Sun TV Network: The Regional Media Empire

I. Introduction & Episode Roadmap

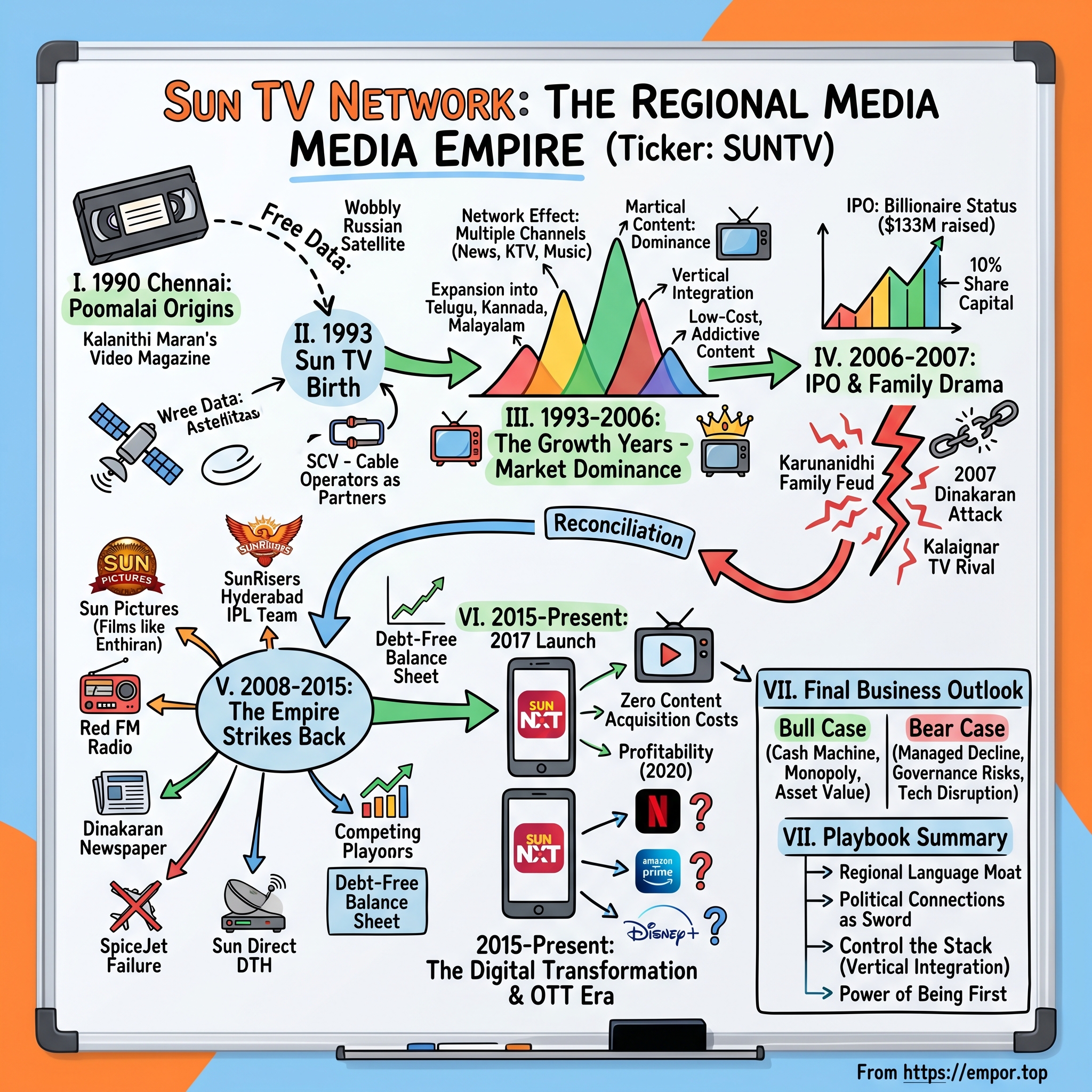

Picture this: It's 1990 in Chennai, and a 26-year-old Kalanithi Maran is hand-delivering VHS cassettes of his video magazine to Tamil households. Pirates are making 200 copies for every original he sells. Most entrepreneurs would see disaster—Maran saw data. Those pirated copies weren't theft; they were proof of massive, untapped demand for Tamil content that nobody else was serving.

Fast forward to today: Sun TV Network commands a media empire spanning 33 television channels, 45 FM radio stations, a streaming platform with millions of subscribers, and even owns the IPL cricket franchise SunRisers Hyderabad. The company broadcasts in six languages—Tamil, Telugu, Kannada, Malayalam, Marathi, and Bangla—reaching over 95 million households across India and beyond. With a market capitalization of ₹23,054 crores and operating margins that make competitors weep (80.41% versus Zee Entertainment's 48.38%), Sun TV isn't just South India's largest media company—it's arguably the most profitable regional media operation on the planet.

But here's what makes this story truly fascinating: Unlike media empires built by tech moguls or entertainment dynasties, Sun TV emerged from the intricate dance between politics and media that defines Tamil Nadu. Kalanithi Maran, grand-nephew of former Tamil Nadu Chief Minister M. Karunanidhi, built his empire at the intersection of family legacy, political power, and brilliant business execution. When offered a political career on a silver platter—a DMK party ticket after his father's death in 2004—he politely declined, choosing boardrooms over ballot boxes.

The question isn't just how a video magazine distributor built South India's most powerful media empire. It's how he navigated family feuds that made headlines, political investigations that threatened everything, and digital disruption that's killing traditional broadcasters worldwide—yet emerged with a debt-free balance sheet generating ₹1,673 crores in annual profit.

This is a story about regional monopolies in the age of global streaming, about the price of political connections, and about why, sometimes, the best business strategy is to dominate a market everyone else ignores. Welcome to the Sun TV saga—where family drama meets financial engineering, where content is both king and kingmaker, and where the real moat isn't technology or capital, but language itself.

II. The DMK Dynasty & Political Origins

The conference room at Sun TV's Chennai headquarters features a portrait that tells you everything about the company's DNA. It's not of the founder, but of Murasoli Maran—former Union Minister, DMK stalwart, and Kalanithi's father. To understand Sun TV, you first need to understand Tamil Nadu's unique political economy, where every major party doesn't just have supporters—they have television channels.

Born on July 24, 1964, Kalanithi Maran entered a family where media and politics were inseparable. His father, Murasoli Maran, wasn't just any politician—he was the DMK's "conscience keeper," a Union Minister who served in Commerce and Industry portfolios, and more importantly, the trusted lieutenant of M. Karunanidhi, who would rule Tamil Nadu for five terms. The family name itself—Murasoli means "voice" in Tamil—embodied their role as the party's media architects. Tamil Nadu's media landscape in the 1990s was unique. The AIADMK had Jaya TV (named after party leader Jayalalithaa), the PMK had Makkal TV, and the DMK controlled Murasoli newspaper. This wasn't just business—it was political warfare fought through prime-time slots and editorial columns. Murasoli Maran was an Indian politician and leader of the Dravida Munnetra Kazhagam (DMK) party, which was headed by his maternal uncle and mentor, M. Karunanidhi. As a Member of Parliament for 36 years, he was Union Minister in three separate central governments, and in charge of Urban Development in the V. P. Singh government; Industry in the Gowda and Gujral governments; and Commerce and Industry under Vajpayee.

The family's media roots ran deep. Outside of politics, Maran was involved in the Tamil-language film industry, writing screenplays for more than 20, producing five, and directing two. This combination of political power, creative influence, and business acumen would prove to be the perfect training ground for young Kalanithi.

But here's where the story takes its first twist. In 2004, when Murasoli Maran died aged 69 on 23 November 2003, the DMK needed someone to carry forward the family's political legacy. Party patriarch Karunanidhi approached Kalanithi with an offer most would kill for: a guaranteed parliamentary seat, likely cabinet position, and a clear path to power. Kalanithi's response? Thanks, but no thanks. He had bigger plans—ones that didn't involve kissing babies or cutting ribbons.

His younger brother Dayanidhi took the political route instead. He was appointed Union Minister for Communications and Information Technology on 26 May 2004. During his tenure as IT and Telecommunication Minister the call rates of mobiles and landlines were drastically reduced which in-turn influenced the growth of subscriptions. During the tenure, he was instrumental in garnering a large amount of Foreign Direct Investments into Communication and Information Technology Sector. The brothers had divided and conquered—one would handle politics, the other would build an empire.

Yet even as Kalanithi stayed out of active politics, the family connections provided something invaluable: protection, access, and most importantly, the ability to navigate Tamil Nadu's byzantine regulatory environment where business licenses could appear or disappear based on which party controlled the state assembly. Critics would later argue that Sun TV's meteoric rise was impossible without these political tailwinds. They weren't entirely wrong—but they weren't entirely right either. Because what happened next proved that while politics opened doors, it was business genius that built the empire.

III. The Poomalai Origins & Sun TV's Birth (1990–1993)

The year was 1990, and 26-year-old Kalanithi Maran was hauling stacks of VHS cassettes through the narrow streets of Chennai's Mylapore district. His product? Poomalai—a monthly video magazine featuring Tamil film clips, songs, and celebrity interviews. The business model was simple: produce 100 copies, sell them for ₹500 each, and hope to break even. The reality was devastating: for every legitimate copy sold, pirates produced 200 bootlegs.

Most entrepreneurs would have seen catastrophe. Maran saw market research being conducted for free. Those 20,000 pirated copies weren't theft—they were proof that Tamil-speaking audiences were desperate for video content. More importantly, the pirates had inadvertently mapped out distribution networks across Tamil Nadu, Sri Lanka, Singapore, Malaysia, and even pockets of Europe where Tamil refugees had settled after fleeing Sri Lanka's civil war. The primary market, surprisingly, wasn't India at all—it was the Tamil diaspora hungry for a connection to home. The financing structure tells you everything about the family dynamics at play. He took a bank loan $86,000 guaranteed by his father, leveraging every personal relationship he had. He also sold out a small stake to his Granduncle M Karunanidhi's family, in against for a minority stake (which Maran later bought out). That last detail—buying out Karunanidhi's stake—would become crucial to understanding Sun TV's later independence.

His original founding team of 25 people were mostly Kalanithi's college friends. This wasn't a corporate launch with hired executives; it was a garage startup with Tamil cinema DNA. The team had cut their teeth on Poomalai, learning what worked and what didn't in the unforgiving school of piracy economics.

The next challenge was securing satellite bandwidth. Kalanithi's initial idea was to approach Subhash Chandra, the owner of the recently established Zee TV, seeking an afternoon slot on the company's transponder. Zee's response was brutal but revealing: there wasn't enough audience for Tamil programming to justify the slot. This rejection—being told your market doesn't exist—would fuel Maran's determination to prove everyone wrong.

Instead of giving up, Maran found an unlikely solution. He partnered with ATN, a smaller player, and pioneered what seemed like an insane strategy: Sun TV was born on 14 April 1993 beaming off the wobbly Russian satellite called Gorizont. While competitors fought for premium satellite spots, Maran used whatever he could get—even if it meant dealing with Soviet-era technology that could fail at any moment.

It was launched on 14 April 1993—Tamil New Year's Day, a calculated choice that signaled this wasn't just another business venture but a cultural mission. The initial programming was just three hours daily, mostly film-based entertainment. But Maran understood something his competitors missed: content wasn't king—distribution was emperor.

This insight led to the most brilliant and controversial move of Sun TV's early days. Kalanithi and his team had to work hard to build cable TV distribution infrastructure in the state, coaxing shop owners to become cable TV operators and set up headends and distribute Sun TV so that it could be seen by Tamilians who had little else to watch in the comfort of their homes. Instead of waiting for cable operators to pick up his channel, Maran created the cable operators. Tea shop owners, grocery store proprietors, anyone with a small business and local connections—Maran turned them into media distribution nodes.

The strategy worked beyond anyone's imagination. Within two years, Sun TV would expand from a three-hour slot to 24-hour programming, setting the stage for the rapid expansion that would follow. The wobbly Russian satellite had become the foundation of a media empire, and the video magazine distributor who'd been destroyed by pirates had learned the ultimate lesson: if you can't beat the distributors, become them.

IV. The Growth Years: Political Tailwinds & Market Dominance (1993–2006)

The boardroom at Sun TV's Chennai headquarters in 1995 was electric with tension. The numbers on the whiteboard told an impossible story: from a three-hour daily slot just two years ago, Sun TV was now broadcasting 24 hours a day and capturing nearly 40% of Tamil viewership. The competitors—established players like Doordarshan's regional service—were hemorrhaging market share. How did a startup crush government-backed incumbents so quickly?

The answer lay in a perfect storm of political timing, distribution genius, and ruthless execution. From 1996 to 2002, the DMK—Kalanithi's family party—controlled Tamil Nadu's government. Critics would later point to this period as proof that Sun TV's success was politically engineered. But the real story was more nuanced: while political connections opened doors, it was Maran's business strategy that built the empire.

The masterstroke was Sumangali Cable Vision (SCV), Sun TV's distribution arm. Instead of depending on independent cable operators who could be swayed by competitors, Maran built his own distribution network. By 2000, SCV controlled cable distribution across Chennai and major Tamil Nadu cities. This wasn't just vertical integration—it was a stranglehold. Competitors could create content, but without SCV's pipes, they couldn't reach viewers.

In the politically dominated Tamil satellite TV industry, the Maran brothers owned Sun TV continues to be on top with a viewership of 51.8 per cent. The numbers were staggering. By the early 2000s, Sun TV commanded a 69% channel share in Tamil Nadu, while its nearest competitor, Vijay TV, languished at 7.6%, and political rival Jaya TV (backed by opposition leader Jayalalithaa) managed just 4.1%.

The content strategy was deceptively simple: give the audience what they want, not what critics appreciate. While competitors chased prestige with high-budget productions, Sun TV perfected the formula of low-cost, high-engagement programming. Daily soap operas featuring family dramas, game shows with local celebrities, and most importantly, a news division that understood Tamil Nadu's unique political culture. The programming wasn't sophisticated—it was addictive.

But here's what really separated Sun TV from its competitors: the network effect. Every new channel Sun launched—Sun News in 2000, KTV (movies) in 2001, Sun Music in 2004—reinforced the others. Advertisers couldn't ignore a network that reached virtually every Tamil household. Content producers had to work with Sun or face irrelevance. Cable operators needed Sun's channels or faced customer revolt.

The expansion beyond Tamil was surgical in its precision. Instead of going national, Maran targeted other South Indian languages where the same playbook could work: fragmented markets, strong regional identity, and competitors who thought like national broadcasters. Sun launched Gemini TV in Telugu, Udaya TV in Kannada, and Surya TV in Malayalam. Each became the market leader within three years of launch.

The true turning point came in 1998 when India liberalised the satellite broadcast industry. Sun Network, positioned perfectly with its established brand and distribution network, was among the first to secure a licence. Since then, Sun TV's growth has been unstoppable, solidifying its dominant position in the South Indian market.

The competition battles during this period were legendary. When Raj TV launched in 1994 with significant fanfare and deep pockets, Sun TV responded not with better content but by making Raj TV harder to find on cable systems. When Star India acquired Golden Eagle Communication and rebranded it as Star Vijay in 2001, Sun TV had already locked up the best content producers with exclusive contracts. And when Jayalalithaa launched Jaya TV in 1999 as a political weapon against the DMK, Sun TV's response was to double down on entertainment while letting Jaya TV exhaust itself with political programming.

By 2006, Sun TV went to become one of the most profitable television channels in India. considering that, as late as 2009, one third of households in India with television sets were in Tamil Nadu and adjacent states. The company wasn't just dominant—it had created a market structure where dominance was self-reinforcing. Every advertiser rupee spent on Sun TV made it stronger; every competing channel that failed made Sun's content library more valuable; every cable operator who joined SCV made the network more essential.

Operating margins told the real story: while competitors struggled to break even, Sun TV was generating margins north of 50%. The secret? Almost zero content acquisition costs (produce everything in-house), monopolistic distribution (SCV controlled the pipes), and advertising rates that reflected market dominance rather than competition. This wasn't just a successful business—it was a money-printing machine that happened to broadcast television.

V. The IPO & Family Drama (2006–2007)

The Mumbai trading floor erupted in applause on April 24, 2006. Sun TV's shares had just begun trading on the Bombay Stock Exchange, opening at a premium that valued the company at over ₹13,000 crores. Sun TV was listed on the Bombay Stock Exchange on 24 April 2006 upon raising $133 million for 10% of the share capital, catapulting him into the billionaire charts. In a single day, Kalanithi Maran had joined India's ultra-wealthy elite. But within a year, this triumph would trigger a family feud so explosive it would leave three people dead and nearly destroy everything he'd built.

The IPO itself was a masterclass in timing. India's economy was booming, foreign investors were hungry for emerging market exposure, and Sun TV's numbers were irresistible: market leadership in four languages, 70% operating margins, and a stranglehold on South Indian advertising. The offering raised about ₹500 crores earmarked for channel expansion and technology investment. Investors got a piece of India's most profitable media company; Maran got the capital to build an empire.

But success bred scrutiny. When they filed the IPO document with the regulator, a Member of Parliament from the BJP wrote a letter to the Prime Minister's office raising questions about Dayanidhi Maran's potential conflict of interest as Telecom Minister while his brother was raising public money. How could a sitting minister's brother run a media empire without regulatory favoritism? The questions were valid, but the IPO proceeded—political connections in India were a feature, not a bug.

The real drama began with a seemingly innocuous business decision. Fresh with IPO proceeds, Kalanithi bought out the Karunanidhi family's minority stake in Sun TV for Rs 100 crore. On paper, this was corporate housekeeping—consolidating ownership before going public. In reality, it was the match that lit the powder keg of family resentment that had been building for years.

Then came the survey that changed everything. In May 2007, Dinakaran caused controversy when it published the results of a series of opinion polls conducted by A.C. Nielsen Co. which appeared to show that Stalin had more public approval than his elder brother Azhagiri – 70% of those polled preferred Stalin, while only 2% preferred Azhagiri. To most readers, it was just another political poll. To M.K. Alagiri, Karunanidhi's elder son who controlled Madurai like a feudal lord, it was a declaration of war.

The response was swift and brutal. The Dinakaran attack was a firebomb attack by M. K. Alagiri's supporters on 9 May 2007 on the Madurai office of Dinakaran, a Tamil language newspaper, which resulted in the deaths of three people. During mass protests throughout the region, the offices of the newspaper were firebombed and two press employees and a private security guard died. The Sun TV office in Madurai was also ransacked. This wasn't just property damage—it was a message: cross the family at your peril.

The patriarch's response revealed the impossible position Maran found himself in. M. Karunanidhi condemned the attack, calling it "an attack on democracy and press freedom", and promised legal action. On the issue of political heirs, he said that "there is no place for dynastic succession in the DMK". Yet actions spoke louder than words. Kalaignar TV, a new channel owned by the Karunanidhi family, was launched as a potential rival to Sun TV when the tensions between Karunanidhi and the Maran brothers were at their height. The government also announced the formation of Tamil Nadu Arasu Cable TV Corporation Limited, a new multiple-system operator, which was intended to end the monopoly of Sun Cable Vision.

The family had turned on its own. Dayanidhi Maran, who usually accompanies Karunanidhi on every function, skipped the celebration of Karunanidhi's 50th year as a legislator—an event attended by Prime Minister Manmohan Singh and Sonia Gandhi. The snub was deliberate and public. The DMK's administrative committee soon empowered Karunanidhi to expel the Maran brothers from the party.

For Kalanithi, this was the darkest period of his career. Political protection had evaporated overnight. Competitors smelled blood. Advertisers, wary of backing the wrong horse in a political fight, began hedging their bets. The stock price, which had made him a billionaire just a year earlier, began sliding as investors worried about regulatory retaliation.

But Maran understood something his attackers didn't: in business, the best revenge is success. While the political drama played out in newspapers, he quietly focused on operations. Sun TV's content continued dominating ratings. Subscription revenues, less dependent on political goodwill than advertising, kept growing. Most importantly, the distribution network he'd built couldn't be dismantled overnight—viewers still wanted their daily serials, regardless of family feuds.

The reconciliation, when it came in December 2008, was as calculated as the feud had been emotional. With elections looming, both sides needed each other. The DMK needed Sun TV's reach to win votes; the Marans needed political cover to operate freely. In December 2008, the Marans made peace with the Karunanidhi family. The prodigal sons had returned, but the relationship would never be the same. Trust, once broken over blood and business, could be restored but never forgotten.

VI. The Empire Strikes Back: Diversification & Expansion (2008–2015)

The peace treaty signing in 2009 wasn't held in a boardroom but at Karunanidhi's Gopalapuram residence. As Kalanithi Maran touched the patriarch's feet in a traditional gesture of respect, both men knew this wasn't reconciliation—it was realpolitik. The DMK needed Sun TV's media muscle for the upcoming elections; Maran needed freedom to build without political interference. Within months, Dayanidhi was back in parliament as Textile Minister, and Sun TV's expansion plans shifted into overdrive.

What followed was perhaps the most audacious diversification spree in Indian media history. While competitors focused on content, Maran went after everything: movies, cricket, radio, airlines, newspapers, and DTH services. The strategy seemed scattershot to analysts, but there was method to the madness. Each new venture either fed content to the TV network, distributed its programming, or leveraged its brand equity. This wasn't diversification—it was building a vertically integrated entertainment ecosystem.

Sun Pictures, the movie production arm, became the first major expansion. Instead of just broadcasting films, why not own them? The unit didn't just produce movies; it revolutionized Tamil cinema's economics. By controlling production, distribution, and broadcast, Sun Pictures could guarantee theatrical releases, manage marketing through its channels, and monetize content across platforms. Films like Enthiran (Robot) with Rajinikanth didn't just break box office records—they demonstrated that regional cinema, properly marketed, could compete with Bollywood.

The 2013 acquisition of the Hyderabad IPL franchise for $85 million raised eyebrows. What was a Tamil media company doing buying a Telugu cricket team? But Maran saw what others missed: sports was content, content was king, and cricket was the only content that commanded higher ad rates than prime-time serials. Renamed SunRisers Hyderabad, the team became a marketing vehicle, a content generator, and surprisingly, a profitable investment as IPL valuations soared. The FM radio expansion was equally aggressive. The group owns 70 FM Radio stations across India broadcasting under the names Red FM, Suryan FM, Magic FM 106.4. This wasn't just about music—radio gave Sun hyperlocal advertising inventory and another touchpoint with audiences. In cities where Sun TV dominated television, Sun's radio stations created an audio-visual stranglehold on advertising mindshare.

Print media came next. Dinakaran was founded in 1977 by K. P. Kandasamy and was acquired from K. P. K. Kumaran by Sun Network in 2005. The acquisition was ironic given the 2007 attack on the newspaper's offices, but it made strategic sense. Newspapers provided credibility that television sometimes lacked, and more importantly, they influenced the political and business elite who still started their day with print.

The DTH (Direct-to-Home) venture, Sun Direct, launched in December 2007, was perhaps the most capital-intensive bet. While competitors relied on cable operators for distribution, Sun Direct gave the company a direct relationship with consumers. By 2015, it had become the fourth-largest DTH provider in India, but more importantly, it was the market leader in South India—Sun's core territory.

But the most puzzling acquisition was SpiceJet. SUN Group acquired 37.7% stake in Indian low-cost carrier SpiceJet in June 2010. What was a media company doing in aviation? The official explanation was diversification, but insiders suggested another motive: Maran wanted to prove he could succeed in any business, not just media. In 2012, Despite the losses, Kalanithi Maran increased his stake in Spicejet by investing ₹1 billion in the airline.

The SpiceJet adventure ended in disaster. By 2014, the airline was bleeding cash, planes were being grounded for non-payment, and Maran faced his first major business failure. In January 2015, the Sun group sold its entire shareholding back to the airline's founder Ajay Singh and transferred control. The exit was clean—no lawsuits, no acrimony—but it was a humbling reminder that media economics didn't translate to aviation.

Yet even this failure couldn't dent Sun TV's core profitability. The company's operating margins remained north of 80%, compared to Zee Entertainment's 48.38%. How? The answer lay in Sun's unique cost structure. While Hindi channels paid astronomical sums for Bollywood content, Sun produced most programming in-house. While national networks spent fortunes on distribution, Sun owned its pipes. While competitors fought for advertising share, Sun had monopolistic pricing power in its markets.

The numbers by 2015 were staggering: 33 television channels, 45 FM radio stations, two newspapers, five magazines, a DTH service, an IPL team, and a movie production house that had delivered multiple blockbusters. Annual revenues crossed ₹3,000 crores, profits exceeded ₹1,200 crores, and the company remained virtually debt-free despite its expansion spree.

But the most remarkable achievement wasn't the scale—it was the integration. A viewer could wake up to Sun TV's morning show, listen to S FM during their commute, read Dinakaran at work, watch Sun News during lunch, catch a Sun Pictures movie in the evening, and fall asleep watching SunRisers Hyderabad on Sun TV. This wasn't just market dominance—it was life dominance, at least in South India. The empire hadn't just struck back; it had conquered territories its enemies didn't even know existed.

VII. The Digital Transformation & OTT Era (2015–Present)

The war room at Sun TV's headquarters in early 2015 looked like a Silicon Valley startup had collided with a traditional broadcaster. On one wall, screens showed Sun TV's commanding 40% share of Tamil GEC market per BARC India. On the opposite wall, a different set of numbers told a scarier story: Netflix had announced India launch plans, Amazon Prime was coming, and smartphone penetration in Tamil Nadu had crossed 40%. The message was clear—disrupt yourself or be disrupted.

Kalanithi Maran faced a classic innovator's dilemma. Sun TV's traditional business was printing money—advertising revenue was growing, subscription fees were steady, and the company maintained its vice-like grip on South Indian viewership. Why cannibalize a business generating ₹1,500+ crore in annual profits to chase digital dreams? But Maran had seen this movie before. Just as satellite TV had killed terrestrial broadcasting, streaming would eventually eat television. The only question was whether Sun would be predator or prey. The launch of Sun NXT in June 2017 was deliberately understated—no celebrity endorsements, no massive marketing blitz, just a quiet rollout to existing Sun TV viewers. Within four days of its launch, the app had obtained 1.1 million downloads. By November it was about seven million. The initial strategy was conservative: leverage existing content, minimize new investment, and treat digital as an extension of TV rather than a replacement.

But the competitive landscape was brutal. Netflix was spending $100 million on Sacred Games alone—more than Sun TV's entire annual content budget. Amazon Prime was acquiring exclusive rights to new releases. Disney+ Hotstar had the IPL. How could a regional player compete with global giants burning billions?

The answer lay in understanding what Sun's audience actually wanted. While Netflix chased urban English speakers with prestige dramas, Sun NXT subscribers wanted their daily serials available on-demand. While Amazon focused on Bollywood blockbusters, Sun's viewers wanted regional films with local stars. The platform had over 4000 movies, allowed live streaming of over 40 television channels and catch-up TV in four languages. This wasn't about competing with global OTT—it was about owning regional OTT.

The business model innovation was equally clever. Instead of the expensive direct-to-consumer approach, Sun NXT partnered with telecom operators. Reliance Jio included Sun NXT in its bundle, instantly giving the platform access to millions of subscribers. Similar deals with Airtel and Vi followed. By February 2020, the platform's subscriber base grew to about 15 million users and started making a profit.

The profitability milestone was remarkable. While global OTT players bled billions, Sun NXT turned profitable within three years. "Our OTT has turned the corner and has now started making profits. So in the last couple of years, we were in an investing phase and now I'm delighted to share with the group that it has moved from red to black," management announced in 2020. The secret? Zero content acquisition costs (using existing library), minimal marketing spend (leveraging TV channels for promotion), and bundled distribution (through telecom partnerships).

By 2023, SunNXT was contributing approximately INR 100 crore to revenue. While modest compared to the ₹2,800 crores from advertising, it represented pure upside—incremental revenue from existing content with minimal additional cost. The platform had become what Maran envisioned: not a Netflix killer, but a profitable complement to the core business.

Yet challenges remained formidable. Cord-cutting accelerated post-COVID, with younger viewers abandoning traditional TV entirely. Global OTT players began investing heavily in regional content—Netflix's Tamil originals, Amazon's Telugu exclusives. The days of easy dominance were ending. Sun TV's 40% share of Tamil GEC market remained strong, but the trajectory was clear: down from 50% five years ago, likely heading to 30% in five years.

The response has been measured but strategic. Sun NXT began investing in originals—web series that couldn't air on family-friendly TV channels. The platform experimented with direct-to-digital movie releases, cutting out theatrical distribution. Most importantly, it started treating digital not as a side business but as the future of the company.

The 2023 advertising revenue of approximately ₹2,800 crores still dwarfed digital revenues, but the writing was on the wall. Smart TVs were replacing cable boxes. Mobile data costs had collapsed to near-zero. A generation was growing up that had never watched scheduled television. Sun TV's challenge wasn't competing with other broadcasters—it was remaining relevant in an on-demand world.

VIII. Financial Analysis & Business Model

Pull up Sun TV's financials and you'll witness something rare in media: a company that prints money without burning it. Market Cap: ₹23,054 Crore, Revenue: ₹3,994 Cr, Profit: ₹1,673 Cr. These aren't just good numbers—they're anomalous. In an industry where competitors struggle for single-digit margins, Sun TV maintains a pre-tax margin of 55% and generates returns on equity of 14% while remaining almost debt-free.

The revenue model appears simple but hides sophisticated economics. Advertising contributes approximately ₹2,800 crores annually, driven by Sun TV's stranglehold on South Indian eyeballs. But here's the genius: unlike national broadcasters who compete fiercely for ad rupees, Sun operates in markets with limited competition. An advertiser wanting to reach Tamil housewives has exactly one meaningful option. This pricing power translates directly to margins—Sun charges what it wants, not what the market dictates.

Subscription revenue adds another ₹1,000+ crores, split between cable and DTH. The beauty of subscription income? It's recurring, predictable, and grows with inflation. Every price hike flows straight to the bottom line since content costs are largely fixed. The company has delivered a poor sales growth of 2.69% over past five years, but when you're generating 50%+ margins, growth becomes less critical than maintaining pricing power.

The cost structure reveals why these margins are sustainable. Unlike Hindi entertainment channels that pay astronomical sums for Bollywood movies or cricket rights, Sun produces most content in-house. A Tamil serial costs a fraction of a Hindi equivalent but commands similar advertising rates in its market. The company operates with remarkable efficiency—fewer than 3,000 employees generate nearly ₹4,000 crores in revenue, translating to over ₹1.3 crores per employee.

But the working capital deterioration tells a concerning story. Days increased from 258 to 617 over recent years, suggesting either aggressive revenue recognition or collection challenges. Earnings include an other income of Rs.692 Cr—nearly 40% of reported profit comes from treasury operations rather than core business. This isn't necessarily problematic for a cash-rich company, but it masks underlying operational trends.

The movie production business adds volatility but strategic value. Films like 2023's Jailer with Rajinikanth can generate ₹200+ crores in theatrical revenue plus additional income from satellite and digital rights. But failures can be equally spectacular—a single flop can wipe out a quarter's earnings. The company treats movies as high-risk, high-reward bets rather than core operations.

Operating profit margins witnessed a fall and stood at 61.8% in FY24 as against 63.5% in FY23. The decline seems marginal, but in a high-fixed-cost business, small margin compressions can signal larger problems. Rising content costs as competition intensifies, increasing talent fees as streaming platforms bid up prices, and pressure on advertising rates as viewership fragments—all suggest the golden age of monopolistic margins may be ending.

The capital allocation deserves scrutiny. The company maintains a healthy dividend payout of 34.6%, returning cash to shareholders rather than chasing growth. But with nearly ₹3,000 crores in investments and cash, the question becomes: why isn't Sun investing more aggressively in digital transformation? Management's conservative approach—spending just ₹150 crores on Sun NXT over 18 months—seems prudent but might prove penny-wise and pound-foolish if competitors capture digital audiences.

Return on Equity (ROE) stands at 18.3%, respectable but not spectacular for a company with Sun's market position. The issue isn't profitability but growth—or lack thereof. Revenue has grown at just 6.1% CAGR over five years, barely keeping pace with inflation. For a company in a supposedly growing media market, this stagnation raises questions about whether Sun has hit natural limits or management has become too comfortable.

The balance sheet strength—virtually debt-free with substantial cash reserves—provides a buffer against disruption but also suggests inefficiency. In an industry undergoing radical transformation, hoarding cash might be less valuable than investing in capabilities, content, or acquisitions. The failed SpiceJet venture showed management can take risks, but recent conservatism suggests those lessons may have been overlearned.

Promoter holding at 75% creates alignment but also governance concerns. The concentrated ownership means minority shareholders have limited influence on strategy or capital allocation. The recent family disputes over "fraudulent share transactions" highlight the risks of such concentration. When family dynamics affect business decisions, minority shareholders often suffer.

The financial picture that emerges is paradoxical: a company with enviable economics showing signs of stagnation, a cash machine that's stopped investing in growth, a market leader whose leadership is being gradually eroded. The numbers remain impressive—any company generating ₹1,673 crores in profit on ₹3,994 crores in revenue deserves respect. But in technology disruptions, great financials often precede great declines. Sun TV's challenge isn't maintaining today's profitability but ensuring tomorrow's relevance.

IX. Playbook: Media Empire Building Lessons

Walk into any media strategy classroom and Sun TV's playbook would seem to violate every rule. Don't compete with national players on content quality—dominate regional markets they ignore. Don't chase prestige—print money. Don't build for critics—build for aunties watching afternoon serials. Yet this contrarian approach built India's most profitable media empire. The lessons aren't just about media; they're about finding monopolies hiding in plain sight.

Lesson 1: Regional Language as an Impenetrable Moat Forbes named him "Television king of southern India"—not India, but southern India specifically. This geographic qualifier isn't a limitation; it's the entire strategy. While Star, Zee, and Sony fought bloody battles over Hindi-speaking audiences, Maran realized Tamil viewers were underserved and undermonetized. A Tamil grandmother doesn't want dubbed Hindi serials; she wants stories in her language, with her cultural references, featuring her stars. This insight seems obvious now but was revolutionary in the 1990s when everyone assumed India would converge toward Hindi/English content.

The moat runs deeper than language. It's about cultural intuition that can't be replicated from Mumbai boardrooms. Sun TV knows that Tamil audiences prefer family dramas to crime thrillers, that they'll watch the same movie hundreds of times if it stars Rajinikanth, that news about local temple festivals can outdraw national headlines. This cultural embedding makes Sun TV essentially un-disruptable by national players—they simply don't know what they don't know.

Lesson 2: Political Connections—The Double-Edged Sword The Maran family's political DNA provided rocket fuel for Sun TV's early growth but nearly destroyed it during the 2007 Dinakaran crisis. The lesson isn't to avoid political connections—in India, that's impossible—but to build businesses that can survive political winters. Sun TV's genius was using political advantage to build structural advantages (distribution networks, content libraries, market position) that persisted even when political winds shifted.

The key insight: political connections open doors, but only business execution keeps them open. When the DMK lost power, Sun TV didn't collapse because viewers didn't care about Maran's politics—they cared about their daily serials. The business had transcended its political origins.

Lesson 3: Vertical Integration in Media—Control the Stack Sun TV's expansion into every part of the media value chain—content production, channel broadcasting, cable distribution, DTH services, movie production, digital streaming—wasn't empire building for its own sake. Each piece reinforced the others. Own production means no content cost inflation. Own distribution means no carriage fee negotiations. Own movies mean exclusive premiere content. Own streaming means direct consumer relationships.

This integration creates a virtuous cycle: more content strengthens distribution, stronger distribution attracts more advertising, more advertising funds more content. Competitors can match any single element but can't replicate the entire system without massive capital and decades of effort.

Lesson 4: The Power of Being First Sun TV wasn't just early to satellite television—it was first in creating the category of regional satellite TV. Being first meant setting viewer expectations, locking up talent, securing distribution, and most importantly, becoming synonymous with Tamil television. Even today, "Sun TV" is shorthand for Tamil TV the way "Xerox" means photocopying.

First-mover advantage in media is particularly powerful because of habit formation. Viewers develop daily routines around specific shows at specific times on specific channels. Once established, these habits are nearly impossible to break. Sun TV became part of the daily rhythm of Tamil households—as essential as morning coffee.

Lesson 5: Family Business Dynamics in Public Markets The Maran saga illustrates both the power and peril of family businesses. The alignment of interests when family wealth is tied to company performance drives long-term thinking. But family feuds can destroy value overnight. Sun TV's solution—clear separation between family members' roles, professional management for operations, family control for strategy—isn't perfect but has proven sustainable.

The concentrated 75% promoter holding might concern governance advocates, but it also enables quick decisions and long-term planning impossible in widely-held companies. When Netflix entered India, Sun TV didn't need quarterly earnings calls to decide strategy—Maran decided, and the company executed.

Lesson 6: Content Economics—The Make vs. Buy Decision Sun TV's decision to produce content in-house rather than acquire it seems obvious in retrospect but was contrarian when everyone else was licensing content. The economics are compelling: produce a serial for ₹10 lakhs per episode, amortize it across multiple airings, sell reruns, monetize digitally. The same content that cost ₹10 lakhs might generate ₹50 lakhs over its lifetime.

But in-house production isn't just about cost—it's about control. Sun TV can ensure content aligns with audience preferences, maintains quality standards, and most importantly, owns intellectual property forever. While competitors' licensed content expires, Sun TV's library appreciates like real estate.

Lesson 7: Distribution as Kingmaker Content might be king, but distribution is kingmaker. Sun TV's investment in cable networks and DTH services wasn't just vertical integration—it was about controlling the last mile to consumers. In negotiations with content producers, Sun TV could guarantee distribution. In negotiations with advertisers, it could guarantee reach. This distribution power became self-reinforcing: the more dominant Sun TV became, the more essential it was for anyone wanting to reach South Indian audiences.

Lesson 8: The Paradox of Monopoly Sun TV's regional monopolies generate extraordinary profits but also breed complacency. When you own 69% market share, innovation becomes optional. The company's slow digital transformation and stagnant growth suggest monopolies' hidden cost: they're profitable until they're not. The playbook that built Sun TV's empire—regional focus, political connections, vertical integration—might be the very things preventing its next evolution.

The ultimate lesson from Sun TV isn't about media or technology or even business strategy. It's about finding markets where you can be a monopoly, building moats that protect that monopoly, and generating cash flows that survive disruption. Whether those lessons apply in a digital, global, platform-dominated future remains the billion-rupee question.

X. Bear vs Bull Case & Future Outlook

The Bear Case: Slow Death by a Thousand Streams

The bear thesis on Sun TV reads like a Victorian novel—a once-great family watching their estate crumble while pretending everything's fine. Revenue growth of 2.69% over five years isn't stagnation; it's decline when adjusted for inflation. The company is literally shrinking in real terms while management collects dividends and hopes nobody notices.

The structural headwinds are accelerating. Linear TV viewership among under-30s has collapsed—they don't even know what "prime time" means. These aren't Sun TV's customers today, but they're everyone's customers tomorrow. When today's 50-year-old serial watchers age out, who replaces them? The pipeline is broken, and Sun TV seems content managing decline rather than fixing the break.

Competition is coming from angles Sun TV can't defend. Netflix spending ₹3,000 crores annually on Indian content makes Sun's entire revenue look quaint. YouTube creators reach larger audiences than Sun TV channels with zero distribution costs. Even regional competitors like Aha (Telugu) and Hoichoi (Bengali) are building streaming-first businesses while Sun treats digital as a side project.

The political risk that once seemed manageable now looks existential. Recent investigations into "fraudulent share transactions" within the promoter family suggest governance issues. The concentrated ownership (75% promoter holding) means minority shareholders are helpless if family disputes escalate. The DMK's return to power provides temporary protection, but Tamil Nadu's political pendulum swings reliably—what happens when it swings back?

The working capital deterioration—days increased from 258 to 617—suggests something rotten in operations. Either advertisers aren't paying, or revenue recognition has become aggressive. When 40% of profit comes from "other income" rather than operations, it's financial engineering, not business success.

Most damning: management's apparent satisfaction with the status quo. The failed SpiceJet adventure seems to have traumatized leadership into extreme conservatism. While competitors invest billions in content and technology, Sun TV returns cash to shareholders. This isn't prudent capital allocation; it's corporate surrender.

The Bull Case: The Cockroach of Indian Media

The bull thesis is simpler: never bet against a monopoly printing money. Sun TV isn't glamorous, isn't growing, isn't innovative—and doesn't need to be. With ₹1,673 crores in annual profit and zero debt, the company could survive a decade of disruption while competitors burn cash chasing digital dreams.

The death of regional TV has been greatly exaggerated. 97 percent of homes in Tamil Nadu own a TV set with even the average daily time spent watching television higher than other states. Rural India, where most Indians still live, remains devoted to television. Sun TV's audience isn't going anywhere—they're aging in place, watching the same serials they've watched for decades.

The competitive moat remains formidable. Unlike national channels relying solely on content, distribution was king for regionals. Sun's distribution network, built over 30 years, can't be replicated with venture capital. The brand equity in Tamil Nadu is priceless—"Sun TV" means television the way "Coke" means cola.

Digital transformation, while slow, is progressing profitably. By February 2020, the platform's subscriber base grew to about 15 million users and started making a profit. Unlike global OTT players bleeding billions, Sun NXT generates positive returns. The company's conservative approach—profitable growth over growth at any cost—might prove prescient when funding winter arrives.

The cash position provides enormous optionality. With nearly ₹3,000 crores in investments, Sun TV could acquire struggling competitors, invest in technology, or simply return more cash to shareholders. In a recession, cash-rich companies don't just survive—they feast on distressed assets.

The sports franchise alone could be worth a fortune. IPL team valuations have soared—some estimates put SunRisers Hyderabad at $1 billion+. That's nearly 20% of Sun TV's market cap in a single non-core asset. The Maran family's history of shrewd asset plays suggests they know exactly what they're sitting on.

The Realistic Outlook: Managed Decline with Occasional Surprises

The truth likely lies between catastrophe and complacency. Sun TV probably faces a long, slow decline in its traditional business offset by modest digital growth and financial engineering. The company won't disappear—it's too profitable, too entrenched, too essential to its core audience. But it won't thrive either—it's too conservative, too unfocused, too wedded to yesterday's business model.

The next five years will probably see: - Traditional TV revenue declining 5-10% annually as viewership fragments - Digital revenue growing but never reaching traditional TV's profitability - Continued high dividends as management returns cash rather than investing - Potential family disputes as succession questions intensify - Gradual market share erosion but maintained pricing power in core markets - Strategic assets (IPL team, real estate) providing unexpected value - A take-private transaction as the family consolidates control at a discount

For investors, Sun TV represents a classic value trap or deep value opportunity depending on time horizon and risk tolerance. The company trades at reasonable multiples, generates real cash, and owns valuable assets. But it's also facing structural decline, governance challenges, and management that seems resigned to milking rather than building.

The bear case seems more probable—disruption usually wins—but Sun TV has survived every prediction of its demise for 30 years. Perhaps the real lesson is that in India's diverse, complex, multilingual market, there's room for both global platforms and regional monopolies. Sun TV might not win the future, but it doesn't need to. It just needs to survive long enough for investors to collect dividends while waiting to see if management finally wakes up or sells out.

Either way, the next chapter in the Sun TV story won't be boring—family drama, technological disruption, and billions in cash rarely combine quietly.

XI. Epilogue & "If We Were CEOs"

Imagine walking into Sun TV's Chennai headquarters tomorrow as the new CEO. The promoter family has miraculously decided professional management is needed (suspend disbelief). You inherit a ₹23,000 crore market cap company generating ₹1,673 crores in annual profit, sitting on ₹3,000 crores in cash, but growing at inflation speed while the world transforms around it. What do you do?

First Priority: Digital Shock Therapy The conservative digital approach must end immediately. Sun NXT needs a ₹1,000 crore war chest over three years, not the paltry ₹150 crores currently allocated. But this isn't about competing with Netflix on prestige drama—it's about owning regional digital.

Launch "Sun Studios"—a content powerhouse producing exclusively for digital. Not family-friendly serials but edgy, youth-oriented content that could never air on traditional TV. Tamil web series about Chennai's startup culture. Telugu dark comedies about Hyderabad tech workers. Malayalam thrillers that actually thrill. Give creative freedom to young filmmakers traditional TV would never tolerate.

Transform Sun NXT from a catch-up TV service to a regional super-app. Integrate news, short-form video (compete with Instagram Reels, not Netflix), local commerce, even dating. If someone in Tamil Nadu picks up their phone, Sun should own that attention. The TAM isn't the 95 million households watching TV—it's the 500 million smartphones in South India.

Second Priority: The Great Unbundling Sun TV's conglomerate structure made sense in the vertical integration era. Today, it's destroying value. Each business—TV channels, radio, newspapers, movies, sports teams—should be evaluated independently. Those without strategic rationale or path to growth get sold or shut.

The IPL team? Sell immediately while valuations are irrationally high. That billion dollars funds digital transformation with change left over. FM radio? Dying business, sell to whoever's buying. Newspapers? Merge with competitors or shut down. Focus relentlessly on video content and distribution—everything else is distraction.

But here's the twist: simultaneously rebundle for consumers. Create "Sun Prime"—₹99 monthly gets you Sun NXT, ad-free news, exclusive movie premieres, IPL streaming, even discounts at Sun Pictures theaters. Bundle aggressively, price below cost if necessary. The goal isn't profit but owning the customer relationship before global platforms lock up South India.

Third Priority: The Platform Play Stop thinking like a broadcaster, start thinking like a platform. Sun TV's real asset isn't content or channels—it's relationships with millions of South Indian households. Monetize those relationships beyond advertising and subscriptions.

Launch "Sun Creator Network"—enable anyone to create Tamil/Telugu/Malayalam content and share revenue. Every wedding videographer, every cooking enthusiast, every village storyteller becomes a Sun content creator. User-generated content costs nothing but creates infinite inventory. YouTube proved this model; Sun just needs to regionalize it.

Build "Sun Commerce"—if you're watching a Tamil serial where the protagonist wears a beautiful sari, click to buy it. Cooking show features a special mixer-grinder? One-click purchase. Regional commerce integrated into content could generate billions in GMV. The advertising revenue model is dying; transaction-based models are the future.

Fourth Priority: International Expansion The Tamil diaspora—10 million people globally—is underserved and overmonetized. They pay $50/month for basic Tamil content packages abroad. Sun should own this market entirely.

Launch localized services for every major diaspora market. Sun USA doesn't just stream Tamil content—it produces local Tamil-American content. Stories about Tamil kids in New Jersey navigating identity. Reality shows about Tamil entrepreneurs in Silicon Valley. News about both Tamil Nadu politics and American immigration policy. Price at $20/month and capture 50% market share—that's $1 billion in incremental revenue.

Fifth Priority: The Talent Revolution Sun TV's biggest weakness? It's still run like a 1990s family business. The digital transformation needs digital natives. Recruit aggressively from Netflix India, Hotstar, even Silicon Valley. Pay whatever it takes—the ROI on great product managers and engineers is infinite in a digital transformation.

But also nurture internal talent. Create "Sun University"—train the next generation of content creators, technologists, and media executives. Make Sun TV the dream employer for every media graduate in South India. Culture eats strategy, and Sun's culture needs a revolution.

The Contrarian Path: Do Nothing Here's the heretical thought: maybe the current strategy is optimal. Sun TV generates ₹1,673 crores in profit with minimal investment. Digital transformation might cost ₹5,000 crores with uncertain returns. Perhaps the smart move is accepting slow decline while maximizing cash extraction.

Increase dividend payout to 75%. Buy back shares aggressively. Sell non-core assets at peak prices. Run the traditional business for cash while it lasts. When it finally becomes unsustainable, sell to a global player desperate for Indian content. Shareholders might do better with this "controlled demolition" than a risky transformation.

The Real Answer The truth is, Sun TV needs both transformation and pragmatism. Invest aggressively in digital but don't abandon the cash cow. Expand internationally but maintain regional focus. Hire fresh talent but respect institutional knowledge. The company that emerges might look nothing like today's Sun TV—part YouTube, part Netflix, part regional broadcaster, part commerce platform.

The saddest outcome would be status quo—watching a great franchise slowly decay while management counts dividends. Sun TV built an empire by ignoring conventional wisdom. Its survival requires remembering that rebellious spirit. The question isn't whether to transform but whether the Maran family has the courage to disrupt themselves before someone else does.

In the end, being CEO of Sun TV would be either the best job in media—inheriting a cash machine with infinite potential—or the worst—managing inevitable decline while family dynamics create chaos. Probably both simultaneously. Which is, come to think of it, very Tamil drama. Perhaps Sun TV's next chapter should be a serial about itself—a media empire fighting for survival in the digital age. At least that would be content people actually want to watch.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube