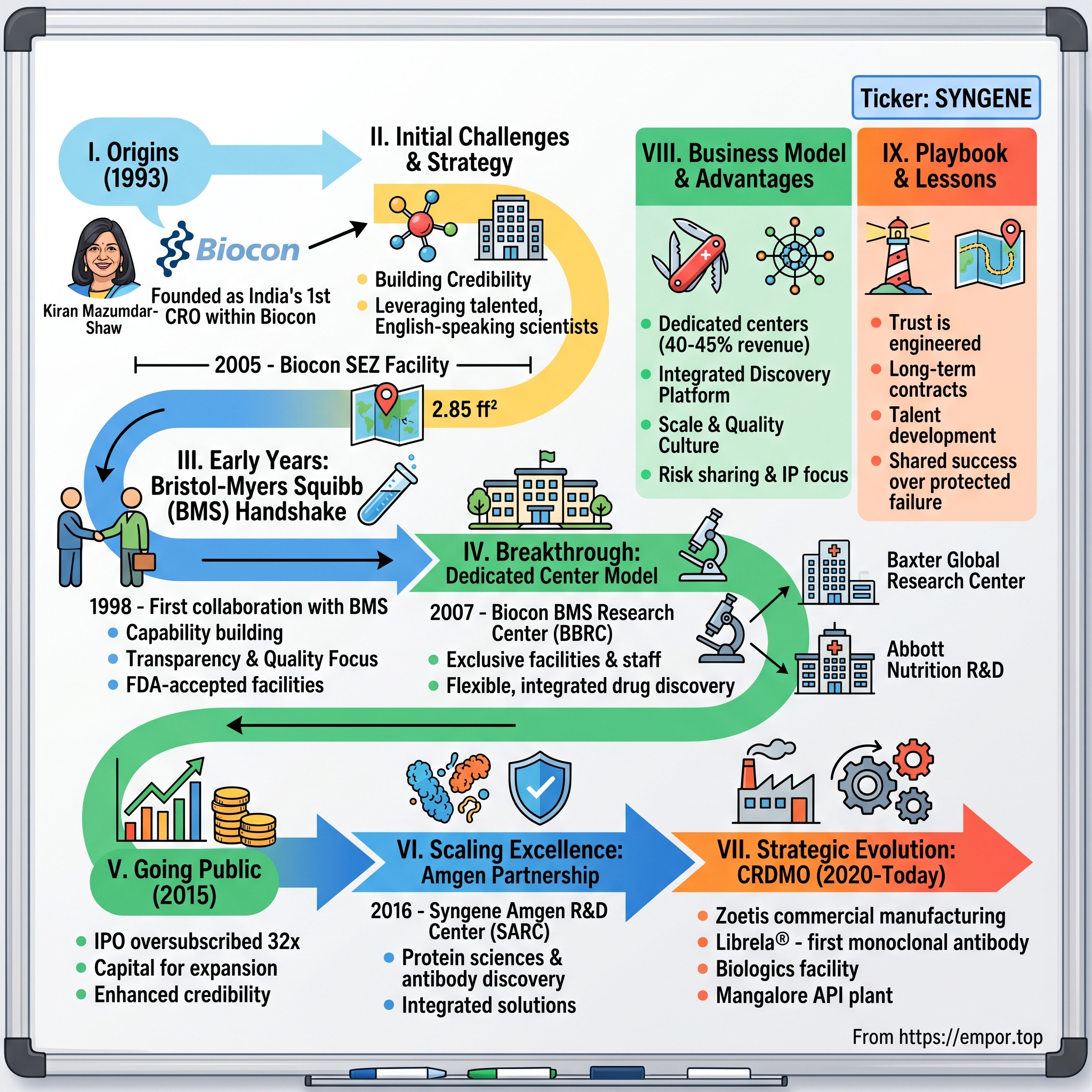

Syngene International: India's Contract Research Powerhouse

I. Introduction & Episode Roadmap

Picture this: It's 2015, and in a nondescript building in Bangalore's Biocon Park, scientists in white coats are synthesizing molecules that might become the next blockbuster drug. But here's the twist—they don't work for Pfizer, Novartis, or any Big Pharma giant. They work for Syngene International, and their lab coats might bear the logo of Bristol-Myers Squibb one day, Amgen the next. This is the new world of pharmaceutical R&D, where the boundaries between companies blur, and innovation happens in unexpected places.

Syngene International isn't just another outsourcing company. It's India's first Contract Research Organization (CRO), established in 1993 when the very concept of outsourcing drug discovery was heretical to Big Pharma. Today, with over 400 active customers and partnerships with 13 of the top 15 global pharmaceutical companies, Syngene has become a $3.5 billion research services powerhouse that's rewriting the rules of how drugs get discovered and developed.

The question that drives this story isn't just how a subsidiary of Biocon became independent and thrived—it's how an Indian company convinced the world's most secretive, IP-obsessed industry to trust it with their crown jewels. How do you build credibility when your country is known for copying drugs, not inventing them? How do you create a business model so sticky that clients sign 10-year contracts in an industry notorious for switching vendors?

This is a story about trust engineering as much as it is about chemical engineering. It's about building bridges between Bangalore and Boston, creating dedicated research centers that feel like extensions of client companies, and navigating the delicate dance between independence and integration. Along the way, we'll explore how Syngene pioneered the dedicated center model, why its IPO was oversubscribed 32 times, and what its journey tells us about the future of global innovation.

We'll journey through seven distinct acts: from the company's origins in Kiran Mazumdar-Shaw's Biocon empire, through its early struggles for credibility, the breakthrough innovation of dedicated centers, the drama of going public, scaling with giants like Amgen, navigating the modern era of AI and precision medicine, and finally, understanding what makes its business model so resilient. Each phase reveals not just corporate milestones but fundamental lessons about building trust, managing complexity, and creating value in the knowledge economy.

So buckle up. This isn't just a story about outsourcing or cost arbitrage. It's about how a company from Bangalore became the extended brain of Big Pharma—and what that means for the future of innovation itself.

II. Origins: The Biocon Story & Founding Context

The year was 1978, and Kiran Mazumdar-Shaw, a 25-year-old brewmaster fresh from Australia, was trying to start a biotechnology company in India. Banks wouldn't lend to her. Employees wouldn't work for her. The very idea of biotechnology in India seemed absurd—this was a country still struggling with basic healthcare, where the Green Revolution was the height of biological innovation. Yet from a rented garage in Bangalore with initial capital of ₹10,000, she founded Biocon, focused initially on industrial enzymes.

Fast forward to 1993. Biocon had grown from that garage startup to a recognized name in industrial biotechnology, but Mazumdar-Shaw saw something others didn't: the massive shift beginning in global pharmaceutical R&D. The blockbuster drug model was starting to crack. R&D costs were exploding—what cost $100 million to develop a drug in the 1970s was approaching $500 million by the early '90s. Big Pharma was desperate for solutions.

Meanwhile, India's pharmaceutical landscape was undergoing seismic shifts. The country had built a formidable generics industry by reverse-engineering patented drugs—perfectly legal under India's 1970 Patents Act, which didn't recognize product patents for pharmaceuticals. Indian companies like Cipla and Dr. Reddy's had become masters of process chemistry, figuring out alternative ways to synthesize complex molecules. But with India's impending entry into the WTO and the coming of TRIPS compliance, this model had an expiration date. It was in this context that Syngene was established in 1994 as a custom research company under the Biocon umbrella. The vision was audacious: create India's first dedicated Contract Research Organization at a time when the very concept seemed oxymoronic. India did research? India did contract manufacturing of APIs, sure. But original research for global innovators? The skepticism was palpable.

What made the timing particularly prescient was the convergence of multiple factors. First, the cost of drug development was entering exponential growth—by 2000, it would breach $800 million per approved drug. Second, the patent cliff loomed large for Big Pharma, with blockbusters worth billions set to lose exclusivity. Third, advances in combinatorial chemistry and high-throughput screening were creating a data deluge that required armies of skilled scientists—armies that were expensive to maintain in Boston or Basel but abundant in Bangalore.

The initial model was deceptively simple: leverage India's pool of talented, English-speaking scientists who could work at a fraction of Western costs. But Mazumdar-Shaw understood something deeper. This wasn't about labor arbitrage—it was about creating a new innovation ecosystem. Incorporated in 1993, Syngene is listed separately on the Indian stock exchanges – NSE and BSE, though this separate listing would come much later in its journey.

The early challenges were monumental. How do you convince a pharmaceutical company to outsource research when a single leaked molecule structure could cost billions? How do you build GMP-compliant facilities when Indian banks wouldn't lend for such ventures? How do you recruit PhD scientists when the brightest minds were fleeing to America?

The answer lay in patient capital and strategic positioning. Being part of Biocon provided the financial cushion and credibility that a standalone startup could never have achieved. It also provided something more subtle but equally important: a deep understanding of Western quality standards and regulatory requirements from Biocon's enzyme export business.

The founding team understood that success would require more than just cost advantages. They needed to build trust in an industry where trust was everything. This meant not just meeting international quality standards but exceeding them. It meant creating information firewalls that would make clients comfortable sharing their most sensitive research. It meant building a culture that could seamlessly integrate with client teams located thousands of miles away.

As Syngene's laboratories began taking shape in Bangalore's emerging Biocon Park, the company was essentially making a bet on the future of pharmaceutical R&D. The bet was that the industry's traditional, vertically integrated model—where everything from discovery to commercialization happened under one roof—was unsustainable. The future belonged to networks, partnerships, and ecosystems. And Syngene positioned itself to be the critical node in this emerging network.

The timing couldn't have been better. As the 1990s progressed, Big Pharma's productivity crisis deepened. Despite spending more on R&D, they were producing fewer new drugs. The industry needed a new model, and Syngene was ready to provide it. But first, it had to prove itself with actual clients, actual molecules, and actual results. The stage was set for what would become one of the most important experiments in pharmaceutical innovation.

III. Building the Foundation: Early Years (1993–2007)

The story of Syngene's early years begins with a single handshake and a leap of faith. In 1998, executives from Bristol-Myers Squibb arrived in Bangalore, skeptical but curious. The American pharmaceutical giant was hemorrhaging money on R&D—their productivity had declined by 50% over the previous decade despite doubling their research budget. They needed something radical, and Syngene's pitch was compelling enough to start what would become a collaboration that has been in place since 1998.

But this wasn't the triumphant beginning it might seem in hindsight. The first Bristol-Myers Squibb scientists who visited Syngene's facilities in 1998 were polite but unconvinced. The labs were basic. The equipment, while functional, wasn't cutting-edge. Most importantly, the Indian scientists, brilliant as they were, had never worked on the kinds of novel molecules that Big Pharma dealt with. They knew generics; they didn't know innovation.

What happened next was a masterclass in capability building. Rather than pretending to be something they weren't, Syngene's leadership took a radically transparent approach. They invited Bristol-Myers Squibb scientists to essentially embed themselves in Bangalore, to train their Indian counterparts not just in techniques but in the culture of pharmaceutical innovation. It was like a reverse colonial experiment—Western knowledge flowing East, but this time invited and on Indian terms.

The early projects were deliberately modest. Simple synthesis work. Analytical method development. Nothing that would catastrophically damage Bristol-Myers Squibb if it went wrong. But with each successful delivery, trust grew incrementally. The Syngene scientists weren't just following protocols—they were improving them. They brought fresh perspectives to problems that had stumped teams in Princeton.

By 2000, Syngene had expanded its laboratory space to over 23,000 square feet and received 100% Export Oriented Unit (EOU) status from the Government of India. This wasn't just a regulatory milestone—it was a signal that the Indian government recognized the strategic importance of what Syngene was building. The tax benefits that came with EOU status allowed Syngene to reinvest aggressively in infrastructure and talent.

The talent equation was particularly fascinating. India was producing 200,000 science and engineering graduates annually, including thousands of PhDs. But most saw research as a waystation to management roles or immigration to the West. Syngene had to create an entirely new value proposition: stay in India, do cutting-edge science, work on molecules that might save millions of lives, and earn a competitive salary without leaving home.

The company developed what internally they called the "MIT Strategy"—not Massachusetts, but "Made in India Talent." They recruited from the Indian Institutes of Technology, the Indian Institute of Science, and other premier institutions. But recruitment was just the beginning. The real innovation was in creating a research culture that felt both Indian and international. One of the critical early milestones came when Acceptance of the clinical and bio-analytical facilities of Clinigene International Limited by the Department of Health and Human Services, FDA was achieved. This wasn't just a regulatory checkbox—it was a validation that an Indian company could meet the gold standard of pharmaceutical quality. The FDA inspectors who came to Bangalore expected to find shortcuts, compromises, the typical developing world approach to regulation. Instead, they found facilities that were not just compliant but exemplary.

The quality systems that Syngene built went beyond mere compliance. They created what they called "quality by design"—building quality into every process rather than testing for it at the end. This meant investing in equipment that was often more sophisticated than what clients had in their home laboratories. It meant creating standard operating procedures that were more rigorous than industry norms. It meant saying no to business that would compromise these standards.

By 2005, Syngene had moved to Biocon SEZ, a 90-acre biopharmaceutical special economic zone, with operations spread over 65,000 square feet. The new facility wasn't just bigger—it represented a fundamental shift in ambition. This was no longer about being a low-cost provider; it was about being a capability provider that happened to have cost advantages.

The evolution of services during this period tells the story of increasing sophistication. Initially focused on chemistry services—synthesizing molecules according to client specifications—Syngene systematically added capabilities in biology, pharmacokinetics, and toxicology. Each addition required not just equipment and expertise but also the trust of clients to handle increasingly sensitive and valuable research.

One pivotal moment came when a major pharmaceutical company asked Syngene to work on a molecule in Phase II clinical trials—a drug candidate worth potentially billions if successful. The chemistry was complex, requiring multiple chiral centers and yields that had stymied the client's own teams. Syngene's chemists not only synthesized the molecule but improved the process, increasing yields from 12% to 34%. This single success story rippled through the industry grapevine.

The human dimension of this growth was equally important. Syngene created career paths that didn't exist before in India—research careers that weren't stepping stones to something else but destinations in themselves. They instituted sabbaticals for scientists to pursue PhDs, created internal research programs where scientists could work on their own projects, and most importantly, created a culture where failure in pursuit of innovation was acceptable.

By 2007, Syngene had crossed an annual turnover of over ₹1,000 million (₹100 crores), but more importantly, it had proven something fundamental: that trust in pharmaceutical research could be engineered through systematic capability building, transparent operations, and relentless focus on quality. The foundation was now solid enough to support something truly ambitious—the dedicated center model that would revolutionize pharmaceutical outsourcing.

The Bristol-Myers Squibb team that visited in 2007 to discuss this new model weren't coming to a startup anymore. They were coming to a proven partner with nearly a decade of successful collaboration, FDA-approved facilities, and most importantly, a track record of keeping secrets and delivering results. The stage was set for the next act in Syngene's evolution.

IV. The Dedicated Center Model: Innovation in Outsourcing (2007–2015)

The research campus, known as Biocon BMS Research Center (BBRC), Syngene's first dedicated R&D Center, was established in 2007—but the story behind this transformational moment reveals a radical reimagining of what pharmaceutical collaboration could be. Picture the scene: Bristol-Myers Squibb's head of discovery, sitting across from Syngene's leadership, proposing something that had never been done before in the industry. Not just outsourcing projects or processes, but creating an entire research campus that would function as an extension of Bristol-Myers Squibb itself.

The pharmaceutical industry in 2007 was in crisis. The number of new drugs approved annually had declined by 50% from the 1990s peak, while development costs had tripled. Bristol-Myers Squibb, facing patent cliffs on several blockbusters, needed to fundamentally restructure its R&D model. The traditional approach—maintaining massive research facilities in high-cost locations—was becoming unsustainable. But the alternative—piecemeal outsourcing—lacked the integration and commitment needed for complex drug discovery.

Syngene's proposal was elegantly simple yet operationally complex: create a dedicated facility within Biocon Park that would be exclusively for Bristol-Myers Squibb, staffed by Syngene scientists who would work solely on Bristol-Myers Squibb projects, using Bristol-Myers Squibb's processes and systems. It would be, in essence, Bristol-Myers Squibb Bangalore—except the scientists would be on Syngene's payroll.

The negotiations for this arrangement took eighteen months. Every detail had to be worked through: How would intellectual property be protected? How would scientists be prevented from working on competitor projects? How would quality standards be maintained? How would the economics work? The final agreement was a 300-page document that created an entirely new template for pharmaceutical collaboration.

The physical manifestation of BBRC was impressive—a 90,000 square foot facility with state-of-the-art laboratories for medicinal chemistry, biology, pharmacology, and drug metabolism. But the real innovation was in the operational model. Syngene created complete information firewalls, with dedicated IT systems, separate badge access, and even separate cafeterias to ensure no inadvertent information sharing with other clients.

The cultural integration was perhaps the most challenging aspect. Bristol-Myers Squibb sent senior scientists to Bangalore for extended periods—not just to train but to embed their research culture. They conducted the same seminars, held the same review meetings, followed the same decision-making processes as in Princeton or Wallingford. The goal was to make geography irrelevant to the science.

It is the largest research and development facility for Bristol-Myers Squibb outside of the United States and plays an integral part within their global research and development network. Within three years, BBRC had grown to house over 400 scientists working on multiple therapeutic areas including oncology, cardiovascular, and immunology. The facility wasn't just executing protocols designed elsewhere—it was originating ideas, designing experiments, and making critical go/no-go decisions on drug candidates.

The success metrics were compelling. BBRC contributed to multiple drug candidates entering clinical trials, with several progressing to late-stage development. The cost savings were significant—estimates suggested 40-50% reduction in research costs—but more importantly, the model provided flexibility and scalability that fixed infrastructure couldn't match.

Watching BBRC's success, other pharmaceutical companies began approaching Syngene with similar proposals. In 2012, Abbott (later AbbVie) partnered with Syngene to establish a dedicated nutrition R&D center, focused on developing products for emerging markets. This wasn't drug discovery but required similar capabilities in formulation, analytical chemistry, and clinical research.

The Baxter collaboration in 2013 took the model in another direction. Collaboration with Baxter International Inc. to establish the 'Baxter Global Research Center', our third dedicated R&D center focused not on discovery but on analytical services for Baxter's global operations. The center supported everything from renal care products to intravenous solutions, requiring expertise in medical devices as much as pharmaceuticals.

Each dedicated center refined the model further. Syngene learned how to rapidly stand up new facilities, how to recruit and train specialized teams, how to integrate with different corporate cultures. They developed modular approaches to laboratory design, standardized training programs that could be customized for specific clients, and governance structures that balanced autonomy with integration.

The economic model of dedicated centers was particularly clever. Clients committed to long-term contracts—typically 7-10 years—providing Syngene with predictable revenue streams that justified upfront investments in infrastructure and training. The contracts typically included annual escalations and performance incentives, aligning interests between Syngene and its clients. For clients, the model converted fixed costs into variable costs while maintaining the control and integration of an internal R&D unit.

But perhaps the most important innovation was in risk sharing. Traditional outsourcing was transactional—you pay for services rendered. The dedicated center model created genuine partnerships where Syngene had skin in the game. Performance metrics weren't just about meeting specifications but about contributing to successful drug development. Some contracts even included milestone payments linked to drugs progressing through clinical trials.

The governance structure of these centers was equally innovative. Joint steering committees with equal representation from Syngene and the client made strategic decisions. Operating committees handled day-to-day management. Scientific advisory boards brought in external expertise. This wasn't vendor management—it was partnership management.

By 2015, the dedicated center model had proven its worth. BBRC alone housed over 400 scientists and had contributed to 10 drug candidates progressing to further development. The model had been replicated with other clients and had become a differentiator for Syngene in a crowded CRO market. But more importantly, it had changed the conversation about pharmaceutical outsourcing from cost arbitrage to capability enhancement.

The success of the dedicated center model also created a new challenge: how to balance the needs of dedicated center clients with the growing fee-for-service business. How to ensure knowledge spillovers that benefited all clients while maintaining strict confidentiality? How to manage careers when scientists were dedicated to single clients for years? These challenges would require new innovations in the years ahead.

As 2015 approached, Syngene faced a critical decision. The dedicated center model had been incredibly successful, but it also created dependencies. With a significant portion of revenue tied to a few large clients, Syngene needed to diversify and grow. The answer would come in the form of an IPO that would provide capital for expansion while maintaining the unique culture and capabilities that made the dedicated center model possible. The next chapter in Syngene's story was about to begin.

V. The IPO Story: Going Public (2015)

July 27, 2015, 10:00 AM. The Bombay Stock Exchange's electronic boards flickered to life as Syngene International's initial public offering opened for subscription. Within minutes, the institutional portion was oversubscribed. By the end of the first day, retail investors had bid for twice the shares on offer. When the three-day bidding window closed on July 29, the IPO was oversubscribed 32.05 times overall, with Qualified Institutional Buyers (QIBs) subscribing 51.47 times and Non-Institutional Investors an extraordinary 90.24 times their allocated portions.

But this moment of market euphoria was years in the making, born from strategic necessity rather than opportunism. By early 2014, Syngene faced a classic growth company dilemma. The dedicated center model had been wildly successful, but each new center required significant upfront capital. Expansion into new therapeutic areas demanded expensive equipment and specialized expertise. Meanwhile, Biocon, the parent company, was pursuing its own capital-intensive biosimilars strategy and couldn't fund both ambitions.

The boardroom discussions at Biocon Park were intense. Kiran Mazumdar-Shaw had built Syngene as an integral part of the Biocon story. Spinning it off into an independent public company meant giving up control, exposing the business to market volatility, and potentially creating a competitor. But it also meant giving Syngene the freedom and resources to pursue its own destiny.

The decision to go public was ultimately driven by three strategic imperatives. First, access to capital markets would fund expansion without depending on Biocon's balance sheet. Second, public listing would enhance credibility with global clients who were increasingly scrutinizing the financial stability of their research partners. Third, it would create currency—in the form of publicly traded stock—for attracting and retaining top talent through employee stock options.

The preparation for the IPO began in earnest in late 2014. Morgan Stanley and Credit Suisse were appointed as lead managers, bringing global credibility to what was essentially an Indian mid-cap offering. The red herring prospectus, filed in July 2015, told a compelling story: revenues had grown from ₹733 crores in FY2013 to ₹1,097 crores in FY2015. Net profit had nearly doubled from ₹127 crores to ₹244 crores. The company served 293 clients, including 8 of the top 10 global pharmaceutical companies.

The price band was set at ₹240-250 per share, valuing the company at approximately ₹10,000 crores (about $1.5 billion). The issue size was ₹550 crores, comprising a fresh issue of ₹250 crores and an offer for sale of ₹300 crores by Biocon. The pricing was aggressive—at the upper band, it implied a P/E ratio of about 41, rich even for a growth company.

The roadshow revealed fascinating dynamics. International investors were immediately drawn to the China-plus-one narrative—the need for pharmaceutical companies to diversify their research partnerships beyond China. Indian institutions saw it as a play on global pharmaceutical R&D spending. Retail investors were attracted by the Biocon pedigree and Kiran Mazumdar-Shaw's track record.

The three-day bidding period was a masterclass in market management. On day one, institutional investors bid cautiously, waiting to gauge overall demand. By day two, as retail enthusiasm became apparent, institutions rushed in, not wanting to miss allocation. The final day saw frantic bidding as the oversubscription multiples created their own momentum.

On August 11, 2015, Syngene International listed on both the National Stock Exchange and Bombay Stock Exchange at ₹295 per share—an 18% premium to the issue price of ₹250. Within minutes, the stock touched ₹315, giving early investors a 26% gain. The market capitalization exceeded ₹12,000 crores, making it one of the most successful IPOs of 2015.

But the real story wasn't in the listing day gains—it was in what the IPO enabled. The ₹250 crores raised from the fresh issue was immediately deployed into expansion. New laboratories were commissioned for biologics research. Advanced analytical equipment for characterizing complex molecules was procured. The Mangalore API manufacturing facility received additional investment.

The IPO also triggered important governance changes. Independent directors with deep pharmaceutical and financial expertise joined the board. Quarterly earnings calls forced management to articulate strategy more clearly. The discipline of meeting market expectations drove operational improvements and efficiency gains.

Perhaps most importantly, the public listing changed Syngene's relationship with clients. The transparency required of a public company—audited financials, regulatory filings, analyst coverage—provided assurance about Syngene's stability and longevity. Clients could now conduct due diligence through public documents rather than lengthy audits. The stock price became a daily referendum on Syngene's business model.

The employee stock option plan, enabled by the public listing, became a powerful retention tool. Scientists who had joined Syngene in its early days saw their stock options multiply in value. This created a culture of ownership, where employees thought like shareholders, focusing on long-term value creation rather than short-term gains.

The post-IPO period also brought challenges. The market's quarter-to-quarter focus sometimes conflicted with the long-term nature of drug development. Currency fluctuations—most revenues were in dollars while costs were in rupees—created volatility in reported earnings. The need to maintain margins while investing for growth required careful balance.

Biocon's decision to remain the majority shareholder—retaining about 74% post-IPO—provided stability but also created complexity. Related party transactions had to be carefully managed and disclosed. The market constantly speculated about potential conflicts of interest. Some investors worried about Biocon's overhang—the possibility of future stake sales depressing the stock price.

Yet, the IPO achieved its strategic objectives. It provided capital for growth, enhanced credibility with clients, and created a currency for talent acquisition. More subtly, it marked Syngene's transformation from a subsidiary serving a specific purpose to an independent company charting its own course. The public market's endorsement validated the business model and set the stage for the next phase of growth.

As 2015 drew to a close, Syngene's stock had settled into a trading range around ₹300-350, maintaining most of its listing gains. The company had successfully transitioned from private to public, from subsidiary to independent, from promise to performance. The capital and credibility gained from the IPO would soon be put to use in ambitious expansions, including the game-changing partnership with Amgen that would define the next chapter of Syngene's evolution.

VI. Scaling Excellence: The Amgen Partnership & Beyond (2016–2020)

The conference room at Amgen's Thousand Oaks headquarters was silent as the proposal was presented. It was early 2016, and Amgen, the world's largest independent biotechnology company, was wrestling with a familiar challenge: how to maintain R&D productivity while managing costs in an era of increasing complexity. The proposal on the table from Syngene wasn't just another outsourcing arrangement—it was a commitment to build While SARC was established in 2016, Syngene's association with Amgen Inc. dates back several years, but this would take the relationship to an entirely new level.

During 2016, Syngene set up an Amgen R&D center in Bangalore—the Syngene Amgen Research and Development Center (SARC). But unlike the BBRC model, which started large, SARC began modestly with 50 scientists, allowing for organic growth based on proven success. This reflected Amgen's more cautious, data-driven culture—they wanted proof of concept before scaling.

The initial focus areas were carefully chosen: protein sciences, antibody discovery, and peptide chemistry—areas where Syngene had built deep expertise but where Amgen needed additional capacity. The first projects were deliberately low-risk: characterizing antibodies, developing analytical methods, routine assays. But within six months, the quality of work and the seamless integration with Amgen's global teams led to more complex assignments.

What made the Amgen partnership particularly interesting was the knowledge transfer component. Amgen didn't just want execution; they wanted innovation. They instituted joint research programs where Syngene scientists could propose novel approaches to Amgen's challenges. Regular video conferences turned into collaborative brainstorming sessions. Publications were co-authored. Patents were jointly filed.

By 2018, SARC had grown to over 100 scientists working across multiple therapeutic areas. The center had moved beyond support functions to become integral to Amgen's drug discovery efforts. The scope of engagement covers integrated drug discovery and development solutions in discovery chemistry and biology, peptide chemistry, antibody and protein reagents, pharmacokinetics and drug metabolism and pharmaceutical development.

Meanwhile, the Bristol-Myers Squibb partnership was reaching new heights. In November 2017, the companies announced a major expansion. The next phase of the partnership will see the addition of a new facility to support future Bristol-Myers Squibb research and development operations, an expansion of the team and the extension of the existing agreement through 2026. This wasn't just a renewal—it was a doubling down on the model that had worked so well.

"We are proud of how the partnership with Syngene and the BBRC has evolved," said Carl Decicco, Ph.D., Head of Discovery, Bristol-Myers Squibb. "At its inception, it was thought that BBRC would be a fast, nimble organization that could partner closely with our R&D organization to accelerate the development of Bristol-Myers Squibb's pipeline and the partnership has exceeded all expectations."

The numbers told a compelling story. BBRC had contributed to 10 drug candidates entering development, multiple patent filings, and significant cost savings. But more importantly, it had become a talent hub, with Syngene scientists moving to Bristol-Myers Squibb facilities in the US for advanced training and Bristol-Myers Squibb scientists spending years in Bangalore, creating deep cultural and scientific exchange.

This period also saw Syngene expanding beyond pharmaceutical companies. Animal health emerged as a significant opportunity. Companies like Zoetis, facing similar R&D productivity challenges as human pharmaceutical companies, found Syngene's model attractive. The scientific capabilities were largely transferable, but the regulatory requirements and development timelines were different, requiring Syngene to adapt its processes.

The expansion into biologics during this period was particularly strategic. While Syngene had built its reputation in small molecule chemistry, the future of pharmaceuticals was increasingly biological—antibodies, proteins, cell and gene therapies. Syngene invested heavily in mammalian cell culture capabilities, protein characterization equipment, and most importantly, expertise in these complex modalities.

The digital transformation initiated during this period was equally important. Syngene implemented electronic laboratory notebooks across all facilities, created data lakes that could integrate information from multiple experiments, and began experimenting with artificial intelligence for drug design. This wasn't just about efficiency—it was about creating competitive advantages in an increasingly data-driven industry.

The governance and compliance infrastructure also evolved significantly. With multiple dedicated centers operating simultaneously, Syngene had to ensure absolute information security while enabling knowledge sharing where appropriate. They implemented what they called "translucent walls"—barriers that prevented inappropriate information flow but allowed for sharing of general expertise and best practices.

Financial performance during this period validated the strategy. Revenues grew from ₹1,154 crores in FY2016 to ₹1,958 crores in FY2020. More importantly, the revenue mix shifted toward higher-margin discovery services and long-term contracts. The EBITDA margin expanded from 28% to 31%, demonstrating that scale and efficiency gains were flowing to the bottom line.

The human capital story was equally impressive. Syngene's workforce grew from about 3,100 scientists in 2016 to over 4,500 by 2020. But this wasn't just quantitative growth. The company was attracting increasingly senior talent, including scientists returning from careers in the US and Europe. The publication record improved dramatically, with Syngene scientists contributing to papers in top-tier journals.

The COVID-19 pandemic that struck in early 2020 became an unexpected test of the model. When lockdowns were imposed in March 2020, Syngene had to rapidly adapt. Critical experiments couldn't stop—drugs in development couldn't wait for the pandemic to end. Syngene implemented bubble protocols, where scientists lived on campus for weeks at a time. Digital collaboration tools, already in place, became lifelines for maintaining client relationships.

The pandemic response revealed the resilience of the dedicated center model. Because scientists were dedicated to specific clients, they could be prioritized for on-site work. Because relationships were long-term, clients were understanding of temporary disruptions. Because capabilities were integrated, work could be redistributed across teams and geographies.

As 2020 ended, despite the pandemic disruption, Syngene had not only survived but thrived. The Amgen partnership had grown to encompass new therapeutic areas. The Bristol-Myers Squibb collaboration was stronger than ever. New clients were signing up for dedicated centers, attracted by the stability and commitment the model provided in uncertain times.

The period from 2016 to 2020 had proven that Syngene's model could scale without losing quality, could diversify without losing focus, and could innovate without losing discipline. The company had transformed from an interesting experiment in pharmaceutical outsourcing to an essential partner in global drug development. The stage was set for even more ambitious expansion in the decade ahead.

VII. Modern Era: Expansion & Strategic Evolution (2020–Today)

April 26, 2021, marked a watershed moment in Syngene's evolution. Syngene announced on April 26, 2021 that it has extended its research collaboration with Bristol Myers Squibb through the end of 2030. But this wasn't just another contract extension—it represented a fundamental reimagining of what a research partnership could be. The extension envisions a 40% increase in the number of scientists and the addition of a new 50,000ft² dedicated laboratory space.

The Bristol Myers Squibb decision to extend until 2030 sent ripples through the pharmaceutical industry. In an era where companies were increasingly distributing risk across multiple partners, Bristol Myers Squibb was concentrating its bet on Syngene. The expansion to nearly 700 scientists made BBRC larger than many biotech companies' entire R&D operations.

Almost simultaneously, During the year we announced the extension of our collaboration with Amgen until the end of 2026, with plans for a new exclusive laboratory will be built to accelerate Amgen projects. The Amgen expansion was particularly significant because it included new modalities—cell and gene therapy capabilities that represented the cutting edge of pharmaceutical innovation.

But the most transformative development of this period was Syngene's aggressive expansion into commercial manufacturing. The company recently signed was with the leading Animal Health company, Zoetis. The 10-year agreement is for manufacturing the drug substance for Librela® (bedinvetmab), a first-in-class monoclonal antibody used for treating osteoarthritis in dogs. This wasn't research services—this was commercial-scale manufacturing of an approved drug, marking Syngene's evolution from CRO to CRDMO (Contract Research, Development and Manufacturing Organization).

The Zoetis deal demonstrated Syngene's ability to win in competitive situations. Multiple CDMOs had bid for the Librela manufacturing contract, including established players in Europe and the US. Syngene won not on price but on its integrated model—the same scientists who had worked on Librela's development would oversee its commercial manufacturing, ensuring seamless knowledge transfer and risk mitigation.

The infrastructure expansion during this period was staggering. The newly upgraded biologics facility - Unit 3 - would be operational for clinical and commercial supply in the second half of 2024. The drug substance capacity includes two production suites with five 2KL single use bioreactors each, for a total capacity of 20KL. The facility also includes two high-speed vial filling lines capable of producing up to 1 million vials per day ranging from 1 to 100mL fill volumes.

The Mangalore API facility, under construction since 2019, represented another strategic bet. Located on 46 acres in the Mangalore Special Economic Zone, this wasn't just additional capacity—it was Syngene's entry into large-scale commercial API manufacturing. The facility was designed to meet the most stringent regulatory requirements, with the flexibility to handle both innovative and generic APIs.

The digital transformation accelerated dramatically during this period. Syngene launched SynVent, Syngene's platform for fully integrated therapeutic discovery and development across large and small molecules. This wasn't just a marketing term—it was a comprehensive digital platform that integrated data from discovery through development, using artificial intelligence to identify patterns and accelerate decision-making.

The China-plus-one strategy that had been discussed during the IPO roadshow became urgent reality. Growing geopolitical tensions between the US and China, coupled with supply chain vulnerabilities exposed by COVID-19, led pharmaceutical companies to actively diversify their research and manufacturing partnerships. Syngene was perfectly positioned to capture this shift, with proven capabilities, Western-standard quality systems, and the English-language advantage.

In September 2022, Biocon divested 5.4% of its shares in Syngene International, reducing its stake to around 52.7%. This wasn't a vote of no confidence—Biocon needed capital for its own biosimilars ambitions—but it did mark another step in Syngene's journey toward complete independence. The market absorbed the shares without significant price impact, demonstrating institutional confidence in Syngene's standalone prospects.

The talent story reached new heights during this period. With a unique business model, a talent pool of 5656 scientists, scientific expertise across new therapeutic modalities, an experienced management team, and an independent Board committee, Syngene had built one of the largest concentrated pools of pharmaceutical research talent outside the US and Europe.

The financial performance reflected this operational excellence. Revenue: 3,727 Cr · Profit: 507 Cr as of the most recent data, with the company maintaining healthy margins despite significant expansion investments. The market capitalization of 26,537 Crore reflected investor confidence in the long-term strategy.

The regulatory achievements during this period were particularly noteworthy. The facility has been approved by the US FDA (with no 483 observations) and EMA. Receiving FDA approval with zero observations—essentially a perfect inspection—is extraordinarily rare in the pharmaceutical industry and speaks to the quality culture Syngene had built.

The expansion into new modalities represented a strategic bet on the future of medicine. Cell and gene therapies, oligonucleotides, PROTACs (Proteolysis Targeting Chimeras), and antibody-drug conjugates weren't just add-on capabilities—they required fundamentally different expertise and infrastructure. Syngene's investment in these areas positioned it for the next wave of pharmaceutical innovation.

The governance evolution continued with the publication of Syngene's first comprehensive ESG (Environmental, Social, and Governance) report. This wasn't just compliance—it reflected genuine commitment to sustainability, with initiatives ranging from renewable energy adoption to water recycling to community health programs. Major pharmaceutical companies were increasingly requiring ESG compliance from partners, and Syngene was ahead of the curve.

The recent developments in 2024-2025 showed no slowdown in ambition. Syngene's new biologics facility in the U.S. New site to increase Syngene's total single-use bioreactor capacity to 50,000 Liters. This marks Syngene's first major facility outside India, a bold step that brings it closer to its primary market and demonstrates confidence in competing directly with established Western CDMOs.

Looking at the current state of Syngene, several themes emerge. First, the company has successfully evolved from a services provider to a strategic partner, deeply embedded in clients' R&D operations. Second, it has proven that the dedicated center model can scale and adapt to different clients and modalities. Third, it has demonstrated that an emerging market company can meet and exceed developed market quality standards.

The challenges remain significant. Competition from Chinese CROs remains intense, with companies like WuXi AppTec having greater scale and resources. The concentration risk from dedicated centers—while mitigated by long-term contracts—remains a concern for investors. The need to continuously invest in new capabilities while maintaining margins requires careful balance.

Yet, Syngene's position as we enter 2025 is stronger than ever. It has 400+ active customers with engagements with 13 out of the top 15 global pharma companies. The combination of dedicated centers providing stable, long-term revenues and the growing fee-for-service business providing diversification creates a resilient business model.

As the pharmaceutical industry continues its transformation—driven by personalized medicine, artificial intelligence, and new therapeutic modalities—Syngene is positioned not just as a beneficiary but as an enabler of this change. The modern era has proven that Syngene's vision of becoming an integral part of global pharmaceutical innovation isn't just achievable—it's already reality.

VIII. Business Model & Competitive Advantages

To understand Syngene's business model, imagine a Swiss Army knife designed for pharmaceutical R&D. Each tool serves a specific purpose, but the real value lies in the integration—the ability to seamlessly move from one function to another without switching hands. This is the essence of Syngene's integrated CRDMO model, serving diverse end-user industries like Pharmaceuticals, Animal Health, Agrochemicals, Consumer Packaged Goods, Chemicals/Polymers.

The business operates through three distinct but synergistic models. First, the dedicated centers—the crown jewels that provide 40-45% of revenues through long-term contracts. Second, the Full-Time Equivalent (FTE) model, where clients essentially rent scientists and infrastructure for defined periods. Third, the Fee-for-Service (FFS) model for discrete projects with defined deliverables. This portfolio approach provides both stability and flexibility, allowing Syngene to serve everyone from cash-strapped biotechs to Big Pharma giants.

The numbers tell a story of scientific prowess: The company holds 400+ patents jointly with clients. But these aren't just paper filings—they represent genuine innovation, from novel synthetic routes that reduce manufacturing costs by 60% to analytical methods that detect impurities at parts-per-billion levels. Each patent is a testament to the collaborative innovation model that Syngene has perfected.

The competitive moat starts with scale. Total research & manufacturing infrastructure for the company is spread across 1.9 million square feet across locations. But square footage alone doesn't create competitive advantage—it's what happens within those walls. Syngene has created capability clusters where chemists, biologists, pharmacologists, and data scientists work in physical proximity, enabling the serendipitous interactions that often lead to breakthroughs.

Consider the integrated discovery platform. A client comes with a biological target for a disease. Syngene's biologists validate the target, chemists design molecules to hit it, DMPK scientists optimize the drug-like properties, toxicologists ensure safety, and process chemists develop scalable synthesis. All under one roof, all talking to each other, all aligned to a single goal. Competitors might offer pieces of this puzzle, but few can provide the complete picture.

The capital efficiency of the model is particularly elegant. Discovery services require relatively modest capital investment—analytical instruments, laboratory equipment, IT infrastructure. The real investment is in human capital, which scales linearly with revenue. Manufacturing, while more capital-intensive, provides higher margins and longer-term contracts. The combination creates a balanced portfolio that can generate 30%+ EBITDA margins while funding continuous capability expansion.

The risk-sharing models Syngene has developed deserve special attention. Traditional fee-for-service work puts all risk on the client—they pay whether the project succeeds or fails. Syngene increasingly offers success-based pricing, where payments are tied to achieving specific milestones. Some contracts even include royalties on eventual drug sales. This alignment of interests changes the dynamic from vendor-client to true partnership.

Let's examine the competitive landscape. WuXi AppTec, the Chinese giant, has greater scale with revenues exceeding $3 billion. But WuXi's model is more transactional, focused on volume and efficiency. Lonza and Samsung Biologics are formidable in manufacturing but lack Syngene's discovery capabilities. Covance (now part of LabCorp) is strong in clinical trials but weak in early discovery. Syngene's integrated model allows it to compete selectively, choosing battles where its unique capabilities provide advantage.

The talent model is a crucial differentiator. While competitors often struggle with 30-40% annual attrition in India, Syngene maintains single-digit attrition in critical roles. How? By creating career paths that don't exist elsewhere in India. A scientist can spend an entire career at Syngene, moving from bench research to project management to client engagement to scientific leadership, all while staying in Bangalore. The company invests 3-4% of revenues in training, far exceeding industry norms.

The information architecture Syngene has built is a hidden asset. Every experiment, every result, every decision is captured in integrated data systems. When a client asks, "Have you seen this problem before?" Syngene can search across thousands of projects (while maintaining confidentiality) to find relevant insights. This institutional memory becomes more valuable with each passing year, creating a compound competitive advantage.

Quality systems represent another moat. Syngene doesn't just meet regulatory requirements—it exceeds them. The company maintains certifications from FDA, EMA, PMDA, and other major regulators. But beyond certifications, it's the culture of quality that matters. Every scientist is trained to think about regulatory implications. Documentation is created with the assumption it will be audited. This quality-first mindset means clients don't have to worry about regulatory surprises.

The geographic advantage is multifaceted. India's time zone allows for follow-the-sun operations with US and European clients. The English-language proficiency enables seamless communication. The large pool of science graduates provides talent depth. The cost structure—while rising—still provides 40-50% savings versus Western alternatives. But Syngene has moved beyond cost arbitrage to capability arbitrage, offering skills and scale that clients can't build internally.

The network effects in Syngene's model are subtle but powerful. Each new client brings new challenges, forcing Syngene to develop new capabilities. These capabilities attract more clients, creating a virtuous cycle. The dedicated centers act as innovation labs, with learnings that benefit the broader organization. Knowledge flows both ways—from dedicated centers to fee-for-service and back—creating synergies that standalone providers can't match.

The platform approach extends to technology infrastructure. Syngene has invested heavily in digital systems that integrate laboratory information management, enterprise resource planning, and customer relationship management. This isn't just about efficiency—it's about creating switching costs. Once a client's systems are integrated with Syngene's, moving to another provider becomes expensive and risky.

Financial resilience is built into the model. Long-term contracts provide visibility—at any point, Syngene has 2-3 years of contracted revenues locked in. The diverse client base—400+ active customers—provides protection against client-specific risks. The mix of discovery and development services provides balance across the drug development cycle. Currency hedging protects against rupee fluctuations.

The innovation in business model extends to pricing. While competitors often compete on hourly rates or project costs, Syngene focuses on value delivered. A synthetic route that reduces manufacturing costs by millions is worth more than the hours spent developing it. An analytical method that accelerates regulatory approval is valued beyond the cost of development. This value-based pricing, while harder to sell, creates win-win outcomes.

Looking at returns on capital, Syngene's model shines. The company generates returns on equity exceeding 20% while maintaining conservative leverage. The asset-light discovery business funds the capital-intensive manufacturing business. The long-term contracts justify infrastructure investments. The result is a business that can self-fund growth while returning cash to shareholders.

The strategic options embedded in the business model provide flexibility for the future. Syngene could acquire specialized capabilities to fill portfolio gaps. It could expand geographically to be closer to clients. It could move up the value chain into drug development risk-sharing. It could leverage its platform for its own drug discovery. Each option creates potential upside without betting the company.

IX. Playbook: Business & Investing Lessons

The Syngene story offers a masterclass in building trust in an industry where trust is everything and skepticism is the default. When pharmaceutical companies entrust you with molecules that could be worth billions, with research that represents years of work, with secrets that competitors would kill to know, trust isn't just important—it's existential.

The first lesson: Trust is engineered, not assumed. Syngene didn't ask clients to trust them; they built systems that made trust inevitable. Physical separation between client projects. Digital firewalls between databases. Legal structures that aligned interests. When Bristol-Myers Squibb's executives could walk through BBRC and see their logo on lab coats, their processes on screens, their culture in action, trust followed naturally.

The second lesson: Long-term contracts change everything. Most businesses optimize for flexibility—short contracts, easy exits, minimal commitment. Syngene went the opposite direction, pursuing 7-10 year agreements that locked both parties into deep partnership. This wasn't just about revenue visibility—it was about creating the stability needed for genuine innovation. Scientists could pursue multi-year research programs. Investments in specialized equipment could be amortized. Relationships could deepen beyond transactional exchanges.

Consider the talent development philosophy: Invest in people like they'll stay forever, even if they won't. Syngene spends multiples of industry norms on training, sends scientists abroad for sabbaticals, funds PhD programs. The conventional wisdom says this is wasteful—why train people who might leave? But Syngene understood that investing in people creates a virtuous cycle. The best want to work where they'll grow. Those who stay become exponentially more valuable. Even those who leave become ambassadors, often in client organizations.

The approach to intellectual property reveals another insight: Shared success beats protected failure. Rather than fighting over IP ownership—a common source of CRO friction—Syngene embraced joint IP creation. 400+ patents jointly with clients means 400+ instances where both parties won. This abundance mindset, rather than zero-sum thinking, created possibilities that defensive positioning would have prevented.

The geographic arbitrage strategy offers a nuanced lesson: Start with cost advantage, but quickly move beyond it. Yes, Indian scientists cost less than American ones. But if that's your only advantage, you're vulnerable to the next low-cost location. Syngene used cost advantage to get in the door, then built capability advantages that made cost irrelevant. Today, clients work with Syngene not because it's cheaper, but because it's better at certain things.

The portfolio approach to risk deserves study: Diversification and concentration can coexist. Having three major dedicated centers creating 40%+ of revenue seems risky. But each center has a 7-10 year contract. Meanwhile, 400+ other clients provide diversification. It's like a barbell strategy—stability on one end, optionality on the other, avoiding the mediocre middle.

The quality philosophy illustrates the power of overcompliance as strategy. Syngene doesn't just meet FDA standards; it exceeds them. This isn't perfectionism—it's business strategy. When you consistently deliver perfect quality, clients stop auditing you as closely. Regulatory approvals come faster. Premium pricing becomes justifiable. The cost of excellence is less than the cost of adequacy plus the cost of failure.

The innovation model teaches us about leveraged learning. Every project Syngene undertakes adds to its knowledge base. But unlike a pharmaceutical company that might run 10 projects annually, Syngene runs hundreds. This creates a learning velocity that individual companies can't match. The key is creating systems to capture, codify, and redeploy these learnings without violating confidentiality.

The approach to competition reveals strategic clarity: Choose your battles based on unique advantages. Syngene doesn't try to compete with WuXi AppTec on scale or with Lonza on biologics manufacturing capacity. Instead, it focuses on integrated discovery and development where its model shines. This isn't weakness—it's focus.

For investors, several lessons emerge:

Look for businesses that benefit from industry structure changes, not just growth. The pharmaceutical industry's R&D productivity crisis isn't getting solved internally. The shift to externalized innovation isn't a trend—it's a structural transformation. Syngene benefits regardless of which drugs succeed or which companies thrive.

Switching costs can be subtle but powerful. It's not just the contract terms that lock in Syngene's clients. It's the integrated systems, the trained teams, the institutional knowledge, the trusted relationships. The cost of switching isn't just financial—it's organizational, temporal, and psychological.

Revenue quality matters more than revenue quantity. A 10-year contract with Bristol-Myers Squibb is worth more than equivalent revenue from multiple short-term projects. The predictability enables planning, investment, and capability building that creates compound advantages.

Management quality in emerging markets is not uniformly distributed. The difference between Syngene and median Indian CROs isn't just scale—it's sophistication. The ability to manage complex stakeholder relationships, navigate regulatory requirements, and maintain quality standards at scale is rare.

Regulatory compliance is a moat, not a cost. Every FDA approval, every successful audit, every year without quality issues raises the bar for competitors. In industries where failure can be catastrophic, proven reliability commands premium valuations.

The capital allocation lessons are instructive. Syngene has avoided the temptation of related diversification—no forays into hospitals or diagnostics or consumer health. Every investment strengthens the core CRDMO model. This discipline, rare in emerging market companies, creates compound returns.

The stakeholder management approach offers insights: Alignment beats control. Biocon's gradual reduction in stake, managed transparently and strategically, has been value-accretive for all parties. Employees with stock options think like owners. Clients with success-based contracts share in upside. This web of aligned interests creates resilience.

The crisis management during COVID-19 revealed organizational character: Culture is what happens when no one's watching. When scientists volunteered to live on campus for weeks, when teams worked around the clock to maintain client projects, when quality standards were maintained despite disruption—this wasn't policy, it was culture manifesting under pressure.

For entrepreneurs, the Syngene story teaches patience: Building trust takes decades; losing it takes moments. The 30-year journey from Biocon's founding to Syngene's current position wasn't linear. There were setbacks, pivots, and periods of doubt. But consistent execution against a clear vision eventually created unstoppable momentum.

The ultimate lesson might be about ambition: Emerging market companies can define global standards. Syngene didn't aspire to be "good for an Indian company." It aspired to be world-class, period. This ambition, backed by execution, created possibilities that constrained thinking would have prevented.

X. Analysis & Bear vs. Bull Case

The Bull Case: Structural Tailwinds and Competitive Positioning

The bull thesis for Syngene starts with an immutable fact: pharmaceutical R&D is becoming increasingly expensive and complex. The average cost to develop a new drug has reached $2.6 billion, with timelines stretching beyond a decade. No amount of internal efficiency can solve this productivity crisis—it requires fundamental restructuring of how drugs are discovered and developed.

Syngene sits at the intersection of two powerful trends. First, the externalization of pharmaceutical R&D, which has grown from 20% of spending in 2000 to nearly 50% today, heading toward 70% by 2030. Second, the shift from China dependency to a "China Plus One" strategy, accelerated by geopolitical tensions and supply chain vulnerabilities. With engagements with 13 out of the top 15 global pharma companies, Syngene has already won the trust battle that new entrants must fight.

The moat is wider than it appears. Those three dedicated centers—BBRC, SARC, and Baxter—represent 15+ years of relationship building that cannot be replicated quickly. The 2030 extension with Bristol Myers Squibb and 2026 extension with Amgen provide visibility that few businesses enjoy. At current run rates, that's over ₹5,000 crores of contracted revenue, not accounting for growth or new contracts.

The expansion into new modalities positions Syngene for the future of medicine. Cell and gene therapies, despite current challenges, represent the next frontier in treating genetic diseases and cancers. Oligonucleotides offer possibilities for previously undruggable targets. PROTACs could revolutionize how we think about protein regulation. Syngene's early investments in these areas create option value that's not reflected in current valuations.

The manufacturing expansion transforms Syngene's economics. Discovery services, while intellectually valuable, are essentially selling time. Manufacturing sells products with tangible margins. The Mangalore facility and expanded biologics capabilities could double Syngene's revenue potential without proportional increases in operating costs. The Zoetis contract alone—manufacturing Librela for 10 years—validates the commercial manufacturing strategy.

Valuation remains reasonable despite the growth. At current levels around ₹650 per share, Syngene trades at approximately 35x trailing earnings. For a company growing revenues at 15%+ annually with 30%+ EBITDA margins and significant operating leverage ahead, this multiple seems conservative compared to global CDMO peers trading at 40-50x earnings.

The talent advantage is sustainable and widening. 5656 scientists represents one of the largest concentrated pools of pharmaceutical research talent outside the US. With India producing 1.5 million STEM graduates annually versus 500,000 in the US, the talent pipeline remains robust. The cost advantage—Indian scientists at 30-40% of US costs—remains despite wage inflation.

The Bear Case: Concentration Risks and Competitive Threats

The bear thesis starts with an uncomfortable truth: Syngene's revenue concentration is significant. Three dedicated centers likely contribute 40-45% of revenues. If Bristol Myers Squibb decided not to renew in 2030, or if Amgen pulled back post-2026, the impact would be severe. While contracts provide protection, they're not ironclad—force majeure, change of control, or strategic shifts could trigger exits.

Chinese competition remains formidable and growing. WuXi AppTec, with revenues exceeding $3 billion versus Syngene's ~$500 million, has scale advantages that translate into capabilities. WuXi can invest more in technology, offer broader services, and absorb pricing pressure. While geopolitical tensions currently favor Syngene, these could reverse if US-China relations improve or if Chinese companies establish Western operations.

The margin structure faces multiple pressures. Wage inflation in India runs at 8-10% annually for skilled scientists, far exceeding developed market inflation. The rupee's depreciation provides some offset, but this isn't guaranteed to continue. New capability development requires continuous investment. Regulatory compliance costs only increase. The 30%+ EBITDA margins that investors have come to expect may not be sustainable.

Biocon's 52.7% ownership creates overhangs both real and perceived. Any stake sale would pressure the stock. Related party transactions, while disclosed and arm's length, create governance questions. The market constantly worries about conflicts of interest, whether Syngene gets the best projects or if Biocon gets preferential treatment. This ownership structure likely creates a 10-15% valuation discount.

The technology disruption risk is real and accelerating. Artificial intelligence and machine learning are revolutionizing drug discovery. Companies like Atomwise, BenevolentAI, and Recursion Pharmaceuticals are using AI to dramatically accelerate and reduce the cost of discovery. If these technologies mature, the need for armies of scientists running physical experiments could diminish significantly.

Customer bargaining power is increasing. As the CDMO industry matures and capacity expands globally, pharmaceutical companies have more options. The switching costs, while real, aren't insurmountable. A new generation of procurement executives, focused on cost reduction and supplier diversification, may be less willing to sign long-term, high-value contracts.

Execution risks multiply with expansion. Managing three dedicated centers was complex enough. Adding new facilities, new modalities, and new geographies increases operational complexity exponentially. The biologics facility in the US represents Syngene's first major international operation. Cultural integration, regulatory compliance, and operational excellence become harder to maintain at scale.

The valuation already embeds significant growth expectations. At 35x earnings and 5.5x book value, Syngene is priced for perfection. Any disappointment—a contract loss, margin compression, regulatory issues—could trigger significant multiple compression. The stock's 20% decline over the past year suggests market skepticism about growth sustainability.

The Verdict: Balancing Promise and Peril

The truth, as always, lies between extremes. Syngene is neither a guaranteed compounder nor a value trap. It's a high-quality business with genuine competitive advantages operating in an attractive industry, but facing real challenges that could constrain returns.

The structural tailwinds are undeniable. Pharmaceutical R&D externalization will continue because the alternative—maintaining massive internal organizations—is economically unviable. The China diversification trend has years to run. The shift to biologics and complex modalities favors integrated providers like Syngene.

But the risks are equally real. Revenue concentration, while managed through long-term contracts, creates vulnerability. Competition from larger, better-capitalized players will intensify. Margin pressures from wage inflation and investment needs could disappoint investors expecting continuous expansion.

For long-term investors, the key question isn't whether Syngene will face challenges—it will. The question is whether management's track record of navigating complexity, building trust, and delivering results will continue. The 30-year journey from Biocon's garage to a ₹26,000 crore enterprise suggests that betting against this team might be premature.

The appropriate stance might be cautious optimism with careful monitoring. Watch the contract renewals with Bristol Myers Squibb and Amgen as they approach. Monitor the success of the US biologics facility and Mangalore operations. Track employee attrition and wage inflation. Observe how new modalities contribute to revenue. Most importantly, watch whether Syngene can maintain its quality standards and client trust while scaling rapidly.

XI. Epilogue & Reflections

Standing at the entrance of Biocon Park in Bangalore today, watching thousands of scientists stream through the gates, it's hard to imagine this was once empty land on the city's outskirts, dismissed as too far from the talent pools of central Bangalore. Yet this physical transformation—from wasteland to one of Asia's largest biotechnology parks—mirrors a deeper transformation in how the world thinks about innovation, geography, and capability.

Syngene's story is, at its heart, a story about trust arbitrage. Not cost arbitrage, though that played a role. Not regulatory arbitrage, though navigating different systems required skill. But trust arbitrage—the gradual, painstaking process of convincing the world's most secretive industry to share its crown jewels with a company 8,000 miles away in a country known more for copying drugs than creating them.

The ripple effects extend far beyond Syngene's campus. Today, Bangalore hosts R&D centers for dozens of global pharmaceutical companies. Indian scientists who might have emigrated now have career options at home. Young students see pharmaceutical research as a viable career, not just a stepping stone. The ecosystem that Syngene helped create—combining talent, infrastructure, and credibility—has made India a serious player in global pharmaceutical innovation.

Consider what this means for the future of innovation itself. The traditional model assumed that cutting-edge research required proximity—to universities, to venture capital, to other researchers. Syngene proved that with the right systems, culture, and technology, innovation can happen anywhere. A molecule designed in Princeton can be synthesized in Bangalore, tested in Singapore, and manufactured in Mangalore, with seamless coordination that makes geography irrelevant.

The implications for emerging markets are profound. Syngene's success demonstrates that developing countries need not remain permanent suppliers of raw materials and cheap labor. With investment in education, infrastructure, and institutions, they can compete at the highest levels of value creation. The ₹26,000 crore valuation isn't just a number—it's validation that Indian companies can create and capture value in knowledge industries.

But perhaps the most important lesson is about time horizons. In an era of quarterly capitalism, where CEOs optimize for the next earnings call and investors flip stocks in microseconds, Syngene represents something almost anachronistic—a company built over decades, with contracts spanning decades, creating value that compounds over decades. The Bristol Myers Squibb relationship, now in its third decade, has created value that no quarterly optimization could have achieved.

The pharmaceutical industry's transformation is far from complete. Personalized medicine promises treatments tailored to individual genetics. Artificial intelligence could accelerate discovery by orders of magnitude. Gene editing might cure diseases rather than just treat them. Each transformation creates opportunities for companies like Syngene that can adapt, learn, and scale.

Yet challenges loom equally large. Healthcare costs are becoming unsustainable globally. Drug pricing pressures will flow through to R&D spending. Regulatory requirements grow ever more complex. Competition from new geographies and new technologies intensifies. Navigating these challenges while maintaining growth and margins will test even the best management teams.

What would Kiran Mazumdar-Shaw, starting Biocon in that garage in 1978, make of what Syngene has become? Would she recognize the company that now employs more scientists than most universities, holds more patents than many pharmaceutical companies, and partners with the world's largest healthcare companies? The entrepreneurial spirit remains, but the scale of ambition has expanded beyond what seemed possible in those early days.

The Syngene story also raises uncomfortable questions about global inequality. The same scientist doing the same work gets paid three times more in Boston than Bangalore. Is this sustainable? Fair? As Indian scientists gain experience and confidence, will they demand global wages? And if they do, what happens to the business model that depends on this arbitrage?

Looking ahead, Syngene faces strategic choices that will define its next chapter. Should it remain purely a services company, or use its capabilities to develop its own drugs? Should it expand globally through acquisitions, or focus on organic growth? Should it maintain independence, or consider strategic partnerships? Each path offers opportunities and risks that will shape not just Syngene's future but the future of the global pharmaceutical industry.

The personal stories within Syngene deserve their own telling. The scientist who joined fresh from university and now leads a team of hundreds. The security guard who studied at night and became a laboratory technician. The CEO who gave up a lucrative career in the West to build something in India. These individual journeys, multiplied thousands of times, create the human fabric that makes Syngene more than just a company.

For investors, Syngene represents a fascinating case study in value creation. Not the explosive, venture-style returns of a software startup, but the steady, compound growth of a business with genuine competitive advantages. The stock price journey—from ₹250 at IPO to current levels around ₹650—masks the volatility and doubts along the way. Long-term holders have been rewarded, but the path required patience and conviction.

The broader lesson for India might be the most important. In a country often criticized for red tape, corruption, and infrastructure challenges, Syngene proves that world-class companies can be built. Not by copying Western models, but by creating uniquely Indian solutions to global problems. The jugaad spirit—innovative problem-solving with limited resources—scaled up to enterprise level.

As we conclude this journey through Syngene's history, from a Biocon subsidiary to a global pharmaceutical partner, one thing becomes clear: this is not an ending but a checkpoint in an ongoing story. The contracts extending to 2030, the facilities under construction, the capabilities being developed—all point to a company still in growth mode, still evolving, still pushing boundaries.

The ultimate judgment of Syngene's success won't come from stock prices or financial metrics. It will come from the drugs developed in its laboratories that save lives, from the diseases cured through its research, from the next generation of scientists it inspires. In an industry where success is measured in lives saved and suffering reduced, Syngene has earned its place at the table—not as an outsourcing destination, but as a true partner in humanity's ongoing battle against disease.

The story that began in a garage in Bangalore has become a global story, an Indian story, a human story. And it's far from over.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube