Shanthi Gears: The Gear Man's Legacy and India's Industrial Transformation

I. Introduction & Episode Roadmap

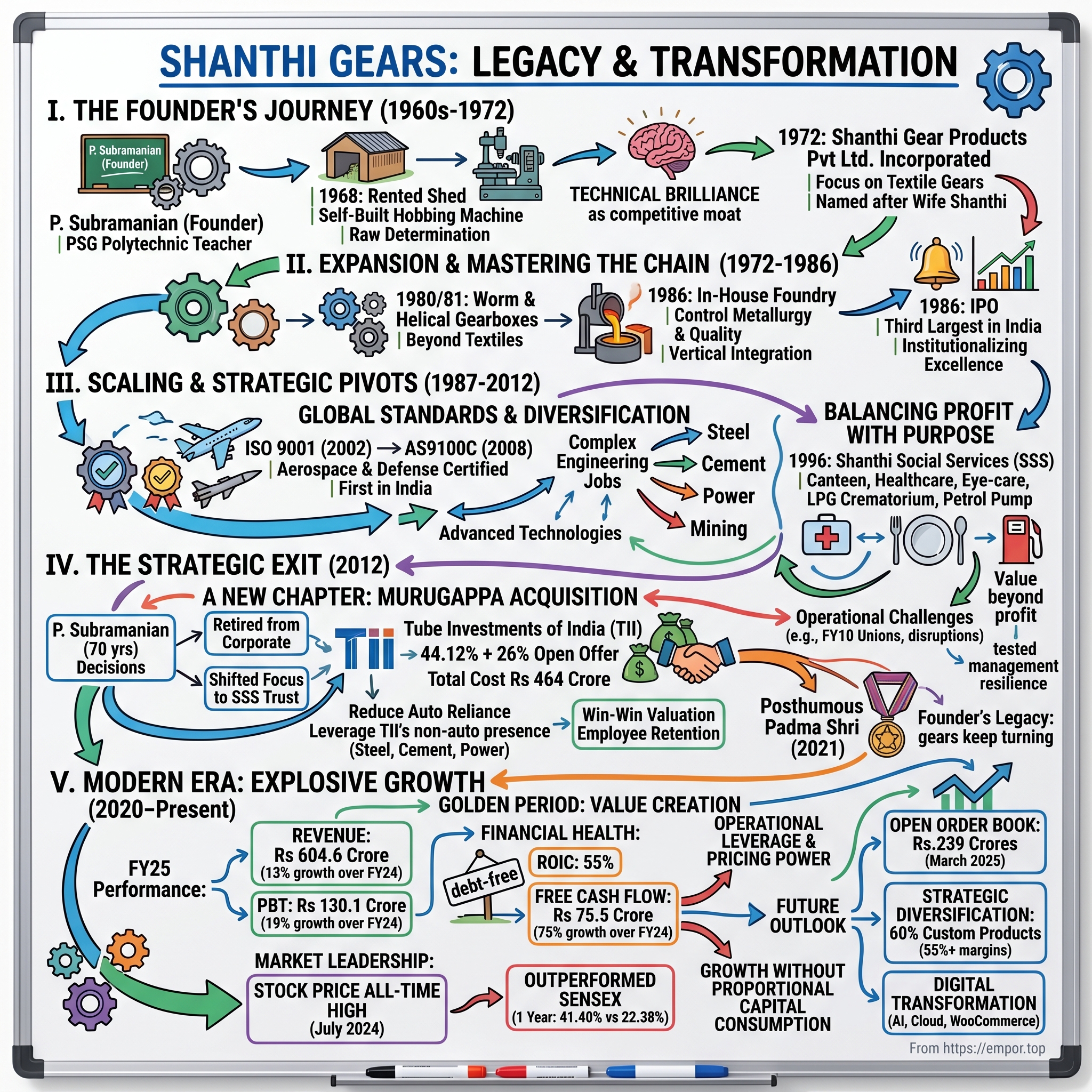

Picture this: A young mechanical engineering teacher in 1968, working with nothing but a rented shed and an audacious dream. No capital. No machinery. Just raw determination and technical brilliance. P. Subramanian set up his own enterprise in gear manufacturing in 1968 in a small rented shed without any capital. In the early stages, being a technocrat, he designed & built a Gear hobbing machine all by himself to meet his manufacturing expectations.

This is the extraordinary story of how a first-generation entrepreneur transformed that humble beginning into a company with market capitalization of ₹3,909 Crore, becoming the 'gear man of Coimbatore'. It's a narrative that spans six decades of Indian industrial evolution—from textile machinery to aerospace components, from import dependence to indigenous excellence.

What makes this tale even more remarkable? Shanthi Gears is a debt-free company with Rs.65-70 crore cash balance. The promoter has decided to sell his stake as he wants to focus more on social service activities. This wasn't just about building a business empire; it was about creating value that transcended profit margins.

In today's episode, we'll unpack how Shanthi Gears evolved from a teacher's side project to India's leading industrial gearbox manufacturer, its strategic acquisition by the Murugappa Group for Rs 464 crore, and its current position as a high-margin, cash-generating machine delivering 55% Return on Invested Capital (ROIC) in FY25 and Free Cash Flow of Rs 75.5 crore during the financial year with 75% growth over FY24.

We'll explore three critical transformations: first, how technical excellence became a competitive moat; second, why selling to a conglomerate at age 70 was a masterstroke; and third, how the company is navigating India's manufacturing renaissance. This isn't just a business story—it's a blueprint for building enduring industrial enterprises in emerging markets.

II. The Founder's Story & Early Foundation (1960s–1972)

The genesis of Shanthi Gears traces back to a classroom at PSG Polytechnic in Coimbatore. Born on November 11th, 1942 to an agricultural family, Shri P. Subramanian, was a first-generation industrialist. He completed his Diploma in LME in Mechanical Engineering in 1963 and a Post Diploma in Production Engineering in 1966, at PSG Polytechnic, Coimbatore and worked as a teaching staff at the same institute.

Think about this context: In the 1960s, Coimbatore was emerging as the "Manchester of South India," driven by textile mills and nascent engineering clusters. For a young teacher from an agricultural background, the leap to entrepreneurship wasn't just bold—it was almost unthinkable. Yet Subramanian saw something others didn't: India's textile industry desperately needed quality gears, and most were being imported at significant cost.

Shanthi Gears traces its rich heritage of engineering way back to 1960, when P Subramanian, an engineer himself, laid down the foundation with a modest small gear manufacturing unit in the town of Coimbatore. But the real entrepreneurial moment came in 1968. Imagine the scene: a teacher moonlighting as an entrepreneur, entering a rented shed after his day job, working late into the night to build—quite literally with his own hands—a gear hobbing machine.

This wasn't just resourcefulness; it was engineering genius meeting entrepreneurial grit. Stories abound that he used to stock high-quality steel for fabricating custom-made machines. Also, at times, when industries would fail to get the replacement of faulty gears from the OEMs within short, they would turn up to Mr. Subramanian who would have solutions for them, and that too, within a short span as well.

The transformation from individual craftsman to organized business came in 1972. In the year 1972, Shanthi Gear Products Private Ltd was incorporated and the company mainly focussed on textile gears. Later on during 1980/81, other products like Worm & Helical Reduction gear boxes were also introduced. This wasn't merely a legal restructuring—it marked a fundamental shift in ambition. The company name itself held deep personal meaning, named after his wife Shanthi, embedding family values into the corporate identity.

Shanthi Engineering and Trading Company, the precursor to Shanthi Gears, that started with simpler processes like milling, grew continuously under visionary leadership and with the toil of its people. It is this strong early foundation that allowed us to build on, to increase our capabilities to include progressively complex engineering jobs—from milling to independent units, fully manned by skilled technicians for manufacturing Patterns, Centrifugal Castings of phosphor bronze rings, Ferrous Castings, Aluminum Castings, Heat Treatment, Forgings, Fabrications and Cutter Manufacturing.

What's striking about this early phase is the systematic capability building. While competitors were content being traders or assemblers, Subramanian was building manufacturing depth. Each new capability—pattern making, casting, heat treatment—wasn't just vertical integration; it was creating an engineering ecosystem within four walls. This would prove crucial when the company later competed for complex, high-margin custom orders.

III. Building the Gear Empire: Expansion & IPO (1972–1986)

The fourteen years between incorporation and IPO represent one of the most remarkable organic growth stories in Indian manufacturing. While liberalization was still a distant dream and the License Raj constrained most businesses, Shanthi Gears found its rhythm in relentless technical advancement.

The pivot in 1980-81 to worm and helical reduction gearboxes wasn't just product diversification—it was a strategic bet on India's industrialization. These weren't simple textile gears anymore; they were complex power transmission systems needed by steel plants, cement factories, and sugar mills. Each new industry meant new technical challenges, tighter tolerances, and deeper engineering expertise.

By the mid-1980s, Shanthi had evolved from a small-scale industry to a formidable engineering enterprise. The company opened its first factory in 1972 and a decade later it expanded the product range by start manufacturing worm gearboxes. In the mid-80`s, SGL took the next step and began manufacturing helical and bevel helical gears. The company has also start producing geared motors simultaneously in this period. In 1986, it has completed the project of putting up its own foundry.

The foundry investment deserves special attention. In 1986, most gear manufacturers were content outsourcing their casting needs. Subramanian saw it differently—controlling the metallurgy meant controlling quality from the molecular level up. This backward integration philosophy would become Shanthi's signature approach: don't just manufacture; master the entire value chain.

Then came the watershed moment: The company got itself listed on the stock exchange in 1986 and became India's third-largest player in the gears industry. In March 1986 it became a Public Limited Company.

Consider what going public meant in pre-liberalization India. The capital markets were nascent, retail participation was limited, and manufacturing companies rarely commanded premiums. Yet Subramanian understood something profound: public listing wasn't just about raising capital—it was about institutionalizing excellence. The scrutiny of public markets would force discipline, the reporting requirements would drive systematic improvement, and the employee stock options would align incentives.

The IPO proceeds funded a critical transformation. In Mar.92, SGL came out with a rights issue to part-finance the expansion-cum-modernisation of its plants. Apart from this, the company made a preferential issue of 3.4 lac equity shares (premium : Rs 160) to banks and mutual funds in Sep.94. These weren't vanity expansions; each investment targeted specific technical capabilities that would differentiate Shanthi in increasingly competitive markets.

By the end of this period, Shanthi Gears had established three critical competitive advantages that would endure for decades: complete vertical integration from casting to finished gears, the ability to customize products for specific applications, and a reputation for reliability that made customers overlook cheaper alternatives. The foundation for the next phase of growth—technical excellence and global recognition—was firmly in place.

IV. Scaling & Technical Excellence (1987–2011)

The post-IPO era marked Shanthi Gears' transformation from a regional player to a nationally recognized engineering powerhouse. But this period also brought its most defining strategic decision: the pursuit of global quality certifications that would open doors to aerospace and defense sectors.

The company also obtained ISO 9001 & AS9100C certification. Let's pause here. In 2002, when Shanthi obtained ISO 9001 certification, it was table stakes for any serious manufacturer. But what happened in 2008 changed everything. Since 2008, Shanthi Gears was certified for AS9100C and re certified for EN 9100: 2018 (AS 9100 D) in 2018. Shanthi Gears is the first Indian Gear Manufacturer certified for AS 9100 including Design & Development of Aerospace & Defence parts.

Think about what AS9100 certification meant. This wasn't just another quality badge—it was admission to the most exclusive club in global manufacturing. Aerospace components operate in environments where failure isn't an option. The temperatures range from -50°C at altitude to hundreds of degrees in engine compartments. The safety margins are measured in microns. And here was a company from Coimbatore, competing with German and Japanese precision engineering giants, earning the right to make components for supersonic jets.

The diversification strategy during this period reveals sophisticated market understanding. Shanthi Gears, which was just the maker of gears for textile machinery when it was started is now producing gears for industries as wide as process, power steel, cement, sugar and aviation. The product range extends from gears for simple applications such as hand-driven jacks to high-tech gears for supersonic jet aircraft.

But success in business often runs parallel to purpose beyond profit. In 1996, he founded Shanthi Social Services, which runs canteens, healthcare facilities and other outreach activities. He was the founder and trustee of a social welfare organization called, Shanthi Social Services, which he had started to serve the people. This wasn't corporate social responsibility as checkbox exercise—it was revolutionary in scope and execution.

The social services model deserves deeper examination. The foundation runs a canteen which served free food to 300 senior citizens every day, apart from selling food for a nominal price for others. The foundation also runs a diagnostic center, a blood bank, an eye-care center, and an LPG crematorium. In the Singanallur on Trichy Road, SSS runs a petrol pump that is famous for selling fuel at pre-hike rates till the old stock is exhausted.

However, this period wasn't without challenges. During the year 2012-13, Tube Investments of India Ltd (TII) acquired his entire stake and followed it up with an Open Offer in line with the regulations and acquired another 26% from the general public. The reference to FY10 in the outline suggests operational challenges—union strikes and production disruptions that tested management's resilience. These challenges, combined with Subramanian approaching 70, set the stage for one of Indian manufacturing's most strategic exits.

What's remarkable about this 24-year period is how Shanthi Gears balanced three seemingly conflicting objectives: maintaining family control while being publicly listed, pursuing cutting-edge technical certifications while serving traditional industries, and building massive social infrastructure while running a for-profit enterprise. This balance would make the company incredibly attractive to strategic acquirers.

V. The Murugappa Acquisition: A New Chapter (2012)

July 13, 2012. The announcement that shook Coimbatore's industrial landscape: Tube Investments of India (TII) will be acquiring the 44.12 per cent stake held by the promoter, P. Subramanian, and associated entities, Shanthi General Finance Pvt. Ltd. and Shanthi Social Services, in Shanthi Gears in a Rs 292 crore deal. The shares of face value of Re. 1 each will be acquired at Rs.81 per share. This is a premium of 28 per cent to the current market price of Rs 63.15 a share.

But the headline numbers only tell part of the story. TII will be making an open offer to the extent of 26 per cent. The total cost of the acquisition, including the public offer, is expected to be Rs 464 crore assuming full response to the proposed open offer pursuant to Sebi regulation.

Why sell to Murugappa? Why now? And why this structure?

The answer begins with understanding P. Subramanian's mindset at 70. In 2012, as he turned 70, he decided to retire from the corporate world and shifted his complete focus towards the development of the Trust. The major sale proceeds received from the sale of Shanthi Gears Ltd, was transferred to the Trust to provide quality services at subsidized prices in various social spheres. This wasn't a distressed sale or a succession crisis—it was a carefully orchestrated transition that prioritized legacy over liquidation.

From Murugappa's perspective, the strategic rationale was compelling. L. Ramkumar, Managing Director, Tube Investments, said that addition of Shanthi's product portfolio would enhance TII's ability to service other industry segments and reduce its reliance on the auto sector, at the same time growing the company's presence in the value-added businesses.

Consider Tube Investments' position in 2012. The flagship company of the 112-year-old Murugappa Group was heavily dependent on automotive chains and cycles. The auto industry's cyclicality was a perpetual concern. The non-auto sectors currently make up 27 per cent of Tube Investments' total turnover. This is expected to get a boost with the addition of Shanthi Gears which has a diversified portfolio across non-auto sectors such as power and infrastructure.

The valuation mathematics reveals sophisticated deal-making. Based on the acquisition price, Shanthi Gear's valuation works out to around Rs 662 crore (for 100 per cent), which is close to four times its FY12 revenues and 9.5 times earnings before interest, taxes, depreciation and amortisation (Ebitda) and around 19 times FY13 estimated earnings at the open offer price of Rs 81 per share. At first glance, these multiples seemed rich for an industrial products company.

But dig deeper into what Murugappa was actually buying: The turnover of the company was Rs 178 crore in FY12 with a profit after tax of Rs 28 crore. Shanthi Gears is debt-free as on March 31, 2012. A debt-free company with 15.7% net margins, aerospace certification, and dominant market position—suddenly the valuation looks prescient rather than pricey.

The market reaction was telling. Shares of Shanthi Gears rose 4.99 per cent to Rs.63.15 while TII's stock closed at 154.75, up 6.21 per cent on Friday. Both stocks rallying suggested the market saw this as a win-win: fair value for sellers, strategic fit for buyers.

The human element of this transition deserves emphasis. The employees at Shanthi Gears are expected to be retained. The company is still discussing on senior management and other restructuring which the gears company may require. This wasn't a slash-and-burn acquisition; it was about preserving and enhancing what Subramanian had built.

Perhaps most poignantly, He was posthumously conferred India's fourth highest civilian honour, Padma Shri, in 2021. P. Subramanian died at the age of 79 on December 11, 2020. The timing—passing away eight years after the sale, having seen his life's work flourish under new ownership while his social initiatives thrived—suggests a founder who achieved that rarest of exits: one with no regrets.

VI. Post-Acquisition Transformation (2012–2020)

The first years under Murugappa ownership revealed the difference between financial engineering and operational transformation. This wasn't about cost-cutting or synergy extraction—it was about unlocking growth potential that existed but couldn't be accessed under previous constraints.

The 2013 strategic pivot deserves careful analysis. In 2022-23, it expanded to encompass institutional sales and business services, diversifying their portfolio and strengthening market presence. The focus on institutional sales meant moving from transactional relationships to strategic partnerships. When a steel plant orders a gearbox, they're not just buying equipment—they're buying uptime, reliability, and lifecycle support. Shanthi's new service orientation recognized this fundamental shift.

The service business transformation was particularly astute. Consider the installed base: thousands of Shanthi gearboxes operating across India's factories, many installed decades ago, still running but suboptimally maintained. By building a dedicated service wing, the company wasn't just generating recurring revenue—it was creating customer stickiness that made switching costs prohibitive.

In 2016-17, the Company launched a program titled Connect 2016. While the specific details aren't fully disclosed, the timing suggests this was about digital transformation and customer engagement—critical capabilities as Industry 4.0 concepts began penetrating Indian manufacturing.

The capacity expansion decisions during this period reflected sophisticated market reading. Rather than broad-based expansion, Shanthi focused on debottlenecking high-margin custom products. The evaluation of joint ventures with foreign players indicated Murugappa's ambition wasn't just to run Shanthi as a standalone profit center but to position it as a platform for technology acquisition and market expansion.

Cultural integration with the Murugappa Group deserves special mention. The Murugappa Group's 124-year heritage brought professional management practices, corporate governance standards, and access to group-wide resources. But critically, it preserved Shanthi's engineering-first culture. This wasn't absorption; it was enhancement.

The doubling of the sales force might seem like a simple commercial decision, but it represented a fundamental shift in go-to-market strategy. Previously, Shanthi's reputation and word-of-mouth drove orders. Now, proactive business development meant reaching customers who didn't even know they needed custom gearbox solutions. This expanded addressable market dramatically.

By 2020, the transformation was complete. Shanthi Gears had evolved from a founder-driven, product-centric company to a professionally-managed, solution-oriented enterprise. The foundation was set for the explosive growth that would follow in the post-pandemic manufacturing boom.

VII. Modern Era: Growth Trajectory & Market Leadership (2020–Present)

The post-pandemic era has been Shanthi Gears' golden period, validating every strategic decision made over the previous decade. The numbers tell a compelling story, but the underlying drivers reveal even more.

Revenue of Rs 604.6 crore in the financial year with a 13% growth over FY24. PBT of Rs 130.1 crore in the financial year with a 19% growth over FY24. This isn't just growth—it's profitable growth, with margins expanding faster than revenues, suggesting pricing power and operational leverage kicking in simultaneously.

The financial metrics deserve forensic analysis. The Return on Invested Capital (ROIC) is 55% in this financial year from 57% in FY24. The Company generated Free Cash Flow (FCF) of Rs 75.5 crore during the financial year and registered 75% growth over FY24. An ROIC of 55% is extraordinary—it means for every rupee invested in the business, Shanthi generates 55 paise in returns. For context, most industrial companies are thrilled with 15-20% ROIC.

The free cash flow surge—75% growth—signals something profound: the business has reached escape velocity. Capital expenditure requirements are moderating while cash generation accelerates. This is the holy grail of industrial companies: growth without proportional capital consumption.

Shanthi Gears Ltd., a smallcap company in the auto ancillary industry, has recently seen a surge in its stock price, reaching an all-time high of Rs 645 on July 8th, 2024. On July 8th, 2024, the company's stock price reached an all-time high, touching Rs 645. The stock market validation reflects institutional recognition of the transformation.

But perhaps more impressive than the absolute performance is the relative outperformance. In the past year, Shanthi Gears Ltd. has outperformed the Sensex, with a growth of 41.40% compared to the Sensex's 22.38%. This isn't just beta—it's genuine alpha generation through operational excellence.

The order book strength provides visibility into future growth. Open order book as on 31st March 2025 was Rs.239 Crores. This represents roughly 40% of annual revenue already locked in, providing cushion against any demand volatility.

Strategic diversification across sectors—steel, cement, thermal & wind power, mining, transportation, construction—means Shanthi isn't dependent on any single industry cycle. When cement capex slows, wind power picks up. When mining moderates, steel expansion accelerates. This portfolio effect smoothens revenue volatility.

The digital transformation initiatives, while not extensively detailed in public disclosures, represent the next frontier. References to cloud applications, AI-driven platforms, WooCommerce, and GoDaddy partnerships suggest Shanthi is building digital capabilities that could revolutionize how industrial gearboxes are designed, sold, and serviced.

The dividend policy reveals management confidence. The Board of Directors have recommended a final dividend of ₹ 2 per share (200%) for the financial year 2024-25. Combined with the interim dividend, Company has been maintaining a healthy dividend payout of 47.9%, striking an optimal balance between rewarding shareholders and retaining capital for growth.

VIII. Competitive Moat & Business Model

Understanding Shanthi Gears' competitive moat requires appreciating the nuances of the industrial gearbox market. This isn't a commodity business where lowest price wins—it's an engineering solutions business where reliability, customization, and lifecycle support determine success.

The acquisition by the Group's flagship company was aimed at diversifying its customer segments and getting stronger foothold on non-auto sector making it a leading gearbox manufacturers in India. Being part of the Murugappa Group isn't just about parentage—it's about access to customers, capital, and capabilities that would be impossible for a standalone company.

The customization capability represents the deepest moat. With 60% of revenues from customized products commanding 55%+ margins, Shanthi operates in a different league from standard product manufacturers. Each custom gearbox is essentially a mini-engineering project—understanding application requirements, designing solutions, prototyping, testing, and iterating. This isn't easily replicable by new entrants or import competition.

The indigenous manufacturing angle aligns perfectly with India's evolving industrial policy. The Make in India initiative isn't just rhetoric—it's driving real substitution of imported industrial equipment. Import of gearboxes happens predominantly in the safety critical applications and high technology areas such as gearboxes for wind turbine generators, power plants and marine applications. While most of these are imported from Europe, China caters to the demand in other segments. Shanthi sits at the sweet spot: sophisticated enough to replace European imports, cost-effective enough to compete with Chinese alternatives.

The service business differentiation cannot be overstated. When a cement plant's kiln drive gearbox fails, every hour of downtime costs lakhs. Shanthi's service capability—rapid response, on-site repairs, spare parts availability—transforms customer relationships from vendor-buyer to strategic partnerships. This recurring service revenue stream, while smaller than product sales, provides stability and deepens customer relationships.

Manufacturing integration and in-house R&D capabilities create formidable entry barriers. Shanthi gears' in house Research and Development department is recognized by the Department of Scientific & Industrial Research (DSIR) under the Ministry of Science & Technology for development of new product/ technologies, design and engineering, improvements in process/ product/ design, developing new methods of analysis and testing. This DSIR recognition isn't just a certificate—it provides tax benefits, easier access to government contracts, and validation of technical capabilities.

The aerospace and defense certification creates an almost insurmountable moat. Directorate General of Quality Assurance (DGQA) is the main Quality Assurance (QA) Organization entrusted with the responsibility of assuring quality & reliability of defense products. Shanthi Gears Limited is certified by DGQA to supply Gears & Gearboxes to Defense factories. The years required to obtain these certifications, the ongoing compliance costs, and the track record needed make this a massive barrier for competitors.

IX. Analysis & Investment Case

From an investment perspective, Shanthi Gears presents a fascinating study in value creation through strategic patience and operational excellence. Let's deconstruct the investment thesis systematically.

Parentage Strength: Tube Investments of India Ltd, the flagship company of the Murugappa Group, holds a 70.46% stake in the company. This isn't passive ownership—it's active value creation through customer introductions, technology access, and management bandwidth. The Murugappa Group's reputation opens doors that would remain closed to standalone players.

Financial Health: Company is almost debt free. In a capital-intensive industry, being debt-free provides enormous strategic flexibility. It means Shanthi can pursue growth opportunities, weather downturns, and maintain pricing discipline without financial pressure.

The stock performance validates the operational improvements. In the past year, Shanthi Gears Ltd. has outperformed the Sensex, with a growth of 41.40% compared to the Sensex's 22.38%. But this isn't just momentum—it's recognition of structural improvements in the business model.

Valuation Considerations: While the stock has performed well, the valuation metrics suggest the market is pricing in continued excellence. The key question for investors: Is this excellence sustainable?

The growth drivers suggest it is. India's infrastructure push is real and multi-decade. The Production Linked Incentive schemes are driving manufacturing investments. The China+1 strategy of global companies is creating opportunities for Indian suppliers. Energy transition—both renewable capacity addition and grid infrastructure—requires massive gearbox installations.

Key Risks: Import competition remains real, especially from China in standard products. However, Shanthi's focus on customization and service partially insulates against this. Commodity price volatility affects margins, though the company has demonstrated pricing power to pass through costs. Industrial slowdowns would impact order flow, but sector diversification provides cushion.

The most significant risk might be execution—maintaining 55% ROIC while growing at double digits requires operational excellence that's hard to sustain. Any slippage in quality, delivery, or service could damage carefully built customer relationships.

The Investment Verdict: Shanthi Gears represents a high-quality play on India's manufacturing renaissance. The combination of technical excellence, service differentiation, and parentage support creates a business that's hard to disrupt. While valuations reflect this quality, the runway for growth—both domestic and export—remains substantial.

For fundamental investors, the question isn't whether Shanthi Gears is a good business—it clearly is. The question is whether the market has already priced in the excellence. Given the structural growth drivers and execution track record, there's a case that the best is yet to come.

X. Lessons & Legacy

The Shanthi Gears story offers timeless lessons for building enduring industrial enterprises. These aren't just platitudes—they're battle-tested principles that created billions in value.

Building from zero capital to market leadership: Subramanian's journey from building his own hobbing machine to creating a 4000-crore enterprise proves that capital constraints can breed innovation. The discipline of bootstrapping—making every rupee count, building capabilities incrementally, earning customer trust through reliability—created a culture that survives even under corporate ownership.

The power of technical expertise combined with entrepreneurship: Pure technical excellence without commercial acumen creates lifestyle businesses. Pure commercial focus without technical depth creates unsustainable ventures. Subramanian's combination—deep engineering knowledge with entrepreneurial hunger—created a compounding machine. This DNA persists: even today, Shanthi's competitive advantage stems from solving engineering problems others can't or won't tackle.

Long-term thinking in a short-term world: Fifty years of consistent growth doesn't happen by accident. Every major decision—backward integration into foundries, pursuing aerospace certification, building social infrastructure—required accepting short-term pain for long-term gain. In an era of quarterly capitalism, Shanthi's half-century perspective stands out.

Balancing profit with purpose: Around 25,000 people, on a daily basis, are directly availing services from the Trust in various fields like Education, Medical, Pharmacy, Optical, Petrol Bunk and Canteen. The Shanthi Social Services model proves that businesses can create social value without sacrificing commercial success. Indeed, the reputation from social initiatives likely contributed to the premium valuation during the Murugappa acquisition.

Strategic exits and succession planning: Subramanian's sale to Murugappa at age 70 was masterful timing. The company was performing well, the buyer was strategic rather than financial, and the structure preserved value for all stakeholders. Too many founders hold on too long, destroying value through succession battles or operational decline. Subramanian's graceful exit enhanced his legacy.

Creating value through consolidation: The Murugappa acquisition demonstrates how strategic consolidation can unlock value. Tube Investments brought capital, customers, and capabilities that Shanthi couldn't access independently. Shanthi brought product expertise, manufacturing excellence, and market position that Tube Investments couldn't replicate. The combination created value exceeding the sum of parts.

The ultimate lesson? Building industrial enterprises isn't about financial engineering or market timing—it's about solving real problems for real customers with real engineering. In an economy increasingly dominated by asset-light, platform businesses, Shanthi Gears reminds us that making physical products that enable other industries remains a path to enduring value creation.

P. Subramanian's legacy extends beyond the company he built. He proved that Indian manufacturing could compete globally not through labor arbitrage but through engineering excellence. He demonstrated that first-generation entrepreneurs from modest backgrounds could build institutions. Most importantly, he showed that business success and social service aren't mutually exclusive—they can be powerfully complementary.

As India embarks on its manufacturing renaissance, aspiring to become the world's factory, the Shanthi Gears story provides both inspiration and blueprint. The challenges are real—global competition, technology disruption, talent availability—but so are the opportunities. Companies that combine technical excellence with commercial acumen, operational efficiency with strategic thinking, and profit generation with purpose-driven leadership will define India's industrial future.

The gear man of Coimbatore may have passed on, but his gears keep turning—in factories across India, in the lives touched by Shanthi Social Services, and in the institution that bears his wife's name. That's the true measure of entrepreneurial success: building something that outlasts the builder.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube