Tata Technologies: Engineering India's Digital Manufacturing Revolution

I. Introduction & Cold Open

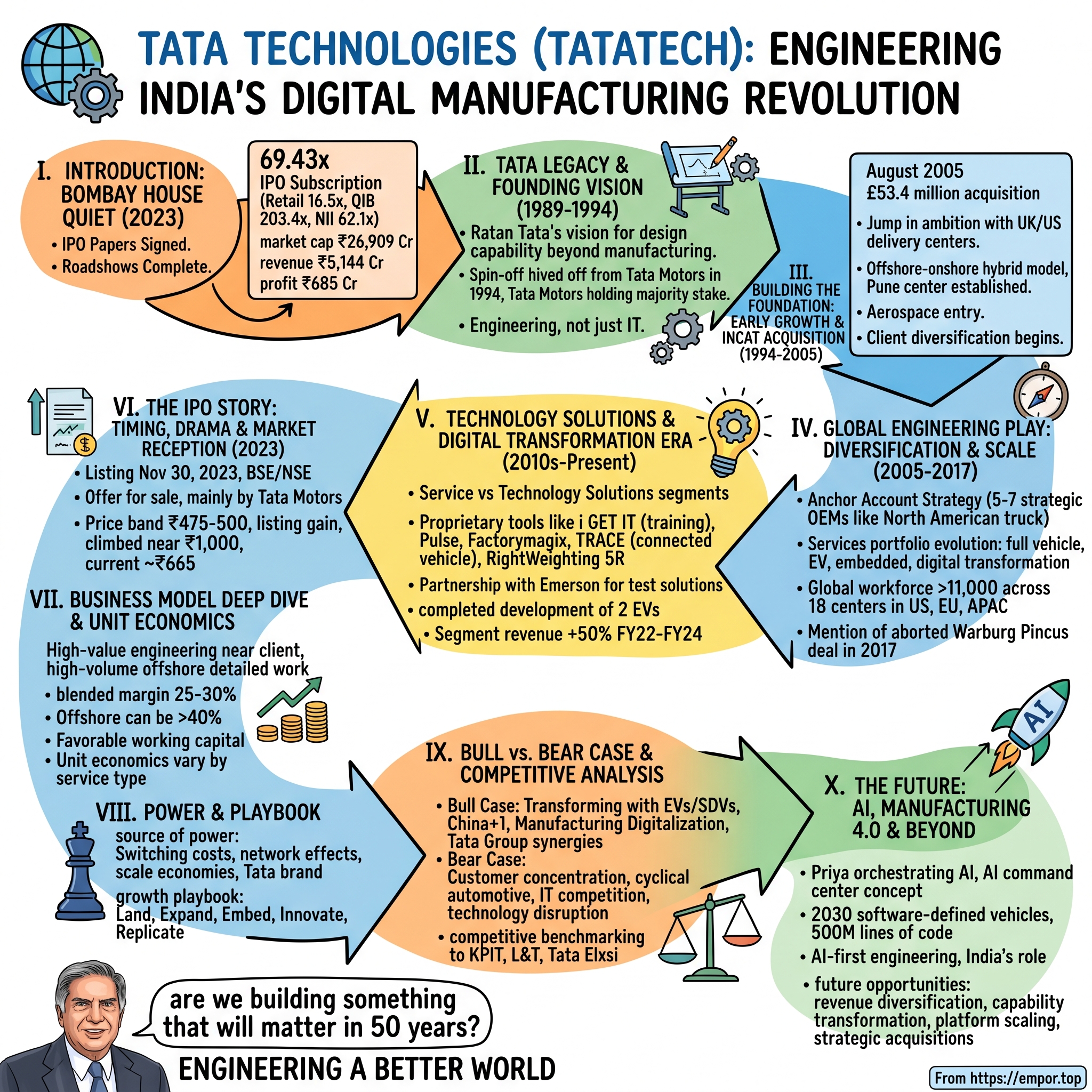

The conference room at Bombay House, Tata Group's colonial-era headquarters, was unusually quiet on a November morning in 2023. After nearly three decades of operating in the shadows of its more illustrious siblings—TCS, Tata Motors, Tata Steel—Tata Technologies was about to step into the spotlight. The IPO papers were signed, the roadshows complete. India's engineering services champion was finally going public.

But this wasn't just another listing. This was the Tata Group's first public offering in nearly two decades, since Tata Consultancy Services' blockbuster debut in 2004. The question hanging in the air: Why had this profitable, growing engineering services company stayed private for so long? And why go public now? The numbers told a stunning story: The IPO was subscribed 69.43 times overall—retail investors bid 16.5 times their allocation, qualified institutional buyers a staggering 203.41 times, and non-institutional investors 62.11 times. This wasn't just demand; it was validation decades in the making.

Today, Tata Technologies sits at a market capitalization of ₹26,909 crore, with revenues of ₹5,144 crore and profits of ₹685 crore—impressive metrics for a company that started as a captive engineering unit. But to understand how we got here, we need to go back to 1989, to the early days of India's automotive ambitions.

The journey from automotive design unit to global engineering powerhouse is a masterclass in patience, strategic positioning, and the art of building capability before scale. It's a story about choosing the harder path—engineering services over IT services—at a time when everyone else was rushing toward Y2K projects and software outsourcing. It's about staying private when going public was fashionable, and finally listing when the market was ready to understand your value.

Most importantly, it's a story about engineering the future—not just of vehicles, but of manufacturing itself. As we'll see, Tata Technologies didn't just ride the waves of automotive evolution; it helped create them. From the early days of CAD design to today's software-defined vehicles and electric powertrains, this company has been at the forefront of every major shift in how products are conceived, designed, and manufactured.

So buckle up. We're about to dive deep into one of India's most underappreciated business stories—a tale of engineering excellence that bridges the analog and digital worlds, connects Detroit to Pune, and transforms metal and code into mobility solutions. This is the Tata Technologies story.

II. The Tata Legacy & Founding Vision (1989-1994)

Picture the Tata Motors plant in Pune, 1989. The assembly lines hummed with the production of commercial vehicles—sturdy trucks and buses that formed the backbone of India's transportation infrastructure. But in a corner office, away from the factory floor, a small team of engineers huddled over drafting tables and early CAD terminals. They weren't building vehicles; they were reimagining how vehicles could be designed.

This was the nascent automotive design unit of Tata Motors, a department that most executives saw as a cost center—necessary but not strategic. India's automotive industry in 1989 was still largely about licensed production and incremental modifications. Original design work? That happened in Detroit, Stuttgart, and Tokyo, not Pune.

But Ratan Naval Tata saw something different. Fresh from his battles modernizing Tata Steel and with ambitious plans for Tata Motors, he recognized that true automotive independence meant more than just manufacturing capability. It meant design capability. Engineering capability. The ability to conceive and create, not just assemble and adapt."I would like to see Tata Technologies being acclaimed as one of the more innovative and successful design companies in the world," Ratan Tata would later say, articulating a vision that seemed almost fantastical for a company operating out of India in the early 1990s. But this wasn't hubris—it was strategic foresight.

The company was envisioned by the then-Tata Group chairman, Mr. Ratan Naval Tata, who saw an opportunity in the evolving product engineering and manufacturing IT space. While the rest of India's IT industry was racing toward Y2K remediation and basic software services, Ratan Tata was playing a different game entirely. He understood that manufacturing was about to undergo a digital revolution, and that the companies that could bridge the physical and digital worlds would hold immense strategic value.

The decision to spin off the design unit as a separate entity in 1994 was both bold and counterintuitive. Tata Technologies was founded in 1989, as the automotive design unit of Tata Motors. It was hived off as a separate company in 1994, with Tata Motors continuing to hold a majority stake and be its biggest client. Most automakers globally were consolidating their engineering capabilities in-house. General Motors had its massive Technical Center in Warren, Michigan. Toyota had its engineering stronghold in Toyota City. Why would Tata Motors divest its engineering capability?

The answer lay in Ratan Tata's understanding of specialization and scale. A captive engineering unit would always be limited by the parent company's product development cycles and budgets. But an independent engineering services company could serve multiple clients, build diverse capabilities, and achieve the scale necessary to invest in cutting-edge tools and talent. It could also, theoretically, become a profit center rather than a cost center.

India's manufacturing ecosystem in the 1990s provided both the challenge and the opportunity. The country was just beginning to liberalize its economy. Foreign automakers were entering through joint ventures. The demand for engineering services was about to explode, but the supply of skilled engineers who understood both traditional mechanical engineering and emerging digital tools was limited.

This was where the Tata legacy became crucial. The group's reputation for ethical business practices and long-term thinking meant that potential clients—both domestic and international—would trust them with sensitive product development work. The Tata name opened doors that would have remained closed to a startup.

But having a famous surname wasn't enough. The newly independent Tata Technologies needed to build real capabilities, fast. The company began investing heavily in CAD/CAM tools, sending engineers abroad for training, and establishing processes that could match international quality standards. This wasn't just about learning to use software—it was about understanding how digital tools could fundamentally transform the product development process.

The strategic positioning was critical: Tata Technologies would not compete with IT services giants like TCS (its own group company) or Infosys in the software services space. Instead, it would focus on the intersection of engineering and IT—a space that required deep domain knowledge in manufacturing, not just coding skills. This was engineering services, not IT services, and that distinction would prove crucial.

As 1994 drew to a close, Tata Technologies stood at the threshold of opportunity. The global automotive industry was beginning to embrace outsourcing. India had the engineering talent. The digital revolution in manufacturing was just beginning. All the pieces were in place. Now came the hard part: execution.

III. Building the Foundation: Early Growth & INCAT Acquisition (1994-2005)

The conference room at INCAT International's UK headquarters hummed with nervous energy in August 2005. On one side sat the British management team of a company that had quietly built a reputation as one of Europe's premier automotive and aerospace engineering firms. On the other, the Tata Technologies leadership, checkbook in hand, ready to make their boldest move yet.

£53.4 million. That was the price tag for INCAT—a figure that made some board members back in Mumbai gulp. For context, this was more than Tata Technologies' annual revenue at the time. But what INCAT offered wasn't just revenue or clients. It was a bridge to the future.

Tata Technologies Inc acquired INCAT International, a UK-and US-based automotive and aerospace engineering company, in August 2005 for £53.4 million. The acquisition represented a quantum leap in ambition. INCAT brought with it established relationships with blue-chip automotive and aerospace clients, delivery centers in the UK and US, and most importantly, credibility in markets where an Indian engineering services company was still viewed with skepticism.

But we're getting ahead of ourselves. To understand why the INCAT acquisition was so transformative, we need to first understand what Tata Technologies built in its first decade of independence.

The early years were defined by a singular focus: becoming indispensable to Tata Motors. This might seem unambitious, but it was strategically brilliant. Tata Motors served as a demanding client that pushed Tata Technologies to constantly upgrade its capabilities. Every new vehicle program became a learning laboratory. The Indica, India's first indigenously developed passenger car launched in 1998, saw Tata Technologies engineers working on everything from styling to engineering analysis.

During this period, the company made a crucial organizational decision that would define its delivery model for decades: the offshore-onshore hybrid approach. While competitors were pushing for maximum offshoring to leverage India's cost advantages, Tata Technologies recognized that engineering services required a different model. Design reviews, prototype testing, and supplier coordination needed physical presence near the client. But detailed engineering, analysis, and documentation could be done from India.

The company established its first offshore delivery center in Pune, equipped with high-speed data links (a significant investment in the late 1990s) and the latest CAD/CAM software. Engineers in Pune could work on designs during Indian daytime, hand them off to colleagues in Detroit or Stuttgart who would continue the work, creating a "follow-the-sun" model that accelerated development cycles.

But serving just Tata Motors, even with its growing ambitions, wouldn't provide the scale needed for global competitiveness. The company began carefully expanding its client base, initially targeting Tata Motors' joint venture partners and suppliers. Each new client was a test case, proving that an Indian company could handle sensitive product development work.

The talent strategy during this period was equally important. Tata Technologies wasn't just hiring engineers; it was building a new category of professional—the offshore engineering specialist. These were engineers who could navigate both the technical complexities of product development and the cultural nuances of working with global clients. The company established extensive training programs, including stints at client locations, to build this hybrid capability.

By 2004, the company had grown to nearly 2,000 engineers and was generating steady profits. But the leadership knew they had hit a ceiling. Breaking into the top tier of global OEMs required more than organic growth. It required a bold acquisition that would provide instant credibility and capabilities.

Enter INCAT International. Founded in the UK with operations in the US, INCAT had spent decades building relationships with premium automotive brands and aerospace companies. Their client list read like a who's who of the automotive industry. But INCAT faced its own challenges—scale limitations and the need for offshore leverage to remain competitive.

The negotiation process was complex. INCAT's shareholders were skeptical about selling to an Indian company. Would clients accept Indian ownership? Would key employees stay? Tata Technologies had to sell not just a price but a vision—combining INCAT's client relationships and domain expertise with Tata Technologies' offshore delivery capabilities and the backing of the Tata Group.

The deal structure was clever. Rather than a hostile takeover, it was positioned as a partnership, with INCAT's senior management staying on and maintaining significant operational autonomy. The message to clients was clear: you're getting the same INCAT quality, now with additional capabilities and scale.

The integration post-acquisition was handled with unusual sensitivity. Rather than immediately pushing for offshoring and cost reduction, Tata Technologies focused first on cultural integration and capability building. Joint teams were formed for new projects. Best practices were shared bidirectionally. INCAT's project management expertise was adopted across Tata Technologies, while INCAT gained access to the offshore delivery infrastructure.

The aerospace entry through INCAT was particularly strategic. Aerospace engineering services required even higher standards of quality and documentation than automotive. AS9100 certification, stringent IP protection, and the ability to work on safety-critical systems—INCAT brought all of this. It opened doors that would have taken Tata Technologies decades to unlock organically.

Within months of the acquisition, the combined entity was winning deals that neither company could have won alone. A European OEM needed engineering support for a new vehicle platform but wanted both onsite presence and offshore leverage. An aerospace company required specialized stress analysis but at a price point that only offshore delivery could achieve. The INCAT acquisition had transformed Tata Technologies from an India-centric engineering services provider to a global player.

By the end of 2005, Tata Technologies had crossed several psychological barriers. It was no longer just a Tata Motors supplier but a company serving multiple global OEMs. It had operations across three continents. It had capabilities spanning automotive and aerospace. Most importantly, it had proven that an Indian company could successfully acquire and integrate a Western engineering services firm.

The foundation was now in place for the next phase of growth—one that would see the company truly diversify its client base and build capabilities that went beyond traditional engineering services into the digital transformation of manufacturing.

IV. The Global Engineering Play: Diversification & Scale (2005-2017)

Warren Buffett once said that diversification is protection against ignorance. But for Tata Technologies in the mid-2000s, diversification was protection against dependency. By 2006, despite the INCAT acquisition, Tata Motors and its ecosystem still accounted for over 60% of revenues. The company needed to solve this concentration risk, but without alienating its most important client.

The solution came through what internally became known as the "anchor account strategy"—a methodical approach to building deep, strategic relationships with a select group of global OEMs rather than chasing every available contract. Each anchor account would be cultivated over years, starting with small, non-critical projects and gradually expanding to mission-critical product development work. The first major breakthrough came with a North American truck manufacturer. Starting with a small contract for cab interior design in 2007, Tata Technologies gradually expanded its scope to include complete vehicle engineering. By 2010, it was handling the entire product development for a new medium-duty truck platform—from concept to production support. The success of this program became a template for expansion with other OEMs.

The services portfolio during this period underwent dramatic evolution. Services include software-defined vehicle, end to end electric vehicle engineering, turnkey full vehicle development, embedded engineering solutions, HIL testing and validation, model-based systems engineering, digital transformation, and smart manufacturing solutions. This wasn't just capability building for the sake of it—each new service line addressed a specific pain point for manufacturers navigating the digital transformation of their industry.

Regional headquarters in the United States (Detroit, Michigan) became the nerve center for North American operations. Detroit wasn't chosen by accident—it put Tata Technologies at the heart of the global automotive industry, close to decision-makers and development centers. The company established similar strategic presences in Stuttgart for the European market and expanded its footprint in Asia-Pacific.

By 2015, the company had achieved remarkable geographic and client diversification. As of 2023, the company has a combined global workforce of more than 11,000 employees across its 18 delivery centres in India, North America, Europe and the Asia-Pacific region. But this growth wasn't just about adding headcount—it was about building specialized capabilities in emerging areas like electric vehicle engineering, autonomous vehicle systems, and industrial IoT.

Then came the Warburg Pincus episode—a deal that would have fundamentally transformed the company's ownership structure and growth trajectory. In 2017, Tata Group announced it would sell a 43% stake to private equity firm Warburg Pincus for $360 million. The transaction valued Tata Technologies at approximately $837 million, a significant premium to its book value.

An affiliate of Warburg Pincus, a leading global private equity firm focused on growth investing, has committed to invest around US$360 million for approximately 43% equity stake in Tata Technologies Limited. The strategic logic was compelling. Warburg Pincus brought not just capital but also expertise in scaling engineering services businesses globally. They had successfully invested in similar companies and understood the sector's dynamics.

For Tata Motors, which was dealing with significant debt from the Jaguar Land Rover acquisition, the partial divestment offered a way to monetize value while retaining a strategic stake. For Tata Technologies, it meant access to growth capital and the potential for aggressive expansion, both organic and through acquisitions.

Warren Harris, then CEO of Tata Technologies, captured the moment's significance: "This investment is a testament to our achievements to date and, more importantly, of our great potential moving forward. As the engineering services outsourcing (ESO) market has matured from cost arbitrage and staff augmentation to increasingly high-end, strategic work, Tata Technologies has been there leading the charge".

But the deal that seemed destined to close hit unexpected headwinds. However, the deal was called off in 2018. The deal worth around Rs 2,320 crore has been called off due to "delays in securing regulatory approval and the recent performance of the company not meeting internal thresholds because of market challenges".

The failed transaction was a pivotal moment. It forced Tata Technologies to confront hard questions about its future. Could it achieve its growth ambitions without private equity backing? Should it continue as a subsidiary of Tata Motors, or seek independence through other means? The answers to these questions would shape the company's next chapter.

During this period, the company also built significant capabilities in digital manufacturing solutions. The acquisition of smaller specialized firms, partnerships with technology providers, and internal R&D investments created a portfolio of proprietary tools and platforms. These weren't just service offerings—they were products that could be licensed and deployed across multiple clients, creating recurring revenue streams.

The offshore leverage model reached new levels of sophistication. The company could now handle entire vehicle programs with minimal onsite presence, using digital collaboration tools, virtual reality for design reviews, and cloud-based project management systems. This dramatically improved margins while maintaining quality—a holy grail in the engineering services industry.

By 2017, despite the Warburg Pincus setback, Tata Technologies had transformed itself into a formidable player in the global engineering services market. Revenue had grown to over ₹2,800 crore. The client base included most major automotive OEMs. The service portfolio spanned the entire product lifecycle. The stage was set for the next act—one that would see the company embrace digital transformation not just as a service provider, but as a technology innovator.

V. Technology Solutions & Digital Transformation Era (2010s-Present)

The AutoCAD screen flickered in the dimly lit training room at Tata Technologies' Pune facility. It was 2010, and instructor Rajesh Sharma was teaching a batch of fresh engineering graduates the basics of 3D modeling. "Someday," he mused to his students, "engineers won't just learn from instructors like me. They'll learn from AI, at their own pace, anywhere in the world." His students laughed. It seemed far-fetched.

Fast forward to 2020, and that same Rajesh was leading the development of i GET IT, Tata Technologies' online training platform for self-paced courses. The platform had trained over 100,000 engineers globally, generating a new revenue stream while solving a critical industry problem: the massive skill gap in digital manufacturing technologies.

This transformation—from service provider to technology solution creator—defines Tata Technologies' current era. The company recognized that pure engineering services, no matter how sophisticated, would eventually commoditize. The future lay in proprietary technology solutions that could scale beyond linear growth.

The journey began with a fundamental reorganization. Operating through Service and Technology Solutions segments, the company created clear boundaries between traditional engineering services and emerging digital solutions. This wasn't just organizational reshuffling—it was a statement of intent. Technology solutions would no longer be an add-on to services; they would be a distinct, high-margin business. The proprietary tools portfolio reads like a manufacturing technologist's wish list. Pulse, an agile product data and management tool; Factorymagix, a manufacturing execution system tool; and AMP.IoT, a suite of modular applications designed to cater to the Industrial IOT requirements of the manufacturing industry. Each tool addressed a specific pain point in the manufacturing value chain, but more importantly, they were designed to work together, creating an integrated ecosystem.

TRACE, a connected vehicle platform that helps OEMs to develop and deliver end-to-end connected services, became particularly strategic as vehicles transformed from mechanical products to rolling computers. The platform wasn't just about telematics—it was about creating new revenue streams for OEMs through services, predictive maintenance, and over-the-air updates.

RightWeighting 5R, a solution that enables manufacturing companies to optimize weight and engineer products, showcased the company's ability to combine engineering expertise with algorithmic optimization. In industries where every gram matters—automotive for fuel efficiency, aerospace for payload—this tool delivered measurable ROI.

The electric vehicle revolution presented perhaps the biggest opportunity. Our end-to-end solutions for future EVs cover engineering, manufacturing, and post-sales service to deliver a great experience to the digital customer of the future and help manufacturers perform in the marketplace. Tata Technologies wasn't just offering EV engineering services; it was providing complete turnkey solutions that could help traditional OEMs rapidly enter the EV market.

In FY24, completed development of 2 EVs for a SEA-based automotive OEM. Segment revenue grew by 50% between FY22 and FY24. These weren't just design exercises—they were complete vehicle programs from concept to production, demonstrating that Tata Technologies could compete with established engineering houses in Europe and Japan.

The software-defined vehicle (SDV) capability became a crucial differentiator. Our software-defined vehicle offerings integrate next-gen technologies with full vehicle systems to deliver elevated customer experiences and new revenue streams for clients. As vehicles increasingly became platforms for software services, Tata Technologies positioned itself at the intersection of mechanical engineering and software development—a space few competitors could credibly occupy. Strategic partnerships amplified these capabilities. Tata Technologies and Emerson (NYSE: EMR) today jointly announced a strategic partnership to innovate integrated testing and validation solutions for global OEMs in the automotive, aerospace and commercial vehicle sectors. By combining Tata Technologies' deep expertise in systems engineering, E/E architecture, and mobility platform development with Emerson's industry-leading, software-connected test and measurement solutions, this partnership aims to empower manufacturers to tackle the complexities of next-generation mobility.

The results were immediate and impressive. In one engagement with a European luxury original equipment manufacturer, the partnership developed electric vehicle powertrain test rigs in five months, representing a 67% reduction from typical 15 month timelines. This wasn't just about speed—it was about fundamentally reimagining how testing and validation could be done in the age of software-defined vehicles.

The i GET IT platform deserves special attention as a case study in platform thinking. What started as an internal training initiative to upskill engineers became a commercially viable product serving the global manufacturing industry. The platform leveraged Tata Technologies' deep domain knowledge to create courses that were immediately applicable to real-world engineering challenges. It solved a critical industry problem—the shortage of engineers skilled in emerging technologies—while creating a high-margin, recurring revenue stream.

The digital transformation services weren't just about implementing technology; they were about reimagining manufacturing processes. When a traditional automotive supplier needed to transform its factories for Industry 4.0, Tata Technologies didn't just install IoT sensors and analytics software. It redesigned the entire manufacturing flow, integrated legacy systems with new digital platforms, and trained the workforce to operate in this new environment.

By 2020, the Technology Solutions segment was contributing an increasingly significant portion of revenue and an even higher portion of profits. The margins on proprietary software and platforms far exceeded traditional engineering services. More importantly, these solutions created stickiness—once a client adopted a Tata Technologies platform, switching costs were high.

The COVID-19 pandemic, rather than slowing this transformation, accelerated it. As physical prototyping became difficult, virtual validation became essential. As supply chains disrupted, digital twins became critical for scenario planning. Tata Technologies' investments in digital solutions positioned it perfectly for this new reality.

The company also made strategic acquisitions and partnerships to fill capability gaps. Small software companies with specialized capabilities in areas like generative design or AI-driven optimization were acquired and integrated into the platform portfolio. Partnerships with cloud providers enabled the delivery of solutions as services, reducing capital requirements for clients.

This era also saw a fundamental shift in how Tata Technologies positioned itself in the market. No longer was it just an engineering services provider competing on cost and quality. It was now a technology company that happened to have deep engineering expertise—a crucial distinction in terms of valuation multiples and growth potential.

The transformation wasn't without challenges. Building software products required different skills than providing engineering services. The sales cycle for platform solutions was longer and more complex than for services. Competition came not just from traditional engineering services companies but also from software giants entering the manufacturing space.

But by 2023, as the company prepared for its IPO, the Technology Solutions strategy had proven its worth. The company had successfully transformed from a linear services business to one with platform leverage, recurring revenues, and global scale. The stage was set for the next chapter—going public and using capital markets to accelerate growth even further.

VI. The IPO Story: Timing, Drama & Market Reception (2023)

The Morgan Stanley conference room in Mumbai was packed beyond capacity on a humid October morning in 2023. Investment bankers, lawyers, and Tata Technologies executives huddled over spreadsheets, debating a number that would define the company's public market debut: the price band. After decades of building value in private, the moment of truth had arrived.

"We need to price this for success, not ego," Warren Harris, the CEO, insisted. The bankers wanted an aggressive price—after all, this was the Tata Group's first IPO in nearly two decades. The market was hungry. But Harris and the board remembered the lessons from other hyped listings that had stumbled. They settled on ₹475-500 per share—a range that valued the company richly but not recklessly.

The timing seemed perfect. India's capital markets were on fire. The country had just become the world's fifth-largest economy. Manufacturing was having a moment, with "Make in India" and "China+1" narratives dominating boardroom discussions. And here was Tata Technologies—a pure play on India's manufacturing and engineering capabilities, backed by the country's most trusted business house.

Tata Technologies IPO bidding started from Nov 22, 2023 and ended on Nov 24, 2023. The shares got listed on BSE, NSE on Nov 30, 2023. Tata Technologies IPO price band is set at ₹500.00 per share.

The structure was notable for what it wasn't—a fresh capital raise. Tata Technologies IPO is a main-board IPO of 6,08,50,278 equity shares of the face value of ₹2 aggregating up to ₹3,042.51 Crores. This was entirely an offer for sale, with existing shareholders—primarily Tata Motors—partially cashing out. The message was clear: the company didn't need capital; it needed currency for acquisitions and employee stock options.

The roadshow was a masterclass in storytelling. Instead of dry presentations about revenue and margins, the management team brought demos. They showed a European OEM's electric vehicle that Tata Technologies had helped design. They demonstrated the TRACE platform connecting vehicles in real-time. They walked investors through a virtual factory powered by their digital solutions. This wasn't just an engineering services company; this was the future of manufacturing.

Retail investors were given special attention. Tata Motors and Tata Motors DVR shareholders are eligible to apply for Tata Tech IPO under the shareholder reservation quota. To be eligible to apply in the shareholder quota, you must be company's existing shareholder by record date i.e., 13 Nov 23 or you must have Tata Motors or Tata Motors DVR shares in your Demat account by 13 Nov 23. This created a sense of inclusion—existing Tata Motors shareholders could participate in the value creation of its most promising subsidiary.

Then came the subscription period, and the numbers were staggering. The Tata Technologies IPO is subscribed 69.43 times by Nov 24, 2023 19:02. Retail category of Tata Technologies IPO subscribed 16.5 times as of date Nov 24, 2023 19:02. The public issue subscribed 16.5 times in the retail category, 203.41 times in the QIB category, and 62.11 times in the NII category.

The QIB subscription of 203.41 times was particularly telling. These were sophisticated institutional investors—mutual funds, insurance companies, foreign portfolio investors—who had done their homework. They saw what retail investors might have missed: this wasn't just another IPO riding the market wave. This was a strategic asset in India's manufacturing transformation story.

Behind the scenes, the allocation process was complex. With such massive oversubscription, most retail investors would get only a fraction of what they bid for. The company and bankers worked to ensure a balanced shareholder base—enough institutions for stability, enough retail for liquidity, and enough high-net-worth individuals for support during volatility.

November 30, 2023—listing day. The pre-open session showed enormous buying interest. When regular trading began, the stock opened at ₹500, exactly at the upper end of the price band. No dramatic pop, no disappointing drop—just a steady, confident debut. By the end of the first day, it had gained modestly, closing around ₹515.

But the real story unfolded over the following weeks. The stock climbed steadily, reaching ₹995 by early 2024—nearly a 100% gain from the issue price. The market was validating not just the IPO pricing but the entire Tata Technologies story. Analysts who had been skeptical about the valuation were upgrading their targets. The company was being re-rated from an engineering services multiple to something approaching a technology company valuation.

The post-IPO performance revealed interesting dynamics. On days when IT services stocks fell, Tata Technologies often held steady—the market was treating it as a differentiated play. When electric vehicle stocks globally rallied, Tata Technologies caught the updraft—investors saw it as a derivative play on the EV revolution without the execution risk of actual vehicle manufacturing.

From ₹500 listing to current ~₹665 represents a complex journey. After hitting peaks near ₹1,000, the stock corrected along with broader market volatility. The 33% decline from peak wasn't company-specific—global factors, including rising interest rates and concerns about automotive sector slowdown, weighed on the stock.

The IPO proceeds' deployment became a focus area for investors. While the company didn't raise fresh capital, the public listing provided it with acquisition currency. Stock options could now be offered to attract talent from competitors. The quarterly earnings calls became platforms to articulate strategy to a broader audience.

The market's initial embrace validated several strategic decisions. The focus on technology solutions over pure services was rewarded with higher multiples. The diversification beyond Tata Motors was appreciated—client concentration risk had been a key concern. The exposure to high-growth areas like EVs and SDVs justified premium valuations.

But the public market also brought new pressures. Quarterly earnings volatility, which could be smoothed in private ownership, now triggered stock price swings. Large project wins or losses became material events requiring disclosure. The comparison with listed peers like KPIT Technologies and L&T Technology Services became constant.

The Tata brand premium was evident but not overwhelming. While the Tata name certainly helped in the IPO subscription, the post-listing performance showed that markets would judge the company on its own merits. The legacy was a door opener, not a permanent valuation prop.

For the Tata Group, the IPO served multiple purposes. It provided a partial exit for Tata Motors at an attractive valuation. It created a separately listed entity that could pursue its own growth strategy. Most importantly, it validated the group's ability to create value in new-age businesses, not just traditional industries.

The IPO also marked a generational transition. The company that Ratan Tata had envisioned in 1994 was now a public entity, accountable to thousands of shareholders. The entrepreneurial phase was over; the institutional phase had begun. This transition, while necessary for scale, would test the company's ability to maintain its innovation edge while meeting quarterly expectations.

VII. Business Model Deep Dive & Unit Economics

Picture two conference rooms, 8,000 miles apart. In Detroit, a team of Tata Technologies engineers sits with client executives from a major OEM, reviewing design modifications for a next-generation electric pickup truck. Simultaneously, in Pune, 50 engineers are running computational fluid dynamics simulations on the same vehicle, optimizing aerodynamics for range improvement. This scene, replayed thousands of times across different projects, captures the essence of Tata Technologies' business model.

The model is deceptively simple yet operationally complex: high-value engineering work done close to the client, high-volume detailed engineering done offshore, all orchestrated through proprietary platforms and processes. But the devil, and the margins, lie in the details. Business Segments: Services (78% in H1 FY25 vs 75% in FY22). The services segment revenue grew by 50% between FY22 and FY24, driven by new business wins with its anchor and non-anchor accounts. This shift toward services isn't just about proportion—it's about margin quality. Services carry higher margins than technology solutions (primarily software reselling), creating a favorable mix shift.

The anchor account strategy deserves deeper examination. Rather than spreading resources across hundreds of small clients, Tata Technologies focuses on 5-7 anchor accounts that each generate over $50 million in annual revenue. These aren't just large contracts; they're strategic partnerships where Tata Technologies becomes embedded in the client's product development process.

Take a typical anchor account relationship: It might start with a $5 million contract for engineering support on a specific vehicle program. Over 3-5 years, this expands to include multiple programs, then moves into adjacencies like digital factory solutions, and eventually encompasses strategic initiatives like EV platform development. The lifetime value of an anchor account can exceed $500 million.

The offshore leverage model is where the economics become compelling. For every onsite engineer billing at $150-200 per hour, there are 3-4 offshore engineers billing at $40-60 per hour but costing the company $15-20 per hour. The blended margin on a typical project runs 25-30%, but the offshore portion can generate margins exceeding 40%.

Working capital dynamics are surprisingly favorable for an engineering services business. The company typically operates on 30-45 day payment terms with clients while managing 60-90 day payment cycles with employees (through monthly payroll). This negative working capital cycle means growth actually generates cash rather than consuming it—a rare advantage in the services industry.

The competition landscape shapes pricing power. Against IT services firms (TCS, Infosys) entering ER&D, Tata Technologies commands a premium due to domain expertise. A TCS might offer engineering services at $35-45 per hour offshore; Tata Technologies gets $40-60 for similar work because of specialized knowledge. Against pure-play ER&D competitors (KPIT, L&T Tech), pricing is more competitive, but Tata Technologies differentiates through its integrated service offering.

Customer concentration remains a double-edged sword. While anchor accounts provide stability and deep margins, they also create vulnerability. Tata Motors and its ecosystem still represent approximately 25-30% of revenue. A downturn at Tata Motors directly impacts Tata Technologies—as seen during JLR's challenges in 2018-2019 when revenue growth stalled.

The Technology Solutions segment operates on a different model. Software reselling generates lower margins (15-20%) but requires minimal working capital and creates recurring revenue streams through licenses and maintenance contracts. The proprietary platforms like i GET IT operate on a SaaS model with 70%+ gross margins once development costs are recovered.

Unit economics vary dramatically by service type. A traditional engineering service project might generate ₹15-20 lakhs revenue per engineer per year with 25% EBITDA margins. A digital transformation project using proprietary tools can generate ₹25-30 lakhs per engineer with 35% margins. Pure software platform revenues can achieve 60%+ margins but represent a smaller portion of total revenue.

Geographic mix impacts profitability significantly. North American clients pay premium rates but require more onsite presence, reducing margins. European clients accept higher offshore ratios but negotiate harder on rates. Asian clients, particularly in emerging markets, offer volume but at lower price points. The optimal mix—achieved through careful portfolio management—targets 40% Americas, 35% Europe, 25% Asia.

The investment cycle in this business is often misunderstood. Unlike IT services where talent is the primary investment, engineering services require significant upfront investment in tools, training, and domain knowledge. Entering a new domain (say, aerospace) might require 2-3 years of investment before achieving profitability. This creates barriers to entry but also limits how quickly Tata Technologies can diversify.

Scalability challenges are real. While software businesses can scale exponentially, engineering services scale linearly with headcount. The company has addressed this through "productization" of services—creating standardized methodologies, reusable components, and automated tools that improve per-engineer productivity. But fundamental limits remain.

The margin structure reveals strategic priorities. EBITDA margins of 18-20% are healthy but not exceptional for the industry. The company could potentially achieve 25%+ margins by focusing solely on high-margin offshore work. But this would sacrifice strategic positioning in emerging areas like EVs and SDVs. The current margin level represents a conscious choice to invest in future growth areas.

Currency dynamics add complexity. With costs primarily in INR and revenues significantly in USD and EUR, the company benefits from rupee depreciation. A 5% rupee depreciation can add 100-150 basis points to margins. But this also creates volatility that must be managed through hedging strategies.

The cash generation profile is robust. With minimal capital expenditure requirements (primarily computers and software licenses) and favorable working capital dynamics, the company converts 70-80% of EBITDA to free cash flow. This supports a dividend payout ratio of 70%, among the highest in the industry.

Looking forward, the business model faces both opportunities and challenges. The shift toward EVs and SDVs favors companies with integrated engineering and software capabilities. But it also requires continuous investment in new capabilities. The key question isn't whether Tata Technologies can maintain current margins, but whether it can capture enough of the value creation in the automotive industry's transformation to justify premium valuations. The answer to that question will determine whether the company remains a solid dividend-paying engineering services provider or transforms into a high-growth technology company.

VIII. Power & Playbook

In the heart of Stuttgart, at the headquarters of a premium German automaker, a crisis unfolded in 2019. The company's ambitious electric vehicle program was six months behind schedule. Software and hardware teams weren't communicating effectively. The traditional automotive engineers didn't understand software development cycles, while the software developers didn't appreciate the complexities of automotive safety standards.

Enter Tata Technologies. Within three weeks, they had deployed a 50-person integrated team that spoke both languages—automotive and software. More importantly, they brought something intangible: trust earned over a decade of successful projects. Six months later, the program was back on track. The German automaker hasn't worked with another engineering services provider since.

This story illustrates Tata Technologies' primary source of power: switching costs that go far beyond the financial. When an OEM embeds an engineering partner into its product development process, the relationship becomes symbiotic. The partner knows the client's tools, processes, standards, even the undocumented tribal knowledge. Replacing them isn't just expensive—it's risky.

Consider what switching really means. Tata Technologies engineers often have access to the client's most sensitive information: future product plans, proprietary technologies, supplier networks. They use client-specific tools and follow client-specific processes developed over years. A new provider would need 12-18 months just to reach baseline productivity. In the fast-moving automotive industry, that delay could mean missing a entire product cycle.

The network effects in engineering services are subtle but powerful. Unlike consumer platforms where network effects are obvious, Tata Technologies' network value comes from the interconnections between capabilities. The more automotive programs they execute, the better their automotive expertise. The better their expertise, the more programs they win. This expertise network effect compounds over time.

But there's another network at play—the talent network. Engineering talent clusters around companies doing the most interesting work. As Tata Technologies wins cutting-edge EV and autonomous vehicle programs, it attracts the best engineers. These engineers bring relationships and knowledge from previous employers, expanding the company's capability network. This creates a virtuous cycle that's hard for competitors to break.

Scale economies in engineering services differ from manufacturing. It's not about spreading fixed costs over more units—it's about the economics of specialization. At 11,000 engineers, Tata Technologies can afford to have specialists in obscure but critical areas. They might have five engineers who are experts in electromagnetic compatibility for electric vehicles. A smaller competitor can't afford such specialization, so they either can't bid for certain projects or must do them less efficiently.

The global delivery infrastructure represents another scale advantage. Tata Technologies operates 18 delivery centers across four continents. Setting up a single delivery center requires millions in investment, years of relationship building, and complex legal and compliance work. This infrastructure isn't just about cost—it's about following the sun, providing 24/7 support, and being physically present where clients need you.

The brand power of Tata in manufacturing circles shouldn't be underestimated. In an industry where failure can mean recalls, lawsuits, and destroyed reputations, the Tata name provides comfort. It signals stability, ethics, and longevity. When a Chief Technology Officer recommends Tata Technologies to the board, they're making a safe choice. Nobody gets fired for hiring Tata.

But brand works differently in B2B than B2C. It's not about emotional connection—it's about risk mitigation. The Tata brand says: "We've been around for 150 years. We'll be here tomorrow. We won't steal your IP. We won't poach your employees. We won't embarrass you." In the conservative world of automotive manufacturing, these assurances matter enormously.

Counter-positioning against IT services firms is perhaps Tata Technologies' cleverest strategic move. When TCS or Infosys pitch engineering services, they position it as an extension of IT services—"We do your IT, we can do your engineering too." Tata Technologies counters: "We're engineers who understand software, not software people trying to learn engineering."

This positioning resonates because it's true. Mechanical engineering, electrical engineering, and manufacturing engineering require years of specialized education and experience. You can't retrain a Java developer to design automotive suspension systems. By positioning itself as engineering-first, Tata Technologies makes IT services firms' engineering offerings seem superficial.

The "Engineering a Better World" narrative ties everything together. It's not just marketing—it's a strategic framework that guides decision-making. When evaluating new opportunities, the question becomes: Does this help us engineer a better world? This clarity helps avoid the strategic drift that plagues many services companies.

The playbook for growth follows a consistent pattern:

- Land: Win a small, low-risk project with a new client

- Expand: Demonstrate competence, build trust, expand to adjacent areas

- Embed: Become integral to client's development process

- Innovate: Bring new capabilities and solutions to solve emerging problems

- Replicate: Use learnings from one client to win similar work with others

This playbook worked with Tata Motors in the 1990s, with North American truck manufacturers in the 2000s, and with European luxury brands in the 2010s. Now it's being deployed with EV startups and new mobility companies.

The platform strategy adds another layer of power. Once a client adopts TRACE for connected vehicle services or uses i GET IT for engineer training, switching becomes even harder. These platforms create recurring touchpoints, generate data insights, and become embedded in the client's operations. They transform Tata Technologies from a vendor to a partner.

The key lesson on patience is profound. Tata Technologies waited 29 years to go public. During that time, it resisted the temptation to diversify into easier, higher-margin IT services. It invested in capabilities that took years to pay off. It built relationships that took decades to mature. This patience—so rare in today's quarterly capitalism—created compounding advantages that faster-moving competitors couldn't replicate.

The conglomerate dynamics add complexity but also opportunity. Being part of the Tata Group means access to patient capital, prestigious brand, and internal clients. But it also means slower decision-making, complex stakeholder management, and sometimes conflicting priorities. The successful IPO suggests Tata Technologies has learned to leverage the advantages while minimizing the disadvantages.

Looking forward, the playbook faces new challenges. Software-defined vehicles require different capabilities than mechanical engineering. Chinese competitors are emerging with aggressive pricing and government support. The shift to EVs might obsolete some traditional capabilities. But the fundamental sources of power—trust, expertise, relationships, and patient capital—remain relevant.

The meta-lesson is about business model evolution. Tata Technologies started as a cost center, became a profit center, and is now transforming into a value creation partner. Each evolution required different capabilities, metrics, and mindsets. But the core power—deep engineering expertise combined with trust—remained constant. This combination of evolution and consistency might be the most powerful playbook of all.

IX. Bull vs. Bear Case & Competitive Analysis

The conference call was tense. It was February 2024, and a prominent hedge fund manager was grilling Tata Technologies' management about their exposure to traditional internal combustion engine (ICE) programs. "If EVs really take off, won't half your revenue disappear?" he challenged. The CEO's response was telling: "We're not betting on ICE or EV. We're betting on complexity. And the transition period will be the most complex in automotive history."

This exchange captures the fundamental tension in evaluating Tata Technologies. Is it a beneficiary of the automotive industry's transformation, or a victim of its disruption? The answer depends on your timeframe and assumptions about the pace of change.

The Bull Case: Riding the Transformation Wave

The bulls see Tata Technologies as perfectly positioned for a multi-decade transformation. The EV/SDV opportunity alone could be worth $100 billion globally by 2030, and Tata Technologies has already proven it can win in this space. Segment revenue grew by 50% between FY22 and FY24, driven by new business wins with its anchor and non-anchor accounts. In FY24, completed development of 2 EVs for a SEA-based automotive OEM—complete vehicles, not just components.

The software-defined vehicle revolution multiplies this opportunity. Traditional automakers need partners who can bridge mechanical and software engineering. A Tesla can hire software engineers directly, but can Volkswagen or General Motors transform their engineering cultures fast enough? The bulls argue they can't, creating massive opportunity for partners like Tata Technologies.

China+1 dynamics add another growth vector. As geopolitical tensions rise, global OEMs are diversifying their engineering partnerships away from China. India, with its large English-speaking engineering talent pool and democratic governance, is the natural beneficiary. Tata Technologies, as India's leading automotive engineering services provider, captures a disproportionate share of this shift.

The manufacturing digitalization megatrend extends beyond automotive. Every manufacturing company needs to digitize, but most lack the expertise. Tata Technologies' solutions address this need across industries. The acquisition of industrial machinery clients proves the model works beyond automotive. With manufacturing contributing 17% to global GDP, even small market share gains represent massive revenue opportunity.

Tata Group synergies are finally bearing fruit. JLR's transition to EVs requires massive engineering support. Tata Motors' commercial vehicle programs need sophisticated engineering. The upcoming Tata semiconductor venture will need design services. These captive opportunities alone could drive 15-20% annual growth.

The valuation math is compelling for bulls. At current valuations around 35-40x P/E, the market is pricing Tata Technologies like a traditional engineering services company. But if it successfully transforms into a technology-enabled services company, multiples could expand to 50-60x. Add 20% annual earnings growth from the opportunities above, and the stock could triple in five years.

The Bear Case: Structural Headwinds

Bears see fundamental challenges that optimists ignore. Customer concentration risk remains acute—Tata Motors and its ecosystem still represent 25-30% of revenue. If Tata Motors struggles (as it has periodically), Tata Technologies suffers disproportionately. The failed Warburg Pincus deal in 2018 happened partly because of disappointments in the core account.

Cyclical automotive exposure is a perpetual concern. Automotive industry downturns are severe and synchronous globally. When OEMs cut costs, engineering services are often first to go. The company's revenue declined in 2019-2020 even before COVID, showing this vulnerability. With many economists predicting a global slowdown, this risk looms large.

Competition from IT majors entering ER&D is intensifying. TCS, Infosys, Wipro, and HCLTech are all aggressively building engineering services capabilities. They have deeper pockets, larger talent pools, and existing client relationships. While Tata Technologies has domain expertise advantages today, these could erode as IT majors gain experience.

The China threat is real and growing. Chinese engineering services companies offer similar services at 30-40% lower costs. As Chinese automakers like BYD and NIO expand globally, they'll bring their engineering partners with them. Tata Technologies' cost advantage versus Western competitors becomes a disadvantage against Chinese ones.

Valuation concerns post-IPO are valid. From ₹500 listing to current ~₹665 represents a 33% gain, but the stock peaked near ₹1,000. The 33% decline from peak suggests the market is reconsidering the growth narrative. At 35-40x earnings, any disappointment in growth or margins could trigger further correction.

Technology disruption could obsolete current capabilities. If generative AI really can automate engineering design (as some claim), what happens to engineering services? If automotive OEMs become software companies (as VW claims it will), won't they insource critical engineering? The bears argue Tata Technologies is selling buggy whips in the age of automobiles.

Competitive Benchmarking

Against KPIT Technologies (market cap ~₹15,000 crore), Tata Technologies looks expensive on valuation but superior on scale and capabilities. KPIT focuses narrowly on automotive software, while Tata Technologies offers integrated engineering. KPIT's pure-play positioning attracts higher multiples, but Tata Technologies' breadth provides resilience.

L&T Technology Services (market cap ~₹50,000 crore) is perhaps the closest comparable. Both offer engineering services across industries, both have parent company relationships, both target similar margins. L&T Tech trades at similar multiples but has better revenue diversification. The market sees them as roughly equivalent risks.

Tata Elxsi (market cap ~₹40,000 crore) offers an interesting comparison within the Tata Group. Despite similar services, Tata Elxsi trades at premium multiples due to better margins and lower customer concentration. This suggests the market would reward Tata Technologies for improving these metrics.

Against global peers like Altran (acquired by Capgemini) or AKKA Technologies, Tata Technologies offers better growth at lower valuations. The India cost advantage and access to talent provide structural advantages. However, global peers have deeper client relationships and more sophisticated capabilities in some areas.

The Verdict: Scenario Analysis

The outcome likely depends on three key variables:

-

EV adoption pace: Faster adoption favors Tata Technologies (more complexity). Very slow adoption also favors them (longer ICE tail). Moderate, smooth transition might be worst case (less complexity).

-

Tata Motors performance: Strong performance provides growth tailwind and validation. Weak performance creates headwinds but might force faster diversification.

-

Technology evolution: Gradual evolution favors established players. Radical disruption favors new entrants. Tata Technologies needs evolution fast enough to create opportunity but slow enough to adapt.

In the optimistic scenario (fast EV adoption, strong Tata Motors, gradual tech evolution), the stock could reach ₹1,500-2,000 in three years. In the base case (moderate everything), expect ₹900-1,200. In the pessimistic scenario (recession, Tata Motors struggles, tech disruption), the stock could revisit ₹400-500.

The risk-reward appears balanced at current levels. Bulls and bears both have valid arguments. The key insight: Tata Technologies isn't a simple bet on EVs or engineering services. It's a complex option on the pace and nature of automotive industry transformation. Those who can correctly gauge this transformation will be rewarded. Those who can't might face significant losses.

For long-term investors, the question isn't whether Tata Technologies will face challenges—it will. The question is whether management's track record of patient adaptation, combined with structural advantages, can overcome these challenges. History suggests yes, but the future remains genuinely uncertain.

X. The Future: AI, Manufacturing 4.0 & Beyond

The year is 2030. In Tata Technologies' new AI command center in Bangalore, an engineer named Priya sits before a wall of screens. She's not coding or designing—she's orchestrating. An AI system has just generated 50 design variations for an electric aircraft's battery cooling system. Another AI is running millions of virtual crash tests on an autonomous truck design. Priya's job is to guide these AIs, interpret their outputs, and make decisions no machine can make—yet.

This isn't science fiction. It's the future Tata Technologies is actively building toward. The question isn't whether AI will transform engineering services—it's whether Tata Technologies will be the disruptor or the disrupted.

The software-defined vehicle revolution represents the most immediate opportunity. By 2030, vehicles will have 500 million lines of code—more than a modern fighter jet. But this isn't just about quantity. It's about fundamental architecture change. Vehicles are becoming computers on wheels, with hardware becoming commoditized and software providing differentiation.

Tata Technologies' approach is pragmatic. Rather than trying to compete with pure software companies, they're positioning themselves as the integration layer. Someone needs to ensure the software works with sensors, actuators, and safety systems. Someone needs to validate millions of scenarios. Someone needs to bridge the virtual and physical worlds. This "someone" requires deep domain knowledge that can't be easily replicated.

Generative AI in engineering and design is already showing promise. Early experiments at Tata Technologies have shown 30-40% productivity improvements in certain design tasks. AI can generate design variations in minutes that would take humans days. But the real value isn't in replacing engineers—it's in augmenting them. An engineer plus AI can do the work of five engineers without AI. This changes the unit economics fundamentally.

The company is developing what it calls "AI-first engineering methodologies." Instead of using AI as a tool within traditional processes, they're redesigning processes around AI capabilities. For example, instead of sequential design-test-refine cycles, AI enables simultaneous exploration of thousands of design spaces with continuous optimization.

India's role in global manufacturing supply chains is evolving rapidly. The "China+1" narrative is real, but it's not just about cost arbitrage anymore. India offers innovation capability, digital expertise, and strategic flexibility. Tata Technologies is positioned to capture value at multiple points: engineering services for companies setting up Indian operations, technology solutions for digitizing these operations, and training services for building local talent.

The manufacturing digitalization opportunity extends beyond traditional clients. Every manufacturer—from textiles to pharmaceuticals—needs digital transformation. Tata Technologies' manufacturing domain knowledge, combined with digital capabilities, creates unique positioning. They're not selling generic IoT or analytics—they're selling manufacturing-specific solutions that actually work on factory floors.

But the future isn't without challenges. The next decade's growth vectors require different capabilities than the past decade's. AI expertise, cloud architecture, cybersecurity—these aren't traditional engineering skills. The company must transform its workforce while maintaining current operations. This is like changing an aircraft's engines mid-flight.

The talent transformation challenge is acute. Of 11,000 current employees, perhaps 20% have the skills needed for 2030's engineering landscape. The company can't simply hire new talent—there isn't enough to go around. They must reskill existing employees while competing with tech giants for new graduates. The i GET IT platform becomes strategic here—it's not just a product but a tool for internal transformation.

The competitive landscape will look different in 2030. Traditional boundaries between engineering services, IT services, and software products are blurring. A company like Tesla is simultaneously an automaker, a software company, and an AI company. Amazon might enter automotive. Apple might finally build its car. In this fluid environment, Tata Technologies must be equally fluid.

What would great execution look like over the next decade?

First, revenue diversification—reducing Tata Motors dependency to under 15% while building 5-10 new anchor accounts generating $100 million+ annually. This isn't just about sales—it's about building deep, strategic relationships in new domains.

Second, capability transformation—becoming known for AI-augmented engineering, not just traditional services. This means landmark projects that showcase new capabilities. Imagine Tata Technologies designing the first fully AI-optimized vehicle or creating the world's first zero-defect factory through digital twin technology.

Third, platform scaling—growing technology solutions to 40-50% of revenue with 40%+ margins. The platforms need to become industry standards, not just tools. TRACE should be the Android of connected vehicles. i GET IT should be the default engineering education platform globally.

Fourth, geographic expansion—establishing significant presence in China (despite geopolitical challenges), deeper penetration in North America, and entry into new markets like Latin America and Africa. Each geography requires different strategies and capabilities.

Fifth, strategic acquisitions—buying capabilities rather than building them. A Silicon Valley AI startup, a German simulation software company, an Israeli cybersecurity firm—these could accelerate transformation by years.

The financial implications of successful execution are substantial. Revenue could grow from ₹5,000 crore to ₹20,000 crore. Margins could expand from 18% to 25% as platform revenues grow. The company could command technology multiples rather than services multiples. Market capitalization could exceed ₹100,000 crore.

But success isn't guaranteed. The transformation could fail for multiple reasons. Culture clash between traditional engineers and software developers. Inability to attract top AI talent. Client reluctance to adopt new models. Competition from unexpected quarters. Technology evolution making current investments obsolete.

The broader implications matter too. If Tata Technologies succeeds, it validates India's evolution from back-office to innovation partner. It proves that engineering services companies can transform into technology companies. It demonstrates that patient, strategic execution can overcome market turbulence.

The next decade will test whether Tata Technologies can maintain its engineering heritage while embracing digital transformation. Can it serve traditional automotive clients while winning new-age mobility companies? Can it preserve the Tata values while competing with aggressive startups? Can it balance quarterly expectations with long-term transformation?

These aren't easy questions, and the answers aren't obvious. But that's what makes the next decade exciting. Tata Technologies stands at the intersection of multiple transformations: automotive to mobility, mechanical to software, products to services, India's emergence, and AI's rise. Few companies have such positioning. Even fewer have the capabilities to capitalize on it.

The journey from 1994's spin-off to 2024's public company took 30 years. The next transformation might take just 10. Speed is accelerating, complexity is increasing, and stakes are rising. But for those who can navigate this complexity—engineers who can code, coders who understand physics, companies that can bridge worlds—the opportunity has never been greater.

XI. Epilogue & Reflections

Ratan Tata didn't live to see Tata Technologies reach its full potential. He passed away in October 2024, less than a year after the company he envisioned finally went public. But in his final months, he witnessed something remarkable: the validation of a three-decade bet on engineering excellence.

At his memorial service, Warren Harris, CEO of Tata Technologies, shared a story. In 2019, during a particularly difficult period when the Warburg Pincus deal had fallen through and automotive markets were struggling, Ratan Tata called him. "Warren," he said, "are we building something that will matter in 50 years?" Not next quarter, not next year—50 years. That long-term perspective, increasingly rare in modern business, defines Tata Technologies' journey.

The patience of building a B2B engineering services business offers profound lessons. Unlike consumer businesses that can scale rapidly through network effects, or software businesses that can grow exponentially through distribution, engineering services scale linearly with expertise. Every engineer must be trained. Every client relationship must be cultivated. Every capability must be earned through experience. There are no shortcuts.

This patience paid off in unexpected ways. While competitors chased hot trends—dot-com, outsourcing, digital—Tata Technologies stayed focused on engineering excellence. This consistency created compound advantages. Clients learned to trust them. Engineers wanted to work for them. Capabilities accumulated like sediment, layer upon layer, creating something substantial and hard to replicate.

Why this story matters for India's manufacturing ambitions becomes clear when you zoom out. India has world-class IT services companies, but manufacturing has lagged. The conventional wisdom says India missed the manufacturing bus—China won that race. But Tata Technologies suggests a different path: instead of competing in low-cost manufacturing, India can lead in high-value engineering and design.

Consider the implications. If India can design the world's products—even if they're manufactured elsewhere—it captures significant value. Design and engineering represent 20-30% of a product's value but require fraction of capital investment of manufacturing. It's cleaner, more sustainable, and plays to India's strengths: educated workforce, English proficiency, and now, proven execution capability.

The key lessons for founders and investors are counterintuitive:

First, timing matters less than persistence. Tata Technologies wasn't first to engineering services, wasn't first to digital manufacturing, wasn't first to go public. But by persisting through cycles, it built capabilities that first-movers lacked.

Second, boring can be beautiful. Engineering services isn't sexy. It doesn't have the appeal of consumer tech or the excitement of startups. But boring businesses with strong moats and steady cash flows create enormous value over time.

Third, culture compounds. The Tata values—integrity, excellence, responsibility—seem quaint in an era of "move fast and break things." But these values created trust, and trust created opportunities that no amount of aggressive sales could generate.

Fourth, complexity is a moat. While everyone seeks simplicity, Tata Technologies embraced complexity. Automotive engineering is hard. Safety standards are stringent. Client requirements are demanding. This complexity keeps competitors out and clients in.

Fifth, patient capital enables transformation. The 29-year journey to IPO would be impossible with typical venture capital or private equity timelines. The Tata Group's patient capital allowed long-term capability building that created lasting value.

The road ahead for TATATECH remains challenging but promising. The stock trades around ₹665, well below its ₹995 peak but above its ₹500 IPO price. This price reflects both opportunity and uncertainty—exactly where interesting investments live.

The company must navigate multiple transitions simultaneously. From services to platforms. From automotive to multi-industry. From engineering to AI-augmented engineering. From Indian to truly global. Each transition carries risk, but also opportunity for value creation.

What would great look like? In 10 years, Tata Technologies could be the world's leading engineering services company, the "McKinsey of manufacturing." It could be the platform powering thousands of factories' digital transformations. It could be the training ground for millions of engineers adapting to AI age. These aren't fantasies—they're logical extensions of current capabilities.

But even moderate success would be meaningful. If Tata Technologies simply maintains its position as India's leading engineering services company, riding the tailwinds of India's growth and manufacturing's digitalization, it could deliver substantial returns to patient shareholders.

The deeper reflection is about business model evolution in emerging markets. The conventional path is to start with cost arbitrage, move to quality, then innovation. Tata Technologies followed this path but added a twist: it built proprietary technology along the way. This combination—services plus products, domain expertise plus digital capability, Indian costs plus global quality—creates something unique.

For India, Tata Technologies represents more than just another successful company. It's proof that Indian companies can compete in complex, high-value domains. It shows that patient capital and ethical business practices can create lasting value. It demonstrates that engineering excellence, not just IT services, can be India's calling card globally.

For the Tata Group, this success validates a different approach to conglomerate management. Rather than forced synergies or financial engineering, the group provided patient capital, ethical framework, and brand umbrella, then let companies find their own paths. This light-touch approach, combined with strong values, created value that aggressive conglomerates couldn't match.

The story also raises questions about the future of work. As AI augments and potentially replaces many engineering tasks, what happens to the millions of engineers in India and globally? Tata Technologies' evolution suggests an answer: humans won't be replaced but augmented. The engineer of 2030 will do different work than the engineer of 2020, but the need for human creativity, judgment, and responsibility remains.

Perhaps the most important lesson is about purpose. "Engineering a Better World" isn't just a tagline—it's a organizing principle that guides decisions and inspires employees. In an era of cynicism about corporate purpose, Tata Technologies shows that genuine commitment to positive impact can coexist with commercial success.

As we close this deep dive into Tata Technologies, it's worth returning to that Mumbai conference room where our story began. The IPO is now history, the stock has found its level, quarterly earnings calls have become routine. The excitement has faded into the regular rhythm of business.

But beneath this normalcy, transformation continues. In Pune, engineers are designing vehicles that don't yet exist. In Detroit, teams are solving problems that haven't been solved. In Stuttgart, relationships built over decades are yielding new opportunities. This is the real story of Tata Technologies—not the financial engineering of an IPO, but the actual engineering of a better world.

The company Ratan Tata envisioned in 1994—"one of the more innovative and successful design companies in the world"—is becoming reality. Not through revolution but through evolution. Not through disruption but through persistence. Not through breaking things but through building them.

For investors, the question isn't whether Tata Technologies will face challenges—it will. The question is whether its combination of capabilities, culture, and patience can overcome these challenges. History suggests yes, but past performance, as they say, doesn't guarantee future results.

For India, the question is whether Tata Technologies represents an isolated success or a template for others. Can India produce more companies that combine engineering excellence with global scale? The answer will shape India's economic future.

For the industry, the question is how the engineering services model evolves. Will it converge with IT services? Will it be disrupted by AI? Will it fragment into specialized niches? Tata Technologies' journey over the next decade will provide clues.

And for all of us, the question is what kind of companies we want to build and invest in. Do we want companies that optimize for quick exits or lasting impact? Do we value patience or speed? Do we seek simplicity or embrace complexity?

Tata Technologies doesn't answer these questions definitively. But its journey from captive unit to public company, from cost center to value creator, from Indian subsidiary to global player, offers a compelling case study in patient value creation.

The story continues. Every day, 11,000 engineers across 18 locations are writing the next chapter. They're designing vehicles that will transport our children. They're digitizing factories that will manufacture products we haven't imagined. They're training engineers who will solve problems we don't yet know exist.

This is perhaps the ultimate reflection: Tata Technologies isn't just engineering products—it's engineering the future. And in a world facing climate change, resource constraints, and technological disruption, we need all the engineering help we can get.

The market will judge Tata Technologies quarterly, annually, perpetually. But the real judgment will come from history. Did it help make transportation safer and cleaner? Did it help make manufacturing more efficient and sustainable? Did it help prepare engineers for the AI age? Did it, in fact, engineer a better world?

The answers won't be found in stock prices or earnings reports. They'll be found in the products we use, the air we breathe, the opportunities we create. And by that measure—the measure that matters—Tata Technologies' most important work lies ahead.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube