founded in 2006, TBO is a global travel distribution platform with $2.73B in Gross Transaction Value ("GTV") for FY23 and a presence in 100+ countries as of 30 June 2023. Dubai was first—a hub for Middle Eastern, African, and South Asian travel. Then came strategic partnerships in Southeast Asia, where the outbound travel boom was just beginning.

The numbers reveal the transformation: About 60% of GTV comes from India (down from 80%+ in FY21), with TBO connecting over 147,000 buyers and suppliers in more than 100 countries. This wasn't just geographic expansion—it was a fundamental shift in the business. International markets had different dynamics. European agents wanted different inventory. American buyers had different payment preferences. Each market required localization, but the platform architecture allowed for this flexibility.

The monthly transacting buyers on its platform rose from 10,401 in fiscal 2021 to 24,530 in fiscal 2023. But raw numbers don't capture the quality of this growth. These weren't just sign-ups—they were active, transacting partners generating real GTV. The platform was becoming truly global, with transactions happening 24/7 across time zones.

The masterstroke came in December 2023 with the Jumbonline acquisition in Spain. This wasn't just buying market share—it was acquiring local expertise, relationships, and most importantly, trust in the European market. Jumbonline brought deep connections with European hotels and transportation providers, inventory that Asian and Middle Eastern agents desperately wanted access to.

Competing with legacy GDS systems required a different approach. TBO couldn't match their installed base or airline relationships built over decades. Instead, they focused on what the GDS couldn't do: provide simple, modern interfaces; offer flexible commercial terms; integrate new-age suppliers like vacation rentals and experience providers. They became the anti-GDS—nimble where the incumbents were rigid, simple where they were complex, affordable where they were expensive.

By 2023, TBO had achieved something remarkable: they had built a parallel infrastructure to the global distribution systems, one that served the long tail of travel—the small agents, the emerging market suppliers, the non-IATA agencies. On average, 40K+ annual transacting buyers get real-time access to a global travel inventory of 700+ airlines and 1M+ hotels on the platform. This wasn't disruption through destruction; it was disruption through inclusion.

The IPO Story & Public Markets Debut (2024)

December 2021: TBO filed its DRHP with SEBI for a ₹2,100 crore IPO during a hot tech market. But Russia's invasion of Ukraine crashed markets and killed tech valuations, forcing them to delay. This was actually TBO's second attempt at going public, as they had previously received regulatory approval but never launched the IPO.

The decision to withdraw wasn't taken lightly. Gaurav and Ankush faced pressure from all sides—investors wanting liquidity, employees holding ESOPs, market watchers questioning their nerve. But they made the call: better to wait for the right market than force a bad outcome. This wasn't retreat; it was strategic patience.

Two years later, November 2023, they're back. The market has stabilized. Travel has fully recovered. Most importantly, TBO's numbers have gotten even stronger. Travel Boutique Online, or TBO Tek Ltd, has filed its draft red herring prospectus (DRHP) with the markets regulator SEBI. This time, the structure is different—more conservative, focused on profitability over growth narrative.

TBO Tek's IPO worth Rs 1,550.81 crore, comprising fresh capital and Offer For Sale. The fresh issue of ₹400 crore would fund technology infrastructure and geographic expansion, while the OFS would provide exits for early investors. Post-issue, promoter stake reduced from 51% to 44%—a carefully calibrated balance between maintaining control and providing liquidity.

The roadshow was a masterclass in expectation management. Instead of promising hockey-stick growth, they emphasized sustainability. Instead of comparing themselves to consumer tech unicorns, they positioned as infrastructure. The message was clear: TBO wasn't a momentum play; it was a compounder.

Then came May 15, 2024—listing day. The IPO was offered at ₹920 per share and listed at ₹1426, delivering listing gain of 55%. In a market where most tech IPOs were struggling, TBO's pop wasn't just about the numbers—it was validation of the B2B model, of patient capital, of building real businesses over chasing valuations.

Current market cap of ₹15,000+ crore reflects not just the company's achievements but the market's recognition of a new breed of Indian tech companies—profitable, global, and built to last. The failed 2021 attempt, rather than being a setback, had become part of the narrative—a company mature enough to walk away from a bad deal, confident enough to wait for the right moment.

VIII. Business Model & Unit Economics Deep Dive

The spreadsheet on the screen shows a number that makes even seasoned investors pause: ROCE 26.7%. In the capital-intensive world of travel distribution, where working capital cycles can stretch for months and technology investments run into millions, TBO has achieved what many thought impossible—generating Revenue of ₹1,830 Cr, Profit of ₹232 Cr, ROCE 26.7%, ROE 24.6%.

The secret lies in understanding that TBO isn't really in the travel business—they're in the liquidity transformation business. Here's how it works: A small travel agent in Indore wants to book a hotel in Paris for a customer. The hotel wants payment upfront. The agent's customer will pay 30 days later. Traditional solution? The agent needs working capital. TBO's innovation? They provide the float, earning not just commission but also the financial spread.

The two-sided technology platform enabling both Suppliers and Buyers to transact seamlessly operates on multiple revenue streams. First, there's the straightforward commission model—suppliers pay TBO a percentage of bookings. But that's just the beginning. There's markup on inventory, forex margins on international transactions, ancillary services, and increasingly, platform fees for premium features.

What makes the unit economics sing is the network density. 40K+ annual transacting Buyers accessing 700+ airlines and 1M+ hotels on the platform creates massive operating leverage. The cost to onboard the 40,001st buyer is essentially zero. The cost to add the millionth hotel is marginal. Every additional transaction makes the platform more valuable for everyone.

The capital efficiency comes from what they don't do. Unlike B2C players, they don't spend on consumer marketing. Unlike traditional distributors, they don't hold inventory. Unlike payment companies, they don't need massive regulatory capital. They're essentially a software company with travel industry revenues—the best of both worlds.

The working capital management deserves its own case study. By negotiating different payment terms with suppliers (pay later) and buyers (pay now), they've turned what should be a capital drain into a capital source. The float generates returns before they even recognize the revenue. It's financial engineering at its finest, hidden inside what looks like a simple booking platform.

But the real moat isn't financial—it's the data network effects. Every search, every booking, every cancellation feeds the machine learning models. The platform gets smarter, recommendations get better, fraud detection gets tighter. A new competitor can copy the interface, match the prices, even poach the people. They can't replicate ten years of transaction data and the intelligence it generates.

IX. Technology & Innovation Strategy: Building TBO's Intelligence Layer

The demo room at TBO's tech center, 2024. A travel agent from a small town in Thailand is booking a complex multi-city European tour. As she types "Paris to Rome," the screen doesn't just show flights—it predicts she'll need a hotel near the Colosseum, suggests a skip-the-line Vatican tour, and offers travel insurance tailored to her client's profile. All of this happens in milliseconds, powered by what TBO calls their "intelligence layer."

Proprietary platform relies heavily on AI/ML to offer unique listings and products. But this isn't generic AI slapped onto a booking engine. This is decade-deep domain expertise encoded into algorithms. The system knows that Indian travelers to Dubai often book desert safaris, that Chinese groups prefer hotels with Asian breakfast options, that Latin American families travel in larger groups during specific holidays. Each insight, learned from millions of transactions, makes the next recommendation smarter.

Weaving generative AI into travel agent journey, Smart Search feature for personalized ranking and recommendations—these aren't buzzwords but fundamental architecture decisions. When an agent searches for "romantic getaway Europe February," the system doesn't just return Paris hotels. It understands romance means different things to different cultures, that February has Valentine's Day but also Chinese New Year, that budget constraints vary by source market. The results are dynamically personalized not just to the end traveler but to the agent's typical client profile.

TBO has automated 70% of special travel requests using AI voice bots, significantly reducing response time for travel agents, as revealed by Garima Pant, VP of Customer Experience. But the real innovation isn't in automation—it's in augmentation. The AI doesn't replace agents; it makes them superhuman. A small agent in Manila can now provide the same level of service as a luxury travel consultant in London, backed by the collective intelligence of the platform.

The data architecture deserves special attention. Unlike consumer platforms that track individual users, TBO's data model is multi-dimensional—tracking agents, their clients, suppliers, routes, seasons, events. They've built what they call a "travel graph"—a massive network of interconnected data points that can predict demand spikes before they happen, identify fraud patterns in real-time, suggest alternative routes when disruptions occur.

Building for scale meant solving problems others hadn't even encountered. How do you handle a booking system that needs to work in 100+ countries with different regulations? How do you manage payments across 55+ currencies with real-time forex? How do you ensure that a hotel in Bali can be booked by an agent in Bolivia serving a client from Belgium? Each solution required not just technical innovation but deep understanding of global travel logistics.

The AI and personalization roadmap points to an even more ambitious future. They're not just building better search or smarter recommendations—they're fundamentally reimagining how travel distribution works. Predictive inventory management that knows what agents will need before they search. Dynamic packaging that creates custom products in real-time. Automated negotiation systems that optimize margins while maintaining competitiveness. The platform is becoming less of a marketplace and more of an intelligent operating system for global travel.

X. Competitive Landscape & Market Position

The war room wall displays a complex chart: Amadeus with $5 billion in revenue, Sabre at $3 billion, Travelport at $2 billion. Then, in a different color, the new-age players: Booking.com's $21 billion gross bookings, Expedia's $12 billion. And there, growing rapidly, TBO's trajectory. The question isn't whether they can compete—it's what game they're actually playing.

TBO has evolved into a leading Top 5 global travel distribution platform, but calling them a GDS competitor misses the point. They're not trying to replace Amadeus—they're building an entirely different infrastructure for a different market. While GDS systems focus on premium airlines and chain hotels serving corporate travelers, TBO aggregates the long tail: budget carriers, independent hotels, local tour operators. It's the difference between building highways and building capillary roads—both essential, serving different needs.

The traditional GDS players operate on a model built in the 1960s: centralized inventory, fixed commercial terms, complex integration. Their moat is their entrenchment—airlines have built their entire operations around GDS protocols. But this strength is also their weakness. They can't serve the small hotel in Goa, can't onboard the local tour operator in Cairo, can't provide credit to the startup travel agency in Lagos. TBO can.

Regional competitors tell a different story. In India, there's Rategain focusing on hotel distribution. In Southeast Asia, WebBeds competing for inventory. In the Middle East, local players trying to aggregate regional supply. But TBO's advantage isn't just scope—it's the network effects from connecting diverse markets. An Indian agent selling to Middle Eastern clients needs both Indian and Arab inventory. A European operator creating Asian packages needs local expertise and global standards. TBO sits at these intersections.

The differentiation strategy is subtle but powerful. While others compete on price or inventory size, TBO competes on enablement. They don't just give agents access to inventory—they help them build businesses. Credit facilities for cash flow, marketing tools for customer acquisition, training programs for skill development. They're not selling a product; they're selling success.

The threat from direct supplier distribution is real but overstated. Yes, airlines and hotels want direct relationships with customers. But the complexity of global travel makes intermediation valuable. A traveler might book a flight directly with Emirates, but when they need a hotel in 15 different cities, local transportation, and activity bookings, they need aggregation. More importantly, suppliers need distribution—especially in emerging markets where direct channels are expensive to build.

What's emerging is a barbell market structure. At one end, mega-platforms like Booking.com serving consumers directly. At the other, specialized tools for direct supplier distribution. In the middle, where complexity lives, platforms like TBO thrive. They're the middleware of travel—unglamorous but essential, complex but valuable, hidden but indispensable.

XI. Playbook: Lessons for Founders & Investors

The conference room is silent except for the clicking of a keyboard. Gaurav pulls up a slide showing two growth trajectories: one labeled "Blitzscale," shooting up vertically then crashing; another labeled "TBO," climbing steadily upward. "This," he says, "is why we're still here when so many aren't."

The first lesson for founders is counterintuitive: in B2B platforms, slow is fast. B2B travel portal TBO Tek, which made a strong market debut in 2024, reported a 35% increase in its net profit to INR 200 Cr in FY24 from INR 148.4 Cr in the previous fiscal year. Operating revenue jumped 31% to INR 1,392.8 Cr from INR 1,064 Cr in FY23. These aren't hockey-stick numbers—they're compound growth rates that build empires.

Capital efficiency is the second playbook element. While competitors raised hundreds of millions, TBO bootstrapped for eleven years. When they did raise, it was strategic capital, not survival capital. The difference is crucial. Strategic capital accelerates a working model; survival capital props up a broken one. Operating profit margins witnessed stability at 18.9% in FY24—in a low-margin industry, consistent profitability is the real moat.

The importance of timing can't be overstated. TBO didn't invent B2B travel platforms—they entered when the infrastructure (internet penetration, payment systems, cloud computing) had matured enough to support their vision but before the market was saturated. They caught the wave at exactly the right moment: India's travel boom, global platform economics, and institutional capital looking for quality assets.

Managing institutional investors while maintaining founder control requires delicate balance. Post-issue, promoter stake reduced from 51% to 44%—enough dilution to provide liquidity, not enough to lose control. The key was performance. When you're delivering 26.7% ROCE, investors don't question strategy. When you're growing 30%+ annually while maintaining margins, boards don't micromanage.

The IPO strategy deserves its own MBA case study. The failed 2021 attempt wasn't failure—it was discipline. Walking away from a ₹2,100 crore IPO because market conditions weren't right showed maturity most founders lack. When they returned in 2024 with a smaller, more focused ₹1,550 crore offering, the market rewarded their patience with a 55% listing pop.

Building global from India requires a different mindset. You can't just transplant an Indian model globally—you need to build a global model that happens to originate from India. TBO's platform architecture, multi-currency capabilities, and culturally neutral design were global from day one. India wasn't their market; it was their laboratory.

For investors, the TBO story offers different lessons. First, look for platforms that own workflows, not just transactions. Second, value network effects over growth rates—dense networks compound, sparse networks collapse. Third, in B2B, customer retention matters more than customer acquisition. Fourth, profitable growth isn't an oxymoron—it's the only sustainable path.

XII. Analysis & Investment Thesis

The spreadsheet glows with numbers that tell two different stories. Bull case: global travel growing at 5% CAGR, TBO growing at 30%+, capturing market share in a $10 trillion industry. Bear case: AI enables direct distribution, China builds competing platforms, economic downturn crushes travel demand. The truth, as always, lies somewhere in between.

The bull thesis rests on structural tailwinds. Global travel isn't just recovering—it's transforming. Emerging market outbound travel, particularly from India and Southeast Asia, is still in early innings. TBO Tek cofounder and joint MD Gaurav Bhatnagar said, "Europe & APAC led the growth with 50%+ YoY growth." These aren't mature markets reaching saturation; they're nascent markets reaching inflection points.

Platform network effects provide the second pillar. We connect over 159,000 travel buyers across more than 100+ countries with millions of travel suppliers globally. Each new buyer makes the platform more valuable for suppliers; each new supplier makes it more valuable for buyers. Unlike consumer marketplaces where network effects can reverse quickly, B2B networks are sticky—switching costs are high, relationships matter, trust takes years to build.

The expansion opportunities are tangible, not theoretical. Current EBITDA of ₹3.16 B INR with EBITDA margin of 18.05% provides the cash flow for self-funded growth. Plans to invest in Europe and North America expansion with IPO proceeds aren't speculation—they're extending a proven playbook into new markets with similar dynamics.

But the bear case has teeth. Competition from legacy GDS systems isn't disappearing—Amadeus and Sabre are investing heavily in modernization. More concerning are the regional super-apps. If Grab in Southeast Asia or Paytm in India decide travel distribution matters, they have the user base and capital to compete aggressively.

Disintermediation risk is real but overstated. Yes, airlines want direct relationships, hotels want to own customers. But travel complexity is increasing, not decreasing. More suppliers, more products, more regulations, more payment methods—complexity creates opportunity for aggregators. The question isn't whether intermediation survives but what form it takes.

Dependency on travel industry health is the existential risk. COVID showed how quickly travel can evaporate. Wars, pandemics, economic crises—travel is discretionary spend that disappears first. But this risk is also priced in. At current valuations, the market isn't pricing in perfection.

The valuation analysis requires nuance. P/E ratio stands at 90.2 times trailing twelve months earnings—expensive by traditional metrics. But platform businesses don't trade on earnings multiples. They trade on growth, margins, and market opportunity. The price to sales ratio stands at 12.5 times—rich but not unreasonable for 30% growth with 18% EBITDA margins.

Peer comparison is challenging because true peers don't exist. Rategain focuses on hotels, Amadeus on airlines, Booking.com on consumers. TBO's unique position—B2B, multi-product, emerging market focused—makes it sui generis. Perhaps that's the biggest risk and opportunity: they're creating a category, not competing in one.

XIII. Future Vision & Strategic Initiatives

The strategy presentation opens with a map—not of countries but of connection points. Lines crisscross between Lagos and London, Jakarta and Dubai, Mexico City and Mumbai. "We're not building a travel company," Gaurav explains. "We're building the infrastructure for how the next billion people will experience the world."

The AI and personalization roadmap isn't about chatbots and recommendation engines—though those matter. It's about predictive inventory management, dynamic pricing optimization, and automated operations. TBO Tek cofounder said, "The company's tech and AI initiatives complement the rapid footprint expansion by helping drive better user experience and by improving platform performance." The vision: a platform that anticipates demand before it materializes, prices inventory before it's requested, and resolves issues before they're reported.

New product launches follow a careful sequence. The hotel business continued to drive the company's growth. Hotel and ancillary services contributed 79% to TBO Tek's overall revenue in FY25. The company rolled out a new booking platform H-Next during the quarter, plus TBO Platinum, featuring exclusive partnerships with luxury hotels for outbound travellers. Each product isn't a standalone offering but an integrated component of the platform ecosystem.

Vertical integration opportunities abound, but the approach is selective. Unlike consumer platforms that try to own every touchpoint, TBO focuses on where they add unique value. They won't become a hotel chain or airline, but they might build payment infrastructure, insurance products, or loyalty programs—services that enhance the platform without competing with suppliers.

The next decade of travel distribution will be defined by three forces: mobile-first emerging markets, artificial intelligence, and sustainability concerns. TBO is positioned for all three. Their platform already handles mobile traffic from markets where smartphones are the only computer. Their AI investments are showing results. And while sustainability isn't yet a revenue driver, it's becoming a selection criterion for corporate buyers.

Geographic expansion continues: In FY25, it expanded its global footprint to over 15 new markets, including Australia, France, Germany. But expansion isn't just about presence—it's about depth. Building local partnerships, understanding regional dynamics, adapting to local regulations. It's the difference between being global and being multinational.

"This gives us the confidence to maintain our expansion plans and aim for market leadership in the next 5-10 years," Bhatnagar said. Market leadership doesn't mean largest by revenue—it means defining how the industry operates. When small players want to go global, when new markets open up, when innovation happens in travel distribution, TBO wants to be the enabling platform.

XIV. Epilogue & Reflections

Mumbai airport, international departures, 2024. A family checks in for their first international vacation—Dubai, booked through their local travel agent who used TBO's platform. They don't know TBO exists. They don't need to. That invisibility isn't a bug—it's the feature. The best infrastructure disappears into the background, enabling experiences without announcing itself.

The surprises from the TBO story aren't in what happened but what didn't. They didn't pivot to B2C when investors pushed. Didn't blow up their unit economics chasing growth. Didn't sell out early when acquisition offers came. Didn't panic when the IPO window closed. Sometimes the most radical thing a startup can do is stay the course.

What this means for Indian B2B startups is profound. You don't need Silicon Valley venture capital to build a global platform. You don't need to burn billions to achieve scale. You don't need to copy Western models to serve emerging markets. You do need patience, discipline, and deep understanding of your domain. The TBO model—bootstrap, build, then raise strategic capital—might be the template for the next generation of Indian B2B unicorns.

The lessons on building global platforms from emerging markets are nuanced. First, emerging markets aren't just cheaper versions of developed markets—they have unique dynamics that create unique opportunities. Second, the constraints of emerging markets (payment friction, trust deficits, infrastructure gaps) force innovation that eventually benefits global operations. Third, talent arbitrage is real but temporary—build for the day when Indian engineers cost the same as Silicon Valley ones.

The future of travel distribution won't be winner-take-all. It will be a complex ecosystem of specialized platforms, each serving specific needs. TBO's bet is that the middle layer—between suppliers and retailers—will remain valuable because complexity isn't disappearing. If anything, travel is becoming more complex: more products, more suppliers, more regulations, more customer expectations.

Looking back at that founding moment in 2006—two entrepreneurs watching travel agents struggle with outdated systems—the journey seems inevitable. But inevitability is retrospective fiction. At every point, failure was more likely than success. What made the difference wasn't superior technology or better timing or more capital. It was the recognition that in every market inefficiency lies an opportunity, and in every intermediary scorned by technologists lies a business that might just need better tools.

The TBO story isn't finished. At ₹15,000+ crore market cap, they're still tiny compared to global travel giants. The next chapter—whether they become the Amadeus of emerging markets or get disrupted by the next wave of innovation—remains unwritten. But they've already proven something important: that Indian companies can build global infrastructure, that B2B platforms can be as valuable as consumer ones, and that sometimes, the best businesses are the ones customers never see.

Travel, after all, is about possibility—the chance to experience something new, to expand horizons, to connect across distances. TBO has built the pipes for those possibilities. Not glamorous, not viral, not disruptive in the traditional sense. Just essential. And in the end, isn't that what the best infrastructure always is?

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube