Solar Industries India: From Railway Stations to Rockets - India's Explosives Empire

I. Introduction & Episode Teaser

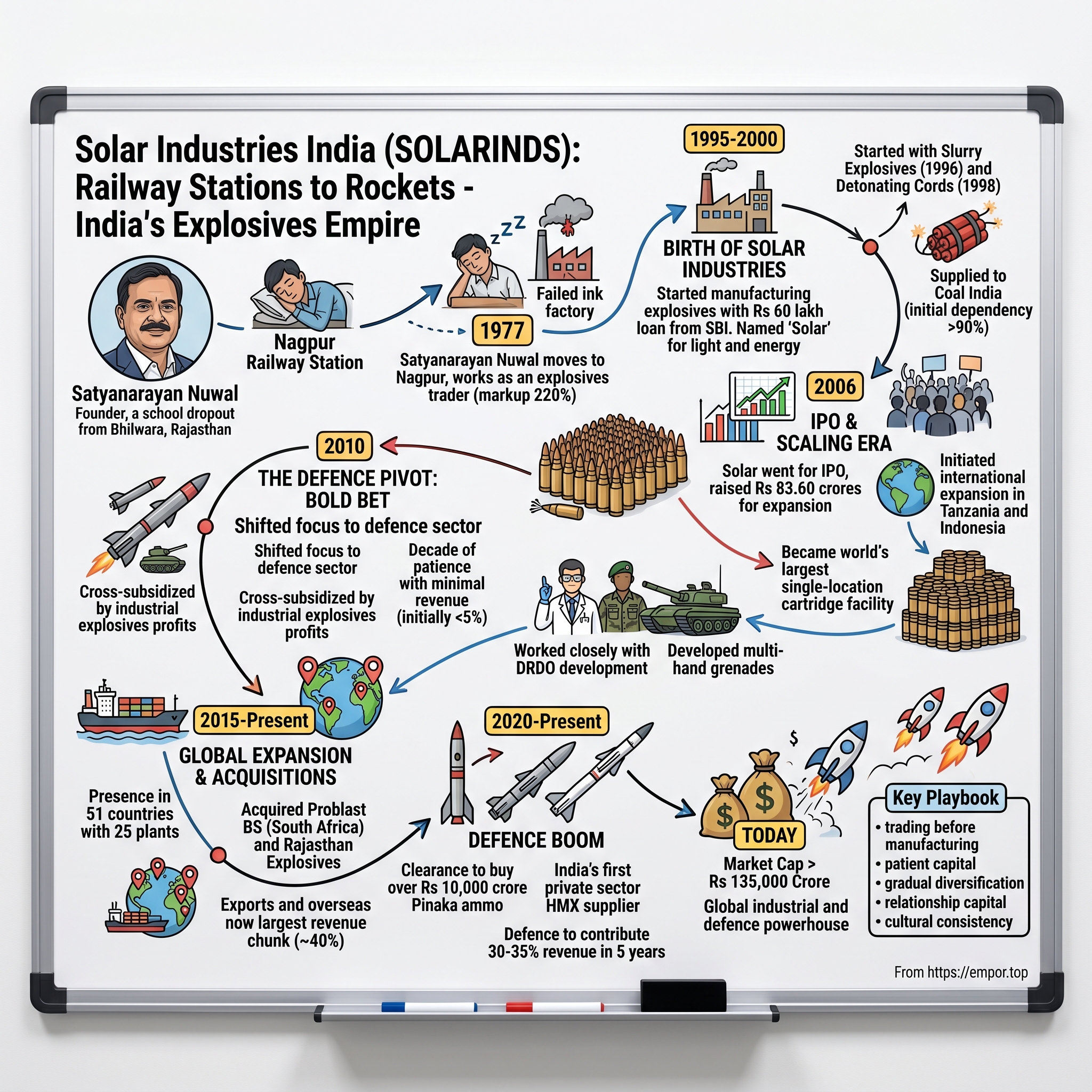

The year is 1977. A young man from Rajasthan sleeps on the platform of Nagpur railway station, his worldly possessions fitting into a single cloth bag. He has no money for rent, no formal education beyond tenth grade, and his first business venture—an ink manufacturing plant—has already failed spectacularly. Yet within this seemingly hopeless situation lies the seed of what would become Solar Industries India Limited, a company that today commands a market capitalization exceeding Rs 135,000 crore and stands as India's explosives and defence manufacturing giant.

This is not merely a rags-to-riches story. It's the chronicle of how Satyanarayan Nuwal transformed from a struggling trader sleeping in railway stations to building India's largest domestic manufacturer of bulk and cartridge explosives. It's about how a company that started by supplying dynamite to coal mines pivoted to manufacturing sophisticated propellants for India's missile systems. It's the unlikely journey from trading explosives at a 220% markup to winning Rs 10,000 crore defence contracts from the Indian government.

Solar Industries today operates 25 plants across eight Indian states and four international locations, with a presence in 51 countries. The company manufactures everything from industrial explosives for mining and infrastructure to composite propellants for Pinaka, Akash, and Brahmos missile systems. Its defence division, once a money-losing bet that the company sustained for over a decade, now promises to contribute 30-35% of revenues within the next five years.

But to understand how Solar Industries became the powerhouse it is today, we must return to those railway platforms of Nagpur, where a young man's desperation met opportunity in the most unexpected way. We must trace the evolution from a Rs 60 lakh loan in 1995 to a company that today stands at the forefront of India's atmanirbhar (self-reliance) defence manufacturing ambitions.

This is the story of patient capital, of betting on defence capabilities fifteen years before they paid off, of managing the delicate transition from family business to professional enterprise, and of riding the twin waves of India's infrastructure boom and defence indigenization. It's about how a school dropout from Bhilwara built one of India's most valuable defence and explosives companies, competing with global giants and winning.

II. The Satyanarayan Nuwal Origin Story

The story of Satyanarayan Nandlal Nuwal reads like a classical tragedy that transformed into an epic triumph. Born into a middle-class family in Bhilwara, Rajasthan, Nuwal dropped out of school after class 10 due to financial constraints. His father worked as a Patwari and earned meagre income to support his family, while his grandfather was a shopkeeper. The young Nuwal lived a simple life in this modest environment, speaking primarily in Hindi and harboring dreams far bigger than his circumstances would suggest.

The entrepreneurial spirit manifested early, though not without its failures. At the age of 18, he opened an ink production plant. Although his first business venture failed miserably, he learnt many things about business. This early failure would have crushed many, but for Nuwal, it was merely the first lesson in what would become a masterclass in perseverance. In the year after he turned 19, he got married, adding family responsibilities to his already challenging circumstances.

The darkest period of Nuwal's journey came when he moved to Nagpur, the city that would eventually become the headquarters of his empire. He moved to Nagpur to work with a relative. He didn't have enough money to rent out a house and spent his initial nights in the big city sleeping in the railway station. During his times of financial struggle, Satyanarayan did not have enough money to rent a house, forcing him to spend many nights at a Railway station. He also sold fountain pens to earn his living during those times. Picture this: a school dropout from rural Rajasthan, sleeping on railway platforms in Nagpur, selling fountain pens during the day to survive, carrying the weight of a failed business and a young marriage on his shoulders.

He tried his hand at many things, including a leasing business and a transport company but everything failed. Yet each failure added another layer of understanding about business, about markets, about survival. These weren't just business failures; they were tuition fees paid to the university of life, each setback teaching him something that no formal education could have provided.

The turning point came in 1977, a moment that would redirect the entire trajectory of Nuwal's life. In 1977, Nuwal came to Balharshah in Chandrapur district of Maharashtra, where he met Abdul Sattar Allahbhai, a dealer in explosives used for digging wells, building roads, and digging mines. This meeting wasn't just a business opportunity; it was destiny knocking on the door of a man who had nothing left to lose.

He got a licence to trade explosives and a warehouse to store them, paying a monthly fee of Rs 1,000 rupees to the licence holder. Nuwal started doing business with Abdul Sattar's by paying Rs 1,000 a month, using his license to sell explosives. Think about the audacity of this arrangement: a man who couldn't afford rent for a house was now paying Rs 1,000 per month—a significant sum in 1977—to access an explosives license. It was a calculated risk that only someone who had already lost everything could take.

The explosives trading business revealed Nuwal's innate understanding of margin and market dynamics. He would buy explosives at 250 rupees per kilogram and sell them at 800 rupees—a markup of 220%. This wasn't gouging; it was understanding the value chain, the risks involved in handling dangerous materials, and the premium that reliability commanded in a market where delays could shut down entire mining operations.

The entrepreneur spent several years supplying explosives to the state-owned coal mines and as a consignment agent for Imperial Chemicals Industry. Soon, the officials of Imperial Chemical Industries, a British firm, noticed Nuwal, and this opened a whole new world for him. The recognition from ICI wasn't just validation; it was an education in international standards, quality control, and the importance of systematic business practices.

For nearly two decades, from 1977 to 1995, Nuwal remained in the trading business. This wasn't stagnation; it was preparation. He was learning the intricacies of the explosives industry—understanding customer needs, building relationships with Coal India's procurement teams, navigating the complex regulatory landscape of handling dangerous goods, and most importantly, accumulating capital and credibility for his next move.

During these years, Nuwal developed an encyclopedic knowledge of the explosives business. He understood the seasonal patterns of demand, the technical specifications different mining operations required, the logistics challenges of transporting hazardous materials, and the importance of maintaining impeccable safety records. He knew which mines preferred which types of explosives, which procurement officers valued reliability over price, and which competitors cut corners on safety.

The trading years also taught him about cash flow management—critical in a business where government entities like Coal India could take months to clear payments. He learned to manage working capital, to negotiate payment terms, to balance the books when large orders meant significant upfront investments. These lessons, learned not in business school but in the harsh reality of day-to-day operations, would prove invaluable when he made the leap to manufacturing.

By the early 1990s, India was liberalizing its economy, and Nuwal sensed opportunity. The explosives market was dominated by a few large players, mostly multinationals or government entities. There was room for an agile, customer-focused Indian company that understood local conditions and could provide customized solutions. But moving from trading to manufacturing meant taking on enormous risk—technical, financial, and regulatory.

The decision to start manufacturing wasn't made lightly. Nuwal had seen traders come and go, but manufacturers—those who controlled their own production—had staying power. They could ensure quality, manage costs, innovate on products, and most importantly, capture a much larger share of the value chain. The trader's margin was limited by what the market would bear; the manufacturer's margin was limited only by their efficiency and innovation.

As 1995 approached, Nuwal had spent 18 years in the explosives business. He had gone from sleeping on railway platforms to becoming a respected trader. He had built relationships, accumulated knowledge, and saved capital. More importantly, he had developed a vision for what an Indian explosives company could be—not just a supplier of commodities, but a partner in India's industrial growth.

The boy from Bhilwara who dropped out after tenth grade had become a man who understood business at a granular level. The failed ink manufacturer had learned from his mistakes. The fountain pen seller had discovered his true calling. The railway platform sleeper had found his home in Nagpur. The stage was set for the transformation from trader to industrialist, from Satyanarayan Nuwal the survivor to Satyanarayan Nuwal the founder of Solar Industries India Limited.

III. The Birth of Solar Industries (1995-2000)

The year 1995 marked the inflection point in Satyanarayan Nuwal's journey. After nearly two decades of trading explosives, understanding every nuance of the business, building relationships, and accumulating capital, he was ready to make the leap from middleman to manufacturer. In 1995, Nuwal started a small unit of manufacturing explosives by taking a loan of Rs 60 lakh from the State Bank of India under the name Solar Explosives Limited.

The decision to name the company "Solar" wasn't arbitrary. It represented light, energy, power—everything that explosives embodied in their controlled release of force. It also suggested something aspirational, reaching for the sun, aiming high. For a man who had spent nights on railway platforms, naming his company after the celestial body that brings light to darkness held profound symbolism.

By the year 1996, Solar established trade network as well as Institutional market. The Company started manufacturing Slurry Explosives in the year 1996 and Detonating Cords in the year 1998. The transition from trader to manufacturer wasn't seamless. Manufacturing explosives required technical expertise, quality control systems, safety protocols, and regulatory compliance at a level far beyond what trading demanded. It meant investing in machinery, training workers, establishing standard operating procedures, and most critically, ensuring zero accidents in an inherently dangerous business.

The initial focus was deliberate and strategic. Nuwal didn't try to manufacture every type of explosive immediately. He started with what he knew best—the products he had been trading for years, the ones where he understood customer requirements intimately. Slurry explosives were widely used in mining operations, particularly by Coal India, his largest customer from his trading days. This wasn't diversification for its own sake; it was vertical integration of a proven business model.

The Rs 60 lakh loan from State Bank of India represented enormous risk. This wasn't venture capital or patient money from investors who understood the long-term vision. This was debt that needed to be serviced from day one, with assets pledged as collateral. For a first-generation entrepreneur without inherited wealth or safety nets, defaulting on this loan would mean not just business failure but complete financial ruin. The pressure must have been immense—every day of production delays, every quality issue, every customer complaint could potentially trigger a cascade toward bankruptcy.

But Nuwal had advantages that weren't visible on a balance sheet. His years of trading had given him something invaluable: trust. Coal India's procurement officers knew him, had dealt with him for years, understood his commitment to timely delivery and quality. When Solar Industries started manufacturing, these relationships translated into orders. The same people who had bought traded explosives from Nuwal were willing to give his manufactured products a chance.

The company incorporated on February 24, 1995 with the name Solar Explosives Limited was promoted by Satyanarayan Nuwal. The formal incorporation was more than paperwork; it was the crystallization of a vision that had been brewing for two decades. This wasn't just another explosives manufacturer entering a crowded market. This was a company founded by someone who had seen the industry from the bottom up, who understood the pain points of customers because he had been solving them as a trader for years.

The early manufacturing operations were modest. The company focused on bulk explosives initially—products that were consumed in large quantities by mining operations. These weren't technically sophisticated products requiring extensive R&D; they were workhorses of the mining industry where reliability, consistency, and price mattered more than innovation. This pragmatic approach allowed Solar to establish its manufacturing credentials without overextending technically or financially.

The location choice of Nagpur as headquarters wasn't accidental. Nagpur sat at the geographic center of India, providing logistical advantages for a company dealing in hazardous materials that required special transportation permits and protocols. It was also close to the coal belt of central India—Chhattisgarh, Jharkhand, Odisha—where the bulk of Solar's customers operated. The city where Nuwal had once slept on railway platforms became the nerve center of his industrial empire.

Quality control became an obsession from day one. In the explosives business, a single quality failure could result not just in customer dissatisfaction but in fatalities. Solar invested heavily in testing equipment, established multiple quality checkpoints, and created a culture where safety wasn't negotiable. Workers were trained not just in manufacturing processes but in understanding why each step mattered, why shortcuts could be fatal, why adherence to protocols was literally a matter of life and death.

The financial management during these early years reflected hard-learned lessons from Nuwal's trading days. Cash flow was managed meticulously. Payment terms with suppliers were negotiated carefully. Customer credit was extended judiciously. The company couldn't afford the luxury of growth at any cost; every expansion had to be self-financing or backed by confirmed orders. This wasn't the Silicon Valley model of blitzscaling; this was the Nagpur model of sustainable, profitable growth.

For a long time, the explosives business was hugely dependent on Coal India (over 90% revenues at one point). "It is down to 38% today. This heavy concentration on a single customer was both a blessing and a curse. It provided steady revenues and simplified operations—Solar could optimize its entire production around Coal India's requirements. But it also created enormous risk. Any change in Coal India's procurement policies, any delay in payments, any shift in mining activity could devastate Solar's business.

The relationship with Coal India during these early years was symbiotic. Coal India needed reliable suppliers who could deliver quality explosives on schedule to keep mining operations running. Solar needed large, creditworthy customers who could provide the volume necessary to achieve economies of scale. The fact that Nuwal had been supplying Coal India as a trader for years gave Solar a crucial advantage—he understood their procurement cycles, their technical requirements, their payment patterns.

Also, they commissioned 10,000 MT capacity Plant for manufacture of bulk explosives in Ramgarh, Jharkhand State, to meet the requirement of Central Coal Fields Ltd. The expansion into Jharkhand represented the next phase of growth—moving production closer to consumption. Transporting explosives across states involved complex regulatory requirements, safety risks, and high costs. By establishing manufacturing near mining sites, Solar could reduce logistics costs, improve response times, and deepen customer relationships.

The technical capabilities built during these early years laid the foundation for everything that followed. Solar learned to handle ammonium nitrate safely at scale. It developed expertise in mixing and formulating different types of explosives for different geological conditions. It created systems for managing inventory of hazardous materials. It built a workforce trained in the unique requirements of explosives manufacturing. These capabilities couldn't be bought or imported; they had to be developed through experience, through trial and error, through gradual accumulation of knowledge.

The competitive landscape during the late 1990s was challenging. Established players like ICI (Imperial Chemical Industries) had technical superiority and global backing. Government entities like IDL (India Defence Limited) had preferential access to certain markets. International players were entering India as the economy liberalized. For Solar to survive and thrive, it needed to find its niche—and that niche was customer service and customization.

Where multinationals offered standardized products designed for global markets, Solar offered customization for Indian conditions. Where government entities operated with bureaucratic slowness, Solar responded with entrepreneurial agility. Where international players struggled with local regulations and relationships, Solar navigated them with ease born from decades of experience. The company's value proposition wasn't just explosives; it was explosives delivered how, when, and where Indian customers needed them.

The financial performance during these early years was modest but steady. This wasn't a company posting spectacular growth rates or revolutionary margins. It was a company building brick by brick, customer by customer, capability by capability. Profits were reinvested into expanding production, improving quality, and deepening market presence. The discipline forged in those early days—the focus on cash flow, the obsession with quality, the commitment to customer service—would become organizational DNA that persisted even as the company grew thousand-fold.

Cultural elements established during this period would prove crucial for Solar's future. The company culture reflected its founder's journey—respectful of humble beginnings, paranoid about cash management, obsessive about safety, and deeply committed to customer relationships. Employees weren't just workers; they were partners in building something significant. Many early employees would stay with the company for decades, growing from operators to managers to leaders as Solar expanded.

By the turn of the millennium, Solar Industries had successfully made the transition from trading to manufacturing. The company that started with a Rs 60 lakh loan was generating crores in revenue. The infrastructure was in place—manufacturing facilities, quality systems, customer relationships, and organizational capabilities. The foundation had been laid for what would come next: explosive growth, literal and metaphorical, that would transform Solar from a regional supplier to a national champion and eventually to a global player in both industrial explosives and defence.

IV. The IPO & Scaling Era (2000-2010)

The period from 2000 to 2010 marked Solar Industries' transformation from a regional explosives manufacturer to a publicly listed company with national ambitions. In 2006, Solar Industries went for an IPO. This wasn't just a financial milestone; it was the validation of a business model that had been built over three decades, from the trading days of the 1970s through the manufacturing establishment of the 1990s.

The IPO details revealed the scale of ambition: a public issue of 44,00,000 equity shares at Rs 190 per share, aggregating to Rs 83.60 crores, with the IPO opening on March 9, 2006, closing on March 13, 2006, and listing on April 3, 2006. For a company that had started with a Rs 60 lakh loan just eleven years earlier, raising Rs 83.60 crores from public markets represented exponential growth and a fundamental shift in scale and ambition.

The IPO prospectus revealed Solar's strategic priorities for the raised capital. The funds were earmarked for expansion projects for manufacturing bulk explosives in India, expansion projects for manufacturing bulk explosives overseas, and to meet the margin requirement for working capital. This wasn't just about growing bigger; it was about internationalizing from the very beginning, recognizing that the explosives business would eventually require geographic diversification.

The timing of the IPO was fortuitous. India's economy was booming, infrastructure spending was accelerating, and mining activity was expanding to feed the country's growing energy and steel demands. The stock market was receptive to manufacturing stories, particularly those tied to India's infrastructure build-out. Solar positioned itself not just as an explosives company but as an essential enabler of India's growth story—every road built, every tunnel blasted, every coal mine expanded required explosives.

Manish joined the company in the mid-nineties. The entry of the second generation marked a crucial transition point. Manish Nuwal brought fresh perspectives, formal education, and international exposure to complement his father's street-smart entrepreneurial instincts. This wasn't the typical second-generation story of reluctant succession or family conflict. Manish had joined when the company was still small, learning the business from the ground up, earning credibility through performance rather than inheritance.

The post-IPO period saw aggressive capacity expansion. By 1996, Solar established trade network as well as Institutional market. The Company started manufacturing Slurry Explosives in the year 1996 and Detonating Cords in the year 1998. The company wasn't just adding production lines; it was building an integrated manufacturing ecosystem. Each new product category—from slurry explosives to detonating cords to electronic detonators—represented deeper technical capabilities and stronger customer lock-in.

Geographic expansion within India accelerated during this period. They commissioned 10,000 MT capacity Plant for manufacture of bulk explosives in Ramgarh, Jharkhand State, to meet the requirement of Central Coal Fields Ltd. This plant-near-customer strategy reduced transportation costs and risks while deepening relationships with key accounts. It also demonstrated Solar's willingness to make customer-specific investments, a level of commitment that multinational competitors often couldn't match.

The international expansion began earlier than most Indian companies of that era contemplated. They incorporated a new overseas subsidiary company, namely Solar Nitrochemicals Ltd at Tanzania. The company incorporated PT Solar Mining Resources at Indonesia as wholly owned Subsidiary. They incorporated three new overseas subsidiaries companies namely Solar Recursos Minerals LDA, Solar Industrias LDA, Solar Agro Florestal LDA, at Mozambique. These weren't vanity projects or speculative ventures; they were calculated moves into markets with significant mining activity and less sophisticated local competition.

Solar became the world's largest cartridge manufacturing facility at a single location. This achievement wasn't just about scale; it represented manufacturing excellence that could compete globally. Building the world's largest facility required not just capital but also process innovation, quality systems, and operational efficiency that matched or exceeded global standards. It sent a signal to customers worldwide that an Indian company could deliver world-class manufacturing at competitive costs.

The organizational structure evolved significantly during this period. The company's wholly owned subsidiaries, Solar Capital Ltd and Solar Industries Ltd merged with the company with effect from April 1, 2008. This consolidation simplified the corporate structure, improved financial transparency, and prepared the company for the next phase of growth. It also reflected growing sophistication in corporate governance, moving from an entrepreneur-driven structure to a professionally managed organization.

Financial performance during this decade validated the growth strategy. Revenue grew from tens of crores to hundreds of crores. Profitability improved as economies of scale kicked in and operational efficiencies improved. The stock price, while volatile during the 2008 financial crisis, generally trended upward, rewarding early investors who had taken a chance on a first-generation entrepreneur's vision.

The customer base diversification accelerated during this period, though Coal India remained dominant. For a long time, the explosives business was hugely dependent on Coal India (over 90% revenues at one point). It is down to 38% today. This gradual reduction in customer concentration didn't happen by accident. Solar systematically targeted other mining companies, infrastructure contractors, and international customers to reduce dependency on any single buyer.

Technology advancement became a priority during this period. Solar wasn't content being a low-cost manufacturer of commodity explosives. The company invested in research and development, working on new formulations, safer products, and more efficient delivery systems. Electronic detonators, for instance, offered precise timing control that could improve blasting efficiency and reduce vibration—critical for mining operations near populated areas.

The human capital development during this decade laid the foundation for future growth. Solar recruited engineers, chemists, and management professionals who brought formal training to complement the practical knowledge of early employees. Training programs were institutionalized. Safety became not just a compliance requirement but a cultural value. The company that had started with workers hired from local communities was now attracting talent from India's top engineering and management institutions.

Quality certifications obtained during this period opened international markets. ISO certifications, safety standards, and environmental compliance weren't just badges to display; they were passports to global markets where customers demanded documented quality systems. For a company with international ambitions, these certifications were essential infrastructure, as important as manufacturing equipment.

The competitive dynamics during this decade were intense. International players were entering India as the economy liberalized. Chinese manufacturers were offering lower prices. Domestic competitors were expanding capacity. Solar's response wasn't to engage in price wars but to focus on service, reliability, and customization. The company's ability to respond quickly to customer needs, to customize products for specific applications, and to provide technical support differentiated it from both low-cost and multinational competitors.

Supply chain management became increasingly sophisticated during this period. Managing raw materials for explosives manufacturing involved dealing with regulated chemicals, ensuring consistent quality, and maintaining safety throughout the supply chain. Solar developed relationships with reliable suppliers, created buffer stocks for critical materials, and implemented quality control at every stage from raw material to finished product.

The regulatory environment during this decade was complex and evolving. Explosives manufacturing involved multiple regulatory bodies—from local police for storage licenses to national authorities for manufacturing permits to international bodies for export licenses. Solar's ability to navigate this regulatory maze, built on decades of experience, became a competitive advantage. New entrants often underestimated the complexity of regulatory compliance in the explosives business.

Risk management evolved from informal processes to formal systems during this period. The company implemented enterprise risk management frameworks, identifying operational, financial, regulatory, and strategic risks. Insurance coverage was expanded. Safety protocols were enhanced. Financial hedging instruments were used to manage commodity price risks. This systematic approach to risk management was essential for a company handling inherently dangerous products.

The brand building during this decade was subtle but effective. Solar didn't need consumer advertising, but it needed recognition among mining engineers, procurement managers, and government officials. The company participated in industry conferences, published technical papers, and demonstrated thought leadership in blasting technology. The brand gradually became synonymous with reliability and technical competence in Indian industrial explosives.

As the decade closed, Solar Industries had successfully transformed from a family-run manufacturing company to a professionally managed, publicly listed corporation. The company had the scale to compete nationally, the capabilities to expand internationally, and the ambition to enter new segments. The foundation was set for the next transformation—the bold pivot into defence manufacturing that would define Solar's next decade and ultimately transform it into one of India's most valuable defence companies.

V. The Defence Pivot: Bold Bet or Natural Evolution? (2010-2020)

The year 2010 marked a watershed moment in Solar Industries' history. In 2010, Solar Industries moved into the defence sector for its next phase of growth. This wasn't an incremental expansion or a natural evolution of existing capabilities. It was a calculated bet on India's future defence needs, made at a time when private sector participation in defence manufacturing was minimal and the path to success unclear.

"We started work on defence in 2010-11, and till the end of 2020, it was a very small share of our revenue. Three years ago, it was about 5%; that has grown to 20% now," says Nuwal. This timeline reveals the extraordinary patience required. A full decade of investment, research, and capability building before defence became a meaningful contributor to revenues. For most companies, particularly publicly listed ones facing quarterly earnings pressure, such a long gestation period would be unthinkable.

"Our core business of explosives was generating profits and that allowed us to invest in defence. That was the comforting factor even though defence was not really delivering results," says Nuwal. This cross-subsidization strategy was crucial. The stable cash flows from the industrial explosives business funded the speculative investment in defence capabilities. It was patient capital in its truest form—profits from today funding the opportunities of tomorrow.

The decision to enter defence wasn't random. Solar understood explosives chemistry, had manufacturing capabilities for hazardous materials, and possessed the quality systems necessary for critical applications. The technical leap from industrial explosives to military-grade materials was significant but not insurmountable. What Solar lacked was specific knowledge of military specifications, testing protocols, and the complex procurement processes of defence establishments.

Initially, though, growth in defence was hard to come by, and there were a host of apprehensions. During the testing phase, money in the form of capex had already been put in and the manufacturing capacity was in place. However, orders were elusive. This period tested Solar's resolve. Capital was deployed, facilities were built, teams were hired, but revenues remained negligible. For a company accustomed to the relatively predictable business of supplying explosives to mining companies, the uncertainty of defence procurement must have been deeply unsettling.

The relationship with DRDO became the cornerstone of Solar's defence strategy. The first was multi-mode hand grenades for which Solar worked closely with the Defence Research and Development Organisation (DRDO) for nearly three years. In many ways, this was the watershed moment for Solar and perhaps for the private sector defence industry as well. This collaboration wasn't just about technology transfer; it was about learning the culture of defence R&D, understanding military requirements, and building credibility with the armed forces.

In the case of Solar Industries, the products are expected to cover the value chain and products/solutions are co-developed or ToT (transfer of technology) is sourced from the DRDO. This co-development model was crucial. Unlike simple technology transfer where a company receives blueprints and manufacturing instructions, co-development meant Solar's engineers worked alongside DRDO scientists, understanding not just the 'how' but the 'why' of defence technologies.

The technology transfer process from DRDO followed established protocols. These are the technologies for which Indian Armed Forces/ MHA/ other Govt. agencies (both central & state) are the only end users. Category 'A' technologies are military technologies and are referred to as "MILTECH". Export of Cat 'A' technologies is subjected to approval process of DRDO and MoD, Govt of India. ToT to the industry is done directly by DRDO for all Category 'A' technologies. Solar had to navigate these complex categorizations, understanding which technologies could be commercialized and which were restricted to government use.

The product portfolio that emerged from this decade of development was sophisticated and diverse. Solar began manufacturing propellants for missiles and rockets, warheads, and warhead explosives. These weren't simple adaptations of industrial explosives; they required entirely new formulations, manufacturing processes, and quality control systems. Missile propellants, for instance, needed to maintain stable performance across extreme temperature ranges, survive years of storage, and deliver precise thrust profiles.

India's first domestic supplier in private sector of HMX & HMX compounded products to defence marked a significant achievement. HMX (cyclotetramethylene-tetranitramine) is one of the most powerful chemical explosives, significantly more potent than TNT. Manufacturing HMX required not just technical capability but also the highest levels of safety protocols and regulatory compliance. For Solar to become India's first private sector supplier demonstrated both technical mastery and institutional trust.

The memory of Uri and Pathankot terrorist attacks are still fresh in our minds. It was also a turning point in the company's defence foray in terms of landing an important order. "India needed a supply base for ammunition, and it was our growth opportunity," says Nuwal. Geopolitical events created urgency around defence preparedness and domestic manufacturing capabilities. The attacks highlighted India's vulnerability and the need for reliable, indigenous suppliers of defence materials.

The organizational structure for defence was carefully designed. The defence business is housed in wholly-owned subsidiary Economic Explosives Ltd. This separation served multiple purposes: it ring-fenced the defence business from commercial operations, allowed for specialized security protocols, and created clarity in financial reporting. It also signaled to defence customers that Solar took their requirements seriously enough to create a dedicated entity.

"We were getting good feedback on our products from Europe and the US. We needed a break in India," he says. International validation preceded domestic success—a common pattern in Indian defence manufacturing where foreign customers often recognize quality before domestic procurement agencies. This international feedback provided both validation of Solar's capabilities and leverage in domestic negotiations.

The investment in defence wasn't just financial; it was also human. Solar recruited specialists in military chemistry, ballistics experts, and professionals with experience in defence procurement. These weren't skills available in the general talent market; Solar had to identify retired defence personnel, academics specializing in energetic materials, and engineers willing to work in a highly regulated, slow-moving sector.

Quality assurance for defence products operated at an entirely different level from commercial explosives. Every batch required extensive testing, documentation, and often witnessed testing by defence personnel. Failure rates that might be acceptable in commercial applications—perhaps one in a thousand—were unacceptable in defence where a single failure could compromise a mission or endanger lives. Solar had to rebuild its entire quality philosophy around zero-defect manufacturing.

The regulatory environment for defence manufacturing was labyrinthine. Beyond the standard explosives licenses, Solar needed security clearances, export licenses for certain materials, and compliance with defence procurement procedures. The company had to establish secure facilities, implement information security protocols, and create audit trails that could withstand scrutiny from multiple government agencies.

"Solar invested way ahead of time in defence. Today, it seems like a smart move, but the important thing is that they stayed the course through multiple challenges," says Vinit Bolinjkar, Head of Research at brokerage Ventura Securities. This external validation highlights what made Solar's defence bet remarkable—not just the foresight to enter the sector but the perseverance to persist through a decade of minimal returns.

The technology evolution during this period was significant. Solar moved from basic explosive materials to sophisticated composite propellants. composite propellants (Pinaka, Akash, Brahmos etc.), rockets & warheads for missiles filling of ammunition & fuzes and high energy material. Each of these systems required different technologies, manufacturing processes, and expertise. Pinaka's propellant, for instance, needed to provide consistent thrust over specific burn rates, while Brahmos required materials that could withstand supersonic flight conditions.

The learning curve was steep and expensive. Early batches often failed testing. Formulations that worked in laboratory conditions failed in field trials. Manufacturing processes that produced consistent results at small scale became unreliable at production volumes. Each failure meant not just financial loss but also potential damage to credibility with defence customers who had limited patience for private sector learning curves.

Financial discipline during this period was crucial. While investing heavily in defence, Solar maintained strict control over costs. The defence facilities were designed to be multipurpose where possible, able to manufacture both defence and commercial products with appropriate segregation. This flexibility reduced the financial burden of idle capacity during the long wait for defence orders.

The cultural transformation within Solar during this decade was profound. The company that had built its success on responsive customer service and quick decision-making had to adapt to the deliberate pace of defence procurement. Employees had to learn that a two-year sales cycle was normal, that technical specifications could change multiple times during development, and that success was measured not in quarterly revenues but in capability milestones achieved.

Risk management became even more critical with defence manufacturing. The consequences of accidents weren't just financial but could include criminal liability and loss of licenses. Solar implemented multiple layers of safety protocols, invested in automated systems to minimize human error, and created a culture where safety concerns could halt production immediately regardless of delivery pressures.

The international landscape during this period was changing favorably for companies like Solar. Global defence companies were looking for Indian partners to access the growing domestic market. Geopolitical tensions were increasing defence spending worldwide. The concept of "China plus one" was driving countries to diversify supply chains away from Chinese manufacturers. Solar positioned itself to benefit from all these trends.

Make in India, announced in 2014, provided additional momentum though its full impact wouldn't be felt until the next decade. The policy signaled government intent to increase domestic defence manufacturing, reduce import dependence, and support private sector participation. For Solar, which had already invested significantly in defence capabilities, this was validation of its early bet.

The decade ended with Solar having established credibility in defence but still waiting for the breakthrough orders that would validate the investment. More importantly, all the pieces of the defence business are in place to pave the way for further growth. The capabilities were built, relationships established, and credentials earned. The stage was set for the dramatic growth that would follow in the 2020s.

Looking back, the defence pivot appears prescient and inevitable. But in 2010, when Solar made the decision to invest heavily in defence with no assured returns, it was a leap of faith. That this leap was taken by a first-generation entrepreneur who had built his business on pragmatism and financial discipline makes it even more remarkable. It demonstrated that Solar wasn't just content being a successful explosives company; it aspired to be a strategic player in India's defence ecosystem.

VI. Global Expansion & Acquisitions (2015-Present)

The period from 2015 onwards marked Solar Industries' transformation from an India-centric company to a truly global player. Manufacturing facilities in 5 countries and presence in 51 countries wasn't achieved through organic growth alone but through strategic acquisitions, partnerships, and a deep understanding of international markets developed over two decades.

The company's two-decades-old presence in the international market helped it manage the South African acquisition better. This experience was crucial. Solar hadn't jumped into international markets overnight; it had methodically built capabilities, understanding local regulations, cultural nuances, and business practices across multiple geographies. This patient approach to internationalization distinguished Solar from companies that expanded internationally prematurely and failed.

Nuwal outlines a couple of important purchases in the last two-three years-Rajasthan Explosives & Chemicals (in April 2023) and South Africa's Problast BS (a blasting solutions company for mining that has enhanced Solar's presence in Africa). These acquisitions weren't random opportunistic purchases but strategic moves that filled specific gaps in Solar's capabilities and market presence.

Solar Industries has acquired 73.99% stake in Problast BS (South Africa), through its South African subsidiary (Solar Mining Services). Problast BS is into the business of complete blasting solutions including open cast mining, drilling, blasting & loading in South Africa. This acquisition represented more than just entering a new market; it was about acquiring integrated capabilities that Solar could leverage across its global operations.

The financial performance of Problast validated the acquisition strategy. It reported revenues of Rs 276 crore in FY22 and Rs 346 crore in FY23. These weren't distressed assets being acquired at bargain prices; they were profitable, growing businesses that could immediately contribute to Solar's top and bottom lines while providing strategic advantages.

Problast BS (Pty) has been recognized as the premier blasting solution provider in South Africa since 2016. This reputation was crucial. Solar wasn't just buying assets or market access; it was acquiring credibility and relationships that would have taken years to build organically. In the mining industry, where safety records and operational reliability determine vendor selection, such reputation was invaluable.

The Company's investment in Problast BS (Pty) Ltd is in line with the long-term business plan of the Company to expand its business operations in African continent. Africa represented enormous potential for Solar. The continent's mining industry was growing, infrastructure development was accelerating, and local explosives manufacturing capabilities were limited. Solar's strategy was to become the dominant player before international competitors recognized the opportunity.

"We could easily adapt to the local culture. A good understanding of the market was a great help," says Nuwal. This cultural adaptability was a competitive advantage often overlooked in financial analyses. Solar's ability to work effectively in diverse cultural contexts—from tribal areas in central India to sophisticated boardrooms in Europe to mining sites in Africa—reflected organizational maturity that couldn't be replicated quickly by competitors.

The Rajasthan Explosives & Chemicals acquisition in April 2023 served a different strategic purpose. This was about consolidating the domestic market, acquiring complementary capabilities, and achieving economies of scale. It demonstrated that Solar's acquisition strategy wasn't just about international expansion but also about strengthening its home market position.

We believe that this acquisition will help Solar Industries to expand its operations in the African continent and to boost its overall exports & overseas revenues (~40% of sales) which declined 12% YoY in FY24. The focus on exports and overseas revenues reflected Solar's evolution from a domestic supplier dependent on Coal India to a global player with diversified revenue streams.

The geographic expansion strategy was carefully calibrated. 25 plants across 8 Indian states and 4 international locations: Zambia, Nigeria, Turkey represented a mix of resource-rich developing markets and strategic locations for serving broader regions. Turkey, for instance, provided access to European and Middle Eastern markets, while African operations served the continent's extensive mining sector.

This strengthened the core business at a time when defence was beginning to yield results. The synergy between international expansion and defence growth was important. The credibility gained from international operations helped in defence sales, while defence capabilities opened doors in countries looking to develop their own defence industries.

The operational complexity of managing facilities across multiple countries was immense. Each country had different regulations for explosives manufacturing, different safety standards, different labor laws, and different business practices. Solar had to develop systems robust enough to ensure consistency while flexible enough to accommodate local requirements.

Technology transfer capabilities developed for defence proved valuable in international operations. Solar could offer not just products but also technical knowledge, training, and capability building to countries looking to develop their own explosives industries. This positioned Solar as a partner rather than just a supplier, creating deeper, more sustainable relationships.

The financial architecture supporting international expansion was sophisticated. Solar had to manage multiple currencies, navigate transfer pricing regulations, optimize tax structures, and ensure capital efficiency across jurisdictions. The company incorporated two new Overseas Subsidiary Companies, namely Solar Overseas Mauritius Ltd at Mauritius and Solar Overseas Netherlands Cooperatie U.A. at Netherlands, creating holding structures that facilitated international operations while maintaining regulatory compliance.

Risk management for international operations added new dimensions to Solar's already complex risk matrix. Political risk in African countries, currency volatility in emerging markets, and regulatory changes in multiple jurisdictions all needed to be monitored and managed. Solar developed early warning systems, diversified across countries to reduce concentration risk, and maintained strong relationships with local governments and communities.

The human capital strategy for international expansion was carefully planned. Solar deployed experienced Indian managers to establish operations but quickly localized management to ensure cultural fit and regulatory compliance. Training programs exported Solar's safety culture and operational excellence while respecting local practices and knowledge.

Supply chain optimization across international operations created significant value. Raw materials could be sourced globally, taking advantage of price differentials and availability. Manufacturing could be allocated based on capacity, capabilities, and proximity to customers. This operational flexibility provided competitive advantages in pricing and service.

The brand building in international markets required different approaches than in India. In Africa, Solar emphasized its developing market credentials and understanding of local conditions. In more developed markets, it highlighted its technical capabilities and cost advantages. The ability to position the brand differently in different markets while maintaining core values demonstrated marketing sophistication.

Competitive dynamics in international markets differed significantly from India. In Africa, Solar competed with Chinese companies offering low prices and European companies offering advanced technology. Solar's sweet spot was providing European-level quality at prices between Chinese and European competitors, with better service and local presence than either.

The integration of acquired companies required delicate balance. Solar needed to preserve what made these companies successful—local relationships, operational practices, market knowledge—while introducing Solar's safety standards, quality systems, and operational efficiencies. This integration was managed gradually, with clear communication about what would change and what would remain.

Customer relationships in international markets often involved government entities, state-owned mining companies, and large multinationals. Solar had to navigate different procurement processes, payment terms, and service expectations. The experience gained from dealing with Coal India and Indian government entities proved valuable in managing these relationships.

Environmental and social governance (ESG) considerations became increasingly important in international operations. International customers, particularly multinationals, demanded adherence to global ESG standards. Solar had to ensure its international operations met these standards while operating in countries where local regulations might be less stringent.

The innovation ecosystem in international operations provided unexpected benefits. Exposure to different mining conditions, geological formations, and customer requirements drove innovation that benefited Solar's global operations. Solutions developed for specific challenges in Africa found applications in India and vice versa.

Looking at the financial impact, international operations transformed Solar's economics. Exports now biggest chunk of revenue, followed by housing/infrastructure, coal companies, defence changed the company's risk profile, growth trajectory, and valuation multiples. Solar was no longer just an Indian explosives company but a global industrial conglomerate with exposure to multiple growth markets.

The strategic patience demonstrated in international expansion mirrored the approach to defence. Solar didn't rush into markets but took time to understand them, build capabilities, and establish sustainable operations. This patient capital approach, funded by profitable domestic operations, created lasting competitive advantages.

As Solar entered 2024, its international presence provided multiple growth vectors. The African mining boom, infrastructure development in emerging markets, and defence exports all represented significant opportunities. The company that had started as a trader in Nagpur was now positioned to capture value from global megatrends in industrialization and defence modernization.

VII. The Defence Boom & Government Orders (2020-Present)

The period from 2020 onwards represents the culmination of Solar Industries' decade-long defence bet, transforming from speculative investment to spectacular returns. In a mega success for indigenous weapon systems, the Cabinet Committee on Security has cleared the project to buy over Rs 10,000 crore worth of ammunition for the Indian Army's Pinaka multi-barrel rocket launcher systems. This single order validated everything—the patient capital, the technology development, the relationship building, the perseverance through years of minimal returns.

The Defence Ministry is set to sign the Rs 10,200 crore contract for ammunition for the Pinaka multi-barrel rocket launcher weapon system on Thursday with Solar Industries, Nagpur and public sector firm Munitions India Limited (MIL). The scale of this order dwarfed Solar's entire market capitalization from just a decade earlier. For a company that had started with a Rs 60 lakh loan, winning a Rs 10,000 crore defence contract represented an almost incomprehensible transformation.

The Indian Army project to buy the Rs 10,000 crore plus ammunition including the Area Denial Munitions and Pinaka Enhanced Range rockets was cleared by the Cabinet Committee on Security in a meeting held on Wednesday, defence sources told ANI. The project would be divided between the rocket manufacturer Solar Industries of Nagpur and the former Ordnance Factory Board company Munitions India Limited (MIL), they said. The division of the contract between Solar and MIL reflected the government's approach to defence procurement—leveraging private sector efficiency while maintaining public sector participation.

Army Chief Gen Upendra Dwivedi in his annual press conference on January 13 had stated that the contract for Pinaka weapon systems munitions including the Rs 5,700 crore for high-explosive ammunition and Rs 4,500 crore area denial munitions were expected to be cleared soon by the government. The breakdown revealed the sophistication of Solar's product portfolio—not just basic ammunition but specialized munitions including area denial systems that required advanced technology and manufacturing capabilities.

The Pinaka system itself represented the pinnacle of India's indigenous defence capabilities. Renowned for its precision strike capability at high altitudes, Pinaka stands among the most advanced artillery rocket systems globally. For Solar to be manufacturing propellants and munitions for such a system positioned it at the forefront of India's defence technology ecosystem.

The Pinaka has already been a major success story in the export sector as it has been bought by Armenia while many European countries including France are showing interest in it. This export potential transformed the economics of Solar's defence business. It wasn't just about serving domestic requirements but potentially accessing global defence markets worth hundreds of billions of dollars.

The geopolitical context amplified the significance of these contracts. The rockets have an impressive 45 km range and are particularly strategic for borders with China and Pakistan. The border tensions with China since 2020 and the ongoing challenges with Pakistan created urgency around indigenous defence capabilities. Solar wasn't just a supplier; it was a strategic asset in national security.

The deployment of Pinaka rocket systems is anticipated to enhance the Indian Army's artillery strength, particularly in high-altitude regions along the northern borders. The specific mention of high-altitude regions highlighted the technical challenges Solar had overcome. Manufacturing propellants that performed reliably at extreme altitudes and temperatures required sophisticated chemistry and extensive testing.

The financial markets responded enthusiastically to these developments. Following the announcement, at 10:00 AM IST, the share price of Solar Industries was at ₹10,110.00 on the NSE, up 5.66% from its previous close. This immediate market reaction reflected investor recognition that Solar had crossed an inflection point from potential to performance in defence.

Beyond the Pinaka deal, Solar's defence portfolio continued expanding. In June 2025, Rs 158 crore MoD order through Solar Defence & Aerospace Ltd demonstrated the steady flow of smaller but significant contracts. These weren't one-off wins but evidence of Solar becoming embedded in India's defence procurement ecosystem.

The technology roadmap for Pinaka showed even greater potential. The DRDO is already in the advanced stages of making a 120 km strike version of the Pinaka rockets and is expected to carry out its first test in the next financial year. Solar's involvement in these advanced versions would require continuous technology upgradation and investment, but also promised sustained revenue growth.

The Make in India and Atmanirbhar Bharat initiatives provided powerful tailwinds. The government's commitment to reducing defence imports from 60% to 30% by 2025 created a massive addressable market for domestic manufacturers. Solar, having invested early and built capabilities patiently, was perfectly positioned to capture this opportunity.

The organizational transformation to support defence growth was remarkable. From a handful of people working on defence projects in 2010, Solar now had hundreds of specialized personnel. Defence facilities that had remained underutilized for years were now running at full capacity with order backlogs extending years into the future.

The technology capabilities built for Pinaka had spillover benefits. The expertise in composite propellants could be applied to other missile systems. The quality systems developed for defence manufacturing improved commercial operations. The relationships with DRDO opened doors to other technology transfers and collaborative developments.

International interest in Indian defence products created export opportunities. With nations like France and Armenia already showing interest, the system is poised to become a crucial component in the international defense sector. For Solar, this meant potential access to NATO markets, Middle Eastern countries modernizing their militaries, and Southeast Asian nations seeking alternatives to Chinese systems.

The competitive landscape in defence remained challenging but Solar had established strong moats. The decade of co-development with DRDO created technical capabilities that couldn't be quickly replicated. The security clearances, certifications, and proven track record created high barriers to entry. Most importantly, the trust earned through successful execution of critical projects gave Solar preferential access to new opportunities.

Risk management in defence operations required extreme diligence. A single quality failure in defence products could result in loss of lives, diplomatic incidents, and permanent exclusion from defence contracts. Solar implemented multiple quality gates, redundant testing protocols, and stringent supply chain controls to ensure zero defects.

The financial impact of defence success was transformative. Defence expected to hit 30-35% of revenue in 4-5 years, rest split between international and domestic meant that a business that contributed nothing a decade ago would soon be Solar's largest segment. The margin profile of defence products, particularly sophisticated munitions, was superior to commercial explosives, driving overall profitability higher.

The human capital in defence had evolved significantly. Solar now employed former military officers who understood operational requirements, DRDO scientists who brought technical expertise, and international defence industry professionals who understood global markets. This talent density in defence was unmatched among Indian private sector companies.

The ecosystem relationships built around defence extended beyond customer-supplier dynamics. Solar collaborated with academic institutions on research, partnered with other defence companies on complex systems, and engaged with startups developing complementary technologies. It had become a node in India's emerging defence innovation network.

Supply chain localization for defence became a strategic priority. Unlike commercial explosives where imported raw materials might be acceptable, defence products required indigenous supply chains for strategic autonomy. Solar invested in developing local suppliers, sometimes funding their capability development, to ensure supply security.

The success in ammunition led to opportunities in more complex systems. Products: Composite propellants (Pinaka, Akash, Brahmos), rockets & warheads, ammunition filling & fuzes represented increasing levels of sophistication. Each successful project enhanced Solar's credentials for the next, creating a virtuous cycle of capability building and order wins.

The cultural impact within Solar of defence success was profound. Employees took pride in contributing to national security. The company that had started by helping mine coal was now protecting national borders. This sense of purpose enhanced employee engagement and helped attract top talent.

Looking ahead, the defence opportunity appeared even larger. Europe's $800 billion defence spending as opportunity, combined with increasing global tensions, suggested a multi-decade growth runway. Solar's early investment, patient capital, and successful execution had positioned it to be one of the primary beneficiaries of the global defence spending surge.

The transformation from 2020 onwards validated Satyanarayan Nuwal's vision and Manish Nuwal's execution. The father who had slept on railway platforms had built capabilities that protected the nation. The son who joined when the company was small had led its transformation into a defence powerhouse. Together, they had created one of India's most remarkable business success stories—from railway stations to rockets, from Rs 60 lakhs to Rs 10,000 crores, from Nagpur to the world.

VIII. Business Model & Competitive Moats

The business model that Solar Industries has constructed over nearly three decades represents a masterwork in building competitive advantages layer by layer, creating moats so deep and wide that potential competitors face nearly insurmountable barriers to entry. At its core, Solar operates in industries where mistakes aren't just costly—they can be catastrophic, creating natural barriers that Solar has reinforced through operational excellence, regulatory compliance, and relationship capital.

The regulatory moat stands as perhaps the most formidable barrier. Manufacturing, storing, and transporting explosives requires licenses at multiple levels—local, state, and national. Each license demands extensive documentation, safety audits, and often personal guarantees from company directors. The process of obtaining these licenses can take years, requires significant capital investment in safety infrastructure, and demands spotless safety records. A single serious accident can result in permanent revocation of licenses, effectively ending a company's ability to operate. Solar's three-decade safety record and comprehensive licensing across multiple states and countries represents an asset that cannot be quickly replicated regardless of available capital.

The relationship moat, particularly with government entities, took decades to build. Solar's relationship with Coal India, cultivated since the 1970s when Nuwal was still a trader, provides preferential access to India's largest consumer of industrial explosives. These relationships operate at multiple levels—from procurement officers who trust Solar's quality to senior executives who value Solar's reliability to field engineers who prefer Solar's technical support. In government procurement, where vendor changes require extensive justification and re-qualification processes, incumbent advantages are substantial. New entrants face the chicken-and-egg problem: they need references to win government contracts, but they need government contracts to build references.

The technology moat in defence is particularly sophisticated. Solar's co-development work with DRDO, technology transfers, and indigenous development capabilities create unique know-how that exists nowhere else in India's private sector. Manufacturing HMX, developing composite propellants for specific missile systems, and producing specialized munitions requires not just technical knowledge but tacit understanding gained through years of trial and error. This knowledge—encoded in processes, embedded in equipment configurations, and embodied in experienced personnel—cannot be transferred through documentation alone. Even if competitors obtained similar technology transfers, they would face a multi-year learning curve that Solar has already climbed.

The manufacturing moat encompasses both scale and scope. Solar became the world's largest cartridge manufacturing facility at single location, achieving economies of scale that reduce unit costs below what smaller competitors can achieve. But beyond scale, Solar's scope—manufacturing everything from basic mining explosives to sophisticated defence products—creates synergies in procurement, technology development, and customer relationships. Raw materials purchased for commercial explosives can sometimes be used for defence products. Quality systems developed for defence applications improve commercial operations. Customers value dealing with a single supplier for multiple requirements.

The vertical integration moat provides control and flexibility that competitors relying on suppliers cannot match. Solar manufactures its own detonators, develops its own formulations, and in many cases, processes its own raw materials. This integration provides multiple advantages: quality control at every stage, ability to customize products without depending on suppliers, protection of proprietary formulations, and capture of margins across the value chain. During supply disruptions, as seen during COVID-19, vertically integrated operations provide resilience that customers value highly.

The geographic moat through international operations provides natural hedging and market access. Solar's presence in Africa, Turkey, and other markets provides diversification that purely domestic players lack. But more importantly, these operations provide intelligence about global trends, exposure to different mining conditions that drive innovation, and credibility with international customers. When French defence companies evaluate Solar as a potential supplier, its international operations demonstrate capabilities beyond what a purely domestic player could claim.

The capital allocation moat reflects decades of disciplined financial management. Solar's ability to fund long-term investments like defence from cash flows of profitable commercial operations demonstrates financial strength that venture-funded or highly leveraged competitors cannot match. This patient capital approach—investing in capabilities years before they generate returns—creates temporal barriers. Even if competitors started investing today in similar capabilities, they would be years behind Solar's learning curve and relationship development.

The human capital moat has been carefully constructed through both recruitment and retention. Solar employs some of India's most experienced explosives engineers, former DRDO scientists, retired military officers, and international defence industry professionals. This talent density creates a virtuous cycle: top talent attracts more top talent, complex projects become possible which attract more complex projects, and reputation enhances recruitment which enhances reputation. The specialized nature of explosives and defence manufacturing means the talent pool is limited, and Solar has captured a disproportionate share.

The safety and quality moat transcends mere compliance. Solar's safety record over three decades of handling hazardous materials creates trust that new entrants cannot quickly earn. In industries where customers' own reputations and legal liabilities depend on supplier safety, this trust translates directly into competitive advantage. Solar's quality certifications, accumulated over years and maintained through continuous investment, open doors that remain closed to uncertified competitors.

The innovation moat, while less visible, provides sustainable differentiation. Solar's R&D investments, while modest by pharmaceutical or technology standards, are significant for the explosives industry. More importantly, Solar's innovation is customer-driven and application-focused rather than purely technical. Understanding that a particular mine needs explosives that perform in wet conditions, or that a specific missile system requires propellants with precise burn rates, and developing solutions for these specific needs creates switching costs for customers.

The network effects moat operates subtly but powerfully. As Solar serves more customers, it learns more about applications, which helps it serve other customers better. As it manufactures more products, it achieves better raw material procurement terms, which improves competitiveness across all products. As it operates in more geographies, it becomes a more attractive partner for global companies. These network effects are weaker than in pure technology businesses but still meaningful in creating competitive advantages.

The reputation moat in defence and government circles took decades to build and would take a single failure to destroy. Solar's successful execution of critical defence projects, its reliability in supplying strategic materials, and its adherence to confidentiality requirements have created a reputation that opens doors to new opportunities. In defence procurement, where national security depends on supplier reliability, reputation matters more than price.

The customer intimacy moat reflects Solar's evolution from trader to manufacturer to solution provider. Solar doesn't just supply explosives; it provides blasting solutions. Its engineers work with customers to optimize blast patterns, reduce costs, improve safety, and solve specific challenges. This consultative approach creates relationships that transcend procurement transactions. Customers don't just buy from Solar; they depend on Solar's expertise.

The execution moat—the ability to consistently deliver on commitments—seems simple but proves difficult to replicate. Solar's ability to deliver explosives on schedule to remote mining sites, to meet stringent defence specifications consistently, and to maintain supply during disruptions creates reliability that customers value highly. This execution excellence requires synchronized operations across procurement, manufacturing, logistics, and service—coordination that takes years to develop.

The ecosystem moat reflects Solar's position at the center of multiple stakeholder networks. Relationships with DRDO for technology, with academic institutions for research, with suppliers for raw materials, with logistics providers for transportation, with regulatory bodies for compliance, and with customers for requirements create an ecosystem where Solar is deeply embedded. Displacing Solar would require competitors to replicate not just Solar's capabilities but its entire ecosystem position.

These moats reinforce each other, creating competitive advantages that compound over time. Regulatory compliance enhances reputation which attracts talent which drives innovation which deepens customer relationships which generates cash flows which fund investments which build capabilities which strengthen competitive position. This virtuous cycle, set in motion decades ago, now spins with momentum that competitors find almost impossible to match.

The result is a business model that generates superior returns on capital while maintaining strong competitive positions across multiple markets. Solar's ability to earn 30%+ returns on equity in industries that might seem commoditized demonstrates the power of these accumulated advantages. For competitors, matching any single element of Solar's business model might be possible; matching all elements simultaneously while Solar continues to advance proves nearly impossible.

IX. Financial Performance & Market Story

The financial transformation of Solar Industries from a Rs 60 lakh loan in 1995 to a company with market capitalization exceeding Rs 135,000 crore represents one of the most spectacular wealth creation stories in Indian corporate history. The numbers tell a story of consistent execution, strategic pivots paying off, and the power of patient capital deployment.

Solar Industries on Wednesday, February 5, reported a 54.85% year-on-year (YoY) increase in its consolidated net profit at ₹314.87 crore for the quarter ended December 31, 2024 (Q3 FY25). Revenue from operations came in at ₹1,973.08 crore, up 38% against ₹1,429.14 crore logged in the December 2023 quarter. These Q3 FY25 results demonstrated the culmination of multiple growth drivers firing simultaneously—defence orders materializing, international operations expanding, and core explosives business maintaining momentum.

During the third quarter of the fiscal year 2025, Solar Industries India Ltd reported a total income of ₹1982.62 crores. This represents a quarter-over-quarter increase of 13.5% from ₹1746.28 crores in the previous quarter, Q2FY25, and a year-over-year increase of 37.7% from ₹1440.05 crores in Q3FY24. The revenue growth indicates strong performance relative to both the previous quarter and the same quarter last year.

Ebitda was highest-ever in Solar Industries' history, growing 46 per cent on year to Rs 536 crore. Ebitda margin expanded by 148 basis points to 27.17 per cent and Net profit margin 158bps to 17.11 per cent in Q3FY25. The margin expansion while scaling revenues demonstrated operational leverage and pricing power—hallmarks of a business with strong competitive moats.

During the quarter, the explosives' company registered the highest-ever Defence revenue of over Rs 400 crore. This defence revenue represented approximately 20% of quarterly revenues, validating the decade-long investment in defence capabilities. From contributing virtually nothing in 2020 to Rs 400 crore quarterly by 2024, defence had become a major growth engine.

Our international business has delivered exceptional third-quarter performance, growing 21 per cent year-on-year. Its revenue was best-ever at Rs 758 crore. International operations contributing Rs 758 crore quarterly meant annualized international revenues approaching Rs 3,000 crore—larger than the entire company's revenue just a few years earlier.

Solar Industries · Mkt Cap: 1,34,794 Crore (up 44.9% in 1 year) · Revenue: 8,010 Cr · Profit: 1,340 Cr · Stock is trading at 30.7 times its book value · Promoter Holding: 73.2% The market capitalization of Rs 134,794 crore valued Solar at approximately 17 times revenues and 100 times profits—premium valuations typically reserved for technology companies rather than industrial manufacturers.

The stock performance reflected investor recognition of Solar's transformation. The stock P/E 108, ROE 32.6%, ROCE 38.1% metrics demonstrated both market enthusiasm and operational excellence. A P/E ratio of 108 might seem excessive for a traditional explosives company, but investors were pricing in the defence opportunity, international expansion, and Solar's proven execution capabilities.

The market value for the solar industries grew 1,700% in a decade, from 1,765 crores in 2012 to more than Rs 35,000 crore by November 2022. This 17-fold increase in market value over a decade represented a compound annual growth rate exceeding 30%—wealth creation that outpaced most equity indices and peer companies.

Its order book was at record high of over Rs 7,100 crore. An order book of Rs 7,100 crore provided visibility for nearly a year of revenues, unusual for an industrial company and reflecting the long-term nature of defence contracts. This order book de-risked the business and provided confidence for continued capital investment.

The profitability metrics revealed the quality of Solar's business model. ROE of 32.6% meant Solar generated Rs 32.60 in profits for every Rs 100 of shareholder equity—exceptional returns for a capital-intensive manufacturing business. ROCE of 38.1% demonstrated efficient capital deployment across the entire business, not just equity.

The working capital management remained disciplined despite rapid growth. Solar's ability to grow revenues 38% year-over-year while maintaining or improving working capital cycles demonstrated operational excellence. In the explosives business, where customers often included government entities with slow payment cycles, this was particularly impressive.

The capital structure evolution reflected growing confidence and capability. From desperately seeking Rs 60 lakh in 1995 to generating over Rs 1,300 crore in annual profits, Solar had become entirely self-financing. The company maintained modest debt levels, using leverage strategically rather than out of necessity.

The segment-wise performance revealed portfolio transformation. Defence contributing 20% of revenues and growing rapidly, international operations at 40% and expanding, domestic commercial explosives maintaining steady growth—this diversification reduced risk while maintaining growth momentum. No single customer, geography, or product line could derail Solar's growth story.