The Maharaja of Leather: The Stanley Lifestyles Story

I. Introduction & Episode Roadmap

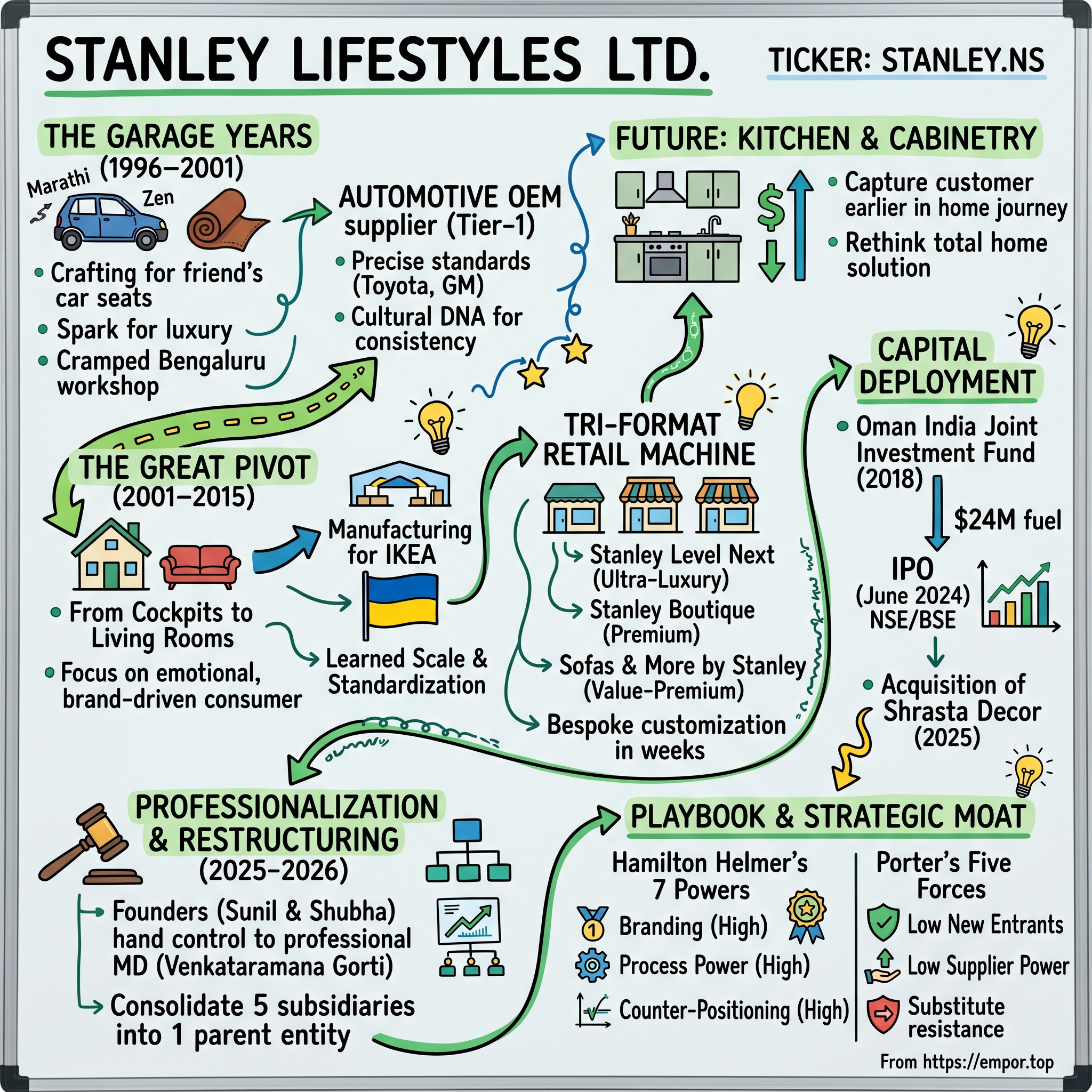

Picture a cramped workshop on Mission Road in Bengaluru in 1996. The air smells of vegetable-tanned hide and machine oil. A young man who has spent his early career stitching premium leather garments for export houses is hunched over the gutted interior of a friend's Maruti Zen — at the time, the little hatchback that signified you had arrived in liberalizing India. He strips out the drab factory upholstery and rebuilds the seats in deep blue leather, hand-finished with contrasting yellow stitching. When the friend sees the result, he is stunned. He pays ₹10,000 for a job that cost roughly ₹2,000 in materials and labor.1

That single car seat was the spark. The young man was Sunil Suresh, and the realization that hit him in that garage would compound for the next thirty years: in a country of a billion-plus people climbing the income ladder, there was a deep, almost emotional hunger for genuine luxury craftsmanship — and almost nobody serving it well. Fast forward to June 2026, and that rented 1,000 square-foot workshop has become Stanley Lifestyles Limited, a publicly listed company on the National Stock Exchange with a national footprint of experience centers, its own multi-lakh-square-foot manufacturing campus, and a brand that wealthy Indians invoke the way an earlier generation invoked imported European furniture.2

Here is the core question this episode wrestles with. India's furniture market is one of the most stubbornly fragmented consumer categories on earth — the overwhelming majority of it runs through the unorganized sector: the neighborhood carpenter who shows up with plywood and a measuring tape and builds a sofa frame in your driveway.11 How do you build a genuine luxury brand on top of that chaos? And how does a homegrown Indian company end up with a luxury retail footprint several times larger than its nearest organized competitor, while staring down the likes of Italy's Natuzzi and France's Roche Bobois on its own soil?

The answer, as it usually is on this show, is not one clever move. It is a chain of them. So here is our roadmap. First, the Garage Era (1996–2001), where car seats and the brutal quality audits of global automakers forged Stanley's industrial DNA. Second, the Great Pivot (2001–2015), the escape from the low-margin automotive supply trap into the Indian living room — with a manufacturing contract from IKEA acting as an unexpected accelerant. Third, the Retail Masterclass, Stanley's unusual three-format showroom machine. Fourth, the Capital Deployment Story — private equity fuel in 2018, the 2024 IPO, and the disciplined buyout of distribution partner Shrasta Decor. Fifth, the Professionalization of 2025–2026, as the founders handed operational control to a global industrial veteran and collapsed a tangle of subsidiaries into one clean entity. And finally, the strategic teardown: Hamilton Helmer's 7 Powers, Porter's Five Forces, and the bull-versus-bear debate with the handful of KPIs that actually matter.

Let's go back to the garage.

II. The Garage Years: Leather, Luxury, and the Maruti Zen

To understand Stanley, you have to understand that it did not begin as a furniture company at all. It began as a leather company that happened to wander into furniture — and that origin is the whole secret.

Sunil Suresh did not come from money or from interior design. He came from the premium leather garment export business, an unglamorous but globally demanding world in which Indian workshops cut and stitched jackets, gloves, and apparel for foreign fashion labels who would reject an entire consignment over a flawed seam or an inconsistent dye lot.1 That apprenticeship mattered more than any business degree, because it taught him two things simultaneously: how to handle hide as a luxury material, and how unforgiving international quality standards really are. In 1996, together with his wife Shubha Sunil, he set up shop in that 1,000 square-foot rented workshop on Mission Road with just three employees.1 Shubha was not a silent spouse-on-the-cap-table; the design sensibility, the obsession with finish and color, the instinct for what an aspirational Indian household actually wanted — that was the other half of the founding partnership, and it would later define the look of the entire brand.

Then came the Zen. The economics of that first reupholstery job — a five-times markup on a humble hatchback's seats — told Sunil something that market research never could. Indians with rising disposable income did not want "good enough." They wanted to feel that they owned something special, and they were willing to pay a startling premium for the feeling. The product was almost beside the point; the emotion was the product. That is a luxury insight, and Sunil had stumbled into it not in a Milan showroom but in a Bengaluru garage.

But a one-off custom car-seat business is a hobby, not a company. What turned it into an industrial operation was timing. Through the late 1990s and early 2000s, India's economic liberalization was pulling the global auto giants into the country. General Motors, Ford, and Toyota were standing up assembly plants and, crucially, hunting for local Tier-1 suppliers who could deliver components to international specification rather than forcing them to import everything. Leather seating was exactly such a component, and Stanley positioned itself as the trusted local vendor.1 Almost overnight, a custom workshop became an automotive OEM supplier.

Here is where the story gets interesting for investors, because what looked like the company's big break was actually its first trap — and Stanley's eventual response to that trap is the entire investment thesis in miniature. Supplying seats to Toyota and General Motors meant submitting to their quality regimes, and those regimes were merciless. A millimeter of misalignment in a stitch line, a hide that varied in thickness, a color that drifted half a shade across a batch — any of it meant rejection of the whole lot. There is a reason Toyota's production discipline is studied in business schools worldwide; being on the receiving end of it as a small Indian supplier was a baptism by fire.

And that is precisely the point. The automotive years gave Stanley something money cannot easily buy: a culture in which repeatable, industrial-grade precision was simply the floor, not the goal. Most furniture companies — certainly most of the carpenters who dominate India's market — treat each piece as a craft object, gloriously inconsistent. Stanley learned to make luxury the way a factory makes engine parts: standardized, audited, defect-tracked, and reproducible at volume. When the company later turned that capability toward sofas, it could promise something almost no luxury furniture maker in India could — that the tenth sofa off the line would be indistinguishable from the first. That manufacturing rigor, internalized in the cockpit-seat years, became the bedrock everything else was built on.

The problem was that the bedrock came attached to a business model Sunil increasingly hated. And so the question that consumed the founders by the turn of the millennium was not "how do we win more auto contracts?" It was "how do we get out?"

III. The Great Pivot: From Cockpits to Living Rooms

Every great consumer company has a moment where the founder looks at a perfectly functional business and decides to walk away from it. For Stanley, that moment came when Sunil Suresh did the math on automotive seating and understood that he had built a beautiful prison.

The B2B automotive supply business is, structurally, a margin desert. The automaker holds all the power: it dictates volumes, dictates price-down schedules year after year, can dual-source you at will, and treats your craftsmanship as an interchangeable commodity line-item. You can be the best leather seat maker in India and still earn thin, fragile margins at the pleasure of a procurement manager in a faraway headquarters. Sunil had felt the squeeze firsthand, and he made a bet that would define the company: walk away from the certainty of OEM volumes and chase the high-margin, emotional, brand-driven consumer market instead. In luxury, the customer pays for feeling, not for cost-plus — and the maker, not the buyer, holds the pricing power.

The pivot did not happen in a single dramatic leap; it happened in deliberate steps. The first leather sofa line rolled out in 1999, taking the same hides and the same automotive-grade construction discipline and pointing them at the living room rather than the dashboard.1 Then, in 2001, came the move that committed the company: Stanley opened its first branded showroom — the original "Stanley Boutique" — in Bengaluru.1 That storefront was a declaration. Stanley was no longer a supplier hiding inside someone else's product; it was a brand that would meet the customer face to face.

To grasp why this was so radical, you have to remember what the choices were for an affluent Indian household in the early 2000s. Option one: import European furniture and absorb punishing customs duties, long shipping lead times, and zero ability to change a dimension or a color to fit your home. Option two: hire the local carpenter, who was affordable and flexible but worked with inferior materials and inconsistent finishing. There was a yawning, unserved gap in the middle — European-grade luxury, made locally, customizable, without the import tax and the half-year wait. Stanley aimed straight at that gap.11

The accelerant arrived between roughly 2011 and 2015, and it came wearing Swedish blue and yellow. Stanley expanded its manufacturing capacity significantly to produce for IKEA.1 Now, IKEA is the philosophical opposite of luxury — it is flat-pack democratization at planetary scale. But manufacturing for IKEA was an extraordinary education. To be an IKEA supplier is to be taught, by one of the most ruthless supply-chain operators in retail history, how to scale production volume while holding standardized quality and cost discipline. It was, in effect, a second apprenticeship — automotive taught Stanley precision, IKEA taught it scale. The contract was also a stamp of approval: if the Swedes trusted your factory, your factory was world-class.

Out of these two apprenticeships, Stanley crystallized the strategic choice that is the heart of the whole company. The easy, capital-light path in Indian luxury furniture was to become a curator — to import beautiful Italian and French pieces and resell them at a markup, owning a showroom but no factory. Plenty of competitors did exactly that. Stanley refused. It chose to own both ends: the factory floor and the retail counter. We will return to the mechanics, but the consequence is worth stating once, plainly: by capturing the manufacturer's margin and the retailer's markup in the same P&L, Stanley unlocked gross margins north of 50% — economics a pure importer-reseller could never touch.4 Management came to call this the "manu-retail" model, and it is the load-bearing wall of everything that follows.

Owning the factory was the foundation. But a factory is just cost until you build the machine that sells what it makes — and Stanley's selling machine was unusually clever.

IV. The Core Engine: Tri-Format Retail & The "Bespoke" Moat

Walk into a Stanley Level Next flagship and the first thing that hits you is the sheer scale of the theater. These are not furniture shops; they are 20,000-plus square-foot experience centers staged like a luxury hotel, where a couple renovating a home can sink into a recliner, run their fingers across European-tanned hide, and spec out an entire residence in an afternoon.[^16] That theater is not decoration. It is the front end of a carefully engineered revenue machine — and that machine is the undisputed heart of the company.

Start with materiality, because it frames everything. Stanley is, at its core, a B2C retail business. Company-owned retail drives the majority of revenue — roughly 57% in FY25 and climbing toward the higher end of the range into FY26 as the store network expands.412 And within that, seating — sofas, recliners, accent chairs — remains the primary margin engine. This is a company that learned to make money on the thing people sit on, and everything else is built around that anchor.

The genuinely clever part is how Stanley segments its market without cannibalizing its own brand. There is an iron law in luxury retail: you cannot sell to the genuinely ultra-wealthy and to the aspirational upper-middle class under the same roof without one of them feeling out of place and the brand losing its meaning to both. Stanley's answer was a three-format architecture, each format a distinct doorway calibrated to a distinct wallet.

At the top sits Stanley Level Next, the ultra-luxury format with ticket sizes that start around ₹5 lakh and climb from there. These are the massive flagship experience centers, the crown jewel of the portfolio, pitched as comprehensive bespoke home solutions rather than as places to buy a couch. This is where Stanley showcases what full vertical integration can do, and it has been the growth leader, expanding revenue in the mid-teens year over year in FY25 and accounting for roughly half of retail sales.4 In the middle sits Stanley Boutique, the original luxury format, with tickets roughly in the ₹3–5 lakh band, focused on premium European-tanned leather furniture and representing something like a quarter to thirty percent of retail. The Boutique format has been undergoing a proactive, brand-led renovation cycle — a deliberate investment in refreshing the older stores that, as we will see, weighs on near-term profit. And at the accessible end sits Sofas & More by Stanley, the super-premium, "value-premium" format with tickets roughly in the ₹1.5–3 lakh range, deliberately omnichannel, designed to bridge the chasm between mass-market imports and full boutique luxury and to capture the customer who is trading up for the first time. It contributes roughly a fifth to a quarter of retail.4

The elegance here is that the three formats let Stanley fish in three different ponds with three different brand promises while sharing one factory, one supply chain, and one set of craftsmen behind the curtain. The upper-middle-class buyer at Sofas & More never feels they are shopping in the same place as the industrialist speccing a Level Next villa — and yet both are feeding the same manufacturing base.

But the format architecture is only the storefront. The real moat is the customization clock. Consider the alternative an affluent Indian buyer faces. Order an ultra-luxury sofa from an imported Italian or French house, and you are typically looking at a three-to-six-month wait, hefty import duties layered onto the price, and — the part that truly stings for a custom home — virtually no ability to alter the dimensions or the color. You get what Milan decided you get, eventually. Stanley flips every one of those variables. Because it manufactures locally in its roughly three-lakh-square-foot Bengaluru campus, it can deliver fully bespoke, European-grade sofas — your sizing, your leather, your finish — in something like four to six weeks rather than four to six months.[^16] Local manufacturing collapses the lead time and erases the import duty; vertical integration makes the customization economically trivial rather than a special-order nightmare.

That combination — equivalent prestige, instant gratification, and true bespoke control — is extraordinarily hard for an importer to answer, because the importer's entire model is built on not having a factory. Stanley's whole company is built on having one. The lead-time advantage is not a marketing claim; it is a structural consequence of where the production happens.

And here is the strategic kicker that sets up the next section. Once you have a customer in a Level Next flagship, treating their entire home as the canvas rather than a single sofa, the natural question becomes: why stop at seating? Why not capture the kitchen too?

V. The Future-Material Hidden Play: Kitchen & Cabinetry

If seating is the story Stanley has already proven, kitchens and wardrobes are the story it is trying to write — and for a long-term investor, this quiet pivot may matter more than anything happening on the sofa floor.

The logic is almost embarrassingly clean once you see it. A customer who walks in for a sofa is a ₹2 lakh customer. A customer who lets Stanley design and build their modular kitchen and wardrobes is a ₹10–15 lakh customer — and, critically, they become that customer earlier in the home-building journey. The kitchen and the wardrobes are among the first things specified in a renovation or a new-home fit-out, long before anyone shops for accent chairs. Capture the kitchen, and you have planted a flag at the very front of the customer's spending cycle, from which you can cross-sell sofas, beds, dining sets, and the rest of the home in the Stanley aesthetic. The kitchen is not just a bigger ticket; it is the entry point that pulls the entire home through the door.

Today this "Kitchen & Cabinetry" or "Full-Home Solutions" segment is still small — a low-to-mid single-digit slice of product revenue, on the order of the mid-single digits.4 But the trajectory is what management is asking investors to watch. The order momentum in modular kitchens and wardrobes has been running hot, with kitchen-and-cabinetry growth in the roughly 20% range and the kitchen share of the incoming order book climbing sharply through FY26 as Stanley leaned into the category.12 When a segment that small is growing that fast off a base of customers who already trust your brand for high-end furniture, the optionality is significant: it is the single most important lever in the forward investment case precisely because it can re-rate the average ticket and deepen the customer relationship at the same time.

It is also where the manu-retail moat compounds. Modular kitchens are an integration-heavy, made-to-measure product — exactly the kind of thing Stanley's vertically integrated, precision-manufacturing DNA is suited to, and exactly the kind of thing that, once installed, locks the customer into the Stanley design language for the whole home. A sofa is easy to swap out. A built-in kitchen is not.

Now, a word on what this section is not about, because it is a useful tell about management discipline. Alongside the home-interiors push, Stanley has dabbled in Stanley Personal — artisanal leather shoes, handbags, and accessories that trade on the same craftsmanship heritage. It is a charming brand extension, and it serves a real if modest purpose: a brand-awareness halo and an affordable entry point that can introduce a younger consumer to the Stanley name years before they can afford a sofa. But it is, candidly, a rounding error in the financials and should be read as exactly that — a lifestyle novelty and marketing touchpoint, not a second engine. The fact that management keeps it small rather than chasing it as a vanity project is, in its own way, reassuring.

The kitchen bet is the growth story. But growth has to be funded, and how Stanley raised and deployed capital — from private equity through the public markets to disciplined M&A — is its own chapter in financial chess.

VI. Capital Deployment: PE Fuel, the IPO, & The Shrasta Decor Benchmark

For its first two decades, Stanley grew on its own cash flow and the founders' nerve. The decision to take outside capital is always a turning point in a founder-led company, and Stanley's first such moment came in 2018.

That year, Stanley brought in its first institutional backer: the Oman India Joint Investment Fund — a sovereign-flavored vehicle jointly sponsored to channel investment between Oman and India. OIJIF injected roughly $24 million, about ₹170 crore at the time, for a stake in the neighborhood of a quarter of the company.[^4]3 For a furniture maker out of Bengaluru, that was validation as much as fuel — a serious institutional investor underwriting the thesis that organized luxury furniture in India was a category worth backing. The capital went toward the national expansion that would build out the experience-center network. Equally important for the eventual public-market story, taking on a sophisticated institutional shareholder forced a degree of governance, reporting, and board discipline that a purely family-run shop can avoid — a maturation that pays off when you later face public investors.

The defining capital-markets moment arrived in June 2024, when Stanley Lifestyles went public. The IPO was priced at ₹369 per share at the top of its band, comprising a fresh issue of ₹200 crore alongside an offer for sale by existing holders, including a partial exit for the early backers.[^3]2 The fresh capital was earmarked for the things a manu-retailer needs to scale: opening more company-owned (COCO) showrooms, upgrading manufacturing machinery, and paying down debt. The market's reception was emphatic — the stock listed at a substantial premium of roughly a third above the issue price on day one, a vote of confidence in the idea that India finally had a homegrown, vertically integrated luxury furniture champion worth owning.4 Stanley had completed the journey from Mission Road garage to the trading screens of the NSE and BSE.

But the most instructive piece of capital allocation came a year later, and it is a small deal that rewards close reading. In August 2025, Stanley moved to clean up its own distribution layer by acquiring the remaining 44.05% stake in Shrasta Decor Private Limited (SDPL), a key distribution partner, for ₹18.15 crore — taking the business to full ownership.5 The headline number is tiny. The discipline behind it is the point.

Run the math. Paying ₹18.15 crore for 44.05% implies a valuation of roughly ₹41 crore for all of Shrasta Decor. Set that against Shrasta's annual turnover, which was in the same ballpark — on the order of ₹41–42 crore — and you find Stanley bought the business at a price-to-sales multiple of roughly one times revenue.5 Now compare that to Stanley's own valuation in the public market, where it traded at a meaningfully higher multiple of sales. In plain terms: Stanley used its more richly valued public currency to buy a related business at a much cheaper private-market multiple. That arithmetic is accretive almost by definition — you are folding in revenue at one times sales into a company the market values at several times that. The deal did three things at once: it captured the distribution margin that was previously leaking to a partner, it removed a related-party relationship that public investors tend to distrust, and it set the table for the broader corporate consolidation that would follow. It was, in short, a small deal that signaled a disciplined capital-allocation mindset — exactly what you want to see from a newly public founder-led company learning to think like a steward of public money.

That clean-up instinct — simplify the structure, align the incentives, present a transparent face to the market — was about to become the dominant theme of the company's next chapter, as the founders prepared to hand the keys to a professional.

VII. The Professionalization & Restructuring Era (2025 – 2026)

There is a moment in the life of every great founder-led company when the founder has to answer the hardest question of all: do I build a job, or do I build an institution? The decision to let go is the decision that separates companies that outlive their founders from companies that don't — and through 2025 and into 2026, Stanley made its choice.

Sunil Suresh recognized that a company straddling national retail, integrated manufacturing, a public listing, and a tangle of subsidiaries had outgrown garage-style family management. So the founders engineered a deliberate, planned transition rather than waiting for a crisis to force one. In early 2026, Sunil stepped back from day-to-day operations, re-designating himself from Chairman & Managing Director to Chairman — moving from running the company to governing it.[^9] The operational baton passed to Venkataramana Gorti, known as Venkat, who was elevated to Managing Director in May 2026.[^9]7

Gorti is a telling hire, and his résumé tells you exactly what Stanley believes its next decade requires. He is a global industrial veteran with more than three decades of leadership experience across some of the most operationally demanding companies in the world — names like ABB, Oracle, GE, and Honeywell appear in his background, spanning industrial automation, enterprise systems, and global manufacturing.7 This is not a luxury-fashion executive brought in to burnish the brand. This is a manufacturing-and-supply-chain heavyweight brought in to do the unglamorous work of industrial discipline: squeezing efficiency out of the factory, hardening the supply chain, tightening the working-capital cycle, and professionalizing execution at scale. The signal is unmistakable. Stanley believes its brand and design are already strong; what it now needs is operational excellence to convert that brand into durable, compounding profit. Handing the company to an industrialist rather than a marketer is a statement about where management thinks the value will be created next.

Crucially, the founders did not cash out and walk away. Sunil and Shubha Sunil retained a controlling combined promoter stake — in the high-fifties percent, around 56–57% — keeping their interests firmly bolted to the public shareholders'.[^11] And in a gesture that markets tend to read closely, Sunil reached into the open market in June 2026 and bought an additional 101,000 shares for roughly ₹1.47 crore, lifting his personal holding during a period when the stock had been consolidating.[^11] Promoter open-market buying is one of the few signals that is hard to fake: a founder spending his own money to add to an already-controlling position, just as he hands operational control to a professional, is putting capital behind his confidence in the transition.

The other half of this chapter is structural, and it is a genuine clean-up. In June 2026, Stanley's board approved a scheme of amalgamation folding five group subsidiaries — Stanley OEM Sofas, Stanley Retail, SANA Lifestyles, Staras Seating, and the now wholly-owned Shrasta Decor — into the listed parent entity.6 To the casual observer this is dry corporate plumbing. To an investor it is meaningful, because that web of subsidiaries had been the source of exactly the kind of related-party-transaction friction that public-market investors penalize. The point was driven home in March 2026, when India's corporate-affairs machinery imposed a penalty on directors of one of those subsidiaries over historical related-party-transaction reporting lapses — a modest financial hit of a few lakh rupees, but a reputational reminder that the old multi-entity structure carried governance baggage.89 Collapsing the subsidiaries into one entity wipes out the inter-company transactions that create that friction, simplifies the balance sheet, and presents public investors with a single, transparent, unified company. It is the corporate-structure equivalent of the Shrasta buyout: simplify, align, clean up.

Taken together, the leadership transition and the consolidation describe a company deliberately shedding its founder-startup skin and putting on the institutional suit it will need to wear as a public company. Whether the new structure and the new manager deliver is the question the moat analysis and the bull-bear debate are built to test.

VIII. Playbook: Durable Business & Investing Lessons

Step back from the chronology and Stanley offers a set of transferable lessons — the kind of durable principles that outlast any single company's stock chart.

Lesson 1: The "manu-retail" moat is the emerging-market luxury cheat code. In a market protected by high import barriers and burdened by an unorganized supply base, the company that owns both the factory and the retail counter captures two margins where rivals capture one. The importer-reseller earns only the retail markup and pays the import duty; the contract manufacturer earns only the factory margin and never touches the customer. Stanley sits in both seats, which is why its gross margins clear 50% and why its lead times embarrass the imports.4 The lesson generalizes: wherever trade barriers and fragmentation coexist, vertical integration is not a cost center — it is the moat.

Lesson 2: Quality control is a culture, and you forge it in the hardest furnace you can find. Stanley did not learn precision by aspiring to it; it learned precision by surviving Toyota and General Motors audits where a millimeter meant rejection. Starting in a B2B arena that punishes every defect builds a rigor that makes consumer-luxury scaling almost easy by comparison. The counterintuitive takeaway for founders: the unglamorous, margin-thin, demanding customer early in your life can be the best teacher you will ever have, precisely because they will not tolerate your mistakes.

Lesson 3: Tiered brand architecture protects equity while capturing volume. You cannot serve the industrialist and the first-time luxury buyer under one banner without diluting the first and intimidating the second. Stanley's three formats — Level Next, Boutique, and Sofas & More — let it span a vast wealth range while keeping each brand promise intact and sharing one manufacturing base. The discipline is in the separation: same factory, different front doors. Done crudely, brand extension destroys value; done with this kind of segmentation, it multiplies the addressable market without cheapening the crown jewel.

Lesson 4: Great founders build institutions, not jobs. The decision to bring in an industrial heavyweight as Managing Director before scale turned messy — rather than clinging to control until something broke — is a masterclass in long-term governance. Pair that with retaining a controlling stake and buying more shares on the way out the operational door, and you get the rare combination markets crave: a founder who lets go of the steering wheel without letting go of the alignment. Succession done proactively is a feature; succession forced by crisis is a wound.

These lessons are the qualitative case. To pressure-test whether they translate into a defensible business, we turn to the two frameworks this show always reaches for.

IX. Strategic Analysis: Hamilton's 7 Powers & Porter's 5 Forces

A good story and a durable business are not the same thing. Let's run Stanley through the analytical machinery and see what actually holds up.

Start with Hamilton Helmer's 7 Powers, the framework that asks not "is this a good company?" but "what specifically stops a competitor from copying it?"

Branding (High). In Indian luxury interiors, "Stanley" has become the aspirational homegrown status symbol — the name an affluent family invokes when they want European-grade furniture without saying "imported." That brand equity is the permission to charge a premium, and it has been built over nearly three decades of consistent craftsmanship. Branding power is real here precisely because luxury is an emotional category where the name on the sofa carries meaning the materials alone cannot.

Process Power (High). This is Stanley's deepest moat. The end-to-end manu-retail workflow — sourcing European hides, custom tanning and marking, precision crafting at automotive-grade tolerances, and shipping bespoke pieces directly through company-owned stores in four-to-six-week lead times — is a complex, tightly coupled system refined over decades.[^16] A local rival cannot replicate it with a checkbook; process power is, by Helmer's definition, the power that resists fast imitation because it is embedded in organization and tacit know-how rather than in any single asset.

Counter-Positioning (High). Stanley is structurally positioned against imported luxury in a way the imports cannot answer without abandoning their own model. Roche Bobois and Natuzzi offer prestige but impose long waits, import duties, and near-zero customization. Stanley offers comparable prestige plus speed plus bespoke control — and the incumbents can't match the speed and customization without building local factories, which would cannibalize their import economics and contradict their global production model. That is textbook counter-positioning: a business model the incumbent cannot copy without damaging its existing business.

Switching Costs (Moderate, and rising). For a single sofa, switching costs are low — a customer can buy their next piece anywhere. But as Stanley pulls customers into Full-Home Solutions, integrating kitchens, wardrobes, and a unified design language across the whole home, the cost of switching climbs. You don't rip out a built-in modular kitchen because you found a cheaper recliner. The kitchen strategy is, among other things, a switching-cost strategy.

Scale Economies (Moderate). Stanley's volume gives it access to large European leather tanneries and procurement terms that boutique studios cannot match. It is not Amazon-scale, but in a fragmented category, even moderate scale in sourcing premium hide is a real edge over the carpenter and the small atelier.

Cornered Resource (Moderate). Stanley has assembled a deep bench of trained in-house artisanal craftsmen — a skilled-labor pool that takes years to build and cannot be hired overnight in a country where this specific blend of leather craft and industrial discipline is scarce.2 That human capital is a genuine, if replicable-over-time, advantage.

Now Porter's Five Forces, the older but complementary lens that asks where the profit pool can leak.

Threat of new entrants: Low-to-Moderate. High brand equity, the multi-year process moat, and the scarcity of skilled craftsmen all slow new players. A well-funded entrant could buy a factory, but it cannot buy thirty years of brand and tacit manufacturing know-how quickly.

Bargaining power of suppliers: Low. This is the quiet payoff of vertical integration. By owning manufacturing, Stanley sidesteps the third-party OEM squeeze that crushed its margins in the automotive years — it is its own supplier for the value-added work, and it sources raw hide from a competitive global tannery base.

Bargaining power of buyers: Moderate. Ultra-luxury buyers are discerning and have the import alternative as leverage. But Stanley's local customization, faster delivery, and after-sale service blunt that power — the buyer's outside option (waiting six months for a non-customizable import) is genuinely worse for most use cases.

Threat of substitutes: Low. The whole premise of the luxury buyer is that they will not substitute down to a mass-market import or a plywood carpenter's job. The emotional premium that Sunil discovered in 1996 is, in effect, substitution resistance.

Intensity of rivalry: Moderate-to-High. The overall furniture market is brutally fragmented and competitive, but the organized luxury slice — the only slice Stanley actually plays in — is thinly populated and Stanley dominates it. Rivalry is fierce at the bottom of the market and sparse at the top, which is exactly where Stanley sits.

Put the two frameworks together and a consistent picture emerges: Stanley's defensibility is real and rooted in process and counter-positioning, but it is not impregnable, and several of its powers are "moderate" rather than "high." That nuance is exactly what the bull and bear case is built to argue over.

X. The Bull vs. Bear Case & KPIs

So where does that leave the investment debate? Let's war-game both sides honestly, because Stanley is genuinely a company where the bull and bear narratives are both coherent.

The Bull Case.

First, the premiumization wave. India is in the middle of a secular housing boom, and the luxury and ultra-luxury end of that boom has been running hottest of all, with record sales of high-end apartments in major metros.11 Every one of those luxury handovers is a furnishing event, and Stanley is the most credible organized brand positioned to capture it. The bull does not need Stanley to take share from carpenters one driveway at a time; they need the organized luxury category to grow, and they need Stanley to remain its default name. The demographic and real-estate tailwinds make that a reasonable base case.

Second, the kitchen-and-cabinetry option. If Full-Home Solutions scales the way the order book suggests it might, it re-rates the entire business — lifting average ticket sizes several-fold, deepening the customer relationship, and raising switching costs all at once.12 This is the optionality the bull is really buying: a proven seating business with a fast-growing, higher-ticket adjacency stapled to it.

Third, operational upside from professionalization. The bull reads the Gorti appointment as a margin catalyst — an industrial operator brought in precisely to optimize the supply chain and shorten the working-capital cycle, converting Stanley's strong brand into structurally better profitability.7

The Bear Case.

First, real estate sensitivity cuts both ways. The same linkage to new-home handovers that powers the bull case is a vulnerability: a large share of furniture demand is tied to property completions, so any cooling in the luxury housing cycle would hit Stanley's order book quickly and directly. Stanley is, in effect, a leveraged play on the Indian luxury-housing cycle, and cycles turn.

Second — and this is the bear's strongest card — the recent financials show what aggressive expansion does to near-term profit. In FY26, Stanley's revenue was roughly flat at around ₹419 crore, but profit after tax collapsed by about 55% to roughly ₹13 crore, down from around ₹29 crore the prior year.10 The cause was deliberate: a wave of new-store openings drove up depreciation, finance costs, and pre-operating expenses well ahead of the revenue those stores will eventually produce.10 The bull calls this "investing for growth." The bear calls it "we'll see" — because the entire thesis now rests on those new stores maturing and same-store sales reaccelerating to justify the spend. If revenue stays flat while the cost base steps up, the margin damage is not an investment; it's just margin damage.

Third, execution risk is unusually concentrated right now. Stanley is simultaneously handing operational control to a newly installed Managing Director, integrating five subsidiaries into one entity, renovating its Boutique fleet, and scaling a new kitchen category — all at once. Each of those is manageable alone; together, in a single window, they are a real test of organizational bandwidth. And the recent regulatory penalty over historical related-party reporting, modest as the rupee figure was, is a reminder that the old structure left loose ends the new structure must now fully tie off.9

The KPIs that actually matter. Cut through the noise and there are three numbers worth tracking, and only three.

The first is same-store sales growth (SSSG) across the company-owned formats. This is the single cleanest read on whether the expensive store expansion is producing real demand or just real depreciation. If SSSG reaccelerates, the FY26 profit dip was an investment; if it stays soft, it was a warning.

The second is the Kitchen & Cabinetry revenue share. This is the direct gauge of the Full-Home Solutions thesis — the optionality that, if it works, re-rates everything. Watch whether that mid-single-digit share climbs steadily toward something material.

The third is operating EBITDA margin. This is the scorecard on professionalization itself. The whole rationale for handing the company to an industrial operator is that he can restore and improve profitability as the expansion matures. The margin line will tell you, quarter by quarter, whether that bet is paying off.

Three numbers — demand, optionality, and profitability — and you can hold the entire Stanley debate in your head.

XI. Epilogue & Surprises

Thirty years separate two images. The first: a young leather craftsman in a rented Bengaluru garage in 1996, reupholstering a friend's Maruti Zen in blue and yellow and being astonished that someone paid him ₹10,000 for it.1 The second: a publicly listed company in June 2026, with annual revenue around ₹419 crore, a national network of experience centers, a professional Managing Director from the world of global industry, and a unified corporate structure built to face public-market scrutiny.106

The surprise, when you trace the whole arc, is that the romantic part of the story — the craftsmanship, the leather, the bespoke artistry — was never actually the part that built the wealth. The craftsmanship was the foundation; plenty of skilled Indian artisans have craftsmanship and remain poor. What Stanley added was the structure: the decision to own the factory and the showroom both, to capture two margins instead of one, to build a brand and a process that an importer cannot copy and a carpenter cannot scale. Sunil Suresh's real insight was not that Indians wanted luxury leather. It was that the wealth in luxury is captured not by the person who makes the beautiful thing, but by the person who controls the path from the factory floor to the customer's living room.

The next decade will test whether that structure holds as the founder steps back, as the kitchen bet scales or stalls, and as the Indian luxury-housing cycle does whatever cycles do. But the lesson is already banked, and it is the one worth carrying out of the garage: in luxury, craftsmanship is the foundation, but vertical integration and retail control are the architecture that actually captures the wealth.

References

-

How Sunil Suresh built Stanley Lifestyles from a garage startup — YourStory, 2024-06-20 ↩↩↩↩↩↩↩↩

-

Stanley Lifestyles Limited — Red Herring Prospectus (RHP), 2024-06 ↩↩↩

-

Stanley Lifestyles raises $24 million from stake sale to Oman firm — Business Standard, 2018-09-03 ↩

-

Stanley Lifestyles Ltd — financials and segment overview — Screener.in ↩↩↩↩↩↩↩

-

Stanley Retail acquires remaining 44.05% stake in Shrasta Decor for ₹18.15 cr — Business Standard, 2025-08-11 ↩↩

-

Stanley Lifestyles approves Scheme of Amalgamation of five subsidiaries — Investing.com, 2026-06-10 ↩↩

-

Stanley Lifestyles elevates Venkataramana Gorti (Venkat) to Managing Director — Business News This Week, 2026-05 ↩↩↩

-

Adjudication order on related-party transaction reporting — Ministry of Corporate Affairs, 2026-03-12 ↩

-

Stanley Lifestyles unit fined by regulator; directors to appeal, parent sees minor impact — Whalesbook, 2026-03-27 ↩↩

-

Stanley Lifestyles Q4 FY26 consolidated results — Business News This Week, 2026 ↩↩↩

-

India Luxury Furniture Market — Size and Competitive Benchmarking — Grand View Research, 2025-12 ↩↩↩

-

Stanley Lifestyles 9M FY26 / Q3 FY26 results and order-book commentary — EquityBulls, 2026 ↩↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube