SRG Housing Finance: The Frontier of Indian Mortgage Lending

I. Introduction & Episode Roadmap

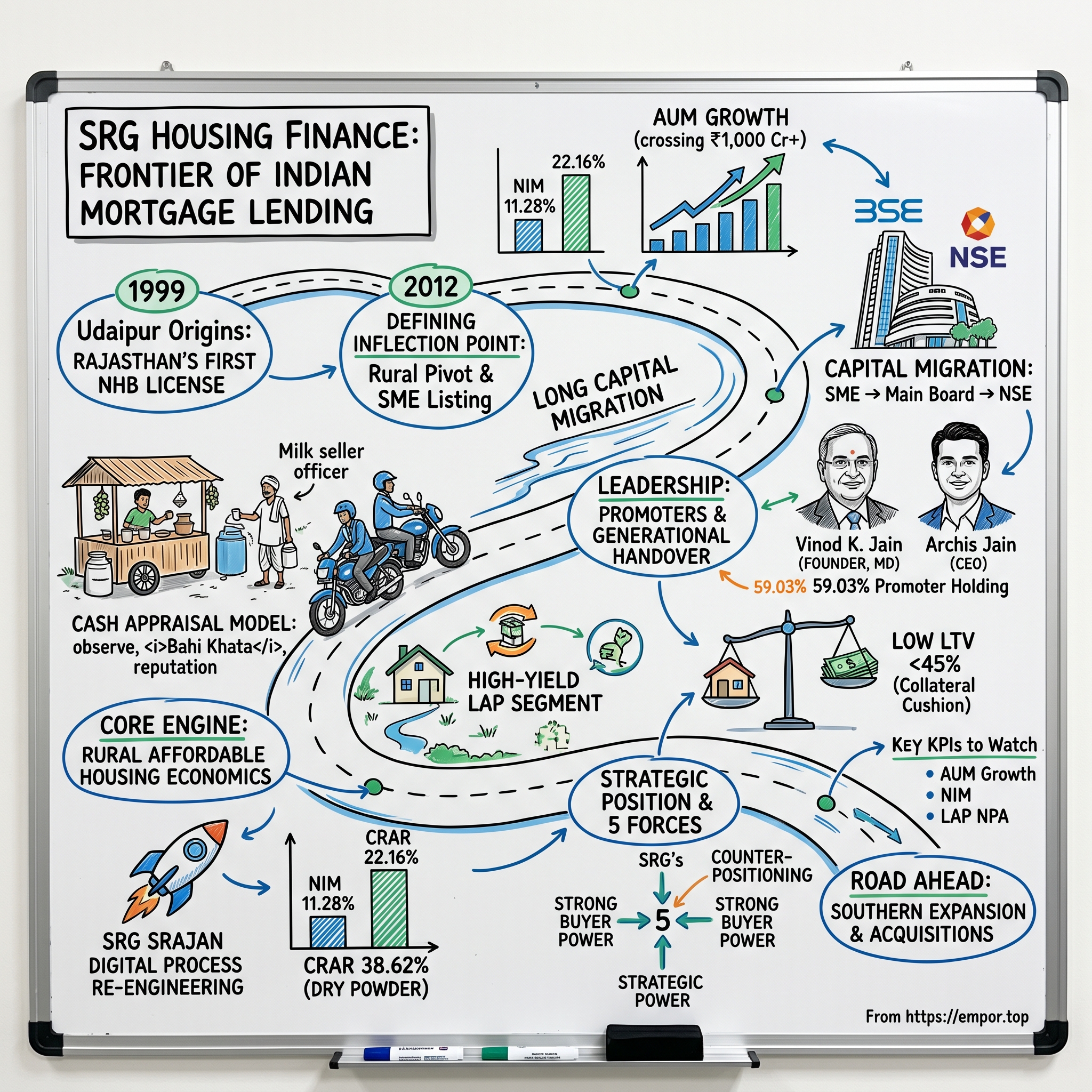

Picture two loan officers leaving for work on the same morning in 2026. The first works for a marquee prime lender in a glass tower in Pune. He spends his day pulling credit bureau scores, scanning three years of income-tax returns, and verifying salary slips, before approving a ₹50 lakh home loan at an interest rate that, after all the competitive pressure from State Bank of India and the big banks, leaves his employer earning a wafer-thin spread. The second loan officer kick-starts a motorcycle in a dusty district town in Rajasthan, rides forty minutes to a village, and parks outside a Kirana grocery shop. He buys a cup of tea, sits down on a plastic stool, and watches. He watches how many customers walk in. He watches the shopkeeper make change from a tin cash box. He flips through a hand-written ledger — the Bahi Khata — that no bank would ever accept. By the end of the afternoon, he has decided whether to lend this man ₹6 lakh to finish building his house. And the loan he writes will yield his employer more than 22% a year.17

That second officer works for SRG Housing Finance Limited, a company most investors have never heard of, headquartered not in Mumbai or Bangalore but in Udaipur, the lake city of southern Rajasthan. And the puzzle at the heart of this episode is simple to state and surprisingly hard to answer: how does a tiny regional housing finance company write mortgages that yield north of 22% — nearly double the rate a borrower would pay at SBI or Bajaj Housing Finance — while keeping its gross non-performing assets below 1.8%?17 That is not supposed to be possible. High yields are supposed to mean high defaults. Cheap money is supposed to mean low risk. SRG breaks the rule, and the way it breaks the rule is the whole story.

The conventional mental model of housing finance is that it is a commodity. A home loan is a home loan; the only thing that varies is the price, and the lowest cost of capital wins. That model describes the prime market perfectly. It does not describe the India that most of India actually lives in. Buried in the country's semi-urban and rural heartlands is a completely different business — one we might call "microfinance-like yields in a mortgage jacket." The collateral is real property, with all the legal protection of a registered mortgage. But the customer looks nothing like a salaried borrower, and the economics look nothing like prime lending.

Consider the duel of business profiles. A prime lender such as Bajaj Housing Finance writes loans averaging around ₹50 lakh to documented, salaried, credit-scored customers, and earns a net interest margin of perhaps three to four percent. SRG writes loans averaging between ₹6 lakh and ₹12 lakh to undocumented tea-stall owners, milk sellers, and rural merchants — and earns a net interest margin of 11.28%.17 These two companies are nominally in the same industry. In reality, they are playing entirely different games, against entirely different opponents, for entirely different prizes.

Here is the roadmap for how we'll unpack this business. First, the founding context in late-1990s Udaipur, and why a regulatory license obtained in 2002 mattered so much. Second, the defining 2012 pivot to rural affordable housing and the unusual decision to list on a small-company exchange. Third, the long capital migration — from SME platform to the main board, and from the Bombay exchange to the National Stock Exchange. Fourth, the promoter family, and the father-son generational handover now underway. Fifth, the actual mechanics of the core housing book versus the high-yield Loans Against Property segment. Sixth, a strategic war-game using Porter's Five Forces and Hamilton Helmer's Seven Powers, applied to the strange art of rural underwriting. And finally, the road ahead: the southern expansion, the freshly announced appetite for acquisitions, and the bull and bear cases an investor should weigh. Let's begin where it began — at the edge of the formal financial system.

II. Udaipur Origins: Rajasthan's First NHB License

In 1999, formal banking in rural Rajasthan was less an institution than a rumor. The branches existed, on paper, in the larger towns. But for a family living in a village two hours from Udaipur who wanted to replace a mud-and-thatch dwelling with a proper concrete house, the bank was effectively a closed door. There were no income-tax returns to show, no salary slips, no credit history, no collateral the bank's manual recognized. So the family did what families had done for centuries: they went to the local moneylender. And the moneylender charged interest of anywhere from 36% to 60% a year, with a quiet, devastating clause — default, and the land is mine.1 This was the financial frontier into which a small company was born.

That company was originally incorporated in 1999 as Vitalise Finlease Private Limited, a generic local finance outfit in Udaipur with no particular specialization.17 Within a year, in 2000, it was rebranded as SRG Housing Finance Private Limited, a name that pointed toward a more specific ambition: housing.1 But a name is not a license, and in Indian housing finance the license is everything.

The pivotal early move came in 2002. Under the stewardship of founder Mr. Vinod K. Jain, SRG became the very first company in the state of Rajasthan to register with the National Housing Bank.16 To appreciate why that mattered, you have to understand what the National Housing Bank — the NHB, the apex regulator and refinancier for housing finance in India, then a subsidiary of the Reserve Bank of India — actually represents. An NHB registration is not a piece of paperwork you file and forget. It is an institutional seal of approval, hard to win and easy to lose, and in the early 2000s it was vanishingly rare for a small regional private firm to hold one.

Why does the seal matter so much in practice? Because it unlocks the plumbing of the entire business. A housing finance company does not lend its own money; it borrows wholesale and re-lends retail, earning the spread in between. Without NHB registration, a tiny Udaipur lender would have had no credible way to borrow from the formal banking system at all. With it, SRG gained access to refinance lines — the ability to borrow from public-sector banks and from the NHB itself, and then channel that capital out to rural borrowers who could never have approached those banks directly.1 In effect, SRG became a translator standing between two worlds: it spoke the language of formal credit ratings and refinance agreements on one side, and the language of cash boxes and ledger books on the other. That translation function — borrowing where money is cheap and organized, lending where it is scarce and undocumented — is the foundation on which everything later was built.

For its first decade, though, SRG did not yet know quite what it wanted to be. It was a small, multi-purpose, urban and semi-urban lender, doing a bit of everything around Udaipur, never large, never famous, and never especially differentiated. The license gave it a right to play. It would take another strategic insight — and a willingness to gamble on the public markets in an era when companies its size simply didn't — to turn that right into a real business. That insight arrived in 2012.

III. The Defining Inflection Point: The 2012 Rural Pivot & SME Listing

Every company has a year it stops being one thing and becomes another. For SRG, that year was 2012. And the pivot began not with a press release but with a question that Vinod Jain had clearly been turning over for years: where, exactly, is a small Udaipur lender supposed to make money?

The honest answer was: not where everyone else was looking. In the urban and semi-urban market for salaried borrowers, SRG was a minnow competing against whales. The public-sector banks had cheaper capital, bigger balance sheets, and the implicit backing of the government. Competing for a school teacher's home loan in a Rajasthan town was a race to the bottom that SRG could only lose. So Jain looked in the opposite direction — toward the customers the whales would not, and structurally could not, serve.

These were the self-employed of the unorganized sector: the milk seller with a steady morning round, the grocer whose tin box filled and emptied every day, the small transport operator with two trucks and a route. People with genuinely stable cash flows and genuine assets, but with zero formal documentation — no income-tax returns, no salary slips, nothing a bank's credit committee could process. This was not a niche. In rural India it was the overwhelming majority. And nobody in formal finance was building a model designed specifically to underwrite them for home loans. That was the goldmine hiding in plain sight.17

So in 2012 SRG launched a dedicated pilot project for Rural Housing Finance, based in Udaipur — a deliberate, contained experiment in lending against self-constructed rural homes to undocumented borrowers.1 The pilot was the laboratory in which the company's entire future underwriting method — the cash-flow appraisal we'll dissect in detail later — was first tested at small scale, where mistakes would be survivable.

But a pivot needs fuel, and fuel means capital. Here SRG made a decision that, in 2012, bordered on the eccentric. On September 11, 2012, it listed on the BSE SME platform — the Bombay Stock Exchange's then-new exchange for small and medium enterprises — becoming the first company from Rajasthan to do so.12 In an era when SME listings were highly unusual and largely untested, a tiny housing financier from Udaipur chose to subject itself to the discipline, disclosure, and scrutiny of public markets. It was a statement of seriousness: a small family firm declaring that it intended to build something durable enough to be owned by outside shareholders.

Concurrently, the company completed the identity transformation it had begun a decade earlier, shedding its holding-company remnants and formally adopting the name SRG Housing Finance Limited — its legal structure now aligned entirely with its specialized rural mortgage strategy.1 The generic local finance firm of 1999 was gone. In its place stood a focused rural housing lender with a public listing, a regulatory license, and a thesis about the frontier that the rest of the industry had ignored. The pilot worked. Now the company had to prove it could scale — and scaling, in finance, is fundamentally a story about capital.

IV. The Capital Migration & Scalability Milestones

There is a brutal physics to small-company finance, and it goes like this: the smaller and more obscure you are, the more your capital costs, which makes it harder to grow, which keeps you small and obscure. Breaking out of that trap is less a single leap than a long climb, and for SRG that climb was a migration up the ladder of capital markets — each rung bringing more visibility, more credible investors, and ultimately cheaper money.

The SME platform had been a useful launchpad, but it had a fatal flaw for a growing lender: poor liquidity and institutional neglect. Serious institutional investors — the national banks, the mutual funds — largely don't touch SME-listed stocks; the volumes are too thin and the governance perception too uncertain. So in 2015, SRG took the next step, migrating from the SME platform to the BSE Main Board.12 The move was less about raising a specific sum and more about changing the company's address in the eyes of the investing world. On the main board, a national bank or a mutual fund could credibly consider lending to SRG or buying its equity. The company had moved from the back room to the showroom floor.

The migration up the exchanges culminated nearly a decade later. On August 21, 2023, SRG listed on the National Stock Exchange — India's largest and most liquid exchange — under the ticker SRGHFL.13 Listing on the NSE put the company in front of the broadest possible pool of domestic and foreign investors, completing its journey from a Rajasthan-only SME curiosity to a genuinely national small-cap name. Each rung of that ladder did the same thing in a different way: it lowered the friction between SRG and the capital it needed to grow.

And grow it did. The trajectory of the company's assets under management — the total loan book it manages — tells the story of a business hitting its stride. From a sleepy regional book, SRG crossed the ₹500 crore AUM mark in 2023.1 By March 31, 2026, the book had reached ₹1,042.15 crore — a major scale milestone — representing roughly 37% year-on-year growth from ₹759.36 crore at the end of FY25.17 In a lending business, growing the book by more than a third in a single year while keeping defaults low is genuinely hard; it means originating quality loans faster than the old ones run off, without loosening standards to do it.

Why does crossing the ₹1,000 crore line matter beyond the symbolism? Because scale changes the very physics of borrowing. As a small HFC, SRG historically faced a punishing cost of funds, often above 11–12%, simply because lenders demand a premium to lend to small, lightly-rated institutions.1 Reaching roughly ₹1,000 crore in assets is the kind of threshold where national rating agencies start to treat a company differently — and in 2026, SRG's credit rating was reaffirmed at BBB+ with a Positive outlook.45 A rating reaffirmation with a positive outlook is the agency's way of saying "we see the next move as up." And in this business, every notch of rating improvement translates directly into cheaper incremental borrowing, which widens the spread, which fattens the margin. Scale, in other words, is not vanity; it is the lever that bends the cost of capital. But a business is only as good as the people steering it — and at SRG, that means a single family with almost everything on the line.

V. Leadership Profile: The Promoters & Generational Handover

In a great many publicly listed companies, you find a familiar and slightly dispiriting pattern: the founders, having raised round after round of capital, have been diluted down to single-digit ownership, their personal fortunes only loosely tethered to how the business actually performs. SRG is the opposite case. The Jain family — the promoter group — collectively holds 59.03% of the company.[^8] That is not a token stake. That is a controlling, fate-binding ownership position, the kind that means the family wins or loses alongside every outside shareholder. In the language of investing, this is pure skin in the game, and it sits at the center of how you should think about the business.

At the head of the family is Mr. Vinod K. Jain, the founder and Managing Director — the man who obtained Rajasthan's first NHB registration in 2002 and who conceived the rural pivot of 2012. His personal alignment with the company is striking. He directly holds 20.48% of SRG — some 3.21 million shares — with a further 4.22% held through the Vinod Jain Hindu Undivided Family entity, a common Indian structure for holding family assets.[^8] When more than a quarter of the company sits in one man's hands, every decision he makes is, quite literally, a decision about his own net worth.

His compensation reinforces that alignment rather than diluting it. Vinod Jain's fixed salary stands at ₹2.16 crore a year, but the more interesting feature is the incentive structure layered on top: he is eligible for a performance incentive of 5% of net profits, capped at 100% of his fixed salary.[^8] Read that carefully, because it is elegantly designed. When the company's bottom line expands, the founder's payout expands in lockstep — but the cap prevents the incentive from ballooning into something that might tempt reckless, profit-chasing behavior. It is an arrangement that says: grow the profits, share in them, but don't bet the house to do it.

Then there is the next generation. Mr. Archis Jain was appointed Chief Executive Officer on April 24, 2023 — the classic moment of generational transition in a family enterprise, when the founder begins handing operational control to his successor.[^8] Archis directly holds 7.49% of the company, and his compensation is structured very differently from his father's: an annual salary in the range of roughly ₹58.3 to ₹70.5 lakh, but 100% fixed, with no profit-linked commission.[^8] That choice is deliberate and revealing. By keeping the incoming CEO's pay fixed, the company steers his focus away from short-term profit maximization and toward the thing that actually matters for a young lender's long-term survival: the stability and quality of the loan book. You do not want the man building the next twenty years of the business to be paid on this quarter's earnings.

The deeper story here is the fusion of two eras. Vinod Jain represents decades of feet-on-the-street underwriting wisdom — the hard-won intuition about which rural borrower will pay and which won't, knowledge that lives in a person, not a spreadsheet. Archis Jain represents the digital-first push the business needs to scale beyond what intuition alone can manage. His signature initiative is "SRG SRAJAN," a business-process re-engineering project designed to move the company from physical, paper-based underwriting toward automated, digital-first workflows — without severing the local credit-officer touchpoints that make the whole model work.1 That last clause is the crux. The bet is that you can digitize the plumbing — the file management, the collections tracking, the back office — while preserving the irreplaceable human act of a credit officer sitting in a village shop, reading a borrower the way no algorithm can. Whether that bet pays off depends entirely on the engine it is meant to improve. So let's open the hood.

VI. Inside the Core Engine: Rural Affordable Housing Economics

Let's go back to that loan officer on the motorcycle, because his afternoon at the grocery shop is, in microcosm, the entire business. The core of SRG — roughly 71% of its assets — is the financing of self-constructed homes, home extensions, and renovations in rural and semi-urban pockets of India.17 Not apartments bought from developers, but houses families build for themselves, brick by brick, often over years. It is the least glamorous corner of Indian finance, and one of the most profitable.

Before we get to how the magic works, it's worth placing SRG on the map of its peers, because scale here tells you something important about strategy. The affordable housing finance space in India has its giants and its boutiques. Aadhar Housing Finance is the national heavyweight, with assets above ₹21,000 crore.1 Aavas Financiers, also rooted in Rajasthan, is the regional powerhouse, with a book north of ₹17,000 crore.1 Home First Finance, the tech-forward specialist focused on the urban periphery, runs around ₹9,000 crore, and Aptus Value Housing, the highly profitable southern star, sits near ₹8,000 crore.1 And then there is SRG, with roughly ₹1,042 crore as of March 2026 — a fraction of any of them.17 SRG is not trying to be the biggest. It is a niche rural boutique, and its smallness is, paradoxically, part of its defense: the segments it serves are too small and too operationally awkward for the giants to bother chasing village by village.

Now, the central mystery. How do you underwrite a borrower who has no pay slip, no tax return, no credit score — nothing the formal system recognizes as evidence that he can repay? SRG's answer is the cash appraisal model, and it is worth walking through slowly because it is genuinely the company's secret recipe.

It begins with the cash-box count. The credit manager physically visits the applicant's grocery shop or workplace and simply observes — for hours. He counts the footfall: how many customers come through, how often, what they buy. He watches cash move in and out of the box. He asks to see the local ledger book, the Bahi Khata, the hand-written record of credit and debit that a village merchant actually keeps. No bank would accept a Bahi Khata as proof of income. To SRG, it is the most honest financial statement the borrower owns.

The second step is the household margin. Knowing what comes in is not enough; you need to know what's left over. So the officer estimates the family's true cost of living — grain consumption, school fees, the local electricity bill, the small unavoidable outflows of rural life — and subtracts it, deriving the actual surplus cash available to service a loan. This is the number that matters: not declared income, but real, observed, after-everything spare cash.

The third step is multi-layered verification. The officer cross-checks the shop's trade standing with its suppliers — does the wholesaler extend this man credit, and does he pay on time? He talks to neighbors. He triangulates reputation. By the end, he has assembled a portrait of creditworthiness that no bureau score could produce, built from a hundred small observations. This is labor-intensive, unscalable-looking, deeply human underwriting — and it is precisely what makes the loan possible at all.

Because these borrowers have essentially no alternative — their only other option is the informal moneylender charging 36% to 60% — they are remarkably insensitive to interest rates.1 The relevant comparison for them is not SRG versus a bank; it is SRG versus the moneylender who might one day take their land. Against that benchmark, a formal mortgage at 22% is a bargain. And so SRG commands an average yield on loans of roughly 22.16% — extraordinary in mortgage lending.17

The flip side is the cost of funds. SRG's cost of borrowing stood at 10.88% in FY26.17 Because it is small and rated BBB+, it cannot raise cheap public deposits the way a bank can; it must borrow wholesale at a premium. That is a real and permanent drag. And yet — and this is the whole point — the arithmetic still works beautifully. Lend at roughly 22%, borrow at roughly 11%, and the net interest margin lands at an exceptional 11.28%, among the very highest in the entire housing finance sector.17 A prime lender borrowing at 7% and lending at 8.5% would kill for a fraction of that spread.

But high yield with high defaults is just a slow-motion disaster, so the real question is risk. How does SRG keep this high-risk-looking book clean? The answer is an almost obsessive conservatism on collateral. SRG maintains an average loan-to-value ratio under 45%, often around 40%.1 Translate that: if a house costs ₹15 lakh to build, SRG lends only about ₹6 lakh, and the borrower must put up ₹9 lakh of his own money. The lender's exposure is buried under a thick cushion of the borrower's own capital.

This is the deepest insight of the whole model, and it flips the usual logic of risk. Because the borrower has put up 60% of the value of his own home, he has overwhelming skin in the game. This is not an investment property he can walk away from; it is the house his family lives in, and he has sunk his life savings into it. As the saying goes inside lenders like this, such a borrower will cut back on food before he defaults on his home. The low LTV does not just limit losses if a default happens — it makes the default far less likely to happen in the first place, because the borrower has everything to lose. The result is asset quality that defies the skeptics who assume rural self-employed lending must be a credit time bomb: gross NPAs of 1.77% and net NPAs of just 0.65% in FY26.17 Those are numbers a prime lender would be proud of, produced in a segment everyone else considers untouchable. That conservatism on the core book also creates room to take a little more yield elsewhere — which brings us to the high-octane sub-plot.

VII. The High-Yield Sub-Plot: Loans Against Property (LAP)

If the core housing book is SRG's steady, low-LTV workhorse, then Loans Against Property is its turbocharger — quieter, less talked about, and disproportionately profitable. This segment makes up about 29% of assets under management, and it is financially material today, functioning as a powerful yield-booster for the overall book.17

The strategic logic flows directly from the customer base. The same rural micro-entrepreneurs SRG already serves — the grocer, the transport operator, the small trader — frequently need capital not for a house but for the business: working capital to stock up before a festival season, funds to buy a second truck, money to expand the shop. Banks, once again, won't touch them. So they do the obvious thing: they pledge the self-constructed home they already own as collateral and take a Loan Against Property. SRG, having already underwritten these families and understood their cash flows, is uniquely positioned to make those loans.

And the yields are even richer than the core book — often reaching 23% to 24%.1 Which raises an obvious question: if LAP is so profitable, why not do more of it? The answer reveals management discipline. SRG deliberately caps LAP at under 30% of the overall book.1 The reason is that LAP is inherently more cyclical and more exposed to cash-flow shocks than a pure home loan. A family will starve before defaulting on the roof over their heads; they will not necessarily make the same sacrifice for a business loan when the business hits a rough patch. So LAP is treated as a high-margin optionality engine — a source of extra spread that is allowed to enhance the story but never to crowd out the core mortgage book that anchors the whole company's risk profile.

The economics of this arrangement are quietly beautiful, and they come down to operating leverage. The expensive infrastructure of this business — the branches, the credit officers on motorcycles, the collection teams walking from village to village — is already paid for by the core housing operation. Every incremental LAP loan written runs through that same already-funded machinery. There is little additional fixed cost; the extra margin drops almost straight to the bottom line. This is what helps drive SRG's return on assets to an estimated 3.12% — a strong figure for any lender, and a direct consequence of layering a high-yield product on top of an infrastructure that's already been paid for.17 The result is a business throwing off healthy returns and accumulating capital. The next question is what management does with that capital — and here the story turns ambitious.

VIII. Capital Deployment & M&A Philosophy

A profitable lender generates a pleasant problem: capital piles up, and management has to decide how to deploy it. SRG's recent moves show a company deliberately building a war chest and then signaling, in unusually direct language, what it intends to do with it.

The capital-building came in two steps. In January 2025, SRG executed a critical equity raise of ₹499.3 million — roughly ₹50 crore — issuing new shares to strengthen its balance sheet.1 It followed this with a ₹35 crore non-convertible debenture issuance in late 2025, adding debt capital on top of the fresh equity.1 These were not desperate, dilutive scrambles for survival; they were tactical reinforcements of a balance sheet preparing to grow.

The clearest evidence of that intent is the capital adequacy ratio — the regulatory measure of how much loss-absorbing capital a lender holds against its risk-weighted loans. After the raises, SRG's CRAR stood at a fortress-like 38.62% as of March 2026.17 To put that in perspective, the regulatory minimum for housing finance companies is a fraction of that. Carrying nearly 39% is not an accident or inefficiency; it is dry powder. A capital ratio that high means the company can roughly double or triple its loan book before it would even need to think about raising more equity. SRG is loaded for expansion.

And the expansion is already underway, on two fronts. The first is geographic. Historically, SRG's strongholds have been in western India — Rajasthan and Gujarat, which together still drive roughly 77% of the book.1 The company is now pushing deliberately into the high-growth, fiercely competitive states of southern India: Andhra Pradesh, Telangana, Karnataka, and Tamil Nadu.1 The logic is that the cash-appraisal model, proven in the villages of Rajasthan, should travel — the southern states are wealthier on average, with their own large populations of undocumented self-employed who are equally invisible to the banks.

The second front is the one that should make investors sit up. In its May 2026 earnings communications, management made a notably explicit statement: it is actively prioritizing "M&A and inorganic portfolio opportunities" to accelerate the company's march toward a ₹1,500 crore AUM target for FY27.1 For a company this size to openly declare an appetite for acquisitions is significant. It tells you management has concluded that building branch-by-branch in unfamiliar southern states organically would simply be too slow — and that buying an existing, seasoned regional loan book might be a faster route to scale.

It's worth framing this against the industry's history of consolidation. The cautionary tale every Indian finance investor knows is Piramal's acquisition of the distressed Dewan Housing Finance — a massive, complex, legacy-ridden book bought out of bankruptcy. SRG's ambitions are nothing like that in scale; what it is hunting for is small, high-yield regional portfolios in the south, the kind of bolt-on books it could absorb and re-underwrite. But the danger in any acquisition is the same one that has humbled far larger acquirers: valuation, and fit. If SRG overpays for a southern portfolio, it dilutes the very return metrics that make it special. Worse, if it acquires a book that was underwritten using relaxed, "salaried" credit standards rather than SRG's battle-tested low-LTV cash-appraisal discipline, it could import asset-quality problems that its own organic book has never had. An acquired loan is only as good as the underwriting that created it — and SRG's entire edge is its underwriting. Buying someone else's looser underwriting could undo the thing that makes the company worth studying. Which is exactly why it's worth formally examining what that edge consists of, and how durable it really is.

IX. Strategic Position: Porter's 5 Forces & Hamilton's 7 Powers

So far we've described what SRG does. Now let's war-game why it can keep doing it — whether its advantages are real moats or merely a head start that competitors will eventually erase. Two frameworks help here: Hamilton Helmer's Seven Powers, which catalogs the genuine sources of durable competitive advantage, and Michael Porter's Five Forces, which maps the structural pressures on an industry. Applied to rural underwriting, they reveal a business that is better defended than its size suggests.

Hamilton's 7 Powers Applied to SRG

The primary power SRG enjoys is Counter-Positioning — and it is the heart of the whole defense. Counter-positioning exists when an incumbent cannot copy a newcomer's business model without damaging its own existing business. The large commercial banks — SBI, HDFC Bank and their peers — simply cannot replicate SRG's cash-appraisal model, and the reason is structural, not a matter of effort. Their entire institutional machinery is built around digital footprints, tax filings, and standardized bureau scores. If a major bank tried to send a high-cost credit officer to sit in a village for an afternoon counting customers at a grocery shop to underwrite a ₹6 lakh loan, the operating cost of that exercise would exceed the interest the loan could ever earn. The banks' cost structures, designed for ₹50 lakh urban loans, make the rural micro-mortgage uneconomic for them by definition. They are not lazy or unaware; they are structurally locked out. That lockout is SRG's shield.

The second power is Scale Economies — but of an unusual, local kind. SRG does not have national scale; it has regional density. Within Rajasthan and Gujarat, its network of 96-plus branches creates genuine operating efficiencies that a thinly-spread competitor cannot match.1 A collection officer can cover several adjacent villages on a single motorcycle trip, keeping per-loan collection costs low, and the dense local presence creates a kind of vigilance moat — the company is simply around, visible, known, watching, in a way that deters delinquency. Density in a defined territory beats sparse presence across a wide one.

The third power is a Cornered Resource: data. Over more than two decades of operating in Rajasthan, SRG has accumulated a proprietary understanding of cash-flow patterns across dozens of micro-industries — regional crop cycles, the seasonal margins of local handicrafts, the rhythms of village trade.1 This is not a database you can buy; it is qualitative, experiential knowledge encoded in the company's underwriting practices and its veteran officers' judgment. A newcomer with capital can build branches, but it cannot instantly acquire twenty-four years of learning about which rural cash flows are real and which are mirages. That accumulated wisdom is genuinely hard to replicate.

Porter's 5 Forces Analysis

Turning to the structural forces, the picture is more mixed — and honest analysis requires acknowledging where SRG is weak as well as strong.

The Power of Suppliers is high, and this is SRG's real vulnerability. The company's "suppliers" are the providers of its raw material: capital. SRG depends on wholesale bank term loans and NHB refinance, and because it lacks a public deposit-taking license and carries only a BBB+ rating, its cost of borrowing — that 10.88% — is a structural drag.17 When macro liquidity tightens and banks grow cautious about lending to small NBFCs, SRG feels it acutely. Its suppliers hold meaningful power over it.

The Power of Buyers, by contrast, is low — and this is the source of all that yield. SRG's borrowers, the rural unorganized, have extremely limited alternatives. They value speed, trust, and simple documentation far above interest rate, and they are highly insensitive to pricing.1 When the buyer can't easily go elsewhere and doesn't haggle hard on rate, the lender keeps the margin. This is the mirror image of the prime market, where rate-shopping borrowers compete lenders down to nothing.

Rivalry is moderate-to-high. While the banks are counter-positioned out of the segment, SRG does face real competition from regional affordable-housing specialists like Aavas Financiers and a long tail of regional NBFCs.1 But here the structure is forgiving: the rural housing market in India is so vast and so underpenetrated that there is room for many players to grow simultaneously without resorting to destructive price wars. The pie is expanding faster than the competitors can eat it. For now, rivalry tempers SRG's growth but does not threaten its margins. With the competitive map drawn, we can step back and extract the transferable lessons.

X. Playbook: Business & Investing Lessons

Strip away the specifics of Rajasthan and rural India, and SRG offers a handful of durable lessons that travel well beyond housing finance.

The first lesson: loan-to-value is the ultimate underwriting truth. In undocumented credit, your assessment of a borrower will never be perfect — you are reading cash boxes and ledger books, not audited statements, and some of your judgments will be wrong. The way you protect yourself is not by pretending to perfect information but by demanding a thick collateral margin. By lending only around 40% of a home's value, SRG makes the borrower a co-investor in the risk, with far more of his own money at stake than the lender's. When you cannot fully trust the information, trust the structure. The margin of safety does the work that perfect underwriting cannot.

The second lesson: do not fear a high cost of funds if you have pricing power. Many analysts take one look at SRG's 10.88% borrowing cost and recoil — surely that's a sign of a fragile, sub-scale business. But that instinct confuses absolute cost with spread, and on the micro-mortgage frontier, spread is what matters.17 A company that borrows at 11% and lends at 22% is structurally far healthier than a prime lender borrowing at 7% and lending at 8.5%. The expensive money is not the problem; the question is always what you can earn on top of it. Pricing power, not cheap funding, is the scarcer and more valuable asset.

The third lesson is a caution about growth itself: beware the gestation trap of organic geographic expansion. Building new branches in unfamiliar states like Karnataka and Andhra Pradesh takes time and money, and new branches lose money during their long "gestation" period before they mature into profitability. This is precisely why a successful regional player, hungry for national scale, is so often tempted toward acquisitions instead — buying a seasoned book skips the gestation pain. But that shortcut carries its own peril, and the lesson comes with a warning attached: inorganic expansion must be executed with extreme valuation discipline, because the wrong acquisition can destroy in one transaction the credit quality built over decades. These lessons set up the central tension every investor in SRG must weigh — the bull case and the bear case.

XI. Analysis & Bear vs. Bull Case

Every compelling small-cap story is really an argument between two plausible futures. For SRG, both the optimistic and the pessimistic cases are grounded in the same facts; they simply weight the risks and the opportunities differently. Let's give each its full due.

The Bull Case

The optimist's argument starts with the southern flight. If the branch expansion and the newly-announced acquisition strategy succeed, SRG can clone its highly profitable Rajasthan playbook into the wealthier southern states — Tamil Nadu, Andhra Pradesh, and their neighbors — where the same population of undocumented self-employed sits unserved by banks. Do that successfully, and the company's ₹1,500 crore AUM target for FY27 looks not just achievable but conservative.1

The second pillar of the bull case is a rating arbitrage. Recall the physics of borrowing: as AUM crosses the next thresholds and the book seasons, a credit-rating upgrade from BBB+ to A- becomes plausible.45 Such an upgrade would shave perhaps 100 to 150 basis points off the cost of borrowing — and because that saving flows straight into the spread, it would expand the net interest margin and return on equity dramatically. In a high-spread business, a cheaper liability is pure profit. This is the single most powerful lever in the entire investment case: the same loan book, financed more cheaply, simply prints more money.

The third pillar is the digital scale multiplier. If the "SRG SRAJAN" re-engineering project genuinely succeeds in digitizing collections and file management, it would drive down operating expenses and push the cost-to-income ratio below 35%, allowing the company to grow the book without growing costs proportionally.1 Automation layered on top of a high-margin business is how a regional lender becomes a national compounder.

The Bear Case

The pessimist begins where the bull's geography ends: regional concentration risk. Despite all the talk of southern expansion, the book today remains heavily concentrated in the Rajasthan-Gujarat corridor, which still drives around 77% of assets.1 A severe regional shock — a serious agricultural drought, a local regulatory disruption, a collapse in some key rural micro-industry — would hit the cash flows of a large slice of the borrower base all at once. Concentration is fine until the day it isn't.

The second bear argument is M&A indigestion — and it is the mirror image of the bull's acquisition optimism. The very strategy that could accelerate growth could also destroy the company's crown jewel. Overpay for a southern portfolio, or fail to integrate a legacy book underwritten to looser standards, and the pristine credit track record could crack, with NPAs rising as acquired loans sour. The thing that makes SRG special — its disciplined underwriting — is exactly the thing an ill-judged acquisition would put at risk.

The third bear concern is the funding squeeze, which flows directly from the high supplier power we identified earlier. SRG's growth engine runs on borrowed wholesale capital. If macro interest rates rise sharply, or if banks broadly retreat from lending to small-cap NBFCs — as they periodically do when sentiment sours — SRG's access to debt could freeze, and the growth machine would stall regardless of how strong rural loan demand remains. A lender that cannot borrow cannot lend, no matter how good its borrowers are.

The 3 KPIs to Watch

Cutting through the noise, three metrics matter most for tracking how this story actually unfolds — and a long-term holder should watch these and largely ignore the rest.

The first is the AUM growth rate: is the book on track toward the ₹1,500 crore FY27 target, and is that growth coming from healthy organic origination and well-priced acquisitions rather than reckless lending? Growth is the headline thesis, and this is its scoreboard.

The second is the net interest margin: is the NIM holding stable above 11%, or is a rising cost of borrowing quietly compressing the spread? The entire economic case rests on that fat margin; the day it starts narrowing meaningfully is the day the story changes.

The third is the gross NPA specifically within the LAP segment: because LAP is the more cyclical, more shock-prone book, it will show stress before the core housing book does. Watching whether LAP defaults stay benign relative to the core is the earliest warning system for the whole portfolio's health.

XII. Epilogue & Outro

The story of SRG Housing Finance is, in the end, a story about who gets to participate in the formal economy. An Udaipur family looked at the millions of rural Indians the banking system had written off as unbankable — the milk sellers, the grocers, the small traders with stable cash and no paperwork — and built, patiently, over more than two decades, a method for lending to them safely and profitably. They did it not by taking wild risks but by being more conservative on collateral than the banks that wouldn't lend at all, and more diligent on the ground than any algorithm could be.

For a long-term investor, SRG represents something rare: a pure play on India's financial-inclusion story, and living proof that in the right hands, rural mortgage lending is not a charity case or a time bomb but one of the most profitable, defensive, and scalable niches in emerging-markets finance. Whether the family can carry that frontier model south, and absorb the temptations and dangers of acquisition without losing the discipline that made it work, is the open question. The next few years — and those three KPIs — will tell.

References

-

SRG Housing Finance — Company Overview, Business Segments, History and Financials ↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩

-

BSE Stock Quote and Corporate Filings — SRG Housing Finance Ltd (SRGHFL / 534680) ↩↩

-

Acuité Ratings & Research — SRG Housing Finance Credit Rating Report, 2026-04-15 ↩↩

-

CARE Ratings — SRG Housing Finance Credit Rating Report, 2025-11-20 ↩↩

-

National Housing Bank — Registered Housing Finance Companies ↩

-

Financial Profile & Ratios — SRG Housing Finance, Screener India ↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube