Sona Comstar: The Story of India's EV Component Champion

I. Introduction & Episode Roadmap

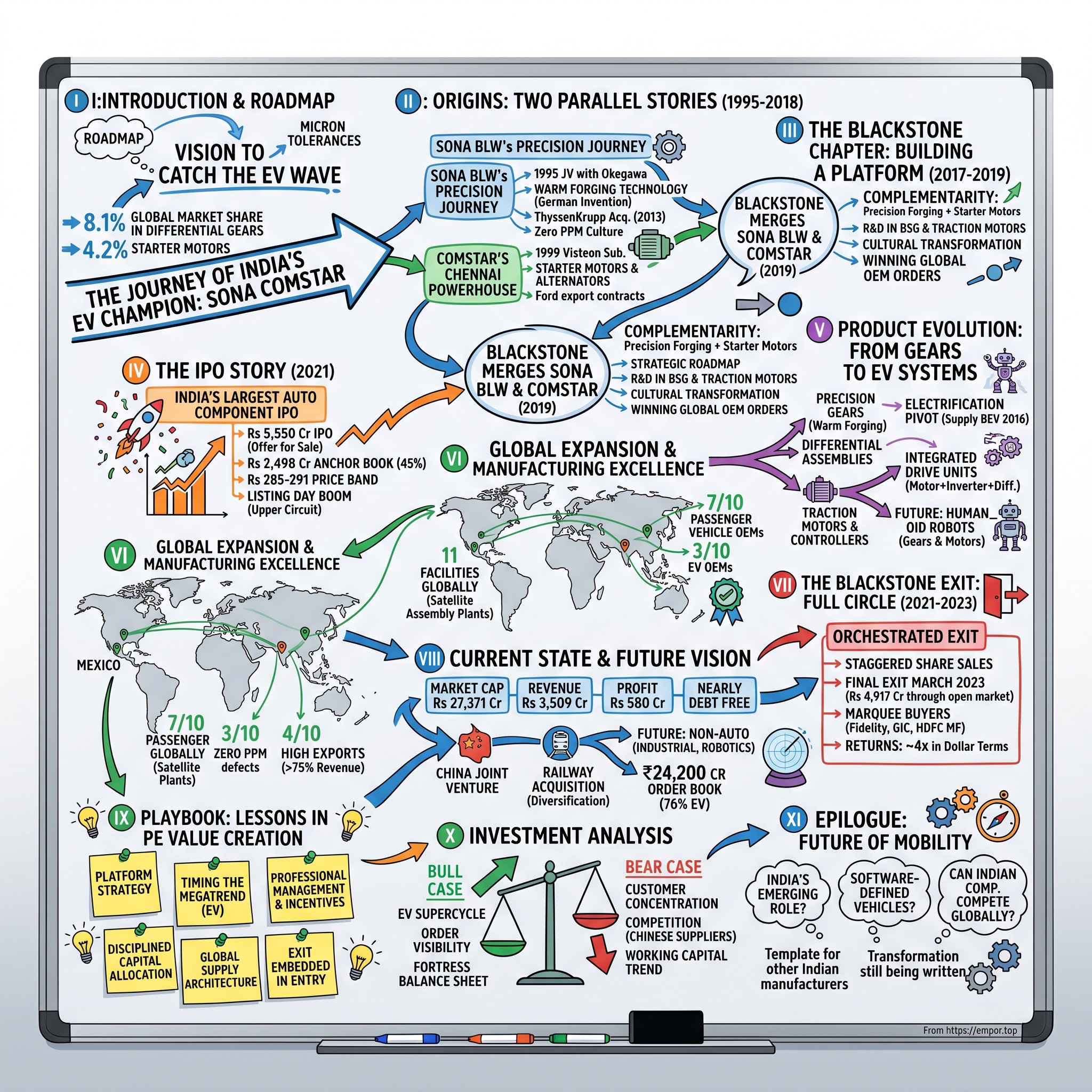

Picture this: In a nondescript industrial facility in Gurugram, engineers huddle over precision forging equipment that can shape metal with tolerances measured in microns. The year is 2019, and two companies—one backed by the world's largest private equity firm—are about to merge into what will become India's answer to the global electric vehicle revolution. This is the story of Sona Comstar, a company that transformed from traditional auto component manufacturers into India's largest EV component supplier, commanding 8.1% global market share in differential gears and 4.2% in starter motors.

The narrative arc is almost cinematic: Two parallel companies, built over decades, brought together by Blackstone's vision, merged at precisely the right moment to catch the EV wave, and executed one of India's largest auto component IPOs. Today, Sona Comstar isn't just another parts supplier—it's a technology company disguised as a manufacturer, designing and producing engineered automotive systems from differential assemblies to EV traction motors across every vehicle category imaginable.

What makes this story particularly compelling is the timing. While Tesla was capturing headlines and traditional automakers were scrambling to announce EV plans, a precision forging company in India quietly positioned itself at the heart of the mobility transition. The company didn't just pivot to EVs—it rebuilt itself from the ground up, transforming culture, capabilities, and capital structure in a masterclass of private equity value creation.

This isn't just about gears and motors. It's about how India can compete in high-precision, high-technology manufacturing on a global stage. It's about how private equity can create platforms rather than flip assets. And fundamentally, it's about reading the future of an entire industry and having the courage to bet everything on that vision. As we'll see, the journey from precision forging to EV leadership required not just capital, but a complete reimagination of what an Indian auto component company could be.

II. The Origins: Two Parallel Stories (1995–2018)

Sona BLW's Journey: The Art of Precision

In 1995, as India was still finding its feet in the post-liberalization era, a joint venture emerged that would lay the foundation for precision manufacturing excellence. Sona Okegawa Precision Forgings Limited—the name itself a mouthful of cross-border ambition—represented something new in Indian manufacturing: a marriage of Japanese precision with Indian entrepreneurial energy.

The company's DNA was international from day one. The partnership with Okegawa brought more than just capital; it brought a philosophy. Japanese manufacturing principles—kaizen, zero-defect mindset, respect for the process—began taking root in Indian soil. When Mitsubishi joined as a partner, the company gained access to global automotive networks that would prove invaluable decades later.

The real transformation began in 2013 with a series of moves that read like a corporate chess game. The Sona Group, led by Sunjay Kapur—a man described by colleagues as having "an engineer's precision with an entrepreneur's vision"—orchestrated the acquisition of ThyssenKrupp's forging business. This wasn't just any forging business; it included BLW, the German company that had literally invented warm forging technology. Simultaneously, they acquired Mitsubishi's 25% stake, gaining full control. The company was rechristened Sona BLW Precision Forgings Limited—a name that honored both its Indian roots and German technological heritage.

Warm forging, for the uninitiated, is the Goldilocks of metal forming—not too hot, not too cold, but just right for creating components with exceptional strength and precision. While competitors were still using traditional hot forging (energy-intensive and less precise) or cold forging (limited in complexity), Sona BLW could create differential gears with tolerances that made German engineers nod in approval.

By 2018, Sunjay Kapur had built something remarkable: a company that could compete with anyone globally on precision, but from an Indian cost base. The facilities in Gurugram and Manesar weren't just factories; they were temples to precision engineering, where operators spoke in microns and quality was measured in parts per million defects—often achieving the holy grail of "zero PPM."

Comstar's Parallel Story: The Chennai Powerhouse

Meanwhile, 2,200 kilometers south in Chennai, another story was unfolding. Comstar's origins in 1999 as a subsidiary of Visteon Corporation—itself a Ford spinoff—gave it impeccable automotive pedigree. This wasn't a startup trying to break into the auto industry; it was born inside it, with Ford's DNA coursing through its operations.

Chennai was India's "Detroit," and Comstar positioned itself at its heart. The company specialized in starter motors, alternators, and starter motor kits—the unglamorous but essential components that bring engines to life. While Sona BLW was perfecting the art of precision forging up north, Comstar was becoming the go-to supplier for anyone who needed reliable starting systems in India. The transformation from Ford unit to independent entity was complex. Comstar was originally a unit within the Ford Automotive Products Operation, established in Chennai in 1999, and when Ford spun off its parts subsidiary as Visteon Corporation in June 2000, Comstar became part of Visteon. But what's fascinating is how this Chennai plant evolved—winning Tata as a customer was considered "a major win for the Chennai plant", signaling its growing importance beyond just being a Ford supplier.

The real independence came in 2007. Visteon Powertrain was sold to Adyar River Ltd., a joint venture between Hong Kong–based Argyle Street Management and Kenyan industrialist Manu Chandaria's investment vehicle, and was renamed Comstar Automotive Technologies. This wasn't just a change in ownership; it was a complete reimagination of what the company could be.

By 2010, Comstar had achieved something remarkable: it won one of its largest contracts in history, supplying 600,000 starter motors annually to Ford's North American operations. Yet despite this export success, only 10% of its starter motors and alternators were sold to Indian OEMs—a dependency on exports that would later prove both a strength and a vulnerability.

The technical capabilities Comstar built were impressive. The company wasn't just making conventional starters; it was developing starters for micro- and mid-hybrid vehicles using the latest "go-green" technologies. This early focus on electrification technologies would prove prescient when the paths of Sona BLW and Comstar would eventually converge under Blackstone's orchestration.

III. The Blackstone Chapter: Building a Platform (2017–2019)

The Vision Takes Shape

In April 2017, the automotive component landscape in India witnessed a seismic shift. Blackstone acquired Comstar Automotive Technology, paying approximately Rs 1,000 crore for what many saw as just another auto parts supplier. But Blackstone saw something different—they saw the foundation of a platform. The strategy became clear in 2018 when Blackstone bought Sona BLW Precision Forgings Ltd, merging the two companies in 2019 to form Sona Comstar. Overall, Blackstone invested around $385 million in both businesses. Blackstone acquired the entire 32% stake held by JM Financials for about $300 million. This wasn't opportunistic deal-making; it was strategic platform building of the highest order.

The genius of the merger lay in its complementarity. Sona BLW brought precision forging capabilities and differential gear expertise. Comstar brought starter motor technology and early electrification capabilities. Together, they could offer integrated powertrain solutions—both for traditional internal combustion engines and the coming electric revolution.

The Transformation Playbook

The 4-year journey from investment to IPO entailed the development of a strategic roadmap to transform the new entity into a technology-led automotive systems supplier focused on electric vehicles. This wasn't just financial engineering; it was a complete cultural and operational transformation.

The integration process was meticulous. Teams from both companies were brought together not just to eliminate redundancies, but to cross-pollinate capabilities. Engineers from Sona BLW's precision forging operations began working with Comstar's electric motor specialists. The result? Products that neither company could have developed independently.

One executive who lived through the merger described it as "organized chaos with a purpose." Systems had to be integrated, cultures aligned, and most importantly, a unified vision for the future had to be created. The vision was clear: become the supplier of choice for the electrification transition.

The operational synergies were immediate and impressive. Sona BLW's customer relationships with global OEMs opened doors for Comstar's products. Comstar's technical capabilities in electric motors accelerated Sona BLW's pivot toward EV components. The combined entity could now offer everything from precision gears to complete electric drive systems.

In December 2018, the Competition Commission cleared the deal involving acquisition of up to 66.28 per cent share capital in Sona BLW by Blackstone Group and merger of Comstar in Sona BLW. With regulatory approval secured, the real work began.

Creating the EV Platform

What Blackstone understood—and what many missed—was that the shift to electric vehicles wasn't just about swapping engines for motors. It required entirely new component architectures, different supply chains, and most critically, the ability to integrate mechanical and electrical systems seamlessly.

Under Blackstone's ownership, Sona Comstar invested aggressively in R&D, particularly in areas like Belt Starter Generator (BSG) systems for hybrid vehicles and traction motors for pure EVs. These weren't incremental improvements; they were moonshot projects that required significant capital and patience.

The company also began a subtle but important shift in its talent strategy. While retaining its core of mechanical engineers who understood precision manufacturing, it began hiring electrical engineers, software developers, and system integration specialists. The company was transforming from a component supplier to a systems integrator.

By 2019, as the merger was being completed, Sona Comstar had already begun winning orders from global OEMs for next-generation electric vehicle components. The timing was perfect—Tesla's Model 3 was proving EVs could be mass-market products, traditional automakers were announcing massive EV investments, and India was beginning to articulate its own electric mobility vision. The stage was set for what would become one of India's most successful auto component IPOs.

IV. The IPO Story: India's Largest Auto Component Listing (2021)

The Perfect Storm

June 2021. The world was emerging from pandemic lockdowns, stock markets were at historic highs, and electric vehicle stocks were the darlings of Wall Street. In this environment, Sona Comstar prepared to test public markets with an audacious proposition: an Indian auto component company positioned for the global EV revolution. The Rs 5,550-crore initial public offer wasn't just large—it was the largest IPO by an auto component maker in India. The structure was telling: Rs 300 crore in fresh capital raise and Rs 5,250 crore as an offer for sale by Singapore VII Topco III Pte Ltd, Blackstone's investment vehicle. This wasn't about raising growth capital; it was about providing an exit at scale.

The anchor book told the real story. Sona Comstar raised Rs 2,498 crore from anchor investors, making it the third largest anchor book size ever. The amount raised was 45% of the total IPO size—extraordinary demand that signaled institutional confidence. 42 investors participated in the anchor book, including 24 foreign portfolio investors, 11 domestic mutual funds, five life insurance companies and two AIFs.

The Pricing Dance

The price band of Rs 285-291 per share valued the company at approximately Rs 17,000 crore—a valuation that made some analysts gulp. At 74 times price-to-earnings, this wasn't value investing territory. Yet the narrative was compelling: here was India's play on the global EV transition, backed by the world's largest private equity firm, with proven execution capabilities and a blue-chip customer base.

The retail portion was deliberately kept small—just 10% or about Rs 555 crore—creating scarcity. The minimum lot size of 51 shares meant retail investors needed to commit at least Rs 14,841, ensuring only serious participants. The institutional portion, at 75% of the offer, was where the real action would be.

The Market Verdict

When trading began on June 24, 2021, the market delivered its verdict emphatically. The stock listed at Rs 301 on the NSE, a modest premium to the issue price. But then something remarkable happened—it hit the upper circuit at Rs 361.20, a gain of over 20% on the listing day.

The subscription numbers had already telegraphed the enthusiasm. The IPO was subscribed 2.28 times overall, with the QIB portion subscribed 3.46 times. But these numbers don't capture the frenzy in the grey market, where premiums reached as high as Rs 20 per share in the days leading up to listing.

What made this IPO particularly notable wasn't just its size or the listing gains. It was the quality of investors it attracted and what it represented for Indian manufacturing. This wasn't a consumer internet company promising network effects and winner-take-all dynamics. This was a manufacturer of precision components, competing globally on quality and technology. The successful IPO validated not just Sona Comstar, but the entire thesis that Indian companies could compete in high-technology manufacturing.

For Blackstone, the IPO was just the beginning of a carefully orchestrated exit that would eventually generate returns that would become legendary in private equity circles. They had transformed two mid-sized component manufacturers into a platform valued at over $2 billion, and they were just getting started.

V. The Product Evolution: From Gears to EV Systems

The Foundation: Mastering Precision

At the heart of Sona Comstar's competitive advantage lies a deceptively simple product: the differential gear. These aren't just chunks of metal; they're precision-engineered components with tolerances measured in microns that must withstand enormous forces while operating silently for hundreds of thousands of kilometers. The company's mastery of warm forging technology—inherited from BLW, the German inventor of the process—allows it to create gears with a grain flow that follows the tooth profile, resulting in strength that cold-forged or machined gears simply cannot match.

Walk through the Gurugram facility, and you'll see operators who speak a different language—not Hindi or English, but the language of precision. "Plus-minus five microns," one might say, referring to a tolerance that's less than one-tenth the width of a human hair. This obsession with precision isn't academic; it's what allows Sona Comstar to achieve the holy grail of manufacturing: zero PPM (parts per million) defect rates for multiple customers.

The product portfolio reads like a mechanical engineering textbook: bevel gears, differential assemblies, synchronizer rings, conventional and micro-hybrid starter motors, BSG systems, and increasingly, EV traction motors. But categorizing these as separate products misses the point. What Sona Comstar really sells is the ability to transmit power efficiently, quietly, and reliably—whether that power comes from a combustion engine or an electric motor.

The Electric Pivot: Reading the Future

The transformation began in 2016 when Sona Comstar started supplying differential bevel gears for battery-electric cars. By 2019, they had developed and begun supplying complete final drive differential assemblies for the same segment. But this was just the beginning. The company started its EV journey in 2016 with the supply of Differential Bevel Gears for battery-electric cars. By 2019, it had developed and started supplying the Final Drive Differential Assembly for the same segment.

The real breakthrough came with the development of traction motors—both BLDC (Brushless DC) and PMSM (Permanent Magnet Synchronous Motor) varieties—and motor controllers for electric two- and three-wheelers, plus Belt Starter Generator (BSG) systems for hybrid cars. The company added several new products including Traction Motors (both BLDC and PMSM), Motor Controllers for electric two- and three-wheelers, and Belt Starter Generators for hybrid cars.

What sets Sona Comstar apart is their ability to be "one of a few companies globally, with the ability to design high power density EV systems handling high torque requirements with a lightweight design." This isn't marketing hyperbole; it's engineering reality. The company's differential assemblies for EVs must handle instantaneous torque delivery that's fundamentally different from internal combustion engines. Electric motors deliver maximum torque from zero RPM—a characteristic that puts enormous stress on drivetrain components.

The Integration Play

The masterstroke in Sona Comstar's EV strategy is integration. Integrated drive units have three key components: differential assembly, high voltage traction motors and high voltage inverters. Since the company already manufactures electric drive motors and inverters for electric 2-wheelers and hybrid PVs, as well as differential assemblies for battery electric passenger vehicles, they are uniquely positioned to integrate these three key constituents into a single matched unit.

This integration capability represents a fundamental shift in the automotive supply chain. Traditional component suppliers sold parts; Sona Comstar sells systems. An OEM can now source a complete electric drive unit—motor, inverter, and differential—from a single supplier, reducing complexity, improving reliability, and potentially lowering costs.

The numbers tell the story of this successful pivot. The company reported BEV sales of ₹1,280 crore in FY25, up 38% from the previous year. The contribution of BEV to total revenue rose from 29% in FY24 to 36% in FY25. This isn't just growth; it's a complete transformation of the revenue mix.

Beyond Automotive: The Next Frontier

In a move that signals ambition beyond traditional automotive, Sona Comstar has begun developing components for humanoid robots, anticipating rapid adoption in the next decade driven by AI, 3D perception, and falling computing costs. Management stated that the company's expertise in gears, motors, controllers, radar sensors, and embedded software positions it well to serve this emerging domain.

This isn't as far-fetched as it might seem. The precision gears and motors that power electric vehicles share fundamental technologies with those needed for robotics. The same expertise in creating lightweight, high-torque, quiet systems applies whether the application is a Tesla Model 3 or a Boston Dynamics robot.

The order book validates the strategy. Sona Comstar secured ₹24,200 Cr order book, with the majority linked to electrified vehicles. This visibility into future revenue—rare in the cyclical auto component industry—provides the confidence to continue investing in R&D and capacity expansion.

VI. Global Expansion & Manufacturing Excellence

The Geographic Chess Game

Sona Comstar's manufacturing footprint reads like a strategic response to global automotive production patterns. The company has 11 manufacturing and assembly facilities across India, China, Mexico, and the USA—seven in India, two in Mexico, and one each in China and the USA. But this isn't just about having flags on a map; it's about being where your customers need you, when they need you.

The facility locations tell a story of strategic thinking. Chennai for proximity to India's automotive hub and export infrastructure. Gurugram and Manesar for access to the northern Indian market and skilled workforce. Mexico for serving North American OEMs while benefiting from USMCA trade agreements. China for localizing in the world's largest EV market. And the USA facility in Tecumseh, Michigan—right in the heart of American automotive country—for final assembly and just-in-time delivery to Detroit's Big Three.

The facilities in Chennai, China, Mexico, and the USA focus on production of Motor business products, while the other facilities in India and one facility in Mexico focus on Driveline business products. The facilities in India serve as manufacturing plants, whereas those in the USA, Mexico, and China operate as satellite final assembly and finishing plants.

This distinction between full manufacturing and satellite assembly is crucial. It allows Sona Comstar to leverage India's cost advantages for complex manufacturing while maintaining local presence for customization, quality control, and rapid response to customer needs. It's a hybrid model that combines the best of global efficiency with local responsiveness.

The Customer Portfolio: A Who's Who of Global Mobility

Walk into any Sona Comstar facility, and you'll see quality certificates and supplier awards from virtually every major global OEM. The customer list reads like a Fortune 500 of automotive: Ford, Volvo, Renault-Nissan, Mahindra, Ashok Leyland, and significantly, some of the world's largest EV manufacturers whose names the company carefully doesn't disclose for competitive reasons. The market share numbers are staggering: 8.1% and 4.2% global market share in the differential gears and starter motors business, respectively, as of CY23. More recent data shows Sona Comstar's global market share in differential gears rose from 8.1% to 8.8% in 2024, while its share in starter motors increased from 4.2% to 4.4%. In India, the company commands a significant market share ranging from 60-90% across different vehicle categories.

These aren't just statistics; they represent deep, multi-decade relationships built on zero-defect quality and on-time delivery. Sona Comstar serves as a preferred partner for leading automotive manufacturers worldwide, including seven of the top 10 passenger vehicle OEMs, three of the top 10 commercial vehicle OEMs, seven of the top 10 tractor OEMs, and four of the top 10 electric vehicle OEMs.

Manufacturing Excellence: The Zero PPM Quest

The pursuit of zero PPM (parts per million) defects isn't just a quality metric; it's a philosophy that permeates every aspect of Sona Comstar's operations. In an industry where a single defective part can trigger million-dollar recalls, achieving consistent zero PPM performance is the ultimate competitive advantage.

The company's manufacturing excellence is built on several pillars. First, the warm forging technology that creates components with superior metallurgical properties. Second, automated inspection systems that check every critical dimension on every part. Third, a culture where line operators have the authority to stop production if they spot a quality issue.

Sona Comstar's journey towards these milestones began with the production of precision forged differential gears at its plant in Gurgaon, Haryana, in 1999. Over the years, the company expanded its production capabilities, marking significant milestones such as the production of 100 million gears in 2013, 200 million gears in early 2018, and 300 million gears in October 2021. The achievement of the 400 million gear milestone within two and a half years underscores the company's robust growth trajectory.

The speed of scaling is remarkable. The company's state-of-the-art facilities and commitment to excellence have enabled it to produce one million differential assemblies in less than nine months. This isn't just about having more machines; it's about continuous improvement in cycle times, yield rates, and overall equipment effectiveness (OEE).

The Export Engine

More than 75% of Sona Comstar's revenues come from outside India—a testament to its global competitiveness. But this isn't low-value, commoditized exports. The company exports sophisticated, mission-critical components that go into some of the world's most advanced vehicles.

The export strategy is nuanced. For mature markets like the US and Europe, Sona Comstar positions itself as a cost-effective alternative to local suppliers without compromising on quality. For emerging markets, it leverages its experience in frugal engineering—creating products that deliver required performance at dramatically lower costs.

The company's ability to navigate complex global supply chains became particularly evident during the pandemic and subsequent supply chain disruptions. While competitors struggled with shipping delays and component shortages, Sona Comstar's distributed manufacturing footprint allowed it to shift production between facilities, ensuring continuity of supply to critical customers.

As one automotive purchasing executive put it: "In our industry, you're only as good as your worst crisis. Sona Comstar proved during COVID that they're not just a supplier; they're a partner you can count on when things go wrong." This reputation for reliability, built over decades and tested in crisis, is perhaps the company's most valuable asset as it continues its global expansion.

VII. The Blackstone Exit: Full Circle (2021–2023)

The Orchestrated Exit

Blackstone's exit from Sona Comstar wasn't a rushed sale or a desperate scramble for liquidity. It was a masterclass in private equity exit strategy, executed with the precision of a Swiss watch over nearly two years. The story begins at the IPO itself, where Singapore VII Topco III Pte Ltd. had sold shares worth Rs 5,250 crore at the time of Sona BLW Precision Forgings' IPO. Consequently, the shareholding of Singapore VII Topco III Pte Ltd. declined to 34.18% on expanded post issue equity base, from 66.28% pre-IPO.

This initial sale at IPO wasn't just about partial monetization; it was about price discovery and creating a liquid market for future exits. By retaining a significant stake post-IPO, Blackstone signaled confidence in the company's future while giving itself optionality for future sales at potentially higher valuations.

The second act came in August 2022. The market had digested the IPO, the company had delivered several quarters of public company earnings, and institutional investors had built conviction in the Sona Comstar story. Blackstone sold 7,94,33,500 shares equivalent to 13.59% stake, with its holding coming down to 20.52%. The timing was deliberate—after the company had demonstrated its EV pivot was working but before any potential market correction.

The Final Exit: A Bidding War in Disguise

March 2023 marked the culmination of Blackstone's journey with Sona Comstar. Private equity firm Blackstone on Monday sold its 20.50 per cent stake in auto component maker Sona BLW Precision Forgings for Rs 4,917 crore through an open market transaction. But the mechanics of this sale reveal sophisticated execution.

Blackstone affiliate firm Singapore VII Topco III sold about 120 million shares at Rs 410 each to mop up Rs 4,917 crore. Among the buyers were HDFC Bank, Singapore's GIC and Societe Generale. The quality of buyers—sovereign wealth funds, global banks, and blue-chip domestic institutions—validated not just the exit but the entire value creation journey.

What's remarkable is who showed up to buy: Marquee investors like the Government of Singapore, Fidelity, FMR, ICICI Prudential Life Insurance and HDFC MF bought shares from Blackstone in the bulk deal. These aren't momentum traders or hedge funds looking for a quick flip; these are long-term institutional investors who conduct extensive due diligence before committing capital at scale.

The Returns: Setting New Benchmarks

The numbers are staggering. Overall, it invested around $385 million in the two businesses. In absolute terms, Blackstone has already made ₹12,800 crore or $1.6 billion in capital gains. This represents a return of over 4x in dollar terms—exceptional for a control buyout in a manufacturing business.

But the headline multiple understates the sophistication of the value creation. Blackstone didn't just buy low and sell high; it fundamentally transformed two regional component manufacturers into a global EV technology platform. The merger synergies, operational improvements, and strategic pivot to electrification created value that wouldn't have existed without active ownership.

Blackstone made a total return of over 15 times on its investment in Sona Comstar according to some calculations, though this likely includes the rupee appreciation and assumes certain cost bases. Even conservative estimates put the return at 10x or higher—extraordinary for a late-stage private equity investment in a traditional industry.

The Legacy: More Than Just Returns

Once completed, the Sona BLW transaction will be Blackstone's most successful exit from India. But the legacy extends beyond financial returns. Blackstone proved that Indian manufacturing companies could be transformed into global technology leaders, that private equity could create platforms rather than just financial engineer individual assets, and that patient capital combined with operational expertise could generate exceptional returns even in traditional industries.

The exit also demonstrated the depth of Indian capital markets. The fact that domestic institutions could absorb such a large stake sale without significant price disruption showed how far Indian markets had evolved. It also validated the IPO pricing—despite initial concerns about valuation, the stock had held up well enough for Blackstone to exit its entire position above the IPO price.

For Sona Comstar, the complete exit by Blackstone marked both an ending and a beginning. The company no longer had a controlling shareholder, giving management more autonomy. But it also meant losing access to Blackstone's global network and operational expertise. The true test would be whether the transformation Blackstone catalyzed would continue without the PE firm's active involvement.

As one investment banker involved in the transaction reflected: "Most PE exits are either distressed sales or opportunistic flips. This was neither. This was a systematic, patient unwinding of a position after creating tremendous value. It's the kind of exit that LPs dream about and GPs use as case studies for decades."

VIII. Current State & Future Vision

Financial Performance: The Numbers Tell the Story

Today's Sona Comstar is a financial powerhouse by auto component standards. With a market capitalization of Rs 27,371 crore, revenue of Rs 3,509 crore, and profit of Rs 580 crore, the company has achieved scale while maintaining profitability—a rare combination in the capital-intensive automotive supplier industry. The 2024 revenue of Rs 3,546 crore represented an 11.34% increase, while earnings of Rs 601 crore showed a 16.23% jump, demonstrating operational leverage as the company scales.

What's particularly impressive is the margin profile. In an industry where single-digit EBITDA margins are common, Sona Comstar consistently delivers 25%+ EBITDA margins and 15%+ net margins. This isn't financial engineering; it's the result of technology leadership, operational excellence, and a product mix increasingly skewed toward high-value EV components.

The balance sheet tells another story of strength: the company is almost debt free. In an industry that typically operates with significant leverage due to capital intensity, Sona Comstar's debt-free status provides enormous strategic flexibility. It can invest in R&D without worrying about interest coverage, pursue acquisitions without stretching the balance sheet, and weather downturns without existential risk.

Strategic Initiatives: Building the Future

The China joint venture for EV components represents a critical strategic move. China isn't just the world's largest EV market; it's where the future of electric mobility is being invented. By establishing local manufacturing and partnerships in China, Sona Comstar gains access to cutting-edge technology, cost-competitive supply chains, and relationships with Chinese EV manufacturers who are increasingly expanding globally.

But perhaps the most intriguing strategic initiative is the railway business acquisition. Signed an agreement to acquire Railway Equipment Division from Escorts Kubota, this move represents diversification beyond automotive into another form of mobility. Railways are undergoing their own electrification transition, and many of the technologies Sona Comstar has developed for automotive—precision gears, electric motors, control systems—have direct applications in rail.

Management's optimism about "future growth through diversification into non-automotive sectors" isn't just rhetoric. The company is systematically identifying adjacent markets where its core competencies in precision engineering and electrification can create value. Industrial automation, renewable energy, and even aerospace represent potential growth vectors.

The R&D investments continue to accelerate. The company isn't just developing products for today's EVs; it's working on technologies for vehicles that won't hit the road for another five years. High-voltage systems for 800V architectures, integrated power electronics, and software-defined vehicle components represent the next frontier.

Technology Partnerships: Competing Through Collaboration

In the technology-intensive world of EV components, no company can innovate alone. Sona Comstar's partnership strategy reflects this reality. We tied up with IRP Nexus of Israel to develop magnet-less traction motors and matching controllers to have a differentiated product offering free of rare earth element dependencies. This isn't just about cost reduction; it's about solving one of the fundamental challenges of EV scaling—dependency on rare earth materials controlled by a handful of countries.

The partnership approach extends beyond product development. Collaborations with software companies for control algorithms, with material science firms for lightweight components, and with universities for fundamental research create an innovation ecosystem that amplifies Sona Comstar's internal capabilities.

The Order Book: Visibility in an Uncertain World

Sona Comstar now has 57 active EV programmes across 32 global customers, with EV programmes constituting 76% of its INR 23,200 crore order book. This order book visibility—rare in the auto component industry—provides confidence for continued investment in capacity and technology.

But the order book isn't just about quantity; it's about quality. These aren't commodity products that could be easily re-sourced. Many of these programs involve co-development with OEMs, multi-year contracts, and components so critical that switching suppliers would require extensive revalidation. This creates switching costs that protect Sona Comstar's position even as competition intensifies.

The Management Vision: Beyond Components

Current management, led by the original promoter family and professional executives, envisions Sona Comstar not as a component supplier but as a mobility technology company. The recent foray into developing components for humanoid robots signals this ambition. Notably, the company has begun developing components for humanoid robots, anticipating rapid adoption in the next decade driven by AI, 3D perception, and falling computing costs. Management stated that the company's expertise in gears, motors, controllers, radar sensors, and embedded software positions it well to serve this emerging domain.

This isn't diversification for its own sake. The core technologies—precision mechanical systems, electric motors, control electronics, and embedded software—remain constant. What changes is the application. Whether it's a differential gear in an electric car, a traction motor in a robot, or a control system in an industrial automation application, the fundamental engineering challenges are similar.

The vision extends to becoming a full-system integrator. Rather than selling individual components, Sona Comstar increasingly offers complete solutions—integrated drive units that combine mechanical, electrical, and software elements. This moves the company up the value chain and creates deeper relationships with customers who prefer dealing with fewer, more capable suppliers.

As we look ahead, Sona Comstar stands at an inflection point. The EV transition is accelerating globally, creating massive opportunities for established suppliers who can meet the technology and scale requirements. But competition is intensifying, particularly from Chinese suppliers who combine government support with aggressive pricing. The next chapter of the Sona Comstar story will be written by how well the company navigates these opportunities and challenges without the guiding hand of Blackstone.

IX. Playbook: Lessons in PE Value Creation

The Platform Strategy: Building at Scale

Blackstone's approach to Sona Comstar exemplifies the "platform strategy" that has become the hallmark of sophisticated private equity. Rather than buying a single asset and trying to optimize it in isolation, Blackstone acquired two complementary businesses and merged them to create something greater than the sum of parts. This wasn't just about cost synergies—though those were significant—but about capability synergies that enabled the combined entity to compete for business neither could have won alone.

The platform approach requires patient capital and operational expertise. It took nearly two years from the first acquisition to complete the merger and integration. During this time, Blackstone had to manage two separate companies, align management teams with different cultures, and create a unified strategy—all while ensuring business continuity for customers who cannot tolerate supply disruptions.

What made this platform creation particularly successful was the complementary nature of the assets. Sona BLW brought precision forging and mechanical excellence; Comstar brought electrical systems and early electrification capabilities. Together, they could offer integrated electro-mechanical solutions—exactly what the automotive industry needed as it transitioned to EVs.

Timing the Megatrend: The EV Pivot

Private equity firms often talk about "riding megatrends," but few execute as precisely as Blackstone did with the EV transition. When Blackstone made its investments in 2017-2018, Tesla was still struggling with Model 3 production, traditional automakers were skeptical about EVs, and the Indian EV market was virtually non-existent. Yet Blackstone saw the writing on the wall: electrification was inevitable, and suppliers who could provide critical EV components would capture enormous value.

The timing wasn't lucky; it was calculated. Blackstone's automotive team had deep relationships with global OEMs and could see their product roadmaps extending into the mid-2020s. They knew that major automakers were planning massive EV investments, even if these plans weren't yet public. This information asymmetry—knowing what's coming before the market does—is a critical source of private equity returns.

But seeing the trend is different from executing against it. Blackstone didn't just bet on EVs; it systematically transformed Sona Comstar's capabilities to serve this market. This meant investing in R&D for products that wouldn't generate revenue for years, hiring engineers with expertise in power electronics and software, and sometimes walking away from profitable ICE business to focus resources on electrification.

Professional Management: The Secret Sauce

One of Blackstone's smartest moves was retaining and empowering existing management while supplementing them with additional expertise. Sunjay Kapur and his team knew the business, had relationships with customers, and understood Indian manufacturing. Blackstone didn't try to replace them with outsiders; instead, they provided resources, opened doors to global customers, and created incentive structures aligned with value creation.

The exit return incentive (ERI) plan that offered compensation of 1-4% of the proceeds that Blackstone would generate from a future sale of its stake in Sona Comstar to select executives was particularly clever. This aligned management with the exit, ensuring they would work toward creating value that could be crystallized in a sale rather than just optimizing current earnings.

Professional management also meant building institutional capabilities. Under Blackstone's ownership, Sona Comstar implemented world-class ERP systems, sophisticated cost accounting, and professional investor relations—capabilities that would prove essential for life as a public company.

Capital Allocation: The Discipline of Saying No

In a capital-intensive industry like auto components, the temptation is always to chase volume by investing in capacity. Blackstone brought discipline to capital allocation, focusing investments on capabilities that would differentiate Sona Comstar rather than just add capacity for commodity products.

This meant saying no to seemingly attractive opportunities. When competitors were expanding aggressively into China, Sona Comstar was selective, entering through a joint venture rather than massive solo investment. When the ICE business was still profitable and growing, the company began shifting resources to EV components, accepting short-term pain for long-term gain.

The discipline extended to acquisitions. Rather than pursuing a roll-up strategy of buying smaller competitors, Sona Comstar focused on organic growth and capability building. The railway equipment acquisition came only after the core transformation was complete and the company had bandwidth to integrate another business.

Global Supply Chain Architecture

Building a global supply chain from an Indian base requires navigating complex trade regulations, currency fluctuations, and geopolitical risks. Blackstone's approach was to create a hub-and-spoke model with India as the hub for complex manufacturing and local facilities in key markets for final assembly and customization.

This architecture provides multiple benefits. It leverages India's cost advantages while maintaining local presence for customer service. It provides natural currency hedging—revenues and some costs in the same currency. It also creates optionality; if trade wars or tariffs make one route unviable, production can be shifted to another location.

The supply chain strategy also extended to suppliers. Rather than depending on single sources, Sona Comstar developed multiple suppliers for critical inputs, often helping smaller suppliers upgrade capabilities in exchange for dedicated capacity. This created a resilient supply base that proved invaluable during the pandemic-era disruptions.

The Exit as Part of the Entry

Perhaps the most important lesson from Blackstone's playbook is that the exit strategy was embedded in the entry thesis. From day one, the plan was to create a company that could go public at a premium valuation. Every decision—from the merger structure to the EV pivot to the management incentives—was made with an eye toward creating a compelling public market story.

This didn't mean short-term thinking; quite the opposite. Because Blackstone knew it would exit through public markets rather than a strategic sale, it could invest in long-term capabilities that might not pay off immediately but would be valued by public investors looking for growth.

The staggered exit—at IPO, one year later, and then the final sale—was also masterful. It allowed Blackstone to capture value creation over time while maintaining enough stake to influence operations. It also sent a signal to public investors: Blackstone wasn't dumping and running but was confident enough to hold significant exposure even after the IPO.

X. Investment Analysis & The Road Ahead

Bull Case: Riding the Electrification Supercycle

The bull case for Sona Comstar starts with a simple observation: the world is electrifying, and someone needs to make the components. With BEV revenue now accounts for 39% of Sona Comstar's total revenue and BEV sales of ₹1,280 crore in FY25, up 38% from the previous year, the company is perfectly positioned to capture this transition.

The order book visibility provides unusual confidence in future growth. With Rs 23,200 crore in orders, of which 76% are EV-related, Sona Comstar has multiple years of revenue visibility—rare in the cyclical auto industry. These aren't speculative orders; they're firm commitments from global OEMs for programs already in development.

The global manufacturing footprint is another strength. Unlike pure-play Indian suppliers who might face tariff barriers or local content requirements, Sona Comstar can serve customers from multiple locations. The recent China JV particularly positions the company to serve the world's largest and most innovative EV market.

Technology leadership in critical components creates a moat that's difficult to replicate. The company's ability to achieve zero PPM quality in precision forged gears, combined with its emerging capabilities in high-voltage EV systems, makes it one of the few suppliers globally who can serve both legacy and EV platforms with equal competence.

The balance sheet strength—being almost debt-free—provides enormous strategic flexibility. The company can invest counter-cyclically during downturns, pursue strategic acquisitions without dilution, and take technical risks that leveraged competitors cannot afford. In a capital-intensive industry, having a fortress balance sheet is a significant competitive advantage.

Bear Case: Challenges in the Fast Lane

The bear case starts with customer concentration. While serving seven of the top 10 global PV OEMs is impressive, it also means significant exposure to a handful of customers. If even one major customer reduces orders or switches suppliers, the impact could be material.

The EV transition timing remains uncertain. While the long-term direction is clear, the pace varies dramatically by geography. Europe and China are moving fast, India is accelerating, but the US remains fragmented. If EV adoption slows—due to technology challenges, infrastructure constraints, or policy changes—Sona Comstar's growth could disappoint.

Competition from Chinese suppliers is intensifying. Chinese companies, often backed by state support and with access to cheap capital, are aggressively expanding globally. They're willing to accept lower margins to gain market share, potentially pressuring Sona Comstar's industry-leading margins.

Working capital days have increased from 76.5 days to 118 days—a concerning trend that suggests either customers are demanding better payment terms or inventory is building up. In an industry where cash conversion is critical, deteriorating working capital metrics could constrain growth or require additional capital.

Valuation remains a concern after the recent correction. While the stock is down 31.2% over the past year, it still trades at premium multiples compared to global auto component peers. The market is pricing in continued high growth and margin expansion—any disappointment could lead to further multiple compression.

The post-Blackstone era introduces execution risk. While management is experienced and capable, they no longer have access to Blackstone's global network, operational expertise, and patient capital. The true test of the transformation will be whether it continues without PE ownership.

Technology Disruption: Friend or Foe?

The shift to software-defined vehicles presents both opportunity and threat. On one hand, vehicles will still need mechanical components—gears, motors, differentials—regardless of how software-defined they become. On the other hand, value is shifting from hardware to software, potentially commoditizing mechanical components.

Sona Comstar's response has been to move up the stack, developing not just motors but motor controllers, not just gears but complete drive units with embedded intelligence. This is the right strategy, but execution is challenging. The company must compete with traditional Tier 1 suppliers who have deep software capabilities while also fending off tech companies trying to enter automotive.

The emergence of new powertrain architectures—like in-wheel motors or solid-state batteries—could obsolete some of Sona Comstar's products. While the company's R&D efforts aim to stay ahead of these trends, technology disruption in automotive is accelerating, and even well-positioned suppliers can find themselves on the wrong side of a technology transition.

The Verdict: Transformation Complete, Journey Continues

Sona Comstar represents a rare success story in Indian manufacturing—a company that transformed from a traditional component supplier to a global technology leader, generated exceptional returns for its private equity sponsor, and emerged as a strong independent entity. The transformation Blackstone catalyzed appears sustainable, with continued revenue growth, margin expansion, and market share gains.

For investors, the key question isn't whether Sona Comstar is a good company—it clearly is—but whether it's a good investment at current valuations. The company trades at a premium to global peers, reflecting its superior growth, margins, and EV exposure. Whether this premium is justified depends on one's view of EV adoption rates, the competitive landscape, and Sona Comstar's ability to maintain technology leadership.

The biggest risk may be that the easy gains from the EV transition have already been captured. As more suppliers pivot to EVs and competition intensifies, maintaining current margins while growing at high rates will become increasingly difficult. The company will need to continue innovating, potentially enter new adjacencies, and perhaps pursue strategic M&A to maintain its growth trajectory.

XI. Epilogue: The Future of Mobility Components

India's Emerging Role in Global EV Supply Chains

As the sun rises over Sona Comstar's Gurugram facility, it illuminates more than just a factory—it reveals India's potential to become a critical node in global EV supply chains. The country that once struggled to produce quality automotive components now manufactures precision gears and sophisticated EV systems that meet the exacting standards of German, American, and Japanese automakers.

India's advantages in this new world order are multifaceted. The engineering talent pool—millions of engineers graduating annually—provides the human capital needed for technology-intensive manufacturing. The cost advantages remain significant, though the real edge now comes from the ability to combine low costs with high quality and technological sophistication. The domestic market, with its unique requirements for frugal engineering and extreme durability, serves as a proving ground for innovations that can be exported globally.

But challenges remain. India's infrastructure, while improving, still lags behind China's integrated industrial ecosystems. The supplier base for advanced materials and electronics isn't as deep. And critically, India lacks the massive domestic EV market that China uses as a springboard for global expansion.

Software-Defined Vehicles: The Next Battlefield

The automotive industry stands at another inflection point. After the transition from mechanical to electrical, the next shift is from electrical to digital. Software-defined vehicles, where functionality is determined more by code than physical components, represent both an existential threat and enormous opportunity for component suppliers.

For Sona Comstar, this transition requires a fundamental expansion of capabilities. It's no longer enough to make excellent motors; those motors need embedded intelligence to communicate with vehicle systems, optimize performance in real-time, and update functionality over-the-air. The company's investments in embedded software and control systems represent early steps in this direction, but the journey is just beginning.

The competitive landscape is also shifting. Traditional boundaries between suppliers, OEMs, and technology companies are blurring. Apple and Google want to define the vehicle experience through software. Tesla believes in vertical integration, bringing component manufacturing in-house. Chinese EV makers are creating new supplier ecosystems that bypass traditional Tier 1 suppliers entirely.

The Humanoid Robot Tangent: Genius or Distraction?

Sona Comstar's foray into components for humanoid robots might seem like science fiction, but it represents strategic optionality. The same precision gears that enable smooth differential operation in cars could power joint movements in robots. The motor control expertise developed for EVs applies directly to robotic actuators. The embedded software capabilities needed for automotive applications translate to robotics control systems.

If humanoid robots achieve even a fraction of the market penetration optimists predict, early movers in component supply could capture enormous value. But this is a bet on an uncertain future, requiring investment today for returns that might not materialize for a decade. It's the kind of strategic option that only a company with strong cash flows and a solid core business can afford to pursue.

Can Indian Companies Compete Globally in High-Tech Components?

Sona Comstar's journey provides one answer to this question: Yes, but it requires more than just low costs. Success demands technology leadership, global presence, world-class quality, and the ability to partner with customers on next-generation products. It requires patient capital willing to invest through cycles. And critically, it requires management with global ambition and execution capabilities.

The broader implications extend beyond Sona Comstar. If Indian companies can compete in precision automotive components—one of the most demanding manufacturing sectors—they can compete in anything. The playbook Sona Comstar has written—partner with global leaders, invest in technology, maintain quality discipline, expand strategically—provides a template for other Indian manufacturers aspiring to global leadership.

Final Reflections: A Story Still Being Written

The Sona Comstar story is far from over. In many ways, the post-Blackstone era is just the beginning of a new chapter. The company must now prove it can sustain the transformation without PE ownership, navigate the EV transition as competition intensifies, and potentially expand into new adjacencies like robotics and rail.

For investors, Sona Comstar represents a bet on multiple themes: the electrification of transport, India's manufacturing competitiveness, the importance of physical components even in a software-defined world, and management's ability to execute a complex global strategy. It's not a simple story, which perhaps makes it more interesting.

For India, Sona Comstar demonstrates what's possible when ambition meets execution. A company that started as a joint venture to bring Japanese forging technology to India has become a global leader in EV components, competing with anyone, anywhere, on technology and quality. It's a validation of India's manufacturing potential and a challenge to others to aim higher.

As the automotive industry undergoes its greatest transformation in a century, component suppliers like Sona Comstar will play a critical but often invisible role. They won't get the headlines that Tesla or Rivian generate. Their CEOs won't become household names. But without their precision gears, sophisticated motors, and intelligent controllers, the electric mobility revolution simply wouldn't be possible.

The story of Sona Comstar is ultimately a story about transformation—of companies, industries, and entire economies. It shows that with the right strategy, capital, and execution, traditional manufacturers can reinvent themselves for the digital age. It demonstrates that emerging market companies can compete globally in high-technology sectors. And it proves that sometimes, the most interesting investments aren't in the flashy disruptors but in the enabling technologies that make disruption possible.

As we look toward a future of electric, autonomous, shared, and software-defined mobility, companies like Sona Comstar will continue to evolve, adapt, and innovate. Their success or failure will determine not just investment returns but the pace and shape of the mobility transformation itself. The gears are turning, the motors are spinning, and the future—electric and beyond—is being forged in facilities from Gurugram to Detroit, Shanghai to Stuttgart. The journey that began with precision forging in the 1990s continues toward horizons we're only beginning to imagine.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube