Surya Roshni: From Steel Pipes to Illuminating India

I. Introduction & Episode Roadmap

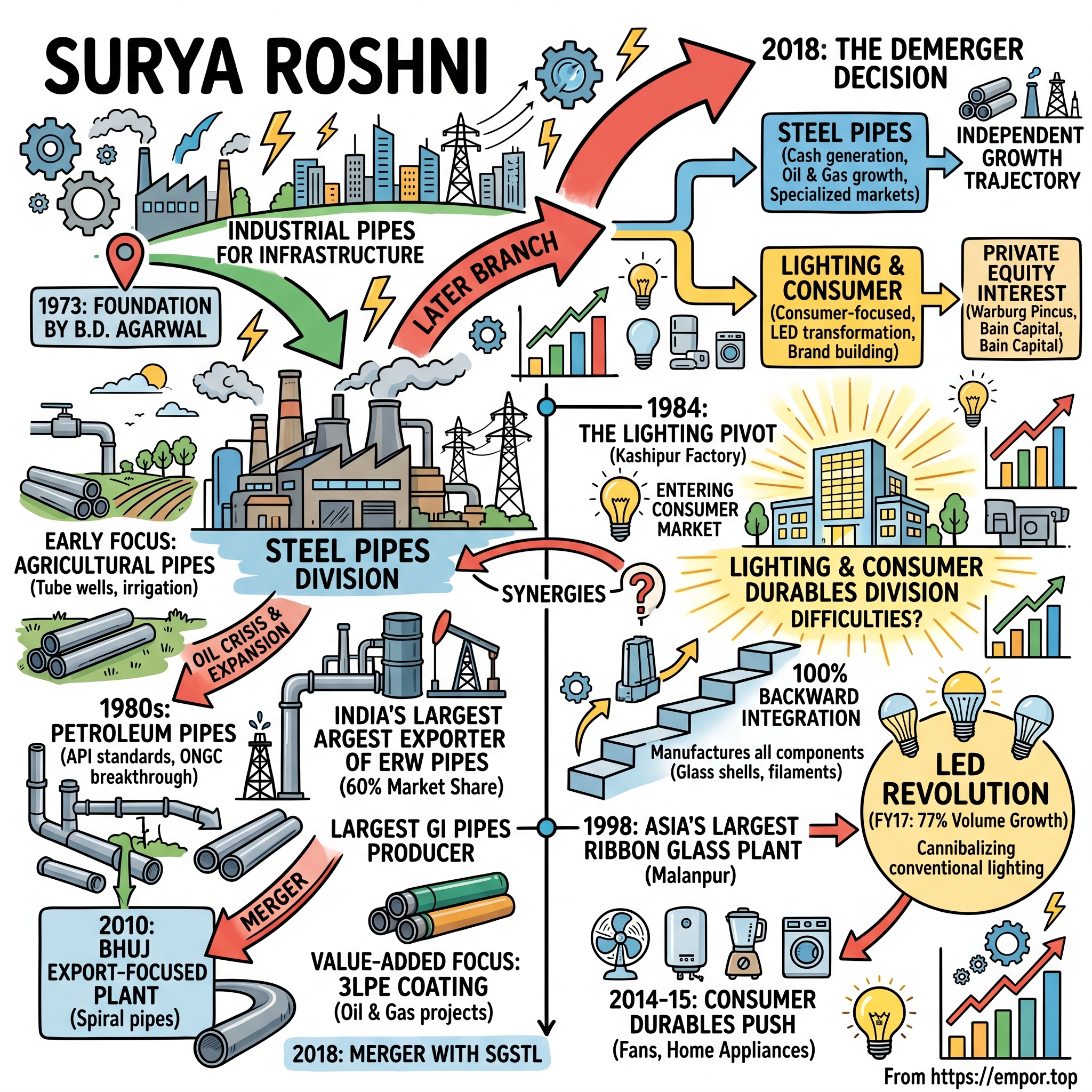

Picture this: In the dusty industrial outskirts of Bahadurgarh, Haryana, 1973, a young entrepreneur named B.D. Agarwal stands before a modest tube-making unit. The air is thick with the smell of molten steel and machine oil. India, barely two decades into independence, desperately needs infrastructure—pipes for water, irrigation, petroleum. Agarwal sees not just pipes, but the arteries of a nation waiting to be built.

Fast forward fifty years. That modest unit has morphed into Surya Roshni Limited—India's largest exporter of ERW pipes commanding 60% market share, the country's biggest manufacturer of galvanized iron pipes, and the second-largest player in lighting. Two completely unrelated businesses, each generating billions in revenue, housed under one roof. The central question that drives our story today: How did a steel pipe manufacturer in post-liberalization India build two completely different billion-dollar businesses—and why are they now splitting apart?

This is a story of unglamorous excellence. While tech unicorns grab headlines, companies like Surya Roshni quietly build the physical infrastructure that makes modern life possible. Every time you turn on a light or water flows through a pipe in India, there's a decent chance Surya Roshni made it happen. It's the story of how family businesses evolve, how conglomerates manage complexity, and most importantly, how to build enduring value in industries everyone else ignores.

What you'll learn today goes beyond one company. We'll explore the art of backward integration in Indian manufacturing, the challenge of managing unrelated diversification, and how distribution networks become competitive moats in a country of 1.4 billion people. We'll see how a Padma Shri awardee built not just businesses but institutions, balancing profit with social consciousness through the Surya Foundation.

The timing of this story couldn't be more relevant. As Surya Roshni prepares to split its two business verticals—with private equity giants like Warburg Pincus and Bain Capital circling the lighting division—we're witnessing a pivotal moment in Indian industrial history. A family conglomerate built for one era is restructuring itself for another.

So buckle up. We're about to journey through five decades of Indian industrialization, from the License Raj to liberalization, from fluorescent tubes to LEDs, from agricultural pipes to oil & gas infrastructure. This is the Surya Roshni story—a masterclass in building where others won't, competing where others can't, and thriving when others don't.

II. Origins: The Agarwal Family & India's Industrial Awakening

The year is 1973. India is reeling from the 1971 war with Pakistan, the economy is struggling with inflation, and Prime Minister Indira Gandhi's government is tightening its grip through the License Raj—that byzantine system of permits and quotas that controlled who could manufacture what, where, and how much. For most entrepreneurs, this was a nightmare. For B.D. Agarwal, it was an opportunity.

Agarwal came from a traditional business family, but he saw something others missed. India's massive infrastructure deficit wasn't just a problem—it was a generational opportunity. The country needed everything: roads, bridges, irrigation systems, power plants. And all of these needed one unglamorous but essential component: steel pipes. While others chased licenses for consumer goods or textiles, Agarwal went after tube-making equipment. The establishment of the Bahadurgarh plant wasn't just about manufacturing—it was about timing. B.D. Agarwal established Surya Roshni in 1973 as a tube making unit, positioning himself perfectly for what was about to unfold. The global oil crisis of 1973-74 had just begun, sending shockwaves through commodity markets. Steel prices were volatile, supply chains were disrupted, and most businessmen were retreating. Agarwal did the opposite—he expanded.

The name itself—Surya Roshni, combining the Sanskrit words for sun and light—hinted at ambitions beyond steel tubes. But in those early days, survival meant focus. The company branded its industrial products as "Prakash Surya," a name that would become synonymous with quality in India's construction and infrastructure sectors over the next two decades. What really set the Agarwals apart was their dual vision of business and society. The company's current chairman is the Padma Shri awardee Jai Prakash Agarwal, son of founder B.D. Agarwal. When Jai Prakash took the reins, he brought a philosophy shaped by Swami Vivekananda's teachings—that business success without social consciousness was hollow. In 1992, he established the Surya Foundation, years before corporate social responsibility became fashionable. This wasn't window dressing—over 2 lakh children have received personality development training through the Foundation's initiatives.

The Foundation would go on to run everything from think tanks on national development to naturopathy centers, from youth training programs to—remarkably—a Sainik School in Gujarat in collaboration with the Government of Gujarat for tribal children. This social infrastructure would prove as valuable as the manufacturing infrastructure, creating goodwill that opened doors and smoothed regulatory paths for decades to come.

But in 1973, all of this was in the future. The immediate challenge was navigating India's socialist economy. The License Raj meant you needed government permission to expand capacity, import machinery, or even change your product mix. Foreign exchange was scarce. Technology transfer was restricted. Competition from public sector units was fierce. Yet within these constraints lay opportunity—if you could master the system, you faced limited competition from new entrants.

The steel shortage crisis of the mid-1970s became Surya Roshni's first major break. India's Green Revolution was picking up steam, requiring massive irrigation infrastructure. The oil discoveries in Bombay High needed pipelines. Cities were expanding, demanding water distribution networks. And here was this company in Bahadurgarh, perfectly positioned to serve North India's booming agricultural heartland, with the technical capability to produce Electric Resistance Welded (ERW) pipes that met stringent specifications.

The "Prakash Surya" brand began appearing on construction sites from Punjab's wheat fields to Rajasthan's desert irrigation projects. Each pipe carried not just water or oil, but the reputation of a company that delivered on time, met specifications, and stood behind its products. In an era where shoddy quality and delayed deliveries were the norm, reliability became Surya Roshni's competitive advantage.

By the end of the 1970s, the company had established itself as a serious player in India's steel pipe industry. But the Agarwals were just getting started. They understood something fundamental about Indian business: in a capital-scarce, relationship-driven economy, the companies that survived weren't necessarily the most innovative or efficient. They were the ones that could navigate complexity, build trust, and spot opportunities where others saw only obstacles. The stage was set for three decades of relentless expansion.

III. Building the Steel Empire: Pipes, Infrastructure & Nation Building (1973–1990s)

The Green Revolution of the 1960s and 70s transformed Indian agriculture, but it also created an infrastructure crisis nobody saw coming. Punjab's farmers, suddenly flush with high-yielding wheat varieties, needed water—lots of it. Traditional flood irrigation wouldn't suffice. The solution? Tube wells and sprinkler systems, all requiring miles and miles of steel pipes. By 1975, Surya Roshni's Bahadurgarh plant was running three shifts, and they still couldn't keep up with demand. The genius of Surya Roshni's strategy wasn't just making pipes—it was understanding where India's growth would come from. While competitors focused on urban construction, the Agarwals bet on agriculture. Surya Roshni emerged as India's largest ERW Pipes exporter, largest GI Pipes producer, a position built pipe by pipe, field by field, throughout the 1980s.

Consider the numbers: a single tube well in Punjab required approximately 200 feet of pipe. By 1985, Punjab alone had over 800,000 tube wells. That's 160 million feet of pipe—just for one state's irrigation needs. Surya Roshni captured a significant chunk of this market by doing three things competitors couldn't or wouldn't: maintaining consistent quality, offering credit to farmers through dealers, and most importantly, being present where the demand was.

The company's "Prakash Surya" brand became synonymous with reliability in the agricultural sector. Farmers would specifically ask for Prakash Surya pipes, willing to wait weeks rather than accept alternatives. This wasn't achieved through advertising—rural India in the 1980s had limited media reach. It was built through what the Agarwals called "performance marketing"—every pipe that didn't leak, every harvest that succeeded because of reliable irrigation, became a testimonial.

But agriculture was just the beginning. The 1980s brought another opportunity: petroleum. India's oil discoveries, particularly the Bombay High field, required thousands of kilometers of high-specification pipes. These weren't your garden-variety tubes—they needed to withstand extreme pressure, corrosion, and meet international American Petroleum Institute (API) standards. Most Indian manufacturers balked at the technical requirements and capital investment needed. Surya Roshni dove in.

The company invested heavily in technology to produce pipes meeting API specifications, a move that seemed risky at the time. The petroleum sector was dominated by public sector units with their own preferred suppliers. Breaking in required not just quality but persistence. The breakthrough came when ONGC faced a supply crisis in 1986—their regular suppliers couldn't deliver on time. Surya Roshni stepped in, delivered ahead of schedule, and suddenly had a foot in the door of India's most lucrative pipe market.

It is the leading manufacturer of ERW GI Pipes in India. It is also the leading exporter of ERW Pipes with a 60% market share. It is a leader in South India and among the top 3 in North India for GI Pipes. This market position wasn't built overnight—it was the result of methodical expansion throughout the 1980s and 90s.

The distribution network became Surya Roshni's invisible asset. By 1990, the company had over 500 dealers across India, from Kashmir's apple orchards needing irrigation to Kerala's rubber plantations requiring water transport systems. Each dealer was more than a sales point—they were credit providers, technical advisors, and brand ambassadors rolled into one. The company's policy of supporting dealers during downturns, extending credit lines when needed, created loyalty that competitors with deeper pockets couldn't buy.

Quality control became an obsession. In an era when Indian manufacturing was synonymous with "good enough," Surya Roshni implemented testing protocols that exceeded Indian Standards Institute requirements. Every batch was tested, defective pieces were melted down rather than sold as seconds, and customer complaints were treated as learning opportunities rather than nuisances. This attention to detail paid off when export markets opened up in the late 1980s.

The company's first major export order came from Nigeria in 1988—10,000 tons of GI pipes for Lagos's water distribution upgrade. The challenge wasn't just manufacturing but logistics—shipping from landlocked Haryana to African ports required coordination that most Indian companies of that era couldn't manage. Surya Roshni pulled it off, delivered on time, and suddenly had international credibility.

By 1990, the Bahadurgarh plant had expanded from its original capacity of 5,000 tons per year to over 50,000 tons. New production lines were added almost annually, funded entirely through internal accruals—a remarkable achievement in an era of expensive capital. The company was generating enough cash to not just sustain operations but to think about something ambitious: diversification.

The steel pipe business had given Surya Roshni scale, credibility, and cash flow. But the Agarwals understood that infrastructure alone wouldn't be enough. India was changing. The middle class was growing. Consumer aspirations were rising. The question was: could a company known for industrial products make the leap to consumer markets? The answer would reshape Surya Roshni's destiny.

IV. The Lighting Pivot: Diversification into Consumer Products (1984–2000s)

The decision to enter lighting in 1984 seemed, on the surface, completely irrational. Surya Roshni was a steel pipe company. They knew metallurgy, not glass. They understood industrial customers, not retail consumers. The lighting market was dominated by established players like Philips, Osram, and Crompton Greaves. Why would a pipe manufacturer pick this fight?

The answer lay in a conversation Jai Prakash Agarwal had with a dealer in rural Uttar Pradesh. The dealer mentioned that farmers who bought pipes also needed lights for their pump houses, but quality bulbs were either unavailable or unaffordable in rural markets. The imported brands were too expensive, the local ones too unreliable. There was a gap—not at the premium end where multinationals competed, but in the vast middle market where value mattered more than brand cachet.

In 1984, Surya set up its first factory, for lighting products, at Kashipur (in Nainital, UP). The location choice was strategic—close enough to Delhi for management oversight, but in a backward area that qualified for tax incentives. The initial plan was modest: manufacture fluorescent tube lights (FTL) for industrial and agricultural use, leveraging the existing dealer network from the pipe business.

But the Agarwals quickly realized that making quality lights required controlling the entire value chain. In lighting, unlike pipes, the components mattered as much as the assembly. Poor quality glass meant shorter life. Inferior phosphor coating meant dimmer output. Substandard filaments meant frequent failures. Most Indian manufacturers simply imported components and assembled them. Surya Roshni decided to make everything in-house.

This backward integration strategy required massive capital investment and technical expertise the company didn't possess. The solution came through an unlikely source: retired engineers from Bharat Electronics Limited. These veterans, forced into early retirement by public sector downsizing, brought decades of experience in precision manufacturing. Surya Roshni hired them as consultants, effectively acquiring institutional knowledge at a fraction of the cost of technology transfer agreements.

In 1992, it built another factory at Malanpur (near Gwalior, MP). Both these state-of-the-art lighting plants were accorded the ISO 9002 certification in the 1980s at a time when the Indian industry was not familiar with such innovative concepts. The Malanpur plant represented a leap in ambition—this would manufacture not just tubes but the entire range of lighting products.

The real breakthrough came in 1998. Asia's largest ribbon glass plant started with annual capacity of 400 Million GLS and 25 Million FTL shells. This wasn't just about scale—it was about achieving a cost structure that could compete with imports while maintaining quality. The ribbon glass process, where molten glass is drawn into continuous ribbons and shaped into bulb shells, required precise temperature control and automation that most Indian companies couldn't manage.

The plant's commissioning was a nightmare. The Italian equipment suppliers sent technicians who couldn't handle Indian summer heat. The power supply was erratic, causing furnace temperature fluctuations that ruined entire batches. Local engineers had never worked with such sophisticated automation. For six months, the plant operated at less than 20% capacity, hemorrhaging money.

The turnaround came when Surya Roshni did something unconventional: they sent their entire technical team to Italy for training, not just the senior engineers. Floor operators, maintenance staff, quality control inspectors—everyone who would touch the equipment learned from the source. When they returned, the plant's efficiency jumped to 80% within three months.

Surya is the only lighting company with 100 per cent backward integration. It manufactures all its components. This complete control over the supply chain became Surya Roshni's competitive moat. While competitors struggled with component quality and availability, Surya could guarantee consistency. When glass prices spiked, they were insulated. When phosphor became scarce, they had inventory.

The consumer brand strategy was different from the industrial approach. While "Prakash Surya" dominated in pipes, the lighting division created the "Surya" brand for consumer products. The positioning was deliberate: not the cheapest, not the most premium, but the most reliable in the middle market. The tagline—"Surya, Roshni ka Bhagwan" (Surya, the God of Light)—resonated in Hindi-speaking markets where the brand first expanded.

Distribution leverage proved crucial. The same dealers selling Prakash Surya pipes to farmers could now offer Surya bulbs and tubes. This wasn't just cross-selling—it was relationship monetization. A dealer who had built trust over pipe quality could extend that trust to lighting products. The economics were compelling: lighting products had higher margins and faster turnover than pipes.

By 2000, Surya Roshni had captured significant market share in the fluorescent tube market, becoming the largest domestic manufacturer. The company was producing everything from standard T12 tubes to compact fluorescent lamps (CFLs), from street lighting to specialty lamps for poultry farms. The product range had expanded from 5 SKUs in 1984 to over 200 by 2000.

The international market opened up almost by accident. A buyer from Nigeria, visiting the Bahadurgarh pipe plant, noticed the lighting products and asked for samples. Six months later, Surya Roshni had its first lighting export order—a container of fluorescent tubes for Lagos. By 2000, the company was exporting to 30 countries, leveraging the relationships built through pipe exports.

But success brought its own challenges. The lighting market was about to undergo its biggest disruption in a century. LED technology was emerging from laboratories, promising to make fluorescent tubes as obsolete as incandescent bulbs. Chinese manufacturers were flooding global markets with cheap products. Energy efficiency was becoming a regulatory requirement, not just a selling point. The comfortable middle market position Surya Roshni had carved out was about to be squeezed from both ends. The question wasn't whether to adapt, but how fast and how far.

V. Expansion & Scale: Geographic Growth & Product Evolution (2000–2015)

The new millennium brought a new India. GDP growth was accelerating, infrastructure spending was exploding, and consumer confidence was soaring. For Surya Roshni, this meant opportunity—but also complexity. The company that had grown organically for three decades suddenly faced choices that would define its next phase: where to expand, what to manufacture, and how to finance it all. The 2010 decision to expand beyond Bahadurgarh represented a fundamental shift in Surya Roshni's strategy. For 37 years, the company had operated from a single steel manufacturing base. Now, in rapid succession, they would establish plants across India's geography. Set up of Steel pipe Plant at Gwalior (MP). A new world-class pipe unit started production at Bhuj (SGSTL- an Associate Company). PVC plant became operational—all in the same year.

The Bhuj facility deserves special attention. Located in Gujarat's Kutch district, just 70 kilometers from the Kandla and Mundra ports, this wasn't just another pipe plant. This was Surya Roshni's bet on exports. The Ultra-modern manufacturing unit operating under the parent company in Bhuj, Gujarat, extensively reaches over an enormous area of 100 acres with a capacity of producing ERW pipes with 230,000 MT and Spiral pipes of 60,000 MT per annum.

The plant was technically established under Surya Global Steel Tubes Limited (SGSTL), an associate company. This structure allowed Surya Roshni to partner with local investors who understood Gujarat's business environment while maintaining operational control. The location was strategic—Gujarat's ports handled 40% of India's cargo, and proximity meant lower logistics costs for both raw material imports and finished goods exports.

The Gwalior plant, meanwhile, served a different purpose. Central India was experiencing an infrastructure boom, but most steel pipe manufacturers were concentrated in the North or West. Transportation costs made pipes expensive in states like Madhya Pradesh, Chhattisgarh, and eastern Maharashtra. By establishing local manufacturing, Surya Roshni could undercut competitors on delivered cost while maintaining margins.

But the most interesting diversification was into PVC pipes. It further ventured into PVC pipes in 2010. This seemed counterintuitive—why would a steel pipe company enter a completely different material category? The answer lay in customer behavior. Contractors and builders were increasingly using both steel and PVC pipes in the same projects. Steel for structural applications and high-pressure lines, PVC for drainage and low-pressure water distribution. By offering both, Surya Roshni could become a one-stop shop.

The PVC entry wasn't smooth. The technology was different, the raw materials were petrochemical derivatives rather than steel coils, and the manufacturing process required entirely different expertise. The company's first batches had quality issues—the pipes would become brittle in extreme temperatures, a critical flaw in India's diverse climate. It took eighteen months of trial and error before the products met market standards.

Into consumer durables like fans and home appliances in 2014-2015. This move seemed even more puzzling. What did fans have to do with pipes or lights? But there was method to this apparent madness. The lighting distribution network—those 2,000-plus dealers—were already selling electrical products. Adding fans and appliances leveraged existing relationships while improving dealer economics through better product mix.

The consumer durables strategy was defensive as much as offensive. Companies like Havells and Crompton were expanding aggressively, using their strong positions in fans and appliances to push into lighting. If Surya Roshni didn't offer a complete portfolio, they risked losing shelf space at retailers. The choice was stark: expand or be marginalized. The 2018 merger of associate company Surya Global Steel Tubes Limited (SGSTL) with Surya Roshni Limited was the capstone of this expansion phase. SGSTL is an exports-focused unit with cost advantages over others and hence, the merger is expected to improve margin and returns of its steel business as well. The merger brought several strategic benefits: creation of a larger and stronger steel pipes business with economies of scale, geographical reach in all major parts of the country, and most importantly, direct control over export operations.

The SGSTL merger wasn't just about consolidation—it was about positioning for the future. The Bhuj plant's proximity to ports made it ideal for serving Middle Eastern markets, where infrastructure spending was booming. The facility's ability to produce large-diameter spiral welded pipes (up to 105 inches) opened doors to oil and gas projects that smaller Indian manufacturers couldn't touch.

Market network of over 2,000 distributors and 2 lakh countrywide retailers across PAN India emerged from this expansion phase. This wasn't achieved through acquisition but through patient network building. Each new geography required understanding local business practices, credit cycles, and competition dynamics. A distributor model that worked in Punjab might fail in Tamil Nadu. Payment terms acceptable in Gujarat might be deal-breakers in West Bengal.

The financial engineering behind this expansion was as impressive as the operational execution. Despite establishing four major manufacturing facilities and entering two new product categories, the company remained largely debt-free. This was achieved through a combination of internal accruals, strategic timing of capital expenditure, and most importantly, rapid capacity utilization. New plants weren't built on speculation—they were responses to confirmed demand.

The geographical diversification also provided risk mitigation. When monsoons failed in one region affecting agricultural pipe demand, construction activity in another region compensated. When steel prices spiked affecting margins in commodity pipes, value-added products like 3LPE coated pipes for oil and gas maintained profitability. The company had evolved from a single-product, single-location manufacturer to a diversified conglomerate with multiple growth engines.

But this complexity came at a cost. Managing four steel plants, two lighting facilities, PVC operations, and consumer durables required different skills, technologies, and market approaches. The synergies that seemed obvious on paper—shared distribution, common customers, operational efficiencies—proved harder to realize in practice. Steel pipe customers didn't necessarily want to buy LED bulbs. Lighting distributors weren't equipped to handle heavy steel pipes.

By 2015, Surya Roshni faced a strategic inflection point. The lighting industry was undergoing its biggest disruption in a century with the LED revolution. The steel pipe business needed massive capital investment to capture opportunities in oil and gas. Consumer durables required brand building and marketing spending. The company couldn't excel at everything simultaneously. Something had to give.

VI. The LED Revolution & Consumer Durables Push (2010–Present)

The LED disruption didn't announce itself with fanfare—it crept in through government tenders. In 2014, when Prime Minister Modi launched the LED bulb distribution scheme UJALA, Surya Roshni's management initially dismissed it as another subsidy program that would fade. They were wrong. Within three years, LED would destroy the carefully constructed economics of the conventional lighting business. The numbers tell the story of transformation: During FY17, volume growth in LED business was 77% yoy, whereas the fan and home appliances business grew by 55% yoy. These weren't incremental gains—they were tectonic shifts. The conventional lighting business that had taken decades to build was being cannibalized at breathtaking speed.

The LED transition exposed a fundamental challenge in Surya Roshni's backward integration strategy. The company had spent millions building Asia's largest ribbon glass plant for incandescent bulbs. They had perfected phosphor coating for fluorescent tubes. They manufactured their own filaments. All of these capabilities became obsolete almost overnight. LED technology required semiconductor expertise, not glass manufacturing. It needed chip mounting, not filament winding.

The initial response was denial, then panic, then pragmatic adaptation. Unable to manufacture LED chips—that required billion-dollar fabs—Surya Roshni pivoted to assembly and design. They imported LED chips from Taiwan and China, focusing on driver design, heat management, and luminaire engineering. It was a humbling comedown for a company that prided itself on making everything in-house.

But the LED disruption also created opportunity. The government's UJALA scheme and street lighting programs created massive tender opportunities. Surya Roshni's reputation with government buyers, built over decades of reliable supply, gave them an edge over Chinese importers and fly-by-night assemblers. They won significant chunks of municipal street lighting contracts, not because they had the best technology, but because they had the best execution track record.

The consumer durables expansion, particularly into fans, followed a different logic. In FY17, the fans segment had 3% market share of the total Indian fan market and achieved sales of Rs180 cr. This might seem modest, but it represented a foothold in a ₹5,000 crore market dominated by established players like Crompton, Havells, and Orient.

The fan market taught Surya Roshni harsh lessons about consumer branding. In pipes and industrial lighting, relationships and reliability mattered more than brand perception. In consumer durables, packaging, advertising, and retailer margins determined success. The company's first fan models, despite being technically competent, failed to gain traction because they looked industrial, not aspirational.

The turnaround came through focus on energy efficiency. Surya developed a 32W super-efficient BLDC fan that saved 60% energy compared to conventional fans. While competitors fought on price and aesthetics, Surya targeted the growing segment of energy-conscious consumers. Government buildings, educational institutions, and corporate offices—already Surya customers for lighting—became early adopters.

Kitchen appliances seemed like a logical extension—leverage the dealer network, offer combo schemes with fans and lights. Reality proved messier. Mixer grinders required after-sales service capabilities Surya didn't have. Induction cooktops needed consumer education in markets unfamiliar with the technology. Water heaters competed with established brands like Racold and Bajaj that had decades of consumer trust.

The period from 2015 to 2020 saw Surya Roshni trying to be everything to everyone. LED lights for government tenders. Designer fans for urban homes. Kitchen appliances for tier-2 cities. PVC pipes for affordable housing. Steel pipes for infrastructure. Each business required different capabilities, capital allocation, and management attention. Meanwhile, a quiet revolution was happening in the steel pipe division. The business has further strengthened with the setting up of 3LPE coating facility unit in 2018 (for the Oil & Gas and CGD sector). This wasn't just another capacity addition—it was a strategic pivot toward value-added products that could command premium pricing.

3LPE (Three Layer Polyethylene) coating represents the cutting edge of pipeline protection technology. The pipes are coated with fusion-bonded epoxy, adhesive, and polyethylene layers that protect against corrosion in the harshest environments. For oil and gas companies laying pipelines through deserts, underwater, or corrosive soil, 3LPE coating can extend pipeline life from 20 to 50 years.

The timing was perfect. India's City Gas Distribution (CGD) sector was exploding, driven by the government's push to increase natural gas usage from 6.5% to 15% of the energy mix. Every CGD project needed thousands of kilometers of coated pipes. Surya Roshni's established relationships with oil and gas majors, combined with the new coating capability, positioned them perfectly to capture this demand.

The order book grew rapidly. Total order book in hand amounted to ₹850 crore for oil and gas sector projects. These weren't commodity pipe orders but specialized, high-margin products with stringent quality requirements. A single order from GAIL or IOCL could be worth ₹100 crore, with execution timelines of 6-12 months providing revenue visibility.

The contrast between the two divisions became stark. The lighting and consumer durables business was fighting for market share in intensely competitive, brand-driven markets with declining margins. The steel pipes division was winning high-value contracts in a specialized market with significant entry barriers. One business was about volume, the other about value.

Technology adoption accelerated across both divisions. Direct Forming Technology (DFT) was introduced in 2022 for manufacturing structural steel sections—a computerized process that could produce customized hollow sections without changing rolls, dramatically reducing setup time and improving efficiency. In lighting, the company invested in smart LED systems for street lighting that could be remotely monitored and controlled.

But managing this complexity was becoming unsustainable. Board meetings became marathons, with discussions jumping from LED chip sourcing to petroleum pipeline specifications, from fan blade aerodynamics to steel coil pricing. Management attention was divided, capital allocation decisions were contentious, and neither business was getting the focused leadership it needed.

By 2017, whispers of a potential demerger began circulating. According to earlier media reports, private equity firms – Warburg Pincus and Bain Capital were interested in buying its lighting business. Another strong contender in the line was Crompton Greaves Consumer Electricals. The interest from sophisticated financial and strategic buyers validated what the market suspected: there was significant value trapped in the conglomerate structure.

The challenge was execution. The two businesses shared corporate services, manufacturing facilities in some locations, and most importantly, the Surya brand. Untangling fifty years of integration wouldn't be simple. But as LED margins continued to compress and oil and gas opportunities expanded, the logic for separation became undeniable. The question wasn't if, but when and how.

VII. The Demerger Decision: Two Businesses, Two Destinies

The boardroom at Padma Tower in New Delhi had witnessed many pivotal decisions over five decades, but the discussion in early 2018 was different. For the first time, the Agarwal family was seriously considering splitting their creation. The catalyst wasn't crisis but opportunity—opportunity that the current structure was preventing both businesses from capturing. Warburg Pincus and Bain Capital have expressed interest to buy into the lighting business of Surya Roshni, as the New Delhi-headquartered company is demerging it into a standalone unit. The interest from these sophisticated investors wasn't random—they saw what the Agarwals were beginning to acknowledge: the conglomerate discount was real and growing.

The strategic rationale for separation was compelling on multiple fronts. As the two businesses are not inter-related and have different business dynamics, maintaining them under one roof was creating inefficiencies. Steel pipes needed patient capital for large infrastructure projects with 12-18 month execution cycles. Lighting required rapid product development and marketing spend to keep pace with technology changes. The capital allocation conflicts were becoming untenable.

However, subdued performance of its Steel Pipes & Strips division was a concern which could have prevented a smooth demerger. This was the catch-22: private equity buyers wanted the lighting business, but only if it came with clean financials and no cross-guarantees with the cyclical steel business. The solution was elegant: strengthen the steel business first, then separate.

Therefore, in 2016 the company merged its associate company, Surya Global Steel Tubes (SGSTL) in its Steel division. This wasn't just consolidation—it was preparation. By merging SGSTL, Surya Roshni created a steel business with sufficient scale, profitability, and strategic assets (like the Bhuj export facility) to stand alone. The merger also cleaned up the corporate structure, eliminating minority interests and inter-company transactions that would complicate a demerger.

The valuation discussions were fascinating. With a net profit of Rs 63.1 crore in FY17, Surya Roshni has a market share of 13% and is the second largest lighting player in India. Private equity firms were valuing the lighting business at 15-20x earnings, implying a valuation of ₹1,200-1,500 crore. The steel business, despite generating higher revenues, was valued at only 8-10x earnings due to its commodity nature and cyclicality.

Buyout funds Warburg Pincus, Advent International-backed Crompton Greaves Consumer Electricals and Bain are among those in the fray to buy a controlling stake in Surya Roshni. Each suitor brought different strategic logic. Warburg Pincus, fresh from successful exits in Bharti Airtel and Havells, saw an opportunity to consolidate India's fragmented lighting market. Bain Capital believed they could accelerate the LED transition and expand into adjacent categories. Crompton Greaves, already a competitor, saw synergies in distribution and manufacturing.

The family's perspective was nuanced. For Jai Prakash Agarwal, this wasn't just a financial transaction—it was about legacy. The steel pipe business was the foundation, the original vision of his father B.D. Agarwal. Letting go of lighting, even partially, meant acknowledging that the diversification strategy of the 1980s had run its course. But keeping both businesses together risked mediocrity in both.

"We would like to submit that we have been suggested by investor community time and again on demerger of lighting and steel business for value creation for the stakeholder. However, presently the said information is speculative", the company stated publicly, maintaining strategic ambiguity while negotiations continued behind closed doors.

The operational challenges of demerger were daunting. The businesses shared everything from IT systems to working capital facilities. Key executives had responsibilities across both divisions. The Surya brand, carefully built over decades, would need to be allocated or shared. Manufacturing facilities in some locations produced both pipes and lighting components. Untangling these threads without disrupting operations required surgical precision.

Market dynamics added urgency. The LED transition was accelerating faster than anticipated. Chinese manufacturers were flooding the market with cheap products. Government tenders, once reliable revenue sources, were becoming cutthroat price battles. Meanwhile, the steel pipe business was entering a golden period—infrastructure spending was booming, oil and gas projects were multiplying, and the 3LPE coating capability was opening high-margin opportunities.

Hence, we believe the de-merger will benefit both the verticals as they will be able to focus on their core competencies and follow an independent growth trajectory. This wasn't corporate speak—it was recognition that the businesses had evolved beyond the point where common ownership added value. The lighting business needed a consumer-focused owner who could invest in brand building and distribution. The steel business needed patient capital for large infrastructure projects and technology upgrades.

The demerger process, however, would prove more complex than anyone anticipated. Regulatory approvals, tax implications, and most importantly, finding the right valuation that satisfied both the family and potential buyers, would stretch the process over years. By 2018, formal announcement of the business reorganization committee was made, but actual separation remained elusive.

What made this particularly interesting from a business strategy perspective was that unlike many conglomerate breakups driven by distress, Surya Roshni was splitting from a position of strength. Both businesses were profitable, growing, and had clear strategic paths forward. The demerger wasn't about survival—it was about unleashing potential that the current structure constrained.

Yet as we sit in 2024, the demerger remains unconsummated. The talks continue, valuations are debated, structures are proposed and rejected. Perhaps this limbo itself tells us something profound about family businesses in India—the difficulty of letting go, even when logic dictates otherwise. Or perhaps it reflects the complexity of unwinding fifty years of integration. Either way, the two businesses continue to coexist, like conjoined twins preparing for an inevitable but traumatic separation.

VIII. Financial Performance & Market Position Analysis

The numbers tell a story of transformation and resilience. Surya Roshni · Mkt Cap: 6,980 Crore (up 1.28% in 1 year) · Revenue: 7,435 Cr · Profit: 348 Cr. Behind these headline figures lies a complex narrative of two businesses pulling in different directions, yet somehow generating substantial value for shareholders. The company has delivered a poor sales growth of 6.34% over past five years, yet Company has delivered good profit growth of 27.8% CAGR over last 5 years. This apparent contradiction reveals the transformation happening beneath the surface—a shift from volume to value, from commodity to specialty products.

The trailing PE ratio is 19.10. Return on equity (ROE) is 15.08% and return on invested capital (ROIC) is 11.80%. These metrics position Surya Roshni in an interesting sweet spot—not cheap enough to be a value trap, not expensive enough to be priced for perfection. The market seems unsure how to value a company undergoing such fundamental change.

Company is almost debt free—a remarkable achievement for a capital-intensive manufacturing business. The company has 1.97 billion in cash and 734.00 million in debt, giving a net cash position of 1.24 billion. This fortress balance sheet provides optionality: the ability to invest in new technologies, weather commodity cycles, or return cash to shareholders without financial stress.

The segment-wise performance tells divergent stories. The steel pipes division, post-SGSTL merger and 3LPE capacity addition, has emerged as a cash generation machine. Operating margins in steel have expanded from low teens to high teens, driven by the shift to value-added products. The ability to charge premium pricing for API-grade and coated pipes has transformed what was once a commodity business.

Leading manufacturer of ERW GI Pipes in India. Also the leading exporter of ERW Pipes with a 60% market share. Leader in South India and among the top 3 in North India for GI Pipes. Ranked no. 1 in states such as AP, Telangana, MP, Chhattisgarh, UP, and Jharkhand. This market dominance translates into pricing power and preferential treatment in large tenders.

The lighting and consumer durables segment presents a more complex picture. Revenues have grown, but margins have compressed. The shift from high-margin conventional lighting to competitive LED products has pressured profitability. Consumer durables, while growing rapidly, operate at lower margins than the legacy lighting business. The segment contributes roughly 40% of revenues but less than 30% of operating profit.

The recent order worth Rs 116.15 crore from GAIL India for supplying coated pipes, expected to be executed over 39 weeks, exemplifies the strength of the steel division. These aren't commodity orders but specialized products requiring stringent quality certifications and coating technologies that few competitors can match.

Working capital management has been exemplary. Despite operating in industries with extended payment cycles—government contracts can take 90-120 days for payment—the company maintains healthy cash conversion. This is achieved through a combination of advance payments for export orders, channel financing arrangements with dealers, and strict inventory management.

The geographical revenue mix reveals strategic positioning. Domestic sales contribute approximately 75% of revenues, with exports accounting for the balance. Within India, the company has achieved remarkable state-level dominance—ranked number one in Andhra Pradesh, Telangana, Madhya Pradesh, Chhattisgarh, Uttar Pradesh, and Jharkhand for GI pipes. This isn't just market share; it's market control in regions where infrastructure spending is highest.

The quarterly volatility tells its own story. In Q2FY25, the company faced several challenges due to seasonal factors, price volatility, and geopolitical tensions affecting export markets. Nonetheless, the company has managed these headwinds through stringent operational efficiencies and proactive capacity expansion, with strategic initiatives in operational efficiency, high-margin product focus, and regional market expansion expected to support improved performance.

The capital allocation evolution has been dramatic. Five years ago, capital expenditure was evenly split between steel and lighting. Today, 70% of capex goes to steel—specifically to value-added capabilities like coating facilities and specialized pipe manufacturing. The company's commitment to enhancing production capacity through a ₹500 crore investment over three years aims to bolster its value-added product offerings.

The order book provides revenue visibility that most manufacturing companies can only dream of. With confirmed orders stretching 6-12 months, the steel division operates with predictability unusual in commodity businesses. Each GAIL or IOCL order represents not just revenue but validation of technical capabilities that took decades to build.

IX. Playbook: Lessons in Indian Manufacturing & Family Business

The Surya Roshni story offers a masterclass in building enduring value in unglamorous industries. The first lesson: boring is beautiful. While entrepreneurs chase the latest trends, companies that focus on essential, everyday products—pipes, lights, fans—build moats through reliability rather than innovation. Every building needs pipes. Every room needs lights. This constancy of demand provides stability that trendy businesses never achieve.

Backward integration in Indian manufacturing isn't just about cost control—it's about quality assurance in an environment where supplier reliability varies wildly. When Surya Roshni decided to manufacture glass shells, phosphor coatings, and filaments for lighting, they weren't just capturing margin. They were ensuring that every product met specifications in a market where "ISI mark" was often more aspiration than achievement.

The art of managing unrelated diversification emerges as perhaps the most nuanced lesson. Conventional wisdom says focus wins. Yet Surya Roshni thrived for decades running steel pipes and lighting simultaneously. The key wasn't synergy—there was little operational overlap. It was capital allocation discipline. When steel was booming, cash funded lighting expansion. When lighting margins compressed, steel carried the company. This portfolio approach, more mutual fund than manufacturer, provided resilience through cycles.

Distribution as competitive advantage in India requires understanding that the country isn't one market but hundreds of micro-markets. A dealer in Punjab operates differently from one in Tamil Nadu—credit terms, relationship dynamics, even business hours vary. Surya Roshni's 2,000-plus dealer network wasn't built through acquisition but through patient relationship building over decades. Each dealer relationship represented social capital that no amount of advertising could replicate.

The balance between family control and professional management presents another crucial insight. The Agarwals maintained strategic control while bringing in professional managers for operational roles. When technology expertise was needed for LED transition, they hired from competitors. When international market knowledge was required, they brought in export specialists. This hybrid model—family vision with professional execution—avoided both the stagnation of pure family management and the short-termism of pure professional management.

The Surya Foundation model demonstrates how social responsibility can be strategic advantage rather than cost center. In India's relationship-driven business environment, the Foundation's work—from Sainik Schools to think tanks—created networks that opened doors no lobbyist could unlock. When competing for government contracts, Surya Roshni's social credibility often tipped scales in their favor.

Export competitiveness from India requires a different playbook than domestic success. Surya Roshni learned that competing globally meant not just meeting specifications but understanding documentation, logistics, and payment mechanisms that domestic businesses never encounter. The Bhuj plant's location near ports wasn't coincidence—it was recognition that in exports, logistics costs often determine competitiveness more than manufacturing costs.

The technology adoption strategy offers lessons in pragmatism. Rather than pursuing cutting-edge innovation, Surya Roshni focused on proven technologies that could be implemented reliably. When they adopted Direct Forming Technology for steel sections, it wasn't the newest technology available—it was the most appropriate for their scale and capabilities. This "appropriate technology" approach avoided the costly failures that plague companies trying to leapfrog technological generations.

Managing commodity cycles requires financial discipline that goes beyond maintaining low debt. It means understanding that good times are temporary, that steel prices will crash just when you've expanded capacity, that new technologies will disrupt established products. Surya Roshni's ability to remain largely debt-free through multiple cycles wasn't luck—it was conscious choice to prioritize balance sheet strength over growth rates.

The governance evolution from founder-led to second-generation leadership illustrates successful succession planning. Jai Prakash Agarwal didn't just inherit the business—he transformed it, adding social consciousness through the Surya Foundation and professional management through external hiring. This evolution, from entrepreneur to institution, is where most family businesses fail. Surya Roshni navigated it while maintaining family values and entrepreneurial spirit.

Geographic expansion strategy teaches the importance of understanding regional economics. The Gwalior plant wasn't located there for tax benefits but because central India's infrastructure boom created local demand. The Bhuj facility leveraged Gujarat's port infrastructure for exports. Each location decision reflected deep understanding of regional comparative advantages rather than following incentives or conventional wisdom.

The brand architecture strategy—maintaining "Prakash Surya" for industrial products while creating "Surya" for consumer products—shows sophisticated market segmentation. Industrial buyers valued the heritage and reliability of Prakash Surya. Retail consumers wanted the modernity of Surya. Same company, different identities, each optimized for its audience.

Perhaps the most profound lesson is about patience. Building market leadership in pipes took two decades. Establishing credibility in lighting took another decade. These aren't Silicon Valley timescales. This is old-economy value creation, where competitive advantages compound slowly but surely. In an era of quarterly earnings obsession, Surya Roshni's half-century perspective offers a different model—one where time in market matters more than timing the market.

X. Bear vs. Bull Case & Future Outlook

Bull Case:

The infrastructure story in India isn't just beginning—it's accelerating. With the government targeting $1.4 trillion in infrastructure investment through 2025, demand for steel pipes will only intensify. Surya Roshni's positioning in high-value segments like oil and gas pipelines, where their 3LPE coating capability provides competitive advantage, means they capture disproportionate value from this spending boom.

The focus on value-added products fundamentally changes the business economics. API-grade pipes for petroleum applications command 30-40% premiums over commodity pipes. The 3LPE coating facility adds another 20-25% to realization. As the product mix shifts from 60% commodity to 40% specialty today, toward 30% commodity and 70% specialty in five years, margins will expand structurally.

The LED transition, while disruptive initially, is still in early innings. Penetration in rural India remains below 30%. Government programs like street lighting upgrades and agricultural pump energization create massive tender opportunities. Surya Roshni's established relationships with government buyers, proven execution capability, and financial strength to handle large contracts position them to capture disproportionate share.

Consumer durables penetration in India remains startlingly low. Fan penetration is only 60% versus 95% in China. Kitchen appliances are below 30% penetration. As electrification reaches rural areas and incomes rise, demand will explode. Surya Roshni's distribution network, already reaching 200,000 retailers, provides ready access to these emerging consumers.

The debt-free balance sheet represents optionality. With nearly ₹200 crore in net cash, the company could pursue acquisitions, accelerate capex, or return capital to shareholders. In a rising interest rate environment, zero debt becomes competitive advantage—competitors paying 10% for working capital while Surya Roshni funds from internal accruals.

The demerger catalyst, while delayed, remains inevitable. Whether through private equity partnership or strategic sale, unlocking value trapped in the conglomerate structure could rerate the entire entity. Based on peer valuations, the lighting business alone could be worth ₹1,500-2,000 crore, nearly 30% of current market cap.

Export opportunities are multiplying. Middle Eastern infrastructure spending, African urbanization, and Southeast Asian industrial growth create demand for exactly what Surya Roshni manufactures. The 60% market share in ERW pipe exports from India provides scale advantages in winning international contracts.

Bear Case:

The poor sales growth of 6.34% over five years cannot be ignored. In a country growing at 7% nominally, growing at less than inflation means losing relevance. This isn't just one bad year—it's a pattern suggesting structural challenges in the business model.

Commodity business exposure remains significant despite all talk of value addition. Steel pipes, even specialized ones, remain subject to raw material price volatility, import competition, and capacity additions by competitors. When steel prices spike, margins compress. When they fall, inventory losses mount. This cyclicality is inescapable.

Competition is intensifying across all segments. In steel pipes, Jindal, Tata, and APL Apollo are expanding aggressively. In lighting, Havells, Philips, and Crompton have deeper pockets and stronger brands. In consumer durables, established players have decades of brand equity. Surya Roshni is perpetually playing catch-up.

The demerger execution risk looms large. After years of speculation, no deal has materialized. This suggests either valuation mismatches, regulatory complications, or family reluctance to cede control. Each passing quarter without resolution increases uncertainty and management distraction.

Technology disruption threats are real. In lighting, smart home integration and IoT capabilities are becoming table stakes. Surya Roshni lacks the R&D capability to compete with global majors. In steel pipes, new materials like composites and plastics are replacing metal in many applications.

Market saturation in core segments is approaching. The easy infrastructure wins—rural electrification, basic water supply, highway construction—are largely complete. Future growth requires competing for replacement demand or entering new segments where Surya Roshni lacks expertise.

Working capital intensity remains high despite operational improvements. The business requires constant capital infusion to grow. Unlike asset-light businesses that scale with minimal investment, manufacturing requires proportional capital for each unit of growth.

Management succession uncertainty exists. While professional managers run operations, strategic decisions remain with the family. As third generation enters the business, questions about vision, capability, and commitment arise. Family businesses often struggle with third-generation transition.

The absence of a clear moat is concerning. Unlike businesses with network effects, switching costs, or technological advantages, Surya Roshni's advantages—distribution, relationships, manufacturing scale—can be replicated with sufficient capital and time.

Margin pressure across segments suggests commoditization. LED lighting has become a commodity. Fans are sold on EMI schemes. Even specialized pipes face import competition from China. When products commoditize, only the lowest-cost producer survives profitably.

Future Outlook:

The next five years will determine whether Surya Roshni transforms from a diversified conglomerate to focused specialists or continues straddling multiple businesses. The demerger, whenever it happens, will be pivotal. A successful separation could unlock significant value and allow each business to pursue optimal strategies.

The steel pipes business appears best positioned for growth. Infrastructure spending, oil and gas expansion, and water supply projects provide multi-decade demand visibility. The shift toward value-added products and export markets reduces commodity risk. This could emerge as a ₹10,000 crore revenue business by 2030.

The lighting and consumer durables face harder questions. Without significant brand investment and technology upgrades, maintaining market position will be challenging. Partnership with a strategic investor—whether Crompton, Havells, or private equity—seems inevitable for this division to remain competitive.

Geographic expansion beyond India represents the next frontier. Middle Eastern infrastructure, African urbanization, and Southeast Asian industrialization offer growth opportunities that could offset domestic saturation. But succeeding internationally requires capabilities—project management, financing, logistics—that need development.

The ultimate question is whether Surya Roshni can transition from being a successful family business to an enduring institution. This requires professional governance, clear strategy, and most importantly, willingness to make hard choices about where to compete and where to exit. The building blocks are there—strong market positions, debt-free balance sheet, established brands. What's needed is strategic clarity and execution excellence.

XI. Epilogue & Reflections

As we conclude this journey through five decades of Surya Roshni's evolution, what emerges is a story larger than one company. This is the narrative of Indian industrialization itself—messy, opportunistic, relationship-driven, yet ultimately successful in creating enormous value. The unsung heroes of Indian economic development aren't the software giants or unicorn startups but companies like Surya Roshni that built the physical infrastructure enabling modern life.

What Surya Roshni tells us about building in India is that success requires a different playbook than Western business schools teach. It's not about disruption or first-mover advantages. It's about patience, relationships, and the ability to navigate complexity that would paralyze companies from more orderly business environments. The License Raj, rather than being purely restrictive, created opportunities for those who could master its intricacies. Family ownership, often seen as liability, provided stability through cycles that would have destroyed quarterly-earnings-focused public companies.

Compared to global peers, Surya Roshni's journey seems almost quaint. While Vallourec or Tenaris built global steel pipe empires through acquisition and technology leadership, Surya Roshni grew organically in one market. While Philips and Osram pursued lighting innovation at the frontier, Surya Roshni focused on manufacturing reliability. Yet this "small ball" approach—singles and doubles rather than home runs—created substantial value with minimal risk.

The future of manufacturing in India will be shaped by companies that can bridge the old and new economies. Surya Roshni's challenge is evolving from a manufacturing company that happens to use technology to a technology company that happens to manufacture. This isn't about adopting buzzwords like Industry 4.0 or IoT. It's about fundamental transformation in how value is created and captured.

The key takeaways for entrepreneurs transcend industry boundaries. First, unglamorous sectors often offer the best risk-adjusted returns because competition is rational and demand is stable. Second, in emerging markets, distribution and relationships matter more than product differentiation. Third, patient capital and conservative leverage create options that aggressive financing destroys. Fourth, social capital, built through genuine community engagement, provides returns that don't appear on balance sheets but determine business success.

For investors, Surya Roshni illustrates the complexity of valuing conglomerates. The sum-of-parts often exceeds the whole, but realizing that value requires catalysts that may never materialize. The company trades at a discount to both its asset value and earnings potential, but such discounts can persist indefinitely without forcing events. This isn't inefficient markets—it's markets rationally pricing execution uncertainty.

The deeper lesson is about the nature of business building itself. In an era obsessed with unicorns and exponential growth, Surya Roshni represents an older model—the rhino rather than unicorn. Slower, steadier, more resilient. Not as exciting perhaps, but more likely to survive and compound value over generations. The company's ₹7,000 crore market capitalization, built over fifty years, may seem modest compared to startups valued at billions within years. But it's real value, backed by assets, cash flows, and market positions that will endure long after today's unicorns have become cautionary tales.

As India stands at an inflection point—poised to become the world's third-largest economy, urbanizing rapidly, building infrastructure at unprecedented scale—companies like Surya Roshni will play crucial but uncelebrated roles. They won't feature in business school case studies or technology conferences. But they'll manufacture the pipes carrying water to new cities, the lights illuminating new homes, the fans cooling new offices. This is the real economy, where value creation is measured not in valuations but in tangible improvements to human life.

The Surya Roshni story ultimately is about transformation—of a family business into an institution, of a single-product company into a conglomerate, of a domestic player into an exporter. But most importantly, it's about the transformation of India itself, from a capital-starved, infrastructure-poor nation to an emerging industrial power. Companies like Surya Roshni didn't just witness this transformation—they enabled it, one pipe and light at a time.

Whether the next chapter brings successful demerger, strategic partnerships, or continued independent evolution, Surya Roshni has already secured its place in Indian industrial history. Not as a pioneer or disruptor, but as a builder—patient, persistent, profitable. In a business environment that often rewards style over substance, Surya Roshni chose substance. In a world of quarterly thinking, they thought in decades. In a market that celebrates exits, they chose to build and stay.

This is perhaps the most important lesson: that building enduring value requires not just vision and execution but also the courage to be boring, the patience to compound slowly, and the wisdom to recognize that the best businesses are often those that everyone else overlooks. Surya Roshni found opportunity in the unglamorous, value in the essential, and built an empire from the everyday. That's a playbook worth studying, a legacy worth honoring, and a future worth watching.

XII. Recent News

The recent developments at Surya Roshni paint a picture of a company in transition yet maintaining operational momentum. The April 2024 announcement of a Rs 116.15 crore order from GAIL India Limited for the supply of coated pipes for projects located in Madhya Pradesh and Uttar Pradesh demonstrates continued strength in the oil and gas segment. The contract involves the delivery of HFW 355.60 X 8.7 & 10.3 WT, GR X-70 PSL-2 coated pipes, highlighting the company's capability in high-specification products.

Financial performance shows resilience despite challenges. Revenue jumped 3.23% year-over-year to ₹2,154.88 Cr in Q4 2024-2025, with a quarterly growth of 15%. More impressively, net profit jumped 25.18% year-over-year to ₹130.09 Cr, with a quarterly growth of 44.71%, suggesting improving operational efficiency and margin expansion.

Corporate actions have been shareholder-friendly. The company fixed January 1, 2025, as the record date for the issuance of bonus shares in the ratio of 1:1, effectively doubling shareholders' holdings. Additionally, the firm announced a dividend of Rs 2.5 per share, demonstrating confidence in cash generation despite capital expenditure requirements.

Management commentary remains cautiously optimistic. The company stated it remains well-positioned to drive growth and value creation in the Steel Pipe business and remains optimistic for coming quarters, driven by a robust order pipeline in the professional lighting segment and sustained demand in consumer durables.

Product innovation continues with Surya Roshni launching Turbo Flex wires, Cubis digital heater with 5-star rating and 7-year warranty, and Prakash water tank with 10-year warranty, showing commitment to expanding the value-added product portfolio.

However, governance issues have surfaced with BSE and NSE fining Surya Roshni Rs 2.80L each (Rs 5.60L total) for delayed independent director appointment, highlighting the need for stronger compliance mechanisms as the company transitions from family-run to institutionally-governed entity.

XIII. Links & Resources

Company Resources: - Annual Reports: Available on BSE/NSE websites and company investor relations section - Investor Presentations: Quarterly updates on financial performance and strategic initiatives - Surya Foundation Publications: Documenting social initiatives and impact since 1992

Industry Analysis: - Steel Pipe Industry Reports by CRISIL and ICRA - Indian Lighting Industry Analysis by ELCOMA (Electric Lamp and Component Manufacturers Association) - Infrastructure Sector Reports by India Infrastructure Research

Books on Indian Family Businesses: - "The Tatas, Freddie Mercury and Other Bawas" by Coomi Kapoor - "Business Maharajas" by Gita Piramal - "The Marwaris: From Jagat Seth to the Birlas" by Thomas A. Timberg

Government Policy Documents: - National Infrastructure Pipeline (NIP) Reports - Make in India Manufacturing Policy Documents - Bureau of Indian Standards specifications for pipes and lighting

Technical Resources: - API (American Petroleum Institute) Standards for Line Pipes - IS (Indian Standards) specifications for ERW and GI pipes - LED Technology Evolution papers from IEEE

Historical Context: - "India After Gandhi" by Ramachandra Guha (for understanding post-independence industrialization) - "India Unbound" by Gurcharan Das (on economic liberalization) - Economic Survey Archives from Ministry of Finance

Competitor Analysis: - APL Apollo Tubes investor presentations - Jindal SAW annual reports - Havells India equity research reports - Crompton Greaves Consumer Electricals quarterly results

Market Research: - India Brand Equity Foundation (IBEF) reports on manufacturing - McKinsey Global Institute's reports on India infrastructure - World Steel Association statistics

Podcast Episodes on Related Topics: - "WTF is with Indian Manufacturing?" - various episodes on Indian industry - "Building in India" - conversations with industrial entrepreneurs - "The Seen and the Unseen" episodes on Indian economy

Academic Papers: - "Family Firms and Economic Development" - IIM Ahmedabad Working Papers - "Diversification Strategies in Emerging Markets" - Journal of Business Research - "The Evolution of Indian Conglomerates" - Economic and Political Weekly

This comprehensive resource list provides multiple perspectives on understanding not just Surya Roshni but the broader context of Indian industrialization, family business evolution, and manufacturing sector dynamics that shaped the company's journey and will determine its future.

[End of Article]

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube