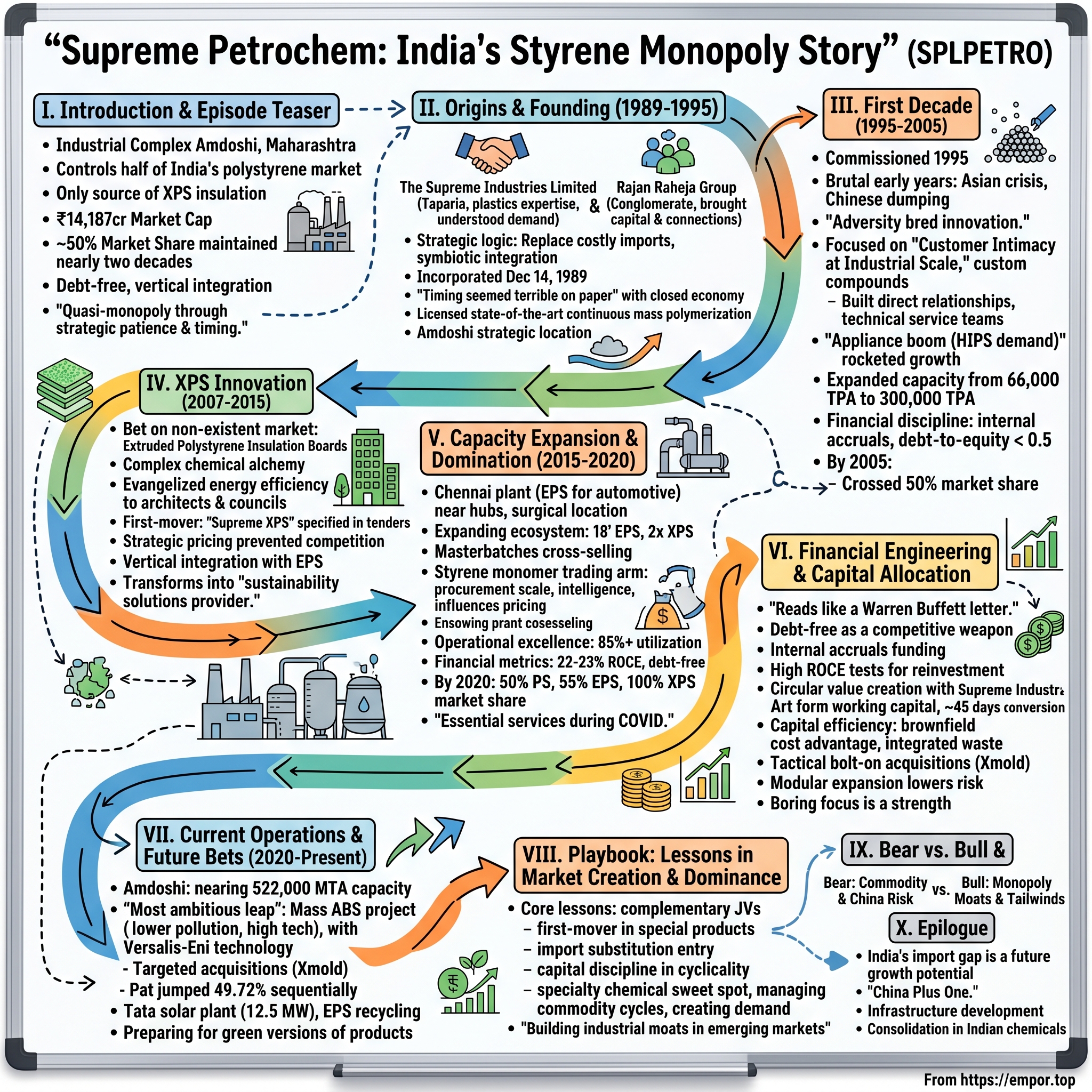

Supreme Petrochem: India's Styrene Monopoly Story

I. Introduction & Episode Teaser

Picture this: A nondescript industrial complex in Amdoshi, Maharashtra, where massive reactors hum 24/7, transforming benzene and ethylene into styrene monomers, then into tiny polystyrene beads that will become everything from yogurt cups to television casings. This isn't Silicon Valley glamour—it's the unglamorous backbone of modern life. Yet this single facility controls half of India's polystyrene market and represents the country's only source of extruded polystyrene insulation boards.

Welcome to Supreme Petrochem Limited, a company that turned a commodity chemical business into a quasi-monopoly through strategic patience, technical mastery, and impeccable timing. With a market capitalization of ₹14,187 crore, revenues touching ₹5,836 crore, and profits of ₹350 crore, SPL has quietly built one of India's most dominant market positions in specialty chemicals—all while remaining virtually debt-free.

The hook that makes this story fascinating? In an industry where Chinese competitors can flood markets overnight and oil price swings can evaporate margins, Supreme Petrochem has maintained 50% market share for nearly two decades. They've done it not through regulatory protection or government contracts, but through a playbook of vertical integration, first-mover advantages, and the kind of operational excellence that would make Toyota engineers nod in approval.

This is the story of how a joint venture between a plastics processor and a real estate conglomerate became India's styrene kingpin—and what it tells us about building industrial moats in emerging markets. It's about recognizing that sometimes the best businesses aren't sexy; they're essential. And in Supreme Petrochem's case, essentially irreplaceable.

II. The Power of Partnership: Origins & Founding (1989-1995)

The Berlin Wall had just fallen. India's economy was still two years away from liberalization. And in a Bombay boardroom in December 1989, two unlikely partners were sketching out plans for a petrochemical venture that would eventually dominate an entire industry.

On one side sat representatives from The Supreme Industries Limited, a plastics processing company that had been quietly building since 1942—nearly five decades of learning every nuance of polymer processing, from PVC pipes to plastic furniture. They understood demand intimately; they knew what manufacturers needed because they were manufacturers themselves. The company's founder, Khemchand Taparia, had built Supreme Industries from a small trading operation into India's largest plastics processor by focusing on one principle: control your raw materials, control your destiny.

Across the table sat the Rajan Raheja Group, a conglomerate so diversified it seemed to have a finger in every pie of India's economy—automobile batteries, cement, ceramic tiles, software, cable television, hotels, real estate. The Rahejas brought something Supreme Industries desperately needed: capital, connections, and the kind of diversified cash flows that could weather the cyclical storms of commodity chemicals.

The strategic logic was elegant. Supreme Industries was spending millions importing polystyrene for its manufacturing operations. Every shipment from Korea or Singapore meant forex outflows, shipping delays, and quality uncertainties. Meanwhile, the Rahejas saw an opportunity to enter a high-growth sector with a partner who understood the market inside-out. It wasn't just vertical integration—it was symbiotic integration.

On December 14, 1989, Supreme Petrochem Limited was incorporated. The timing seemed terrible on paper. India's economy was closed, industrial licenses were nightmarish to obtain, and the global petrochemical industry was dominated by giants like BASF and Dow Chemical who could crush local players with scale alone. But the founders saw what others missed: India's consumption of polystyrene was growing at 15% annually, almost entirely served by imports. The opportunity wasn't to compete globally—it was to replace imports locally.

The joint venture structure itself was fascinating. Rather than a simple equity split, the partners created interlocking value chains. Supreme Industries would guarantee offtake for a significant portion of production, providing revenue visibility. The Raheja Group would leverage its real estate and construction businesses to create demand for insulation products. Both would share technology sourcing and capital deployment decisions. It was industrial strategy as jazz improvisation—each partner playing their strengths while maintaining harmony.

Between 1989 and 1995, while the plant was being constructed, India underwent its most dramatic economic transformation since independence. The 1991 liberalization opened markets, reduced tariffs, and suddenly made their import-substitution strategy even more critical. Foreign competitors could now enter India more easily, but so could foreign technology. SPL licensed state-of-the-art continuous mass polymerization technology, becoming one of the few plants globally to use this process—more efficient, less waste, better economics.

The Amdoshi site selection itself was strategic brilliance. Located in Maharashtra's chemical belt, close to ports for raw material imports, near automotive and appliance manufacturing hubs for customers, with access to skilled chemical engineers from nearby institutes. Every decision reflected a deeper understanding: this wasn't just about making chemicals cheaper—it was about making them better, faster, and closer to customers than any importer ever could.

III. The First Decade: Building the Foundation (1995-2005)

The first polystyrene pellets rolled off the production line at Amdoshi in 1995, marking the beginning of what would become a methodical march toward market dominance. The initial capacity of 66,000 tonnes per annum seemed modest—global plants were producing millions of tonnes. But SPL's founders understood something fundamental about emerging markets: you don't need to be the biggest globally, you need to be the most responsive locally.

The early years were brutal. Asian financial crisis of 1997 sent raw material prices spiraling. Chinese manufacturers, recovering from their own economic reforms, began dumping products at prices below SPL's production costs. One former executive recalled nights spent recalculating break-even points as styrene monomer prices swung 30% in a month. "We were essentially running a chemical plant and a commodity trading desk simultaneously," he noted.

But adversity bred innovation. Unable to compete on price alone, SPL pioneered something revolutionary for Indian chemicals: customer intimacy at industrial scale. While importers offered standard grades on 60-day delivery schedules, SPL created custom compounds for specific applications—a slightly different melt flow for a Pune injection molder, a modified impact resistance for a Delhi toy manufacturer. The sales team wasn't just taking orders; they were sitting in customers' factories, understanding their processes, solving their problems.

The distribution strategy was equally unconventional. Instead of relying solely on traders—the traditional model in Indian chemicals—SPL built direct relationships with end-users. They created technical service teams that would visit customer plants, troubleshoot processing issues, even train operators. When a major appliance manufacturer complained about surface defects, SPL's engineers spent three weeks on their shop floor, eventually modifying the polymer structure to eliminate the problem. That manufacturer never imported polystyrene again.

By 2000, just five years after commissioning, SPL had captured 30% market share. But the real breakthrough came from an unexpected source: the Indian appliance boom. As washing machines, refrigerators, and air conditioners became middle-class aspirations, demand for high-impact polystyrene exploded. SPL was the only domestic manufacturer who could guarantee consistent quality and supply. Imports meant forex approvals, shipping delays, inventory costs—SPL offered same-week delivery from local warehouses.

The numbers tell the story: capacity expanded from 66,000 TPA to 150,000 TPA by 2002, then to 300,000 TPA by 2005. But more importantly, product grades multiplied from 5 to over 50. General purpose polystyrene for disposables, high-impact polystyrene for appliances, expandable polystyrene for packaging—each grade optimized for specific applications, each creating switching costs for customers who had redesigned processes around SPL's products.

The financial discipline during this period was remarkable. Despite aggressive capacity expansion, debt-to-equity never exceeded 0.5. Every expansion was funded through internal accruals, a practice that would become SPL's hallmark. The company was essentially using customer prepayments and rapid inventory turns to fund growth—a negative working capital model in a capital-intensive industry.

By 2005, SPL had crossed 50% market share, becoming the undisputed leader in Indian polystyrene. The Amdoshi plant had grown into one of Asia's largest single-location PS facilities. But more than scale, SPL had built something harder to replicate: a network of relationships, technical capabilities, and market knowledge that made them not just a supplier, but an essential partner to India's manufacturing ecosystem. The foundation was set for the next phase—moving from market leader to market creator.

IV. The XPS Innovation: First Mover Advantage (2007-2015)

In 2007, while India was riding high on 9% GDP growth and construction cranes dotted every urban skyline, SPL's leadership made a bet that seemed bizarre to industry observers: they would invest millions in a product category that didn't exist in India—extruded polystyrene insulation boards.

The decision emerged from an unlikely source. A board member, returning from a green building conference in Singapore, presented a startling fact: buildings consumed 40% of global energy, mostly through heating and cooling losses. In India, with its extreme temperatures and energy deficits, the opportunity seemed obvious. Yet no Indian manufacturer had attempted XPS production. The technology was complex, the market was non-existent, and established European producers like BASF and Dow were already eyeing India.

SPL's technical team spent eighteen months in stealth mode. Engineers were sent to Germany and Japan, studying extrusion processes, foaming agents, cell structures. The challenge wasn't just technical—it was chemical alchemy. XPS required forcing styrene polymer through a carefully controlled extrusion process while injecting blowing agents that would create millions of tiny, uniform cells. Too much pressure and the board would collapse; too little and insulation properties would fail. The process demanded precision at micron levels in an industry accustomed to millimeter tolerances.

The first XPS board rolled out in late 2007, making SPL India's first and only producer. But having a product meant nothing without a market. What followed was a masterclass in market creation. SPL didn't just sell insulation boards; they evangelized energy efficiency. Technical teams conducted thermal audits for architects, showing how XPS could reduce air conditioning loads by 30%. They partnered with green building councils, becoming registered suppliers for IGBC and GRIHA certifications. Sales engineers attended architectural colleges, educating the next generation about building envelope design.

The early adopters were predictable—five-star hotels, IT campuses, premium residential projects where energy costs mattered and green certifications provided marketing premiums. But SPL's genius was in expanding the market beyond premium segments. They developed different grades for different applications—high-compression XPS for parking decks, moisture-resistant variants for basements, specialized profiles for cold storage. Each application opened new market segments.

The timing proved prescient. India's green building movement, nascent in 2007, exploded by 2010. The Indian Green Building Council's registered projects grew from 500 to 5,000 in five years. Every project needed insulation, and SPL was the only domestic source. Imports existed but came with 40% duties, long lead times, and no technical support. SPL offered immediate delivery, on-site training, and customization that foreign suppliers couldn't match.

The monopoly dynamics created fascinating pricing power. XPS boards commanded 40-50% gross margins compared to 20-25% for commodity polystyrene. But SPL resisted the temptation to maximize short-term profits. Prices were kept just high enough to earn superior returns but low enough to discourage new entrants. It was strategic pricing at its finest—extracting value while protecting the moat.

By 2012, SPL's XPS capacity had expanded three times, yet still couldn't meet demand. Orders were booked months in advance. Construction companies began specifying "Supreme XPS" in tender documents, creating a brand pull rare in B2B chemicals. The product that didn't exist five years earlier was now generating 15% of SPL's profits despite being less than 5% of volumes.

The innovation had broader implications. XPS production used expandable polystyrene as raw material—a product SPL already manufactured. This vertical integration created cost advantages no competitor could match. Moreover, XPS technology expertise opened doors to other foam applications—technical insulation for refrigeration, flotation boards for marine applications, specialized packaging for pharmaceuticals. Each niche application further strengthened the monopoly.

The environmental narrative added another layer of moat. As India committed to emission reductions under various climate accords, building insulation became not just economically sensible but regulatorily necessary. SPL positioned itself as enabling India's climate commitments—a powerful narrative for investors, customers, and regulators alike. The XPS innovation transformed SPL from a commodity chemical producer to a sustainability solutions provider, commanding valuation multiples that reflected this evolution.

V. Capacity Expansion & Market Domination (2015-2020)

By 2015, the Amdoshi complex had evolved into something resembling a petrochemical city—422,000 metric tonnes of annual capacity spread across multiple plants, each interconnected through a maze of pipelines carrying styrene monomer, the lifeblood of the operation. But SPL's leadership knew that in chemicals, standing still meant falling behind. What followed was an expansion strategy that would cement their dominance for the next decade.

The Chennai plant decision in 2015 revealed sophisticated strategic thinking. Rather than simply adding capacity at Amdoshi, SPL chose Manali New Township near Chennai for their second expandable polystyrene facility. The location was surgical—Chennai's proximity to South India's automotive hub meant shorter delivery times to Hyundai, Ford, and Renault suppliers. The 33,000 MTA facility was designed specifically for automotive-grade EPS, with clean rooms and quality controls that met stringent automotive specifications.

But the real masterstroke was the timing. The expansion coincided with the government's push for "Make in India" and new automotive safety regulations requiring better packaging for components. SPL wasn't just adding capacity; they were pre-positioning for regulatory-driven demand that wouldn't fully materialize for another two years. When it did, SPL was the only supplier with automotive-certified capacity ready to go.

The board's 2018 decision to add another 30,000 MTPA of expandable polystyrene, double XPS capacity to 100,000 cubic meters, and increase masterbatch capacity by 50,000 MTA seemed aggressive to analysts. The street worried about overcapacity in a cyclical industry. But SPL's management saw what others missed: they weren't just expanding similar products—they were completing an ecosystem.

The masterbatch expansion, in particular, was brilliant. Masterbatches—concentrated color and additive compounds—were high-margin products that leveraged the same customer relationships but served different needs. A refrigerator manufacturer buying white HIPS could now source antimicrobial masterbatches for food-contact applications from the same supplier. It was classic cross-selling, but with industrial chemicals.

The import trading business for styrene monomer, often overlooked by analysts, became a strategic weapon during this period. SPL didn't just import for their own consumption—they became one of India's largest styrene traders, selling to smaller manufacturers. This gave them three advantages: scale in procurement driving lower costs, market intelligence on competitor activities, and the ability to influence industry pricing. When styrene prices spiked in 2017, SPL's trading arm actually generated higher profits than some manufacturing divisions.

The operational excellence during this expansion was remarkable. Despite adding 150,000 MTA of capacity across products, plant utilization never dropped below 85%. This wasn't luck—it was meticulous planning. Capacity was added in modules, each commissioned only when forward order books justified it. New lines were designed for flexibility—able to switch between grades with minimal downtime. The Amdoshi plant could produce twenty different grades simultaneously, a complexity that would cripple most chemical operations but which SPL had mastered through two decades of experience.

Financial metrics during this period defied industry norms. While global chemical companies averaged 12-15% ROCE, SPL consistently delivered 22-23%. The secret was capital efficiency—brownfield expansions cost 40% less than greenfield projects, shared utilities reduced operating costs, and integrated operations meant waste from one process became feedstock for another. The company remained debt-free throughout, funding the entire expansion through internal accruals while maintaining dividend payouts above 40%.

Market share statistics by 2020 were staggering: 50% in polystyrene, 55% in expandable polystyrene, 100% in XPS boards. But more importantly, SPL had become systemically important to Indian manufacturing. When COVID-19 struck and supply chains shattered, SPL kept running. They were deemed essential services, supplying packaging for pharmaceuticals, components for medical devices, insulation for vaccine cold chains. The pandemic, rather than disrupting their dominance, actually reinforced it—customers who had flirted with imports came back to the reliability of domestic supply.

VI. Financial Engineering & Capital Allocation

In the testosterone-fueled world of petrochemicals, where competitors leverage themselves to the hilt chasing scale, Supreme Petrochem's capital allocation strategy reads like a Warren Buffett letter: boring, disciplined, and devastatingly effective.

The debt-free status isn't just a balance sheet curiosity—it's a competitive weapon. During the 2018 IL&FS crisis when Indian credit markets froze, chemical companies dependent on working capital loans saw operations grind to a halt. SPL, flush with cash, actually extended credit terms to customers, gaining market share while competitors scrambled for liquidity. One CFO of a competing firm admitted privately: "They turned their balance sheet into a market-share acquisition tool."

The capital allocation framework is deceptively simple. Every rupee of profit faces three tests: Can it generate over 20% ROCE if reinvested? Will it strengthen the core moat? Can shareholders deploy it better themselves? This framework led to fascinating decisions. In 2019, when private equity firms offered to fund a ₹2,000 crore overseas acquisition, SPL walked away. The acquisition would have doubled revenues but diluted returns. Instead, they announced a ₹300 crore buyback, signaling confidence while returning cash to shareholders.

The dividend policy—maintaining 40-50% payout ratios—seems generous for a growth company. But it serves a strategic purpose. The Supreme Industries, holding 61.08%, receives substantial dividends which it redeploys across its ecosystem, creating demand for SPL's products. It's circular value creation—cash flows from SPL fund Supreme Industries' expansion, which increases demand for SPL's polymers, which generates more cash flows. The Raheja Group's stake provides similar ecosystem benefits through their real estate and construction ventures.

Working capital management at SPL is an art form. Despite being in a commodity business with volatile raw material prices, cash conversion cycles average just 45 days. The secret lies in the business model architecture. Styrene monomer—70% of costs—is imported on 180-day letters of credit. Finished goods are sold on 30-60 day terms. SPL essentially uses supplier credit to fund operations, generating negative working capital during growth phases. It's the chemical industry equivalent of Dell's famous cash flow model.

The ROCE consistency—22.8% through cycles—deserves deeper analysis. Most chemical companies show volatile returns as commodity prices swing. SPL's stability comes from three sources: product mix optimization (shifting to higher-margin grades during downturns), cost flexibility (variable cost structure allows quick adjustments), and pricing discipline (maintaining spreads rather than absolute prices). The company essentially runs a spread business disguised as a manufacturing operation.

The recent acquisition strategy reveals evolved thinking. Rather than big-bang acquisitions, SPL prefers tactical bolt-ons. The Xmold Polymers acquisition brought specialized automotive compounds technology. Small investment, high strategic value. They're not buying revenues; they're buying capabilities that would take years to develop organically. Each acquisition is funded entirely from cash, integrated within quarters, and accretive to returns immediately.

The capital expenditure philosophy is equally disciplined. SPL follows a "modular expansion" approach—adding capacity in 25,000-30,000 MT increments rather than massive 100,000 MT plants. This reduces execution risk, allows demand-matching, and preserves capital efficiency. The latest Mass ABS project, adding 70,000 MTPA by March 2025, is being executed in three phases, with each phase self-funding the next through generated cash flows.

What's remarkable is what SPL doesn't do with capital. No unrelated diversification, no trophy assets, no financial engineering through complex structures. In an era of conglomerates chasing everything from fintech to renewable energy, SPL remains boringly focused on styrene polymers. This focus might seem limiting, but it's precisely what enables their returns. Every rupee of capital deployed benefits from twenty-five years of accumulated expertise, relationships, and operational knowledge.

VII. Current Operations & Future Bets (2020-Present)

The pandemic changed everything for chemical companies, but for Supreme Petrochem, it was validation of a twenty-five-year strategy. While global supply chains collapsed and competitors scrambled for containers, SPL's Amdoshi complex hummed along, designated as essential services, supplying critical polymers for vaccine cold chains, pharmaceutical packaging, and medical devices. The crisis that broke others made SPL stronger.

Today's Supreme Petrochem operates at a scale that would have seemed fantastical to its 1995 founders. The Amdoshi complex, approaching 522,000 MTA capacity with the imminent Mass ABS commissioning, represents one of Asia's largest integrated styrenics facilities. The first phase of the Mass ABS project with 70,000 MTPA capacity is expected to be completed by March 2025, which along with the EPS Phase II expansion will take overall capacity at Amdoshi complex to 522,000 MTA.

The ABS project represents SPL's most ambitious technological leap yet. The Mass ABS process is clean and environmentally friendly compared to conventional emulsion process, due to elimination of water pollution. Partnering with Versalis-Eni for technology, SPL isn't just adding capacity—they're entering a new product category that commands premium pricing in automotive and electronics applications. The product has very low volatiles (odour free), high whiteness index and low gel count, all of this making it suitable for technical applications in automobile interiors.

The strategic acquisition of Xmold Polymers signals evolved thinking about growth. Rather than massive acquisitions that dilute returns, SPL is making targeted capability additions. Xmold brings specialized automotive compounds expertise—critical as India's automotive industry shifts toward electric vehicles requiring new material specifications. It's not about buying revenues; it's about acquiring knowledge that would take years to develop organically.

The petrochemicals company reported a decline of 18.71 per cent year-on-year in its profit after tax (PAT), at ₹106.9 crore, compared to ₹131.5 crore reported during the same quarter of the previous fiscal year. However, the PAT has jumped 49.72 per cent on a sequential basis, from ₹71.35 crore reported in Q3FY25. While the headline numbers might concern some investors, the sequential improvement and management's projection of 13% volume growth for FY26 reflect the underlying strength of the business model.

The sustainability initiatives aren't greenwashing—they're strategic positioning. SPL has setup a 12.5 MW solar power plant in joint venture with Tata Renewable Energy Ltd. to reduce its reliance on conventional energy sources. The EPS recycling program addresses the circular economy mandates that will inevitably tighten. SPL is pre-positioning for a world where environmental compliance becomes a competitive advantage, not a cost center.

The operational complexity SPL manages daily would overwhelm most chemical companies. Twenty different product grades running simultaneously, custom compounds for hundreds of customers, just-in-time delivery to automotive plants, technical support teams embedded at customer sites—this isn't commodity chemical production, it's industrial ballet. The fact they do it while maintaining 85%+ utilization rates and 22%+ ROCE speaks to operational excellence that's been refined over decades.

What's fascinating about SPL's current phase is the optionality being created. The ABS platform opens doors to engineering plastics. The masterbatch expansion enables entry into specialty additives. The XPS monopoly could extend into technical insulation applications. Each move creates platforms for future growth without betting the company on any single initiative. It's growth through calculated iteration rather than revolutionary disruption.

The market dynamics remain favorable. India's per capita plastic consumption at 13 kg remains a fraction of the global average of 45 kg. As income levels rise and manufacturing localizes, demand for specialty polymers will multiply. SPL isn't just riding this wave—they're positioned to capture disproportionate value through their established moats and expanding capabilities.

VIII. Playbook: Lessons in Market Creation & Dominance

After analyzing Supreme Petrochem's journey from a 66,000 TPA startup to India's styrene monopoly, several strategic principles emerge that transcend the chemical industry. This isn't just about making polymers—it's about building industrial moats in emerging markets.

The Power of Complementary Joint Ventures

The Supreme Industries-Raheja Group partnership worked because each partner brought irreplaceable assets. Supreme Industries provided market knowledge and guaranteed demand; Raheja brought capital and diversification. But the genius was in the structure—interlocking value chains that made separation economically irrational. Modern founders obsess about control; SPL's founders obsessed about alignment. The lesson: in capital-intensive industries, the right partner can be the difference between regional player and national champion.

First-Mover Advantage in Specialized Products

SPL's XPS monopoly demonstrates a counterintuitive truth: in emerging markets, it's often better to create a market than compete in an existing one. By investing in XPS when India had no demand, SPL didn't just capture first-mover advantage—they shaped the entire market's development. They wrote standards, trained architects, influenced regulations. By the time demand materialized, SPL wasn't just the incumbent; they were the industry infrastructure. The playbook: identify products that developed markets need but emerging markets haven't discovered, then evangelize aggressively.

Import Substitution as Market Entry

While economists debate import substitution's merits, SPL proved its tactical brilliance. Starting with import replacement provided immediate addressable market, customer relationships, and pricing benchmarks. But SPL went beyond simple substitution—they provided superior service, customization, and technical support that importers couldn't match. The strategy works when you solve the real pain points of imports (delivery uncertainty, customization difficulty, technical support absence) rather than just competing on price.

Capital Discipline in Cyclical Industries

Remaining debt-free in a capital-intensive, cyclical industry seems impossible, yet SPL achieved it through three principles: fund expansion through internal accruals, time capacity additions to demand visibility, and maintain operational flexibility to adjust costs quickly. The discipline to walk away from debt-funded acquisitions, even when private equity beckoned, preserved balance sheet strength that became a competitive weapon during credit crunches. The lesson: in cyclical industries, financial conservatism isn't limitation—it's optionality.

The Specialty Chemical Sweet Spot

SPL found the perfect position between commodities and specialties. Their products are specialized enough to avoid pure price competition but standardized enough to achieve scale. This "specialty commodity" positioning provides pricing power without the R&D burden of true specialty chemicals. The sweet spot exists in many industries—products that require technical expertise but serve broad markets.

Managing Commodity Cyclicality

Rather than fighting styrene monomer price volatility, SPL built a business model that thrives on it. The trading operation provides market intelligence and procurement scale. The spread-based pricing maintains margins regardless of absolute price levels. The flexible cost structure allows rapid adjustment to market conditions. Instead of hedging commodity risk, they architected a business model resilient to commodity cycles.

Creating Demand for New Categories

The XPS story reveals how to create markets, not just serve them. SPL didn't wait for demand; they manufactured it through education, standard-setting, and ecosystem development. They made XPS synonymous with green building in India, similar to how Intel made processors matter to consumers. The playbook: when introducing new product categories, sell the problem before selling the solution, make your product a symbol of a larger trend, and embed yourself in the ecosystem's infrastructure.

These principles explain why SPL commands a PE ratio of 28.68 versus the industry's 19.62—markets are valuing not just current earnings but the strategic moats that ensure future earnings. The playbook SPL developed for dominating Indian styrenics could be applied to any emerging market industry where import substitution, technical complexity, and market creation intersect.

IX. Bear vs. Bull Case Analysis

The Bull Case: Monopoly Moats and Structural Tailwinds

The bull thesis rests on a simple observation: SPL has built moats that would take competitors decades and billions to replicate. Start with the numbers—trading at a PEG ratio of 0.62, SPL offers growth at a reasonable price in a market where quality chemical companies routinely trade at PEG ratios above 1.0. The 50% market share in polystyrene and 100% monopoly in XPS aren't just statistics—they represent switching costs, technical barriers, and relationship moats that compound over time.

The capacity expansion trajectory provides clear growth visibility. With the Mass ABS project adding 70,000 MTPA in 2025 and another 70,000 MTPA planned, SPL is entering a ₹15,000 crore addressable market where they can leverage existing customer relationships and technical expertise. ABS commands 50-60% higher margins than commodity polystyrene—even capturing 20% market share would transform SPL's earnings profile.

India's construction and manufacturing boom provides multi-decade tailwinds. Building insulation will transition from optional to mandatory as energy codes tighten. The automotive industry's localization push means more components manufactured domestically, driving demand for engineering plastics. SPL sits at the intersection of these megatrends, with the infrastructure to capture disproportionate value.

The financial fortress—zero debt, 22.8% ROCE, consistent dividend payouts—provides resilience and optionality. During the next downturn, SPL can acquire distressed assets, extend customer credit, or accelerate capacity expansion while leveraged competitors struggle. This isn't just a balance sheet metric; it's a strategic weapon in a cyclical industry.

Management's execution track record deserves premium valuation. They've successfully navigated commodity cycles, executed complex capacity expansions, and maintained market leadership for two decades. The recent acquisition strategy—small, targeted, capability-adding—shows evolved capital allocation thinking. This isn't a management that will destroy value chasing growth.

The Bear Case: Commodity Exposure and Concentration Risks

The bear thesis starts with an uncomfortable truth: despite all the moats, SPL remains exposed to global styrene monomer prices, which can swing 30-40% in months. With raw materials comprising 70% of costs, margin compression during adverse cycles is inevitable. The recent quarterly results showing 18.71% PAT decline year-over-year, despite volume growth, illustrates this vulnerability.

China looms as the perpetual threat. Chinese chemical companies, backed by state capital and operating at massive scale, could flood Indian markets if domestic demand slows. While tariffs provide some protection, a determined Chinese push could erode margins across the industry. SPL's import substitution moat becomes a vulnerability if imports become dramatically cheaper.

The product concentration risk is real. Despite multiple grades and applications, SPL essentially makes variations of the same thing—styrene-based polymers. A technological disruption (bio-based alternatives, advanced recycling methods) or regulatory shift (single-use plastic bans extending to styrenics) could impact the entire product portfolio simultaneously.

Environmental regulations represent a slow-moving but inevitable challenge. Polystyrene recycling remains problematic, with less than 10% actually recycled globally. As circular economy mandates tighten and extended producer responsibility costs rise, SPL's core products could face structural headwinds. The XPS monopoly, while profitable today, could become a liability if building codes shift toward bio-based insulation.

Customer concentration, while not disclosed in detail, likely exists given the industrial nature of the business. Large appliance manufacturers, automotive companies, and construction firms probably account for significant revenue percentages. Losing a major customer or facing procurement pressure from consolidated buyers could impact profitability.

The valuation premium—PE of 28.68 versus industry average of 19.62—leaves little room for disappointment. Any execution stumbles, demand slowdown, or margin compression could trigger multiple compression. The market is pricing in flawless execution and continued market dominance—a dangerous assumption in a cyclical industry.

The Verdict: Quality at a Reasonable Price

The weight of evidence tilts bullish, but with caveats. SPL represents a high-quality business with sustainable competitive advantages trading at reasonable valuations given growth prospects. The monopoly positions, capacity expansion pipeline, and balance sheet strength provide multiple ways to win. However, investors must stomach commodity volatility and accept that earnings will be cyclical even if the business remains structurally sound.

The optimal approach might be accumulating during styrene price spikes when margins compress and sentiment sours, then holding through cycles. SPL isn't a buy-and-forget compounder—it's a high-quality cyclical requiring active monitoring but offering superior through-cycle returns for patient investors who understand the business dynamics.

X. Epilogue: The Future of Specialty Chemicals in India

As we conclude this deep dive into Supreme Petrochem's remarkable journey, it's worth zooming out to consider what this story tells us about India's industrial future and the opportunities that lie ahead in specialty chemicals.

India's chemical industry stands at an inflection point similar to China's position in 2000. The country consumes $180 billion worth of chemicals annually but produces only $100 billion domestically. This $80 billion import gap represents not just current opportunity but future growth potential as consumption compounds at 9-11% annually. Within this macro opportunity, specialty chemicals offer the most attractive risk-reward—higher margins than commodities, lower capital intensity than pharmaceuticals, and deep linkages with India's manufacturing ambitions.

The "China Plus One" strategy, accelerated by geopolitical tensions and supply chain resilience concerns, is directing global chemical companies to establish alternative supply bases. India, with its large domestic market, established chemical infrastructure, and improving ease of doing business, emerges as the natural beneficiary. SPL's success blueprint—import substitution followed by innovation—could be replicated across dozens of chemical categories.

The sustainability transition, rather than threatening companies like SPL, might actually strengthen their moats. As regulations tighten, informal players exit and established companies with technical expertise and compliance capabilities gain share. SPL's early moves in recycling, renewable energy, and green building position them to benefit from, rather than be disrupted by, the sustainability transition. The ability to produce "green" versions of existing products could command premium pricing while creating new barriers to entry.

Infrastructure development provides multi-decade demand visibility. India needs to build the equivalent of one Chicago every year to accommodate urbanization. Each building needs insulation, each vehicle needs plastics, each appliance needs polymers. Companies like SPL that serve these fundamental needs with local production and technical expertise will compound wealth for decades.

But perhaps the most important lesson from SPL's story is about industrial strategy in emerging markets. Success didn't come from copying Western models or competing on cost alone. It came from understanding local market needs, building technical capabilities, creating ecosystems, and maintaining financial discipline through cycles. This playbook—patient capital, technical excellence, market creation, and operational discipline—could build champions across India's industrial landscape.

The next decade will likely see consolidation in Indian chemicals as subscale players struggle with compliance costs and technology requirements. Companies with strong balance sheets, like SPL, will have opportunities to acquire capabilities and capacities at attractive valuations. The industry structure that emerges—fewer but stronger players with regional or product leadership—will be more profitable and sustainable.

For investors, Supreme Petrochem represents a specific expression of a broader theme: investing in India's industrial champions that combine technical expertise with market dominance. These aren't glamorous technology companies promising disruption; they're the boring backbone of industrial civilization, generating cash flows that compound through cycles.

The Supreme Petrochem story ultimately isn't about chemicals—it's about the patient accumulation of competitive advantages in industries that matter. It's about recognizing that in emerging markets, the biggest opportunities often lie not in creating entirely new industries but in professionally managing industries that already exist. It's about understanding that sustainable wealth creation comes from solving real problems for real customers with real products.

As India marches toward becoming a $10 trillion economy, companies like Supreme Petrochem will play an unglamorous but essential role. They won't make headlines or inspire startup founders. But they will manufacture the materials that house, transport, and sustain billions of people. And for investors wise enough to recognize their value, they will compound wealth with the inevitability of industrial progress itself.

In the end, that might be the most important lesson from this deep dive: sometimes the best investments aren't in the companies trying to change the world, but in those quietly enabling the world to change.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube