Sula Vineyards: The Story of India's Wine Pioneer

I. Introduction & Episode Roadmap

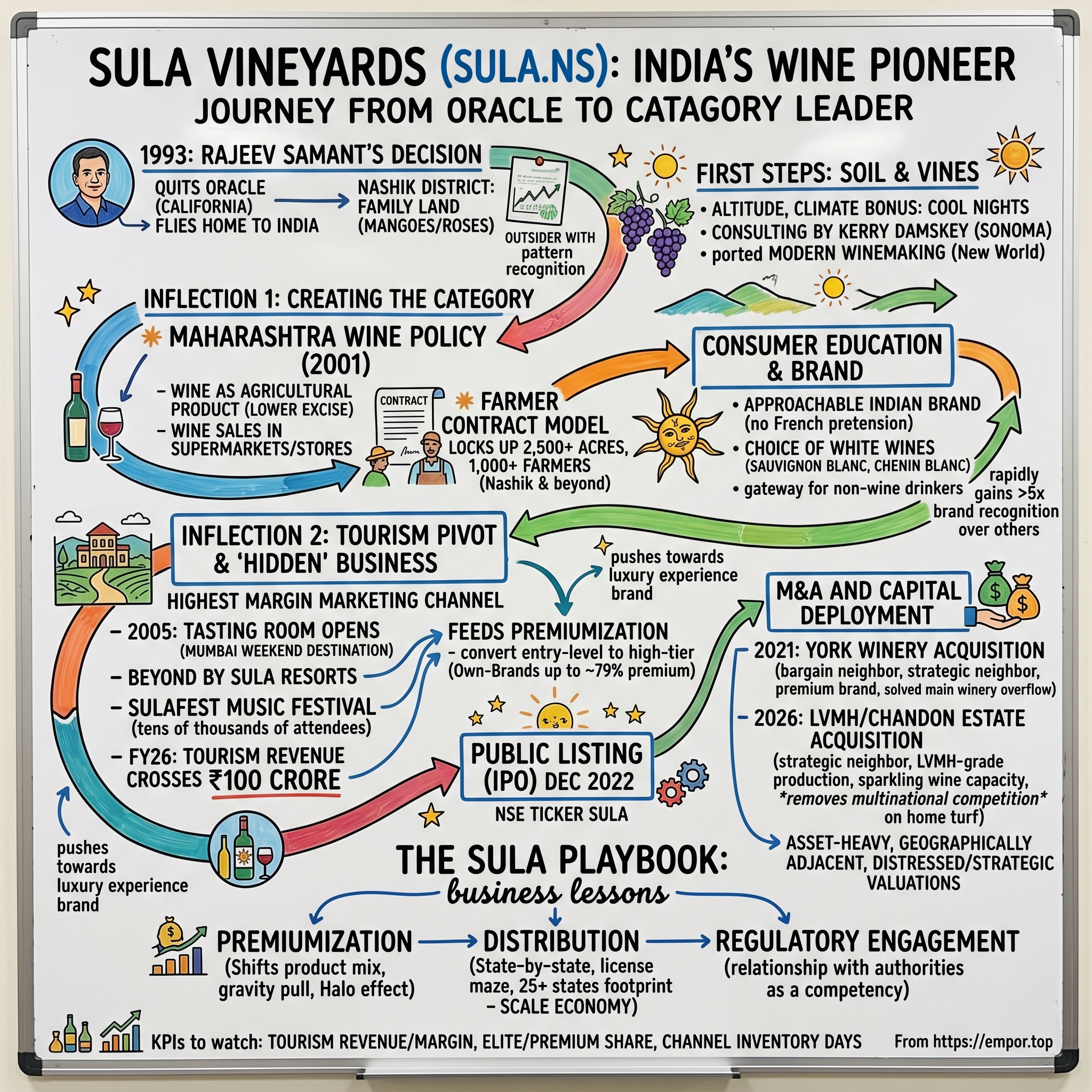

Picture this scene. It is the late 1990s, and a 32-year-old Stanford graduate is standing on a hillside in Nashik district नाशिक, roughly 180 kilometers northeast of Mumbai. The land beneath his feet had been a mango and rose orchard, a quiet patch of family terrain that his father had bought decades earlier. The young man, Rajeev Samant राजीव सामंत, had just walked away from a comfortable, salary-and-stock-options life at Oracle in Redwood Shores, California. His parents, by his own retelling, thought he had lost his mind. Friends in Mumbai sniggered. The premise sounded absurd on its face: take a tropical, monsoon-soaked stretch of the Deccan plateau, plant grapes, and try to convince a country of 1.3 billion whiskey drinkers that wine was for them too.4

That decision became Sula Vineyards सुला विनेयार्ड्स, India's first true scaled wine business and, two-and-a-half decades later, a publicly listed company that commands roughly 60% of the Indian wine market and trades on the National Stock Exchange under the ticker SULA.1

The "aha" of Sula is not really about wine. Wine is the surface story. The deeper story is about how an outsider, armed with Silicon Valley pattern recognition, walked into a category that did not exist in his home country and constructed every layer of it himself. He had to plant the vines, train the farmers, write the playbook for state policy, build the tasting rooms, invent the festival, teach the urban Indian middle class how to swirl a glass, and then, once all of that was in place, build a distribution machine that could carry the bottles into 25-plus states under a patchwork of excise rules that change every fiscal year.

That kind of category creation is rare. It is rarer still when the founder is also patient enough to spend two-plus decades on it. And it is rarest of all when, after creating the category, the company manages to defend a 60%-ish share against deep-pocketed multinationals like LVMH, who themselves entered India with the Chandon brand and, in 2026, walked out and handed the keys to Sula.[^4]

Here is the roadmap for this episode. We will start in 1993, when Rajeev quits Oracle and flies home. We will trace the first bottle of Sauvignon Blanc in 1999, the Maharashtra Wine Policy of 2001 that effectively codified the rules of the road, the launch of the Sula tasting room in 2005 and Beyond by Sula shortly after, the bolt-on of York Winery in 2021, the IPO in December 2022, the explosion of wine tourism past the ₹100 crore mark in FY26, and finally the LVMH/Chandon estate acquisition announced in March 2026.[^4][^5] Along the way we will dissect the 7 Powers, war-game the bear case, and ask the only question that really matters for a long-term investor: is Sula a luxury conglomerate in the making, or just a really well-run agricultural commodity business in a fancy bottle?

Pour yourself something nice. This is going to take a while.

II. Roots: From Oracle to the Orchard

There is a scene that Rajeev Samant likes to tell. It is 1993. He is in Redwood Shores at Oracle, walking out of a glass-walled conference room, and he realizes that the next 30 years of his life are visible from where he is standing — promotions, options vesting, more conference rooms. He does the unthinkable for a first-generation Indian-American immigrant working in Larry Ellison's empire. He resigns. He flies back to India. His father, a former MD at a Tata company, was not thrilled. His mother was not thrilled either.4

Rajeev had grown up partly in Mumbai and partly on family land near a small town in Nashik district. The family had about 30 acres of dusty, rocky upland. His father had bought it decades earlier with no plan in particular. Mangoes, roses, the usual things you do with such land. Rajeev took it over with vague ambitions of becoming an agro-entrepreneur. He tried teak. He tried table grapes. Nothing quite worked. The breakthrough came almost by accident: a visiting Californian viticulturist looked at the soil, the elevation (roughly 600 meters), the daytime temperatures, and the rare-for-India bonus of cool nights, and told him this land could grow wine grapes.4

This is the part of the story that gets glossed over. India does have a sliver of altitude-and-latitude geography where Vitis vinifera, the European wine grape, can survive. Most of the country cannot grow it. Maharashtra's Nashik-Sangli belt and pockets of Karnataka's Nandi Hills are essentially the only viable zones at scale. So before Rajeev even planted a vine, geography had already narrowed the field to a few hundred square kilometers — and his family happened to own land in the middle of one of them. That is the closest thing to a cornered resource you can have at the outset of a business: you cannot reproduce Nashik in Lucknow.

But knowing the dirt can grow grapes is not the same as knowing how to make wine. Enter Kerry Damskey, a then-mid-career Sonoma-based winemaking consultant who had spent his career in California. Rajeev reached out, talked him into a consulting trip, and Damskey came over to look at the site. Damskey would end up consulting for Sula for over two decades, essentially porting California "New World" winemaking methodology — stainless-steel fermentation, temperature control, varietal-focused labeling — into the Indian context.4 This transfer of knowledge mattered for a non-obvious reason: India had no wine-making tradition of its own. There were no apprenticeships. There were no schools. The few existing producers, like Indage, were chasing French traditional methods with mixed results. Sula leapfrogged into a more modern, sun-belt style that suited the climate and, conveniently, suited the palate of Indians who had never tasted wine before.

The first commercial Sula vintage was bottled in 1999 — a Sauvignon Blanc and a Chenin Blanc.4 White wines, not reds. That choice itself was strategic. White wines drink well chilled in a tropical climate. They pair more obviously with Indian food than tannic reds. And they are forgiving for a first-time wine drinker, because they avoid the bitter-astringent shock that reds give to a beer-and-whiskey palate.

So before we even get to inflection point one, notice what Rajeev had already done. He had picked a defensible piece of geography. He had imported world-class winemaking expertise. He had chosen the right starting product for the market he wanted to build. And he had done all of this in a country where, in some states, you still needed a permit to buy alcohol at all. The runway was set. The plane just had not taken off yet.

III. Inflection Point 1: Creating the "Wine Capital of India"

In 1999, the year the first Sula bottle hit a shelf in Mumbai, the per-capita wine consumption in India was, charitably, a rounding error. Industry estimates put it at well under 10 milliliters per adult per year, compared to a global average measured in liters.[^11] This is the part of category creation that nobody glamorizes. You are not stealing share from a competitor; you are converting non-consumers. Every bottle Sula sold was, in effect, an evangelism event.

The early years were brutal. Rajeev would personally drive cases of Sula to Mumbai restaurants and beg sommelier-less restaurant managers to put it on the menu. Hotels were skeptical. Distributors were uninterested. The Indian Made Foreign Liquor (IMFL) machine — which routes the country's spirits, mostly whiskey, through state corporations and aggressive distributor networks — had no template for a small, premium domestic wine producer. Wine occupied a regulatory no-man's-land. Was it food? Was it liquor? Each state had a different answer, and each answer carried different excise consequences.

Here is where the second masterstroke happened. Rajeev did not just lobby for himself. He lobbied for the entire category. Together with a small group of producers, he worked with the Maharashtra state government to craft what became the Maharashtra Grape Wine Industry Policy of 2001. The policy did three things that mattered enormously. It classified wine as an agricultural product, which meant lower excise compared to spirits. It opened the door to wine sales in supermarkets and walk-in stores under specific licensing, which was extended further in 2022.[^10] And it provided incentives for farmers to convert from table grapes to wine grapes.[^11]

This was Sula's first textbook display of what Hamilton Helmer would call a Cornered Resource play. Rather than buy or lease more land, Rajeev pioneered the farmer contract model. Sula would provide vines, technical advisory, and a guaranteed off-take at a contracted price. Local farmers would convert table-grape acreage to wine-grape acreage. By the late 2010s, Sula had locked up roughly 2,500 acres of contracted vineyards across a network of more than 1,000 farmers.2[^11] A competitor could not just walk into Nashik and replicate this. The farmers were not for sale; the contracts were not for sale; the trust, built over a decade of paying on time, was definitely not for sale.

In parallel, Sula was educating the consumer. Sauvignon Blanc and Chenin Blanc — easy-drinking, fruit-forward whites — were positioned as the gateway. The Sula label, with its now-iconic stylized sun motif, was deliberately approachable. No French chateau pretension. No Latin tasting notes. Just a clean, modern, very Indian-feeling brand that suggested "yes, this is for you, not for some sommelier in Paris."

By the mid-2000s, this was working. Wine consumption in India was growing at double-digit annual rates from a near-zero base, and Sula was capturing a wildly disproportionate share. The competition was thin. Indage was a more traditional producer that would later spectacularly implode. Grover Vineyards was building from Bangalore. Fratelli would not arrive until 2007. The market structure was effectively "Sula and the others," and Sula's brand recognition by the end of the decade was on the order of 5x to 10x the next-best player.[^11]

What this period taught the company — and what we will see echo through every subsequent inflection — is that in a market this nascent, category creation and market share capture are the same activity. You do not have the luxury of choosing one or the other. Sula needed to make the Indian wine market exist in order to dominate it. By 2005, that mission was essentially done. Nashik was on its way to being branded the "Wine Capital of India," a phrase that, when you say it now, sounds obvious — and that nobody would have said in 1999.

The next question, naturally, was what to do with all that brand equity. The answer turned out to be: invite everybody over for dinner.

IV. Inflection Point 2: The Tourism Pivot & "Hidden" Business

In 2005, Sula opened a tasting room.

That sentence sounds banal. Plenty of wineries have tasting rooms. But in the Indian context in 2005, a tasting room was a genuinely radical concept. Nashik was not on any tourist circuit. The road from Mumbai was rough. The idea that an urban couple would drive four hours up the Western Ghats to taste wine and stay overnight at a winery would have sounded, to a 2005 hospitality consultant, like a guaranteed business plan disaster.

It worked spectacularly. The Sula tasting room became, almost overnight, a weekend destination for Mumbai's growing professional class.[^11] Within a few years, Sula added accommodation under the Beyond by Sula brand, then a second resort tier, then an outdoor amphitheater, and then the annual SulaFest music festival, which by the late 2010s was drawing tens of thousands of attendees and an entire ecosystem of food trucks, sponsors, and influencers.2

To understand why this is structurally important — and not just a nice side hustle — you need to think about what tourism actually does for a wine business. Tourism is the highest-margin marketing channel in the wine industry, anywhere in the world. It is also a customer acquisition tool that produces the most loyal possible customers, because someone who has stood in your barrel cellar, tasted your wine with food on a hilltop, and slept in your villa will buy your label for the rest of their life. Robert Mondavi figured this out in Napa in the 1970s. The Antinori family figured it out in Tuscany. Rajeev figured it out for India.

The financial implications matured slowly, then suddenly. In FY26, Sula's Wine Tourism business crossed the ₹100 crore revenue mark for the first time.[^5] To put that in scale, when Sula went public in December 2022, this segment was running well under half that size. Crossing ₹100 crore matters not just because of the absolute number, but because of the margin profile. Hospitality at Sula's scale carries EBITDA margins that have historically run in the 30%-plus range for the segment — meaningfully above the blended company margin — because once the resort assets are paid down, every additional room-night and tasting fee converts at extremely high incremental contribution.2[^5]

There is a second-order benefit that the numbers do not capture cleanly. The tourism business feeds premiumization. A tourist who walks into the cellar and tastes the entry-level Sula Sauvignon Blanc alongside the higher-tier Rasa Shiraz and the top-shelf The Source will, more often than not, walk out converted to the higher labels. The premium portfolio — labels that retail in the ₹1,000-and-above range — has grown from a single-digit percentage of revenue a decade ago to roughly 79% of Own-Brands sales in recent reporting.2[^13] That kind of mix shift, sustained over years, is the single most important driver of Sula's gross margin trajectory.

Strategically, the tourism pivot is what separates Sula from being a pure agricultural-commodity business and pushes it toward something closer to a luxury experience brand. Compare this to how, say, LVMH thinks about Moët or Veuve Clicquot. The bottle is one revenue line. The brand experience — the chateaux, the boutiques, the partnerships — is what underwrites the price premium. Sula is, on a tiny scale, walking the same path.

It also explains why management keeps reinvesting in Nashik real estate. Adding capacity in the same district is not just about more wine; it is about more tourism nodes. The eventual rollout into Dindori डिंडोरी and the broader Nashik corridor turns the entire valley into a Napa-style cluster where Sula is the dominant gateway operator.

By 2020 the playbook was visible. Wine + tourism + brand + farmer network = a vertically integrated luxury asset in a country that had only just discovered it wanted one. The next question was: with everything organic firing, would Sula start to deploy capital inorganically? In 2021, it did.

V. M&A and Capital Deployment: The York and Chandon Plays

For a company that has spent most of its life building from scratch, Sula has been remarkably disciplined about acquisitions. Two transactions tell you essentially everything about its M&A philosophy: York Winery in 2021 and the Chandon India estate in 2026.

The York deal is the kind of acquisition that, on a transcript, sounds boring and, on a balance sheet, is fantastic. York Winery was a Nashik neighbor — literally just down the road from Sula. It had been founded in 2008 by the Gurnani family, had built up a respectable premium portfolio with brands like Arros, and had carved out a niche as a higher-end alternative to Sula in the same district. By 2020, however, York was financially stretched. Capacity utilization was poor. The COVID-19 hospitality shock did not help.[^7]

Sula stepped in and acquired the business in 2021 for approximately ₹17 crore, a price that worked out to roughly 1x trailing sales for an asset that included a winery with around 400,000 liters of annual production capacity, a tasting room, brand IP, and inventory.[^7] Let us put that valuation in context. If you were valuing a standalone, distressed boutique winery in any developed market — Napa, Tuscany, the Barossa Valley — you would not be able to buy 400,000 liters of installed capacity plus a working tasting room plus an established brand for anywhere near 1x sales. The replacement cost alone would dwarf that number. Sula was paying bargain prices for a strategic neighbor, and the reason it could do so was that York's other potential acquirers — international wine groups, large Indian liquor companies — either did not understand the asset or did not want to deal with the regulatory complexity of Indian alcohol.

This is what makes Sula's M&A so interesting from an investor's perspective. The pool of potential bidders in their adjacent geography is essentially zero. They are the only natural consolidator. Every adjacent winery in Nashik that gets into trouble — and several have, over the years — is essentially a put option on Sula's M&A desk. That structural position is rarer than people realize.

Operationally, York solved a very specific problem. By the late 2010s, the Sula main winery was running near capacity during the tourism peak season, and Sula was effectively turning away tasting-room visitors. York was just up the road. It gave Sula a second tourism node, a second production line that could be flexed for overflow batches, and — crucially — a separate premium brand that could be positioned without cannibalizing the core Sula label. Three problems solved with one ₹17 crore check.

Fast forward to 2026. The second big move was an even more interesting transaction. In March 2026, Sula announced it would acquire the Chandon India production facility from Moët Hennessy, the LVMH subsidiary that had operated the Indian arm of the famed Chandon sparkling wine brand for over a decade. The transaction was valued at approximately ₹20 crore for the production assets.[^4]8

The strategic backstory matters. LVMH had entered India in the early 2010s with a strategy of producing Chandon sparkling wine locally at a facility in Nashik, betting on Indian wedding-and-celebration demand. The Indian operation never quite scaled to LVMH's global return thresholds. By the mid-2020s, the global parent decided to exit local production and serve the Indian market via imports of its global Chandon brand instead.8 That left the Indian production facility — modern, well-equipped, in the heart of Nashik — looking for a home.

Sula was, again, the only natural buyer. ₹20 crore for an LVMH-grade production facility, in the same district as Sula's existing assets, with built-in capability for méthode traditionnelle sparkling wine, is the kind of price-to-replacement-cost ratio that makes a CFO blush. It strengthens Sula's sparkling wine credibility, adds capacity precisely where the company already operates, and removes the only multinational producer on its home turf.

What both deals tell you about capital allocation is that Sula prefers asset-heavy, geographically adjacent, brand-accretive acquisitions at distressed or strategic-exit valuations, rather than the more glamorous alternative of buying its way into spirits or expanding into another state. Management has been explicit that they will not chase whiskey or vodka acquisitions. They have one job: dominate Indian wine. Every capital-allocation decision they make is consistent with that.

This kind of focus rolls downhill from the people at the top, which is the natural pivot to talking about the management bench.

VI. Management & Skin in the Game

Founder-CEO companies are different animals. A founder who has run a business for 25 years, through near-failure and category creation and a public listing, has internalized the institutional memory of the company in a way that no external hire ever does. The question every long-term investor asks of such a company is: what happens when the founder steps back? And the related question: is the founder still showing up?

For Sula, the answer to both is currently encouraging.

Rajeev Samant remained as Managing Director and CEO through 2026, and the board re-appointed him for another term, signaling continuity at the top.57 More importantly, he has been buying shares in the open market. In late 2025 and into early 2026, Rajeev disclosed purchases of company stock worth approximately ₹3 crore — small relative to his existing promoter stake but a meaningful insider-buying signal at a time when the share price had cooled from its post-IPO highs.7 Insider buys are noisier signals than insider sells in most markets, but a founder topping up his own position after a 25-year career is the closest thing to "I'm still in" you can get without a press release.

Underneath Rajeev, the post-IPO era has brought a structural upgrade in management depth. Two appointments stand out.

Abhishek Kapoor joined as CFO from an FMCG background, bringing the kind of disciplined finance function that public-market investors expect — clean reporting, segment-level disclosure, working capital management.7 The shift from a founder-and-spreadsheet finance setup to a professionalized FMCG-grade CFO function is one of the under-appreciated value-creation events of the post-IPO transition. It is not glamorous, but it is exactly what the next decade of Sula's scaling will require, especially as multi-state excise compliance and trade-receivable management get more complex.

Gorakh Gaikwad is the COO and Chief Winemaker. He is the inside man — a 15-year-plus Sula veteran who rose through the operations ladder, deeply embedded with the farmer network and with the production process.7 His presence is significant for two reasons. First, it means the production know-how is institutionalized inside Sula, not lodged solely with an external consultant or with the founder. Second, it sends a powerful internal signal that long-tenured operators can ascend to the top of the house, which matters for retaining the next layer of operational talent.

On the incentive structure, Sula rolled out an ESOP plan around 2021 ahead of the IPO and refreshed it in 2023, broadening the pool of employees with equity-linked compensation. This is standard for a listed Indian consumer-discretionary company, but it is worth flagging because of the founder-led-to-professional-team transition: aligning the next layer of leadership with the equity outcome matters far more after an IPO than before, when the founder's word and a verbal promise could carry the team.2

On the ownership side, Sula is interesting because of the presence of Verlinvest, the Belgian Frère/De Spoelberch family-office-style investment firm that has been an institutional anchor since well before the IPO.[^11] Verlinvest's pedigree — early backers of brands like Vita Coco and significant positions in the global consumer space — gives Sula a non-trivial signaling and governance benefit. They tend to be patient capital and they tend to know consumer brand-building. Their continued presence on the cap table, alongside the founder, is one of the under-discussed quality markers of the equity story.

A note on promoter holding: it has come down meaningfully post-IPO, in line with regulatory minimum public-shareholding norms and Verlinvest's pre-IPO sell-down structure.2 That mechanical reduction is not the same as the founder losing interest — but it is worth tracking, because at some point the question of long-run founder economics versus operational stewardship will get sharper.

When you put it all together, the management story right now reads as: founder still engaged and putting personal capital in, financial function professionalized, operations institutionalized, ownership backed by patient long-term consumer-focused capital. There are weaker founder stories trading at much richer multiples in India. Whether that, by itself, is enough to justify a position is a different question, and we will get to it.

What this management bench is now executing is what we should turn to next: the playbook itself.

VII. The Playbook: Business and Investing Lessons

If you sat down with Sula management and asked them to describe their strategy in three words, they would probably say premiumization, distribution, and policy. These are the three load-bearing pillars of the current playbook, and each of them deserves a careful look.

Premiumization is, in many ways, the headline story of the last five years at Sula. The company splits its own-brand wine portfolio into categories: Elite, Premium, Economy, and Popular. Elite and Premium together — the ₹700-and-above price points — have grown from a minority of Own-Brands revenue a decade ago to roughly 79% in recent reporting.2[^13] That kind of mix shift is what separates a margin-stagnant alcohol business from a margin-expanding one.

The mechanics of premiumization are subtle. It is not just about launching more expensive bottles. It is about (a) shifting the internal customer up the ladder through the tasting room experience, (b) refusing to chase volume in price-driven entry-level segments where competition from cheap imported wines is increasing, and (c) using the brand halo of the top-shelf labels — Dindori Reserve, Rasa, The Source — to lift the perception of the entire portfolio. Once a brand is established as the "premium choice" in a category, the gravitational pull works in your favor across price points.

There is a useful analogy here. Think about how Apple manages its product mix. The iPhone Pro Max exists not because the marginal buyer needs the Pro Max but because its existence makes the standard iPhone look like a value-tier deal. Sula does a softer version of this with its Elite tier. Most of the volume is in the next tier down, but the existence of the Elite line legitimizes the rest.

Distribution is the second pillar, and arguably the more durable moat. India's alcohol distribution is a state-by-state, license-by-license, distributor-by-distributor maze. To list a wine in Maharashtra requires a different regulatory dance than to list the same wine in Delhi, Karnataka, or Telangana. Each state has its own excise structure, its own corporation, its own quirks of route-to-market.[^11] A small wine producer simply cannot make this work; the fixed costs of multi-state compliance and distributor management eat them alive. Sula, with its scale and twenty-plus years of relationships, has built a presence in 25-plus states, which is roughly 8x to 9x the multi-state footprint of its nearest dedicated wine competitor.[^11][^13]

This is a textbook scale economy moat. The cost of running the distribution apparatus is largely fixed; the revenue spread across more states is variable. Each additional bottle, in essence, makes the apparatus more profitable, and each new state opens a market that competitors will need to spend years to crack.

The third pillar is regulatory engagement. Sula learned early — back in the 2001 Maharashtra policy era — that in an alcohol business, your relationship with state excise authorities is not a cost center; it is a competency. The "Wine is Food" classification battle, the in-store sales rules, the export incentives, the agricultural classifications: each is a regulatory micro-battle that compounds.[^10][^11] Sula has institutional muscle here that newer competitors cannot replicate by spending money.

There is, of course, a flip side to that regulatory exposure. When a state surprises the industry — as Karnataka did in 2025-2026 with an excise restructuring that briefly disrupted Sula's Karnataka sales and forced inventory destocking through the channel — the impact on quarterly numbers can be ugly.6 That destocking episode, which weighed on a couple of quarters of margins, was a useful reminder that no amount of regulatory expertise can fully insulate a state-by-state alcohol business from policy whiplash. The right way to think about this is the way one thinks about reinsurance underwriting: most years it is a tailwind; occasionally it is a shock; the long-run expected value remains attractive if management is paying attention.

What unites all three pillars is the flywheel between them. The premium mix improves gross margins, which funds distribution investment, which expands the addressable market, which justifies regulatory engagement, which protects the channel, which protects the premium mix. Each turn of the wheel reinforces the next.

Now that we have laid out the offensive playbook, it is time to defend it analytically, which brings us to the framework section.

VIII. Analysis: 7 Powers and Porter's 5 Forces

Frameworks are dangerous things. Used well, they sharpen judgment. Used badly, they turn into checklists that paper over weaknesses. Let us use both Hamilton Helmer's 7 Powers and Michael Porter's 5 Forces on Sula with deliberate care.

Starting with 7 Powers.

Cornered Resource — strong. The combination of (i) suitable terroir clustered in a narrow Nashik-Sangli geography, (ii) two-plus decades of contracted relationships with 1,000-plus farmers, and (iii) trained local viticulture talent forms a resource bundle that a new entrant cannot reproduce by writing a check. You can build a winery anywhere in India. You cannot build Nashik anywhere in India.2[^11]

Branding — strong, possibly Sula's single most valuable asset. The Sula brand has, for the urban Indian consumer, achieved the kind of category-defining status that is rare even in mature consumer categories. In the same way that "Xerox" became synonymous with photocopying or "Maggi" with instant noodles in India, "Sula" is the default mental shortcut for wine. That is brand equity money cannot easily buy.[^11]

Scale Economies — meaningful but not unlimited. Sula's scale advantage is real in distribution (25-plus states), in production (multi-site Nashik operations), and in marketing (one festival, one brand, national reach). It is less of a moat in raw input procurement, because grapes are still grapes, and competitors with smaller scale do not face dramatically worse input economics.[^13]

Network Economies — weak. Wine is not a network-effects business. A bottle does not become more valuable to you because more people are drinking it (though one could argue the festival ecosystem has mild network effects on the tourism side).

Switching Costs — modest. Consumers can switch wine brands trivially. Restaurants and retailers do have some switching friction because of established route-to-market relationships, but this is not Salesforce-grade lock-in.

Counter-Positioning — interesting and underrated. Foreign wine importers, including the Chandon India effort, found that they could not match Sula on a combination of price, distribution, and local-knowledge fronts. The LVMH exit in 2026 was, in part, an admission that the counter-positioned local incumbent was too well dug-in to dislodge profitably.[^4]8

Process Power — modest. The internal know-how built up over 25 years of Indian-climate viticulture and Indian-channel distribution is meaningful but not unique to the point that a well-funded entrant with patience could not eventually replicate it.

Net: Sula has at least two strong powers (Cornered Resource + Branding), one moderate-to-strong (Scale), and one underrated (Counter-Positioning). That is a more durable competitive position than the casual investor would assume.

Now to Porter's 5 Forces.

Threat of New Entrants — low to moderate. The capital cost of a credible Nashik winery, the multi-state distribution complexity, and the brand-first behavior of Indian wine consumers create real barriers. The 2026 LVMH exit is the most expensive recent evidence that even multinational entrants find this market unwelcoming.

Bargaining Power of Suppliers — managed. The 1,000-plus farmer network is structured through contracts that lock in supply at predictable prices. A grape shortage in a bad weather year still hurts, but the supplier side is not in a position to extract excess rents from Sula.2

Bargaining Power of Buyers — mixed. End consumers have low individual bargaining power. The state alcohol corporations, however, can be powerful counterparties, and the trade channel (modern trade, hotels, restaurants) has meaningful leverage during contract negotiations.

Threat of Substitutes — high. This is the single biggest five-forces concern for Sula. India remains a whiskey and beer market. The substitution risk is not from other wines; it is from younger consumers picking up a craft beer or a flavored gin or a ready-to-drink cocktail instead of a glass of Sauvignon Blanc.

Intra-Industry Rivalry — low at the top, higher at the bottom. Within the premium wine segment, Sula is essentially the category. In the popular and economy tiers, rivalry from imported bulk wines and other domestic players is more intense, which is one reason management has emphasized walking away from low-end volume.[^13]

The composite picture: Sula sits in a defensible position with the most pressure coming from substitutes — the slow, structural question of whether Indian consumers will adopt wine at the rates global benchmarks suggest is possible.

Is Sula the LVMH of India? It is the right vision to aspire to, but it is too soon to make that comparison rigorous. LVMH spans dozens of luxury maisons. Sula is one brand house operating in one category in one country. The right comparison, today, is closer to Robert Mondavi in 1990s Napa — a regional category-creating brand with a national platform and a defended position, waiting to see whether the underlying consumption curve will lift it to the next level.

That underlying curve is the heart of the bear-and-bull debate.

IX. Bear vs. Bull Case

Sula's stock, like most consumer-discretionary names in India, swings between two narratives depending on the macro mood. Let us steel-man both, because both contain real signal.

The Bear Case

Start with climate. Indian viticulture sits at the edge of what Vitis vinifera can tolerate. Nashik's harvest is delicate. A shift in monsoon timing, an unseasonal hailstorm in February, a heat wave during véraison can compress yields. A bad weather year does not just hurt the top line in that year; it pulls forward grape costs and degrades inventory quality. As climate variability increases globally, the structural exposure of a single-region, single-country wine producer is real.2

Add state-level excise volatility. The Karnataka destocking episode in 2025-2026 was a textbook illustration: an unexpected regulatory change at the state level forced inventory unwind through the channel, which compressed reported revenues and margins for a couple of quarters.6 India has 28 states and 8 union territories, and each one can, in principle, change the rules every fiscal year. You cannot diversify away this exposure entirely.

Add substitution risk. Indian Gen Z and millennial consumers are forming alcohol preferences right now, and the evidence so far is that they are gravitating toward craft beer, premium spirits, and ready-to-drink cocktails as much as toward wine. If wine does not become a serious mass-market category by the time today's 25-year-olds are 40, the Sula thesis weakens materially. The hopeful counter-evidence — that wine consumption is growing — is real, but it is growing from a base so small that it is easy to over-extrapolate.[^11]

Add the valuation question. Sula trades at consumer-discretionary multiples that imply continued double-digit revenue growth and steady margin expansion. Any quarter that breaks that narrative — and there have been such quarters — compresses the multiple painfully.

And finally, add distribution complexity as both a moat and a liability. The same multi-state distribution that protects Sula from competitors also exposes it to working-capital cycles, receivables stretching from state corporations, and the occasional inventory mismatch.

The Bull Case

The headline bull number is per-capita consumption. India's per-adult wine consumption sits somewhere under 100 milliliters per year, compared to a global average measured in liters and developed-market norms of several liters per adult per year.[^11] If India simply moves from "negligible" to "modest" — say, 500 milliliters per adult — that is a multi-fold expansion of the category. Sula, at roughly 60% share, captures the largest slice of that.1 You do not need a heroic forecast of Indians drinking like the French. You need a modest forecast of Indians drinking like, say, Russians or Brazilians.

Add margin expansion through premiumization. The mix shift from popular to elite/premium is far from done. Each year that the premium share of own-brands expands further, gross margin and EBITDA margin compound.2[^13]

Add the hospitality moat. The ₹100+ crore tourism business is not just incremental revenue; it is a high-margin moat that nobody else in Indian wine can replicate.[^5] As Sula adds Nashik and Dindori capacity, the tourism flywheel deepens.

Add direct-to-consumer. Indian state regulations are slowly evolving toward allowing more retail wine access — supermarket sales, online ordering, walk-in stores. Maharashtra opened wine in supermarkets in 2022.[^10] Each such liberalization is, in effect, a free expansion of Sula's potential channel without proportional cost.

Add the M&A optionality. Sula has demonstrated an ability to buy distressed-but-strategic Nashik assets at attractive prices. With LVMH's exit and other capacity overhangs in the district, the consolidation runway is not done. Each such bolt-on, like York and the Chandon facility, expands capacity and brand at well-below-replacement-cost prices.[^4][^7]8

Add the long-run founder alignment. Rajeev Samant has spent 25-plus years building this category and is still buying shares. The base case is that he keeps doing what he has been doing for another decade.7

A note on second-layer diligence overlays worth carrying as you watch this name: the climate exposure shows up in segment notes around grape costs; the regulatory exposure shows up in receivables and inventory days; the consumer adoption curve shows up in the share of own-brands sales and the elite/premium mix; and the M&A runway shows up in capex and intangibles on the balance sheet. None of these is hidden, but each rewards attention.

Myth versus Reality

A few consensus narratives deserve fact-checking. The first is that Sula is "just an agricultural commodity dressed up as a consumer brand." Reality: with tourism at ₹100+ crore, premium mix at ~79% of own-brands, and a brand that defines the category, the consumer-brand framing is closer to right than the commodity framing.2[^5][^13]

The second is that "wine in India is a flash in the pan; the country will always be a whiskey market." Reality: even in mature whiskey-and-beer markets globally, wine has carved out durable double-digit share of the alcohol wallet within a generation. India's structural setup is not different in kind, only in timing.

The third is that "Sula's competitors will catch up." Reality: the nearest dedicated wine competitor operates at roughly an order of magnitude smaller scale, and the entry of LVMH and its 2026 exit suggests that even global luxury muscle does not automatically translate into Indian wine market share.[^4][^11]

KPIs worth watching. If you can only track two or three things to assess how Sula is doing each quarter, the most important are:

- Wine Tourism segment revenue and EBITDA margin — the cleanest proxy for the moat health and the premiumization flywheel.

- Elite and Premium share of Own-Brands revenue — the single best read on whether the mix shift is continuing.

- State-level channel inventory days and receivables — the early-warning indicator for excise-driven disruptions that can compress quarters before they hit the headline P&L.

If those three numbers are heading in the right direction, the rest of the story usually takes care of itself.

X. Epilogue and Closing

Step back from the spreadsheets for a moment. Picture the Nashik hillside again — but now, in 2026.

Where there were once mango trees and rocky soil, there are 2,500-plus contracted acres of trellised vines stretching toward the horizon. Where Rajeev Samant once drove cases of an unloved Sauvignon Blanc in his car trunk to Mumbai restaurants, there are now Sula tastings happening in 25-plus states, restaurant lists with multiple Sula labels by the glass, supermarket aisles in Maharashtra carrying Sula bottles next to bread and milk.[^10][^13] Where a "wine festival" in India was once an oxymoron, SulaFest is a fixture of the calendar.

The most remarkable part of the story is how patient it has been. Twenty-seven years from the founding to the LVMH exit-and-handover. That is a generation. It is the kind of patience that public-market investors increasingly find hard to underwrite, because quarterly reporting cadence trains everyone to want returns faster than category-building actually happens.

The legacy of Rajeev Samant is, in some ways, larger than Sula itself. He did not just build a wine company. He built a wine industry. The Maharashtra Wine Policy. The farmer network. The tasting-room model. The festival format. The premium pricing architecture. The very idea that an Indian consumer could legitimately prefer an Indian wine over an imported one. Each of these is now infrastructure that any future Indian wine producer — including Sula's own competitors — will use, knowingly or not.

The next chapter is partially visible already. The Chandon facility integration will play out over the coming year. The tourism business will continue its march beyond the ₹100 crore mark and, if the resort expansion plays out, the segment will compound at attractive rates from here.[^4][^5] The premium portfolio will keep grinding higher in mix. State-level liberalization will keep adding incremental channels. And somewhere in Mumbai or Bangalore or Delhi, a 24-year-old who has never thought of wine as her drink will walk into a supermarket, pick up a bottle with a stylized sun on the label, and accidentally write the next chapter of this story herself.

Whether Sula becomes the LVMH of India, or the Robert Mondavi of India, or something entirely new that does not yet have a label, is a question the next decade will answer. What is already clear is that the company that opened the door to Indian wine has, after a quarter-century, walked through it — and is now standing on the other side, asking everyone else when they will join.

That is the Sula story. From an Oracle cubicle in Redwood Shores to a publicly listed wine pioneer in Nashik. From a 20-acre mango orchard to a 60%-share national category. From a "crazy idea" in 1993 to a ₹100 crore tourism business and a Chandon facility in 2026. Twenty-seven years. One founder. One bet. Cheers.

References

References

-

Red Herring Prospectus (RHP) — SEBI / Sula Vineyards Limited ↩

-

The Sula Story: From Oracle to Nashik's Vineyards — INSEAD Knowledge ↩↩↩↩↩

-

Rajeev Samant's Vision for Indian Wine — Forbes India, 2024 ↩

-

Q4 FY26 Earnings Call Transcript — Sula Vineyards Limited ↩↩

-

Financial Summary and Management Remuneration — Simply Wall St ↩↩↩↩↩

-

LVMH's Chandon India Exit and Sula's Strategic Capture — Reuters, 2026-03-25 ↩↩↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube