Star Health: India's Health Insurance Pioneer

I. Introduction & Episode Thesis (8–12 min)

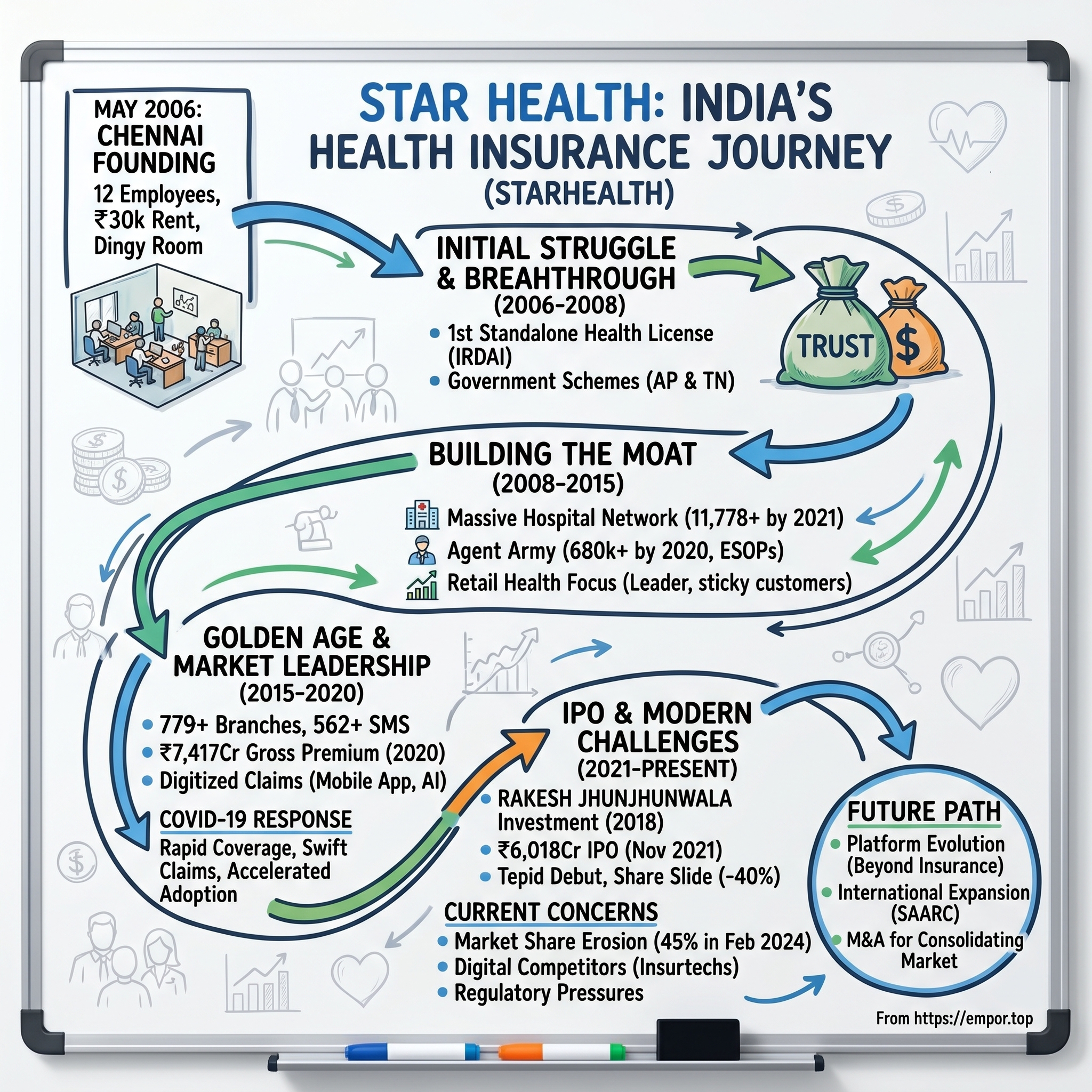

Picture Chennai's steamy morning of May 2006: twelve employees crammed into a dingy room on Madha Church Road, monthly rent of ₹30,000, typewriters leased to save money. In May 2006, when Venkatasamy Jagannathan started Star Health and Allied Insurance Company (Star Health), he and his 12 employees were sitting in a dingy room on Madha Church Road in Chennai with a monthly rent of about Rs 30,000. The air conditioning struggles against the humidity. Outside, the chaos of Indian traffic mirrors the chaos of the health insurance market—fragmented, inefficient, desperately in need of transformation.

Fast forward to today: Star Health stands as India's largest private health insurance company with leadership in the attractive retail health segment. With a market share of 15.8% in the Indian health insurance market in Fiscal 2021, the company has written over ₹15,000 crore in gross premiums and commands a market capitalization hovering around ₹26,000 crore—nearly a thousand-fold increase from that humble beginning.

The central question driving this episode: How did a startup entering India's heavily regulated insurance sector—dominated by government behemoths and multinational giants—become the country's health insurance champion in just 15 years?

The answer lies in a perfect storm of regulatory reform, demographic necessity, and entrepreneurial vision. India in 2006 was a nation where less than 3% of the population had any form of health insurance, where a single hospitalization could bankrupt a middle-class family, and where the concept of standalone health insurance didn't even exist. Star Health didn't just build a company; it created an entire category.

What makes this story particularly remarkable is the context: India's healthcare crisis. With out-of-pocket expenses accounting for over 60% of healthcare spending, the lowest doctor-to-patient ratio among major economies, and a public health system stretched beyond capacity, Star Health's emergence wasn't just a business success—it was addressing a fundamental societal need. This is the story of how one company transformed from a regulatory opportunity into India's insurance champion, and what it means for the future of healthcare in the world's most populous nation.

II. The Indian Insurance Landscape Pre-2006 (30–40 min)

To understand Star Health's emergence, we must first comprehend the byzantine world of Indian insurance before liberalization—a landscape so dominated by government monopoly that the very concept of choice was foreign to consumers.

For nearly five decades, insurance in India meant one thing: government control. Life Insurance Corporation (LIC), established in 1956, held absolute monopoly over life insurance. On the general insurance side, the government nationalized the sector in 1972, creating General Insurance Corporation (GIC) and its four subsidiaries. These monolithic entities moved with the speed of geological time. Claims took months, sometimes years. Customer service was an oxymoron. Innovation was non-existent.

The irony was palpable: in a country where healthcare was largely private and expensive, health insurance was merely an afterthought—a minor add-on to fire and marine policies. GIC's health portfolio contributed less than 10% of premiums. Products were standardized, one-size-fits-all affairs. A 25-year-old software engineer in Bangalore paid the same premium as a 55-year-old factory worker in Bihar. Pre-existing conditions? Forget coverage. Senior citizens? Too risky. The message was clear: health insurance wasn't really for health.

Then came 1999—the year everything changed. The Insurance Regulatory and Development Authority (IRDA) Act opened the sector to private players. But even then, health remained the orphan child. New entrants like ICICI Lombard and HDFC ERGO focused on the profitable motor and fire segments. Health was considered a loss-making proposition, a necessary evil to maintain a "balanced portfolio."

The numbers painted a stark picture of opportunity: India's health insurance penetration stood at a mere 0.36% of GDP, compared to a global average of 2%. Out-of-pocket expenses drove 63 million Indians into poverty annually. Healthcare costs were rising at 15% per year, double the inflation rate. The middle class was expanding—from 50 million in 1995 to 160 million by 2005—creating a demographic desperately seeking financial protection against medical catastrophes.

Yet no one wanted to touch standalone health insurance. The conventional wisdom was unanimous: health insurance in India would always be a loss-maker. Too much fraud, too little data, too many unknowns. The regulatory framework didn't even exist for standalone health insurers.

Founded in 2006, the company carved out a significant space in the competitive insurance market by specializing exclusively in health insurance products, but this specialization was revolutionary precisely because everyone said it couldn't be done. The stage was set for disruption. All it needed was someone crazy enough—or visionary enough—to believe that India's health insurance market wasn't broken; it simply hadn't been built yet.

III. Founding Story & Early Vision (2005–2008) (35–45 min)

Jagannathan started his career at Hercules Insurance Company on June 3, 1970, and became an administrative officer with United India during Nationalisation. In his sure-footed pursuit of success, he slowly climbed up the rungs of the ladder to become CMD of the company one day. It was after his retirement that he joined hands with ETA Star Group to start Star Health.

The founding of Star Health reads like a classic David versus Goliath tale, except David was a 62-year-old insurance veteran who had already conquered one Goliath. Before Star Health, he had scripted a real turnaround saga with state-run United India Insurance Company (United India). When he took over as chairman and managing director (CMD) of United India in 2001, the company was ratcheting up losses of Rs 50 lakh. By the time he retired, United India was profitable, efficient, and had pioneered several government health schemes.

But retirement for Jagannathan was merely an intermission. "In the public sector, we had an established office. Here, I had to start from A to Z. We entered health because I thought the middle-income group needed financial wherewithal," he says. The vision was deceptively simple yet revolutionary: create India's first standalone health insurance company, focused exclusively on health, designed specifically for Indian conditions.

Headquartered in Chennai, began operations in 2006 as India's first standalone Health Insurance provider, but the path to that milestone was anything but smooth. The regulatory framework for standalone health insurers didn't exist until 2005. Jagannathan spent months lobbying regulators, explaining why health needed specialized attention, why the motor insurance model wouldn't work for medical claims.

The founding consortium was eclectic—a mix of financial institutions and strategic investors who saw the long-term potential. The initial capital came together piece by piece, relationship by relationship. In 2007, Star Health obtained its license from the Insurance Regulatory and Development Authority of India (IRDAI)—the first standalone health insurance license ever issued in India.

The early product suite revealed the company's ambition. While others offered basic indemnity products, Star Health launched comprehensive family floaters, senior citizen policies (when everyone else considered them untouchable), and coverage for pre-existing conditions after waiting periods. Each product addressed a specific pain point that Jagannathan had observed during his four decades in insurance.

But products alone don't make a company. For the first two years, people looked at the venture with trepidation of failure. However, getting two government health insurance programmes, first in Andhra Pradesh and then in Tamil Nadu, turned out to be a game changer for the company, following which people started reposing trust in Star Health.

The distribution challenge was monumental. Insurance in India was sold, not bought. It required feet on the street, relationships, trust. Jagannathan's approach was characteristically unconventional: Jagannathan recalls how he ensured branch managers were hired from their respective areas and how the founder would field customer calls, often at midnight. This wasn't just customer service; it was building a movement.

The company created a team of doctors to look into every minutiae of every bill. While competitors outsourced claims processing, Star Health built in-house expertise. The message to the market was clear: this wasn't another insurance company that would find reasons to reject claims. This was a health company that happened to be in insurance.

IV. Building the Moat: Distribution & Product Innovation (2008–2015) (45–55 min)

By 2008, Star Health had survived its infancy. Now came the real test: scale. In insurance, distribution isn't just important—it's everything. And Star Health's distribution strategy would become the stuff of legend.

The numbers tell only part of the story. Star Health built one of the largest health insurance hospital networks in India with more than 11,778 hospitals by 2021, but the journey to build this network started with Jagannathan personally visiting hospitals, negotiating cashless treatment agreements one at a time. Each hospital partnership was a small victory, a node in an expanding network that would become Star Health's most formidable moat.

The agent network grew even more dramatically. From a few hundred agents in 2008 to over 680,000 by 2020—Star Health built an army. But this wasn't just about numbers. Jagannathan is credited with starting lunch for Star Health employees and even offering employee stock ownership plans (ESOPS) at the branch manager level, going against the grain of companies restricting ESOPs to senior-level executives only. The message was revolutionary: every agent, every employee was an owner.

Product innovation during this period wasn't about copying Western models—it was about solving uniquely Indian problems. Senior citizens, shunned by every other insurer, found a home at Star Health. The company launched policies covering people up to 75 years old when the industry standard cut-off was 60. Pre-existing conditions, the bane of insurance seekers, were covered after reasonable waiting periods.

The masterstroke was the focus on retail health insurance when everyone else was chasing corporate group policies. Group insurance was easier—one negotiation, thousands of lives covered, predictable claims patterns. But Jagannathan understood something others missed: retail customers were sticky. They stayed longer, recommended others, built the brand. Strong growth for Star Health is attributable to its leadership in retail health segment, which has grown at a CAGR of 33% over FY19-21 and commands the industry's highest market share of 31% in retail health segment (ex. Travel & PA) in FY21.

Technology investments during this period were strategic, not cosmetic. While competitors were building websites, Star Health was digitizing the entire claims process. By 2015, a customer could upload bills through a mobile app and receive claim approvals within hours. This wasn't just efficiency—it was trust at scale.

Competition was intensifying. ICICI Lombard, backed by deep pockets and banking relationships, was growing aggressively. HDFC ERGO leveraged its parent's brand. Newer entrants like Apollo Munich brought hospital partnerships. But Star Health had something none of them could quickly replicate: seven years of health-only claims data, relationships with 400,000 agents who knew nothing but health insurance, and a brand that had become synonymous with health coverage in tier-2 and tier-3 cities.

The 2008-2015 period established Star Health's competitive advantages: massive distribution, specialized products, and operational excellence in health claims. While others treated health as a portfolio addition, Star Health treated it as a calling. The moat wasn't just wide—it was specifically designed for the unique terrain of Indian health insurance.

V. The Growth Years & Market Leadership (2015–2020) (40–50 min)

The period from 2015 to 2020 would prove to be Star Health's golden age—a time when all the foundational work crystallized into undisputed market leadership. But this growth came with its own set of challenges and opportunities, particularly as India itself was transforming.

As of September 30, 2021 the distribution network had grown to 779 health insurance branches spread across 25 states and 5 union territories in India. Its existing branches are also supplemented by an extensive network of over 562 Sales Managers Stations ("SMS"), which are small individual service centres, and over 6,892 in-house sales managers, as of September 30, 2021. But these weren't just numbers on a spreadsheet—each branch represented a beachhead in India's vast geography, from the metropolitan centers of Mumbai and Delhi to the emerging cities of Coimbatore and Vishakhapatnam.

The digital transformation that began earlier now accelerated into high gear. Star Health wasn't just digitizing existing processes—it was reimagining the entire customer journey. Policy issuance that once took days now happened in minutes. Claims that required stacks of paperwork could be filed with a few smartphone photos. The company launched AI-powered claim assessment tools that could flag potential fraud while fast-tracking legitimate claims.

By 2020, Star Health reported a Gross Written Premium (GWP) of approximately ₹7,417.45 crore—a remarkable achievement considering the company had started with virtually nothing just 14 years earlier. But the real story wasn't in the premiums collected; it was in the lives touched. Having covered more than 17 crore lives since inception, Star Health had become an integral part of India's healthcare infrastructure.

The market dynamics were shifting favorably. Government initiatives like Ayushman Bharat were creating health insurance awareness even in rural areas. Rising incomes meant more families could afford coverage. Lifestyle diseases were unfortunately becoming endemic, making health insurance not a luxury but a necessity. Star Health was perfectly positioned to capture this wave.

Then came 2020—and with it, COVID-19.

Initially, the pandemic looked like an existential threat. Would claims skyrocket? Would the business model collapse? But Star Health's response was swift and decisive. The company launched specialized COVID-19 coverage products, offered free coverage to healthcare workers, and most importantly, honored all COVID-related claims without exceptions. While some competitors found technicalities to reject claims, Star Health's message was clear: "We're here when you need us most."

The pandemic paradoxically accelerated adoption. Indians who had postponed buying health insurance for years suddenly understood its importance. Star Health's digital infrastructure, built over years, proved invaluable when physical interactions became impossible. Policies were sold online, claims were settled remotely, and customer service went completely digital almost overnight.

The company's claim settlement track record speaks volumes: over Rs. 30,300 crore in paid claims since inception, with claim settlement ratios consistently above industry averages. This wasn't just operational excellence—it was brand building at its finest. Every settled claim created a evangelist, every smooth experience generated word-of-mouth marketing that no advertisement could buy.

VI. The Investor Story & IPO Drama (2018–2021) (50–60 min)

The transformation of Star Health from a startup to a unicorn is incomplete without understanding the investor saga—a story that features some of the biggest names in Indian and global finance, culminating in one of the most watched IPOs of 2021.

Star Health has raised $783M in funding from investors like ICICI Venture, Apis Partners and WestBridge Capital. But the real inflection point came in 2018. A consortium of Rakesh Jhunjhunwala along with WestBridge Capital has acquired Chennai-based Star Health Insurance. Though the deal amount has not been officially disclosed, reports say it is of Rs 6,500 crore. Rakesh Jhunjhunwala-led consortium outshined ICICI Lombard General Insurance which had placed a bid amount of about Rs 5,800 crore to acquire the Health insurance Company.

The entry of Rakesh Jhunjhunwala—India's own Warren Buffett—wasn't just about capital. It was validation. Rakesh Jhunjhunwala was a promoter of Star Health. He (14.39 per cent or 8.28 crore shares) and his wife Rekha Jhunjhunwala (3.10 per cent or 1.78 crore shares) held 17.49 per cent stake in the firm as of June 2022 quarter, shareholding pattern data show. The Jhunjhunwalas' stake in the insurance firm was worth Rs 7,017.5 crore.

Jhunjhunwala's investment philosophy was simple: bet on India's growth story. And what better way to play that theme than health insurance? In an interview with business news website Moneycontrol, stated that the recently-IPOed Star Health Insurance has a 31 per cent market share in the retail space in India, which is a rarity in the space. He added that he was both optimistic and hopeful about the same and therefore, decided not to sell any shares in the issue.

The road to IPO began in earnest in 2021. The timing seemed perfect—Indian capital markets were booming, retail participation was at all-time highs, and the pandemic had made health insurance a dinner table conversation. IPO of 6,68,82,461 equity shares aggregating up to ₹6,018.68 Crores, priced at ₹900 per share. The IPO raised approximately ₹3,217 crore and received a tremendous response from investors, though the reality was more nuanced.

Star Health IPO opens on November 30, 2021, and closes on December 2, 2021. The shares got listed on BSE, NSE on December 10, 2021. The listing day told a different story. On December 10, 2021, Star Health and Allied Insurance shares made a tepid debut on the stock market by 6 per cent discount to Rs 848.8 per share on the BSE and Rs 845 per share on the NSE as compared to issue price of Rs 900 per share at the upper end.

The lukewarm response was a reality check. Despite the India growth story, despite the market leadership, despite Jhunjhunwala's backing, the market was sending a message: prove your profitability, show sustainable growth, demonstrate that health insurance in India can generate returns.

Post-IPO, the challenges mounted. The stock continued to slide, eventually falling over 40% from its IPO price. Shares of Star Health Insurance have slipped 40.47 per cent from their listing price of Rs 845 on December 10, 2021. They are down 44.11 per cent from their IPO price of Rs 900. The reasons were multiple: intense competition from new-age insurtechs, concerns about claim ratios, questions about the sustainability of the agent-led distribution model in a digital age.

The tragic passing of Rakesh Jhunjhunwala in August 2022 added another layer of uncertainty. Most of the shares in Rakesh Jhunjhunwala's portfolio were trading lower today following his sudden death on Sunday. Aptech Ltd and Star Health fell up to 5 per cent in early trade. The company had lost not just an investor but a champion, someone who could move markets with his conviction.

VII. Business Model Deep Dive (35–45 min)

To truly understand Star Health's trajectory, we must dissect its business model—a complex machinery that transforms uncertainty into predictability, risk into revenue.

At its core, the insurance business model appears simple: collect premiums, invest the float, pay claims, keep the difference. But in health insurance, especially in India, this equation becomes exponentially more complex. Unlike motor insurance where claim sizes are predictable, or life insurance where actuarial tables provide certainty, health insurance operates in a realm of constant variability.

Star Health's premium collection mechanism reveals the first layer of sophistication. The company distributes its health insurance policies primarily through individual agents, which accounted for 78.9% of its GWP in Fiscal 2021. This heavy reliance on agents—while expensive with commission ratios hovering around 15-20%—provides something algorithms can't: trust. In a country where insurance is still seen with suspicion, where claims rejection horror stories circulate on WhatsApp, the agent becomes the human face of assurance.

The investment income component—often overlooked—is crucial. Insurance companies essentially run two businesses: underwriting and investment management. With thousands of crores in float, even a 1% improvement in investment returns can swing profitability dramatically. Star Health's investment portfolio, conservatively managed with focus on government securities and highly-rated corporate bonds, generated returns of 7-8% annually—not spectacular, but steady.

The claims ratio management is where the rubber meets the road. Star Health's claims ratio of around 64-66% might seem high compared to motor insurance (around 75%) but remember: health claims are fundamentally different. Today, it has 400 doctors and is credited with having one of the largest health insurance hospital networks in India, encompassing 13,000 hospitals. These in-house doctors don't just process claims—they negotiate with hospitals, identify unnecessary procedures, and ensure medical necessity without becoming claim rejection machines.

The unit economics tell a fascinating story. For every ₹100 in premium collected:

- ₹64-66 goes to claims

- ₹15-20 goes to agent commissions

- ₹10-12 goes to operational expenses

- ₹5-7 goes to reinsurance

- What's left—if anything—is underwriting profit

Most quarters, there isn't much left. The real profit comes from investment income on the float. This is why scale matters enormously in insurance. The larger your premium base, the larger your float, the more investment income cushions your underwriting losses.

Technology leverage has become increasingly critical. AI in underwriting helps price risk more accurately—a 30-year-old marathon runner pays less than a 30-year-old smoker. Fraud detection algorithms flag suspicious claims patterns—the same MRI being billed multiple times, sudden spikes in claims from specific hospitals. These technologies don't replace human judgment but augment it, making the massive scale manageable.

The network effects in Star Health's model are subtle but powerful. More customers mean more negotiating power with hospitals. More hospitals mean better service for customers. More agents mean deeper penetration. More data means better underwriting. It's a virtuous cycle that took 15 years to build and would take competitors years to replicate.

VIII. Modern Challenges & Digital Transformation (2021–Present) (40–50 min)

The post-IPO era has been Star Health's trial by fire. The company that had dominated through physical distribution and relationship-based selling suddenly found itself in a world where 25-year-olds were buying insurance on apps, where claims were expected to be settled in hours not days, and where digital-native competitors were raising hundreds of millions to "disrupt" the industry.

Market Cap: 26,095 Crore (down -23.7% in 1 year) tells only part of the story. The real challenge is structural. Companies like Acko and Digit Insurance aren't just competitors—they represent a fundamental rethinking of health insurance. No agents, no branches, no paper. Just algorithms, apps, and APIs.

The digital natives' playbook is seductive: eliminate the agent commission (15-20% of premiums), use that saving to offer lower prices or better coverage, acquire customers online at a fraction of traditional cost. In theory, it's brilliant. In practice, it's complicated. Health insurance isn't a commodity purchase like booking a cab or ordering food. It requires explanation, customization, trust—things that Star Health's 700,000 agents provide but apps struggle to replicate.

Star Health's digital transformation hasn't been about abandoning its traditional model but augmenting it. Star Health Q1 FY26: 13% premium growth, 44% PAT rise, digital channel grows 73%, new Chairperson appointed. The 73% growth in digital channels shows the company isn't standing still. The Star Health app now allows everything from policy purchase to claim tracking, but crucially, it's integrated with the agent network. Agents use tablets to sell policies, customers can reach their agents through the app, and claims processing—whether initiated digitally or through agents—follows the same streamlined backend process.

The regulatory environment has added another layer of complexity. IRDAI's standardization efforts, while good for customers, have commoditized basic products. The regulator's push for "insurance for all by 2047" means companies must serve unprofitable segments. The recent caps on commission rates squeeze distribution economics. Insurance Regulatory and Development Authority of India imposed a penalty of ₹3.39 crore and issued a warning to Star Health and Allied Insurance Company for violations under Irdai Information & Cyber Security Guidelines, 2023.

Competition has intensified beyond just insurtechs. In comparison to its competitors in the standalone health insurance industry, Star Health Insurance, the biggest standalone health insurance provider, has seen a considerable drop in market share. By the end of March 2022, Star Health Insurance had about 55% of the market for stand-alone health insurance; but, by March 2023, this percentage had fallen to 49%, and by February 2024, it had further decreased to 45%. Over the previous two years (March 2022-February 2024), this decline reflects an approximately 1,000 basis point (BPS) or 10% reduction in market share.

The market share erosion is particularly concerning because it's happening during a period of industry growth. Aditya Birla Health Insurance increased by 270 bps or 2.7%, Niva Bupa Health Insurance by 355 bps or 3.55%, Care Health Insurance by 260 bps, or 2.6%, and Niva Bupa Health Insurance by 50 BPS or 0.5%. While Star Health remains the largest, the trajectory is worrying.

Technology investments have become a survival necessity, not a competitive advantage. Telemedicine integration, wellness programs, preventive care incentives—every competitor offers these now. The challenge is deeper: how to use technology to fundamentally improve the loss ratio without alienating customers or agents.

With over 15,000 employees managing scale, organizational transformation is equally critical. The company that grew through entrepreneurial branch managers now needs data scientists, product designers, and growth hackers. Culture change at this scale is glacial, but the market won't wait.

IX. Playbook: Lessons for Founders & Investors (25–35 min)

Star Health's journey from a regulatory opportunity to India's largest standalone health insurer offers a masterclass in building in emerging markets. The lessons transcend insurance, applicable to any founder attempting to build in complex, regulated environments.

First-Mover Advantage in Specialized Verticals

Being first isn't always an advantage—unless you're first in a category others don't believe should exist. Star Health didn't compete with existing health insurance; it created standalone health insurance. This wasn't just about timing; it was about vision. While others saw health as a loss-making appendage to profitable lines, Jagannathan saw it as a specialized field requiring dedicated expertise, systems, and culture.

The lesson: In emerging markets, the biggest opportunities often lie not in doing something better but in doing something others believe can't be done profitably.

Building Trust in Low-Trust Markets: The India Challenge

Insurance in India carries historical baggage—decades of claim rejections, fine-print exclusions, and bureaucratic nightmares. Star Health's approach was radical transparency. The founder would field customer calls, often at midnight. This wasn't sustainable at scale, but it set a cultural precedent: we're available, we're accountable, we're human.

Trust compounds slowly but erodes quickly. Every claim settled strengthens the edifice; every rejection—justified or not—weakens it. In markets where word-of-mouth drives purchase decisions, reputation becomes the ultimate moat.

Distribution as Competitive Advantage

In the digital age, betting on 700,000 agents seems anachronistic. But Star Health understood something Silicon Valley often misses: in complex, trust-based purchases, human intermediation isn't friction—it's feature. The agent doesn't just sell; they educate, advocate, and handhold through claims.

The playbook: Build distribution that aligns incentives. Star Health's ESOP program extended to branch managers, making them owners, not employees. When agents prosper from customer retention, not just acquisition, the model becomes self-reinforcing.

Regulatory Navigation: Dancing with the System

Rather than fighting regulation, Star Health shaped it. Jagannathan's credibility from his United India days gave him a seat at the policy table. The company didn't just comply with regulations; it often exceeded them, building buffers that became competitive advantages when regulations eventually tightened.

The lesson for founders: In regulated industries, work with regulators to shape sensible policy. They're not adversaries; they're stakeholders who want the industry to succeed sustainably.

The Power of Focus

Multi-line insurers have diversification benefits—motor profits can subsidize health losses. Star Health had no such luxury. Every rupee lost in health insurance was a rupee lost, period. This constraint became a strength. While competitors could afford inefficiency in health operations, Star Health optimized relentlessly.

Focus forces excellence. When you can't subsidize losses with profits from elsewhere, you must solve the fundamental equation.

Patient Capital: The Long Game

Insurance is a business of decades, not quarters. Policies written today will pay claims years later. Brand built today will generate premiums for generations. Star Health's investors—from early venture capital to Jhunjhunwala—understood this temporal arbitrage.

The playbook: Align capital with timeline. Quarterly earnings pressures and insurance building are fundamentally incompatible. Patient capital isn't just helpful; it's existential.

X. Analysis & Investment Case (25–35 min)

Bull Case: The Demographic Dividend

The bull case for Star Health rests on a simple mathematical reality: Indian health insurance penetration of only 0.36% of GDP in 2019, compared to global average of 2%. This isn't just a gap; it's a chasm representing hundreds of millions of uninsured Indians who will inevitably need coverage.

The demographic tailwinds are undeniable. India's middle class, estimated at 300 million, is projected to reach 580 million by 2030. Rising incomes, increasing health awareness, and growing lifestyle diseases create a perfect storm of demand. COVID-19 has permanently changed the perception of health insurance from "nice to have" to "must have."

Star Health's entrenched position provides enormous advantages. Star Health Insurance's market share was up 22 bps among general insurance companies to 5.26%; while it continued to maintain its leadership in the retail health insurance sector with a 33% market share. In a business where scale drives profitability, where data accumulation improves underwriting, where network effects strengthen over time, the leader's advantage compounds.

The distribution moat remains formidable. While digital natives struggle to acquire customers profitably (customer acquisition costs often exceeding first-year premiums), Star Health's agent network generates organic growth. The Company has further strengthened its distribution network with an addition of 16,000 agents in Q4FY24 and 75,000 agents in FY24, taking the overall number of agents servicing customers to 7,01,000.

Government initiatives provide additional tailwind. Insurance for all by 2047, Ayushman Bharat's awareness creation, GST benefits for health insurance—policy support is unequivocal. As India aspires to universal health coverage, private insurers like Star Health will be essential partners, not competitors, to government schemes.

Bear Case: The Disruption Dilemma

The bear case is equally compelling. Company has a low return on equity of 11.9% over last 3 years. For a market leader in a supposedly high-growth industry, this ROE is disappointing. It suggests structural challenges in the business model that scale alone won't solve.

Competition isn't just intensifying; it's shape-shifting. Insurtech startups backed by billions in venture capital are reimagining the entire value chain. They're not trying to build better insurance companies; they're trying to build technology companies that happen to sell insurance. When Acko raises $255 million or Digit becomes a unicorn, they're not buying market share—they're buying time to disrupt.

The market share erosion is accelerating. Losing 10 percentage points in two years isn't just a blip; it's a trend. New players are cherry-picking profitable segments—young, urban, digital-savvy customers—leaving Star Health with an increasingly adverse risk pool.

Regulatory caps on pricing and commissions squeeze profitability from both ends. You can't charge more, and you can't spend less on distribution. This regulatory compression forces operational excellence, but there are limits to efficiency gains.

The technology transformation required isn't incremental; it's fundamental. Star Health needs to rebuild its technology stack, retrain its workforce, and transform its culture—all while maintaining current operations. It's like changing the engine of a plane mid-flight.

The high claims ratio post-COVID suggests either pricing inadequacy or adverse selection. If health insurance becomes a loss-leading product category—as it is in many developed markets—then Star Health's focused model becomes a liability, not an asset.

The Verdict: Navigating Contradictions

The investment case for Star Health embodies the contradictions of emerging market investing. The opportunity is massive but so are the challenges. The moat is wide but potentially obsolete. The brand is strong but increasingly insufficient.

What's clear is that Star Health stands at an inflection point. The next five years will determine whether it transforms from India's health insurance pioneer to its health platform leader, or whether it becomes a cautionary tale of disruption—the Kodak of Indian insurance.

XI. Future Outlook & Strategic Options (15–20 min)

Star Health's future hinges on its ability to execute a three-dimensional transformation: digital without abandoning physical, growth without sacrificing profitability, and innovation without losing focus.

The Platform Play: Beyond Insurance

The most intriguing strategic option is evolution from insurer to health platform. Star Health sits on a goldmine: health data of millions of Indians, relationships with 14,000 hospitals, and trust of 30 million customers. This positions them uniquely to orchestrate the entire health journey—from prevention to treatment to recovery.

Imagine Star Health launching a WhatsApp-based health assistant that reminds you about medications, schedules preventive check-ups, and provides instant medical consultation. Or a hospital rating system based on actual claim and treatment data. Or a chronic disease management program that reduces claims while improving outcomes. The insurance product becomes just one monetization avenue in a broader health ecosystem.

International Expansion: The SAARC Opportunity

Markets like Bangladesh, Sri Lanka, and Nepal face similar challenges: low insurance penetration, rising healthcare costs, and emerging middle classes. Star Health's playbook—agent-led distribution, localized products, and gradual digital transformation—could translate effectively. The regulatory expertise gained in India, often more complex than neighboring countries, provides an edge.

M&A in a Consolidating Market

With over 30 health insurers and most struggling for profitability, consolidation is inevitable. Star Health's currency—both cash and stock—positions it as a natural acquirer. Acquiring a digital-native player could accelerate technology transformation. Buying a struggling traditional player could provide scale and elimination of a competitor simultaneously.

The Data Monetization Question

Star Health's claims data—properly anonymized and analyzed—could be invaluable for pharmaceutical companies, medical device manufacturers, and public health agencies. Understanding disease patterns, treatment efficacies, and cost trends could generate high-margin revenue streams. But this requires navigating privacy concerns and regulatory boundaries carefully.

Partnerships: The Ecosystem Approach

Rather than building everything internally, Star Health could become the orchestrator of a health ecosystem. Partner with Practo for doctor consultations, PharmEasy for medicine delivery, Cure.fit for wellness programs. The insurance company becomes the financial backbone of a comprehensive health solution.

The Path to Sustainable Profitability

Ultimately, all strategic options must lead to sustainable profitability. This requires: - Improving the loss ratio through better underwriting and fraud prevention - Reducing distribution costs through digital adoption without alienating agents - Increasing customer lifetime value through cross-selling and retention - Generating fee income from value-added services - Optimizing investment returns within regulatory constraints

The challenge is executing all simultaneously while competing with focused attackers on each front.

XII. Epilogue & Key Takeaways (10–15 min)

As we reach the end of Star Health's story—though really, we're perhaps only at the end of its first chapter—several profound lessons emerge about building in emerging markets.

What Star Health Got Right

Timing, above all, was impeccable. Entering the market just as regulations enabled standalone health insurance, just before the Indian middle class exploded, just as healthcare costs started spiraling—this wasn't luck but vision. Jagannathan saw not what the market was but what it would become.

Focus, maintained religiously despite temptations to diversify, created expertise that broader competitors couldn't match. When you process millions of health claims, patterns emerge, expertise accumulates, and competitive advantages compound.

Distribution, built person by person and relationship by relationship, created a moat that technology alone cannot cross. In markets where trust is earned slowly and lost quickly, human networks remain powerful.

The Unfinished Journey

But Star Health's story also reveals the challenges of success. Market leadership attracts competition. Traditional advantages face technological disruption. Regulatory protection becomes regulatory burden. The very factors that enabled ascent now complicate evolution.

The company that pioneered standalone health insurance must now pioneer its digital transformation. The organization that built trust through human touch must now build efficiency through automation. The insurer that focused solely on health must now decide whether to remain an insurer at all or become something larger.

Lessons for Healthcare Startups

For entrepreneurs eyeing healthcare in emerging markets, Star Health offers both inspiration and caution. The opportunity is real—billions lack adequate healthcare financing. The challenges are equally real—regulation, trust deficits, operational complexity, and uncertain profitability.

Success requires patient capital, regulatory engagement, and most importantly, solving real problems for real people. Health insurance isn't a financial product; it's a social contract. Companies that honor this contract through consistent claim settlement, transparent pricing, and genuine care will build institutions that outlast market cycles.

The Insurance Industry Transformation Ahead

Star Health's next decade will be shaped by forces beyond its control: artificial intelligence making underwriting instantaneous, blockchain making claims processing transparent, genomics making risk prediction precise, and telemedicine making healthcare accessible. The question isn't whether these changes will transform insurance but whether incumbent insurers will transform themselves.

Final Thoughts: Building Where It Matters

In Silicon Valley, success is often measured in valuations and exits. Star Health reminds us of a different scorecard. Having covered more than 17 crore lives since inception means 170 million Indians had financial protection during medical crises. Over Rs. 30,300 crore in paid claims means countless families avoided bankruptcy, children received treatment, and elderly parents got care they needed.

This is the ultimate measure of Star Health's success: not the stock price or market share, but lives protected and catastrophes averted. In a country where a medical emergency can destroy generations of progress, Star Health built a safety net, one policy at a time.

The story continues. Whether Star Health remains India's health insurance champion or gets disrupted by the next wave of innovation, it has already secured its place in history. It proved that specialized health insurance could work in India, that private enterprise could address social needs, and that patient building in regulated industries, while difficult, can create enduring value.

For founders, investors, and anyone interested in emerging markets, Star Health's journey offers this final insight: the biggest opportunities lie not in serving the served better, but in serving the unserved at all. In that gap between what exists and what's needed, between regulation and innovation, between tradition and transformation, lie the companies that will define the next era of emerging market capitalism.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube