Tata Motors: The Rise of India's Global Automotive Empire

I. Introduction & Episode Teaser

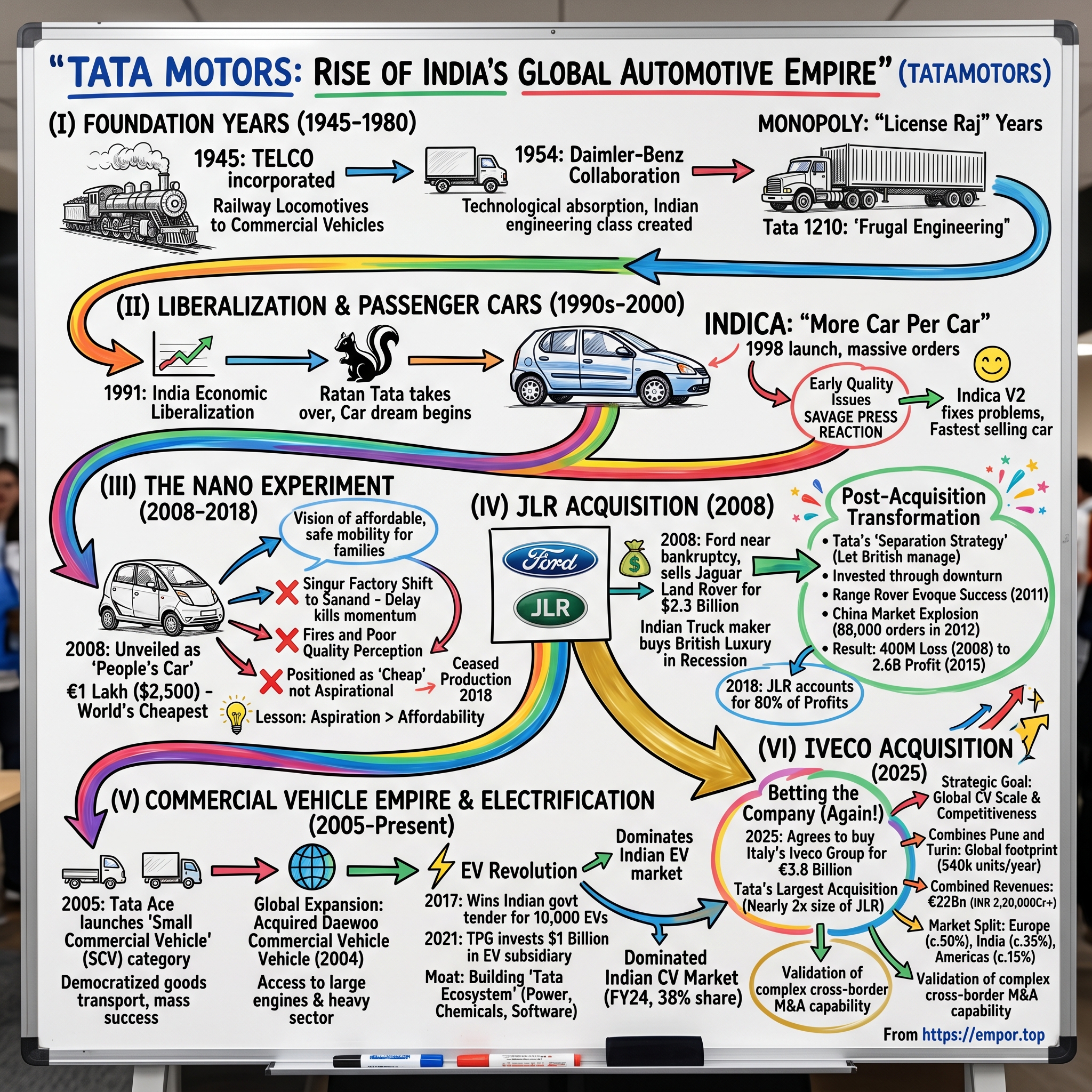

The boardroom at Bombay House fell silent on July 30, 2025. N. Chandrasekaran, Chairman of Tata Sons, had just signed the papers that would commit Tata Motors to its largest acquisition ever—€3.8 billion for Italy's Iveco Group. Outside, Mumbai's morning traffic honked and sputtered, the same chaotic symphony that had soundtracked every major Tata decision for nearly eight decades. But this wasn't just another acquisition. This was a ₹38,000 crore bet that would transform an Indian truck maker into one of the world's largest commercial vehicle empires, with 540,000 units rolling off production lines from Turin to Pune. Consider this for a moment: The Offer represents a total consideration of approximately EUR 3.8 billion for Iveco Group, excluding Iveco's defence business, making it the largest acquisition by the Tata Group in the automotive space, almost twice the size of its $2.3 billion Jaguar Land Rover purchase in 2008. It's a deal that would create combined revenues of c.€22bn (INR 2,20,000Cr+) split across Europe (c.50%), India (c.35%) and the Americas (c.15%)—instantly catapulting an Indian company into the premier league of global commercial vehicle manufacturers.

How does a company that started making railway locomotives for a newly independent nation transform itself into a ₹4,37,968 crore revenue behemoth that owns British luxury brands, dominates Indian highways, and now controls one of Europe's legendary truck makers? The answer lies not in a single brilliant strategy, but in eight decades of calculated risks, spectacular failures, and the unique ability to learn from both.

This is the story of Tata Motors—a company that embodies India's entire post-independence economic journey. From the protected monopoly years of the License Raj to the brutal competition of liberalization, from the humiliation of the failed Nano to the triumph of turning around Jaguar Land Rover during the worst financial crisis since the Great Depression. It's a narrative that teaches us how emerging market companies can compete globally not by copying Western playbooks, but by writing entirely new ones.

The roadmap ahead takes us through time and continents. We'll start in the chaos of 1945 Bombay, where a vision for industrial self-reliance was born. We'll witness the painful birth of India's first indigenous car, the Indica, and dissect why the world's cheapest car became one of its biggest commercial failures. We'll be in the room when Ratan Tata negotiated with Ford to buy brands that Ford itself couldn't save. And we'll analyze how a truck company from Mumbai is betting ₹38,000 crores that the future of global transportation runs through both Turin and Pune.

II. The Tata Legacy & Foundation Years (1945-1980)

The monsoon of 1945 had just broken over Bombay when Sumant Moolgaokar walked into the offices of Tata Sons with a proposal that would have seemed absurd to anyone but J.R.D. Tata. India was still two years away from independence, the British Raj was crumbling, and the industrial landscape was dominated by foreign companies. Yet here was Moolgaokar, suggesting that Tatas should manufacture locomotives and commercial vehicles—products that required sophisticated engineering India had never attempted before.

J.R.D. Tata, the French-educated pilot who had inherited Jamsetji Tata's empire at just 34, saw something others missed. While politicians debated India's future, he understood that a nation without its own heavy industry would never be truly independent. The British had built railways to extract resources; Tata would build trucks to distribute prosperity. On February 1, 1945, Tata Engineering and Locomotive Company (TELCO) was incorporated with a capital of ₹30 million—a staggering sum when the average Indian earned less than ₹200 per year.

The early years were an exercise in industrial archaeology. TELCO's first factory in Jamshedpur was assembled from whatever could be salvaged or improvised. The company started by manufacturing steam locomotives, but Moolgaokar's real vision lay elsewhere. He had studied the reconstruction of post-war Europe and Japan, noting how commercial vehicles—not passenger cars—formed the backbone of economic recovery. India, with its vast distances and underdeveloped rail network, would need trucks even more desperately.

In 1954, TELCO signed its most important agreement yet: a collaboration with Daimler-Benz of Germany. The Germans, still rebuilding from the war, were eager for new markets. The Indians were eager for technology. It was a marriage of convenience that would prove transformative. German engineers arrived in Jamshedpur, shocked by the monsoon humidity that rusted their precision tools overnight. Indian workers, many of whom had never seen an automobile engine, learned to assemble Mercedes-Benz trucks by watching and copying, often without understanding the underlying engineering principles. The cultural chasm was profound. The Benz engineers were sticklers for perfection, as were JRD and Moolgaokar. Once every week all the parts rejected by the German technicians in Jamshedpur were displayed and a post-mortem held. This 'major attention to minor details' was a painful exercise for the Indian engineers but it was through such discipline that TELCO's standard was jacked up. What emerged from this painful process was more than just trucks—it was India's first generation of world-class automotive engineers.

The numbers tell only part of the story. In 1954, they negotiated a successful joint venture and Tata's first truck rolled out. It was the TMB 312, a medium-duty truck with a diesel engine. It was a highly advanced truck compared to the ones that were out there. But what the numbers don't capture is the audacity of the moment. India was importing everything from needles to locomotives. The idea that Indians could manufacture complex automotive products was met with skepticism even within government circles.

Moolgaokar, who would later become chairman, understood something fundamental about nation-building that economists often miss. Moolgaokar said, "There is a belief in our country that our culture and our Indian character cannot allow our people to attain consistently high standards, that shoddiness and carelessness are our God-given, unalterable way of life. But if, with faith in them, you ask our men for their best, they rise to your belief and in their worth and relate a momentum towards improvement. Often I have seen men who are considered ordinary rise to extraordinary heights.

The License Raj years, often derided as a period of stagnation, were paradoxically TELCO's golden age. With imports restricted and competition limited, the company enjoyed near-monopoly status in commercial vehicles. By 1969, when the collaboration with Daimler-Benz ended, TELCO had absorbed enough technology to go it alone. The famous "T" logo replaced the Mercedes star, symbolizing not just corporate identity but industrial independence.

Yet even in monopoly, TELCO innovated. The company developed vehicles specifically for Indian conditions—higher ground clearance for rural roads, reinforced chassis for overloading (a common practice despite regulations), and simplified maintenance for mechanics who often worked without proper tools. The Tata 1210, launched in 1964, could carry 40% more payload than its predecessor while consuming less fuel—a feat of frugal engineering that would become Tata's signature.

By 1980, TELCO had transformed from an assembler of foreign designs to a genuine automotive manufacturer. The company produced over 40,000 vehicles annually, employed 40,000 workers, and had spawned an entire ecosystem of suppliers and service centers. More importantly, it had created something intangible but invaluable: the belief that Indian companies could master complex technologies and compete globally. This confidence would prove crucial when the walls of protection came crashing down in 1991.

III. Liberalization & The Passenger Car Dream (1990s-2000)

The summer of 1991 changed everything. India's foreign exchange reserves had dwindled to barely three weeks of imports. The IMF demanded reforms. Finance Minister Manmohan Singh stood before Parliament and quoted Victor Hugo: "No power on earth can stop an idea whose time has come." Within months, decades of industrial licensing was dismantled. Foreign companies could now enter India. For TELCO, comfortable in its commercial vehicle dominance, the new world was both threat and opportunity.

Ratan Tata, who had taken over as chairman in March 1991, saw the writing on the wall before most. The truck business, while profitable, was cyclical and tied to industrial growth. The real opportunity—and threat—lay in passenger cars. Maruti-Suzuki, a joint venture between the Indian government and Japan's Suzuki, had already captured 80% of the car market. Now, with liberalization, everyone from Hyundai to Honda was preparing to enter India. TELCO had two choices: remain a truck company and slowly become irrelevant, or take the fight to the global giants.

The board was skeptical. TELCO had never made a passenger car. The investment required—estimated at ₹1,700 crores—was more than the company's entire net worth. Critics within Tata Sons whispered that Ratan, who had spent years running the group's struggling textiles and electronics divisions, didn't understand automobiles. One board member reportedly said, "We make trucks that carry 10 tons. Why should we make cars that carry four people?"

Ratan Tata's response was to create a skunkworks team, hidden from the main organization. He recruited young engineers, many fresh from college, who hadn't yet learned what was "impossible." The brief was audacious: create a car that could compete with Maruti on price but offer the space of much larger vehicles. And do it in less than four years—half the time it typically took to develop a new vehicle.

The team worked in a converted warehouse in Pune, far from TELCO's main operations. They bought competitor cars, tore them apart, studied every component. They realized that traditional car design wasted enormous space—the engine bay alone took up a third of the vehicle length. What if they could push the wheels to the corners, maximize interior space, and create a car that was small outside but big inside?

The Indica, as it would be called, was India's first indigenous car design. But "indigenous" understates the achievement. This wasn't just assembly or adaptation—it was ground-up engineering. The team developed a new engine with help from an Austrian firm, a new transmission, a new platform. They made 3,500 design changes after initial prototypes. Cost overruns mounted. By 1997, the project had consumed ₹1,800 crores, more than initially budgeted for the entire car division. The launch at the 1998 Auto Expo was electric. At the 1998 Auto Expo, a harried Ratan Tata pushed through a sea of people to reach the exit of Hall No. 11 at Pragati Maidan. It was a cold January day but the jam-packed hall felt hot and stuffy. "I need air," gasped the then 60-year-old chairman of Telco (now Tata Motors) who was swamped by a gaggle of media, employees, industry executives, government officials and well-wishers eager to greet and congratulate the man who had just unveiled the Tata Indica. After years of secrecy, hype and speculation that swelled around Tata's dream to build India's first truly indigenous car, this was the moment the automobile world was waiting for. It was a packed house that January 15th afternoon at the Telco pavilion which, spread over an acre, was by far the largest at the 1998 Auto Expo.

Tata introduced the Indica on 30th December 1998 with a tagline 'More car per car'. The hatch was spacious inside and was really affordable. This is what made it so popular amongst the customers that the Indica gained more than 1,15,000 orders within a week of launch. The starting price of ₹2.6 lakh undercut Maruti significantly, while offering features like air conditioning and power windows that were previously restricted to imported cars.

But euphoria quickly turned to crisis. When first launched, the Indica prompted many complaints from early purchasers, who claimed that the vehicle did not deliver horsepower and mileage as promised. In response to the customer complaints, Tata Motors re-engineered the internals of the car and launched it as Indica V2 (version 2), which solved most of the complaints and emerged as one of the most sought-after cars in the Indian automobile industry. The early quality problems nearly killed the dream. Customers complained about everything from panel gaps to engine refinement. The automotive press, initially enthusiastic, turned savage.

The competition became hyperactive and began to write premature epitaphs for the Indica. A constant refrain heard in those days was that Tata Motors and Ratan Tata had made a big mistake in betting on an indigenously made car. And there is of course no dearth of condescending Western and Indian minds who never miss an opportunity to take potshots at India and other developing nations, which remain, in their minds, lands that are best suited to snake charmers, forests and elephants. So, was this the sad end of the Tata dream to make India's first car? Would it spell disaster for Tata Motors, which had made the back-breaking investment of Rs 1700 crore in the Indica project? Like the Titanic, had the Indica hit a fatal iceberg? Would it now drag down with it one of the most venerable companies of the Tata group?

Ratan Tata's response defined his leadership style. Rather than blame or deflect, he acknowledged the problems and committed to fixing them. The Indica V2, launched in 2001, addressed most issues. The impact of the Indica V2 was extraordinary and immediate. It marked not merely the revival of the Indica but its brilliant success. It became the fastest-selling automobile in Indian history when it completed sales of 100,000 cars in less than eighteen months. Despite an overall economic slowdown in 2001, it recorded a growth of over 46 per cent in that year, whereas most international competitor brands clocked only single-digit growth during the same period.

The Indica story taught Tata Motors invaluable lessons: the importance of quality from day one, the power of listening to customers, and the courage required to enter new segments. These lessons would prove crucial when, a decade later, the company would attempt something even more audacious—creating the world's cheapest car. But first, it had proven something fundamental: an Indian company could design, engineer, and manufacture a modern passenger vehicle that could compete with global players. The truck maker had become a car company.

IV. The Nano Experiment: Vision vs Reality (2008-2018)

The Geneva Motor Show in March 2000 was buzzing with the usual parade of European engineering excellence when something unexpected caught everyone's attention. In a corner of the exhibition hall, away from the Ferraris and Mercedes, stood a small car painted in an audacious nail-polish pink. It was the Tata Indica, making its international debut. European journalists snickered at first—what was an Indian truck maker doing at Geneva? But when they learned the car's price point and specifications, the snickers turned to genuine interest. One German auto journalist was overheard saying, "If they can build this for this price, what else can they do?"

That question would be answered eight years later in the most dramatic fashion possible. On January 10, 2008, at the Auto Expo in New Delhi, Ratan Tata pulled a white cloth off what looked like a toy car. The Nano—the "People's Car"—stood there, almost apologetically small, while the audience erupted. At ₹1 lakh ($2,500), it was the cheapest car ever made. The international media went into overdrive. CNN called it "the car that could change the world." The Economist wondered if this was "the birth of the Model T for the 21st century. "But the origin story of the Nano wasn't in a boardroom—it was on a rain-soaked Mumbai street in 2003. Ratan Tata stepped out and saw it: a family of four crammed onto a single scooter—dad at the front steering, a child perched between him and mom, another child balanced precariously. He thought: "Surely there must be a safer, affordable way…" That moment famously ignited what would become the People's Car initiative. He envisioned not just a cheap vehicle, but a radically affordable, safe, and dignified form of transport for India's millions. His idea was simple—and revolutionary: a four-wheeler priced at ₹100,000 (~$2,000–$2,500 at the time), aimed at families who would otherwise cling to scooters out of necessity.

The engineering challenge was staggering. The Nano's design implements many measures to reduce manufacturing costs. The Nano (2012) was a 38 PS (28 kW; 37 hp) car with a two-cylinder 624 cc engine mounted in the rear of the car. The car complied with Bharat Stage 4 Indian Emissions Standards, which are roughly equivalent to Euro 4. The development of the Nano led to 31 design and 37 technology patents being filed. The team stripped everything non-essential: only one wing mirror, one windshield wiper, three lug nuts per wheel instead of four, no fuel filler cap. They used adhesive instead of welding where possible. The seats were fixed to save on adjustment mechanisms. Yet somehow, they managed to create a vehicle that could seat four adults and meet safety standards.

On January 10, 2008, Tata Motors unveiled its (U.S. dollars) USD2,500 car (also called "Rs1 lakh car" or "the people's car") at the ninth Auto Expo in New Delhi. The Tata Nano brought a media blitz and a crush of onlookers that required top-level security. It was one of the longest-awaited and most talked-about automobile debuts in India. The initial response was phenomenal. The Nano was officially launched in March 2009, amid much fanfare. Tata Motors received an overwhelming response, with over 200,000 bookings in the initial phase.

But then everything went wrong. First came the Singur controversy. And as people were waiting for the launch, Tata announced the shift of the brand's production plant from Singur, West Bengal to Sanand, Gujarat on October 7, 2008. The West Bengal government, led by Mamta Banerjee accused Tata Motors of land acquisition and initiated the "Save Farmland" movement with local farmers and environmental activists. Tata Motors had to leave the state and was welcomed by Gujarat to set up their plant at Sanand. The delay killed momentum. The political battle turned ugly, with violent protests and eventually Tata's withdrawal from West Bengal entirely.

Then came the fires. Many times, the initial models of Tata Nano caught fire and burst into flames on the road. Some said it was because of the faulty wiring. Others said a foreign object had entered the exhaust system. Each incident made headlines, reinforcing perceptions of poor quality. The damage to the brand was immediate and severe.

But the biggest mistake was in the positioning itself. Tata Nano was often called "Lakhtakiya," translated as "worth a lakh." Tata Motors used the penetration pricing strategy. The company marketed it as the cheapest car in the world to make it accessible to the masses irrespective of their socio-economic background. The media hyped the positioning and it backfired. A noble idea went kaput because it could not sell entitlement. People did not want to own an item known for its cheap cost. Also, with the tag of cheap, quality stereotypes are bound to arise. People assumed that cost-effectiveness comes with quality compromises, and hence Tata Nano could not find its footing.

The numbers tell the story of decline. Tata Motors projected production figures of 250,000 annually at launch. This was not achieved, and various factors led to a decline in sales volume, including delays during the factory relocation from Singur to Sanand, early instances of the Nano catching fire and the perception that the Nano was unsafe and lacked quality from its aggressive cost cutting. Actual sales reached 7,591 for model year 2016-2017. By 2018, production ceased entirely.

The project lost money, as confirmed by former Tata Sons chairman Cyrus Mistry and by 2017 Tata Motors management. Yet Ratan Tata, reflecting on the Nano years later, refused to call it a failure. In his view, it had democratized the conversation about affordable mobility. It had pushed engineering boundaries. It had shown that Indian companies could innovate, not just copy. The Nano's failure taught Tata Motors perhaps its most valuable lesson: in automobiles, aspiration matters more than affordability. A car isn't just transportation—it's identity. This understanding would prove crucial when, just months after unveiling the Nano, Tata Motors would make its boldest bet yet: buying two of Britain's most storied luxury brands.

V. The JLR Acquisition: Betting the Company (2008)

The Waldorf Astoria hotel in New York had hosted many historic negotiations, but few as unlikely as the one taking place in March 2008. On one side sat Alan Mulally, CEO of Ford Motor Company, desperately trying to avoid bankruptcy. On the other, Ratan Tata, chairman of an Indian truck maker that had just unveiled the world's cheapest car. Between them lay the fate of Jaguar and Land Rover—brands that epitomized British automotive aristocracy, now being negotiated over like distressed real estate.

Ford was hemorrhaging money—$12.7 billion lost in 2006 alone. The financial crisis was tightening its grip. General Motors and Chrysler were weeks away from needing government bailouts. Ford had mortgaged everything, including its blue oval logo, to raise cash. Jaguar and Land Rover, acquired during Ford's empire-building days for $5.3 billion, were now deadweight. Ford needed them gone, and fast.

The auction had attracted the usual suspects. Private equity firms circled like vultures. Mahindra & Mahindra, Tata's Indian rival, expressed interest. But as negotiations progressed, bidders dropped out one by one. The brands were losing £400 million annually. The factories needed billions in investment. The workforce was unionized and expensive. Who would be crazy enough to buy British luxury brands during the worst recession since the 1930s?Ratan Tata, apparently. On June 2, 2008, India-based Tata Motors completed the acquisition of the Jaguar and Land Rover (JLR) units from the US-based auto manufacturer Ford Motor Company (Ford) for US$ 2.3 billion, on a cash free-debt free basis. Ford contributed about US $600 million to the Jaguar Land Rover pension plans. The purchase consideration included the ownership by Jaguar and Land Rover or perpetual royalty-free licences of all necessary Intellectual Property Rights, manufacturing plants, two advanced design centres in the UK, and worldwide network of National Sales Companies.

The financing alone was a nightmare. Tata Motors had to raise $3 billion through a bridge loan at punitive interest rates. The company's debt-to-equity ratio would balloon from 0.5 to 2.2. Credit rating agencies threatened downgrades. One analyst at Morgan Stanley wrote: "This is either the deal of the century or corporate suicide. Given it's happening in 2008, we lean toward the latter."

The immediate aftermath seemed to confirm the skeptics. The year was 2008 when the US market was slipping into a recession and hence the demand for luxury cars and SUVs (Jaguar and Land Rover's respective area of forte) were sliding. The cash-strapped iconic British automotive brands were creeping towards major loss. JLR lost £400 million in 2008. By early 2009, with the global financial crisis in full swing, sales had collapsed by 30%. Tata Motors' stock price plummeted from ₹750 to ₹75. The Indian press, which had celebrated the acquisition as a triumph of Indian ambition, now called it "Ratan Tata's Waterloo."

Inside JLR's headquarters in Gaydon, Warwickshire, the mood was equally grim. Workers who had survived multiple ownership changes—from British Leyland to BMW to Ford—now wondered what an Indian truck company could possibly know about building luxury cars. The cultural gap seemed insurmountable. Tata executives arriving from Mumbai were shocked by the British work culture: strict union rules, tea breaks that couldn't be disturbed, and a deep skepticism of any changes proposed by the new owners.

But Ratan Tata had learned something crucial from the Indica experience: sometimes the best strategy is to do nothing. Rather than impose Indian management practices or attempt cost-cutting through layoffs, Tata made a counterintuitive decision. Mike O'Driscoll, managing director of Jaguar Cars under Ford, says he met with top executives, including Ratan Tata, chairman of the parent Tata Group, as the deal was being hammered out and is encouraged that the new owners will let the Jaguar staff run the company with little interference. Tata "will give us some space. They want us to run our business, be a premium British car company."

The study reveals that Ford used organizational integration strategies, which limited the quality of decision making of Jaguar Land Rover management team. On the other hand, Tata has implemented "Separation strategy" and empowered decentralized decision making to Jaguar Land Rover's managers. That has allowed Jaguar Land Rover to reinvest their profits in technology development and promotion of their brand image. Tata kept British management intact, maintained design centers in the UK, and most importantly, continued investing in new products even as losses mounted.

To staunch the hemorrhage at the British unit, Tata's management focused on reducing costs, improving efficiencies and managing cash flow — lessons that Tata Motors had learned during the downturn in 2001. Tata also infused $1 billion to fund operations and new product launches. When the market turned, the premier car maker was well poised to reap the benefits and turned profitable during the quarter ended Dec. 31, 2009, with a net profit of 55 million pounds ($90.6 million).

The turning point came with a single product: the Range Rover Evoque. Launched in 2011, it was smaller, more fuel-efficient, and aimed at a younger demographic—particularly in China, where nouveau riche buyers wanted British luxury without the guilt of conspicuous consumption. The Evoque became JLR's fastest-selling model ever, with over 88,000 orders before the first car rolled off the production line. China became the engine of JLR's transformation. In late 2012, the company announced a joint venture for Jaguars and Land Rovers to be built in China, now the world's biggest car-market. The agreement was with Chery, China's sixth largest auto manufacturer, and called for a new Chinese factory in Changshu to build vehicles starting in 2014. But more important than manufacturing was understanding Chinese luxury buyers. They wanted longer wheelbases for chauffeur-driven comfort. They cared about rear-seat amenities more than driving dynamics. They valued technology displays over understated British elegance.

JLR responded with China-specific models while maintaining global brand consistency. Between 2013 and 2017, Chinese sales exploded, accounting for nearly 40% of JLR's global volume. In January 2014, the Wall Street Journal reported that Jaguar Land Rover sold a record 425,006 vehicles in 2013 as demand for its luxury vehicles increased in all major markets including in China, North America and Europe. This is a glimpse into how Jaguar Land Rover (JLR) was transformed from a 400 million pound loss in 2008 to 2.6 billion pound profit in 2015, even as the iconic British brand takes a leap into new megatrends of electrification and autonomous mobility.

The numbers were staggering. JLR's revenues grew from £5 billion in 2008 to £25 billion by 2018. Employment increased from 16,000 to over 40,000. The company that Ford couldn't make profitable was now contributing over 80% of Tata Motors' profits. Jaguar Land Rover had become so valuable that analysts estimated it was worth more than the entire market capitalization of Tata Motors—implying the Indian operations had negative value.

But success brought new challenges. JLR was hit particularly hard by falling sales in China. Its sales fell 22% there in 2018. Sales of premium rivals BMW, Mercedes-Benz and Audi rose in China in 2018, with JLR's drop put down to quality issues and an unruly dealer network. JLR was struggling by mid-2019 and Tata Motors wrote down its investment in JLR by $3.9 billion. Much of the financial problem was due to a 50% drop in sales in China during 2018, although the situation was improving by autumn 2019.

The JLR story offers a masterclass in cross-border M&A. First, cultural sensitivity matters more than synergies. Tata's hands-off approach preserved what made JLR special while providing capital and strategic patience Ford couldn't afford. Second, timing in M&A is everything—buying during distress requires nerves of steel but offers transformational upside. Third, emerging market companies can successfully acquire and run developed market luxury brands if they respect the brand heritage while adapting to new markets.

Most importantly, the JLR acquisition proved that Tata Motors could execute complex global deals. This wasn't just about buying assets—it was about managing across cultures, technologies, and market segments simultaneously. These capabilities would prove essential as Tata Motors prepared for its next transformation: the shift to electric vehicles and, ultimately, the massive Iveco acquisition that would create a global commercial vehicle giant.

VI. The Commercial Vehicle Empire & Global Ambitions (2010-2024)

While the world watched the JLR drama unfold, something quieter but equally significant was happening back in India. In 2005, a small team at Tata Motors' Pune facility was given an unusual brief: create a commercial vehicle that costs less than a used three-wheeler but can carry more cargo. The result would revolutionize not just Indian logistics but become a template for emerging markets worldwide.

The Tata Ace, launched in May 2005, didn't look like much—a tiny four-wheeled truck that seemed almost toy-like next to Tata's traditional heavy vehicles. But at ₹2.25 lakhs, it created an entirely new category: the small commercial vehicle (SCV). Within six months, Tata was selling 10,000 units per month. Competitors scrambled to copy it. The Ace had done for goods transportation what the Nano failed to do for personal mobility—democratize access by understanding aspiration, not just affordability.

By 2010, Tata Motors controlled 60% of India's commercial vehicle market. But dominance at home wasn't enough. The company had watched Chinese manufacturers like Dongfeng and FAW expand globally by acquiring distressed assets. If Tata didn't move fast, these new competitors would eventually challenge them even in India. The strategy was clear: buy established players in key markets before the Chinese did. The first major international acquisition came in 2004. Tata acquired Daewoo Commercial Vehicle Company from the bankrupt Daewoo Group for $102 million. The principal reasons behind the acquisition were to reduce Tata's dependence on the Indian commercial vehicle market (which was responsible for around 94% of its sales in the MHCV segment and around 84% in the light commercial vehicle segment) and expand its product portfolio by leveraging on Daewoo's strengths in the heavy-tonnage sector. The South Korean operation gave Tata access to larger engines, advanced cabin designs, and most importantly, a manufacturing base to export to Southeast Asia.

The numbers paint a picture of methodical expansion. In the financial year 2024, Tata Motors dominated the domestic commercial vehicle market across India with a share of around 38 percent. In that year, the company had an overall revenue of around 4.4 trillion Indian rupees. But what set Tata apart wasn't just market share—it was the breadth of the portfolio. From the tiny Ace that revolutionized last-mile delivery to massive mining trucks, from CNG buses for Delhi's public transport to defense vehicles for the Indian Army, Tata had a vehicle for every commercial need.

The real revolution, however, came with electrification. In 2017, Tata won a tender to supply 10,000 electric vehicles to the Indian government—the largest EV order in the country's history. But rather than just deliver cars, Tata saw an opportunity to build an entire ecosystem. They partnered with Tata Power for charging infrastructure, with Tata Chemicals for battery technology, with TCS for fleet management software. This wasn't just vertical integration—it was creating a new industry from scratch. The validation came in October 2021. On 12 October 2021, private equity firm TPG invested $1 billion in Tata Motors' electric vehicle subsidiary. TPG Rise Climate along with co-investors shall invest Rs 7,500 Cr in compulsory convertible instruments to secure between 11 % to 15 % stake in this company translating to an equity valuation of up to $9.1 bn. The new company shall leverage all existing investments and capabilities of Tata Motors Ltd and will channelise the future investments into electric vehicles, dedicated BEV platforms, advanced automotive technologies and catalyse investments in charging infrastructure and battery technologies.

The TPG investment wasn't just about money—it was Silicon Valley's stamp of approval on an Indian industrial company's tech ambitions. TPG's Jim Coulter joined the board, bringing expertise from investments in Uber and Airbnb. The message was clear: Tata Motors wasn't just making electric vehicles; it was building a mobility platform for the future.

Over the next 5 years, this company will create a portfolio of 10 EVs and in association with Tata Power Ltd, catalyse the creation of a widespread charging infrastructure to facilitate rapid EV adoption in India. The strategy was comprehensive: from battery chemistry research with Indian Institute of Science to recycling partnerships with global firms, from subscription models for fleet operators to battery-as-a-service for individual buyers.

By 2024, Tata Motors controlled over 70% of India's electric passenger vehicle market. But the commercial vehicle transformation was equally significant. Electric buses for public transport, electric trucks for e-commerce delivery, hydrogen fuel cells for long-haul transport—Tata was placing bets across the entire spectrum of clean mobility. The company that had started with steam locomotives was now pioneering the post-fossil fuel era of transportation.

The global expansion continued through partnerships rather than acquisitions. Assembly plants in Bangladesh, Kenya, and Indonesia. Technical centers in Europe for emissions compliance. Joint ventures in Southeast Asia for market entry. Each move was calculated to build presence without the massive capital requirements of wholly-owned operations. The commercial vehicle business had become a global platform, setting the stage for the transformative Iveco acquisition that would create a truly global commercial vehicle powerhouse.

VII. The Iveco Acquisition: Doubling Down on Scale (2025)

The leaked WhatsApp message hit Mumbai's business circles like a thunderbolt on a clear January morning in 2025. "Tata looking at Iveco. Serious talks. Could be bigger than JLR." Within hours, both companies' stocks were moving, analysts were frantically updating models, and CNBC's Mumbai studio was running breaking news tickers. But inside Bombay House, Tata's headquarters, the planning had been underway for over a year.

The global commercial vehicle industry in 2024 was at an inflection point. Chinese manufacturers like Geely and BYD were expanding aggressively into Europe. Tesla's Semi was finally ramping production. Traditional players were struggling with the dual challenge of electrification and autonomous driving. Consolidation wasn't just likely—it was inevitable. The question was who would consolidate whom.

Iveco Group's story mirrored the challenges facing the entire European automotive industry. Spun off from CNH Industrial in 2022, Iveco had strong brands—the trucks, the buses, FPT Industrial's engines. But as a standalone company with €15 billion in revenue, it lacked the scale to compete with Daimler Truck or Volvo Group, let alone invest in the electric and hydrogen technologies reshaping the industry. The numbers painted a clear picture: Iveco Group's consolidated revenues of €15 billion split across three main divisions—€10 billion from trucks, €2.6 billion from buses, and €3.5 billion from powertrains (FPT Industrial), with operating margins hovering around 5-6%. For comparison, Daimler Truck's margins were double that. The combined Tata-Iveco entity would have sales of over 540,000 units per year and combined revenues of approximately €22 billion, divided between Europe (approximately 50%), India (approximately 35%) and the Americas (approximately 15%), with attractive positions in emerging markets in Asia and Africa.

The strategic logic was compelling. Iveco's product range included Light, Medium and Heavy Commercial Vehicles (IVECO), Powertrain (FPT Industrial), Buses (HEULIEZ, IVECO BUS), Financial Services (IVECO CAPITAL), Specialty Vehicles (IDV, ASTRA). Iveco Bus maintained leadership in the intercity bus segment in Europe, confirming a 50.5% share, while significantly growing in the city bus segment, where Iveco Bus in 2024 held a 2nd position with 19.6% market share. In the subsegment of electric city buses, Iveco Bus reached the 2nd position in the European market 2024 with 14.2%.

But beyond products, this was about creating global scale in an industry where scale increasingly determined survival. The combined group would be better positioned to invest in and deliver innovative, sustainable mobility solutions by leveraging both supplier networks to serve customers globally. It would also unlock superior growth opportunities and create significant value for all stakeholders in a dynamic marketplace.

The negotiation itself was a masterclass in cross-border dealmaking. Unlike the JLR acquisition, where desperation gave Tata leverage, Iveco had options. Chinese companies were interested. Private equity funds saw an opportunity for financial engineering. The Agnelli family's Exor holding company, which controlled Iveco, was sophisticated and patient—they didn't need to sell.

The Offer represents a total consideration of approximately EUR 3.8 billion for Iveco Group, excluding Iveco's defence business and the net proceeds from the defence business separation. The completion of the offer is conditional, inter alia, on the separation of Iveco's defence business. The offer price of EUR 14.1 per share represented a premium to market price, making it attractive to shareholders.

The financing structure showed how much Tata Motors had evolved since the scramble to fund JLR in 2008. This time, the company had secured committed financing before announcing the deal. The debt markets, which had been closed to Indian companies during the financial crisis, now welcomed Tata's paper. The company's investment-grade rating, earned through years of prudent management, meant competitive interest rates.

Under a set of agreed covenants, Iveco's headquarters will remain in Turin, and no plant closures or workforce reductions are planned for at least two years following the settlement. N. Chandrasekaran stated: "This is a logical next step following the demerger of the Tata Motors Commercial Vehicle business and will allow the combined group to compete on a truly global basis with two strategic home markets in India and Europe".

The market reaction was mixed but telling. Tata Motors had just clawed its way back to near-zero net debt after years of deleveraging. Now, between this deal, JLR's EV transition, and the new Sanand plant for EVs in India, it's once again taking on a fair bit of leverage. And if global rates rise or sales disappoint, those repayments could pinch. Analysts worried about execution risk, integration challenges, and whether Tata was overreaching.

But there was a deeper strategic logic that the market initially missed. This wasn't just about buying market share or technology—it was about creating a platform for the next phase of globalization. As supply chains regionalized post-COVID, having manufacturing in Europe, India, and through partners in other regions became a hedge against geopolitical risk. As emissions regulations tightened globally, having FPT Industrial's engine expertise would accelerate the transition to alternative fuels.

Most importantly, the Iveco acquisition positioned Tata Motors for a world where commercial vehicles would become increasingly connected, autonomous, and service-oriented. The company wasn't just buying trucks and buses—it was buying capabilities to compete in a future where vehicles would be nodes in a logistics network, where uptime mattered more than ownership, where data would be as valuable as steel.

VIII. Business Model & Competitive Dynamics

Standing in the design studio at Tata Motors' Pune facility, you can see the entire evolution of Indian automotive ambition. In one corner, original blueprints of the 1954 TMB truck, yellowed with age. On the far wall, CAD renderings of the latest electric SUV. Between them, decades of vehicles that tell the story not just of a company, but of how emerging market firms can build sustainable competitive advantages against global giants.

The Tata Motors business model defies easy categorization. It's neither a pure-play luxury company like Ferrari, nor a volume manufacturer like Toyota. It's not focused solely on commercial vehicles like Paccar, nor just on passenger cars like most automakers. Instead, it operates what might be called a "portfolio arbitrage" model—using profits from dominant positions in some segments to fund aggressive expansion in others, while leveraging the broader Tata Group ecosystem for capabilities that would be impossibly expensive to build independently.

Consider the capital allocation over the past decade. JLR, which represents about 70% of revenues, has invested over £15 billion in new products and technologies. The Indian commercial vehicle business, with its 38% market share, generates steady cash flows that fund R&D. The passenger vehicle business in India, despite lower margins, provides volume for supplier negotiations and manufacturing scale. The EV subsidiary, valued at $9 billion by TPG, represents the future growth engine.

This portfolio approach creates resilience but also complexity. When China's car market crashed in 2018-2019, hitting JLR hard, the Indian CV business provided stability. When COVID-19 devastated commercial vehicle sales globally, JLR's recovery in luxury SUVs offset the damage. When semiconductor shortages crippled production in 2021-2022, having multiple sourcing options across geographies provided flexibility.

The competitive dynamics vary dramatically across segments. In Indian commercial vehicles, Tata faces Ashok Leyland, a capable but smaller domestic rival, and increasing pressure from global entrants like Volvo and Daimler's BharatBenz. The competitive advantage here isn't just market share—it's the ecosystem. Tata's 5,000+ touchpoints across India, financing through Tata Motors Finance, insurance through Tata AIG, and the ability to provide total solutions from vehicles to telematics gives them a moat that's expensive to replicate.

In passenger vehicles, the challenge is different. Maruti Suzuki, backed by Suzuki's global scale, dominates with 40% market share. Hyundai and Kia have Korean technology and aggressive pricing. Chinese brands like MG (owned by SAIC) and soon BYD are entering with electric vehicles. Tata's strategy here has been to focus on specific segments—SUVs, where they've grown from 2% to 14% market share, and electric vehicles, where they have over 70% share. They're not trying to beat Maruti at small cars; they're changing the game entirely.

The JLR competitive position is perhaps most precarious and most valuable. Against German premiums (BMW, Mercedes, Audi), JLR offers British heritage and design distinctiveness. The Range Rover brand, in particular, occupies a unique position—it's the only luxury brand that's equally at home at a polo match and climbing a mountain. But maintaining this position requires constant investment. Every new Range Rover model costs £1-2 billion to develop. The shift to electric threatens to reset competitive advantages built over decades.

The Tata Group synergies are often invisible but crucial. When JLR needed to quickly develop electric vehicles, Tata Consultancy Services (TCS) provided software expertise. When the Indian EV business needed batteries, Tata Chemicals' lithium-ion cell development provided a path to local manufacturing. When commercial vehicle customers needed financing, Tata Capital could structure solutions. No single synergy is transformative, but collectively they provide capabilities that standalone automakers struggle to match. The financial architecture tells the story in numbers. Tata Motor saw a total revenue of around 4.3 trillion Indian rupees in financial year 2024—approximately $52 billion. But the breakdown reveals the complexity: JLR contributing 71% of revenues with EBIT margins around 8.5%, the Indian CV business with 12% EBITDA margins but lower volumes, and the PV business with improving but still modest 7-8% margins. The consolidated EBITDA margin of 14.3% masks wide variations across segments and geographies.

The competitive response to Chinese entrants deserves special attention. As BYD, Geely, and others expand globally with deep pockets and government support, traditional automakers face an existential challenge. Tata's response has been nuanced. Rather than compete directly on cost (impossible against Chinese scale) or technology (where Chinese EV companies have advantages), Tata leverages relationships and ecosystem advantages. In India, the "Make in India" narrative resonates. Globally, the British heritage of JLR and Italian legacy of Iveco provide differentiation that Chinese brands will take decades to build.

Risk management in this complex portfolio requires sophisticated thinking. Currency exposure alone is daunting—revenues in pounds, euros, rupees, and dozens of other currencies, while costs are similarly distributed. The company uses natural hedging where possible (UK revenues offsetting UK costs) and financial hedging for residual exposure. But the real hedge is operational flexibility—the ability to shift production, sourcing, and even model allocation based on currency movements.

The technology strategy represents perhaps the biggest challenge and opportunity. Unlike Tesla, which can focus solely on EVs, or Toyota, which can leverage massive scale for hybrid development, Tata must simultaneously manage: ICE technology for commercial vehicles that will remain relevant for decades, luxury EVs for JLR that must compete with German engineering excellence, affordable EVs for India that must be profitable at price points others can't imagine, hydrogen fuel cells for long-haul trucks, and autonomous technology for everything from mining trucks to luxury sedans.

The investment required is staggering—over £3.5 billion annually across the group. But the alternative—falling behind technologically—is existential. The solution has been selective partnerships: with Stellantis for small commercial vehicles, with Cummins for engines, with Microsoft for connected vehicle platforms. Each partnership trades some control for reduced investment and faster time-to-market.

The human capital dimension often goes unnoticed but is crucial. Tata Motors employs over 80,000 people directly, from software engineers in Bangalore to craftsmen hand-stitching leather at JLR's SVO division. Managing this diverse workforce—unionized factory workers in Italy, highly paid engineers in the UK, cost-conscious operators in India—requires cultural sensitivity that financial metrics don't capture. The company's ability to maintain labor peace while restructuring operations has been remarkable, particularly compared to the strikes and disruptions that have plagued competitors.

Looking forward, the business model faces inflection points. The shift from products to services—selling mobility rather than vehicles—will require new capabilities. The consolidation of the global auto industry will create opportunities and threats. The regionalization of supply chains post-COVID will advantage companies with distributed manufacturing. Climate regulations will accelerate the shift to clean transportation. In each transition, Tata Motors' portfolio approach—messy and complex as it is—may prove more resilient than focused strategies that bet everything on a single technology or market.

IX. Playbook: Lessons in M&A and Transformation

The conference room at Harvard Business School was packed beyond capacity. MBA students lined the walls, venture capitalists filled the back rows, and several Fortune 500 CEOs sat in the front, all waiting to hear Natarajan Chandrasekaran, Chairman of Tata Sons, explain how an emerging market conglomerate had successfully executed some of the most complex cross-border acquisitions in automotive history. His opening line was unexpected: "The secret to successful M&A is knowing when not to integrate."

This counterintuitive wisdom captures the essence of the Tata M&A playbook, refined over two decades and billions of dollars in deals. Unlike the traditional Western approach—integrate quickly, extract synergies, impose corporate culture—Tata has developed what might be called "patient capital with strategic intent." It's a philosophy born from both success (JLR, Iveco) and failure (Corus Steel), and it offers lessons that transcend industry boundaries.

The first principle: Preserve the crown jewels. When Tata acquired JLR, conventional wisdom suggested integrating purchasing to leverage scale, centralizing R&D to reduce costs, and imposing Indian cost discipline on British operations. Tata did none of this. They recognized that what made Jaguar and Land Rover valuable—British heritage, design capability, brand prestige—would be destroyed by integration. Instead, they provided capital and strategic patience while maintaining arms-length governance. The same principle is being applied to Iveco, with its headquarters remaining in Turin and Italian management retained.

The second principle: Buy distress, not disaster. Both JLR and Iveco were acquired when their sellers were desperate but the assets remained fundamentally sound. JLR had strong brands and products; it just needed capital and time. Iveco had leading market positions and technology; it lacked scale and investment capacity. This differs fundamentally from buying broken businesses hoping to fix them—a strategy that rarely works. The key is identifying assets where temporary distress has created a valuation discount but hasn't destroyed fundamental capabilities.

The third principle: Ecosystem, not synergy. Traditional M&A focuses on cost synergies—eliminating duplicate functions, reducing headcount, consolidating facilities. Tata focuses on ecosystem benefits that create value without integration. JLR uses Tata Technologies for engineering services but maintains its own design centers. Iveco will benefit from Tata's presence in emerging markets but won't be forced to use Tata distribution. The EV business leverages TCS's software capabilities but develops its own vehicle platforms. These voluntary collaborations often create more value than forced integration.

The pattern recognition across deals reveals sophisticated learning. The JLR acquisition in 2008 was funded through expensive bridge financing that nearly broke the company when markets crashed. For Iveco in 2025, financing was secured in advance with better terms. With JLR, Tata initially tried to send Indian managers to the UK, creating cultural friction. With Iveco, they committed upfront to maintaining local management. Each deal builds on lessons from the previous one.

The timing dimension deserves special attention. Tata has consistently bought during periods of industry disruption: JLR during the financial crisis when luxury spending collapsed, Daewoo during Asian financial turmoil, Iveco as the industry transitions to electric and autonomous vehicles. This isn't opportunism—it's strategic patience. By maintaining strong balance sheets during good times, Tata can act decisively when others are paralyzed by crisis.

Risk management in these mega-deals shows institutional learning. The JLR acquisition was essentially a bet-the-company move—if it had failed, Tata Motors might not have survived. The Iveco deal, while large, is structured to preserve financial flexibility. The purchase consideration is clearly defined, the separation of the defence business reduces complexity, and the financing doesn't jeopardize the credit rating. This isn't risk aversion—it's risk intelligence.

The cultural dimension transcends national boundaries. Tata's approach to cross-border M&A reflects Indian philosophy—the concept of "Vasudhaiva Kutumbakam" (the world is one family) translates into respecting local cultures while building global capabilities. This is different from both American-style aggressive integration and Chinese-style hands-off financial investment. It's a middle path that preserves identity while enabling collaboration.

The transformation agenda post-acquisition follows a consistent pattern. First, stabilize operations and restore confidence. With JLR, this meant guaranteeing wages and maintaining product plans despite losses. Second, invest in products and technology. JLR received billions for new models even when losing money. Third, expand strategically. JLR's China entry and Iveco's emerging market expansion will follow proven templates. Fourth, build ecosystem connections. Gradually introduce capabilities from across the group without forcing integration.

The failure points are equally instructive. The Nano showed that engineering excellence without market understanding leads to failure. The struggles with passenger cars in India demonstrate that competing against entrenched leaders requires differentiation, not just competence. The 2018-2019 JLR crisis revealed the dangers of over-dependence on a single market (China). Each failure has refined the playbook, making subsequent executions more sophisticated.

For other companies contemplating transformative M&A, the Tata playbook offers actionable insights. Start with strategic intent, not financial engineering. Ensure cultural compatibility, not just strategic fit. Maintain operational flexibility rather than pursuing rigid integration. Invest through downturns rather than withdrawing. Build ecosystems rather than hierarchies. Most importantly, measure success over decades, not quarters.

The meta-lesson is about capability building. Each acquisition hasn't just added assets—it has enhanced Tata's ability to execute the next deal. The company that struggled to integrate a single domestic acquisition twenty years ago now confidently manages a global portfolio spanning continents, cultures, and technologies. This learning curve advantage may be the most valuable outcome of all.

X. Bull & Bear Case Analysis

The equity research analyst at Morgan Stanley Mumbai had been staring at her Tata Motors model for three hours. Every assumption she tweaked seemed to swing the valuation by billions. The company was either dramatically undervalued or a value trap—depending entirely on which future you believed. Her report would influence billions in institutional investment, but first she had to resolve the fundamental tension: How do you value a company that's simultaneously in four different businesses, three major transformations, and exposed to every major automotive trend?

The Bull Case: A Global Powerhouse in Formation

The optimistic scenario starts with sheer scale. Post-Iveco, Tata Motors becomes one of the world's largest commercial vehicle manufacturers with unmatched geographic diversity. This isn't just about size—it's about resilience. When European truck demand falls, Indian infrastructure spending compensates. When Chinese luxury car sales decline, American SUV demand fills the gap. This portfolio diversification, properly managed, could deliver more stable earnings than focused peers.

The EV leadership position in India represents a potentially massive moat. With over 70% market share in electric passenger vehicles and growing dominance in electric commercial vehicles, Tata has first-mover advantage in what could become the world's largest EV market by volume. The $9 billion valuation placed on the EV subsidiary by sophisticated investors like TPG suggests the market hasn't fully appreciated this option value. If India achieves even half its EV adoption targets, this business alone could be worth more than Tata Motors' current market capitalization.

JLR's transformation potential remains underappreciated. The Range Rover brand has pricing power comparable to German luxury brands but at much lower volumes. The new Range Rover sells for £100,000+ with operating margins exceeding 15%. If JLR can successfully launch electric versions while maintaining brand prestige, the earnings potential is substantial. A successful Jaguar relaunch as an ultra-luxury electric brand could add billions in value.

The Iveco acquisition at 0.5x revenues compares favorably to precedent transactions in the commercial vehicle space, typically done at 0.8-1.2x revenues. If Tata can improve Iveco's margins from 6% to even 8%—still below industry leaders—the value creation would exceed the purchase price. The revenue synergies from accessing emerging markets through Tata's distribution could add another €1-2 billion in high-margin revenues.

The technology transformation presents massive optionality. Tata's partnerships with Microsoft for connected vehicles, with Tata Technologies for engineering services, and with TCS for software development provide capabilities that standalone automakers must build or buy expensively. The market values Tesla's software capabilities at hundreds of billions; even a fraction of that value creation would transform Tata Motors' valuation.

The Tata Group backing provides a competitive advantage that's hard to quantify but real. Access to patient capital, ability to leverage group companies for capabilities, brand trust in emerging markets, and financial support during crises create strategic flexibility that independent automakers lack. This "conglomerate premium" (rather than discount) could become more valuable as the industry consolidates.

Valuation metrics support the bull case. At current prices, Tata Motors trades at approximately 5x forward P/E versus global automaker averages of 7-8x. The EV/EBITDA multiple of 3x compares to luxury automakers at 5-7x. If you value JLR like a luxury company, the Indian operations like an emerging market leader, and the EV business like a growth story, the sum-of-parts valuation exceeds the current market cap by 50-70%.

The Bear Case: Complexity Overwhelming Capability

The pessimistic scenario starts with execution risk. Managing JLR's luxury transformation, Iveco's integration, Indian EV expansion, and commercial vehicle cycles simultaneously stretches management bandwidth beyond breaking point. History shows that companies attempting multiple transformations usually fail at all of them. The Nano debacle and passenger car struggles in India demonstrate that Tata's execution isn't infallible.

Debt levels post-Iveco acquisition approach uncomfortable territory. While management claims the deal won't affect credit ratings, rating agencies are watching nervously. If JLR's cash generation falters or Iveco integration costs exceed estimates, the company could face a credit crunch similar to 2008-2009. Rising global interest rates make refinancing expensive, and automotive companies are vulnerable to sudden demand drops that destroy cash flow.

Chinese competition represents an existential threat across all businesses. BYD is entering India with EVs priced 30% below Tata's. Geely is expanding in Europe, competing directly with Iveco. Chinese luxury brands like Nio and Li Auto are attacking JLR's market in China. The speed and scale of Chinese expansion, backed by government support and massive domestic markets, could overwhelm Tata's carefully built positions.

The EV transition timing creates a valley of death scenario. ICE vehicle profits will decline before EV profits materialize. The billions required for EV investment must be funded from declining ICE cash flows. JLR needs £15+ billion for electrification. The Indian EV business requires massive charging infrastructure investment. Iveco needs new platforms for electric trucks. The capital requirements could exceed cash generation for years.

Cyclical headwinds are strengthening across all markets. Global economic slowdown reduces commercial vehicle demand. Luxury car sales correlate with wealth effects that are turning negative. Indian economic growth is moderating from post-COVID highs. European recession risks are rising. A synchronized global downturn—increasingly likely—would hit all of Tata Motors' businesses simultaneously.

The complexity discount is real and justified. Investors struggle to value conglomerates, typically applying 20-30% discounts to sum-of-parts valuations. Tata Motors is essentially four different companies (JLR, Indian CV, Indian PV, Iveco) with different economics, cycles, and growth profiles. This complexity makes it uninvestable for many funds with specific mandates. The persistent undervaluation might be structural, not temporary.

Technology disruption could obsolesce existing advantages. If autonomous vehicles arrive faster than expected, the value of manufacturing expertise diminishes. If mobility-as-a-service replaces vehicle ownership, asset-heavy manufacturers suffer most. If battery technology breakthroughs favor new entrants, existing EV investments become stranded assets. Tata Motors' traditional capabilities might become liabilities in a disrupted future.

The Probabilistic View

Reality likely lies between extremes. The highest probability scenario involves successful but slow transformation. JLR maintains luxury position but with compressed margins due to EV transition costs. Iveco integration proceeds without major issues but synergies take longer to realize. The Indian EV business grows but faces increasing competition. Commercial vehicles remain cyclical but structural growth in India provides support.

In this base case, Tata Motors generates adequate returns for patient investors but doesn't deliver spectacular outperformance. The company successfully navigates the EV transition but at significant cost. Market share is defended but margins compress. The stock delivers returns in line with global automaker averages—adequate but not exceptional.

The key variables to monitor are JLR's order book (leading indicator of luxury demand), Indian CV market share (proxy for competitive position), EV business losses (cash burn versus market share gains), Iveco integration metrics (synergy realization versus cost), and balance sheet stress indicators (debt/EBITDA, interest coverage). Significant deviation in any of these could tilt the probability toward either the bull or bear scenario.

For investors, Tata Motors represents a complex option on multiple automotive megatrends. Those believing in India's growth, luxury market resilience, successful EV transition, and management execution should be buyers. Those worried about Chinese competition, execution complexity, technology disruption, and cyclical headwinds should avoid. There's no middle ground—this is either a multi-bagger or a value trap. The beauty and terror of investing in transformation is that both outcomes remain entirely possible.

XI. Future Outlook & Strategic Questions

The war room at Tata Motors' Pune headquarters runs 24/7 now. Multiple screens track everything from lithium prices in Chile to semiconductor availability in Taiwan, from Chinese EV registrations to European emissions regulations. A team of strategists, half under 30 years old, debates scenarios that would have seemed like science fiction a decade ago. Should they partner with Apple on autonomous vehicles? Can they compete with BYD's vertical integration? Will hydrogen fuel cells make battery investments obsolete? The questions coming at Tata Motors aren't just about business strategy—they're existential.

The EV Transition: Dancing with Dragons

The electric vehicle transformation isn't a choice anymore—it's survival. But the pathway remains treacherous. In India, Tata's 70% EV market share looks dominant until you realize the market is only 2% of total sales. The real test comes when Chinese manufacturers enter seriously. BYD has already announced plans for a local factory. Their ability to produce EVs at 30% lower cost through vertical integration—they make their own batteries, chips, even tires—represents a competitive threat unlike anything Tata has faced.

The response requires careful calibration. Tata can't match Chinese scale or government subsidies. But they have advantages: understanding of Indian consumer preferences, established service networks, and the emotional appeal of buying Indian. The strategy emerging involves selective partnerships (battery cells with Chinese or Korean partners), focus on specific segments (commercial vehicles where local knowledge matters), and ecosystem play (bundling vehicles with charging, financing, and insurance through Tata companies).

JLR's electrification presents different challenges. Range Rover customers will pay premiums for electric versions that maintain luxury and capability. But Jaguar's rebirth as an ultra-luxury electric brand—competing with Bentley and Rolls-Royce rather than BMW—requires flawless execution. One failed model or quality issue could destroy decades of brand building. The investment required—£15+ billion over five years—will consume most of JLR's cash generation, leaving little room for error.

Software-Defined Vehicles: The Capability Gap

The shift from hardware to software as the primary value driver in vehicles represents Tata Motors' biggest capability gap and opportunity. Tesla's ability to improve vehicles through over-the-air updates, generating recurring revenue from software features, has redefined automotive business models. Chinese EV makers have followed suit, offering everything from karaoke systems to gaming platforms in their vehicles.

Tata's response leverages group capabilities but faces integration challenges. TCS, one of the world's largest IT services companies, provides software expertise but lacks automotive domain knowledge. Tata Elxsi offers design and validation services but isn't a product company. The solution emerging involves partnerships (with Microsoft for cloud infrastructure, with Google for infotainment) while building internal capabilities through acquisition and hiring.

The commercial vehicle opportunity might be even larger. Fleet management software, predictive maintenance, route optimization, and driver assistance systems could generate recurring revenues exceeding vehicle sales. Iveco's existing telematics capabilities combined with TCS's analytics expertise could create a platform serving millions of commercial vehicles globally. But execution requires cultural change—shifting from selling products to providing services.

Autonomous Driving: Partner or Perish

The autonomous vehicle revolution keeps receding into the future—always five years away for the past decade. But when it arrives, the impact will be catastrophic for unprepared manufacturers. The investment required to develop Level 4/5 autonomy exceeds $10 billion, beyond Tata Motors' capacity. The choice isn't whether to develop autonomous capability but with whom to partner.

The options each have trade-offs. Partnering with Waymo or Cruise provides technology but reduces Tata to a contract manufacturer. Joining an industry consortium shares costs but dilutes competitive advantage. Focusing on specific use cases (mining trucks, defined route buses) reduces investment but limits market opportunity. The emerging strategy involves selective participation—advanced driver assistance systems for passenger vehicles, autonomous capability for controlled environments, partnerships for robo-taxi services.

The Next Decade: Scenarios and Strategies

Three scenarios frame Tata Motors' strategic planning for the 2030s:

Scenario 1: "Gradual Transition" - EVs reach 30% penetration by 2035, ICE vehicles remain relevant, autonomy limited to specific applications. In this world, Tata's portfolio approach thrives. JLR maintains luxury position with mixed powertrains. Indian operations balance ICE and EV. Iveco focuses on alternative fuels for long-haul. The company generates steady returns without dramatic transformation.

Scenario 2: "Disruption Acceleration" - EVs reach 60% penetration by 2030, Chinese players dominate, mobility-as-a-service replaces ownership in cities. Here, only the paranoid survive. Tata must accelerate transformation, potentially divesting lagging businesses, forming bold partnerships, accepting lower returns during transition. Success requires perfect execution and some luck.

Scenario 3: "Regional Fragmentation" - Geopolitical tensions create regional blocks, supply chains localize, technology standards diverge. This scenario favors Tata's distributed manufacturing and multi-brand portfolio. Indian operations serve South Asia and Africa. JLR focuses on Anglo markets. Iveco dominates Europe. The complexity becomes an advantage in a fragmented world.

The strategic questions cascading from these scenarios don't have clear answers:

- Should Tata Motors remain integrated or split into focused companies?

- Can premium brands like JLR and Iveco coexist with value segments in India?

- How much debt is acceptable to fund transformation?

- When does financial prudence become strategic timidity?

- Should they build, buy, or partner for critical technologies?

- How do you balance quarterly earnings pressure with decade-long transformation?

Succession Planning: The Leadership Challenge

The human dimension might be most critical. The generation that built Tata Motors—engineers who understood mechanical systems, leaders who navigated License Raj and liberalization—is retiring. The new generation must be equally comfortable with software and steel, Silicon Valley and Mumbai, quarterly earnings calls and decade-long transformations.

The leadership transition extends beyond individuals to institutional capability. Can a company with a 150-year heritage develop startup agility? Can engineers trained in mechanical excellence embrace software thinking? Can an organization built on trust and relationships compete with companies optimized for efficiency? These cultural transformations often determine success more than strategic choices.

The Unasked Questions

The most important strategic questions might be ones not yet being asked:

What if personal vehicle ownership becomes socially unacceptable due to climate concerns? What if India leapfrogs directly to autonomous shared vehicles, skipping personal EV adoption? What if breakthrough technologies (solid-state batteries, hydrogen fuel cells, or something not yet invented) obsolete current investments? What if the next generation simply doesn't care about driving?

These aren't idle speculation—they're the kind of discontinuities that have destroyed seemingly invincible companies. Kodak invented digital photography but couldn't imagine a world without film. Nokia dominated mobile phones but missed the smartphone revolution. Could Tata Motors, for all its transformation, be preparing for the last war while the next one takes a completely different form?

The answer lies not in predicting the future but in building adaptability. The companies that survive technological discontinuities aren't necessarily those with the best strategies but those with the ability to recognize change and respond quickly. Tata Motors' complex portfolio, often criticized by financial markets, might be its greatest asset—multiple options for multiple futures.

As one senior executive put it during a late-night strategy session: "We don't know if the future is electric, hydrogen, or something else. We don't know if people will own vehicles or share them. We don't know if drivers will be human or artificial. But we know transportation needs will exist, and we're determined to serve them, whatever form they take." This humility about the future, combined with determination to participate in it, might be the most important strategic asset of all.

XII. Recent News

The news alerts never stop. Every morning, Tata Motors' leadership team receives a digest of overnight developments—new Chinese EV launches, European regulation changes, commodity price movements, competitor announcements. The velocity of change in the automotive industry has never been higher. Here are the critical developments shaping Tata Motors' near-term trajectory:

The Q3 FY25 results announced in January 2025 showed resilience despite headwinds. JLR delivered record quarterly revenue with the highest EBIT margin in a decade, though order books were declining from peaks. The Indian CV business saw volumes decline but margins improve through cost control. The PV business maintained market share despite increasing competition. But beneath the headlines, structural shifts were evident—the mix shifting toward EVs, commercial customers demanding total solutions rather than just vehicles, and luxury buyers increasingly considering Chinese alternatives.

The integration of Iveco remains on track for completion by Q2 2026, but early challenges are emerging. European unions are demanding stronger job guarantees despite Tata's commitments. The separation of the defence business is proceeding but complex. Some suppliers are concerned about payment terms under new ownership. These are typical acquisition challenges, but their resolution will determine whether synergies materialize on schedule.

Regulatory developments are accelerating globally. India's FAME III policy, expected by March 2025, will reshape EV subsidies and potentially alter competitive dynamics. European Euro 7 emissions standards, delayed but not cancelled, require billions in engine development. The US Inflation Reduction Act's local content requirements complicate JLR's electric vehicle strategy. Each regulation requires strategic response, investment allocation, and often architectural changes to products.

Technology partnerships are proliferating. The collaboration with Stellantis on light commercial vehicles provides scale without investment. The Microsoft partnership on connected vehicle platforms accelerates software capability development. Discussions with multiple battery manufacturers for Indian cell production continue. Each partnership involves trade-offs between control and capability, speed and strategic flexibility.

The competitive landscape keeps intensifying. BYD's entry into India with the Atto 3 and Seal has begun, with aggressive pricing and strong products. Vinfast from Vietnam is expanding globally with massive funding and ambitious plans. Traditional competitors like Volkswagen and Toyota are accelerating their own transformations. The window for establishing sustainable positions in new segments is narrowing rapidly.

Market Dynamics and Financial Implications

The stock market's reaction to recent developments has been volatile but revealing. The initial 4% drop after the Iveco announcement has reversed as investors better understand the strategic logic. But the stock remains range-bound, caught between enthusiasm for transformation potential and concern about execution complexity. Institutional investors are particularly focused on free cash flow generation during this capital-intensive period.

Credit markets are carefully watching debt metrics. While the Iveco acquisition financing was well-received, rating agencies have placed Tata Motors on watch for potential downgrade if integration costs exceed estimates or if JLR's cash generation weakens. The spread on Tata Motors' bonds versus government securities has widened slightly, indicating some investor concern but not alarm.

The currency markets add another layer of complexity. The pound's strength versus the rupee helps JLR translation but hurts competitiveness. The euro's weakness makes Iveco acquisition financing cheaper but reduces translated earnings. The rupee's stability versus the dollar helps input cost management but makes exports less competitive. Managing these cross-currents requires sophisticated treasury operations and strategic hedging.

Supply chain disruptions continue despite improvement from COVID peaks. Semiconductor availability has improved but isn't fully normalized. Battery cell supply for EVs remains tight globally. Specialized steel for lightweight vehicles faces periodic shortages. Logistics costs, while down from peaks, remain elevated. Each disruption requires tactical response while maintaining strategic direction.

Looking Ahead: Key Milestones to Watch

The next twelve months will be pivotal. The Range Rover Electric launch in late 2025 will test JLR's ability to maintain luxury positioning in EVs. The Iveco integration milestones will indicate execution capability. The Indian EV market share battle with BYD and others will show competitive resilience. The commercial vehicle cycle in India, potentially turning up in H2 FY25, will impact cash generation.

Investor presentations scheduled for the coming months will provide more granular guidance. The Capital Markets Day in March 2025 will detail the Iveco integration plan and synergy targets. The annual investor meet in May will update on EV strategy and capital allocation. Quarterly earnings calls will track progress against ambitious transformation goals.