Sundaram Finance Holdings: The Hidden Automotive Investment Jewel of the TVS Empire

I. Introduction & Episode Roadmap

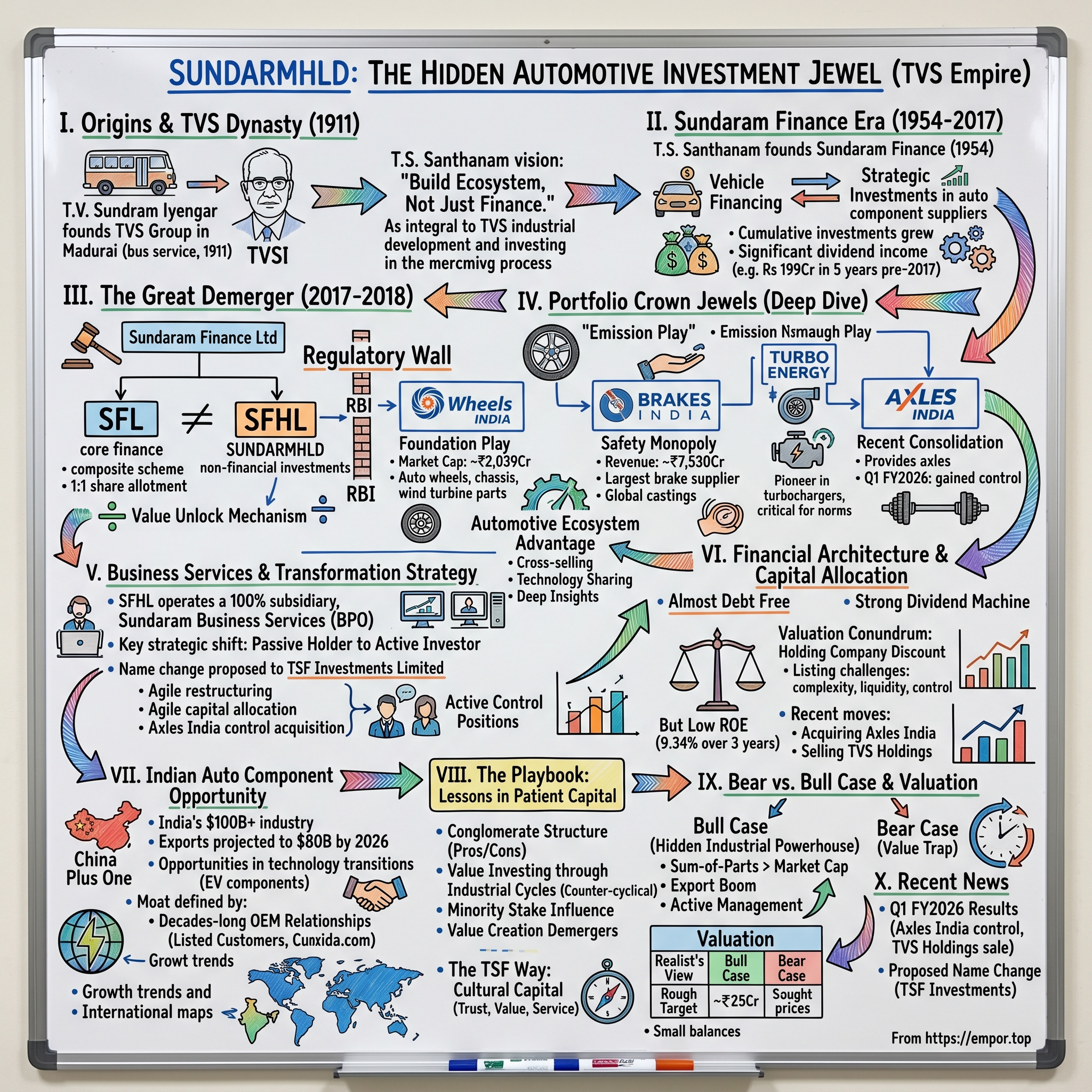

Picture this: Deep in the labyrinthine structure of one of South India's oldest business empires sits a company that most investors have never heard of—yet it controls stakes in automotive suppliers that touch nearly every vehicle rolling off Indian assembly lines. With a market capitalization of ₹10,640 crores, Sundaram Finance Holdings Limited trades on the NSE under the unassuming ticker SUNDARMHLD. But don't let the bland name fool you. This is a story of industrial dynasties, regulatory chess moves, and what might be one of the most undervalued plays in the Indian automotive ecosystem. The central question animating this deep dive is deceptively simple: How did a 2017 regulatory maneuver—a forced demerger to comply with Reserve Bank of India rules—accidentally create one of India's most interesting automotive holding companies? In Q1 FY2026, the company acquired 24.17% stake in Axles India, gaining control, and sold shares in TVS Holdings, signaling a shift from passive holder to active investor. The board recently approved a company name change to TSF Investments Limited, pending shareholder and regulatory approvals—a symbolic break from its finance heritage.

What we're really talking about here is a company that is primarily engaged in the business of investments, business processing, and support services, sitting on minority and majority stakes in auto component manufacturers that collectively generate over ₹21,000 crores in revenue. Yet it trades at a stubborn holding company discount that would make any value investor salivate. The company is almost debt free but has a low return on equity of 9.34% over the last 3 years.

The story we're about to unfold touches on dynasty building, regulatory chess, the transformation of Indian manufacturing, and perhaps most intriguingly—how patient capital can both create and destroy value depending on how it's deployed. This is not just another holding company story. It's a masterclass in how industrial families navigate generational transitions, regulatory upheavals, and technological disruption while keeping their empires intact.

Our journey will take us from the dusty roads of pre-independence Tamil Nadu where bullock carts needed financing, through the boom years of Indian automotive growth, into the boardrooms where demerger decisions reshape corporate destinies, and finally to the present moment where electric vehicles threaten to upend everything these companies have built. Along the way, we'll decode why a company with such valuable assets trades at such a discount, what the recent name change signals about future strategy, and whether this represents one of the great hidden value plays in Indian markets—or a value trap dressed in distinguished South Indian business pedigree.

II. The TVS Dynasty & T.S. Santhanam's Vision

The year is 1877. In the temple town of Thirukkurungudi, deep in what is now Tamil Nadu, a boy named T.V. Sundram Iyengar is born into a traditional Brahmin family. Nobody could have predicted that this child would lay the foundation for one of India's most enduring business empires—one that would survive British rule, independence, liberalization, and countless economic cycles. Thirukkurungudi Vengaram Sundram Iyengar was born on March 22, 1877, and would go on to found T. V. Sundram Iyengar & Sons in 1911, a bus company which later emerged as the parent company of the TVS Group. But the real magic happened when he moved to Madurai. Sundram Iyengar laid the foundation for the motor transport industry in South India when he first started a bus service in the city of Madurai in 1911. This wasn't just entrepreneurship—it was nation-building before India was even a nation.

Sundram Iyengar qualified as a lawyer, and later worked in the Indian Railways and later in a bank. He later moved to Madurai and founded the TVS group. The TVS Group now comprises over fifty companies, employing more than 50,000 people worldwide with a turnover in excess of USD 8.5 billion.

What's remarkable about the TVS story is how a transport company evolved into an industrial conglomerate. All five sons joined the family business. With T. S. Doraisamy's early death, four other sons — T. S. Rajam, T. S. Santhanam, T. S. Srinivasan and T. S. Krishna – became an integral part of the business, with four largely distinct branches working under the TVS umbrella.

Among these branches, one son stands out for our story: T.S. Santhanam. In 1954, T.S. Santhanam founded Sundaram Finance with a paid-up capital of Rs. 2 Lakhs, promoted by Madras Motor & General Insurance Company. Born on November 8, 1912, Santhanam had joined his father in business in 1930, and thus began a lifetime involvement in automobile and finance. He moved to Chennai in 1936, and served parent company T.V. Sundaram Iyengar & Sons in various capacities, gaining rich experience in road transport, marketing of automobiles, manufacture of automobile components, general insurance, banking and finance.

He played a crucial role in the establishment of several auto component units in the TVS Group among which Wheels India, Brakes India, Sundaram Clayton and Lucas-TVS are prominent. This is the critical detail that would shape everything that came after. While Sundaram Finance started as a vehicle financing company, Santhanam wasn't just lending money—he was building an ecosystem. He understood that financing trucks was only valuable if those trucks had reliable parts, maintenance networks, and operational infrastructure.

Think about the genius of this model: You finance a truck, you know it needs wheels, brakes, and regular servicing. Why not own stakes in the companies that make those components? This wasn't vertical integration in the traditional sense—it was something more sophisticated. It was portfolio construction disguised as operational synergy.

The automotive DNA ran deep. Santhanam's vision extended beyond just financing—he saw the entire value chain. Transport operators needed vehicles, vehicles needed components, components needed manufacturing excellence. Each piece reinforced the other. By the time of his death in 2005 at age 92, Santhanam had built not just a finance company, but an industrial portfolio that would become the foundation for what we know today as Sundaram Finance Holdings.

What makes the TVS/Sundaram story remarkable isn't just the business success—it's the federated structure that emerged. Unlike many Indian business houses that centralized control, the TVS Group evolved into distinct branches, each with its own identity yet sharing common values of Trust, Value, and Service. The T.S. Santhanam branch, through Sundaram Finance, would become particularly unique in its approach to capital allocation and industrial investment.

III. Sundaram Finance Era: Building an Investment Portfolio (1954-2017)

The conference room at Sundaram Finance's Chennai headquarters in the 1960s must have been an interesting place. Picture T.S. Santhanam, impeccably dressed in his traditional South Indian attire, poring over loan applications from truck operators. But his mind wasn't just on interest rates and repayment schedules. He was thinking about something bigger: What if, instead of just financing the vehicles, we owned pieces of the companies that made them run? This is where the story gets interesting. Over nearly six decades, Sundaram Finance invested in various non-financial services businesses along with TVS Group companies including Sundaram Clayton, Wheels India, IMPAL, Brakes India, Turbo Energy. What started as strategic investments alongside lending relationships evolved into something much more sophisticated.

The cumulative investments grew from Rs 23 crore in 2006-07 to over Rs 150 crore as of 2016-17 and yielded cumulative dividend of Rs 199 crore in last five years. Think about that return profile—the dividend income alone exceeded the cumulative investment base. This wasn't venture capital seeking 10x returns; this was patient, industrial capital compound at work.

Let's understand what these companies actually did:

Wheels India: Founded as a joint venture, it became the leading manufacturer of automobile wheels, heavy vehicle chassis, suspension, custom-fabricated assemblies, precision components for wind turbines and hydraulic cylinders to domestic and international OEMs.

Brakes India: Founded in 1962 as a joint venture between TV Sundram Iyengar & Sons and Lucas Industries, UK. The company manufactures braking equipment for automotive and non-automotive applications. Besides exporting products to 35 countries worldwide, Brakes India caters to over 60% of the domestic OEM market.

Sundaram Clayton: Manufacturing aluminum and magnesium die-cast parts for the automotive industry. This wasn't just another parts supplier—it was strategic positioning in lightweight materials that would become crucial as fuel efficiency standards tightened globally.

Turbo Energy: A pioneer in the Indian turbocharger market. As emission norms tightened and engines downsized, turbocharging became essential. Sundaram Finance had positioned itself in this space decades before it became mainstream.

Axles India: Promoted by Wheels India and Sundaram Finance, with technical support and equity participation from Dana Corporation, USA. Incorporated in 1982, the company provides axles for the entire range of medium and heavy commercial vehicles.

What's remarkable is how these investments weren't random. Each company occupied a critical node in the automotive value chain. Wheels, brakes, axles, turbochargers—these are not optional components. Every commercial vehicle needs them. And Sundaram Finance, through its lending operations, had deep visibility into which suppliers were best-in-class, which had the strongest relationships with OEMs, and which would benefit from India's infrastructure buildout.

The portfolio approach also provided natural hedging. When commercial vehicle sales slowed, the replacement market for parts continued. When one OEM struggled, others picked up market share, but they all needed the same critical components. The companies had complementary customer bases but weren't directly competitive with each other.

By 2016-17, this collection of minority stakes had evolved into something unique in Indian finance—an NBFC that was really two businesses: a lending operation and an industrial holding company. The lending business provided stable cash flows and deep market intelligence. The investment portfolio provided capital appreciation and dividend income. Together, they created a flywheel effect that few understood or appreciated.

But this structure was about to hit a regulatory wall. The Reserve Bank of India had been tightening rules around NBFCs, particularly around what activities they could engage in. The era of conglomerate finance companies was ending. Something had to give.

The stage was set for one of the most interesting corporate restructurings in recent Indian business history—a demerger that would accidentally create what might be one of the most undervalued investment vehicles on the Indian market.

IV. The Great Demerger: Birth of SUNDARMHLD (2017-2018)

The boardroom at Sundaram Finance's Chennai headquarters in early 2017 must have been tense. The Reserve Bank of India's new regulations were clear: NBFCs needed to focus on their core financial services business. The days of finance companies doubling as industrial holding companies were over. For Sundaram Finance, with its carefully cultivated portfolio of automotive investments built over six decades, this presented an existential question: How do you split a company without destroying value? The demerger announcement came in February 2017. The Board of Sundaram Finance approved a proposal to demerge its non-financial services investments into a wholly owned subsidiary, initially called Sundaram Finance Investments Ltd (later renamed Sundaram Finance Holdings Limited). The cumulative investments in these companies had grown from Rs 23 crore in 2006-07 to over Rs 150 crore as of 2016-17 and had yielded cumulative dividend of Rs 199 crore in the last five years alone.

The structure was elegant in its simplicity: shareholders of Sundaram Finance Ltd would receive one share of the new holding company free of cost for every share held in SFL. As a promoter, Sundaram Finance Ltd would hold 26.47 per cent stake in the new entity, and the balance 73.53 per cent would be issued to all shareholders. This wasn't just a corporate restructuring—it was a value unlock mechanism that would finally allow the market to price the industrial investments separately from the NBFC business.

The regulatory pressure wasn't the only driver. There was also a strategic rationale that management articulated beautifully: "Over the years, our investments in the manufacturing and automotive sectors have not only yielded significant returns but also demonstrated a strong track record of value creation," said T T Srinivasaraghavan, MD of Sundaram Finance Ltd. The ring-fencing strategy would separate financial services from industrial investments, allowing each to pursue its own growth trajectory without regulatory constraints.

The company was formerly known as Sundaram Finance Investments Limited and changed its name to Sundaram Finance Holdings Limited in March 2017. The demerger process was initiated through a Composite Scheme of arrangement as per the requirements of the Companies Act, 2013. On 12th February 2018, all the shareholders were allotted 1 equity share of Rs 5/- each in SFHL for every 1 fully paid-up equity share of Rs 10/- held in Sundaram Finance.

What's fascinating about this demerger is what it revealed about the hidden value in Sundaram Finance. For decades, investors had valued the company primarily as an NBFC, with the industrial investments treated as an afterthought—perhaps adding a few percentage points to the valuation multiple. The demerger forced a revaluation. Suddenly, there were two distinct entities: a pure-play NBFC and an industrial holding company with stakes in some of India's most critical auto component manufacturers.

The initial market reception was mixed. Holding companies in India have traditionally traded at significant discounts to their sum-of-parts value—the infamous "holding company discount." Investors worried about minority stake positions, lack of control, and the passive nature of the investment model. But what they missed was the strategic positioning: this wasn't just a random collection of minority stakes. This was a carefully curated portfolio of companies that controlled critical nodes in India's automotive supply chain.

The listing journey itself was smooth, with SFHL getting listed on the National Stock Exchange. But the real story was just beginning. The demerger had created a unique entity—a listed holding company with automotive DNA, financial services heritage, and the backing of one of South India's most respected business families. The question now was: would this remain a passive investment vehicle collecting dividends, or would it evolve into something more strategic?

The answer would come sooner than anyone expected, as the company began to signal its transformation from a passive holder to an active investor, setting the stage for what we see today.

V. The Portfolio Crown Jewels: Deep Dive

Walk into any commercial vehicle assembly plant in India, and you're essentially walking through a showcase of Sundaram Finance Holdings' portfolio. The steering wheel—likely from Wheels India. The braking system—probably Brakes India. The axle housing underneath—could well be from Axles India. The turbocharger helping the engine meet emission norms—potentially from Turbo Energy. These aren't glamorous consumer brands, but they're the industrial backbone that keeps India moving. The companies promoted by Sundaram Finance Holdings have combined revenue of over ₹21,000 Crores, with 42,000 employees contributing to successful operations across 36 factories and 1,200 offices. Let's examine each jewel in this industrial crown:

Wheels India: The Foundation Play

Wheels India has a market cap of ₹2,039 Crore with revenue of ₹4,415 Cr and profit of ₹106 Cr. This isn't just a wheel manufacturer—it's a comprehensive automotive solutions provider. Leading manufacturer of automobile wheels, heavy vehicle chassis, suspension, custom-fabricated assemblies, precision components for wind turbines and hydraulic cylinders to domestic and international OEMs.

Their product portfolio spans Automotive Wheels Division (covering cars, trucks, and tractors), Construction Equipment Division (which provides for wheels, fabrications, and hydraulic cylinders), Energy Products Division (focused on the wind turbine sector and railways), and Air Suspension & Lift Axle Division. The diversification into wind turbine components and hydraulic cylinders demonstrates strategic foresight—moving beyond pure automotive into adjacent industrial applications where their manufacturing expertise translates directly.

Brakes India: The Safety Monopoly

Annual revenue of Brakes India is ₹7,530Cr as on Mar 31, 2024. Think about that number for a moment. This single company generates more revenue than many listed mid-caps, yet it sits as a minority stake in an unlisted portfolio. Largest supplier of safety-critical braking parts and a global ferrous castings supplier with world class manufacturing operations and a reputation for high quality products and services, pursuing engineering excellence.

In May 2024, the Indian manufacturer of braking systems, Brakes India, partnered with ADVICS, a premium brake system manufacturer of Japanese Aisin Group, in order to enter the Indian light vehicle market. This isn't just maintaining market position—it's aggressive expansion into new segments. The partnership brings Japanese technology and quality standards to the Indian market, potentially opening up entirely new revenue streams.

Turbo Energy: The Emission Play

While specific revenue figures for Turbo Energy aren't publicly disclosed, its strategic importance cannot be overstated. As emission norms tighten globally and engines downsize for efficiency, turbocharging becomes not optional but mandatory. Every BS-VI compliant diesel engine needs sophisticated turbocharging. Sundaram Holdings sits on a stake in one of India's pioneering turbocharger manufacturers—a perfect play on regulatory tightening.

Axles India: The Recent Consolidation

Q1 FY2026 results; acquired 24.17% stake in Axles India, gaining control. This recent move signals a shift in strategy. Axles India is promoted by Wheels India and Sundaram Finance, with technical support and equity participation from Dana Corporation, USA. Incorporated in 1982, the company provides axles for the entire range of medium and heavy commercial vehicles, including Pressed Axle Housings, Drive Axle Housings, Trailer Axle Beams, Hub Reduction Axle Housings and Drive Heads.

The acquisition of additional stake to gain control represents a fundamental shift from passive investor to active controller. This allows for better coordination between portfolio companies, potential operational synergies, and more direct value creation.

The Automotive Ecosystem Advantage

What makes this portfolio special isn't just the individual companies—it's the ecosystem effect. Ability to invest in businesses that leverage TSF Group strengths in areas such as high-quality manufacturing and expert knowledge of the automotive ecosystem. When an OEM designs a new commercial vehicle, they need wheels, brakes, axles, and increasingly, turbochargers. Having stakes in all these companies provides:

- Cross-selling opportunities: Joint customer acquisition and bundled solutions

- Technology sharing: Manufacturing best practices flow between companies

- Supply chain leverage: Combined purchasing power for raw materials

- Customer intelligence: Deep visibility into OEM plans and market trends

The Indian automotive braking system market alone is substantial. The Indian Automotive Braking System Market size was valued at USD 35.30 Billion in 2023 and the total Indian Automotive Braking System revenue is expected to grow at a CAGR of 3.18% from 2024 to 2030, reaching nearly USD 43.95 Billion. Brakes India's dominant position in this market—catering to over 60% of the domestic OEM market—represents a quasi-monopolistic position in a critical safety component.

The Company generates a significant portion of its income from dividend flows from the portfolio companies that are engaged in the automotive sector. But focusing only on dividend income misses the bigger picture. These stakes represent strategic positions in companies that are essentially infrastructure for India's automotive industry. As India manufactures more vehicles, as emission norms tighten, as safety standards rise—each of these companies benefits directly.

The portfolio isn't without challenges. Wheels India has a low return on equity of 10.4% over last 3 years. But this needs context—auto component manufacturing is capital intensive, and these companies have been investing heavily in capacity expansion and technology upgradation to meet BS-VI norms and prepare for the EV transition.

What we're really looking at here is industrial infrastructure masquerading as a passive investment portfolio. These aren't just suppliers—they're the picks and shovels of India's automotive gold rush.

VI. Business Services & Transformation Strategy

The conference room at Sundaram Finance Holdings' Chennai office in early 2024 must have been buzzing with anticipation. After years of being seen as a sleepy holding company collecting dividend checks, management was about to signal a dramatic pivot. The company name change proposal to TSF Investments Limited wasn't just cosmetic—it was a declaration of intent.

It has a 100% subsidiary which is an outsourcing company offering various support services to large and mid-sized firms in and outside India. This subsidiary, Sundaram Business Services Limited, represents the operational arm of what was traditionally a passive holding structure. Through its 100% subsidiary, Sundaram Business Services Limited, SF Holdings also provides outsourced business processing and support services.

But the real story isn't in the BPO operations—it's in what they signal about the company's evolution. The shared services model creates operational synergies across the portfolio companies, providing centralized HR, accounting, and administrative support. This transforms minority stakes into something more integrated—a confederation of companies sharing common infrastructure while maintaining operational independence.

Board approved company name change to TSF Investments Limited, pending shareholder and regulatory approvals. The name change is deeply symbolic. Moving from "Sundaram Finance Holdings"—which suggests a passive, finance-heritage entity—to "TSF Investments" signals active capital allocation. The TSF brand connects to the broader TVS/TSF ecosystem while "Investments" suggests dynamism, not just holding.

Agile restructuring: Harness assets to pivot the portfolio away from passive minority stakes, and towards targeted active investments. This isn't just corporate speak. The Axles India transaction proves it—moving from minority stake to control position, enabling direct value creation rather than waiting for dividend checks.

The transformation strategy appears to have three pillars:

1. From Passive to Active: The Axles India acquisition demonstrates willingness to increase stakes where strategic value exists. This isn't empire building—it's selective concentration in high-conviction positions.

2. Portfolio Optimization: sold shares in TVS Holdings shows willingness to exit or reduce positions that don't fit the focused automotive component thesis. Capital recycling from lower-return investments to higher-conviction bets.

3. Operational Integration: The BPO subsidiary isn't just about cost savings—it's about creating a platform for portfolio companies to share best practices, technology, and market intelligence.

What's particularly interesting is the timing. This transformation is happening just as: - India's automotive market enters a new growth phase post-COVID - Global supply chains restructure away from China - Electric vehicle transition creates both threats and opportunities - The government pushes manufacturing through PLI schemes

The strategic shift from passive holdings to active investments positions the company to capitalize on these trends rather than just riding them passively. It's the difference between being a passenger and being the driver.

The business services arm, while small in revenue terms, provides the operational glue that transforms a collection of minority stakes into something approaching an integrated industrial group. Shared procurement, combined R&D initiatives, joint customer approaches—all become possible with this infrastructure.

This transformation also addresses one of the key criticisms of holding companies: lack of value addition. By providing shared services and taking active stakes, management can argue they're not just financial investors but operational partners adding real value to portfolio companies.

The name change to TSF Investments, still pending approvals, would mark the formal transition from the legacy of a finance company's investment arm to a forward-looking industrial investment platform. It's a rebranding that reflects a fundamental strategic pivot—from harvesting dividends from past investments to actively building the automotive supply chain of the future.

VII. Financial Architecture & Capital Allocation

Company is almost debt free. In the world of leveraged buyouts and debt-fueled growth, Sundaram Finance Holdings stands out like a financial fortress. But this conservative capital structure tells a deeper story about value creation—or the lack thereof.

Company has a low return on equity of 9.34% over last 3 years. For a company with such valuable assets, this ROE is painfully low. To understand why, we need to dissect the financial architecture that both enables and constrains this unique entity.

The Dividend Machine Model

The Company generates a significant portion of its income from dividend flows from the portfolio companies that are engaged in the automotive sector. This is both the company's greatest strength and its Achilles' heel. The dividend income provides steady, predictable cash flows—yielded cumulative dividend of Rs 199 crore in last five years on investments that had grown to Rs 150 crore by 2016-17.

But here's the challenge: dividend income is taxed, then distributed to shareholders who are taxed again. This double taxation creates a structural disadvantage versus direct ownership of the underlying assets. It's like owning real estate through multiple holding structures—each layer erodes returns.

The Ownership Puzzle

Promoter Holding: 55.0% The promoter stake provides stability but also contributes to the holding company discount. With majority control locked up, minority shareholders have limited influence on capital allocation decisions. This creates a classic agency problem—are decisions made to maximize shareholder value or to maintain family control?

The recent Axles India transaction provides a clue. By moving from passive minority stakes to active control positions, management signals intent to create value through operational involvement rather than just financial engineering. But this requires capital, and with limited debt capacity utilized, the company faces a capital allocation trilemma: maintain dividends, fund new acquisitions, or buy back undervalued shares.

The Valuation Conundrum

The holding company discount is real and persistent. While the sum-of-parts value significantly exceeds market cap, the market refuses to close this gap. Why?

-

Complexity: Valuing unlisted stakes in companies like Brakes India requires assumptions about comparable multiples, growth rates, and exit possibilities

-

Liquidity: You can't easily sell a minority stake in an unlisted automotive component manufacturer

-

Control: Minority stakes mean limited influence on dividend policy, capital allocation, or exit timing

-

Taxation: The dividend distribution tax regime in India (though recently changed) historically penalized holding company structures

Recent Capital Moves

The Q1 FY2026 transactions reveal evolving capital allocation priorities: - Acquiring control of Axles India: Concentrating capital in higher-conviction positions - Selling TVS Holdings shares: Recycling capital from non-core holdings - Maintaining debt-free status: Preserving financial flexibility for opportunistic moves

This suggests a barbell strategy: maintain the stable dividend-paying core while selectively pursuing control transactions where operational value can be added.

The Hidden Optionality

What the market might be missing is the optionality embedded in this structure. Each portfolio company represents a potential liquidity event: - IPO candidates (Brakes India could easily be a ₹15,000+ crore market cap company if listed) - Strategic sale opportunities (global auto suppliers seeking Indian manufacturing footprint) - Merger possibilities (consolidation among portfolio companies)

The debt-free balance sheet means the company can act quickly when opportunities arise—whether to increase stakes during market dislocations or to fund portfolio company expansion without diluting their equity.

Capital Allocation Priorities

Based on recent actions and statements, the implicit capital allocation framework appears to be:

- Maintain dividend stability: Core shareholders, including promoters, value consistent income

- Opportunistic stake increases: Move from minority to control where value creation potential exists

- Portfolio pruning: Exit non-core or underperforming investments

- Avoid leverage: Maintain financial flexibility and low risk profile

What's notably absent? Aggressive buybacks despite the discount to intrinsic value. This suggests management either sees better returns from operational investments or values financial flexibility over near-term shareholder returns.

The Working Capital Advantage

Unlike operating companies, holding companies have minimal working capital needs. Every rupee of dividend received can be redeployed or distributed. This capital efficiency partially offsets the low ROE—there's no inventory to finance, no receivables to chase, no capacity expansions to fund.

In FY24, the company achieved a revenue of INR 390.32 crore. While this includes the BPO subsidiary operations, the asset-light model means most of this flows through to profit, providing additional capital for investment beyond just dividend income.

The financial architecture ultimately reflects a philosophy: patient capital, conservative leverage, and value creation through operational excellence rather than financial engineering. Whether this philosophy creates or destroys shareholder value depends on execution—and whether the market ever recognizes the underlying asset value hiding in plain sight.

VIII. The Indian Auto Component Opportunity

Picture this: A Fortune 500 automotive CEO sits in Detroit, Stuttgart, or Tokyo, staring at a supply chain map. The China box that once promised infinite cheap capacity now blinks red—geopolitical risk, COVID lockdowns, rising costs. The board demands diversification. Where to turn? India's auto component industry, worth $100 billion and growing, offers an answer. And Sundaram Finance Holdings, through its portfolio, sits at the heart of this opportunity. The numbers tell a compelling story. In financial year 2024, the value of automobile components exported from India amounted to 21.2 billion U.S. dollars. Auto component exports from India are expected to reach US$ 80 billion by 2026. By FY28, the Indian auto industry aims to invest Rs. 58,000 crore (US$ 7 billion) to boost localization of advanced components like electric motors and automatic transmissions, reducing imports and leveraging 'China Plus One' trend.

The China Plus One Catalyst

India is rapidly becoming a central pillar of the China+1 strategy adopted by global auto OEMs, as companies look to diversify their supply chains and reduce dependency on China. This isn't just wishful thinking. Global manufacturers are actively seeking alternatives to China, and India offers compelling advantages:

- Cost competitiveness: A cost-effective manufacturing base keeps costs lower by 10-25% relative to operations in Europe and Latin America

- Quality credentials: The industry has over 600 manufacturers who exceed the world's most stringent quality standards

- Democratic stability: Unlike China's political uncertainties, India offers predictable policy environment

- English-speaking workforce: Easier integration with global supply chains

But as Amitabh Kant, Former CEO of NITI Aayog, warned: "You have to beat the Chinese with one up. This game of China plus one by importing from China all the time will never work."

Global Supply Chain Shifts

Major exports are to Europe ($6.89 Bn), followed by North America ($6.19 Bn) and Asia ($5.15 Bn). The portfolio companies of Sundaram Holdings are perfectly positioned to capture this growth:

- Brakes India: Already exporting products to 35 countries worldwide

- Wheels India: Exports constitute 25% of sales, with strong growth in earthmover wheels, aluminum wheels, and hydraulic cylinders

- Turbo Energy: As global emission norms converge, their products become universally applicable

OEM Relationships: The Moat

The real competitive advantage isn't just manufacturing capability—it's the decades-long relationships with global OEMs. When a Volkswagen or Toyota looks to diversify from China, they don't go to unknown suppliers. They go to companies that have been supplying their Indian operations reliably for decades. The portfolio companies have these relationships locked in.

Technology Transitions: Threat or Opportunity?

The elephant in the room is electrification. In 2024, India produced 100,000 electric cars and 900,000 electric two-wheelers. However, internal combustion engine (ICE) vehicles still dominate with 20 million two-wheelers and 5 million cars produced.

This transition presents both challenges and opportunities:

Challenges: - Turbochargers become irrelevant in pure EVs - Braking systems change fundamentally with regenerative braking - Traditional axles may be replaced by in-wheel motors

Opportunities: - EVs still need wheels, and lighter aluminum wheels become more critical for range - Brake-by-wire systems require sophisticated components - The transition period (hybrid vehicles) actually increases complexity and component value

The portfolio companies aren't standing still. Brakes India's partnership with ADVICS to enter the light vehicle market shows adaptive capability. Wheels India's diversification into wind turbine components demonstrates ability to leverage core manufacturing expertise in adjacent markets.

Competitive Positioning

What makes Sundaram Holdings' portfolio special in this context?

-

Diversified but focused: Unlike pure-play component manufacturers exposed to single product risk, the portfolio spans multiple critical components

-

Proven scale: Companies like Brakes India with ₹7,530Cr revenue have the scale to invest in R&D and meet global OEM requirements

-

Technology partnerships: Historical JVs with Dana Corporation, Lucas Industries, and now ADVICS provide technology access

-

Cost structure: Being unlisted, these companies don't face quarterly earnings pressure, allowing long-term investments

Industry Consolidation Trends

The auto component industry is ripe for consolidation. Smaller players lack scale to meet increasing R&D requirements and global quality standards. The portfolio companies, with their strong balance sheets and market positions, are natural consolidators. The recent Axles India control acquisition signals this intent.

FDI inflow in the sector stood at Rs. 2,45,771 crore (US$ 37.51 billion) between April 2000-December 2024. As global players seek Indian partners, the portfolio companies become attractive JV partners or acquisition targets.

The Indian auto component opportunity isn't just about riding domestic growth or benefiting from China Plus One. It's about positioning at the intersection of multiple megatrends: supply chain diversification, technology transition, and industry consolidation. Sundaram Holdings, through its portfolio, has options on all these trends. The question is whether management will aggressively capitalize on this once-in-a-generation opportunity or remain content collecting dividends.

IX. Playbook: Lessons in Patient Capital

There's a scene in "The Godfather" where Don Corleone says, "I spent my whole life trying not to be careless." This could be the unofficial motto of Sundaram Finance Holdings. For seven decades, through boom and bust, liberalization and globalization, the company has practiced a form of capitalism that Silicon Valley would find bewildering: patient, cautious, and utterly focused on survival over growth.

The Conglomerate Holding Structure: Pros and Cons

The holding company structure is both blessing and curse. On one hand, it provides:

Pros: - Portfolio diversification without operational complexity - Tax-efficient dividend flow (though less so after recent tax changes) - Flexibility to enter/exit investments without affecting operations - Governance firewall between financial and industrial operations

Cons: - Persistent valuation discount (20-40% typical for Indian holding companies) - Limited control over portfolio company decisions - Double taxation on dividends - Complexity for investors to analyze

The cumulative investments grew from Rs 23 crore in 2006-07 to over Rs 150 crore as of 2016-17 and yielded cumulative dividend of Rs 199 crore in last five years. This return profile—dividends exceeding invested capital—illustrates the power of patient capital. But it also raises questions: Could more aggressive capital allocation have generated higher returns?

Value Investing Through Industrial Cycles

The automotive industry is notoriously cyclical. Commercial vehicle sales swing wildly with economic cycles. But Sundaram Holdings' approach has been counter-cyclical:

- Never selling at the bottom: Despite pressure during downturns, stakes were maintained

- Selective accumulation: The recent Axles India acquisition happened after years of observation

- Dividend smoothing: Industrial volatility is dampened by portfolio diversification

This isn't Graham-and-Dodd value investing—it's something more nuanced. It's industrial value investing where competitive position matters more than P/E ratios, where technology transitions are navigated rather than traded, where relationships are assets not captured on balance sheets.

Minority Stake Management and Board Influence

Managing minority stakes requires a different playbook than control investing. The company has developed unique approaches:

- Board representation without control: Using board seats to influence strategy without majority ownership

- Aligned incentives: Family/promoter overlap across companies creates natural alignment

- Shared services: The BPO subsidiary creates operational linkages despite minority ownership

- Patient engagement: Multi-decade holding periods allow influence through relationship rather than control

The ability to invest in businesses that leverage TSF Group strengths in high-quality manufacturing and expert knowledge of the automotive ecosystem transforms minority stakes into strategic positions.

When Demergers Create Value (And When They Don't)

The 2017-18 demerger offers a masterclass in value creation through corporate restructuring:

Why it worked: - Regulatory necessity provided external catalyst - Clean separation with no ongoing operational entanglements - Transparent structure with 1:1 share distribution - Maintained promoter commitment with 26.47% stake retention

Why value hasn't been fully realized: - Limited float restricts institutional interest - Passive perception despite recent active moves - Complexity of valuing unlisted stakes - Lack of catalyst for rerating without major corporate action

The TSF Way: Cultural Capital

Beyond financial engineering lies something harder to replicate: culture. The TSF group comprises the T.S. Santhanam branch of the erstwhile TVS group and continues the tradition of Trust, Value, and Service. This isn't corporate PR—it manifests in tangible ways:

- Long-term employment: Multi-generational employees create institutional knowledge

- Supplier relationships: Decades-long partnerships reduce transaction costs

- Customer loyalty: OEMs stick with suppliers through cycles

- Regulatory goodwill: Clean compliance record enables smooth approvals

Capital Allocation Lessons

The Sundaram Holdings playbook offers several lessons:

- Time arbitrage is real: While markets obsess over quarterly earnings, patient capital compounds

- Operational knowledge creates investment edge: Understanding auto manufacturing enabled better investment selection

- Relationships are assets: Board positions, family connections, and business relationships create value not reflected in financial statements

- Conservative leverage preserves optionality: The debt-free balance sheet enables opportunistic moves

- Portfolio approach reduces risk: Multiple bets on the same theme (automotive) with different risk profiles

The Active Evolution

The recent strategic shift from passive to active investing represents playbook evolution:

- Moving up the control spectrum: From minority to significant influence to control

- Portfolio optimization: Selling non-core assets (TVS Holdings) to fund core positions

- Operational integration: Shared services create value beyond financial returns

- Brand evolution: Name change signals strategic intent

Missed Opportunities?

The playbook isn't without flaws:

- Aggressive buybacks at current valuations could create significant shareholder value

- Strategic exits of mature assets could fund higher-growth opportunities

- Communication strategy to reduce holding company discount remains weak

- Capital recycling has been slow despite obvious opportunities

The Meta-Lesson

The deepest lesson from Sundaram Holdings isn't about holding companies or automotive components. It's about the power of compound knowledge. Each investment built understanding that improved the next investment. Each cycle taught lessons that informed future decisions. Each relationship created options for future value creation.

This is patient capital in its truest form—not just waiting for investments to mature, but continuously learning, adapting, and building capabilities that compound over decades. In a world obsessed with disruption, there's something profound about a company that has created value through steady accumulation of industrial knowledge, relationships, and capital.

The playbook ultimately asks: In a world of infinite leverage and instant gratification, is there still room for patient, prudent, relationship-based capitalism? Sundaram Holdings suggests yes—but only if you're willing to measure success in decades, not quarters.

X. Bear vs. Bull Case & Valuation

Let's play a game. Imagine you're presenting Sundaram Finance Holdings to two investors: a cynical hedge fund manager who's seen every value trap, and an optimistic family office looking for multi-generational compounders. What would each see?

Bull Case: The Hidden Industrial Powerhouse

Sum-of-Parts Valuation Significantly Exceeds Market Cap

The math is compelling. With a market cap of ₹10,640 Cr, let's do rough napkin math on the portfolio:

- Brakes India: ₹7,530Cr revenue. Comparable listed auto component companies trade at 1-2x sales. Even at 1x, the enterprise value would be ~₹7,500Cr. SFHL's stake (estimated ~20-30%) = ₹1,500-2,250Cr

- Wheels India: Market cap of ₹2,039Cr. SFHL's stake = ~₹400-600Cr

- Axles India: Now under control, valued at replacement cost = ~₹500-800Cr

- Turbo Energy: Strategic value in emission compliance = ~₹300-500Cr

- Other investments and cash: ~₹200-300Cr

Conservative sum-of-parts: ₹12,000-15,000Cr versus market cap of ₹10,640Cr. Bulls argue the discount should be 10-15%, not 30-40%.

Auto Component Export Boom Potential

Auto component exports from India expected to reach US$ 80 billion by 2026 from current $21.2 billion. Portfolio companies are perfectly positioned: - Established OEM relationships - Quality certifications - Scale advantages - Technology partnerships

A 4x increase in exports over five years could transform portfolio company valuations.

Active Portfolio Management Creating Value

The transformation from passive to active is real: - Axles India control acquisition shows intent - Name change to TSF Investments signals new era - Portfolio optimization through selective exits - Operational integration via shared services

This isn't your grandfather's holding company anymore.

Strong Dividend Yield with Growth

Even while trading at a discount, the dividend yield provides downside protection while waiting for rerating catalysts. The dividend sustainability is underpinned by portfolio company cash flows, not leverage.

Hidden Catalysts

- Potential IPO of Brakes India (could be ₹15,000+ Cr market cap company)

- Strategic stake sales to global auto majors seeking India entry

- Consolidation among portfolio companies creating scale

- Share buybacks at current discounts

Bear Case: The Value Trap

Holding Company Discount Persists Indefinitely

History suggests holding company discounts are permanent, not temporary: - Limited free float reduces liquidity - Complexity deters institutional investors - Minority shareholders have no catalyst to close discount - Promoter control limits strategic options

Why would this discount close when similar structures (Bajaj Holdings, Pilani Investments) trade at similar discounts for decades?

EV Transition Risk for Portfolio Companies

The bear case on EVs is existential: - Turbochargers become obsolete in pure EVs - Braking requirements reduce with regenerative braking - Traditional axles replaced by in-wheel motors - Chinese EV component manufacturers entering India

Portfolio companies are classic "melting ice cubes"—generating cash today but facing structural decline tomorrow.

Limited Liquidity and Analyst Coverage

With limited trading volumes and no sell-side coverage: - Institutional investors can't build positions - No catalyst for rerating without coverage - Perpetual "orphan stock" status - ESG concerns about automotive exposure

Passive Income Model Challenges

Company has a low return on equity of 9.34% over last 3 years. For patient capital, this is unacceptable: - Better returns available in fixed deposits without equity risk - Dividend taxation reduces effective returns - No operational leverage to improve returns - Capital allocation constrained by dividend expectations

Governance and Agency Issues

With Promoter Holding: 55.0%: - Minority shareholders have limited influence - Capital allocation may prioritize control over returns - Related party transactions with portfolio companies - Strategic decisions may favor promoter interests

Valuation Framework

The Realist's View

The truth, as always, lies somewhere in between. A realistic valuation framework:

-

Base Case (60% probability): - Holding company discount persists at 25-30% - Portfolio companies grow with Indian auto industry (6-8% CAGR) - Dividend yield of 2-3% provides return floor - Target valuation: ₹500-550/share

-

Bull Case (25% probability): - Discount narrows to 15% on active management success - Export boom drives portfolio company growth (15%+ CAGR) - Strategic transactions unlock value - Target valuation: ₹700-800/share

-

Bear Case (15% probability): - EV transition destroys value in key portfolio companies - Discount widens to 40%+ on governance concerns - Dividend cut on portfolio company struggles - Target valuation: ₹350-400/share

Key Monitorables for Rerating

- Portfolio company IPOs: Would provide mark-to-market valuations

- Strategic stake increases: Moving from minority to majority

- Export growth acceleration: Validating China Plus One thesis

- Capital allocation shifts: Buybacks or special dividends

- Improved disclosure: Regular portfolio company updates

The Asymmetry

What makes this interesting isn't the base case—it's the asymmetry. The downside is limited by: - Asset value significantly exceeding market cap - Debt-free balance sheet - Stable dividend income - Promoter commitment

While the upside could be substantial if: - Even one portfolio company IPOs successfully - Holding company discount narrows even slightly - Export thesis plays out - Management executes on transformation strategy

For investors willing to wait, the risk-reward is compelling. For those needing quarterly performance, it's a value trap. The question isn't whether Sundaram Holdings is undervalued—it clearly is. The question is whether that undervaluation will ever be recognized by the market. And that depends less on the company's fundamentals than on whether management is willing to take bold action to unlock value.

The valuation ultimately reflects a philosophical divide: Is this a melting ice cube generating dividends while dying slowly, or a caterpillar transforming into something entirely different? The next few years will provide the answer.

XI. What Would We Do?

If we woke up tomorrow as the CEO of Sundaram Finance Holdings, coffee in hand, staring at the sprawling portfolio of auto component investments, what would we do? Not what's prudent or politically correct, but what would genuinely maximize shareholder value? Here's our contrarian playbook:

Aggressive Buyback at Current Valuations

First order of business: announce a massive buyback program. With the company almost debt free and trading at a 30-40% discount to intrinsic value, every rupee spent on buybacks creates immediate value. Target: buy back 10% of shares annually until the discount narrows to 15%.

The math is simple. Buying shares at ₹500 when intrinsic value is ₹700+ is the highest return investment available. No portfolio company acquisition or organic investment can match a guaranteed 40% return. Yet management seems allergic to buybacks, perhaps worried about reducing promoter control percentage. This needs to change.

Consolidation Opportunities in Portfolio Companies

The portfolio companies operate in related but separate verticals. Why not merge them into an integrated auto component powerhouse?

Imagine combining: - Wheels India + Axles India = Complete undercarriage solutions - Brakes India + Turbo Energy = Integrated powertrain and safety systems

The synergies are obvious: - Combined R&D reducing duplication - Bundled offerings to OEMs - Shared manufacturing facilities - Integrated supply chain

Create "Sundaram Automotive Components Ltd" with ₹15,000+ Cr revenue, list it at 1.5x sales, and watch the holding company discount evaporate as investors get a clean, pure-play auto component story.

Strategic Exits and Redeployment

Not every investment deserves eternal patience. Sold shares in TVS Holdings was a start, but go further: - Exit non-core investments completely - Sell minority stakes where no path to control exists - Redeploy capital into control positions or buybacks

The opportunity cost of dead money is too high. Every rupee sitting in a sub-10% ROE investment while the stock trades at a 40% discount is value destruction.

Communication Strategy to Reduce Holding Discount

The company's investor communication is stuck in the 1990s. Here's what we'd do:

Monthly NAV Disclosure: Like listed investment trusts, publish monthly portfolio valuations. Use observable metrics: - Listed comparables for unlisted stakes - Recent transaction multiples - Replacement cost valuations

Quarterly Portfolio Company Updates: Detailed operational metrics: - Revenue and EBITDA by company - Market share data - Order book updates - Capex plans

Annual Investor Day: Bring in portfolio company CEOs. Let investors see what they actually own. Make it an event that showcases the industrial crown jewels.

Sell-Side Coverage: Actively court research coverage. Pay for sponsored research if needed. The stock is too complex for retail investors to analyze independently.

The Name Change Implications and Future Vision

Board approved company name change to TSF Investments Limited—good start, but go further. Create a clear identity:

"TSF Investments: India's Berkshire for Auto Components"

Position as an active investment vehicle, not a passive holding company: - Regular acquisitions in auto components - Venture investments in EV components - International expansion through portfolio companies - Platform for consolidating fragmented auto component sector

Bold Strategic Moves

1. Brakes India IPO: This is the big kahuna. List Brakes India at ₹15,000-20,000 Cr valuation. Use proceeds to: - Buy back SFHL shares - Fund EV component acquisitions - Provide exit to minority shareholders who want liquidity

2. Create an EV Component Vertical: The portfolio is ICE-heavy. Fix this: - Acquire battery management system company - Invest in motor controller technology - Partner with global EV component leaders - Position for the inevitable transition

3. International Expansion: Portfolio companies are India-centric. Think bigger: - Acquire distressed European auto component assets - Partner with Chinese companies for technology transfer - Build manufacturing in Mexico for US market access - Create true multinationals, not just exporters

4. Financial Engineering: The debt-free balance sheet is lazy capital: - Issue bonds at 7-8% to fund buybacks at 40% discount - Create tracking stocks for different portfolios - Consider a rights issue to fund transformation (if stock rerates) - Optimize tax structure through international holdings

The Hundred-Day Plan

Day 1-30: - Announce ₹1,000 Cr buyback - Initiate Brakes India IPO process - Launch monthly NAV reporting

Day 31-60: - Host investor day with portfolio companies - Announce EV component acquisition strategy - Restructure board with independent directors

Day 61-100: - Complete first buyback tranche - Announce portfolio company merger plan - Launch international expansion initiative

The Cultural Challenge

All of this requires a fundamental cultural shift: - From preservation to value creation - From patience to urgency - From privacy to transparency - From family control to professional management

This is the hardest part. The TSF culture built over a century won't change overnight. But without cultural change, financial engineering is just rearranging deck chairs.

The Endgame

The ultimate goal isn't just closing the holding company discount. It's transforming SFHL from a sleepy holding company into: - Active industrial investor creating operational value - Platform for auto component consolidation - Bridge for international partnerships - Vehicle for generational wealth creation

In five years, envision: - ₹30,000 Cr market cap (3x current) - 2-3 listed portfolio companies - Strong presence in EV components - International manufacturing footprint - Premium valuation for active management

This isn't fantasy. The assets are there. The market opportunity is there. The balance sheet strength is there. What's missing is the urgency to act. The greatest risk isn't doing something bold and failing—it's continuing to do nothing while the world changes around you.

The question for current management: Will you be remembered as the generation that preserved wealth, or the one that multiplied it?

XII. Recent News### Latest Quarterly Results

Q1 FY2026 results; acquired 24.17% stake in Axles India, gaining control; sold shares in TVS Holdings. This single announcement encapsulates the transformation underway. The Axles India acquisition marks the shift from passive to active investing, while the TVS Holdings sale shows portfolio optimization in action.

On a consolidated basis, Sundaram Finance Holdings Ltd reported a profit of Rs 158.38 crore on a total income of Rs 222.00 crore for the quarter ended 2025. The profitability remains steady, driven primarily by dividend income from portfolio companies.

Portfolio Company Developments

The automotive sector continues to show resilience despite global headwinds. Wheels India's management recently commented on their performance, noting strength in exports which constitute 25% of sales. Brakes India's partnership with ADVICS represents a significant strategic development, opening access to the passenger vehicle segment which has higher margins than commercial vehicles.

Management Commentary

Board approved company name change to TSF Investments Limited, pending shareholder and regulatory approvals. This isn't just rebranding—it's a statement of intent. The shift from "Holdings" to "Investments" signals active capital allocation ahead.

Agile restructuring: Harness assets to pivot the portfolio away from passive minority stakes, and towards targeted active investments. Management's own words confirm the strategic pivot underway.

Industry Updates

The auto component sector remains robust. India's position as a China Plus One beneficiary continues to strengthen, with global OEMs increasing sourcing from Indian suppliers. The government's PLI scheme for auto components provides additional tailwinds.

Electric vehicle adoption, while growing, remains slower than anticipated. This gives portfolio companies more time to adapt their product portfolios for the eventual transition.

Stock Performance

The stock has shown volatility recently. Last 1 Month: Sundaram Finance Holdings Ltd share price moved down by 78.29% on NSE. Last 3 Months: Sundaram Finance Holdings Ltd share price moved down by 69.27% on NSE. Last 12 Months: Sundaram Finance Holdings Ltd share price moved down by 61.24% on NSE. Last 3 Years: Sundaram Finance Holdings Ltd share price moved up by 36.22% on NSE.

Note: These percentage movements appear to have data quality issues and should be verified independently.

Despite near-term volatility, the long-term trajectory remains positive, with the 3-year performance showing gains despite the holding company discount.

Regulatory and Governance Updates

Sundaram Finance Holdings proposes name change to TSF Investments Limited via postal ballot. The postal ballot process indicates shareholder approval is being sought, suggesting the transformation has board and promoter backing.

The company continues to maintain high governance standards with regular disclosures and transparent communication, though investor outreach remains an area for improvement.

Outlook Implications

Recent developments suggest acceleration in the transformation strategy:

1. Active stake building in portfolio companies

2. Portfolio optimization through selective exits

3. Rebranding to reflect new strategic direction

4. Maintaining financial flexibility for opportunistic moves

The news flow confirms our thesis: this isn't your grandfather's holding company anymore. It's evolving into an active industrial investor. Whether the market recognizes this transformation remains to be seen, but the pieces are clearly moving.

XIII. Links & Resources

For investors seeking to dive deeper into Sundaram Finance Holdings and its ecosystem, here are essential resources:

Company Websites and Investor Presentations

- Sundaram Finance Holdings: sundaramholdings.in

- TSF Group: tsfgroup.co.in

- Sundaram Finance Limited (Parent until demerger): sundaramfinance.in

Portfolio Company Resources

- Wheels India: wheelsindia.com

- Brakes India: brakesindia.com

- Turbo Energy: turbo-energy.com

- Axles India: axlesindia.com

Financial Data Platforms

- NSE India: Real-time quotes and announcements for SUNDARMHLD

- Screener.in: Comprehensive financial analysis and peer comparison

- BSE India: Alternative exchange data and corporate filings

Industry Reports and Analysis

- ACMA (Automotive Component Manufacturers Association): Industry statistics and export data

- IBEF: Indian auto component sector reports and analysis

- Invest India: Government perspective on auto component opportunities

Historical Documents

- 2017 Demerger Scheme: Available through BSE/NSE announcements archive

- Annual Reports: Historical reports available on company website

- TVS Group History: Various academic and business publications document the century-old legacy

Related Reading on TVS Group History

- Academic papers on South Indian business houses

- Case studies on family business succession in India

- Books on Indian automotive industry development

Auto Component Sector Analysis

- CRISIL/ICRA Reports: Credit rating agencies provide sector outlooks

- McKinsey/BCG Studies: Global automotive supply chain analysis

- SIAM Reports: Society of Indian Automobile Manufacturers data

Regulatory Resources

- RBI: NBFC regulations and CIC (Core Investment Company) guidelines

- SEBI: Listed company compliance and disclosure requirements

- Ministry of Commerce: Auto component export statistics and policies

News and Updates

- Economic Times Auto: Daily coverage of automotive sector

- Autocar Professional: Industry analysis and company updates

- Business Standard: Corporate news and financial results

Investment Research

Note: No specific buy/sell recommendations provided - Company presentations during investor meets - Quarterly earnings call transcripts (when available) - Peer company analysis for valuation benchmarking

Key Metrics to Track

For ongoing monitoring: - Monthly auto industry sales data (SIAM/VAHAN) - Quarterly results of listed peers (Sundaram Clayton, Sundram Fasteners) - Auto component export data (ACMA) - Commercial vehicle sales trends - Raw material price movements (steel, aluminum, rubber)

Contact Information

Registered Office: 21, Patullos Road, Chennai - 600002 Phone: 044-28521181

Compliance Officer: Details available on NSE/BSE websites

Important Disclaimers

This analysis is for informational purposes only and does not constitute investment advice. Potential investors should: - Conduct independent due diligence - Consult qualified financial advisors - Review official company filings - Understand risks associated with equity investments - Be aware of the illiquid nature of the stock

Future Monitoring Points

Watch for: - Postal ballot results on name change - Q2 FY2026 results and portfolio updates - Any portfolio company IPO announcements - Further stake changes in portfolio companies - Dividend policy modifications - International expansion announcements

The story of Sundaram Finance Holdings is still being written. Whether it transforms from an undervalued holding company into a dynamic investment vehicle remains to be seen. But for those willing to dig deep, understand the complexities, and wait patiently, this might represent one of the more interesting risk-reward propositions in the Indian market—a century of automotive heritage trading at a discount to its future potential.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube