Sundram Fasteners: The Precision Engineering Story Behind India's Auto Revolution

I. Introduction & Episode Roadmap

Picture this: It's 1984, and in a nondescript factory in Madras (now Chennai), engineers are huddled around a quality certification document that would change everything. Sundram Fasteners had just become the first Indian fastener company to receive ISO 9001 certification—a moment that seems routine today but was revolutionary then. In an era when "Made in India" meant compromise on quality, here was a company declaring to the world: we can match anyone on precision.

Today, Sundram Fasteners commands a market capitalization of ₹19,700 crore, with revenues touching ₹5,991 crore. But these numbers barely hint at the real story—how a family-run fastener business transformed into a critical supplier to the world's largest automakers, from General Motors to Renault-Nissan, manufacturing everything from high-tensile bolts that hold wind turbines together to precision components that power automotive engines across the globe.

The question that drives this entire narrative is deceptively simple: How did a company making seemingly commodity products—nuts, bolts, and fasteners—build such deep moats that global giants depend on them for mission-critical components? The answer lies not in any single breakthrough but in a half-century accumulation of technical expertise, relationship capital, and an almost obsessive focus on quality that predated India's quality revolution by decades.

This is a story that spans four generations of the TVS family, multiple technology transitions, and the entire arc of India's industrial evolution. It's about building capabilities when none existed, earning trust in markets that had never heard of Indian precision engineering, and navigating family dynamics while competing on the global stage. We'll explore how Sundram Fasteners rode every wave of India's automotive boom while simultaneously building positions in aerospace, wind energy, and infrastructure—sectors where failure isn't just expensive; it's catastrophic.

The company operates across 18% export markets, competing in Germany against companies that invented precision engineering, in Japan where quality is religion, and in Detroit where suppliers are squeezed to the last penny. Yet they've not just survived but thrived, becoming a case study in how emerging market companies can climb the value chain from commodity to engineered products.

What makes this particularly fascinating for investors is the contrast between the company's steady operational excellence and its relatively modest market recognition. While software companies with fraction of their revenues command premium valuations, Sundram Fasteners exemplifies the "boring is beautiful" philosophy—consistent execution in an unglamorous industry that literally holds the modern world together.

II. The TVS Legacy: From Trading to Manufacturing Empire

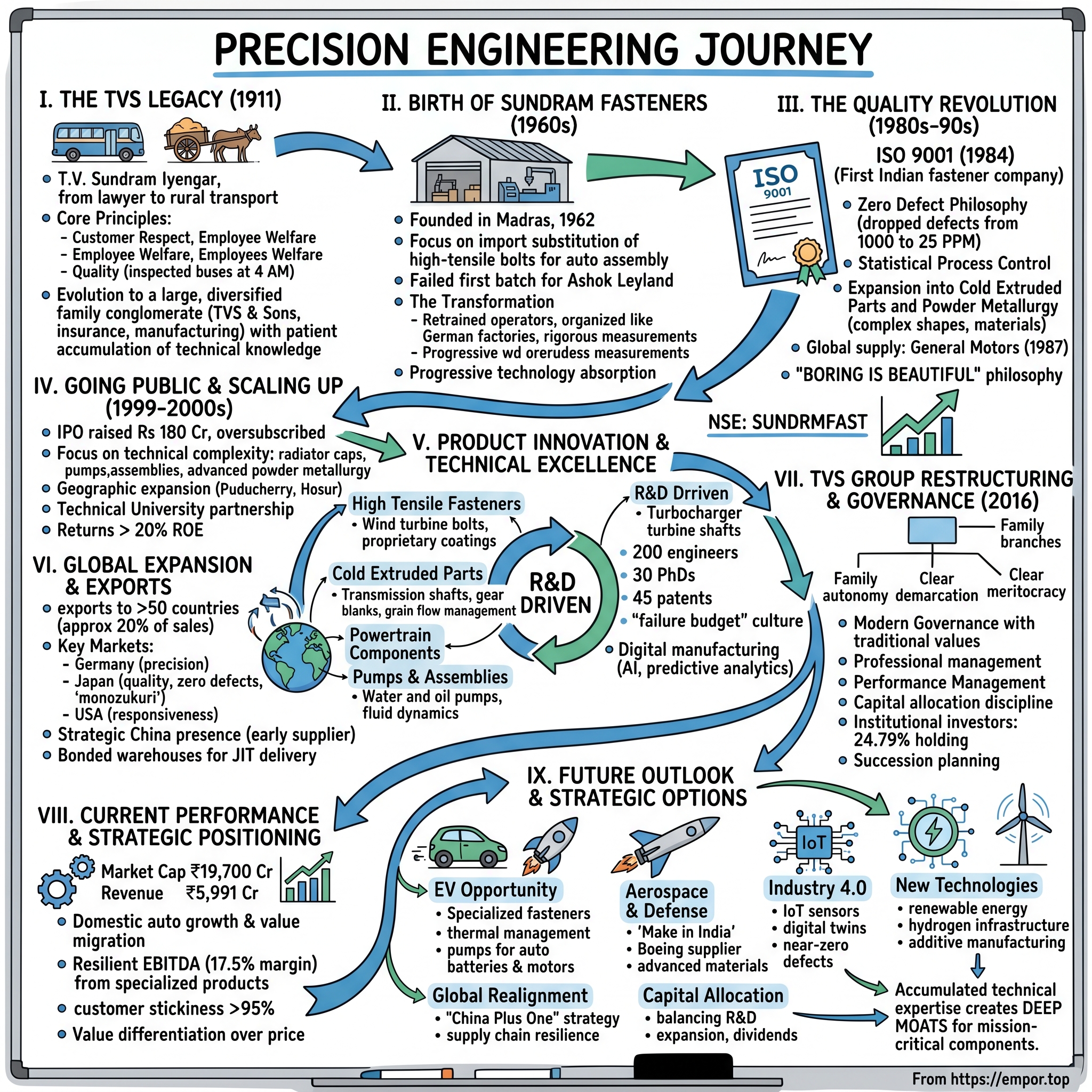

The year was 1911, and in the temple town of Thirukkurungudi in southern Tamil Nadu, a young man named T.V. Sundram Iyengar was making a decision that would ripple through Indian industrial history. Born in 1877 into a traditional Iyengar Brahmin family, Sundram had trained as a lawyer—a respectable, safe profession for someone of his background. But something in him rebelled against the predictable arc of a legal career. Perhaps it was the winds of change sweeping through colonial India, or simply an entrepreneur's instinct that sensed opportunity where others saw only tradition.

Sundram's first venture wasn't manufacturing—it was transportation. He established TVS & Sons as a rural transport company, running bus services that connected remote villages to towns. In an era when most Indians traveled by bullock cart, if at all, Sundram saw mobility as the key to economic development. His buses didn't just carry passengers; they carried aspirations, connecting agricultural markets to urban centers, students to schools, and families to opportunities. This wasn't just business; it was nation-building through private enterprise, decades before independence.

The genius of T.V. Sundram Iyengar lay not in any single business insight but in establishing a value system that would outlive him by generations. He embedded three principles into TVS's DNA: customer respect bordering on reverence, employee welfare as a moral obligation, and quality as non-negotiable—even when it cost more. These weren't just corporate platitudes; they were practiced with an almost religious fervor. Stories from the 1920s tell of Sundram personally inspecting buses at 4 AM, checking everything from engine oil to passenger seat comfort.

By the time Sundram passed away in 1955, TVS had evolved from a transport company into a sprawling conglomerate. The group structure that emerged—TVS & Sons, Sundaram Industries, and various holding companies—wasn't designed by McKinsey consultants but evolved organically as different family members took charge of different ventures. This federal structure, which would later prove both a strength and a source of tension, allowed entrepreneurial energy to flourish while maintaining family control.

The second generation, led by T.S. Santhanam and T.S. Krishna, transformed TVS from a regional player into a national force. They diversified into automobile dealerships, finance, insurance, and crucially, manufacturing. But they maintained their father's ethos—when TVS Motor Company started making mopeds in the 1970s, they insisted on testing them for 100,000 kilometers before launch, a standard that even Japanese companies found excessive.

What distinguished the TVS Group from other Indian business houses wasn't just diversification—everyone was doing that in the License Raj era. It was their approach to building capabilities. While others sought quick returns through trading or licensed production, TVS invested in understanding the underlying engineering. They sent engineers to Germany and Japan not just to learn how to operate machines but to understand why those machines were designed that way. This patient accumulation of technical knowledge would prove crucial when they established Sundram Fasteners.

The family culture deserves special attention. The TVS families lived modestly despite their wealth, with stories of third-generation scions taking public buses to work well into the 1990s. Board meetings began with Sanskrit prayers, and major decisions were often made after consulting family elders who might have no formal business training but possessed what the family called "wisdom capital." This blend of traditional values and modern business practices created a unique corporate culture—professionally managed but family-guided, global in ambition but rooted in Tamil ethos.

This was the ecosystem that would birth Sundram Fasteners in the 1960s—not as a standalone venture but as a natural extension of the TVS philosophy: identify a critical need in India's development, build genuine capabilities to address it, and execute with uncompromising quality. The family's reputation for integrity meant that when they approached foreign partners for technology transfer, doors opened that remained closed to others.

III. The Birth of Sundram Fasteners (1960s–1970s)

The Madras of 1962 was a city caught between its colonial past and industrial future. The Marina Beach still carried the salt-tinged breeze of centuries past, but in the industrial estates of Ambattur and Guindy, a new India was taking shape. It was here, amid the clanging of metal and the hum of newly imported machines, that Sundram Fasteners opened its first facility—though calling it a facility might be generous. It was more a large shed with a few cold-heading machines, operated by engineers who had learned their craft from German technicians flown in at considerable expense.

The timing was no accident. India's Second Five-Year Plan (1956-61) had prioritized heavy industry, and domestic automobile production was finally beginning under the protective umbrella of import substitution. But here lay the problem: while companies like Hindustan Motors and Premier Automobiles could assemble cars, they struggled to source quality components locally. Fasteners—the nuts, bolts, and screws that literally held vehicles together—were either imported at precious foreign exchange or manufactured locally with quality so poor that failure rates approached 15%.

G. K. Sundaram, representing the second generation of the TVS family, saw opportunity where others saw only problems. His vision was audacious for its simplicity: why couldn't India manufacture fasteners that matched global standards? The question seems obvious in hindsight, but in 1962, it required a leap of faith. The technology existed—cold forging and thread rolling were well-established processes in Germany and Japan. The challenge was transplanting this technology to an environment where precision meant plus-or-minus 5mm, not the plus-or-minus 0.05mm that automotive fasteners demanded.

The early days were an exercise in frustration and learning. The company's first major order came from Ashok Leyland, the commercial vehicle manufacturer that was itself a Leyland-India joint venture. The specifications called for high-tensile bolts that could withstand the punishment of Indian roads—potholed, overloaded, and brutal on machinery. The first batch failed spectacularly. Not some, not most—every single bolt failed testing. The German consultant brought in to investigate was blunt: "Your operators are treating precision machines like flour mills."

This failure triggered what employees from that era call "the transformation." Sundram didn't just retrain workers; they rebuilt the entire manufacturing philosophy. Operators were sent to technical schools in the evenings. The factory floor was reorganized on German principles—everything in its place, measurements at every stage, and a culture where stopping the line for quality was not just permitted but mandatory. The company introduced something unheard of in Indian manufacturing then: operators were given calipers and taught to read technical drawings. The message was clear: you're not just machine operators; you're precision engineers.

The technology transfer agreements signed in this period reveal the careful strategy. Unlike many Indian companies that sought turnkey solutions, Sundram negotiated for progressive technology absorption. The initial agreement with a German firm (name not disclosed in available records) wasn't just for machines but included eighteen months of on-site training, periodic audits, and crucially, the right to modify processes for Indian conditions. This last point proved vital—German processes assumed consistent power supply and controlled-temperature environments, luxuries that 1960s Chennai couldn't provide.

By 1968, Sundram had achieved what seemed impossible six years earlier: consistent quality that matched imported fasteners. But matching wasn't enough for the emerging automotive industry. The real breakthrough came through an insight that seems obvious now but was radical then: fasteners weren't just components; they were critical safety elements. A brake caliper bolt failing wasn't just inconvenient; it was potentially fatal. This reframing—from commodity supplier to safety partner—changed how Sundram approached customer relationships.

The 1970s brought new challenges and opportunities. The oil crisis of 1973 forced Indian manufacturers to focus on fuel efficiency, which meant weight reduction, which in turn meant stronger fasteners that could maintain structural integrity with less material. Sundram's response was to establish India's first metallurgical lab focused on fastener applications. They hired metallurgists from IIT Madras—paying salaries that raised eyebrows in the industry—and gave them a simple mandate: understand failure before it happens.

This period also saw the company's first exports, modest shipments to Sri Lanka and Malaysia, markets where "Made in India" still carried some weight. But even these small victories required enormous effort. Export documentation that takes hours today took weeks then. Quality certificates had to be notarized, re-notarized, and sometimes personally carried to customers by senior managers. Yet these early exports taught Sundram valuable lessons about international expectations that would prove crucial in later decades.

The internal culture that developed during these formative years would define Sundram for generations. Monthly quality circles—inspired by Japanese practices but adapted to Indian sensibilities—became forums where machine operators could suggest improvements to engineers without hierarchy getting in the way. The company newsletter from 1974 proudly notes that a suggestion from a junior operator saved 12% on raw material waste, earning him a bonus equal to three months' salary.

By the end of the 1970s, Sundram Fasteners had evolved from a hopeful startup to a serious player in Indian auto components. Revenue figures from this period aren't publicly available, but employment had grown from the initial 50 workers to over 400. More importantly, the company had earned something money couldn't buy: reputation. When Maruti Suzuki began operations in 1981, looking for local suppliers who could meet Japanese quality standards, Sundram Fasteners was on the shortlist—not because of connections or government pressure, but because they had spent two decades preparing for exactly this moment.

IV. The Quality Revolution: First Mover Advantage (1980s–1990s)

The conference room at Sundram Fasteners' Chennai headquarters was thick with tension on a humid August morning in 1983. Across the table sat a team of auditors from Bureau Veritas, the French certification body, their faces betraying skepticism. They had been invited to assess whether an Indian fastener company could meet ISO 9001 standards—a certification that no Indian company in this sector had attempted. The lead auditor's opening question set the tone: "Show us your documented quality system." The Sundram team produced twenty-three bound manuals, each detailing processes from raw material inspection to final packaging. The auditor's eyebrows rose slightly—perhaps this wouldn't be the short visit he expected.

What happened over the next six months would revolutionize not just Sundram Fasteners but Indian manufacturing's global perception. The ISO 9001 certification, received in 1984, wasn't just a certificate to frame on the wall. It was a declaration that Indian manufacturing could compete on quality, not just price. For context, many European manufacturers hadn't yet achieved this certification. Japan was still teaching the world about quality. And here was a company from Chennai, a city most global executives couldn't locate on a map, demonstrating world-class quality systems.

The journey to this certification revealed the depth of Sundram's transformation. R. Thyagarajan, who led the quality initiative (and would later become Chairman), approached it with scientific rigor. Every process was mapped, measured, and analyzed. Statistical Process Control (SPC)—a concept barely known in Indian manufacturing—was implemented across all production lines. Workers who had joined as eighth-standard-pass operators were now plotting control charts and calculating process capability indices.

But the real revolution wasn't in the systems; it was in the mindset shift. Indian manufacturing had long operated on the principle of "chalta hai" (it works, good enough). Sundram instituted what they called "Zero Defect Philosophy"—not as a slogan but as measurable reality. When defect rates dropped from 1000 parts per million (PPM) to 100 PPM in eighteen months, even the German technical partners were impressed. When it dropped further to 25 PPM by 1986, they were astounded.

The expansion of the product portfolio during this period reads like a textbook in climbing the value chain. Cold extruded parts required different expertise than simple fasteners—understanding material flow, die design, and crucially, predicting how metals behave under extreme pressure. Sundram didn't just buy machines for this; they developed internal expertise. Engineers were sent to Germany's Technische Hochschule to study metal forming. The company hired India's first female metallurgist in a production role—a minor revolution in conservative Chennai's industrial culture.

The relationship with global OEMs developed through a careful dance of capability demonstration and trust building. When General Motors first approached Sundram in 1987 for supplying to their global operations, the American executives were skeptical. The audit team that visited Chennai expected to recommend a polite rejection. Instead, they found quality systems that exceeded many of their North American suppliers. The first order was small—fasteners for GM's Brazil operations—but it represented something bigger: validation from the world's largest automaker.

Building these relationships required cultural adaptation that went beyond quality certificates. American customers expected quarterly business reviews with detailed metrics. German customers wanted to discuss metallurgy and process philosophy. Japanese customers expected continuous improvement with documented kaizen events. Sundram developed what internally they called "customer anthropology"—understanding not just technical requirements but cultural expectations. Senior managers learned German and Japanese, not fluently but enough to show respect. Meeting rooms were redesigned to accommodate different cultural preferences for seating and presentation styles.

The hot forging expansion in the late 1980s deserves special attention because it represented a technological leap. Hot forging—shaping metal at temperatures exceeding 1000°C—required completely different competencies. The investment was substantial, but more challenging was developing the expertise. Sundram's approach was characteristic: they didn't just hire experts; they created them. Young engineers were sent for two-year assignments to forging companies in Germany and Japan, not as observers but as workers, learning by doing.

The powder metallurgy venture launched in 1989 illustrated Sundram's strategy of entering complex technologies when competition was minimal. Powder metallurgy—creating components by compressing and sintering metal powders—was virtually unknown in India. The technology allowed manufacturing of complex shapes impossible through conventional methods. The initial investment of ₹15 crores (substantial for that era) was questioned by board members, but R. Thyagarajan's presentation was compelling: "We're not buying machines; we're buying a five-year head start on competition."

The internal culture evolution during this period was as significant as the technological advancement. The company instituted what they called "Quality Month"—not a celebration but an intensive audit where every process was challenged and improved. Workers were encouraged to stop production if they noticed quality issues—revolutionary in an era where production targets were sacred. The story of Murugan, a machine operator who stopped a line producing parts for a major export order because he noticed a 0.1mm deviation, became company legend when investigation revealed his intervention prevented a potential recall.

Financial performance during this period validated the quality-first strategy. While specific numbers from the 1980s aren't publicly available, industry reports suggest Sundram's margins exceeded industry averages by 300-400 basis points. More importantly, customer concentration decreased even as total revenue grew—the company was winning new customers faster than existing ones were growing, a sign of competitive strength.

The competitive advantage built during this period proved durable because it wasn't based on any single factor. It wasn't just ISO certification, or technology, or relationships—it was the combination, creating what strategists call "cumulative advantage." Competitors could buy the same machines, hire consultants for ISO certification, even poach employees. But they couldn't replicate two decades of accumulated learning, the trust earned through thousands of defect-free shipments, or the culture where quality was personal.

By 1990, Sundram Fasteners had transformed from a local supplier to a global player. Export revenues had grown from virtually nothing to 12% of total sales. The company was supplying to 14 different countries. More significantly, they were now being approached by customers rather than having to seek them out. The quality revolution that began with skeptical French auditors had positioned Sundram for the next phase: going public and scaling to become a truly global operation.

V. Going Public & Scaling Up (1999–2000s)

The Bombay Stock Exchange was buzzing with unusual interest on a September morning in 1999. IPOs were common enough in the dot-com era, but this was different—an auto component manufacturer from Chennai, a sector that rarely excited retail investors. Yet Sundram Fasteners' public issue was oversubscribed 2.3 times, with institutional investors showing particular interest. The pricing at ₹85 per share seemed aggressive for a manufacturing company, but the roadshow presentations had revealed something investors hadn't expected: margins that matched software companies and return on capital employed that exceeded 30%.

The decision to go public wasn't driven by capital needs alone—the TVS Group had deep pockets and banking relationships. Rather, it represented a strategic shift. K. M. Mammen, who had taken over as Managing Director, articulated the vision: "Public listing brings discipline that family ownership, however benevolent, cannot match. Every quarter, we must justify our existence to thousands of shareholders. That pressure creates performance."

The ₹180 crore raised through the IPO had specific deployment plans that revealed Sundram's strategic thinking. Rather than building new factories for existing products—the obvious move—the company invested in three areas that seemed unrelated but shared a common thread: technical complexity. A new facility for radiator caps might seem pedestrian, but these weren't ordinary caps. Modern radiator caps are precision pressure-relief valves that must operate reliably at temperature extremes while handling coolant chemicals that corrode most metals. The technology required was closer to aerospace than traditional auto components.

The geographic expansion strategy during this period defied conventional wisdom. While competitors rushed to build facilities near major automotive hubs like Gurgaon and Pune, Sundram chose locations like Puducherry and Hosur. The logic became clear only later: these locations offered not just lower costs but access to technical institutions and, crucially, workers without preconceived notions about manufacturing. It was easier to train fresh graduates in precision manufacturing than to retrain workers who had learned shortcuts in other factories.

The diversification into pumps and assemblies in 2001 illustrated Sundram's approach to capability building. Water and oil pumps for engines aren't just mechanical devices; they're fluid dynamics systems that must operate reliably for hundreds of thousands of kilometers. Sundram didn't just license technology; they established a fluid dynamics laboratory, hiring PhDs from IIT to work alongside shop-floor engineers. When the first prototype water pump failed after 50,000 kilometers of testing (the requirement was 200,000), the team spent six months redesigning not just the pump but the entire testing methodology.

The powder metallurgy expansion during this period deserves detailed examination because it represented a bet on technological change. Traditional manufacturing methods—forging, casting, machining—waste significant material. Powder metallurgy could achieve near-net shapes with minimal waste, crucial as raw material costs soared. But the real advantage was the ability to create materials with properties impossible through conventional methods. By mixing different metal powders, Sundram could create components with varying properties in different zones—hard wearing surfaces with tough cores, for instance.

The relationship with global customers evolved significantly post-IPO. Being a listed company with quarterly disclosures and professional governance gave international customers confidence that went beyond quality certificates. General Motors expanded orders from single components to entire assemblies. Renault-Nissan, initially skeptical of Indian suppliers, became a major customer after visiting Sundram's facilities and reviewing their listed company disclosures. The transparency required by public listing became a competitive advantage in winning global business.

The internal transformation required for public company compliance created unexpected benefits. Quarterly reporting requirements forced systematic data collection and analysis that hadn't existed before. The company discovered inefficiencies that family-style management had masked—inventory turns were lower than global benchmarks, working capital cycles were longer than necessary. The discipline of explaining quarterly variations to analysts forced operational improvements that might never have happened otherwise.

The technological investments during this period reveal forward-thinking that wouldn't pay off for years. In 2003, when electric vehicles were science fiction in India, Sundram began researching components for hybrid powertrains. The investment seemed questionable—even Toyota's Prius was struggling commercially. But the research created capabilities in electronics integration and thermal management that would prove valuable in unexpected areas like wind energy components.

The 2000s also saw Sundram's first serious international acquisition attempts, though not all succeeded. A proposed acquisition of a German forging company fell through when cultural differences proved insurmountable—the German workers' council couldn't accept Indian ownership despite Sundram's superior financial position. This failure taught valuable lessons about international expansion that would inform later strategies. Instead of acquisitions, Sundram focused on technical collaboration agreements that brought technology without cultural complications.

The financial performance during the 2000s validated the IPO promise. Revenue grew from ₹650 crores in 2000 to ₹2,100 crores by 2009, a compound annual growth rate exceeding 14% despite two global recessions. More impressively, return on equity averaged 22% throughout the decade, exceptional for a capital-intensive manufacturing business. The stock price, despite the 2008 financial crisis, delivered returns that beat the Sensex by a significant margin.

The human capital development during this period set foundations for future growth. Sundram established an internal technical university, partnering with Michigan Technical University to deliver courses on-site. The investment seemed excessive—₹5 crores annually for training—but the returns were measurable. Employee suggestions saved ₹12 crores annually by 2005. Attrition rates dropped to single digits in an industry where 20% was normal. Most importantly, Sundram developed internal capabilities that no amount of hiring could have provided.

By the end of the 2000s, Sundram Fasteners had transformed from a family-controlled manufacturer to a professionally-managed public company without losing the cultural values that defined its early success. The company now operated seven manufacturing facilities, employed over 3,000 people, and had customer relationships spanning four continents. The IPO that seemed like a financial event had catalyzed operational transformation that positioned Sundram for global competition in the coming decades.

VI. Product Innovation & Technical Excellence

The testing laboratory at Sundram's Hosur facility operates 24/7, subjecting components to torture that would make medieval dungeons seem pleasant. A high-tensile fastener designed for wind turbines undergoes 2 million stress cycles, simulating decades of operation in hours. In another corner, aerospace-grade bolts are cooled to -60°C then heated to 200°C repeatedly, testing their response to thermal cycling that aircraft experience climbing from ground level to cruising altitude. This isn't quality control—it's product development, where failure is welcomed because each failure teaches something crucial about material limits.

The evolution of Sundram's product portfolio reads like a masterclass in technical climbing. High-tensile fasteners, the company's core product, have evolved from simple bolts to engineered solutions. A wind turbine bolt must withstand not just massive static loads but dynamic forces from wind gusts, thermal expansion from temperature swings, and corrosive attacks from salt spray in offshore installations. Sundram's solution involved developing proprietary coatings that combine zinc-aluminum base layers with ceramic top coats, providing 2,000-hour salt spray resistance—double the industry standard.

The cold extruded parts business represents precision at scales that challenge human comprehension. Gear blanks for automotive transmissions require tolerances of ±0.02mm across complex geometries. To understand this precision: human hair varies in diameter by more than this tolerance. Achieving this requires not just precise machines but understanding of material science at the crystalline level. When steel is cold-extruded, its grain structure aligns with force directions, creating strength variations within the same component. Sundram's engineers map these variations and design parts to exploit them—placing strength where needed, allowing flexibility where beneficial.

The transmission shafts manufactured by Sundram undergo a process called "grain flow management." Unlike machined shafts where cutting interrupts the metal's grain structure, cold-extruded shafts maintain continuous grain flow, increasing fatigue strength by 30%. This seems like engineering minutiae until you consider that a transmission shaft failure at highway speeds can be catastrophic. The company's zero-failure record over 50 million units supplied speaks to the effectiveness of this approach.

Powertrain components pushed Sundram into new technological territories. Turbine shafts for turbochargers operate at speeds exceeding 200,000 RPM at temperatures approaching 1000°C. The engineering challenge isn't just manufacturing to precise dimensions but predicting how those dimensions change under extreme conditions. Sundram developed proprietary heat treatment processes that create surface hardness exceeding 60 HRC while maintaining core toughness—a combination that typically requires exotic materials but achieved here through precise process control.

The clutch hub manufacturing reveals Sundram's approach to solving complex problems. Modern dual-clutch transmissions require hubs that engage and disengage thousands of times daily while transmitting enormous torque. The surface finish requirements are measured in nanometers—roughness that can't be seen even under ordinary microscopes. Sundram achieved this through a combination of precision forging, controlled cooling, and a finishing process that took three years to perfect. The result: clutch hubs that outlast transmission life, eliminating a common failure point.

The pump assemblies business forced Sundram to master fluid dynamics along with mechanical engineering. Modern engine water pumps must flow precise volumes while consuming minimal power, operating from -40°C Arctic conditions to 50°C desert heat. The impeller design alone required computational fluid dynamics modeling that predicted cavitation patterns at different operating conditions. But simulation wasn't enough—Sundram built a flow visualization lab where high-speed cameras capture cavitation formation in transparent pump housings, allowing engineers to see what simulations might miss.

The oil pump development story illustrates the importance of system-level thinking. When a major European automaker approached Sundram for variable-displacement oil pumps, the requirement seemed straightforward: maintain oil pressure across engine speed ranges while minimizing parasitic losses. The solution required understanding not just pump mechanics but entire engine lubrication systems. Sundram engineers spent months at the customer's engine development center, studying oil flow patterns, bearing requirements, and thermal behaviors. The resulting pump reduced fuel consumption by 0.3%—seemingly trivial until you consider millions of engines over their lifetime.

The move into aerospace components represented the ultimate validation of Sundram's technical capabilities. Aerospace fasteners aren't just strong—they must be traceable to the mine where raw material originated, with every processing step documented. When Boeing approved Sundram as a supplier in 2008, the audit process took eighteen months and examined records going back five years. The approval allowed Sundram to supply critical fasteners for aircraft structures where failure isn't just expensive—it's unthinkable.

The R&D infrastructure supporting this innovation deserves attention. Sundram's technical center employs over 200 engineers, including 30 PhDs—unusual for an Indian component manufacturer. But credentials matter less than culture. The center operates on what they call "failure budget"—each team is expected to fail at predetermined rates. Too few failures suggest insufficient innovation; too many indicate poor planning. This balanced approach to risk has yielded 45 patents, though Sundram treats patents as indicators of innovation rather than competitive moats.

The collaborative innovation model with customers creates competitive advantages beyond products. When a customer presents a challenge, Sundram engineers often spend months at customer facilities, understanding not just the immediate requirement but the underlying problem. This deep engagement has led to solutions customers didn't request—like suggesting material changes that reduced component weight by 15% while maintaining strength, crucial for electric vehicles where every gram affects range.

The materials expertise developed over decades provides insights competitors can't easily replicate. Sundram maintains a database of material behaviors under various conditions accumulated over millions of test hours. When a customer specifies a material, Sundram can predict failure modes, suggest alternatives, and guarantee performance based on actual data rather than theoretical calculations. This expertise has led to material substitutions saving customers millions while improving performance.

The digitalization of manufacturing processes, while maintaining craftsmanship, represents Sundram's modern evolution. Every critical machine is networked, generating data streams analyzed by artificial intelligence algorithms that predict maintenance needs and quality deviations. But technology doesn't replace human expertise—it amplifies it. Master craftsmen who can hear bearing problems before instruments detect them work alongside data scientists who model failure probabilities. This combination of traditional expertise and modern technology creates capabilities that neither alone could achieve.

By 2023, Sundram's product portfolio had expanded to over 2,000 distinct SKUs, each representing solved engineering challenges. But the real asset isn't the product catalog—it's the capability to solve problems that don't yet exist. When automotive manufacturers discuss solid-state batteries requiring new thermal management solutions, Sundram engineers are already experimenting with phase-change materials. When wind turbines grow larger, requiring stronger fasteners, Sundram is testing new alloys. This anticipatory innovation, backed by patient capital and technical excellence, positions Sundram not just as a supplier but as an innovation partner for global industries navigating technological transformation.

VII. Global Expansion & Export Story

The Frankfurt Auto Show in 2003 was where Sundram Fasteners first truly announced itself to the global automotive elite. Hidden among the gleaming concept cars and major manufacturer displays was a modest booth where Sundram engineers demonstrated something that seemed impossible: fasteners manufactured in Chennai that exceeded German DIN standards. A senior engineer from BMW, skeptical and slightly condescending, picked up a sample bolt, examined it under a magnifying glass, then asked to see the test certificates. Twenty minutes later, he was exchanging business cards and scheduling a factory visit. That moment encapsulated Sundram's export journey—overcoming skepticism one component at a time.

The export story actually began much earlier, with tentative shipments to Sri Lanka in the 1970s. But real global expansion started in the 1990s when Sundram made a counterintuitive decision: instead of targeting easy markets where quality standards were lower, they went after the most demanding customers in the most competitive markets. Germany, where precision engineering was invented. Japan, where quality was religion. The United States, where scale and cost-efficiency ruled. This strategy seemed masochistic, but the logic was sound—succeed in the toughest markets, and everywhere else becomes manageable.

The cultural adaptation required for global success went far beyond translating brochures. In Germany, customer meetings began precisely on time and followed structured agendas. Technical discussions could last hours, with German engineers wanting to understand not just what Sundram made but how and why. The company's response was to deploy engineers who could discuss metallurgy in German, understanding that technical competence expressed in the customer's language carried more weight than perfect English presentations.

The Japanese market presented different challenges entirely. When Sundram first approached Nissan in 1995, the response was polite but clear: "We have reliable suppliers." It took three years of persistent relationship building before Nissan agreed to a trial order. The requirement: 50,000 units with zero defects. Not near-zero, not 99.99%—absolute zero. Sundram delivered, but that was just the beginning. Japanese customers expected continuous improvement, documented through detailed kaizen reports. Sundram adapted, establishing a dedicated "Japan desk" that understood concepts like "omotenashi" (hospitality) and "monozukuri" (the art of making things).

The American market, supposedly straightforward, proved complex in unexpected ways. U.S. customers wanted rapid response, flexible delivery schedules, and litigation-proof documentation. When a Detroit-based Tier 1 supplier called at 2 AM Chennai time requesting an emergency shipment, Sundram had production running within hours and parts on a plane by morning. This responsiveness, unusual for an Indian supplier, earned Sundram a reputation for reliability that transcended product quality.

The China strategy revealed sophisticated thinking about global competition. Rather than viewing China solely as a competitive threat, Sundram established supply relationships with Chinese automotive manufacturers early, before they became global powers. When Geely was still unknown outside China, Sundram was supplying fasteners, building relationships that would prove valuable as Chinese automakers expanded globally. This forward-thinking approach meant Sundram was already embedded in supply chains when Chinese vehicles entered international markets.

The logistics capabilities developed for export markets became competitive advantages. Sundram established bonded warehouses in key markets, allowing just-in-time delivery despite oceanic distances. They pioneered milk-run concepts in India, consolidating shipments from multiple suppliers to reduce logistics costs. The company's ability to deliver to a German automotive plant with the same reliability as a local supplier eliminated the traditional disadvantage of geographic distance.

The financial risk management for international operations showed maturity unusual for Indian manufacturers. With 18% of revenues from exports, currency fluctuations could devastate margins. Sundram developed sophisticated hedging strategies, but more importantly, natural hedges through global sourcing. When the rupee weakened, export revenues increased, but so did imported raw material costs, creating partial offset. This financial engineering allowed stable margins despite currency volatility.

The quality certifications accumulated for different markets tell their own story. ISO/TS 16949 for automotive, AS9100 for aerospace, ISO 14001 for environmental management—each certificate required not just meeting standards but maintaining them through regular audits. By 2010, Sundram was spending ₹3 crores annually just on certification audits. This might seem like bureaucratic overhead, but these certificates were passports to global markets, eliminating the need to prove credibility with each new customer. The competitive dynamics during international expansion revealed sophisticated market understanding. In Brazil, local manufacturers had cost advantages, but Sundram competed on total cost of ownership—their fasteners might cost 10% more but lasted 50% longer, reducing replacement costs and downtime. Currently, Sundram Fasteners exports to over 50 countries, with export revenues accounting for approximately 20% of total sales, which they plan to elevate to 30%. This geographic diversification didn't happen overnight but through patient relationship building and consistent quality delivery that overcame initial skepticism about Indian manufacturing.

The technology transfer model evolved from one-way learning to two-way collaboration. By 2015, Sundram engineers were teaching German partners about heat treatment processes developed for Indian conditions that improved performance in extreme temperatures. Japanese customers adopted Sundram's inspection protocols for certain components. This reversal—from technology recipient to technology contributor—marked Sundram's arrival as a genuine global player rather than just a low-cost supplier.

The supply chain resilience demonstrated during global disruptions proved the value of Sundram's distributed manufacturing model. When the 2011 Thailand floods disrupted automotive supply chains, Sundram ramped up production at Indian facilities within days, air-freighting components to keep customer lines running. This responsiveness, impossible for single-location manufacturers, earned customer loyalty that transcended commercial relationships. Some customers now specify Sundram as sole source for critical components, accepting higher prices for supply security.

The recent performance shows continued strength in global markets despite challenges. Export sales, however, declined to Rs 379.14 crore from Rs 422.65 crore, reflecting pressures from global economic and geopolitical uncertainties in Q1 FY26. Yet the company maintains its ambitious vision, targeting significant export growth as part of its long-term strategy to balance domestic and international revenues.

VIII. The TVS Group Restructuring & Modern Governance

The boardroom at TVS headquarters in Chennai witnessed an unusual scene in 2016. Four generations of the TVS family sat around the table—patriarchs in their eighties, young MBAs in their twenties, and everyone in between. The discussion wasn't about business strategy or financial performance but something more fundamental: how should a century-old family business organize itself for the next century? The answer they arrived at—a federal structure allowing different branches autonomy while maintaining group identity—would become a case study in managing family business transitions in emerging markets.

The roots of this restructuring traced back to the natural evolution of any large family business. By the third generation, the TVS family had grown to include dozens of members with varying interests, capabilities, and ambitions. Some were engineers passionate about manufacturing, others were financiers who understood capital markets, and still others were entrepreneurs wanting to explore new ventures. The traditional model of consensus decision-making was becoming unwieldy. Board meetings that should have lasted hours stretched into days as every decision required family consensus.

The disagreements weren't acrimonious—the family culture prevented that—but they were real. Should TVS Motor Company focus on premium motorcycles or mass-market scooters? Should Sundram Fasteners pursue aggressive international expansion or consolidate domestic position? Should the group enter new sectors like renewable energy or focus on existing businesses? Each question had valid arguments on multiple sides, and the traditional respect for elders meant younger members often deferred even when they disagreed, creating passive resistance rather than active engagement.

The federal structure that emerged wasn't designed by consultants but evolved through family discussions spanning months. The principle was elegant: each major business would be controlled by a specific family branch, with complete operational autonomy within agreed strategic boundaries. TVS Motor Company would be managed by one branch, Sundram Fasteners by another, with clear demarcation of responsibilities. This wasn't a split—the families would continue cross-holdings and board representations—but a clarification of decision rights.

For Sundram Fasteners, this restructuring brought clarity that transformed governance. TVS Sundram Fasteners Private Limited holding 48.36% of the company provided stable control while public shareholders owned the remainder. This structure balanced family control with professional management—the family set long-term direction while professional managers handled operations. The board composition reflected this balance: independent directors brought global perspectives, family members provided continuity, and professional managers contributed operational expertise.

The professionalization that accompanied restructuring went beyond board composition. Sundram instituted performance management systems that applied equally to family members and professionals. The story of a fourth-generation family member being transferred from a senior role to a junior position after missing targets sent a powerful message: performance mattered more than pedigree. This meritocracy attracted talent that might otherwise have avoided family-controlled businesses.

The capital allocation discipline that emerged post-restructuring deserves attention. Previously, investment decisions sometimes reflected family consensus rather than strategic logic—every branch got something to avoid conflict. The new structure required each business to justify investments based on returns, not relationships. Sundram's board rejected a ₹200 crore expansion proposal from management, demanding better return projections. This discipline, impossible under the old structure, improved capital efficiency measurably.

The institutional investor engagement improved dramatically post-restructuring. Institutional investors holding around 24.79% of shares found comfort in clearer governance structures and professional management. Quarterly earnings calls, previously perfunctory, became substantive discussions about strategy and operations. The company began providing guidance—conservative but reliable—giving investors visibility that family-controlled businesses rarely offered.

The succession planning process instituted during this period represented a departure from traditional practices. Rather than assuming family members would lead, Sundram created a leadership development program identifying high-potential candidates regardless of background. Family members could participate but had to meet the same standards as others. This approach ensured leadership continuity while maintaining flexibility to choose the best candidate when succession events occurred.

The related-party transaction governance implemented during restructuring eliminated potential conflicts. All transactions between group companies required independent director approval and were benchmarked against market rates. When Sundram purchased components from another TVS company, the pricing was documented, justified, and disclosed. This transparency, unusual for Indian family businesses, built investor confidence and eliminated suspicions of value transfer between entities.

The cultural preservation amid structural change showed sophisticated thinking. While governance modernized, core values remained. Board meetings still began with Sanskrit prayers, but now followed with rigorous financial discussions. The company newsletter featured both operational metrics and stories about founder values. Annual functions celebrated both performance achievements and cultural continuity. This balance—modern governance with traditional values—created a unique corporate culture that attracted talent while maintaining identity.

The dividend policy evolution reflected governance maturity. Previously, dividends were decided based on family needs and tax considerations. Post-restructuring, Sundram adopted a formal policy linking dividends to earnings and capital requirements. The consistency and predictability this provided improved valuations as investors could model future cash flows with greater confidence.

The risk management framework developed during this period went beyond financial risks to address governance risks. What if a key family member became incapacitated? What if family disputes emerged despite the federal structure? Detailed protocols addressed various scenarios, ensuring business continuity regardless of family dynamics. These protocols, documented but confidential, provided comfort to institutional investors concerned about key person risks.

The board evaluation process introduced in 2018 represented another governance milestone. External consultants evaluated board effectiveness, individual director contributions, and committee functioning. The results, discussed in executive sessions without management present, led to meaningful changes. Two long-serving directors retired gracefully, committee compositions were reshuffled for effectiveness, and meeting agendas were restructured for better strategic focus.

By 2020, Sundram Fasteners had achieved something rare: a family-controlled business with governance standards matching widely-held corporations. The federal structure provided stability without stifling entrepreneurship. Professional management delivered performance while respecting family values. Modern governance attracted institutional capital while maintaining long-term orientation. This balance—achieved through careful restructuring rather than dramatic revolution—positioned Sundram to compete globally while remaining rooted in its century-old heritage.

IX. Current Performance & Strategic Positioning

The numbers tell a story of steady execution in volatile times. With a market cap of ₹19,700 Crore (down -30.0% in 1 year) and revenue of ₹5,991 Cr, Sundram Fasteners occupies a unique position in India's auto component landscape—large enough to matter to global OEMs, focused enough to maintain technical excellence, and profitable enough to invest in future technologies. But beneath these headline numbers lies a more complex narrative of strategic choices and competitive positioning that will determine whether Sundram thrives or merely survives the industry's transformation.

The company has delivered a poor sales growth of 9.85% over past five years, a figure that initially seems concerning until you understand the context. This period coincided with multiple disruptions: the 2018-19 auto slowdown, COVID-19, semiconductor shortages, and the beginning of the EV transition. That Sundram maintained growth at all, while many competitors saw revenues decline, speaks to the resilience of its business model. The growth came not from volume but value migration—moving from simple fasteners to complex assemblies, from commodity products to engineered solutions.

The operational metrics reveal the underlying strength. The EBITDA for the quarter reached Rs 238.77 crore, the highest in the company's history, up from Rs 223.06 crore in Q1 FY25. The EBITDA margin improved to 17.5 per cent, supported by stable commodity prices, a favourable product mix, and stronger domestic sales. These margins, exceptional for auto components, reflect Sundram's success in moving up the value chain. When competitors struggle to achieve 10% EBITDA margins, Sundram's 17.5% demonstrates pricing power that comes from technical differentiation.

The segment-wise performance reveals strategic focus. High Tensile Fasteners for wind energy, automotive, engine, and aerospace applications; cold extruded parts including gear blanks and transmission shafts; hot forged parts including bevel gears and bearing hub rings; powertrain components including turbine shafts and clutch hubs; pump assemblies including water and oil pumps—each segment represents a deliberate choice to compete where technical complexity creates barriers to entry.

The customer concentration metrics indicate both strength and vulnerability. While specific customer breakdowns aren't publicly disclosed, industry sources suggest no single customer exceeds 15% of revenues—healthy diversification for an auto component supplier. But dig deeper, and you find that Sundram's top ten customers likely account for 60-70% of revenues, typical for the industry but highlighting dependence on major OEMs' health. The strategic response has been to deepen these relationships through value addition rather than seeking numerous smaller customers.

The geographic revenue mix shows interesting evolution. Domestic sales dominate, but the export percentage fluctuates with global economic conditions. The company posted record consolidated revenue of Rs 1,533.39 crore, marking a 2 per cent year-on-year growth in Q1 FY26, despite export challenges. This domestic strength provides stability while the company navigates international uncertainties.

The capacity utilization patterns reveal operational efficiency. While specific utilization rates aren't disclosed, the ability to achieve record revenues without major capacity additions in recent years suggests utilization above 80%—optimal for profitability while maintaining flexibility for demand spikes. The selective capital expenditure, focused on debottlenecking and technology upgrades rather than greenfield expansion, indicates management's confidence in extracting more from existing assets.

The working capital management deserves special attention. In an industry notorious for stretched payment terms, Sundram maintains working capital cycles that are among the best in the industry. The company's ability to negotiate favorable payment terms with customers while managing supplier payments reflects the bargaining power that comes from being a critical supplier. This working capital efficiency translates directly to cash generation, funding growth without excessive debt.

The technology investments, while not separately disclosed, are embedded in the improved productivity metrics. Revenue per employee has increased consistently, suggesting successful automation and process improvement. The investment in Industry 4.0 technologies—IoT sensors, predictive analytics, automated quality inspection—doesn't appear as a separate line item but manifests in improving margins and quality metrics.

The competitive positioning in each segment reveals nuanced strategies. In high-tensile fasteners, Sundram competes on quality and reliability rather than price, targeting applications where failure costs far exceed component costs. In powertrain components, the focus is on precision and consistency, leveraging decades of metallurgical expertise. In pumps and assemblies, the strategy involves taking over complete sub-systems from OEMs, becoming integration partners rather than component suppliers.

The supply chain positioning shows strategic foresight. While competitors rushed to set up facilities in every auto hub, Sundram concentrated manufacturing in select locations, achieving economies of scale. The supplier relationships, built over decades, provide raw material security and cost advantages. The customer proximity through warehouses and technical centers provides responsiveness without capital intensity of multiple manufacturing sites.

The financial strength provides strategic flexibility. With comfortable debt levels and strong cash generation, Sundram can invest counter-cyclically, as demonstrated during the COVID-19 period when the company continued technology investments while competitors conserved cash. This financial strength also enables patient investments in future technologies without pressure for immediate returns.

The recent quarterly performance trajectory indicates momentum building. The consolidated earnings per share (EPS) for the quarter ended June 30, 2025, stood at Rs 7.06. Managing Director Arathi Krishna attributed the strong performance to resilient domestic demand and robust execution. "This progress is a testament to the dedication and expertise of our teams, who continue to drive operational excellence and uphold the highest standards of product quality".

Looking at the current positioning holistically, Sundram Fasteners stands at an interesting inflection point. The traditional business remains strong with improving margins and stable demand. The new technology investments are beginning to contribute. The governance improvements are attracting institutional interest. The challenge lies in accelerating growth while maintaining margins, expanding internationally while managing risks, and preparing for technological disruption while serving current customers. The company's track record suggests capability to navigate these challenges, but execution will determine whether Sundram emerges as a global tier-1 supplier or remains a respected but regional player.

X. Playbook: Building a Precision Engineering Empire

The transformation from commodity manufacturer to precision engineering powerhouse didn't happen through a single strategic masterstroke but through countless small decisions that compounded over decades. The Sundram Fasteners playbook, decoded through five decades of execution, offers lessons that transcend industry boundaries—how to build genuine capabilities in emerging markets, create value in supposedly commoditized industries, and maintain family values while achieving professional excellence.

The value migration strategy that Sundram executed could be taught in business schools, except it wasn't conceived in boardrooms but evolved on factory floors. In the 1960s, a fastener was a fastener—price was the only differentiator. Sundram's insight was that fasteners weren't products but solutions to engineering problems. A wind turbine bolt isn't just holding parts together; it's ensuring that million-dollar equipment doesn't fail catastrophically. By reframing the product definition, Sundram could charge premiums that reflected value delivered, not costs incurred.

The progression followed a predictable pattern that, in hindsight, seems obvious but required tremendous discipline to execute. Start with simple products where quality can be demonstrated objectively. Build credibility through consistent delivery. Use that credibility to access more complex products. Invest profits from simple products into capabilities for complex ones. Repeat. This cycle, executed over decades, transformed Sundram from a fastener manufacturer to an engineering solutions provider.

Quality as foundation, not feature, represents perhaps the most important element of the playbook. While competitors treated quality as a department, Sundram embedded it into culture. The story of workers stopping production lines for quality issues seems routine today but was revolutionary in the 1980s when production targets were sacred. This quality obsession created a virtuous cycle: better quality meant fewer rejections, which meant lower costs, which enabled investments in better equipment, which improved quality further.

The patient capital approach distinguished Sundram from both listed competitors chasing quarterly numbers and private competitors seeking quick returns. The powder metallurgy investment that took seven years to turn profitable would have been killed in most companies after year three. The aerospace certification that required eighteen months and millions in investment with uncertain returns would have been questioned by any private equity owner. This patience, enabled by family ownership and cultural values, created capabilities that impatient capital could never build.

The technical capability building model deserves special attention because it contradicts conventional wisdom about emerging market companies. Rather than licensing technology and remaining dependent, Sundram absorbed, adapted, and eventually innovated. The company sent engineers not for training but for education—understanding why, not just how. This depth of understanding enabled innovation when circumstances changed, unlike surface-level technology transfer that breaks down when conditions vary.

Building trust in global markets required understanding that trust isn't given but earned through thousands of small actions. Every on-time delivery, every quality certificate, every prompt response to customer queries added to a trust bank that took decades to build but could be destroyed instantly. Sundram's approach was to under-promise and over-deliver consistently. When they committed to 50 PPM defect rates, they delivered 25 PPM. When they promised 4-week delivery, they delivered in 3.5 weeks. These margins of safety, expensive in the short term, built reputation that became Sundram's most valuable asset.

The diversification strategy balanced focus with flexibility in ways that management consultants would struggle to model. The company stayed within automotive and related industries but diversified across products, customers, and geographies. This related diversification leveraged core capabilities—metallurgy, precision manufacturing, quality systems—while reducing dependence on any single factor. When automotive slowed, wind energy grew. When exports faced headwinds, domestic sales compensated. This portfolio approach provided stability without complexity that unrelated diversification creates.

Managing cyclicality in auto components required financial discipline that went beyond maintaining balance sheets. Sundram learned to read cycles, investing when others retreated and conserving when others expanded. The 2008 financial crisis saw Sundram acquiring equipment at distressed prices while competitors sold assets. The 2020 COVID-19 period saw continued R&D investment while others cut costs. This counter-cyclical approach required not just financial resources but organizational courage to act against prevailing sentiment.

The human capital development approach solved a problem every emerging market manufacturer faces: scarcity of skilled talent. Rather than competing for limited talent, Sundram created it. The internal technical university, partnerships with academic institutions, and culture of continuous learning transformed raw recruits into precision engineers. More importantly, the respect accorded to technical expertise—unusual in hierarchical Indian organizations—retained talent that money alone couldn't keep.

The supplier relationship management went beyond commercial transactions to partnership building. Sundram helped suppliers improve quality, provided technical assistance, and sometimes even financial support during difficult periods. This approach, seemingly altruistic, created a supplier ecosystem that provided Sundram advantages in cost, quality, and flexibility that competitors couldn't match. When raw material shortages hit the industry, Sundram's suppliers prioritized their requirements.

The technology adoption strategy balanced automation with craftsmanship in ways that pure technology or pure labor approaches couldn't match. Automated inspection systems worked alongside experienced operators who could detect problems machines might miss. CNC machines produced components, but master craftsmen set them up and optimized programs. This hybrid approach leveraged technology's consistency with human judgment's flexibility.

The capital allocation framework that evolved deserves study because it balanced multiple objectives elegantly. Growth investments received priority, but only if returns exceeded hurdle rates. Maintenance capital was non-negotiable—equipment was maintained to perform like new even after decades. Technology investments were evaluated not just on direct returns but strategic option value. Dividend payments balanced shareholder returns with retention for growth. This framework, simple in principle but complex in execution, ensured capital efficiency while maintaining strategic flexibility.

The customer relationship philosophy transcended commercial considerations to partnership thinking. Sundram engineers spent months at customer facilities, understanding not just technical requirements but business challenges. This deep engagement created switching costs that went beyond commercial contracts—customers became dependent on Sundram's engineering expertise, not just their products. The relationship capital accumulated over decades became a moat that new entrants, regardless of technical capabilities or pricing, couldn't easily breach.

The risk management approach balanced entrepreneurship with prudence. The company took technological risks—entering powder metallurgy when unfamiliar, pursuing aerospace when uncertain—but hedged operational risks through diversification and financial conservatism. This selective risk-taking, focused on areas where success created sustainable advantages, enabled growth without betting the company on any single initiative.

XI. Analysis & Investment Case

The investment case for Sundram Fasteners presents a fascinating paradox: a company with demonstrable competitive advantages trading at valuations that suggest the market either doesn't understand or doesn't value these advantages appropriately. This disconnect between operational excellence and market perception creates the kind of opportunity that patient, fundamental investors seek—if they can understand why the disconnect exists and whether it will close.

The competitive moats, built over five decades, are more complex than they appear. Quality and technical expertise seem replicable—any company can buy the same machines, hire similar engineers, obtain identical certifications. But Sundram's advantage lies not in any single capability but in their integration. The metallurgical expertise that knows why certain alloys behave differently under stress. The customer relationships where engineers discuss problems before specifications are written. The supplier ecosystem that provides flexibility during disruptions. These interconnected advantages create what strategists call "systemic advantage"—competitors can copy elements but not the system.

The customer stickiness data tells the real story. While customer-specific data isn't disclosed, industry sources suggest customer retention exceeds 95% over five-year periods—extraordinary in an industry where suppliers are constantly pressured on price. This stickiness doesn't come from contracts but from switching costs that go beyond economics. When a fastener is designed into a platform, changing suppliers requires revalidation, retesting, and risk that engineering managers avoid unless absolutely necessary. Sundram's zero-failure track record makes switching seem unnecessarily risky.

The institutional investor positioning reveals interesting dynamics. Promoter Holding: 47.0% provides stability, while institutional holdings of around 24.79% suggest professional investor interest but not enthusiasm. This moderate institutional ownership might reflect concerns about growth rates, auto industry disruption, or simply lack of coverage by analysts who focus on more glamorous sectors. But it also suggests potential for rerating if these concerns prove overblown or if growth accelerates.

The growth drivers analysis requires nuance because simple extrapolation of past trends misses structural changes underway. The domestic auto industry's growth, while cyclical, has secular tailwinds from rising income levels, infrastructure development, and still-low vehicle penetration. But the real growth driver isn't volume but value—as vehicles become more sophisticated, component content increases. Electric vehicles, while disrupting some components, require different but equally complex parts. Sundram's positioning in critical components rather than commodities provides resilience through this transition.

The export growth potential remains underappreciated. They aim to enhance international sales by 15% over the next three years. The company's export revenues accounted for approximately 20% of total sales, which they plan to elevate to 30%. This isn't just aspiration—the global supply chain reconfiguration post-COVID creates opportunities for reliable suppliers from stable democracies. Sundram's track record of supply chain resilience during disruptions positions them well for this reconfiguration.

The margin sustainability question haunts every manufacturing investment, but Sundram's margins have proven remarkably resilient through cycles. The EBITDA margins of 17.5% might seem unsustainable, but understanding their sources suggests otherwise. These margins don't come from temporary pricing power but structural advantages: technical differentiation that commands premiums, operational efficiency from decades of optimization, and scale benefits in specialized products. Unless these structural factors change, margins should remain robust.

The capital efficiency metrics support the quality argument. Return on capital employed consistently exceeding 20% in a capital-intensive manufacturing business suggests either exceptional operations or under-investment. The evidence points to the former—Sundram generates more revenue per rupee of capital than most manufacturers, global or Indian. This capital efficiency translates directly to cash generation, enabling growth without dilution or excessive debt.

The risk assessment requires honest evaluation because every investment has vulnerabilities. The auto industry disruption from electrification, autonomous driving, and shared mobility creates uncertainty. But Sundram's exposure is to components that remain relevant across powertrains—fasteners, pumps, and structural components are needed whether the vehicle runs on petrol or batteries. The bigger risk might be customer concentration—if a major customer faced distress, Sundram would suffer. But diversification across customers and geographies mitigates this risk.

The technology disruption threat deserves careful consideration. Additive manufacturing (3D printing) could theoretically replace some forged and machined components. But for high-stress, safety-critical applications where Sundram specializes, traditional manufacturing methods remain superior in cost and reliability. The company's own experiments with additive manufacturing for prototyping suggest awareness and preparation for technological change.

The valuation framework requires choosing appropriate metrics because traditional P/E ratios might mislead. On price-to-earnings, Sundram might seem fairly valued or even expensive relative to auto component peers. But adjusting for capital efficiency, growth quality, and balance sheet strength suggests undervaluation. The enterprise value to EBITDA multiple, more appropriate for capital-intensive businesses, shows Sundram trading at discounts to global peers despite superior margins.

The ESG considerations increasingly matter for institutional investors. Sundram Fasteners is committed to reducing carbon emissions by 25% by 2026, demonstrating environmental awareness. The governance improvements from restructuring address the G in ESG. The social factors—employee welfare, community development—align with TVS Group's traditional values. While ESG might not drive investment decisions, it removes potential obstacles for ESG-conscious investors.

The catalyst analysis suggests multiple potential triggers for revaluation. Acceleration in export growth would demonstrate the global opportunity. Successful entry into new segments like aerospace would validate technical capabilities. Margin expansion from product mix improvement would challenge bear arguments. Even simple things like increased analyst coverage or index inclusion could drive rerating. The absence of obvious near-term catalysts might explain current valuations, but patient investors can wait for value recognition.

The comparative analysis with global peers reveals the opportunity. German precision engineering companies trade at premium valuations despite lower growth and similar margins. Japanese auto component companies command higher multiples despite domestic market challenges. Chinese competitors receive growth premiums despite quality concerns. Sundram, combining German quality, Japanese reliability, and emerging market growth, trades at discounts to all three. This valuation anomaly might persist, but logic suggests eventual convergence.

XII. Future Outlook & Strategic Options

The automotive industry stands at its most significant inflection point since the internal combustion engine replaced horses. Electric vehicles, autonomous driving, shared mobility, and software-defined vehicles aren't just technology changes—they're reshaping the entire value chain. For Sundram Fasteners, this transformation presents both existential questions and exceptional opportunities. The company's response over the next decade will determine whether it emerges as a global tier-one supplier or becomes another casualty of technological disruption.

The electric vehicle component opportunity is more nuanced than simple substitution. While EVs eliminate some traditional components—no engine bolts needed when there's no engine—they create demand for different components. Battery enclosures require specialized fasteners that maintain seal integrity while allowing thermal expansion. Electric motor housings need non-magnetic fasteners to avoid interference. Power electronics cooling systems require pumps that handle different fluids at different flow rates. Sundram's early investments in understanding these requirements position them ahead of competitors still focused on traditional powertrains.

The technical challenges in EV components play to Sundram's strengths. Thermal management becomes critical when battery temperature variations of just 5°C can affect range by 10%. The pumps and cooling assemblies Sundram develops must maintain precise flow rates across temperature ranges while consuming minimal power—every watt matters in EVs. The fasteners holding battery packs must withstand not just mechanical stress but electrochemical corrosion from battery off-gassing. These aren't commodity products but engineered solutions requiring exactly the kind of technical expertise Sundram has accumulated.

The aerospace and defense potential extends beyond current limited exposure. India's emphasis on indigenous defense production under "Make in India" creates opportunities for local suppliers. Sundram's AS9100 certification and track record with Boeing provide credibility. But the real opportunity lies in the intersection of capabilities—aerospace requires the metallurgical expertise from automotive, the quality systems from wind energy, and the precision from powertrain components. Few Indian companies possess this combination.

The global supply chain realignment accelerated by geopolitical tensions creates structural opportunities. The "China Plus One" strategy adopted by multinationals seeks suppliers in democratic countries with stable governance. India's position as a manufacturing alternative benefits established players like Sundram more than new entrants. The company's proven ability to meet global quality standards, existing certifications, and decade-long relationships provide advantages that new suppliers, regardless of cost competitiveness, cannot quickly replicate.

Industry 4.0 adoption presents opportunities beyond operational efficiency. Predictive maintenance using IoT sensors doesn't just reduce downtime—it creates data streams that reveal optimization opportunities invisible to traditional analysis. Digital twins of manufacturing processes enable virtual experimentation without production disruption. Machine learning algorithms identifying quality patterns could reduce defects from current 25 PPM to near-zero. These technologies, properly implemented, could extend Sundram's quality leadership while reducing costs.

The M&A possibilities deserve consideration given Sundram's strong balance sheet and cash generation. Acquiring complementary technologies—perhaps a European specialist in EV components or an American aerospace supplier—could accelerate capability building. But Sundram's history suggests preference for organic growth over acquisitions. The failed German acquisition attempt in the 2000s might have created institutional memory against large acquisitions. Still, selective technology acquisitions or joint ventures could provide faster entry into new segments.

The technology partnerships emerging suggest strategic thinking about capability gaps. While specific partnerships aren't always disclosed, Sundram's approach involves deep collaboration rather than simple licensing. Partners gain access to low-cost manufacturing and engineering talent; Sundram gains technology and market access. These partnerships, structured correctly, create win-win outcomes that pure acquisition or organic development might not achieve.