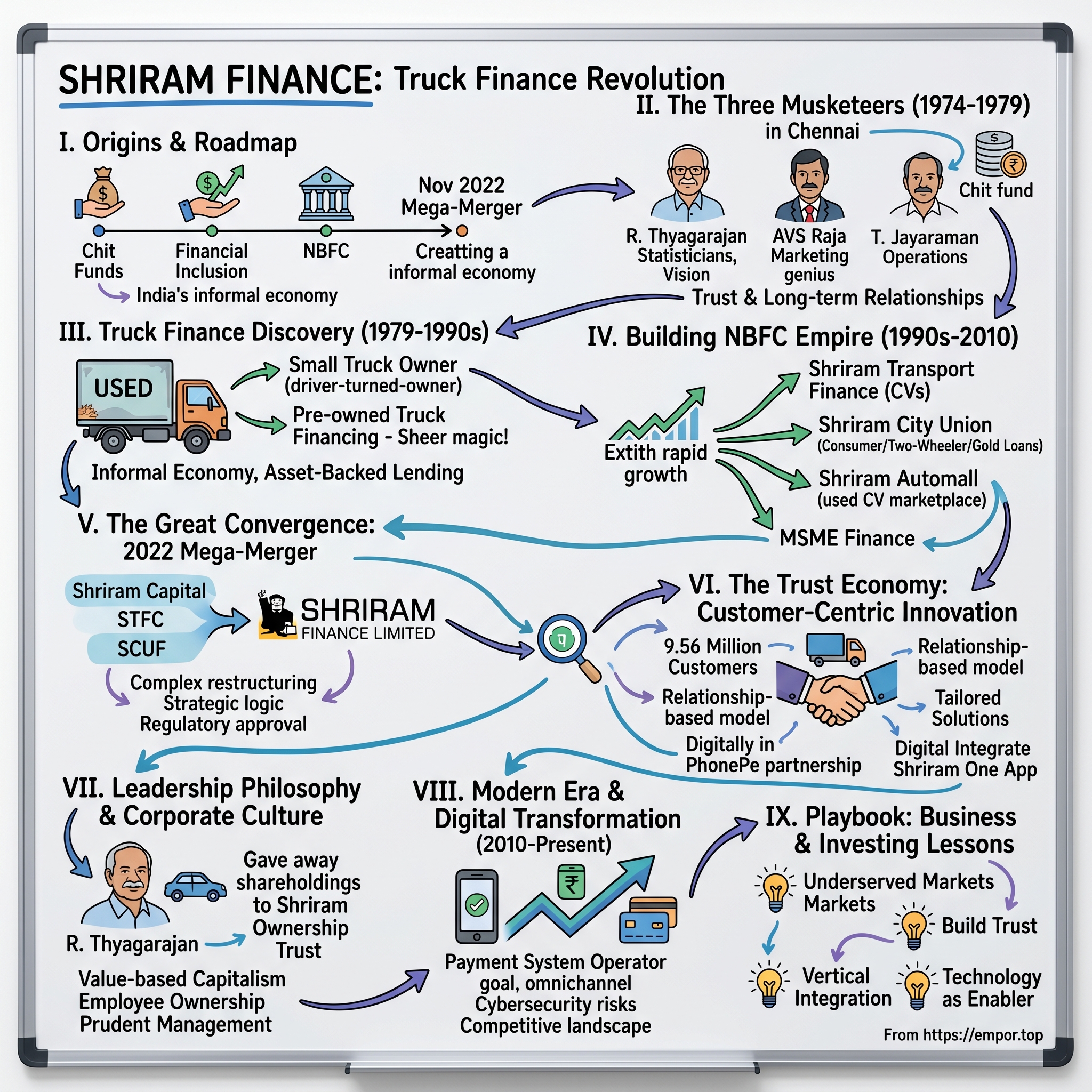

Shriram Finance: India's Truck Finance Revolution

I. Introduction & Episode Roadmap

The story of Shriram Finance begins not in gleaming corporate towers or Silicon Valley garages, but in the dusty truck stops along India's national highways. Today, this financial behemoth commands an Asset Under Management of over Rs 2.6 trillion, making it India's largest retail asset financing NBFC. Yet its origins trace back to a remarkably simple insight: millions of India's truck drivers, the backbone of the nation's economy, couldn't get a loan from a bank.

The question that drives this narrative forward is deceptively straightforward: How did three middle-class professionals build a financial empire by lending to India's unbanked truckers? The answer reveals not just a business success story, but a masterclass in understanding India's informal economy, building trust where none existed, and creating value in markets that traditional finance had written off as too risky.

What we know today as Shriram Finance is the result of a transformative merger completed in November 2022, combining Shriram Transport Finance, Shriram City Union Finance, and Shriram Capital into a single powerhouse entity. This merger wasn't just a financial transaction—it was the culmination of nearly five decades of patient empire-building, starting from humble chit fund operations in Chennai to becoming a financial services conglomerate that touches the lives of nearly 10 million customers across India.

The Shriram story is fundamentally about seeing opportunity where others saw only risk. It's about understanding that a truck driver who can't produce income tax returns might still be creditworthy, that a small business owner without formal documentation might be running a profitable enterprise, and that serving the underserved isn't charity—it's good business when done right.

This journey from chit funds to challenging the banking establishment represents one of India's most remarkable entrepreneurial achievements. It's a story of three visionaries who understood that financial inclusion wasn't just a social good but could be the foundation of a massive business. Their creation now stands as testament to a different kind of financial institution—one built on relationships rather than algorithms, trust rather than collateral, and deep market understanding rather than standardized products.

The post-merger Shriram Finance represents the ultimate validation of this approach. With a market capitalization exceeding Rs 1.18 lakh crore, revenue of Rs 43,778 crore, and profits of Rs 9,705 crore, it has proven that serving India's informal economy isn't just sustainable—it's extraordinarily profitable when executed with the right philosophy and operational excellence.

II. The Three Musketeers & Founding Vision (1974-1979)

The story of Shriram Finance begins on April 5, 1974, in Chennai, when three middle-class professionals decided to pool their resources and ambitions to create something that would eventually transform India's financial landscape. R. Thyagarajan, AVS Raja, and T. Jayaraman founded what would initially be Shriram Chits, a modest chit fund operation that would grow into one of India's most formidable financial services conglomerates.

R. Thyagarajan, the intellectual architect of the group, brought impressive academic credentials with master's degrees in Mathematics and Mathematical Statistics from the prestigious Indian Statistical Institute. His professional journey began in 1961 as a Trainee Officer with New India Assurance Company Limited, where he would spend two decades learning the intricacies of India's financial services industry. After his undergraduate and master's education in Chennai, he spent three years at the Indian Statistical Institute in Kolkata, developing the analytical mindset that would prove crucial in understanding risk in unconventional markets.

AVS Raja, described as the marketing genius of the trio, came from Indian Railways. Born into a traditional Brahmin family as the son of a government school teacher, Raja would travel 12 kilometers by walk and later by cycle to complete his education, eventually earning a BA in History. His understanding of middle-class struggles and his natural flair for marketing would become instrumental in building trust with Shriram's eventual customer base. The initial arrangement was clear: AVS Raja would handle sales and marketing, T. Jayaraman would manage operations, and Thyagarajan would advise and invest.

T. Jayaraman, Thyagarajan's brother-in-law, was brought in to handle finance and operations. This family connection, rather than weakening the enterprise, would prove to be a source of strength, creating bonds of trust that went beyond mere business partnerships. The three complemented each other perfectly—Thyagarajan with his analytical mind and industry connections, Raja with his marketing prowess and understanding of the common man, and Jayaraman with his operational expertise.

The philosophical foundation of Shriram was revolutionary for its time. Thyagarajan had a vision to build an organization that could cater to the vast and often neglected sections of society, particularly the lower-income groups and small businesses, which were systematically excluded from mainstream financial institutions. This wasn't charity or corporate social responsibility as we understand it today—this was a fundamental business insight that millions of Indians needed financial services but couldn't access them through traditional channels.

Despite coming from a well-to-do farming family in Tamil Nadu where he grew up surrounded by servants, Thyagarajan always had an analytical and egalitarian-oriented mind. This background gave him the security to take risks, but also the perspective to understand that prosperity shouldn't be the privilege of a few. He challenged the conventional belief that lending to individuals without credit histories or stable incomes was too risky, aiming to prove this notion wrong by offering loans at affordable rates and demonstrating that such lending could be both secure and lucrative.

The early days were humble, almost comically so by today's standards. Shriram Chits was officially born on April 5, 1974, operating out of modest premises in Chennai. The chit fund business, while not glamorous, was perfectly suited to their target market. Chit funds operated on principles of mutual benefit and community trust—concepts deeply embedded in Indian society. Members would contribute monthly amounts to a common pool, and through an auction system, those in need could access lump sums when required. It was financial inclusion at its most basic, yet most effective level.

What set Shriram apart from other chit fund operators was the founders' vision of scale and systematization. They weren't content to remain a local Chennai operation. They saw chit funds not as the end goal but as the beginning—a way to understand their customers, build trust, and create a foundation for something much larger. The majority of financial services were focused on the urban elite, leaving rural and semi-urban India underserved. Recognizing this gap, the founders built Shriram Group's business model around catering to these underserved populations, offering affordable financing options to individuals, small traders, and rural entrepreneurs.

The philosophy that would guide Shriram for the next five decades was established in these early years. Thyagarajan emphasized trust and long-term relationships with customers. Unlike many other financial institutions that focused primarily on short-term profits, the Shriram Group built its reputation on providing tailored financial solutions that were both accessible and sustainable. This wasn't just good ethics; it was good business. In markets where formal documentation was scarce and traditional collateral non-existent, trust became the currency that mattered most.

An interesting precursor to what would become Shriram's core business emerged during this period. People in Chennai came to Thyagarajan seeking money to buy used trucks, and he gave them loans from his inheritance. Gradually, that side venture morphed into his life's main act. This personal experience of lending to truck buyers would soon transform into the insight that would make Shriram's fortune.

The founders' approach to growth was methodical and patient. Thyagarajan had invested in many companies before Shriram, including India Chemicals, Kartik Pharma, Novhem Labs, Sahyatha Chit Fund, Shrilekha Chit Funds, and Madras Motor Finance. All of them failed to take off except for Shriram. Yet he didn't give up investing even though most of his other ventures failed. This persistence, combined with the lessons learned from failure, would prove invaluable.

By 1979, after five years of running the chit fund business, the founders had accumulated enough capital, experience, and most importantly, understanding of their market to make their next move. They had proven they could operate a financial services business profitably. They had built a small but loyal customer base. They had developed systems and processes that could be scaled. Most crucially, they had identified a massive market opportunity that everyone else had overlooked—financing for used commercial vehicles, particularly trucks.

The transition from chit funds to vehicle finance wasn't obvious to outsiders, but for the Shriram founders, it was a natural evolution. Through their chit fund operations, they had come into contact with thousands of small entrepreneurs, traders, and transport operators. They understood their financial needs, their business cycles, and their capacity to repay. They also understood something that banks didn't—that these customers, despite lacking formal credit histories, were actually excellent credit risks when properly evaluated.

Interestingly, Thyagarajan didn't quit his insurance job to join Shriram full-time until 1985, eleven years after the company's founding. This cautious approach—maintaining a steady income while building the business—exemplified the prudent, risk-managed philosophy that would characterize Shriram's growth. It also meant that the early years were truly entrepreneurial, with Raja and Jayaraman handling day-to-day operations while Thyagarajan provided strategic guidance and capital.

The culture that emerged in these formative years would become Shriram's enduring competitive advantage. Thyagarajan emphasized prudent management practices, focusing on transparency, integrity, and innovation. But beyond these corporate virtues, there was something more fundamental—a genuine belief that serving the underserved was not just profitable but morally important. This wasn't corporate social responsibility grafted onto a profit-making enterprise; this was a business model where social impact and profitability were inseparable.

As the 1970s drew to a close, Shriram stood at a crucial juncture. The chit fund business had provided proof of concept, working capital, and most importantly, deep market insights. The founders had identified their next big opportunity—truck finance. They had the team, the vision, and the initial capital. What they were about to do would transform not just their company but the entire landscape of vehicle finance in India. The stage was set for Shriram Transport Finance Company, and with it, the transformation of Shriram from a regional chit fund operator to a national financial services powerhouse.

III. The Truck Finance Discovery (1979-1990s)

The year 1979 marked a pivotal transformation in Shriram's trajectory. Established in 1979, Shriram Transport Finance Company Limited (STFC) was incorporated on June 30th in Chennai, marking the group's strategic entry into the vehicle financing business. This wasn't just another diversification move—it was the discovery of a business model that would revolutionize financial services for India's transport sector.

The market insight that drove this transformation was both simple and profound. STFC decided to finance the much neglected Small Truck Owner. Shriram understood the power of 'Aspiration' much before marketing based on 'Aspiration' became fashionable. They started lending to the Small Truck Owner to buy new trucks but found a mismatch between the Aspiration and Ability. The Truck Operator was honest but the Equity at his command was not sufficient to support the credit levels required to buy a new truck.

This discovery led to what would become Shriram's defining innovation. They did not have the heart to send the Truck Operator back empty handed; they decided to fund Pre-owned Trucks. This was the most momentous decision that they made. What followed was Sheer magic. From Driver to Owner, even if only of a Pre-owned Truck and from Pre-owned Truck to the New Truck, they have been with him in their journey of Prosperity.

The economics of India's trucking industry in the late 1970s and early 1980s presented a paradox. Road transport was the lifeblood of India's economy, with trucks carrying everything from agricultural produce to industrial goods across the vast subcontinent. Yet the people who operated these trucks—the small road transport operators who typically owned less than five vehicles—were systematically excluded from formal credit markets. Banks considered them too risky, lacking proper documentation, credit histories, or traditional collateral.

The founders of Shriram saw what others missed. It is estimated that 80% of trucks in the country are in the hands of individuals. These weren't large fleet operators with corporate structures and audited financials. These were individual entrepreneurs, often former drivers who had saved enough to buy their first truck, operating in what economists would later call the informal economy. The formal financial system's inability to serve this market wasn't just a gap—it was a chasm.

The used truck market presented an even more compelling opportunity. On average, a commercial vehicle in India is resold three times during its operational lifecycle of approximately 12 years. This meant that for every new truck sold, there were three used truck transactions happening in the market. Yet no financial institution was systematically serving this segment. The reasons were obvious to traditional bankers: how do you value a used truck? How do you assess the creditworthiness of a buyer with no formal income proof? How do you recover your loan if things go wrong?

Shriram's answer to these questions was revolutionary in its simplicity: you don't try to force informal sector customers into formal sector frameworks. Instead, you build new frameworks that work for them. Indeed, Shriram Transport, which started in 1979, is often referred to as the "truck driver's bank." This wasn't just a catchy phrase—it represented a fundamental reimagining of what a financial institution could be.

The company's approach to risk assessment was particularly innovative. Traditional banks relied on income tax returns, audited statements, and formal documentation. Shriram developed entirely different metrics. They looked at the route a trucker operated—some routes were more profitable than others. They assessed the condition of the vehicle through physical inspection. They checked the driver's reputation in the transport community. They understood that a truck wasn't just collateral; it was a productive asset that generated daily income.

Shriram Transport Finance Company primarily dealt with financing pre-owned trucks and Small Truck Owners. STFC had been financing the often ignored owners of small trucks since a very long time. They understood the need to finance this segment of small businesses as they understood the importance of small businesses in the country. They realised that the small truck owners with their hand to mouth earnings would not be able to meet the required credit to purchase a new truck.

The operational model Shriram developed was equally innovative. Rather than trying to build a traditional branch banking network, they created a hybrid model that combined company-owned branches with partnerships with local financiers. These local partners weren't just agents; they were integral to the business model. They knew the local transport operators, understood the economics of different routes, and could assess creditworthiness in ways that no centralized system could replicate.

By focusing on the 5-12 year old truck segment, Shriram found a sweet spot in the market. These vehicles were affordable enough for first-time buyers but still had significant productive life remaining. A five-year-old truck could operate profitably for another seven years, generating enough income to repay the loan and provide a livelihood for the owner. This wasn't subprime lending as understood in Western markets—it was inclusive finance that recognized the economic potential of underserved segments.

The trust-building mechanisms Shriram employed were sophisticated in their simplicity. Loan officers would visit truck stops, build relationships with transport unions, and become familiar faces in the transport community. They understood that in the absence of formal credit bureaus, reputation in the community was the most valuable form of collateral. A defaulter would not just lose his truck; he would lose his standing in the tight-knit transport community.

For Shriram, credit-worthiness of the Small Truck Owner has always been an article of faith. This faith has guided their journey from their pioneering days in financing Small Truck Owners to the present day leadership. This wasn't blind faith but faith based on deep understanding and systematic risk management.

The company's pricing strategy was equally nuanced. While interest rates were higher than what banks charged their corporate clients, they were significantly lower than what informal moneylenders charged. Shriram positioned itself as the ethical alternative to usurious lending while still maintaining healthy margins. This pricing discipline would prove crucial to the company's long-term sustainability.

Technology adoption in these early years was minimal by today's standards, but Shriram was innovative in its use of simple systems to manage complex operations. They developed standardized valuation models for different truck models and ages. They created simplified documentation processes that worked for semi-literate customers. They built collection systems that aligned with the cash flow patterns of the transport business.

The geographic expansion strategy during the 1980s and early 1990s was methodical. Starting from their base in South India, particularly Tamil Nadu, they gradually expanded along major trucking routes. Each new location wasn't just a branch opening; it was an investment in understanding local market dynamics, building relationships with local transport associations, and adapting their model to regional variations.

The pre-owned commercial vehicle segment, which is STFC's primary focus area, is largely driven by aspirations of a unique customer segment – either first-time users or driver-turned-owners. This, aided by the lower deal size, results in a potent combination that has largely eluded economic downturns. The company is the market leader in lending to this segment and therefore remains least affected by economic downturns.

By the early 1990s, Shriram Transport Finance had established itself as the undisputed leader in used commercial vehicle finance. They had proven that lending to the informal sector wasn't just viable but could be more resilient than traditional corporate lending. During economic downturns, large corporations might delay capital expenditure, but small truck operators still needed vehicles to earn their daily bread. This counter-cyclical characteristic would become one of Shriram's greatest strengths.

The cultural DNA established during this period would endure for decades. The company culture emphasized field presence over desk analysis, relationships over transactions, and long-term value creation over short-term profits. Employees were encouraged to spend time at truck stops, to understand the economics of transport operations, and to see customers not as credit risks but as partners in prosperity.

According to Shriram group's founder, R. Thyagarajan, lending to low-income borrowers shunned by banks may be a form of socialism. But by offering a cheaper interest rate than the punitive rates available to the unbanked, he proved that lending to such borrowers can be safe and profitable. He has held on to this conviction since 1974, when he entered the industry.

The regulatory environment during this period was both a challenge and an opportunity. As a Non-Banking Financial Company (NBFC), Shriram operated under different regulations than banks. While this meant they couldn't accept demand deposits like banks, it also gave them more flexibility in their lending practices. They could innovate faster, adapt quicker, and serve segments that regulatory constraints prevented banks from serving effectively.

The success metrics Shriram focused on were different from traditional financial institutions. While banks measured success by size of loans and corporate relationships, Shriram measured success by the number of drivers who became owners, the number of single-truck operators who expanded to multiple trucks, and the economic multiplier effect of their lending. Each loan wasn't just a financial transaction; it was an investment in India's transport infrastructure and economic development.

As the 1990s progressed, competition began to emerge. Some banks started exploring commercial vehicle finance, and other NBFCs tried to replicate Shriram's model. But Shriram's first-mover advantage, combined with their deep market knowledge and established relationships, proved difficult to overcome. They had spent over a decade building trust in a low-trust environment, and that trust became their moat.

The company's approach to bad loans was particularly instructive. Rather than writing off non-performing assets quickly, they worked with borrowers to restructure loans, understanding that a truck sitting idle helped nobody. They might extend tenure, reduce installments during lean periods, or help operators find work during economic slowdowns. This patient approach not only improved recovery rates but also strengthened customer loyalty.

By the end of the 1990s, Shriram Transport Finance had transformed from an experimental venture into a proven business model. They had financed hundreds of thousands of trucks, created a network that spanned across India, and most importantly, proved that financial inclusion and profitability weren't mutually exclusive. The stage was set for the next phase of growth—building a financial services empire that would extend far beyond truck finance while never forgetting the core insights that made their success possible.

IV. Building the NBFC Empire (1990s-2010)

The period from the 1990s to 2010 marked Shriram's transformation from a specialized truck finance company into a diversified financial services conglomerate. This expansion wasn't random diversification—it was a systematic application of their core philosophy to adjacent markets with similar characteristics: underserved customers, informal economy participants, and asset-backed lending opportunities.

Shriram City Union was started in 1986 and built by Shriram group's founder, Thyagarajan, on the same philosophical principle he used at Shriram Transport: lending money to borrowers with limited documentary income proof and credit history. This new entity would become the vehicle for Shriram's expansion beyond commercial vehicles into consumer finance.

The two-wheeler financing business became Shriram's first major diversification success. Established in 1986, Shriram City Union is part of the three decade-old Shriram Group. Started as a deposit-accepting non-banking financial company (NBFC), Shriram City Union has transformed itself into one of India's premier financial services company specializing in retail finance. The logic was compelling: if they could finance trucks for small operators, why not motorcycles and scooters for individual consumers?

Two-wheeler financing in India presented unique opportunities. India was emerging as one of the largest manufacturers and users of two-wheelers in the world, with motorcycles and scooters becoming the primary mode of transport for millions of middle and lower-middle-class families. The market dynamics were similar to truck financing—customers with irregular income, limited documentation, but genuine need and capacity to repay.

Over time, Shriram City Union created a strong market position in the MSME loan and two-wheeler financing segments. Also, it diversified into providing home loans (through a housing finance subsidiary), loans against gold ornaments, and loans for personal consumption. Each of these expansions followed the same template: identify an underserved market, understand its unique characteristics, develop appropriate risk assessment models, and build distribution networks that could reach customers where they were.

The MSME (Micro, Small, and Medium Enterprises) finance vertical was particularly strategic. These businesses—kirana stores, small manufacturers, traders—formed the backbone of India's economy but were largely ignored by banks. They operated in cash, maintained minimal documentation, and couldn't provide the collateral banks demanded. For Shriram, with their deep understanding of informal sector economics, this was familiar territory.

Gold loans emerged as another natural extension. In India, gold isn't just jewelry—it's the savings account of the poor and middle class. When families faced emergencies or needed working capital for businesses, they would traditionally turn to local pawnbrokers charging usurious rates. Shriram saw an opportunity to formalize this market, offering transparent pricing, proper documentation, and fair valuation while still maintaining the speed and accessibility customers needed.

The expansion wasn't just about adding products—it was about building an integrated ecosystem. A truck driver financed by Shriram Transport might need a two-wheeler loan for his son from Shriram City Union. A small shopkeeper who took an MSME loan might later need a gold loan for his daughter's wedding. This cross-selling potential created powerful network effects.

Shriram City has a comprehensive range of offerings, which has made Shriram City a dominant player in the field and the only NBFC to offer such a wide range of products under one roof. This one-stop-shop approach was particularly valuable for customers who found dealing with multiple financial institutions challenging.

The organizational structure during this period evolved to support this diversification. Rather than trying to manage everything under one entity, Shriram created specialized subsidiaries for different business lines. Shriram Transport Finance continued to focus on commercial vehicles. Shriram City Union handled consumer finance. Later subsidiaries would handle insurance, housing finance, and other specialized products. This structure allowed each entity to develop deep expertise while sharing the group's overall philosophy and risk management approach.

Technology adoption accelerated during this period, though Shriram's approach remained pragmatic rather than cutting-edge. They invested in core banking systems that could handle their growing scale, risk management tools that could assess diverse loan types, and gradually, digital channels that could complement their physical presence. The key was maintaining the human touch that had been central to their success while using technology to improve efficiency and reach.

The partnership strategy during this period was particularly sophisticated. Shriram Life Insurance is the life insurance arm of the group, and a joint venture between Shriram Group and South African company Sanlam. These weren't just capital partnerships but knowledge partnerships, bringing global best practices to India while maintaining local market understanding.

Distribution innovation continued to be a key differentiator. For two-wheeler loans, Shriram established presence directly in dealerships, making the loan process seamless for buyers. For gold loans, they set up dedicated gold loan branches in market areas where customers felt comfortable bringing their valuables. For MSME loans, they deployed relationship managers who understood specific business sectors and could assess creditworthiness based on business flows rather than just documentation.

Risk management evolved significantly during this period. With multiple product lines, Shriram couldn't rely solely on asset-backed security. They developed sophisticated credit scoring models that incorporated non-traditional data points—utility payment history, references from existing customers, business cycle patterns. They also pioneered the use of psychometric testing for loan assessment, understanding that character often mattered more than collateral.

The growth numbers during this period were staggering. From a single product company in 1990, Shriram had become a financial conglomerate with dozens of products by 2010. Assets under management grew exponentially. Employee count expanded from hundreds to tens of thousands. Geographic presence extended from South India to national coverage.

Shriram City Union Finance grew rapidly over the same period by providing loans for financing two-wheelers, homes, small businesses and loans against gold as well as personal loans — businesses that are not as cyclical as financing commercial vehicles. This diversification provided stability, reducing dependence on any single sector or economic cycle.

Innovation during this period wasn't limited to products. Shriram pioneered new business models that would later become industry standard. The Shriram Automall concept, launched in the 2000s, created India's first organized marketplace for used commercial vehicles. Automall is the first-of-its-kind mall that offers a common meeting platform for the potential buyers and sellers where the valuation of the vehicle is determined through a transparent public auction process.

The regulatory environment during this period presented both challenges and opportunities. As Shriram grew larger, it attracted more regulatory scrutiny. The Reserve Bank of India introduced new regulations for NBFCs, requiring higher capital adequacy, better disclosure, and improved governance. Shriram not only complied but often exceeded regulatory requirements, understanding that regulatory credibility was crucial for long-term success.

Competition intensified during this period. Banks, seeing Shriram's success, began entering segments they had previously ignored. New NBFCs emerged, trying to replicate Shriram's model. Microfinance institutions began competing for the same customer base. Shriram's response was to deepen rather than broaden—focusing on better serving existing customers rather than just acquiring new ones.

Although it was a much smaller operation than Shriram Transport, it was more profitable. Just prior to the merger, the standalone Shriram City Union had assets under management of about INR 33,000 crores. Pretax earnings for FY22 were about INR 1,500 crores. This translates into a pretax return on equity of 17% for the year. The company also had a capital adequacy ratio of 27% and a CRISIL AA/Stable rating on its long-term debt.

The financial performance during this period validated the diversification strategy. Different products had different margin profiles and growth trajectories. The new CV interest rate ranges, anywhere from 11% to 13% and old CVs would be again 13% to 16%. MSME would be 14% to 18%, while gold loans and personal loans commanded even higher rates. This product mix optimization allowed Shriram to improve overall returns while managing risk through diversification.

Employee development became increasingly important as the organization grew. Shriram invested heavily in training programs, creating Shriram City Union Finance Academy to develop specialized skills. They promoted from within, ensuring that senior management understood ground realities. The culture of empowerment that Thyagarajan had established from the beginning became even more critical as the organization scaled.

Customer service evolution during this period reflected changing expectations. While maintaining their high-touch, relationship-based approach for loan origination, Shriram invested in technology to improve post-disbursement service. Online EMI payments, SMS alerts, and gradually, mobile apps made it easier for customers to manage their loans. Yet they never forgot that many of their customers preferred face-to-face interactions, maintaining extensive branch networks even as they digitized.

The global financial crisis of 2008 provided a crucial test of Shriram's model. While many financial institutions globally faced existential crises, Shriram weathered the storm relatively well. Their focus on asset-backed lending, conservative leverage, and deep customer relationships proved resilient. The crisis actually strengthened their position as competitors retreated and customers valued stability.

By 2010, Shriram had successfully transformed from a single-product truck finance company into a diversified financial services conglomerate. They had proven that their model could work across multiple products and geographies. They had built brands that were trusted by millions of Indians who had never had access to formal finance before. Most importantly, they had created a template for inclusive finance that was both socially impactful and commercially successful.

The foundation was now in place for the next phase of growth—technology adoption, international expansion, and eventually, the transformative merger that would create one of India's largest NBFCs. But the core principles established during this period of empire-building would remain unchanged: serve the underserved, build trust through relationships, and never forget that behind every loan is a human aspiration.

V. The Great Convergence: The 2022 Mega-Merger

In November 2022, Shriram Group's entities – Shriram Transport Finance Company Limited, Shriram City Union Finance Limited, and Shriram Capital Limited – merged to form Shriram Finance Limited. This wasn't just another corporate restructuring—it was one of the most complex and transformative mergers in Indian financial services history, creating the country's largest retail Non-Banking Financial Company.

The strategic rationale for the merger had been building for years. By 2021, the Shriram Group had evolved into a complex web of entities, each successful in its own right but operating in silos. Shriram Transport Finance had become the undisputed leader in commercial vehicle finance with assets under management exceeding Rs 1.27 lakh crores. Shriram City Union Finance had built a formidable presence in consumer finance with AUM of around Rs 30,425 crores, where Small Enterprise Finance loans comprised 47.3%, Two-Wheelers 22.2%, Personal Loans 9.3%, and others 21.2%.

The announcement came on December 14, 2021, when Shriram Group unveiled its restructuring plan. This restructuring of the Financial Services Business of Shriram Group would lead to the creation of India's largest retail finance non-banking financial company (NBFC) with the merger of Shriram City Union Finance Limited and Shriram Transport Finance Limited. The complexity of the transaction was staggering—it involved merging two listed entities and one unlisted holding company, each with its own shareholder base, debt structure, and operational systems.

The ownership structure presented particular challenges. Shriram Capital Limited (SCL) was the holding company of Shriram Transport and Shriram City Union where it owned 26.04% and 33.86% stake respectively. This holding company had its own investors, including Ajay Piramal-led Piramal Group and TPG Capital, who needed an exit mechanism. The merger would result in the exits of these strategic investors while creating a simplified ownership structure.

The regulatory approval process was extensive and meticulous. Last month, the group had received approval for the merger of SCL and SCUF with STFC from the Reserve Bank of India (RBI). This was just one of many approvals required. The companies needed clearances from the National Company Law Tribunal (NCLT), Securities and Exchange Board of India (SEBI), stock exchanges, and multiple creditor classes. Each approval required detailed documentation, fairness opinions, and assurances about protecting stakeholder interests.

The share exchange ratios had to be carefully calibrated to ensure fairness to all shareholders. Independent valuers were appointed to assess the relative values of the three entities. The challenge was compounding by the different business profiles—Shriram Transport's commercial vehicle business had different growth and margin characteristics than Shriram City Union's consumer finance business. The final ratios had to balance multiple considerations: current profitability, growth prospects, asset quality, and strategic value.

Operational integration planning began even before regulatory approvals were secured. Post-merger of Shriram Transport Finance and Shriram City Union Finance, the merged entity would have 2,796 branches. Currently, Shriram Transport was having 1,825 branches and Shriram City Union Finance was having 971 branches. The challenge wasn't just combining physical locations but integrating different operational cultures, IT systems, and business processes.

The technology integration was particularly complex. Each entity had developed its own core banking systems, loan origination platforms, and risk management tools over decades. Simply choosing which systems to retain and which to retire required months of analysis. Data migration had to be executed flawlessly—millions of customer records, loan accounts, and transaction histories needed to be consolidated without any disruption to customer service.

Human resource integration presented its own challenges. The combined entity would have over 70,000 employees, each accustomed to different organizational cultures, compensation structures, and career paths. Retention of key talent was crucial, particularly in specialized areas like commercial vehicle valuation or gold loan assessment. The companies had to harmonize HR policies while maintaining morale and productivity during the transition.

The timeline was ambitious but realistic. YS Chakravarti, MD & CEO of Shriram City Union Finance, stated in April 2022: "We are in the process and we expect that formalities to be completed between September and October. The NCLT process has to be completed by October." The companies managed to stay largely on schedule, with the record date fixed for November 30, 2022.

Customer communication was handled with exceptional care. The companies had to reassure nearly 10 million customers that their loans, deposits, and other financial products would continue uninterrupted. Branch staff were trained to explain the merger benefits to customers, emphasizing that they would now have access to a wider range of products and services from a stronger, more diversified institution.

The debt restructuring aspect was equally complex. Shriram City Union Finance had its own Non-Convertible Debentures (NCDs) that needed to be exchanged for NCDs of the merged entity. Wednesday, November 30, 2022 was fixed as the Record Date for the purpose of determining the holders of Non-Convertible Debentures of SCUF for issuance of Non-Convertible Debentures of the Company as per the exchange ratio provided for in the sanctioned Scheme.

Brand integration required delicate handling. Both Shriram Transport Finance and Shriram City Union Finance had built strong brand equity over decades. The decision to adopt "Shriram Finance Limited" as the merged entity's name preserved the core Shriram brand while signaling a new, unified identity. Marketing teams worked to ensure brand continuity while communicating the enhanced value proposition of the combined entity.

The subsidiary structure added another layer of complexity. Shriram Transport owns a subsidiary company i.e., Shriram Automall, where it owns 44.56% stake, while Shriram City Union also has one subsidiary named Shriram Housing, in which it holds an 85.02% stake. Post the merger, these 2 subsidiaries- Shriram Automall and Shriram Housing would remain the subsidiary companies of Shriram Finance.

Regulatory compliance for the merged entity required careful planning. The combined entity would be systemically important, attracting enhanced regulatory scrutiny. Capital adequacy requirements, provisioning norms, and governance standards all needed to be upgraded to reflect the merged entity's scale and significance. The companies proactively engaged with regulators to ensure smooth compliance transition.

The cultural integration strategy recognized that Shriram Transport Finance and Shriram City Union Finance, despite sharing the same parent group and philosophy, had developed distinct organizational cultures. Transport Finance had a culture shaped by dealing with truck operators and rural markets, while City Union Finance had evolved serving urban and semi-urban consumers. The integration plan respected these differences while building a unified culture around shared values.

Financial synergies were carefully quantified and communicated to stakeholders. Cost synergies would come from eliminating duplicate corporate functions, optimizing branch networks, and achieving better procurement terms due to scale. Revenue synergies would emerge from cross-selling opportunities, shared customer acquisition costs, and the ability to offer comprehensive financial solutions to customers.

The governance structure of the merged entity was designed to reflect best practices while maintaining the Shriram Group's entrepreneurial spirit. Now a new company (merged) would be formed as 'Shriram Finance' where the promoter holding would be 20%, where there are 2 companies- Shriram Ownership Trust and Shriram Financial Ventures Private Limited (SFVPL). These 2 promoter companies would own 1.88% and 18.23% stakes respectively, while the rest 79.89% would be owned by other Public Shareholders.

Risk management framework integration was critical given the diverse asset classes the merged entity would manage. The combined entity needed unified policies for credit risk, operational risk, market risk, and liquidity risk, while maintaining specialized expertise for different product segments. New risk committees were formed, combining expertise from both legacy entities.

The competitive positioning of the merged entity was significantly enhanced. As India's largest retail NBFC, Shriram Finance would have better access to capital markets, stronger negotiating power with partners, and the scale to invest in technology and innovation. The diversified business model would provide resilience against sector-specific downturns.

International investor communication was carefully orchestrated. The Shriram group companies had significant foreign institutional ownership, and these investors needed confidence that the merger would create value. Roadshows were conducted, detailed merger documents were prepared, and regular updates were provided throughout the process.

The integration execution was remarkably smooth given the complexity involved. Customer attrition was minimal, employee retention remained high, and operational disruptions were avoided. The stock market response was positive, with both stocks performing well as the merger progressed. Due to the acquisition of SHRIRAM CITY UNION FINANCE LTD by SHRIRAM TRANSPORT FINANCE, the shares of SHRIRAM TRANSPORT FINANCE (SRTR.NS) were increased according to the stock terms of the transaction.

Post-merger integration continued well into 2023, with the focus shifting from legal and operational integration to strategic optimization. Product portfolios were rationalized, best practices were identified and scaled across the organization, and new growth initiatives were launched leveraging the combined entity's strengths.

The success of the merger validated the strategic vision of creating a unified financial services powerhouse. The merger of the financial services arm of the group was a sensible action by the Shriram Group, creating a stronger platform for future growth while maintaining the core philosophy of financial inclusion that had driven the group since its inception.

By creating Shriram Finance Limited through this complex merger, the group had not just simplified its corporate structure—it had created a financial services giant with the scale, diversification, and capabilities to compete with banks while maintaining its unique positioning serving India's underserved segments. The merger stands as a case study in executing complex financial services consolidation while maintaining operational excellence and stakeholder value.

VI. The Trust Economy: Customer-Centric Innovation

The essence of Shriram Finance's success lies not in sophisticated algorithms or cutting-edge technology, but in something far more fundamental: trust. Their emphasis on trust and long-term relationships with customers, built through providing tailored financial solutions that were both accessible and sustainable, has created what can only be described as a trust economy—a parallel financial system where reputation matters more than credit scores, and relationships trump documentation.

We are part of the 50 year old Shriram Group, a financial conglomerate that has emerged as a trusted partner in creating transformative experiences and lasting impressions in customers' lives. This isn't corporate speak; it's the lived reality of millions of customers who have experienced financial inclusion for the first time through Shriram. The Shriram Finance Limited is one of the India's leading NBFCs, with 9.56 Million (as on March 31, 2025) private and corporate customers across India.

The philosophy that drives this trust economy is deceptively simple. We pride ourselves on the perfect understanding of the common person. Our financial services are tailor-made to perfectly suit customer needs through quality non-banking financial services. This guiding philosophy of putting people first has brought the company closer to the grassroots, and we are the preferred choice for serving the underserved, nurturing talent, and empowering people.

The trust-based model isn't just philosophy—it's operational reality. During the difficult years of 2012-2013, when the commercial vehicle sector was in crisis, this approach proved its worth. He said to me, "Trust begets trust." There is a social dynamic in relationships known as the Law of Reciprocity—when you're nice to someone, it's a natural human instinct to respond positively. This insight from founder R. Thyagarajan to then-MD Umesh Revankar became the cornerstone of crisis management.

This relationship-based model that we developed worked to our advantage not just during the bad times, but our customers stayed loyal to us even when things started improving, and often recommended STFC to all other truckers as a trusted brand that wouldn't abandon them when times were tough. The result was remarkable: The trust-based lending worked and got us far ahead of the competition. Today (as of September 1, 2022), the company has a market cap of `35,952 crore, assets under management of almost Rs 1.3 lakh crore and over two million customers.

Product innovation at Shriram has always been customer-centric rather than technology-driven. Shriram's customers benefit from a broad range of diverse product portfolio: Fixed Deposits, Fixed Investment Plan, Commercial Vehicle Loans, Passenger Vehicle Loans, Construction Equipment Loans, Farm Equipment Loans, Two-Wheeler Loans, Gold Loans, MSME Finance and Personal Loans. Each product emerged from understanding specific customer needs rather than copying competitors or following global trends.

The Fixed Deposit program exemplifies this approach. While banks offered similar products, Shriram understood that their customers—often without regular banking relationships—needed different service models. They accepted smaller deposits, provided doorstep collection services in some areas, and most importantly, maintained the personal touch that made customers comfortable entrusting their savings to the company.

Gold loans became a particularly successful vertical because Shriram understood the emotional and economic significance of gold in Indian households. Unlike banks that treated gold loans as secured lending products, Shriram recognized they were often emergency funding mechanisms. Speed of disbursement, privacy, fair valuation, and respectful handling of family jewelry became differentiators more important than interest rates.

The MSME finance vertical showcased Shriram's ability to understand business cycles better than traditional lenders. They recognized that small businesses often face temporary cash flow mismatches rather than fundamental viability issues. By structuring loans that aligned with business cash flows—daily collection for vegetable vendors, weekly for small traders, monthly for established shops—they reduced default rates while serving customer needs better.

This leads to considerable reduction in turnaround time between transactions, provides real-time access to required information and also ensures highest standards of transparency in the customer-company relationship. STFC have been able to leverage its well-established technology systems to maintain trust and transparency with its clients. Technology adoption at Shriram has been pragmatic, focused on enhancing rather than replacing human relationships.

The digital transformation journey has been carefully calibrated. Powered by cutting-edge technology, Shriram Finance is a digitally mature financial institution that reflects the banking needs of the Millennial and Gen Z customers. We offer priority financial services to those in the unbanked and underbanked sectors, expanding our innovative product pipeline at every stage of disruption. Yet this digital maturity doesn't come at the cost of personal service—it enhances it.

Shriram Finance Limited (SFL) has entered into a partnership with PhonePe Lending Services Private Limited to offer Unsecured Business loan to PhonePe merchants These partnerships with fintech companies demonstrate Shriram's approach to innovation: collaborate rather than compete, ensuring technology serves the customer rather than replacing the relationship.

The Shriram One app represents this balanced approach to digitalization. It offers comprehensive services—from loan applications to insurance purchases, from fixed deposit management to bill payments—while maintaining the option for customers to visit branches or call customer service. The app isn't meant to replace physical touchpoints but to provide additional convenience for those who want it.

Customer service philosophy at Shriram goes beyond mere transaction processing. At Shriram Finance, we are committed to meeting our customers at every touchpoint of their financial journey so that they get to explore unlimited possibilities through us. This means being present not just when disbursing loans but throughout the customer's financial lifecycle—from the first two-wheeler loan to eventual business expansion financing.

The branch network strategy reflects deep understanding of customer psychology. As on March 31, 2025, with a network of 3,220 branches and a workforce of 79,872 Shriram Finance has combined Assets Under Management (AUM) worth ₹ 263,190.3 crores. These aren't just service points—they're trust anchors in communities where the physical presence of a financial institution matters as much as its products.

Risk management in this trust economy operates on different principles. With the depletion in economic conditions, the company continued to critically scrutinize each asset class and ensured lower delinquencies. With the economic uncertainties profound, STFC chose to grow responsibly rather than grow rapidly. As a result, it reduced Loan-to-value (LTV) ratio by 5 per cent to mitigate any doubts in earning capacity. This led to reduced business but proved a huge fillip for the company's asset quality.

The collection philosophy exemplifies the trust-based approach. Rather than aggressive recovery mechanisms, Shriram focuses on understanding why customers default and working with them to find solutions. This might mean restructuring loans during difficult periods, providing temporary relief during medical emergencies, or helping customers find additional income sources. The approach builds long-term loyalty that transcends individual transactions.

Over the decades, the company has achieved significant success by creating transparency and a strong sense of belonging. Operational efficiency, truthfulness and a robust emphasis on catering to the needs of the common man by providing him with high quality and cost-effective products & services are the values driving Shriram Finance. These core values are deep-rooted within the organization and have been firmly adhered to over the years.

Employee empowerment is crucial to maintaining this customer-centric culture. Branch managers have significant autonomy in decision-making, recognizing that they understand local conditions better than any centralized system. This decentralization might seem risky, but it's essential for maintaining the responsiveness that customers value. Regular training ensures employees understand not just products and processes but the philosophy of inclusive finance.

The feedback loop between customers and product development is remarkably tight. New products often emerge from patterns observed by field staff. When multiple customers in agricultural areas needed loans for bore wells, Shriram developed specialized products. When small traders needed working capital for festival seasons, seasonal loan products emerged. This bottom-up innovation ensures products meet real needs rather than perceived ones.

As a leading financial enterprise with a rich business history, Shriram Finance is founded on inclusion and sustainability, helping us unlock value for generations to come. Our presence spans across the agrarian heartlands of rural India to its vibrant, cosmopolitan metros where we set wings to aspirations. This geographic and demographic diversity isn't just about market coverage—it's about understanding India in all its complexity.

Pricing strategy in the trust economy reflects a sophisticated understanding of value. While Shriram's interest rates are often higher than banks, customers understand they're paying for accessibility, speed, flexibility, and most importantly, availability when banks won't lend to them. The transparency in pricing—no hidden charges, clear communication about total costs—builds trust even when rates are higher.

The role of technology in enhancing transparency has been transformative. Customers can track loan applications, check balances, and understand charges through digital channels. But technology never replaces the human explanation—if a customer doesn't understand something online, they can always walk into a branch or call customer service for clarification.

Community engagement goes beyond traditional corporate social responsibility. Shriram understands that their success is intertwined with community prosperity. Financial literacy programs, health camps for truck drivers, scholarship programs for customers' children—these initiatives build social capital that translates into business success.

Our customer loyalty is a testimony to our journey. This loyalty manifests in multiple ways: customers who return for second and third loans, families where multiple generations bank with Shriram, and most powerfully, customers who become advocates, recommending Shriram to others in their community.

The evolution of customer needs has driven service innovation. As customers prospered—moving from cycles to motorcycles to cars, from small shops to larger businesses—Shriram evolved its products to support this growth. The company became a partner in prosperity rather than just a lender, understanding that customer success directly drives their own growth.

Looking ahead, the trust economy model faces new challenges and opportunities. Younger customers, while valuing digital convenience, still seek the human touch in financial services. The challenge is maintaining personal relationships at scale while leveraging technology for efficiency. Shriram's response has been to use technology to free up human resources for relationship building rather than replacing human interaction entirely.

The trust economy Shriram has built over five decades isn't easily replicable. It's not just about processes or products but about organizational DNA—a fundamental belief that serving the underserved isn't charity but good business, that trust is more valuable than collateral, and that patient relationship building creates more value than aggressive sales. In a world increasingly dominated by algorithmic lending and digital-only banks, Shriram's trust economy stands as proof that human relationships remain at the heart of financial services.

VII. Leadership Philosophy & Corporate Culture

The leadership philosophy of R. Thyagarajan represents one of the most extraordinary examples of value-based capitalism in modern business history. R Thyagarajan gave away more than 750 million dollars (Rs 6210 crore). He gave away all his shareholdings to a group of employees. He transferred the entire money to the Shriram Ownership Trust. This wasn't a retirement gesture or a tax optimization strategy—it was the culmination of a lifetime philosophy that wealth creation should benefit those who help create it.

In 2006, Thyagarajan did something remarkable—he gave away all his shareholdings in Shriram companies to a group of employees. The Shriram Ownership Trust was set up to ensure that those who helped build the company would also benefit from its success. This predated the giving pledges of Western billionaires by years and was done without fanfare or publicity seeking. Thyagarajan's wealth was transferred to the Shriram Ownership Trust, which benefits 44 group executives.

The personal lifestyle of Thyagarajan stands in stark contrast to typical billionaire behavior. R. Thyagarajan, despite his immense wealth, chooses to live modestly. He lives in a simple home, drives a car worth Rs 6 lakh, and doesn't own a mobile phone, as he believes it's a distraction from life's true priorities. This isn't performative frugality—it's a genuine belief that material excess distracts from what truly matters.

Thyagarajan drives a normal car and doesn't own a mobile as he believes they are a distraction. He also lives in a small house. In an era where business leaders compete to display wealth, Thyagarajan's approach is revolutionary in its simplicity. Beyond business, Thyagarajan enjoys classical music and stays updated by reading Western business magazines. These simple pleasures reflect a life focused on intellectual and spiritual enrichment rather than material accumulation.

The philosophical underpinnings of Thyagarajan's approach run deep. Despite his business success, Thyagarajan's focus was not solely on accumulating wealth. A self-proclaimed proponent of leftist beliefs, he aimed to improve the lives of those facing challenges and difficulties. This wasn't socialism imposed on capitalism but a unique synthesis—using market mechanisms to achieve social goals.

R. Thyagarajan is an industrialist and founder of Chennai-based Shriram Group, a financial services conglomerate along with AVS Raja and T. Jeyaraman. He was awarded the Padma Bhushan, India's third highest civilian award, in 2013 in the field of trade and industry. This recognition came not for business success alone but for demonstrating that business could be a force for social transformation.

The timing of Thyagarajan's entrepreneurship is particularly instructive. He started entrepreneurship at an age of 37. He began his entrepreneurial journey at 37, proving that it's never too late to start. Today, his group owns 30 companies and serves over 23 million customers, growing from humble beginnings into a massive enterprise. This late start, after two decades of employment, gave him the maturity and perspective that shaped Shriram's unique culture.

The employee ownership model goes beyond simple wealth sharing. Shriram Capital (formerly Shriram Financial Ventures) is the holding company and promoter of Shriram Group's financial services and insurance businesses. It is jointly owned by Shriram Ownership Trust (59.3%) and Sanlam Group (40.7%). This structure ensures that employees aren't just beneficiaries but owners, aligning long-term interests in a way that traditional compensation never could.

Thyagarajan's journey serves as an inspiring example of how business success can align with social responsibility. By providing accessible financial services while maintaining profitability, he shattered perceptions about lending to the underserved. His legacy in the industry demonstrates that empathy and innovation can lead to transformative impact.

The corporate culture that emerged from this leadership philosophy is unique in Indian business. Decision-making is decentralized, with branch managers having significant autonomy. Employees are encouraged to think like owners because many of them actually are owners through the trust structure. This creates a level of engagement and commitment rare in large organizations.

Compensation philosophy at Shriram reflects these values. While the company might not always match market rates for senior positions, the combination of ownership stakes, job security, and purposeful work creates a different value proposition. Employees stay not for the highest salary but for the opportunity to be part of something meaningful.

In 1974, Thyagarajan founded the Shriram Group in Chennai, initially focusing on lending money to low-income borrowers overlooked by traditional banks. His belief in helping the underserved drove the growth of the group, which now boasts a valuation exceeding USD 750 million (Rs 6210 crore) and comprises 30 companies with over 23 million consumers.

The leadership transition planning at Shriram has been carefully orchestrated to preserve values while bringing in professional management. Rather than creating a family dynasty, Thyagarajan ensured that leadership would pass to professionals who understood and embodied Shriram's philosophy. This approach ensures institutional continuity beyond individual leaders.

Meet Shriram Group's founder R Thyagarajan who views lending money to underserved individuals as welfare, as it caters to the poor and those overlooked by traditional banks. R Thyagarajan is arguably one of the world's most idiosyncratic financiers – in no small part because his multibillion-dollar business, the Shriram Group, has thrived in an industry that tripped up countless others around the globe. His approach involves offering loans at more affordable rates, demonstrating that lending can be both secure and lucrative.

The impact of this leadership philosophy extends beyond Shriram. R Thyagarajan's journey from humble beginnings to becoming an Indian business tycoon with a heart of gold showcases that business success can be a vehicle for positive societal change. His dedication to inclusivity, empathy, and philanthropy has not only reshaped the financial landscape but also left an indelible mark on the lives of countless individuals.

Risk-taking at Shriram is encouraged but within a framework of values. The company will take risks on customers that banks won't serve, but not risks that compromise customer trust. They'll innovate with new products but not if it means exploiting customer ignorance. This principled approach to risk has created sustainable competitive advantages.

R. Thyagarajan's journey exemplifies how business success can be aligned with social responsibility and philanthropy. His dedication to inclusivity and empowerment has reshaped the financial landscape and positively impacted countless lives. As a business tycoon with a heart, Thyagarajan's legacy continues to inspire future generations to pursue success with a conscience.

The learning culture at Shriram emphasizes understanding over credentials. Field experience is valued more than academic qualifications. Employees are encouraged to spend time with customers, understanding their businesses and challenges. This ground-up learning approach ensures that Shriram's products and services remain relevant to customer needs.

Communication within the organization emphasizes transparency and directness. Financial results are shared openly, challenges are discussed frankly, and feedback flows both ways. This transparency builds trust internally, which then translates into the trust-based relationships with customers.

Today, the Shriram Group stands as a testament to Thyagarajan's vision. With a workforce of 108,000 individuals, the group's current valuation surpasses USD 750 million (Rs 6210 crore). The flagship company, Shriram Finance Limited, commands a market value of about 8.5 billion dollars and reported a profit of approximately 200 million dollars in the June quarter.

The succession philosophy ensures continuity of values rather than just business operations. Leaders are developed internally, spending years understanding different aspects of the business. External hires at senior levels are carefully selected not just for expertise but for cultural fit with Shriram's values.

Innovation at Shriram is driven by purpose rather than competition. New products emerge from identified customer needs rather than market gaps. Technology is adopted to serve customers better, not just to reduce costs. Growth is pursued to extend financial inclusion, not just to increase market share.

Thyagarajan has contributed over Rs 6,210 crore to charitable causes and has transferred his shareholdings to an employee trust, reinforcing his commitment to social responsibility. He believes in maintaining focus and simplicity, choosing not to own a mobile phone as he views it as a distraction.

The performance measurement systems at Shriram balance financial and social metrics. Branch success is measured not just by loan disbursements but by customer progression—how many drivers became owners, how many small businesses expanded. Employee evaluations consider not just targets achieved but relationships built and trust maintained.

Conflict resolution within the organization emphasizes reconciliation over punishment. Mistakes are treated as learning opportunities. Disagreements are resolved through discussion rather than hierarchy. This approach creates psychological safety that encourages innovation and honest communication.

The vendor and partner relationships reflect the same philosophy. Shriram works with thousands of small vendors and partners, often helping them grow their businesses. Payments are made promptly, terms are fair, and relationships are long-term. This creates an ecosystem of mutual benefit rather than exploitation.

Looking at the global landscape, Thyagarajan's model offers an alternative to both shareholder capitalism and state socialism. It demonstrates that private enterprise can achieve social goals without sacrificing profitability. It shows that employee ownership can work at scale. Most importantly, it proves that values-based leadership can create enduring business success.

The legacy of R. Thyagarajan isn't just the business empire he built but the demonstration that business can be a force for good without sacrificing commercial success. His life and leadership philosophy stand as a rebuke to the greed-is-good ethos that dominates much of modern capitalism. In giving away his wealth to those who helped create it, he didn't just transfer money—he validated a different vision of what business success can mean.

VIII. Modern Era & Digital Transformation (2010-Present)

The period from 2010 to the present represents Shriram Finance's most dramatic transformation yet—a careful navigation between preserving its core identity as India's trusted lender to the underserved while embracing the digital revolution that threatens to upend traditional financial services. Shriram Finance Limited is set to make a bold mark in India's dynamic fintech landscape, announcing its intention to launch a comprehensive suite of digital payment solutions. As one of the nation's top non-banking financial companies, Shriram Finance is seeking regulatory approval from the Reserve Bank of India to become a Payment System Operator, a move that signals its commitment to redefining digital payments and financial inclusion across the country.

The digital transformation journey began gradually in the early 2010s, as Shriram recognized that technology could enhance rather than replace its relationship-based model. Initial investments focused on backend digitization—core banking systems upgrades, data analytics capabilities, and basic digital channels for customer service. The approach was pragmatic rather than revolutionary, ensuring that technology served the business rather than driving it.

The competitive landscape shifted dramatically during this period. The payments sector is fiercely competitive. Paytm, backed by SoftBank and Alibaba, and PhonePe, owned by Walmart, dominate the UPI space, while Bajaj Finance's entry in 2023 underscored the sector's profitability. New-age fintech companies began targeting the same underserved segments that had been Shriram's exclusive domain, armed with venture capital funding and digital-first approaches.

Shriram Finance's core business—personal loans, auto finance, and insurance—has long thrived in rural and semi-urban markets. By adding payments infrastructure, the company seeks to deepen customer engagement and monetize transaction data. Its CEO, Arul Chakravarthi, emphasized that this move aligns with the firm's "digital-first" vision. This digital-first vision, however, doesn't mean abandoning the physical infrastructure that has been central to Shriram's success.

The financial performance during this transformation period has been remarkable. With a 10% YoY jump in standalone net profit to ₹2,139 crore in Q4 2025, Shriram Finance is financially robust enough to fund the expansion. Shriram Finance's Q4 results underscore its strength. Net interest income surged 13% YoY to ₹6,051 crore, while revenue from operations jumped 21% to ₹11,454 crore. Fee and commission income more than doubled to ₹331 crore, signaling a shift toward recurring revenue streams.

The COVID-19 pandemic accelerated Shriram's digital transformation in ways that years of planning couldn't have achieved. Lockdowns forced even the most traditional customers to embrace digital channels. Shriram responded by rapidly scaling its digital infrastructure, launching video KYC processes, enabling fully digital loan applications, and creating contactless collection mechanisms. What might have taken five years to implement was accomplished in months.

Post-COVID resilience became a defining characteristic of Shriram's modern era. While many NBFCs struggled with asset quality issues and liquidity crunches, Shriram's diversified portfolio and strong customer relationships helped it weather the storm. The company's understanding of its customers' cash flows and business cycles allowed it to restructure loans proactively, maintaining portfolio quality while supporting customers through difficult times.

The company's upcoming digital offerings are designed to meet the evolving needs of modern consumers, including mobile wallets, prepaid cards for food and gifting, and FASTag services. This strategic expansion into digital payments is expected to provide customers with a secure, seamless, and cashless experience, perfectly aligning with the growing demand for digital convenience in daily transactions.

The 2024 sale of Shriram Housing Finance to Warburg Pincus for ₹4,630 crore represented a strategic portfolio optimization. Rather than trying to be everything to everyone, Shriram chose to focus on its core strengths while monetizing non-core assets at attractive valuations. This transaction provided capital for digital investments while simplifying the corporate structure.

Already a powerhouse in consumer finance, insurance, and housing finance, Shriram Finance's foray into the fintech sector is a natural progression in its mission to offer comprehensive financial solutions under one trusted brand. The company's vast network, strong brand reputation, and deep understanding of the Indian market position it advantageously as it prepares to compete with established fintech players and other NBFCs. By integrating digital payments into its portfolio, Shriram Finance is not only enhancing customer engagement but also reinforcing its role as a key driver of India's financial digitalisation.

The technology challenges facing Shriram are significant. As financial technology (fintech) rapidly evolves, Shriram Finance faces the challenge of staying competitive with new digital offerings. Falling behind on tech advancements, such as AI-driven lending or blockchain-based solutions, could result in a loss of market share to more agile, tech-savvy competitors, affecting the company's growth trajectory and stock valuation.

Partnership strategies have become crucial in the digital era. Rather than trying to build everything in-house, Shriram has partnered with technology providers, fintech companies, and digital platforms. These partnerships allow Shriram to offer cutting-edge services while focusing on its core competency of understanding and serving India's underserved segments.

As Shriram Finance continues to digitize its services to stay competitive, it faces cybersecurity risks. Any data breaches or tech failures could lead to operational disruptions, reputational damage, and regulatory fines, all of which could negatively affect the stock. The company has invested heavily in cybersecurity infrastructure, understanding that trust in the digital age requires not just personal relationships but also data security.

The regulatory environment has evolved significantly during this period. The Reserve Bank of India has introduced stricter norms for NBFCs, particularly around digital lending and data privacy. Shriram has proactively engaged with regulators, often exceeding compliance requirements to maintain its reputation as a responsible lender.

Industry experts believe that Shriram Finance's entry will intensify competition, bringing fresh energy and innovation to the market, while leveraging its established customer base and extensive reach in semi-urban and rural areas. As the fintech sector continues to evolve, all eyes will be on how Shriram Finance leverages its legacy, expertise, and innovative approach to deliver secure, user-friendly, and inclusive digital solutions for millions of Indians.

Market dynamics have shifted with the rise of digital lending platforms. Competition now comes not just from banks and NBFCs but from pure-play digital lenders who can offer instant loans through apps. With the non-banking financial company (NBFC) sector in India becoming increasingly competitive, Shriram Finance may face challenges in maintaining its market share. Aggressive competition from both new and established players could put pressure on its margins and limit growth, which might impact its stock performance.

The customer acquisition strategy has evolved to blend digital and physical channels. While younger customers might discover Shriram through digital marketing and apply for loans online, the company maintains its branch presence for customers who prefer face-to-face interactions. This omnichannel approach ensures no customer segment is left behind.

Data analytics has become a crucial competitive advantage. Shriram's decades of lending data provide insights that new fintech entrants lack. By applying modern analytics techniques to this historical data, Shriram can make better credit decisions, identify cross-selling opportunities, and predict customer needs before they articulate them.

The product innovation pipeline has accelerated. Beyond traditional loans, Shriram now offers digital gold, insurance products through partnerships, and is exploring embedded finance opportunities. The goal is to become a comprehensive financial services provider while maintaining the trust and accessibility that defines the brand.

Shriram Finance's entry into digital payments is a high-risk, high-reward bet. On one hand, its rural footprint and financial muscle position it to capture a slice of India's $2.2 trillion digital payments market. The 21% YoY revenue growth and robust net interest income suggest it can weather the upfront costs.

Employee capability building has been a major focus area. Traditional relationship managers are being trained in digital tools, data analysis, and new product offerings. The company has hired digital natives for specialized roles while ensuring knowledge transfer between generations of employees.

The rural digitization opportunity remains massive. As smartphone penetration increases and internet connectivity improves in rural India, Shriram is uniquely positioned to bridge the digital divide. The company's trusted brand and physical presence provide the comfort factor needed to encourage digital adoption among traditionally conservative customer segments.

Regulatory technology (RegTech) adoption has helped Shriram manage compliance more efficiently. Automated reporting, real-time monitoring, and predictive compliance tools ensure that the company stays ahead of regulatory requirements while reducing compliance costs.

The sustainability agenda has gained prominence. Shriram has begun incorporating ESG (Environmental, Social, and Governance) factors into its lending decisions, recognizing that sustainable business practices are increasingly important to investors, regulators, and customers alike.