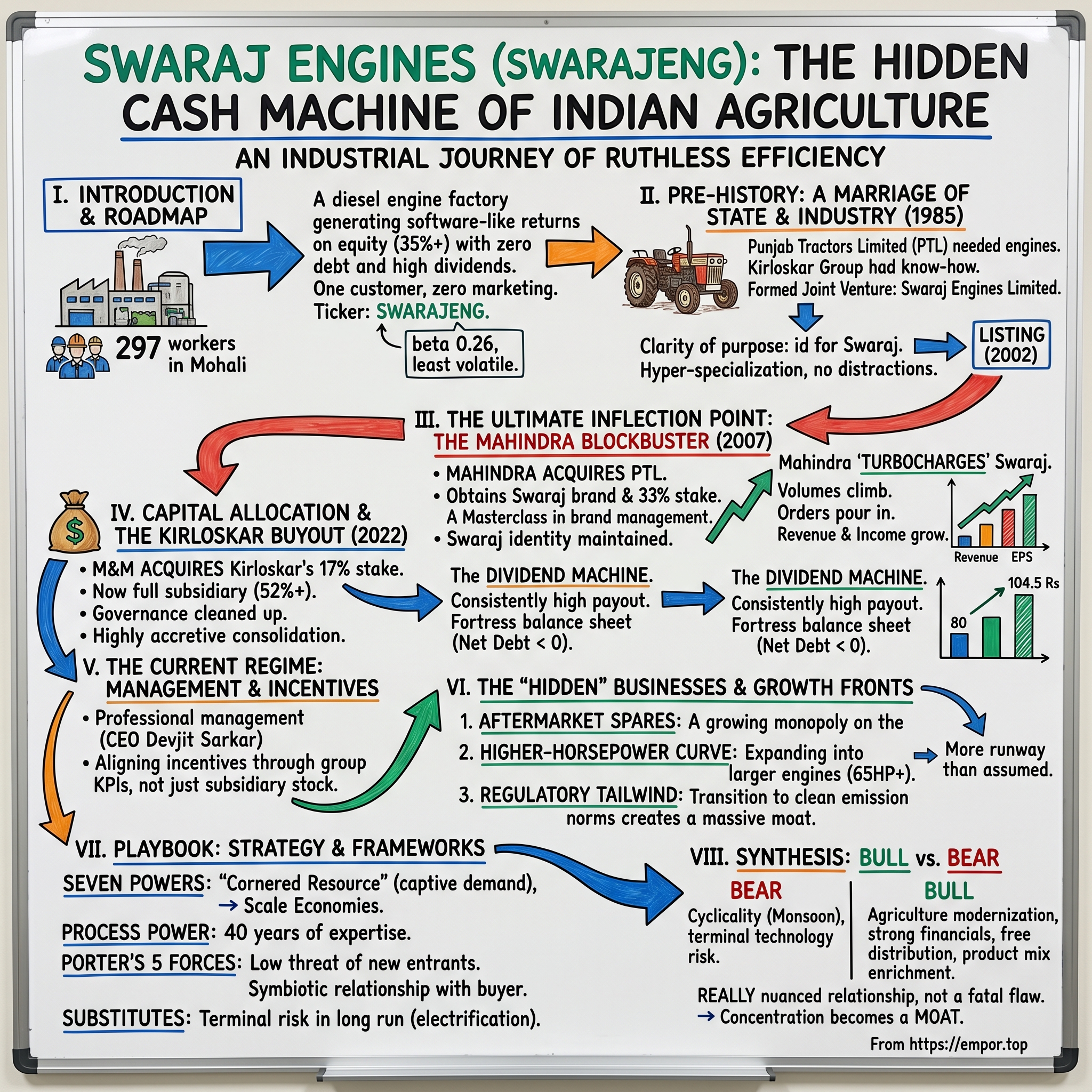

Swaraj Engines: The Hidden Cash Machine of Indian Agriculture

I. Introduction and Episode Roadmap

Picture a factory floor in Mohali, Punjab. It is not glamorous. There are no sleek robots assembling smartphones, no venture capitalists snapping selfies for LinkedIn. Just 297 employees, working methodically on diesel engine blocks destined for the fields of India's agricultural heartland. The company behind this factory, Swaraj Engines Limited, does not advertise on television. It does not have a consumer brand. It does not even have a second major customer. And yet, it routinely generates returns on equity north of thirty-five percent, operates with essentially zero debt, and pays out the vast majority of its profits as dividends to shareholders. In a country obsessed with flashy tech IPOs and consumer internet darlings, Swaraj Engines is the kind of business that makes value investors quietly smile.

So how does a company with essentially one major customer, zero consumer marketing budget, and a single core product become one of the most ruthlessly efficient, cash-generating industrial assets in India? That is the question at the heart of this story.

Swaraj Engines Limited, listed on the National Stock Exchange under the ticker SWARAJENG, manufactures diesel engines, engine components, and spare parts for tractors. Specifically, it builds the engines that go into Mahindra's Swaraj-branded tractors, one of the most recognized names in Indian farming. The company was incorporated in 1985 and is headquartered in Mohali, in the state of Punjab. As of early 2026, it trades at roughly three thousand five hundred rupees per share with a market capitalization of approximately four thousand two hundred crore rupees, employs fewer than three hundred people, and carries a beta of just 0.26, making it one of the least volatile stocks on the Indian exchange.

This is the story of how a sleepy 1980s state-backed joint venture got swept up in one of the most important acquisitions in Indian automotive history, how it achieves software-like returns on equity in heavy manufacturing, and why its parent company recently decided to buy out its original partners. We will trace the arc from a provincial engine shop to a subsidiary of one of India's largest conglomerates, examine the financial mechanics that make this business so unusual, and ask the question that every long-term investor must eventually confront: how long can a diesel engine manufacturer remain relevant in a world that is slowly electrifying?

II. The Pre-History: A Marriage of State and Industry (1985)

To understand Swaraj Engines, you first need to understand the peculiar world of Indian tractor manufacturing in the 1970s and 1980s. India was still largely a command economy. Industrial licenses dictated who could manufacture what. And agriculture, which employed the overwhelming majority of the population, was mechanizing at a pace that was simultaneously too slow for the country's ambitions and too fast for its supply chains.

In this environment, the state government of Punjab decided it needed its own tractor brand. Punjab was, and remains, India's breadbasket. The Green Revolution of the 1960s and 1970s had transformed its wheat and rice yields, but mechanization lagged behind. Farmers needed affordable, rugged tractors suited to the specific soil and crop conditions of Northern India. The result was Punjab Tractors Limited, or PTL, which gave birth to the "Swaraj" tractor brand. The name itself, meaning "self-rule" in Hindi, carried echoes of India's independence movement. It was a deliberate choice, a brand that spoke of self-reliance and national pride, resonating deeply with the Punjabi farming community.

PTL could build tractor chassis, transmissions, and the surrounding mechanicals. But engines are a different beast entirely. A tractor engine is not simply a smaller version of a car engine. It must produce enormous torque at low RPMs, operate for thousands of hours in dusty, hot conditions, run on sometimes-adulterated diesel fuel, and be simple enough for a village mechanic to repair with basic tools. Building a reliable tractor engine requires deep metallurgical expertise, precision machining capabilities, and years of iterative testing. PTL did not have this capability in-house.

Enter the Kirloskar Group. The Kirloskar family has been building engines and industrial equipment in India since 1888. Kirloskar Oil Engines Limited, or KOEL, was one of the country's premier diesel engine manufacturers. In 1985, PTL and KOEL formed a joint venture: Swaraj Engines Limited. The partnership was elegant in its simplicity. Kirloskar brought the engineering know-how and manufacturing blueprints. PTL brought the guaranteed customer. From its very first day, Swaraj Engines was built to do exactly one thing: manufacture diesel engines for Swaraj tractors.

This hyper-specialization might seem like a weakness, and in many business strategy textbooks, it would be flagged as dangerous concentration risk. But in practice, it gave Swaraj Engines something invaluable: clarity of purpose. There were no distracting product lines, no empire-building acquisitions, no expensive forays into adjacent markets. Every rupee of capital expenditure, every hour of engineering time, every process improvement on the factory floor was directed toward making better, cheaper diesel engines for one buyer. The factory was set up in Mohali, just outside Chandigarh, strategically close to PTL's tractor assembly plants to minimize logistics costs and enable just-in-time delivery.

For two decades, Swaraj Engines quietly hummed along in this arrangement. It was not a particularly exciting business. PTL was a regional tractor brand, strong in Punjab and Haryana but without the national scale of Mahindra or TAFE. Swaraj Engines grew as Swaraj tractors grew, which was steadily but not spectacularly. The company went public in 2002, listing on the NSE, but remained largely under the radar of mainstream investors. And then, in 2007, everything changed.

III. The Ultimate Inflection Point: The Mahindra Blockbuster (2007)

To appreciate the magnitude of what happened in 2007, you need to understand the competitive landscape of Indian tractor manufacturing in the mid-2000s. India is the largest tractor market in the world by volume, not by a small margin, but by a landslide. Indian farmers buy more tractors annually than the United States, Europe, and China combined. The reasons are structural: Indian farms are small, fragmented, and labor-intensive, making compact tractors essential. And the market was, and remains, dominated by a handful of players: Mahindra and Mahindra, TAFE (which licenses Massey Ferguson technology), Escorts, and Swaraj.

Mahindra and Mahindra, commonly known as M&M, had been locked in a fierce battle to become the undisputed king of Indian farm equipment. Under the leadership of Anand Mahindra, the group was executing an ambitious strategy to dominate not just the domestic market but to become a global force. They had already partnered with international players and were eyeing every possible avenue for growth.

Then Punjab Tractors went up for sale.

The details of the PTL acquisition are worth lingering on because they illuminate how M&M thinks about competitive strategy. PTL was not just any tractor company. It had something that money alone cannot easily buy: ferocious brand loyalty in Northern India. Swaraj tractors were not merely agricultural equipment in Punjab; they were cultural artifacts. Farmers passed down their Swaraj tractors through generations. Village mechanics knew every bolt and bearing. The brand had an emotional resonance that no amount of advertising could replicate.

In 2007, M&M acquired Punjab Tractors Limited. The transaction gave Mahindra control of the Swaraj tractor brand and, almost as a side effect, PTL's approximately thirty-three percent stake in Swaraj Engines. Consider the narrative drama from Swaraj Engines' perspective. Overnight, your biggest rival's parent company becomes both your largest shareholder and your sole customer. The anxiety in the Mohali factory must have been palpable. Would Mahindra shut down the Swaraj brand and fold everything into its own tractor line? Would they bring engine manufacturing in-house? Would they squeeze Swaraj Engines on pricing until margins evaporated?

What Mahindra did instead was a masterclass in brand management, and it fundamentally altered the trajectory of Swaraj Engines. M&M recognized that the Swaraj brand was worth more alive than dead. Rather than cannibalizing it, they maintained the Swaraj identity as a distinct brand within the Mahindra portfolio, similar to how Volkswagen Group operates Audi and Skoda as separate brands targeting different segments. Swaraj continued to serve the value-conscious farmer in Northern India, while Mahindra's own-branded tractors targeted different geographies and price points.

But here is where it gets interesting for Swaraj Engines. Mahindra did not just maintain the Swaraj brand; it turbocharged it. M&M poured capital into Swaraj Tractors' manufacturing capacity, expanded its dealer network, and invested in new model development. The distribution muscle of India's largest tractor manufacturer was now behind a brand that previously had regional reach. Swaraj tractors started appearing in states where they had never been sold before. Sales volumes climbed steadily.

And every single one of those new tractors needed an engine from the factory in Mohali.

This is the beautiful flywheel that the 2007 acquisition created. Mahindra's investment in the Swaraj brand drove tractor volumes higher. Higher tractor volumes meant more engine orders for Swaraj Engines. More engine orders meant better capacity utilization, lower per-unit costs, and expanding margins. And because Swaraj Engines required minimal capital expenditure (it was not building the tractor, just the engine), the incremental revenue dropped almost directly to the bottom line and then flowed out as dividends. Swaraj Engines went from supplying a regional player to riding the slipstream of a global agricultural juggernaut.

The financial evidence is striking. In the years following the Mahindra acquisition, Swaraj Engines' revenue grew from a few hundred crore rupees to over sixteen hundred crore by fiscal year 2025. Net income followed a similar trajectory, climbing from approximately ninety-two crore in fiscal 2021 to one hundred sixty-six crore in fiscal 2025. Earnings per share rose from seventy-six rupees to nearly one hundred thirty-seven rupees over the same period. And the stock price, which had languished in the hundreds for years, climbed past three thousand five hundred rupees. The 2007 acquisition was not just a corporate event; it was the gravitational force that reshaped Swaraj Engines' entire orbit.

IV. Capital Allocation and The Kirloskar Buyout (2022)

For fifteen years after the Mahindra acquisition of PTL, Swaraj Engines operated with what can only be described as an awkward cap table. Mahindra and Mahindra held roughly thirty-four percent of the shares, inherited from the PTL deal. Kirloskar Oil Engines still held approximately seventeen percent, a legacy of the original 1985 joint venture. The remaining shares floated with public investors. It was functional but messy. Two industrial groups with different strategic priorities co-owned a company that was operationally tied to only one of them.

The tension was subtle but real. Kirloskar had no operational role in Swaraj Engines' business. It was not providing technology, customers, or management expertise. It was simply collecting dividends on a legacy investment. For M&M, the situation was similarly suboptimal. They controlled the customer relationship and the product roadmap, but they did not have majority ownership of a key supplier, which created governance complexities and limited their ability to fully integrate Swaraj Engines into the Mahindra supply chain.

In September 2022, Mahindra made its move. M&M acquired Kirloskar's entire seventeen-and-a-half percent stake for approximately two hundred ninety-six crore rupees, at a price of roughly fourteen hundred rupees per share. The transaction pushed Mahindra's ownership past fifty-two percent, transforming Swaraj Engines from an associate company to a full subsidiary.

The price Mahindra paid deserves scrutiny because it reveals how shrewd their capital allocation team is. At fourteen hundred rupees per share, M&M was acquiring additional ownership in a debt-free company generating returns on equity above thirty-five percent at roughly fifteen times earnings. For context, comparable industrial companies in India and globally were trading at twenty-five to thirty times earnings at the time, often with significantly lower capital efficiency and carrying real debt on their balance sheets. It was not a hostile takeover or a splashy headline deal. It was a quiet, precisely timed, highly accretive consolidation executed just ahead of what turned out to be an agricultural upcycle. Mahindra essentially bought more of a proven cash machine at a discount.

The buyout also cleaned up the governance structure. With majority ownership, M&M could now fully align Swaraj Engines' strategic decisions with its own tractor division's roadmap, coordinate capital expenditure timing, and streamline intercompany pricing. The awkward three-way dance between Mahindra, Kirloskar, and public shareholders was simplified to a straightforward parent-subsidiary relationship.

What makes Swaraj Engines' capital allocation story even more compelling is what the company does with its own cash. In a world where industrial companies routinely embark on ambitious diversification programs, building new factories, acquiring competitors, or entering adjacent markets, Swaraj Engines does essentially none of that. Because it relies on Mahindra for R&D direction, product roadmap decisions, and distribution, Swaraj Engines requires minimal capital expenditure relative to its revenue. Capex-to-revenue has consistently hovered between one and three percent, a figure that would make a software company jealous.

The result is a dividend machine. In fiscal 2022, the company paid eighty rupees per share. By fiscal 2025, that had climbed to one hundred four rupees and fifty paise. The payout ratio consistently sits between seventy and eighty percent of earnings. For a manufacturing company, this is extraordinary. Most industrial businesses retain a substantial portion of their earnings to fund growth, replace aging equipment, or build war chests for acquisitions. Swaraj Engines, by contrast, distributes nearly everything it earns because there is simply no productive internal use for the cash. The factory runs, the engines ship, the money flows back to shareholders. Zero empire-building, maximum capital return.

The balance sheet reinforces this picture. As of fiscal 2025, Swaraj Engines carried total equity of approximately four hundred nineteen crore rupees against total assets of six hundred seventy-two crore. It held short-term investments and cash of roughly one hundred eighty-seven crore, with virtually zero long-term debt. Net debt was negative by over one hundred seventy crore rupees. The current ratio was nearly two, indicating abundant liquidity. This is a fortress balance sheet attached to a business that generates nearly forty percent returns on equity. It is, by any definition, a compounding machine.

V. The Current Regime: Management and Incentives

There is no "founder CEO" story at Swaraj Engines. No visionary entrepreneur burning the midnight oil in a garage. This is a professionally managed Mahindra subsidiary, and understanding its management structure is essential to understanding how the business actually operates day to day.

Devjit Sarkar took over as CEO and Whole-Time Director in late 2024. His background is deeply embedded in the Mahindra tractor ecosystem. With more than thirty-six years of industry experience, Sarkar previously ran Mahindra's tractor operations in Turkey, a role that required navigating a completely different regulatory environment, managing export-quality manufacturing standards, and operating in a market where Mahindra competes against established European tractor brands. That international exposure is significant because it suggests Mahindra selected a leader who understands not just the Indian agricultural equipment market but global manufacturing standards and competitive dynamics.

Sarkar's compensation is modest by any standard. His annual pay stands at approximately eighty lakh rupees, a figure that would barely register as a rounding error at a comparable Western industrial company. More notably, he holds zero percent of Swaraj Engines' shares. This is a hallmark of Mahindra's modern corporate governance model. Executive incentives at subsidiary companies are not driven by direct equity concentration in the subsidiary itself. Instead, they are structured around operational KPIs: engine output targets, defect rates, margin defense, capacity utilization. The broader incentive alignment comes through group-level ESOPs in Mahindra and Mahindra, which tie subsidiary executives' fortunes to the overall performance of the Mahindra conglomerate rather than the specific stock price of the subsidiary.

This structure has both advantages and risks that investors should understand. On the positive side, it prevents the kind of short-term stock price manipulation that can occur when CEOs hold large personal positions. It also ensures that subsidiary management decisions are aligned with the parent's strategic interests, not with inflating the subsidiary's standalone valuation. On the risk side, there is a legitimate question about whether a CEO with no equity stake in the specific company has the same intensity of focus as a founder-operator. Mahindra mitigates this through tight board oversight and clear operational mandates.

The board itself reflects this principal-agent architecture. It is chaired by Rajya Vardhan Kanoria, an independent director, which provides at least formal separation between the controlling shareholder and the governance structure. Heavy-hitting M&M executives, including Harish Chavan, who heads the Swaraj division at the group level, sit on the board and ensure tight strategic alignment between the parent buyer and the subsidiary supplier. The CFO, Mahesh Gupta, manages the financial operations, while Mukesh Bansal serves as General Manager of Manufacturing and Plant Head, the person who ensures the Mohali factory runs at peak efficiency.

The lean management structure mirrors the lean organization. With fewer than three hundred employees total, Swaraj Engines has one of the highest revenue-per-employee ratios in Indian manufacturing. There are no sprawling corporate offices, no layers of middle management, no bloated overhead. It is a factory operation managed with the discipline of a private equity portfolio company, which in a sense, is exactly what it is, except the "private equity firm" happens to be one of India's largest industrial conglomerates.

For investors, the key question about management is not whether these are brilliant visionary leaders. It is whether they can execute a narrow operational mandate with discipline and consistency. And on that metric, the track record is compelling. Under successive Mahindra-appointed leaders, Swaraj Engines has maintained operating margins in the range of twelve to eighteen percent, kept capex disciplined, and delivered consistent dividend growth. The management machine works.

VI. The "Hidden" Businesses and Growth Frontiers

If you only look at Swaraj Engines' headline revenue number and assume it is a simple story of "build engines, sell to Mahindra," you are missing several important dimensions of value creation that are quietly reshaping the company's economics.

The first, and perhaps most significant, is the aftermarket spare parts business. Think about the installed base mathematics. Every Swaraj tractor sold in the last twenty years is still, in all likelihood, operational somewhere in India's countryside. Indian farmers do not discard tractors the way consumers discard smartphones. A well-maintained Swaraj tractor can run for decades. And every one of those tractors periodically needs engine components: pistons, rings, cylinder liners, gaskets, fuel injection parts. These replacement parts must come from Swaraj Engines because aftermarket compatibility and quality assurance demand OEM-sourced components. The village mechanic does not trust random third-party parts when an engine failure during harvest season can mean financial ruin.

This creates a spares monopoly that grows automatically as the installed base expands. Each new tractor sold is not just a one-time engine sale; it is the beginning of a multi-decade stream of high-margin parts revenue. The margin structure on spare parts dramatically outpaces OEM engine sales because the manufacturing cost of individual components is relatively low while the pricing power is significant, farmers will pay a premium for genuine parts that protect their livelihood. This dynamic is invisible in the top-line revenue number but is a meaningful driver of profitability.

The second growth frontier is the migration up the horsepower curve. Historically, Swaraj Engines was known for producing engines in the twenty to fifty horsepower range, the workhorses of small and medium Indian farms. But Indian agriculture is evolving. Farm consolidation, government subsidies for mechanization, and the introduction of more sophisticated farming techniques are driving demand toward higher-horsepower tractors, machines in the sixty-five horsepower and above category that can handle heavy-duty implements, commercial transportation, and larger acreage.

Higher-horsepower engines are not simply scaled-up versions of smaller ones. They require different metallurgy to handle increased combustion pressures, more sophisticated fuel injection systems, enhanced cooling architectures, and tighter tolerances. They are also significantly higher margin products because the engineering complexity and material costs create real barriers for competitors attempting to replicate them. Swaraj Engines' quiet expansion of its R&D capabilities into these higher-horsepower segments, coordinated with Mahindra's new tractor model launches in premium categories, represents a meaningful margin expansion opportunity.

The third dimension, and arguably the most important for the medium term, is the regulatory tailwind created by India's new tractor emission norms. India is progressively enforcing TREM (Tractor Emission) standards, moving from TREM Stage III-A toward Stage IV and eventually Stage V. For non-technical readers, this is essentially the same trajectory that European and American car engines went through over the past two decades, moving from simple mechanical fuel injection to electronically controlled, cleaner-burning systems.

This transition is a massive moat-builder for Swaraj Engines. The shift from mechanical injection to electronic common-rail injection systems transforms a tractor engine from a relatively simple mechanical device into a sophisticated electromechanical system with sensors, electronic control units, exhaust after-treatment devices, and calibrated software. The engineering investment required to develop TREM IV and V compliant engines is substantial, and the testing and certification timelines are lengthy. For any potential new entrant, this regulatory hurdle effectively raises the cost of competing with established players like Swaraj Engines by an order of magnitude.

Swaraj Engines has already navigated earlier emission transitions successfully, and its R&D infrastructure, much of it coordinated with Mahindra's central engineering resources, positions it well for the next round. Each regulatory tightening increases the technology content per engine, which in turn increases the average selling price and margin potential. The irony is beautiful: environmental regulation, which many view as a cost burden, actually strengthens the competitive position of incumbents in markets with high certification barriers.

These three dynamics, growing spares revenue, higher-HP engine migration, and emission norm upgrades, collectively suggest that Swaraj Engines' revenue and margin trajectory has more runway than the simplistic "commodity engine maker" narrative implies.

VII. Playbook: Strategy and Frameworks

To truly understand Swaraj Engines' competitive position, it helps to run the business through established strategic frameworks. The conclusions are unusually clear for an industrial company.

Start with Hamilton Helmer's Seven Powers. The most relevant power here is what Helmer calls a "cornered resource." Swaraj Engines has guaranteed, captive demand from Mahindra's Swaraj tractor division. Its Customer Acquisition Cost is literally zero. The company does not need a sales team, does not run marketing campaigns, does not bid for contracts. The orders flow because the parent company directs them. In most industries, cornered resources refer to patents, proprietary technology, or exclusive talent. Here, the cornered resource is the customer relationship itself, embedded in the ownership structure.

Scale economies further reinforce the position. By producing a narrow range of engine variants at high volume for a single buyer, Swaraj Engines achieves per-unit economics that no competitor could replicate without equivalent scale. The factory in Mohali is optimized for a specific set of engine platforms. There is no wasted capacity serving diverse customers with different specifications. Every production line, every quality control process, every inventory management system is tuned for maximum throughput on a limited product range. This operational focus yields fixed asset turnover ratios above fourteen times, a figure that many industrial companies would consider aspirational.

Process power, another of Helmer's categories, also applies. Decades of producing the same product family have created institutional knowledge that is difficult to replicate. The workforce knows the tolerances, the material suppliers are long-established, and the quality systems have been refined through millions of engine hours of field data. This is not the kind of advantage that appears in a patent filing. It lives in the accumulated expertise of shop floor teams and in the muscle memory of an organization that has been doing one thing, and doing it well, for over forty years.

Now consider Porter's Five Forces, and the analysis reveals an interesting paradox. Buyer power is, on paper, extreme. Mahindra accounts for virtually all of Swaraj Engines' revenue. In a typical buyer-supplier relationship, this level of concentration would be catastrophic for the supplier. The buyer could squeeze pricing, demand unfavorable payment terms, or threaten to shift volumes to an alternative supplier. But the Swaraj Engines situation inverts this dynamic because the buyer owns the supplier. M&M has no incentive to destroy margins at Swaraj Engines because those margins ultimately flow back to M&M through dividends and consolidated earnings. The relationship is symbiotic rather than extractive. Mahindra wants Swaraj Engines to be healthy and profitable because a healthy supplier ensures consistent engine quality and reliable delivery.

The threat of new entrants is minimal. The combination of scale requirements, emission certification barriers, established supplier relationships, and the captive customer dynamic creates a moat that no rational competitor would attempt to breach. No new entrant could achieve the volume necessary to out-price Swaraj Engines for Mahindra's business, and no independent engine manufacturer would invest in dedicated capacity for a customer it could never win.

Supplier power is moderate. Swaraj Engines sources raw materials like cast iron, steel, and aluminum from multiple vendors, which limits any single supplier's leverage. The company's consistent ordering patterns and long-term relationships provide some negotiating advantage, though commodity price fluctuations remain a margin variable.

The most important competitive force to watch is the threat of substitutes, and this is where the long-term bear case lives. Electric vehicle technology is gradually making its way into agricultural equipment. Several global manufacturers, including John Deere and Monarch Tractor, are developing electric and autonomous tractors. For now, the physics of heavy agricultural work creates a natural defense for diesel: battery energy density is insufficient for the sustained, high-torque demands of plowing, harvesting, and hauling across large fields. Charging infrastructure in rural India is essentially nonexistent. And the total cost of ownership for an electric tractor remains prohibitive for Indian farmers.

But "safe for now" is not the same as "safe forever." The trajectory of battery technology is relentless, and the fifteen-to-twenty-year horizon is genuinely uncertain for diesel engine manufacturers. This does not make Swaraj Engines a bad investment today, but it does mean that the terminal value assumptions embedded in any long-term valuation model deserve careful thought.

VIII. Bull vs. Bear Case and Final Synthesis

The bear case for Swaraj Engines is straightforward and honest. Start with the concentration risk: the company's revenue is almost entirely dependent on a single customer, which in turn is dependent on the Indian monsoon cycle. A bad monsoon means poor harvests, which means farmers defer tractor purchases, which means Swaraj Engines' order book thins out. This is not theoretical. The revenue flatness between fiscal 2023 and fiscal 2024, when revenue hovered around fourteen hundred twenty crore both years, illustrates how agricultural cyclicality directly impacts this business.

Beyond cyclicality, there is the terminal risk. Diesel engines are a nineteenth-century technology being asked to remain relevant in a twenty-first-century world. Rural electrification in India is accelerating. Government policy is increasingly favoring clean energy. While EV tractors remain years away from mass adoption in India, the directional trend is clear. The specific timeline is debatable, but the destination is not. At some point, measured in decades rather than years, the demand for new diesel tractor engines will structurally decline.

There is also a governance risk inherent in the parent-subsidiary structure. Minority shareholders in Swaraj Engines are, in a sense, along for the ride on whatever Mahindra decides. If M&M chose to internalize engine manufacturing, restructure intercompany pricing, or delist the subsidiary, public shareholders would have limited recourse. Mahindra's track record as a parent has been benign, even generous through the high dividend policy, but investors are fundamentally trusting the continued goodwill of the controlling shareholder.

The bull case rests on several structural pillars. India's agricultural mechanization remains profoundly underpenetrated compared to developed economies and even compared to China. The number of tractors per thousand hectares of arable land in India is a fraction of what it is in the United States or Europe. As Indian agriculture continues to modernize, driven by government subsidies, rural credit expansion, and the simple economics of replacing human labor with machines, the demand for tractors has a long secular growth runway. And every new tractor needs an engine.

The financial characteristics of the business are genuinely exceptional. A return on equity consistently above thirty-five percent, achieved in heavy manufacturing with zero leverage, is extraordinarily rare. For comparison, most global industrial companies are thrilled with returns on equity in the mid-teens, and they typically use significant debt to get there. Swaraj Engines generates these returns on an unlevered basis, meaning the underlying business economics are even more impressive than the headline ROE suggests.

The dividend growth trajectory is equally compelling. From fifteen rupees per share in fiscal 2020 to one hundred four rupees in fiscal 2025, dividends have compounded at a rate that transforms Swaraj Engines into a legitimate income investment alongside its capital appreciation potential. For long-term investors who reinvest dividends, the effective compounding is substantial.

The high-HP migration and emission norm upgrades provide a pricing and margin tailwind that the market may be underappreciating. Each regulatory transition increases the value-add per engine, raising the average selling price without requiring proportionally higher input costs. The spare parts annuity continues to build as the installed base grows. And the Mahindra ecosystem provides a growth engine that Swaraj Engines does not need to pay for, essentially getting free distribution and R&D leverage from its parent.

When evaluating this company on an ongoing basis, two KPIs matter more than anything else. The first is engine volume throughput, measured as the number of engines shipped per quarter. This single metric captures the health of the underlying tractor market, the strength of the Swaraj brand relative to competitors, and the factory's operational execution. The second is operating margin, which signals whether the company is maintaining pricing discipline against input cost fluctuations and whether the mix shift toward higher-HP engines and spare parts is flowing through to profitability. Revenue alone can be misleading because it blends price and volume; margin tells you whether the economic model is intact.

Myth versus reality. The consensus narrative on Swaraj Engines is that it is "just a captive supplier with no growth optionality." The reality is more nuanced. Yes, customer concentration is real and permanent. But the captive relationship, precisely because the buyer and supplier are aligned through ownership, eliminates the most dangerous risk that a concentrated supplier normally faces: the risk of being replaced. No competitor can take this business away. The growth optionality lies not in customer diversification but in product mix enrichment, aftermarket expansion, and the structural growth of Indian tractor demand. The myth treats single-customer dependency as a fatal flaw. The reality is that when the customer owns you and wants you to succeed, concentration becomes a moat rather than a vulnerability.

Swaraj Engines is a masterclass in staying in your lane. By not trying to be everything to everyone, and by deeply integrating with a dominant parent, the company has engineered one of the most profitable industrial positions in emerging markets. The factory in Mohali will not make headlines. The stock will not be the subject of breathless CNBC segments. But for investors who appreciate the beauty of a relentlessly efficient, capital-light, cash-generating industrial compounder, few businesses in India tell a more compelling story. The only question is how many decades the diesel chapter has left to run, and whether the characters in Mohali can write a new one when the time comes.

IX. Outro and Essential Reading

The story of Swaraj Engines sits at the intersection of several of the most important themes in Indian industrial history: the transition from state-led manufacturing to private sector dynamism, the rise of Mahindra as a global farm equipment powerhouse, and the ongoing mechanization of the world's most populous agricultural economy.

For those who want to go deeper, the essential starting points are Swaraj Engines' annual reports, which are refreshingly straightforward for an Indian industrial company. The 2022 annual report, in particular, contains detailed commentary on the Kirloskar stake acquisition and the strategic rationale behind the subsidiary consolidation. The Mahindra and Mahindra 2007 annual report provides invaluable context on the Punjab Tractors acquisition, a deal that reshaped the Indian tractor landscape. For broader context on Indian agricultural mechanization trends, the reports published by the Tractor and Mechanization Association of India offer granular data on state-level tractor penetration and demand forecasting. And for anyone interested in the emission norm transition, the Central Pollution Control Board's TREM stage implementation timeline documents are worth reviewing to understand the regulatory cadence that will shape engine technology requirements over the next decade.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube