Shilpa Medicare: The Oncology API Pioneer's Journey from Raichur to Global Markets

I. Introduction & Episode Roadmap

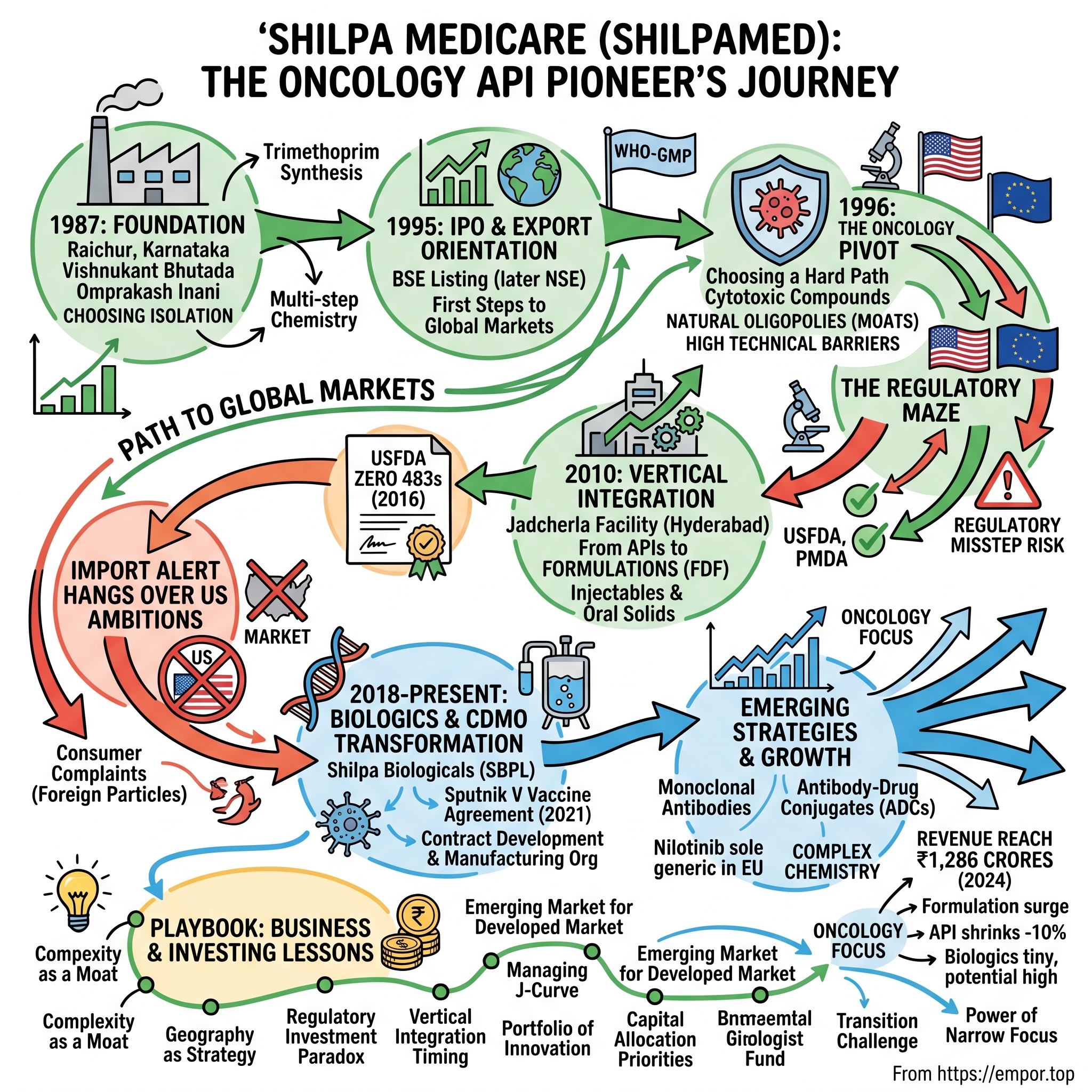

Picture this: A dusty industrial area in Raichur, Karnataka, 1987. While India's pharmaceutical giants clustered around Hyderabad and Mumbai, a group of entrepreneurs led by Vishnukant Bhutada chose this unlikely location—400 kilometers from Bangalore, far from any major pharma hub—to start what would become one of India's most specialized oncology API manufacturers. Today, Shilpa Medicare commands an ₹8,596 crore market capitalization, exports to over 100 countries, and runs facilities approved by the world's strictest regulators.

The central question isn't just how they got here—it's why a company would deliberately choose the hardest possible path in pharmaceuticals. While peers chased volume with simple generics, Shilpa bet everything on complex oncology molecules. While others stayed in APIs, they integrated forward into formulations. And just when that playbook was working, they pivoted again—into biologics and contract manufacturing.

This is a story about finding competitive advantage through complexity. It's about building in India's tier-3 cities for the world's tier-1 markets. And it's about the peculiar economics of cancer drugs—where a single successful molecule can generate hundreds of crores, but a single regulatory misstep can shut down entire facilities.

For investors, Shilpa Medicare presents a fascinating puzzle. Here's a company with regulatory approvals from FDA, EMA, PMDA Japan, and a dozen other agencies—moats that take decades to build. Yet it trades at valuations suggesting the market doesn't quite believe the story. Revenue grew 11.56% in 2024 to ₹1,286 crores, but the API business actually shrank 10%. The formulation business surged 64%, but an unresolved FDA import alert hangs over their US ambitions.

What you'll learn in this deep dive: How pharmaceutical companies really make money (hint: it's not just about the molecules). Why oncology APIs create natural oligopolies. How Indian pharma companies navigate the regulatory maze of selling to developed markets. And perhaps most importantly—whether Shilpa's transformation from manufacturer to services provider represents the future of Indian pharma or a risky departure from core competencies.

Let's start where all great business stories begin—with an entrepreneur who saw opportunity where others saw obstacles.

II. The Foundation Story: Building from Raichur (1987-1995)

The year was 1987, and India's pharmaceutical industry was experiencing its first golden age. The Patent Act of 1970 had created a reverse-engineering paradise, allowing Indian companies to copy any drug as long as they used a different process. But while Ranbaxy and Dr. Reddy's were making headlines in Delhi and Hyderabad, Vishnukant Bhutada was quietly setting up shop in Raichur—a choice that raised eyebrows across the industry.

"Why Raichur?" was the question everyone asked. The answer revealed the strategic thinking that would define Shilpa's next four decades. Land was cheap—dramatically so compared to established pharma hubs. Labor was available and eager. Most importantly, the Karnataka government was offering incentives to bring industry to its northern districts. But Bhutada saw something else: isolation as advantage. Away from the talent-poaching and competitive intelligence gathering of pharma clusters, Shilpa could build its capabilities in relative secrecy.

The company's first product choice was equally telling: Trimethoprim IP/BP, an antibiotic intermediate requiring multi-step synthesis. While competitors were importing and tableting simple molecules, Shilpa started with complex chemistry. The technology was developed entirely in-house—no licensing, no technical collaboration, just Indian chemists working with basic equipment to crack the synthesis. Commercial production began in November 1989, and within months, the product was being exported. The partnership that would shape Shilpa's governance came through an unexpected route. Omprakash Inani, who had more than 35 years of business experience and would become Chairman, wasn't originally from pharma. He was Managing Director of Inok Cottons Private Limited, part of Raichur's thriving cotton economy. His involvement brought not just capital but crucial local connections—as Managing Committee Member of Karnataka State Cotton Association, Hubli, he understood how to navigate Karnataka's business ecosystem. This cotton-pharma alliance might seem odd, but it reflected a pattern common in Indian business: diversification through partnerships that brought complementary strengths.

Vishnukant Bhutada, one of the founder members, became the main guiding force behind the company's progress. With a bachelor's degree in pharmacy and a chemist's mindset, he embodied the technical DNA that would define Shilpa. His dedication and foresight positioned Shilpa Medicare as one of the leading suppliers of oncology pharmaceutical ingredients—though that specialization would come later. In these early years, the focus was simpler: prove you could manufacture to international standards from a tier-3 Indian city.

The transformation from partnership to public company happened with remarkable speed. In November 1993, Shilpa Medicare converted to a Public Limited Company, listing on the Bombay Stock Exchange on June 19, 1995, and later on the National Stock Exchange on December 3, 2009. The 1995 IPO raised modest capital—just enough to expand the product line beyond Trimethoprim. But more importantly, it forced the company to professionalize. Quarterly reporting, board meetings, auditor scrutiny—these weren't just compliance burdens but discipline mechanisms that would prove crucial when dealing with global regulators.

By 1995, Shilpa had established the three pillars of its early strategy: complex chemistry capabilities (not just buying and tableting), export orientation from day one, and most critically, the willingness to tackle products others avoided due to technical difficulty. Revenue was still in the low crores, but the foundation was set. The question now was where to focus this capability—and the answer would transform not just Shilpa but create a template for Indian pharma's evolution from supplier to specialist.

III. The Oncology Pivot: Finding the Niche (1995-2010)

The boardroom discussion in 1996 was heated. Should Shilpa continue as a broad-spectrum API manufacturer, competing with hundreds of Indian companies in antibiotics and vitamins? Or should they specialize? The answer came from an unlikely source: a rejected customer inquiry. A European company needed an oncology API but couldn't find an Indian supplier willing to handle the cytotoxic compound. The safety requirements were daunting, the volumes were small, and the regulatory scrutiny was intense. Every major Indian pharma company had passed.

Bhutada saw opportunity where others saw obstacles. Oncology APIs represented everything the Indian pharma industry typically avoided: high technical barriers, expensive safety infrastructure, limited market size per molecule, and extreme regulatory oversight. But flip those challenges around, and you had a business with natural moats. Few competitors meant better pricing. Regulatory approvals became competitive advantages. And cancer prevalence was rising globally—slowly but inexorably.

The economics of oncology were counterintuitive but compelling. While a blockbuster antibiotic might sell thousands of kilograms annually, a cancer drug might move just hundreds. But the value per kilogram could be 10-100x higher. More importantly, oncology APIs weren't commoditized. Each synthesis required specialized handling, containment systems, and waste treatment. Workers needed extensive training in handling cytotoxic materials. The entire factory floor had to be redesigned with negative pressure systems and specialized HVAC.

Building these capabilities took years and absorbed every rupee of profit. The first dedicated oncology block, completed in 1998, looked like something from a science fiction movie—workers in full protective suits, airlocks between sections, specialized waste treatment that could neutralize cytotoxic compounds. The investment seemed excessive for a company with less than ₹50 crores in revenue. But it was table stakes for the game Shilpa wanted to play. The regulatory journey started with WHO-GMP certification in the late 1990s—table stakes for any serious exporter. Subsequently, Shilpa Medicare gained World Health Organization-Good Manufacturing Practices (GMP) Certificate recognition. But Bhutada understood that WHO-GMP was just the beginning. The real money was in regulated markets: US, Europe, Japan. Each required different standards, different documentation, different inspection protocols.

The first major breakthrough came with European approvals in the early 2000s. Then came the prize: FDA approval for the Raichur facilities. The inspection process was grueling—five days of scrutiny, every batch record examined, every SOP challenged. But when the approval came through, it transformed Shilpa's market position overnight. Suddenly, they could sell to the world's largest pharmaceutical market.

By 2010, Shilpa had assembled an impressive collection of regulatory badges: API facilities approved by USFDA, EU, Cofepris-Mexico, PMDA-Japan, Korean FDA, TPD Canada, and TGA-Australia. Each approval represented years of work and millions in investment. But more importantly, each created a higher barrier for competitors. A Chinese company might offer lower prices, but could they match Shilpa's regulatory track record?

The numbers told the story of transformation. Shilpa Medicare successfully set up a 100% EOU project in FY10 incurring capital expenditure of nearly Rs.1000 million. This wasn't just expansion—it was a statement of intent. The Export Oriented Unit would focus exclusively on complex oncology molecules for regulated markets. By 2010, Shilpa was supplying more than 30 oncology APIs to various regulated markets including USA, Europe, Japan, South Korea, Russia, Mexico, and Brazil.

The technical moat was equally impressive. Handling cytotoxic compounds required specialized equipment—isolators, contained transfer systems, dedicated HVAC with HEPA filtration. Workers underwent months of training. Quality control procedures were exponentially more complex than standard pharmaceuticals. A single contamination event could shut down production for weeks. This complexity scared away competitors but created pricing power for those who mastered it.

As the decade closed, Shilpa faced a strategic inflection point. They'd proven they could manufacture complex APIs to global standards. But APIs were ultimately commodities—even complex ones. The real margins were in finished formulations. The question was whether a company built on chemistry could master the entirely different discipline of drug formulation. It would require new facilities, new expertise, and most dauntingly, new regulatory approvals. But the potential rewards—moving from ingredient supplier to drug manufacturer—were too significant to ignore.

IV. Vertical Integration: From APIs to Formulations (2010-2018)

The board meeting in early 2010 was tense. CFO presentations showed the stark reality: despite all their regulatory approvals and technical capabilities, Shilpa's API margins were under pressure. Chinese manufacturers had learned to make oncology APIs too, and while they couldn't match Shilpa's quality consistency, they could undercut on price. Meanwhile, Shilpa's customers—the big pharma companies buying their APIs—were capturing 70-80% of the value chain by turning those APIs into finished drugs.

"We're leaving money on the table," Bhutada argued. The math was compelling. An oncology API might sell for $1,000 per kilogram. That same kilogram, formulated into injectable vials, could generate $10,000 or more in revenue. The margin expansion wasn't just incremental—it was transformational. But the risks were equally large. Formulation required entirely different expertise: pharmaceutical scientists instead of chemists, cleanrooms instead of reactors, lyophilization instead of crystallization.

The decision to build a formulation facility in Jadcherla, near Hyderabad, was strategic on multiple levels. First, it put Shilpa in India's pharma capital, making it easier to recruit formulation experts. Second, it created physical separation from the API operations—crucial for regulatory compliance. Third, it allowed Shilpa to present itself as a full-service oncology company, not just an ingredient supplier.

Construction began in 2011, and even by Shilpa's standards, the specifications were ambitious. The facility would produce both injectable and oral oncology formulations. The injectable suite included isolator technology—robotic systems that allowed operators to work with cytotoxic drugs without direct exposure. The investment was staggering for a company of Shilpa's size, but Bhutada saw it as existential. "Either we move up the value chain, or we get squeezed out of the market. "The product portfolio that emerged was impressive in scope. Shilpa's Formulation (Oral Solids & Injections) manufacturing facility located at Jadcherla, Telangana, has been issued EU GMP certificate by AGES, Austria for the inspection done during 13 to 17 Jan 2020. The facility produced formulation products consisting of 16 injectable dosage forms and 19 oral solid dosage forms under SML. Additionally, wholly owned subsidiary Shilpa Therapeutics manufactured 13 formulations, focusing on innovative delivery systems.

The real validation came from FDA approvals. Formulation facility audited by USFDA from July 18 to July 26, 2016 and audit was successfully completed with Zero 483s. This was extraordinary—most facilities receive observations (483s) that require remediation. Zero 483s meant Shilpa's quality systems were considered flawless by the world's strictest regulator.

The product approvals started flowing. Shilpa Medicare Limited formulation division has received U.S Food and Drug Administration final approval for its ANDA, Docetaxel Injection USP, 20 mg/mL, 80 mg/4 mL (20 mg/mL), and 160 mg/8 mL (20 mg/mL) on 16.05.2019. Docetaxel was a blockbuster oncology drug. Shilpa Medicare Ltd formulation division has received U.S Food and Drug Administration final approval for its ANDA, Zoledronic Acid Injection, 4 mg/5 mL on 15.05.2019. Each approval represented not just a product but validation of Shilpa's transformation.

The economics of integration proved even better than projected. Where Shilpa previously sold APIs at commodity prices to formulators, they now captured the entire value chain. A kilogram of API that generated ₹10 lakhs in revenue might yield ₹50-100 lakhs when formulated and packaged. Margins expanded from 15-20% on APIs to 30-40% on formulations. Customer relationships deepened—instead of being one supplier among many, Shilpa became a strategic partner offering end-to-end solutions.

But success bred complexity. Running formulation facilities required different skills than API manufacturing. Quality control became exponentially more complex—testing not just chemical purity but dissolution profiles, stability, sterility. Regulatory requirements multiplied. Each market had different packaging requirements, labeling rules, serialization mandates. The Jadcherla facility needed its own management team, quality systems, and culture.

The real test came in February 2020. Shilpa Medicare Limited has successfully completed USFDA inspection at both API sites located at Raichur (Unit-1 & Unit-2) between 3rd and 7th Feb, 2020 with ZERO 483s. Two facilities, two inspections, zero observations—a feat that established Shilpa among the elite of Indian pharma. But just as they were celebrating, a different FDA inspection at the formulation facility would reveal challenges that would haunt them for years.

The warning signs were subtle at first. Consumer complaints for batches of injection related to the presence of foreign particles; these complaints have not been properly evaluated to prevent reoccurrence. Your investigation concluded, with no scientific evidence, that the root cause was related to the use of a [specific device] by the end user. What seemed like isolated incidents would cascade into a full import alert, shutting Shilpa out of the US formulation market just as they were gaining momentum.

As 2018 ended, Shilpa faced a crossroads. The formulation strategy had worked—technically and commercially. But the regulatory challenges showed the risks of vertical integration. Meanwhile, the pharmaceutical industry itself was transforming. Biologics were displacing small molecules. Contract manufacturing was booming as big pharma outsourced production. The question wasn't whether to evolve, but how fast and in which direction.

V. The Biologics & CDMO Transformation (2018-Present)

The pharmaceutical industry's tectonic plates were shifting in 2018, and Bhutada could feel it. At industry conferences, every conversation circled back to biologics—complex proteins manufactured in living cells rather than chemical synthesis. The top 10 drugs by revenue were increasingly biologics. Oncology, Shilpa's specialty, was going biological with checkpoint inhibitors and monoclonal antibodies commanding $100,000+ per patient per year. The writing wasn't just on the wall; it was in flashing neon.

"We can either watch our market shrink or we can evolve," Bhutada told the board. The challenge was that biologics required completely different capabilities. Instead of chemical reactors, you needed bioreactors. Instead of crystallization, you needed chromatography columns the size of industrial refrigerators. Instead of chemists, you needed cell biologists. The investment required would dwarf anything Shilpa had attempted.

The strategy that emerged was characteristically ambitious: build biologics capability while simultaneously transforming into a Contract Development and Manufacturing Organization (CDMO). The logic was compelling. Global pharma companies were increasingly outsourcing manufacturing, especially for complex products. A CDMO model would provide steadier revenues than the lumpy income from launching individual products. And Shilpa's regulatory track record—those coveted FDA and EMA approvals—would be their calling card. The proof of concept came unexpectedly in 2021. Shilpa Biologicals Private Limited (SBPL), Shilpa's wholly-owned subsidiary, entered into a three-year definitive agreement with Dr. Reddy's Laboratories for production-supply of Sputnik V vaccine from its integrated biologics R&D cum manufacturing center at Dharwad. The timing was perfect—India desperately needed vaccine manufacturing capacity during COVID-19. The targeted production of the dual vector Sputnik V for the first 12 months was 50 million doses (50 million of Component 1 and 50 million of component 2), from the date of start of commercial production.

This wasn't just a manufacturing deal—it was validation. Dr. Reddy's, one of India's pharmaceutical giants, chose Shilpa's biologics facility for one of the most high-profile products in the world. The technology transfer process revealed how far Shilpa had come. The company views Biologics as a strategic growth area and has made significant investments in setting up a High end, Flexible Biologics facility in Dharwad to cater to the requirements of the fast growing biologics field, that include the adenoviral, subunit & DNA vaccines, Monoclonal antibodies & fusion proteins.

The CDMO transformation happened in parallel. Shilpa launched a new full-service 'hybrid' CDMO with oncology as therapeutic specialty, serving both small and large molecules customers as well as peptides. The offering was comprehensive: discovery, clinical, and commercial outsourcing services plus commercially ready 'off-the-shelf' novel formulations for exclusive B2B licensing. This wasn't just contract manufacturing—it was positioning Shilpa as a development partner.

The economics were compelling but lumpy. Biologics segment revenue of 15-20 crores from just one product (Atalia) in the last financial year was expected to double in FY26. The biologics division overall was expected to double sales due to additional indications approval. But these weren't linear growth stories—a single successful biosimilar could generate hundreds of crores, while development failures could burn through capital with no return. The recent milestones validated the strategy. Company's biologics arm Shilpa Biologics site at Dharwad, Karnataka, has received its European GMP certification for manufacturing of test batches based on the inspection between February 18-20, 2025, conducted by the competent authority of Austria. The inspection was closed with Zero observations. This EU GMP approval was crucial—it opened doors to European CDMO opportunities at a time when Western companies were desperately seeking alternatives to Chinese manufacturers.

The ambition kept expanding. Shilpa Biologicals, a full-service contract development and manufacturing organisation (CDMO), announces the opening of a dedicated bioconjugation suite at its Dharwad site in India. This wasn't just another manufacturing line—it was entry into one of pharma's hottest areas: antibody-drug conjugates (ADCs). At full capacity, the bioconjugation suite will be able to manufacture about 30 kg of ADC per year.

The strategic partnerships revealed Shilpa's evolving role in the global pharma ecosystem. mAbTree Biologics has signed an exclusive co-development and commercialisation partnership with Shilpa Biologicals Pvt, a fully owned subsidiary of Shilpa Medicare, for its biologic asset for immuno-oncological applications. This wasn't just contract manufacturing—Shilpa was becoming a development partner for innovative biotechs.

But transformation came with challenges. The biologics division, while growing rapidly, was still subscale. The CDMO business required different commercial capabilities—relationship management, project management, regulatory support across multiple products and clients simultaneously. Most critically, the capital intensity was staggering. Each new capability—whether biosimilars, ADCs, or viral vectors—required specialized equipment, expertise, and validation.

The market response was mixed. While the stock price surged on regulatory approvals and partnership announcements, fundamental investors remained skeptical about execution. Could a company with ₹1,286 crores in revenue really compete with global CDMO giants? Was the biologics pivot too late, given that Chinese and Korean companies had years of head start? And most pressingly—with the unresolved FDA import alert still hanging over the formulation business, could Shilpa execute multiple transformations simultaneously?

As 2024 ended, Shilpa stood at an inflection point. The pieces were in place—world-class facilities, regulatory approvals, strategic partnerships. But the question remained whether they could execute fast enough to capture the opportunity before competitive windows closed.

VI. Financial Performance & Market Dynamics

The numbers tell a story of transformation—messy, non-linear, but ultimately pointing upward. In 2024, Shilpa Medicare's revenue reached ₹1,286 crores, up 11.56% year-over-year. But that headline number masks dramatic shifts underneath. Earnings surged 145.63% to ₹78.29 crores—a jaw-dropping jump that had analysts scrambling to understand what changed.

Dig into the segment data and the picture becomes clearer—and more complex. API Business Revenue came in at INR 182 crores, down 10% YoY. This was the core business, the foundation Shilpa was built on, and it was shrinking. Pricing pressure from Chinese competitors, customer consolidation, patent cliffs on key molecules—the headwinds were multiple and mounting.

Yet Formulation Revenue told a different story: INR 118 crores, up 64% YoY. Despite the FDA import alert limiting US access, other markets were taking off. Europe, Australia, emerging markets—everywhere Shilpa had approvals, formulation sales were accelerating. The margin differential was even more dramatic. Where APIs might generate 15-20% EBITDA margins, formulations were delivering 30-35%.

The real surprise was biologics. At INR 18 crores, up 43% YoY, it was still tiny—less than 2% of total revenue. But the trajectory was exponential. From essentially zero three years ago to potential doubling in FY26, this was hockey-stick growth in its early stages. More importantly, biologics contracts came with upfront payments, milestone revenues, and long-term supply agreements—steadier, more predictable income than the lumpy API business.

But zoom out to a five-year view and concerns emerge. Sales growth averaged just 7.22% annually over the past five years—barely above inflation. Return on equity languished at 1.57% over the last three years. For a company with such impressive operational capabilities, why weren't the financials following?

The answer lay in the business model's inherent lumpiness. Pharmaceutical revenues don't grow linearly. A single FDA approval can add ₹100 crores overnight. A lost tender can subtract ₹50 crores just as quickly. Patent expirations create cliffs. New product launches create spikes. The licensing revenue model amplified this volatility—one quarter might see ₹30 crores in milestone payments, the next quarter nothing.

Capital allocation revealed management's priorities—and challenges. The company was simultaneously funding API capacity expansion, formulation facility upgrades, biologics infrastructure, and CDMO capabilities. Each required not just capital expenditure but working capital as inventory cycles stretched with more complex products. The balance sheet showed the strain—debt levels creeping up even as profitability improved. The Q3 FY25 results provided a snapshot of the transformation in progress. Net Profit: ₹32 crore, a significant increase compared to ₹4.6 crore in Q3 FY24, marking a strong turnaround. Revenue: ₹319 crore, up 11% from ₹287 crore YoY, driven by increased demand across key product categories. More impressively, EBITDA: ₹81 crore, up 21.4% from ₹66.4 crore YoY, indicating operational efficiency improvements. EBITDA Margin: Improved to 25.2% from 23% YoY, showcasing effective cost management.

The margin expansion story was particularly compelling. Despite API pricing pressure, overall margins were expanding due to the formulation and biologics mix shift. Vishnukant Bhutada, managing director of Shilpa Medicare, said, Our 3QFY25 performance reflects robust growth in profitability driven by an improved business mix. The quarter witnessed healthy YoY growth in our key verticals of FDF & Biologics, which was partially offset by muted API performance.

The competitive landscape added another layer of complexity. In APIs, Shilpa competed with Chinese giants who could leverage scale and lower costs. In formulations, they faced established Indian players like Sun Pharma and Cipla with deeper pockets and broader portfolios. In biologics, they were late entrants competing against companies with years of head start. Yet Shilpa's narrow focus—oncology—gave them expertise that broader competitors couldn't match.

The market's valuation reflected this uncertainty. Trading at 3.63 times book value with a market cap of ₹8,596 crores, Shilpa was valued like a commodity API manufacturer rather than an integrated pharma company. The unresolved FDA import alert cast a long shadow—until that cleared, US formulation revenues (potentially the highest margin business) remained off-limits.

Looking at cash flows revealed the capital intensity challenge. Every new product required upfront investment in development, regulatory filing, and inventory build. The CDMO business required even more working capital as Shilpa had to maintain raw material inventory for clients. The biologics facility alone had absorbed hundreds of crores with meaningful revenues still years away.

Yet management remained optimistic. During the quarter we have launched Nilotinib in the EU region, where we are a sole generic; on the biologics front, we have initiated Ph3 trials for Aflibercept; and we have initiated commercial launch quantities for OLC, a US CDMO opportunity. I am also highly optimistic on receiving approval for our NCE NorUDCA in this financial year. With positive traction on our new product launches in the coming quarters, I am confident of delivering strong revenue growth in each business vertical.

The financial story, ultimately, was one of transition. The old model—selling commodity APIs with thin margins—was dying. The new model—integrated oncology specialist with biologics and CDMO capabilities—was being born. The question for investors was whether they had the patience to wait for the transformation to complete and whether management could execute without stumbling on the numerous operational and regulatory hurdles ahead.

VII. Regulatory Challenges & Quality Journey

The warning letter arrived in October 2020, and with it, Shilpa's US formulation dreams came crashing down. The FDA inspection at the Jadcherla facility had identified significant violations of current good manufacturing practice (CGMP) regulations. The details were damning: You received multiple consumer complaints for batches of (b)(4) Injection related to the presence of foreign particles; these complaints have not been properly evaluated to prevent reoccurrence. Your investigation concluded, with no scientific evidence, that the root cause was related to the use of a (b)(4) by the end user. You indicated that you evaluated the drug product using (b)(4) and observed no problem, while the complainants used an (b)(4). You do not have sufficient scientific data, including but not limited to functionality test data, to support your root cause that the foreign particles and stopper separations or "seal coring" defects are caused by the use of a (b)(4).

This wasn't Shilpa's first regulatory rodeo. Inadequate OOS investigations is a repeat CGMP violation from the 2017 FDA inspection. The pattern was concerning—despite all their technical capabilities, quality systems were failing at critical moments. The import alert that followed effectively banned Shilpa's formulations from the US market, shutting off what should have been their highest-margin revenue stream.

The irony was painful. Just months earlier, Shilpa had celebrated zero 483s at their API facilities. They had dozens of regulatory approvals globally. Yet here they were, locked out of the world's largest pharmaceutical market due to quality system failures that seemed almost elementary—not investigating customer complaints properly, not having sufficient scientific data to support conclusions.

The remediation effort that followed was massive. Consultants were hired—former FDA inspectors who knew exactly what the agency wanted to see. Quality systems were rebuilt from the ground up. Standard operating procedures were rewritten. Training programs were revamped. The investment ran into crores, but more costly was the opportunity loss—every month without US market access meant lost revenues and damaged customer relationships.

The global regulatory landscape Shilpa navigated was extraordinarily complex. Each geography had different requirements, different inspection approaches, different documentation standards. What passed in Europe might fail in Japan. What Japan accepted, Brazil might reject. Maintaining compliance across all these jurisdictions required an army of regulatory professionals and quality assurance staff—overhead that smaller competitors simply couldn't afford.

Yet when Shilpa got it right, the results were spectacular. The recent certifications told the story: EU GMP for Jadcherla with zero observations. Saudi Arabia GMP for the Bengaluru facility with zero observations. The biologics facility receiving EU GMP clearance with zero observations. These weren't just certificates—they were validations of capability, tickets to the global pharmaceutical game.

The cost of this quality infrastructure was staggering. Industry estimates suggested maintaining FDA compliance alone cost ₹10-15 crores annually in personnel, systems, and consultants. Add EU, Japan, Australia, and other markets, and the number could triple. For a company with ₹1,286 crores in revenue, this represented a significant fixed cost burden. But it was also a moat—competitors couldn't enter these markets without similar investments.

The learning curve had been steep and expensive. Early inspections revealed gaps in documentation, training, investigation procedures. Each failure taught lessons, but at tremendous cost. The 2017 FDA observations about OOS (Out of Specification) investigations. The 2020 warning letter about complaint handling. Each revealed systemic issues that required not just fixes but cultural change.

What emerged from this crucible was a more sophisticated understanding of quality. It wasn't just about following procedures—it was about building a culture where quality was everyone's responsibility. Where operators felt empowered to stop production if something seemed wrong. Where investigations sought root causes, not convenient explanations. Where documentation wasn't a burden but a discipline.

The unresolved import alert remained the elephant in the room. Industry sources suggested resolution could take 2-3 years—if everything went perfectly. Re-inspection, demonstration of sustained compliance, gradual product-by-product clearance. The process was glacial, and there were no shortcuts. Meanwhile, competitors were capturing market share Shilpa should have owned.

But there was a silver lining. The regulatory challenges had forced Shilpa to build world-class quality systems. The same capabilities that would eventually get them back into the US market were opening doors elsewhere. European customers, seeing the EU GMP certifications with zero observations, were increasingly comfortable with Shilpa as a supplier. Japanese partners appreciated the attention to detail. The CDMO business benefited from clients' confidence in Shilpa's quality systems.

The regulatory journey, ultimately, was about maturation. From a company that could make complex molecules to one that could make them consistently, documentably, and in full compliance with the world's strictest standards. The price had been high—in money, time, and lost opportunities. But what emerged was a company capable of competing at the highest levels of global pharma.

VIII. Playbook: Business & Investing Lessons

The Shilpa Medicare story offers a masterclass in building competitive advantage through deliberate complexity. While business schools teach simplification and focus, Shilpa's journey suggests the opposite can work—if you have the patience and capital to see it through.

Lesson 1: Complexity as a Moat The decision to focus on oncology APIs wasn't about following market demand—it was about finding a space where competition would be limited by technical and regulatory barriers. Every additional level of complexity—cytotoxic handling, containment requirements, waste treatment—scared away competitors. What looked like operational headaches were actually competitive advantages. The principle: In commoditizing industries, complexity that others avoid becomes your differentiation.

Lesson 2: Geography as Strategy Starting in Raichur seemed like a disadvantage—far from talent pools, infrastructure, and customers. But it provided cost advantages that funded early growth and isolation that prevented talent poaching. More importantly, it forced Shilpa to build everything in-house—from R&D to training programs—creating capabilities that companies in clusters often outsourced. The insight: Sometimes being far from the action forces you to build muscles that become competitive advantages.

Lesson 3: Vertical Integration Timing Shilpa's move from APIs to formulations came when API margins were still healthy—not when they were desperate. This gave them breathing room to learn, fail, and iterate. Too many companies integrate vertically as a defensive move when their core business is struggling. Shilpa did it offensively, using profits from APIs to fund formulation capabilities. The lesson: Vertical integration works best when you don't need it yet.

Lesson 4: The Regulatory Investment Paradox Every regulatory approval Shilpa obtained—FDA, EMA, PMDA—required massive upfront investment with uncertain returns. But collectively, they created a barrier that grew stronger over time. A new competitor would need to spend years and crores just to reach the starting line. The paradox: Regulatory compliance is a cost center that becomes a profit center through competitive advantage.

Lesson 5: Managing the J-Curve Shilpa's financial performance followed a classic J-curve pattern. New initiatives—whether formulations, biologics, or CDMO—required upfront investment that depressed margins before generating returns. Managing this required patient capital and clear communication with stakeholders. Many companies abandon transformative initiatives during the downward part of the J-curve. Shilpa's persistence through multiple J-curves created today's diversified platform.

Lesson 6: The Portfolio Approach to Innovation Rather than betting everything on one breakthrough, Shilpa built a portfolio: multiple APIs, various formulations, different biologics, CDMO services. Some would fail—like certain API molecules facing Chinese competition. Others would succeed beyond expectations—like becoming sole generic supplier for certain European markets. The portfolio approach reduced risk while maintaining upside exposure.

Lesson 7: Capital Allocation in Capital-Intensive Industries Shilpa's capital allocation revealed clear priorities: regulatory compliance first, capacity expansion second, new capabilities third. This hierarchy ensured they never lost market access while building for the future. Too many companies chase growth while skimping on compliance—a recipe for disaster in regulated industries.

Lesson 8: Building in Emerging Markets for Developed Markets Shilpa leveraged India's cost advantages while meeting developed market quality standards. This wasn't about labor arbitrage—skilled pharmaceutical workers aren't cheap anywhere. Instead, it was about combining emerging market entrepreneurship with developed market discipline. The hybrid model created advantages neither pure emerging market nor developed market companies could match.

Lesson 9: The Transition Challenge Moving from product company to service company (via CDMO) required different capabilities—project management, customer service, flexible manufacturing. Shilpa's struggle to balance product and service businesses highlights a universal challenge: organizational capabilities that make you good at one thing can make you bad at another. The solution wasn't choosing one or the other but building separate organizations with different cultures.

Lesson 10: The Power of Narrow Focus While competitors diversified across therapeutic areas, Shilpa stayed focused on oncology. This concentration created deep expertise—from handling cytotoxic compounds to understanding oncology regulations to relationships with cancer drug companies. In an industry where breadth often wins, Shilpa proved depth could triumph too.

For investors, these lessons translate into analytical frameworks. Look for companies building capabilities in areas others avoid. Value regulatory approvals not as compliance costs but as competitive moats. Understand that transformation takes time—judge progress by capability building, not just financial metrics. And recognize that in technical industries, complexity that seems like a burden can become a barrier that protects returns.

The Shilpa playbook isn't universally applicable. It requires patient capital, technical expertise, and regulatory sophistication. But for companies willing to embrace complexity, build through cycles, and invest ahead of returns, it offers a path from commodity supplier to specialized partner—a transformation that creates value for all stakeholders.

IX. Analysis & Bear vs. Bull Case

The investment case for Shilpa Medicare splits analysts into two camps, each armed with compelling evidence. The disagreement isn't about facts—both sides see the same regulatory approvals, financial statements, and market dynamics. The divergence lies in interpretation: Is Shilpa a transformation story in mid-flight or a complex conglomerate struggling to find direction?

The Bull Case: A Coiled Spring Ready to Unleash

Bulls see Shilpa as dramatically undervalued relative to its capabilities and opportunities. The oncology market is growing at 10-15% annually, driven by rising cancer incidence and new therapeutic developments. Shilpa's position—supplying 30+ oncology APIs to regulated markets—places them at the center of this growth.

The formulation business, despite the US import alert, is inflecting. The quarter witnessed healthy YoY growth in our key verticals of FDF & Biologics, which was partially offset by muted API performance. European approvals are opening new markets. The sole generic position on Nilotinib in Europe could generate ₹50-100 crores annually. With 16 injectable and 19 oral oncology formulations approved or in pipeline, the revenue potential is multiples of current levels.

The biologics and CDMO transformation is where bulls get most excited. The biologics facility receiving EU GMP with zero observations positions Shilpa among a handful of Indian companies capable of manufacturing biosimilars for Europe. The ADC capability being built could tap into one of pharma's hottest segments—the ADC market is expected to reach $30 billion by 2030. Even capturing 0.1% would transform Shilpa's economics.

The CDMO opportunity is particularly compelling. Global pharma companies are desperately seeking alternatives to Chinese manufacturers. Shilpa's regulatory track record, oncology expertise, and integrated capabilities (API to finished formulation) make them an ideal partner. CDMO contracts typically come with better margins, longer tenure, and stickier relationships than product sales.

Valuation provides the margin of safety bulls crave. At ₹8,596 crores market cap against ₹1,286 crores revenue, Shilpa trades at just 6.7x sales. Comparable CDMO companies trade at 10-15x. If Shilpa successfully transforms into a specialized CDMO with biologics capabilities, the rerating potential is enormous.

The regulatory overhang, bulls argue, is temporary and priced in. The FDA import alert will eventually resolve—it's a when, not if. Meanwhile, other markets are more than compensating. Every quarter without US access that Shilpa survives and grows proves the resilience of their model.

The Bear Case: Complexity Masking Fundamental Challenges

Bears see a company spreading itself too thin across too many initiatives. The API business—still the largest revenue contributor—is in structural decline. Chinese competition isn't going away. Pricing pressure will continue. The 10% revenue decline in APIs isn't a blip but a trend.

The formulation business faces its own challenges. The FDA import alert has no clear resolution timeline. Industry precedents suggest 3-5 years isn't unusual. Meanwhile, competition in generic oncology formulations is intensifying. Indian peers like Natco and Hetero have similar capabilities. The sole generic positions Shilpa celebrates are temporary—competition always arrives.

The biologics pivot, bears argue, is too late. Companies like Biocon and Dr. Reddy's have years of head start. The investment required—hundreds of crores—may never generate adequate returns. Biosimilar margins are compressing as more players enter. The ADC facility is interesting but unproven. Building capabilities doesn't guarantee commercial success.

The CDMO story sounds compelling but faces execution risks. Transitioning from product company to service provider is harder than it appears. Customer acquisition in CDMO is relationship-driven and takes years. Established players like Syngene and Divi's have locked up many large pharma relationships. Breaking in requires either exceptional capabilities or price competition—neither great for margins.

Financial performance validates bear concerns. The company has delivered a poor sales growth of 7.22% over past five years. Return on equity at 1.57% over three years is abysmal. These aren't metrics of a company successfully transforming—they're signs of capital misallocation.

The complexity itself is a problem. Shilpa is simultaneously trying to: revive the API business, resolve FDA issues, scale formulations, build biologics, develop CDMO capabilities, and maintain compliance across multiple geographies. That's too many balls in the air. Something will drop, and when it does, the consequences could be severe.

The Synthesis: A Calculated Bet on Execution

The truth likely lies between these extremes. Shilpa has built genuine capabilities that create long-term value. The regulatory approvals, technical expertise, and oncology focus are real moats. But transitioning from capability to commercial success requires execution excellence that remains unproven.

The key variables to watch: 1. FDA import alert resolution: This remains the biggest near-term catalyst 2. Biologics revenue ramp: Need to see the 2x growth materialize 3. CDMO client wins: Announcements of major contracts would validate the strategy 4. API stabilization: Even flat growth would be positive given current trends 5. Margin trajectory: EBITDA margins expanding toward 30% would signal mix shift success

For investors, Shilpa represents a complex risk-reward equation. The upside—successful transformation into a specialized CDMO with biologics capabilities—could deliver multibagger returns. The downside—execution failures leading to continued subpar performance—is cushioned by real assets and capabilities.

The investment decision ultimately comes down to conviction about management's ability to execute a complex transformation while navigating regulatory challenges, competitive pressures, and capital constraints. The pieces are in place. Whether they can be assembled into a coherent whole remains the billion-rupee question.

X. Epilogue & "If We Were CEOs"

Standing at the crossroads of 2025, Shilpa Medicare resembles a chess player who has developed all their pieces but hasn't yet coordinated them for the winning attack. The capabilities are impressive—world-class facilities, regulatory approvals, technical expertise. But capabilities don't equal outcomes. The next five years will determine whether Shilpa becomes a case study in successful transformation or another example of potential unrealized.

If we were sitting in Vishnukant Bhutada's chair today, three strategic priorities would dominate our agenda:

Priority 1: Resolve the FDA Import Alert—Whatever It Takes The US formulation opportunity isn't just about revenue—it's about credibility. Every month this drags on, customers question Shilpa's quality systems. Competitors capture share that should be ours. We'd throw everything at this: hire the best consultants, implement whatever systems FDA wants, over-communicate progress. Set a deadline: resolved within 18 months or we restructure the entire quality organization. The cost doesn't matter—the opportunity cost of inaction is far higher.

Priority 2: Pick a Biologics Lane and Own It The biologics strategy is too scattered—biosimilars, vaccines, ADCs, contract manufacturing. We'd focus ruthlessly on one area where we can be top 3 globally. Given our oncology heritage, ADCs make most sense. Partner with one or two innovative companies, become their exclusive manufacturer, share the upside. Build depth, not breadth. Become known as the ADC CDMO rather than another biologics player.

Priority 3: Create Two Separate Organizations The product business (APIs and formulations) and service business (CDMO) require different operating models, cultures, and metrics. Trying to run both from the same organization creates confusion and suboptimal outcomes. We'd create Shilpa Products and Shilpa Services as distinct entities with separate leadership, incentives, and strategies. Let each optimize for their model rather than compromise for corporate unity.

Beyond these priorities, several strategic questions demand answers:

Geographic Expansion: Should Shilpa double down on India's pharmaceutical ambitions or hedge by building capabilities in other geographies? Vietnam and Bangladesh offer lower costs. Eastern Europe provides closer proximity to EU markets. The answer isn't obvious, but standing still isn't an option.

The China Question: Chinese API manufacturers aren't going away. Instead of competing on price, could Shilpa partner selectively? Use Chinese intermediates for non-critical steps while maintaining control of key technology? The politics are sensitive, but the economics might be compelling.

Capital Allocation 2.0: With limited resources and unlimited opportunities, where do you place bets? Our framework would be simple: invest where we have right to win. Oncology? Yes. ADCs? Yes. Biosimilar insulin? Probably not. Saying no is harder than saying yes, but capital discipline determines outcomes.

The Talent Challenge: Raichur was brilliant for starting up but challenging for scaling up. How do you attract world-class biologics scientists to rural Karnataka? The answer might be hybrid—R&D in Bangalore or Hyderabad, manufacturing in Raichur. Or embrace remote work more aggressively than peers.

Looking ahead, Shilpa's role in India's pharmaceutical evolution is still being written. India has proven it can be the world's pharmacy for generic drugs. The next chapter is about innovation, complex manufacturing, and specialized services. Companies like Shilpa—with deep technical capabilities and global regulatory expertise—will determine whether India captures this opportunity or watches it pass to other nations.

The macro tailwinds are strong. Oncology market growing. Biologics exploding. Supply chain diversification accelerating. CDMO demand surging. But tailwinds alone don't guarantee success. Execution determines who captures value from structural trends.

The lessons from Shilpa's journey apply broadly to building in regulated, technical industries: - Start with the hard problems others avoid - Build capabilities before you need them - Accept that transformation takes longer and costs more than planned - Regulatory compliance is an investment, not a cost - Focus beats diversification, but platforms beat products - Geographic disadvantage can become strategic advantage - Patient capital enables aggressive strategies

What might the next decade hold? In our optimistic scenario, Shilpa becomes India's premier oncology specialist—the partner of choice for global pharma companies needing complex oncology products manufactured to highest standards. Revenue reaches ₹5,000 crores. Margins expand to 30%+. The stock re-rates to reflect CDMO valuations.

In our realistic scenario, Shilpa successfully navigates the transformation but faces continued challenges. The FDA issue resolves but takes longer than expected. Biologics grows but margins disappoint. CDMO wins some clients but competition limits pricing power. The company muddles through to ₹2,500 crores revenue with 20-25% margins. The stock delivers market returns.

In our pessimistic scenario, execution challenges multiply. FDA issues persist. Biologics investments don't pay off. CDMO struggles to win clients. Chinese competition intensifies. The company survives but value erodes. Private equity eventually takes it private at a discount.

The beauty of Shilpa's position is that even the pessimistic scenario isn't catastrophic. The assets are real. The capabilities are valuable. Someone—whether current management, new leadership, or an acquirer—will eventually unlock the value.

For investors, employees, and stakeholders, Shilpa Medicare represents something bigger than quarterly earnings. It's a test case for whether Indian companies can move beyond cost arbitrage to capability advantage. Whether complexity can be a source of competitive advantage. Whether patience and persistence pay off in industries where overnight success takes decades.

The story is still being written. The ending remains uncertain. But one thing is clear: Shilpa Medicare's journey from a single-product manufacturer in Raichur to a global oncology specialist is already remarkable. Whether it becomes legendary depends on decisions being made in boardrooms and laboratories today. The pieces are on the board. The game is in play. The next moves will determine whether Shilpa achieves checkmate or stalemate.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube