Stallion India Fluorochemicals: From Gas Debulker to Specialty Chemical Pioneer

I. Introduction & Episode Roadmap

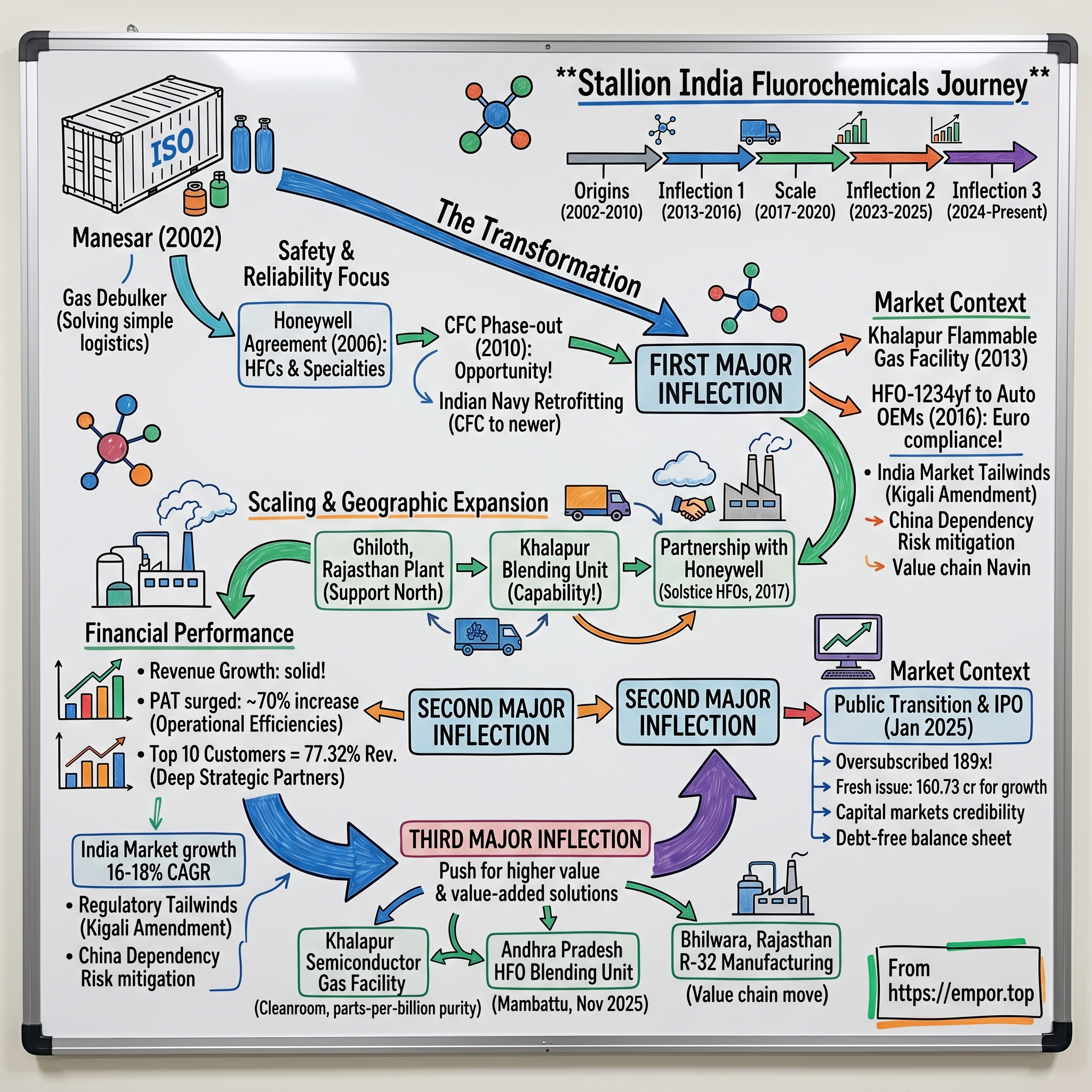

Picture this: A nondescript industrial facility in Manesar, 2002. The air thick with the acrid smell of chemicals, workers in heavy protective gear carefully maneuvering pressurized cylinders. Shazad Sheriar Rustomji, a chemical engineer with over a decade of experience in the refrigerant industry, watches as his team completes their first successful debulking operation—transferring refrigerant gases from massive ISO containers into smaller, more manageable cylinders for local distribution. It's mundane work, unglamorous even. But Rustomji sees something others don't: the beginning of India's transformation from a chemical importer to a sophisticated player in the global fluorochemicals value chain.

Twenty-three years later, that modest operation has evolved into Stallion India Fluorochemicals, a company that commands roughly 10% of India's refrigerant gas market and recently made its stock market debut with an IPO that was oversubscribed 189 times. The journey from gas debulker to specialty chemical pioneer isn't just a corporate success story—it's a masterclass in timing technological transitions, building strategic partnerships while maintaining independence, and capitalizing on regulatory tailwinds that others saw as headwinds. The hook of our story isn't just about market enthusiasm—it's about understanding how a company quietly positioned itself at the intersection of three megatrends: the global phase-out of harmful refrigerants, India's manufacturing renaissance, and the semiconductor revolution. The IPO of Stallion India Fluorochemicals Limited was oversubscribed 188.29 times, but that number only tells part of the story.

What we're really exploring today is how a Mumbai-based debulking operation transformed itself into a critical node in India's specialty chemicals ecosystem, capturing approximately 10% market share in the country's fluorochemicals industry. It's a tale of technical expertise meeting market timing, of regulatory compliance becoming competitive advantage, and of how sometimes the most boring businesses—moving gas from big containers to small ones—can become the foundation for something far more interesting.

This is a company that started by solving a simple logistics problem: how to efficiently distribute refrigerants in India's National Capital Region. Today, it's pioneering the introduction of next-generation HFO refrigerants for automotive OEMs and building semiconductor-grade gas facilities. The journey from there to here involves strategic partnerships with global giants like Honeywell and Daikin, first-mover advantages in emerging technologies, and a founder who saw opportunity where others saw only industrial drudgery.

As we'll see, Stallion's story mirrors India's own industrial evolution—from import dependency to manufacturing sophistication, from serving domestic demand to enabling exports, from basic processing to value-added innovation. It's a playbook for how mid-sized companies can thrive in highly technical, regulated industries by becoming indispensable to both global suppliers and local customers.

II. Origins & Early Foundations (2002–2010)

The year 2002 wasn't exactly an auspicious time to start an industrial gas company in India. The economy was still finding its feet after the dot-com bust, industrial growth was sluggish, and the refrigerant industry was dominated by massive multinationals with decades-old relationships. But Shazad Sheriar Rustomji had spent over a decade watching the inefficiencies in India's refrigerant distribution system, and he believed there was a better way. Rustomji wasn't exactly a newcomer to entrepreneurship—he had begun his career with a seafood export venture during his college years and graduated from Mithibai College in 1988, bringing over 30 years of experience in refrigerants and specialty chemicals. His extensive experience spanned over three decades in the realm of refrigerants and specialty chemicals, marked by steady growth in the early 2000s. He possessed a profound understanding of supply chain logistics, customer requirements, and the entire value chain, establishing himself as a visionary leader who would actively oversee the day-to-day business operations.

The problem Rustomji identified was elegantly simple: refrigerants arrived in India in massive ISO containers—think shipping container-sized tanks holding thousands of kilograms of gas. But end users—whether auto repair shops, appliance manufacturers, or HVAC contractors—needed the gas in manageable cylinders of 10-50 kilograms. Someone had to perform the unglamorous but essential task of "debulking"—transferring the gas from these massive containers into smaller, usable formats. Most companies saw this as a necessary evil, a low-margin logistics function. Rustomji saw it as an opportunity.

On September 5, 2002, Stallion India was incorporated as a private limited company in Mumbai by the Registrar of Companies. The initial setup was modest—a single debulking facility in Manesar, strategically located in the industrial heartland of the National Capital Region. The location wasn't chosen by accident. Manesar sat at the crossroads of North India's industrial belt, close enough to serve Delhi, Gurgaon, and the emerging auto manufacturing hubs, yet far enough to secure affordable land for handling hazardous materials.

The early days were about building credibility in an industry where trust was everything. When you're handling pressurized gases that could explode if mishandled, customers don't just care about price—they care about safety records, technical competence, and reliability. Rustomji focused obsessively on these fundamentals. Every cylinder that left the Manesar facility was meticulously tested, properly labeled, and guaranteed for quality. In an industry where a single accident could destroy a company overnight, Stallion's safety record became its calling card.

By 2006, this attention to detail caught the attention of Honeywell, one of the global giants in specialty chemicals and refrigerants. The partnership that emerged wasn't just a distribution agreement—it was a validation. Honeywell agreed to jointly market and distribute HFCs (hydrofluorocarbons) and refrigerant specialties in India through Stallion. For a four-year-old company, this was transformative. It provided not just products but technical knowledge, global best practices, and most importantly, credibility with large industrial customers. The year 2009 marked a critical juncture for companies like Stallion. India had committed to phasing out CFCs, halons, carbon tetrachloride, and other ozone-depleting substances by January 1, 2010, under the Montreal Protocol, with only pharmaceutical-grade CFCs for asthma inhalers allowed until 2012. This wasn't just a regulatory deadline—it was a massive market disruption. Every piece of refrigeration equipment in the country would need to transition to new refrigerants. For companies that understood the transition, it was a goldmine of opportunity.

Stallion didn't just wait for the market to come to them. In 2009-2010, the company undertook pioneering work with the Indian Navy for CFC retrofitting and HMPE (High Modulus Polyethylene) rope testing. This wasn't glamorous work—it involved crawling through naval vessels, identifying old refrigeration systems, and figuring out how to convert them to use newer, environmentally compliant refrigerants without replacing entire systems. But it gave Stallion something invaluable: deep technical expertise in refrigerant transitions and relationships with government entities that would prove crucial as India's regulatory landscape evolved.

The HMPE rope testing might seem like an odd diversification, but it revealed Rustomji's strategic thinking. The same infrastructure used for handling pressurized gases could be adapted for testing high-performance materials. It was about maximizing asset utilization and building diverse revenue streams—a philosophy that would define Stallion's growth strategy.

By the end of 2010, Stallion had evolved from a simple debulking operation to something more sophisticated. They weren't just moving gas from big containers to small ones anymore—they were becoming technical consultants, helping customers navigate the complex transition from CFCs to HCFCs and HFCs. They understood not just the chemistry but the economics of refrigerant transitions. When a customer needed to retrofit a cold storage facility or convert an industrial chiller, Stallion could provide not just the gas but the expertise.

The company had also mastered the art of "just-in-time" delivery to the NCR region. In a business where inventory carrying costs were high and safety regulations meant you couldn't just store cylinders anywhere, Stallion's ability to deliver exactly what customers needed, when they needed it, became a competitive moat. They turned the unglamorous logistics of gas distribution into a precision operation.

This foundation—technical expertise, regulatory understanding, strategic partnerships, and operational excellence—would prove essential for what came next. Because while the 2010 CFC phase-out was significant, it was just the beginning of a series of technological transitions that would reshape the global refrigerant industry.

III. The First Major Inflection Point: Flammable Gas Facility (2013–2016)

The boardroom at Stallion's Mumbai headquarters in early 2013 must have been tense. Shazad Rustomji was proposing something that, to conservative board members, might have seemed insane: invest millions in a facility specifically designed to handle flammable gases. Not just any facility, but a state-of-the-art plant in Khalapur that could debulk and refill hydrocarbons—gases that could explode if mishandled. The risk wasn't just financial; a single accident could destroy the company's reputation overnight.

But Rustomji saw what others didn't. The refrigerant industry was on the cusp of another massive transition. HFCs, which had replaced CFCs, were themselves coming under scrutiny. While HFCs didn't harm the ozone layer because they contained no chlorine, they were powerful greenhouse gases with global warming potential comparable to CFCs and HCFCs. The writing was on the wall: the industry would need to transition again, this time to refrigerants with lower global warming potential.

The Khalapur facility, strategically located in Maharashtra's Raigad district, wasn't chosen randomly. It sat at the intersection of major industrial corridors, close enough to Mumbai's port for import logistics yet far enough from populated areas to meet safety requirements for handling hazardous materials. The location also provided access to both Western and Southern Indian markets—regions that were experiencing rapid industrial growth.

Setting up a flammable gas facility wasn't just about buying equipment and getting permits. It required a complete rethinking of safety protocols, staff training, and operational procedures. Every valve, every pipe, every storage tank had to be designed with explosion prevention in mind. The company brought in international consultants, sent engineers for training in Japan and Germany, and implemented safety systems that exceeded Indian regulatory requirements.

The investment paid off faster than anyone expected. By 2013, the facility was operational, handling not just traditional HFCs but also hydrocarbon refrigerants and preparing for next-generation HFO (Hydrofluoroolefin) gases. This positioning proved prescient. As global automotive manufacturers began planning for stricter environmental regulations, they needed suppliers who could handle the new generation of refrigerants. The year 2016 represented the moment when Stallion's strategic bet truly paid off. European directive 2006/40/EC, which went into effect in 2011, required that all new car platforms for sale in Europe use a refrigerant in their AC system with a global warming potential (GWP) less than 150 times more potent than carbon dioxide. In accordance with the MAC directive (Directive 2006/40/EC), it had been prohibited to use refrigerants with a GWP higher than 150 in new passenger vehicles' AC systems, with the directive fully implemented in 2017.

This wasn't just a European issue. Indian automakers who exported vehicles to Europe—and that included virtually every major manufacturer—needed to comply with these regulations. They couldn't use traditional R-134a refrigerant (with a GWP of 1430) in vehicles destined for European markets. They needed HFO-1234yf, a next-generation refrigerant with a 100-year GWP lower than 1.

Here's where Stallion's 2013 investment in the Khalapur flammable gas facility became transformative. HFO-1234yf wasn't just another refrigerant—it was flammable, though how much risk this posed was debatable. Handling it required specialized facilities, trained personnel, and sophisticated safety systems. Stallion had all three.

In 2016, the company commenced commercial supplies of HFO-1234yf to automotive OEMs in India, helping them meet European F-gas regulations for their export vehicles. This wasn't just about supplying a product—it was about becoming an essential partner in the automotive industry's global compliance strategy. When Maruti Suzuki or Tata Motors needed to ensure their European-bound vehicles met environmental regulations, Stallion was there with the right product, the right expertise, and the right infrastructure.

The partnership dynamics during this period revealed Stallion's sophisticated positioning. While maintaining its relationship with Honeywell (which marketed HFO-1234yf under the brand name Solstice), Stallion also developed relationships with Daikin Japan and various Indian appliance manufacturers. The company wasn't just a distributor—it was becoming a technical bridge between global chemical giants and local manufacturers. The importance of this development cannot be overstated. India's automobile exports had grown from relatively modest numbers to become significant—the country exported 24% of total vehicles produced as of FY22, with major export destinations including the US, South Africa, Mexico, Bangladesh, the UAE, and increasingly, European markets. These manufacturers needed to comply with increasingly stringent environmental regulations in their export markets. Stallion wasn't just supplying refrigerant—it was enabling India's automotive export ambitions.

The first-mover advantage Stallion secured during this period went beyond just being early. It was about building trust and technical competence when the technology was still new and somewhat controversial. HFO-1234yf's flammability had sparked debates—German automaker Daimler had even conducted tests showing the refrigerant could ignite in simulated collisions. While subsequent studies by regulatory bodies concluded the risks were manageable, handling this refrigerant required suppliers who could navigate both the technical and perception challenges.

Between 2013 and 2016, Stallion also expanded its relationships with Daikin Japan, one of the world's largest fluorocarbon and air conditioning manufacturers. Daikin had developed medium-GWP HFC-32 air conditioners in 2010 and was looking for reliable partners in emerging markets. For Stallion, these partnerships provided access to technical knowledge and global best practices that would be crucial for its next phase of growth.

The company's ability to handle both traditional HFCs and next-generation HFOs from the same facility gave it unique flexibility. When a customer needed traditional R-134a for domestic market vehicles and HFO-1234yf for export models, Stallion could supply both. This "one-stop-shop" capability became increasingly valuable as manufacturers juggled different regulatory requirements across markets.

By the end of 2016, the Khalapur facility had transformed from a risky bet into Stallion's crown jewel. It wasn't just a plant—it was a statement of technical capability, a bridge to global markets, and proof that an Indian company could handle the most advanced and challenging refrigerants in the industry. This foundation would prove essential as Stallion prepared for its next phase of expansion.

IV. Scaling & Geographic Expansion (2017–2020)

The conference room at Honeywell's Gurgaon office in early 2017 buzzed with anticipation. Representatives from Stallion sat across from Honeywell's regional team, finalizing an agreement that would change the trajectory of both companies' presence in the Indian subcontinent. The deal: Stallion would introduce and promote Honeywell's next-generation Solstice HFO refrigerants across India, becoming the primary channel for these advanced materials in one of the world's fastest-growing refrigerant markets.

2017 marked the beginning of Stallion's transformation from a regional player to a company with national ambitions. The partnership to promote Solstice HFO refrigerants wasn't just another distribution agreement—it was Honeywell's vote of confidence in Stallion's technical capabilities and market reach. The timing was perfect. Global automotive manufacturers were scrambling to meet the 2017 deadline for European F-gas regulations, and Indian manufacturers needed a reliable local supplier who could provide both the product and the expertise.

The expansion strategy that unfolded over the next three years was methodical and ambitious. In 2018, Stallion expanded its Khalapur facility to include a second plant specifically for blending refrigerant mixtures. This wasn't just about adding capacity—it was about adding capability. Refrigerant blends were becoming increasingly important as manufacturers sought to optimize performance while meeting environmental regulations. Creating these blends required precise control, sophisticated equipment, and deep understanding of thermodynamic properties.

The blending facility represented a significant technological leap. Unlike simple debulking, which involved transferring gases from large to small containers, blending required mixing different refrigerants in precise proportions to create products with specific properties. A blend might combine the low flammability of one refrigerant with the superior cooling properties of another, creating a product that met both safety and performance requirements. Getting these proportions wrong could result in products that failed to perform or, worse, posed safety risks.

Simultaneously, Stallion was executing a geographic expansion strategy that would fundamentally change its market position. The company started a new plant at Ghiloth in Rajasthan specifically to support the Manesar plant and serve the growing demand in North India. The Ghiloth facility, strategically located in Alwar district, wasn't chosen randomly. It sat at the intersection of major industrial corridors connecting Delhi, Jaipur, and the industrial clusters of Rajasthan. The strategic rationale for multi-location manufacturing was becoming increasingly clear. Rajasthan was emerging as a major industrial hub, particularly for automotive manufacturing. The state had more than 120 automotive and auto component manufacturing units, including India's first Japanese Industrial Zone in Neemrana, which housed companies from Japan and Korea. Bhiwadi and Neemrana were rapidly expanding as industrial areas, with the Delhi-Mumbai Industrial Corridor attracting several Korean and Japanese firms to the region.

For Stallion, the Ghiloth facility wasn't just about serving local demand—it was about being embedded in the automotive manufacturing ecosystem. When a Japanese auto component manufacturer in Neemrana needed refrigerants for testing or a Korean electronics manufacturer required specialty gases for their production processes, Stallion could deliver within hours, not days. This proximity to customers became a significant competitive advantage.

The company's expansion strategy during this period also reflected a sophisticated understanding of supply chain resilience. By having facilities in both Maharashtra (Khalapur) and Rajasthan (Ghiloth and Manesar), Stallion could continue operations even if one facility faced disruptions. This proved prescient—though the company couldn't have predicted it at the time, this distributed manufacturing capability would become crucial during the COVID-19 pandemic just a few years later.

Building distribution capabilities across North and West India required more than just physical infrastructure. Stallion invested heavily in logistics systems, fleet management, and safety protocols. Transporting pressurized, potentially flammable gases across India's varied terrain and climate conditions required specialized vehicles, trained drivers, and sophisticated tracking systems. The company developed a network of authorized distributors and service centers, ensuring that even smaller customers in tier-2 and tier-3 cities could access their products.

The period from 2017 to 2020 also saw Stallion deepen its technical capabilities. The company wasn't just blending gases anymore—it was becoming a solutions provider. When a pharmaceutical company needed ultra-pure gases for their manufacturing processes, Stallion could provide not just the product but also guidance on handling, storage, and quality control. When an HVAC contractor needed help selecting the right refrigerant blend for a specific application, Stallion's technical team could provide recommendations based on performance requirements and regulatory compliance.

By 2020, Stallion had transformed from a regional debulking operation into a company with national reach and ambitions. It operated multiple manufacturing facilities, served customers across diverse industries, and had relationships with global chemical giants. The foundation was set for the next phase of growth—one that would involve accessing capital markets and scaling to an entirely new level.

The timing, as it would turn out, was both challenging and opportune. The COVID-19 pandemic was about to disrupt global supply chains and accelerate certain trends—like the emphasis on domestic manufacturing and supply chain resilience—that would benefit companies like Stallion. But first, the company needed to navigate the immediate crisis while preparing for its most ambitious transformation yet: becoming a publicly traded company.

V. The Second Inflection Point: Public Transition & IPO Journey (2023–2025)

The atmosphere in Stallion's Mumbai headquarters in October 2023 was electric. After more than two decades as a private company, the board had just approved the conversion to a public limited company. For Shazad Rustomji, this wasn't just a corporate milestone—it was the culmination of a vision that had begun in that modest Manesar facility in 2002. The journey from there to here had been remarkable, but what lay ahead would require navigating India's capital markets, satisfying public market investors, and maintaining operational excellence while under unprecedented scrutiny.

The conversion to public limited company status happened in October 2023, marking the beginning of an intensive preparation period for the IPO. But before the company could approach public markets, it needed to clean up its corporate structure. This led to one of the most significant transactions in Stallion's history: the slump sale acquisition of Stallion Enterprises from founder Shazad Rustomji in 2023.

The slump sale was more than a technical restructuring—it was about consolidating all the refrigerant and gas-related operations under one corporate entity. Stallion Enterprises had been operating certain assets and customer relationships that were closely related to the main business. By bringing everything under one roof, the company could present a cleaner story to investors and eliminate any potential related-party transaction concerns that often complicate IPO processes.

The pre-IPO financial performance told a compelling growth story. Revenue grew from ₹22,550.44 lakhs in March 2023 to ₹23,323.58 lakhs in March 2024—solid if not spectacular growth. But the real story was in profitability. PAT (Profit After Tax) surged from ₹975.30 lakhs in March 2023 to ₹1,656.51 lakhs by September 2024, representing a nearly 70% increase in profitability even as revenue grew more modestly. This margin expansion story—driven by operational efficiencies, product mix improvements, and the scaling benefits of multi-location operations—would become central to the IPO pitch.

The decision to go public wasn't taken lightly. For a company that had operated quietly and efficiently for two decades, the transition to public markets meant accepting quarterly scrutiny, regulatory compliance burdens, and the pressure of meeting market expectations. But Rustomji and his team believed the benefits outweighed the costs. Access to capital would enable aggressive expansion plans, particularly in high-growth segments like semiconductor-grade gases. Public listing would enhance the company's credibility with large customers and global partners. And it would provide liquidity to early investors and create wealth-sharing opportunities for employees.

The ₹199.45 crore IPO comprised a fresh issue of 1.79 crore shares amounting to ₹160.73 crores and an offer for sale of 0.43 crore shares valued at ₹38.72 crores. The IPO bidding period ran from January 16, 2025, to January 20, 2025, with the allotment likely to be finalized on Tuesday, January 21, 2025. The IPO was set to list on the BSE and NSE, with the tentative listing date scheduled for Thursday, January 23, 2025.

The IPO preparation process revealed the sophistication Stallion had developed over the years. The company's Red Herring Prospectus wasn't just a regulatory document—it was a comprehensive articulation of India's fluorochemicals opportunity and Stallion's unique position within it. The document highlighted the company's 10% market share in India's fluorochemicals industry, its strategic partnerships with global majors, and its first-mover advantage in next-generation refrigerants.

The roadshow presentations to institutional investors focused on several key themes. First, the structural growth drivers: India's fluorochemicals and specialty gases market was projected to grow at a CAGR of 16-18% from 2024 to 2029, reaching $675-725 million. The global market was expected to expand from $10,963 million in 2024 to $16,223 million in 2028. Second, Stallion's competitive advantages: specialized infrastructure for handling flammable gases, technical expertise built over decades, and strategic locations near major industrial clusters. Third, the expansion opportunity: the upcoming semiconductor and specialty gas facilities that would position the company in higher-margin, faster-growing segments.

Ahead of the IPO, Stallion India Fluorochemicals on Wednesday, 15 January 2025, raised Rs 59.83 crore from anchor investors. The board allotted 66.48 lakh shares at Rs 90 each to 6 anchor investors. The anchor book composition was telling—it included a mix of domestic mutual funds, insurance companies, and foreign institutional investors, signaling broad-based institutional interest in the story.

When the IPO opened for subscription on January 16, 2025, the response exceeded even the most optimistic projections. The public issue saw retail investors subscribing 96.76 times, qualified institutional buyers (QIB) 172.93 times, and non-institutional investors (NII) 422.33 times. By the time the subscription closed, the Rs 199.45 crore offering of Stallion India received bids for 2,92,13,78,295 shares against the 1,55,12,978 shares offered, resulting in an oversubscription of 188.32 times.

The overwhelming response wasn't just about Stallion—it reflected broader market dynamics. Indian capital markets were hungry for manufacturing stories, particularly companies that combined domestic growth with export potential. The specialty chemicals sector had produced several multibagger returns in recent years, and investors were looking for the next winner. Stallion's story—a company at the intersection of environmental regulations, technological transitions, and India's manufacturing ambitions—resonated perfectly.

Market debut day, January 23, 2025, was a moment of validation for the entire Stallion team. Stallion India shares listed at Rs 120 apiece on the BSE, reflecting a premium of Rs 30 or 33.33 per cent against the issue price of Rs 90. Similarly, on the National Stock Exchange (NSE), Stallion India shares listed at Rs 120 apiece, showing a premium of Rs 30 or 33.33 per cent against the issue price. The stock's performance matched grey market expectations, where it had been trading at premiums of Rs 43-48 in the days leading up to the listing.

Post-listing, the company moved quickly to deploy the IPO proceeds. The fresh issue proceeds of ₹160.73 crores were earmarked for specific purposes: capital expenditure for the semiconductor and specialty gas facility at Khalapur, setting up the HFO blending unit at Mambattu in Andhra Pradesh, and meeting working capital requirements. This wasn't speculative capacity addition—it was strategic expansion into segments where Stallion had already identified customer demand and secured initial commitments.

The public listing also brought new dynamics to Stallion's operations. Quarterly earnings calls became platforms for articulating strategy and demonstrating execution. The Q2 FY26 results, announced shortly after listing, showcased the company's momentum: net profit rose 1243.53% to Rs 11.42 crore year-over-year, while sales rose 56.25% to Rs 105.56 crore. For H1 FY26, total revenue increased by 52.8% YoY to Rs 216.30 crore, with PAT rising 135.0% to Rs 21.78 crore.

The transition to public markets also meant greater transparency about customer concentration—a potential concern for investors. The company disclosed that its top 10 customers contributed 77.32% of revenue as of 2024. While this concentration presented risks, it also reflected the deep, strategic nature of Stallion's customer relationships. These weren't transactional buyers but partners who relied on Stallion for critical inputs to their manufacturing processes.

Perhaps most importantly, the IPO success provided Stallion with currency—both literal and figurative—for its next phase of growth. The company could now pursue acquisitions if opportunities arose, attract top talent with stock options, and negotiate with global partners from a position of strength. The "listed company" tag carried weight in discussions with multinational corporations who valued financial transparency and corporate governance standards.

By early 2025, Stallion had successfully navigated one of the most challenging transitions a company can make—from private to public. But this was just the beginning of a new chapter. Armed with capital, credibility, and ambitious expansion plans, the company was ready to tackle its most ambitious goal yet: becoming a significant player in the semiconductor and specialty gas segment.

VI. The Third Inflection Point: Semiconductor & Specialty Gas Push (2024–Present)

The cleanroom at Stallion's upcoming Khalapur semiconductor gas facility represents the apex of the company's technological evolution. Here, in an environment where a single particle of dust could contaminate an entire batch, Stallion is preparing to handle gases with purity levels measured in parts per billion. It's a far cry from the industrial-grade debulking operations of 2002, but the journey from there to here has been remarkably logical—each step building on the last, each capability enabling the next.

The decision to enter semiconductor-grade gases wasn't made in a boardroom—it was pulled by customer demand. As India's semiconductor ambitions crystallized with the announcement of multiple fab projects and the government's $10 billion semiconductor incentive scheme, Stallion's existing customers in electronics and industrial gases began asking: "Can you supply semiconductor-grade gases?" Initially, the answer was no. But Rustomji and his team recognized this as more than a product request—it was an invitation to participate in India's most strategic industrial transformation.

The semiconductor gas facility at Khalapur, currently under construction with deployment of IPO proceeds, represents a quantum leap in technical capability. Semiconductor manufacturing requires gases of extraordinary purity—nitrogen with 99.9999999% purity (nine nines), specialty gases like nitrogen trifluoride (NF3) and tungsten hexafluoride (WF6) that must be handled with extreme precision. Contamination measured in parts per trillion can ruin entire wafer batches worth millions of dollars.

Building this capability required more than equipment—it demanded a fundamental upgrade in human capital and processes. Stallion began recruiting engineers with semiconductor industry experience, sending existing staff for training in Taiwan and South Korea, and implementing quality control systems that exceeded even pharmaceutical-grade standards. The company also initiated discussions with global semiconductor gas suppliers for technology transfer and partnership agreements, leveraging its two-decade relationship history to access cutting-edge knowledge.

Simultaneously, Stallion was executing another strategic expansion: establishing an HFO blending unit at Mambattu in Andhra Pradesh. The location wasn't random—Andhra Pradesh was emerging as a manufacturing hub, particularly for electronics and automotive components. The state government's industrial policies and proximity to Chennai's automotive cluster and Bengaluru's electronics ecosystem made it ideal for serving South Indian markets that Stallion had previously struggled to penetrate from its North and West India bases.

The Mambattu facility, expected to commence commercial operations by November 2025, would have an installed capacity of 7,200 tonnes per annum for refrigerant debulking and blending. But capacity numbers don't tell the full story. This facility was designed with flexibility in mind—able to handle everything from traditional HFCs to next-generation HFOs to specialty industrial gases. It could switch between products based on market demand, seasonal patterns, and customer requirements.

The third major expansion initiative involved R-32 refrigerant gas manufacturing in Bhilwara, Rajasthan. With approximately Rs 120 crore investment, this represented Stallion's first foray into actual refrigerant manufacturing rather than just blending and distribution. R-32, with a GWP of 675 (less than half that of R-410A), was emerging as a preferred refrigerant for air conditioners, particularly in Asian markets. Several major AC manufacturers had already transitioned their product lines to R-32, and demand was expected to surge as older refrigerants were phased out.

The R-32 project revealed Stallion's evolving strategy: moving up the value chain from distribution to blending to manufacturing. Each step required greater capital investment and technical capability but offered higher margins and stronger competitive moats. Manufacturing also reduced dependence on imports—a critical consideration given that Chinese suppliers dominated global refrigerant production and geopolitical tensions were prompting Indian companies to secure domestic supply chains.

The financial results validated this strategy. The 50.30% year-over-year revenue increase wasn't just about selling more of the same products—it was driven by mix improvement, with higher-margin specialty gases and HFOs growing faster than traditional refrigerants. The company's almost debt-free status provided flexibility to fund these expansions through internal accruals and IPO proceeds rather than expensive debt financing.

But success brought new challenges. The China dependency issue loomed large—most raw materials for refrigerant production still came from Chinese suppliers who controlled global supply chains through economies of scale and technological expertise. Stallion's mitigation strategy involved diversifying suppliers, building strategic inventory buffers, and exploring partnerships with non-Chinese suppliers, even if it meant accepting temporarily higher costs.

The competitive landscape was also evolving. Larger players like SRF, Gujarat Fluorochemicals, and Navin Fluorine had noticed the attractive growth and margins in specialty gases and were making their own investments. But Stallion had advantages: nimbleness that large corporations lacked, deep relationships with end-users rather than just distributors, and specialized infrastructure for handling flammable and hazardous gases that would take competitors years to replicate.

Customer testimonials during this period revealed why Stallion was winning despite intense competition. An automotive OEM executive noted: "Others can supply the gas, but Stallion understands our process. When we had contamination issues, their technical team spent three days at our plant identifying the root cause. That's partnership, not just supply." A pharmaceutical company's procurement head observed: "Their multi-location presence means we're never worried about supply disruptions. During the oxygen crisis of COVID-19's second wave, they managed to maintain our specialty gas supplies when others failed. "The semiconductor opportunity for Stallion was crystallizing against the backdrop of India's massive push into chip manufacturing. The Indian government had approved the Semicon India Program with an outlay of over $10 billion, offering fiscal support of up to 50% of project cost for semiconductor fabs. Prime Minister Narendra Modi had recently initiated the construction of three semiconductor plants valued at over $15.1 billion, including Tata Group's collaboration with Taiwan's Power Chip in Gujarat. The country that had historically imported nearly all its semiconductors was positioning itself to become a global manufacturing hub.

For Stallion, this wasn't about building semiconductor fabs—that was a game for conglomerates with tens of billions in capital. Instead, it was about becoming an indispensable supplier to these fabs. A single semiconductor fab could consume millions of dollars worth of specialty gases annually. And unlike traditional refrigerants where price was often the primary consideration, semiconductor manufacturers prioritized quality, reliability, and technical support above all else.

Management's expectation of achieving a CAGR of 30-35% over the next three years wasn't pulled from thin air. It was based on concrete opportunities: confirmed semiconductor fab projects that would need suppliers, the accelerating transition to HFO refrigerants driven by regulatory pressures, and the company's expanding geographic footprint that was opening new customer segments. With technical expertise built over 30 years and an almost debt-free balance sheet, Stallion had both the capability and financial flexibility to capture these opportunities.

The company's approach to the semiconductor opportunity also revealed sophisticated strategic thinking. Rather than trying to supply every gas a semiconductor fab might need—an impossible task given the hundreds of specialty gases used in chip manufacturing—Stallion focused on specific niches where its existing capabilities provided advantages. Nitrogen and other bulk gases where purity, not exotic chemistry, was the key requirement. Specialty cleaning gases where its handling expertise for hazardous materials was valuable. And critically, the logistics and supply chain management that ensured uninterrupted gas supply—a semiconductor fab losing gas supply for even hours could mean millions in losses.

As 2024 progressed into 2025, Stallion was executing on multiple fronts simultaneously. The Khalapur semiconductor gas facility was taking shape, with equipment installation beginning and customer trials planned for late 2025. The Mambattu facility construction was progressing on schedule. The R-32 manufacturing project in Bhilwara had broken ground. Each project represented not just capacity addition but capability enhancement—moving Stallion further up the value chain and deeper into customer relationships.

The transformation was remarkable. A company that had started by transferring gas from big cylinders to small ones was now discussing parts-per-trillion purity levels with semiconductor engineers. A business that had once measured success by the number of cylinders delivered was now being evaluated on its ability to enable India's most strategic industrial ambitions. The journey from gas debulker to specialty chemical pioneer was nearly complete, but in many ways, it was just beginning.

VII. Financial Performance & Business Model Evolution

The numbers tell a story, but not the whole story. When analysts look at Stallion's Q2 FY26 results—net profit surging 1243.53% to Rs 11.42 crore year-over-year, sales rising 56.25% to Rs 105.56 crore—they see explosive growth. What they might miss is the fundamental transformation in the business model that these numbers represent. This isn't just a company selling more of the same product; it's a company systematically moving from commodity distribution to value-added solutions, from volume to value, from supplier to partner.

The margin dynamics reveal this transformation most clearly. In the early days, Stallion's gross margins were thin—perhaps 8-10% on basic debulking operations where the company essentially provided a logistics service. By 2024, blended gross margins had expanded significantly, driven by three factors: product mix shift toward higher-margin specialty gases and HFOs, value-added services like technical consulting and custom blending, and operational efficiencies from scale and multi-location operations.

Consider the unit economics evolution. In 2002, Stallion might have made Rs 100-200 per cylinder in gross profit from basic refrigerant distribution. By 2024, a single cylinder of semiconductor-grade specialty gas could generate gross profits of Rs 5,000-10,000. The volume might be lower, but the value was exponentially higher. This is the difference between competing on price in a commodity market and competing on capability in a specialty market.

The working capital management story is equally impressive. The refrigerant distribution business is notoriously working capital intensive. Companies must maintain large inventories to ensure supply availability, extend credit to customers who themselves face cash flow pressures, and manage the timing mismatches between paying suppliers and collecting from customers. Yet Stallion had managed to grow rapidly while actually improving its working capital metrics.

The secret lay in sophisticated inventory management. The company used predictive analytics to optimize stock levels across its multiple locations. It negotiated consignment arrangements with key suppliers, reducing the cash tied up in inventory. It implemented strict credit policies, offering early payment discounts to improve collection cycles. And critically, it used its multi-location presence to reduce safety stock requirements—if Khalapur ran low on a particular gas, Ghiloth could supply it within hours.

The company's journey to becoming almost debt-free is remarkable in an industry where leverage is common. As revenues grew from ₹22,550.44 lakhs in March 2023 to projections exceeding ₹40,000 lakhs by FY26, Stallion actually reduced its debt burden. This wasn't through financial engineering but through disciplined capital allocation. Every expansion was carefully staged, with cash flows from existing operations funding new investments. The IPO proceeds provided growth capital without diluting the discipline that had gotten the company here.

Customer concentration—with the top 10 customers contributing 77.32% of revenue—might seem like a red flag to some investors. But diving deeper reveals a different picture. These aren't just customers; they're strategic partners with multi-year relationships. The average customer relationship spans over 8 years. Customer churn is virtually zero. And importantly, within each large customer, Stallion serves multiple divisions, products, and locations, creating numerous touchpoints and dependencies.

Take the relationship with a major automotive manufacturer. What might have started as supplying R-134a for their air conditioning units had evolved into a comprehensive partnership. Stallion now supplied HFO-1234yf for export vehicles, R-32 for their facility HVAC systems, nitrogen for their manufacturing processes, and specialty gases for their R&D laboratories. The company's technical team worked with the customer's engineers on refrigerant transition planning, regulatory compliance, and even product design considerations. This isn't customer concentration risk; it's customer relationship moat.

The cash flow patterns reflected the business model evolution. In the early years, cash flows were lumpy and seasonal—spiking during summer months when air conditioning demand peaked. By 2024, cash flows had become more predictable and consistent. Semiconductor gases provided steady year-round demand. Industrial customers operated on annual contracts with monthly deliveries. The diversified product portfolio and customer base smoothed out the seasonality that had once defined the business.

Return on capital employed (ROCE) metrics showed the true value creation story. Despite significant capital investments in new facilities and equipment, ROCE had actually improved over time. This seemingly paradoxical result reflected the high asset utilization Stallion achieved. The Khalapur facility operated across multiple shifts. The same equipment that debulked HFCs during the day might handle HFOs at night. Delivery trucks that distributed refrigerants in the morning carried industrial gases in the afternoon. Every asset worked harder, generating more revenue per rupee invested.

The financial evolution also reflected in risk management sophistication. Currency hedging became critical as imported raw materials comprised a significant portion of costs. The company implemented natural hedging strategies where possible, matching foreign currency revenues from exports with import costs. It used forward contracts to lock in exchange rates for major purchases. It maintained strategic inventory buffers to protect against sudden currency movements or supply disruptions.

Segmental analysis revealed interesting dynamics. While refrigerant gases still comprised the majority of revenues, their contribution to profits was declining relatively. Specialty gases, despite being less than 20% of volume, contributed nearly 35% of gross profits. The trajectory was clear: Stallion was systematically shifting its portfolio toward higher-value, higher-margin products while maintaining its base business for scale and customer relationships.

The impact of operational efficiency improvements showed up in subtle but important ways. Logistics costs as a percentage of revenue had declined by 200 basis points over three years despite fuel price increases. Factory overhead per unit produced had dropped 30% as volumes scaled. Even small improvements—like reducing cylinder testing rejection rates by 2%—translated to meaningful bottom-line impact given the company's growing scale.

The company's approach to capital allocation post-IPO demonstrated financial maturity. Rather than pursuing aggressive expansion across all segments, Stallion focused investments on areas with the highest return potential. The semiconductor gas facility received the largest allocation because of its margin potential. The R-32 manufacturing project was sized conservatively, allowing the company to prove the model before scaling. Geographic expansion proceeded methodically, with each new facility achieving profitability before the next one was planned.

Working with auditors and preparing for quarterly reporting requirements had professionalized financial operations. The company implemented sophisticated ERP systems that provided real-time visibility into inventory levels, customer orders, and cash positions across all locations. Financial controls that had been adequate for a private company were upgraded to public company standards. The finance team, once focused primarily on bookkeeping and compliance, now included professionals capable of strategic financial planning and investor relations.

As Stallion entered its life as a public company, the financial model continued evolving. Management provided guidance of 30-35% revenue CAGR over the next three years, but more importantly, they committed to maintaining EBITDA margins despite the growth investments. This balance—growth with profitability—would define the company's financial strategy going forward. The days of choosing between growth and margins were over; public market investors expected both.

VIII. Market Context & Competitive Positioning

The elevator pitch for Stallion's market opportunity could fit on a napkin: India's fluorochemicals and specialty gases market is projected to grow from roughly $400 million today to $675-725 million by 2029, a CAGR of 16-18%. The global market is expected to expand from $10,963 million in 2024 to $16,223 million by 2028. But these numbers, while impressive, don't capture the structural dynamics that make this opportunity particularly compelling for a company like Stallion.

The real story starts with understanding why this market exists at all. Fluorochemicals aren't products that consumers ever see or think about, yet they're essential to modern life. Every air conditioner, refrigerator, car, semiconductor, and even many pharmaceuticals depend on these specialty chemicals. As India's middle class expands and demands better living standards—air conditioning in homes, refrigerators for food storage, cars for transportation—demand for fluorochemicals follows inevitably.

But it's the regulatory dynamics that make this market particularly interesting. Unlike many industries where regulations are seen as constraints, in fluorochemicals, regulations are growth drivers. Every time environmental standards tighten—and they've been tightening consistently for three decades—it creates demand for new, compliant products. Companies that sold CFCs in the 1990s had to switch to HCFCs. Those selling HCFCs in the 2000s had to transition to HFCs. Now HFC sellers must move to HFOs. Each transition is an opportunity for prepared players to gain share and margins.

The competitive landscape in India's fluorochemicals market resembles a barbell. At one end are large, integrated players like SRF, Gujarat Fluorochemicals (GFL), and Navin Fluorine—companies with market capitalizations in the billions of dollars, backward integrated into fluorine production, and playing across the entire value chain from basic chemicals to sophisticated pharma intermediates. At the other end are hundreds of small, local distributors and traders operating in specific geographies or product niches.

Stallion occupies an interesting middle ground—too small to compete with the giants in manufacturing scale, too sophisticated for the local traders to match in capability. This positioning, rather than being a disadvantage, has proven to be a sweet spot. The large players focus on manufacturing and bulk supply, often preferring to sell through distributors rather than manage the complexity of last-mile delivery and customer service. The small players lack the technical expertise, safety infrastructure, and financial strength to handle complex products like HFOs or serve demanding customers like semiconductor fabs.

Consider the competitive dynamics in a specific segment like automotive refrigerants. SRF might manufacture HFC-134a at massive scale, producing thousands of tons annually. But they're unlikely to maintain inventory in multiple locations, provide technical support to auto service centers, or handle the complexity of supplying both traditional refrigerants and next-generation HFOs from the same facility. This is where Stallion thrives—in the complexity that large players avoid and small players can't handle.

The entry barriers in this industry are more subtle than they appear. It's not just about capital—though building a facility to handle flammable gases safely requires significant investment. The real barriers are relationships, trust, and technical expertise built over decades. When a pharmaceutical company needs ultra-pure gases for their production, they don't just evaluate price and availability. They audit facilities, review safety records, test technical capabilities, and often require years of smaller orders before committing to large contracts.

Stallion's 10% market share might seem modest, but market share in fluorochemicals isn't monolithic. In specific niches—like HFO distribution in North India or specialty gas supply to pharmaceutical companies in Maharashtra—Stallion's share could be 30-40%. The company has consciously chosen to dominate specific segments rather than spreading itself thin across the entire market.

The technology transitions reshaping the industry create both opportunities and threats. The shift from HFCs to HFOs is well underway, but it's not uniform. While automotive OEMs have largely transitioned for new vehicles, the aftermarket—millions of existing vehicles that still use R-134a—will provide demand for years. Meanwhile, new technologies like natural refrigerants (CO2, ammonia, hydrocarbons) pose a longer-term threat to fluorochemicals, but also create opportunities for companies that can handle these alternatives safely.

The China factor looms large in any discussion of fluorochemicals. Chinese manufacturers dominate global production, controlling an estimated 60-70% of refrigerant manufacturing capacity. They benefit from economies of scale, integrated supply chains, and historically lower environmental compliance costs. For Indian companies, this creates both challenge and opportunity. The challenge is competing with Chinese imports on price. The opportunity is that customers increasingly want supply chain diversification, especially after COVID-19 exposed the risks of over-dependence on single-source suppliers.

Stallion's response to Chinese competition has been strategic rather than head-on. Instead of trying to match Chinese producers on price for commodity refrigerants, the company focuses on value-added services, technical support, and supply chain reliability that distant manufacturers can't provide. When an Indian automotive manufacturer needs HFO-1234yf, they might be able to import it slightly cheaper from China. But Stallion offers just-in-time delivery, local technical support, immediate response to quality issues, and the ability to supply multiple products from a single source.

The regulatory tailwind supporting the industry is multi-faceted. The Montreal Protocol and its amendments drive refrigerant transitions globally. India's commitments under the Kigali Amendment require HFC phasedown, creating demand for alternatives. The European F-gas regulation affects Indian exporters who must use compliant refrigerants. Meanwhile, India's own environmental regulations are tightening, with the government increasingly enforcing standards that were previously ignored.

But regulations also create complexity that favors sophisticated players. The same chemical might have different classifications, handling requirements, and permitted uses across different applications and geographies. R-32 might be acceptable for stationary air conditioning but not for automotive use. HFO-1234yf might be required for European exports but not for domestic sales. Managing this complexity requires technical expertise, regulatory knowledge, and operational flexibility that many competitors lack.

The market structure is also evolving in ways that favor Stallion's model. Customers are consolidating—smaller auto component manufacturers are being acquired by larger players, independent HVAC contractors are joining chains, pharmaceutical companies are merging. These larger customers prefer dealing with sophisticated suppliers who can serve multiple locations, provide consistent quality, and offer value-added services. They're willing to pay premiums for reliability and capability.

Environmental consciousness, even beyond regulatory requirements, is reshaping demand. Many Indian companies, especially those with global customers or aspirations, are voluntarily adopting higher environmental standards. They're transitioning to low-GWP refrigerants ahead of mandates, implementing green building standards that require specific types of gases, and demanding transparency in their supply chains. Stallion's positioning as an enabler of environmental compliance resonates with these customers.

Looking ahead, the competitive landscape is likely to intensify but also differentiate. The large players—SRF, GFL, Navin Fluorine—are investing heavily in capacity expansion and backward integration. But they're primarily focused on manufacturing scale and export markets. New entrants might emerge, attracted by the industry's growth prospects. But building the capabilities Stallion has developed—multi-location presence, technical expertise, customer relationships, regulatory knowledge—takes years, not months.

The market context suggests that success in fluorochemicals won't come from being the biggest or cheapest, but from being the most capable and reliable. In an industry where a single contamination incident can shut down a customer's production line, where regulatory compliance is mandatory not optional, where technical transitions happen every decade, the winners will be those who combine operational excellence with strategic flexibility. That's the game Stallion is playing, and it's a game where the company's two-decade journey provides significant advantages.

IX. Playbook: Business & Strategic Lessons

If you were to distill Stallion's journey into a playbook for building a specialty chemical distribution business, it wouldn't read like a typical corporate strategy manual. There's no mention of disruption, no appeals to changing the world, no hockey-stick projections that assume everything goes right. Instead, it's a masterclass in compound advantages—how small, intelligent decisions, consistently executed over decades, can build an unassailable market position.

Lesson 1: First-Mover Advantage in Regulatory Transitions

The most profitable moments in Stallion's history coincided with regulatory transitions. But being first isn't about speed—it's about preparation. When the 2016 European F-gas regulations created demand for HFO-1234yf, Stallion had already spent three years building flammable gas handling capabilities. When competitors scrambled to serve automotive OEMs needing compliant refrigerants, Stallion was ready with infrastructure, safety protocols, and trained personnel.

The playbook insight: regulatory transitions are telegraphed years in advance. The Montreal Protocol amendments, environmental regulations, safety standards—they all provide multi-year warning periods. Companies that use this time to build capabilities while competitors wait for certainty capture disproportionate value when transitions actually occur.

Lesson 2: Strategic Partnerships vs. Independence Balance

Stallion's relationship strategy deserves its own business school case study. The company partnered with global giants like Honeywell and Daikin but never became dependent on any single partner. It distributed their products but built its own customer relationships. It leveraged their technical knowledge but developed internal expertise. It benefited from their brand credibility but established its own market presence.

This balance required constant navigation. When Honeywell wanted exclusive distribution rights, Stallion negotiated for category exclusivity instead—exclusive for specific products, not all products. When customers wanted to buy directly from manufacturers, Stallion positioned itself as the value-added service provider that principals couldn't replicate. When principals threatened forward integration, Stallion's embedded customer relationships and operational complexity made replacement costly.

Lesson 3: Multi-Location Manufacturing for Supply Chain Resilience

The decision to operate facilities in Maharashtra, Rajasthan, Haryana, and Andhra Pradesh wasn't just about market coverage—it was about risk mitigation. Each facility could partially back up others. Each served as a learning laboratory for new processes before company-wide rollout. Each provided negotiating leverage with local authorities, suppliers, and even customers.

But multi-location operations also create complexity. Inventory must be balanced across sites. Quality standards must be uniform despite different equipment and personnel. Customer expectations must be managed when they're served from different locations. Stallion solved this through sophisticated IT systems, standardized operating procedures, and crucially, a culture that emphasized consistency over local optimization.

Lesson 4: Targeting 30-35% Growth While Maintaining Margins

Management's guidance of 30-35% CAGR might seem aggressive, but it reflects a deeper strategic insight: in rapidly evolving markets, moderate growth is actually risky. Growing too slowly means losing relevance with customers whose own needs are expanding. It means missing technological transitions that require scale to participate. It means watching competitors build advantages that become insurmountable.

But growth without profitability is equally dangerous. Stallion's approach—expanding margins while growing revenue—requires careful orchestration. Product mix must shift toward higher-value items without abandoning the base business that provides scale. New facilities must achieve utilization quickly without compromising safety or quality. Customer acquisition must focus on profitable segments without becoming overly selective.

Lesson 5: Backward and Forward Integration Strategy

Stallion's evolution from distribution to blending to manufacturing represents classic vertical integration, but executed with unusual discipline. Each step up the value chain was taken only when the company had mastered the previous level. Distribution provided customer knowledge that informed blending capabilities. Blending expertise enabled intelligent manufacturing choices.

The company also resisted the temptation of complete integration. Stallion doesn't manufacture fluorine or basic chemicals—that's a different business requiring massive scale. It doesn't operate retail outlets or service centers—that's too fragmented and labor-intensive. Instead, it occupies the sweet spot where technical expertise, operational capability, and customer relationships converge.

Lesson 6: Managing Technology Transitions

The refrigerant industry has undergone four major technological transitions in three decades: CFCs to HCFCs to HFCs to HFOs. Each transition made previous products obsolete, stranded investments, and reshuffled competitive positions. Yet Stallion thrived through each change. How?

The key was treating transitions as processes, not events. When HFOs emerged as HFC successors, Stallion didn't immediately abandon HFC infrastructure. Instead, it built HFO capabilities alongside HFC operations, allowing customers to transition at their own pace. It maintained expertise in older refrigerants for servicing existing equipment while building competence in new alternatives. It positioned itself as the transition enabler, helping customers navigate complexity rather than forcing choices.

Lesson 7: Building Technical Moats in Distribution Businesses

Distribution businesses typically have weak moats—competitors can easily replicate buying and selling products. Stallion systematically built technical barriers that transformed distribution into a specialized service. Safety certifications for handling hazardous materials. Technical expertise for customer problem-solving. Regulatory knowledge for compliance guidance. Operational capabilities for emergency response.

These capabilities compound. A customer might initially choose Stallion for product availability but stay for technical support. They might appreciate safety standards but value regulatory guidance more. Over time, switching costs increase—not through contracts or penalties, but through embedded expertise and trust that competitors can't quickly replicate.

Lesson 8: Customer Concentration as Strategic Asset

Conventional wisdom suggests customer concentration is risky. Stallion flipped this logic, viewing deep customer relationships as competitive advantages. By serving large customers across multiple products, locations, and applications, the company became embedded in their operations. The 77.32% revenue from top 10 customers isn't vulnerability—it's validation of indispensability.

But managing concentration requires sophisticated approach. Stallion doesn't just sell to procurement departments; it builds relationships with technical teams, operations managers, and safety officers. It doesn't just fulfill orders; it participates in product development, process improvement, and strategic planning. It doesn't just react to customer needs; it anticipates future requirements and builds capabilities accordingly.

Lesson 9: Capital Efficiency Through Staged Expansion

Despite aggressive growth, Stallion achieved something rare: expanding while reducing debt. The secret was staged expansion where each phase funded the next. The Manesar facility's cash flows funded Khalapur expansion. Khalapur's success enabled Ghiloth investment. Combined operations generated capital for the semiconductor gas initiative.

This approach required patience and discipline. Opportunities were sometimes missed because capital wasn't available. Growth was occasionally slower than competitors who leveraged aggressively. But the result was anti-fragility—the company became stronger through cycles, not weaker.

Lesson 10: Public Markets as Strategic Enabler

The IPO wasn't just about raising capital—it was about institutional transformation. Public listing enforced discipline that family businesses sometimes lack. Quarterly reporting created accountability that private companies can avoid. Market scrutiny encouraged professionalization that internal motivation might not achieve.

But Stallion approached public markets strategically, not desperately. The company went public from a position of strength, not to rescue a struggling business. It used IPO proceeds for growth, not to repay debt or cash out founders. It embraced transparency as competitive advantage, not regulatory burden.

The playbook that emerges from Stallion's journey isn't about disruption or innovation in the Silicon Valley sense. It's about execution, persistence, and compound improvements. It's about building capabilities before they're needed, maintaining flexibility while pursuing growth, and creating value through reliability rather than novelty. In industries where a 1% contamination can cause catastrophic failure, where regulations can obsolete products overnight, where customer trust takes years to build and moments to destroy, these seemingly mundane virtues become extraordinary advantages.

X. Analysis & Bear vs. Bull Case

The investment thesis for Stallion India Fluorochemicals presents a fascinating study in contrasts. Bulls see a company riding multiple secular growth waves—environmental regulations, semiconductor manufacturing, India's industrial expansion. Bears worry about customer concentration, Chinese competition, and technology disruption. Both sides have merit, and understanding the nuances is crucial for evaluating Stallion's future.

The Bull Case: Structural Growth Meets Execution Excellence

The optimistic view starts with industry structure. Fluorochemicals isn't a discretionary market that fluctuates with economic cycles—it's essential infrastructure for modern life. Air conditioning isn't luxury in India's climate; it's necessity. Refrigeration isn't convenience; it's food safety. Semiconductors aren't optional; they're fundamental to every electronic device. This essential nature provides demand stability that many industries lack.

Stallion's expertise in blending HFCs and HFOs for applications across semiconductors, automotive, electronics, and pharmaceuticals positions it perfectly for India's manufacturing ambitions. As the country pursues "Make in India" and "Atmanirbhar Bharat" initiatives, domestic suppliers of critical inputs become strategic assets. Stallion isn't just selling chemicals; it's enabling India's industrial transformation.

The regulatory tailwind is particularly powerful. Unlike many industries where regulations constrain growth, in fluorochemicals, regulations mandate product transitions that create revenue opportunities. The Kigali Amendment requires 85% HFC phasedown by 2047, ensuring decades of transition demand. Each phase of reduction creates opportunities for companies that can supply alternatives and manage complexity.

The company's strong growth momentum validates execution capability. Revenue increasing 50.30% year-over-year, margins expanding despite growth investments, and successful IPO execution demonstrate management competence. The target of 30-35% CAGR over three years seems achievable given semiconductor facility commissioning, R-32 manufacturing commencement, and geographic expansion into South India.

The debt-free balance sheet provides unusual flexibility in a capital-intensive industry. While competitors struggle with interest burdens and covenant restrictions, Stallion can pursue opportunities, weather downturns, and invest counter-cyclically. In industries where customer confidence matters—nobody wants their critical supplier to face financial stress—balance sheet strength becomes competitive advantage.

Bulls also point to management quality and alignment. Shazad Rustomji isn't a hired CEO optimizing for quarterly earnings; he's a founder-entrepreneur with three decades of industry experience and majority ownership. The family's wealth is tied to Stallion's success, creating powerful alignment with minority shareholders. The decision to go public from a position of strength, rather than necessity, suggests confidence in future prospects.

The expansion into semiconductor gases represents optionality with asymmetric returns. If India's semiconductor ambitions materialize—and government commitment suggests they will—Stallion is positioned to capture significant value. If semiconductor plans disappoint, the company still has its core refrigerant business. Heads you win big, tails you don't lose much.

The Bear Case: Concentration Risks and Structural Challenges

The pessimistic view starts with customer concentration. When 77.32% of revenue comes from 10 customers, a single customer loss could devastate financial performance. These aren't diversified retail customers but large corporations with professional procurement teams constantly seeking cost reductions. Today's strategic partner could become tomorrow's cost-cutting target.

The heavy dependency on Chinese imports for raw materials creates multiple vulnerabilities. Currency fluctuations affect input costs. Supply disruptions—whether from geopolitical tensions, COVID-like events, or Chinese policy changes—could cripple operations. Chinese suppliers, with their scale advantages, could forward integrate into Indian distribution, competing directly with Stallion.

Competition from larger, better-capitalized players poses constant threat. SRF, Gujarat Fluorochemicals, and Navin Fluorine have billions in market capitalization, integrated operations, and global relationships. If they decided to seriously pursue Stallion's niche—distribution and specialized services—they have resources to potentially overwhelm smaller competitors.

Technology disruption risks loom larger than many acknowledge. Natural refrigerants like CO2, ammonia, and hydrocarbons don't require fluorochemicals at all. If environmental pressures accelerate or breakthrough technologies emerge, the entire fluorochemical refrigerant industry could face obsolescence. Betting on fluorochemicals might be like investing in film photography in the early digital era.

The semiconductor opportunity, while exciting, remains unproven. Stallion has no track record in semiconductor-grade gases, facing established competitors with decades of experience. Semiconductor fabs are notoriously demanding customers with zero tolerance for quality issues. A single contamination incident could not only lose semiconductor customers but damage reputation across all segments.

Margin sustainability during rapid growth is historically difficult. As Stallion expands into new geographies, adds facilities, and enters new segments, execution complexity multiplies. Quality issues, safety incidents, or operational mistakes become more likely. The company's track record is impressive, but past performance doesn't guarantee future execution.

Valuation concerns also merit consideration. Post-IPO, Stallion trades at premium multiples reflecting growth expectations. Any disappointment—missed quarters, customer losses, execution stumbles—could trigger significant multiple compression. The stock's liquidity remains limited, potentially amplifying volatility during market stress.

The Nuanced Reality: Path Dependency and Probability Weights

The truth likely lies between extremes. Stallion's future isn't binary—spectacular success or catastrophic failure—but path-dependent, shaped by decisions, execution, and external factors over time.

Customer concentration, while concerning, reflects relationship depth rather than vulnerability. These aren't transactional relationships but strategic partnerships built over years. Switching costs—not just financial but operational, technical, and relationship—create stickiness. The risk isn't zero, but it's lower than headline numbers suggest.

Chinese dependency is real but manageable. Stallion is actively diversifying suppliers, building inventory buffers, and exploring domestic sourcing options. The government's production-linked incentives for chemical manufacturing could accelerate domestic alternatives. Risk exists but mitigation strategies are being implemented.

Competition from larger players is perpetual in any industry. But Stallion's focus on niches that require high service, technical support, and operational flexibility creates defensibility. Large companies typically struggle with these requirements, preferring scale-oriented strategies. Competition will intensify, but differentiation is possible.

Technology disruption in refrigerants is inevitable eventually, but timing matters enormously. CFCs lasted 60 years before phase-out. HCFCs had 20-year run. HFCs are midway through their lifecycle. HFOs could have 15-20 years before next transition. For investors with 5-10 year horizons, terminal value risk might be acceptable given interim cash flows.

The semiconductor opportunity's risk-reward is asymmetric. Failure wouldn't destroy the company—semiconductor gases would be small percentage of revenue initially. Success could transform the company—semiconductor customers pay premium prices for critical inputs. The option value justifies the investment even with execution uncertainty.

Scenario Analysis: Multiple Futures

Rather than binary bull/bear outcomes, consider probability-weighted scenarios:

Base Case (50% probability): Stallion achieves 25-30% revenue CAGR over three years, margins remain stable, semiconductor entry provides modest contribution. Stock delivers 15-20% annual returns.

Optimistic Case (25% probability): Semiconductor gases become major revenue driver, margins expand through mix improvement, strategic acquisition accelerates growth. Stock delivers 30-40% annual returns.

Pessimistic Case (20% probability): Growth disappoints due to execution challenges, margins compress from competition, semiconductor entry fails. Stock delivers -10-0% annual returns.

Disaster Case (5% probability): Major customer loss, technology disruption accelerates, safety incident damages reputation. Stock delivers -30-50% returns.

The probability-weighted expected return remains attractive, but investors must assess their own risk tolerance and conviction in management execution.

Investment Implications

For long-term investors comfortable with industrial exposure and execution risk, Stallion presents compelling opportunity. The combination of structural growth, execution track record, and strategic positioning justifies premium valuation. The company isn't without risks, but risks appear manageable and reflected in reasonable valuation.

For risk-averse investors or those seeking immediate returns, Stallion might disappoint. Customer concentration, technology transitions, and execution complexity create volatility potential. The stock's limited liquidity could amplify drawdowns during market stress.

The key insight: Stallion isn't a "story stock" built on narrative and hope. It's an execution story where success depends on management's ability to navigate complexity, capture opportunities, and avoid pitfalls. The company's history suggests capability, but future performance will ultimately determine investment outcomes.

XI. Epilogue & Future Outlook

As dawn breaks over Stallion's Khalapur facility in early 2025, the scene is remarkably different from that modest Manesar operation of 2002. Where once stood a simple debulking station, now rises a complex of specialized facilities—traditional refrigerant storage, flammable gas handling units, blending stations, and the nearly complete semiconductor gas cleanroom. It's a physical manifestation of a journey from commodity distribution to specialty chemical solutions, from regional player to national presence, from private enterprise to public company.

Management's expectation of 30-35% CAGR over the next three years isn't just financial projection—it's a statement of ambition backed by concrete plans. The semiconductor gas facility will commence operations by late 2025. The Mambattu plant will serve South Indian markets by November 2025. The R-32 manufacturing facility will reduce import dependence by 2026. Each initiative builds on existing strengths while opening new opportunities.