Sky Gold: The B2B Engine of the Indian Jewelry Renaissance

I. The Invisible Giant

Walk into any large organized jewelry showroom in India and you will be handed a narrative. The brand will tell you about purity, about hallmarking, about the legacy of the family that founded the chain, about the trust that has been earned over decades. What the brand will not tell you — because it is commercially inconvenient and emotionally deflating — is that it very likely did not make the piece in your hand. It bought it. From someone like Sky Gold.

This is the central, almost subversive thesis of the Sky Gold story: in the Indian jewelry value chain, the glamour and the economics live in completely different rooms. The glamour lives at the storefront, where retailers spend enormous sums on real estate, gold inventory, celebrity endorsements, and the theater of the showroom. The economics — the quiet, repeatable, scalable economics — live one step upstream, in the factory, where the actual gold is shaped into product. Sky Gold operates in that upstream room, and it has discovered something that the retailers, for all their brand equity, structurally cannot replicate: you can grow a manufacturing business at the speed of demand without bleeding capital into a thousand showrooms.

Consider the scale of the consumer-facing machine that Sky Gold quietly feeds. Industry estimates suggest that large branded retailers, including a giant like टाइटन Titan, outsource somewhere between 70% and 90% of their actual manufacturing to third-party makers.1 The retailer's genius is in trust, distribution, and brand. The manufacturer's genius is in design libraries, casting yields, turnaround time, and cost. These are different sports played on the same field, and over the last three years the manufacturer's sport has been compounding faster.

The numbers that frame this episode are almost difficult to believe. In the financial year ending March 2025, Sky Gold reported revenue of roughly ₹3,548 crore.2 One year later, in FY26, that figure had vaulted to approximately ₹6,295 crore — growth of around 103% in a single year — while net profit grew faster still, up roughly 228% year on year.3 This is not the growth profile of a sleepy supplier. This is the growth profile of a company catching a structural wave at exactly the right moment, with exactly the right model.

So the puzzle we want to solve across this episode is twofold. First: how did a Mumbai partnership firm, founded in the middle of the 2000s and casting traditional gold ornaments by hand, end up as the picks-and-shovels supplier to India's jewelry gold rush? And second, the harder question for any long-term investor: is the moat real, or is this simply a commodity job-shop enjoying a cyclical sugar high in a country that has never stopped loving gold? To answer both, we have to start where every good origin story starts — with a family, a workshop, and a bet.

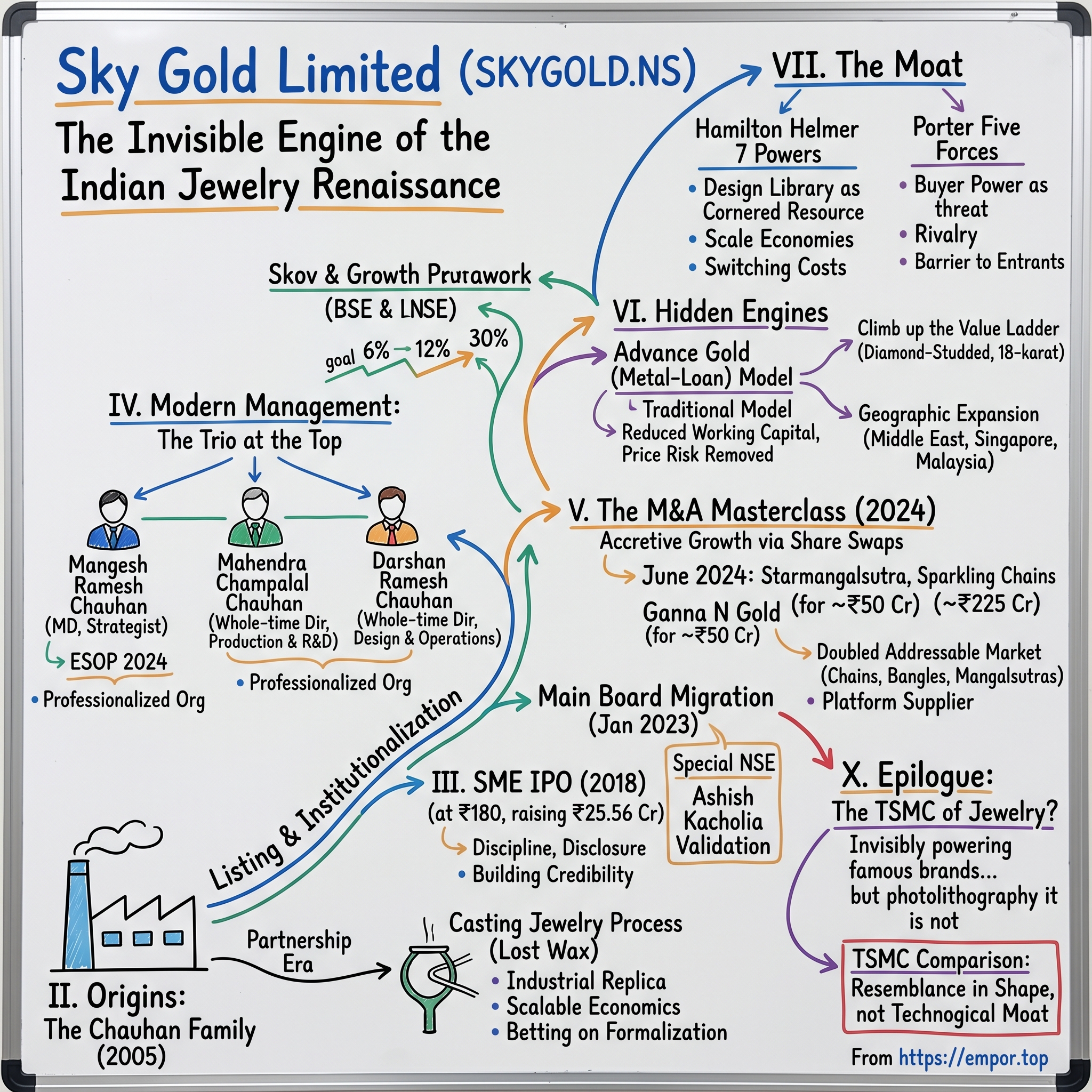

II. Origins: The Chauhan Family and the Partnership Era

Picture the lanes of Mumbai's jewelry manufacturing belt in the mid-2000s. This is not the polished world of air-conditioned showrooms. This is the back-of-house of the Indian gold economy: cramped workshops with the smell of solder and the hiss of blowtorches, artisans called karigars hunched over benches, rubber moulds and wax trees and trays of half-finished ornaments, and a culture of business conducted on relationships, trust, and word-of-mouth credit that had barely changed in a hundred years. It was, by any modern standard, gloriously unorganized — fragmented across thousands of tiny units, opaque on pricing, and entirely dependent on the personal reputation of the man at the bench.

Into this world, in 2005, the चौहान Chauhan family set up a partnership firm with a deceptively simple focus: कास्टिंग ज्वेलरी casting jewelry.4 To understand why that choice mattered, you need to understand what casting actually is, because it is the technical heart of this entire business. Traditional Indian goldsmithing was largely handmade — a karigar shaping each piece individually, a process that is beautiful, slow, and impossible to scale. Casting is the industrial alternative. You start with a master design, create a rubber mould from it, inject wax to produce exact replicas, assemble those wax models onto a "tree," encase the tree in plaster, melt the wax out, and pour molten gold into the cavity that remains. The result is dozens or hundreds of identical pieces from a single design, reproduced with consistency a human hand cannot match.

In layman's terms: casting is to handmade jewelry what the printing press was to the handwritten manuscript. It trades the romance of the individual artisan for the relentless, repeatable economics of reproduction. And in a country where demand for gold ornaments runs into hundreds of tonnes a year, reproduction at scale is where the volume — and eventually the money — lives.

The Chauhans were not, in those early years, doing anything that thousands of other Mumbai workshops weren't also attempting. What separated them was a reading of where the river was flowing. For most of independent India's history, jewelry retail was as fragmented as manufacturing — your jeweler was a neighborhood figure, a family you'd bought from for generations. But a megatrend was building. The organized, branded, multi-state retail chains were beginning their long march, consolidating a market that had been the exclusive preserve of the corner shop. As these chains grew, they would need something the corner jeweler never did: a reliable, high-volume, consistent, professional supply chain that could deliver thousands of designs on a corporate schedule.

The corner jeweler could call his cousin's workshop. A retailer opening fifty showrooms a year could not run a business on cousins. That gap — between the artisanal supply base that existed and the industrial supply base that organized retail would require — was the opportunity the Chauhans positioned themselves to fill. They were betting, in effect, not on gold, but on the formalization of the gold economy. It would take the better part of two decades for that bet to fully pay, but the direction was set early, and everything that followed is a story of building the capacity, the credibility, and the capital to ride a wave they could see forming before most others had felt the swell.

The first step in turning a workshop into an institution was to stop being a private family secret and start being a public company.

III. The First Inflection: Listing and Institutionalization

The Sky Gold partnership formally became a corporate entity when it was incorporated as Sky Gold Private Limited in May 2008, and it converted into a public limited company, taking the name Sky Gold Limited, in June 2018.5 That second date is the one that matters, because it set up the moment when this private family business stepped, somewhat nervously, onto a public stage.

In September 2018, Sky Gold launched its initial public offering — not on the glamorous main board, but on the BSE SME platform, the exchange's dedicated venue for small and medium enterprises. The offer opened on September 18 and closed on September 21, 2018, priced at ₹180 per share, raising roughly ₹25.56 crore through a fresh issue of about 14.2 lakh shares.6 By the standards of the company Sky Gold would later become, this was a rounding error — twenty-five crore is a sum it would one day generate in a matter of days of revenue. But the money was never really the point of an SME listing. The point was transformation.

The SME IPO did something to Sky Gold that no amount of internal ambition could have achieved on its own: it imposed discipline. A listed company, even on the SME board, must publish audited accounts, hold itself to disclosure norms, answer to outside shareholders, and submit to the cold scrutiny of a market price. Overnight, the family's casting workshop became a corporate supplier with a public report card. For a B2B business trying to win contracts with large, professionally managed retail chains, that report card was itself a marketing document. A purchasing head at a national jewelry retailer can sign a far larger order with a listed, audited, transparent manufacturer than with a private firm whose books are a black box. The listing, in other words, was less about raising capital and more about raising credibility — converting a relationship business into a reputation business.

The second, larger inflection came in January 2023, when Sky Gold migrated from the SME platform to the main boards of both the BSE and the नेशनल स्टॉक एक्सचेंज National Stock Exchange.7 If the SME IPO was the company learning to walk in public, the main-board migration was it learning to run. Main-board listing dramatically widens the universe of investors who are permitted, and willing, to own the stock — mutual funds, insurance companies, and the large institutional pools of capital that simply cannot or will not touch an illiquid SME ticker. It is the difference between fishing in a pond and fishing in the ocean.

And here is where a single name entered the Sky Gold story and changed its gravitational field: अशिश काचोलिया Ashish Kacholia, one of India's most closely watched small-cap investors, whose entry into a stock is treated by a certain segment of the retail market as a flare in the night sky. His association — held through the vehicle Bengal Finance and Investment, which appeared among the company's notable public shareholders with a stake of roughly 1.7% as of late 2024 — functioned as a powerful signal.8 The "Kacholia effect" is not really about the size of any one holding; it is about validation. When a respected institutional name plants a flag, the perceived risk of the business falls in the eyes of the broader market, the stock attracts research coverage and liquidity, and — crucially for a company that runs on capital — the cost of raising money drops. A business that can issue equity at a high valuation has, in effect, been handed a cheaper currency than its competitors. Hold that thought, because Sky Gold was about to spend that currency in spectacular fashion.

But cheap capital in the wrong hands destroys value. To understand why, in Sky Gold's hands, it compounded value instead, we have to meet the people holding the wallet.

IV. Modern Management: The Trio at the Top

Family businesses are graded, ultimately, on a single hard question: can the people who inherited the relationships also run the institution? At Sky Gold, the answer to that question lives in three men who share a surname and have, by design, split the company into three domains of responsibility.

At the top sits मंगेश रमेश चौहान Mangesh Ramesh Chauhan, the Managing Director and the closest thing the company has to a public face.4 Mangesh is the strategist and the capital allocator — the one who decides what the company buys, how it funds itself, and what story it tells the market. In the great divide of business leadership, between operators who optimize what exists and allocators who decide where the next rupee goes, Mangesh is firmly an allocator. The aggressive use of equity as an acquisition currency, the back-to-back fundraises, the public revenue targets that read as audacious even to bulls — these bear his fingerprints. His own shareholding, reported at roughly 17% of the company, makes him the single largest individual owner among the promoters and aligns his personal fortune directly with the share price he is so actively trying to compound.9

Beside him stands महेंद्र चंपालाल चौहान Mahendra Champalal Chauhan, a Whole-time Director and, in the internal mythology of the company, the production and R&D mind.4 If Mangesh decides where the company should go, Mahendra is responsible for the machinery that gets it there. The shift this business has made — from artisanal casting to CNC machining, 3D printing of master models, and the engineering of higher casting yields that lose less precious metal in production — is the kind of unglamorous, technical, margin-determining work that an operations leader either masters or fumbles. Gold loss during manufacturing is not a footnote in this industry; it is the difference between a profitable order and a loss-making one, because the raw material is, quite literally, gold. A factory that loses fractionally less metal per kilogram cast is structurally more profitable, order after order, forever.

The third brother, दर्शन रमेश चौहान Darshan Ramesh Chauhan, also a Whole-time Director, anchors design and operations — the daily rhythm of the floor and the creative library that, as we will see, is one of the company's genuine competitive assets.4 Three brothers, three domains: capital, production, design. It is a clean division of labor, and its cleanliness is part of what allowed the company to move as fast as it did without tripping over the internal politics that paralyze so many family firms.

But three brothers cannot personally cast 1,200 kilograms of gold a month, and here Sky Gold made a telling decision. In 2024 it introduced an Employee Stock Option Plan, the ESOP 2024 scheme, granting an initial tranche of 38,839 options to employees at an exercise price of ₹10 with a one-year vesting period.10 On its face this is a small, almost token grant. In substance, it signals something larger: the deliberate transition from a purely family-run shop, where loyalty was assumed and ownership was a birthright, to a professionalized organization that must attract and retain talent the modern way — by making employees owners. For a business whose entire growth thesis depends on scaling operations and engineering capability faster than competitors, the ability to keep good people is not a soft HR concern. It is a hard operational moat.

The other defining feature of this management team is its obsession with lean cost. Sky Gold runs on famously thin operating overheads relative to traditional competitors, a structure that lets it accept the wafer-thin margins of high-volume B2B work and still earn an attractive return on the capital it deploys. We will return to those margins, because they are both the company's discipline and its vulnerability. For now, the point is cultural: this is a management team that has chosen to win on efficiency and capital deployment rather than on brand or pricing power. And the single clearest expression of that choice was the acquisition spree that turned 2024 into the most consequential year in the company's history.

V. The M&A Masterclass: Accretive Growth

Every so often a company finds itself holding a tool so powerful that the only real risk is failing to use it. In mid-2024, Sky Gold was holding exactly such a tool — a richly valued, highly liquid, freshly main-board-listed equity currency — and it proceeded to use it with a precision that deserves to be studied.

The blitz began in June 2024. Sky Gold's board approved the 100% acquisition of two privately held manufacturers, Starmangalsutra Private Limited and Sparkling Chains Private Limited, completing the deals on June 22, 2024.11 Starmangalsutra was acquired for roughly ₹23.98 crore and Sparkling Chains for about ₹26 crore — and critically, both were paid for not in cash but through a share swap, with Sky Gold issuing its own equity to the sellers.12 Together, the two targets added approximately 300 kilograms per month of production capacity, lifting Sky Gold's total to around 1,050 kilograms per month.13 A third transaction followed in the same campaign: the acquisition of the Ganna N Gold business, in a share-swap deal valued at approximately ₹225 crore, extending the company's reach into chains and bangles.14

Now, to the untrained eye, a company issuing fresh shares to buy other companies looks like dilution — existing owners giving up a slice of the pie. To understand why these deals were, in fact, a masterstroke for Sky Gold's public shareholders, you have to look at the arithmetic of the swap, and it is genuinely elegant.

Sky Gold's own stock, in 2024, traded at a rich multiple — on the order of forty times earnings, the kind of valuation the market awards to a fast-growing favorite. The private companies it was acquiring, by contrast, were valued in these transactions at a tiny fraction of that — figures in the neighborhood of low-single-digit multiples of their earnings.1 Think carefully about what that means. Sky Gold was printing a currency the market valued at forty, and using it to buy earnings priced at, say, three. Every rupee of profit it absorbed from the targets was, the instant it landed inside the listed company, re-rated by the market to Sky Gold's own lofty multiple. This is the financial equivalent of buying gold bars with Monopoly money that everyone has agreed to treat as real — except here the Monopoly money was real, and the gold bars were genuine earnings. The transaction is accretive: earnings per share go up, not down, despite the new shares issued, because the earnings bought were so much cheaper than the currency used to buy them.

There is, of course, a sharp and fair objection lurking here — and any serious investor should sit with it rather than wave it away. The companies Sky Gold acquired were, in several cases, connected to the promoter family and its circle. Related-party acquisitions are one of the classic ways minority shareholders in family-controlled businesses get quietly fleeced: the family sells its private assets to the public company at inflated prices, transferring wealth from outside investors to insiders. So the question is not academic. Did the Chauhans overpay themselves at public shareholders' expense?

The defense, on the numbers available, is that the deals were struck at low multiples that flattered the buyer rather than the seller — the opposite of the usual abuse — and that they delivered immediate, tangible capacity and product breadth. But the honest verdict is that this is precisely the kind of arrangement a diligent shareholder must keep watching, because the same mechanism that created value here could, with different pricing, destroy it later. Related-party M&A is a tool that cuts in whichever direction the controlling family points it.

What the blitz unambiguously achieved, however, was strategic transformation. Before these deals, Sky Gold was essentially a casting specialist, and casting addresses only a slice of what a jewelry retailer needs to buy — by the company's own framing, roughly a third of the total opportunity. Chains, bangles, and mangalsutras are made by different processes and had sat outside Sky Gold's reach. By absorbing makers of exactly those categories, the company roughly doubled its addressable market in a single quarter, moving from supplying one product family to supplying most of what a retailer puts in its display case.1 In one stroke, Sky Gold went from being a specialist vendor a retailer calls for certain items to a one-stop manufacturing partner a retailer can lean on for the bulk of its catalog. That shift — from component supplier to platform supplier — is worth far more than the kilograms of capacity alone, because it deepens the company's hold on every customer it serves.

To fund the cash needs and balance sheet that this larger ambition required, the company turned back to the capital markets — and to a new, more sophisticated way of making money that has nothing to do with the price of gold at all.

VI. Hidden Engines and the Advance Gold Model

The most important thing to understand about a traditional gold manufacturer is that it is, whether it likes it or not, a leveraged bet on the gold price. The maker buys gold to turn into product. Between the day it buys the metal and the day it sells the finished piece, the price of gold can move — and because the value of the metal dwarfs the value of the labor that shapes it, even a modest swing in the gold price can swamp the entire profit on an order. The manufacturer's real skill — making beautiful, consistent jewelry efficiently — gets drowned out by the noise of a commodity it cannot control. It is like running a bakery whose profits depend less on the bread you bake than on hourly bets on the wheat market.

Sky Gold's answer to this problem is the single most strategically interesting thing about the company, and it goes by an unassuming name: the "advance gold," or gold-metal-loan, model. The mechanism is simple to describe and profound in its consequences. Instead of Sky Gold buying the gold itself, the customer — or a bank acting on the customer's behalf — supplies the physical metal to the factory. Sky Gold takes that gold, transforms it into finished jewelry, and books as revenue only the मेकिंग चार्जेस making charges — the fee for its labor, design, and craftsmanship. The gold never sits on Sky Gold's books as a price risk. The bakery, in this analogy, has been handed the flour for free and now simply charges for the baking.

The implications ripple outward in every direction. First, it strips out gold-price volatility, transforming an unpredictable commodity-linked business into something far closer to a pure manufacturing-services fee. Second, it dramatically reduces the working capital the company must tie up in inventory, because it is no longer financing a warehouse full of gold. Third — and this is the part the market cares about most — the reported margin profile improves, because the revenue line strips out the pass-through cost of metal and reflects more purely the value-added work. The advance gold share of Sky Gold's volumes climbed from under 6% in FY25 to roughly 11–12% in FY26, and management has spoken of pushing it toward 30% by the end of the decade.3 Each percentage point of that shift makes the business a little less of a commodity play and a little more of a services platform.

Running alongside this is a deliberate climb up the value ladder. Historically, Sky Gold's output was overwhelmingly plain 22-karat gold ornaments — the staple of the Indian market, but also the lowest-margin, most undifferentiated work. The company has been steadily pushing into higher-value categories: 18-karat jewelry, 9-karat pieces, and especially diamond-studded and stone-set designs, where the craftsmanship premium — and therefore the margin — is far richer. This "studding" work is more technically demanding and harder for a low-end competitor to replicate, which is exactly why it is attractive. The studded and value-added share remains modest, on the order of low single digits of sales as of FY26, which is precisely the point for a bull: it is a lever the company has barely begun to pull.3 The cumulative effect of these mix shifts showed up in the gross margin, which expanded from roughly 7.1% in FY25 to about 8.5% in FY26 — driven, management said, by lower gold loss, the rising advance-gold share, and the move into value-added products.15 In a business that runs on net margins of four-and-a-half percent, a 140-basis-point improvement in gross margin is not a rounding error; it is a meaningful share of the entire profit pool.

The third hidden engine is geographic. Sky Gold has been building an export business — to the Middle East, with Dubai as a hub, and to markets including Singapore and Malaysia — that rose to roughly 11–12% of revenue in FY26, up from a smaller base the prior year, with management targeting a materially higher share over the coming years.3 Exports matter for more than just incremental volume. They diversify the company away from a single domestic demand cycle, they often carry the value-added and advance-gold characteristics that lift margins, and they reposition Sky Gold from an Indian supplier into a node in a global jewelry supply chain — a manufacturer that international brands and retailers can plug into, not just a vendor to the home market.

Funding all of this expansion required fresh capital, and in October 2024 Sky Gold raised approximately ₹270 crore through a qualified institutional placement, drawing in marquee institutional names including Motilal Oswal's small-cap fund, Kotak Mahindra Life Insurance, and Bank of India's flexi-cap fund.16 A QIP is a fast, institution-only equity raise, and the quality of the names that participated was itself a second round of validation — sophisticated investors writing real checks at a real price. Around the same time, the company rewarded existing holders with a dramatic 9-for-1 bonus issue, handing nine new shares for every one held, with a record date in December 2024.17 A bonus issue creates no new value on its own — it simply slices the same pie into more pieces — but it lowers the per-share price, widens the shareholder base, and is, frankly, a confidence signal a management team sends when it believes the growth runway justifies a bigger float. Both moves, the QIP and the bonus, are the actions of a company treating its own equity as a strategic instrument rather than a static fact.

All of which raises the question every durable-business analysis must eventually confront: behind the financial engineering and the clever model, is there an actual moat?

VII. The Moat: Seven Powers and Five Forces

Let us war-game this business honestly, using the two frameworks every serious operator keeps in a back pocket: Hamilton Helmer's 7 Powers and Michael Porter's Five Forces. The temptation with a fast-growing stock is to assume the growth is the moat. It is not. Growth is the prize; the moat is whatever lets you keep the prize. So where, specifically, are Sky Gold's defenses — and where are the gaps in the wall?

Start with the strongest claim: the cornered resource. Sky Gold's most genuinely defensible asset is its design library — by its own description, on the order of hundreds of thousands of unique designs — combined with the accumulated process knowledge of casting at high yield and the CNC and 3D-printing workflows that turn a sketch into a sellable master in a fraction of the traditional time.1 A design library is a peculiar kind of asset: it is cheap to store, expensive and slow to build, and it compounds. Every season of designs a retailer's customers respond to feeds back into the catalog, making the next pitch to the next retailer richer than the last. A new entrant cannot buy two decades of accumulated, market-tested designs at any price; it has to live them. That is the textbook definition of a cornered resource.

Next, switching costs. Once Sky Gold is wired into a large retailer's procurement — understanding its design preferences, its quality tolerances, its delivery cadence, its seasonal ordering rhythms — it becomes inconvenient to rip out. The integration is not as hard-coded as enterprise software, so one should be careful not to overstate it; a retailer can and does multi-source. But the practical friction of re-qualifying a new manufacturer, re-establishing trust on gold purity and delivery reliability, and re-building the design dialogue is real, and it rises with the breadth of categories a single supplier covers. This is precisely why the M&A push into chains, bangles, and mangalsutras matters strategically: the more of a retailer's catalog Sky Gold supplies, the more entangled — and the stickier — the relationship becomes.

Third, scale economies. The expanded Navi Mumbai facility, which lifted capacity into the range of 1,200 kilograms per month, gives Sky Gold the ability to absorb very large orders from very large customers — orders that a small workshop simply cannot fulfill on time.1 In a business where a national retailer needs reliable, high-volume delivery on a corporate calendar, scale is itself a qualification to bid. Bigger plants also spread fixed costs across more kilograms and, combined with lower gold loss, drive the unit economics that let Sky Gold thrive on margins that would starve a less efficient rival.

Now the harder reckoning, through Porter's lens. Buyer power is the obvious threat: Sky Gold sells to a concentrated set of large, sophisticated retailers who know exactly what manufacturing costs and are entirely capable of squeezing a supplier or bringing production in-house. This is the central structural vulnerability of the whole model. Sky Gold's defense is design diversity and breadth — by offering an enormous range of designs across most product categories, it makes itself harder to replace and more valuable to keep than a single-trick vendor whose one product can be commoditized away. But let us be clear-eyed: in a B2B relationship between a small supplier and a large customer, the customer holds the better cards, and the supplier's job is to make itself too useful to discard. Supplier power, by contrast, is muted, because the dominant input — gold — is a globally traded commodity available to all, and the advance-gold model removes even the financing of it from Sky Gold's plate.

Rivalry is intense, and intellectually honest analysis demands we name it. India's jewelry manufacturing landscape is crowded, ranging from thousands of unorganized workshops to listed peers and the captive in-house manufacturing of giants like Titan and राजेश एक्सपोर्ट्स Rajesh Exports. Sky Gold's edge here is its position as a fast-moving, organized consolidator riding the formalization wave — but it does not have the market to itself, and price competition in commodity 22-karat casting is unforgiving. The threat of substitutes and new entrants is more comforting: the design library, the scale, the certifications, and the retailer relationships together raise the bar for a credible new competitor well above what a single ambitious workshop can clear. The barrier is not impregnable, but it is real and rising.

The synthesis is this: Sky Gold's moat is genuine but young, resting primarily on a cornered design resource, accumulating switching costs, and scale — while its principal exposure is the buyer power of a concentrated, powerful customer base. It is a moat in construction, not a moat completed. And the playbook the company is running is precisely an attempt to deepen it before the window closes.

VIII. Playbook: The Business and Investing Lessons

Step back from the specifics and the Sky Gold story resolves into a handful of durable lessons that travel far beyond jewelry.

The first is the enduring power of the picks-and-shovels position. In every gold rush — literal or metaphorical — the people who sell the picks and shovels often earn a steadier living than the prospectors. Sky Gold captured the tailwind of India's shift to organized, branded jewelry retail without taking on the brutal capital intensity of the retail business itself. It did not have to win the brand war, sign the celebrity, lease the high-street storefront, or finance a showroom's worth of gold inventory. It simply had to be the indispensable supplier to whichever brands won. When a structural megatrend is underway but it is unclear which consumer brand will capture it, owning the upstream supplier that serves all of them can be the higher-quality bet. The shovel-seller is agnostic to which prospector strikes it rich.

The second lesson is equity as a strategic currency, used while it is cheap. Sky Gold's management understood something many operators never internalize: a highly valued stock is not just a scoreboard, it is a tool. When the market hands you a forty-times multiple, you can buy earnings priced at a fraction of that and create value for existing shareholders in the very act of issuing new shares. The discipline lies in using that currency only for genuinely accretive purposes and only while the market is willing to grant the premium — because the same mechanism reverses brutally if the multiple compresses and the company still needs to raise. The art is in the timing and the price, and Sky Gold's back-to-back swaps, QIP, and bonus issue show a management team treating its capital structure as an active lever rather than a passive constraint.

The third lesson is technology as the quiet differentiator in an "old" industry. Jewelry is one of the oldest businesses on earth, drenched in tradition and sentiment, and it is exactly the kind of industry where outsiders assume nothing can change. Yet Sky Gold's edge is substantially a technology edge — the migration from the individual artisan's hand to CNC machining, 3D-printed masters, and process engineering that squeezes out gold loss kilogram by kilogram. In a low-margin, high-volume business, these are not incremental niceties; they are the entire difference between a profit and a loss. The broader lesson is that the most durable advantages in unglamorous industries often come from importing discipline and technology from outside the industry's own traditions, and applying them where incumbents are too sentimental or too sleepy to bother.

The fourth, more subtle lesson is about moving up the value chain before the commodity tide forces you to. The advance-gold model and the studded-jewelry push are both attempts to escape the gravitational pull of pure commodity casting before margins are competed to the bone. The most dangerous place to be in any business is the undifferentiated middle, where you compete only on price. Sky Gold's strategy is a continuous attempt to climb out of that middle — toward fee-based services, toward higher-value products, toward export markets — and the investor's job is to watch whether it keeps climbing or slides back. That tension between the comfortable commodity volume of today and the harder-won, higher-margin business of tomorrow is exactly the terrain on which the bull and bear cases are fought.

IX. Myth vs. Reality: The Bull and Bear Case

Before weighing the two sides, it is worth puncturing one piece of received wisdom, because the company's own ambition has outrun the early narrative. The story circulated for a time that Sky Gold was a company chasing a ₹5,000 crore revenue target by 2027 — an aim that, when first floated, sounded aggressive. Reality has overtaken the myth: the company crossed roughly ₹6,295 crore in FY26 itself, and management has publicly guided to approximately ₹8,100 crore in FY27, with a far longer-range ambition of ₹18,000–19,000 crore by FY30.3 The relevant debate is no longer whether a modest target is reachable; it is whether a wildly more aggressive one is, and whether the margins can hold as the top line explodes. That reframing is the right way into the bull and bear cases.

The bull case begins with the runway. Capacity utilization in FY26 sat at only around 55% — roughly 650 kilograms a month against installed capacity of about 1,200 kilograms — which means the company can nearly double output from existing assets before it needs to pour concrete for new ones.3 That is operating leverage waiting to be harvested: revenue can grow substantially while fixed costs barely move, and profit grows faster than sales. Layer on the structural tailwind of an Indian jewelry market still consolidating from unorganized workshops toward organized players that outsource manufacturing, and Sky Gold is positioned in the fastest-formalizing slice of a very large pie. Then add the three margin levers we have already examined — the rising advance-gold share, the climb into studded and 18-karat product, and the export mix — each of which pushes the blended margin upward from today's thin base. The bull's thesis is that revenue growth, operating leverage, and margin expansion stack on top of one another, which is precisely the recipe behind a net profit that grew more than three times faster than revenue in FY26. A management team that has consistently met or beaten its own aggressive guidance earns, for now, the benefit of the doubt.

The bear case is equally coherent and deserves equal airtime. Start with the margin itself: a net margin of around 4.5% leaves almost no cushion.3 This is a high-volume, low-margin business in which a small adverse move — a spike in gold loss, a pricing concession to a big customer, a misjudged inventory position — can erase a meaningful share of profit. Razor-thin margins magnify every operational error. Second, customer concentration: selling to a handful of large retailers means the loss, or the hard bargaining, of even one major client could leave a visible dent, and as those retailers grow they may choose to manufacture more in-house, turning today's customer into tomorrow's competitor. Third, regulatory and commodity exposure: this is a business conducted at the mercy of government policy on gold — import duties set in the केंद्रीय बजट Union Budget, hallmarking rules, and the broader monetary backdrop that drives gold prices and, with them, consumer demand. A sharp adverse policy shift or a demand shock can ripple straight through the order book. Fourth, the related-party question we flagged earlier remains a live governance watch-item; the acquisitions that looked accretive must continue to be priced in minority shareholders' favor, not the family's. And fifth, execution risk at the guided pace: tripling revenue toward the FY30 ambition demands flawless operational scaling, working-capital management, and capital discipline, with little room for the stumbles that almost always accompany hyper-growth.

How, then, should a long-term investor actually monitor whether the bull or bear case is winning, without drowning in quarterly noise? Three key performance indicators carry most of the signal. The first is the advance-gold (gold-metal-loan) share of volumes — the single cleanest gauge of the shift from commodity manufacturer toward a higher-margin, lower-risk services model. If that number keeps climbing toward management's stated ambition, the moat is deepening; if it stalls, the business stays a commodity. The second is gross and net margin, watched together — the direct scoreboard for whether the climb up the value chain is real or merely talked about. And the third is capacity utilization, the truest measure of demand health and operating leverage: rising utilization means the growth is being fed by real orders rather than by speculative capacity, and it tells you how much runway remains before the next expansion cycle. Track those three, and the rest of the story largely tells itself.

X. Epilogue: The TSMC of Jewelry?

Return, for a moment, to the workshop in the Mumbai lanes — the solder and the blowtorches, the karigars at the bench, the rubber moulds and the wax trees. The remarkable thing about the Chauhan brothers' journey is not that they made jewelry; thousands of families in those same lanes have made jewelry for generations. It is that they looked at the most traditional, most sentimental, most relationship-bound corner of the Indian economy and saw, underneath the romance, an industrial supply-chain problem waiting to be solved at scale. They bet on formalization before it was obvious, built the credibility of a public company before they needed the capital, used that capital to consolidate before the window closed, and engineered their way out of commodity risk before the margin tide could pull them under.

The provocative comparison floated around this company is that Sky Gold is the "TSMC of jewelry" — a reference to 台積電 TSMC, the Taiwanese contract chipmaker that became indispensable by manufacturing the world's most advanced semiconductors for brands that design but do not fabricate. It is a flattering analogy, and it is worth holding up to the light honestly. The resemblance is real in shape: both are upstream, both are invisible to the end consumer, both make the thing the famous brand sells, and both win by being the supplier everyone depends on. But the analogy strains where it matters most. TSMC's moat is built on a technological lead measured in billions of dollars and years of process superiority that no customer can replicate — a genuine, near-unassailable cornered resource. Sky Gold's moat, real as it is, rests on a design library, accumulating switching costs, and scale in an industry whose barriers, while rising, are nowhere near as high as a leading-edge fab. Casting gold is hard; it is not photolithography.

So the honest verdict is not a grade and not a price. It is a frame. Sky Gold is a company that has executed an genuinely impressive strategic transformation — from a family casting shop into the organized manufacturing backbone of one of the world's great jewelry markets — and it is doing so on the back of a real structural tailwind and a clever, margin-aware model. Whether it becomes a durable compounding institution or remains a brilliantly-run, cyclically-exposed job-shop will be decided by the three things worth watching: the advance-gold mix, the margin trajectory, and the discipline with which a family-controlled company treats its minority shareholders as it scales. The bet the Chauhans made two decades ago — that the future of Indian jewelry belonged not to the loudest brand but to the most reliable supplier — has paid off beyond what anyone in those Mumbai lanes could have imagined. The next chapter will test whether the moat they have started to build can hold the prize they have already won.

References

-

Sky Gold deep dive — manufacturing model, clients, capacity and design library, Shankarnath (Substack), 2024 ↩↩↩↩↩

-

Sky Gold FY26 results: revenue ₹6,295 cr, PAT +228%, margins, advance gold, exports, FY27/FY30 guidance — Moneymuscle, 2026 ↩↩↩↩↩↩↩

-

Sky Gold IPO — promoters Mangesh, Mahendra and Darshan Chauhan; partnership origins and business — Chittorgarh, 2018 ↩↩↩↩

-

Sky Gold Limited — incorporation 2008, conversion to public limited company 2018 — Samco, 2018 ↩

-

Sky Gold IPO details — dates, ₹180 price, issue size, BSE SME listing — Chittorgarh, 2018 ↩

-

Sky Gold migration from BSE SME to main board of BSE and NSE, January 2023 — Screener.in ↩

-

Ashish Kacholia-backed Sky Gold — Bengal Finance stake and 9:1 bonus — Goodreturns, 2024 ↩

-

Sky Gold shareholding pattern and promoter holding — Moneycontrol ↩

-

Sky Gold grants 38,839 stock options at ₹10 under ESOP 2024 — ScanX, 2024 ↩

-

Sky Gold acquires 100% of Starmangalsutra and Sparkling Chains, completed June 22, 2024 — Business Standard, 2024-06-22 ↩

-

Sky Gold acquisition values — Starmangalsutra ₹23.98 cr, Sparkling Chains ₹26 cr, via share swap — India Retailing, 2024-06-24 ↩

-

Sky Gold acquires three companies to boost capacity to 1,050 kg per month — Business Standard, 2024-06-15 ↩

-

Sky Gold completes 100% acquisition of Ganna N Gold for ₹225 crore via share swap — Angel One, 2024 ↩

-

Sky Gold gross margin expansion to ~8.5% in FY26 from ~7.1% in FY25 — Moneymuscle, 2026 ↩

-

Sky Gold raises ₹270 crore via QIP with Motilal Oswal, Kotak Life, Bank of India funds — WebIndia123, 2024-10-23 ↩

-

Sky Gold 9:1 bonus issue, December 2024 record date — Goodreturns, 2024 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube