Shadowfax Technologies: The Asset-Light Crowdsourcing Rebel

I. Introduction & Episode Roadmap

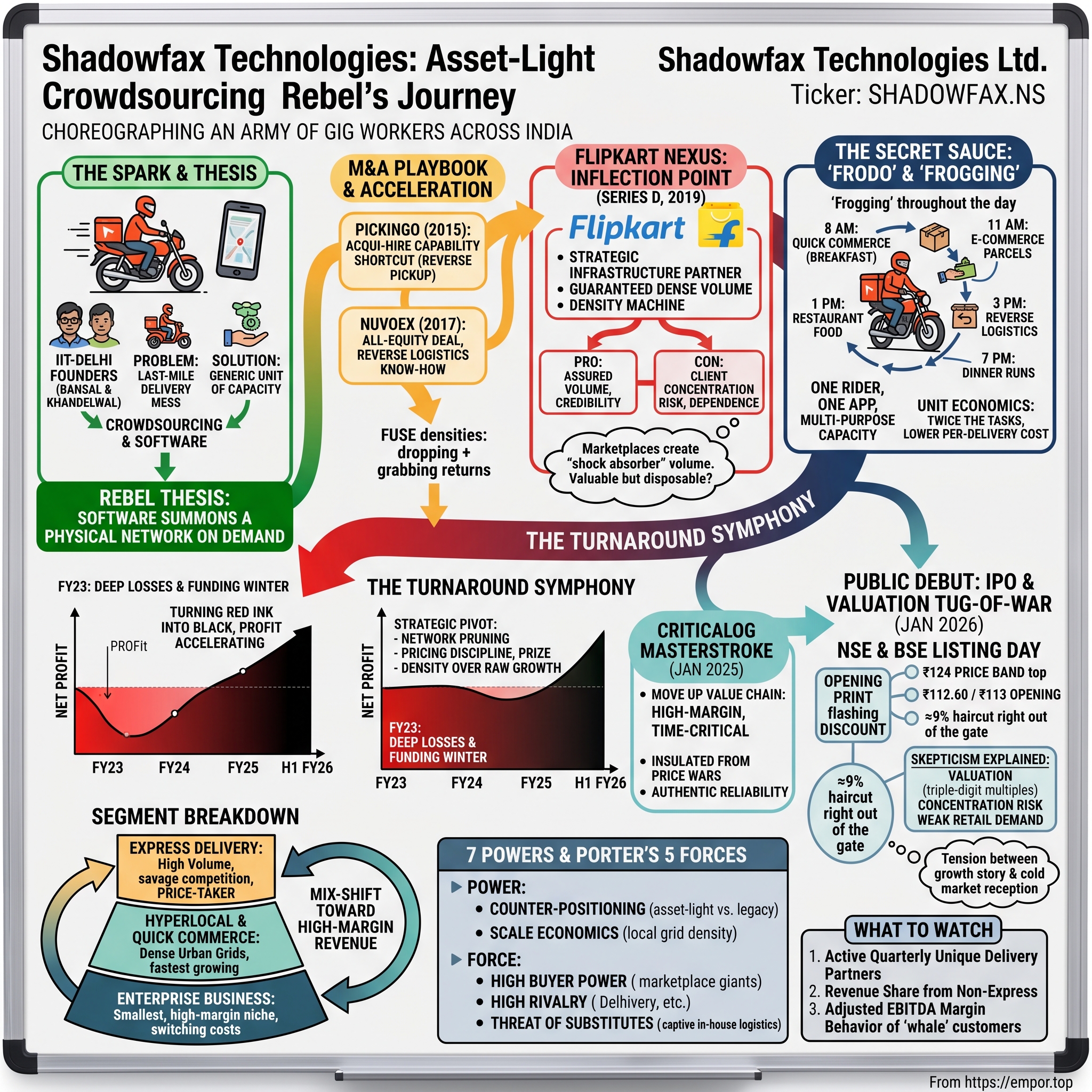

On the morning of January 28, 2026, a scrum of traders on the National Stock Exchange of India watched a ticker they had been arguing about for weeks finally go live. Shadowfax Technologies — a company most Indians had never heard of, even though its riders had probably handed them a package that same week — was about to open. The order book had been priced at ₹124 a share, the top of a ₹118–124 band.[^3] The opening print flashed: ₹112.60. A 9.19% discount, right out of the gate.[^5] On the BSE, it was scarcely better, opening at ₹113, an 8.87% haircut.[^5]

Here was the paradox that hung in the air. This was not a zombie company limping to the exit. Shadowfax had grown revenue at roughly a 33% compound annual rate from FY23 to FY25.6 It had just flipped from years of losses to a maiden net profit.6 It sat at the center of the two hottest currents in Indian consumer life — e-commerce and quick commerce — as an invisible utility. And yet the public market, in its first act of price discovery, decided the thing was worth less than the founders and their bankers had asked. Why the skepticism?

That gap — between a beautiful growth story and a cold market reception — is the whole episode. To understand it, you have to understand what Shadowfax actually is, because it is not what "logistics company" conjures in your head. It owns almost no trucks. It employs very few salaried delivery staff. Instead, it choreographs a fluid army of more than 200,000 active gig workers each quarter, reaching into more than 14,700 pin codes across India.6 It is less a fleet than an operating system for other people's motorcycles.

The people who built it were not logistics lifers. Abhishek Bansal and Vaibhav Khandelwal were IIT-Delhi classmates who looked at India's last-mile delivery mess and saw not a problem of warehouses and vehicles, but a problem of math — of matching supply to demand, minute by minute, across a chaotic urban grid.6 Their bet was that if you treated a delivery rider as a generic unit of capacity rather than a "food delivery boy" or a "courier," you could keep that rider busy across the whole day and undercut everyone weighed down by fixed assets.

So how did two engineers build an asset-light machine that went toe-to-toe with capital-heavy titans like Delhivery and Blue Dart, absorbed smaller rivals to buy time and capability, survived the funding winter that killed weaker startups, turned profitable, and became the quiet nervous system behind India's ten-minute-grocery obsession — only to be met with a shrug on listing day?

Here is the roadmap. We start with the 2015 founding spark and the asset-light thesis. We trace the early M&A playbook — Pickingo and NuvoEx — as capability shortcuts. We hit the Flipkart inflection and the double-edged sword of a strategic backer who is also a customer. We open up the "secret sauce," the Frodo engine and a trick called "frogging." We follow the grinding turnaround from deep losses to black ink. We examine the CriticaLog acquisition, a deliberate move up the value chain. We deconstruct the January 2026 IPO and its listing discount. We break the business into its three segments. And finally we run it through the 7 Powers and Porter's Five Forces before staging a bull-versus-bear stress test. Let's begin where every asset-light dreamer begins: with a problem nobody wanted to own.

II. The Founding Context: On-Demand and Asset-Light

Picture urban India in 2015. The smartphone had arrived in the pocket of the aspiring middle class, cheap data was on the horizon, and a generation of founders had caught the "Uber-for-X" fever sweeping in from Silicon Valley. Swiggy and Zomato were teaching Indians to expect dinner at the door. Flipkart and Snapdeal were teaching them to expect a parcel. But underneath all that consumer promise sat an ugly operational truth: India's physical delivery layer was not built for any of it.

The incumbents — Blue Dart, DTDC, the old courier houses — had been engineered for a slower world. Their networks assumed three-to-five-day timelines, business-to-business documents, and predictable intercity trunk routes. Drop an explosion of small, unpredictable, cash-on-delivery e-commerce parcels onto that architecture and it groaned. Cash-on-delivery meant failed deliveries and cash reconciliation nightmares. Returns — reverse logistics — were a black hole of cost. The last mile, the final hop from a local hub to a customer's door, was where the money leaked out fastest, and nobody had a clean answer.

Into this walked Abhishek Bansal and Vaibhav Khandelwal, two friends out of IIT-Delhi.6 What made them different was less pedigree than framing. A logistics veteran looks at the last mile and sees a need for more feet on the ground, more vans, more hubs — more assets. Bansal and Khandelwal, trained to think in systems and optimization, looked at the same mess and saw an allocation problem. There were already millions of young men in Indian cities who owned a motorcycle and a smartphone and needed income. The vehicles existed. The labor existed. What was missing was software to match that latent supply to the flood of demand in real time.

That was the rebel thesis, and it inverted the industry's capital logic. Instead of hiring salaried riders — a fixed cost you pay whether volume shows up or not — and buying vans that depreciate in your garage, why not build a platform that crowdsources local riders who already own the wheels? Turn the biggest fixed costs of logistics into variable costs that flex with demand. When orders spike, more riders log on. When they fall, you are not bleeding money on idle payroll and parked vehicles.

It is worth pausing on the two men, because their temperaments shaped the company more than any single strategy document. Bansal, who would take the chief-executive role and eventually the chairmanship, was the commercial and operational mind — the one who thought in terms of routes, payouts, and merchant relationships.6 Khandelwal, who took the chief-technology seat, was the systems builder, the person for whom the delivery network was a graph to be optimized.6 They were classmates first and co-founders second, which matters: the durability of a founding partnership through a decade of near-death moments is itself a form of institutional stability, and the fact that both were still running the company as it went public — Bansal as chairman and managing director, Khandelwal as whole-time director and CTO — is a data point a long-term investor should not skip past.6 Founder-led companies that survive the funding wars tend to have this in common: the people who made the original bet are still there to defend it when it gets hard.

They set up shop in Bengaluru and, tellingly, spent their scarce early capital not on concrete but on code and onboarding.6 While better-funded peers were pouring venture money into warehouses and sortation centers, Shadowfax obsessed over the two things that actually made the asset-light model work: how fast and cheaply you could sign up a new rider, and how intelligently you could route him once he was on the platform. Early institutional money came from Eight Roads Ventures, an investor that would remain one of the company's largest shareholders all the way to the IPO, holding some 14% of the company at listing.6 That patient, decade-long presence on the cap table tells you the model was never a quick flip; it was a long, grinding bet that density and software could eventually beat trucks and payroll.

There is a subtler point buried in the choice of Bengaluru and the choice of what to fund first. Every logistics founder faces a fork: build the physical network first and layer software on top, or build the software first and let it summon a physical network on demand. Delhivery and the incumbents took the first path, which is why they carry heavy balance sheets. Shadowfax took the second, which is why its balance sheet is light — and why its fate is tied so completely to whether the software is genuinely good enough to run a network it does not own. The whole company is a wager that the second path is cheaper. For years, the losses suggested the wager was still open. The point of everything that followed was to close it.

The elegance of the pitch, though, hid the fragility. An asset-light model is only "light" when volume is dense and steady. In a thin market — a sleepy pin code, a slow afternoon — a crowdsourced fleet is expensive and unreliable, because riders won't sit around for scraps and quality collapses. The entire edifice depended on getting enough demand into a small enough geography to keep riders earning and busy. Shadowfax needed density, and it needed it fast. That hunger for scale is what sent two founders, barely months into the journey, shopping for their first acquisition.

III. The Acceleration Engine: The Early M&A Playbook

Most startups spend their first year heads-down, building. Shadowfax spent part of its first year shopping. In November 2015 — the company was practically an infant — it moved to absorb Pickingo, a Gurgaon-based hyperlocal delivery startup that was running low on cash.[^11] On paper it looked like a tiny deal between two tiny companies. In practice it revealed the mental model that would define Shadowfax's entire M&A career.

The point of buying Pickingo was not its revenue, which was negligible, nor its brand, which would vanish. It was what practitioners call an acqui-hire wrapped around a capability shortcut.[^11] Pickingo had already done the unglamorous engineering work of integrating with local merchants and building reverse-pickup protocols — the plumbing for collecting a package from a customer's home and getting it back to a seller. Rebuilding that from scratch would have cost Shadowfax months it did not have. By swallowing Pickingo's technology and, crucially, its core engineering team, Shadowfax bought time and a running start in northern India. In a land-grab market, time is the scarcest asset of all, and buying a distressed rival is often cheaper than out-hiring it.

The pattern repeated, with a twist, in October 2017. This time the target was NuvoEx, a specialist in e-commerce reverse logistics.3 The backdrop mattered: 2017 was a wobbly year for Indian e-commerce, funding had tightened, and smaller players were struggling to stay afloat. A cash-rich acquirer might have overpaid to eliminate a competitor. Shadowfax, still capital-constrained, did something more disciplined — it structured an all-equity transaction, absorbing NuvoEx's assets in exchange for handing NuvoEx's shareholders a minority stake in Shadowfax.3 No precious cash left the building.

What Shadowfax got in return was disproportionate to the price. NuvoEx brought an instant footprint across dozens of cities and, more valuably, established relationships with major e-commerce clients who trusted it with the hardest job in the business: returns.3 Reverse logistics is a nightmare precisely because it is the mirror image of delivery — instead of one warehouse fanning out to many homes, you are collecting from many scattered homes and consolidating back. It is low-density, high-friction, and easy to lose money on. But it is also sticky, because merchants hate switching a vendor who has finally gotten their returns under control.

The strategic logic was the marriage of two densities. Shadowfax had built forward-delivery density — lots of packages going out in a given area. NuvoEx had reverse-logistics know-how — the discipline of getting packages back. Fuse them, and the same rider who drops a parcel on the way out can grab a return on the way back, spreading the cost of that trip across two tasks instead of one. That drove down the dreaded return-to-origin cost that eats merchant margins. It was, in miniature, the same idea Shadowfax would later industrialize into its core technology: never let a rider or a trip do just one job.

There is a broader lesson in how Shadowfax financed these moves. Both Pickingo and NuvoEx were absorbed with minimal cash — the first an acqui-hire of a distressed startup, the second an all-equity asset deal that handed the sellers paper rather than money.[^11]3 For a young, capital-constrained company, using equity as acquisition currency is a double-edged instrument: it conserves precious cash and aligns the seller's incentives with the buyer's future, but it also dilutes existing owners and quietly seeds the cap table with small stakes that must be managed for years afterward. The discipline Shadowfax showed was in refusing to overpay in either currency — no cash bidding wars, no richly valued stock swaps for vanity scale. That restraint, repeated across three acquisitions over a decade, is one of the more genuinely reassuring signals in the whole story for anyone worried about how management will behave with public shareholders' money.

These early deals also told you something about temperament. Bansal and Khandelwal were willing to move fast and buy rather than build when buying was faster, but they refused to buy vanity. Each acquisition plugged a specific gap — northern reach, reverse-logistics muscle. That discipline would be tested far harder when a very different kind of partner came knocking, one who could hand Shadowfax the density it craved but attach a string that would tug at the company for years.

IV. The Flipkart Nexus: The Series D Inflection Point

By 2019, the polite phase of Indian logistics was over. Third-party logistics — 3PL, the business of delivering other companies' parcels — had become a knife fight. Delhivery was scaling into a national juggernaut on a mountain of venture capital. Xpressbees and Ecom Express were heavily funded and hungry. And the two giants at the top of the food chain had gone captive: Amazon ran its own transportation arm, and Flipkart moved most of its volume through its in-house network, eKart. For an independent 3PL, the terrifying question was whether the marketplaces would ever need you at all.

Then, in December 2019, Flipkart answered that question in Shadowfax's favor — by leading a roughly $60 million Series D round into the company.[^9] For a business built on the premise that it could out-hustle the asset-heavy incumbents, this was the inflection point, the moment the story bent. Overnight, Shadowfax went from being one more 3PL vendor in a crowded field to something closer to strategic infrastructure for the Flipkart ecosystem — a preferred partner for the categories eKart could not or would not fully own, from groceries and fresh produce to, eventually, quick commerce through Flipkart's ten-minute offering.

To grasp why this mattered, you have to internalize the one variable that rules all logistics economics: density. Here is the intuition. Imagine a rider who has to deliver four parcels scattered across a five-kilometer radius — he spends most of his shift riding, not delivering, and each drop is expensive. Now imagine those same four parcels are packed into a single one-kilometer cluster — he delivers all four in the time it used to take to do one, and the cost per parcel collapses. Guaranteed volume from a giant like Flipkart is a density machine. It floods specific geographies with orders, and density is what turns an asset-light model from a fragile idea into a profitable one.

But strategic money from a customer is a double-edged sword, and this is where the neutral lens matters. On the good edge: assured, dense volume that no amount of sales hustle could replicate, plus the credibility of a marquee backer. On the bad edge: dependence. When one or two clients come to control a dominant share of your volume, the power in the relationship quietly flips. They set the pricing. They dictate service levels. And every rupee of margin you make is a rupee they might decide to claw back at contract renewal. Shadowfax was buying growth with a slice of its own independence.

It is worth dwelling on why marketplaces outsource delivery at all, because the answer defines both Shadowfax's opportunity and its vulnerability. A marketplace runs its own captive network — an eKart, an Amazon Transportation Services — for its predictable base-load volume, the steady river of parcels it can plan around. But demand is spiky: festival surges, regional bursts, new categories like fresh groceries with their own strange logistics. Building captive capacity for the peaks means paying for idle capacity in the troughs. So marketplaces keep a captive core and rent flex capacity from third parties like Shadowfax to absorb the spikes and the awkward categories. That makes Shadowfax structurally the shock absorber — valuable, but also the first volume a cost-cutting client pulls back in when it wants to fill its own network. The very flexibility that makes Shadowfax useful is what makes its volume the most disposable.

That dependence was not hypothetical. By FY25, the DRHP disclosed that the top five clients accounted for close to half of revenue, with Flipkart and the social-commerce platform Meesho standing as the two largest customers by a wide margin.6 A business can ride a whale for years and prosper. But it lives with a permanent tail risk: the whale can build its own boat. Flipkart already had eKart. Meesho, as we will see, would later launch its own logistics play. The Series D that saved Shadowfax's independence in 2019 also planted the seed of the concentration risk that the public market would fixate on in 2026. To justify that risk, Shadowfax needed to be genuinely, structurally cheaper to run than anyone else — and that came down to a piece of software.

V. The Secret Sauce: "Frodo" and the Magic of "Frogging"

Start with the problem that quietly bankrupts gig-delivery businesses: dead time. A rider who only delivers restaurant food is a millionaire of idleness for most of the day. Lunch runs from roughly noon to three, dinner from seven to ten, and in between he sits, earning nothing while his motorcycle depreciates and his patience wears thin. A rider who only carries e-commerce parcels has the opposite affliction — a flat daytime shift, then nothing during the lucrative late-night food peaks. Either way, the rider's earning hours are a fraction of his working hours, so he either quits or demands a higher rate per task to make the day worthwhile. High churn and high per-delivery cost are the twin taxes of single-purpose gig fleets.

Shadowfax's answer, and its most genuinely differentiated piece of intellectual property, is a practice it calls "frogging," run by a proprietary logistics engine named Frodo.[^8] The name is a wink — Frodo, the small hero carrying a burden across a vast map — but the idea underneath is serious. Frogging means treating a single rider as multi-purpose capacity and hopping him across delivery verticals through the day, so his idle hours get filled with whatever demand happens to be live at that moment.

Here is a day in the life under Frodo, and it reads nothing like a traditional courier's shift. At eight in the morning, the rider is dropping quick-commerce groceries — the ten-minute stuff people order for breakfast. By late morning, demand for groceries fades and he is carrying e-commerce parcels for the likes of Meesho or Flipkart. At lunchtime he swings into restaurant food. In the afternoon, the quiet window, he handles reverse-logistics pickups — those returns nobody else wants. And by evening he is back on food and quick-commerce dinner runs.[^8] One rider, one app, five distinct demand curves stitched into a single busy day.

The trick is not the schedule; it is the real-time orchestration. Frodo continuously clusters demand from all these different verticals at once, matching each incoming order to the nearest suitable rider based on live location and destination proximity.[^8] Think of it as a dispatcher who never sleeps and can see every order and every rider on the map simultaneously, constantly re-solving the puzzle of who should carry what next. The magic is not moving one package; it is co-mingling flows that every single-vertical competitor keeps in separate, half-empty buckets.

The economic payoff is measured in tasks per hour. On a single-vertical platform, a rider might average around 1.5 completed tasks an hour once you account for all the dead time. By flattening the demand curve across the whole day, Shadowfax says frogging can push that toward three or more.[^8] Sit with what that does to the unit economics. If a rider completes twice as many tasks in the same hour, he earns more per hour — which keeps him from quitting — while Shadowfax can pay a lower effective rate per individual delivery and still leave him better off. Higher rider earnings, lower cost per task, and reduced churn, all from the same lever. That is the closest thing Shadowfax has to a structural moat.

A useful analogy: think of a hospital operating theatre. Its most expensive resource is not the building but the surgical team's time, and the whole economics of a hospital depend on keeping that theatre booked back-to-back rather than idle between cases. A single-vertical delivery platform is like an operating theatre that only ever performs one kind of surgery for three hours a day and sits dark the rest of the time — the fixed cost of the asset is spread over far too few procedures. Frogging is the scheduling logic that keeps the theatre running all day with whatever case is next in the queue, so the cost of the resource is amortized across many more billable hours. The rider is the theatre; Frodo is the scheduler; frogging is a full booking sheet. Once you see it that way, you understand why utilization — not headcount, not pin codes — is the number that actually drives this company's cost curve.

There is one more layer to appreciate. Because Frodo sees every vertical at once, it can also make routing decisions no single-purpose dispatcher could. A rider heading east to drop a grocery order can be handed an e-commerce parcel and a return pickup that lie along the same path, so a single trip does three jobs instead of one. This "batching across verticals" is the operational descendant of the forward-plus-reverse logic Shadowfax first stitched together with NuvoEx, now generalized to every category the company touches. It is also the reason the company's cost advantage is so hard to see from the outside and so hard to copy from the inside: it lives not in any one clever feature but in the accumulated messiness of running millions of co-mingled tasks and learning, trip by trip, how to pack them tighter.

But keep the skeptic's hat on. Frogging's benefits are real only where demand across verticals is genuinely dense and overlapping — dense metros and large towns. In thinner markets the co-mingling thins out and the advantage fades. And the efficiency gains, however clever, run straight into an industry where buyers hold the pricing whip. A better engine can lower your cost; it cannot by itself force a giant customer to let you keep the savings. Which is exactly why, for years, all that operational cleverness still added up to losses — and why the turnaround that followed is the real test of whether the model works.

VI. The Turnaround Symphony: Turning Red Ink into Black

Rewind to FY23, the year the music nearly stopped. On the surface Shadowfax looked like a success — revenue had reached ₹1,415 crore, a big number for an asset-light logistics upstart.6 Underneath, it was hemorrhaging. The company posted a net loss on the order of ₹143 crore for the year, with deeply negative operating profitability, and it was doing so in the worst possible environment.6 The pandemic-era funding party had ended, interest rates had spiked, and the venture capital that had subsidized Indian startup growth for a decade suddenly demanded a path to profit. For a cash-burning company, a funding winter is not an inconvenience; it is an existential clock.

Management's credibility is best judged by behavior under exactly this kind of pressure, and the FY23 crisis is the cleanest test in the company's history. Plenty of Indian startups faced the same winter and responded with cosmetics — a round of layoffs, a rebrand, a slide deck promising profitability "next year" that never arrived. The relevant question for an investor is whether Shadowfax's leadership made structural changes that showed up in the numbers, or merely talked about them. The bench that drove the response — Bansal and Khandelwal alongside operations and commercial lieutenants, several of them IIT-Delhi alumni who had grown up inside the company — chose the harder, structural path.6

This is the moment that separates a fad from a franchise, and it is worth being precise about what management actually did, because "we cut costs and focused on unit economics" is what every struggling company says. The Shadowfax pivot, led by Bansal with Khandelwal on technology and a bench that included operations and commercial chiefs, had three concrete strands. First, network pruning: closing unprofitable routes and walking away from low-density pin codes where the asset-light model simply could not work. Second, pricing discipline: raising rates on low-volume merchants and renegotiating contracts rather than chasing every parcel at any price. Third, and most important, a deliberate choice to prize density over raw growth — pouring volume into existing urban hubs to feed the Frodo engine rather than sprinkling thin volume across a vanity map of pin codes.

The financial arc that followed is the spine of the whole investment case, so follow the trajectory rather than the individual digits. In FY24, revenue climbed to roughly ₹1,885 crore, and the net loss shrank dramatically — from around ₹143 crore of red ink to under ₹12 crore, with operating profitability crossing into positive territory for the first time.6 The bleeding had nearly stopped. Then, in FY25, revenue reached about ₹2,485 crore, up roughly a third year on year, and the company printed a maiden net profit of around ₹6 crore.6 After years of losses, the sign on the bottom line finally flipped.

What makes the turnaround more than a one-quarter fluke is what happened next. In the first half of FY26 — the six months running into the IPO — revenue jumped roughly 68% year on year to about ₹1,806 crore, and net profit more than doubled to around ₹21 crore versus ₹9.8 crore in the year-ago half.65 Profit was not just present; it was accelerating, and margins were widening off a razor-thin base.

Now the analytical read, held in balance. The bull interpretation is that this is operating leverage doing exactly what the thesis promised: as density rises in mature hubs, each incremental parcel drops more to the bottom line, and the asset-light model finally shows its designed-in advantage. That is genuinely encouraging, and it is not a paper turnaround — it came with real network cuts and pricing fights. The bear interpretation is sobering: even at its best, this is a business earning single-digit-crore-scale profits on thousands of crores of revenue. The margins are wafer-thin, which means there is almost no cushion. A modest rise in rider payouts, or a single large customer squeezing price, could wipe out the profit that took years to conjure. Both readings are true at once — and the company chose that exact moment to try to buy its way toward a thicker margin.

VII. The CriticaLog Masterstroke

Every low-margin business eventually confronts the same tempting question: is there a richer neighborhood we can move into? For Shadowfax, the core e-commerce delivery business was a race to the bottom, with merchants paying something like ₹15–25 per parcel and fighting over every rupee. You can be the most efficient operator in that arena and still be poor, because the buyers are giants and the product is a commodity. To thicken its margins structurally, Shadowfax needed a foothold in the opposite kind of logistics — low-volume, high-value, high-stakes shipments where customers pay a premium for reliability rather than haggling over pennies.

That foothold arrived on January 27, 2025, when Shadowfax completed its acquisition of CriticaLog, a Bengaluru-based specialist in high-value, time-critical enterprise logistics.[^7] Where the deal-making showed discipline was in the price and structure. Rather than a single splashy buyout, Shadowfax built its position in tranches, and the arithmetic stayed modest — the final increment was a 10.41% stake for about ₹5.59 crore, with the total consideration for the business landing near ₹55.7 crore.[^7] For a company that had only just clawed its way to profitability, restraint on price was not optional; it was survival. The pattern from the Pickingo and NuvoEx days held — buy a capability, not a trophy.

What CriticaLog bought was access to a genuinely different economic universe. Its world is the delivery of things that cannot simply be left at a doorstep: healthcare and medical devices, luxury retail, critical IT hardware, high-value automotive spares.[^7] Imagine the difference between dropping a ₹400 apparel order and hand-carrying a heart stent or a replacement server component that must reach a hospital or a data center within a tight window, with a full chain-of-custody and a strict service-level agreement. The second job commands a vastly higher price because the cost of failure is enormous and the barriers to doing it reliably are real. That is why this niche carries margins in a different league from consumer parcels.

Strategically, the move did three things at once. It diversified Shadowfax away from its dependence on a handful of low-margin marketplace clients. It introduced genuine switching costs — enterprise clients who integrate a logistics partner into cold-chain or high-security workflows do not swap vendors casually, unlike an e-commerce seller who can re-route parcels through a shipping aggregator in an afternoon. And it lifted the blended gross-margin profile of the whole company by mixing a sliver of premium revenue into the commodity base.

Worth sitting with the contrast in physics between the two ends of Shadowfax's business. Consumer express is a game of volume and velocity — millions of low-value parcels, thin margins, and a rider who succeeds by doing more drops per hour. Critical logistics is the inverse — few shipments, high value, and success measured by never failing. A courier who loses a ₹400 shirt costs the merchant a refund; a courier who loses or delays a medical device or a critical server part can cost a life or shut down a data center, which is why customers in these categories pay for guaranteed windows, chain-of-custody documentation, and specialized handling like temperature control. The skills, the culture, and the pricing power of the two businesses barely overlap, which is precisely why Shadowfax bought the capability rather than trying to grow it organically out of a low-cost parcel operation. You cannot bolt a premium-reliability culture onto a race-to-the-bottom one; you have to acquire it intact.

The honest caveat is scale. CriticaLog is, for now, the smallest of Shadowfax's three businesses, and a high margin on a small base does not move the consolidated needle much. The bull case rests entirely on whether management can grow this segment from a rounding error into a meaningful slice of revenue. If it can, the company re-rates. If CriticaLog stays niche, it is a nice hedge and little more. There is also a management-credibility read here. A leadership team that had just fought its way to a slim profit could easily have declared victory and coasted, or worse, chased a large, splashy acquisition to juice the pre-IPO growth story. Instead, the CriticaLog deal was small, staged, and cheap — a continuation of the same disciplined M&A temperament shown a decade earlier, now applied under the brighter lights of an imminent listing.[^7] For an investor trying to forecast how a management team will behave with public shareholders' capital, the most reliable evidence is the pattern of decisions it made before it had to. Shadowfax's pattern — buy capability, never vanity; use equity carefully; refuse bidding wars — is about as consistent a through-line as a decade-old startup can offer. That consistency does not guarantee the mix-shift bet pays off, but it does suggest the bet was made soberly rather than to dress a window.

Either way, the acquisition told investors something about intent: Shadowfax knew its core business was structurally thin and was actively hunting for a way out of the margin trap. Whether the market would reward that intent was about to be tested in the most public way possible.

VIII. The Public Debut: January 2026 IPO & Valuation Tug-of-War

By late 2025, the machinery of going public was in motion. Shadowfax had converted into a public limited company in preparation for the listing, the legal rite of passage that turns a private startup into a creature of the public markets.[^6] It filed its draft prospectus with SEBI, laying its financials, its client concentration, and its risks bare for the first time.1 The offer that emerged was substantial: a total issue of about ₹1,907 crore, split between a fresh issue of roughly ₹1,000 crore — money that would flow into the company to fund expansion and repay debt — and an offer for sale of about ₹907 crore, which let early venture backers cash out part of their long-held stakes.[^3][^5]

The IPO opened for subscription from January 20 to 22, 2026, at a price band of ₹118 to ₹124 per share, with the final price fixed at the top of the band, ₹124.[^3] Demand was respectable but not euphoric: the book was subscribed roughly 2.86 times overall by the close.2 For a company at the intersection of two hot themes, "2.86 times" was a lukewarm number in a market that had grown used to popular IPOs being subscribed dozens of times over. The tepid interest was a warning shot, and the loudest silence came from the wealthy individual investors — the non-institutional bucket, whose portion was undersubscribed, a classic tell that the smart retail money smelled thin listing gains.

Then came listing day, January 28, and the discount we opened with — ₹112.60 on the NSE, down about 9% from the issue price.[^5] So why did the market pour cold water on a growing, newly profitable company? Three reasons, and they are worth separating because they point at different things.

The first and biggest was valuation. At ₹124 a share, the company was priced at more than 1,000 times its trailing FY25 net profit of roughly ₹6 crore — a headline multiple so absurd it is almost meaningless, because it divides a large market value by a tiny, just-born profit.6 The more charitable way to look at it is forward-looking: annualize the accelerating H1 FY26 profit and you get something in the ₹42 crore range, which brings the forward multiple down to a still-demanding neighborhood of roughly 45 to 50 times earnings.6 Even on the generous math, the price left essentially no margin for error. Investors were being asked to pay up front for a profitability ramp that had only just begun and could stall.

The second was the concentration risk we have already met — Flipkart and Meesho looming over the revenue base — sharpened by a specific fear: that Meesho was building its own logistics network and could one day pull its volume in-house.6 The third was the mood-reading: the muted subscription, especially from wealthy individuals, dampened the grey-market enthusiasm that often front-runs a strong debut. In the Indian IPO ecosystem, the non-institutional and grey-market signals function as a rough crowd-sourced forecast of listing gains; when the wealthy money sits on its hands, the debut usually disappoints, and here it did.

There is also a capital-allocation subtext worth naming. Nearly half the total issue was an offer for sale — existing shareholders, largely early venture backers, selling down rather than fresh capital entering the business.[^3][^5] That is entirely normal for a company a decade old whose earliest investors are due an exit; funds have their own clocks. But a listing where insiders are net sellers of nearly ₹900 crore, priced at a triple-digit trailing earnings multiple, invites the obvious skeptical reading — that the people who know the business best were monetizing into public enthusiasm near the top of a valuation range. That is not an accusation of anything improper; it is simply the tension every richly priced, OFS-heavy IPO carries, and the market appeared to price it in on day one.

Step back and the listing discount reads less as a verdict on the business and more as a verdict on the price. The public market was not saying Shadowfax is a bad company; it was saying this is a fragile, thin-margined, concentration-heavy company, and you priced it like a proven compounder. That tension — a genuinely interesting operating story wrapped in a demanding valuation — is the single most important thing for a long-term investor to hold in mind. And to judge whether the growth can grow into the price, you have to look under the hood at where the money is actually made.

IX. Segment Breakdown: Where the Money is Made

If you want to understand any logistics company, ignore the marketing and follow the parcels. Shadowfax runs on three engines that could hardly be more different in character — one huge and thin, one fast and dense, one tiny and rich — and the company's entire future depends on shifting its weight from the first toward the third.

The first and dominant engine is express delivery — standard e-commerce parcel delivery and reverse logistics — which makes up the bulk of revenue, on the order of 60–70%.6 This is the high-volume backbone, the business that moves Meesho and Flipkart packages across those 14,700-plus pin codes.6 It is also, bluntly, the worst business of the three. Margins here are wafer-thin, competition is savage, and the field is crowded with Delhivery, Xpressbees, and Ecom Express all fighting over the same merchants.[^14] Shadowfax competes on operational sharpness — faster reverse pickups, same-day delivery in metros using its local hubs — but the honest truth is that it has essentially no pricing power in this segment. When your customers are giants and your rivals are numerous, you are a price-taker. This engine provides the density that makes everything else work, but it does not, on its own, make anyone rich.

The second engine is hyperlocal and quick commerce, roughly 20% of revenue and the fastest-growing piece, expanding well north of 50% year on year.6 This is the ten-minute-groceries world — providing third-party rider capacity to the quick-commerce platforms during their brutal peak hours. The economics here are better than express because the density is extraordinary: quick commerce concentrates enormous order volume into tight urban grids, which is precisely the condition under which an asset-light crowdsourced fleet shines. When a platform needs a surge of riders for the dinner rush, Shadowfax can supply that flex capacity and capture the highest yield-per-hour its riders will earn all day. Strategically, this is the segment that most vindicates the original thesis — Shadowfax's gig fleet is natively built for the speed quick commerce demands, and being the largest independent, non-captive network gives it a seat at every platform's table.

The third engine is the value-added enterprise business anchored by CriticaLog — the smallest slice at roughly 10% of revenue, but by far the highest margin, in a different league from the consumer segments.6 This is where the high-value, time-critical shipments live, where switching costs are real and contracts come with strict service-level guarantees. It is the antidote to everything painful about the other two engines: insulated from consumer pricing wars, protected by integration and trust, and durable through cycles.

Before drawing the strategic conclusion, it is worth puncturing a couple of consensus myths that cling to this stock. The first myth is that Shadowfax is a "quick-commerce company" riding the ten-minute-grocery wave. The reality is that quick commerce is only about a fifth of revenue; the company is, first and foremost, a commodity e-commerce parcel business with a fast-growing hyperlocal wing.6 Buyers who priced the IPO as a pure quick-commerce play were buying a different company than the one in the prospectus. The second myth is that "asset-light" means "capital-light forever." In truth, an asset-light logistics network still consumes real cash — not on trucks, but on the relentless acquisition and retention of riders who churn at rates approaching total turnover each year. The capital simply shifts from the balance sheet (vehicles) to the income statement (rider incentives), where it is harder to see but no less real. Calling the model capital-light describes where the money goes, not whether it is spent.

Here is the strategic geometry that a long-term investor should hold onto. The largest engine is the one with the worst economics; the smallest is the one with the best. Shadowfax's bull case is, at its core, a mix-shift story — the hope that hyperlocal and enterprise grow faster than commodity express, dragging the blended margin upward over time. The bear case is that express is so dominant that even rapid growth in the small, rich segments cannot move the consolidated margin fast enough before a customer defection or a payout spike knocks the whole thing back into the red. Which of those futures wins is not a matter of narrative; it is a matter of competitive structure — so let's war-game it properly.

X. Hamilton Helmer's 7 Powers & Porter's 5 Forces

To test whether Shadowfax has a durable edge or merely a clever trick, it helps to run it through two disciplined frameworks: Hamilton Helmer's 7 Powers, which asks what actually protects a company's profits, and Michael Porter's Five Forces, which asks how much of the value a company creates it can keep versus surrender to customers, suppliers, and rivals. The two together separate a real moat from a good story.

Start with the powers Shadowfax can plausibly claim. Its strongest is scale economies — but of an unusual, local kind. This is not the global scale of a chip fab; it is grid-level density. The more shipments Shadowfax pushes through a specific city grid, the higher its rider utilization, the lower its cost per delivery, and the wider its margin. That local-density flywheel is genuinely defensive within a market, though it must be won city by city rather than nationally. Layered on top is a network effect of the classic two-sided kind: a deeper pool of active riders means faster, more reliable delivery, which attracts more merchants, whose volume boosts rider earnings, which draws still more riders. It is real but only medium-strength, because in this industry loyalty on both sides is shallow — riders and merchants alike will defect for a better deal.

The most interesting claim is counter-positioning. Shadowfax's asset-light, gig-based, fully-variable cost structure is something the legacy carriers structurally cannot copy without cannibalizing themselves. Blue Dart and the integrated players are locked into trucks, planes, hubs, and salaried staff — fixed costs that make sense for their world and become an anchor in on-demand delivery. An incumbent that tried to go asset-light would be admitting its existing model is obsolete, so it hesitates. That hesitation is the essence of counter-positioning, and it is a high-strength advantage against the old guard, though notably not against other gig-native upstarts who share the same structure.

The Frodo engine and the operational know-how of herding a 200,000-strong fluid workforce function as a cornered resource of medium strength — hard to replicate, but not patent-protected magic; a determined, well-funded rival could approximate the frogging logic over time. And switching costs are the weakest link. In the core e-commerce business they are low: merchants re-route parcels through shipping aggregators with a few clicks, which is why Shadowfax has no pricing power there. Only in the CriticaLog enterprise niche do switching costs turn genuinely high, and that is the smallest part of the company.

Now the Five Forces, which mostly explain why the margins are so thin. The threat of new entrants is low-to-medium — writing routing software is easy, but assembling and managing a reliable network of hundreds of thousands of distributed gig riders, with all the onboarding, payouts, and local sortation hubs, is a punishing operational barrier. The bargaining power of buyers, however, is extremely high — the marketplace giants can and do squeeze 3PL pricing to the bone, and that single force is the biggest reason express margins are microscopic. The bargaining power of suppliers — the riders — is medium-to-high and rising, because annual churn runs near total and every quick-commerce and food-tech player is bidding for the same fleet, forcing Shadowfax to keep spending on acquisition and retention.

The two forces that should worry an investor most are substitutes and rivalry. The threat of substitutes is high and specific: Shadowfax's own biggest customers are building captive, in-house logistics. Meesho launched Valmo, a marketplace that crowdsources micro-logistics partners directly — precisely the layer Shadowfax provides.4 Flipkart keeps optimizing eKart. If either succeeds in pulling volume in-house, Shadowfax loses density where it hurts most. And competitive rivalry among Delhivery, Xpressbees, and Ecom Express is brutal, an ongoing price war that keeps industry-wide net margins paper-thin. It is instructive to hold Shadowfax up against Delhivery, the listed incumbent that took the opposite path. Delhivery built a heavy, integrated network — its own sortation centers, line-haul trucks, and infrastructure — and its investment case rests on the durability of that physical moat and the operating leverage of owned scale.[^14] Shadowfax's case rests on the opposite proposition: that owning nothing and renting everything is cheaper and more flexible, especially in the ultra-fast hyperlocal segment where a fixed truck-and-hub network is the wrong tool entirely. Neither is obviously right; they are bets on different futures of Indian commerce. If the future is dominated by intercity, planned e-commerce shipments, the heavy model's control and reliability win. If it tilts toward local, unplanned, ten-minute delivery, the asset-light gig model is structurally better suited. Shadowfax is, in effect, a leveraged bet that the center of gravity in Indian delivery keeps shifting local and fast — which is also why the disintermediation threat is so dangerous, since the platforms driving that local shift are the very ones that could build their own gig networks.

Run both frameworks together and the verdict is nuanced: Shadowfax has a real, defensible edge in local density and counter-positioning against legacy carriers, but that edge is hemmed in by powerful buyers, volatile suppliers, and the ever-present threat that its customers become its competitors. The moat is real; it is just narrow. From that structural reading flow the wider lessons.

XI. Playbook: Business & Investing Lessons

Step back from the parcels and the P&L, and Shadowfax offers a handful of durable lessons — for operators building in low-margin industries and for investors trying to tell a genuine edge from a well-told story.

The first lesson is the power of cross-vertical asset sharing, and it generalizes well beyond delivery. The holy grail of any low-margin, capacity-constrained business is to raise the utilization of an expensive shared resource. Airlines obsess over load factor; hotels over occupancy; Shadowfax over tasks per hour. Its real insight was to stop thinking of a rider as a "food delivery boy" or a "courier" — job titles that lock a worker into one demand curve and one set of idle hours — and to reconceive him as a generic unit of delivery time that can be pointed at whatever demand is live. By abstracting the rider and sharing him across verticals through frogging, Shadowfax unlocked utilization rates a single-vertical platform structurally cannot match. Wherever you find a business sitting on an underutilized shared asset, ask whether someone could co-mingle demand across it the way Frodo does across riders. The catch, and the reason this is a lesson rather than a guarantee, is that co-mingling only pays when the pooled demand is dense enough to keep the asset genuinely busy — in a thin market, sharing an idle resource across five verticals just spreads the idleness. The strategy is powerful precisely where scale already exists, which is why it tends to entrench incumbents in dense geographies rather than help challengers in sparse ones.

The second lesson is M&A as a capability shortcut, not a vanity purchase. Across a decade, Shadowfax's acquisitions traced one consistent logic. Pickingo bought a running start and an engineering team in the north. NuvoEx bought instant reverse-logistics scale and client relationships without spending cash. CriticaLog bought entry into a high-margin enterprise niche at a disciplined price. None of these were about buying revenue to look bigger; each plugged a specific technical or market-access gap that would have taken too long to build. For investors, the tell of good M&A is exactly this — small, purposeful deals that close a capability gap — versus the warning sign of large, expensive deals justified by "scale" and "synergies" that never quite materialize.

The third lesson is the darker one: the danger of monopsony in B2B logistics. Volume is the lifeblood of an asset-light network, but volume concentrated in the hands of a couple of massive marketplaces is a poisoned gift. When your two biggest customers control a dominant share of your parcels, you are, functionally, a captive vendor wearing the costume of an independent public company. They set your price, and they hold the option to replace you with something they build themselves. True independence — the kind that supports durable pricing power and a premium valuation — requires a diversified base of high-yielding customers who need you more than you need any one of them. Shadowfax knows this; the CriticaLog move and the hyperlocal push are both attempts to escape it. Whether they escape fast enough is the question that hangs over the whole investment, and it is best examined by stress-testing the bull and bear cases directly.

XII. Stress Test: The Bull vs. Bear Case & Current Risk Radar

Every investment case is really an argument between two futures. Here is Shadowfax's, argued honestly from both sides, framed around the risks that could decide it.

Take the risk radar first, because these are the specific mechanisms that could break the story. The most acute is client disintermediation. Meesho's Valmo is not an abstract threat; it is a live platform designed to crowdsource micro-logistics partners directly, cutting out the 3PL middle layer that Shadowfax occupies.4 If Meesho migrates a meaningful share of its volume onto its own rails, Shadowfax does not just lose a customer — it loses the density that makes its urban economics work, and thin margins can flip back to losses quickly when density falls. The same logic applies, more slowly, to Flipkart and eKart.

The second radar item is regulatory. The entire asset-light edifice rests on treating riders as independent gig workers rather than employees. India's evolving labor architecture — the Code on Social Security and a wave of state-level gig-worker protection bills — threatens exactly that arrangement.[^12] If courts or state governments mandate provident-fund contributions, insurance, or minimum wages for gig workers, the "fully variable cost" that defines Shadowfax's model would harden into fixed cost, and its structural advantage over the salaried incumbents would erode overnight. This is not a tail risk to wave away; it is an active, watch-this-space overhang for every gig-economy business in the country. The mechanism to model is straightforward: today a rider is paid per task and nothing else, so when volume falls, Shadowfax's cost falls in lockstep. Impose a floor — mandatory social-security contributions, a minimum guaranteed wage, insurance — and a portion of that cost becomes fixed, owed regardless of how many parcels move. In a business earning low-single-digit margins, even a few percentage points of newly fixed rider cost is the difference between profit and loss. The cruel irony is that the same regulation would hit every gig competitor too, so it would not necessarily change Shadowfax's relative position; it would simply compress the whole industry's economics and could force delivery prices up, testing how much of the cost the marketplace giants would tolerate passing on to consumers. It is a systemic risk more than a company-specific one, but it strikes at the load-bearing assumption of the entire model.

The third is rider-cost inflation. With quick-commerce and food-tech players all scaling and bidding for the same fleet, the price of acquiring and retaining riders can spike, and on margins this thin, a modest rise in payouts is enough to erase the profit. These three risks — disintermediation, regulation, and rider costs — are the load-bearing walls of the bear case.

The bull case is genuinely compelling on its own terms. Shadowfax is the premier independent, non-captive hyperlocal network in a country where quick commerce and direct-to-consumer brands are exploding. Brands that want ten-minute delivery but refuse to build their own fleet have a natural partner, and being the neutral option — not owned by any one marketplace — is itself a selling point to platforms wary of feeding a rival. If management can scale CriticaLog and the broader enterprise segment from roughly a tenth of revenue toward a fifth or a quarter, the blended EBITDA margin could climb from its current low-single-digit level toward the mid-single digits, and in a thin-margin business, a doubling of margin drives a dramatic re-rating. And the profitability engine is demonstrably on — the accelerating H1 FY26 numbers are the operating leverage the thesis always promised, now showing up in cash.6

The bear case is equally coherent, and an activist skeptic would press three points. First, the margin trap: the 70%-ish core is structurally broken, caught between buyers who compress price and riders who demand more, and no amount of routing cleverness repeals that vise. Second, the captive-future risk: should Flipkart or Meesho pull volume in-house, Shadowfax is left with stranded capacity and collapsing density — the asset-light model run in reverse. Third, the valuation: even after a listing discount, the forward multiple prices in flawless execution, so any quarterly wobble in volume or rider retention invites a sharp de-rating. On governance and disclosure, a skeptic would also flag the founder-and-strategic-investor overlap — a top customer, Flipkart, sitting on the cap table as a major shareholder — as a related-party dynamic worth watching at contract-renewal time.6

The neutral synthesis is that both cases hinge on the same variable: can the mix shift toward higher-margin, stickier revenue outrun the erosion of the low-margin core? That is not a question of storytelling. It is a question of a few measurable numbers, which is where a disciplined investor should focus.

XIII. Epilogue & What to Watch

Shadowfax will spend the next twelve to eighteen months doing something it has never had to do before: proving itself to a skeptical public market, quarter by quarter, in full view. The listing discount was the market's opening bid in a long negotiation over whether this crowdsourced machine can compound durable profits or merely survive on thin ones. The company does not get to argue the point; it has to demonstrate it.

For a long-term investor, the noise will be endless and most of it will not matter. Three metrics do. The first is active quarterly unique delivery partners — the roughly 200,000-plus rider base that is the company's true capacity.6 If that number holds or grows, the density flywheel keeps spinning; if it erodes under rider-cost competition, the whole model tightens. The second is the revenue contribution from non-express segments — hyperlocal plus enterprise. A rising share here is the single clearest signal that the mix-shift bull case is actually happening rather than merely being promised, and it is the number that most directly refutes or confirms the margin-trap bear case. The third is the adjusted EBITDA margin itself, which needs to march steadily off its low-single-digit base toward the mid-single digits to justify anything like a technology multiple. Why these three and not the dozen others a company discloses? Because each maps directly onto one leg of the investment thesis. The rider count is the supply side of the density flywheel — lose it and the cost advantage unwinds. The non-express revenue mix is the escape route from the margin trap — the single cleanest measure of whether the mix-shift bull case is materializing. And the EBITDA margin is the scoreboard — the number that ultimately decides whether the market's triple-digit-earnings-multiple skepticism was justified or whether operating leverage bails the valuation out. Revenue growth, by contrast, is almost a distraction here; this company has never struggled to grow the top line. Its entire question, from the first year of losses to the first year of profit, has always been whether growth converts into durable margin. Track the margin and the mix, and you are asking the only question that has ever mattered for Shadowfax.

One more thing a patient investor should keep an eye on: the behavior of its two whale customers. Any disclosure that Flipkart or Meesho is expanding its captive network, or any sign in the numbers that a large client's volume is shrinking, is the earliest warning that the density thesis is cracking. Conversely, a broadening of the client base — new large marketplaces, more direct-to-consumer brands, a growing enterprise book — would be the strongest evidence that Shadowfax is escaping the monopsony trap that defines its risk. The story from here is not about whether the machine works; it manifestly does. It is about who controls the volume that feeds it.

Watch those three, and you are watching the real business rather than the daily price.

Shadowfax began as a software-first rebel making an audacious claim: that you do not need to own the trucks to run a logistics empire — that a rider, a smartphone, and a good enough algorithm could beat concrete and capital. It has already won that argument with the venture capitalists, who funded it through a brutal winter, and with the operating results, which finally turned black. The unresolved question — the one that will define whether the January 2026 discount looks in hindsight like a bargain or a warning — is whether an asset-light machine, dependent on a handful of giant customers and a churning army of gig workers, can convert its cleverness into the kind of durable, compounding profit that public markets ultimately pay for. The engine is running. Now it has to prove it can pull the weight.

XIV. Outro & Links

This has been a deep dive into Shadowfax Technologies — the asset-light crowdsourcing rebel, its Frodo engine, its turnaround, its debut, and the tug-of-war over what it is truly worth. The comprehensive source materials and data are listed below.

References

-

Draft Red Herring Prospectus (DRHP) — Securities and Exchange Board of India, 2025-10-31 ↩

-

Shadowfax IPO Subscription Status — ICICI Direct, 2026-01-22 ↩

-

Shadowfax Acquires Reverse Logistics Firm NuvoEx — Business Standard, 2017-10-31 ↩↩↩↩

-

Meesho Launches Logistics Marketplace Valmo to Disintermediate 3PL Players — Moneycontrol, 2024-02-14 ↩↩

-

Shadowfax H1 FY26 Financial Disclosures — National Stock Exchange of India ↩

-

Shadowfax DRHP: Shareholding Structure & Key Executives — Inc42, 2025-11 ↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube