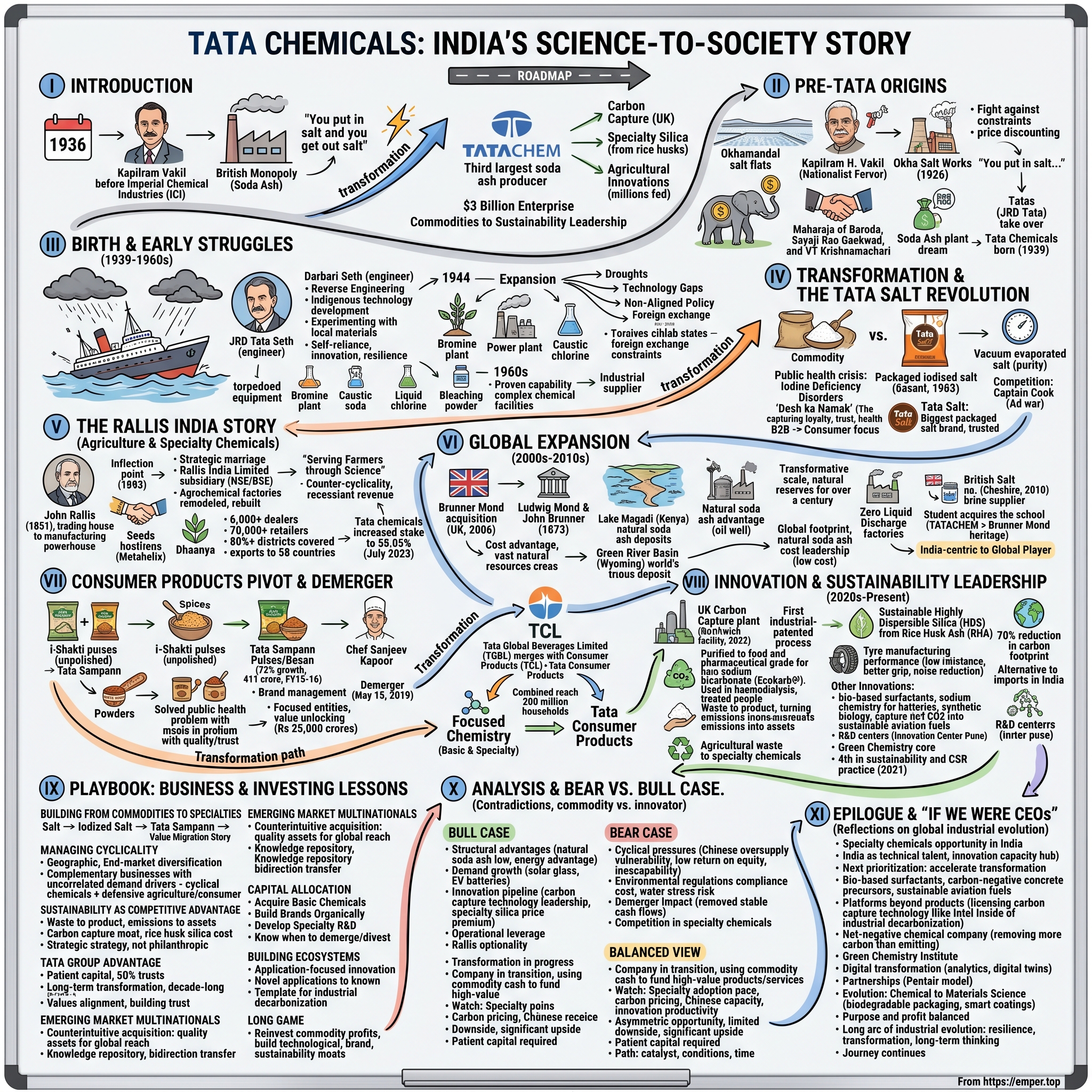

Tata Chemicals: India's Science-to-Society Story

I. Introduction & Episode Roadmap

Picture this: It's 1936, and a young Indian chemical engineer named Kapilram Vakil stands before the towering executives of Imperial Chemical Industries, the British chemical giant that monopolizes soda ash production in the subcontinent. He's asking for technology transfer, for help building India's own chemical industry. Their response? "You put in salt and you get out salt." The dismissive taunt would echo through history—not as an insult, but as the spark that ignited one of the most remarkable industrial transformations in emerging market history.

Today, that mocked venture has become Tata Chemicals Limited, the world's third-largest soda ash producer with operations spanning four continents. From its humble beginnings in the salt flats of Gujarat, the company has evolved into a $3 billion enterprise that captures carbon dioxide in the UK, produces specialty silica from rice husks in India, and feeds millions through its agricultural innovations. Listed on the National Stock Exchange under the symbol TATACHEM, it represents something far more profound than just another chemical company—it's a case study in how emerging market companies can leap from commodities to cutting-edge sustainability leadership.

The fundamental question driving this narrative isn't just how a salt works in Mithapur became a global chemical powerhouse. It's about understanding how a company born in colonial subjugation transformed itself into a pioneer of green chemistry, how it navigated the treacherous waters of commodity cyclicality while building consumer brands, and why its story matters for investors looking at the next wave of industrial transformation. This is a tale of nation-building through science, of patient capital meeting urgent social needs, and of how sustainability—once considered a cost center—has become the ultimate competitive moat in the chemical industry.

What makes Tata Chemicals particularly fascinating for students of business history is its refusal to follow conventional playbooks. While Western chemical giants consolidated and focused on scale, Tata Chemicals diversified from basic chemicals into nutrition. While others outsourced to Asia, it acquired century-old British and American chemical companies. And while the industry grappled with its environmental legacy, Tata Chemicals built the UK's first industrial-scale carbon capture plant that turns emissions into food-grade sodium bicarbonate.

This journey from salt to science, from Gujarat to global, offers profound lessons about industrial evolution in the 21st century. It challenges our assumptions about emerging market multinationals, about the relationship between profitability and purpose, and about what it truly means to build enduring value in commodity businesses. As we trace this nearly century-long arc, we'll discover how a company that started with borrowed technology and torpedoed equipment became a teacher to the world in sustainable chemistry.

II. The Pre-Tata Origins: Kapilram Vakil's Vision (1926–1939)

The story begins not in a Bombay boardroom but in the scorching salt flats of Okhamandal, where the Arabian Sea meets the Gujarat coast. In 1926, Kapilram H. Vakil—grandson of the late Indian justice Nanabhai Haridas—arrived with an audacious dream. While others saw barren land suitable only for traditional salt farming, Vakil envisioned an industrial complex that would challenge the British chemical monopoly. His Okha Salt Works would become the foundation stone of India's chemical independence, though he couldn't have imagined the century-long impact of his vision. Vakil wasn't just any engineer—he was educated in England and returned to India with both technical expertise and a burning nationalist fervor. In an era when Indian industrialists were systematically excluded from modern technology, he represented a new breed of technocrats who believed that scientific advancement and political independence were inseparable. As the pioneer of the salt industry in Saurashtra, he eventually founded the Okha Salt Works in 1926, transforming what colonial administrators dismissed as wasteland into the foundation of India's chemical sovereignty.

The early years tested every ounce of Vakil's determination. He struggled against the constraints placed by the British and had to deal with cartels from Aden and fierce price discounting designed to kill Indian manufacturing. The British colonial government's policy actively favored imports from the Empire, creating an ecosystem where Indian entrepreneurs faced not just market competition but institutional sabotage. Yet Vakil persisted, driven by a vision that transcended profit margins—he saw chemical production as a pathway to national self-reliance.

The turning point came when Vakil approached the Maharaja of Baroda, Sayaji Rao Gaekwad, who was always keen to develop his princely state and gave his assent. The Maharaja wasn't just offering capital; he was making a political statement. In the complex chess game of princely states navigating between British suzerainty and nascent nationalism, supporting indigenous industry was both economically strategic and symbolically powerful. VT Krishnamachari, the Diwan of Baroda, laid the foundation stone, lending administrative gravitas to what many dismissed as a quixotic venture.

By the mid-1930s, Vakil had proven the skeptics wrong—his salt works were operational and profitable. But salt was just the beginning. The real prize was soda ash, the fundamental building block of modern industry, essential for glass, textiles, paper, and dozens of other products. Without domestic soda ash production, India would remain perpetually dependent on imports, vulnerable to supply disruptions and price manipulation. A decade after establishing the salt works, Vakil wanted to expand and set up a soda ash plant, but did not have the financial resources required.

This is where the story takes its most fateful turn. Imperial Chemical Industries (ICI), located in the Sindh province of what is now Pakistan, was the only company in the subcontinent with the necessary know-how and technology. When approached, they taunted Vakil, saying: "You put in salt and you get out salt". The dismissal was more than technical skepticism—it was colonial condescension distilled to its essence. To the British chemical establishment, the idea that Indians could master complex chemical processes was not just unlikely but laughable.

The insult would prove to be ICI's strategic blunder and India's industrial catalyst. Vakil approached the Tatas, who agreed to take over the company, and Tata Chemicals was born in 1939. For the Tata Group, already established in steel and power generation, chemicals represented the next frontier of industrial development. For Vakil, it meant his vision would be backed by patient capital and technical expertise that could match any British enterprise.

Vakil stayed on as director, ensuring continuity between the entrepreneurial passion that birthed the venture and the institutional capability that would scale it. But more importantly, the British taunt had awakened something profound in the Indian industrial psyche. Darbari Seth, a young chemical engineer who had recently joined Tata Chemicals, was stung by their arrogance and resolved to build the best soda ash plant in India. This wasn't just about building a factory—it was about proving that Indians could master any technology, compete with any rival, and build industries that would outlast empires.

The transformation from Okha Salt Works to Tata Chemicals represented more than a change in ownership. It marked the moment when individual entrepreneurship merged with institutional ambition, when a regional venture became a national mission, and when salt—that most basic of commodities—became the foundation for one of the most sophisticated chemical enterprises in the developing world. The stage was set for an industrial saga that would span continents and centuries.

III. Birth of Tata Chemicals & Early Struggles (1939–1960s)

Tata Chemicals Limited was incorporated on January 23, 1939, in what would prove to be one of history's most turbulent periods. War clouds gathered over Europe, independence movements convulsed across Asia, and the global economy teetered between depression and militarization. Into this chaos, JRD Tata—then just 34 years old and five years into his tenure as chairman of Tata Sons—made a bet that would test the limits of industrial endurance. The location itself told a story of defiance. The township Mithapur, derives its name from "Mitha" which means salt in Gujarati language, but this linguistic sweetness masked harsh realities. The site sat between Okha and Dwarka on the western tip of the Saurashtra Peninsula—remote, arid, with temperatures that could crack concrete and monsoons that either never came or arrived with devastating fury. Where others saw impossibility, JRD saw opportunity: proximity to the sea for salt production, isolation that would force self-reliance, and distance from British industrial centers that might foster indigenous innovation.

That it was wartime compounded the problem, as the ship carrying the material to set up the plant was torpedoed and sunk. This wasn't just a setback—it was nearly catastrophic. The specialized equipment for soda ash production, ordered from Europe before the war intensified, now lay at the bottom of the ocean. In an era before global supply chains and just-in-time manufacturing, losing your primary equipment shipment meant years of delay. But it also meant something else: Tata Chemicals would have to innovate, improvise, and develop its own technology under the most challenging circumstances imaginable.

Under JRD's Chairmanship, the Tata group took over Okha Salt Works, developing its own technology to manufacture soda ash — an especially challenging feat during WW II. The young Darbari Seth, still burning from ICI's insult, became the driving force behind this indigenous technology development. Working with limited resources, cut off from international expertise by the war, Seth and his team reverse-engineered processes, experimented with local materials, and essentially rebuilt chemical engineering from first principles. It was industrial archaeology in reverse—instead of discovering how things were made, they were inventing how things could be made.

The challenges cascaded relentlessly. The war disrupted not just equipment delivery but also raw material supplies, skilled labor availability, and even basic construction materials. The British colonial government, fighting for its survival against the Axis powers, had little interest in supporting Indian industrial development. Coal was rationed, steel was requisitioned for the war effort, and technical expertise was conscripted for military production. Yet somehow, against these impossible odds, the second soda ash plant built in India by Kapilram Vakil started operating in the year 1944.

JRD Tata would later reflect on this period with characteristic understatement: "Of all the companies with which I have been concerned, none has had to overcome so many difficulties compounded with bad luck as has been the lot of Tata Chemicals." But what he called bad luck was actually the crucible that forged the company's character. Every obstacle overcome—from the torpedoed equipment to the technology embargo—built institutional knowledge that money couldn't buy. The company wasn't just learning to produce chemicals; it was learning to be self-reliant, innovative, and resilient.

The immediate post-independence years brought new challenges wrapped in opportunity. India's partition in 1947 suddenly placed ICI's Sindh operations in Pakistan, leaving India with even greater need for domestic chemical production. The new government of independent India, led by Nehru with his vision of scientific socialism, saw companies like Tata Chemicals as pillars of the planned economy. But government support came with expectations—the company would need to serve national interests, not just shareholder returns.

Soda ash is as fundamental to chemical industries as steel is to the engineering sector, and newly independent India desperately needed both. The company expanded aggressively, setting up auxiliary units: between 1942 and 1949, it commissioned a bromine plant, an auxiliary power plant, and began producing caustic soda, liquid chlorine, and bleaching powder. Each expansion was a calculated risk in a capital-starved economy, but also a statement of faith in India's industrial future.

The 1950s tested this faith severely. Droughts ravaged Gujarat, affecting salt production—the fundamental raw material for the entire operation. Technology gaps became apparent as global chemical production advanced rapidly while India, isolated by its non-aligned foreign policy and foreign exchange constraints, struggled to keep pace. Financial challenges mounted as the company needed continuous capital investment while generating modest returns. Many board members questioned whether chemicals was truly a viable business for India, whether the country should focus on its comparative advantages in textiles and agriculture rather than chase industrial dreams.

Yet JRD persisted with a patience that would define the Tata approach to building businesses. He understood that some investments measured their returns not in quarters but in generations. The struggles of the 1940s and 1950s weren't just about building a chemical plant; they were about building capabilities that would compound over decades. Every engineer trained, every process mastered, every problem solved added to an invisible asset base that no balance sheet could capture.

By the 1960s, Tata Chemicals had achieved something remarkable: it had proven that India could build and operate complex chemical facilities using primarily indigenous technology and talent. The plant that ICI said would only "put in salt and get out salt" was now producing a range of sophisticated chemical products. More importantly, it had created an ecosystem—suppliers who understood chemical industry needs, workers trained in process manufacturing, and managers who could navigate both technical and commercial complexity.

The foundation was set, but the company remained essentially an industrial supplier, selling to other businesses in a slow-growing economy. The next transformation would require not just technical capability but marketing imagination—the ability to see consumers where others saw only commodity buyers. That vision would arrive in the most unexpected form: table salt.

IV. Transformation & the Tata Salt Revolution (1970s–1990s)

The boardroom at Bombay House in 1982 witnessed an unusual debate. Senior executives of Tata Chemicals, men who had spent careers optimizing steam pressures and reaction yields, were discussing packaging designs and advertising jingles. The proposal on the table seemed almost absurd: take common salt—a commodity sold loose in gunny bags for centuries—package it in polyethylene pouches, add iodine, and sell it at a premium to Indian households. "We're a B2B chemical company," one director reportedly said, "not a consumer goods operation." But one executive understood something others missed. India faced a massive public health crisis: iodine deficiency disorders affected millions, causing goiter, mental retardation, and developmental problems particularly in children. The government had been trying to promote iodine supplementation for years with limited success. What if a commercial enterprise could solve a public health problem while building a profitable business? Tata Salt was launched in 1983 by Tata Chemicals as India's first packaged iodised salt brand, transforming both the company and the nation's health landscape.

The technical challenge was formidable. Its vacuum-evaporated salt was untouched by hands, thus upholding the highest standards of purity. This wasn't just marketing speak—the vacuum evaporation technology represented a quantum leap from traditional salt production methods. While competitors relied on solar evaporation in open pans, exposed to contamination and producing inconsistent grain sizes, Tata's process delivered pharmaceutical-grade purity with uniform iodine distribution. The plant at Mithapur, spread across 37,000 acres, could produce 450,000 tonnes of quality iodised salt annually.

In a market characterised by loose, unbranded salt of dubious quality, Tata Chemicals pioneered the concept of salt iodisation in India. The pricing strategy was audacious—Tata Salt came along with a premium that was two to three times over the unbranded competition. In a price-sensitive market where consumers haggled over every paisa, asking them to pay triple for something as basic as salt seemed like commercial suicide. Yet the company understood that they weren't selling salt; they were selling trust, health, and modernity.

The marketing genius lay not in the product but in the positioning. Namak ho Tata ka, Tata Namak — this jingle captured the audience's imagination in the early '80s. The concept of branded salt was non-existent back then. But the real masterstroke came with the evolution to "Desh ka Namak"—the nation's salt. In the Indian cultural context, "namak" carries profound emotional weight. The phrase "Maine aapka namak khaya hai" (I have eaten your salt) signifies loyalty, gratitude, and an unbreakable bond. By positioning their product as the nation's salt, Tata transformed a commodity purchase into an act of patriotism.

Our genesis was in partnering with the government to address the issue of micro-nutrient deficiency in the country. Tata Salt was the first iodised salt brand in India. Today, 92 per cent of the country's population is iodised and about 78 per cent adequately iodised (15ppm). We are extremely proud of the key role we have played in that journey. This wasn't just corporate social responsibility—it was building a business model where profit and purpose were inseparable.

The transformation rippled through the entire organization. Chemical engineers who had spent careers optimizing soda ash yields now studied consumer behavior. The distribution network, built for industrial customers, had to reach millions of retail outlets. Marketing budgets, virtually non-existent for a B2B operation, suddenly became critical. The company had to learn entirely new competencies while maintaining its core chemical operations.

Competition arrived swiftly and aggressively. In the late 1980s, DCW Ltd launched Captain Cook salt with a marketing blitz, positioning it as "free flowing, iodised salt" and pricing it 50% higher than Tata Salt to create a perception of superior quality. The advertising war that followed became legendary in Indian marketing circles. When Captain Cook's advertisements featuring the popular actress Kitty claimed superiority, Tata Salt responded with "Karamchand, Kitty don't be silly," directly challenging the competitor while emphasizing their own product's purity. The legal battles, creative one-upmanship, and market share wars that ensued would fill marketing textbooks for decades.

By the 1990s, The brand is now the biggest packaged salt brand in India, with a market share of 17%. But more importantly, Tata Salt had fundamentally changed how Indians thought about everyday products. It proved that Indian consumers would pay premiums for quality, that health messaging could drive purchasing decisions, and that emotional branding could transform commodities into beloved products.

Today, Tata Salt is the only brand from the house of Tata to consistently feature in the country's Top 10 most trusted brands, according to The Economic Times Brand Equity's 'Most Trusted Brands' survey. It not only garners more than 25 per cent market share in the country but is also four times bigger than its nearest competitor.

The success of Tata Salt did more than add a profitable product line—it transformed Tata Chemicals' corporate DNA. The company learned that its expertise in chemistry could extend beyond industrial applications to touch consumers directly. It discovered that solving social problems could create sustainable competitive advantages. Most importantly, it proved that an Indian company could build consumer brands that competed not on price but on quality and trust.

This consumer pivot would set the stage for the company's next major expansion. If salt could be branded and premiumized, what about other everyday products that Indians consumed? The lessons from Tata Salt—the importance of quality, the power of emotional branding, the value of solving real problems—would guide the company as it ventured into pulses, spices, and water purification. But first, it needed to strengthen another pillar of its business: agriculture.

V. The Rallis India Story: Agriculture & Specialty Chemicals

The year was 1851, and in the bustling trading rooms of Calcutta, a Scottish merchant named John Rallis was building what would become one of India's oldest continuously operating companies. Fast forward to 1993: Tata Chemicals' boardroom faced a strategic inflection point. India's agricultural sector, employing nearly 60% of the population, remained woefully underproductive. The Green Revolution had stalled, crop yields lagged global averages by 40-50%, and farmers struggled with pests, diseases, and soil degradation. The opportunity was massive, but so were the risks. Tata Chemicals has a publicly listed subsidiary called Rallis India. Rallis India is a subsidiary of Tata Chemicals, and is listed on both the National Stock Exchange and the Bombay Stock Exchange. The acquisition that would create this powerhouse wasn't just a financial transaction—it was a strategic marriage between chemical expertise and agricultural know-how spanning more than a century.

Fisons and Tatas become the chief shareholders of Rallis India, with Fisons taking charge of Rallis' management and the Tatas reserving the right to nominate the Chairman. The relationship between Rallis and the Tata Group had deep roots, going back to the 1960s when the British conglomerate Fisons partnered with Tatas to rescue the struggling company. Fertilisers and pesticides are carved out as full-fledged divisions. A strong credit discipline and astute management see Rallis India turn around its fortunes in the latter part of the 1970s. All divisions except pharmaceuticals are soon brimming with profits. The rehabilitation is now complete, and Rallis is set to leap into a growth phase.

The 1980s marked a turning point. The era of cotton trading comes to an end, and Rallis decides to bet big on its engineering, agrochemicals, and pharmaceutical business. It buys Indian Standard Metals and establishes three new manufacturing units, including a pharmaceutical facility in Ankleshwar, Gujarat, with the license for five new drugs, and two agrochemical units in Dera Bassi, Punjab, and Ankleshwar. This transformation from a trading house to a manufacturing powerhouse positioned Rallis perfectly for what would come next.

The 1990s restructuring was brutal but necessary. In a short span of four years from 1990-94, the Company shed all its engineering businesses, sold off its share in Boehringer Mannheim and shut down all its formulation factories in the Pharma division. Agrochemical factories were remodeled, razed to the ground and rebuilt to international standards. New plants were added and the Company's research center began developing 6 new compounds every year. This wasn't just corporate restructuring—it was industrial rebirth.

Pesticide maker Rallis India is now a subsidiary of Tata Chemicals. The latter acquired a further 4.09 per cent stake in Rallis, part of the Tata Group and one of the oldest major private sector companies in the country, for about Rs 89 crore to make it a subsidiary. Tata Chemicals has acquired 980,000 shares at Rs 908.51 a share, inclusive of premium of Rs 898.51 a share, through a preferential allotment yesterday. "With the said acquisition, the shareholding of the company in Rallis has increased from 45.97 per cent to 50.06 per cent and Rallis has become a subsidiary of the company," said Tata Chemicals in 2009, marking a watershed moment in Indian agribusiness.

The strategic rationale was compelling. Tata Chemicals, which generate over 40 per cent of its revenue from fertilisers such as urea, DAP and NPK, has annual sales of about Rs 12,200 crore and Rallis India has sales of over Rs 850 crore from crop protection products which includes pesticides, insecticides, seeds, micro nutrients and contract manufacturing of agrochemicals for multinationals. Rallis is the sole distributor for Tata Chemicals fertilisers in its main markets in the north and north-east regions. The synergies were obvious: Tata Chemicals had the manufacturing muscle and chemical expertise, while Rallis brought distribution reach and farmer relationships built over decades.

Rallis, a subsidiary of Tata Chemicals, has established a reputation of being a trusted solutions provider for agri-inputs, globally, with an accent on innovation, a thorough knowledge of farm science and a penetrative distribution network. The company has established a presence across the value chain, with a healthy pipeline of sustainable products and services. This wasn't just about selling chemicals to farmers—it was about transforming Indian agriculture through science.

The numbers tell a story of remarkable reach. The company's 6,000+ dealers and 70,000+ retailers reach a vast multitude of India's farmers covering more than 80% of India's districts and exports to over 58 countries. Consider the scale: India has over 600 districts, meaning Rallis touches nearly 500 of them. In a country where the last mile of distribution often determines success or failure, this network represents an irreplaceable asset.

Rallis' acquisition of Metahelix Life Sciences, a research-based company on seeds, in 2010-11, gives it a prominent position in the seeds market. This acquisition wasn't just about adding another product line—it was about controlling the entire agricultural value chain from seeds to harvest. The seeds business, marketed under the "Dhaanya" brand, gave Rallis entry into the highest-margin segment of agricultural inputs while deepening farmer relationships from the very start of the crop cycle.

The innovation engine has been relentless. Rallis has evolved its innovation strategy on 'Serving Farmers through Science'. Accordingly, it develops innovative solutions to enable farmers to improve their productivity. The company's research centers don't just adapt global molecules for Indian conditions; they develop entirely new formulations suited to local pest pressures, soil conditions, and cropping patterns.

What makes Rallis particularly valuable within the Tata Chemicals portfolio is its counter-cyclical nature to the basic chemicals business. When soda ash prices slump due to oversupply, agricultural demand often remains steady or grows, driven by population growth and food security needs. Rallis is strategically important for TCL as it is the only group company catering to agrochemical space. Further, it might be noted that TATA chemicals recently increased stake in Rallis India to 55.05% in July 2023 from 50.06% earlier further reiterating Rallis' strategic importance to the group.

The sustainability angle has become increasingly important. Rallis defined its sustainability model and continuously working towards safer and environment friendly operations along with conservation of resources like water and energy. The boilers now use bio briquettes in place of furnace oil to have least impact on environment. It has invested heavily to ensure zero liquid discharge in factories first time in those industrial areas. In an era where agricultural chemicals face increasing scrutiny, Rallis's proactive approach to environmental stewardship provides both regulatory protection and brand differentiation.

The export story deserves special attention. While most Indian agrochemical companies focus on generic manufacturing for global giants, Rallis has built its own international presence, establishing relationships with distributors in over 58 countries. This isn't just contract manufacturing—it's brand building on a global scale, taking Indian agricultural science to farmers from Africa to Latin America.

Looking at Rallis today, one sees not just a subsidiary but a strategic weapon in Tata Chemicals' arsenal. It provides exposure to the agricultural megatrend, offers recession-resistant revenues, and creates a direct connection to millions of farmers who represent both customers and a political constituency. As climate change intensifies and food security becomes paramount, Rallis's role in ensuring agricultural productivity while maintaining environmental sustainability becomes ever more critical.

The journey from John Rallis's trading house to a science-driven agricultural solutions provider mirrors India's own agricultural transformation. And as we'll see in the next chapter, this appetite for strategic expansion would soon take Tata Chemicals far beyond India's borders, in a series of acquisitions that would reshape the global soda ash industry.

VI. Global Expansion: From Mithapur to the World (2000s–2010s)

The boardroom at Brunner Mond's Winnington Works in Cheshire, England, must have felt the weight of history in 2006. This wasn't just any chemical facility—it was where John Brunner and Ludwig Mond had pioneered the ammonia-soda process in 1873, essentially inventing modern industrial chemistry. Now, executives from a company that British chemists had once mocked were about to acquire this crown jewel of British chemical heritage. The irony was delicious, the symbolism profound. Since 2006, Tata Chemicals has owned Brunner Mond, a United Kingdom-based chemical company with operations in Magadi (Kenya). The acquisition wasn't just about buying capacity—it was about acquiring 133 years of chemical heritage, cutting-edge technology, and most importantly, access to natural soda ash resources that would fundamentally alter Tata Chemicals' cost structure.

On 24 November 2005, TCL agreed to acquire (via a wholly-owned subsidiary) approximately 63.5 per cent of the entire issued share capital of Brunner Mond, amounting to a controlling interest. TCL subsequently made an offer on 6 January 2006 to acquire the remaining shares in Brunner Mond and now owns 100 per cent of its share capital. The total consideration of approximately £100 million seemed modest for what Tata Chemicals was acquiring: not just production facilities but a piece of industrial history.

Brunner Mond brought with it the crown jewel—the Magadi Soda Company in Kenya, sitting atop Lake Magadi's vast natural soda ash deposits. During 1924, Brunner Mond acquired the Magadi Soda Company of Kenya, and this asset alone would prove worth multiples of the acquisition price. Natural soda ash, formed over millennia in alkaline lakes, requires only extraction and processing, not energy-intensive chemical conversion. In an era of rising energy costs and carbon consciousness, this was like owning an oil well in the chemical industry.

Post-acquisition, the parties estimate that they have a combined share of approximately 5 per cent in the global supply of soda ash. While the merged entity has become the third largest soda ash producer in the world. The transformation was immediate—from an India-centric producer to a global player with operations spanning continents. More importantly, Tata Chemicals now had natural soda ash capacity that provided a 30-40% cost advantage over synthetic producers, a moat that would prove invaluable during commodity downturns.

But Prasad Menon, then Managing Director of Tata Chemicals, wasn't done. On 27 March 2008, Tata Chemicals Ltd acquired General Chemical of US, part of the company's strategy to become a truly global chemical company. Tata Chemicals Ltd, part of India's second-largest business group, agreed to buy US-based General Chemical Industrial Products Inc for $1 billion to become the world's second-largest maker of soda ash.

The General Chemical acquisition was transformative in scale. General Chemical has the capacity to produce 2.5 million tons of natural soda ash used to make glass and detergents at its facility in Green River Basin, Wyoming. The privately held company had revenue of $400 million last year and was debt free. This wasn't just adding capacity—it was acquiring the world's largest natural trona deposit, with reserves estimated to last over a century.

The timing seemed audacious. The acquisition closed just as the global financial crisis erupted, with Lehman Brothers collapsing six months later. Credit markets froze, commodity prices crashed, and many questioned whether Tata Chemicals had overextended itself. Shares of Tata Chemicals fell 7.3 percent on the Bombay Stock Exchange on announcement, valuing the maker of caustic soda and fertilizers at about $1.8 billion—barely more than what it was paying for General Chemical.

Yet the strategic logic was impeccable. TCL is third largest soda ash producer globally, with over two-third of its capacity being natural soda ash translating into cost-effective production. While competitors struggled with high energy costs for synthetic production, Tata Chemicals' natural soda ash operations remained profitable even during the downturn. The company had effectively arbitraged geography—using Indian capital to acquire American and African natural resources to serve global markets.

The integration challenges were formidable. Managing operations across time zones, regulatory environments, and corporate cultures tested the company's managerial bandwidth. Throughout the 2000s and 2010s, energy costs doubled; as soda ash is energy intensive to produce, the firm responded via the purchase of a gas-fired combined heat & power plant from the European utility firm E.ON. This wasn't just cost management—it was building energy independence in an energy-intensive industry.

In December 2010, Brunner Mond B. V. acquired British Salt, a Cheshire-based brine supplier, for around £93 million; this vertical acquisition gave longer term raw commodity price certainty and an economy of transport distance for one of the company's largest factories. The logic was elegant: control your raw materials, control your destiny. British Salt's brine wells had a residual life of 50 years, providing multi-generational security of supply.

The global footprint created unexpected synergies. Technology developed in Wyoming could be applied in Kenya. Best practices from Britain improved operations in India. Customer relationships in one geography opened doors in another. The Company has a global presence with key subsidiaries in United States of America ('USA'), United Kingdom ('UK') and Kenya that are engaged in the manufacture and sale of soda ash, industrial salt and related products.

By 2011, the transformation was complete. Brunner Mond was re-branded Tata Chemicals Europe, signaling not just ownership change but cultural integration. The company that British chemists had once dismissed now owned their chemical heritage. The student had not just equaled the teacher—it had acquired the school.

The financial returns vindicated the strategy. Despite the massive capital deployed, return on invested capital improved as natural soda ash's cost advantages flowed through. Market share gains in growing Asian markets offset weakness in mature Western markets. Most importantly, Tata Chemicals had transformed from a price-taker in a commodity business to a cost leader with genuine competitive advantages.

Looking back, the 2006-2008 acquisition spree represents a masterclass in strategic M&A from an emerging market perspective. Tata Chemicals didn't just buy assets—it bought capabilities, resources, and market positions that would have taken decades to build organically. It proved that Indian companies could execute complex cross-border transactions, integrate global operations, and compete with anyone.

But even as the company celebrated its global success, change was brewing at home. Consumer preferences were evolving, health consciousness was rising, and the lines between chemicals, nutrition, and wellness were blurring. The next chapter would require not just geographic expansion but portfolio transformation.

VII. The Consumer Products Pivot & Demerger (2010s–2020)

The conference room at Bombay House in 2018 witnessed an unusual presentation. N. Chandrasekaran, Chairman of Tata Sons, was reviewing a portfolio that seemed schizophrenic: soda ash plants next to spice packets, chemical tankers alongside pulse processing facilities. Tata Chemicals had evolved—or perhaps mutated—into a hybrid that defied easy categorization. The question on everyone's mind: was this diversification or distraction? The journey to this moment had started innocuously. In 2011, the company created the i-Shakti range of pulses, subsequently rebranded Tata Sampann and broadened the product portfolio to include spice powders as well. What began as an experiment in branded staples had grown into a full-fledged consumer products division generating hundreds of crores in revenue. The question was whether this tail was beginning to wag the chemical dog. The i-Shakti story illustrated both the promise and peril of this diversification. In 2010, the company extended the brand equity of i-Shakti to a premium segment and launched a new brand "Tata i-Shakti" with a range of unpolished pulses. To overcome this problem, in October 2015, the company's portfolio of pulses, gram flour and food grade soda under "Tata i-Shakti" label has migrated into a new brand "Tata Sampann". The company also launched a range of spices under the brand name of "Tata Sampann".

The rationale behind getting into this category was described by R. Mukundan, Managing Director and CEO, as, "To not only increase production of pulses in India and help bridge the existing gap between demand and supply, but also provide better quality and hygienic pulses for the Indian household." But beneath this social mission lay a hard commercial reality: the Indian staples market represented a Rs 600,000 crore opportunity, largely unorganized and ripe for consolidation.

Tata Sampann's growth was explosive. In FY 2015-16, the Tata Sampann Pulses and Besan businesses grew by 72% to reach a turnover of 411 crore. The brand expanded from 91,000 outlets to over 122,000 outlets in key focus markets. At the sourcing end, as part of its 'Grow More Pulses' initiative, TCL engaged with 400,000+ farmers in 10 districts across 3 states. This wasn't just distribution—it was building an entire ecosystem from farm to fork.

The spices launch in October 2015 marked a critical escalation. Tata Sampann spices made a successful launch after a test launch in Punjab, Haryana and Himachal Pradesh. Though almost 75% of the market was still unbranded, the branded segment was growing at a faster rate of 26% p.a. in terms of value. The product gained traction and garnered a market share of 1.2% in markets where it was launched—impressive for a new entrant in a category dominated by regional players and centuries-old brands.

Chef Sanjeev Kapoor's association brought credibility and aspiration to what had traditionally been a commodity category. The range of blended spice products like 'dal tadka' masala, 'garam' masala, 'Punjabi chole' masala represented not just products but a lifestyle upgrade for the emerging middle class. Tata Sampann's range of spices carries the promise of authenticity & goodness of Natural Oils, ground from whole spices such that they retain native natural oils ensuring that spices are delivered to the customer just the way nature intended.

But success created its own challenges. By 2018, Tata Chemicals was running what were essentially two distinct businesses under one roof. The consumer products division required different capabilities—brand management, consumer insights, retail relationships—than the core chemicals business. Capital allocation decisions became increasingly complex: should the next crore go to expanding soda ash capacity or building a spice processing plant?

The answer came on May 15, 2019, when The Boards of Directors of Tata Global Beverages Limited ("TGBL") and Tata Chemicals Limited ("TCL"), at their respective meetings held today, have approved the de-merger of the Consumer Products Business of TCL into TGBL through a National Company Law Tribunal ("NCLT") approved scheme of arrangement. The proposed transaction will create a focused Consumer Products Company with a combined turnover and EBITDA of Rs. 9,099 crore and Rs. 1,154 crore respectively.

N Chandrasekaran, Chairman of Tata Sons, articulated the strategic logic: "Tata Consumer Products consolidates our current presence in food & beverages in the fast-growing consumer sector. Through this combination, we have created a strong growth platform to meet the growing aspirations of Indian consumers." The demerger combined key brands such as "Tata Salt", "Tata Tea", "Tata Sampann" and "Tetley" under a single umbrella.

For Tata Chemicals shareholders, the demerger represented both loss and liberation. TCL shareholders will retain their ownership of a focused science-led chemistry solutions and specialty products company with a leading portfolio of products in basic and specialty chemicals and strong cash flows to support future growth. They would also receive shares in the new consumer entity, participating in both value streams.

R Mukundan, Managing Director and CEO of Tata Chemicals, framed it positively: "This combination provides significant benefits to our shareholders by unlocking the value of our Consumer Products Business. In line with its strategy to be a leading science-based solutions company, Tata Chemicals will aggressively grow its Specialty Chemistry business in the areas of Agro-Science, Nutrition Science, Material Science and Energy Storage Science."

The market's reaction was telling. Overall value unlocking was around Rs 25,000 crores. The market cap of the Resulting Company increased thrice from 2019 after receiving nod from NCLT. This wasn't just financial engineering—it was strategic clarity. Each entity could now focus on its core competencies, allocate capital more efficiently, and build management teams suited to their specific challenges.

Formerly known as Tata Global Beverages Limited (TGBL), Tata Consumer Products was formed when the consumer products business of Tata Chemicals merged with Tata Global Beverages in February 2020. The company now operates in the food and beverages industry, with ~56% of their revenue coming from India while the rest is from their international businesses. The combined consumer business would benefit from a combined reach of over 200 million households, a broader portfolio to deepen distribution, enhanced innovation capabilities, as well as a strong product pipeline.

Looking back, the consumer products journey represented both triumph and teaching moment. Tata Chemicals had proven it could build consumer brands from scratch, compete in entirely new categories, and create billions in shareholder value. But it also learned that excellence in chemicals didn't automatically translate to consumer goods, that focus matters as much as diversification, and that sometimes the best way to maximize value is to let businesses fly free.

The demerger marked the end of one chapter and the beginning of another. Freed from the demands of consumer marketing, Tata Chemicals could now pursue its most ambitious transformation yet: becoming a leader in sustainable chemistry and carbon capture. The future belonged not to those who could make products, but to those who could make them without destroying the planet.

VIII. Innovation & Sustainability Leadership (2020s–Present)

The Northwich facility in Cheshire, England, had witnessed many firsts in its 150-year history, but nothing quite like this. On a gray morning in 2022, engineers flipped switches that would capture carbon dioxide from the plant's emissions, purify it to pharmaceutical grade, and inject it directly into the sodium bicarbonate production process. This wasn't just another efficiency improvement—it was alchemy for the climate age, turning waste into product, liability into asset. In 2022, Tata Chemicals, through its subsidiary Tata Chemicals Europe, set up the UK's first industrial-scale carbon capture and usage plant. The plant can capture 40,000 tonnes of carbon dioxide per annum. The plant captures 40,000 tonnes of carbon dioxide each year – the equivalent to taking over 20,000 cars off the roads and reduces TCE's carbon emissions by more than 10%. But the numbers barely captured the revolutionary nature of what was happening.

In a world-first, carbon dioxide captured from energy generation emissions is being purified to food and pharmaceutical grade and used as a raw material in the manufacture of sodium bicarbonate which will be known as Ecokarb®. This wasn't sequestration—hiding carbon underground and hoping it stayed there. This was utilization—transforming emissions into products that saved lives. Much of the sodium bicarbonate exported will be used in haemodialysis to treat people living with kidney disease.

The £20 million investment represented more than capital expenditure—it was a bet on the future of manufacturing itself. This unique and innovative process is patented in the UK with further patents pending in key territories around the world. Ecokarb® will be exported to over 80 countries worldwide and with high-end and pharmaceutical uses it will be used to help treat millions of people across the globe.

Martin Ashcroft, Managing Director of Tata Chemicals Europe, understood the historical significance: "Manufacturing has been key to this area for over 150 years. We're demonstrating that industry can continue to thrive while addressing climate change. This isn't about choosing between jobs and the environment—it's about creating jobs through environmental innovation."

The technical achievement was remarkable. Carbon dioxide captured from energy generation emissions is then purified to food and pharmaceutical grade for use as a raw material. The CCU plant will be capable of capturing and producing up to 40,000 tonnes of carbon dioxide per year and will reduce our carbon emissions at the CHP plant by over 10%. Already one of the most efficient power plants in the UK, our CHP plant is a low-carbon source of electricity, currently producing half the amount of carbon dioxide per kWh of electricity generated compared to a typical gas fired power station. Parallel to the carbon capture breakthrough, another innovation was revolutionizing Tata Chemicals' sustainability story. Sustainably developed Highly Dispersible Silica using the rice husk route offering all the required quality parameters for tyre manufacturing. Produced trial quantities of specialised grades of Highly Dispersible Silica (HDS) from Rice Husk Ash (RHA) to address the sustainability needs of tyre customers.

This wasn't incremental improvement—it was circular economy in action. Rice husk, traditionally agricultural waste burned in fields contributing to air pollution, was being transformed into high-value specialty chemicals. Tata Chemicals now extracts silica from rice husk ash, which is agricultural waste. As silica can be produced from rice husk ash at temperatures between 135 and 240 degrees Celsius, this has also allowed us to use less energy from employing quartz, which formerly required temperatures between 1200 and 1400 degrees Celsius.

The products—TYSIL™ 175GR-RHA and TREADSIL™ 175GR-RHA—weren't just green alternatives but performance enhancers. With customised BET and CTAB properties, TREADSIL™ 175GR-RHA ensures the highest level of rubber reinforcement to optimise wet and dry traction (safety), along with low rolling resistance (better fuel efficiency) in tyre tread compounds. HDS developed through the rice husk route has all the required quality parameters for use in tyre manufacturing. It imparts low rolling resistance, better grip and noise reduction to tyres.

The market timing was perfect. Global tire manufacturers faced increasing pressure to reduce carbon footprints while improving performance for electric vehicles. Tyre industry globally is shifting to HDS Silica. In India, we offer HDS silica to our customers as an alternative to imports. The rice husk-based silica offered a 70% reduction in carbon footprint compared to conventional silica, while meeting all performance specifications.

Beyond silica and carbon capture, Tata Chemicals' innovation pipeline suggested even more radical transformations ahead. The company developed bio-based surfactants from agricultural waste using green chemistry principles. Used as an ingredient in detergents, this bio-based surfactant will be a sustainable alternative to non-biodegradable surfactants. This patented product has proven to be biodegradable, non-skin irritant, and non-flammable during ongoing trials.

The Research and Development Center Tata Chemicals Innovation Center located at Pune, Maharashtra started operations in 2004. The team of scientists is working in the following areas: Food Science & Technology, Advanced Materials, Green Chemistry. With 239 passionate and highly competent scientists working continuously, the company wasn't just adapting to sustainability trends—it was creating them.

The financial impact was already visible. With the speciality product business's prebiotics & formulations and specialty silica products gaining significant customer traction, and Tata Chemicals specialty products revenue registering a growth of 45% in FY 2021-22, Green Chemistry and green applications will continue to be at the core of the Tata Chemical's growth story. The Specialty Chemicals business segment, comprising Agrochemicals, Specialty Silica, Prebiotics, has emerged as a strong strategic focus area at Tata Chemicals.

Looking at the broader portfolio transformation, the numbers told a compelling story. In 2021, Tata Chemicals was ranked 4th among Indian corporations in terms of sustainability and CSR practice. But more importantly, the company had proven that sustainability wasn't a cost center but a profit driver. Products developed using green chemistry commanded premium prices, attracted sticky customers, and opened new markets previously inaccessible to traditional chemical companies.

The innovation roadmap for the future read like science fiction: sodium chemistry for batteries to support the energy storage revolution, synthetic biology platforms for specialty chemicals, conversion of captured CO2 into sustainable aviation fuels, recovery of salts and minerals from waste streams. Each project represented not just a product but a potential platform for entirely new businesses.

What made Tata Chemicals' sustainability journey particularly compelling was its authenticity. This wasn't greenwashing or compliance-driven incrementalism. The company was fundamentally reimagining what a chemical company could be in the 21st century—not a polluter seeking forgiveness but a solution provider for humanity's greatest challenges.

The transformation from salt producer to sustainability leader represented more than strategic evolution—it was existential adaptation. In a world where carbon would be priced, where circular economy would be mandated, where consumers would demand transparency, Tata Chemicals had positioned itself not just to survive but to thrive. The company that British chemists had once mocked for attempting to make soda ash was now teaching the world how to make chemicals without destroying the planet.

IX. Playbook: Business & Investing Lessons

The conference room at any business school could benefit from studying Tata Chemicals' nearly century-long journey. Here was a company that had transformed from a colonial-era salt works into a global sustainability leader, navigating commodity cycles, technological disruptions, and fundamental portfolio shifts. The lessons embedded in this trajectory offer a masterclass in long-term value creation, particularly for companies operating from emerging markets.

Building from Commodities to Specialties: The Value Migration Story

The fundamental playbook begins with understanding value migration in chemical industries. Tata Chemicals didn't abandon basic chemicals—it still produces millions of tons of soda ash—but it systematically moved up the value chain. The journey from salt (commodity) to iodized salt (branded commodity) to Tata Sampann (consumer brand) to specialty silica (technology product) to carbon-captured sodium bicarbonate (sustainability solution) represents a textbook case of value accretion.

Each step required different capabilities: manufacturing excellence for commodities, marketing for brands, R&D for specialties, and systems thinking for sustainability. The key insight: companies needn't choose between commodities and specialties but can use cash flows from the former to fund transformation into the latter. TCL is third largest soda ash producer globally, with over two-third of its capacity being natural soda ash translating into cost-effective production—this cost advantage funds innovation in higher-margin businesses.

Managing Cyclicality Through Diversification

Chemical businesses are notoriously cyclical, but Tata Chemicals has built remarkable resilience through strategic diversification across multiple dimensions. Geographic diversification across four continents means that weakness in one region is offset by strength in another. End-market diversification—from glass and detergents to pharmaceuticals and food—provides natural hedging. Most cleverly, the combination of industrial chemicals (cyclical) with agricultural inputs through Rallis (defensive) and consumer products (stable) created a portfolio that could weather any storm.

The 2008 financial crisis provided the ultimate stress test. While soda ash demand collapsed as construction froze globally, Tata Salt and Rallis' agricultural products remained stable, providing cash flow to survive the downturn. The lesson: diversification isn't about being unfocused—it's about building complementary businesses that share capabilities but have uncorrelated demand drivers.

Sustainability as Competitive Advantage

The carbon capture plant at Northwich represents more than environmental responsibility—it's a strategic moat. By turning CO2 emissions into pharmaceutical-grade sodium bicarbonate, Tata Chemicals transformed a liability (carbon tax exposure) into an asset (premium product). The rice husk silica technology similarly converts agricultural waste into high-value specialty chemicals, creating cost advantages while meeting sustainability mandates.

This isn't philanthropic capitalism—it's hardheaded business strategy. As carbon pricing spreads globally, as supply chains demand emissions transparency, as consumers prefer sustainable products, Tata Chemicals' early investments in green chemistry become competitive advantages that are expensive and time-consuming for competitors to replicate. The plant captures 40,000 tonnes of carbon dioxide each year—that's 40,000 tonnes of competitive advantage annually.

The Tata Group Advantage: Patient Capital and Values-Based Growth

The Tata Group's ownership structure—66% held by philanthropic trusts—provides a unique advantage: patient capital. While public market investors might balk at decade-long transformation journeys, Tata Chemicals could invest in building Mithapur in the 1940s, develop Tata Salt over years in the 1980s, and spend millions on R&D for rice husk silica with uncertain payoffs. This patience has compounded into irreplaceable assets: production sites that couldn't be permitted today, brands that define categories, and technologies protected by patents.

Equally important is values alignment. When Tata Chemicals launched iodized salt to combat deficiency disorders, when it invested in carbon capture before regulations required it, when it developed products for small farmers through Rallis, it wasn't sacrificing returns for responsibility. Instead, it was building trust—with regulators, communities, and customers—that translates into tangible benefits: faster permits, social license to operate, and pricing power.

Emerging Market Multinationals: Going Global from India

Tata Chemicals' international expansion offers crucial lessons for emerging market companies with global ambitions. The acquisition strategy was counterintuitive: instead of buying distressed assets cheaply, Tata Chemicals paid full prices for quality assets like Brunner Mond and General Chemical. The logic was sound: these weren't just production facilities but repositories of knowledge, customer relationships, and regulatory approvals that would take decades to build organically.

The integration approach was equally sophisticated. Rather than imposing Indian management styles on Western operations, Tata Chemicals maintained local leadership while transferring specific capabilities bidirectionally. Technology from Brunner Mond improved Indian operations, while cost management expertise from India enhanced Western margins. The result: a truly global company where innovation could come from any geography.

Capital Allocation: When to Acquire vs Build Organically

Tata Chemicals' capital allocation decisions reveal a nuanced framework. Basic chemical capacity in new geographies was acquired (Brunner Mond, General Chemical) because building greenfield plants would face insurmountable regulatory and competitive barriers. Consumer brands were built organically (Tata Salt, Tata Sampann) leveraging the Tata brand and distribution. Specialty chemicals were developed through R&D investment because intellectual property creation required internal capabilities.

The demerger of consumer products to Tata Consumer Products in 2019 demonstrated another dimension: knowing when to let go. Recognizing that consumer goods required different capabilities than chemicals, the company unlocked Rs 25,000 crores in value through separation. The lesson: capital allocation isn't just about where to invest but also about when to divest, even successful businesses, if they can create more value independently.

The Innovation Imperative

With 239 scientists across three R&D centers, Tata Chemicals spends more on innovation than many pure-play specialty chemical companies. But the approach is distinctive: instead of basic research, the focus is on application—taking known chemistry and applying it in novel ways. Rice husk silica isn't new chemistry; using it for tire reinforcement is new application. Carbon capture isn't breakthrough technology; integrating it into sodium bicarbonate production is breakthrough business model.

This application-focused innovation delivers faster returns and lower risk than fundamental research while still creating defensible intellectual property. The company's 100+ patents aren't for new molecules but for new processes, formulations, and applications that solve specific customer problems. The lesson: innovation doesn't require Nobel Prize-winning science—it requires deep customer understanding and creative problem-solving.

Building Ecosystems, Not Just Businesses

Perhaps the most sophisticated element of Tata Chemicals' strategy is ecosystem creation. Through Rallis, the company doesn't just sell pesticides to farmers but provides complete crop management solutions. The rallis touches 400,000+ farmers across India, creating relationships that go beyond transactions. Similarly, the carbon capture plant doesn't just reduce emissions but creates a template for industrial decarbonization that governments and competitors will follow.

This ecosystem approach creates network effects and switching costs that pure product competition cannot. When a farmer uses Rallis seeds, fertilizers, and pesticides in an integrated package with advisory services, switching to another supplier means rebuilding the entire farming system. When a tire company adopts rice husk silica, it's not just buying a product but joining a sustainability narrative that resonates with its own customers.

The Long Game in Commodity Businesses

Perhaps the most important lesson from Tata Chemicals is that commodity businesses needn't be commodity investments. By combining cost leadership (natural soda ash), operational excellence (integrated manufacturing), market power (global scale), and adjacency expansion (specialties and consumer products), the company has generated returns that belie its commodity exposure.

The key is time horizon. Over quarters, soda ash prices fluctuate wildly. Over decades, demand grows steadily with GDP. Over centuries, the companies that survive are those that reinvest commodity profits into building moats—whether technological, brand, or sustainability-based. Tata Chemicals' journey from salt to science demonstrates that with patience, purpose, and strategic clarity, even the most basic businesses can create extraordinary value.

For investors evaluating chemical companies, for executives managing commodity businesses, for entrepreneurs building from emerging markets, Tata Chemicals offers a playbook worth studying: diversify thoughtfully, innovate practically, expand carefully, and always—always—play the long game.

X. Analysis & Bear vs. Bull Case

Standing at the intersection of chemistry and commerce in 2024, Tata Chemicals presents a fascinating study in contradictions. It's simultaneously a commodity producer vulnerable to Chinese oversupply and a specialty innovator pioneering green chemistry. It trades at modest multiples suggesting market skepticism yet commands premium valuations within its peer group. Understanding both the bull and bear cases requires peeling back layers of complexity that few analysts fully appreciate.

The Bull Case: Structural Advantages in a Transforming World

The bullish thesis begins with an unassailable fact: TCL is third largest soda ash producer globally, with over two-third of its capacity being natural soda ash translating into cost-effective production. In an industry where energy costs represent 30-40% of production for synthetic soda ash, Tata Chemicals' natural deposits in Wyoming and Kenya provide a structural cost advantage that no amount of Chinese capacity addition can erode.

The numbers are compelling. Natural soda ash production requires 50% less energy than the synthetic Solvay process. With carbon pricing spreading globally—the EU's Carbon Border Adjustment Mechanism (CBAM) being just the beginning—this energy advantage translates directly into competitive advantage. A $50 per tonne carbon price would add $20-30 per tonne to synthetic soda ash costs while leaving natural producers largely unaffected.

The demand outlook strengthens the bull case further. Solar glass for photovoltaic panels requires ultra-pure soda ash, a market growing at 20% annually. Electric vehicle batteries use lithium carbonate, produced using soda ash, with demand expected to grow 10x by 2030. Even traditional end markets like flat glass benefit from urbanization in emerging markets. McKinsey projects global soda ash demand to grow from 60 million tonnes today to 80 million tonnes by 2030—and Tata Chemicals is one of the few companies with permitted, expandable natural capacity to meet this demand.

The innovation pipeline suggests transformation beyond commodities. Carbon capture technology leadership positions the company for a world where industrial decarbonization is mandatory, not optional. The UK facility capturing 40,000 tonnes annually is just the beginning; the technology is scalable across all Tata Chemicals facilities and licensable to other producers. At $100 per tonne of CO2—a conservative estimate for 2030 carbon prices—the capture technology alone could generate hundreds of millions in value.

The specialty chemicals pivot is already delivering results. Specialty silica from rice husks commands 40-50% price premiums over conventional silica while reducing carbon footprint by 70%. With tire companies facing pressure to meet sustainability targets, Tata Chemicals' green silica could capture significant market share in a $6 billion global market. The prebiotics business, though small, grows at 30% annually in a market expected to reach $15 billion by 2030.

Perhaps most underappreciated is the operational leverage inherent in the business model. Soda ash plants, once built, run for decades with minimal maintenance capex. As volumes grow and fixed costs spread, incremental margins can exceed 50%. The company's integrated operations—using salt to produce soda ash, soda ash to produce sodium bicarbonate, and waste heat for power generation—create cost advantages difficult to replicate.

Rallis India Limited provides additional optionality. As a separately listed subsidiary, it offers exposure to Indian agricultural transformation while maintaining strategic flexibility. With ~13 million farmer contracts and distribution reaching 80% of Indian districts, Rallis has built an agricultural ecosystem that technology startups would need decades and billions to replicate.

The Bear Case: Cyclical Pressures and Structural Challenges

The bearish perspective begins with sobering financial metrics. Company has a low return on equity of 4.87% over last 3 years—barely covering cost of capital. For a company with supposedly strong competitive advantages, these returns suggest either poor capital allocation, intense competition, or both.

China looms large in bear narratives. Chinese soda ash capacity has grown from 20 million tonnes in 2010 to over 35 million tonnes today, with another 10 million tonnes planned. While most is synthetic and higher-cost, Chinese producers have shown willingness to export below cost during downturns, destroying global pricing. The 2015-2016 period, when Chinese oversupply crashed soda ash prices by 40%, offers a preview of potential future pain.

Commodity cyclicality remains inescapable. Soda ash prices have varied from $150 to $400 per tonne over the past decade—a range that can swing Tata Chemicals from substantial profits to near losses. Unlike consumer products with pricing power or specialty chemicals with differentiation, commodity chemicals face pure price discovery where the marginal producer sets prices for everyone.

Environmental regulations present both opportunity and threat. While carbon capture provides competitive advantage, it also requires substantial capital investment with uncertain returns. The £20 million spent on the UK carbon capture plant could have been returned to shareholders or invested in higher-return specialty chemicals. As regulations tighten globally, compliance costs could accelerate faster than carbon credit revenues.

Water stress poses existential risk, particularly for Indian operations. Soda ash production is water-intensive, requiring 10-15 cubic meters per tonne. With Gujarat facing increasing water scarcity and competing demands from agriculture and urbanization, production constraints or costly water procurement could erode margins. Climate change intensifies these risks—ironic for a company positioning itself as a sustainability leader.

The demerger of consumer products, while unlocking value, removed stable cash flows that cushioned commodity volatility. Tata Salt and Tata Sampann provided predictable revenues during chemical downturns. Without this buffer, Tata Chemicals is more exposed to cyclical swings, potentially requiring conservative balance sheet management that limits growth investments.

Competition in specialty chemicals is intensifying. While rice husk silica offers sustainability advantages, established players like Evonik and PPG have decades of customer relationships and application expertise. Breaking into specialty markets requires not just superior products but extensive technical service, regulatory approvals, and customer validation—processes that take years and offer no guarantee of success.

The Balanced View: Transformation in Progress

The reality likely lies between extremes. Tata Chemicals is neither a pure commodity play destined for cyclical mediocrity nor a specialty chemical champion commanding premium multiples. It's a company in transition, using cash flows from advantaged commodity positions to fund transformation into higher-value products and services.

The key variables to monitor are clear. First, the pace of specialty chemical adoption—whether rice husk silica and bio-surfactants can scale from promising technologies to material revenue contributors. Second, carbon pricing evolution—how quickly and broadly carbon costs are imposed on chemical production. Third, Chinese capacity discipline—whether oversupply crashes prices or rational competition prevails. Fourth, innovation productivity—whether R&D investments generate returns that justify the capital deployed.

For long-term investors, Tata Chemicals offers an asymmetric opportunity. The downside appears limited by replacement cost of assets, natural resource advantages, and Tata Group support. The upside, if sustainability transformation succeeds, could see rerating from commodity to specialty multiples—potentially doubling or tripling valuation. But this requires patience measured in years, not quarters, and comfort with volatility along the journey.

The investment decision ultimately depends on one's view of the future. If you believe the world will price carbon, value sustainability, and demand responsible production, Tata Chemicals is positioning itself on the right side of history. If you believe commoditization, Chinese competition, and cost pressure will dominate, the transformation story may prove more aspiration than reality. Like the chemical reactions it manages, Tata Chemicals' future depends on having the right catalysts, conditions, and time for transformation to occur.

XI. Epilogue & "If We Were CEOs"

As we reach the end of this chemical odyssey, it's worth reflecting on what Tata Chemicals represents in the broader narrative of global industrial evolution. This is a company that began when India was a colony and chemistry was alchemy, survived wars and partition, thrived through liberalization and globalization, and now stands at the forefront of sustainability transformation. The question isn't just where Tata Chemicals goes from here, but what its journey teaches us about industrial strategy in an age of radical transition.

The Specialty Chemicals Opportunity in India

India's specialty chemicals market is projected to reach $64 billion by 2025, growing at 12% annually—twice the global rate. This isn't just about cost arbitrage anymore. India offers a unique combination of technical talent (producing 400,000 engineers annually), manufacturing capability, and increasingly, innovation capacity. Tata Chemicals, with its century of experience and established infrastructure, is ideally positioned to capture this opportunity.

If we were CEO, the first priority would be accelerating the specialty chemicals transformation. The rice husk silica technology shouldn't be limited to tire applications—it could revolutionize cosmetics, food additives, and pharmaceuticals. The carbon capture capability shouldn't just produce sodium bicarbonate—it could create precursors for biodegradable plastics, sustainable aviation fuels, and carbon-negative concrete. Every ton of CO2 captured is a raw material waiting for innovation.

The key is thinking beyond products to platforms. Just as Amazon Web Services emerged from Amazon's internal IT needs, Tata Chemicals' sustainability technologies could become platforms for other companies. Imagine licensing carbon capture technology to cement plants, steel mills, and power generators—turning Tata Chemicals into the "Intel Inside" of industrial decarbonization. The company wouldn't just sell chemicals; it would sell the technology to make chemicals sustainably.

Green Chemistry and the Net-Zero Transition

The global chemical industry must reduce emissions by 90% by 2050 to meet climate targets—a transformation comparable to replacing horses with automobiles. This isn't incremental improvement but fundamental reinvention. Tata Chemicals' early moves in green chemistry position it to lead, not follow, this transition.

If we were CEO, we'd make Tata Chemicals the first net-negative chemical company—removing more carbon from the atmosphere than it emits. This isn't fantasy; it's achievable through a combination of renewable energy (solar/wind for power), carbon capture (for remaining emissions), and carbon utilization (turning CO2 into products). The marketing value alone—"the chemical company that cleans the air"—would justify the investment.

But green chemistry goes beyond carbon. It's about designing out waste, toxicity, and risk from chemical processes. The bio-surfactants from agricultural waste, the water-free production processes, the circular economy approach to raw materials—these aren't just products but previews of chemistry's future. We'd establish a Tata Chemicals Green Chemistry Institute, partnering with universities globally to develop next-generation sustainable processes. The IP generated would be worth more than any acquisition.

Lessons for Chemical Companies in Emerging Markets

Tata Chemicals' journey offers a playbook for chemical companies across the developing world. The key lesson: don't try to compete with China on scale or with Europe on heritage. Instead, leverage unique advantages—natural resources, market understanding, sustainability needs—to build differentiated positions.

For Latin American companies sitting on lithium deposits, for African companies with access to critical minerals, for Southeast Asian companies with agricultural waste, Tata Chemicals demonstrates how to transform local resources into global advantages. The path isn't easy—it requires patient capital, technical capability, and strategic clarity—but the destination justifies the journey.

If we were advising emerging market chemical companies, we'd emphasize three principles. First, start with advantaged raw materials—whether natural deposits, waste streams, or renewable feedstocks—that provide structural cost or sustainability advantages. Second, build capabilities systematically—don't try to leap from commodities to specialties overnight but climb the value ladder deliberately. Third, think globally from day one—international expansion isn't a luxury for after achieving domestic success but a necessity for achieving scale and learning.

What Would We Do Differently?

With the benefit of hindsight, several strategic choices warrant reconsideration. The consumer products business, while successful, perhaps distracted from the core chemical transformation. Those years spent building Tata Sampann could have been invested in specialty chemicals R&D or international expansion. The demerger, though value-creating, came a decade late.

If we were CEO, we'd be more aggressive about portfolio transformation. Commodity chemicals would be managed for cash, not growth, with capital allocated ruthlessly toward specialties and sustainability. We'd exit sub-scale positions—perhaps divesting marginal soda ash facilities to fund innovation. Warren Buffett's capital allocation principles would guide decisions: deploy capital where returns exceed cost of capital, return it to shareholders otherwise.

We'd also accelerate digital transformation. Chemical plants generate enormous data—temperatures, pressures, flows, qualities—but most companies use fraction of this information. Advanced analytics could optimize yields, predict maintenance, and reduce energy consumption by 20-30%. Digital twins of chemical plants would enable virtual experimentation, reducing innovation cycles from years to months. The chemical company of the future is as much a data company as a molecule company.

Partnerships would be another focus area. Instead of trying to develop all technologies internally, we'd create an ecosystem of innovation partners—startups for agility, universities for science, customers for application development. The recent partnership model with Pentair for carbon capture shows the way: combine Tata Chemicals' operational expertise with partners' technical capabilities to accelerate innovation while sharing risk.

The Next Decade: From Chemistry to Materials Science

Looking forward, the boundaries between chemicals, materials, and biology are blurring. Synthetic biology enables microorganisms to produce chemicals previously requiring petroleum. Advanced materials like graphene and carbon nanotubes promise revolutionary properties. Quantum computing could simulate molecular interactions, designing new chemicals in silico before synthesis.

Tata Chemicals must evolve from a chemical company to a materials science company—not just producing molecules but engineering solutions. The speciality silica business points the way: customers don't buy silica; they buy tire performance, food texture, cosmetic feel. Understanding and delivering these functionalities, regardless of underlying chemistry, becomes the competitive advantage.

If we were CEO, we'd establish Tata Materials Sciences as a new division, recruiting talent from aerospace, electronics, and biotechnology. This wouldn't compete with existing businesses but explore adjacencies—biodegradable packaging, energy storage materials, smart coatings that respond to environment. The investments would be modest initially but could birth billion-dollar businesses within a decade.

The Ultimate Question: Purpose and Profit

Throughout its history, Tata Chemicals has balanced purpose and profit—from iodizing salt to capturing carbon. This isn't corporate social responsibility bolted onto a profit-maximizing machine but purpose embedded in business model. The question for the next century is whether this balance can be maintained as competition intensifies and stakeholder demands multiply.

If we were CEO, we'd double down on purpose-driven innovation. Every new product would require a sustainability thesis—how does it reduce environmental impact, improve human health, or advance social equity? This isn't altruism but strategy. In a world where consumers, regulators, and investors increasingly value sustainability, purpose becomes the ultimate differentiator.