Steelcast Limited: The Hidden Champion of India's Steel Casting Industry

I. Introduction & Episode Setup

Picture this: A freight train thundering across the American Midwest, carrying thousands of tons of grain from Iowa to Chicago. Beneath each railcar, critical cast steel components—side frames and bolsters—bear the crushing weight and violent forces of momentum. These unglamorous parts, invisible to passengers and shippers alike, represent one of the most demanding engineering challenges in transportation. And increasingly, they carry a stamp that might surprise you: "Made in India."

This is the unlikely story of Steelcast Limited, a company that began in a modest Bhavnagar foundry in 1972 and somehow cracked one of the most fortress-like markets in global manufacturing—the American railroad supply chain. How does a Gujarat-based steel casting company, founded by the late F P Tamboli during India's License Raj era, become a critical supplier to Union Pacific and BNSF Railway? How do you convince the notoriously conservative Association of American Railroads to certify an Indian foundry when Chinese competitors with decades of experience struggle to meet the same standards?

The answer reveals a masterclass in patient capability building, strategic certification accumulation, and the compounding power of technical excellence. Steelcast's journey from partnership firm to Rs. 2,230.65 Cr market cap company isn't just another emerging market success story—it's a blueprint for how industrial companies from developing nations can systematically work their way into the most demanding global supply chains.

What makes this particularly fascinating is the timing. Steelcast didn't ride the IT services wave that made Indian companies household names in Silicon Valley. They didn't benefit from the telecom revolution or the consumer internet boom. Instead, they chose perhaps the hardest path: competing in heavy manufacturing against established players from China, Russia, and Eastern Europe, in markets where a single component failure could derail trains and destroy reputations.

The company's transformation accelerated dramatically in recent years. Over the past 6 months, the Steelcast share price has increased by 35.35% and in the last one year, it has increased by 65.74%. But these numbers only hint at the deeper story—one of methodical capability building, strategic patience, and the courage to invest in certifications and quality systems years before they would pay dividends.

As we'll see, every major inflection point in Steelcast's history—from the Kurimoto technical collaboration to the game-changing AAR certification in 2012, from the solar power investments to the recent breakthrough in defense exports—represents a deliberate strategic choice to build capabilities before markets were ready to reward them. It's a playbook that challenges conventional wisdom about how emerging market companies should compete globally.

II. Founding Story & Early Years (1960–1980s)

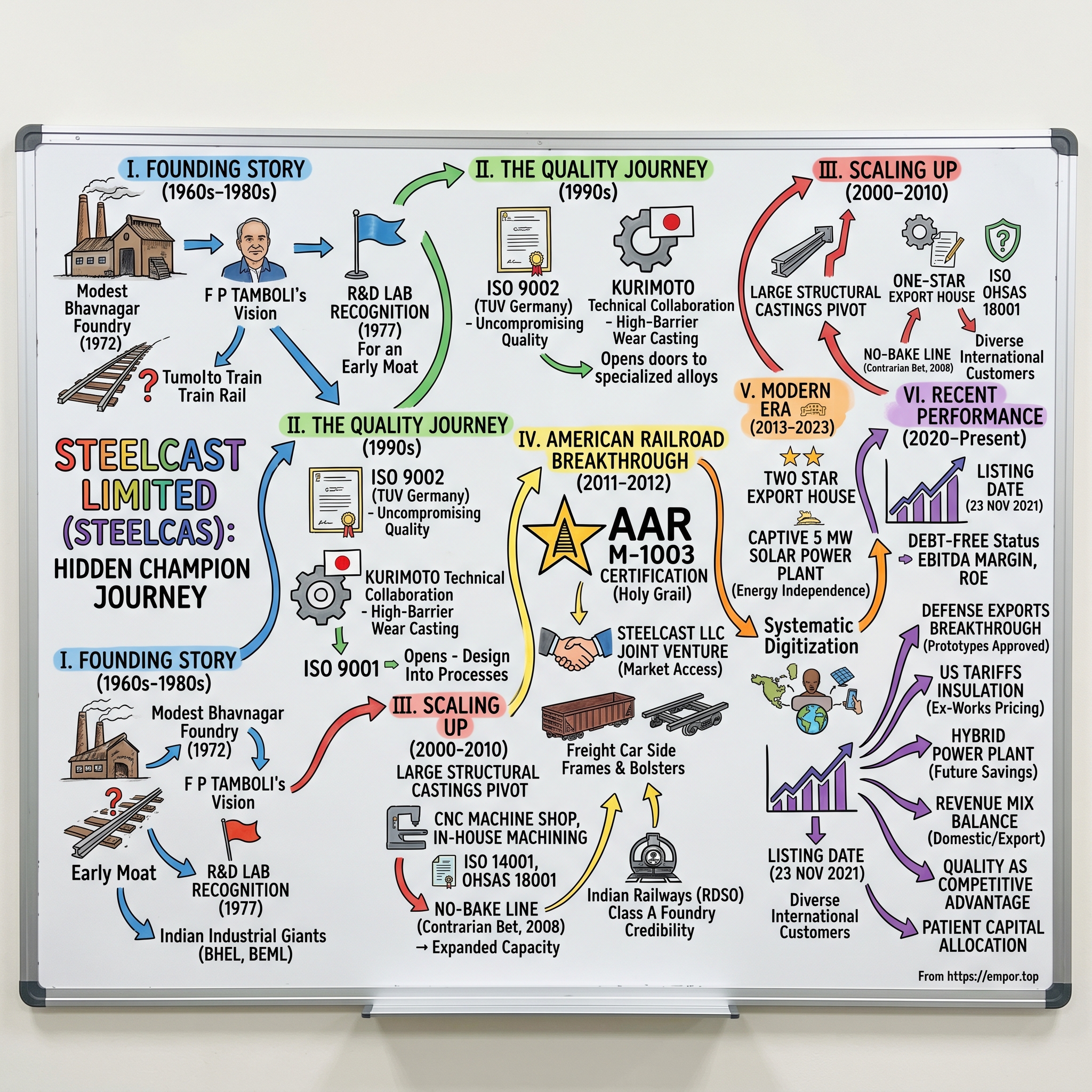

The year was 1960, and India was barely a teenager as an independent nation. In the dusty industrial outskirts of Bhavnagar, Gujarat, a partnership firm quietly came into existence—so modest that its founders probably never imagined it would one day supply components to American locomotives. This was the India of Nehru's Five Year Plans, where private enterprise operated in the shadows of massive state-owned steel plants like Bhilai and Rourkela.

F P Tamboli of Jamnagar had a different vision. While the government poured resources into integrated steel plants, he saw opportunity in the unglamorous world of steel castings—the complex shaped components that form the backbone of industrial machinery. In 1972, twelve years after starting as a partnership, Tamboli transformed the venture into a private limited company, giving it the structure needed for serious industrial ambition.

The timing seemed almost perverse. This was peak License Raj—that byzantine system where you needed government permission to produce, expand, or sometimes even breathe as a business. Getting an industrial license could take years. Importing machinery required navigating foreign exchange controls that would make Kafka weep. Yet Tamboli persisted, perhaps understanding something his contemporaries missed: in a controlled economy, technical excellence could become an unassailable moat.

The breakthrough came in 1977, when the company achieved something remarkable for a small Bhavnagar foundry: Recognition of "Research & Development Laboratory" by the Department of Science & Technology, Government of India. Think about what this meant—while larger competitors focused on production volumes and political connections, this small foundry was investing in R&D capabilities. It was like a neighborhood restaurant getting a Michelin star while everyone else was fighting over location permits.

This early focus on technical capability wasn't abstract philosophy—it translated into concrete customer wins. Through the late 1970s and early 1980s, the company methodically built relationships with India's industrial giants. The customer list read like a who's who of Indian heavy industry: Neyveli Lignite Corporation needed wear-resistant castings for their massive mining operations; Northern Coalfields required components that could withstand the brutal abrasion of coal extraction; cement giants like Kesoram and Raasi needed crusher parts that wouldn't disintegrate under continuous impact.

What's fascinating about this customer roster is what it reveals about Tamboli's strategy. These weren't easy customers—they were technically demanding, quality-obsessed, and had alternatives. BHEL (Bharat Heavy Electricals Limited) and BEML (Bharat Earth Movers Limited) were particularly significant wins. These companies had access to imported components and relationships with established suppliers. Winning their business meant competing on quality, not just price.

The 1980s brought a subtle but important change. Economic liberalization was still a decade away, but cracks were appearing in the License Raj. Forward-thinking industrialists could sense change coming. In December 1988, the company made a seemingly cosmetic but symbolically important move: it renamed itself to 'Steelcast Limited'. The new name was modern, international, and—critically—in English. It signaled ambitions beyond the Gujarat industrial belt.

By the end of the 1980s, Steelcast had established something rare in Indian manufacturing: a reputation for technical excellence backed by genuine R&D capabilities. They weren't the biggest foundry, nor the most politically connected. But when a customer needed a casting that wouldn't fail under extreme conditions—whether in a coal mine, a cement plant, or a power station—Steelcast had quietly become the name they trusted. This foundation of technical credibility would prove invaluable when India's economy finally opened to the world.

III. The Quality Journey: ISO Certifications & Technical Collaboration (1990s)

The year 1991 changed everything. As Dr. Manmohan Singh stood in Parliament announcing the dismantling of the License Raj, boardrooms across India buzzed with equal parts excitement and terror. For Steelcast, liberation meant competition—suddenly, customers could import from anywhere. The protective walls were coming down. The question wasn't whether to compete globally, but how to survive the onslaught.

Steelcast's answer was audacious for its time: if Indian customers could now buy from German foundries, then Steelcast would become German-certified. During 1995-96, Company was certified by the RW TUV, Germany for the Quality Standards ISO 9002. To understand the significance, imagine a small-town boxer suddenly training with Mike Tyson's coach. TÜV wasn't just any certification body—it was the gold standard, the German institution whose stamp meant uncompromising quality.

The certification process itself was transformative. TÜV inspectors didn't just check boxes; they scrutinized every process, questioned every procedure, and demanded documentation that most Indian foundries had never imagined maintaining. Workers who had learned their craft through apprenticeship suddenly had to follow written procedures. Quality control evolved from visual inspection to statistical process control. It was organizational revolution disguised as certification.

But Steelcast didn't stop there. They understood that certification without capability was just expensive paper. The game-changer came through a technical collaboration with Kurimoto, the Japanese engineering giant. This wasn't a typical licensing deal where technology gets transferred and forgotten. Kurimoto brought expertise in super grades of wear and abrasion-resistant ferrous castings—exactly the high-margin, high-barrier products where Chinese competitors struggled.

The Kurimoto collaboration revealed something profound about Japanese industrial philosophy that resonated with Steelcast's DNA. Where American companies might focus on breakthrough innovation, and German firms on engineering precision, the Japanese brought kaizen—continuous, incremental improvement. Every casting became an opportunity to refine the process. Every customer complaint triggered root cause analysis. Slowly, almost imperceptibly, Steelcast's castings began outperforming specifications.

By 1999, the company upgraded to ISO:9001 certification by TUV NORD, Germany (formerly:RWTUV). The progression from ISO 9002 to 9001 might seem like alphabet soup to outsiders, but it represented a fundamental shift from quality control to quality management. ISO 9001 meant Steelcast wasn't just inspecting quality into products—they were designing it into processes.

The impact on customer relationships was immediate and dramatic. Renowned customers include Neyveli Lignite Corporation, Northern Coalfields, Kesoram Cement, NMDC, Raasi Cement, BEML and BHEL. But now these relationships evolved from vendor-buyer transactions to technical partnerships. When Neyveli Lignite faced excessive wear in their bucket teeth, Steelcast's engineers would visit the mines, analyze wear patterns, and develop customized alloys. This wasn't just selling castings—it was solving problems.

The 1990s also saw Steelcast master a critical capability: producing austenitic manganese steel castings. This material, with its unique work-hardening properties, becomes harder under impact—perfect for crusher jaws and grinding components. The metallurgy is notoriously difficult; get the heat treatment wrong, and the casting becomes brittle. Steelcast's ability to consistently produce these castings opened doors to mining and cement customers globally.

What's remarkable about this period is what Steelcast didn't do. They didn't chase volumes in commodity castings. They didn't diversify into unrelated businesses, as was fashionable among Indian conglomerates. They didn't relocate to a metro city or build a glitzy headquarters. Instead, they stayed in Bhavnagar, stayed focused on technical excellence, and kept investing in capabilities that wouldn't pay off for years.

By the decade's end, Steelcast had transformed from a local foundry into an internationally certified manufacturer with Japanese technical collaboration and German quality credentials. They had built what strategists call "credibility capital"—the accumulated trust and certification that would let them knock on doors that remained firmly shut to most emerging market manufacturers. Little did they know that their biggest door—the American railroad industry—was about to crack open.

IV. Scaling Up: Export House Status & Infrastructure (2000–2010)

The new millennium arrived with Y2K fears and dot-com dreams, but in Bhavnagar, Steelcast was focused on something more fundamental: building the infrastructure to compete globally. The company had the certifications and technical knowledge, but competing internationally meant scale, sophistication, and capabilities that no amount of certification could substitute.

The transformation began in 2001 with a strategic pivot toward Large scale development of high integrity structural castings. This wasn't just making bigger castings—it was entering an entirely different league. Structural castings for railways, mining equipment, and industrial machinery require metallurgical precision that makes regular castings look like kindergarten crafts. A side frame for a freight car experiences millions of stress cycles, extreme temperatures, and impact loads that would shatter ordinary steel. One failure could derail a train and end a supplier relationship forever.

By 2004, Steelcast's export momentum earned recognition from the Indian government: Accorded the status of One-Star Export House. This wasn't just a bureaucratic achievement—it came with tangible benefits like priority foreign exchange allocation and simplified export procedures. More importantly, it signaled to international customers that Steelcast was a serious global player, not just another job shop looking for overflow work.

The year 2006 marked an inflection point in Steelcast's capabilities. First came dual certification under ISO:14001 & OHSAS:18001 by TUV NORD, Germany. Environmental and safety certifications might seem like regulatory compliance, but for international customers—especially in Europe and North America—they were table stakes. You couldn't even bid on contracts without them.

More critically, 2006 saw the Commissioning of In-House CNC Machine Shop & Expansion of Shell Moulding facility. This was strategic vertical integration at its finest. Most foundries shipped rough castings to customers, who then machined them to final specifications. By bringing CNC machining in-house, Steelcast could deliver finished components, capture more value, and—crucially—control quality through the entire production process. The shell molding expansion enabled production of complex, thin-walled castings with superior surface finish—exactly what high-end customers demanded.

The infrastructure buildup accelerated in 2007. The Commissioning of State-of-the-Art Induction Hardening facility gave Steelcast the ability to selectively harden wear surfaces while maintaining tough, ductile cores—critical for components like track shoes and grinding media. That same year, Setting up of Plant-3 (Sand Castings) expanded capacity and diversified production capabilities.

Then in 2008, just as the global financial crisis struck, Steelcast made a contrarian bet: Setting up of pilot No-Bake Line. No-bake molding technology—using chemically bonded sand that hardens without heating—was the future of large casting production. While competitors froze capital expenditure as credit markets seized, Steelcast kept building capabilities. It was either prescient or foolish, but definitely brave.

The decade's infrastructure investments reveal a coherent strategy that many missed at the time. Steelcast wasn't randomly adding capacity—they were systematically eliminating every reason a global customer might say no. Can't machine to our specifications? Built a CNC shop. Worried about environmental compliance? Got ISO 14001. Need specialized heat treatment? Installed induction hardening. Each investment removed a barrier to global competition.

What's fascinating is how Steelcast financed this expansion. They didn't dilute equity or take on massive debt. Instead, they plowed back profits, maintained conservative leverage, and grew at a pace they could self-fund. This patient capital allocation would prove crucial when the next opportunity—American railroads—required years of investment before generating returns.

The human dimension of this transformation often gets overlooked. Imagine being a furnace operator in Bhavnagar, trained in traditional sand casting methods passed down through generations, suddenly working with computerized no-bake molding lines. Or quality inspectors moving from visual checks to ultrasonic testing and spectrographic analysis. Steelcast didn't just install machines—they transformed their workforce from craftsmen to precision manufacturers.

By 2010, Steelcast had built something remarkable: a fully integrated, internationally certified, technically sophisticated casting operation in small-town Gujarat. They had 4500 tpa capacity and capabilities spanning austenitic manganese steel, carbon steel, low/high alloy steel and high chromium ferrous alloys. But their biggest breakthrough was about to come from an unexpected direction—a joint venture that would crack open the American market.

V. The American Railroad Breakthrough: AAR Certification (2011–2012)

The email arrived in early 2010, and it might as well have been written in Sanskrit for all the sense it made to outsiders: "Opportunity for AAR M-1003 certification partnership." To Steelcast's management, however, those three letters—AAR—represented the holy grail of the global casting industry. The Association of American Railroads doesn't just set standards; it gatekeeps one of the world's most lucrative and demanding markets for steel castings.

In June 2010, Steelcast Ltd. along with Michigan Steel, USA had formed a 50:50 joint venture company, Steelcast LLC. This wasn't just another joint venture—it was a carefully orchestrated entry strategy into a market where relationships mattered as much as quality. Michigan Steel brought something Steelcast couldn't buy: decades of relationships with American railroads, understanding of AAR's Byzantine certification process, and credibility with purchasing managers who had never heard of Bhavnagar.

The path to AAR certification makes climbing Everest look like a weekend hike. The Association doesn't just test your products—they audit your entire existence. Metallurgical processes, quality systems, testing protocols, worker training, even financial stability. They assume you'll fail and make you prove otherwise. For side frames and bolsters—the critical suspension components that bear the entire weight of loaded freight cars—the standards are unforgiving. A single failure could kill people and trigger lawsuits that would bankrupt a small foundry.

Through 2011, while commissioning their State of Art Automated No-Bake Flaskless Moulding Line, Steelcast simultaneously pursued two critical certifications. First came the Class A Foundry Certification accorded by Indian Railways (RDSO). This might seem like a domestic achievement, but it was strategic positioning. Indian Railways' RDSO certification gave Steelcast credibility in technical discussions with AAR inspectors—proof they could meet rigorous railway standards.

The automated no-bake line wasn't just new equipment—it was a $10 million bet on American railroads before having a single order. The technology enabled production of large, complex castings with dimensional consistency measured in millimeters over components weighing hundreds of kilograms. Every side frame had to be identical, because in railroad operations, interchangeability isn't convenience—it's survival.

Then came the moment that changed everything. In 2012, Steelcast received Accreditation by Association of American Rail Road (AAR) for "Quality Assurance Certification as per M1003" facilitating manufacturing of Side Frame & Bolsters for American Railroad Freight & Locomotive Industry. To put this in perspective, imagine a small Indian software company suddenly getting approved as a core systems vendor for NASA. That's the level of credibility leap we're talking about.

The certification immediately repositioned Steelcast in the global supply chain. India exports of side frames and bolsters into North America represent 15-18% of assignable imports, and Steelcast had just become one of the few Indian companies qualified to participate. They weren't competing against Indian foundries anymore—they were up against established suppliers from China, Russia, and Eastern Europe who had been serving American railroads for decades.

What made Steelcast's entry particularly strategic was timing. American railroads were recovering from the 2008 financial crisis and facing a capacity squeeze as oil-by-rail shipments exploded with the shale boom. They needed suppliers, but not just any suppliers—ones who could meet AAR standards, deliver consistently, and scale production quickly. Chinese suppliers, despite their cost advantages, were struggling with quality issues and intellectual property concerns. Russian suppliers faced geopolitical complications. Steelcast offered a compelling alternative: Indian cost structures, Western quality standards, and English-language business ease.

The technical challenges of serving American railroads went beyond just meeting specifications. Railroad components operate in conditions that test the limits of metallurgy—from -40°F Minnesota winters to 120°F Arizona summers, carrying loads that can exceed 286,000 pounds per car. The steel needs to be tough enough to absorb impact without cracking, yet hard enough to resist wear over millions of miles. Steelcast's years of developing specialized alloys for mining and cement industries suddenly became invaluable.

But perhaps the most underappreciated aspect of the AAR breakthrough was the psychological transformation it triggered within Steelcast. Employees who had been making castings for Indian coal mines were suddenly producing components for Union Pacific and BNSF. Quality control evolved from important to existential. Every casting carried not just Steelcast's reputation but India's industrial credibility. The pride and pressure transformed the company culture in ways no management consultant could have engineered.

The American railroad breakthrough also validated Steelcast's patient capability-building strategy. Every certification, every technical collaboration, every infrastructure investment over the previous two decades had been building toward this moment. When the opportunity arrived, Steelcast was ready—not because they were lucky, but because they had been preparing for a door they didn't even know would open. The AAR certification wasn't the end of Steelcast's transformation—it was the beginning of their emergence as a global player.

VI. Modern Era: Solar Power & Export Growth (2013–2023)

The years following AAR certification should have been smooth sailing for Steelcast. They had cracked the American market, built world-class capabilities, and established a profitable niche. Most companies would have coasted. Steelcast did the opposite—they accelerated their transformation with moves that seemed puzzling at the time but proved prescient in hindsight.

The first signal of enhanced ambition came with their elevation to Two Star Export House from Directorate General of Foreign Trade. This wasn't just bureaucratic recognition—it reflected a fundamental shift in Steelcast's revenue mix. The company had architected a careful balance: domestic sales provided stable base demand while exports drove growth and better margins. When American railroads slowed orders, Indian mining companies picked up slack. When domestic cement industry struggled, international contracts cushioned the blow.

But the boldest move came in renewable energy. The Company has commissioned its 5 MW Solar Power Plant in Umrala Taluka of Bhavnagar District in Gujarat for captive use effective from March 30, 2023. On the surface, a foundry investing in solar power seems like ESG virtue signaling. The reality was hard-nosed economics. Foundries are energy gluttons—electric arc furnaces, induction heating, CNC machines running 24/7. Energy costs could swing quarterly profitability more than steel prices.

The solar investment revealed sophisticated thinking about competitive advantage. While competitors remained hostage to grid electricity prices and availability, Steelcast was building energy independence. In a business where margins often came down to single digits, saving 2-3% on energy costs could mean the difference between winning and losing international contracts. The solar plant wasn't just reducing carbon footprint—it was creating a structural cost advantage that competitors couldn't easily replicate.

The manufacturing capabilities by this period had evolved into something remarkable. With 4500 tpa capacity, Steelcast wasn't the largest foundry, but they might have been the most versatile. Their product range—austenitic manganese steel, carbon steel, low/high alloy steel and high chromium ferrous alloys—read like a metallurgist's wish list. Each alloy category represented years of expertise and customer relationships that new entrants couldn't quickly replicate.

What's fascinating about this period is what didn't happen. Steelcast didn't chase the China+1 narrative that had every manufacturer setting up facilities in Vietnam or Bangladesh. They didn't diversify into unrelated businesses despite sitting on cash. They didn't relocate operations to a special economic zone for tax benefits. Instead, they doubled down on Bhavnagar, on casting expertise, and on serving customers who valued quality over just cost.

The export growth trajectory through this period tells a story of systematic market development. Beyond American railroads, Steelcast was quietly winning customers across European mining companies, Middle Eastern cement plants, and Southeast Asian industrial machinery manufacturers. Each market required different certifications, relationships, and sometimes custom alloys. The company was building what strategists call a "portfolio of options"—multiple growth paths that could be accelerated based on market conditions.

The technological investments continued through this period, though less visible than the solar plant. Simulation software for casting design reduced development time from months to weeks. Automated spectrometers ensured alloy consistency to parts-per-million precision. Real-time monitoring systems tracked every casting through production. This wasn't Industry 4.0 buzzword bingo—it was systematic digitization of processes that had been manual for decades.

The human capital story of this era deserves recognition. Steelcast was creating a cadre of engineers and metallurgists who could hold their own in technical discussions with customers anywhere in the world. Young engineers from regional colleges were being trained on equipment and processes that rivaled facilities in developed countries. The company was proving that manufacturing excellence didn't require Silicon Valley wages or Manhattan addresses—it could thrive in small-town India with the right vision and investment.

COVID-19 tested every assumption about global supply chains, but Steelcast navigated the crisis with remarkable agility. When international logistics collapsed, their domestic business provided ballast. When demand snapped back, their expanded capabilities allowed them to capture more than their fair share. The pandemic proved the wisdom of their balanced domestic-export strategy and conservative financial management.

By 2023, Steelcast had evolved from a certified supplier to a strategic partner for many customers. They weren't just casting metal—they were solving problems, developing new alloys, and sometimes redesigning components for better performance. The company that started as a partnership firm in 1960 had become something far more valuable: a trusted name in global industrial supply chains where trust is earned over decades and lost in moments.

VII. Financial Transformation & Recent Performance (2020–2025)

The morning of November 23, 2021, marked a watershed moment in Steelcast's history. Listing date: 23 Nov, 2021—the company's shares began trading on the National Stock Exchange, transforming a closely-held Bhavnagar foundry into a public company with thousands of shareholders. The IPO wasn't just about raising capital; it was about institutional evolution, transparency, and creating a currency for future growth.

What followed was a stock market performance that made even seasoned investors take notice. Over the past 6 months, the Steelcast share price has increased by 35.35% and in the last one year, it has increased by 65.74%. In a market where manufacturing stocks often trade at single-digit multiples and are ignored for sexier software stories, Steelcast was delivering software-like returns with foundry fundamentals.

The first quarter of fiscal year 2026 provided a glimpse into why investors were bidding up the stock. Steelcast Ltd reported a 53.8% year-on-year rise in net profit to ₹1,988.26 lakh in Q1FY26. This wasn't just revenue growth trickling down—it was margin expansion and operational leverage kicking in. Q1 FY26, achieving a revenue of ₹106.7 crore, The company achieved an EBITDA margin of 28.1%. For context, 28% EBITDA margins in a foundry business are like a marathon runner maintaining sprint speeds—theoretically possible but rarely sustained.

The capital allocation decisions revealed management confidence. The Board declared a first interim dividend of ₹1.80 per equity share of face value ₹5 (36% payout). This wasn't token dividend to keep investors happy—36% payout ratio signaled substantial cash generation while retaining enough for growth investments. Even more boldly, the board announced a Stock split announcement: 1:5 ratio, subject to shareholder approval, making shares more accessible to retail investors and improving liquidity.

But the real story lies in the long-term financial transformation. Over the last 5 years, net income has grown at a yearly rate of 55.35%, vs industry avg of 22.92%. This isn't just beating the industry—it's playing a different game. While peers struggled with commodity cycles and pricing pressure, Steelcast's specialized products and diversified customer base delivered consistent outperformance.

The return metrics tell an even more compelling story. Company has a good return on equity (ROE) track record: 3 Years ROE 29.8%. Nearly 30% ROE in a capital-intensive manufacturing business challenges conventional wisdom about industrial returns. This wasn't financial engineering or leverage gaming—Company has reduced debt. Company is almost debt free. Steelcast was generating these returns through operational excellence and strategic positioning.

The debt-free status deserves particular attention. In an industry where companies routinely leverage 2-3x to fund working capital and capacity expansion, Steelcast chose a different path. They grew at the pace their cash flows could support, avoided the leverage trap that destroyed many manufacturers during downturns, and maintained strategic flexibility to invest countercyclically. When credit markets seized during COVID, Steelcast kept investing. When competitors struggled with debt servicing, Steelcast was paying dividends.

The quarterly progression revealed accelerating momentum. Each quarter wasn't just beating previous numbers—margins were expanding, working capital was turning faster, and customer concentration was declining. The company had reached that virtuous cycle where success breeds success: better margins allowed more R&D investment, which won higher-value customers, which improved margins further.

What's particularly impressive about the financial performance is its quality. This wasn't revenue recognition games or one-time gains. The cash flows were real, converting to actual bank balances that funded dividends and growth investments. The order book was diversified across geographies and industries. The customer relationships were sticky, with multi-year contracts and high switching costs.

The market's revaluation of Steelcast reflected growing institutional understanding of the business model. This wasn't a commodity foundry subject to steel price swings and Chinese dumping. It was a specialized manufacturer with regulatory moats (AAR certification), technical advantages (specialized alloys), and strategic relationships that took decades to build. The market was beginning to price Steelcast less like a foundry and more like an industrial technology company.

Management's recent commentary revealed quiet confidence about the trajectory. They weren't making bold predictions or promising moon shots. Instead, they talked about continuous improvement, customer partnership, and patient capability building—the same philosophy that had driven the company since 1972. The financial transformation wasn't a departure from Steelcast's DNA—it was the ultimate expression of it.

VIII. Current Challenges & Opportunities (2024–Present)

The geopolitical chessboard of 2024 presents Steelcast with its most complex strategic environment yet. The specter of renewed U.S.-China trade tensions looms large, with potential tariffs threatening to reshape global steel casting supply chains. But here's where Steelcast's positioning becomes particularly interesting: All sales, whether domestic or exports, are on an ex-works basis, meaning customers are responsible for any additional tariffs. Therefore, the tariffs do not directly affect Steelcast.

This ex-works arrangement isn't just smart contract structuring—it's strategic insulation. While competitors scramble to absorb tariff impacts or renegotiate contracts, Steelcast watches from the sidelines. More intriguingly, The total duties for Indian products are significantly lower than those for Chinese products, potentially making Steelcast more competitive as American buyers seek alternatives to Chinese suppliers.

But the real excitement comes from an unexpected quarter: defense. Small breakthrough in defense exports, with prototypes approved after field trials. The company expects to ship another lot by September and anticipates scaling up. Defense contracts aren't just another revenue stream—they're a different universe. The margins are higher, contracts are longer, and once you're approved, switching costs create near-permanent relationships. If Steelcast can replicate their railroad success in defense, it opens a market measured in decades, not quarters.

The challenge of delays in railroad component approvals and the impact of U.S. tariffs reveals the double-edged sword of regulatory moats. The same AAR certification process that keeps competitors out also slows new product introductions. Each new component design requires months of testing, field trials, and bureaucratic navigation. It's like having a castle with a moat so wide that even friendly visitors struggle to cross.

Yet Steelcast isn't standing still. The 2.4 megawatt hybrid power plant is expected to be commissioned by March 2026. It will result in annual energy cost savings of 3.5 to 4 crores. This isn't just doubling down on renewable energy—it's building what economists call a "structural cost advantage." When energy represents 15-20% of production costs, saving 4 crores annually drops straight to the bottom line. In a business where contracts are won by 2-3% price differences, this could be the margin of victory.

Mining and earthmoving sector opportunities represent another growth vector as global infrastructure spending accelerates. The beauty of mining sector components is their consumable nature—crusher jaws, grinding balls, and track shoes wear out and need replacement regularly. It's not selling equipment; it's selling razor blades. And with Steelcast's expertise in wear-resistant alloys, they're selling premium razor blades that last longer but command higher prices.

Management remains optimistic about future growth, particularly in the mining, earthmoving, and defense sectors. This optimism isn't based on hope—it's grounded in capabilities already built and relationships already established. The mining sector knows Steelcast from decades of supplying Indian operations. The defense breakthrough proves they can meet military specifications. The earthmoving opportunity leverages the same metallurgical expertise that won railroad contracts.

What makes the current environment particularly favorable for Steelcast is the global push for supply chain resilience. Post-COVID, single-source dependency is corporate suicide. Buyers are actively seeking to diversify suppliers, and India's diplomatic positioning—friendly with both East and West—makes it an attractive alternative. Steelcast isn't just benefiting from India's manufacturing rise; they're helping drive it.

The operational challenges are real but manageable. Skilled labor availability in Bhavnagar isn't what it is in Pune or Chennai. Raw material price volatility requires sophisticated hedging strategies. Technology gaps with Chinese competitors in automation need addressing. But these are execution challenges, not existential threats. Steelcast has navigated the License Raj, survived global financial crises, and thrived through pandemics. Current challenges seem almost quaint by comparison.

The opportunity set has never been richer, but neither has the competition. Chinese foundries are automating aggressively. Vietnamese manufacturers are attracting foreign investment. Even African foundries are emerging as cost competitors. Steelcast's challenge isn't just maintaining position—it's continuing to climb the value chain faster than competitors can catch up. The company that took 50 years to reach the first billion in revenue might need just five years for the next.

IX. Playbook: Business & Strategy Lessons

After six decades of patient building, Steelcast's journey offers a masterclass in how emerging market manufacturers can systematically penetrate global supply chains. The playbook isn't about disruption or blitzscaling—it's about compound improvements that create insurmountable advantages over time.

Building Quality Credentials as Competitive Advantage

Steelcast understood something profound: in industrial markets, quality isn't just a feature—it's the entire product. When a side frame failure can derail a train carrying hazardous materials through a populated area, customers don't shop on price. They shop on trust. Every certification Steelcast accumulated—from ISO 9001 to AAR M-1003—was another layer of trust that competitors couldn't quickly replicate. It's like building a pyramid: each stone makes the next one easier to place, but starting from scratch becomes progressively harder for competitors.

The Power of International Certifications in Emerging Markets

Here's the counterintuitive insight: international certifications matter more for emerging market companies than developed market ones. An American foundry doesn't need German certification to prove competence—their zip code provides presumed credibility. But a foundry from Bhavnagar? They need every stamp, seal, and certificate to get past procurement departments' first filter. Steelcast weaponized this disadvantage, accumulating certifications that became their calling card globally.

Patient Capital Allocation and Infrastructure Building

While peers leveraged up to chase growth, Steelcast grew at the pace their cash flows allowed. This wasn't timidity—it was strategic patience. By staying nearly debt-free, they could invest countercyclically, buying equipment when competitors were selling assets, hiring talent when others were firing, and building capabilities when markets didn't yet value them. The solar power investments exemplify this: spending crores on renewable energy before carbon credits or ESG mandates made it fashionable, simply because the math worked long-term.

Navigating Geopolitical Supply Chain Dynamics

Steelcast's ex-works pricing strategy reveals sophisticated understanding of geopolitical risk. By making customers bear tariff risk, they transformed a vulnerability into competitive advantage. When U.S.-China tensions escalate, Steelcast benefits from tariff differentials without bearing direct exposure. It's judo strategy—using opponents' weight against them. Chinese competitors' scale becomes a liability when tariffs hit, while Steelcast's Indian origin becomes an asset.

Export-Domestic Balance as Risk Mitigation

The balanced portfolio approach—neither fully domestic nor fully export-dependent—created antifragility. Domestic contracts provided steady cash flows and relationships with technically demanding customers. Export contracts brought better margins and foreign exchange. When rupee depreciated, export revenues cushioned the blow. When international markets struggled, domestic demand provided support. This wasn't hedging—it was building a business that could thrive in multiple scenarios.

The Compounding Effect of Technical Collaborations

The Kurimoto collaboration wasn't just technology transfer—it was capability multiplication. Japanese expertise in specialized alloys combined with Indian cost structures created products that neither could produce alone. More importantly, it transformed Steelcast's innovation culture. Engineers trained by Kurimoto went on to develop proprietary alloys. Quality systems implemented for Japanese products elevated standards across all products. Knowledge compounds in ways that financial capital cannot.

Breaking into Fortress Markets

The American railroad market was a fortress—protected by certification requirements, relationship networks, and conservative purchasing practices that favored incumbents. Steelcast's joint venture with Michigan Steel was brilliant tactical execution: they didn't storm the castle, they got invited in. The partnership provided market access while Steelcast provided manufacturing excellence. Once inside, their quality and cost advantages could shine. The lesson: sometimes the best way through a wall is to find someone with a key.

Energy Independence Through Renewable Investments

The solar and hybrid power investments reveal systems thinking about competitive advantage. In commodity manufacturing, you can't control steel prices or customer demand. But you can control your cost structure. By systematically reducing energy costs—one of the largest variable expenses—Steelcast created margins that let them win contracts while maintaining profitability. It's the industrial equivalent of Warren Buffett's float: a structural advantage that compounds over time.

The meta-lesson from Steelcast's playbook is that sustainable competitive advantages in manufacturing don't come from any single factor. They emerge from the interplay of multiple reinforcing elements—technical capability, quality credentials, cost structure, market access, and management patience—that create a system competitors can see but cannot easily replicate. It's not about being the biggest or the first or the cheapest. It's about being the most trusted partner for customers who cannot afford failure.

X. Analysis & Investment Case

The numbers tell a story that would make even growth investors take notice of this industrial stalwart. Over the last 5 years, net income has grown at a yearly rate of 55.35%, vs industry avg of 22.92%. This isn't a software company scaling with zero marginal cost—it's a foundry melting metal and shipping heavy castings. Growing earnings at 55% annually in such a capital-intensive business challenges everything MBA programs teach about industrial economics.

Company has a good return on equity (ROE) track record: 3 Years ROE 29.8%. For context, most foundries celebrate ROE in the mid-teens. Achieving nearly 30% returns while being almost debt free suggests either accounting creativity or exceptional business economics. Given the conservative management style and audited financials, it's clearly the latter.

Competitive Positioning vs Global Peers

Steelcast occupies a unique position in the global casting landscape. Chinese competitors have scale but face tariff headwinds and quality perception issues. Russian suppliers have technical capabilities but geopolitical complications. Eastern European foundries have quality but high cost structures. Steelcast threads the needle: Indian cost advantage, Western quality standards, and geopolitical neutrality that keeps doors open globally.

The company isn't trying to be everything to everyone. They've carved out specific niches—railroad components, mining wear parts, specialized alloys—where technical expertise matters more than pure scale. It's the industrial equivalent of specialty pharmaceuticals versus generic drugs: lower volumes but higher margins and stickier customers.

Moat Analysis

The AAR certification represents a regulatory moat that money alone cannot buy. The certification process takes years, requires extensive testing, and demands proven track records. Even if a competitor started today with unlimited capital, they couldn't supply American railroads for at least 3-5 years. By then, Steelcast would have deepened customer relationships and expanded product offerings.

Customer relationships in industrial supply chains are marriages, not dates. Switching suppliers for critical components requires requalification, testing, and risk that purchasing managers avoid unless absolutely necessary. Steelcast's multi-decade relationships with companies like BHEL and Neyveli Lignite create switching costs measured not in money but in career risk for procurement managers.

The technical expertise in specialized alloys—particularly austenitic manganese steel and high-chromium ferrous alloys—represents accumulated knowledge that can't be hired or bought. It's embedded in processes, recipes, and troubleshooting experience that takes decades to develop. New entrants might match Steelcast's equipment but not their metallurgical instincts.

Risk Factors

Customer concentration remains a concern. While Steelcast has diversified across industries and geographies, large customers like American railroads or Indian mining companies still drive significant revenue chunks. A downturn in railroad traffic or mining activity could impact earnings disproportionately.

Commodity input volatility is structural to the business. Steel, ferrochrome, and ferromanganese prices fluctuate with global supply-demand dynamics beyond Steelcast's control. While they can pass through costs eventually, timing lags can squeeze margins in volatile periods.

The tariff environment remains fluid and unpredictable. While Steelcast's ex-works pricing provides protection, dramatic tariff changes could still affect competitiveness. If Indian products faced punitive tariffs while Chinese competitors found workarounds, Steelcast's positioning advantage could evaporate.

Technological disruption, while slow in foundries, isn't impossible. 3D printing of metal parts is advancing, though still far from competing on cost for large components. Automation advantages that Chinese competitors are building could eventually erode Steelcast's cost advantages. The question isn't if technology will disrupt traditional casting, but when and how fast.

Growth Drivers

The defense sector breakthrough opens a market with fundamentally different economics. Defense contracts offer cost-plus pricing, multi-year commitments, and technical requirements that favor quality over cost. If Steelcast can establish itself as a trusted defense supplier, it could transform the company's margin profile.

Global infrastructure spending, particularly in emerging markets, drives demand for mining and earthmoving equipment. Every mine opened, every road built, every tunnel dug requires wear parts that Steelcast specializes in. The beauty is the replacement cycle—these aren't one-time sales but recurring revenue streams as components wear out.

The energy transition ironically benefits Steelcast. Wind turbines require massive cast components. Electric vehicle production needs specialized castings for motors and battery housings. Solar panel mounting structures use cast components. The infrastructure for renewable energy might reduce fossil fuel demand, but it increases casting demand.

Railroad modernization in India and other emerging markets presents a multi-decade opportunity. As railways upgrade from colonial-era infrastructure, demand for modern, high-performance components explodes. Steelcast's dual positioning—serving both Indian Railways and American railroads—makes them uniquely qualified to capture this demand.

The Investment Thesis

Steelcast represents a rare combination: industrial heritage with technology adaptation, emerging market costs with developed market quality, conservative management with growth ambition. The company has already proven it can compound earnings at software-like rates while maintaining foundry-like stability. The question for investors isn't whether Steelcast is a quality company—that's demonstrable. It's whether the market will continue rerating industrial companies that demonstrate sustainable competitive advantages and secular growth drivers.

The current valuation implies the market is beginning to understand Steelcast's unique positioning but hasn't fully grasped the optionality in defense, renewable energy, and infrastructure spending. For patient investors who appreciate the power of compound growth in unsexy industries, Steelcast offers an interesting proposition: the stability of industrial manufacturing with the growth trajectory of technology companies, wrapped in a conservative balance sheet and proven management team.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube