SJVN Limited: The Story of India's Renewable Energy Transformation

I. Introduction & Episode Roadmap

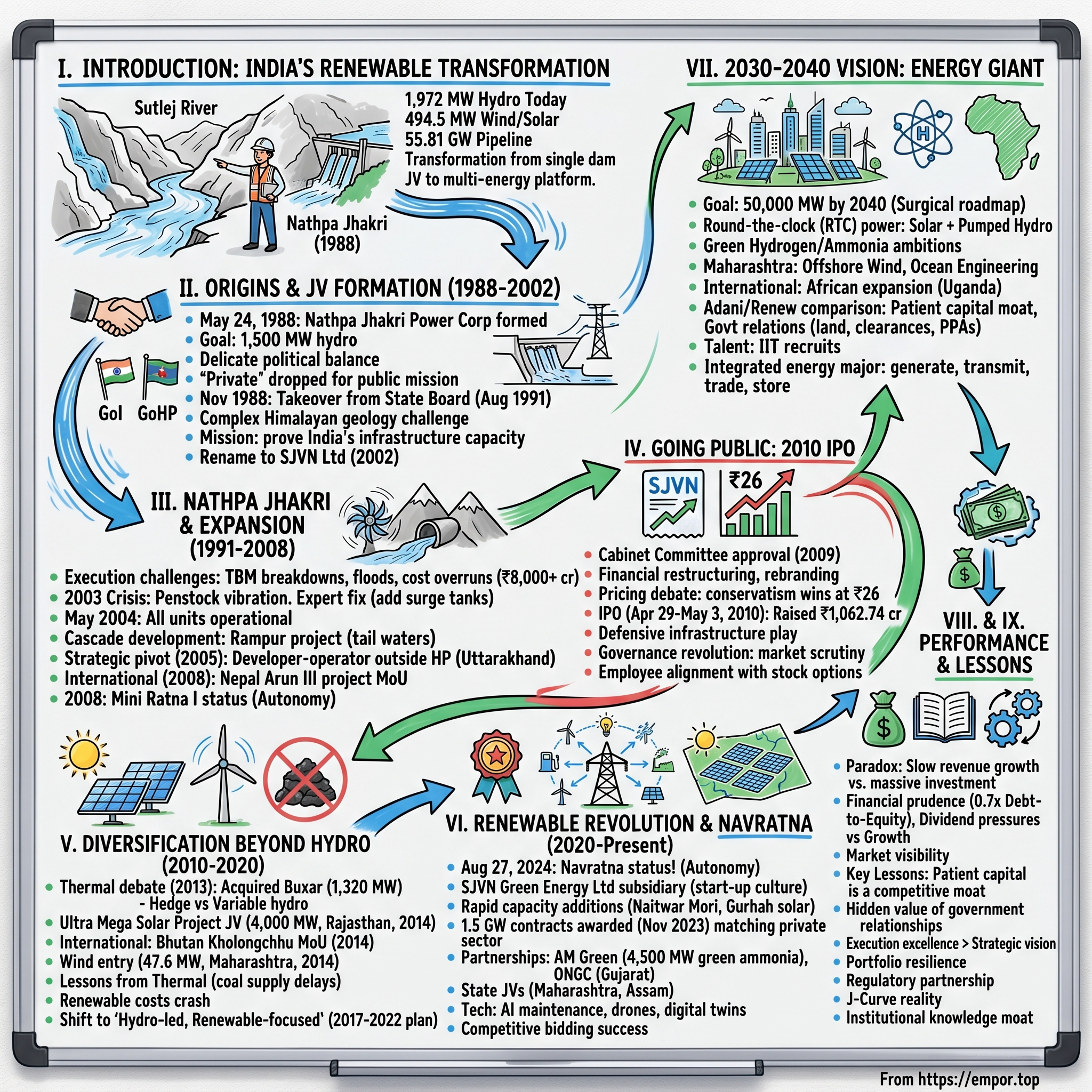

Picture this: A government engineer stands at the edge of the Sutlej River gorge in 1988, staring down at the rushing waters that would soon power millions of Indian homes. The Nathpa Jhakri project site stretches before him—raw earth, untamed river, impossible dreams. This is where SJVN's story begins, not in boardrooms or stock exchanges, but in the Himalayan valleys where India's energy future would be carved from rock and water.

Today, SJVN operates 1,972 MW of hydroelectric capacity and another 494.5 MW of wind and solar assets. The company that started as a single-dam joint venture between two governments has morphed into something far more ambitious: a 55.81 GW energy platform spanning hydro, solar, wind, and thermal power across multiple countries. It's a transformation that poses a fundamental question: How did a government hydropower company built for one mega project become India's renewable energy powerhouse?

The answer isn't just about dams and turbines. It's about how a public sector undertaking (PSU) navigated India's liberalization, survived private sector competition, and positioned itself at the center of the world's most ambitious renewable energy transition. It's about the peculiar advantages of patient government capital in an industry where projects take decades to mature. And it's about whether a company born in the license raj can compete in the age of Adani and Ambani.

This is that story—from the monsoon-fed rivers of Himachal Pradesh to the solar fields of Rajasthan, from a ₹26 IPO price to Navratna status, from 1,500 MW to chasing 50,000 MW. Along the way, we'll explore the playbook of government-led infrastructure development, the economics of power generation, and what SJVN's journey tells us about India's energy future.

II. Origins & Government Joint Venture Formation (1988-2002)

The year was 1988. India's power deficit stood at a staggering 8.8%, with peak shortages reaching 14.8%. Industrial growth was throttled by daily power cuts. In the northern states, the situation was particularly dire—factories ran on diesel generators, middle-class families planned their evenings around load-shedding schedules, and farmers watched their crops wither for lack of irrigation pumps. This was the India that birthed SJVN.

On May 24, 1988, the Nathpa Jhakri Power Corporation came into existence through a handshake between two governments. The Government of India and the Government of Himachal Pradesh each took equal stakes in what would become a template for cooperative federalism in infrastructure. The mandate was singular and audacious: harness the Sutlej River's 1,500 MW potential through what would become India's largest hydroelectric project.

But here's what made this joint venture unique—it wasn't just about building a dam. The structure reflected a delicate political balance. Himachal Pradesh, rich in hydro potential but poor in capital, needed central government resources. The center, desperate for power generation capacity, needed state cooperation for land, water rights, and local clearances. The 50-50 structure wasn't just equity; it was a political compact that would define how India approached mega infrastructure projects for decades.

By November 1988, barely six months old, the company made its first strategic move—dropping "private" from its name. This wasn't mere semantics. It was a declaration of intent. This would be a public mission, accountable to parliaments rather than profit margins. The renamed Nathpa Jhakri Power Corporation was positioning itself as the vehicle for India's hydroelectric ambitions.

The real action began in August 1991 when SJVN took over the Nathpa Jhakri construction from the Himachal Pradesh State Electricity Board. The state board had managed preliminary work since 1978, but the project's complexity demanded specialized expertise. Underground desilting chambers, a 27.4-kilometer headrace tunnel boring through the Himalayas, surge shafts descending 301 meters—this wasn't just construction; it was underground engineering at a scale India had never attempted.

Consider the context of early 1990s India. The economy had just opened up. Private players were eyeing infrastructure opportunities. Yet here was the government doubling down on public sector execution for its most critical power project. Why? Because private capital in 1991 India meant foreign capital, and foreign capital meant dollar-denominated debt for rupee revenues—a risk the government wouldn't take for strategic infrastructure.

The decade that followed was marked by relentless execution challenges. Tunnel boring machines broke down in the Himalayan geology. Monsoons flooded construction sites. Cost estimates ballooned from ₹2,475 crores to over ₹8,000 crores. Yet the project pressed on, driven by what insiders called "missionary zeal"—the belief that completing Nathpa Jhakri would prove India could execute world-class infrastructure.

By September 2002, as the first turbines neared commissioning, the company shed its project-specific identity. The transformation from Nathpa Jhakri Power Corporation to Satluj Jal Vidyut Nigam Limited signaled ambitions beyond a single dam. "Satluj" (Sutlej) represented the river basin approach. "Jal Vidyut Nigam" (Water Power Corporation) suggested a platform for multiple projects. The foundation was set for what would become India's hydroelectric champion.

III. The Nathpa Jhakri Mega Project & Expansion (1991-2008)

The morning of October 2003 should have been a celebration. After twelve years of construction, the first 250 MW unit of Nathpa Jhakri was ready for synchronization. Instead, engineers huddled around control panels, watching pressure readings spike dangerously. The penstock—the massive pipe carrying water to the turbine—was vibrating at frequencies that threatened catastrophic failure. This was SJVN's darkest hour, with ₹6,000 crores already spent and the nation watching.

What followed was a masterclass in crisis management that rarely makes it into corporate histories. SJVN flew in specialists from Switzerland, Norway, and Canada. For six months, teams worked round-the-clock to redesign the hydraulic system. The solution—installing additional surge tanks and pressure relief valves—added ₹400 crores to the budget but saved the project. By May 2004, all six units were operational, delivering 1,500 MW to the northern grid.

The numbers tell one story: 1,500 MW capacity, 6,950 million units annual generation, feeding five states. But the human story was equally remarkable. Over 15,000 workers had lived in purpose-built colonies in Jhakri and Rampur for over a decade. Engineers' children grew up attending schools built for the project. A micro-economy emerged in the valleys—from mess contractors to equipment suppliers. Nathpa Jhakri wasn't just a power plant; it was a city built for a singular purpose.

Success at Nathpa Jhakri triggered immediate expansion. In 2004, the government allocated the Luhri project, and SJVN signed implementation agreements for Rampur—a 412 MW project that would use Nathpa Jhakri's tail waters. This cascading development model was brilliant engineering: one project's outflow became another's input, maximizing river utilization without additional environmental impact.

But 2005 marked a strategic pivot that would define SJVN's future. The company ventured beyond Himachal Pradesh, securing three projects in Uttarakhand on a Build-Own-Operate (BOO) basis. The Devsari (252 MW), Naitwar Mori (60 MW), and Jakhol Sankri (44 MW) projects represented a new model—SJVN as developer-operator rather than just government contractor. This shift required new capabilities: land acquisition expertise, environmental clearance navigation, and critically, the ability to negotiate Power Purchase Agreements (PPAs) with multiple state utilities.

The international opportunity came knocking in 2008. Nepal's 900 MW Arun III project had defeated global developers for two decades—the World Bank had withdrawn support in 1995, calling it too risky. When SJVN signed the MoU in March 2008, skeptics called it foolhardy. A Indian PSU succeeding where the World Bank failed? Yet SJVN's leadership saw what others missed: Nepal's hydro potential was similar to Himachal's, the geology was familiar, and most importantly, India's power deficit meant guaranteed offtake for any electricity generated.

Recognition came that same year when the government granted SJVN Mini Ratna Category I status. This wasn't just a certificate; it was operational autonomy. The board could now approve projects up to ₹500 crores without government clearance, make technology decisions independently, and most critically, retain and deploy surplus cash for expansion. For a capital-intensive business like hydro power, this financial flexibility was transformative.

By 2008's end, SJVN's portfolio had expanded from one operational project to a pipeline of 5,000 MW across multiple states and countries. The company had proven it could execute India's most complex infrastructure project and was ready for its next transformation—from government department to public market entity.

IV. Going Public: The 2010 IPO & Market Entry

The PowerPoint slide that convinced the Cabinet Committee on Economic Affairs in 2009 was remarkably simple. It showed two lines: India's projected power demand climbing steeply upward, and generation capacity struggling to keep pace. The gap—shaded in red—represented not just an infrastructure challenge but an investment opportunity worth hundreds of billions. SJVN's IPO would be the government's way of inviting public participation in bridging that gap.

The transformation began in September 2009 when Satluj Jal Vidyut Nigam became SJVN Limited—dropping the Hindi nomenclature for a crisp, market-friendly identity. Behind this rebranding was a year of preparation: financial restructuring to clean up government receivables, corporatization of HR policies, and most importantly, creating an equity story that would resonate with retail investors who had never bought infrastructure stocks.

The IPO roadshow in April 2010 was unlike anything India's capital markets had seen from a PSU. Instead of bureaucrats reading prepared statements, SJVN's leadership team—led by CMD H.K. Sharma, a career power engineer—spoke passionately about India's energy future. They didn't just sell shares; they sold a vision of cascade development on the Sutlej, run-of-river projects that didn't require large reservoirs, and 30-year PPAs that guaranteed returns.

The pricing decision sparked intense debate. Investment bankers pushed for ₹30-32 per share, pointing to private power companies trading at higher multiples. But the government, burned by previous PSU IPO failures, insisted on ₹26—a price that left something on the table for retail investors. This wasn't just conservatism; it was strategic positioning. The government wanted SJVN's IPO to restore faith in PSU offerings after the NHPC debacle just months earlier.

From April 29 to May 3, 2010, the IPO window opened. The response was measured but positive—institutional investors bid 2.8 times, retail 1.4 times. Not the blockbuster oversubscription of private IPOs, but solid enough to raise ₹1,062.74 crores. The government's offer for sale of 10.03% equity achieved its dual objectives: raising capital for the fiscal deficit and creating public ownership in strategic infrastructure.

May 20, 2010, listing day, revealed the market's verdict. SJVN opened at ₹28 on the BSE—a modest 7.7% premium that actually pleased the government. Too high a pop would have meant leaving money on the table; too low would have signaled weak demand. The steady debut positioned SJVN as a defensive infrastructure play—not exciting, but dependable.

What most analyses missed was the governance revolution hidden in the IPO fine print. As a listed entity, SJVN now faced quarterly scrutiny from analysts, independent directors on its board, and minority shareholders who could question capital allocation. The government retained 89.97% (later diluted to 81.8%), ensuring control while accepting market discipline. This hybrid model—government control with market oversight—would become the template for PSU reform.

The immediate impact was cultural. Engineers who had spent careers focused on megawatts and plant load factors now tracked stock prices and PE ratios. The employee stock options, offered at IPO price, created alignment between project execution and market value. A power station commissioning ahead of schedule could now directly impact employee wealth—a capitalist incentive in a socialist structure.

By 2010's end, SJVN's market cap had stabilized around ₹11,000 crores, valuing the company at approximately ₹7 crores per MW of operational capacity. Expensive compared to thermal power but cheap versus private hydro developers. The market was essentially saying: we believe in the assets but need proof of execution beyond Nathpa Jhakri. That proof would come through a dramatic pivot that nobody saw coming—the entry into thermal power.

V. Diversification Beyond Hydro (2010-2020)

The boardroom in SJVN's Shimla headquarters erupted in rare discord in early 2013. On the table was a proposal that split the leadership: acquire a 1,320 MW thermal power project in Bihar's Buxar district. The hydro purists called it heresy—SJVN's DNA was clean, green hydroelectric power. The pragmatists saw reality: hydro projects took 8-10 years to build, faced increasing environmental opposition, and generated variable power depending on river flows. Thermal was dirty but dependable. After heated debate, pragmatism won.

The July 2013 acquisition of the Buxar Thermal Power Project from Nabha Power marked SJVN's most controversial strategic shift. The project came with 1,980 MW of coal linkage from Central Coalfields—a scarce resource that private players would kill for. Critics pointed to NTPC, India's thermal giant, and asked why SJVN was entering their territory. The answer lay in portfolio theory: thermal's steady baseload generation would complement hydro's seasonal peaks, creating a natural hedge.

But the real diversification bombshell dropped in January 2014. SJVN announced a joint venture with Rajasthan government entities for a 4,000 MW Ultra Mega Solar Project in the Thar Desert. From water to coal to sun—SJVN was rapidly transforming from a hydro specialist to an all-weather energy company. The JV structure was clever: SJVN brought project management expertise while Rajasthan provided land and state support, replicating the cooperative federalism model that birthed SJVN itself.

March 2014 brought validation of the core hydro strategy when the 412 MW Rampur project achieved commercial operation. Using Nathpa Jhakri's tail waters, Rampur added 1,770 million units annually at an incremental cost of just ₹2,800 crores—a fraction of greenfield project costs. The cascade development model was working, turning the Sutlej into India's most productive river per kilometer.

The international thrust accelerated in April 2014 when SJVN signed an MoU with Bhutan's Druk Green Power Corporation for the 600 MW Kholongchhu project. Unlike the Nepal adventure, Bhutan offered political stability and India-friendly policies. The project economics were compelling: Bhutan provided the site and water rights, India funded construction, and both shared the power generated. It was infrastructure diplomacy at its finest.

May 2014 marked entry into wind energy with the commissioning of the 47.6 MW Khirvere project in Maharashtra. Small by wind farm standards, Khirvere was significant for what it represented—SJVN's willingness to experiment with distributed generation. Wind sites could be developed in 18 months versus hydro's decade-long gestation, providing quick wins while mega projects matured.

The transformation wasn't without casualties. The thermal foray proved particularly challenging. Coal supply disruptions, environmental clearance delays, and local protests pushed Buxar's commissioning timeline from 2017 to beyond 2020. By 2015, with coal block auctions making fuel supply uncertain, SJVN quietly shelved thermal expansion plans. The experiment had taught valuable lessons about sticking to core competencies.

Meanwhile, renewable energy was becoming impossible to ignore. Solar prices crashed from ₹15/kWh in 2010 to ₹4/kWh by 2016. Wind technology improved dramatically, with capacity utilization factors jumping from 20% to 35%. The government announced ambitious targets: 175 GW of renewable capacity by 2022. SJVN's leadership recognized the shift—the future wasn't in fossil fuels but in renewables backed by hydro's storage potential.

The strategic pivot crystallized in the 2017-2022 corporate plan. SJVN would remain "hydro-led" but become "renewable-focused." The target: 5,000 MW by 2023, with significant solar and wind components. Thermal would complete but not expand. International projects would accelerate. The transformation from single-technology to multi-technology platform was complete.

By 2020, SJVN operated assets across the energy spectrum: 1,972 MW hydro, 97.6 MW solar, 47.6 MW wind, and thermal under construction. Revenue had diversified from pure generation to include consultancy services, where SJVN's project execution expertise commanded premium fees. The company that started with one river and one technology had become India's most diversified public sector power producer.

VI. The Renewable Revolution & Navratna Status (2020-Present)

The WhatsApp message that pinged across SJVN leadership phones on August 27, 2024, contained just two words and an emoji: "Navratna confirmed 🎉". After a four-year campaign involving countless presentations, ministry meetings, and performance reviews, SJVN had joined India's elite club of PSUs with enhanced autonomy. But the real revolution had already been underway since 2020, hidden in project sites across India where SJVN was quietly building the country's renewable energy future.

The transformation began with an organizational restructuring that would have been unthinkable in the old PSU culture. In 2022, SJVN created SJVN Green Energy Limited, a wholly-owned subsidiary focused exclusively on solar and wind projects. This wasn't just corporate reorganization—it was cultural revolution. The subsidiary operated like a startup within a PSU: faster decision-making, performance-linked incentives, and critically, recruitment from private renewable developers who brought market expertise.

The numbers tell the acceleration story. Between 2020 and 2024, SJVN added more renewable capacity than in its entire previous history. The December 2023 commissioning of the 60 MW Naitwar Mori hydro project in Uttarakhand and the 75 MW Gurhah solar project in Jammu & Kashmir happened within weeks of each other—a feat of simultaneous execution across different technologies and terrains that showcased newfound project management maturity.

But the real shock came in November 2023 when SJVN announced it had awarded 1.5 GW of renewable energy contracts to seven firms at ₹4.38-4.39/kWh. The scale was staggering—equivalent to an entire Nathpa Jhakri project but in solar and wind. More importantly, the tariff discovery through competitive bidding proved SJVN could match private sector efficiency. The old criticism of PSUs overpaying for everything was being systematically demolished.

The June 2024 partnership with AM Green represented SJVN's boldest bet yet. The MoU for 4,500 MW of carbon-free energy wasn't just about electrons—it was about green hydrogen, green ammonia, and the entire value chain of tomorrow's energy economy. AM Green brought electrolyzer technology and international market access; SJVN brought land, permits, and critically, the government backing that made 25-year investments feasible.

Navratna status unleashed capabilities that had been bottlenecked for years. The board could now approve projects up to ₹1,000 crores independently, enter joint ventures without government approval, and most importantly, raise capital through bonds and international markets. Within weeks of the announcement, SJVN launched a ₹5,000 crore capital expenditure program targeting 5 GW of capacity additions by 2027.

The state-level partnerships revealed sophisticated political management. The 5 GW joint venture with Maharashtra leveraged the state's manufacturing demand and coastal wind potential. The 1 GW Assam partnership targeted the Northeast's untapped hydro resources while addressing regional development aspirations. Each deal was structured to align local political interests with national renewable targets—a playbook perfected over decades of center-state negotiations.

The international portfolio expanded dramatically. Nepal's Arun III project finally achieved financial closure after 16 years of negotiations. Bhutan approved the second phase of Kholongchhu. But the surprise was Uganda—SJVN won a contract to develop 200 MW of solar projects, marking entry into Africa. The vision was ambitious: become India's renewable energy ambassador, using government backing to compete with Chinese state-owned enterprises in emerging markets.

Technology adoption accelerated beyond recognition. SJVN deployed AI-powered predictive maintenance systems that reduced hydro plant downtime by 23%. Drone surveys cut project assessment time from months to weeks. Digital twins of power plants enabled remote monitoring and optimization. The organization that once moved at geological pace was now iterating like a tech company.

The portfolio composition by late 2024 revealed the transformation's magnitude: 55.81 GW total pipeline, with 25.66 GW in renewable energy. The operational base of 2,466 MW would expand to 8,000 MW by 2027, with 70% coming from solar and wind. Round-the-clock power solutions, combining solar with battery storage, moved from concept to contracted reality. SJVN was no longer following the energy transition—it was leading it.

VII. The 2030-2040 Vision: From PSU to Energy Giant

The slide that CMD Sushil Sharma presented to the Prime Minister's Office in September 2024 contained a single audacious number: 50,000 MW by 2040. The bureaucrats in the room did quick math—that meant adding more than 3,000 MW annually, equivalent to building two Nathpa Jhakris every year for sixteen years. The skepticism was palpable until Sharma pulled up the next slide: a detailed, project-by-project roadmap with sites identified, initial surveys completed, and state governments aligned.

The 2030 target of 25,000 MW breaks down into surgical precision: 8,000 MW hydro, 12,000 MW solar, 4,000 MW wind, and 1,000 MW of hybrid projects. But the real innovation lies in the execution strategy. SJVN will develop 40% directly, acquire 30% through strategic purchases of distressed assets, and partner for 30% through joint ventures. It's portfolio construction theory applied to infrastructure—diversification not just in technology but in development models.

The round-the-clock (RTC) power strategy represents SJVN's biggest competitive differentiation. By combining solar generation with pumped hydro storage, the company can guarantee 24x7 power supply—solving renewable energy's intermittency problem. The first RTC project in Himachal Pradesh will use excess solar power during the day to pump water uphill, then release it through hydro turbines at night. It's elegant engineering that leverages SJVN's unique hydro expertise in the renewable age.

Green hydrogen ambitions moved from PowerPoint to project sites. The partnership with ONGC for a 500,000 tons per annum green ammonia plant in Gujarat positions SJVN at the intersection of energy and chemicals. With European markets mandating green ammonia for fertilizers by 2030, the export opportunity could generate revenues exceeding traditional power sales. The government backing means access to strategic petroleum reserves for hydrogen storage—an advantage no private player can replicate.

The Maharashtra mega-venture deserves special attention. The 5,000 MW joint venture with the state government includes 2,000 MW of offshore wind—India's first commercial ocean-based wind farm. The engineering challenges are immense: installing turbines in Arabian Sea conditions, underwater transmission cables, and maintenance in corrosive marine environments. Yet SJVN's engineers, who conquered Himalayan geology, see ocean engineering as the next frontier.

International expansion follows a careful script. Target countries must have stable governments, dollar-denominated PPAs, and critically, strategic importance to India's foreign policy. Nepal and Bhutan provide hydropower for India's northern grid. Bangladesh offers a market for surplus power. African projects align with India's diplomatic push for Global South leadership. Each international MW strengthens both SJVN's portfolio and India's soft power.

The competitive landscape has shifted dramatically. When SJVN entered renewables, skeptics pointed to Adani Green's 20,000 MW portfolio and ReNew Power's technology edge. But SJVN's advantages are becoming apparent: patient capital that can accept 12% returns versus private players needing 16%+, government backing that ensures land acquisition and clearances, and relationships with state utilities that guarantee power purchase agreements.

The human capital transformation is equally ambitious. SJVN plans to recruit 5,000 engineers by 2030, with 50% from IITs and renewable energy programs. The average employee age will drop from 47 to 35. Performance bonuses will link directly to capacity addition and plant efficiency. It's a cultural revolution wrapped in expansion plans—transforming a government department into an execution machine.

Financial engineering supports the physical expansion. SJVN will raise ₹50,000 crores through a mix of green bonds (40%), international climate funds (30%), and internal accruals (30%). The investment-grade rating and government backing mean access to 100-year bonds from European pension funds desperate for climate-aligned infrastructure assets. It's patient capital meeting patient assets—a perfect match that private developers can't access.

The technology roadmap extends beyond generation. SJVN is investing in grid infrastructure, building transmission lines that can wheel power from remote projects to demand centers. Energy trading desks will optimize portfolio returns by selling power to the highest bidder across multiple states. Digital platforms will enable peer-to-peer power trading, allowing factories to buy directly from SJVN plants.

By 2040, SJVN envisions itself as India's integrated energy major: generating, transmitting, trading, and storing power across technologies and geographies. The 50,000 MW target isn't just about size—it's about becoming systemically important to India's energy security, too big and too critical to fail, the PSU that proved government ownership and market efficiency aren't mutually exclusive.

VIII. Financial Performance & Market Dynamics

The Excel model that SJVN's CFO presented to the board in March 2024 contained a paradox that perfectly captured the company's financial reality. Revenue had grown at just 2.59% annually over five years—barely beating inflation. Yet the capital expenditure column showed ₹15,000 crores of ongoing investments. The company was simultaneously stagnant and hyperactive, generating modest returns while building massive future capacity. Understanding this contradiction requires diving deep into the peculiar economics of infrastructure PSUs.

The headline numbers paint a picture of steady but unspectacular performance. Market capitalization of ₹38,508 crores values SJVN at approximately ₹15.6 crores per operational MW—rich compared to thermal players but reasonable for renewable-heavy portfolios. Revenue of ₹3,119 crores translates to roughly ₹1.26 crores per MW, reflecting high plant availability but also regulated tariffs that prioritize affordability over profits.

The profitability metrics reveal the PSU paradox. Net profit of ₹689 crores delivers a margin of 22%—healthy by infrastructure standards. But Return on Equity of just 7.29% would make private equity investors weep. The reason? SJVN carries ₹9,463 crores of equity on its books, accumulated over decades of retained earnings and government infusions. It's overcapitalized by private sector standards but appropriately capitalized for 30-year infrastructure projects.

Working capital deterioration tells a troubling story. Debtor days increased from 41.3 to 65.8 over five years as state electricity boards delayed payments. SJVN now carries ₹562 crores in receivables—two months of revenue locked up in government IOUs. The cruel irony: a government company waiting for payment from government customers, with the government shareholder caught in between.

The capital allocation framework reveals strategic priorities. Of every ₹100 in operating cash flow, ₹40 goes to dividends (keeping the government shareholder happy), ₹50 funds new projects, and ₹10 covers debt service. This 40-50-10 formula has remained remarkably stable, suggesting either disciplined capital management or bureaucratic rigidity, depending on your perspective.

Stock performance reflects market ambivalence. Trading at 2.72x book value suggests optimism about future growth. But the stock's 52-week range of ₹90-150 shows 67% volatility—high for a utility, reflecting uncertainty about execution capabilities. The 81.8% government holding creates a liquidity challenge: only ₹7,000 crores of free float trades actively, making the stock susceptible to momentum swings.

The dividend story deserves special attention. SJVN pays out ₹275-300 crores annually, providing steady income to the cash-strapped government. But this 40% payout ratio means less retained earnings for growth. It's a classic PSU dilemma: balance the government's fiscal needs against corporate expansion requirements. The recent Navratna status might provide flexibility to retain more earnings, but political pressures for dividends remain strong.

Debt metrics show conservative financial management. Debt-to-equity of 0.7x and interest coverage of 5.2x would qualify as boring in banking circles—exactly what infrastructure investors want. The ₹6,600 crore debt book carries an average cost of 7.8%, with 60% from government-backed institutions. Recent green bond issuances at 7.2% show SJVN can access competitive financing despite PSU status.

The valuation puzzle persists. At ₹98 per share, SJVN trades at 14x trailing earnings—neither cheap nor expensive. DCF models using 10% discount rates suggest fair value between ₹85-115, depending on capacity addition assumptions. The wide range reflects genuine uncertainty: will SJVN execute its 50,000 MW vision or remain a 5,000 MW player with big dreams?

Comparative analysis reveals SJVN's unique position. NTPC trades at 1.2x book value despite similar government ownership, reflecting thermal's decline. Adani Green commands 8x book despite minimal current profits, betting on future growth. SJVN sits between these extremes—more growth potential than NTPC, more current earnings than Adani Green. It's the Goldilocks of power PSUs—not too hot, not too cold, just confusingly in between.

IX. Playbook: Business & Investing Lessons

The conference room in Mumbai's Nariman Point was packed with fund managers when SJVN's CEO made a startling admission in 2023: "Our biggest competitive advantage is that we can afford to fail." The room went silent. In a world where private infrastructure players live on leverage and die on execution delays, SJVN's government backing provided something invaluable—the ability to take 20-year bets without 2-year performance pressures.

Lesson 1: Patient Capital as Competitive Moat SJVN's ability to accept 12% equity returns while private players need 18%+ creates an insurmountable advantage in competitive bidding. When Adani Green bids for a solar project, they're solving for private equity exits. When SJVN bids, they're solving for 30-year social returns. This patience premium—worth 600 basis points—means SJVN can win projects at tariffs that would bankrupt private players. It's not inefficiency; it's strategic advantage.

Lesson 2: The Hidden Value of Government Relationships Every infrastructure project needs three things: land, clearances, and power purchase agreements. SJVN's government parentage delivers all three. State governments provide land at circle rates, not market prices. Environmental clearances that take private players years arrive in months. PPAs with state utilities come with sovereign guarantee equivalents. Calculate the value: land cost savings (20% of project cost), time savings (₹1 crore per MW per year of delay), and PPA certainty (worth 200 basis points in cost of capital). The government ownership that depresses PE multiples actually creates enormous operational value.

Lesson 3: Execution Capability vs Strategic Vision SJVN's history reveals an uncomfortable truth: execution excellence matters more than strategic brilliance in infrastructure. The company's strategic pivots—into thermal, international projects, renewables—were often late and reactive. But when SJVN commits to building something, it gets built. Nathpa Jhakri took 15 years but works at 98% availability. Private players announce projects faster but SJVN completes them. In infrastructure, the tortoise beats the hare because reliability compounds over decades.

Lesson 4: The Platform Power of Diversification SJVN's multi-technology platform creates portfolio benefits that pure-play competitors miss. Hydro provides storage for solar intermittency. Thermal offers baseload when renewables falter. Geographic diversification across states reduces regulatory risk. This portfolio approach means SJVN can offer solutions (round-the-clock power) that technology specialists cannot. The market values pure plays for clarity but infrastructure rewards platforms for resilience.

Lesson 5: Capital Allocation in Political Economy SJVN's capital allocation reveals how PSUs navigate political economy. The 40% dividend payout keeps government treasuries happy. The 50% reinvestment rate maintains growth narrative. The 10% debt service shows financial prudence. This formula isn't optimal in pure financial terms but it's sustainable in political terms. Understanding this trade-off is crucial for PSU investing—these companies optimize for stakeholder balance, not shareholder value.

Lesson 6: The Talent Arbitrage Opportunity SJVN pays its CEO ₹50 lakhs annually—what Adani Green pays a vice president. Yet SJVN attracts top engineering talent through job security, prestigious projects, and nation-building narrative. This talent cost arbitrage—getting IIT engineers at 30% of private sector cost—provides sustainable advantage. The lesson: in human capital intensive industries, non-monetary compensation can be a powerful differentiator.

Lesson 7: Regulatory Capture vs Regulatory Partnership Critics call PSUs victims of regulatory capture—forced to accept low returns by government mandate. SJVN's reality is subtler: regulatory partnership. The company helps shape policy (renewable purchase obligations, hydro purchase requirements) that then creates demand for its services. It's not capture but co-evolution—SJVN and regulators jointly creating markets that private players then enter. First-mover advantage in regulated markets comes from helping write the rules.

Lesson 8: The Infrastructure J-Curve Reality SJVN's financial trajectory follows the infrastructure J-curve: massive upfront investment, years of negative cash flow, then decades of steady returns. Private markets struggle with this J-curve, demanding quick returns. SJVN's government backing allows it to stay invested through the valley of death. The lesson: infrastructure investing requires either patient capital or financial engineering—SJVN has the former, private players need the latter.

Lesson 9: Technology Adoption in Legacy Organizations SJVN's digital transformation offers lessons in modernizing legacy organizations. Instead of wholesale transformation, SJVN created digital islands (Green Energy subsidiary) that gradually influenced the mainland. New technology came wrapped in familiar processes. Change agents were internal engineers, not external consultants. The result: adoption without antibodies, transformation without trauma.

Lesson 10: The Compound Value of Institutional Knowledge SJVN's greatest asset doesn't appear on balance sheets: institutional knowledge of building and operating power plants in India's complex environment. This knowledge—how to manage tribal land issues, navigate forest clearances, handle monsoon construction, manage high-altitude logistics—took decades to accumulate and cannot be quickly replicated. It's the ultimate moat in infrastructure: experience that compounds with each project.

X. Bear vs Bull Case Analysis

The Bull Case: India's Energy Transformation Vehicle

The bull thesis starts with a simple observation: India needs to add 500 GW of renewable capacity by 2030 to meet its climate commitments. At current market share, SJVN would capture 5% of this—25 GW of additions worth ₹1.5 lakh crores in capital investment. But the real opportunity lies in SJVN's unique position to capture more than its fair share.

Navratna status changes everything. Operational autonomy means faster decision-making, competitive compensation to attract talent, and critically, ability to raise capital without government approval. Watch for SJVN to issue India's first 100-year infrastructure bond to European climate funds—patient capital meeting patient assets at unprecedented scale. The governance upgrade alone could be worth 20-30% rerating as execution accelerates.

The round-the-clock power solution represents a ₹50,000 crore opportunity that only SJVN can fully capture. Combining solar with pumped hydro storage requires both technologies, existing hydro sites, and 30-year investment horizons. Private players have the technology but not the sites. NTPC has sites but focuses on thermal. SJVN sits at the sweet spot—hydro expertise, renewable ambitions, and government backing for three-decade investments.

International expansion provides uncorrelated growth. Nepal's 10,000 MW potential, Bhutan's 30,000 MW reserves, and Bangladesh's energy deficit create a $100 billion regional opportunity. SJVN's government backing means access to credit lines, diplomatic support, and critically, ability to accept sovereign risk that private players cannot. Each international MW strengthens both portfolio diversification and India's energy security.

The financial trajectory shows explosive potential. If SJVN achieves even 50% of its 25 GW target by 2030, revenues would reach ₹15,000 crores (5x current), profits ₹3,000 crores (4.5x current). At sector-average valuations, market cap could reach ₹1.5 lakh crores—a 4x return from current levels. The risk-reward favors patient investors willing to bet on execution.

Long-term Power Purchase Agreements provide unmatched revenue visibility. Unlike merchant power players facing price volatility, SJVN's 30-year PPAs with state utilities offer bond-like certainty. As interest rates decline, these long-duration cash flows become increasingly valuable. The hidden optionality: if power markets deregulate, SJVN can sell above PPA rates while maintaining floor prices.

The Bear Case: Structural Challenges in a Competitive Market

The bear thesis begins with brutal math: SJVN's 5-year revenue CAGR of 2.59% during India's greatest infrastructure boom. If management couldn't deliver growth when conditions were perfect, why expect improvement when competition intensifies? The track record suggests execution capabilities chronically lag ambitions.

Competition has fundamentally changed. Adani Green adds 5 GW annually—SJVN's entire operational base—with execution speed SJVN cannot match. ReNew Power brings international technology and capital markets expertise. Tata Power combines private efficiency with conglomerate stability. Against these formidable competitors, SJVN's government backing becomes a liability—slow decision-making when speed wins, bureaucracy when agility matters.

The working capital crisis deepens structural concerns. State electricity boards owe SJVN ₹562 crores and payment delays are lengthening. The cruel reality: the same government that owns SJVN also owns the defaulting utilities. This circular debt problem—government entities defaulting on government entities—has no clear resolution. Every MW of capacity added increases receivables exposure.

Return metrics remain abysmal for a growth story. ROE of 7.29% barely beats fixed deposit rates. In a world where infrastructure funds target 15% returns, SJVN destroys value with every rupee invested. The government's social return requirements mean SJVN can never optimize for financial returns. It's structurally condemned to subpar profitability.

Execution risk on the 50 GW target appears insurmountable. SJVN took 15 years to build 1,500 MW at Nathpa Jhakri. Now they promise 3,000 MW annually—twenty times the historical run rate. The engineering talent doesn't exist, the project management systems aren't ready, and the balance sheet cannot support ₹3 lakh crores in capital expenditure. The targets are political theater, not operational reality.

Technology disruption threatens the entire business model. Distributed solar plus battery storage could make centralized generation obsolete. Rooftop solar with net metering eliminates utility intermediation. Green hydrogen might bypass electricity altogether. SJVN's investing billions in yesterday's technology while tomorrow's solutions emerge elsewhere.

The dividend trap constrains growth potential. Government's fiscal pressures mean dividend demands will increase, not decrease. Every rupee paid in dividends is a rupee not invested in growth. The 40% payout ratio might become 50%, then 60%, starving the company of growth capital precisely when investment needs are highest.

Valuation already prices in perfect execution. At 2.72x book value and 14x earnings, SJVN trades at premiums to global utilities despite inferior returns. The market has already given credit for future growth. Any execution disappointment could trigger 30-40% correction. The risk-reward skews negative for momentum investors.

XI. Epilogue: The Future of Government-Led Energy Transition

The Sutlej River flows today much as it did in 1988, but everything else about SJVN has transformed. From a single-project joint venture to a 55 GW energy platform, from Himalayan valleys to Thar Desert solar fields, from government department to listed company—SJVN's journey mirrors India's own energy evolution. But the fundamental question remains: Can a government-owned company lead India's transition to renewable energy in an age of nimble private competitors?

The answer lies not in ideology but in infrastructure economics. Energy transition requires three elements that favor patient, public capital: decade-long development cycles that outlast private fund horizons, social returns that justify sub-market financial returns, and strategic importance that demands sovereign backing. SJVN possesses all three. The surprise isn't that a PSU is competing—it's that anyone expected otherwise.

The international context matters enormously. China's state-owned enterprises dominate global renewable deployment. European governments are renationalizing energy assets. Even America's Inflation Reduction Act represents massive public intervention in energy markets. The global energy transition isn't being led by free markets but by state capital. In this context, SJVN isn't an anachronism but ahead of the curve.

Yet execution remains the binding constraint. SJVN's ambitious targets—25 GW by 2030, 50 GW by 2040—require operational excellence that PSUs historically lack. The cultural transformation from bureaucracy to business, from seniority to performance, from risk-aversion to innovation, remains incomplete. Navratna status provides tools but changing organizational DNA takes generations.

The investment implications are nuanced. SJVN isn't a momentum play for traders seeking quick returns. It's a decade-long bet on India's energy transformation, suitable for patient capital willing to accept infrastructure-like returns for utility-like stability. The government ownership that caps upside also floors downside. In a portfolio context, SJVN offers uncorrelated returns and inflation protection—boring but valuable attributes.

For India's energy security, SJVN represents something irreplaceable: a national champion that prioritizes reliability over returns, access over margins, and strategic autonomy over market efficiency. When private players chase profitable urban markets, SJVN electrifies remote villages. When international tensions threaten energy supplies, SJVN's domestic focus provides resilience. It's infrastructure as public good, not just private gain.

The next decade will determine whether SJVN's transformation from hydro specialist to renewable platform succeeds. Key milestones to watch: successful commissioning of round-the-clock power projects, execution of the 5 GW Maharashtra venture, and critically, ability to attract and retain young engineering talent. If SJVN can execute even 70% of its stated ambitions, it will have created enormous value—for shareholders, stakeholders, and society.

The story that began with an engineer staring at the Sutlej River continues today with thousands of engineers staring at solar radiation maps, wind velocity charts, and hydrogen electrolyzer specifications. The mission remains unchanged: turning India's natural resources into national prosperity. The means have evolved from concrete and turbines to silicon and inverters. But the end—affordable, reliable, clean energy for 1.4 billion Indians—remains as audacious and essential as ever.

SJVN's journey proves that government ownership and market efficiency aren't mutually exclusive, that patient capital can compete with private velocity, and that national missions sometimes require national champions. Whether SJVN fulfills its ambitious vision or remains trapped between government constraints and market pressures will shape not just one company's future but India's entire energy trajectory.

The Sutlej still flows, but now it powers a nation's dreams.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube