Shringar House of Mangalsutra: The Category King of the Sacred Thread

I. The "Invisible Giant" of the Indian Wedding

Picture the scene inside any Tanishq showroom during wedding season. The glass cases gleam with kundan sets, diamond bangles, and temple-gold necklaces. A mother and daughter-in-law lean over one particular counter, voices animated. They are not debating earrings or anklets. They are selecting the mangalsutra — the sacred black-and-gold thread that a bride will wear every single day of her married life. It is arguably the most emotionally charged purchase in the entire Indian jewelry ecosystem. And there is a very good chance the piece they are holding was not designed or manufactured by Tanishq at all.

It was made by a company most consumers have never heard of: Shringar House of Mangalsutra Limited.

India's jewelry market is estimated at roughly eighty billion dollars, making it one of the largest in the world. The names that dominate public consciousness are the retail behemoths — Titan's Tanishq, Malabar Gold and Diamonds, Kalyan Jewellers, Joyalukkas. These are the brands that run the full-page newspaper ads, sponsor cricket tournaments, and open gleaming high-street stores. But behind these retail facades sits a vast, largely invisible supply chain of specialized manufacturers. And within that supply chain, Shringar occupies a position so unusual it borders on the absurd: this is a company that does exactly one thing. It makes mangalsutras. Nothing else. No bangles, no rings, no earrings, no necklaces. Just the sacred thread.

Think of it as the "picks and shovels" play of the Indian wedding boom. While retail jewelers battle each other for foot traffic, pay exorbitant rents in malls and high streets, and pour money into brand advertising, Shringar sits upstream, supplying them all. It serves thirty-four corporate clients — including several of the biggest names in Indian retail jewelry — along with over a thousand wholesalers and eighty-one retailers across twenty-four states and four Union Territories. Its business model is pure B2B. No storefronts. No consumer marketing battles. Just an obsessive focus on being the single best manufacturer of one product category.

India hosts roughly ten million weddings every year. In the vast majority of Hindu ceremonies, the mangalsutra is not optional. You might negotiate down the size of the trousseau. You might skip the extra pair of jhumkas. But you do not skip the mangalsutra. It occupies a cultural position somewhere between a wedding ring and a religious sacrament — a symbol so deeply embedded in the social fabric that even as Gen Z Indians reimagine traditions, the mangalsutra endures, albeit in more contemporary designs. Shringar recognized this non-discretionary demand decades before anyone thought to build a company around it.

The story that follows traces how a 1963 goldsmith workshop in Mumbai transformed itself into the dominant organized manufacturer of India's most culturally essential piece of jewelry. It is a story about the power of radical specialization, about a family that resisted the temptation to diversify when every instinct in Indian business culture pushes toward becoming a conglomerate, and about a B2B company that quietly built what may be one of the most defensible niche positions in the entire Indian consumer economy. From a cramped workshop to a 2025 IPO valued at roughly seventeen hundred crores, from processing eight hundred kilograms of gold a year to building capacity for four thousand kilograms — this is the Shringar playbook.

II. Founding and The Great Pivot

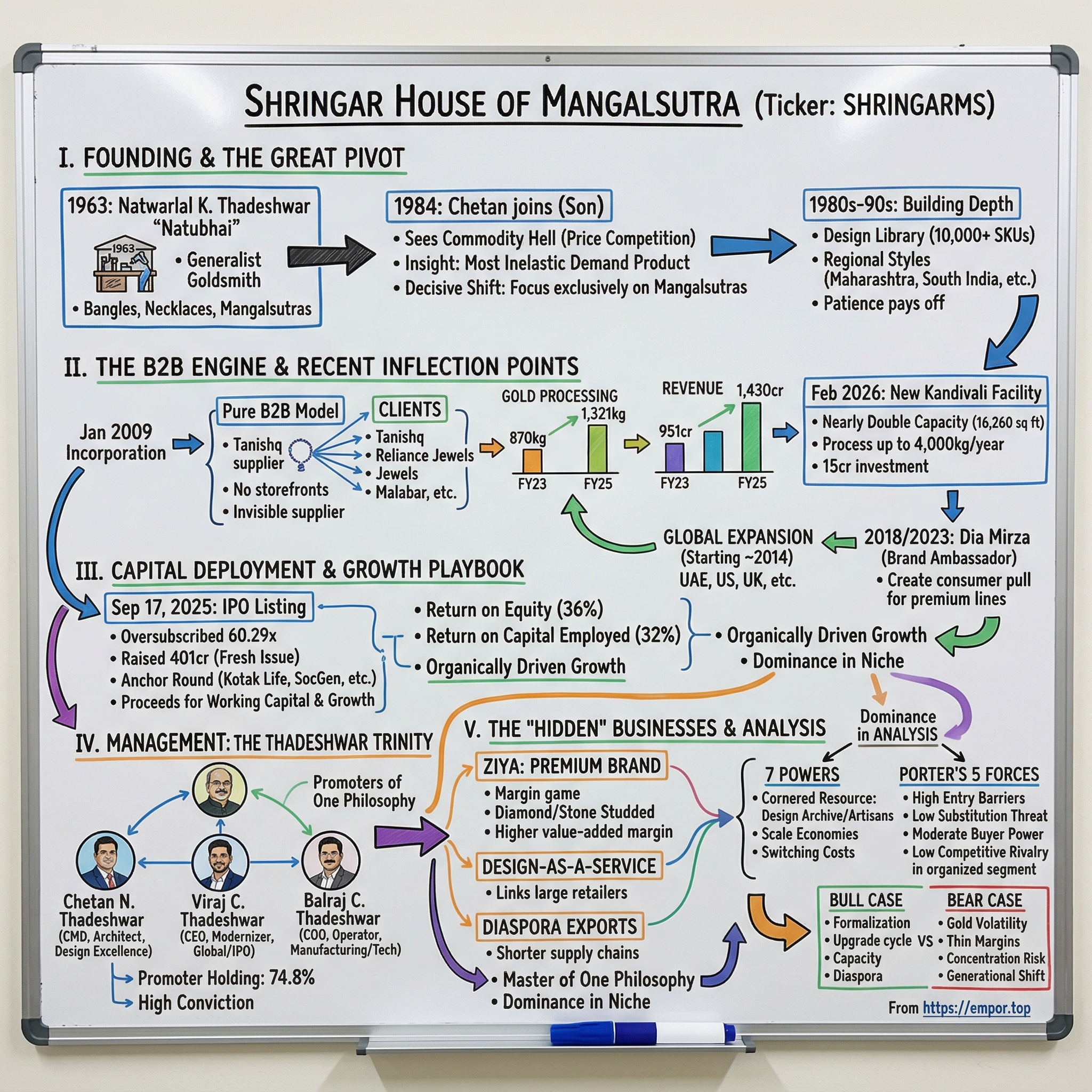

The jewelry bazaars of 1960s Mumbai were a world unto themselves — narrow lanes in neighborhoods like Zaveri Bazaar and Kalbadevi, where goldsmiths worked in workshops barely larger than a living room, hammering, soldering, and setting stones under fluorescent tube lights. It was in this milieu that Natwarlal K. Thadeshwar — known to everyone as Natubhai — established himself in 1963 as a master goldsmith specializing in bridal jewelry. Natubhai was not running a business in the modern sense. He was running a craft workshop, one of thousands in Mumbai, producing whatever jewelry his clients demanded: bangles, necklaces, nose rings, ear studs, mangalsutras.

This was the traditional model of Indian jewelry manufacturing, and it had remained essentially unchanged for centuries. A goldsmith was a generalist. He made what was ordered. His competitive advantage was his hands — the precision of his craftsmanship, the trust of his local network, and his ability to deliver on time during the frenetic wedding seasons of November through February and April through June. There was no branding, no specialization, no scale. If you were a particularly skilled goldsmith, your reward was more orders, which you fulfilled by hiring more artisans into your workshop.

Natubhai was, by all accounts, exceptionally skilled, particularly with mangalsutra designs. But the business remained what it was — a traditional workshop operation, profitable but constrained, growing linearly with the number of hands it could employ.

The inflection point came in 1984, when Natubhai's son Chetan joined the family business. Chetan had grown up watching his father's workshop and understood its economics intimately. He could see the fundamental problem: in the generalist model, you were always competing on price with the workshop next door. Your margins were thin because your clients could always find another goldsmith who would do the same work for slightly less. You were, in Silicon Valley terminology, stuck in commodity hell.

Chetan's insight was deceptively simple but radical in its implications. He looked at the entire catalog of bridal jewelry and asked: which product has the most inelastic demand? Which piece does every single customer absolutely have to buy, regardless of their budget? The answer was obvious — the mangalsutra. A bride's family might economize on bangles or skip the matching earrings. But the mangalsutra was non-negotiable. It was the one purchase with near-zero price elasticity in the context of a wedding budget.

So Chetan made what his peers in the Zaveri Bazaar must have thought was a lunatic decision. He stopped making everything else. No more bangles. No more necklaces. No more rings. The workshop would make mangalsutras and only mangalsutras.

This was not how business was done in the Indian jewelry trade. Diversification was survival. You never knew which product category would be in demand next season, so you offered everything. Chetan was turning this logic on its head. His argument was that by focusing every rupee of capital, every hour of design time, and every artisan's skill on a single product, Shringar could become so good at making mangalsutras that it would be the obvious choice for any retailer or wholesaler looking for reliable, high-quality supply. In an industry of generalists, the specialist would be king.

The logic was sound, but the execution required patience. It took years — through the late 1980s and 1990s — for the strategy to bear fruit. Chetan invested in building a design library that was exclusively focused on mangalsutra variations: regional styles from Maharashtra, South India, Gujarat, and Bengal; traditional patterns and contemporary interpretations; gold-only designs and pieces incorporating black beads, pearls, and stones. While competitors spread their design resources across dozens of product categories, Shringar was accumulating what would become a proprietary archive of over ten thousand active SKUs — all mangalsutras.

The formal incorporation came relatively late, in January 2009, when the business was registered as Shringar House of Mangalsutra Private Limited. But the strategic foundation had been laid a quarter century earlier, in that pivotal moment when Chetan chose depth over breadth. It was a decision that would define everything that followed — a bet that in a fragmented, commoditized industry, the company that mastered one category would ultimately capture disproportionate value. The "Master of One" philosophy, long before the phrase became a Silicon Valley cliché, was already the Thadeshwar family's operating principle.

III. The B2B Engine and Recent Inflection Points

To understand how Shringar actually makes money, you have to understand the plumbing of India's jewelry supply chain — because it looks nothing like what most consumers imagine.

When a customer walks into a Tanishq store and picks out a mangalsutra, they assume Titan designed and manufactured it. Sometimes that is true. But more often, particularly for specialized categories like mangalsutras, the large retailers outsource manufacturing to specialists. The retailer provides the gold (or buys it through the manufacturer), specifies a design from a catalog, and the manufacturer produces the finished piece. The retailer then sells it under their own brand, with their own hallmark, at their own markup.

Shringar is the backend of this process for some of the biggest names in Indian jewelry. Titan's Tanishq, Reliance Retail's Reliance Jewels, Malabar Gold, GRT Jewellers, Joyalukkas — the company's client list reads like a who's who of Indian jewelry retail. As of fiscal year 2025, Shringar served thirty-four corporate clients, over a thousand wholesalers, and eighty-one retailers. This is a pure B2B operation. Shringar does not operate a single retail store. It does not sell directly to consumers. It is, in the truest sense, the invisible supplier behind the glass counter.

The economics of this model are worth dwelling on. A retail jeweler like Tanishq has to pay for prime real estate, hire sales staff, run advertising campaigns, manage consumer financing, and deal with returns and exchanges. Their operating margins, while healthy by retail standards, are burdened by these costs. Shringar, by contrast, has none of these expenses. Its costs are gold (the primary raw material), labor, manufacturing overhead, and a modest sales infrastructure. The company's operating margin hovered around six percent in recent years — which sounds thin until you realize that in jewelry manufacturing, the revenue base is dominated by the cost of gold passing through the books. The actual value-added margin on the manufacturing and design work is considerably higher than the headline number suggests.

The period from 2009 to 2023 saw Shringar systematically industrialize what had been an artisanal craft. The company's original manufacturing facility in Lower Parel, Mumbai, spanned about 8,300 square feet. It was a capable operation, but it had a ceiling. Processing capacity was roughly 2,500 kilograms of gold per year, and utilization was running at sixty to seventy percent in most years.

Look at the gold processing trajectory to understand the growth: in fiscal 2023, the company processed 870 kilograms. By fiscal 2024, that jumped to 1,221 kilograms. In fiscal 2025, it reached 1,321 kilograms. Revenue followed the same curve — from 951 crores in fiscal 2023 to 1,103 crores in fiscal 2024 to 1,430 crores in fiscal 2025. That is a three-year revenue compound annual growth rate of roughly twenty-one percent, and a near-doubling of net profit from 23 crores to 61 crores over the same period.

But the real step-change came in February 2026, when Shringar inaugurated a new manufacturing facility in Kandivali, a suburb of Mumbai. At 16,260 square feet — nearly double the Lower Parel operation — the Kandivali plant represented a quantum leap in capacity. The new facility can process up to 4,000 kilograms of gold annually, a sixty percent increase over the old plant's theoretical maximum. The investment was roughly fifteen crores, financed entirely through internal accruals. Commercial production began on February 23, 2026, with full incremental capacity expected to come online by mid-2026.

The global expansion story adds another dimension. Starting around 2014, Shringar began supplying international markets — initially the UAE, where a large Indian diaspora drives significant demand for traditional wedding jewelry. The company now exports to the United States, United Kingdom, New Zealand, and Fiji, serving diaspora-focused jewelers like Damas Jewellery in the Gulf. The logic is straightforward: Indian families abroad still perform traditional weddings, still require mangalsutras, but have fewer local sources of high-quality, authentic designs. Shringar fills that gap, and the export channel tends to carry higher margins because it bypasses layers of domestic wholesale intermediation.

Then there was the move that puzzled industry observers: in 2018, Shringar appointed Bollywood actress and social activist Dia Mirza as its brand ambassador. Why would a B2B company that does not sell to consumers spend money on celebrity branding? The answer reveals a sophisticated understanding of how B2B demand actually works in the jewelry industry. When a consumer walks into a jewelry store and specifically asks for a "Shringar-style" or "Ziya" mangalsutra, that creates pull-through demand that makes it harder for retailers to switch to a different supplier. The brand ambassador was not about selling to consumers directly — it was about making consumers aware enough to influence their retailers' purchasing decisions. Dia Mirza was reappointed in 2023, specifically to represent the premium Ziya collection, and the company has described her as embodying "elegance and empowerment — qualities that resonate with modern women." For a B2B manufacturer, this kind of consumer-facing investment is unusual, and it speaks to a management team that understands the full dynamics of its supply chain.

IV. Capital Deployment and the Growth Playbook

On September 17, 2025, Shringar House of Mangalsutra listed on both the BSE and NSE at a price of 188.50 rupees per share — a 14.24 percent premium over its IPO price of 165 rupees. The listing was, by any measure, a validation. The IPO had been oversubscribed 60.29 times, with institutional investors (QIBs) leading the charge at over 101 times subscription. Even retail investors — typically more cautious with unfamiliar names — subscribed 27 times over. The company raised approximately 401 crores through a fresh issue of 2.43 crore equity shares, with no offer for sale component. This meant the Thadeshwar family was not cashing out — every rupee raised was going into the company.

The anchor round, completed ahead of listing, brought in institutional names including Kotak Mahindra Life Insurance, Societe Generale, and Maybank Securities, who collectively invested 120 crores at the IPO price. For a company that most of the market had never heard of, this was a notable vote of confidence from sophisticated capital allocators.

Where is the money going? The prospectus was refreshingly clear: roughly 280 crores was earmarked for working capital, with the remainder allocated to general corporate purposes. In jewelry manufacturing, working capital is the lifeblood. Gold is expensive, payment cycles with large retailers can stretch, and the ability to carry sufficient inventory of finished and semi-finished goods during peak wedding season is what separates reliable suppliers from those who miss delivery windows. The IPO proceeds, in essence, were ammunition for growth — enabling Shringar to take on larger orders from existing clients and onboard new ones without straining its balance sheet.

One aspect of Shringar's capital deployment that deserves close attention is the Kandivali plant investment. At fifteen crores for a facility that nearly doubles production capacity, the spend was remarkably efficient. Compare this to what a retail jeweler would invest to open a single flagship store — often fifty crores or more for build-out, inventory, and initial operating costs. Shringar's approach to capital is fundamentally different from the retail jewelry model. Instead of acquiring brands or prime retail real estate, the company acquires manufacturing capacity. The return profile is different: lower glamour, but significantly higher return on invested capital because you are not paying for foot traffic.

The company's balance sheet tells a story of disciplined growth. Total borrowings stood at 123 crores in fiscal 2025, against a net worth of roughly 201 crores. Post-IPO, with the 401 crore infusion, the debt-to-equity profile improved substantially. Return on equity was running at 36 percent and return on capital employed at nearly 32 percent in fiscal 2025 — figures that would be exceptional in almost any industry, let alone one as capital-intensive as gold manufacturing.

The stock's journey since listing has been instructive. After listing at 188.50, shares rallied to a fifty-two-week high of 266.50 rupees — roughly sixty-one percent above the IPO price — as the market digested the company's growth numbers and unique positioning. But the subsequent correction brought the price back to around 180 rupees by early April 2026, roughly where it listed. This round-trip is not unusual for recent IPOs in India, where initial euphoria often gives way to a more sober assessment. At 180 rupees, the stock traded at approximately eighteen times trailing earnings — a moderate multiple for a company growing revenue at over twenty percent annually and profit at even faster rates.

The question investors are wrestling with is whether Shringar should be valued like a manufacturer — in which case eighteen times earnings is fair or even generous — or like a branded consumer franchise with switching costs and pricing power, in which case it looks cheap relative to retail jewelers trading at twenty-five to forty times earnings. The answer likely lies somewhere in between, and much depends on whether the Ziya brand and the consumer-pull strategy can shift the company's positioning over time.

One thing is clear: Shringar has not pursued acquisitions as a growth strategy. There are no reported M&A transactions in the company's history. Growth has been entirely organic — expanding the product catalog, deepening relationships with existing clients, adding new wholesale and retail accounts, and investing in manufacturing capacity. In an era when many newly listed Indian companies rush to deploy IPO proceeds on acquisitions of dubious strategic value, Shringar's restraint is notable. The management team appears to believe that their competitive advantage lies in doing one thing exceptionally well and scaling that capability, not in diversifying into adjacent categories.

V. Management: The Thadeshwar Trinity

In the cramped design rooms of Shringar's offices, somewhere between the CAD workstations and the sample trays, a ritual plays out regularly. A new collection is being finalized. The designers have done their work, the prototypes are ready, and the production team is standing by. But nothing moves to manufacturing until one person signs off: Chetan N. Thadeshwar, Chairman and Managing Director, the man who has been making mangalsutras for over forty years and who, even now, insists on personally reviewing key designs.

Chetan is the architect of Shringar's identity. It was his decision in 1984 to pivot exclusively to mangalsutras, his patience that sustained the strategy through the lean years when the bazaar doubted the wisdom of such radical specialization, and his deep knowledge of regional design traditions — Maharashtrian, South Indian, Gujarati, Bengali — that built the catalog into what is now a library of over ten thousand active designs. He serves not just as CMD of Shringar but as a zonal committee member of the All India Gem and Jewellery Domestic Council, a role that keeps him plugged into the broader industry ecosystem. At industry events, he is known as a quiet but authoritative presence — the kind of person other jewelers seek out for technical opinions on alloy composition or stone-setting techniques. He reportedly authored a coffee table book titled "The Story of Mangalsutra," an effort to document the cultural and artistic heritage of the product category he has spent his life mastering.

The next generation entered the business in two waves. Viraj C. Thadeshwar, Chetan's son, joined the company from its formal inception in February 2009, making him a fifteen-year veteran by the time of the IPO. As Executive Director and CEO, Viraj represents the modernizing force in the family. His domain is everything that extends beyond the workshop floor: the global expansion into the UAE, US, UK, New Zealand, and Fiji; the institutional investor relationships that culminated in the 2025 IPO; and the strategic positioning of the Ziya premium brand. Where Chetan's strength is in craft and design, Viraj's contribution has been in building the corporate infrastructure — the kind of systems, processes, and institutional relationships that transform a family-run manufacturing operation into a company that institutional capital can trust.

Balraj C. Thadeshwar, Chetan's second son, joined in June 2019 as Whole-time Director and COO. Holding a bachelor's degree in management studies from the University of Mumbai, Balraj oversees the day-to-day operations — the manufacturing floor, supply chain logistics, artisan workforce management, and the integration of new technologies including 3D printing and advanced CAD/CAM systems. With the new Kandivali facility ramping up, Balraj's operational role has become increasingly central to the company's execution capability.

Together, the three form a complementary triad that is unusually well-suited to the company's current stage: a founder-generation visionary who guarantees design excellence and cultural authenticity; a second-generation strategist managing growth, capital, and global expansion; and a second-generation operator ensuring the manufacturing engine can deliver on the promises the other two make.

The skin-in-the-game story is compelling. Promoter holding stands at 74.8 percent — an exceptionally high figure even by Indian standards, where promoter-led companies are the norm. The IPO was a one hundred percent fresh issue with no offer for sale, meaning the family sold zero shares at listing. This level of retained ownership sends an unambiguous signal about the family's conviction in the company's long-term trajectory. When three-quarters of the equity sits with the people making day-to-day decisions, the alignment between management and minority shareholders is about as tight as it gets.

The post-IPO transition from a private family business to a publicly listed entity has required adjustments. The company now operates under a structured governance framework with independent directors, a formal CFO in chartered accountant Ritesh Doshi, and the disclosure obligations that come with an NSE listing. The shift from what were presumably "family drawings" — the traditional method by which promoter families extract cash from their businesses — to a more transparent compensation structure linked to performance metrics and dividends is still in its early stages, but the framework is in place.

One human note: in March 2026, the Thadeshwar family experienced a loss when Rasilaben Natwarlal Thadeshwar — a member of the promoter group and likely the wife of founder Natubhai — passed away on March 13. She held no shares at the time, but her passing represents the closing of a chapter that connects the current enterprise back to its origins in that 1963 workshop.

VI. The "Hidden" Businesses

Walk into Shringar's showroom — the one space where the company does display its work, not to sell but to show wholesale buyers what is possible — and you will notice that the mangalsutras are not all the same. Some are traditional: heavy gold chains with black beads and a simple pendant. These are the workhorses, the volume drivers, the bread-and-butter designs that account for the majority of orders. But then your eye catches something different. A piece where the pendant is set with stones, where the chain features intricate filigree work, where the design would not look out of place in a Cartier window display. This is Ziya.

Ziya is Shringar's premium brand, and it represents the single most important strategic initiative for the company's margin profile. While the core mangalsutra business is a volume game — process as many kilograms of gold as possible with consistent quality and competitive pricing — Ziya is a margin game. The premium collection features higher-value materials, more complex craftsmanship, and designs that target younger, urban, style-conscious women who view the mangalsutra not just as a religious obligation but as a fashion statement.

The brand positions itself as "the ONLY brand in the mangalsutra space" — a claim that is more defensible than it might initially sound, because most mangalsutras are sold as unbranded products through retail jewelers' own labels. By creating a distinct brand identity for its premium line, Shringar is effectively trying to do what Intel did with "Intel Inside" — create consumer awareness for a component brand that sits inside someone else's finished product. This is where the Dia Mirza partnership becomes strategically coherent: she is the face of Ziya, not of Shringar's commodity business, and her appointment is designed to create the aspirational pull that drives consumers to ask for the premium line by name.

The economics of the shift from plain gold to premium stone-studded pieces are significant. A basic gold mangalsutra is priced primarily on gold weight, which means the manufacturer's value-added margin is relatively thin — a few percentage points on top of the gold price. But when you add diamond or gemstone setting, intricate design work, and brand positioning, the value-added component rises dramatically. The gold content becomes a smaller proportion of the total price, and the margin on craftsmanship and design increases correspondingly. This is why the segment data matters: the diamond and premium stone category has been growing from what was roughly five percent of the company's product mix toward what management clearly envisions as a much larger share.

Beyond Ziya, Shringar has quietly built another valuable business line that rarely gets mentioned in analyst reports: design-as-a-service. Large retailers do not just buy finished mangalsutras from Shringar — they buy access to the company's design capabilities. Shringar's proprietary library of over ten thousand active designs, built over four decades of single-category focus, is a resource that no competitor can replicate quickly. When a retailer like Tanishq or Malabar needs to refresh their mangalsutra collection for the upcoming wedding season, they often turn to Shringar's design team for trend forecasting and new concepts. This is high-margin, knowledge-intensive work that leverages the company's deep expertise in a way that pure manufacturing alone does not.

The diaspora export arm deserves separate attention because its economics are structurally different from the domestic business. When Shringar supplies a domestic wholesaler, there are typically multiple intermediaries between the manufacturer and the end consumer, each taking a margin. In the export channel — serving jewelers in the UAE, US, UK, New Zealand, and Fiji — the supply chain is shorter. Shringar works more directly with diaspora-focused retailers, often on a smaller number of higher-value orders. The "Brand India" premium is real in these markets: Indian families abroad are willing to pay more for authentic, high-quality mangalsutras sourced from recognized Mumbai manufacturers, and the competitive landscape is far less crowded than in domestic markets where thousands of small workshops compete for business.

All three of these "hidden" businesses — Ziya, design-as-a-service, and diaspora exports — share a common thread: they allow Shringar to capture more value per kilogram of gold processed. As the new Kandivali facility ramps up and processing capacity expands toward four thousand kilograms annually, the mix between volume-driven commodity work and margin-rich premium and export work will be the single most important driver of profitability. If premium and export segments grow from their current levels to, say, a quarter of the total mix, the impact on bottom-line margins could be transformative, even if headline revenue growth slows.

VII. The Playbook: Seven Powers and Five Forces

To understand why Shringar's competitive position is more durable than it might appear to a casual observer, it helps to examine the business through two analytical frameworks that sophisticated investors use to assess the quality and longevity of competitive advantages.

Start with Hamilton Helmer's Seven Powers — the framework that asks what structural forces could allow a company to sustain excess returns over time.

The most obvious power Shringar possesses is what Helmer calls a Cornered Resource. In Shringar's case, the cornered resources are twofold. First, there is the Thadeshwar design archive — four decades of accumulated mangalsutra-specific design knowledge, encompassing over ten thousand active SKUs across regional styles, contemporary interpretations, and premium collections. This archive is not simply a catalog of drawings. It embodies an understanding of cultural nuances, regional preferences, seasonal trends, and manufacturing feasibility that can only be built through decades of single-minded focus. You cannot hire consultants to replicate it. You cannot buy it. It must be accumulated. Second, there is the karigar network — the community of skilled artisans trained specifically in Shringar's techniques and quality standards. In an industry facing a well-documented shortage of skilled craftspeople, having a deep bench of experienced artisans who understand the specific requirements of mangalsutra production at industrial scale is a genuine advantage that cannot be quickly replicated.

Scale Economies represent the second power. At 4,000 kilograms of annual gold processing capacity, Shringar operates at a scale that no other specialized mangalsutra manufacturer in India approaches. This scale advantage manifests in several ways: better negotiating power on gold procurement, lower per-unit manufacturing overhead, the ability to invest in advanced CAD/CAM and 3D printing technologies that smaller workshops cannot justify, and the capacity to serve multiple large clients simultaneously without creating bottlenecks. For a small workshop processing a few hundred kilograms a year, the economics of investing in a 16,000-square-foot modern facility with advanced machinery simply do not work. Shringar has crossed the scale threshold where its unit economics become increasingly difficult for smaller competitors to match.

The third and perhaps most underappreciated power is Switching Costs. When a major retailer like Tanishq integrates Shringar into its supply chain for a specific mangalsutra catalog, switching to a different manufacturer is not a simple decision. The retailer has invested time qualifying Shringar's quality, aligning design catalogs, establishing delivery protocols, and training their own teams on Shringar's product specifications. During peak wedding season — when any disruption to inventory can mean lost sales measured in crores — the risk of switching to an unproven manufacturer is enormous. The switching cost is not financial in the traditional sense; it is operational risk. A retailer will not change a supplier that delivers consistently, even if a competitor offers a slightly lower price.

Now apply Porter's Five Forces to understand the industry dynamics.

Barriers to Entry are high and getting higher. The organized mangalsutra manufacturing segment requires a combination of design expertise, manufacturing infrastructure, quality certification, relationship networks with major retailers, and working capital to carry gold inventory. You cannot replicate forty years of mangalsutra-specific CAD/CAM designs overnight. You cannot build relationships with Tanishq or Reliance Jewels without a track record of consistent delivery. And the capital required to set up a modern facility — even at Shringar's relatively modest investment of fifteen crores for Kandivali — is prohibitive for the small workshop operators who constitute the bulk of the competition.

Threat of Substitution is remarkably low. In the context of a traditional Indian wedding, there is no substitute for a mangalsutra. Alternative wedding jewelry formats — synthetic materials, non-gold options, Western-style wedding bands as sole marital symbols — have not gained meaningful traction. Interestingly, the data suggests the opposite of what one might expect: younger Indian couples are not abandoning the mangalsutra but rather upgrading it, moving from plain gold to diamond-studded and designer versions. This "upgrade cycle" plays directly into Shringar's premium Ziya segment.

Buyer Power is moderate. Shringar's largest clients are massive corporations with significant negotiating leverage. Tanishq and Reliance could, in theory, pressure Shringar on pricing. However, the switching costs discussed above, combined with the relatively small portion of the retailer's total procurement that any single supplier represents, limit the extent to which buyers can extract value. Moreover, Shringar's design capabilities give it leverage that a commodity manufacturer would not have — retailers are paying not just for gold processing but for design innovation and trend forecasting.

Supplier Power is limited. Gold is a commodity traded on global exchanges, so no individual supplier has pricing power. Shringar's scale as a buyer — processing over a thousand kilograms annually — gives it access to competitive procurement rates.

Competitive Rivalry within the organized mangalsutra manufacturing segment is, counterintuitively, low. This is because the segment is barely organized. Shringar holds approximately six percent of India's organized mangalsutra market as of calendar year 2023, yet positions itself as the country's only large-scale, organized, specialized mangalsutra manufacturer. The competition comes primarily from thousands of small, unorganized workshops — the very model that Natubhai Thadeshwar operated before Chetan's pivot. These workshops compete on price in local markets but cannot match Shringar's scale, consistency, design range, or ability to serve national and international retailers.

The combination of these structural advantages creates what looks like a durable competitive moat. It is not an impregnable fortress — no business position ever is — but it would take a competitor years and significant capital to replicate what Shringar has built. The most likely competitive threat comes not from other manufacturers but from the large retailers themselves deciding to vertically integrate mangalsutra manufacturing in-house. However, the economics and operational complexity of doing so have historically kept retailers focused on their core competency: selling to consumers.

VIII. The Bull vs. Bear Case and Epilogue

The bull case for Shringar rests on a compelling convergence of structural tailwinds.

India's middle class is expanding rapidly, and with it, the average wedding budget. The mangalsutra, as a non-discretionary purchase, captures a portion of every wedding regardless of economic conditions — but as household incomes rise, families are upgrading from basic gold to premium, stone-studded designs. This "upgrade cycle" is Shringar's most powerful growth driver because it shifts the product mix toward higher-margin segments. A family that once bought a plain gold mangalsutra for fifty thousand rupees now considers a diamond-studded Ziya piece for two or three times that amount. The gold throughput is similar, but the value-added margin is dramatically higher.

The formalization of India's jewelry industry is another tailwind. Government mandates around hallmarking (the HUID system that Ziya prominently features), GST compliance, and anti-money-laundering regulations are systematically squeezing out unorganized workshops that cannot meet these requirements. Every small workshop that shuts down represents potential market share flowing to organized players like Shringar. With only six percent of the organized market, the runway for share gains is enormous.

The Kandivali facility expansion provides the physical capacity to capture this opportunity. Going from roughly 1,300 kilograms of actual processing to a theoretical capacity of 4,000 kilograms means the company can nearly triple its output without another major capital expenditure. If demand materializes — and the trajectory of ten million annual Indian weddings plus a growing diaspora suggests it will — the operating leverage embedded in this capacity expansion could drive significant profit growth.

The diaspora opportunity adds a geographic dimension to the growth story. Indian communities in the Gulf, North America, and the UK represent a market that is underserved by organized, branded mangalsutra manufacturers. Shringar's early moves into these markets position it to capture this demand before competitors recognize the opportunity.

Now for the bear case, because no investment thesis is complete without stress-testing the narrative.

Gold price volatility is the most obvious risk. Shringar's revenue is heavily influenced by the price of gold — when gold prices rise, revenue inflates even if unit volumes are flat, and when prices fall, the reverse occurs. More importantly, sharp gold price movements can disrupt buying patterns. A sudden spike in gold prices can cause consumers to postpone mangalsutra purchases or trade down to lighter, cheaper designs. While the non-discretionary nature of the mangalsutra provides some insulation, it is not immunity.

The six percent operating margin, while structurally explained by the pass-through nature of gold costs, leaves limited room for error. Any combination of rising labor costs, gold price volatility, or client pressure on manufacturing charges could compress margins below a level where the business generates adequate returns. The company's profitability is highly sensitive to the value-added spread between what it pays for gold and what it charges for finished products.

Concentration risk is real. While the company serves thirty-four corporate clients, the largest few — Tanishq, Reliance, Malabar — likely represent a disproportionate share of revenue. The loss of any single major account, while unlikely given switching costs, would have an outsized impact.

The generational shift in Indian wedding culture is the most existential bear argument, though also the most speculative. If younger Indians begin to view the mangalsutra as an outdated symbol, or if interfaith and cross-cultural marriages (which may not involve mangalsutras) grow significantly as a percentage of total weddings, the addressable market could shrink. Current data does not support this thesis — mangalsutra adoption remains robust, and the trend is toward modernization of design rather than abandonment of the tradition — but it is a long-term risk worth monitoring.

For investors tracking Shringar's ongoing performance, two key performance indicators stand out as the most revealing.

The first is gold throughput per quarter — the number of kilograms of gold actually processed and shipped. This is the single most direct measure of business volume, cutting through the noise of gold price fluctuations. If throughput is growing, the manufacturing engine is humming. If it stalls, something is wrong — either demand is weakening or capacity utilization is declining.

The second is revenue per kilogram of gold processed. This metric captures the product mix shift from basic gold mangalsutras to premium, stone-studded designs. If revenue per kilogram is rising faster than gold price movements alone would explain, it means the company is successfully moving up the value chain — selling more Ziya, more design-intensive pieces, more export-channel products. This is the margin story, and it matters more for long-term profitability than top-line revenue growth.

As the company reported trailing twelve-month sales of roughly 1,872 crores and a market capitalization of approximately 1,740 crores as of early April 2026, Shringar trades at a price-to-sales ratio below one — a rarity for a company with its growth profile and competitive positioning.

The final reflection on Shringar is perhaps the most interesting. In an Indian business culture that celebrates conglomerates — the Tatas, the Ambanis, the Adanis, each sprawling across dozens of industries — Shringar represents the opposite philosophy. It is a company that survived and thrived by refusing to grow wide. Where peers diversified into diamonds, gold coins, silverware, and fashion jewelry, Shringar chose to grow deep into a single product category. The Thadeshwars bet their family's legacy on the proposition that mastery of one thing is more valuable than competency in many things. Four decades later, processing over a thousand kilograms of gold annually, supplying the biggest names in Indian retail jewelry, and carrying a market capitalization that would have seemed fantastical to Natubhai in his 1963 workshop, that bet appears to have paid off.

The question now is whether the next chapter — the post-IPO chapter, the Viraj-and-Balraj chapter, the Kandivali chapter — can sustain that disciplined focus while scaling the business to meet the enormous opportunity in front of it. If Shringar can resist the very human temptation to diversify into adjacent categories and instead keep deepening its dominance in the one market where it has an unassailable position, the company may prove that the most powerful strategy in business is not doing more things, but doing one thing better than anyone else in the world.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube