Tata Communications: The Digital Fabric of the Global Internet

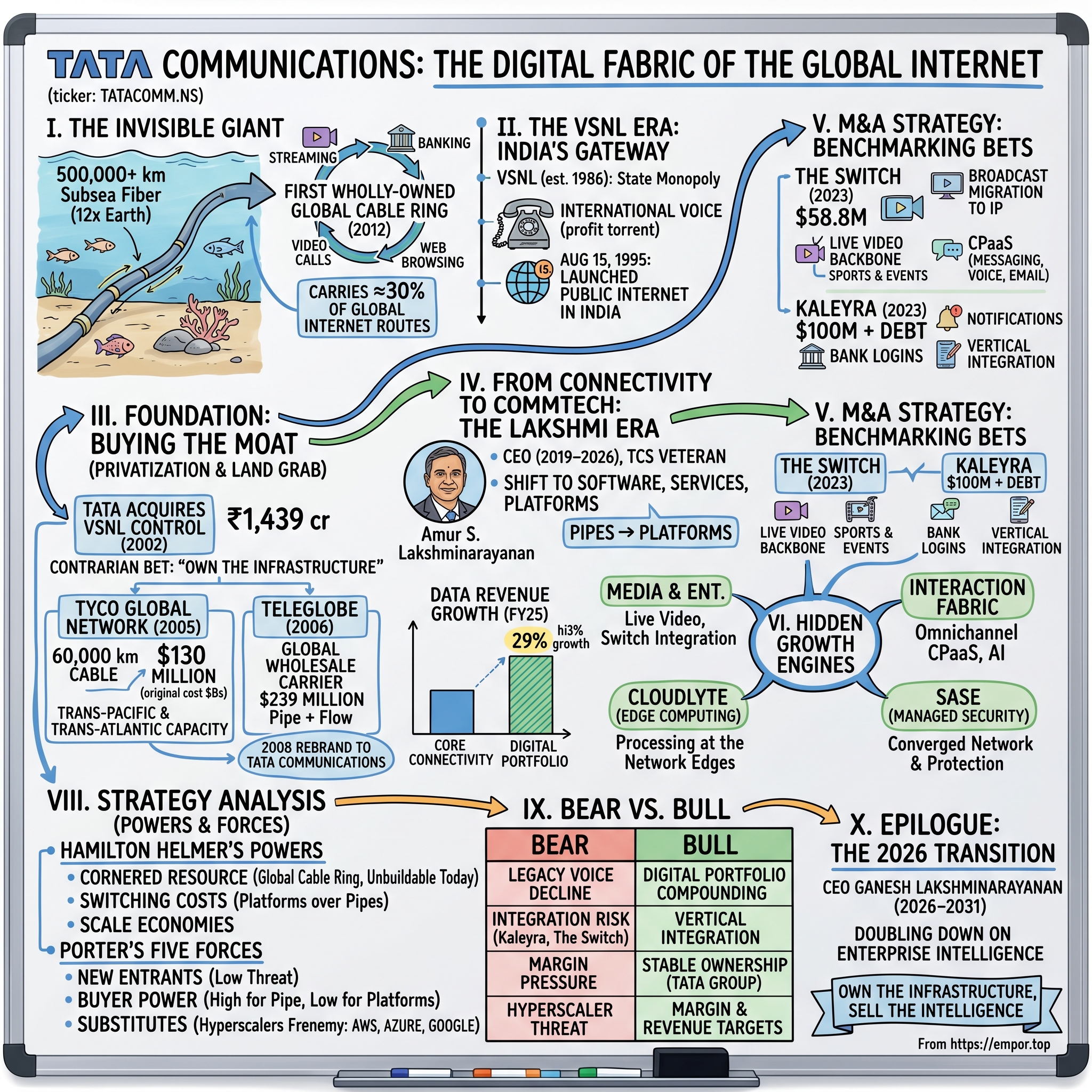

I. The Invisible Giant

Picture the floor of the Atlantic Ocean. Two and a half miles down, in cold and total darkness, lies a cable about as thick as a garden hose. Inside its armored sheath, past the steel wires and the copper conductor and the petroleum jelly that keeps the seawater out, are a few hair-thin strands of ultra-pure glass. Down those strands, lasers fire pulses of light billions of times per second. Every email between London and New York, every transatlantic trade confirmation, every Netflix stream — it does not travel by satellite, as most people vaguely assume. It travels through glass on the seabed. Satellites carry a rounding error of intercontinental traffic; the cables carry essentially all of it.

This is the business Tata Communications quietly came to dominate. Not the visible, consumer-facing layer of the internet — the apps, the websites, the brands you actually name — but the invisible plumbing underneath. The company likes to call itself a "digital fabric," and once you understand the metaphor it is hard to unsee. Fabric is woven from individual threads, and on its own each thread is unremarkable. But woven together, the threads become something you can build a life on top of. Tata Communications weaves connectivity, cloud routing, security, and communications software into a single mesh that enterprises stitch into the foundations of their operations.

It is worth dwelling for a moment on why these cables matter so much, because the intuition most people carry is simply wrong. Ask the average person how an email gets from London to Singapore and they will gesture vaguely upward — to satellites, to "the cloud," to something orbital and wireless. The reality is almost defiantly physical. More than 95% of all intercontinental data — voice, video, financial transactions, the entire machinery of globalization — travels through fewer than five hundred subsea cables lying on the ocean floor. A satellite link introduces a delay of roughly half a second as the signal climbs to geostationary orbit and falls back; a fiber cable does the same job in a fraction of that, with vastly more capacity. When a trader in Mumbai executes against a price in Chicago, the few milliseconds of difference between one cable route and another can be worth millions. The cables are not a backup to the wireless internet. They are the internet. Everything else — the cell tower, the home router, the Wi-Fi — is just the last few feet of a journey that was almost entirely undersea.

The companies that own these cables, then, occupy a position of strange and quiet power. They are toll-keepers on roads that no one can see and few can build. And among them, Tata Communications is unusual not because it participates — dozens of carriers do — but because of the completeness of what it controls.

The scale is genuinely difficult to fathom. The company operates more than 500,000 kilometers of subsea optical fiber — enough to wrap around the Earth more than a dozen times — plus over 200,000 kilometers of terrestrial fiber threading through cities and across continents.1 In 2012, it became the first company on Earth to complete a wholly-owned fiber ring all the way around the globe: a continuous loop of cable it alone controlled, so that traffic could circle the planet in either direction and reroute instantly if any single segment was cut by an earthquake, a ship's anchor, or a fishing trawler.2 Most carriers own pieces of cables through consortiums, sharing the cost and the capacity. Tata built and bought enough that it could draw an unbroken circle and call the whole thing its own.

For a long-term investor, the first thing to internalize is this: Tata Communications is not a telco in the way Verizon or भारती एयरटेल Bharti Airtel are telcos. It does not chase millions of retail mobile subscribers or fight over data-pack pricing in crowded markets. Its customers are governments, banks, broadcasters, cloud providers, and roughly the largest enterprises in the world. It sells the underlying capacity — and, increasingly, the intelligence layered on top of it — to the organizations that everyone else depends on. There is no consumer brand to build, no retail churn to manage, no subsidized handsets to give away. The business is wholesale and enterprise to its core, which is exactly why it is invisible to the public and yet sits at the center of nearly everything the public does online.

This invisibility has a curious financial consequence. Because the company sells no product you can hold and runs no advertisements you will ever see, it trades and is discussed far less than its strategic importance would suggest. It is the kind of asset that institutional infrastructure investors prize precisely because the broader market under-attends to it: mission-critical, hard to replicate, and embedded in the operations of customers who cannot easily leave. The thesis a patient investor is being asked to underwrite is whether a company that owns this much irreplaceable physical infrastructure can successfully transform itself into something that earns software-like economics on top of it.

How a 1980s Indian state monopoly came to own that fabric is the heart of the story, and it begins in an era when an international phone call from Mumbai was a small bureaucratic adventure.

II. The VSNL Era: India's Gateway to the World

To understand Tata Communications, you have to first understand what India was like before it. In 1986, placing a call from Delhi to a relative in Chicago meant going through an operator, waiting — sometimes for hours — and paying a fortune for a crackling, delayed connection. There was exactly one organization permitted to carry that call across India's borders, and in March 1986 the government gave it a formal name: विदेश संचार निगम लिमिटेड Videsh Sanchar Nigam Limited, or VSNL — literally, "Foreign Communications Corporation."3

VSNL was a classic state monopoly, and it behaved like one. It held an exclusive license over all international long-distance (ILD) traffic into and out of India. Every overseas call, every telex, every early data link — all of it had to pass through VSNL's gateways. In a liberalizing-but-still-protected economy, this was an extraordinary franchise. It was a tollbooth on the only road out of the country, and it had no competitors by law.

To appreciate just how lucrative that tollbooth was, you have to remember the economics of international calling in the 1990s. Settlement rates between national carriers were sky-high, and a single minute of a call between India and the Gulf or India and the United States could be priced at a level that today looks almost comical. With a vast Indian diaspora scattered across the Middle East, North America, and the United Kingdom — millions of workers and families who needed to call home — VSNL sat on a torrent of inbound and outbound minutes that it could meter at monopoly prices. The company was, for years, one of the most reliably profitable public-sector enterprises India had, throwing off cash with the placid certainty of an organization that faced no competition and set its own tariffs within a regulated band. It is hard to overstate how comfortable this was, and comfort, in business, is usually the prelude to disruption.

But VSNL's most consequential act was not a phone call. It was an internet connection. On August 15, 1995 — India's Independence Day, a date chosen for maximum symbolism — VSNL switched on the Gateway Internet Access Service, making public internet access available in India for the very first time.[^4] In a country of, at that point, hundreds of millions of people, VSNL was the single doorway through which the entire nation would meet the World Wide Web. It is difficult to overstate the strategic significance of being the company that literally connected India to the internet. VSNL was not merely a participant in the digital revolution arriving on Indian shores; it was the gate.

That gatekeeper position is exactly what made VSNL so valuable — and so politically fraught — when the question of privatization arrived. By the turn of the millennium, the Indian government was selling down stakes in its public-sector enterprises under a broader liberalization push, and a tightly-controlled telecom asset sitting astride all of India's international connectivity was one of the crown jewels. The early Indian IT-services boom was underway. Bangalore and Hyderabad were filling with software engineers writing code for American banks, and every line of that code — every batch of processed data shipped back to a client in New Jersey or London — had to travel out of the country over an international link. Whoever owned the gateway owned a chokepoint on the most important growth industry India had ever produced.

There was, however, a clock ticking that made the franchise far less eternal than it looked. The government had already committed to ending VSNL's monopoly on international long-distance — competition was scheduled to arrive, and when it did, those fat settlement margins would compress brutally. So the privatization was, in a sense, a sale of a melting asset dressed up as a sale of a monopoly. The buyer would be inheriting the cash flows of yesterday and the obligation to invent the business of tomorrow. This is the crucial context for understanding why the Tatas, of all the bidders, were the natural and motivated buyer.

In February 2002, the government did the deal. It disinvested a 25% stake in VSNL — along with management control — to Panatone Finvest Limited, a vehicle of the Tata Group, for a reported ₹1,439 crore.4 On paper it was "just" a quarter of the equity, but the transfer of management control was the real prize: the Tatas now ran the company. For one of India's most storied industrial houses — a 150-year-old conglomerate that, at the time, was building the dominant Indian IT-services giant in टीसीएस Tata Consultancy Services — acquiring the gatekeeper to global connectivity was a strategically obvious move. Tata's IT business lived and died on international bandwidth. Owning the company that supplied it was both an offensive bet on India's digital future and a defensive hedge on its own supply chain.

What the Tatas inherited, though, was a company built for a world that was about to vanish. VSNL's profits came overwhelmingly from international voice — those expensive, regulated phone calls — and that business was already being hollowed out by deregulation and by the internet itself. Voice-over-internet technology was beginning to make it possible to route a call as data packets for a tiny fraction of the cost of a traditional circuit, and once that genie was out, no monopoly license could put it back. The new owners faced a stark choice that would define the next twenty years: defend a melting ice cube with lawyers and lobbying, or take the cash it was still throwing off and buy a position in something that would actually last.

They chose to buy — and not timidly. The Tatas understood that a former monopolist's worst instinct is to defend the old business to the death, and that the companies which survive technological transitions are the ones willing to cannibalize themselves before someone else does it for them. The capital VSNL had accumulated through its monopoly years was about to be redeployed into a global land grab, executed with a contrarian's timing that would prove to be one of the great opportunistic infrastructure trades of the decade.

III. The Foundation: Buying the Moat

In the early 2000s, the conventional wisdom in technology was that the smart money went "asset-light." The dot-com crash had just incinerated hundreds of billions of dollars, and a disproportionate share of that wreckage was in physical infrastructure — especially telecom. Companies had laid fiber across oceans on the assumption that internet traffic would grow to infinity overnight, financed it with mountains of debt, and then watched demand arrive more slowly than the interest payments. The fashionable lesson investors drew was: never own the heavy stuff. Own the brand, the software, the customer relationship. Let someone else sink billions into the ground and the sea.

Tata looked at the same wreckage and drew the opposite conclusion. If the world had just massively overbuilt subsea cable and then gone bankrupt, then the cable was about to be available for cents on the dollar. The most expensive part of owning a global network — actually building it — had already been paid for by someone else's shareholders. All Tata had to do was show up with cash at the liquidation sale.

This is a deceptively profound insight, and it is worth slowing down to appreciate the contrarian courage it required. The dominant narrative of 2002–2004 was that physical telecom infrastructure was a value trap — a graveyard where capital went to die. Companies like Global Crossing, which had spent something on the order of $15 billion building a worldwide network, had collapsed into bankruptcy. The smart, fashionable money was fleeing anything with a high fixed-cost base. To walk into that fire and start buying cable required believing two things that the market did not: first, that internet traffic would eventually grow into and far past the overbuilt capacity (it would, spectacularly); and second, that a physical asset acquired below replacement cost is one of the most defensible positions in all of business, because no rational competitor will ever build a duplicate when they could just buy the existing one. Tata was, in effect, making a bet on mean reversion in the most capital-intensive corner of technology — and funding it with the cash flows of a dying voice monopoly. It was financial jiu-jitsu: use the melting asset to buy the permanent one.

The marquee purchase came in 2005. Tyco International, the industrial conglomerate then mired in one of the era's most notorious corporate scandals, had built the Tyco Global Network (TGN): a sprawling, state-of-the-art undersea cable system spanning roughly 60,000 kilometers across North America, Europe, and Asia, with points of presence in a dozen countries. It had cost an estimated several billion dollars to construct. VSNL bought essentially the entire thing for $130 million in cash.5 Read that again. A network that cost billions to lay was acquired for a figure that, against its replacement cost, rounds to a rounding error. It was the infrastructure equivalent of buying a skyscraper for the price of a parking space because the previous owner needed to raise cash by Friday.

This single transaction transformed VSNL from a regional Indian gateway into a genuinely global carrier overnight. It now owned trans-Pacific and trans-Atlantic capacity outright — the literal physical paths between the world's largest economies — along with thirty points of presence across a dozen countries, the on-ramps where the cable meets the land-based networks.5 Think about what that means strategically: an Indian company, barely two years out of government hands, suddenly controlled glass running directly between the United States and Japan, between Europe and Asia. It was no longer asking other carriers for permission to reach the world's data centers; it owned the road and could let others on, for a fee. The acquisition did not just add assets to a balance sheet. It changed the category the company competed in.

There is a second-order lesson here that long-term investors should file away. Distressed acquisitions of this kind only create value if the buyer can actually operate the asset and fund its ongoing maintenance — subsea cable requires constant, expensive upkeep, repair ships, and capacity upgrades. Plenty of bargain-hunters buy cheap infrastructure and then choke on the running costs. Tata could carry it because it had both the engineering depth inherited from VSNL and the financial backing of one of India's largest industrial groups. The bargain was only a bargain in hands that could keep it lit.

The very next year, Tata moved up the value chain. In February 2006, it completed the acquisition of Teleglobe, the Canadian wholesale-communications player, in a deal with an enterprise value of about $239 million — roughly $178 million in equity at $4.50 per share, plus the assumption of around $61 million in net debt.6 If TGN was the road, Teleglobe was the toll-collection business that ran on roads like it. Teleglobe was one of the world's largest wholesale carriers of international voice and data, the company that other telcos quietly handed their overseas traffic to. It came with more than a thousand wholesale customers and tens of billions of minutes of annual voice traffic. Tata had bought the pipe; now it bought the flow.

Here is the strategic elegance that is easy to miss. Tata was buying voice and data infrastructure at the exact moment voice was beginning its long decline — and it knew it. The bet was never that international phone minutes would stay lucrative. The bet was that the underlying glass — the cables themselves — would become the substrate for an explosion in data that almost nobody had yet priced in. Voice was the cash flow that justified the purchase price; data was the option you got for free on top. Owning the physical network meant that as voice margins eroded, Tata would still own the road, and could simply re-tenant it with the far larger traffic that streaming, cloud computing, and the mobile internet were about to generate.

This pattern — buy a declining business for its cash and its infrastructure, then ride the infrastructure into the next, larger market — is one of the most reliable value-creation playbooks in capital-intensive industries, and Tata ran it with unusual discipline. Compare it to the alternative path most legacy carriers took: defending voice revenue with regulatory lobbying, milking it for dividends, and waking up a decade later with a stranded asset and no growth story. Tata instead treated the glass as the asset and the traffic running over it as fungible. Voice minutes today, internet packets tomorrow, video feeds and cloud connections the day after — the cable did not care what flavor of light it carried, and neither did Tata's strategy.

In February 2008, the company retired the old VSNL name and rebranded everything — the Indian gateway, the global cables, the wholesale-voice business — under a single banner: Tata Communications.7 It was more than a marketing exercise. It was a declaration that this was no longer an Indian state monopoly with some foreign assets bolted on, but a global communications company that happened to be headquartered in India. The legacy telco trap — clinging to a dying voice business until it dragged you under — had been sidestepped by the simplest possible means: owning an asset so cheap and so durable that it would outlive whatever ran across it.

The infrastructure was now in place. The harder transformation — turning a company of cable engineers into a company that sold software and intelligence — would require a different kind of leader, and that leader arrived a decade later.

IV. From Connectivity to CommTech: The Lakshmi Era

In late 2019, Tata Communications handed its top job to a man who had spent his entire adult life inside the Tata Group, but almost none of it in telecom. अमुर स्वामीनाथन लक्ष्मीनारायणन Amur Swaminathan Lakshminarayanan — universally known simply as "Lakshmi" — became Managing Director and Group CEO effective November 26, 2019.8 His résumé read like a map of Tata's global ambitions: roughly 35 years inside the house of Tata, the overwhelming majority of it at Tata Consultancy Services, where he had been the country manager who built up TCS's business in the United Kingdom starting in 1999, gone on to run its operations across Europe and the United States, and then spent his final pre-Tata-Communications years as chief executive of TCS's joint venture in Japan with 三菱商事 Mitsubishi Corporation.8

Why does it matter that the man chosen to lead a cable-and-connectivity company came from a software-services background rather than a telecom one? Because his appointment was itself the strategy. Tata Communications did not need someone who could lay another cable. It needed someone who could sell software, services, and platforms — who instinctively saw the network not as the product but as the distribution channel for far more valuable products layered on top. Lakshmi's TCS pedigree was a signal: this company was going to stop thinking of itself as a carrier and start thinking of itself as what management began calling a "CommTech" company — communications plus technology, infrastructure plus intelligence.

Consider what TCS taught him. Tata Consultancy Services is the company that, more than any other, taught the world that Indian firms could sell sophisticated, high-margin technology services to the most demanding global enterprises — that the relationship with the client, deepened year after year through embedded teams and mission-critical projects, was worth far more than any single transaction. A leader steeped in that culture looks at a megabit of bandwidth and sees not a product to be sold once, but a beachhead from which to sell a deepening stack of services for a decade. He looks at a Fortune 500 customer buying connectivity and asks: what else of theirs can we run? Their security? Their cloud routing? Their customer messaging? That instinct — to convert a transaction into a relationship, and a relationship into a platform — is the genetic material Lakshmi imported from TCS into a company that had spent its life selling capacity by the meter.

It is also worth noting the cultural fit. Both companies are part of the same house of Tata, governed by the same values and the same ultimate shareholder in Tata Sons. Parachuting a TCS veteran into Tata Communications was not a hostile cultural transplant; it was moving a star player between two teams in the same franchise, with the implicit blessing of the group to remake the business in the image of its more celebrated sibling.

Lakshmi's leadership style carried the rigor of a services executive obsessed with execution and metrics, and nowhere was that more visible than in how he was paid. His own compensation was structured as a deliberate piece of "skin in the game." For FY2025 (the year ended March 2025), his total remuneration came in at roughly ₹19.2 crore, up about 12.6% year on year.9 But the headline number matters less than its shape. The company structured the package so that only a minority was guaranteed fixed pay; the bulk came through performance-linked incentives and restricted stock units that vested only against corporate-performance conditions set by the board's nomination and remuneration committee.10 In plain terms, most of the CEO's pay was contingent on the company actually hitting its targets and on the share price doing well — the variable, at-risk portion dwarfed the safe, guaranteed portion. For an investor, an executive who has voluntarily tied the majority of his own income to outcomes he is forecasting is a more credible forecaster.

The strategic shift Lakshmi drove can be summarized in one phrase: stop selling pipes, start selling platforms. A "pipe" is dumb capacity — a megabit of bandwidth between two points, indistinguishable from any competitor's megabit, sold on price, with margins that grind lower every year as the technology gets cheaper. This is the curse of the connectivity business: bandwidth, like memory chips, gets relentlessly cheaper per unit, so even as the volume of traffic explodes, the revenue per unit collapses. Running just to stand still. A "platform," by contrast, is something an enterprise customer builds on and cannot easily leave: a cloud-networking fabric, a security service, a messaging engine wired into their applications. Pipes are a commodity sold on price; platforms are a relationship priced on value. The entire transformation is an attempt to escape the deflationary gravity of the first by climbing into the second.

The clearest evidence that this pivot is working shows up in the company's revenue mix. In FY2025, total revenue reached about ₹23,109 crore, up roughly 10% over the prior year's ₹20,785 crore, with "data" (everything other than legacy voice) now making up around 84% of the business.11 Within that data business, management splits the world into "core connectivity" — the traditional, network-centric services — and the "digital portfolio," the higher-value software and platform layer. And the digital portfolio has been growing far faster: it expanded from about ₹7,032 crore in FY2024 to roughly ₹9,103 crore in FY2025, a jump of nearly 29%, even as old-fashioned voice revenue kept shrinking.11 The company now describes its data business as split roughly 53% core connectivity, 47% digital platform — meaning the high-value, "sell the intelligence" half of the business has nearly caught up with the "sell the pipe" half it was supposed to replace.11

That inflection — the moment the new, fast-growing, higher-margin business becomes large enough to actually move the whole company — is precisely what a long-term investor in a transformation story is waiting for. For years, the frustration with companies undergoing a "pivot" is that the exciting new business is too small to matter; it grows 40% a year but off a base so tiny that the lumbering legacy business still dictates the overall result. Tata appears to have crossed the threshold where that is no longer true. When the digital half is growing near 30% and is approaching the size of the connectivity half, simple arithmetic begins to work in the company's favor: the fast-growing piece increasingly sets the pace of the whole.

And much of the digital portfolio's recent acceleration came not from organic growth alone, but from two pointed, opportunistic acquisitions made when the market handed Tata a discount. Those deals deserve a close look, because they reveal how this company thinks about price — and how consistently the 2005 fire-sale instinct has persisted in its corporate DNA.

V. M&A Strategy: Benchmarking the Recent Bets

There is a through-line connecting the $130 million Tyco purchase in 2005 to the deals Tata Communications struck nearly two decades later: this is a company that buys when others are forced to sell. Twice in 2023, Tata closed acquisitions that looked, on the surface, like modest bolt-ons. Look closer and you see the same playbook — wait for a dislocation, then acquire a strategically valuable asset at a "managed infrastructure" price rather than a "hot tech startup" price.

The first was The Switch Enterprises, a New York–headquartered company that most people outside the broadcast industry have never heard of but whose work they have certainly watched. The Switch is, in effect, the live-video backbone for major sports and events: it operates the networks and production services that carry live feeds from stadiums and arenas to the broadcasters who put them on your screen, connecting hundreds of the world's largest content producers, distributors, and sporting venues.12 When a live match is captured by cameras at a venue and somehow appears, seconds later, on televisions across continents, a company like The Switch is doing the invisible work of getting that signal there cleanly and reliably. Tata announced the deal on December 22, 2022, and completed it on May 1, 2023, for $58.8 million in cash (about ₹486 crore).12

Consider what that price represents. Media-technology peers in this space frequently traded at well over one times revenue. Tata paid a multiple of roughly 0.72 times The Switch's revenue — buying a premium footprint across the United States and Europe, with deep relationships at the most valuable sporting venues in North America, at a discount to what comparable media-tech assets fetched.12 The genius is in the framing: live-sports transmission is, at its core, an exquisitely demanding networking and infrastructure problem — exactly Tata's home turf. So Tata could value The Switch as a managed-infrastructure asset (its specialty, where it knows precisely what the gear and the network are worth) rather than as a glamorous media business (where it might have been tempted to overpay). It bought a content-industry crown jewel using a network engineer's spreadsheet.

Why does The Switch fit so naturally? Because the broadcast industry is in the middle of its own great migration — away from dedicated satellite trucks and bespoke point-to-point links, and toward IP-based, fiber-delivered video that can be produced remotely and distributed globally over general-purpose networks. A producer no longer needs a satellite uplink truck parked outside every stadium; the feed can travel over high-capacity fiber to a control room continents away. That migration plays directly to the strength of the company that owns the world's largest private fiber network. The Switch gave Tata the specialized production and transmission expertise — the people who know how broadcasters actually work, the relationships with leagues and networks — to sell its raw connectivity advantage into one of the most demanding, highest-value verticals there is. The cable was already there; The Switch supplied the know-how to monetize it at media-grade prices rather than commodity-bandwidth prices.

The second 2023 deal was larger and, strategically, even more important. Kaleyra was a global CPaaS company — and here a plain-language detour is warranted, because "CPaaS" is one of those acronyms that hides a genuinely large idea. CPaaS stands for Communications Platform as a Service. The simplest way to understand it: every time your bank texts you a login code, your food-delivery app messages you that the driver is two minutes away, or an airline emails your boarding pass automatically, a business is sending a programmable message to a customer. CPaaS companies provide the software "plumbing" — the application programming interfaces, or APIs — that let any business send those texts, voice calls, emails, and app notifications at massive scale without building telecom infrastructure themselves. It is the picks-and-shovels layer of the entire customer-communication economy. The category's poster child is トゥイリオ Twilio, the American firm whose stock once traded at a euphoric 20 times revenue at its pandemic-era peak.

Tata announced the Kaleyra acquisition on June 28, 2023, and completed it on October 5, 2023, in an all-cash transaction valued at roughly $100 million plus the assumption of Kaleyra's outstanding debt.13 Now run the benchmarking exercise. Kaleyra was acquired at well under one times its sales. Against Twilio's frothy peak of around 20 times revenue — or even the more sober 2-to-3 times that the sector commanded after the bubble deflated — Tata was buying a real, revenue-generating CPaaS engine for a fraction of what the category had recently been worth.

Did they overpay? The honest answer is the opposite: they exploited a market that had fallen out of love with unprofitable communications-software companies to buy one cheaply. The CPaaS sector had been a darling of the zero-interest-rate era, when investors paid lavishly for revenue growth and ignored the fact that much of CPaaS revenue is low-margin "pass-through" — the cost of the underlying telecom carriage that the platform simply marks up. When rates rose and the market demanded profits instead of growth-at-any-cost, CPaaS valuations cratered, and a once-public company like Kaleyra found itself worth a fraction of its former self. Tata, with its contrarian's eye and its balance sheet, was waiting.

And here is the deeper strategic point that makes Tata a more natural owner of a CPaaS business than almost anyone: the very thing that crushes a standalone CPaaS company's margins — the cost of the underlying network carriage — is something Tata already owns. A pure-play CPaaS firm has to buy connectivity from carriers like Tata and resell it at a thin markup. Tata, by contrast, can run the messages over its own pipes, capturing both the software margin and the carriage margin in a single integrated stack. Kaleyra brought a programmable voice and messaging engine and a large book of enterprise customers, instantly vaulting the company into direct competition with global CPaaS players like スウェーデン Sinch and アメリカの Vonage. (The company's deal materials touted a customer base in the four figures; the precise count is best treated as approximate, since it was not stated in the closing press release.13) For a connectivity company that already moved a huge share of the world's traffic, owning the software layer that businesses use to send messages over that traffic was vertical integration of the most natural kind. Tata owned the road and the toll booth; with Kaleyra it bought the trucking company — and could now charge for the truck, the cargo, and the road all at once.

Two deals, two dislocations exploited, both folded into the digital portfolio. The question for an investor is what these acquisitions actually became once inside the company — and that requires opening up the hood on the businesses most outsiders never see.

VI. The Hidden Businesses and Growth Engines

Ask a casual observer what Tata Communications does and you will hear "undersea cables." That answer is a decade out of date. The most interesting parts of the company today are four businesses that barely existed in the VSNL era, each riding a structural wave, each woven into the same underlying fabric.

The first is Media and Entertainment Services — the home of the newly-acquired Switch. This is the business of moving live and broadcast video around the planet with broadcast-grade reliability, the kind of work that cannot tolerate a half-second of buffering when a hundred million people are watching a goal. Tata's network carries live feeds for marquee global events and broadcasters, and the segment has become one of the fastest-growing in the digital portfolio, generating roughly ₹1,285 crore of revenue in FY2025 and, in recent quarters, posting year-on-year growth as high as around 30%.1114 The strategic logic is that live sport and event broadcasting is migrating from satellite to fiber-based, IP-delivered workflows — and Tata happens to own the world's largest privately-held fiber network to deliver it on.

The second is the interaction layer — CPaaS and the broader "customer interaction" suite, which is where Kaleyra now lives alongside Tata's home-grown DIGO platform.15 The strategic arc here is a march away from plain SMS toward "omnichannel" communication: a single programmable platform through which a business can reach a customer by text, voice, email, chat, social message, or video, choosing the right channel automatically. Imagine a bank that wants to alert you to a suspicious transaction. The crude version sends a text. The sophisticated version knows you prefer the app, falls back to WhatsApp if you don't respond, escalates to a voice call if the alert is urgent, and logs the entire conversation so a human agent has full context if you call back — all orchestrated by software, at the scale of millions of customers. That orchestration is the interaction fabric, and it is exactly the kind of thing a business builds into its core systems and then never wants to rip out.

This matters for one unglamorous but decisive reason — margins, and the trajectory of margins. Moving a raw international phone minute is a low-margin commodity whose price falls every year. Helping an enterprise orchestrate millions of contextual customer interactions through software is a high-margin, sticky, recurring business whose value rises as you add intelligence — AI-driven routing, sentiment analysis, automated chatbots. This is why the company has begun branding its next-generation interaction stack around artificial intelligence: the more the platform decides what to say and when, rather than just carrying the message, the further it climbs from commodity carriage toward genuine software economics. The interaction fabric is, in management's framing, the high-margin future — and it is the part of the portfolio most directly leveraged to the broader enterprise-AI wave.

The third engine is edge computing, embodied in a platform called CloudLyte, which Tata launched on May 7, 2024.16 Here, another plain-language explanation earns its keep. For years the trend was to centralize computing in giant, far-away data centers — "the cloud." Concentrating computing power in a few massive facilities is wonderfully efficient, but it has one unavoidable flaw: distance equals delay. Light travels fast, but it does not travel instantly, and a round trip to a data center hundreds or thousands of kilometers away introduces latency measured in tens of milliseconds. For watching a movie, that is invisible. For a growing class of applications — a factory's machine-vision system inspecting a thousand parts a minute, a retailer's real-time inventory cameras, a self-driving system that cannot wait for a round trip to a distant server, an AI model doing live inference on a video feed — those milliseconds are the difference between working and not working. Such applications need the computing to happen physically near where the data is generated. That is "edge computing": pushing processing power out to the edges of the network, closer to the user and the machine.

CloudLyte is Tata's "solution-in-a-box" for this — bundling the platform, the infrastructure, the network, the managed services, and even the use case into one integrated offering rather than asking the customer to assemble the pieces.16 And note the structural advantage, which is the same theme echoing through every one of these businesses: a company that already owns a global network with points of presence in cities and landing stations all over the world is uniquely positioned to put computing at the edge, because it already has the edges. The hardest part of edge computing — having physical real estate and network presence close to where customers operate — is precisely the thing Tata accumulated over two decades of buying and building network. The cable network that looked like a 20th-century asset turns out to be the ideal launchpad for a 21st-century one. This is the deepest pattern in the whole company: assets acquired for one era keep finding second and third lives in the next.

The fourth engine is managed security, increasingly delivered through an architecture the industry calls SASE — Secure Access Service Edge (pronounced "sassy").17 The plain-language version is worth getting right because it is one of the most important shifts in enterprise IT. For decades, corporate security worked like a medieval castle: build a strong wall around the office network, put everything valuable inside, and check everyone at the gate. The trouble is that the castle emptied out. Applications moved to the cloud — outside the wall. Employees moved to their homes and coffee shops — outside the wall. Suddenly the thing you were protecting and the people accessing it were both outside the very perimeter you had spent millions fortifying. SASE is the answer: instead of a wall around a place, it wraps protection around each user and each connection, delivered from the cloud, so that security travels with you to wherever you actually are. It fuses networking and security into one service rather than two.

Why is Tata structurally advantaged here? Because SASE is, at its heart, a network service — it works best when the security checkpoints sit inside the network itself, close to the user, rather than as a bolt-on appliance. A company that already operates a global network with points of presence everywhere can deliver "network-plus-security" as a single, integrated, in-network service in a way that a pure security-software vendor cannot. Enterprises, meanwhile, are exhausted by the alternative: stitching together a dozen separate security point-solutions, each with its own console, contract, and blind spots. There is a powerful consolidation pull toward buying connectivity and security together from one provider who already runs your network. That is precisely Tata's pitch, and the managed-security business has been growing at double-digit rates as a result — riding both the secular explosion in cyber-threats and the structural shift toward converged, cloud-delivered protection.

What unites all four — media, interaction, edge, and security — is that none of them are "pipes." They are platforms and services that sit on top of the pipe, command higher margins, and embed themselves into a customer's operations in ways that a raw bandwidth contract never could. Which brings us to the deeper question every long-term investor must ask of an infrastructure company: how defensible is all of this, really? Before answering it, it is worth clearing away three persistent myths about Tata Communications — because the consensus story is wrong in instructive ways.

VII. Myth vs Reality

Myth one: "Tata Communications is just the old VSNL — an Indian telco with some cables." This is perhaps the most common misconception, and it is roughly a decade stale. The legacy voice business that defined VSNL has shrunk to a small and shrinking sliver of revenue, while the company has become a global enterprise-technology business whose largest growth engines — media transport, cloud networking, customer-interaction software, security — barely existed in the VSNL era. Reality: this is an Indian-headquartered global infrastructure-and-software company, not an Indian telco. The "telco" mental model leads investors to the wrong comparables (domestic mobile operators) and the wrong worries (subscriber churn, spectrum auctions) entirely.

Myth two: "Owning cables is a low-growth, commoditized business — a utility at best." Half true, and the half that's false is where the value is. Raw bandwidth is commoditizing, and if Tata only sold that, the skeptics would be right. But the company has spent years deliberately migrating its revenue mix toward services that are neither low-growth nor commoditized — the digital portfolio's near-30% growth rate is not a utility's growth rate. Reality: the physical network is the moat, not the product. The product is increasingly the intelligence sold on top of an irreplaceable moat, which is a fundamentally different — and more attractive — economic proposition than "owning a utility."

Myth three: "The hyperscalers will inevitably crush them." The most sophisticated bear argument, and the one that deserves the most respect — but it overstates the inevitability. Yes, Amazon, Microsoft, and Google are building their own subsea cables. But they build them primarily to connect their own data centers to each other, not to offer neutral, carrier-grade global connectivity-plus-security-plus-media-transport to thousands of enterprises across competing clouds. In fact, Tata's neutrality is an asset precisely because enterprises increasingly want to run across multiple clouds and do not want their network controlled by one cloud vendor who is also trying to sell them everything else. Reality: the hyperscaler relationship is genuinely double-edged — a real long-term risk and a real near-term revenue source — but the "inevitable crushing" thesis ignores the structural value of being the Switzerland between the warring cloud empires.

With the myths cleared, the real question of defensibility comes into sharp relief.

VIII. Strategy Analysis: Powers and Forces

The most useful way to interrogate Tata Communications' durability is to run it through two complementary frameworks — Hamilton Helmer's "7 Powers," which asks what specifically protects the profits, and Michael Porter's "Five Forces," which asks how attractive the industry structure is. They tell a coherent and, in places, genuinely formidable story.

Start with Helmer's most relevant power for this business: the Cornered Resource. A cornered resource is preferential access to a coveted asset that others simply cannot obtain. Tata's Tier-1 subsea cable ring is close to a textbook example. The crucial point is not merely that the network is expensive — it is that it may be effectively unbuildable today at any price. Laying new subsea cable now means navigating a thicket of marine-environmental regulation, securing landing-station permits across dozens of sovereign jurisdictions, and dealing with geopolitical sensitivities around critical infrastructure that barely existed when Tata acquired its core assets for pennies in the post-dot-com fire sale. A new entrant cannot simply spend its way to a wholly-owned global ring; in many waters, the permission to lay the cable is harder to get than the capital to build it. Tata acquired its moat at the one historical moment the moat was on clearance, and the drawbridge has since risen behind it.

The second decisive power is Switching Costs. This is the quiet force that makes the platform strategy so valuable. When an enterprise runs its connectivity through Tata's network, that is replaceable — annoying to switch, but doable. But once that same enterprise has woven its multi-cloud routing through Tata's IZO fabric, layered its SASE security on top, and wired its customer communications through Tata's interaction platform, leaving becomes a multi-year migration nightmare touching every part of the IT estate. Each additional platform a customer adopts deepens the entanglement and raises the cost of ever leaving. This is the entire economic rationale for the "sell platforms, not pipes" pivot: pipes have low switching costs, platforms have high ones, and high switching costs are what turn a commodity vendor into an annuity. A third Helmer power, Scale Economies, reinforces both — the fixed cost of a global network is enormous, but the marginal cost of carrying one more customer's traffic is tiny, so the largest network can profitably serve customers at prices a sub-scale rival cannot match.

Now Porter's Five Forces. The Threat of New Entrants is about as close to zero as exists in any major industry, for exactly the cornered-resource reasons above: the capital and, more importantly, the regulatory and geopolitical permissions required to build a competing global IP backbone are prohibitive. Rivalry among existing players is real but rational — this is an oligopoly of a handful of Tier-1 carriers, not a fragmented price war. The most interesting force is the Bargaining Power of Buyers, and here lies the central tension of the whole investment case. For commodity "dumb pipe" bandwidth, buyer power is high — customers can shop the price and squeeze margins mercilessly. But for the specialized platforms — broadcast-grade media transport, integrated network-plus-security, embedded interaction software — buyer power is low, because those services are differentiated and entangled. The entire strategic project of the last several years can be read as a deliberate migration of revenue from the high-buyer-power left side of the ledger to the low-buyer-power right side.

The genuine threat sits in Porter's Threat of Substitutes and the Power of Suppliers/Complements — specifically, the hyperscalers. アマゾン Amazon's AWS, マイクロソフト Microsoft's Azure, and グーグル Google Cloud have been building their own private subsea cables and their own networking services, and they are simultaneously Tata's largest partners and its most dangerous potential competitors. A cloud giant that decides to offer global networking directly to enterprises could disintermediate parts of Tata's business. This frenemy dynamic — depending on the very players who could one day eat your lunch — is the single most important structural risk to monitor.

It helps to locate Tata against its actual competitive set, because "the internet backbone" is not a monopoly — it is a small oligopoly of global carriers, each fighting on a different front. On raw global connectivity, Tata competes with the likes of America's Lumen Technologies (the former CenturyLink/Level 3, now wrestling with a heavy debt load) and the international arms of European incumbents such as フランスの Orange and Germany's Deutsche Telekom, plus Asia-Pacific players like オーストラリアの Telstra. Tata's edge against these is its uniquely complete, wholly-owned global ring and its disproportionate exposure to the high-growth India–to–world corridor. In CPaaS and interaction, the rivals are different again — Sweden's Sinch, America's Twilio and Vonage, and a thicket of regional messaging aggregators. There, Tata is a challenger rather than the leader, betting that owning the underlying network lets it undercut software-only competitors on the cost of carriage. The strategic picture, then, is of a company that is dominant in the layer it has owned for two decades (connectivity) and an ambitious insurgent in the layers it is climbing into (interaction, security, media, edge). That combination — fortress below, insurgency above — sets up the bull-and-bear debate squarely.

IX. Bear vs. Bull, and the Playbook

Lay the cases side by side, because both are real.

The bear case begins with the melting ice cube that never fully melts away on the income statement: legacy voice. International voice revenue has been in structural decline for years — from about ₹1,699 crore in FY2024 to ₹1,633 crore in FY2025 — and while it is now a small slice of the whole, its erosion is a persistent drag that the growth businesses must continually out-run.11 Second, integration risk: Tata absorbed both Kaleyra and The Switch in quick succession, and Kaleyra in particular came with debt and the perennial challenge of folding an entrepreneurial software company into a large infrastructure incumbent without losing its talent or its customers. Third, and most fundamentally, margins have actually been under pressure rather than expanding — the company's overall EBITDA margin slipped to around 20% in FY2025 from roughly 21% the year before, even as revenue grew.11 A bear reads that as evidence that the high-margin digital future is being diluted by integration costs and competitive pricing faster than it is arriving. And looming over all of it is the hyperscaler threat: if AWS and Azure move decisively into enterprise networking, Tata's most defensible-seeming franchise could face a competitor with effectively infinite capital.

The bull case turns each of those on its head. The voice decline is precisely why the digital portfolio's near-29% growth matters so much: the future is not just arriving, it is arriving fast enough that the mix is shifting visibly each year, with the digital platform now nearly half the data business.11 The margin "pressure," on this reading, is the temporary cost of integration and investment, not a structural ceiling — and management has publicly committed to a target EBITDA margin band of 23–25% and a return on capital employed above 25% as those investments mature and the higher-margin platforms scale.18 The bull also points to the targets management has set for itself: the company has guided toward a data-revenue base of roughly ₹28,000 crore in the coming years, a substantial step up from the FY2025 level of about ₹19,513 crore, signaling confidence that the growth engines can keep compounding.111 The bull sees a company that has done the hard, unglamorous work of buying an irreplaceable physical moat at a generational discount and is now methodically layering software economics on top of it. If the margin target is hit while the digital portfolio keeps compounding, the result is a business with both a fortress balance-sheet asset and a growing annuity stream — the rare combination of a deep moat and a real growth rate.

A word on second-layer diligence, the things that do not show up in the headline growth rate but can quietly make or break the thesis. First, the capital-intensity question: a subsea network demands relentless maintenance and periodic upgrade capex, so investors should watch that the push for margin expansion does not come at the cost of under-investing in the physical asset that is the moat — starving the network to flatter near-term EBITDA would be a classic value-destroying mistake. Second, integration and goodwill: two acquisitions in quick succession create execution risk and goodwill on the balance sheet that must be earned out through performance; a stumble in folding Kaleyra or The Switch in cleanly would show up first in margins and only later in growth. Third, the ownership backdrop is unusually clean and stable — with the Government of India having fully exited and the Tata group holding a controlling stake of roughly 58–59% through Panatone Finvest and Tata Sons directly, this is a tightly-held company with a patient, strategic anchor shareholder rather than a free float at the mercy of activist agitation.21 That stability cuts both ways: it lowers the risk of disruptive ownership changes, but it also means minority shareholders are along for whatever ride the Tata group chooses to take.

The playbook lesson here — the thing that travels beyond this one company — is a clean one: own the infrastructure, then sell the intelligence on top of it. Tata's entire history rhymes with this single idea. Buy the cable when it is cheap and the world thinks physical assets are foolish. Hold it through the commoditization of whatever first ran across it. Then, when the asset is irreplaceable and the moat is dug, climb the value chain and sell the high-margin services that can only exist because you own the thing underneath. It is the opposite of the asset-light gospel, and it has compounded quietly for two decades.

For an investor trying to track whether the thesis is actually working, the noise can be cut down to a very small number of signals. First and most important: the digital portfolio's revenue and its growth rate — this is the single number that tells you whether the "sell platforms, not pipes" pivot is real or rhetorical; as long as it compounds at a healthy clip and keeps gaining share of the total, the transformation is on track. Second: the consolidated EBITDA margin, and its progress toward the stated 23–25% band — this is the litmus test for whether all that platform revenue is actually more profitable, or whether competition and integration are eating the gains. A reader who watches only those two lines — digital-portfolio growth and EBITDA margin trajectory — will understand more about this company's trajectory than someone tracking a dozen lesser metrics. (A third worth a glance is return on capital employed, the ultimate scorecard for a capital-intensive business, against management's >25% ambition.)

There is one more thread to pull, because every great infrastructure story is ultimately also a story about the people steering it — and this one is, as of 2026, in the middle of a changing of the guard.

X. Epilogue: The 2026 Transition

Every long arc of corporate transformation eventually meets the question of succession, and Tata Communications met it on a precise date. A. S. Lakshminarayanan — the TCS lifer who reframed a cable company as a CommTech company — retired as Managing Director and CEO at the close of business on April 13, 2026.19 He left behind a company materially different from the one he inherited in 2019: a business where the digital portfolio had grown from a promising sideline to nearly half of the data revenue, where two opportunistic acquisitions had been folded in, and where the language of platforms had genuinely begun to displace the language of pipes.

The handoff carries a delightful, and genuinely confusing, twist of nomenclature. Lakshmi's successor is also a Lakshminarayanan — गणपति लक्ष्मीनारायणन Ganapathi S. Lakshminarayanan, known as "Ganesh," and entirely unrelated to the outgoing chief despite the shared surname.20 Ganesh was named MD and CEO designate effective January 21, 2026, and took the reins as MD and CEO on May 20, 2026, for a five-year term running to May 2031.20 His background is its own statement of intent: more than three decades spanning enterprise technology and telecom leadership, including running ServiceNow's India business, leading Airtel's enterprise arm, and advisory roles across the technology and venture ecosystem.20 Where the first Lakshmi brought a global IT-services sensibility, the second brings deep enterprise-software and Indian-market operating experience — a signal, perhaps, that the next chapter doubles down on selling intelligence to enterprises rather than carrying their bits.

The continuity in leadership philosophy matters more than the change in personnel. Both men were chosen for the same reason VSNL was bought and Tyco's cables were scooped up at a discount: a conviction that the prize goes to whoever owns the foundational layer and is patient and disciplined enough to build value on top of it over years, not quarters. Succession risk is real in any company — a new chief executive can change strategy, culture, or capital allocation — but the Tata group's habit of grooming insiders steeped in its long-termist culture, combined with a controlling shareholder that does not flinch at multi-year transformations, lowers the odds of a destabilizing lurch. The thing to watch is whether Ganesh continues the margin-expansion and digital-mix discipline, or whether the temptation to chase growth at the expense of returns reasserts itself.

Step back, and the largest frame comes into view. Tata Communications is the digital nervous system of a conglomerate founded in 1868 — a 19th-century industrial house that built India's first steel mills and luxury hotels, navigating its way to the literal center of the 21st-century internet. The same group that once symbolized old-economy Indian industry came to own the only wholly-owned fiber ring around the planet and to carry a third of the world's internet routes, all while the Government of India, the company's former parent, fully exited its remaining stake in 2021.21 From a state monopoly that took an hour to connect a phone call to Chicago, to the invisible fabric beneath live global sport, programmable enterprise messaging, and the routing of the open internet — the throughline was never the technology of any given decade. It was a single, patient conviction: own the thing everyone else has to rent, and then, slowly, sell them everything that runs on top of it.

References

-

Corporate Presentation FY26 (subsea/terrestrial fiber, segment revenues, margins, targets) — Tata Communications, 2025-08 ↩↩

-

Tata Communications Completes World's First Wholly-Owned Cable Network Ring Around the World — Submarine Telecoms Forum, 2012 ↩

-

Tata Communications business profile (carries ~30% of world's internet routes; largest wholly-owned subsea network) — Tata Group ↩

-

Govt to sell 16.12% stake in Tata Comm through OFS, rest to Tata Sons arm (history of 2002 disinvestment to Panatone) — Business Standard, 2021-03-12 ↩

-

VSNL Acquires the Tyco Global Network (≈60,000 km, $130 million) — Submarine Networks ↩↩

-

VSNL Acquires Teleglobe (enterprise value $239M; $178M equity at $4.50/share; ~$61M net debt) — Submarine Networks ↩

-

VSNL Global Ambitions: Teleglobe acquisition and rebranding to Tata Communications — Tele.net.in ↩

-

Leading with Rigour: Amur Lakshminarayanan (career at TCS UK/Europe/US and TCS Japan JV; appointed MD & CEO effective 26 November 2019) — Tata Group Newsroom ↩↩

-

A. S. Lakshminarayanan director remuneration history (FY25 total ₹19.2 crore, +12.6%) — Trendlyne ↩

-

Integrated Annual Report FY2024-25 (CEO remuneration structure: fixed plus PLI / RSU variable components) — Tata Communications ↩

-

Corporate Presentation FY26 (FY24/FY25 total, data, voice, core connectivity and digital portfolio revenues; 53/47 split; EBITDA margins) — Tata Communications, 2025-08 ↩↩↩↩↩↩↩↩

-

Tata Communications Completes Acquisition of The Switch Enterprises ($58.8M; announced 22 Dec 2022, completed 1 May 2023; live video production/transmission) — PR Newswire, 2023-05-01 ↩↩↩

-

Tata Communications Completes Acquisition of Kaleyra, a Leading Global CPaaS Platform Player (~$100M cash plus debt; completed 5 October 2023) — PR Newswire, 2023-10-05 ↩↩

-

Tata Communications Q2 FY26 earnings call summary (next-gen connectivity and media ~30% YoY growth) — Yahoo Finance ↩

-

Tata Communications launches DIGO, integrated platform for converged and contextual conversations — Tata Communications ↩

-

Tata Communications CloudLyte Opens New Vistas to Edge Computing (launched 7 May 2024) — PR Newswire, 2024-05-07 ↩↩

-

Tata Communications SASE / IZO SD-WAN secure access service — Tata Communications ↩

-

Tata Communications management sets EBITDA margin target of 23–25%, expects ROCE recovery — ScanX ↩

-

Tata Communications CEO A. S. Lakshminarayanan retires; Ganesh Lakshminarayanan set to take over (retirement 13 April 2026) — Storyboard18 ↩

-

Tata Communications appoints Ganapathi S. Lakshminarayanan as MD & CEO (designate 21 Jan 2026; MD & CEO from 20 May 2026; term to 19 May 2031) — Adgully ↩↩↩

-

Government of India to divest residual stake in Tata Communications via OFS and transfer to Tata Sons arm (full exit, 2021) — Business Standard, 2021-03-12 ↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube