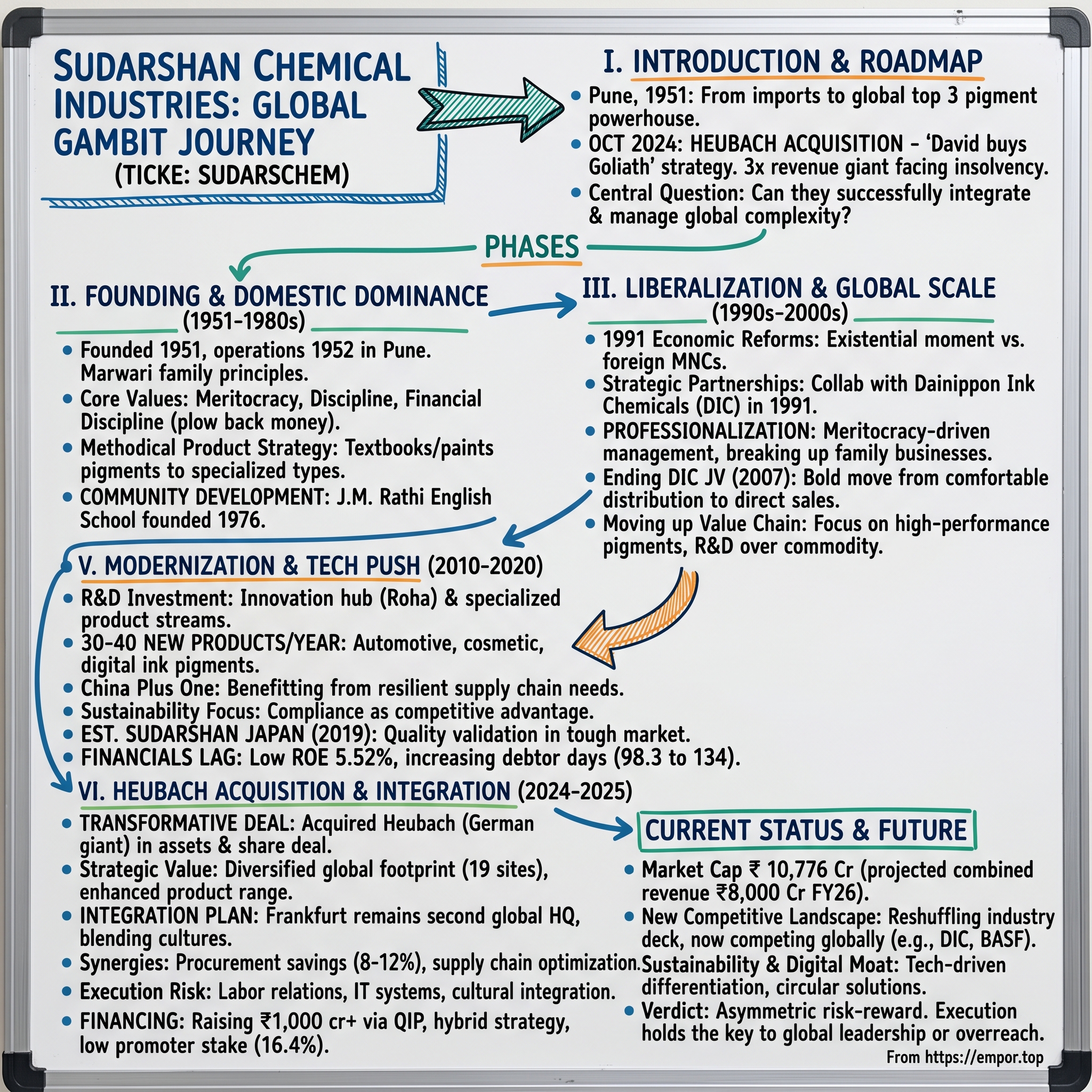

Sudarshan Chemical Industries: The Pigment Powerhouse's Global Gambit

I. Introduction & Episode Roadmap

Picture this: It's monsoon season in Pune, 1951. As newly independent India takes its first tentative steps toward industrialization, a group of visionary brothers gather in a modest office, examining imported pigment samples that cost more than most Indians earn in a month. They dream not just of making colors, but of painting India's industrial future in vibrant hues. Seven decades later, their company stands as the 3rd largest pigment manufacturer globally, having just pulled off one of the most audacious acquisitions in Indian chemical industry history.

This is the story of Sudarshan Chemical Industries Limited—a company that was incorporated in 1951 and started manufacturing pigments in 1952, transforming from a post-independence startup into a global color solutions provider. With 35% market share in India's pigment market and operations spanning continents, Sudarshan's journey mirrors India's own evolution from a protected economy to a confident global player.

But here's what makes this story particularly compelling: In October 2024, this family-controlled Indian company announced it would acquire Heubach Group—a 200-year history German pigment giant that's three times its size in revenue. It's David buying Goliath, if David had the backing of surging institutional investors and a clear-eyed turnaround strategy.

The central question we'll explore: How did a company founded by the Rathi brothers in newly independent India position itself to swallow a European behemoth facing insolvency? And more importantly, can they successfully integrate a company with over a billion euros in revenue in FY21 and FY22 while navigating European labor laws, cultural differences, and the complexities of global supply chains?

We'll trace Sudarshan's evolution through four distinct phases: the foundational years of building domestic dominance, the liberalization-driven expansion into global markets, the strategic pivot toward specialty chemicals and innovation, and finally, the transformative Heubach acquisition that could either cement its position as a global leader or become a cautionary tale of overreach.

Along the way, we'll examine how this ₹10,776 Crore market cap company maintains its competitive edge against rivals like Ultramar & Pigments, Poddar Pigments, Kiri Industries, while dealing with operational challenges including debtor days increased from 98.3 to 134 days and low return on equity of 5.52% over last 3 years.

This isn't just a business story—it's a narrative about ambition, timing, and the delicate art of cross-border M&A in an industry where relationships are measured in decades and mistakes in quarters. Let's dive in.

II. Founding & The Early Years (1951-1980s)

The year is 1951, and the air in Pune carries the intoxicating mix of possibility and uncertainty that defined newly independent India. In this atmosphere, the company was started in 1951 by my uncle—who completed his PhD in chemical engineering in the United States—along with my father and his other brothers, as Rajesh Rathi would later recount. The founding wasn't just about business—it was about building something fundamentally Indian in an economy dominated by foreign players.

From the outset, it was a profit-making company, based on three principles. The first was meritocracy. Despite not being the eldest, the third brother was made CEO because he was the most educated. This decision, radical for a traditional Marwari business family, would set the tone for decades to come.

The second principle was equally unconventional: discipline. The second principle was discipline, with regard to coming in to work on time. In the 1950s, coming from a Marwari family, you didn't start work before 11 a.m., but there was a rule that everyone had to report to work at 8:45 a.m. I remember as a child, if my father was even five minutes late for work, he would be very upset because a quarter of his day's salary would be docked.

The third pillar: financial discipline: Plow money back into the company and lead a very simple lifestyle. These weren't just operational guidelines—they were a philosophy that would enable the company to survive the tumultuous early decades of Indian independence.

The Rathi family's vision extended beyond mere import substitution. When Sudarshan Chemical Industries was founded in 1952 (the company was incorporated in 1951 but began operations in 1952), India's chemical industry was virtually non-existent. Every premium pigment was imported, making Indian manufacturers dependent on foreign suppliers who could dictate terms and prices.

The company's early product strategy was methodical. They started manufacturing pigments in 1952 and since have expanded to a breadth of products that cover Azo Pigments, High Performance Polycyclic Pigments, CICP (Complex Inorganic Colored Pigments), Solvent Dyes, Pigment Preparations and Effect Pigments. But this expansion didn't happen overnight. The initial focus was on basic inorganic pigments—products that Indian textile and paint manufacturers desperately needed but couldn't afford to import.

Geography played a crucial role in the company's development. The decision to establish operations in Maharashtra, specifically in Roha, and Mahad, wasn't accidental. These locations offered proximity to Mumbai's port for raw material imports and finished goods exports, while maintaining lower operational costs than the commercial capital itself. The Roha facility, in particular, would become the backbone of Sudarshan's manufacturing prowess.

The 1970s brought both challenges and opportunities. The License Raj system meant that every expansion required government approval, every import needed permits, and foreign exchange was scarcer than gold. Yet, these constraints forced Indian companies to innovate. Sudarshan couldn't simply license technology from abroad—they had to develop their own processes, often through painstaking trial and error.

This period also saw the Rathi family's commitment to community development. In 1976, the founders of Sudarshan also founded the J.M. Rathi English School & Junior College (JMRES) to ensure that the children of employees who are relocated to Roha, which is an important industrial center, would not have to compromise on the quality of education. This wasn't corporate social responsibility as we know it today—it was pragmatic community building. If you wanted skilled workers to move to industrial townships, you needed to provide quality education for their children.

By the late 1970s, Sudarshan had established itself as a reliable domestic player. But reliability alone wouldn't be enough for what was coming. The company sensed that India's closed economy couldn't last forever. International competition would arrive eventually, and when it did, only those who had built genuine technical capabilities would survive.

The foundation was set, but the real test would come with liberalization. As the 1980s drew to a close, whispers of economic reform began circulating in Delhi's corridors of power. The Rathi family knew that their small Pune-based operation would soon compete not just with other Indian companies, but with global giants who had centuries of experience and billions in resources.

III. Building Scale & Market Position (1990s-2000s)

The summer of 1991 changed everything. As India's foreign exchange reserves dwindled to barely three weeks of imports, Finance Minister Manmohan Singh stood before Parliament and dismantled four decades of economic isolation. For Sudarshan Chemical, liberalization wasn't just a policy shift—it was an existential moment. Would they be crushed by incoming multinationals, or could they leverage their local knowledge to compete globally?

The answer came through a strategic masterstroke. Recognizing that technology would be the differentiator, Sudarshan entered into collaborations with international players. In Jan.91, it commenced manufacture of a new range of organic pigments such as pthalocyanine with technology from Dainippon Ink Chemicals, Japan. This wasn't just a technology transfer—it was a marriage of Japanese precision with Indian entrepreneurship.

But Rajesh Rathi, who had returned from the United States with an MBA from the University of Pittsburgh, understood that the real transformation needed to happen from within. In the 1990s, at the peak, I think we had 14 family members working in various businesses across the group. There were seven or eight of us at one point within the Sudarshan Group, which included Sudarshan Chemicals and some of the engineering group. Our founders realized that wasn't sustainable and decided to break up the businesses. As we started growing, the family made a unanimous decision that meritocracy should be the predominant factor, so we slowly made the organization more professional, and built a good pipeline of leaders.

This professionalization coincided with aggressive market expansion. The company developed a multi-brand strategy that would become its signature: Sudaperm, Sudafast, Sudacolor, Sudadur, Sudafine, Sudajet, Sudasol, Sudatherm, Sudanyl, Sumica, Sumica NXR, Sumicos, and Prestige brands each targeted specific applications in coatings, paints, plastics, inks, cosmetics, and textiles.

The relationship with Dainippon Ink and Chemicals (DIC) evolved beyond mere technology transfer. The real growth began in 2007 when we and Dainippon Ink and Chemicals mutually agreed to end our joint venture. We had an exclusive global distribution agreement with them, and at that point, almost 60 percent of our sales were as a result of that agreement. However, we had ambitions to move into direct sales and transform our portfolio.

This decision to end a comfortable arrangement that generated 60% of revenues was either brave or foolhardy. Most Indian companies of that era would have clung to such partnerships. But the Rathi family understood that true global competitiveness required direct customer relationships, not intermediated ones.

The 2000s brought new challenges. China's entry into the WTO in 2001 fundamentally altered global chemical markets. Suddenly, Indian companies weren't just competing with European and American firms with high cost structures—they were facing Chinese competitors who could undercut prices while rapidly scaling production.

Sudarshan's response was to move up the value chain. Instead of competing on volume in commodity pigments where Chinese producers had advantages, they focused on specialty products requiring technical expertise and customer intimacy. The company also began investing heavily in environmental compliance, anticipating that regulations would eventually become a differentiator.

The global financial crisis of 2008-09 tested every assumption. As demand collapsed across industries, pigment consumption plummeted. Companies with high debt or weak customer relationships folded. But Sudarshan's conservative financial management—that third founding principle of plowing money back into the business—proved its worth. While competitors retrenched, Sudarshan maintained its R&D spending and even selectively expanded capacity.

Listing date: 16 Jan, 1995 marked another crucial milestone, providing access to capital markets that would fund future growth. The public listing brought scrutiny but also discipline, forcing the company to professionalize further and maintain transparent governance standards.

By 2010, Sudarshan had achieved something remarkable: it was simultaneously a trusted supplier to global MNCs and a fierce competitor to them in emerging markets. The company that had started by reverse-engineering imported pigments was now setting standards in product quality and application expertise.

But success brought its own challenges. With great market position came great expectations—from shareholders demanding returns, customers demanding innovation, and a new generation of family members questioning whether the chemical industry was the right place for their ambitions. The next decade would test whether Sudarshan could maintain its entrepreneurial edge while operating at institutional scale.

IV. The Public Markets Journey & Capital Structure Evolution

The transformation from a closely-held family enterprise to a public company deserves careful examination. When Listing date: 16 Jan, 1995 arrived, it marked not just a financial milestone but a fundamental shift in how the Rathi family would run their business. The Bombay Stock Exchange floor that day buzzed with an energy that reflected both optimism about India's liberalizing economy and skepticism about whether family-run chemical companies could deliver consistent returns.

The IPO pricing and initial reception told a story of measured expectations. This wasn't a software company promising to revolutionize the world—it was a chemical manufacturer in a capital-intensive industry with long development cycles. Early investors were primarily domestic institutions who understood the Indian industrial landscape and could appreciate the value of Sudarshan's distribution network and customer relationships.

Through the late 1990s and early 2000s, Sudarshan's stock performed steadily if unspectacularly. The company delivered consistent dividends, maintained conservative debt levels, and reinvested profits into capacity expansion. This wasn't the path to generating headlines, but it built trust with a specific type of investor—those who valued predictability over promises.

The 2008 financial crisis created an inflection point. As global markets crashed and credit markets froze, highly leveraged competitors struggled to service debt or fund working capital. Sudarshan's conservative balance sheet, which some analysts had criticized as inefficient during the boom years, suddenly looked prescient. The company emerged from the crisis with its reputation enhanced and its competitive position strengthened.

The real shift in capital structure dynamics began around 2017-2018. Around 2017, we analyzed each of our businesses and came up with three or four necessary criteria for each of them. We asked questions such as: Can we make this into a world-class business? Can we attain global leadership? If the answer was no, we exited the business. This strategic focus led to divestments including the divestment of its Industrial Mixing Solutions Division on 26th April 2019 to GMM Pfaudler Limited, for an Enterprise Value of approx. Rs. 29 Crores.

These weren't distress sales but strategic choices to concentrate capital and management attention on the core pigments business. The proceeds were reinvested into R&D and capacity expansion, particularly in high-performance and effect pigments where margins were superior to commodity products.

The evolution of promoter holding tells its own story. Starting from typical Indian family business levels above 50%, the Rathi family gradually diluted their stake to fund growth while maintaining operational control. By 2024, Sudarshan management currently owns only 30.5% of the company, though this would drop further to 16.4% after recent reclassifications and the Heubach acquisition funding.

This declining promoter stake created both opportunities and vulnerabilities. On one hand, it attracted institutional investors who preferred companies with professional management and distributed ownership. Mutual fund holding increased dramatically, particularly in recent years. On the other hand, it raised questions about the family's long-term commitment and the company's vulnerability to hostile takeovers.

The institutional investor base evolved significantly over this period. On August 24, 2021, Axis Mutual Fund A/c Axis Smallcap Fund purchased 589,498 equity shares, representing a 0.85 per cent stake of Sudarshan Chemical at a price of Rs 565 per share, signaling growing institutional interest. By 2024-25, mutual funds would become major stakeholders, with holdings reaching 21.63% at the end of 25/7/2025.

Stock performance through this period reflected these structural changes. The company delivered 136% gain in past year leading up to the Heubach announcement, driven by improving fundamentals and speculation about strategic moves. Yet underlying operational metrics painted a more complex picture: Company has a low return on equity of 5.52% over last 3 years and Debtor days have increased from 98.3 to 134 days.

The October 2024 decision to pursue the Heubach acquisition necessitated a complete rethinking of capital structure. The Board of Sudarshan Chemical Industries at its meeting held on 16 October 2024 has approved raising of funds of Rs 1,000 crore plus green shoe option upto 25% by way of issuance of Equity Shares or any other eligible securities. This would be the largest capital raise in the company's history, fundamentally altering its ownership structure.

The market's initial reaction was euphoric—shares of SCIL jumped 19.1 per cent to Rs 1,208, valuing the company at Rs 8,359 crore on the announcement day. But this enthusiasm was tempered by practical concerns about execution risk, integration challenges, and the dilution facing existing shareholders.

The capital markets journey reveals a company constantly balancing competing demands: family control versus institutional governance, conservative financial management versus growth ambitions, domestic focus versus global aspirations. Each choice created path dependencies that would culminate in the transformative decision to acquire Heubach—a bet that would either validate decades of patient capital allocation or expose the limitations of ambitious emerging market companies trying to swallow developed market giants.

V. Modernization & Technology Push (2010-2020)

The second decade of the 21st century opened with Sudarshan at a crossroads. Chinese competitors were flooding global markets with low-cost pigments, European companies were consolidating to achieve scale, and customers increasingly demanded not just products but complete color solutions. The company's response would define whether it remained a successful regional player or emerged as a genuine global force.

R&D investment became the cornerstone of transformation. The company systematically upgraded its research facilities, moving beyond basic color matching to fundamental research in particle engineering, surface chemistry, and dispersion technology. The Roha research center evolved from a quality control lab into an innovation hub where PhD chemists worked alongside application engineers to solve customer problems before customers knew they had them.

Under him, the company churns out 30-40 new products every year. This wasn't innovation for innovation's sake—each new product addressed specific market gaps. High-performance pigments for automotive coatings that could withstand extreme weather. Effect pigments for cosmetics meeting increasingly stringent safety regulations. Specialized dispersions for digital printing inks compatible with emerging jet technologies.

The numbers tell a story of successful transformation. The company achieved Revenue growth at 14.35% CAGR over 5 years vs industry average of 9.43%, consistently outpacing market growth. This wasn't just riding industry tailwinds—it was taking market share from established competitors through superior products and service.

Digital technology adoption accelerated through this period, though not in the flashy way of software companies. Sudarshan implemented sophisticated color-matching software that could predict pigment behavior in different polymer systems. Production planning systems optimized batch scheduling across multiple plants. Customer portals provided real-time order tracking and technical documentation. These weren't revolutionary innovations, but their cumulative impact on operational efficiency was substantial.

The company also diversified beyond pure pigments. The Group also manufactures Pollution Control Equipment, Size Reduction Equipment and Grinding Equipments for industrial applications. This wasn't random diversification—it leveraged core competencies in particle processing while providing steadier revenue streams less subject to raw material price volatility.

Sustainability emerged as both challenge and opportunity. European regulations like REACH required extensive testing and documentation for chemical products. Rather than viewing compliance as a burden, Sudarshan positioned it as a competitive advantage. Many smaller competitors, particularly from China, couldn't meet these standards, effectively creating non-tariff barriers that protected compliant producers.

The COVID-19 pandemic in 2020 tested every assumption about global supply chains. Operations were shut down following the Covid-19 pandemic from March 2020 and have now resumed with directives from the Government. But the crisis also accelerated certain trends. Customers began prioritizing supply chain resilience over pure cost optimization. "China Plus One" strategies meant manufacturers sought alternative suppliers outside China. Sudarshan, with its established infrastructure and compliance credentials, was perfectly positioned to benefit.

Investment during this period was substantial. During Fiscal Year 2020, the company has invested Rs. 227 Crore in projects to expand their operations and for the production capacities of Roha and Mahad sites. This expansion wasn't just about volume—it included sophisticated equipment for producing effect pigments and high-performance grades that commanded premium prices.

The establishment of Sudarshan Japan Limited, a Wholly Owned Subsidiary of the company was established in Japan in 2019 signaled ambitions beyond traditional emerging markets. Japan, with its exacting quality standards and relationship-based business culture, represented the ultimate test of Sudarshan's capabilities. Success there would validate the company's transformation from cost-competitive supplier to technology partner.

Management culture evolved significantly during this period. Common traits across our leadership team are boldness and ambition. One of my responsibilities is to ensure that I keep coaching and directing our leaders toward the common aim of the company being a world-class, global leader. The company recruited talent from MNCs, bringing global best practices while maintaining entrepreneurial agility.

Yet challenges persisted. Despite operational improvements, financial metrics lagged. Company has a low return on equity of 5.52% over last 3 years. Working capital management deteriorated, with Debtor days have increased from 98.3 to 134 days. These weren't signs of fundamental weakness but rather growing pains of a company transitioning from transactional vendor to strategic partner requiring longer payment terms and higher service levels.

By 2020, Sudarshan had successfully modernized its operations and technology base. It had the products, processes, and people to compete globally. What it lacked was scale—the kind of scale that would provide leverage with raw material suppliers, justify investments in next-generation technologies, and ensure a seat at the table when global customers consolidated their vendor bases. This recognition would drive the next chapter of the company's evolution: the audacious pursuit of Heubach.

VI. The Heubach Acquisition: Bold Bet or Masterstroke? (2024-2025)

The boardroom in Pune was unusually quiet on that October morning in 2024. Rajesh Rathi looked around the table at his directors, knowing the decision they were about to make would either transform Sudarshan into a global powerhouse or become a cautionary tale studied in business schools. The target: Heubach Group, a German pigment giant with revenues three times Sudarshan's size, now facing insolvency.

Mumbai, October 11th, 2024 — Sudarshan Chemical Industries Limited ("SCIL" or "Company") today announced that it has entered into a definitive agreement with the Germany-based Heubach Group, on its acquisition in a combination of an asset and share deal. The announcement sent shockwaves through the global pigments industry. How could a company with roughly €400 million in revenue acquire a business generating over €1 billion just two years prior?

The answer lay in Heubach's spectacular fall from grace. In 2022, Heubach became the world's second-largest pigment player after integrating with Clariant. The integration of Clariant's pigments business should have created a European champion. Instead, it created a disaster. The Group faced financial challenges over the past two years due to rising costs, inventory issues, and high interest rates.

But where others saw insolvency, Rathi saw opportunity. The acquisition price of Rs 1,180 crore (€127.5 million) for a business that had generated over a billion euros in revenue in FY21 and FY22 represented an extraordinary valuation at 0.2x CY23 sales with no debt transfer. For context, comparable pigment businesses typically traded at 1-2x sales. This wasn't just a discount—it was a fire sale.

The structure of the deal revealed sophisticated financial engineering. The proposed transaction includes the acquisition of assets and business operations of Heubach Colorants Germany GmbH, Heubach GmbH (c) Dr Hans Heubach GmbH, and Heubach Group GmbH and participations held by Heubach Holding Switzerland AG, in downstream Group Companies in various countries from insolvency administrator. By acquiring assets from insolvency administrators rather than the company directly, Sudarshan could cherry-pick valuable operations while leaving behind problematic liabilities.

The strategic rationale was compelling. It will enhance SCIL's product portfolio, giving it access to a diversified asset footprint across 19 international sites. Overnight, Sudarshan would transform from an India-centric player with export ambitions to a truly global company with manufacturing presence across 19 sites in all regions.

The deal's completion on March 3rd, 2025 marked the end of one chapter and the beginning of another. Commenting on the closure of the acquisition, Mr. Rathi said, "Today marks an exciting new chapter as we unite with Heubach to become an inspirational leader in the colorants industry. The combined company builds on the rich legacies of both Sudarshan and Heubach. Our goal is now to create the world's most valuable pigment company with great financial strength and profitability."

But the celebration was tempered by the magnitude of challenges ahead. Heubach's 200-year history came with legacy obligations, particularly in Europe where labor laws made restructuring difficult and expensive. The German works councils, powerful entities that could block major operational changes, would need to be convinced that an Indian acquirer could be trusted with German jobs.

The cultural integration posed perhaps the greatest challenge. Creating a single culture is going to be very important going forward—it's not just about processes, it's also about people. Heubach's employees, many with decades of service, had to accept leadership from a company they might have viewed as an upstart competitor just years earlier.

Geographic expansion brought operational complexity. We will carefully integrate these two companies to create a truly global pigments company, with Frankfurt remaining a strategically important location. The decision to maintain Frankfurt as a second headquarters wasn't just symbolic—it was pragmatic recognition that European customers and employees needed reassurance about continuity.

The financing structure revealed careful balance between ambition and prudence. While the board approved raising of funds of Rs 1,000 crore plus green shoe option upto 25%, management committed to achieving zero debt level within a few years. This wasn't just financial conservatism—it was recognition that integration would require flexibility that high leverage would preclude.

Market reaction was initially euphoric, with the stock hitting upper circuit at 20% on Friday following the announcement. But institutional investors' response was more telling—mutual funds increased their stake significantly, viewing the acquisition as transformational despite execution risks.

The integration philosophy emphasized pragmatism over ideology. A company with customer centricity (Sevā) at its heart: Post-acquisition SCIL envisages to become the supplier of choice for all customers. Rather than imposing Indian management practices on German operations, Sudarshan sought to blend the best of both cultures—German technical excellence with Indian entrepreneurial agility.

Early signs were encouraging. Customer retention remained strong, with many viewing the combination positively as it ensured continuity of supply with enhanced financial stability. The technical teams found unexpected synergies, with Heubach's expertise in effect pigments complementing Sudarshan's strength in high-performance grades.

Yet questions lingered. Could Sudarshan successfully manage operations across 19 sites when it had previously run just two major facilities? Would European customers accept an Indian company as a strategic supplier? Could the promised synergies be realized without destroying the capabilities that made Heubach valuable?

As 2025 progressed, one thing became clear: this wasn't just an acquisition. It was a bet on the future of the global pigments industry, where scale, sustainability, and supply chain resilience would determine winners. Sudarshan had placed its chips on the table. The wheel was spinning.

VII. Financial Engineering & Funding Strategy

The arithmetic was daunting. Sudarshan needed approximately 2100 Cr for this transaction (1200 Cr for the deal + 900 Cr as working capital & other restructuring expenses). To put this in perspective, the balance sheet size of Sudarshan Chemicals as of FY24 is 2346 Cr. The company was essentially doubling its balance sheet overnight—a financial high-wire act that would make even seasoned investment bankers nervous.

The funding strategy revealed sophisticated thinking about capital markets and stakeholder management. Rather than relying solely on debt, which would have crushed the balance sheet, or entirely on equity, which would have massively diluted existing shareholders, management crafted a hybrid approach that balanced multiple considerations.

The cornerstone was the Qualified Institutional Placement (QIP) route. They are going the QIP route to partially fund this acquisition. QIPs offered speed—crucial when dealing with insolvency administrators who wanted certainty—and flexibility in pricing. More importantly, they brought in institutional investors who could provide not just capital but credibility to the transaction.

Yet the QIP created its own dilemma. But this brings in another problem for the management – low promoter holding. You see, Sudarshan management currently owns only 30.5% of the company. Equity dilution at this point will further dilute their overall holding. The promoter stake had already fallen to 16.4% by late 2025, raising questions about whether the family was cashing out or simply accepting dilution as the price of transformation.

Management's response was nuanced. When asked this question in the recent con call, the management clarified that some promoters in the past opted to discontinue being labeled as promoters while remaining as shareholders. This reclassification—where family members remained invested but weren't counted as promoters—was partly semantic but sent important signals about professional management taking precedence over family control.

The debt component was carefully structured to avoid overleveraging. Unlike many leveraged buyouts where acquirers load targets with debt, there is no debt transfer from Heubach to Sudarshan. It is purely an assets and operations transfer. This clean structure meant Sudarshan wasn't inheriting Heubach's financial problems, just its operational assets.

Working capital financing presented unique challenges. Heubach's operations required substantial working capital—customer payment terms in Europe were longer than in India, while raw material suppliers demanded faster payment given Heubach's recent distress. The 900 Cr as working capital & other restructuring expenses allocation showed management understood that acquisition price was just the entry fee; the real cost would be in restoration.

Institutional investors' response validated the strategy. Mutual funds dramatically increased exposure, with holdings rising from historical levels to 21.63% by mid-2025. These weren't momentum traders chasing a story but sophisticated investors who had done their homework on integration economics.

The commitment to achieve zero debt level within a few years wasn't just financial prudence—it was strategic positioning. Management understood that the next few years would require operational flexibility. High debt would limit ability to invest in integration, upgrade facilities, or pursue opportunistic acquisitions if competitors struggled.

Currency hedging added another layer of complexity. With operations now spread across euros, dollars, and rupees, but reporting in rupees, foreign exchange management became critical. A 10% currency swing could wipe out or double reported profits, making hedging strategy as important as operational execution.

The board's approval of Rs 1,000 crore plus green shoe option upto 25% provided cushion for uncertainties. The green shoe—ability to raise an additional 25% if needed—was insurance against integration costs exceeding estimates or working capital requirements proving higher than modeled.

Synergy assumptions underpinned the entire financial architecture. Management projected significant EBITDA improvements by 2028-29, based on cost synergies from procurement scale, operational efficiencies from best practice transfer, and revenue synergies from cross-selling. If achieved, these would justify the dilution and risk. If not, shareholders would face years of subpar returns.

The market's initial enthusiasm—stock jumping 20% on announcement—suggested investors bought into the logic. But bond markets, generally more skeptical than equity markets, would provide the real test. Could Sudarshan maintain investment-grade ratings while absorbing a business three times its size?

Tax structuring added hidden value. By acquiring through Sudarshan Europe BV, a wholly-owned subsidiary in the Netherlands, the company could optimize tax treatment of future cash flows. The Netherlands' extensive tax treaty network meant profits could be repatriated efficiently, crucial for servicing acquisition debt.

As the funding closed and integration began, the financial engineering would be tested by operational reality. Every synergy target missed would increase pressure on the balance sheet. Every working capital overrun would strain banking relationships. The elaborate structure that enabled the acquisition would either prove robust enough to weather integration storms or become an albatross that constrained the combined entity for years.

The stakes couldn't be higher. Success would validate the thesis that emerging market companies could acquire and turn around developed market assets. Failure would reinforce skeptics who believed such ambitions exceeded emerging market capabilities. The financial engineering was complete. Now came the hard part: making the numbers work in reality.

VIII. Integration & Transformation Playbook

The real work began on March 4, 2025—the day after the acquisition closed. Rajesh Rathi stood in Heubach's Frankfurt headquarters, addressing hundreds of German employees who viewed this moment with a mixture of relief (they still had jobs) and apprehension (their new owners were from India). His opening words would set the tone: "We're not here to impose Indian ways on German operations. We're here to combine German engineering excellence with Indian entrepreneurial spirit."

The integration philosophy departed from traditional acquisition playbooks. Rather than immediate cost-cutting or forced standardization, Sudarshan adopted what they called "respectful integration." We will carefully integrate these two companies to create a truly global pigments company, with Frankfurt remaining a strategically important location. This wasn't just rhetoric—Frankfurt would genuinely serve as the second global headquarters, with significant decision-making authority.

The organizational structure reflected this balanced approach. Instead of installing Indian executives across all positions, Sudarshan retained key Heubach managers, particularly those with deep customer relationships and technical expertise. The integration team itself was deliberately multicultural—Indian financial controllers working with German plant managers, German sales leaders collaborating with Indian supply chain experts.

Culture of agility and customer focus will be at the center of this integration. But creating this culture required navigating fundamentally different work philosophies. German operations ran on precision and planning—production schedules set months in advance, maintenance windows rigorously defined. Indian operations thrived on flexibility—quickly adjusting to customer requests, finding creative solutions to supply disruptions.

The first 100 days revealed both quick wins and unexpected challenges. Quick wins came in procurement, where Sudarshan's relationships with Asian suppliers immediately reduced raw material costs by 8-12% for certain categories. Heubach had been paying premium prices due to its financial distress; Sudarshan's balance sheet strength restored negotiating power.

Challenges emerged in areas nobody had anticipated. IT systems integration proved nightmarish—Heubach ran on SAP while Sudarshan used a combination of Oracle and custom systems. Data definitions differed, process flows conflicted, and even basic terms like "customer" had different meanings in different systems. The budgeted three-month integration stretched to nine months and cost twice the original estimate.

Labor relations required delicate handling. European works councils, particularly in Germany, wielded significant power. They could block plant closures, veto organizational changes, and mandate extensive consultation periods. Sudarshan's approach was patient engagement rather than confrontation. Management committed to no forced redundancies for 18 months, giving time to achieve efficiencies through natural attrition and voluntary programs.

The customer retention strategy proved remarkably successful. Post-acquisition SCIL envisages to become the supplier of choice for all customers. The company will have a wide product portfolio across segments and applications and it will be able to offer the best-in-class product portfolio to customers. Rather than approaching customers with integration synergies and cost savings, Sudarshan emphasized continuity and enhancement—same technical support, same product quality, but now with better financial stability and broader product range.

Supply chain optimization offered the greatest near-term value creation opportunity. Heubach had 19 plants often producing similar products for local markets. Sudarshan began rationalizing production—concentrating specific product lines in facilities best equipped to handle them, regardless of geography. This required overcoming "not invented here" syndrome and convincing plant managers that specialization would enhance rather than diminish their importance.

R&D integration followed a "best of both worlds" approach. Heubach's strength in effect pigments and Sudarshan's expertise in high-performance grades created natural complementarity. Rather than consolidating R&D in one location, the company maintained multiple centers of excellence—Frankfurt for effect pigments, Roha for organic pigments, specific sites for application development.

The commercial integration strategy balanced standardization with local autonomy. While implementing common CRM systems and pricing guidelines, regional sales teams maintained authority over customer relationships and tactical decisions. This prevented the alienation of sales staff who knew their markets better than any headquarters executive could.

Financial integration proceeded methodically. Treasury functions centralized quickly to optimize cash management and reduce banking costs. However, local finance teams remained to handle country-specific compliance and reporting requirements. The goal wasn't maximum centralization but optimal balance between efficiency and local responsiveness.

Nine months into integration, patterns emerged. German operations initially resistant to change began appreciating Indian colleagues' problem-solving creativity. Indian teams gained respect for German systematic approaches to quality and documentation. Creating a single culture is going to be very important going forward—it's not just about processes, it's also about people. This cultural fusion was happening organically through daily collaboration rather than through forced team-building exercises.

Performance metrics showed encouraging progress. Customer retention exceeded 95%, far above the 80-85% typical in distressed acquisitions. Employee turnover remained below 10%, suggesting successful change management. Operational synergies began materializing, with procurement savings funding investment in neglected maintenance and system upgrades.

Yet integration was far from complete. The hardest decisions—potential plant closures, brand consolidation, organizational delayering—still lay ahead. These would test whether the "respectful integration" philosophy could survive when respect conflicted with economics. The transformation playbook was being written in real-time, with each decision creating precedents that would define the combined entity's culture for decades.

IX. Current Market Position & Competitive Dynamics

By mid-2025, as integration dust began settling, a new competitive landscape emerged in the global pigments industry. Sudarshan's absorption of Heubach hadn't just changed the company—it had reshuffled the entire industry deck. The combined entity now commanded respect from competitors who had previously dismissed Sudarshan as a regional player punching above its weight.

The numbers painted a picture of transformation. With Market Cap ₹ 10,776 Cr and projected combined revenues approaching 8,000 Cr in revenue for the full year FY26, Sudarshan had catapulted into a different league. The company that had fought for recognition in international markets now had customers calling them, worried about supply continuity if they weren't prioritized.

The competitive landscape had shifted dramatically. Sudarshan Chemicals major competitors are Ultramar & Pigments, Poddar Pigments, Kiri Industries, Fineotex Chemical, Aditya Birla Real, Heubach Colorants(I), Shree Pushkar Chem. But post-acquisition, many of these were no longer peers. Ultramar and Poddar, once comparable in scale, now looked like regional players. The real competition came from global giants like BASF, Clariant (minus its divested pigments business), and DIC.

Market share dynamics revealed interesting patterns. In India, Sudarshan maintained its 35% market share, with the Heubach acquisition actually strengthening domestic position through expanded product portfolio. Customers who previously split orders between Sudarshan and imported Heubach products could now single-source, improving their own efficiency.

The China factor loomed large in competitive dynamics. Chinese pigment producers, who had dominated through cost leadership, faced increasing challenges. Environmental regulations in China had shut down numerous small producers. Trade tensions made Western customers nervous about supply chain dependence. Sudarshan, with its new European manufacturing base, offered an alternative that was both cost-competitive and politically palatable.

Product portfolio positioning became crucial differentiator. The combined entity offered everything from commodity iron oxides to sophisticated effect pigments for luxury cosmetics. This range allowed bundling strategies competitors couldn't match. A customer buying basic pigments could access advanced technical support for specialty applications, creating switching costs beyond simple price considerations.

Yet operational challenges persisted. Debtor days have increased from 98.3 to 134 days, reflecting the reality of serving sophisticated customers who demanded extended payment terms. Company has a low return on equity of 5.52% over last 3 years, a metric that would need improvement to justify the acquisition premium and shareholder dilution.

Management's response was strategic patience. The management has guided EBITDA margins to be around 12-15%, acknowledging that near-term margins would suffer as integration costs hit the P&L. The focus was on building competitive advantages that would endure beyond quarterly earnings cycles.

The sustainability angle provided unexpected competitive advantage. Heubach's European operations met stringent environmental standards that many Asian competitors couldn't match. Combined with Sudarshan's investments in green chemistry, the company could credibly position itself as the sustainable choice—crucial for European customers facing their own ESG pressures.

Digital capabilities emerged as a surprising differentiator. While pigments seemed like an old-economy business, digital tools transformed customer engagement. Color-matching apps, virtual product demonstrations, and AI-powered formulation recommendations created stickiness that pure product quality couldn't achieve. The combined IT investments of both companies, painful during integration, now provided competitive moat.

Regional dynamics varied significantly. In Europe, the combined entity had to overcome skepticism about Indian ownership while leveraging local manufacturing presence. In Asia, Sudarshan's reputation opened doors that Heubach alone couldn't access. In Americas, the company positioned itself as a stable alternative to Chinese suppliers without the high costs of local production.

Innovation pipeline suggested future competitive strength. The combined R&D capabilities were yielding results—new sustainable pigments replacing traditional heavy-metal based products, effect pigments enabling new automotive finishes, specialized grades for emerging applications like 3D printing. The company churns out 30-40 new products every year, but post-acquisition, both the pace and sophistication of innovation increased.

Customer concentration remained a strategic consideration. The top 20 customers accounted for significant revenue share, making relationship management crucial. The acquisition helped here—customers saw increased investment capacity and technical capabilities as positive signals about long-term partnership potential.

Competitive intelligence suggested rivals were responding. Clariant accelerated its specialty chemicals focus, effectively ceding commodity pigments market. BASF increased investment in high-performance grades. Chinese producers consolidated, with government support creating national champions. The industry was polarizing between scale players and niche specialists, with mid-sized generalists increasingly squeezed.

As 2025 progressed, Sudarshan's market position solidified but remained fragile. Success in integration had bought credibility, but sustained performance would determine whether the company could maintain its elevated status. The competitive game had changed from fighting for survival to fighting for leadership—a challenge requiring different skills and strategies than those that had brought Sudarshan this far.

X. Bear vs. Bull Case & Investment Analysis

The investment community remained sharply divided on Sudarshan's prospects post-Heubach acquisition. Sell-side analysts' price targets ranged from ₹900 to ₹1,800—an unusual 100% spread reflecting fundamental disagreements about integration success, market dynamics, and management capability. Both bulls and bears had compelling arguments, grounded in legitimate analysis rather than mere speculation.

The Bull Case: Path to Global Leadership

Bulls saw Sudarshan as the classic emerging market champion story—a company leveraging cost advantages and entrepreneurial agility to acquire and revitalize developed market assets. The acquisition math was compelling: buying €1 billion revenue business for 0.2x CY23 sales when industry multiples averaged 1-2x suggested massive value creation potential even with modest operational improvements.

Scale advantages would compound over time. Procurement savings alone could add 200-300 basis points to margins as the combined entity leveraged volumes with raw material suppliers. Production rationalization across 19 plants offered another 200-300 basis points as capacity utilization improved and logistics costs reduced. These weren't theoretical synergies—early results showed procurement savings materializing faster than projected.

The market structure favored consolidated players. Environmental regulations were forcing smaller competitors out of business. Customers wanted fewer, more capable suppliers who could provide global coverage and technical support. Sudarshan, with its expanded footprint and capabilities, was perfectly positioned to capture share from subscale competitors and challenged Chinese producers.

Financial flexibility remained robust despite the acquisition. Management's commitment to achieve zero debt level within a few years wasn't just aspiration—cash generation from the combined business could realistically achieve this given projected EBITDA improvements. Once deleveraged, the company would have firepower for organic investment or further acquisitions in a consolidating industry.

Valuation remained attractive even after stock appreciation. At 7,500 Cr current market cap, the company traded at less than 1x projected FY26 revenues—a discount to global peers despite superior growth prospects. As integration risks receded and synergies materialized, multiple expansion seemed inevitable.

The Bear Case: Integration Complexity and Structural Challenges

Bears pointed to sobering realities that enthusiasm obscured. Return on equity of 5.52% over last 3 years suggested structural profitability challenges that acquisition wouldn't solve. Adding a distressed European business with its own profitability issues seemed like doubling down on problems rather than solving them.

Working capital deterioration was particularly concerning. Debtor days have increased from 98.3 to 134 days before the acquisition; European customers' payment terms would make this worse. Cash conversion, already weak, could deteriorate further as the company funded European working capital requirements with expensive debt.

Integration execution risk remained enormous. Managing 19 plants across multiple countries required operational expertise Sudarshan hadn't demonstrated. European labor laws made restructuring difficult and expensive. IT systems integration was already over budget and behind schedule. These weren't just teething problems—they suggested fundamental challenges in absorbing a business three times the acquirer's size.

Promoter holding at just 16.4% raised governance concerns. The family's declining stake suggested either lack of confidence or prioritization of liquidity over long-term value creation. Without skin in the game, would management make tough decisions required for successful integration?

Competition wasn't standing still. Chinese producers, backed by government support, were moving up the value chain. Global giants like BASF had deeper pockets and superior technology. Sudarshan might have bought scale, but competitors had capabilities that couldn't be acquired—decades of customer relationships, proprietary technologies, brand equity in premium segments.

Market dynamics posed structural headwinds. Global manufacturing growth was slowing. Automotive production—a key end market—faced disruption from electrification reducing paint consumption per vehicle. Digitalization meant less printing ink demand. These secular trends would pressure volumes regardless of competitive position.

The Verdict: Asymmetric Risk-Reward

The investment case ultimately hinged on execution—specifically, whether management could realize projected synergies while maintaining business momentum. Early indicators were mixed but slightly positive. Customer retention exceeded targets, employee turnover remained manageable, and procurement savings were materializing. But the hard work of restructuring and integration lay ahead.

Risk-reward appeared asymmetric but in different directions depending on time horizon. Near-term risks were skewed negative—integration costs, margin pressure, and working capital consumption would likely disappoint. But long-term potential was skewed positive—if management achieved even 70% of targeted synergies, equity value could double from current levels.

The smart money was taking a barbell approach—either staying completely away until integration proved successful or taking meaningful positions betting on transformation. Half-measures made little sense given the binary nature of outcomes. This wasn't an investment for the faint-hearted or those requiring quarterly earnings predictability.

XI. Epilogue: The Future of Global Pigments

As the monsoon clouds gathered over Pune in mid-2025, Rajesh Rathi stood in the same office where his father and uncles had founded Sudarshan 74 years earlier. But the view from the window had changed dramatically. What was once a small industrial estate had become a sprawling corporate campus. The company that started with a handful of employees now employed thousands across continents. The dream of making Indian colors had evolved into something far grander—and far more complex.

The pigments industry stood at an inflection point that would determine winners and losers for the next generation. Sustainability was no longer optional—European regulations were forcing the phase-out of heavy metal-based pigments, creating opportunities for companies with green chemistry capabilities. Sudarshan's combined R&D resources positioned it well, but the investment required was substantial and returns uncertain.

China's evolution from low-cost manufacturer to technology competitor was reshaping competitive dynamics. Chinese companies were no longer content with commodity products—they were investing heavily in R&D, acquiring Western technology, and building global brands. The window for emerging market companies to leverage cost advantages while building capabilities was closing. Sudarshan's acquisition of Heubach might have been just in time—or perhaps too late.

Digital transformation was touching even traditional industries like pigments. Customers expected digital color matching, online ordering, real-time supply chain visibility, and predictive maintenance recommendations. The combined Sudarshan-Heubach entity had the scale to invest in these capabilities, but implementation across 19 sites with different systems and cultures would test organizational capacity.

The sustainability imperative created both opportunities and threats. Customers increasingly demanded not just compliant products but transparent supply chains, carbon footprint reporting, and circular economy solutions. Heubach's European operations provided credibility, but Sudarshan's Indian facilities needed upgrading to meet evolving standards. The capital required was substantial, coming at a time when the balance sheet was already stretched.

Supply chain resilience had become paramount post-COVID. The era of optimizing for cost alone was over—customers wanted multiple supply sources, regional manufacturing presence, and inventory buffers. Sudarshan's expanded footprint addressed these needs, but managing complexity across multiple sites increased operational risk and capital requirements.

Our goal is now to create the world's most valuable pigment company with great financial strength and profitability. This ambition, stated at acquisition announcement, would be tested by harsh realities. Creating value required more than financial engineering—it demanded operational excellence, innovation leadership, and cultural transformation.

The lessons from Sudarshan's journey offered insights for other emerging market companies harboring global ambitions. First, patient capital and conservative financial management created optionality when opportunities arose. Second, technical capability and customer relationships mattered more than cost advantages in sustainable differentiation. Third, cultural humility and integration patience were essential when acquiring developed market assets.

But perhaps the most important lesson was about timing and courage. The Rathi family's decision to acquire Heubach wasn't made in a boardroom spreadsheet—it was the culmination of decades of preparation, learning, and relationship building. When the moment arrived, they had the confidence to act decisively despite the risks.

The story of Sudarshan Chemical Industries ultimately transcends pigments and profits. It's about transformation—of a family business into a professional corporation, of a domestic manufacturer into a global player, of an emerging market company into a potential industry leader. Whether this transformation succeeds will depend not on the past achievements we've chronicled, but on decisions yet to be made, challenges yet to be faced, and opportunities yet to be seized.

As we close this chapter, Sudarshan stands at a crossroads that many emerging market champions face—having achieved the scale to compete globally but not yet the consistent performance to lead. The acquisition of Heubach was a bold bet that emerging market companies could revitalize developed market assets through entrepreneurial energy and strategic focus. Whether this bet pays off will determine not just Sudarshan's future, but provide a template—or a warning—for other ambitious emerging market companies eyeing global leadership.

The pigments industry will continue evolving, shaped by sustainability mandates, technological disruption, and shifting global supply chains. Winners will be those who combine scale with agility, efficiency with innovation, global reach with local responsiveness. Sudarshan has assembled the pieces required for leadership. Now comes the harder task: making them work together to create something greater than their sum.

The Rathi family's journey from post-independence entrepreneurs to global industrialists reflects India's own transformation. But unlike India's story, which continues to unfold across decades, Sudarshan's defining moment is now. The next three years will determine whether the Heubach acquisition was masterstroke or misadventure, whether the company becomes a global champion or a cautionary tale.

In the end, business success comes down to fundamentals that haven't changed since 1951: understanding customers, managing costs, investing wisely, and executing consistently. The scale is different, the complexity greater, but the principles remain. Whether Sudarshan can apply these principles while managing unprecedented transformation will determine if the company's next 75 years are even more remarkable than its first.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube