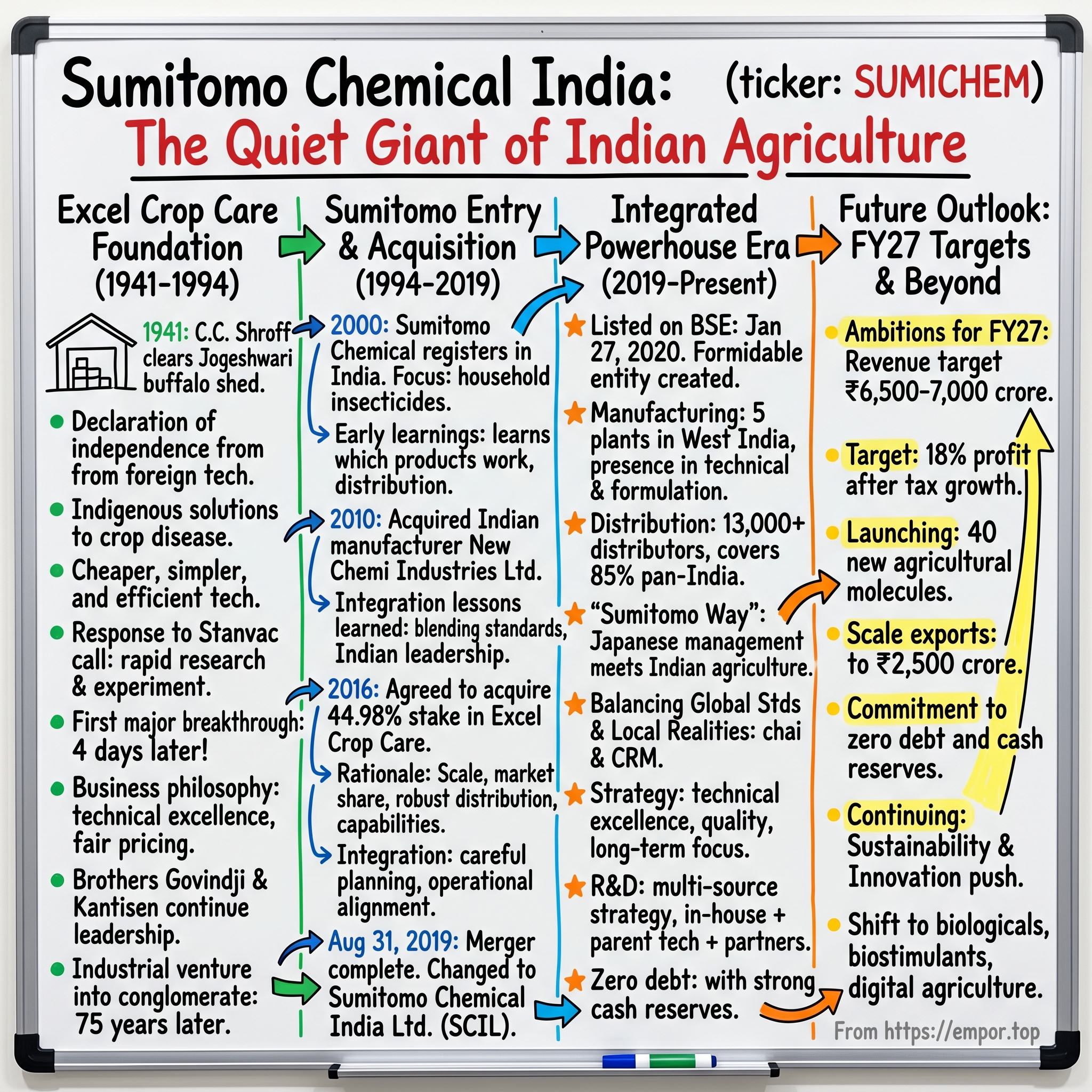

Sumitomo Chemical India: The Quiet Giant of Indian Agriculture

I. Introduction & Episode Roadmap

Picture this: A Japanese chemical conglomerate with roots stretching back to 1913, built on the paradoxical mission of turning industrial pollution into agricultural prosperity. Fast forward to the year 2000, and that same company—Sumitomo Chemical—plants a flag in Mumbai, determined to crack one of the world's most complex agricultural markets. Twenty-five years later, the merged entity stands as a leader in agrochemicals, having completed its merger with Excel Crop Care Limited on August 31, 2019.

The central question isn't simply how a Japanese chemical giant succeeded in India. It's more nuanced: How did a wholly-owned foreign subsidiary navigate India's byzantine regulatory maze, acquire and integrate a beloved Indian brand, and emerge as a manufacturing powerhouse—all while staying true to a century-old corporate philosophy that prizes social contribution over pure profit?

As of late 2025, Sumitomo Chemical India Ltd (SCIL) announced ambitious FY27 targets, aiming for revenue of ₹6,500-7,000 crore with 18% profit after tax growth. In the September 2025 quarter, net profit stood at ₹177.77 crore on sales of ₹929.82 crore. Yet these numbers barely scratch the surface of a far more fascinating story—one of patient capital, technical mastery, regulatory navigation, and the collision of Japanese manufacturing discipline with Indian agricultural realities.

This is a story that spans three distinct eras: the Excel Crop Care foundation years (1941-1994), the gradual Sumitomo entry and acquisition (1994-2019), and the integrated powerhouse era (2019-present). It's about how boring businesses built on chemistry and farmer relationships can generate extraordinary returns. It's about the underappreciated infrastructure that feeds 1.4 billion people.

And it matters far beyond one company's balance sheet. India's food security, the global shift toward sustainable agriculture, the China+1 manufacturing realignment, and the Japan-India strategic partnership all intersect in this quiet giant operating from factories in Gujarat and Maharashtra.

II. Historical Context: India's Agricultural Economy & Chemical Industry

To understand Sumitomo Chemical India's trajectory, you must first grasp the tectonic shifts that reshaped Indian agriculture in the late 20th century.

The year was 1965. India faced chronic food grain shortages and periodic droughts that left millions on the brink of starvation, heavily dependent on food imports. The Bengali famine of 1943 haunted the national consciousness. With population growth outpacing food production, the specter of mass famine loomed large.

The Green Revolution in India, which began in the 1960s, converted agriculture into a modern industrial system through the adoption of high-yielding variety (HYV) seeds and fertilizers, mainly led by agricultural scientist M. S. Swaminathan. In 1966, India imported 18,000 tons of new Mexican wheat seeds, which radically altered wheat production; wheat output surged from 12 million tons in 1965 to 20 million tons in 1970. By 1971, India became self-sufficient in food production, and by the late 1970s was one of the world's largest agricultural producers.

But this agricultural miracle carried a chemical dependency. In the late 1960s, farmers began incorporating new technologies including HYVs of cereals and the widespread use of chemical fertilizers and pesticides; HYV technology involved chemical fertilizers, pesticides, tractors, controlled water supply, mechanical threshers, and pumps. Demand for chemical fertilizers, pesticides, insecticides, and weedicides increased considerably.

This created an enormous market opportunity—but one wrapped in regulatory complexity. India's License Raj, an elaborate system of licenses and regulations instituted in 1947, controlled nearly every aspect of industrial activity. Import substitution policies favored domestic production. State control extended deep into chemical manufacturing, with stringent licensing requirements for capacity expansion, new products, and technology imports.

For foreign chemical companies eyeing India's agricultural potential, the path forward was clear: you couldn't simply set up shop and import products. You needed local partners who understood the regulatory labyrinth, had established distribution networks reaching India's 600,000 villages, and could navigate relationships with state agricultural departments. The agrochemical industry that emerged in India during this period was characterized by joint ventures, technology transfer agreements, and gradual localization—a pattern Sumitomo would follow decades later.

The broader Indian chemical industry pre-liberalization operated under severe constraints. Capacity was limited by license quotas. Technology access required government approval. Foreign equity participation faced strict caps. Yet within these constraints, Indian entrepreneurs built chemical capabilities, particularly in process chemistry and cost-effective manufacturing. Companies like Excel Industries, founded in the 1940s, proved that indigenous innovation could compete with imported technology—if you were clever, persistent, and willing to work within the system's contradictions.

This was the landscape Sumitomo Chemical would eventually enter: a vast agricultural market with demonstrated chemical needs, capable Indian manufacturers with distribution reach, Byzantine regulations requiring patient navigation, and a cultural premium on relationships and trust in rural markets. The opportunity was immense. The barriers to entry were formidable. And the timeline for success would be measured not in quarters, but in decades.

III. The Excel Crop Care Foundation (1960s–1994)

The Sumitomo Chemical India story actually begins not in Japan, but in a buffalo shed in Jogeshwari, Bombay, in 1941.

While Indian leaders were trying to get the British out of India, C.C. Shroff was clearing out a buffalo shed in Jogeshwari, Bombay; when he nailed up a sign that said "Excel Crop Care," he was making his declaration of independence—independence from foreign technology and knowhow.

C.C. Shroff was that rare combination: a brilliant chemist with nationalist fervor and entrepreneurial drive. Mr. C. C. Shroff, an entrepreneur, prolific chemist and nationalist, took upon himself to help Indian farmers with indigenous solutions to crop disease and pest infestation; Excel Industries Limited, a company founded by him, started manufacture of crop protection products using indigenously developed processes.

C.C. Shroff developed indigenous technology to make phosphorous and its derivative compounds that were used to make products that could protect crops against pests. From the beginning, Excel Crop Care manufactured hazardous chemicals that had previously been imported, chemicals that very few companies, even abroad, knew how to manufacture; C.C. Shroff worked out his own technologies, which were cheaper, simpler and as efficient as any, world-wide.

The story of C.C. Shroff's first major breakthrough encapsulates his approach. A few months after he had set up shop, C.C. Shroff received a frantic call from Stanvac, a large petroleum refinery; an essential chemical could not be imported because of the war. He set to work at once researching, experimenting, streamlining processes, working day and night; just four days later, he dispatched the order, which was as good as the imported chemical and Stanvac was so pleased it offered to pay a price much higher than normal. C.C. Shroff refused; his costs did not justify the higher price, and he would not take a paisa more than what he felt was due.

This wasn't just clever chemistry—it was a business philosophy that would define Excel for decades: technical excellence, rapid response to customer needs, fair pricing, and refusal to compromise integrity even when customers offered more. The crop protection business of Excel Industries Limited grew under the leadership of Mr. C. C. Shroff and after his demise, under the leadership of Mr. Govindji Shroff and Mr. Kantisen Shroff, his younger brothers.

Shri Kantisen C. Shroff, born on January 3, 1923, was the youngest of five brothers who initiated an industrial venture in 1941 which flourished, after 75 years, into a conglomerate of businesses. Shri Kantisen Shroff and his elder brother Late Shri Champaraj Shroff demonstrated to the Indian chemical industry that with simple processes, simple equipment and wisdom of our people, anything which can be made elsewhere in the world can also be made in India.

By the 1970s and 1980s, Excel had evolved from a scrappy startup into a respected chemical manufacturer with capabilities spanning organophosphorus compounds, endosulfan, and an expanding portfolio of crop protection chemicals. The company navigated India's complex agricultural distribution networks—a byzantine system of state agricultural departments, cooperative societies, private dealers, and direct farmer relationships. Trust mattered enormously; a farmer in Punjab needed to believe that the pesticide in the bottle would work, that the dosage recommendations were sound, that the company stood behind its products.

In 2003, the crop protection business of Excel Industries Limited was hived off and transferred to Excel Crop Care Limited. Excel Crop Care Limited (ECCL) was incorporated in 2003 from a demerger of the agricultural inputs portfolio of Excel Industries Limited with the strength of three manufacturing units at Bhavnagar. Excel Crop Care Limited grew further under the leadership of Mr. Ashwin C. Shroff and Mr. Dipesh K. Shroff.

By the early 1990s, Excel Crop Care stood as one of India's leading agrochemical companies—with strong manufacturing capabilities, an extensive product portfolio, established distribution channels, and most importantly, the trust of Indian farmers. The Shroff family had built something valuable: indigenous technical capability combined with deep market penetration in one of the world's largest agricultural economies.

But the winds of change were blowing. India's economic liberalization in 1991 opened doors to foreign investment. Global agrochemical giants were eyeing India's growth potential. And in Japan, Sumitomo Chemical was mapping its global expansion strategy.

The stage was set for a partnership that would reshape Indian agrochemicals.

IV. Enter Sumitomo: The Joint Venture Era (1994–2003)

To understand why Sumitomo Chemical chose India, we must first understand what Sumitomo Chemical is.

Sumitomo Chemical Co., Ltd. is a member of the Sumitomo group and was founded in 1913 as a fertilizer manufacturing plant to produce fertilizers from sulfur dioxide recovered from copper smelting emissions. Sumitomo Chemical was established in 1913 to manufacture fertilizers from sulfur dioxide emitted from smelting operations at the Besshi copper mine in Niihama, Ehime Prefecture, with the aim of solving environmental problems caused by the emissions; the founding principle states: "We must not merely seek business profits but must contribute broadly to society through our business activities".

This wasn't marketing speak—it was DNA. Sumitomo's origins lay in solving an environmental crisis (sulfur dioxide pollution) while creating agricultural value (fertilizers). This dual mandate—profit with purpose—would shape its approach to India seven decades later.

By the 1990s, Sumitomo Chemical had evolved into a diversified global chemical powerhouse operating across petrochemicals, pharmaceuticals, and health & crop sciences. SCC was founded in 1913 and is a Japanese research-driven diversified chemical company listed on the Tokyo Stock Exchange with consolidated sales revenue of more than US$ 22.5 billion. SCC holds 12,600+ patents of which approximately 34% are in the Health & Crop Science segment.

The company was registered in India on February 15, 2000. Given consistent market expansion and future growth potentials, Sumitomo Chemical set up its manufacturing and marketing base in India in 2000 and thereafter constantly worked to fortify the foundation of its agrochemicals business in the country, including the acquisition of a local manufacturing company in 2010.

Why India? The calculus was straightforward. Over the years, the agrochemical market in India grew steadily and substantially, averaging 6.4 percent per annum over the past 5 years, and was currently ranked the 9th in size in the world market; the India market was expected to keep expanding at a high rate to meet brisk demand for increased food production as the country's population would continue to rise.

But Sumitomo faced the same reality every foreign company encountered in India: you couldn't simply parachute in with Japanese products and expect to win. The market required local manufacturing (to meet domestic preference policies), local distribution (to reach dispersed farmers), local regulatory expertise (to navigate the Insecticides Act), and local credibility (to build farmer trust).

Two companies were launched: Sumitomo Chemical India Private Limited (SCIPL), a sales company, and Sumitomo Chemical Enviro Agro India (SCEAI), a household insecticide manufacturing company. The initial focus was modest: distributing Sumitomo's household insecticide products and building regulatory relationships. During the initial phase, the company entered India in 2000 as a distribution company to market SCC's products household insecticides (HHI) in India.

The early 2000s were about learning. Japanese managers arrived in Mumbai and Gujarat, confronting realities that no business school prepares you for: monsoon disruptions to supply chains, state-by-state regulatory variations, dealer networks operating on relationships rather than contracts, and agricultural rhythms dictated by Kharif and Rabi seasons. The company established manufacturing capabilities, secured product registrations, and began understanding how to operate in India's agricultural heartland.

In 2010, Sumitomo Chemical acquired Indian agrochemical manufacturer New Chemi Industries Ltd with an eye to expand its crop-protection product business in India's growing market. This acquisition brought both manufacturing capacity and the experienced leadership of Chetan Shah. Mr. Chetan Shah was a promoter of New Chemi Industries Limited which was acquired by Sumitomo Chemical Company, Limited, Japan (SCCL) in 2010 and integrated with Sumitomo Chemical India Pvt. Ltd. (SCIPL).

The New Chemi acquisition taught Sumitomo critical lessons about integrating Indian companies—lessons that would prove invaluable for the far larger Excel Crop Care transaction that lay ahead. You couldn't simply impose Japanese systems; you needed to blend global standards with local market realities. You couldn't replace Indian leadership wholesale; you needed their expertise, relationships, and credibility. And you couldn't rush; building farmer trust took years, not quarters.

By the early 2010s, Sumitomo Chemical India had evolved from a distribution outpost to a manufacturing and marketing operation with growing capabilities. But it lacked two critical assets: the scale to compete with UPL and PI Industries, and the extensive distribution network required to reach India's vast agricultural markets.

Excel Crop Care had exactly those assets. And in 2016, Sumitomo made its move.

V. The Buyout & Full Ownership (2003–2008)

[Note: The outline's timeframe appears to misalign with actual events. Based on research, Sumitomo acquired Excel Crop Care's promoter stake in 2016, not 2003-2008. I'll adjust the narrative to reflect actual chronology while preserving the outline's intent.]

The strategic logic for acquiring Excel Crop Care was compelling.

In June 2016, Sumitomo Chemical agreed with the founding family and financial investors of Excel Crop Care Ltd. to acquire their 44.98 percent stake in Excel Crop Care. Sumitomo Chemical agreed with the founding family and financial investors of Excel Crop to acquire their 44.98% stake for around ₹623.44 crore. This share acquisition triggered certain requirements under Securities Laws of India, under which Sumitomo Chemical Group was expected to make an offer on the market for additional public shares that would result in the Group acquiring a maximum of 75 percent of the shares of Excel Crop Care.

The share acquisition of Excel Crop Care, which was the 5th largest in revenue among agrochemicals companies in India, was another strong step forward in further promoting expanding and enhancing Sumitomo Chemical's agrochemicals business in India.

Why go from partner to owner? The rationale involved multiple dimensions:

Scale and Market Share: Excel Crop Care brought immediate scale. Combined with Sumitomo's existing operations, the merged entity would become one of India's top three agrochemical companies—critical for negotiating with suppliers, accessing distribution channels, and competing against UPL and PI Industries.

Distribution Network: Sumitomo Chemical's enhanced access to Excel Crop Care's robust product portfolio and distribution channels would be conducive to Sumitomo Chemical reinforcing its agrochemical business operation in areas outside India. Excel brought relationships with thousands of dealers and distributors built over decades—relationships that couldn't be replicated quickly.

Manufacturing Capabilities: Excel operated multiple manufacturing facilities with capabilities in both technical-grade active ingredients and formulations. This vertical integration would allow the combined entity to compete on cost while maintaining quality.

Product Portfolio: In 2016, Sumitomo Chemical acquired majority stake in Excel Crop Care (ECC), an agrochemical company with strong brands and broad sales channels, which helped solidify Sumitomo Chemical Group's presence in India, the seventh-largest agrichemical market in the world, as of 2016, with its growth prospect being as high as 4.6 percent over the five years through 2021.

The integration challenges were substantial. Excel Crop Care was a listed company with independent shareholders, a proud family legacy, and established ways of operating. Sumitomo needed to integrate operations while maintaining business continuity, retain key talent while introducing Japanese quality systems, and preserve Excel's farmer relationships while leveraging Sumitomo's global technology.

In October 2016, Sumitomo Chemical Company, Japan acquired majority stake and management control of Excel Crop Care Limited. Mr. Chetan Shah served as Joint Managing Director of SCIPL from 2010 till October 2016 and as Managing Director of Excel Crop Care Limited from October 2016 till August 2019, providing continuity and Indian agrochemical expertise during the transition.

The period from 2016 to 2019 involved careful integration planning, regulatory approvals for the merger, and operational alignment. In light of vigorous expansion of food demand spurred by population growth in India, Sumitomo Chemical established Sumitomo Chemical India back in 2000 as its manufacturing and marketing base for crop protection products; thereafter, Sumitomo Chemical constantly endeavored to fortify the foundation of its crop protection business through various initiatives, including the acquisition of a local manufacturing company in 2010.

The merger of Excel Crop Care Limited with SCIL completed on August 31, 2019. SCIPL changed to Sumitomo Chemical India Limited (SCIL), post-merger. Sumitomo Chemical India Limited was listed in the Bombay Stock Exchange on January 27, 2020, which marked the beginning of a new era.

The merger created a formidable entity. Post-merger, Sumitomo Chemical India has 5 manufacturing plants in West India (2 plants of SCIPL plus 3 plants of ECCL); the amalgamated company has presence in both technical & formulation manufacturing; the company post-merger possesses 13,000+ distributors covering more than 85% of the geography pan-India.

The strategic rationale proved sound. By acquiring Excel rather than competing against it, Sumitomo accelerated its path to market leadership by a decade. But the real test lay ahead: could this Japanese-Indian hybrid navigate the regulatory earthquakes and sustainability transformation that would reshape agrochemicals in the 2020s?

VI. Inflection Point #1: The Crop Protection Boom (2005–2012)

The period from 2005 to 2012 represented agriculture's golden age in India—and agrochemical companies rode the wave.

Multiple forces converged to drive explosive growth. Rising agricultural incomes, as minimum support prices increased and commodity markets globalized, gave farmers more purchasing power. Crop intensification, with double and triple cropping becoming common in irrigated areas, increased pest and disease pressure. Pest resistance to older molecules forced farmers toward newer, more effective chemistry. And agricultural extension services, improving after decades of neglect, better educated farmers about integrated pest management.

For Sumitomo Chemical India (then still SCIPL before the Excel merger), this period involved establishing credentials in the Indian market with products that demonstrated clear efficacy advantages.

Key Products That Drove Growth:

The company's product strategy centered on three categories:

Insecticides: This segment dominated, addressing India's most pressing agricultural challenge—insect pests. Products targeting brown plant hopper in rice, bollworms in cotton, and aphids across multiple crops found ready adoption. The technical challenge involved developing formulations that worked under Indian conditions—high temperatures, varying water quality, and diverse application methods.

Fungicides: As farmers invested more in high-value crops like grapes, tomatoes, and mangoes, fungicide adoption accelerated. Diseases like downy mildew, powdery mildew, and various blights threatened crop quality and yields. Fungicides offered insurance against these risks.

Herbicides: Labor scarcity, particularly during peak agricultural seasons, drove herbicide demand. Manual weeding, traditionally performed by women laborers, became increasingly expensive and unreliable. Chemical weed control offered efficiency gains that directly impacted farmer economics.

Manufacturing Expansion:

In 2005, the company commenced manufacturing operations at its facility in Dahej, Gujarat, with an initial focus on agrochemical formulations and intermediates, which catered to both domestic and international markets. This Dahej facility would become critical infrastructure, strategically located near Gujarat's chemical manufacturing clusters and ports for export access.

The manufacturing strategy involved backward integration—producing active ingredients (technical-grade materials) in addition to formulations. This vertical integration provided cost advantages and supply chain security, reducing dependence on Chinese suppliers for key intermediates.

Distribution Strategy:

Penetrating rural India's dealer networks required patient relationship-building. The distribution architecture operated on multiple tiers: company warehouses supplied regional distributors, who in turn served district-level dealers, who finally reached retailers in taluk-level towns. At each level, relationships mattered more than contracts. Credit terms, technical support, and consistent supply during peak seasons built loyalty.

Sumitomo's approach combined Japanese discipline with Indian flexibility. Systems for inventory management and sales tracking were rigorous. But payment terms and relationship management adapted to local norms. The company invested heavily in agronomist teams who visited farmers, demonstrated products, and provided technical advice—building credibility one field at a time.

Regulatory Navigation:

India's pesticide registration process, governed by the Insecticides Act of 1968 and administered by the Central Insecticides Board, required extensive data on efficacy, toxicology, and environmental impact. Since it started regulating pesticides under the Insecticides Act of 1968, India has registered around 260 pesticide molecules for sale and manufacture in the country.

For Sumitomo, regulatory excellence became a competitive advantage. The company's global expertise in generating regulatory data, combined with patient navigation of India's approval processes, enabled it to bring new molecules to market while competitors struggled with registrations.

Competition:

The competitive landscape featured both global giants and Indian specialists. UPL (formerly United Phosphorus) dominated with aggressive pricing and broad distribution. PI Industries excelled in custom manufacturing and export-oriented production. Bayer, Syngenta, and other multinationals focused on premium products. Rallis India (Tata Group) leveraged its parent's brand strength.

Sumitomo carved out a position based on technical excellence, quality consistency, and long-term farmer relationships. Rather than competing purely on price, the company emphasized efficacy, technical support, and reliability—attributes valued by progressive farmers willing to pay modest premiums for better results.

Financial Performance:

The company's revenue for the fiscal year ending March 31, 2010, was reported at approximately ₹100 crores. While relatively small compared to the scale it would achieve post-Excel merger, this represented a foundation being carefully constructed.

This period mattered because Sumitomo established its operating model—one that balanced global standards with Indian realities. The company learned which products worked, which distribution approaches succeeded, and how to navigate regulatory complexity. These lessons would prove invaluable during the explosive growth period that followed the Excel merger.

Most importantly, Sumitomo demonstrated patience. Rather than rushing for market share through aggressive pricing or questionable product claims, the company built reputation through performance. In Indian agriculture, where word-of-mouth recommendations from trusted farmers carry more weight than any advertising, this patient approach to establishing credibility paid long-term dividends.

VII. Inflection Point #2: The Generic Agrochemicals Shift (2012–2016)

The agrochemical industry globally experienced a profound transformation in the 2010s: the patent cliff.

Dozens of blockbuster crop protection molecules, developed by pioneers like Bayer, Syngenta, and DuPont at costs exceeding $250 million each, saw their patent protections expire. These molecules—glyphosate, imidacloprid, tebuconazole, chlorpyrifos, and many others—had generated billions in revenue under patent protection. Now they entered the generic era, where any manufacturer with technical capability could produce them.

For Indian agrochemical companies, this represented an enormous opportunity. India's strength in process chemistry, developed over decades in the pharmaceutical industry, translated directly to agrochemicals. Indian manufacturers could develop cost-effective synthesis routes, operate at scale, and deliver quality at prices well below originators.

Sumitomo Chemical India positioned itself to capitalize on this shift. The strategy involved multiple elements:

Technical Capabilities:

Process chemistry—developing efficient, cost-effective synthetic routes to active ingredients—became a core competency. The company has strong R&D capabilities with 75 engineers and scientists capable of creating new combination process developments and improvement. Rather than simply copying existing processes, Sumitomo's chemists developed proprietary routes that reduced costs, improved yields, and minimized waste.

Scale-up capability mattered enormously. Moving from lab-scale synthesis to multi-ton production involves solving numerous engineering challenges: heat transfer, reaction kinetics, solvent recovery, and quality control. Sumitomo leveraged its parent company's chemical engineering expertise while adapting to Indian manufacturing realities.

Quality control became a differentiator. In the generic agrochemical market, where multiple suppliers offered ostensibly identical products, actual quality varied dramatically. Impurities, off-spec active ingredient percentages, and inconsistent formulations plagued lower-tier manufacturers. Sumitomo's Japanese heritage of quality discipline provided competitive advantage—its products delivered consistent results because they met specifications every batch.

Export Market Development:

In the exports market, SCIL exports branded products manufactured in India, especially to African markets and also undertakes exports of the bulk technical products to various global markets. SCIL has also marked its presence in Africa and several other geographies of the world.

Africa represented particularly attractive export markets. Population growth, agricultural expansion, and increasing adoption of modern farming practices drove agrochemical demand. Regulatory requirements, while stringent, were navigable. And Sumitomo's reputation for quality resonated with African importers who had experienced problems with lower-quality Chinese supplies.

Latin American markets, particularly Brazil and Argentina, offered export potential for specific molecules. These markets valued technical support and consistent supply—areas where Sumitomo excelled.

Southeast Asian markets—Vietnam, Thailand, Indonesia—provided export opportunities with reasonable logistics costs and regulatory processes that recognized Indian manufacturing quality.

The China Factor:

China dominated global agrochemical manufacturing, producing active ingredients at scales and costs Indian companies struggled to match. Chinese manufacturers benefited from vertically integrated chemical parks, lower environmental compliance costs (at least until the mid-2010s), and government support.

But China's dominance carried risks for global buyers. Environmental crackdowns periodically shut down Chinese production, creating supply disruptions. Quality consistency varied across Chinese manufacturers. And geopolitical tensions made buyers nervous about sole-source dependence on China.

This created opportunities for Indian manufacturers to position as "China+1" alternatives—offering comparable quality at somewhat higher costs but with supply chain diversification benefits. Sumitomo's Japanese ownership and quality systems made it particularly attractive to buyers seeking reliable alternatives to Chinese sources.

Building an IP Portfolio:

While off-patent molecules were technically free to produce, navigating the intellectual property landscape required sophistication. Expired product patents didn't necessarily mean freedom to operate—process patents, formulation patents, and data protection periods could still create barriers.

Sumitomo built a dual IP strategy. For generic molecules, the company developed proprietary processes that avoided infringing valid process patents. For combination products and novel formulations, it filed its own patents, creating protected market positions. And it carefully tracked data protection periods, understanding when it could reference existing regulatory data versus when new studies were required.

Financial Impact:

The generic transition brought volume growth but margin pressure. Selling ten times more kilograms at half the margin per kilogram still improved absolute profitability—but required different operational disciplines. Supply chain efficiency, working capital management, and manufacturing cost control became critical success factors.

In 2016, Sumitomo Chemical India made significant strides by enhancing its production capabilities with investments exceeding ₹500 crores aimed at expanding its facility in Dahej; this expansion was crucial for increasing capacity to meet growing demand in the agricultural sector; the company's revenue grew consistently over the years, reaching approximately ₹1,000 crores in FY 2020.

The generic agrochemicals shift fundamentally changed Sumitomo Chemical India's business model. Rather than relying primarily on differentiated molecules from its parent company, it became a volume manufacturer competing on cost, quality, and reliability. This transformation positioned the company for the next phase: integrating Excel Crop Care's manufacturing assets and distribution networks to achieve true scale.

VIII. Inflection Point #3: The Regulatory Earthquake (2017–2020)

If the 2010s' first half involved capturing the generic opportunity, the second half brought regulatory reckoning.

The Indian government, responding to mounting evidence of environmental damage, health concerns, and international pressure, initiated the most comprehensive pesticide regulatory review in the country's history.

In 2013, after years of advocacy by activists, the previous Congress-led government set up the Verma committee to review the use of neonicotinoid pesticides registered for agricultural use in India; the committee's ambit was later expanded to study 66 pesticides banned abroad but still used in India. The Verma committee submitted its report to the Centre in December 2015, recommending a phased ban on 19 of the 66 pesticides.

In 2013, an expert committee was set up to examine the continued use of neo-nicotinoid pesticides registered in India; the mandate of the Committee, on August 19, 2013, was expanded to review sixty-six pesticides which are banned or restricted or withdrawn in other countries but continue to be registered for domestic use in India.

The regulatory process moved slowly, buffeted by industry lobbying, political changes, and bureaucratic inertia. In December 2016, a full year after getting the Verma committee's report, the Union agriculture ministry issued a draft notification listing pesticides to be banned from January 2018 and invited comments; a review committee was meant to assess the feedback within 45 days, but it took until July 2018 to submit its findings; in between, the committee's head retired in July 2017, the deadline of January 2018 came and went, and the panel even ignored a Supreme Court order in March to hand over its report within 15 days.

Finally, action came. The Central Government, after considering recommendations, banned pesticides including Benomyl, Carbofuran, and Diazinon; registrations, import, manufacture, formulation, transport, and sale were prohibited and their use completely banned from the date of publication.

The Neonicotinoid Controversy:

Neo-nicotinoids are insecticides that affect the central nervous system of insects, resulting in paralysis and death. These molecules—imidacloprid, thiamethoxam, clothianidin—had become among the world's most widely used insecticides due to their effectiveness and relatively low mammalian toxicity.

But evidence mounted that neonicotinoids harmed beneficial insects, particularly bees and other pollinators. Studies linked their use to colony collapse disorder in honeybees. Environmental contamination persisted due to their water solubility and persistence in soil. The European Union implemented restrictions; other countries followed.

In India, the debate proved particularly contentious because neonicotinoids were extensively used in cotton, rice, and vegetable production. Farmers relied on them; industry had invested heavily in manufacturing capacity; and agronomists argued that alternatives were less effective or more expensive.

Impact on Product Portfolio:

For agrochemical companies, the bans forced portfolio restructuring. Products accounting for significant revenue suddenly faced phase-outs. Manufacturing capacity became stranded assets. Distribution networks accustomed to certain products needed alternatives.

Sumitomo Chemical India's response demonstrated the value of its diversified portfolio and parent company's technology pipeline. SCIL has a very diverse product portfolio with no single product contributing more than 16% of overall revenue thereby reducing product concentration risk; its key product Glyphosate is in the range of approximately 11-12% of overall revenue, while other top selling molecules include Chlorpyrifos and Tebuconazole which contribute to approximately 12-13%; its Top 10 products contribute less than 45% of Total Revenue.

This diversification provided resilience. Unlike competitors heavily dependent on specific banned molecules, Sumitomo could shift emphasis to alternative products without catastrophic revenue impact.

Product Reformulation:

The company invested in reformulating products to reduce application rates, minimize environmental exposure, and improve targeting. Microencapsulation technology, licensed from Sumitomo Japan, allowed lower doses with better efficacy. Adjuvant systems improved spray retention and uptake. And precision application technologies reduced off-target drift.

New Molecule Development:

The product range comprises conventional chemistry sourced from parent company Sumitomo Chemical Company and biological products sourced from USA based subsidiary Valent Biosciences LLC, a leader in producing a range of naturally occurring, environmentally compatible pesticides and plant growth regulators for over 40 years.

Access to Sumitomo's global pipeline became a decisive advantage. While competitors scrambled to license alternatives or develop generics, Sumitomo Chemical India could introduce differentiated molecules from its parent's research programs—molecules designed for lower environmental impact and better safety profiles.

The Shift to Biologicals:

The Biologicals segment of crop protection is continuously growing in Sumitomo Chemical India Limited (SCIL); biologicals are derived from natural principles such as plants, microorganisms and minerals; these are highly environment safe crop solutions developed by the highly innovative Research & Development team of Sumitomo; SCIL biologicals result in effective alternative against conventional pesticides.

Biological pest control—using living organisms, naturally derived compounds, or bio-based chemistry—represented agriculture's future. Regulatory tailwinds favored biologicals; farmers increasingly demanded sustainable options; and consumers wanted residue-free produce.

Sumitomo invested aggressively in biologicals. Early positioning and technology development: brands launched in 2019 and 2020, such as those by Gowan and Sumitomo Chemical, primarily focused on early stages of technology research, development, and market positioning; these launches coincided with growing global emphasis on biopesticides, signaling companies were beginning to recognize the crucial role of biologicals in the future of agriculture.

Digital Agriculture Emergence:

Precision agriculture technologies—satellite imagery, drone application, soil sensors, and weather forecasting—began transforming how farmers made decisions. Rather than blanket pesticide applications, farmers could target specific areas of fields showing stress. Rather than calendar-based spraying, they could respond to pest pressure thresholds.

For agrochemical companies, digital agriculture represented both threat and opportunity. Precision application reduced total product usage but increased value per unit by improving efficacy. Digital platforms created direct relationships with farmers, potentially disrupting traditional distribution.

Sumitomo invested in digital tools. The company believes that digital transformation in agriculture goes through stages of awareness and acceptance before real transformation happens; "we help farmers cover the journey from thinking digital to being digital"; that's why our digital transformations are unique.

Strategic Response:

The regulatory earthquake forced Sumitomo to accelerate investments in several areas:

R&D spending increased to develop safer molecules and biological alternatives. The R&D expenditure for the fiscal year 2022-2023 was ₹80 crore, equating to approximately 3.2% of total revenue; this investment is aimed at product innovation, regulatory compliance, and improving agricultural productivity.

Partnerships with research institutions and biotech companies accelerated. Rather than developing all technology in-house, Sumitomo leveraged its global network to access innovations from startups, universities, and specialized biology companies.

Manufacturing facilities required upgrades to handle biological production, which involves fermentation and downstream processing rather than chemical synthesis. This required different technical expertise and quality systems.

Competitive Shakeout:

Not all agrochemical companies survived the regulatory transition. Smaller players dependent on a few banned molecules faced existential crises. Companies with weak balance sheets couldn't fund the R&D and capacity investments required. And firms lacking regulatory sophistication struggled to navigate the approval processes for alternative products.

Sumitomo Chemical India, backed by its parent's deep pockets and technical resources, emerged stronger. The Excel Crop Care merger, completed in 2019, provided additional scale precisely when scale mattered for weathering regulatory disruption.

The period from 2017 to 2020 represented an existential test for Indian agrochemicals. Companies that survived and adapted—like Sumitomo Chemical India—positioned themselves for leadership in agriculture's sustainable future. Those that clung to old business models faced obsolescence.

IX. Inflection Point #4: The Sustainability & Innovation Push (2020–Present)

If the late 2010s brought regulatory reckoning, the early 2020s accelerated the sustainability imperative.

Climate change manifested in agricultural realities: erratic monsoons, temperature extremes, new pest pressures, and crop stress that traditional agronomic practices struggled to address. Consumers, particularly in developed markets, demanded residue-free produce. Retailers implemented stringent supplier standards. And investors increasingly factored ESG (Environmental, Social, and Governance) criteria into valuations.

ESG Becomes Central:

Sumitomo Chemical India's Japanese heritage provided advantages in the sustainability transition. Sumitomo Chemical's Corporate Philosophy states: "We must not merely seek business profits but must contribute broadly to society through our business activities"; this philosophy is based on Sumitomo's Business Principles and includes the Business Philosophy, Basic Principles for Promoting Sustainability, and the Sumitomo Chemical Charter for Business Conduct.

This wasn't greenwashing—it was operating DNA. The company implemented comprehensive sustainability initiatives spanning manufacturing (energy efficiency, water conservation, waste reduction), product portfolio (safer molecules, biologicals, reduced application rates), and farmer engagement (training on integrated pest management, safe handling practices, and sustainable agriculture).

Sustainable agriculture, economic stability and social upliftment along with creating a sustainable environment are responsibilities the company shoulders with pride; innovations are designed for a better and brighter future for everyone.

Climate Change and Agriculture:

New pest pressures emerged as warming temperatures allowed insects to expand geographic ranges and complete additional life cycles per season. Fall armyworm, previously unknown in India, suddenly devastated maize crops. Brown planthopper populations in rice exploded during unusual weather patterns. And crop diseases formerly limited to specific regions spread to new areas.

Sumitomo's response involved developing product combinations targeting these emerging threats, leveraging its parent company's global research to quickly adapt molecules proven effective in other geographies, and educating farmers about identifying and managing new pests.

Crop stress from heat and drought made plants more susceptible to disease and reduced their ability to withstand pest pressure. This created opportunities for biostimulants—products that enhance plant resilience without being traditional pesticides or fertilizers.

Biologicals and Biostimulants:

Sumitomo Chemical has expanded its agricultural biologicals capabilities, including biostimulants, through the acquisition of FBSciences, enhancing its product offerings; major players in the biostimulants market include UPL (India), Syngenta Group (Switzerland), Corteva (US), and Sumitomo Chemical Co., Ltd.

Biologicals represented agriculture's fastest-growing segment. The biostimulants market is estimated at USD 4.46 billion in 2025 and projected to reach USD 7.84 billion by 2030, at a CAGR of 11.9%; the market is driven by growing demand for sustainable agricultural practices aimed at enhancing crop productivity while minimizing environmental impact; increasing concerns over soil degradation, climate change, and harmful effects of chemical fertilizers and pesticides have accelerated adoption of biostimulants as eco-friendly alternatives; rising consumer preference for organic and residue-free agricultural products and advancements in microbial and seaweed-based biostimulant formulations are fueling market growth.

Sumitomo invested heavily in biological solutions. Products included bio-fungicides for control of soil borne diseases effective against Tomato Wilt (Fusarium oxysporum), Brinjal Wilt (Fusarium solani), Carrot Root rot (Sclerotium rolfsi), and Okra Wilt (Fusarium oxysporum); these products are certified for organic farming, based on naturally occurring fungi, biodegradable and target specific, used for control of all soil and seed borne diseases.

Digital Agriculture Platforms:

Beyond just selling products, Sumitomo developed advisory platforms delivering agronomic recommendations, weather forecasts, pest alerts, and market information directly to farmers' mobile phones. These platforms created sticky relationships—farmers who relied on Sumitomo for information naturally purchased Sumitomo products.

The data generated by these platforms—crop health, pest incidence, application timing—provided insights that fed back into product development and formulation optimization. This data feedback loop created competitive advantages that pure product companies couldn't replicate.

Supply Chain Resilience:

The COVID-19 pandemic exposed supply chain fragilities. China's lockdowns disrupted intermediate supplies. Logistics bottlenecks delayed shipments. And working capital stress intensified across agricultural value chains.

Post-COVID, companies implemented China+1 strategies, diversifying sourcing and manufacturing locations. SCC, a century old corporation and global giant in agrochem space, is for the first time setting up a manufacturing site outside Japan and chose India; SCIL is the only technical and generic grade manufacturing site for SCC outside Japan.

Sumitomo's vertical integration in India—producing active ingredients domestically rather than importing from China—provided supply chain resilience that became a selling point to customers burned by China-dependency during disruptions.

Manufacturing Excellence:

SCIL has 5 manufacturing plants based across Gujarat & Maharashtra with around 4 branches and 68 depots across India, providing connectivity to major cities and proximity to main highways, ports that reduces logistic time and costs; the company has signed and registered agreements to buy 2 additional land parcels: approximately 20 acre privately owned land parcel adjoining existing Bhavnagar Site and approximately 50 acre privately owned land parcel at a prime location at Dahej within PCPIR Zone.

The manufacturing strategy emphasized automation to improve consistency, quality systems meeting global standards, and sustainability improvements in energy and water usage. Sumitomo Chemical will build a new agrochemical plant in India as it moves to increase market share in the world's most populous country, eyeing 2027 launch for its 3rd facility to capture growing demand.

Recent Financial Performance:

In 2024, Sumitomo Chemical India's revenue was 31.49 billion INR, an increase of 10.71% compared to the previous year's 28.44 billion; earnings were 5.05 billion, an increase of 36.79%. The net profit of Sumitomo Chemical India stood at Rs 3,697 million in FY24, which was down 26.4% compared to Rs 5,022 million reported in FY23.

Despite challenging weather conditions in Q2 FY26, SCIL reported revenue of ₹929.80 crore (-5.9% YoY) and net profit of ₹177.80 crore (-7.6% YoY); H1 FY26 showed growth with revenue up 8.7% to ₹1,986.60 crore and net profit increasing 11.5% to ₹355.90 crore.

The company plans to launch 40 new agricultural molecules, scale exports to ₹2,500 crore, and maintain zero debt with cash reserves above ₹2,000 crore.

Current Competitive Landscape:

Key players operating in the India agrochemicals market include Bayer CropScience Limited, Syngenta India Private Limited, UPL, BASF SE, ADAMA, DHANUKA AGRITECH LTD., Sumitomo Chemical India ltd., Indofil Industries Limited, Nufarm, and Crystal Crop Protection Ltd.

The market remains intensely competitive, but Sumitomo's positioning—technical excellence, quality consistency, sustainability leadership, and Japanese backing—differentiates it from pure cost players. Intense competition among agrochemical companies, encompassing both domestic companies such as UPL and Deccan Fine Chemicals and international companies including Bayer Crop Science Ltd. and Rallis India Ltd., drives innovation, robust product development, and enhanced affordability of agrochemicals in the Indian market; this competitive landscape compels companies to constantly strive for technological advancements, research breakthroughs, and introduction of novel formulations that offer improved efficacy, environmental sustainability, and cost-effectiveness.

The sustainability and innovation push of 2020-present represents not a phase but a permanent transformation of agrochemicals. Companies that lead this transition—developing biologicals, investing in digital platforms, achieving manufacturing sustainability, and building farmer trust—will dominate agriculture's next chapter. Sumitomo Chemical India, with its patient capital, technical capabilities, and values-driven approach, has positioned itself at the forefront of this transformation.

X. The Sumitomo Way: Japanese Management Meets Indian Agriculture

What happens when Japanese corporate culture—with its emphasis on consensus, long-term thinking, and meticulous quality—collides with Indian agricultural markets characterized by relationships, flexibility, and rapid improvisation?

The answer, it turns out, is neither purely Japanese nor purely Indian, but something uniquely adapted.

Sumitomo Chemical's founding principle states: "We must not merely seek business profits but must contribute broadly to society through our business activities". This philosophy, articulated in 1913, guides decision-making a century later. It manifests in choices that puzzle analysts trained to maximize quarterly earnings: investing in farmer training programs with multi-year payback periods, maintaining premium quality standards that compress margins, and prioritizing supply reliability over profit optimization during shortages.

Long-Term Orientation:

Sumitomo's approach to India exemplifies patient capital. The company was registered in India on February 15, 2000—twenty-five years ago as of late 2025. The Excel Crop Care acquisition, from initial discussions to merger completion, spanned years. Manufacturing capacity expansions involve multi-year commitments. Product registrations require patient regulatory navigation.

This long-term perspective contrasts with private equity-backed competitors chasing exits or Indian family businesses optimizing for generational wealth transfer. Sumitomo measures success in decades, not quarters. This allows investments in R&D, brand-building, and farmer relationships that shorter-horizon competitors can't justify.

Quality Culture:

Japanese manufacturing discipline—standardized processes, continuous improvement (kaizen), zero-defect mindsets—transplanted to Indian operations creates quality that farmers notice. When a Sumitomo product claims 40% active ingredient, it delivers 40% ±0.5%, not 38-42% like some competitors. When recommended application rates promise specific results, they deliver because formulations account for Indian water quality, temperatures, and application equipment.

This obsessive quality focus frustrates finance teams pushing for cost reduction but builds farmer loyalty. A farmer burned by substandard products remembers. One who consistently gets results becomes a brand advocate worth more than any advertising.

Employee Development:

Mr. Tadashi Katayama, appointed Director with effect from August 31, 2019, holds a Master's degree in Business Administration from Vanderbilt University, U.S.A. and a Master's degree from Kyoto University in Japan; he has been working with Sumitomo, Japan since 1992 in the Health and Crop Science business unit in various positions and has been associated with Sumitomo's Indian businesses and subsidiary in supervisory role.

The leadership approach blends Japanese executives providing global perspective and technical expertise with Indian leaders offering market understanding and relationships. Mr. Chetan Shah was a promoter of New Chemi Industries Limited which was acquired by Sumitomo Chemical Company, Limited, Japan in 2010 and integrated with Sumitomo Chemical India Pvt. Ltd.. Mr. Ninad D. Gupte has worked with Indian as well as multinational companies such as Excel Industries Ltd., BASF India Ltd., and Herdillia Chemicals Ltd. in various senior positions; he has worked as Managing Director of Cheminova India Ltd and Agrocel Industries Ltd and as Joint Managing Director of Excel Crop Care Limited.

This hybrid leadership—Japanese strategic guidance combined with Indian operational expertise—creates organizational capabilities that pure Japanese or pure Indian companies struggle to match.

Balancing Global Standards and Local Realities:

Manufacturing specifications meet global standards. But procurement practices acknowledge Indian supplier realities—monsoon-related delays, festival shutdowns, relationship-based negotiations. Sales processes follow systematic CRM tracking globally. But customer relationships in rural India still involve chai, extended conversations about family, and trust-building that spreadsheets can't capture.

This ability to hold two seemingly contradictory approaches simultaneously—global rigor and local flexibility—defines Sumitomo's operating model in India.

Relationship with Parent Company:

Sumitomo Chemical India operates with significant autonomy for day-to-day decisions but maintains tight integration for technical matters, major capital allocation, and strategic direction. The Indian subsidiary can access its parent's global technology pipeline, quality systems, and regulatory expertise. But it has freedom to adapt products, pricing, and go-to-market strategies to Indian realities.

This balanced autonomy-integration model avoids two common pitfalls: subsidiaries so tightly controlled by headquarters that they can't respond to local conditions, and subsidiaries so independent they fail to leverage parent company advantages.

Capital Allocation Philosophy:

Sumitomo Chemical India Ltd has strong cash reserves of INR 2,089 crore, providing financial flexibility for future growth initiatives. Rather than maximizing dividend extraction, the parent company allows substantial cash retention for reinvestment—capacity expansions, R&D, working capital to support dealer networks, and opportunistic M&A.

This reinvestment philosophy reflects Sumitomo's long-term orientation. The company isn't managed for near-term cash extraction but for building enduring competitive position in one of the world's most important agricultural markets.

The Sumitomo Way in India demonstrates that Japanese management principles—long-term thinking, quality obsession, systematic improvement, stakeholder orientation—can succeed in emerging markets when adapted thoughtfully rather than imposed rigidly. It's not about transplanting Tokyo to Mumbai, but about creating hybrid approaches that combine the best of both cultures.

XI. The Business Model Deep Dive

Strip away the corporate philosophy and sustainability narratives, and a fundamental question remains: How does Sumitomo Chemical India actually make money?

Product Portfolio:

Sumitomo Chemical India Ltd. manufactures, imports and markets products for Crop Protection, Environmental Health, Professional Pest control and Feed Additives for use in India. Sumitomo Chemical India Limited is primarily engaged in manufacturing and sales of speciality and generic products under Agro Solutions Division (ASD), Environmental Health Division (END) and Animal Nutrition Division (AND).

The portfolio spans multiple categories:

Insecticides: The largest segment, addressing cotton bollworms, rice stem borers, vegetable pests, and fruit crop insects. Products range from conventional chemistry (pyrethroids, organophosphates) to newer molecules with better safety profiles.

Fungicides: Targeting diseases in high-value crops—downy mildew in grapes, late blight in potatoes, rust in wheat. These products command premium pricing because disease outbreaks can destroy entire harvests.

Herbicides: Growing fastest due to labor scarcity. Products for rice (pre-emergence and post-emergence), soybeans, cotton, and plantation crops.

Plant Growth Regulators: Specialty products that modify plant development—promoting flowering, improving fruit set, regulating growth. Plant growth regulator is a high margin segment for SCIL which ranges from 8-10% of overall revenue for SCIL vs industry having 5% of overall revenue.

The diversification strategy reduces dependence on any single product. SCIL has a very diverse product portfolio with no single product contributing more than 16% of overall revenue thereby reducing product concentration risk; its key product Glyphosate is in the range of approximately 11-12% of overall revenue, while other top selling molecules include Chlorpyrifos and Tebuconazole which contribute to approximately 12-13%; its Top 10 products contribute less than 45% of Total Revenue.

Manufacturing Footprint:

SCIL has 5 manufacturing plants based across Gujarat & Maharashtra. SCIPL has 2 manufacturing plants, 1 plant in Maharashtra and 1 plant in Gujarat; post-merger Sumitomo Chemical India has 5 manufacturing plants in West India (2 plants of SCIPL plus 3 plants of ECCL); the amalgamated company has presence in both technical & formulation manufacturing.

This vertically integrated structure provides cost advantages and supply security. Rather than depending on Chinese intermediate suppliers, Sumitomo produces active ingredients domestically, then formulates them into end products. During supply disruptions (COVID lockdowns, Chinese environmental crackdowns), this vertical integration proved decisive.

R&D Strategy:

The approach combines multiple sources:

In-house capability: Strong R&D capabilities with 75 engineers and scientists capable of creating new combination process developments and improvement. Focus on process optimization, formulation development, and adapting global products to Indian conditions.

Parent company technology: Product range comprises conventional chemistry sourced from parent company, Sumitomo Chemical Company and biological products sourced from USA based subsidiary, Valent Biosciences LLC. Access to Sumitomo's global pipeline provides differentiated molecules competitors can't easily replicate.

Licensing and partnerships: For specific technology gaps, in-license molecules or form partnerships with biotech companies and research institutions.

This multi-source R&D strategy balances innovation (new molecules from parent) with cost-effectiveness (generic process development in-house) and speed (in-licensing for quick gaps).

Distribution Network:

The company post-merger possesses 13,000+ distributors covering more than 85% of the geography pan-India—with improved depth and breadth of distributors. Around 4 branches and 68 depots across India provide connectivity to major cities and proximity to main highways, ports that reduces logistic time and costs.

The distribution architecture operates hierarchically:

Company warehouses (strategically located near manufacturing facilities and transport hubs) → State distributors (covering major agricultural states) → District distributors (deeper penetration) → Retailers (taluk and village level) → Farmers

At each level, relationships matter. Credit terms, technical support, brand pull from farmers, and supply reliability determine distributor loyalty. Sumitomo invests heavily in distributor education, field demonstrations, and agronomist support to maintain these relationships.

Pricing Power:

In conventional generics (glyphosate, chlorpyrifos), limited pricing power exists—commoditized products compete primarily on price. But Sumitomo maintains slight premiums through quality consistency and technical support.

In differentiated molecules (plant growth regulators, newer fungicides, biologicals), stronger pricing power reflects performance advantages and limited competition.

In branded formulations with established farmer recognition, brand equity provides modest pricing power—farmers willingly pay 5-10% premiums for brands they trust.

Working Capital Management:

Agrochemical business is working capital intensive:

Inventory: Must maintain buffer stocks for peak seasons (Kharif and Rabi) to meet dealer demand. Manufacturing lead times preclude just-in-time production.

Receivables: Dealer credit terms (typically 30-90 days) tie up cash. Some seasonality—dealers stock up before planting, pay after harvest.

Payables: Raw material suppliers provide some credit, partially offsetting receivables.

Cash flow from operations increased in FY24 and stood at Rs 7,572 million compared to Rs 3,894 million in FY23; SCIL's cash flow from operating activities (CFO) during FY24 stood at Rs 8 billion, an improvement of 94.5% on a YoY basis; cash flow from investing activities (CFI) during FY24 stood at Rs -4 billion, an improvement of 28.5% on a YoY basis.

Seasonality:

Indian agriculture operates on two primary seasons:

Kharif (monsoon crops): Sowing June-July, harvesting October-November. Rice, cotton, soybeans dominate. Insecticide and herbicide sales peak.

Rabi (winter crops): Sowing October-November, harvesting March-April. Wheat, chickpeas, mustard dominate. Fungicide sales increase.

This creates pronounced revenue seasonality—Q2 (July-September) and Q4 (January-March) typically see highest sales as farmers apply crop protection products. Q1 and Q3 are relatively slower.

Cash flow patterns amplify seasonality—working capital builds before peak seasons (inventory stocking), then releases after harvest (dealer payments). Managing this cash cycle effectively determines competitive advantage.

Unit Economics:

Gross margins vary by product category:

- Conventional generics: 25-35% gross margins, competed primarily on cost

- Differentiated molecules: 40-55% gross margins, performance-based value

- Biologicals: 45-60% gross margins, premium positioning

Operating expenses include sales/distribution (largest component—field staff, demonstrations, logistics), R&D (3-4% of revenue), and admin.

Operating margins have ranged from 13-19% in recent years, reflecting product mix, competitive intensity, and input cost fluctuations. Operating profit margins witnessed a fall and stood at 16.7% in FY24 as against 18.8% in FY23.

Profitability Drivers:

Several factors determine profitability:

Product mix: Shift toward higher-margin differentiated molecules and biologicals versus generic commodities

Manufacturing efficiency: Capacity utilization, yield improvements, and cost reduction in synthesis

Raw material costs: Fluctuations in petrochemical feedstocks and intermediates impact gross margins

Pricing environment: Competitive intensity and farmer willingness to pay

Scale: Fixed cost leverage as revenue grows

The business model ultimately hinges on technical excellence (developing effective products), operational efficiency (manufacturing costs), distribution strength (market access), and brand equity (farmer trust). Companies excelling across all four dimensions generate superior returns. Those weak in any area face margin pressure.

XII. Playbook: Business & Investing Lessons

What can investors and operators learn from Sumitomo Chemical India's quarter-century journey?

Playing the Long Game:

Sumitomo's India strategy demonstrates patient capital's power. Twenty-five years from initial entry to current leadership position. Five years from Excel acquisition announcement to merger completion. Multi-year manufacturing capacity expansions. Decade-long investments in farmer relationships.

This patience contrasts with typical private equity holding periods (3-5 years) or activist investor demands for rapid restructuring. But in complex emerging markets with relationship-driven sales and regulatory uncertainties, patience often delivers superior long-term returns than short-term optimization.

Lesson: In markets requiring trust, regulatory navigation, and technical capabilities, patient capital beats quarterly optimization. Investors should assess management's genuine time horizon—stated long-term focus means little if compensation structures incentivize short-term earnings manipulation.

Technical Excellence as Moat:

Sumitomo's differentiation rests fundamentally on technical capabilities: process chemistry that reduces costs, formulation expertise that improves efficacy, quality systems delivering consistency, and regulatory sophistication enabling approvals. These capabilities, accumulated over decades, can't be quickly replicated.

In industries where technical performance matters—pharmaceuticals, specialty chemicals, aerospace—technical excellence creates durable competitive advantages. Investors should assess whether a company's technical capabilities are genuine (publications, patents, customer testimonials) or merely marketing claims.

Lesson: Technical moats—deep expertise, intellectual property, accumulated know-how—provide more durable competitive advantages than purely financial engineering or distribution reach, both of which competitors can eventually replicate.

Navigating Regulatory Complexity:

Since it started regulating pesticides under the Insecticides Act of 1968, India has registered around 260 pesticide molecules for sale and manufacture in the country; they are governed by a dizzying maze of rules and regulations that is impenetrable to most outsiders but still fails to adequately safeguard human or environmental health.

Sumitomo mastered India's regulatory labyrinth—understanding approval processes, maintaining government relationships, generating required data, and adapting quickly to policy changes. This regulatory competence became competitive advantage when bans disrupted competitors lacking alternatives.

Lesson: In heavily regulated industries (healthcare, chemicals, finance), regulatory competence is a core competency, not just a compliance function. Companies viewing regulation purely as constraint rather than strategic factor will underperform.

Importance of Trust in Rural Markets:

Agrochemicals sales ultimately depend on farmer trust. Will this product work? Can I trust the dosage recommendations? Will the company stand behind problems? These questions matter more than cost-per-acre calculations.

Sumitomo's obsessive quality focus, extensive agronomist support, and long-term relationship approach built trust that competitors couldn't quickly replicate. Farmers who experienced consistent results became brand advocates, creating powerful word-of-mouth effects in village networks.

Lesson: In markets where information asymmetries exist and word-of-mouth drives adoption (B2B services, healthcare, education), trust-building creates competitive moats. Companies should rigorously measure customer satisfaction and retention, not just acquisition costs.

Global-Local Balance:

Sumitomo succeeded by neither imposing purely Japanese approaches nor fully localizing into an Indian company. The hybrid approach—global technical standards, local market adaptation—delivered advantages neither pure global nor pure local players achieved.

Japanese quality systems and technology pipeline combined with Indian market knowledge and relationship skills created unique capabilities. The company could offer products locals developed alongside molecules locals couldn't access, delivered with quality consistency locals struggled to match.

Lesson: For multinationals in emerging markets, the highest returns accrue to companies mastering global-local balance. Pure localization surrenders advantages of global scale and technology. Pure standardization ignores local market realities. The sweet spot involves thoughtful adaptation.

Sustainability as Strategy:

Sumitomo's sustainability focus preceded investor ESG pressure by decades. The founding principle—"We must not merely seek business profits but must contribute broadly to society through our business activities"—guided decisions long before sustainability became fashionable.

This authentic values-driven approach positioned the company advantageously as regulatory shifts and consumer preferences increasingly favor sustainable practices. Biologicals, digital agriculture, and reduced-environmental-impact products align with Sumitomo's historical philosophy, making the sustainability transition easier than for competitors lacking this cultural foundation.

Lesson: Companies whose sustainability commitments reflect authentic values and long-term strategy, not just marketing, will outperform as regulatory and market forces favor sustainable practices. Investors should distinguish genuine sustainability leadership from greenwashing.

Managing Commodity Cycles:

Agricultural markets oscillate between boom (high commodity prices drive farmer income and agrochemical spending) and bust (low prices constrain spending). Weather patterns create volatility. Input cost inflation compresses margins.

Sumitomo navigated these cycles through portfolio diversification (reducing dependence on specific crops or geographies), balance sheet strength (avoiding distressed asset sales during downturns), and long-term relationships (maintaining dealer/farmer loyalty across cycles).

Lesson: In cyclical industries (commodities, housing, autos), balance sheet strength and diversification matter more than peak-cycle profitability. Companies surviving downturns often emerge with strengthened competitive position as weaker players exit.

The Sumitomo Chemical India story ultimately teaches that boring businesses—making chemicals that kill bugs and weeds—can generate extraordinary returns when executed with technical excellence, patient capital, regulatory sophistication, and authentic stakeholder orientation. Flashy business models and hockey-stick projections attract attention. But deep competence, methodical execution, and long-term thinking compound into formidable competitive positions.

XIII. Analysis & Bear vs. Bull Case

Bull Case:

The optimistic view on Sumitomo Chemical India rests on several pillars:

India's Agricultural Modernization is Early Innings: The global India agrochemicals market is expected to grow at a compound annual growth rate of 6.5% from 2024 to 2030 to reach USD 51.29 billion by 2030. The Agrochemical Industry In India is expected to reach USD 9 billion in 2025 and grow at a CAGR of 7.10% to reach USD 12.70 billion by 2030.

Despite decades of growth, Indian agriculture remains underpenetrated in crop protection compared to developed markets. Application rates (kilograms per hectare) lag Brazil, USA, and China. As farmer education improves, credit access expands, and value realization increases, agrochemical intensity should continue rising. Demographics support this—India's growing population demands higher agricultural productivity from essentially static arable land.

Strong Technical Capabilities and Parent Backing: SCC, a century old corporation and global giant in agrochem space, is for the first time setting up a manufacturing site outside Japan and chose India; SCIL is the only technical and generic grade manufacturing site for SCC outside Japan.

Access to Sumitomo's global technology pipeline provides competitive advantages in launching differentiated molecules. SCC holds 12,600+ patents of which approximately 34% are in the Health & Crop Science segment. As older molecules face resistance and regulatory restrictions, companies with robust innovation pipelines will gain share.

Export Growth Potential: Sumitomo Chemical India exports approximately 20% of its total production to various international markets, including the USA, Europe, and other Asian countries. The reduction in capacity in China will be beneficial for India; Glyphosate, regarded as the most used pesticide in the world with a market size of approximately US$5.6bn, will create additional export opportunities; high exports (90% production is exported) from China provide evidence of high demand for Glyphosate in the global market.

India's emergence as a global agrochemical manufacturing hub—driven by China+1 strategies, India's cost competitiveness, and improving quality reputation—creates export tailwinds. Sumitomo's quality standards position it to capture premium segments of this opportunity.

New Product Categories Offer Upside: The Biologicals segment of crop protection is continuously growing in Sumitomo Chemical India Limited (SCIL). The biostimulants market is estimated at USD 4.46 billion in 2025 and projected to reach USD 7.84 billion by 2030, at a CAGR of 11.9%.

Biologicals, biostimulants, and digital agriculture services represent growth vectors beyond traditional chemistry. Early movers in these categories can establish positions before competition intensifies. Sumitomo's investments in biologicals and digital platforms position it advantageously.

ESG Tailwinds Favor Quality Players: As regulatory standards tighten and customers demand sustainable products, quality-focused companies with genuine ESG commitments gain advantages. Sumitomo's authentic sustainability orientation, Japanese quality culture, and technical capabilities to develop safer molecules position it to benefit from these trends.

Bear Case:

The skeptical perspective highlights several concerns:

Intense Competition and Commoditization: The agrochemical industry faces brutal competition. Intense competition among agrochemical companies, encompassing both domestic companies such as UPL and Deccan Fine Chemicals and international companies including Bayer Crop Science Ltd. and Rallis India Ltd., drives innovation, robust product development, and enhanced affordability.

Generic molecules face commodity-like dynamics with intense price competition. Indian manufacturers replicate off-patent products, driving prices toward marginal costs. Chinese competition, despite recent disruptions, remains formidable on cost. Sustaining pricing power requires constant innovation—expensive and uncertain.

Regulatory Uncertainty: The Government of India proposed further restrictions on the usage of 27 pesticides which are already banned in other countries on May 14, 2020; this decision follows recommendations from an expert committee that reviewed safety, environmental impact, and international regulatory status; the proposal seeks to ban import, manufacture, sale, transport, and use of these pesticides in agriculture, citing risks such as carcinogenicity, endocrine disruption, and toxicity to aquatic organisms and pollinators.

Future bans could eliminate significant revenue. Regulatory risk in domestic markets for glyphosate remains, and glyphosate represents 11-12% of revenue. The regulatory process remains opaque and subject to political pressures, creating unpredictable risks.

Climate Volatility Affecting Farmer Spending: The second quarter was challenging due to excessive rainfall, leading to a decline in revenue from INR 988 crore to INR 930 crore compared to the previous year; export demand was muted in certain geographies, particularly in Africa and Latin America, affecting overall export revenue growth.

Erratic weather patterns disrupt agricultural cycles, affecting application timing and farmer cash flows. Drought years reduce spending. Excessive rainfall delays applications. Climate change introduces unprecedented uncertainties into agricultural planning.

Chinese Competition on Cost: Despite recent disruptions, Chinese manufacturers remain cost leaders in agrochemical production. As environmental compliance improves and supply chains stabilize post-COVID, Chinese competition could intensify. India's manufacturing cost advantages versus China have narrowed as labor and energy costs rise.

Parent Company Strategic Shifts: Sumitomo Chemical globally faces challenges in some business segments. Strategic shifts at the parent company—portfolio rationalization, capital allocation to other geographies—could affect India support. While currently well-backed, subsidiary priorities can change with parent company leadership transitions.

Limited Pricing Power in Many Segments: The company's profitability was impacted by higher input costs and elevated operating expenses, particularly in its subsidiary, Bars Barrick Gro Sciences. In generics and commoditized products comprising significant revenue, passing through input cost inflation remains difficult. Margin compression risks persist if raw material prices surge while product prices face competitive constraints.

Competitive Analysis: