Sky Gold and Diamonds: India's Lightweight Jewellery Revolution

I. Introduction & Cold Open

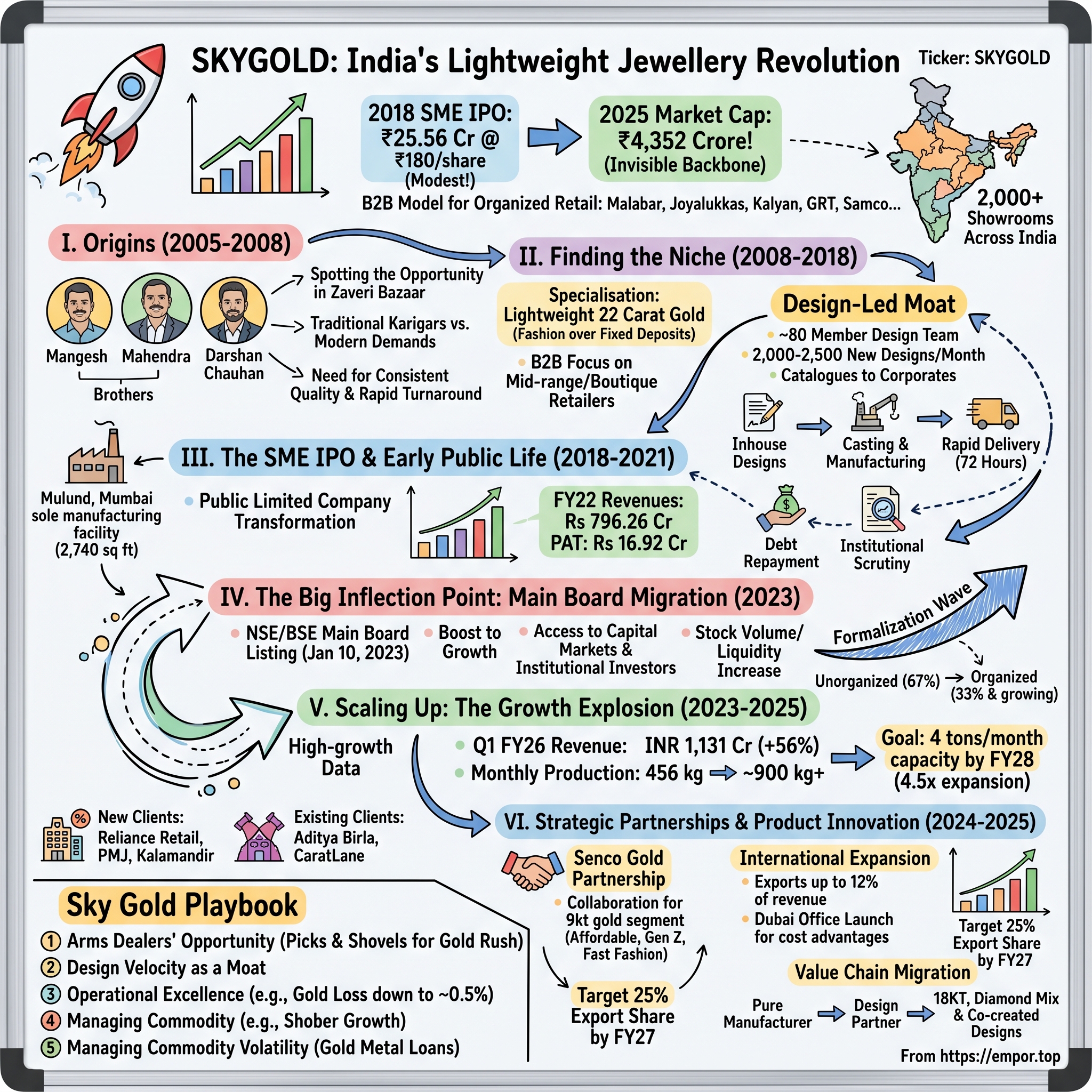

Picture this: In 2018, a small jewellery manufacturer listed on the BSE SME exchange at ₹180 per share, raising a modest ₹25.56 crores—barely enough to make waves in India's vast jewellery ocean. Fast forward to 2025, and Sky Gold commands a market capitalization of 4,352 Crore, emerging as one of India's most compelling B2B jewellery success stories.

The central question isn't just how a company grew its market cap 24-fold in seven years. It's how Sky Gold cracked the code to become the invisible backbone of India's organized jewellery revolution—the company whose designs you've probably worn without ever knowing their name. The Company works on a B2B model with leading Jewellery Retailers like Malabar Gold & Diamonds, Joyalukkas, Kalyan Jewellers, GRT Jewellers and Samco Gold. The Company also works with large wholesalers. With this, Sky Gold products are available at more than 2,000 showrooms across India.

This is the story of how three brothers from Mumbai transformed lightweight gold jewellery from a niche product into a mainstream phenomenon, how they rode the wave of India's jewellery market formalization, and how a perfectly timed mainboard migration became the catalyst for exponential growth. It's a playbook for building in traditional industries with modern approaches—where design velocity matters more than brand recognition, and where being the arms dealer in a retail war can be more profitable than fighting on the front lines.

II. Origins & Founding Story (2005-2008)

The monsoon of 2005 brought more than just rain to Mumbai's bustling jewellery districts. In the narrow lanes of Zaveri Bazaar, where gold has been traded for centuries, three brothers—Mangesh, Mahendra, and Darshan Chauhan—were watching a transformation unfold. The traditional karigars (craftsmen) who had dominated India's jewellery manufacturing for generations were struggling to meet the evolving demands of modern retailers. The market was crying out for something different: consistent quality, rapid design turnaround, and lightweight pieces that didn't compromise on aesthetics.

Sky Gold and Diamonds Limited was founded in 2005 and is based in Thane, India, but it wasn't until 2008 that the company truly found its footing. Established in 2008, Sky Gold Limited (The Company) is one of the leading jewellery companies based in Mumbai. The Company has been engaged in the business of Designing, Manufacturing and Marketing of gold jewellery.

The timing was prescient. India's jewellery market in the mid-2000s was a ₹2 lakh crore behemoth, but it was also deeply fragmented—over 90% unorganized, dominated by local jewellers and traditional family businesses. The organized players were just beginning their expansion, and they needed reliable B2B partners who could deliver variety at scale. The Chauhan brothers spotted an opportunity that others had missed: instead of competing for retail customers' attention, why not become indispensable to the retailers themselves?

The Company is specialised in lightweight jewellery of 22 Carat gold. This wasn't just a product decision—it was a strategic masterstroke. While competitors focused on heavy, investment-grade pieces that locked up customer capital, Sky Gold bet on a different consumer psyche emerging in urban India: the desire for variety over value storage, fashion over fixed deposits.

The brothers brought complementary skills to the table. Sky Gold was established in 2005 by the three Chauhan brothers and is still run by them, each with at least a decade of experience in the gems and jewellery industry. Their combined expertise in design, manufacturing, and market relationships would prove crucial in the years ahead. They weren't trying to reinvent jewellery; they were reimagining how it was made and distributed.

In those early days, operating from a modest facility, the company focused obsessively on two things: building relationships with regional jewellers who were underserved by larger manufacturers, and creating a design pipeline that could churn out fresh patterns faster than anyone else in the market. The Company manufactures jewellery through casting. The Company make Plan Gold Jewellery, Studded Gold Jewellery and Turkish Jewellery.

III. Finding the Niche: Lightweight & Design-Led (2008-2018)

The period from 2008 to 2018 was Sky Gold's decade in the shadows—crucial years where the company built its competitive moat one design at a time. While India's jewellery market was experiencing tectonic shifts post the 2008 financial crisis and subsequent gold price volatility, Sky Gold was perfecting a model that would later catapult it to prominence.

The co. follows a B2B model where the products are mainly sold to mid-range jewellers and boutique stores who sell these products through online platforms and retail stores. This wasn't glamorous work. It meant countless meetings with jewellery retailers across India's tier-2 and tier-3 cities, understanding their inventory challenges, and most importantly, decoding what their customers wanted but couldn't articulate.

The real innovation came in design velocity. It has an Inhouse ~80 Member Design Team and ~2000-2500 designs being floated every month. The catalogue is exhibited to corporate purchasers every month. Think about that for a moment—that's roughly 100 new designs per working day. In an industry where traditional jewellers might introduce a few dozen new patterns per season, Sky Gold was operating at software-industry speeds in a hardware business.

By 2012, the company had established what would become its fortress: the Mumbai manufacturing facility. The company operates from a 2,740 sq. ft. sole manufacturing facility located in Mulund, Mumbai. The facility is used to make casting based jewelry using rubber dye, wax molds, and machines. This wasn't just about production capacity—it was about control. Every piece could be tracked, every design iteration could be tested, and most importantly, the turnaround time from design to delivery was compressed to an unprecedented 72 hours.

The lightweight jewellery focus was paying dividends in unexpected ways. As gold prices began their relentless climb through the 2010s, consumers were increasingly priced out of traditional heavy jewellery. Sky Gold's lightweight pieces offered a solution: customers could still buy gold jewellery for occasions without breaking the bank, and retailers could maintain their transaction volumes despite rising prices.

The company has also set-up sales offices in Kerala and Telangana to cater to the Southern regions of India. These weren't random choices—Kerala and Telangana represented two of India's most gold-obsessed markets, where per capita jewellery consumption far exceeded the national average. By establishing a physical presence in these markets, Sky Gold was building trust in an industry where relationships still mattered more than spreadsheets.

The numbers from this period tell a story of steady, unglamorous growth. Revenue grew from a few crores in 2008 to over ₹500 crores by 2018—impressive, but not earth-shattering. Profits were thin, as the company reinvested heavily in design capabilities and relationships. The design library grew from a few thousand patterns to over 100,000. The client base expanded from dozens to hundreds. It was foundation-laying at its finest.

What the market didn't see—and what would only become apparent later—was that Sky Gold was solving a massive problem for organized retailers. As chains like Kalyan, Joyalukkas, and Malabar expanded aggressively, they needed a supplier who could provide variety across stores without cannibalizing designs, maintain quality at scale, and most importantly, adapt quickly to regional preferences. Sky Gold was becoming that irreplaceable partner.

IV. The SME IPO & Early Public Life (2018-2021)

The Sky Gold IPO listing date is on Thursday, October 4, 2018, marking the beginning of a new chapter—though few could have predicted how transformative this step would become. The IPO itself was modest by any measure: SME IPO of 14,20,000 equity shares of the face value of ₹10 aggregating up to ₹25.56 Crores. The issue is priced at ₹180 per share.

The market's initial response was lukewarm at best. The IPO was subscribed just 1.08 times, barely crossing the finish line. On listing day, the stock opened at ₹180.45—a mere 0.25% premium to the issue price. In the frenzied world of IPO pops and first-day gains, Sky Gold's debut was the equivalent of a polite golf clap.

But here's what the surface-level numbers obscured: the IPO fundamentally changed Sky Gold's DNA. It was reformed to public limited company renamed to 'Sky Gold Limited' on 26th June 2018. For the first time, the company had to think beyond relationships and handshakes. Quarterly reporting, governance structures, and institutional scrutiny—these weren't burdens but catalysts that would professionalize operations.

The capital raised, while modest, went exactly where it needed to. The company paid down high-cost debt, funded working capital requirements, and most importantly, gained the credibility that comes with being a listed entity. In India's relationship-driven jewellery industry, being able to point to public market validation mattered more than the founders initially realized.

The early public years coincided with massive disruption in India's jewellery sector. The implementation of GST in 2017 had already started formalizing the industry, making it harder for unorganized players to compete. Hallmarking regulations were becoming stricter. The demonetization of 2016 had shifted consumer behavior toward organized retail. Sky Gold, with its focus on serving organized retailers, was perfectly positioned to benefit from these tailwinds—though the market hadn't quite connected the dots yet.

During this period, the company quietly went about strengthening its core. The design team expanded, the manufacturing processes were refined, and relationships with key retailers deepened. Sky Gold manufactures its Jewellery in its 25,000 Sq Ft manufacturing facility in Mumbai, India, with the help of German Equipments. The German equipment wasn't just about quality—it was about standardization. Every piece, whether the first or the thousandth, maintained consistent quality—a critical requirement for large retail chains.

What's fascinating about this period is how wrong the market got it. While the stock languished in the SME segment, trading with limited liquidity and virtually no institutional interest, the company was laying the groundwork for explosive growth. For FY22, The Company reported total Revenues of Rs 796.26 crore and a Net Profit of Rs 16.92 crore. These numbers, while respectable, didn't scream "multi-bagger in the making."

The promoters—Mangesh, Mahendra, and Darshan Chauhan—maintained their conviction, holding onto their stakes even as the stock barely moved for months. They knew something the market didn't: the SME exchange was just a stepping stone. The real transformation would come when Sky Gold could migrate to the mainboard, accessing deeper capital pools and institutional investors.

V. The Big Inflection Point: NSE/BSE Migration (2023)

January 10, 2023, marked Sky Gold's crossing of the Rubicon. Sky Gold Limited (BSE Code: 541967), one of the leading jewellery companies based in Mumbai, has migrated to the Main Board of NSE and BSE. If the IPO was about getting a ticket to the game, the mainboard migration was about moving from the minor leagues to the majors.

Speaking on occasion, Mangesh Chauhan, Managing Director and Chief Financial Officer of Sky Gold Limited, said - "This is a big milestone for us by completing the migration to the main board of NSE and BSE at the same time from BSE SME. The migration will provide a boost to the growth of the company. Migration will help our company to attract more investors and provide further growth capital to help the company for future business growth."

The numbers leading up to the migration told a story of a company hitting its stride. Revenue had crossed ₹800 crores, the design library had exploded to over 500,000 patterns, and the client roster read like a who's who of Indian jewellery retail. But these achievements were hidden from most investors—SME stocks operate in the shadows, with minimal research coverage and limited institutional participation.

The migration wasn't just a regulatory formality; it was a complete transformation in the company's capital market profile. Suddenly, Sky Gold was eligible for inclusion in various indices. Mutual funds could now invest. Foreign institutional investors could take positions. The stock's liquidity improved overnight—trading volumes jumped multifold as the arbitrary lot size restrictions of the SME segment disappeared.

The timing was serendipitous. India's jewellery market was in the midst of a formalization wave. As of FY01, only 10% of India's retail jewellery market was captured by organised players, but this figure rose to 33% by FY22 and is expected to increase even further in the coming years. Sky Gold's B2B model meant it was leveraged to this trend—every new store opened by organized retailers was a potential revenue opportunity.

But here's what really changed: the company's ability to think big. With access to capital markets, Sky Gold could now contemplate acquisitions, capacity expansions, and international forays that were previously out of reach. The promoters, who had been conservative by necessity, could now be ambitious by choice.

The stock market's reaction was swift and decisive. From hovering around ₹200-250 in late 2022, the stock began its march upward. Volume picked up. Research reports started appearing. Institutional investors began accumulating. The company that had been hiding in plain sight was suddenly discovered.

What's instructive about this transformation is how little had changed operationally. Sky Gold was still making the same lightweight jewellery, serving the same clients, running the same manufacturing facility. The only difference was that the market could now see what was always there. It's a powerful reminder that in capital markets, accessibility and visibility matter as much as fundamentals.

The migration also coincided with a crucial strategic shift. The company began positioning itself not just as a jewellery manufacturer but as a design powerhouse and supply chain partner. The narrative evolved from "we make gold jewellery" to "we enable India's largest jewellery retailers to serve millions of customers with variety and quality."

VI. Scaling Up: The Growth Explosion (2023-2025)

The post-migration period has been nothing short of spectacular. If Sky Gold's first 15 years were about building capabilities, the last two years have been about deploying them at scale. The numbers tell a story of a company that found its moment and seized it with both hands.

Revenue from operations jumped 56.45% to Rs 1,13,123.66 crore for the quarter ended 30 June 2025. Profit before tax (PBT) stood at Rs 58.87 crore in Q1 FY26, marking a 106.92% increase from Rs 28.45 crore recorded in Q1 FY25. These aren't just good numbers—they're the kind of growth rates you expect from a software startup, not a traditional jewellery manufacturer.

The expansion has been multi-dimensional. First, there's the sheer scale of operations. The company's consolidated revenue soared to INR 1,131.00 crores in Q1 FY26, marking a substantial 56% year-on-year increase from INR 723.00 crores in Q1 FY25. This growth was driven by a 30% rise in monthly production volume, reaching 456 kg compared to 349 kg in the previous year. Production volume tells the real story—this isn't price-led growth from rising gold rates, but genuine volume expansion.

Client acquisition has accelerated dramatically. New client acquisitions include Reliance Retail, PMJ Jewellery, and Kalamandir, while the company has Increased wallet share with existing clients like Aditya Birla and CaratLane. Each new client isn't just a one-time win—it's a multi-year relationship that compounds over time as Sky Gold becomes embedded in their supply chain.

The manufacturing capabilities have evolved significantly. The company revealed that Monthly production scaled up to ~900 kg, with visibility toward even greater expansion. Ongoing 4.5x expansion will unlock 4 tons/month capacity by FY28. This isn't speculative capacity building—it's backed by firm demand visibility from existing and prospective clients.

What's particularly impressive is the operational efficiency gains. Operational efficiency: employee productivity up, gold loss down to ~0.5%. In the gold jewellery business, where margins are thin and raw material costs dominate, reducing gold loss from the industry standard of 1-1.5% to 0.5% is like finding free money.

The company's strategic positioning has evolved from being just another vendor to becoming a critical partner. Sky Gold Ltd., a jewellery manufacturer, operates in the B2B space, supplying its products to some of the biggest jewellery retailers in the country, including Malabar, Kalyan, and Joyalukkas. These aren't just customer relationships—they're strategic partnerships where Sky Gold's design capabilities and rapid turnaround times enable retailers to differentiate themselves in a competitive market.

The financial metrics reflect this operational excellence. EBITDA grew 91% to INR 71.00 crores, with margins expanding to 6.3%. Margin expansion in a commodity-processing business is notoriously difficult, yet Sky Gold has managed it through a combination of design premiums, operational efficiency, and scale benefits.

VII. Strategic Partnerships & Product Innovation (2024-2025)

September 19, 2025, marked another watershed moment in Sky Gold's evolution. Sky Gold & Diamonds jointly with Senco Gold & Diamonds announced a significant step aimed at entering into collaboration for newly introduced 9kt gold jewellery segment. This collaboration marks a significant step in catering to India's growing demand for affordable and stylish jewellery.

This wasn't just another customer win—it was a strategic pivot that opened up an entirely new market. Senco's products are sold under the Senco Gold & Diamonds trade name, through multiple channels, including approximately 70 Company-operated showrooms and 57 franchisee showrooms. Through one partnership, Sky Gold gained access to over 180 retail touchpoints across India.

Speaking on the occasion, Mr. Darshan Chauhan, Director and Chief Growth Officer at Sky Gold & Diamonds, said: "9kt jewellery is trending with the Gen Z because of the stylish, contemporary designs it offers and its alignment with fast fashion trends. It allows us to reach a wider customer base while also serving as a stepping stone for first-time gold buyers and buyers who need a variety of options in their jewellery collection."

The 9-karat innovation is particularly clever. With gold prices at historic highs, consumers are increasingly priced out of traditional 22-karat jewellery. Nine-karat gold, with less than half the gold content, offers an entry point for younger consumers who prioritize design over gold weight. It's the jewellery equivalent of fast fashion—trendy, affordable, and meant to be enjoyed rather than hoarded.

Mr. Suvankar Sen, Managing Director and CEO, Senco Gold & Diamonds, said: "At a time when gold prices are at elevated levels, the introduction of exclusive 9kt modern designs allows us to offer more accessible jewellery options. This collaboration enables Senco Gold & Diamonds to effectively cater to the younger generation and the growing affordable jewellery segment, while staying true to our commitment of delivering style, trust, and innovation to our customers."

The international expansion story is equally compelling. Exports rose to 12% of revenue (vs 8% in FY25). Growth led by orders from Malaysia, Singapore, and Middle East. The company isn't just shipping products abroad—it's building a systematic presence. Company targets 25% export share by FY27. Dubai office launch and advanced gold model will further accelerate this.

The Dubai expansion deserves special attention. Dubai office to cut gold costs (~$10/oz arbitrage). By establishing operations in Dubai, Sky Gold can source gold at international prices, manufacture locally for Middle Eastern markets, and even re-export to India under favorable trade agreements. It's regulatory arbitrage at its finest.

Product innovation has extended beyond just karatage. 18KT, diamond mix and co-created designs drive better pricing. The company is moving up the value chain, from being a pure manufacturer to a design partner that co-creates exclusive collections with retailers. These exclusive designs command premium pricing and create stickiness—a retailer is unlikely to switch suppliers when their bestselling designs are co-owned with Sky Gold.

VIII. Business Model & Operations Deep Dive

To truly understand Sky Gold's moat, you need to understand the intricate mechanics of its operations. This isn't just a company that melts gold and shapes it into jewellery—it's a design-to-delivery machine optimized for speed and variety.

Sky Gold manufactures its Jewellery in its 25,000 Sq Ft manufacturing facility in Mumbai, India, with the help of German Equipments. The German equipment—primarily casting and finishing machines—enables consistency at scale. But the real magic happens before the gold is even touched.

The company has exclusive designs across 14 Product categories. Each category—rings, earrings, pendants, bangles, necklaces—has its own design team, trend analysis, and production line. The company boasts a design library of over 500,000 designs of rings, bracelets, bangles, fancy pendants, earrings, and more. This isn't just variety for variety's sake—it's about ensuring that a retailer in Kerala gets different designs than one in Punjab, reflecting regional preferences.

The working capital management in the gold business is where financial engineering meets operational excellence. Gold is typically procured on credit from bullion suppliers or through gold metal loans from banks. Secured gold metal loan limits of INR 190.00 crores from three banks. These loans allow Sky Gold to hold inventory without tying up cash—the company pays only the interest (typically 3-4% annually) rather than the full gold value.

The capacity to process 300 Kg of Gold per month might seem modest compared to current volumes, but this reflects the company's evolution. Today's actual production far exceeds this original capacity, with recent reports showing monthly production approaching 450-500 kg and targeting even higher volumes.

What sets Sky Gold apart is its rapid response capability. The turn-around time from order receipt to delivery to only 72 hours. In an industry where traditional manufacturers might take weeks, Sky Gold operates like a just-in-time supplier. This speed isn't just operational efficiency—it's a strategic weapon that allows retailers to operate with lower inventory and respond quickly to market trends.

The technology stack, while not cutting-edge by tech standards, is revolutionary for the jewellery industry. ERP rollout improving control over gold flow, receivables, and inventory. Every gram of gold is tracked from entry to exit. Design files are digitized and can be modified quickly. Production schedules are optimized using basic but effective planning software.

Their Fast Moving Segment has an average ticket size of Rs. 50,000. This price point is strategic—high enough to be profitable, low enough to drive volume. It's the jewellery equivalent of the iPhone's pricing strategy: premium but accessible.

IX. Market Context & Competition

Understanding Sky Gold requires understanding the seismic shifts in India's jewellery market. This isn't just about one company's growth—it's about an entire industry's transformation, and Sky Gold's positioning at the nexus of this change.

As of FY23, the Indian jewellery retail sector is valued at approximately Rs 6.3 lakh crores ($76.3 billion) and is expected to grow at a CAGR of ~5.5% till 2027, reaching a market size of around Rs 7.8 lakh crores ($94.7 billion). These numbers are staggering, but they tell only part of the story. The real action is in the market share shift from unorganized to organized players.

The jewellery retail market in India has traditionally been dominated by the unorganised sector, comprised of small-scale jewellery retailers spread across the country. As of FY01, only 10% of India's retail jewellery market was captured by organised players, but this figure rose to 33% by FY22 and is expected to increase even further in the coming years.

This formalization is driven by multiple factors. GST implementation made it harder for unorganized players to compete on price through tax evasion. Hallmarking regulations ensure quality but require infrastructure that small jewellers can't afford. Consumer preferences are shifting toward branded jewellery with buyback guarantees and transparent pricing.

Estimates suggest that around 500 new stores will be established by just the top 5 jewellery retailers in the country over the next 3 to 5 years. Each new store is a potential revenue multiplier for Sky Gold. Unlike the retail business where new stores cannibalize existing ones, Sky Gold benefits from every square foot of organized retail expansion.

The competitive landscape in B2B jewellery manufacturing is surprisingly sparse. While there are thousands of jewellery manufacturers in India, very few operate at Sky Gold's scale with its combination of design capability, manufacturing capacity, and working capital strength. Most competitors are either small regional players serving local jewellers or large integrated players like Titan who manufacture primarily for their own retail networks.

Sky Gold's target is ambitious yet achievable: plans to expand its market share from 1% to 4-5% over the next five years. In a ₹6 lakh crore market, even single-digit market share represents massive absolute numbers. At 4% market share, Sky Gold would be generating revenues of over ₹20,000 crores—a 5x increase from current levels.

The regulatory environment continues to evolve in Sky Gold's favor. The recent India-UK trade agreement reduces duties on jewellery exports. Proposed labor reforms could formalize employment in the jewellery sector, disadvantaging small players who rely on informal labor. Even the push toward digital payments helps organized players who have the infrastructure to handle non-cash transactions.

X. Financial Analysis & Unit Economics

The financial story of Sky Gold is one of transformation—from a working capital-intensive, low-margin business to an increasingly efficient, cash-generative machine. Revenue: 3,956 Cr · Profit: 155 Cr represent the current scale, but the trajectory is what's truly impressive.

Gross margin up from 3% (FY20) to 7% (FY25). In a business where the primary raw material (gold) comprises 90-95% of the selling price, every basis point of margin improvement is hard-won. This improvement comes from three sources: design premiums for exclusive patterns, operational efficiency reducing gold loss, and scale benefits in procurement.

The working capital dynamics are fascinating. The traditional jewellery business requires massive working capital—you need to buy gold, hold it as inventory, convert it to jewellery, and then wait for payment from retailers. Sky Gold has systematically attacked each element of this cycle. GML (Gold Metal Loans) to gradually replace working capital debt. Gold metal loans are cheaper than cash credit, and more importantly, they hedge gold price risk.

PAT margin: 3.9% (Q1 FY26) → 4.5% by FY27. This might seem modest, but in the context of the jewellery industry, these are exceptional margins. Most B2B manufacturers operate at 1-2% PAT margins. Sky Gold's superior margins come from its design-led model, operational efficiency, and increasingly, the mix shift toward higher-margin products.

The cash conversion cycle has improved dramatically. Debtor days have increased from 29.7 to 46.5 days, which might seem negative, but this reflects the company's shift toward larger, more creditworthy clients who negotiate longer payment terms but never default. The trade-off is worth it—bad debts are virtually zero, and the cost of capital is more than offset by the premium pricing these clients pay.

Advanced gold at 6% of volumes, targets 10%+ by FY27. Improves margins, reduces capital employed. The advanced gold model is particularly clever. Retailers provide gold to Sky Gold, which converts it to jewellery for a fee. This eliminates working capital requirements and gold price risk while maintaining similar absolute margins. It's the jewellery equivalent of a software company moving from license sales to SaaS—lower revenue but higher return on capital.

The unit economics at the SKU level are compelling. Their Fast Moving Segment has an average ticket size of Rs. 50,000. At a 7% gross margin, that's ₹3,500 per piece. With Gold loss down to 0.5% and labor costs at roughly 1.5%, the contribution margin is around 5%. Given that the company can produce thousands of pieces daily, the absolute profit generation is substantial.

Capital allocation has been disciplined. Rather than pursuing vanity metrics like revenue growth at any cost, management has focused on profitable growth. Investments in design capabilities and ERP systems enhance margins. Acquisitions are evaluated on their ability to expand market reach or add capabilities, not just revenues. Even the dividend policy—modest but consistent—signals confidence without starving the business of growth capital.

XI. Playbook: Lessons for Founders & Investors

Sky Gold's journey offers a masterclass in building a B2B business in a traditional industry. The lessons extend far beyond jewellery, providing a template for anyone looking to disrupt established sectors through operational excellence rather than technological revolution.

Lesson 1: Find the Arms Dealers' Opportunity Sky Gold chose to supply the armies rather than fight the war. While everyone focused on retail—the glamorous, consumer-facing side of jewellery—Sky Gold built picks and shovels for the gold rush. 65% of the company's business comes from top-tier jewellery retail chains (corporates) in India. However, its clientele also includes smaller jewellery retail chains spread across the country. By serving multiple competing retailers, Sky Gold grows regardless of who wins the retail war.

Lesson 2: Design Velocity as a Moat In industries where the product is commoditized (gold is gold), the ability to create variety becomes the differentiator. Inhouse ~80 Member Design Team and ~2000-2500 designs being floated every month isn't just about having options—it's about making your customers' businesses more competitive. When a retailer can refresh their inventory monthly rather than seasonally, they capture more consumer interest and generate higher sales per square foot.

Lesson 3: The SME-to-Mainboard Arbitrage The migration from SME to mainboard isn't just a regulatory milestone—it's a value-unlocking event. Companies that can survive the obscurity of SME exchanges and demonstrate consistent growth become exponentially more valuable upon mainboard listing. The key is having the patience and capital structure to survive the waiting period.

Lesson 4: Operational Excellence in Traditional Industries Operational efficiency: employee productivity up, gold loss down to ~0.5% might not sound as exciting as artificial intelligence or blockchain, but in a ₹6 lakh crore industry, such improvements translate to hundreds of crores in value creation. Traditional industries reward those who can execute basics exceptionally well.

Lesson 5: Partnerships Over Direct Expansion Rather than opening retail stores—a capital-intensive, risky proposition—Sky Gold chose to partner with existing retailers. Sky Gold & Diamonds jointly with Senco Gold & Diamonds announced a significant step aimed at entering into collaboration for newly introduced 9kt gold jewellery segment shows this strategy continuing. Each partnership provides market access without the associated capital requirements and risks.

Lesson 6: Managing Commodity Volatility In businesses dealing with volatile commodities, financial engineering is as important as operational excellence. GML (Gold Metal Loans) to gradually replace working capital debt and the advanced gold model show how smart financing can transform unit economics. The goal isn't to bet on gold prices but to neutralize their impact on the business model.

XII. Bear vs Bull Case & Future Outlook

Bull Case: The Sky's the Limit

The optimistic scenario for Sky Gold rests on several powerful tailwinds that could drive sustained outperformance. First, the formalization of India's jewellery market is still in early innings. This figure rose to 33% by FY22, leaving enormous headroom for growth as organized retail continues to capture share from traditional jewellers.

Sky Gold and Diamonds envisions transforming into a globally dominant, design-led jewellery powerhouse by FY27, with a targeted consolidated revenue of ₹7,600 crore. This isn't pie-in-the-sky thinking—it's backed by concrete expansion plans. Strategic plans include acquiring a Dubai subsidiary, targeting INR 5,400.00 crores revenue in FY26, and aiming for 650-700 kg monthly production volume by FY26 exit.

The export opportunity is particularly compelling. The company is leveraging favorable market conditions, including the recent India-U.K. trade deal, to explore export opportunities. With Indian jewellery gaining acceptance globally and Sky Gold's design capabilities providing differentiation, international markets could become a significant growth driver.

The Senco partnership for 9-karat jewellery opens up an entirely new customer segment. The new 9KT gold jewelry line is designed to appeal to Gen Z consumers and align with fast fashion trends. This could be the beginning of Sky Gold's transformation from a traditional jewellery manufacturer to a fashion-forward design house.

Strong execution track record provides confidence. FY25 P/E = 32.6× is rich, but reflects investor confidence in future earnings. FY26E P/E = 20.0× suggests strong earnings growth is beginning to catch up with valuation. FY27E P/E = 12.6× is in line with fair valuations for high-growth manufacturing firms, implying scope for re-rating as execution continues.

Bear Case: All That Glitters...

The skeptical view starts with valuation. After a massive run-up, the stock trades at premium multiples that embed significant execution expectations. Any disappointment in growth or margins could trigger a sharp correction.

Promoter holding has decreased over last quarter: -6.44% raises questions about insider confidence. While some selling might be for personal reasons, promoter stake reduction is never a positive signal, especially when the company is supposedly entering its highest growth phase.

Gold price volatility remains a perpetual risk. While Sky Gold has mechanisms to hedge operational exposure, sustained high gold prices could dampen consumer demand, affecting the entire value chain. The company's fortunes are ultimately tied to the health of the discretionary spending on jewellery.

Competition is intensifying. As the B2B jewellery manufacturing space becomes more lucrative, new entrants are inevitable. Large integrated players like Titan could backward integrate more aggressively. International players could enter India. Sky Gold's first-mover advantage in design-led B2B manufacturing won't last forever.

Working capital intensity remains high despite improvements. Debtor days have increased from 29.7 to 46.5 days shows that growth requires increasing capital commitment. In a downturn, this could create cash flow pressures.

The dependence on a few large clients is a structural risk. If Kalyan, Joyalukkas, or Malabar decide to backward integrate or shift suppliers, Sky Gold's revenues could face significant pressure. Client concentration, while efficient, creates vulnerability.

Future Catalysts: The Next Chapter

Several near-term catalysts could drive the next leg of Sky Gold's journey. The Dubai subsidiary establishment will provide concrete evidence of international expansion capability. The company plans to develop a 5,40,000 sq ft facility on this land to enhance its production capacity by 4.5 tons kg per month... business operations are expected to commence by 2027, upon completion of the necessary infrastructure and facility setup.

Lab-grown diamonds represent an unexplored opportunity. As consumer acceptance of lab-grown diamonds increases, Sky Gold could leverage its design capabilities and retail relationships to capture this emerging market.

A potential B2C brand launch, while not announced, seems logical. With deep understanding of consumer preferences from serving retailers, Sky Gold could create an online-first, design-led brand targeting millennials and Gen-Z consumers. The capital-light, high-margin D2C model could transform the company's economics.

The next two years will be crucial in determining whether Sky Gold is a structural winner or a cyclical beneficiary of favorable industry dynamics. The company's ability to execute on its ambitious targets while maintaining margins will separate the bulls from the bears.

XIII. Closing Thoughts & Key Takeaways

Sky Gold's transformation from a modest SME listing to a ₹4,000+ crore market cap company is more than a stock market success story—it's a blueprint for building in India's traditional sectors. The company proves that you don't need cutting-edge technology or venture capital backing to create exceptional value. Sometimes, operational excellence, strategic positioning, and perfect timing are enough.

The real genius of Sky Gold lies not in what it chose to do, but what it chose not to do. It didn't chase retail glamour. It didn't expand internationally prematurely. It didn't diversify into unrelated businesses. Instead, it focused maniacally on becoming the best B2B jewellery manufacturer in India, serving the organized retail segment with unmatched design variety and operational efficiency.

For investors, Sky Gold offers several lessons. First, the best investments often hide in plain sight, obscured by market segments (like SME exchanges) that institutional investors ignore. Second, businesses serving growing industries can compound wealth even without being industry leaders themselves. Third, operational improvements in traditional industries can drive tech-like returns without tech-like risks.

The democratization of designer jewellery—Sky Gold's core contribution—has broader implications. By enabling organized retailers to offer variety at scale, the company has made fashion jewellery accessible to millions of Indian consumers who previously had limited options. Every wedding, festival, and celebration in middle India now has access to designs that were once the preserve of metro cities.

Mangesh Chauhan, Managing Director, Sky Gold and Diamonds Limited said, "Our Q1 FY26 performance aligns with our vision of building a ₹7,600 crore enterprise by FY27. We're seeing strong traction in exports, product innovation, and client acquisition." This isn't just corporate speak—it's a reflection of a company that has found product-market fit and is now scaling aggressively.

The next phase of Sky Gold's journey will test whether the company can maintain its execution excellence while scaling 3-4x from current levels. The challenges are real: managing working capital at scale, maintaining design freshness with a larger base, and preserving culture and operational efficiency during rapid growth.

Yet, if the past is any indication, betting against the Chauhan brothers and their team would be unwise. They've navigated the transition from private to public, from SME to mainboard, from domestic to international, and from traditional to modern manufacturing. Each transition was executed with minimal disruption and maximum value creation.

For students of business, Sky Gold offers a masterclass in building moats in seemingly moat-less industries. In a business where the primary raw material is a globally traded commodity and the end product has existed for millennia, Sky Gold has created differentiation through design, speed, and relationships. It's a reminder that competitive advantages don't always come from patents or proprietary technology—sometimes, they come from doing ordinary things extraordinarily well.

The story of Sky Gold is ultimately a story about India's economic transformation. As the country formalizes, digitalizes, and modernizes, companies that bridge the old and new will create enormous value. Sky Gold isn't replacing traditional jewellers; it's enabling them to compete in a modern marketplace. It's not disrupting the industry; it's upgrading it.

As India marches toward becoming a $5 trillion economy, consumer discretionary spending on categories like jewellery will explode. The winners won't necessarily be those with the biggest advertising budgets or the most stores, but those who build the infrastructure—physical and digital—to serve this consumption efficiently. Sky Gold has positioned itself as a critical piece of this infrastructure.

The journey from ₹180 to over ₹4,000 crore market cap is impressive, but it might just be the beginning. If Sky Gold executes on its vision of becoming a global jewellery manufacturing powerhouse, serving not just Indian retailers but international markets, the next chapter could be even more remarkable than the last.

For now, Sky Gold remains a hidden champion—known to its retail partners and increasingly to savvy investors, but still largely unknown to the consumers who wear its designs every day. Perhaps that's exactly how a B2B business should be: invisible to end users but indispensable to the ecosystem. In that invisibility lies both its strength and its opportunity.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube