Snowman Logistics: Building India's Cold Chain from Frozen Foundations

I. Introduction & Episode Roadmap

Picture this: In the sweltering heat of a Mumbai summer, a truck carrying ice cream from a factory in Pune to retail outlets across the city breaks down. Within hours, thousands of rupees worth of product melts into an unusable puddle. Multiply this scene across India's vast geography—from the frozen seafood of Kerala's coasts to the dairy products of Punjab's farms, from pharmaceutical vaccines requiring precise temperature control to the french fries destined for McDonald's kitchens—and you begin to understand the staggering challenge.

This wasn't a logistics problem. It was a trillion-dollar infrastructure gap.

India is the world's largest producer of milk, second largest producer of fruits and vegetables and has a substantial production of marine, meat and poultry products. Yet for decades, nearly 40% of perishable produce rotted before reaching consumers because the country lacked a functioning cold chain. The economic waste was astronomical. The human cost—in terms of food security and public health—was incalculable.

Enter Snowman Logistics, a company with perhaps the most delightfully incongruous name for an Indian enterprise. How did a company that commenced its business as a trader of frozen marine products in Kochi, Kerala in 1993 transform itself into India's largest integrated cold-chain logistics provider, operating 44 warehouses on over 3 million+ sq ft across 21 cities?

This is the story of Snowman Logistics—a tale that encompasses Japanese conglomerates betting on Indian infrastructure, a euphoric IPO during the Modi bull market, a dramatic acquisition attempt by the Adani Group that fell apart during COVID-19, and an ongoing transformation into what the company calls "5PL" (Fifth-Party Logistics). It's about building invisible infrastructure in a country where organized cold storage barely existed, competing in a market that's currently dominated by the unorganised segment, and doing so profitably enough to survive three decades.

The stakes? India's cold chain market reached INR 2,287.5 Billion in 2024 and is expected to reach INR 6,061.7 Billion by 2033, exhibiting a growth rate of 10.86%. This is one of the defining infrastructure plays in India's consumption story.

Here's what we'll unpack: Snowman's unlikely origins in frozen seafood trading, the strategic pivot that transformed it from trader to logistics platform, the role foreign investors played in professionalizing the business, the spectacular 2014 IPO that saw 59.75x oversubscription, the expansion to over 100,000 pallets of capacity, the Adani deal that almost happened, the shift to an asset-light model, and the company's pioneering move into 5PL services.

This is a story about patient capital, execution in fragmented markets, and the unsexy but essential work of building cold rooms and deploying refrigerated trucks. It's about why infrastructure investing is so difficult—and occasionally, so rewarding.

II. Context: India's Cold Chain Challenge & Opportunity (1990s–2000s)

To understand Snowman's significance, you must first understand the magnitude of India's cold chain problem.

In the early 1990s, as India embarked on economic liberalization, the country's food supply chain was essentially medieval. Farmers harvested produce, loaded it onto non-refrigerated trucks, and hoped it would reach wholesale markets before spoiling. Dairy cooperatives like Amul had built some cold storage capacity, but these were isolated efforts. For most products—seafood, meat, processed foods, pharmaceuticals—the cold chain was fragmented, unreliable, or nonexistent.

The numbers were staggering. Post-harvest losses in fruits and vegetables exceeded 30%. Seafood exporters lost millions because they couldn't maintain temperature integrity from boat to port. International food brands looking to enter India faced a fundamental question: How do you distribute ice cream or frozen food when there's no reliable way to keep it frozen?

But beneath this dysfunction lay extraordinary opportunity. Rising disposable incomes, increasing middle class population, growing organised food retail, increased production and consumption of perishable food products, and rapid urbanisation and industrialisation were creating demand that the existing infrastructure simply couldn't serve.

Consider the transformation underway: In 1991, organized retail barely existed in India. Supermarkets were rare. International quick-service restaurant chains were just beginning to explore the market—McDonald's wouldn't open its first Indian outlet until 1996, Pizza Hut arrived in 1996, and Domino's in 1996. These QSR chains required something Indian infrastructure couldn't provide: absolute temperature control from supplier to store.

The market structure was equally challenging. The Indian cold chain market can be segregated into organised sector and unorganised sector, with the unorganised segment exhibiting clear dominance. Small, local cold storage operators dominated—often single-warehouse operations focused on potatoes (India's most common cold-stored product). They lacked the capital, technology, or ambition to build integrated national networks.

This fragmentation created both a problem and an opportunity. The problem: No single player had the scale to serve national brands. The opportunity: The first mover to build a professional, pan-India cold chain network would capture enormous value.

The economics were daunting. Cold chain infrastructure is brutally capital-intensive. Each temperature-controlled warehouse requires specialized insulation, industrial refrigeration equipment, backup power systems, and precision monitoring. Refrigerated trucks—"reefers" in industry parlance—cost multiples of standard vehicles. The payback period stretches years. Most Indian entrepreneurs, accustomed to faster-turning businesses, avoided the sector.

Yet the fundamentals were compelling. Once built, cold storage assets generated recurring revenue from long-term customer contracts. Switching costs were high—no brand manager wanted to risk product spoilage by changing cold chain providers. Network effects would benefit the first national player: A company with warehouses in Mumbai, Delhi, Bangalore, and Chennai could offer something competitors couldn't—end-to-end temperature-controlled logistics.

The policy environment was shifting too. Economic liberalization meant FDI was flowing into retail and FMCG. International food companies were entering India, bringing global standards and deep pockets. They needed reliable cold chain partners.

This was the landscape in the 1990s: Massive need, negligible supply, punishing capital requirements, and the promise that whoever solved this first would build an extraordinary moat. It was classic infrastructure investing—patient capital required, but potential for decades of compounding returns.

Into this opportunity stepped an unlikely player: a frozen seafood trader in Kerala that would eventually become Snowman Logistics, transforming from commodity trader to essential infrastructure provider in one of the world's most challenging operating environments.

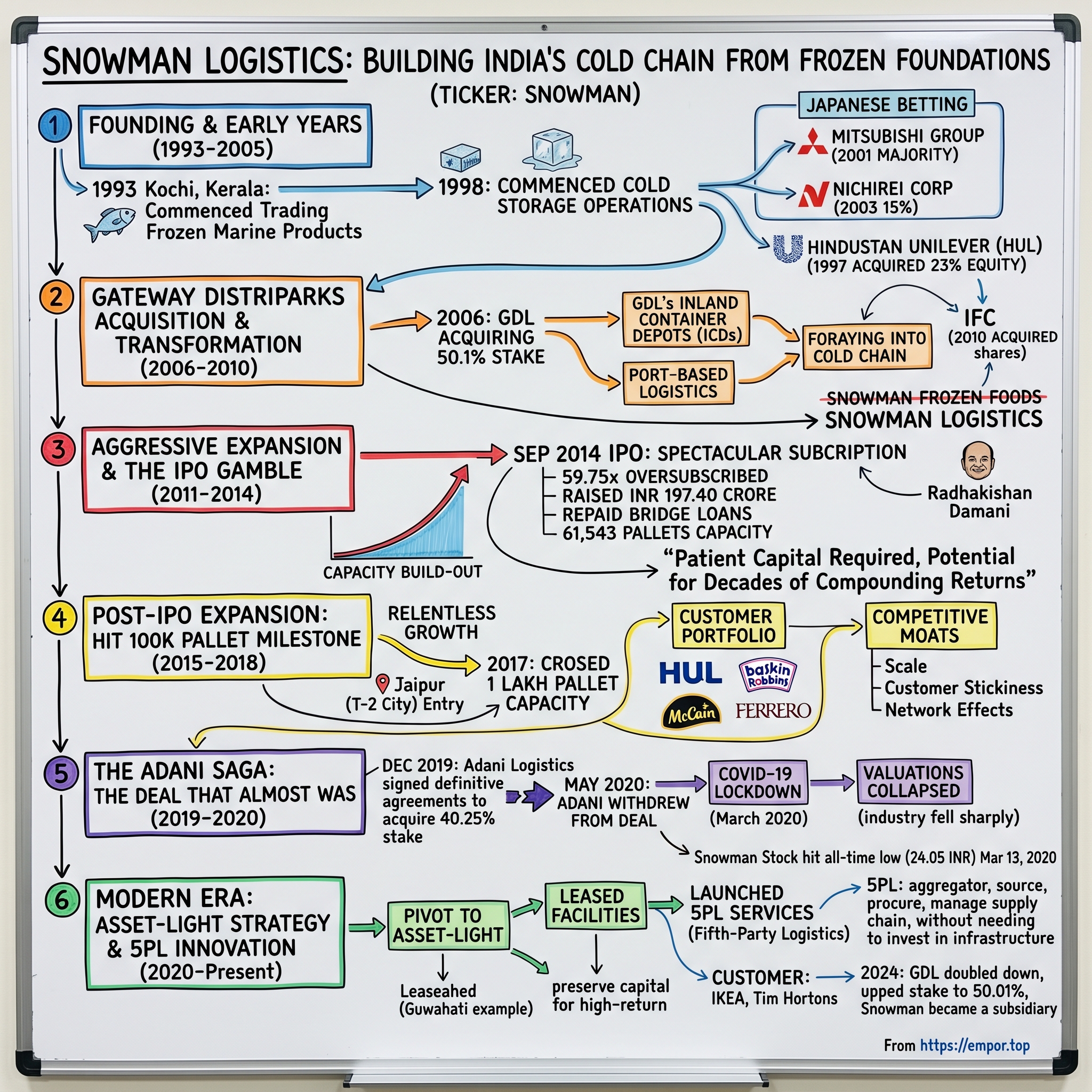

III. Founding & Early Years: From Seafood to Cold Storage (1993–2005)

Snowman Logistics Limited was incorporated in March, 1993 in Kochi, Kerala. The original business was straightforward: trading frozen marine products. Kerala, with its extensive coastline and thriving fishing industry, was a natural location. The company bought frozen seafood from processors and sold to exporters and domestic buyers.

But something interesting happened in those early years. While trading frozen seafood, the company's founders confronted the fundamental infrastructure problem firsthand: India lacked adequate cold storage. Snowman commenced its business as a trader of frozen marine products and in Fiscal 1998, the company commenced cold storage operations at 4 (four) locations.

This pivot—from trading to infrastructure—was the first critical decision in Snowman's evolution. Rather than remain a commodity trader (low margins, limited differentiation), the company began building cold storage warehouses. The logic was simple: Control the infrastructure, control the value chain.

The early validation came quickly—and from unexpected sources. In a move that would prove prescient, in 1997, Hindustan Unilever Limited (then, Brooke Bond India Limited) acquired 23% of the company's equity share capital. This was extraordinary. HUL, India's premier FMCG company with legendary operational standards, was betting on a small Kerala-based cold storage startup. The investment brought more than capital—it brought credibility, operational expertise, and a marquee customer.

Then came the Japanese. In 2001, Mitsubishi Group acquired majority stake; in 2003, Nichirei Corporation acquired 15%. This foreign institutional interest was remarkable for a sector most Indian investors ignored. Both Mitsubishi and Nichirei understood cold chain logistics intimately—Nichirei was (and remains) one of Japan's largest frozen food and cold storage companies. They saw in India what few others did: A massive market at the cusp of transformation.

What did the Japanese bring beyond capital? Operational discipline, technology transfer, and quality standards. Gateway operated its cold chain and logistics subsidiary Snowman Frozen Foods, now known as SLL, in partnership with Mitsubishi Logistics Corporation, Mitsubishi Corporation, Nichirei Logistics group and the International Finance Corporation, who collectively owned 26% stake. These weren't passive financial investors. They brought global best practices to an Indian infrastructure company.

During this period, Snowman was methodically building capacity and refining its model. The business wasn't glamorous—operating cold storage warehouses, maintaining refrigeration equipment, managing inventory for customers. But it was essential. And crucially, it was difficult to replicate. Each warehouse required significant capital, regulatory approvals, and years to reach optimal utilization.

The early customer wins were telling. The Bengaluru-based Snowman provided temperature-controlled storage services, catering to customers such as HUL, Baskin Robbins, Pizza Hut, Mother Dairy and ITC, among others. These weren't small local businesses—these were national and international brands with exacting standards. Landing them as customers validated Snowman's operational capability.

The company's positioning was becoming clear: Not the cheapest option, but the most reliable. In cold chain logistics, reliability is everything. A temperature deviation can destroy millions of rupees worth of inventory. A power outage without adequate backup can spoil an entire warehouse. Snowman was building a reputation for "zero downtime"—a claim that would become central to its competitive advantage.

By 2005, Snowman had established itself as a credible, professionally-managed cold storage operator with backing from Japanese conglomerates and HUL. It had built multiple warehouses, developed operational expertise, and secured blue-chip customers. But it remained relatively small—a regional player with ambitions but limited capital to scale nationally.

The company needed something more to truly transform: A strategic parent with deep pockets, logistics expertise, and the ambition to build national infrastructure. That parent was about to arrive, and the acquisition would fundamentally alter Snowman's trajectory.

IV. The Gateway Distriparks Acquisition & Transformation (2006–2010)

The year 2006 marked Snowman's first major inflection point.

Gateway Distriparks Ltd (GDL), a port-based container logistics company, announced the acquisition of a majority stake of 50.1 per cent in Snowman Frozen Foods Ltd for a consideration of Rs 48.12 crore. To understand why this mattered, you need to understand Gateway Distriparks.

Gateway Distriparks Limited is an Indian logistics company based in Mumbai with three business verticals: container freight stations (CFS), inland container depots (ICD) with rail movement and cold chain storage and logistics. Founded in 1994, GDL had established itself as one of India's leading container logistics companies, handling import-export cargo at major ports. It was profitable, well-managed, and hungry for growth beyond traditional container freight.

The strategic logic was elegant. GDL was foraying into the cold chain logistics segment, expecting a surge in domestic demand for movement of frozen and chilled food in the wake of the boom in the retail sector. Container logistics at ports was a mature business; cold chain was the future. GDL saw adjacencies: Both required handling cargo with precision, both needed warehouse infrastructure, both served FMCG and food companies.

But GDL did something smart. GDL entered into a share subscription and shareholders agreement with Snowman and its present shareholders — Mitsubishi Corporation, Mitsubishi Logistics Corporation and Nichirei Logistics Group of Japan. The three shareholders would continue to hold a total of 48.69 per cent shareholding in Snowman. Rather than buy out the Japanese completely, GDL structured a partnership. The Japanese expertise would remain, but GDL would control operations and provide capital for expansion.

The synergies ran deeper than expected. GDL set up cold storage facilities at its network of Container Freight Stations, which were leased out to Snowman. This was brilliant capital allocation—GDL built warehouses at its existing CFS locations, reducing land acquisition costs and leveraging existing infrastructure. Snowman operated them, utilizing GDL's physical network while focusing on cold chain operations.

The scale Snowman achieved was impressive. Snowman, which moved about 9,000 tonnes of frozen and chilled products every month within India, bundled the entire spectrum of the supply chain from procurement to storage and right down to retail distribution. This integrated model—handling procurement, storage, transportation, and last-mile delivery—was exactly what national FMCG and QSR brands needed.

Then came another validation in 2010. IFC acquired 20,570,000 equity shares of the Company. The International Finance Corporation, the World Bank's private sector investment arm, was known for backing companies with development impact and strong fundamentals. IFC's entry brought not just capital but signaled to the market that Snowman had investment-grade governance and growth potential.

The shareholder base by 2010 was remarkable: Gateway Distriparks (controlling shareholder), Mitsubishi Group, Nichirei, and IFC. Each brought something different—GDL brought operational logistics expertise and capital, the Japanese brought cold chain technology and quality standards, IFC brought governance benchmarks and global credibility.

The strategic repositioning became official in March 2011. On March 17, 2011, the name of the company was changed to Snowman Logistics Limited pursuant to a new certificate of incorporation. The change in name was to better capture the nature of the business of the company. "Snowman Frozen Foods" suggested a trading business; "Snowman Logistics" signaled infrastructure and services. The rename reflected the company's transformation.

By 2011, Snowman had evolved from a regional cold storage operator into a serious logistics platform with national ambitions, backed by a diversified set of institutional investors who understood the opportunity. Gateway's deep pockets, the Japanese's operational excellence, and IFC's governance standards created a compelling foundation.

But to truly scale nationally, Snowman would need something more: Public market capital. The company began preparing for what would become one of 2014's most dramatic IPO stories, setting the stage for the next major transformation.

V. Aggressive Expansion & The IPO Gamble (2011–2014)

Between 2011 and 2014, Snowman executed an aggressive capacity buildout strategy, preparing for public market fundraising. The goal was audacious: Establish Snowman as India's undisputed cold chain leader before competitors could mobilize.

The expansion was capital-intensive. Snowman clocked revenue from operations of Rs 153 crore in FY14, up 37% YoY, and earned EBITDA of Rs 40 crore, up 54% YoY, leading to an EBITDA margin of 25.9%, on back of rising warehousing capacity. Revenue was growing rapidly, margins were expanding—but the debt burden was becoming concerning.

By March 2014, Snowman had 23 temperature controlled warehouses across 14 locations in India with a warehousing capacity of 61,543 pallets and operating 370 reefer vehicles (307 leased, 63 owned). The geographic footprint was impressive: Serampore near Kolkata, Taloja near Mumbai, Palwal near Delhi, Mevalurkuppam near Chennai, Bengaluru—all major consumption centers.

But here's the tension: FY14 profit before tax declined to Rs 13.7 crore, from Rs 14.4 crore in FY13, as most of the expansion came in through expensive bridge loans. Interest burden ballooned from Rs 2.4 crore in FY13 to Rs 11.2 crore in FY14! Snowman was borrowing aggressively to build capacity before the IPO, expecting to refinance expensive short-term debt with equity capital. This was a calculated risk: Build capacity to demonstrate scale, then raise equity to clean up the balance sheet.

The company had raised debt as of 31st March 2014 that stood at Rs 130 crore, of which Rs 40 crore was bridge loan. This bridge loan rose to Rs 80 crore as of 31st July 2014, which would be repaid entirely from proceeds of the IPO, thus easing interest expense from H2FY15 onwards.

This aggressive pre-IPO expansion explains the IPO structure. The public issue was for 42,000,000 equity shares of face value of Rs 10 each at a price of Rs 47 per equity share, aggregating Rs 197.40 crores. This was entirely a fresh issue—new money for the company, not promoter selling. The capital would repay bridge loans and fund further expansion.

The validation came from CRISIL. The issue had been graded by CRISIL as 4 out of 5, indicating that the issue was fundamentally above average relative to other listed equity securities. A 4/5 CRISIL grade was strong—it indicated solid fundamentals despite the high leverage.

The IPO opened on Aug 26, 2014 and closed on Aug 28, 2014, priced at Rs 44-47 per share. The equity shares were proposed to be listed on the Bombay Stock Exchange (BSE) and National Stock Exchange (NSE).

And then something remarkable happened.

The IPO of Snowman Logistics was subscribed 59.75 times with total bids for 194.49 crore shares, compared with 4.20 crore shares on offer. The issue opened on 26 August 2014 and closed 28 August 2014. Let that sink in: Nearly 60 times oversubscription. The demand wasn't just from retail investors hoping for listing gains. The qualified institutional buyers (QIBs) portion was subscribed 16.98 times. Non Institutional Investors portion was subscribed 221.79 times. Retail Individual Investors (RIIs) portion was subscribed 41.26 times.

Why the frenzy? Multiple factors converged. This was September 2014—Narendra Modi had swept to power four months earlier on a pro-business platform, foreign portfolio investors were flooding Indian markets, and investors were hunting for plays on India's infrastructure and consumption story. A cold chain logistics company backed by Japanese conglomerates and IFC, serving HUL and Baskin Robbins, looked like the perfect structural growth bet.

The listing day performance was euphoric. Shares of Snowman Logistics listed on the stock exchanges on 12 September 2014 and settled at Rs 78.75 on BSE, a premium of 67.55% over the IPO price of Rs 47. The stock debuted at Rs 75, a premium of 59.57% to the IPO price.

Smart money was buying. Reliance Mutual Fund Tax Saver (ELSS) fund bought 16 lakh shares at Rs 79.80 per share and Reliance Mutual Fund bought 20 lakh shares at Rs 79.04 per share. Derive Investments, an investment firm run by independent investor Radhakishan Damani, also bought 23.70 lakh shares at Rs 78.90 a piece. Radhakishan Damani—the billionaire founder of D-Mart and one of India's most astute value investors—was accumulating Snowman on listing day. That sent a powerful signal.

But the euphoria masked fundamental tensions. At Rs 47, shares were being issued at PE multiple of 20-21 times expected current year earnings. Norwest Partners, about a year back in July 2013, had picked up ~14% stake at Rs 35 per share. Hence, asking price was up by 34% (at Rs 47 per share). However, Norwest entered the company at PE multiple of 21 times on historic basis (FY13), while the IPO price was 21 times based on current year expected earnings (FY15).

The valuation wasn't cheap—investors were paying for growth and market leadership. The bet was that Snowman would use IPO proceeds to expand capacity, improve utilization, and scale into profitability. The stock was up 101% from IPO price by September 19, 2014, reaching its all-time high of 134.65 INR on Nov 18, 2014.

The IPO had succeeded spectacularly. Snowman raised capital, repaid expensive debt, and had cash to continue expanding. The public market validation was complete. Now came the hard part: Delivering on the growth promise in a brutally competitive, capital-intensive business.

The post-IPO years would test whether Snowman could maintain its first-mover advantage and scale profitably—or whether competitors would erode margins and turn cold storage into a commoditized, low-return business. The answer would determine whether that 60x oversubscribed IPO was visionary or frothy.

VI. Post-IPO Expansion: Hitting 100K Pallet Milestone (2015–2018)

With IPO capital in hand and expensive bridge loans repaid, Snowman accelerated capacity expansion. The strategy was clear: Establish a national network so comprehensive that no competitor could match it, locking in customers and building economies of scale.

In 2015, warehousing capacities were added at Mumbai, Chennai, Bhubaneswar, Pune, Surat and Visakhapatnam, taking the total installed capacity from 61,700 pallets at the start of the year to 85,500 pallets. In transportation division, the fleet size increased from 370 to 501 trucks during the year 2015. This was ambitious—adding nearly 24,000 pallets of capacity (39% growth) in a single year while expanding the reefer fleet by 35%. Each new city required identifying real estate, constructing temperature-controlled warehouses with specialized equipment, hiring staff, and signing customers.

The expansion continued relentlessly. In 2016, warehousing capacities were added at Mumbai, Bangalore and Jaipur taking the total installed capacity from 85,500 pallets at the start of the year to 98,500 pallets. Jaipur was strategic—a tier-2 city but a growing consumption center. Snowman was moving beyond metros into emerging markets.

Then in 2017 came a symbolic milestone. An additional capacity of 5,100 pallets was added at Kochi during FY17, taking the total installed capacity to 103,600 pallets. The Company crossed 1 lakh pallet capacity with the commencement of operations at the Cochin Warehouse in 2017.

One lakh pallets—100,000 storage positions across India. This wasn't just numerical significance. It represented network effects kicking in. A national QSR chain or FMCG company could now work with a single partner—Snowman—for cold storage from Kolkata to Kochi, Delhi to Chennai. Competitors with 10,000 or 20,000 pallets couldn't offer this integrated service.

The customer portfolio reflected this scale advantage. Snowman, given its first-mover advantage and established infrastructure, had been able to use these strengths to attract Hindustan Unilever, Baskin Robbins, Ferrero Rocher and McCain. These weren't transactional relationships—these were multi-year contracts with blue-chip brands that required absolute reliability.

The operational infrastructure backing this was sophisticated. Command centers tracked temperatures 24/7 across warehouses and vehicles. 100% power backup ensured zero downtime. ERP systems provided inventory visibility to customers. The technology might not have been Silicon Valley-grade, but for cold chain logistics in India, it was differentiated.

The competitive moats were becoming visible:

Scale: With one lakh plus pallets of warehousing capacity spread across the country and a fleet of 293 trucks traversing the length and breadth of the country, Snowman was in a unique leadership position. No competitor came close to this national footprint.

Customer stickiness: Once a brand integrated Snowman into its supply chain—training staff on systems, calibrating inventory levels, establishing delivery routes—switching costs were high. A temperature breach during transition could destroy inventory worth millions. Most customers preferred to stick with the devil they knew.

Network effects: Each new warehouse made the entire network more valuable. A customer using Snowman in Mumbai and Chennai would prefer Snowman when entering Pune or Bangalore, rather than cobbling together multiple vendors.

But the expansion wasn't without costs. The capital intensity was brutal. Each pallet of capacity required significant investment in land, construction, refrigeration equipment, and working capital. The utilization ramp-up took time—new warehouses didn't reach optimal occupancy for 12-18 months. This created a J-curve: Invest heavily upfront, wait for utilization to climb, eventually reach profitability.

The transportation division remained an "enabler" to the core warehousing business, as management consistently described it. Trucking was lower-margin but necessary to provide integrated solutions. Customers wanted end-to-end service: Store products in Snowman's warehouse, transport them in Snowman's trucks, deliver to retail outlets. Snowman couldn't be just a storage company.

The pharmaceutical opportunity was emerging too. Vaccines, biologics, and specialty drugs required ultra-precise cold chain with complete audit trails. Snowman's quality infrastructure positioned it well for this high-value segment, though pharma remained a smaller portion of revenue compared to FMCG and QSR.

By 2018, Snowman had achieved something remarkable: It had built India's first truly national cold chain network, backed by operational quality that met international standards. The company had survived the post-IPO execution test and validated its business model.

But storms were gathering. Competition was intensifying as others saw the opportunity. Profitability, while improving, still wasn't stellar given the capital deployed. Return on equity remained modest. And the capital requirements for further expansion seemed endless.

The company needed strategic options: Continue the capital-intensive buildout independently, find a strategic partner to accelerate growth, or pivot the model toward asset-light expansion. What happened next—the Adani Group's dramatic entrance and equally dramatic exit—would force Snowman to confront these choices.

VII. The Adani Saga: The Deal That Almost Was (2019–2020)

December 27, 2019. Adani Logistics Limited, a wholly owned subsidiary of Adani Ports and SEZ Limited, announced it had signed definitive agreements to acquire 40.25% stake in Snowman Logistics Ltd from Gateway Distriparks Ltd.

The Adani Group—one of India's largest conglomerates with interests spanning ports, power, energy, and infrastructure—was making a major move into cold chain logistics. The purchase price of INR 44 / share represented a 3.2% premium to the market price of December 27, 2019 and a 12% premium to 60 day VWAP. The total transaction value: Rs 296 crore.

The strategic rationale was compelling. Karan Adani, while announcing the acquisition said, "The acquisition is in line with our strategy and vision to be a leader in providing integrated logistics services in India and moving from port gate to customer gate. Cold chain is key product in customer gate strategy given India's consumer-driven demand".

Think about the Adani playbook: The group controlled major ports through Adani Ports & SEZ. They were building multimodal logistics parks, operating rail freight, and expanding warehousing. But they lacked the final mile for perishables—temperature-controlled distribution. Acquiring Snowman would complete their logistics value chain, allowing them to offer food and pharma companies integrated services from import terminal to retail outlet.

For Gateway Distriparks, the exit made financial sense. GDL had bought control in 2006 for Rs 48.12 crore. Now, selling 40.25% for Rs 296 crore valued the entire company at roughly Rs 735 crore—a solid multiple on the original investment. Gateway could monetize, retain significant upside through remaining shares, and let the Adani Group provide growth capital.

As part of the transaction, Adani Logistics would make a mandatory open offer for a maximum 26% of the public shareholding in the Company. Acquisition was subject to customary condition precedents and expected to close by March 31, 2020.

The market reacted positively. Shares of Adani Ports and SEZ gained nearly 2 per cent in early trade on the BSE on Monday after Adani Logistics announced on Friday it had signed an agreement to acquire a 40.25 per cent stake in Snowman Logistics from Gateway Distriparks for Rs 296 crore.

For Snowman's public shareholders, the Adani acquisition carried mixed implications. On one hand, joining the Adani Group meant access to the conglomerate's capital, operational resources, and political relationships. Adani could accelerate Snowman's expansion far faster than Gateway. On the other hand, Adani-group companies often traded at conglomerate discounts, and minority shareholders sometimes felt sidelined.

But something went wrong.

The timeline became problematic almost immediately. The deal was supposed to close by March 31, 2020. But COVID-19 exploded across India in March 2020. On March 24, 2020, the Indian government imposed one of the world's strictest lockdowns. Business activity froze. Supply chains seized up. Stock markets crashed.

On March 13, 2020, Snowman stock reached its all-time low of 24.05 INR. The stock had collapsed from the highs of 2014, reflecting not just COVID panic but years of disappointing profitability.

Then on May 12, 2020, came the bombshell: Adani Logistics, the wholly-owned subsidiary of Adani Ports & Special Economic Zone (APSEZ), withdrew itself from the deal to acquire shareholdings in the cold chain logistics provider Snowman Logistics from Gateway Distriparks.

The official explanation was procedural. The stock exchange filing read "This is to inform you that the condition for completion of transaction by March 31, 2020, was not met by the acquirer, and the seller has notified the acquirer and the company that the agreement is not in force due to repudiation of the agreement by the acquirer."

But market observers suspected the real reasons were more complex. Sources close to the deal said Adani Logistics decided not to go ahead after valuations in the industry fell sharply due to the ongoing Coronavirus pandemic. On Monday, Snowman Logistics was trading on the BSE at Rs 27.5 a share with a total market valuation of Rs 459 crore. In December last year, Adani Logistics had announced acquisition of 40 per cent stake in Snowman for Rs 296 crore at a price of Rs 42 a share.

The math was stark: Adani had agreed to pay Rs 296 crore for 40.25% when the company's market cap was around Rs 735 crore. By May 2020, the entire market cap had fallen to Rs 459 crore. Adani was being asked to pay Rs 296 crore for a stake in a company now worth Rs 459 crore total. The deal made no sense at those valuations.

But there were likely other factors too. The Adani Group was facing its own pressures—COVID had disrupted port operations, airport traffic, and power demand. Deploying Rs 296 crore plus open offer money into cold chain logistics during a pandemic, when restaurants were closed and food consumption patterns were chaotic, seemed risky.

There's also this: Adani Logistics noted that parties were in discussion in relation to the purchase of its 40.25 per cent stake in Snowman. "ALL has received a letter issued by GDL in relation to a purported repudiation of the SPA and ALL has duly responded to the same. ALL has categorically denied the correctness and basis of the statements, assertions and claims being made by GDL," suggesting legal disputes over who was responsible for the deal collapse.

Snowman even invoked arbitration against Adani Logistics regarding the proposed sale, though later withdrew the arbitration as both parties moved on.

What did this reveal about Snowman's strategic value?

The Positive: A conglomerate like Adani saw enough strategic value in cold chain to bid Rs 296 crore. The business model was validated even if the deal fell apart.

The Negative: The deal falling through during stress exposed Snowman's fundamental challenge—it remained a capital-intensive business with modest returns, vulnerable to valuation swings and dependent on continuous expansion to justify valuations.

The Reality Check: Cold chain infrastructure was essential but not necessarily highly profitable. Network effects existed but weren't winner-take-all. Margins were constrained by competition and capital needs.

For Gateway Distriparks, the failed sale left them still controlling Snowman, committed to funding its growth ambitions, but without the expected exit liquidity. For Snowman's management, it was back to executing independently, finding capital for expansion, and proving the business could deliver compelling returns.

The episode would ultimately push Snowman toward a different strategic path: asset-light expansion and service innovation, leading to the 5PL model that would become central to the company's next chapter.

VIII. Gateway Distriparks Doubles Down (2020–2024)

After the Adani deal collapsed, Gateway Distriparks faced a choice: Gradually exit the capital-intensive cold chain business, or double down and accelerate Snowman's growth. Gateway chose the latter.

The company, which owned 44.27 per cent stake in Snowman Logistics, upped its stake to 44.75 per cent. Rather than sell, Gateway was accumulating. The logic became clearer over time: Snowman's nationwide network of temperature controlled warehouses, and a large fleet of refrigerated vehicles, offered a unique advantage as it catered to various segments such as pharma, vaccines, e-commerce, quick service restaurants, seafood, poultry, dairy, batteries, industrial products, etc.

The COVID-19 crisis paradoxically demonstrated Snowman's value. Snowman's business was considered 'essential services' as per Ministry of Home Affairs; all warehouses remained fully operational. While restaurants closed and consumption patterns shifted, cold chain infrastructure became even more critical. Vaccine distribution—especially for COVID vaccines requiring ultra-cold storage—highlighted how essential professional cold chain networks were.

Gateway was betting that structural trends favored cold chain despite near-term disruption: E-commerce growth, QSR expansion, pharmaceutical requirements, and formalization of unorganized food sectors all pointed to rising demand for temperature-controlled logistics.

Then in December 2024 came the ultimate commitment. Gateway Distriparks acquired a further 16,65,284 equity shares of Snowman Logistics on December 23, 2024. With this, the current shareholding of GDL in Snowman Logistics now stands at 50.01%.

Fifty-point-zero-one percent. This wasn't symbolic—it was structural. Accordingly, Snowman Logistics has become a subsidiary company of GDL. Gateway had moved from controlling shareholder to majority owner, consolidating Snowman into the GDL group and signaling long-term commitment.

The object of acquisition was described as a strategic investment and both GDL and Snowman Logistics are in the same line of business, i.e. logistics. The synergies were real: Gateway's container terminals could integrate with Snowman's cold chain for food imports/exports. Gateway's inland container depots could co-locate with Snowman's warehouses. Cross-selling opportunities abounded.

This subsidiary structure created strategic flexibility. Gateway could fund Snowman's expansion through debt or equity at the GDL level. Financial reporting would consolidate, allowing Gateway to showcase Snowman's growth as part of its integrated logistics platform. Most importantly, Gateway could take a truly long-term view without quarterly pressure from public markets to show immediate cold chain profitability.

The commitment from Gateway was significant because cold chain remained brutally capital-intensive. But Gateway had faith that the moat Snowman had built—national network, customer relationships, operational quality—would compound over decades. Infrastructure plays required patient capital, and Gateway was providing it.

For Snowman's minority shareholders, the subsidiary status was neutral to slightly negative—less independence but more stability. The company wouldn't face existential capital constraints, but strategic decisions now flowed from Gateway's boardroom.

The Adani episode, in hindsight, had been a useful forcing function. It tested whether Snowman could attract strategic buyers at decent valuations, revealed the company's strengths and weaknesses during diligence, and ultimately pushed Gateway to make a definitive commitment rather than remain a financial investor hoping for eventual exit.

With that commitment secured, Snowman's management could focus on execution and innovation rather than fundraising and M&A. The question shifted from "Who will own Snowman?" to "How will Snowman deliver returns worthy of Gateway's investment?" The answer would emerge through strategic pivots in both capex approach and service offerings.

IX. Modern Era: Asset-Light Strategy & 5PL Innovation (2020–Present)

By 2020, Snowman faced a fundamental tension: Growth required adding capacity, but building owned warehouses consumed enormous capital. The company needed to scale faster without destroying returns.

The solution: Go asset-light.

The Company added 10,518 additional pallets in FY 2022. In addition, it ventured into dry warehousing for providing a comprehensive solution to store both temperature controlled and dry goods. But more significantly, the how of expansion was changing.

The turning point came in Guwahati. Snowman commenced operations at a newly leased multi-temperature controlled warehouse in Guwahati, Assam, boasting a total capacity of 5,152 pallets. CEO Sunil Nair expressed the significance of this venture, stating it aligned with the strategic move towards an asset-light approach. The expansion elevated the overall pallet capacity to over 141,000.

"Newly leased"—those two words signaled the pivot. Sunil Nair said "The inauguration of our latest facility in Guwahati signifies a momentous achievement for Snowman Logistics. This establishment marks our initial venture into a fully leased cold storage facility, aligning with our strategic move towards becoming asset-light."

Rather than buy land, construct warehouses, and own assets (high capex, long payback), Snowman would lease built-out facilities. This flipped the model: Lower upfront investment, faster deployment, operational flexibility. The trade-off: Landlords captured some economic value, but Snowman preserved capital for high-return opportunities.

The asset-light shift made strategic sense. Snowman's competitive advantage wasn't owning real estate—it was operating cold storage better than anyone else, managing customer relationships, and providing integrated logistics. Let others own the bricks and compressors; Snowman would focus on operational excellence.

Current scale reflected this approach: The company operates facilities with a total pallet capacity of 1,54,330, with advanced temperature control systems to handle products requiring storage from +25°C to -25°C. That's 154,330 pallets—a 50% increase from the 100,000-pallet milestone just years earlier. But the expansion hadn't required proportional capital deployment because leasing reduced upfront investment.

Then came an even more audacious strategic innovation: 5PL services.

The Company launched 5PL (Fifth-Party Logistics) services in India in 2023. "We are the first company to introduce this service in the cold chain logistics and supply chain management sector in India."

What's 5PL? 5PL companies operate as an aggregator for 3PL companies. But it goes deeper than aggregation. In this model, Snowman operates as an integral part of the client's organisation, develops suppliers, negotiates pricing on behalf of customers, audits manufacturing plants, shares production/requirement planning, buys stocks from them, consolidates in warehouse, and sells to the clients.

This was transformative. Traditional 3PL (third-party logistics) meant: Client tells you what to store and move, you store and move it. 5PL meant: Client gives you demand forecast and budget, you figure out sourcing, negotiate with suppliers, manage inventory, handle entire supply chain.

CEO Sunil Nair said, "The launch of 5PL services has opened up a huge opportunity for us to convert our existing 3PL accounts to 5PL accounts. Being the industry leader in cold chain and integrated solutions for the last three decades, this is a win-win situation for us and our customers. By using our expertise, network of suppliers and customers and offer distribution and consolidation services in addition to our existing solutions, we are now offering one-stop distribution services, right from the manufacturing plant to the consumption points through which we are able to add further value and enhance earnings from our existing businesses without needing to invest in infrastructure."

That last phrase is key: "without needing to invest in infrastructure." 5PL was margin-accretive services layered on existing assets. Instead of just earning storage and trucking fees, Snowman could capture procurement margins, consolidation economics, and supply chain optimization value.

Early customers validated the model. Snowman had already started offering this service to IKEA, Tim Hortons and Baskin Robbins and was targeting aggressive growth in this segment. These weren't experiments—IKEA, a notoriously demanding customer, was letting Snowman manage food supply chain end-to-end.

Mohit Khattar, CEO, Graviss Foods Pvt Ltd – Baskin Robbins, testified, "Snowman has been our 3PL partner for the last decade or so. Their national presence, experience in cold chain logistics and quality infrastructure across cities adds value and assurance to our partners and to our operations."

The 5PL model addressed several challenges simultaneously:

Capital efficiency: Services didn't require warehouses or trucks—leverage existing assets.

Margin expansion: Procurement and supply chain management commanded higher fees than basic storage.

Customer lock-in: Once Snowman managed a client's entire cold chain—sourcing, inventory, distribution—switching costs became prohibitive.

Competitive differentiation: Few competitors had the network, expertise, or customer relationships to offer true 5PL.

The transformation over a decade was striking: From building warehouses with borrowed capital to leasing facilities and layering on high-margin services. From "we'll store your products" to "we'll manage your entire cold chain supply chain."

By 2025, Snowman was operating 43 strategically located warehouses with a total pallet capacity of 1,50,754, spread across 20 cities, including key hubs such as Mumbai, Chennai, Bengaluru, and Kolkata. The network was comprehensive, the service offering sophisticated, the business model materially improved from the debt-laden pre-IPO days.

But challenges remained. Profitability, while improving, was inconsistent. Competition was intensifying. And the fundamental capital intensity of cold chain—even with asset-light strategies—meant returns wouldn't reach software-like levels.

Still, Snowman had achieved something rare: It had survived and strengthened over three decades in one of India's most difficult infrastructure sectors, adapted its strategy multiple times, and built a network no competitor could easily replicate. The question was whether this translated to compelling shareholder returns.

X. Business Model Deep Dive

Understanding Snowman's economics requires unpacking how cold chain logistics actually makes money—and why it's so difficult to make a lot of money.

Revenue Segments:

Snowman operates three primary business lines:

-

Warehousing Services: This is the core. Customers pay for storage capacity measured in pallets (each pallet holds roughly one tonne of product). Revenue from warehousing services was at Rs 55.67 crore in a recent quarter. Pricing depends on temperature zone (frozen vs. chilled vs. ambient), location (metro vs. tier-2), and contract duration. Long-term contracts (2-5 years) provide stability but limit pricing flexibility.

-

Transportation Services: The reefer fleet handles inter-city transport and last-mile delivery. Revenue from transportation services was at Rs 35.82 crore (up 12.04% YoY) in the same period. This division "acts as an enabler" to provide integrated solutions. Margins are thinner than warehousing because trucking is more competitive and requires continuous fleet maintenance.

-

Trading and Distribution: This encompasses the newer 5PL services—sourcing, procurement, inventory management. Revenue from trading and distribution stood at Rs 51.96 crore (up 45.54% YoY). That 45% growth rate reflects the 5PL rollout. Margins depend on product categories and the value-add Snowman provides beyond basic logistics.

Unit Economics:

The key metric is pallet utilization—what percentage of storage capacity is rented. An empty warehouse hemorrhages cash (refrigeration runs 24/7 regardless of occupancy). Industry benchmarks target 80-90% utilization at maturity. New facilities start at 40-50% and ramp over 12-24 months, creating that painful J-curve.

For the reefer fleet, the metric is effective kilometers per truck per month—how much the assets are utilized. Empty backhauls (truck returns empty after delivery) destroy economics. Snowman's network helps here: A truck delivering from Mumbai to Bangalore might pick up a return load to Delhi, minimizing empty runs.

Technology Infrastructure:

The Company's infrastructure comprises of compartmentalized temperature-controlled warehouses, with transportation division acting as an enabler. The Company is focused on its core business of temperature-controlled warehousing for frozen and chilled products.

Technology is the invisible edge. Command centres track every warehouse and vehicle in real-time. Temperature deviations trigger alerts. Customers get inventory visibility through ERP integration. This isn't bleeding-edge tech, but it's differentiated in Indian cold chain where many competitors still operate on WhatsApp and Excel.

The infrastructure also includes blast freezing capabilities at select locations—rapidly freezing products to preserve quality. The company offers blast freezing facilities at its temperature controlled warehouses in Bengaluru, Mevalurkuppam near Chennai, Visakhapatnam, Serampore near Kolkata, Taloja near Mumbai, Ahmedabad, Palwal near Delhi, Mubarakpur near Chandigarh and Surat.

Service Differentiation:

Snowman's pitch isn't "we're cheapest"—it's "we're most reliable." The company offers 100% power backup (critical given India's power infrastructure), 24/7 temperature monitoring, and audit trails for pharmaceutical compliance. For brands like HUL or Ferrero, reliability trumps cost. A single temperature breach destroying Rs 1 crore of inventory makes Snowman's premium pricing look inexpensive.

The service portfolio includes value-added offerings: Value added services include kitting, labelling, sorting, stuffing, and de-stuffing of containers, repacking, and bulk breaking. Additionally, it engages in trading and distribution that includes sourcing, vendor development, inventory planning, procurement, and sales.

Capital Allocation:

The asset-light pivot changed capital allocation. Previously, Snowman built warehouses (Rs 10-15 crore capex per facility). Now, increasingly, it leases. This preserves capital for high-ROI investments: Technology systems, fleet expansion where ownership matters, and working capital for 5PL operations where Snowman takes inventory ownership temporarily.

The challenge? Company has low interest coverage ratio and a low return on equity of 2.22% over last 3 years. That's the tension: Revenues growing nicely, but profitability inconsistent. Why?

Several factors: (1) New capacity takes time to ramp, dragging margins. (2) Competition limits pricing power. (3) Debt servicing consumes cash. (4) Working capital for 5PL ties up funds. (5) The business is structurally lower-margin than software or branded consumer businesses.

But there's also this: Infrastructure assets compound slowly. A warehouse built today generates cash for 20-30 years. Current accounting captures depreciation and interest expense but not the long-term option value of the network. Patient investors betting on India's cold chain expansion might accept low current ROE if the terminal value is compelling.

The business model boils down to this: Build or lease warehouses and trucks (moderate to high capex), sign long-term contracts with blue-chip customers (sticky revenue), operate with fanatical reliability (defensibility), layer on value-added services like 5PL (margin expansion), and pray that volume growth and utilization improvement eventually deliver acceptable returns.

It's not a sexy model. But it might be a durable one—and durability in infrastructure has value.

XI. Competitive Landscape & Industry Dynamics

Cold chain logistics in India remains frustratingly fragmented, which is both Snowman's opportunity and its challenge.

The Indian cold chain market can be segregated into organised sector and unorganised sector. Currently, the unorganised segment exhibits clear dominance in the market. What does "unorganised" mean? Small, regional cold storage operators—often family-run businesses focusing on single commodities (potatoes dominate). They lack national networks, technology systems, or the quality standards that multinational brands require.

The temperature-controlled logistics industry continues to be heavily fragmented with a large part of the requirement being addressed by unorganised players. Increased industry awareness has brought in several new players in recent times.

Organized Competitors:

Snowman Logistics's top competitors include CONCOR, Stellar Value Chain and TESSOL, and TCI Cold Chain Solutions.

Container Corporation of India (CONCOR): A government PSU with massive rail infrastructure. CONCOR operates some cold storage but primarily focuses on containerized freight. Not a direct cold chain pure-play.

TCI Cold Chain Solutions: Part of Transport Corporation of India, TCI operates integrated cold chain services. A credible competitor with national presence, though generally perceived as less focused than Snowman.

Gati-KWE (now Allcargo Gati): Logistics company with cold chain offerings. After acquisition by Allcargo, it's been integrated into broader logistics portfolio.

Others: ColdEx, Kelvin Cold Chain, various regional players.

But here's the reality: Snowman is a subsidiary of Gateway Distriparks. The company operates the largest cold chain network in India, with 44 warehouses on over 3 million+ sq ft across 21 cities. Snowman is meaningfully larger than any organized competitor.

Market Dynamics:

The organized cold chain market is estimated at only 6-7% of total temperature-controlled warehousing and 15-20% of transportation. The rest? Unorganized. This fragmentation creates massive consolidation potential, but it also means competitors are everywhere, many operating at lower costs (if also lower quality).

Entry Barriers:

Cold chain has genuine barriers to entry, but they're not insurmountable:

-

Capital Requirements: Building temperature-controlled warehouses requires Rs 10-15 crore per facility. Reefer trucks cost 2-3x standard trucks. Total capex to reach meaningful scale: Hundreds of crores. This deters casual entrants.

-

Technology & Operations: Maintaining precise temperatures 24/7/365, managing complex logistics, and providing audit trails requires operational sophistication. Many companies claim cold chain capability; few deliver reliably.

-

Customer Relationships: Blue-chip FMCG and QSR brands conduct rigorous audits before onboarding cold chain vendors. Winning these relationships takes years. Once won, they're sticky.

-

Network Effects: A truly national network with presence in all major cities creates value competitors can't match. This is Snowman's strongest moat.

However, barriers aren't absolute. Well-funded competitors or strategic entrants (like Adani attempted) could build parallel networks. Existing logistics companies (Delhivery, Mahindra Logistics) could expand into cold chain. E-commerce giants (Amazon, Flipkart) might build proprietary cold infrastructure.

Strategic Positioning:

Snowman is one of the largest-serving cold storage companies in India, operating since 1996. Furthermore, for temperature-regulated logistic services, such as cold storage, transport and other additional services, Snowman has emerged as the biggest market leader in India.

This market leadership matters because:

- Blue-chip customers gravitate to established leaders: Risk aversion in supply chain drives customers to proven vendors.

- Scale economies kick in: Larger networks optimize asset utilization and backhaul logistics better.

- Talent attraction: Quality operations staff prefer working for industry leaders.

Future Threats:

-

Deep-pocketed entrants: Adani's interest revealed cold chain's strategic value. Others—Mahindra Logistics, Delhivery, or even Reliance—could enter aggressively.

-

E-commerce captive infrastructure: Amazon and Flipkart might build proprietary cold chains for grocery/perishables, bypassing third-party providers.

-

Technology disruption: IoT, route optimization AI, and blockchain for cold chain traceability could commoditize operations if technology becomes easily accessible.

-

Customer backward integration: Very large brands might insource cold chain to capture margins.

Competitive Response:

Snowman's strategy seems to be: (1) Expand network breadth faster than competitors, (2) Deepen customer relationships through 5PL services that increase switching costs, (3) Focus on operational quality to justify premium pricing, (4) Pursue asset-light leasing to accelerate expansion without proportional capital.

The competitive landscape suggests Snowman has a window—perhaps 5-10 years—to cement its leadership before the industry consolidates or new entrants achieve scale. Whether the company can translate this leadership into strong financial returns remains the open question.

XII. Financial Performance & Challenges

Let's confront the numbers honestly—because Snowman's financial performance tells a story of growth with inconsistent profitability.

Revenue Trajectory:

The revenues of SNOWMAN stood at Rs 5,101 m in FY24, which was up 20.0% compared to Rs 4,252 m reported in FY23. That's Rs 510 crore in FY24, representing strong topline growth. On an annual basis for FY24, Company recorded revenue of Rs 503.37 crore as against Rs 417.65 crore during FY23. EBITDA increased to Rs 108.32 crore from Rs 96.07 crore.

The most recent full year showed continued momentum. For FY25, revenue stood at ₹552.53 Crores, marking a 9.8% increase over ₹503.37 Crores in FY24.

So revenue growth is consistent: 20%+ year-over-year growth in recent years. The company crossed the Rs 500 crore milestone—psychologically and operationally significant.

Profitability Challenges:

Here's where it gets complicated. PAT during FY24 was Rs 12.71 crore as against Rs 13.40 Crore during FY23. The reason for decline in PAT is due to deferred tax asset reversal of Rs 4.34 crore which is not a cash outflow.

Strip out the accounting adjustment, and core profitability was roughly flat despite 20% revenue growth. Why?

The company's operating profit increased by 14.7% YoY during FY24. Operating profit margins witnessed a fall and stood at 20.2% in FY24 as against 21.2% in FY23. Margins contracted even as revenue grew—typical of capacity expansions where new facilities aren't yet at full utilization.

More concerning, For FY25, annual EBITDA was ₹93.53 Crores (FY24: ₹108.32 Crores), and PAT was ₹5.69 Crores (FY24: ₹12.71 Crores). EBITDA declined 14% and PAT declined 55% year-over-year despite revenue growth. That's troubling.

Return Metrics:

Company has a low return on equity of 2.22% over last 3 years. That's anemic. For context, Indian equity markets historically deliver 12-15% returns. A business generating 2% ROE destroys shareholder value.

The ROCE for the company improved and stood at 10.2% during FY24, from 8.8% during FY23. Return on capital employed is better than ROE but still modest for the risk profile.

Company has low interest coverage ratio. Interest coverage ratio improved and stood at 2.1x during FY24, from 2.0x during FY23. An interest coverage of 2x means earnings barely cover debt servicing—leaving little room for error.

Capital Structure:

The debt burden remains material. Long-term debt down at Rs 624 million as compared to Rs 776 million during FY23, a fall of 19.5%. Snowman is reducing leverage, which is positive, but debt servicing still consumes significant cash.

Cash Flow:

Cash flow from operating activities during FY24 stood at Rs 878 million, an improvement of 1.6% YoY. Overall, net cash flows for the company during FY24 stood at Rs 54 million from Rs -134 million net cash flows seen during FY23.

Operating cash flow is positive and improving, though the company's capex and working capital needs absorb much of it. Free cash flow generation remains constrained.

Stock Performance:

SNOWMAN reached its all-time high of 134.65 INR on Nov 18, 2014 and all-time low of 24.05 INR on Mar 13, 2020. That's an 82% decline from peak to trough—reflecting both COVID panic and fundamental disappointment.

In terms of performance, Snowman Logistics share price has increased by 8.4% over the past six months and has declined by 32.03% over the last year. The stock remains volatile and well below its 2014 highs.

What's Going Wrong?

Several factors explain the profitability challenges:

-

Continuous Expansion: Adding capacity—even through leasing—requires investment and creates near-term margin dilution before new facilities ramp.

-

Competition: Cold chain remains fragmented but competitive. Pricing power is limited.

-

Fixed Cost Structure: Warehouses and trucks have high fixed costs. If utilization slips even slightly, margins compress fast.

-

Working Capital for 5PL: Taking inventory ownership in the 5PL model ties up working capital, increasing financial expenses.

-

Depreciation and Interest: Even asset-light strategies require some capex, and legacy debt servicing continues.

Management Perspective:

Chairman Prem Kishan Dass Gupta said: "The Company delivered strong revenue growth during the year, driven by continued expansion of its distribution business and the strategic shift towards a 5PL model. This performance was achieved despite a challenging market environment, marked by muted consumption trends across India."

Management frames this as growth investment—short-term margin pressure to capture long-term market leadership. That's the bull case: Accept low current returns because terminal value is significant.

The Challenge for Investors:

Infrastructure businesses often look mediocre on traditional metrics (ROE, P/E) during growth phases. Snowman has built a near-monopoly national cold chain network—that has value. But translating network leadership into strong financial returns has proven elusive.

The company's financials present a paradox: Impressive operational scale and customer relationships, but uninspiring returns. Whether this represents a temporary growth investment phase or structural issues with cold chain economics is the trillion-rupee question.

For investors considering Snowman, the financial performance demands honest assessment: This is not a high-return compounder like Asian Paints or HDFC Bank. It's a slow-growth infrastructure play where the bet is on long-term structural demand outweighing mediocre current profitability.

XIII. Playbook: Business & Investment Lessons

Snowman's 30-year journey offers rich lessons for entrepreneurs, operators, and investors—particularly those interested in infrastructure, logistics, and emerging market operating challenges.

1. Timing the Infrastructure Gap

Snowman's founding insight was recognizing that India's economic liberalization and retail modernization would create massive demand for cold chain infrastructure years before that demand materialized. The company commenced cold storage operations in Fiscal 1998—when organized retail barely existed.

Lesson: True infrastructure plays require betting years ahead of obvious demand. By the time everyone sees the opportunity, competitive advantage erodes. But this demands patient capital and tolerance for long gestation periods.

2. Foreign Investor Validation

In 2001, Mitsubishi Group acquired majority stake; in 2003, Nichirei Corporation acquired 15%. These weren't typical financial investors—they were global leaders in cold chain bringing operational expertise.

Lesson: In infrastructure and specialized logistics, strategic investors who bring operational know-how often matter more than pure financial investors. HUL, Mitsubishi, Nichirei, and IFC each brought something beyond capital—credibility, technology, governance, or customer relationships.

Myth vs Reality Box:

Myth: Indian infrastructure companies don't need foreign partners if they have domestic market knowledge.

Reality: Foreign strategic investors brought Snowman technology transfer, quality standards, and signaling value that accelerated customer wins. The Japanese partnership was transformational.

3. The IPO Window

The IPO was subscribed 59.75 times with total bids for 194.49 crore shares. Snowman caught a perfect market window—September 2014, Modi bull market, infrastructure euphoria, limited cold chain investment options.

Lesson: For capital-intensive businesses, timing IPO windows matters enormously. Snowman raised money when markets were receptive, allowing it to expand before competitors mobilized. Companies waiting for "perfect" fundamentals often miss market windows.

But there's a corollary: The stock reached all-time high of 134.65 INR on Nov 18, 2014 just two months after listing, then declined for years. IPO euphoria doesn't guarantee sustained shareholder returns—fundamentals eventually matter.

4. The Pivot That Matters

Snowman commenced its business as a trader of frozen marine products and in Fiscal 1998, commenced cold storage operations. The pivot from trading to infrastructure was the defining decision.

Lesson: The best business model pivots leverage existing expertise while moving up the value chain. Snowman knew frozen products from trading; it pivoted to building the infrastructure those products required. Adjacencies matter.

Contrast this with companies that pivot to completely unrelated businesses—those rarely work. Snowman's pivot was logical, defensible, and created long-term moats.

5. Capital Structure Trade-offs

Net profit declined from Rs 14.4 crore in FY13 to Rs 13.7 crore in FY14 as expansion came through expensive bridge loans; interest burden ballooned from Rs 2.4 crore to Rs 11.2 crore in FY14.

Lesson: Aggressive debt-funded growth can work—if you can refinance before interest costs crush profitability. Snowman's pre-IPO bridge loans were risky but calculated: Build capacity to demonstrate scale, then raise equity. It worked, but barely.

The counter-lesson: Company has low interest coverage ratio and low return on equity of 2.22% over last 3 years. Even after refinancing, Snowman's profitability remains constrained by debt servicing. High leverage in capital-intensive, moderate-margin businesses leaves little room for error.

6. Strategic M&A Complexities

The Adani saga offers multiple lessons. Adani Logistics signed agreement to acquire 40.25% stake in Snowman for INR 296 Crores in December 2019, only to withdraw from the deal in May 2020.

Lesson: M&A in infrastructure is fraught. Timing matters (COVID crashed valuations). Buyer's remorse is real when market conditions shift. For sellers (Gateway), having deal certainty mechanisms and walkaway rights is critical. For target companies (Snowman), being dependent on strategic M&A for growth capital is risky—deals fall apart.

The deeper insight: The failed deal revealed Snowman's strategic value (Adani saw enough to bid Rs 296 crore) while exposing valuation sensitivity. In cyclical, capital-intensive businesses, valuation swings are massive.

7. Asset-Light Transition

The Guwahati facility marked Snowman's initial venture into a fully leased cold storage facility, aligning with the strategic move towards becoming asset-light.

Lesson: Even companies built on owning physical assets can pivot to asset-light models once they've established brand, operational capabilities, and customer relationships. Snowman realized its competitive advantage wasn't owning warehouses—it was operating them better than anyone else.

This is classic strategy evolution: Build owned assets to prove the model and establish credibility, then shift to leasing/franchising/licensing to accelerate growth without proportional capital.

8. Innovation Leadership

The Company launched 5PL services in India in 2023. "We are the first company to introduce this service in the cold chain logistics and supply chain management sector in India."

Lesson: In "boring" infrastructure businesses, service innovation can be as valuable as physical assets. 5PL transformed Snowman from commodity storage provider to strategic supply chain partner—increasing margins, customer stickiness, and differentiation.

The pattern: Find higher-margin, harder-to-replicate services you can layer on top of your physical infrastructure. This is how infrastructure companies escape commodity economics.

9. Execution in Fragmented Markets

The unorganised segment exhibits clear dominance in the market. Yet Snowman built the largest cold chain network in India with 44 warehouses on over 3 million+ sq ft across 21 cities.

Lesson: In highly fragmented, unorganized Indian markets, the first mover to bring professional management, technology, and quality standards can capture disproportionate value—even if the overall market remains fragmented. You don't need to consolidate the entire industry; you need to capture the premium segment (multinational brands, organized retail) that values reliability.

But the counter-lesson: Fragmentation persists because it's structurally difficult to eliminate. Low-cost unorganized players survive by serving price-sensitive segments. Snowman won the quality segment but couldn't achieve monopoly-like margins because alternatives exist.

10. Patient Capital Required

Snowman was founded in 1993. It's 2025—32 years later—and the company is still building out national infrastructure, still not generating stellar returns, still capital-constrained.

Lesson: Infrastructure is a decades-long game. If you're investing or building in this space, you need generational patience. Quarterly or even annual performance is noise. The question is: What does this network look like in 2035 or 2045?

That requires a specific type of capital—either long-term institutional investors (like Gateway), strategic parents willing to subsidize growth, or founders/management with zero urgency to exit.

The Meta-Lesson:

Snowman demonstrates both the opportunity and the challenge of infrastructure investing in emerging markets. The opportunity: Massive market, limited competition, structural tailwinds, genuine moats once built. The challenge: Brutal capital intensity, moderate returns, slow payback, vulnerable to competitive entry, and execution complexity.

It's not for everyone. But for those with patience, operational skill, and genuinely long-term horizons, infrastructure can compound value in ways high-growth tech never will—slowly, invisibly, and durably.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube