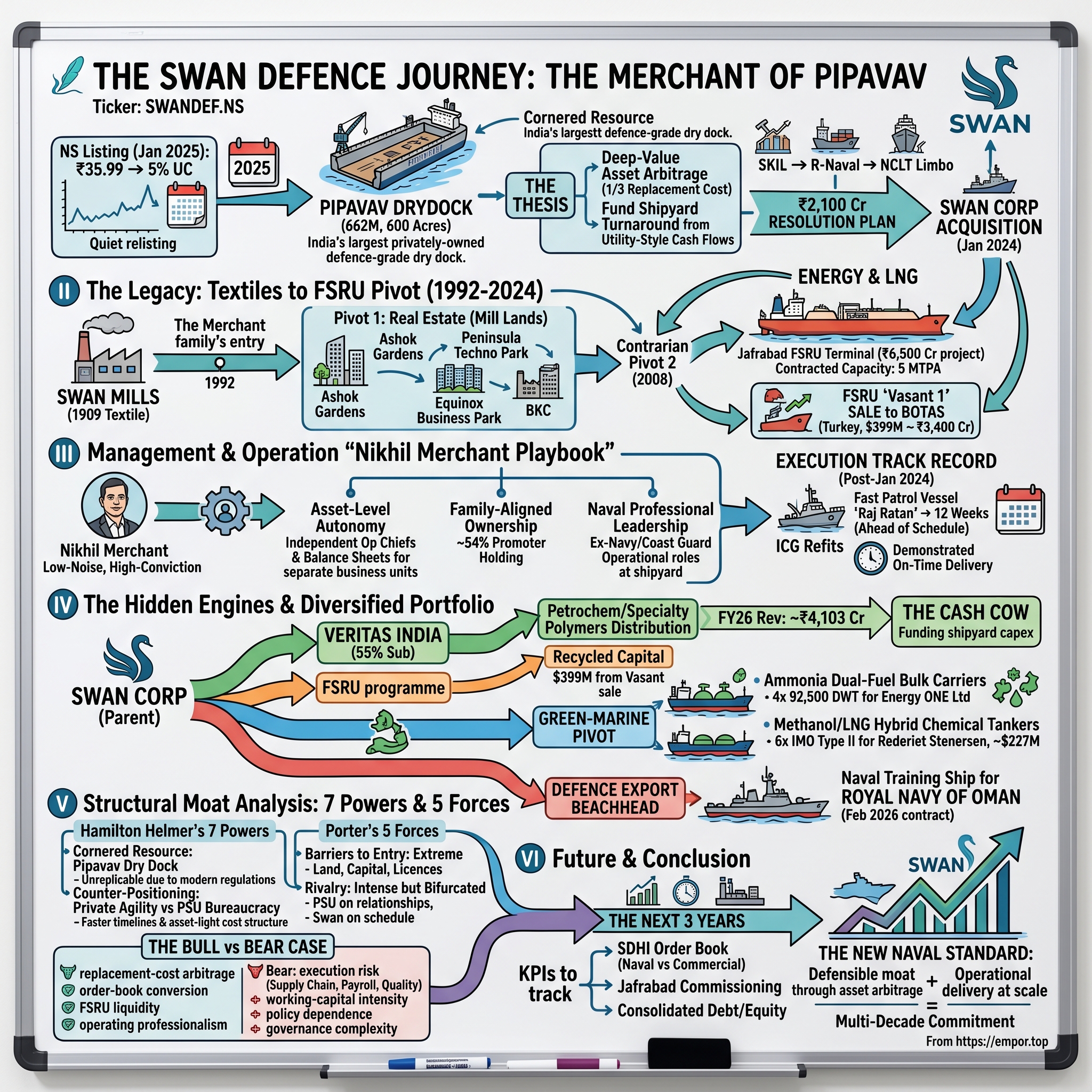

Swan Defence: The Merchant of Pipavav

I. Introduction & The "Asset Arbitrage" Thesis

On a humid January morning in 2025, a small bell rang in the trading hall of the National Stock Exchange in Bandra-Kurla. The ticker that lit up on the boards — SWANDEF — was the resurrected ghost of one of the most famous shipwrecks in modern Indian capital markets. The script opened at a polite ₹35.99, hit its 5% upper circuit at ₹37.78 by midmorning, and immediately did what relisted insolvency assets are supposed to do: nothing.16 For most of the old shareholders, that quiet listing was an obituary. For one family from south Bombay — the Merchants — it was a starting gun.

The asset behind that ticker was not a software company, not a fintech, not a pharma exporter. It was steel and concrete: six hundred acres of reclaimed coastline on the western edge of Gujarat, with a 662-metre dry dock at its heart — the single largest such pit ever excavated in India.11 You can stand at the wall of that dock and not see the other end. A Very Large Crude Carrier — 330 metres of double-hulled steel — fits inside it with room left over. A विक्रांत Vikrant-class aircraft carrier would, too. Yet for nearly a decade, this cathedral of heavy engineering produced almost nothing. It bankrupted SKIL Infrastructure, then bankrupted Anil Ambani's Reliance Naval, then sat in राष्ट्रीय कंपनी कानून न्यायाधिकरण National Company Law Tribunal (NCLT) limbo while lenders argued over the corpse.

This is the story of हंस सुरक्षा और भारी उद्योग लिमिटेड Swan Defence and Heavy Industries Ltd (SWANDEF.NS) and its parent, हंस कॉर्प Swan Corp (formerly Swan Energy). It is, at its core, a deep-value asset arbitrage trade dressed in the language of आत्मनिर्भर भारत Atmanirbhar Bharat and the Indian Navy's submarine ambitions. A 116-year-old Mumbai textile mill, run by a low-profile Gujarati family, walked into India's biggest shipyard bankruptcy with a ₹2,100 crore cheque and walked out with the keys to the country's only privately-owned defence-grade dry dock.9

The investment question is deceptively simple. The Pipavav dry dock would cost — by every credible engineering estimate — between ₹4,500 and ₹6,000 crore to replicate today, even before you priced in the decade of coastal clearances. The Merchants bought it for about a third of that, with the old debt wiped clean by the resolution plan. So the headline arbitrage is real. But Pipavav has eaten the careers of two of India's most aggressive industrialists already. Why should a textile-mill-turned-LNG-trader fare any better?

The answer the company offers is a portfolio: an FSRU programme that just sold a single vessel to Turkey for $399 million,5 a ₹4,000-crore-plus petrochemicals distribution arm,[^23] and a fresh slate of orders that include a Norwegian chemical-tanker contract and a defence export deal to the سلطنة عُمان Sultanate of Oman.21 The thesis, in short, is that you can fund a shipyard turnaround out of utility-style cash flows — and that the moat around a 600-acre dry dock is wider than any of its prior owners ever appreciated.

This episode walks through how the Merchant family got there: from a 1909 cotton mill, through the FSRU gamble at Jafrabad, into the heart of one of the most complicated NCLT resolutions India has yet produced.

II. The Legacy: From Textiles to the First Pivot

Walk down सेवरी Sewri in central Mumbai today, past the flamingo viewpoint and the disused docks, and you will pass a glass-clad residential tower called Ashok Gardens. It sits, almost incongruously, on land that for most of the twentieth century was a cotton-and-polyester mill — हंस मिल्स Swan Mills, incorporated on the 22nd of February, 1909, in the days when Bombay's mill economy still ran on coal and Lancashire ledgers.1 The mill changed hands several times. By the early 1990s it was owned by the J.P. Goenka group, which had run out of patience with textiles. In 1992, the Dave and Merchant families — two related Gujarati clans with backgrounds in trading and petrochemicals — bought the company.1

What they bought, technically, was a textile manufacturer. What they actually wanted was the land.

This is the founding pattern of the Merchant playbook, and it is worth dwelling on. The Mumbai mill lands were, by the 1990s, the most contested piece of urban real estate in India. The compound at Sewri eventually became Ashok Gardens. A second mill plot was developed into Peninsula Techno Park in Kurla. A third became Equinox Business Park in बांद्रा-कुर्ला कॉम्प्लेक्स BKC. None of this was particularly visible from the outside; the family did not throw lavish parties, did not court journalists, and never appeared on lists of "young promoters to watch." But by 2008, the textile mill on paper had quietly become a real-estate developer with a balance sheet large enough to do something genuinely audacious.

In 2008, Swan Mills pivoted into energy.1 The country was, at that moment, staring down a structural gas deficit. Imported LNG was beginning to substitute for domestic gas, and the only regasification capacity in India was concentrated at Dahej and Hazira — both controlled by the larger oil-and-gas players. निखिल मर्चेंट Nikhil Merchant, who had taken over operations as Managing Director, looked at the math and saw the obvious gap: India needed more regas terminals, and the fastest way to build one was not to dig a fixed onshore plant, but to floats one — a Floating Storage and Regasification Unit, or FSRU.

For non-technical listeners, the FSRU is one of the more elegant pieces of energy infrastructure invented in the last two decades. It is, essentially, a specialised LNG tanker that has been retrofitted with a regasification plant on its deck. You moor it permanently to a jetty, pipe the natural gas out from its hull, and you have — in roughly eighteen months — what would otherwise have taken five years to build onshore. The catch is that an FSRU is a single piece of steel that costs the better part of half a billion dollars, and you cannot easily move it once you commit it to a location.

Swan signed up to develop India's first newbuild FSRU at जाफराबाद Jafrabad on the Saurashtra coast, with a contracted capacity of around 5 million tonnes per annum and a project cost of roughly ₹6,500 crore.3 To put that figure in perspective: the company's entire textile-and-real-estate enterprise at the time of the pivot was a fraction of the cost of the single vessel it had agreed to build. This is what private-sector capital allocation in India looks like at its most contrarian — a mill family writing a defence-budget-sized cheque for a piece of offshore steel because the larger players could not move fast enough.

The Jafrabad terminal itself has had a long road. Onshore commissioning has slipped repeatedly, and in December 2024 Swan and the AG&P group signed a heads-of-agreement to form a joint venture to actually run the regasification operation.4 But the vessel — the वसंत Vasant-1 — was already built, already on the water, and already earning charter income. The first pivot had produced an asset.

That asset, as the next section shows, would become the war-chest for the second, much bigger pivot.

III. The Inflection Point: The Fall and Rise of Pipavav

To understand what Swan acquired in early 2024, you have to first understand what Pipavav was — and what it had cost the men who tried to own it before.

The shipyard was conceived in 1997 by निखिल गांधी Nikhil Gandhi, the SKIL Infrastructure founder who also built the adjoining Pipavav port. The original entity, "Pipavav Ship Dismantling & Engineering," was a wholly-owned SKIL subsidiary intended to break up old ships on a green-recycling model.12 Over the next decade, the ambition expanded — from ship-breaking to ship-building, from commercial tankers to warships. By the late 2000s the company had received an industrial licence to build warships and submarines for the Indian Navy, the only such licence ever issued to a private-sector Indian shipyard. The 600-acre site grew a 662-metre dry dock, a 340-metre wet basin, a 600-tonne Goliath crane, and 1.2 kilometres of waterfront.11 It was, on paper, the most ambitious greenfield shipyard ever built in India.

On paper.

In practice, Pipavav never managed to close the gap between its engineering capability and its order book. Indian naval procurement is famously slow; commercial shipbuilding from India had been priced out by Korean and Chinese yards a decade earlier. The yard burned cash. And in March 2015, Anil Ambani's Reliance Infrastructure rode in — buying an initial 17.66% stake at around ₹63 per share, eventually building to 36.5% via the open offer, in a deal valued at roughly $130 million.13 The company was renamed Reliance Defence and Engineering in March 2016, and then Reliance Naval and Engineering in September 2017.14 Anil Ambani told investors that the yard would be the cornerstone of the family's defence strategy. The branding worked. The execution did not.

By September 2018, IDBI Bank had filed for insolvency under the दिवालियापन और शोधन अक्षमता संहिता Insolvency and Bankruptcy Code (IBC) against Reliance Naval, citing roughly ₹9,492 crore of outstanding loans across a consortium of lenders.8 The case wound through the NCLT for over a year before Reliance Naval was formally admitted into the corporate insolvency resolution process by the NCLT Ahmedabad bench in January 2020.[^32] What followed was — even by the standards of Indian bankruptcy — a long, ugly, ten-bidder slog through a global pandemic.

Enter Swan. The Merchant family's vehicle for the bid was a special-purpose entity called Hazel Infra, in which Swan Energy held 74% and Hazel Mercantile the balance. Their resolution plan: ₹2,100 crore, with the entire pre-existing debt extinguished against that cash and a near-total wipeout of the old equity.9 The NCLT Ahmedabad bench approved the plan on the 23rd of December, 2022. A new board took charge on the 8th of December, 2023, and Swan formally assumed management control on the 4th of January, 2024.9 In August 2024, Swan disclosed that it had paid an additional ₹331 crore to the lenders ahead of the resolution-plan due date — a small but meaningful signal to the consortium that this owner intended to honour the timeline.10

Now the arbitrage. Cochin Shipyard's new dry dock — 310 metres long, with a 75-metre beam — cost the Indian taxpayer ₹1,799 crore to build, and was inaugurated only in January 2024.[^26]24 Pipavav's dry dock is more than twice that length, with greater beam and depth, and was acquired by Swan as part of a ₹2,100 crore portfolio that also included 600 acres of land, a 600-tonne crane, a wet basin, and the warship-building licence. Reasonable engineering estimates put the replacement cost of Pipavav, today, at ₹4,500 to ₹6,000 crore — and that is before you assume any of the coastal-zone or environmental clearances are still procurable. Swan, in effect, paid roughly 35-40% of replacement value, with the legacy debt wiped clean.

The mechanism that produced this arbitrage was the IBC itself — a piece of regulatory machinery that did not exist when Anil Ambani bought the yard in 2015. In other words: Swan did not out-bid Ambani. Swan waited until the law allowed the underlying asset to be detached from the historical debt, then walked in. Whether they can extract economic value from that asset is the next question. It does not change the fact that they bought it well.

IV. Management & The "Nikhil Merchant" Playbook

निखिल मर्चेंट Nikhil Merchant is, by all accounts, an unusual specimen among contemporary Indian promoters. He does not give magazine cover interviews. He does not headline industry forums. He is not on a CNBC television panel in the evenings. When the 2024 Forbes World Billionaires list appeared in print, listing him at a net worth of roughly ₹8,350 crore, several Mumbai journalists confessed they had never written about him.2 He is, in the Bombay-trading parlance, "low-noise, high-conviction."

The biographical sketch is sparse but consistent. Merchant took operational charge of Swan Mills in 1992 along with the broader Dave-Merchant family acquisition.29 He is described in board-level summaries as the principal driver behind every major pivot: the redevelopment of the mill lands in the 1990s and 2000s, the entry into LNG in 2008, the Veritas acquisition in 2022, and the Reliance Naval bid that closed in 2024. Crucially, he is the architect of the corporate skeleton — a tangle of subsidiaries and joint ventures that allowed Swan Energy, a company with a market capitalisation that for most of its history hovered in the low thousands of crores, to underwrite multi-billion-dollar capital commitments.

His governance style, as far as it can be reconstructed from filings and counterparty interviews, leans on three pillars. First, asset-level autonomy: each operating company — Veritas, Swan LNG, Swan Defence, the real-estate vehicles — has its own balance sheet and its own operating chief. Second, family-aligned ownership: promoter holding in Swan Corp sits around 53.96%, which is high enough to provide political cover during contentious M&A but not so concentrated that it discourages institutional participation.26 Third — and this is the soft skill that ultimately determines whether the Pipavav thesis works — a willingness to put naval and defence professionals, rather than family members, into operational roles at the shipyard.

That third pillar matters more than it sounds. Indian family-owned industrials, when they enter regulated sectors, often try to run them with the same generalist trading mindset that built the family fortune. It does not work. Defence shipbuilding is a regulated, security-cleared, navy-supervised activity in which trust is built slowly and in which a single bad weld in a hull plate can sink a multi-year programme. At Pipavav, Swan has deliberately put ex-Navy and ex-Coast Guard officers into the operational chain — the kind of people who can walk a भारतीय तटरक्षक बल Indian Coast Guard admiral around a refit bay without having to look at a brochure. The first publicly visible test of that arrangement was the refit of राज रतन Raj Ratan, an Indian Coast Guard fast patrol vessel which arrived at Pipavav on the 4th of September, 2024.22

The dock had been silent for almost five years. Within twelve weeks, on the 30th of November, 2024, the refit was complete — ahead of schedule.22 It was a deliberately conservative first project: a refit, not a new build; a coastal patrol vessel, not a frigate. But it produced the most important asset Swan needed from year one — a demonstrated, on-time delivery to an Indian armed force.25 A second Coast Guard refit followed soon after, also ahead of schedule.23 This is what "private-sector speed versus PSU bureaucracy" looks like in practice — not a magazine quote, but a vessel out of the water in twelve weeks instead of twenty-four.

The incentive structure at the top of the group is calibrated for this kind of execution. Merchant family wealth is, in effect, indexed to two things: the order book at the shipyard, and the toll-style cash flows from the energy infrastructure. Neither of those metrics responds to share-price hype; both respond to operational delivery. It is, in a sense, the opposite of the Anil Ambani approach.

V. The Hidden Engines: FSRU, Veritas & The Green Pivot

If you only read the headlines, you might assume Swan is a shipyard company. The cash flows tell a very different story — and understanding that story is the difference between treating SWANDEF as a speculative defence proxy and treating it as a real industrial conglomerate.

Start with the petrochemicals arm. In May 2022, Swan signed a Share Purchase Agreement to acquire 55% of वेरिटास इंडिया Veritas (India) Ltd, a Mumbai-listed distribution platform that moves petrochemicals, polymers, paper and rubber for global majors into the Indian market.[^22] Veritas became a Swan subsidiary effective the 20th of January, 2023.[^22] In FY2025-26, Veritas reported revenues of approximately ₹4,103.92 crore and a profit of ₹113.56 crore.[^23] That is not a small business. It is, in fact, the largest single line on Swan Corp's consolidated topline — bigger than the energy segment, bigger than the shipyard, and growing at double-digit rates as Indian manufacturing demand for specialty polymers expands. Veritas is, in the language of conglomerate analysis, the cash cow. It funds the more capital-intensive bets without requiring Swan to repeatedly tap the equity markets.

Then there is the FSRU programme, which has produced the single most consequential transaction in Swan's corporate history. On the 15th of August, 2024, Swan announced that it would sell its 51% stake in the FSRU Vasant 1 to Turkey's state-owned BOTAŞ Boru Hatları ile Petrol Taşıma BOTAS for $399 million; the remaining 49% is held by इफको IFFCO.5 The vessel had been on a one-year time charter to BOTAS at Saros Bay since February 2023 and entered commercial operation in April 2023, so by the time the sale closed BOTAS had been operating the unit under its own crew for over eighteen months and effectively knew exactly what it was buying.6 The consideration is being received in tranches over the closing period, subject to regulatory and shareholder approvals.7

Why does this matter? Because $399 million is — depending on exchange rate and the timing of tranches — roughly ₹3,300 to ₹3,400 crore. That is more than 1.5x the entire ₹2,100 crore Swan paid for Pipavav. In one transaction, the company essentially monetised its first major industrial bet and recycled the proceeds into the second. This is what capital recycling looks like when the assets in question are individually larger than the company that owns them. It is also why Swan can credibly underwrite multi-year shipyard capex without raising the kind of debt that sank Reliance Naval.

The third leg of the portfolio is the green-marine pivot, which is newer and more speculative but strategically important. In a press release from the company, SDHI announced it had secured what it described as India's first ammonia dual-fuel bulk carrier order — four 92,500 DWT vessels for Energy ONE Ltd.27 The vessels, each measuring roughly 229.5 metres by 37 metres, are being designed by South Korea's KMS-EMEC and classed by DNV Det Norske Veritas; first delivery is targeted for October 2029, with subsequent vessels following at four-month intervals.28

Layer onto that the chemical-tanker contract. Swan Defence signed a Letter of Intent with Norway's Rederiet Stenersen AS for six IMO Type II chemical tankers of up to 18,000 DWT each, valued at approximately $220 million.17 The deal was firmed up on the 23rd of January, 2026 at a revised $227 million.18 The vessels feature hybrid propulsion convertible between methanol and LNG, with battery upgrades of up to 5,000 kWh.19 This is not legacy bulk shipbuilding — it is the high-spec, fuel-flexible end of the commercial market, the segment that Korean and Chinese yards are most aggressive in. Whether Pipavav can compete on cost is unproven. The fact that an experienced Norwegian shipowner placed the order at all is the relevant signal: Stenersen does not need to subsidise an Indian shipyard for political reasons. They placed the order because the unit economics worked.

A second defence export — a ~3,500-tonne naval training ship for the سلطنة عُمان Royal Navy of Oman, contracted in February 2026, with first delivery targeted within eighteen months — closes the loop on the export thesis.2021 Swan is no longer pitching the Pipavav story on theoretical capacity. They are pitching it on a real order book.

The Jafrabad terminal will, eventually, layer a utility-style toll on top of all this — but for now, the cash that funds the shipyard turnaround is coming from Veritas, from the FSRU sale, and from working-capital advances on the new orders.

VI. Playbook: Porter's 5 Forces & Hamilton's 7 Powers

Step back from the operating details and the question becomes structural: is what Swan owns actually defensible? The right framework to ask that question with is the one Hamilton Helmer popularised in 7 Powers, layered against Michael Porter's classic five-forces map of the shipbuilding industry. The answer, in both frames, is more interesting than the consensus view.

Cornered Resource. This is Helmer's term for a one-of-a-kind asset that cannot be replicated through ordinary capital expenditure. The Pipavav dry dock — at 662 metres long, 65 metres wide, capable of accommodating ships up to 400,000 deadweight tonnes — is the cleanest example of a cornered resource in Indian heavy engineering today.11 You cannot build another one. Not in the practical sense. India's coastal-zone regulations were tightened materially in the late 2010s. The land aggregation alone — 600 acres of contiguous coastal frontage with dredged access — is now essentially unobtainable. The most recent comparable build in the country, Cochin Shipyard's new dry dock, came in at 310 metres and ₹1,799 crore — and that was a state-owned yard with full PSU backing.[^26] Pipavav, in contrast, was built by the private sector in a regulatory environment that no longer exists. Anyone trying to replicate it today would face a ten-year clearance path and capital costs north of $600 million.

Counter-Positioning. Helmer uses this term for a business model that incumbents cannot copy without cannibalising themselves. Swan's positioning against the public-sector shipyards — मझगांव डॉक Mazagon Dock, कोचीन शिपयार्ड Cochin Shipyard, गार्डन रीच Garden Reach, हिंदुस्तान शिपयार्ड Hindustan Shipyard — is exactly this. The PSU yards are constrained by procurement rules, by union structures, and by the bureaucratic cadence of रक्षा अधिग्रहण परिषद Defence Acquisition Council approvals. Swan, as a private operator, can quote, contract and deliver on commercial timelines. It is not a competitor PSUs can easily copy, because the very thing that makes Swan agile — its private ownership and its asset-light cost structure — is the thing the PSUs cannot legally adopt.

Scale Economies. Limited, in the conventional sense — Swan is not yet operating at sustained throughput. But the dock itself provides a kind of scale economy in reverse: it can accommodate vessels that no other Indian private yard can. That makes Swan the only credible Indian bidder for VLCC repairs, very large bulk carrier refits, and aircraft-carrier-class new builds. The implicit pricing power is real, even if it has not yet been fully exercised.

Switching Costs. Low in commercial shipbuilding (a shipowner will go wherever the price is right), but high in naval contracts. Once the Indian Navy or the Royal Navy of Oman has put a training vessel into Pipavav's order book, the documentation, design ownership and follow-on refit contracts tend to stay with the original builder. The Oman contract, in particular, is a foothold that — if executed well — creates a multi-decade refit relationship.21

On the Porter side, the picture is clean. Barriers to entry are extreme — capital, land, licensing, security clearances. Bargaining power of buyers is genuinely concentrated; the Indian Navy and Coast Guard are oligopsony customers. But Swan's negotiating position is materially better than its predecessors' because, on the relevant tonnage class, it is the only domestic option that does not require waiting in the PSU queue. Bargaining power of suppliers — steel, propulsion systems, electronics — is real but standardised. Threat of substitutes — building abroad — is the existential one, and the long-term answer for India is that strategic platforms cannot be substituted abroad, full stop. Rivalry is intense but structurally bifurcated: PSU yards compete on relationships, Swan competes on schedule.

The thing Helmer warns about, and the thing the bear case will pick up, is that a cornered resource is only valuable if you can fill the dock. Pipavav, under two prior owners, demonstrated exhaustively that you can own the asset and still go bankrupt.

VII. Analysis & The Bear vs. Bull Case

The bull case for Swan Defence is, fundamentally, a case about replacement-cost arbitrage and order-book conversion. The arbitrage piece is, by now, well-established: the yard was acquired for a meaningful discount to replacement cost, with the legacy debt wiped clean.9 But arbitrage on its own does not produce a re-rating; the dock must be turned into cash flow. And here, the early signals are genuinely encouraging. The Raj Ratan refit, delivered ahead of schedule in November 2024, demonstrated that the yard could execute a real customer project after years of dormancy.25 The follow-on Coast Guard refit reinforced the point.23 The Stenersen chemical-tanker order — placed by a sophisticated commercial counterparty, not subsidised by policy — was the first genuine third-party validation of Pipavav's competitiveness.17 And the Oman naval-training contract, signed in February 2026, was the moment the defence-export thesis stopped being theoretical.21

Add to this the financial engineering. The $399 million Vasant-1 sale gave Swan the kind of liquidity cushion that previous owners simply did not have — enough to deleverage, fund working capital for new builds, and underwrite Jafrabad's onshore commissioning all at once.5 Promoter alignment is high; institutional dilution risk is contained at the parent level.26 The Veritas cash cow keeps the lights on while the shipyard scales.[^23]

Myth versus reality. Three pieces of the consensus narrative deserve scrutiny.

The first myth is that Pipavav's dry dock is "the largest in India at 740 metres." It is not. The published specifications put the dock at 662 metres in length and 65 metres in width — still the largest in India, still capable of accommodating ships up to 400,000 DWT, but a real number that should be cited correctly.11 Investor decks that repeat the 740-metre figure are working from old marketing material.

The second myth is that Swan is "the L&T of the seas." That framing, while flattering, understates how dependent Swan is on a single asset. लार्सन एंड टुब्रो Larsen & Toubro has a defence portfolio that spans submarines (Hazira), missiles, radars, and full-system integration. Swan, at present, is a single yard with a growing order book and a green-marine bet. The comparison is aspirational, not operational.

The third myth is that the Indian Ministry of Defence will reliably channel naval orders to private yards under मेक इन इंडिया Make in India. The policy direction is real, but the procurement cadence is glacial. The PSU yards still hold the largest share of the Navy's order book, and the bidding rules continue to favour incumbents on certain platform classes. Swan's near-term order book is more likely to be filled by Coast Guard refits, export defence contracts, and commercial work than by big Indian Navy new-builds.

The bear case is straightforward. Execution risk at Pipavav has, historically, been the single most common cause of failure. The yard's payroll, supply chain and quality systems have been dormant or partial for years; rebuilding them at scale is a multi-year project. Working-capital intensity in shipbuilding is brutal — each new build ties up capital for two to four years, and a single delayed milestone can swing the whole project from profitable to loss-making. Policy dependence is real: a change in केंद्रीय बजट Union Budget priorities, a shift in defence-export licensing, or a delay in Jafrabad's commissioning can each compress the cash-flow runway. And the broader Swan Corp balance sheet, while improved post-Vasant, still carries meaningful debt against capital projects that are not yet fully revenue-generating.

There is also a less-flagged risk: governance complexity. The Swan-group structure is, by Indian standards, intricate — Swan Corp at the top, Hazel Mercantile alongside, Veritas as a 55% subsidiary, SDHI as a separately-listed entity, Swan LNG as a joint venture, and the Jafrabad project moving toward an AG&P JV. Investors who underwrite the holding company are exposed, indirectly, to all of these. Disclosure is reasonable but not always granular, and the related-party transactions between these entities will warrant ongoing scrutiny as the shipyard scales.

Key KPIs to track — and these are the ones that will determine whether the thesis is working: first, the SDHI order book, broken out between naval/defence and commercial; second, the timeline to Jafrabad's commercial commissioning and the eventual tolling revenue from it; and third, the debt-to-equity trajectory at the consolidated Swan Corp level as shipyard capex and Veritas working capital both ramp.

VIII. Epilogue: The New Naval Standard

The question that opened this episode was whether a textile-mill family from south Bombay could finally make Pipavav work. The honest answer, eighteen months into Swan's ownership, is that they have done the things their predecessors did not. They have monetised an adjacent asset to fund the core. They have put naval professionals into the operational chain. They have delivered, on time, the first two test projects. They have a credible commercial order book and a defence-export beachhead. None of this guarantees success at scale, but all of it is more than SKIL or Reliance Naval ever managed to assemble.

The broader lesson is one that recurs in Indian industrial history. The most defensible moats are not the ones with the loudest brand. They are the ones with the longest construction time. A 600-acre coastal site with a 662-metre dry dock is the kind of asset that — if you can keep it running — gets more valuable, not less, with each passing year of regulatory tightening. The Merchants understood this in 2008 when they bought a single FSRU, and they understood it again in 2022 when they wrote a ₹2,100 crore cheque for a defunct shipyard. The thesis they are betting on is that the price of building physical infrastructure in India is going only one way — and that the value of having already built it is therefore also going only one way.

Whether Swan Defence becomes the L&T of the seas, or whether it becomes the next cautionary tale, will depend on the next three years of order book conversion and balance-sheet discipline. But the asset itself — the dock, the land, the licence, the dry-water frontage — is, finally, in the hands of an owner who treats it as a multi-decade industrial commitment rather than a quick-turn defence-and-defence-only flip.

That, more than any single contract, is the change worth tracking.

References

References

-

Meet Nikhil Merchant with Rs 8,350 cr net worth — DNA India, 2024 ↩

-

Swan Energy acquires India's first FSRU to commission Jafrabad terminal — ProjectsToday ↩

-

BOTAS to buy Swan Energy's FSRU for $399 million — LNG Prime, 2024-08-15 ↩↩↩

-

Swan Energy to sell majority stake in FSRU for $399m — Splash247, 2024-08 ↩

-

India's Swan Energy to sell 51 per cent stake in FSRU — Baird Maritime, 2024-08 ↩

-

IDBI Bank moves NCLT against Reliance Naval to recover loan — Business Standard, 2018-09-06 ↩

-

Swan Energy takes management control of Reliance Naval & Engineering — Business Standard, 2024-01-04 ↩↩↩↩

-

Swan Energy paid Rs 331 crore to lenders before Dec 23, 2024 due date — Business Standard, 2024-08-08 ↩

-

Facilities & Infrastructure — Swan Defence and Heavy Industries (company website) ↩↩↩↩

-

Reliance Infra to pick up 25% stake in Pipavav Defence — Business Standard, 2015-03-05 ↩

-

Reliance Naval and Engineering shares get relisted at Rs 35.99 — Insolvency Tracker, 2025-01-20 ↩

-

Swan Defence shares relist on NSE, BSE, freeze at 5% upper circuit — Business Standard, 2025-01-20 ↩

-

Swan Defence signs $220 million LoI to build six chemical tankers at Pipavav — NewsOnProjects ↩↩

-

Swan Defence $227 million chemical vessel order at Pipavav — Business Standard, 2026-01-23 ↩

-

Swan Defence and Heavy Industries inks deal for six advanced chemical tankers — ScanX Trade ↩

-

Swan Defence to build naval training ship for Oman — Naval Technology ↩

-

Swan Defence bags major contract to build training ship for Oman's Navy — The Week, 2026-02-08 ↩↩↩↩

-

Swan's shipyard resumes operations with successful refit of ICG vessel Raj Ratan — BusinessWorld ↩↩

-

Swan Defence completes 2nd Indian Coast Guard vessel refit — Maritime Gateway ↩↩

-

PM to inaugurate new dry dock & International Ship Repair Facility — Zee Business, 2024-01 ↩

-

India's Pipavav Shipyard delivers its first project after re-opening — Maritime Executive ↩↩

-

SDHI secures India's first ammonia dual-fuel bulk carrier order — Swan Corp press release ↩

-

SDHI secures India's first ammonia dual-fuel bulk carrier order — MarineLink ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube