Suprajit Engineering: The Global Puppet Master of Mechanical Controls

I. Introduction & The "Invisible" Giant

Picture a Tuesday morning rush in suburban Munich. A commuter slides into the driver's seat of a Volkswagen Polo, tugs the lever beside the seat to adjust the height, and pulls the parking brake. Three thousand kilometres south, a delivery rider in Chennai swings a leg over a TVS Jupiter, squeezes the front brake, and rolls the throttle. Five thousand miles west, a homeowner in suburban Kansas yanks the starter cord on a John Deere lawnmower to attack the weekend grass. Three different continents. Three different machines. Three different price points. And in all three, the small, unsexy, jacketed steel wire that translates human force into mechanical action almost certainly bears the same stamped origin: a sprawling cluster of plants headquartered in ಬೆಂಗಳೂರು Bengaluru, India.

That stamp belongs to Suprajit Engineering Limited, and it is one of the most quietly consequential industrial stories that almost no consumer has ever heard of. The company moved from a single-product garage operation in 1985 to become the world's second-largest manufacturer of automotive control cables, with manufacturing on four continents and customer logos that read like a roll-call of the global auto industry: Ford, Volkswagen, Stellantis, Tata, Maruti, Bajaj, TVS, Hero, Renault, Briggs & Stratton, and Husqvarna among them.1 By the close of FY2024 the group had crossed ₹2,950 crore in consolidated revenue, employed more than 13,000 people, and operated 22 plants across India, the United States, Mexico, the United Kingdom, Hungary, Germany, China, and Italy.1

The hook here is not that Suprajit makes cables. The hook is that cables — humble, mid-tech, low-margin commodity-sounding cables — turned out to be a perfect structural moat once you understood the customer. A modern passenger vehicle contains anywhere from 15 to 30 Bowden cables. Each one is engineered to fit a specific chassis, validated over 18 to 24 months, qualified through cyclic-load and salt-spray and thermal-shock tests that mimic 10 to 15 years of customer abuse, and then locked into a Bill of Materials that nobody at the OEM has any incentive to disturb. Once you are in the part-number, you are in for the life of the platform. Once you are in for the life of the platform, the OEM's cost-down negotiator has to look elsewhere for his annual scalp. And once you are scaled enough to serve a global OEM across three continents simultaneously, the regional players quietly fall away.

The thesis we will walk through in this episode is straightforward: Suprajit was built by founder ಅಜಿತ್ ಕುಮಾರ್ ರೈ Ajith Kumar Rai on a single, almost stubborn idea — that the boring parts of a vehicle, taken seriously, would compound into a global franchise long after the glamour categories had been competed away.2 The company then layered three big bets on top of that base: a 2002 pivot from two-wheelers into passenger vehicles, a 2015–2024 acquisition spree that turned a domestic vendor into a global oligopolist, and a quiet, deliberately under-marketed buildup of an in-house electronics division that exists to cannibalise the very cable business it lives inside.

What follows is an examination of how a family-led Indian firm, operating out of a city better known for software than steel, executed surgical M&A in the global "boring but essential" hardware space — and why the next five years for this company will be more interesting than the last fifteen. We will trace the founding story and the 1995 inflection that took the company public, walk through the playbook deals at Phoenix Lamps, Wescon, Kongsberg LDC, and SCS Stahlschmidt, profile the management trio that runs the place today, and then sit with the genuinely existential question that hangs over the entire enterprise: what happens to a cable company when the world goes drive-by-wire? Suprajit's answer to that question is the most important thing to understand about the stock, and it has nothing to do with cables at all.

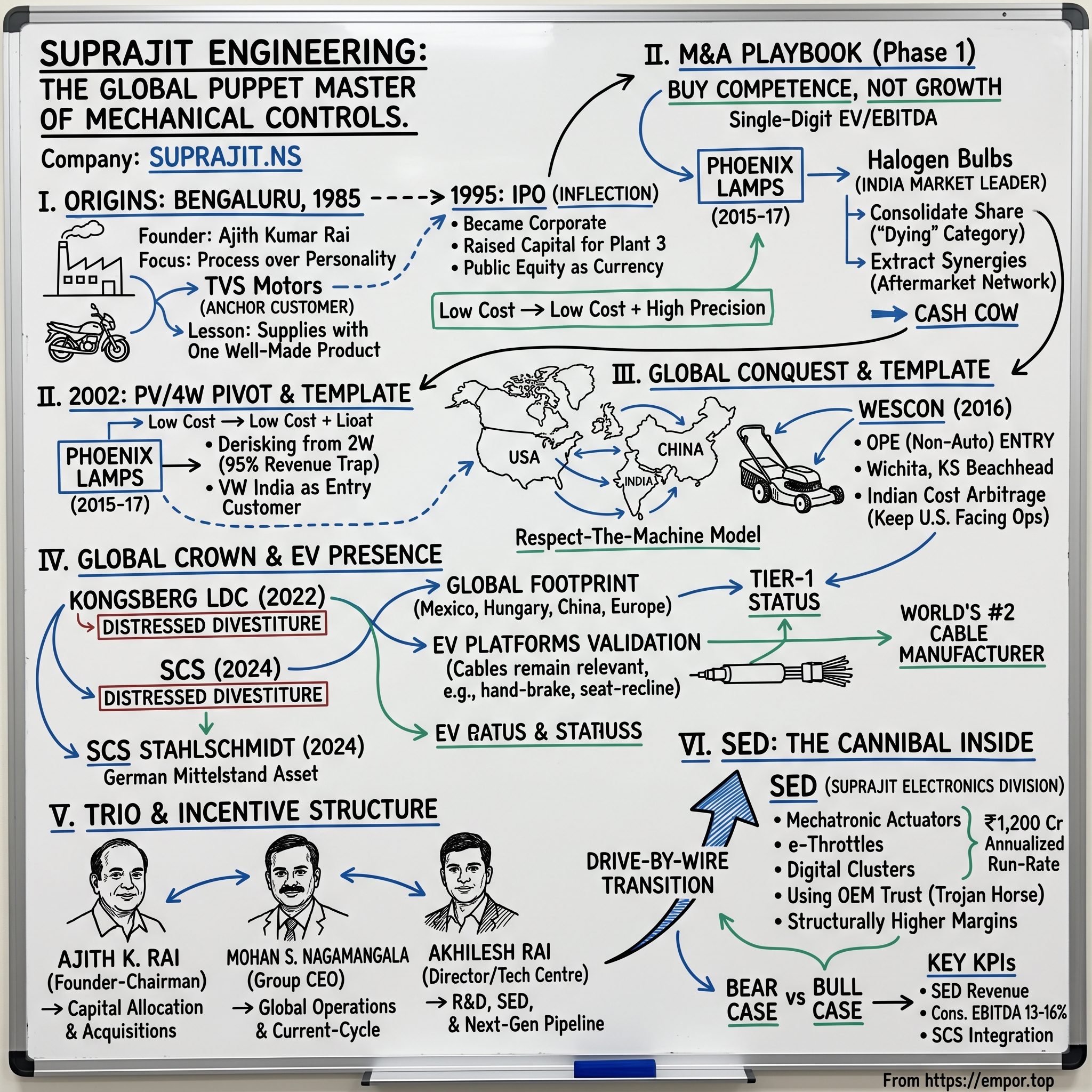

II. Origins: The TVS Connection & The 1995 Inflection

The year was 1985. India's economy was still a closed shop. The Maruti 800 had only been on sale for two years, the Bajaj Chetak scooter was the dominant aspirational good for the middle class, and an Indian engineer with global ambitions had essentially two career paths: take a flight out, or find a domestic patron and grind. Ajith Kumar Rai chose the second. He had spent the early part of his career at TI Cycles of India and had absorbed two lessons that would shape the rest of his life: first, that supplying a single anchor customer with one well-made product was a perfectly acceptable place to start a manufacturing company; and second, that India in the 1980s had a deep talent advantage in engineering hidden under a thick layer of regulatory dysfunction. He bet the rest of his career on both lessons at once.2

Suprajit's first factory was a modest single-shed operation in Bengaluru. The first product was a liner cable assembly. The first and essentially only customer was TVS Motors, then a regional motorcycle and scooter maker that would over the next two decades become one of the largest two-wheeler companies in the world. The relationship was symbiotic in the way that early-stage Indian industrial relationships tended to be — TVS got a hungry, technically competent, locally based vendor it could mould to its quality systems; Rai got the cash flow and the production discipline that came with feeding an OEM that did not tolerate excuses. This was not the kind of founder-customer pairing that lent itself to TED talks. It was however the kind that lent itself to compounding, because every year of zero-defect deliveries earned Suprajit another part-number, another platform, another inch of share of wallet.2

What separated Rai from the typical first-generation Indian industrialist of the 1980s was a stubborn insistence on process over personality. The standard pattern in Indian small-cap manufacturing at that time was promoter-led, family-staffed, gut-driven, and allergic to delegation. Rai pushed in the opposite direction almost from day one. He hired professional managers, instituted process audits, and insisted on what he later called the "boring monthly review" — a discipline that, in interviews years later, he credited with the company's ability to integrate factories on three continents without imploding.2 This was not glamorous; it was, in fact, the opposite of glamour. But it built a chassis that would later support some surprisingly ambitious global moves.

The first inflection came in 1995, when Suprajit listed its shares on the Indian stock exchanges to raise capital for a third manufacturing plant.3 In hindsight, the IPO was the moment Suprajit stopped being a vendor and started becoming a corporate. The discipline of quarterly disclosure forced a level of governance that family-run competitors of the era simply did not impose on themselves. It also gave Rai a currency — public equity — that he would deploy with surgical patience two decades later when global assets started coming up for sale at distressed prices. For most of the 1990s, however, the company stayed in its lane: cables, scooters, motorcycles, and the relentless mechanical reliability that comes from doing the same thing very well, every day, for years.

Then came 2002, and the moment Rai later described as recognising the company's "death trap". By the turn of the millennium, Suprajit derived roughly 95% of revenue from two-wheelers, almost all of it Indian.2 A single bad monsoon, a single fuel price shock, a single regulatory rule change on emissions, and the company's earnings would have cratered. The pivot, when it came, was deliberate: Rai targeted the four-wheeler passenger vehicle segment, and the entry-customer he chose was Volkswagen India. The decision was not commercially obvious. Passenger-vehicle cables required tolerances an order of magnitude tighter than scooter cables, and the validation cycles were measured in years rather than months. But the prize on the other side of that grind was access to a global supply chain — because if you were on a VW chassis in Pune, you could be on the same chassis in Puebla. The 4W pivot transformed Suprajit's DNA from "low cost" to "low cost plus high precision", and it set up everything that came next.2

A founder who started with one customer, listed his company before he needed to, and then spent the entire 2000s methodically derisking — that is the chassis on which the next chapter of acquisitions was built.

III. M&A Playbook Phase 1: Beyond Cables & Phoenix Lamps

The first thing to understand about Suprajit's M&A approach is that it almost never bought what was fashionable. In a market obsessed with growth multiples and category leaders, Rai and his team developed a near-religious attachment to two ideas: buy at single-digit EV/EBITDA, and buy categories that the consensus had already written obituaries for. The Phoenix Lamps acquisition in 2015 was the perfect crystallisation of both.4

Phoenix Lamps was, on paper, a strange asset. It was India's largest manufacturer of automotive halogen bulbs, with roots going back to a Halonix-branded operation and a dominant share of the Indian aftermarket. By 2015, however, the auto-lighting world had decided that halogen was over. LEDs were coming, were cheaper to run, lasted longer, and looked better; the industry-press consensus was that halogen was a melting ice cube on a 5–10 year fade. Argonaut Private Equity, which had owned Phoenix Lamps since acquiring it from the previous promoter group in 2010, was a motivated seller. The asset was profitable, generating roughly 14–16% EBITDA margins, with a strong aftermarket franchise and meaningful exports — but it was unloved.4

Suprajit paid roughly 6.7x EV/EBITDA for the deal, completing the acquisition of a controlling stake and then merging Phoenix Lamps into Suprajit Engineering by an order of the National Company Law Tribunal that took effect in 2017.4 The multiple is the entire story. Indian auto-ancillary peers at the time were trading in the low teens on EV/EBITDA. Global auto-lighting peers were higher still. A market leader in a "dying" category was available at less than half the going rate, and Rai walked in and paid the asking price because he had a thesis the seller did not believe in.

That thesis had two prongs. First, the Indian car parc was not a U.S. car parc. The installed base of halogen-equipped vehicles in India was vast, growing, and lived in a market where a ₹150 replacement bulb was a routine purchase and a ₹1,500 LED retrofit was not. The aftermarket runway for halogen replacements in India alone, Rai argued internally, was twenty years. Second, Suprajit's distribution network — fifty thousand-plus retailers built around brake cables and accelerator cables — was almost perfectly congruent with the auto-lighting aftermarket. The kirana mechanic who replaced a clutch cable also replaced a headlamp bulb. By layering Phoenix onto the same trucks and the same dealers, Suprajit could extract synergies the previous private-equity owner had no way to access.[^5]

The market hated it. Sell-side analysts who covered the deal published notes asking, in not-particularly-veiled language, why a perfectly good cables franchise was wasting capital on a category that LEDs would euthanise. Management's answer became something of a refrain at investor conferences over the following five years: "The aftermarket for halogens will last twenty years. We will be the last man standing." It was a cash-cow play, executed with full knowledge that being the last man standing in a shrinking category is sometimes the most profitable place on the entire battlefield. While competitors abandoned halogen capacity to chase LED, Suprajit consolidated share, kept utilisation high, and used the cash generation to fund the next set of acquisitions.[^5]

By FY2024, the lighting business — by then rebranded inside the group as the Suprajit Technology Centre and broadened into LED and electronic lighting through internal R&D — was contributing meaningfully to consolidated EBITDA and had become a textbook example of what Rai called "buying competence, not growth".1 The Phoenix deal also normalised something subtler inside the organisation: the idea that Suprajit could integrate a public-company-sized asset, restructure its capital, merge its legal entity, and pull cost out without breaking the operations. That muscle would matter a lot in the deals that followed.

If Phoenix Lamps was the first proof of the playbook, what came next was the moment Suprajit decided to take the same playbook global.

IV. Global Conquest: Wescon & The North American Beachhead

Wichita, Kansas in 2016 was not where most Indian acquirers were looking for deals. The American industrial Midwest in the mid-2010s was a tough place to be a mid-sized specialty manufacturer — Chinese competition had eaten into the lawn-and-garden equipment supply base, private-equity owners had largely run their cost-out playbooks, and the demographic profile of the engineering workforce was older than anyone wanted to admit. Wescon Controls, a Kansas-headquartered specialist in cable-and-control assemblies for what the industry calls Outdoor Power Equipment — lawnmowers, snowblowers, leaf blowers, riding mowers, agricultural and construction OEMs — fit that profile almost exactly. It was a category leader. It was a quality operation. It was tired.5

Suprajit announced the Wescon acquisition in September 2016 at a deal value of $44 million, funded through a combination of internal accruals and offshore debt.5 The purchase price worked out to roughly 7x EV/EBITDA, which, benchmarked against the typical 10–12x range that U.S. specialty industrial assets commanded at the time, was an unambiguous bargain. The seller was a financial owner; the buyer was a strategic one with a low-cost manufacturing base in India and a stated intention to keep the U.S. operation running. The handshake worked.

The strategic logic was layered. On the surface, Wescon delivered three things Suprajit could not buy in any other way: direct OEM relationships with Briggs & Stratton, Husqvarna, John Deere, MTD, Toro, and the rest of the U.S. OPE customer base; a Kansas-based manufacturing footprint with deep customer trust; and an entry into a non-automotive end-market that ran on a completely different demand cycle from passenger cars. Lawnmowers do not care about car-sales recessions. Snowblowers do not correlate with motorbike registrations in Maharashtra. The Wescon deal cleanly broadened Suprajit's revenue mix away from its automotive concentration in a way that organic expansion could not have replicated in any reasonable time frame.5

The deeper logic, however, was cost arbitrage. The OPE business had been quietly outsourcing low-complexity cable production to Mexico and China for a decade, but the wage gap between a Kansas line worker and a Bengaluru line worker was, even after freight, a structural margin opportunity that nobody else was positioned to exploit. Suprajit's playbook — and this was a recurring move across all of its overseas deals — was to keep the customer-facing operations in the acquired geography, but to gradually migrate the high-volume, low-complexity production lines back to India and dual-source out of Mexico for the remainder. The customer never lost a single delivery window. The cost curve, however, bent in Suprajit's favour quarter after quarter.

Cultural integration was the part of the deal that the financial press underestimated. The American industrial heartland is famously sceptical of foreign acquirers, and acquirers from emerging markets in particular get watched closely for signs of "stripping the plant". Rai's approach was old-school: he flew to Wichita, met every senior employee, kept the U.S. management team in place with retention packages, and made an early visible decision not to close the Kansas plant. The plant was upgraded, capex was actually increased in the first two years post-deal, and the local press coverage of the new Indian owner turned, somewhat improbably, friendly. Inside the Suprajit holding structure, Wescon became the template for what would later be called the "respect-the-machine" model: do not assume your way is better; learn what works; then surgically apply the cost base advantage where it does not damage the customer relationship.1

By FY2024, the Wescon platform — together with the post-2022 Kongsberg LDC integration — represented the bulk of Suprajit's non-India revenue, which had grown to around 45% of group consolidated sales.1 The Wescon deal also seeded something more important than revenue: it normalised, internally, the idea that Suprajit could buy, hold, and run an American business through Indian ownership without breaking either side. The next deal would scale that template by an order of magnitude.

V. The Global Crown: Kongsberg LDC & SCS

By the early 2020s, Suprajit was the dominant cable player in India, a meaningful one in the U.S. OPE market, and a top-five global player overall — but it was not yet on the table when global Tier-1 cable contracts were awarded. The acquisition that changed that arrived in April 2022, and it carried a name that nobody outside the industry recognised but everybody inside it did: Kongsberg Automotive's Light Duty Cables division.[^7]

Kongsberg Automotive, the Norwegian-listed Tier-1, had spent the previous decade restructuring its portfolio. The LDC business — light-duty mechanical cables for global passenger vehicles — was non-core to Kongsberg's preferred direction, which was higher-margin electronic and fluid-transfer systems. For Suprajit, it was the exact opposite: an absolute strategic gift. The asset came with plants in Mexico, Hungary, and China; a global engineering team headquartered in Pravia, Spain; pre-qualified status on platforms at Ford, Stellantis, Daimler, Volkswagen, Renault, and several global Tier-1 seat-systems vendors; and book-of-business contracts that ran years into the future. The purchase price was $42 million, financed primarily through internal accruals and a modest debt drawdown.[^7]

The headline number deserves a moment. Suprajit paid roughly the same dollar amount for the Kongsberg LDC business in 2022 as it had paid for Wescon in 2016 — but Kongsberg LDC came with multi-continent footprint, blue-chip global OEM contracts, and revenue that was several times larger than Wescon's. It was, in effect, a distressed-divestiture price for what should have been a strategic-buyer asset. Kongsberg wanted to exit the category; nobody else credible was bidding on a global-scale low-margin cable platform; Suprajit walked in with the integration playbook from Wescon already battle-tested and walked out with the keys to a global business.[^7]

The "Tesla moment" inside the deal was less about Tesla specifically and more about EV platforms broadly. Mechanical cables, contrary to the headline thesis, do not disappear in an EV — there is no clutch cable or accelerator cable, but there are still hand-brake cables, hood cables, seat-recline cables, charging-port-release cables, and trunk-release cables. Inheriting the Kongsberg LDC contracts gave Suprajit immediate, qualified presence on the cable bill-of-materials of every major global EV programme, exactly at the moment that those programmes were ramping. Within two years of the closing, Suprajit was the world's number-two cable manufacturer by volume, behind only Hi-Lex of Japan.1

The integration ran the same playbook as Wescon, scaled up. Customer-facing engineering stayed in Europe. Mexico stayed as the North American near-shoring hub. The Hungarian plant became the European hub. The Chinese operation stayed local-for-local. And Bengaluru gradually absorbed the high-volume, low-complexity SKUs. EBITDA margins on the acquired business, which had been in the low single digits at closing, expanded meaningfully over the following 18 months as Suprajit rationalised the SKU portfolio and renegotiated raw-material contracts at the larger consolidated scale.1

Then, in May 2024, Suprajit announced its next move: the acquisition of Germany's Stahlschmidt Cable Systems (SCS) out of insolvency proceedings for an enterprise value of €13.5 million.6 SCS was a 100-year-old engineering name, headquartered in Wuppertal, with plants in Germany and Morocco and a customer book that included multiple German Tier-1s and OEMs. It had run aground on the combined pressure of European energy costs, German labour rigidity, and the slow EV transition shock that had hit the entire German Mittelstand auto-supplier base.

The purchase price worked out to roughly 0.27x trailing sales — a number that, in any other context, would suggest the buyer was getting a dumpster fire. The Suprajit thesis was the same thesis it had run twice before: the customer relationships were worth more than the German cost base implied, and the Moroccan footprint was a near-shoring asset for Europe that mirrored the Mexico-for-U.S. and India-for-India templates the group had already perfected.6 Whether SCS ultimately becomes a Wescon-style success or a slower-burn integration is a story still being written in 2025 and 2026, but the structural logic — buy distressed European footprint, lean on Moroccan and Indian cost bases, retain the customer trust — is consistent.

Three deals across nine years, all at single-digit multiples, all in categories the consensus had written off, all stitched into the same global manufacturing chassis. The acquisition compounding here is genuinely rare, and it sets up the question of who exactly was making these calls.

VI. Management Analysis: The Trio & The Incentive Structure

Walking into the Suprajit head office in Bengaluru, the first thing visitors typically notice is what is not there. No marble lobby. No commissioned art. No "wall of fame" with photographs of the chairman shaking hands with prime ministers. The corporate office is a functional building attached to the original manufacturing plant, the conference rooms are named after engineering concepts, and the chairman's office is, by reliable account, the same one Ajith Kumar Rai has occupied since the late 1990s. This is not asceticism for its own sake; it is a deliberate signal. Frugality, in Rai's framing, was always the virtue. Quality was always the mandate. Anything else was overhead.2

Rai himself is the patriarch of the operation. Born and educated in coastal Karnataka, trained as an engineer, and shaped by the small-town discipline of South Indian middle-class professional life, he ran Suprajit as managing director from founding through 2019, when he stepped back from day-to-day operations to focus, in his own words, on "the ten-year picture".2 The transition was not theatrical — there was no Jack Welch-style succession spectacle — but it was substantive. Rai retained the chairmanship and the strategic agenda, but the operating cockpit moved to a professional management team that he had spent the better part of a decade quietly building.

The professional CEO is Mohan Srinivasan Nagamangala, who took over as Managing Director and Group CEO. Mohan's background is the antithesis of the Indian promoter-mafia model: trained in mechanical engineering, with multi-decade career stops at global Tier-1 suppliers including Bosch and ZF Friedrichshafen, and exposure to both European and Asian manufacturing cultures. He arrived at Suprajit with the credibility of someone who had seen how the global majors ran their plants and the willingness to import that thinking without breaking the founder-led culture that had built the company.1 His compensation is structured around base, performance-linked annual bonus (roughly 20% of base in target-hit years), and a stock-option overlay that aligns his outcomes with shareholder returns rather than purely with topline growth — a non-trivial design choice in an industry where revenue-chasing has destroyed plenty of value.

The third leg of the management trio is Akhilesh Rai, the founder's son, who serves as a director and heads the Technology Centre. Akhilesh's portfolio is deliberately forward-looking: he runs the in-house electronics R&D programme, oversees the Suprajit Technology Centre that anchors the company's product development across cables, lighting, and mechatronics, and is widely understood inside the company to be the eventual stewardship figure for the next generation. The succession architecture here is unusual in Indian family-business contexts. Rather than placing the next-generation family member directly in the operating CEO seat, the company split the role: professional CEO runs operations and current-cycle execution; family director runs technology, R&D, and the long-cycle product pipeline.1 Founder-Chairman supervises capital allocation and acquisitions. The clean separation reduces the standard family-business risk that the next generation gets handed a job they are not yet ready for and breaks the asset on the way to learning how to run it.

Skin in the game runs deep. The Rai family promoter group owns approximately 38.5% of the company on a fully diluted basis, and the family has been a consistent net buyer of shares from the open market through 2024, 2025, and into early 2026 — including disclosed promoter purchases as recently as March 2026.7 In a market where Indian promoters have a habit of pledging shares against personal debt or trimming holdings into rallies, the Suprajit promoters have done the opposite for more than a decade. The signal is unambiguous: the family believes the long-cycle compounding story is in front of them, not behind them.

There is a cultural footnote worth dwelling on, because it explains why this management structure has held together as well as it has. Rai is famously allergic to what he has called, in investor calls and informal settings, "performative ambition". He does not announce three-year guidance numbers. He does not preannounce acquisitions before they close. He does not hold quarterly press conferences to announce strategic initiatives. The investor presentations are dense, technical, and largely unchanged in format from year to year. What changes are the numbers underneath. That patience — the willingness to be boring on the surface while compounding underneath — is the cultural through-line that explains both why the company has been undervalued by the market for stretches of its history and why the people running it appear to enjoy that fact rather than fight it.

A leadership team that thinks in decades, an incentive structure that ties professional managers to shareholder outcomes, and a founder who chose to step aside while still alive and engaged — this is the operating context for the most important strategic bet currently underway inside the company.

VII. The "Hidden" Business: Suprajit Electronics Division (SED)

There is a question that hangs over every conversation about Suprajit, and every careful investor in the stock has had to confront it: what happens to a cable company when the world goes drive-by-wire? It is the single most important strategic question facing the business, and the management's answer is the most interesting thing about the entire enterprise.

The "drive-by-wire" thesis is straightforward in its mechanics. As vehicles electrify and digitise, mechanical control linkages are replaced by electronic actuators and signal wires. The throttle cable becomes an electronic throttle. The clutch cable disappears (because the EV has no clutch). The gear-shift cable becomes a shift-by-wire pushbutton. The parking-brake cable becomes an electric park-brake actuator with a motor and a control unit. In the limit case, an EV could theoretically have half the cable count of an internal-combustion vehicle. For a company that derives the bulk of its revenue from mechanical control cables, this is not an abstract threat; it is the central existential risk of the business model.[^10]

Suprajit's answer was the Suprajit Electronics Division, internally referred to as SED, which has been quietly built up inside the group over the past several years. The strategic insight here is subtle and worth slowing down on. Rai's framing, repeated across investor interactions, was that the company had two choices: either passively defend the cable franchise and watch it erode as platforms electrified, or actively build the electronic-actuator replacement business and use the existing OEM relationships to land the new products on the same vehicle platforms. They chose the second.[^10]

SED's product portfolio reads like a deliberate map of the cable bill-of-materials, translated into electronics. Digital instrument clusters for two-wheelers and entry passenger vehicles. Electronic throttle bodies. Mechatronic actuators for transmission and parking-brake applications. Sensor-integrated control modules. Speed and position sensors. The pitch to a long-standing cable customer is essentially: "You already buy your accelerator cable from us. When you electrify the throttle, buy the e-throttle from us too. We already know your chassis."[^10]

The numbers, in the segments the company has disclosed, support the strategic thesis. SED revenue has been growing at year-on-year rates in the 27–35% band, and the run-rate revenue is closing in on the order of ₹100 crore per month — translating to a roughly ₹1,200 crore annualised business, up from a fraction of that just a few years earlier.[^10] Margins on the electronics products, as the company has guided, are structurally higher than mechanical cables once the volume scales, because the cost base is increasingly software-and-firmware rather than copper-and-steel.

The Trojan-horse framing is genuinely apt. Forty years of zero-defect cable supply built relationships with every meaningful two-wheeler and passenger-vehicle OEM in India and a meaningful subset of the global majors. Those relationships are platform-level, not procurement-level. The OEM engineering team trusts the Suprajit engineering team, the validation history is on file, and the supplier-development infrastructure is already in place. Walking that trust across the table from cables into digital instrument clusters is not a free pass — the products still have to meet specifications — but it is a structural advantage that a pure-play electronics newcomer simply does not have.

There is a deeper, almost philosophical point about cannibalisation inside the SED strategy. Most incumbents in any industrial category eventually fail not because they cannot see the disruption coming but because they cannot bring themselves to attack their own legacy revenue. Kodak saw digital photography coming. Nokia saw smartphones coming. Both companies were undone not by ignorance but by the institutional impossibility of telling their own salespeople to sell against their own gross margin. Suprajit's structural choice — putting SED under Akhilesh Rai's direct sponsorship, funding it from group cash flow even when it diluted current margins, and explicitly positioning it inside the company as the replacement for current cable revenue rather than as an adjacent diversification — is the institutional choice that most incumbents fail to make.[^10]

The risk, of course, is one of pace. If electrification accelerates faster than SED can scale, the cable business erodes before the electronics business compensates. If it accelerates slower, Suprajit harvests the cable cash cow for longer and gets even more time to build SED into a global business. Both scenarios are bounded by management's ability to read the cadence of platform transitions across geographies — and that, ultimately, is the bet the long-term shareholder is making on the team.

The next layer of analysis is to step back and ask what kind of structural powers and competitive dynamics are actually at work behind both the cable and the electronics franchises.

VIII. Strategy Analysis: The 7 Powers & 5 Forces

Run Suprajit through Hamilton Helmer's 7 Powers framework and the structural story becomes legible in a way that the quarterly numbers, on their own, do not surface.

Start with Scale Economies, the first and most obvious power. Cables are a unit-cost game. The fixed cost of a Bengaluru plant, a Mexican plant, and a Hungarian plant — the engineering, the tooling, the quality systems, the supplier base for steel wire and polymer jacketing — is roughly the same whether you make ten million cables or fifty million. Suprajit makes roughly 350 million cables a year across the group, which puts unit fixed costs at a level no domestic-only competitor can match.1 More importantly, the global footprint allows Suprajit to serve a global OEM like Ford or Volkswagen simultaneously in three regions, which is something only Hi-Lex and Suprajit can do at scale. Regional players are structurally locked out of these global awards.

Second, Switching Costs. This is the underrated moat in the cable business. Every cable design is platform-specific and chassis-specific. Once a Suprajit cable is locked into a Ford F-150's parking-brake architecture, switching to a different supplier requires the OEM to re-validate the new cable across the full chassis, redo the durability and salt-spray tests, qualify the supplier's plant, requalify the production lots, and accept the warranty risk of a part-number change on a platform that has run for years. The cost of all that is measured in tens of millions of dollars per platform, against an annual cable cost of single-digit dollars per vehicle. The math never works. The incumbent stays.

Third, Process Power, which is the harder-to-articulate but arguably most durable moat the company has built. "Process Power", in Helmer's framing, is the kind of advantage that lives inside the organisational DNA rather than inside a single asset — Toyota's TPS being the canonical example. Suprajit's version of it is what the company privately calls the "India cost base plus global proximity" formula: high-complexity engineering and high-volume manufacturing in India, finishing and customer-facing assembly close to the OEM in Mexico, Hungary, or the U.S. Replicating that requires not just capital but two decades of integration experience and the cultural capability to run plants on three continents without snapping. Hi-Lex has scale; nobody else has the same India-anchored cost base.

The other four Helmer powers — Network Economies, Branding, Cornered Resource, and Counter-Positioning — are less load-bearing here. Cables do not have network effects. End-consumers do not know which cable is in their car. There is no rare-earth dependency. And the counter-positioning argument — that incumbents like Kongsberg and Hi-Lex have structurally chosen to deprioritise cables in favour of richer categories, leaving Suprajit free to consolidate the leftovers — is real but better described as a happy by-product of Suprajit's last-man-standing strategy than as a Helmer-style power in itself.

Now Porter's 5 Forces, which describes the industry's structural attractiveness rather than any one firm's moat.

Threat of new entrants: minimal. The barrier is not capital — anyone can build a wire-drawing plant. The barrier is the qualification cycle. An OEM does not award a cable contract to a vendor without years of zero-defect supply history. To get years of zero-defect supply history, you need a first contract. To get a first contract, you need years of zero-defect supply history. The recursion is the moat. New cable vendors do not appear in the global OEM supply base.

Bargaining power of suppliers: moderate. Steel wire, plastic conduit, and stamped components are commodity inputs with multiple vendors. Suprajit's group scale gives it negotiating leverage that smaller players do not have, particularly post-Kongsberg-LDC.

Bargaining power of buyers: real and significant. Global OEMs are large, sophisticated, and run annual cost-down programmes. The mitigant is the switching-cost moat described above; the OEM can extract price concessions, but it cannot easily change vendors.

Threat of substitutes: this is the entire SED conversation. The electronic actuator is the substitute, and the company's strategic response — build the substitute in-house — is the most important defensive move it has ever made.

Industry rivalry: rational, structurally. The global cable industry has consolidated into Hi-Lex, Suprajit, and a long tail of regional players. The Tier-1 majors that historically participated (Kongsberg LDC being the cleanest example) have largely exited. Rational duopoly behaviour, not price warfare, is the equilibrium.

The "myth versus reality" check is worth running here, because the consensus framing of Suprajit has been wrong in two directions at different times. The myth — that cables are a melting ice cube and the company is a value trap — is contradicted by the reality that mechanical cable count per vehicle has declined far more slowly than the consensus expected, that EVs still contain meaningful cable content, and that the SED programme is meaningfully ahead of where the consensus was modelling it three years ago. The opposite myth — that Suprajit is an Indian export-manufacturing growth story to be priced on aggressive multiples — is contradicted by the reality that the company has consistently allocated capital to single-digit-multiple acquisitions and disciplined organic capex rather than chasing growth-multiple revenue.

For the long-term holder, the key performance indicators that actually matter are narrower than the typical investor dashboard implies. Watch the SED revenue trajectory — month-on-month run rate and segment EBITDA contribution — because that is the answer to the existential question. Watch the consolidated EBITDA margin, currently in the 13–16% band, because margin sustainment under wage-inflation pressure in Mexico and Europe is the principal operational test of the global footprint thesis.1 Watch the integration cadence on SCS as the proof-of-replication of the playbook on the most recently acquired asset. Three KPIs. That is the dashboard.

IX. Playbook & Bear vs. Bull Case

The bull case for Suprajit is structurally simple and tactically nuanced. Start with the last-man-standing thesis: the global cable industry has been quietly consolidating for fifteen years, and the players who remain at scale — Hi-Lex and Suprajit — are positioned to absorb the share of the regional competitors who lack the multi-continent footprint to serve global OEMs. The Phoenix lighting franchise is the same story in miniature: as competitors abandoned halogen, Suprajit consolidated the residual share and harvested the cash flow. The same dynamic is now playing out in European cables as German Mittelstand suppliers either restructure (SCS being the textbook case) or exit entirely. Every cycle of industry attrition is a tailwind to the remaining scaled player.1[^7]

Layer onto that the SED option. If the electronics division compounds at the 27–35% trajectory it has shown over the past several years, it crosses meaningful scale within a 24–36 month window and changes the company's revenue mix and margin profile substantially. The bull case is not that mechanical cables grow; it is that mechanical cables hold their cash flow while SED grows into a higher-margin, multi-hundred-million-dollar adjacent business inside the same OEM relationships.[^10]

Capital allocation is the bull case's quiet ballast. Three acquisitions over nine years, all at single-digit EV/EBITDA multiples, all in categories the consensus discounted, all integrated without operational breakage. A management team with skin in the game and a measurable record of compounding rather than empire-building. A founder who chose to step aside while engaged, and a professional CEO whose incentive structure is anchored in shareholder returns. This is the kind of capital-allocation track record that, in any market, deserves to be a structural part of the valuation rather than a discretionary multiplier on it.12

The bear case is real and needs to be taken seriously. The first risk is pace. If EV penetration accelerates faster in core markets — Europe, China, North America — than the consensus model assumes, the mechanical cable bill-of-materials per vehicle compresses faster than SED scales, and there is a multi-year window in which group revenue stagnates or declines while the business mix transitions. This is the classic "valley of death" risk for any incumbent attempting to disrupt its own legacy product, and it is a real possibility rather than an academic one.

The second risk is cost-base inflation in the international plants. Mexican manufacturing wages have moved materially over the past three years; European energy costs (the precise issue that pushed SCS into insolvency in the first place) remain elevated; and the global supply chain reset has not finished. The 14–16% EBITDA margin band that the consolidated business has held is contingent on the assumption that India-cost-base offsets compensate for inflation in the international plants. If that assumption breaks — if, for instance, currency moves compress the arbitrage, or if union pressure in Mexico tightens — the consolidated margin profile compresses meaningfully.1

The third risk is acquisition integration. SCS, acquired out of insolvency, is the most operationally complex deal the group has done. The Suprajit playbook has worked three times, but Stahlschmidt's German labour structure and Moroccan footprint are a fundamentally different integration challenge from Wescon's Kansas operation or Kongsberg LDC's diversified geography. A misstep on SCS would not be fatal — the purchase price was small — but it would be the first credibility crack in the M&A track record, and the market would price that.6

The fourth risk is the optionality the SED programme actually delivers. The 27–35% growth is impressive, but it is growing off a base that is small relative to the consolidated group, and the global competition in automotive electronics — Bosch, Continental, Denso, Marelli — is structurally tougher than the global competition in cables. Suprajit's relationship-driven Trojan-horse model into existing OEM accounts is real, but it does not provide a permanent moat against global Tier-1s with deeper R&D budgets. SED has to win not just on relationships but on product, and the runway for that proof is the next 36 months.[^10]

The playbook lesson — the thing that an investor takes away from the Suprajit story regardless of where the stock prints next quarter — is the one the company has been quietly demonstrating for forty years: do not buy growth at 20x EBITDA. Buy competence at 7x and fix the operations. Buy categories the consensus has written off, not the ones it has fallen in love with. Build the cannibal inside the company before the disruptor builds it outside the company. Let the family-and-professional management split do its work. And let the boring monthly review compound.

The puppet master metaphor in the title is not accidental. A cable, fundamentally, is a transmission of human intent — a pull on one end becomes an action at the other. Suprajit's business, as it stands in 2026, is increasingly something analogous: a quiet transmission between the world's automotive OEMs and a Bengaluru-anchored manufacturing network that has been built, deliberately and patiently, to translate global industrial demand into local Indian production economics. Whether that translation continues to work as the cars themselves go electric, digital, and software-defined is the question every long-term holder is now sitting with — and it is the question the next three years of SED scaling will answer, one platform at a time.

References

References

-

Annual Report FY 2023-24 — Suprajit Engineering Limited ↩↩↩↩↩↩↩↩↩↩↩↩↩↩

-

Ajith Rai, the man who built Suprajit Engineering into a global giant — Forbes India, 2016-11-23 ↩↩↩↩↩↩↩↩↩

-

Investor Relations Landing Page — Suprajit Engineering Limited ↩

-

Suprajit Engg-Phoenix Lamps merger: What it means for investors — Moneycontrol, 2017-01-05 ↩↩↩

-

Suprajit Engineering acquires Wescon Controls — Reuters, 2016-09-07 ↩↩↩

-

Suprajit Engineering to acquire Stahlschmidt Cable Systems — The Economic Times, 2024-05-15 ↩↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube