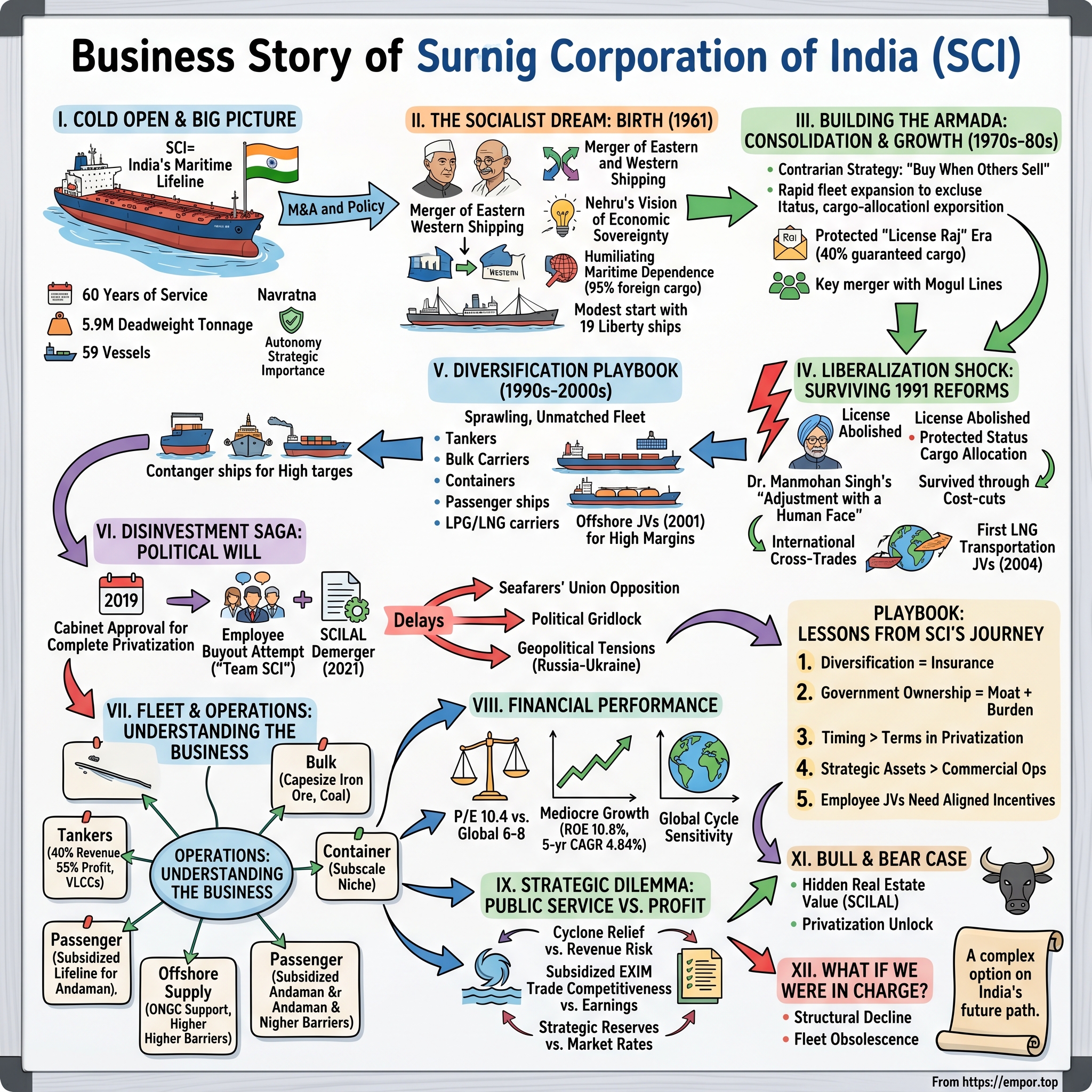

Shipping Corporation of India: The Story of India's Maritime Pioneer

I. Cold Open & The Big Picture

Picture this: A massive crude oil tanker, the size of three football fields, cutting through the Arabian Sea. Its hull bears the unmistakable red and white livery of the Shipping Corporation of India. For six decades, vessels like this have been India's maritime lifeline—carrying the nation's energy needs, connecting its trade routes, and flying the tricolor across international waters. Yet today, this 5.9 million deadweight tonnage fleet, operating 59 vessels across every conceivable shipping segment, faces an uncertain future.

SCI holds the prestigious "Navratna" status—one of only fourteen central public sector enterprises deemed crown jewels of the Indian state. This designation, meaning "nine gems" in Sanskrit, grants extraordinary financial and operational autonomy. Navratna companies can invest up to ₹1,000 crores without government approval, enter joint ventures, and restructure boards. It's the highest honor for a state enterprise, reserved for companies with consistent profits, strategic importance, and global competitiveness. Think of it as India's version of national champions—companies too important to fail, yet paradoxically, SCI is now slated for complete privatization with management control transfer.

The contradiction is striking. Here's India's largest shipping company by capacity, a profitable enterprise generating ₹906 crores in annual profit, a net foreign exchange earner for the country, and the government's go-to maritime operator during emergencies. During the 1990 Gulf War, SCI vessels evacuated 110,000 Indians from Kuwait. During COVID-19, its ships maintained critical supply chains when private operators balked. Yet the same government that depends on SCI during crises has approved its sale, attempting since 2019 to divest its 63.75% stake.

This isn't just another privatization story. It's a narrative about how a socialist-era institution navigated the treacherous waters of liberalization, survived competition from nimble private players, and remained relevant through six decades of political and economic upheaval. From its birth with 19 vessels in 1961 to today's diverse fleet of 59 ships, SCI has been witness to—and participant in—every major chapter of independent India's economic journey.

The timing of this story matters. As global supply chains realign, shipping capacity becomes strategic leverage. China controls 18% of global shipping capacity through state-owned enterprises. Singapore's NOL, South Korea's HMM, Japan's NYK—all demonstrate how nations use shipping companies as instruments of economic policy. Against this backdrop, India's decision to privatize its sole major shipping company raises fundamental questions about the role of state in strategic sectors.

What follows is the definitive account of how SCI was built, how it survived, and why its potential sale represents more than just another disinvestment transaction. It's a story about industrial policy, maritime ambition, and the eternal tension between public service and profit maximization. Most importantly, it's about what happens when a nation's strategic assets meet the market's invisible hand.

II. The Socialist Dream: Birth of a National Carrier (1961)

The monsoon had just broken over Bombay on that humid October morning in 1961. At Ballard Pier, where the Gothic revival architecture of the Port Trust Building watched over the Arabian Sea, officials gathered for what would seem, to casual observers, like routine bureaucratic reshuffling. Two small government shipping companies—Eastern Shipping Corporation and Western Shipping Corporation—were being merged. The documents were signed on October 2nd, Gandhi's birthday, a date deliberately chosen to signal that this was about more than corporate restructuring. This was nation-building.

To understand why Prime Minister Nehru's government obsessed over creating a national shipping company, you need to grasp the humiliation of maritime dependence. In 1947, when India gained independence, 95% of its international trade moved by sea—yet barely 6% of this cargo traveled on Indian-owned vessels. British shipping lines like P&O and British India Steam Navigation Company dominated Indian waters, extracting what economists called "the freight drain"—an estimated ₹60 crores annually flowing to foreign shipowners, equivalent to billions in today's money.

The geopolitical context made this dependence existential. The Suez Crisis of 1956 had demonstrated how quickly maritime routes could become weapons. When Egypt's Nasser nationalized the canal, global shipping rates spiked 40% overnight. India, importing essential commodities and oil, found itself at the mercy of foreign shipping cartels who could effectively blockade the economy without firing a shot. Nehru, architecting the Non-Aligned Movement, understood that political independence meant nothing without economic sovereignty—and economic sovereignty required controlling your own shipping.

The two companies being merged had humble origins. Eastern Shipping Corporation, established in 1950, operated from Calcutta with a handful of coastal vessels. Western Shipping Corporation, formed in 1956, ran services from Bombay. Together, they brought 19 vessels to the union—a modest fleet of 200,000 deadweight tons, mostly aging Liberty ships purchased from post-war surplus. The largest vessel, M.V. State of Bombay, displaced just 10,000 tons. Compare that to today's ultra-large container vessels exceeding 400,000 tons, and you understand the David-versus-Goliath nature of the undertaking.

The first Chairman, Sumati Morarjee, deserves special mention—not just as one of India's first female corporate leaders, but as someone who understood shipping viscerally. Daughter of a wealthy Marwari family, she had defied convention to enter business, taking over Scindia Steam Navigation Company after her husband's death. When appointed to lead SCI, she brought a fighter's instinct and deep industry knowledge. Her first board meeting allegedly lasted eleven hours as she grilled executives on every operational detail, from bunker fuel costs to crew training standards.

Under Morarjee's leadership, SCI's initial strategy was deliberate and focused: establish regular liner services connecting India to Europe, East Africa, and Southeast Asia. The company's first major route—Bombay to UK via Suez—launched in 1962 with fortnightly sailings. Freight rates were set 15% below conference rates (the shipping cartels that controlled pricing), a move that sparked retaliation from established players but won loyalty from Indian exporters tired of discrimination.

The early operations revealed systemic challenges. Indian ports lacked modern cargo-handling equipment, leading to turnaround times averaging 15 days versus 3-4 days in Singapore or Rotterdam. Ship maintenance expertise was scarce—SCI had to send engineers to Japan and Germany for training. Insurance was problematic; Lloyd's of London charged Indian-flagged vessels premiums 30% higher than British ships, citing "inexperienced crews"—a colonial hangover that took years of accident-free operations to overcome.

Yet the infant company had advantages state ownership provided. The government directed all public sector cargo—food grains from PL-480 imports, development materials for Five Year Plan projects, crude oil for new refineries—to travel on SCI vessels when available. This guaranteed cargo base, roughly 40% of revenues in early years, provided stability to invest in fleet expansion. By 1965, SCI had added 12 more vessels and ventured into tanker operations, anticipating India's growing energy needs.

The human dimension of building SCI often gets overlooked in corporate histories. The company recruited directly from maritime training institutes in Bombay and Calcutta, offering cadets something unprecedented—careers that could culminate in commanding positions, not just subordinate roles under foreign captains. Captain J.C. Anand, among SCI's first Indian masters, recalled in memoirs how emotional it was to hoist the Indian flag on international waters: "We weren't just sailing ships; we were showing the world that Indians could navigate, manage, and excel in global shipping."

This nation-building fervor sustained SCI through early crises. The 1962 Indo-China War disrupted Asian trade routes. The 1965 Indo-Pakistan War saw Pakistani submarines threatening Indian merchant vessels. During both conflicts, SCI ships continued operations, with crews volunteering for hazardous voyages to maintain essential supplies. The M.V. State of Uttar Pradesh, carrying wheat from Australia during the 1965 war, famously evaded submarine detection by sailing without lights through the Arabian Sea—a feat that earned its captain a gallantry award.

By the decade's end, SCI operated 38 vessels totaling 500,000 deadweight tons, a modest but meaningful presence in global shipping. Revenue had grown from ₹8 crores in 1961 to ₹45 crores in 1970. More importantly, the psychological impact was profound. Indian exporters no longer faced discriminatory conference rates. The freight drain reduced by 60%. And critically, India had demonstrated it could build strategic industrial capacity despite starting from virtually nothing—a template that would be replicated in steel, oil, and other sectors.

The socialist dream of maritime self-reliance was taking shape. But as SCI would soon discover, building ships was easier than navigating the choppy waters of global competition, oil shocks, and eventually, liberalization's creative destruction.

III. Building the Armada: Consolidation & Growth (1970s–1980s)

The telex machine at SCI's Nariman Point headquarters wouldn't stop chattering on that October morning in 1973. Oil prices had quadrupled overnight. The Yom Kippur War had triggered what would become known as the First Oil Shock, and shipping rates were going haywire—tanker spot rates jumping 300% in weeks. For most shipping companies, this was catastrophe. For SCI, paradoxically, it became the catalyst for transformation into India's undisputed maritime champion.

The crisis coincided with SCI's absorption of Jayanti Shipping Company, a private operator with 6 vessels that had fallen into financial distress. This wasn't charity—it was opportunistic expansion. Jayanti brought something precious: experienced crews and established routes to the Persian Gulf. As global shipping companies reeled from fuel costs that had surged from $20 to $400 per ton, SCI's protected position in Indian trades provided insulation. The government, needing to ensure oil imports regardless of cost, guaranteed SCI's tanker operations a cost-plus-15% return. This certainty, while private competitors bled cash, allowed aggressive fleet expansion.

The man orchestrating this expansion was Captain B.K. Gokhale, who took over as Chairman in 1974. A master mariner who'd worked his way up from cadet, Gokhale understood shipping cycles viscerally. "When others are selling, you buy. When others are buying, you build," he reportedly told his board. Following this contrarian philosophy, SCI acquired 15 second-hand tankers during 1974-75, when distressed sellers accepted 40% below replacement cost. The fleet jumped from 500,000 to 1.2 million deadweight tons in eighteen months.

The License Raj era, much maligned for stifling private enterprise, paradoxically enabled SCI's golden age. Every import required government permission, every foreign exchange allocation needed approval, and SCI sat at the nexus of this controlled economy. The Shipping Development Fund Committee, which allocated routes and cargo, essentially guaranteed SCI 40% of all government-controlled cargo—fertilizers for the Green Revolution, coal for power plants, crude for expanding refineries. Private Indian operators got 30%, foreign lines the remaining 30%. It was economic planning at its most dirigiste, but it worked for SCI.The strategic importance of shipping during conflict came into sharp focus during the 1971 Indo-Pakistan War. SCI vessels supported naval operations, with the Indian Navy blockading East Pakistan ports, cutting off escape routes for stranded Pakistani soldiers, effectively aiding what would become Bangladesh's independence. While private operators might have hesitated, SCI ships maintained operations throughout the conflict, demonstrating how state ownership guaranteed continuity during national emergencies. Captain K.S. Subramanian, commanding an SCI tanker during the war, later recalled navigating without navigation lights to avoid detection—commercial suicide for a private operator, but acceptable risk for a national carrier.

The 1986 merger with Mogul Lines Limited brought different dynamics. Mogul, established in 1906 and nationalized in 1974, operated prestigious passenger services including the famed Haj pilgrimages to Saudi Arabia. This wasn't just about adding vessels; it was about inheriting relationships, routes, and most critically, the technical expertise in passenger operations that SCI lacked. The combined entity now operated across every conceivable shipping segment—tankers, bulk carriers, passenger vessels, container ships—a diversification that would prove crucial when individual segments faced downturns.

But the protected paradise couldn't last forever. By the late 1980s, cracks were appearing in the License Raj edifice. Private operators, working through loopholes and political connections, began nibbling at SCI's guaranteed cargo base. International shipping lines, leveraging diplomatic pressure, demanded greater access to Indian trades. The Shipping Development Fund Committee's cargo allocation formula—40% SCI, 30% private Indian, 30% foreign—came under attack from all sides. SCI's revenue growth, which averaged 18% annually through the 1970s, slowed to single digits by decade's end.

The human capital SCI built during this period deserves recognition. The company established training institutes in Mumbai and Chennai, producing not just ratings and officers for its own fleet, but for the entire Indian maritime sector. By 1989, over 15,000 Indians worked on SCI vessels, with thousands more alumni commanding ships globally. This wasn't corporate social responsibility—it was strategic nation-building. Every trained Indian seafarer reduced dependence on foreign expertise, earned foreign exchange through remittances, and created a reserve pool for emergency mobilization.

Fleet modernization during the 1980s revealed both the advantages and constraints of state ownership. SCI could access concessional Japanese shipbuilding loans through government-to-government agreements, acquiring modern vessels at rates private competitors couldn't match. Yet every purchase required navigating bureaucratic approvals, from initial proposal through cabinet sanction to parliamentary oversight. A vessel acquisition that might take a private owner six months took SCI eighteen. The fleet grew to 2.5 million deadweight tons by 1990, but the average vessel age crept up to 15 years, compared to 10 years for leading global operators.

The financial performance during this consolidation phase was solid if unspectacular. Revenues grew from ₹45 crores in 1970 to ₹890 crores in 1990. Profit margins, protected by cost-plus government contracts, averaged 12-15%. Return on equity, however, declined from 18% in the mid-1970s to 11% by 1990, as capital employed expanded faster than profits. SCI was profitable, stable, and strategically important—but increasingly sclerotic, a characteristic that would nearly prove fatal when liberalization arrived.

As the 1980s ended, SCI stood as one of the world's largest shipping companies, ranking among the top 20 by deadweight tonnage. It had achieved what Nehru envisioned—maritime self-reliance, reduced freight drain, strategic autonomy. Yet this success bred complacency. Protected markets meant limited innovation pressure. Guaranteed cargo reduced customer service focus. Cost-plus contracts eliminated efficiency incentives. The company that had fought so hard to establish itself now faced its greatest challenge: not foreign competition or capital constraints, but its own institutional inertia. The comfortable monopoly was about to meet the market's creative destruction.

IV. Liberalization Shock: Surviving the 1991 Reforms

The telex that arrived at SCI headquarters on July 24, 1991, was brief but seismic: "Industrial licensing abolished for all industries except 18 specified sectors. Shipping not in the exception list." In one bureaucratic stroke, four decades of protected markets evaporated. The comfortable certainty of guaranteed cargo allocations, regulated freight rates, and restricted competition vanished into the monsoon humidity of that Mumbai morning. For an organization that had never truly competed, the liberalization earthquake measured 9.0 on the corporate Richter scale.

Dr. Manmohan Singh, the mild-mannered economist engineering India's economic transformation as Finance Minister, had warned state enterprises to prepare for "adjustment with a human face." But for SCI's 18,000 employees, watching private operators like Varun Shipping and Great Eastern suddenly free to compete for any cargo, any route, at any rate, this felt less like adjustment and more like abandonment. The Shipping Development Fund Committee, which had guaranteed SCI 40% of government cargo since the 1960s, was disbanded within months. The freight rate conferences that had provided pricing predictability dissolved into spot-market chaos.

The immediate impact was brutal. In fiscal 1991-92, SCI's capacity utilization plummeted from 94% to 67% as customers, freed from cargo allocation requirements, switched to cheaper or faster alternatives. Freight rates on the India-Europe container route, SCI's cash cow, collapsed 35% in six months as Maersk, Mediterranean Shipping Company, and Evergreen flooded the market with capacity. The company's first response was denial—surely the government wouldn't abandon its maritime champion? When reality hit, panic followed. Emergency board meetings stretched through nights as directors grappled with concepts alien to their experience: customer acquisition costs, yield management, competitive bidding.

Chairman Rear Admiral S.C. Chopra, appointed just months before liberalization, deserves credit for preventing complete collapse. A decorated naval officer who'd commanded the Eastern Fleet, Chopra understood crisis management viscerally. His first insight: SCI's problem wasn't ships but mindset. "We operated like a government department that happened to own vessels," he told senior management in a famous August 1991 all-hands meeting. "Now we must become a shipping company that happens to have government ownership."

The transformation began with brutal cost-cutting. Administrative expenses, bloated by decades of bureaucratic expansion, were slashed 30%. Non-core activities—the company guest houses, the sports clubs, the sprawling Mumbai residential colony—were divested or shut down. Early retirement schemes, offering packages up to 60 months' salary, reduced headcount by 3,000 within eighteen months. Union resistance was fierce; wildcat strikes paralyzed operations repeatedly through 1992. But Chopra, leveraging his military credentials and personal charm, kept complete breakdown at bay. More radical was the strategic pivot to international operations. Unable to compete on Indian coastal routes dominated by smaller, cheaper operators, SCI redirected its fleet to cross-trades—carrying Brazilian iron ore to China, Australian coal to Japan, Middle Eastern oil to Europe. These routes, requiring larger vessels and sophisticated logistics, played to SCI's strengths while avoiding direct competition with domestic players on Indian routes. By 1993, international operations generated 60% of revenues versus 35% in 1990.

Fleet modernization became existential necessity rather than strategic choice. The average vessel age of 15 years in 1990 made SCI uncompetitive against international operators running 7-8 year old fleets. Leveraging its sovereign backing to access Japanese export credits and European shipyard financing, SCI ordered 12 new vessels between 1992-1995, including its first VLCCs (Very Large Crude Carriers) and modern container ships. The capital expenditure—₹2,800 crores over three years—strained finances but proved prescient when shipping markets recovered in the mid-1990s.

The most visionary move was entering LNG transportation through joint ventures with Japanese shipping lines and a Qatari company, forming India LNG Transport Companies to operate vessels like S.S. Disha and S.S. Raahi, delivered in 2004 on 25-year charters to Petronet LNG. This wasn't opportunistic diversification but strategic positioning for India's energy transition. Natural gas would become increasingly critical for power generation and fertilizer production. By establishing early LNG transportation capability, SCI secured long-term contracts that would provide stable revenues for decades.

The human dimension of adjustment proved most challenging. Employees accustomed to lifetime employment faced performance reviews, variable compensation, and the specter of privatization. The officer-to-rating ratio, bloated at 1:3 compared to international standards of 1:5, required painful restructuring. Yet Chopra's masterstroke was converting resistance into ownership—literally. The employee stock purchase scheme, offering shares at discounted prices, made 8,000 employees shareholders by 1995. When workers owned the company, protecting its value became personal.

Customer service, an alien concept in the monopoly era, required cultural revolution. SCI established India's first 24/7 shipping customer service center in 1993, staffed by officers who could track cargo, resolve documentation issues, and handle claims in real-time. The company introduced electronic bills of lading, automated container tracking, and guaranteed transit times—innovations that seem routine today but were revolutionary for a PSU in the 1990s. Customer satisfaction scores, non-existent before liberalization, reached 76% by 1995.

Competition from foreign lines proved less devastating than feared, partly because SCI adapted quickly but mainly because India's trade growth exceeded all projections. Container traffic through Indian ports grew 15% annually through the 1990s. Crude oil imports doubled as refineries expanded. The pie grew faster than new entrants could consume it. SCI's market share in Indian trades declined from 40% to 22%, but absolute volumes increased 60%. The company that nearly collapsed in 1991-92 posted record profits of ₹215 crores by 1995-96.

The survival story contained broader lessons about economic transition. Protected enterprises could adapt to market competition, but required leadership willing to challenge institutional inertia, capital to modernize operations, and time to transform culture. SCI had all three—barely. Many other PSUs lacking these ingredients didn't survive liberalization's creative destruction. The Shipping Corporation that emerged from the 1990s crisis was leaner, more competitive, and strategically positioned for the next phase: diversification beyond traditional shipping into the entire maritime value chain.

V. The Diversification Playbook (1990s–2000s)

The boardroom at Shipping Bhawan erupted in rare applause on March 12, 1998. SCI had just won the contract to manage the Indian Navy's auxiliary fleet—a deal that seemed minor but represented a fundamental strategic shift. No longer would SCI define itself merely as a ship owner. It would become, in the words of then-Chairman Captain S.S. Srivastava, "India's complete maritime solutions provider." This wasn't diversification for its own sake—it was a calculated bet that maritime services would generate higher margins than commodity shipping while leveraging SCI's unique capabilities as India's only operator across all vessel segments.

The breadth of SCI's fleet by the late 1990s was staggering—perhaps unmatched globally for a single company. It operated crude oil tankers from MR (Medium Range) to VLCCs, making it India's largest tanker owner. The bulk carrier division handled everything from grain to coal. Container vessels served both mainline and feeder routes. The passenger ships, inherited from Mogul Lines, connected mainland India to the Andaman Islands and serviced Haj pilgrimages. LPG carriers transported cooking gas. Offshore supply vessels supported ONGC's oil exploration. This diversity, initially accidental—accumulated through mergers and government directives—now became strategic advantage.

Consider the LNG transportation entry, which exemplified SCI's evolving sophistication. When Petronet LNG needed ships for its Dahej terminal, SCI partnered with premier Japanese shipping lines and a Qatari company to form joint ventures in Malta, taking 29.08% equity stakes while securing 25-year charters for vessels delivered in 2004. The structure was elegant: Japanese partners brought technical expertise, Qatar provided Middle East relationships, Malta registration offered tax efficiency, and SCI contributed Indian market access plus operational management. The IRR exceeded 15%—remarkable for shipping investments.

The offshore services expansion told a different story—of nimble response to emerging opportunities. When ONGC accelerated deepwater exploration in the Krishna-Godavari basin in 2001, foreign offshore supply vessel (OSV) operators quoted rates that ONGC deemed excessive. SCI, which had never operated OSVs, acquired four vessels within six months, recruited Norwegian officers to train Indian crews, and underbid international competitors by 30%. Within five years, SCI dominated Indian offshore support, operating 16 vessels generating ₹400 crores annually—higher margin business than traditional shipping.

Technical and management services emerged as the hidden gem. SCI's maritime training institute, established in 1987, had produced thousands of certified officers. By 2000, SCI began marketing this expertise—managing third-party vessels, providing crew management services, conducting ship inspections, offering maritime consultancy. The Indian Navy contract was just the beginning. Soon SCI managed vessels for the Coast Guard, Geological Survey of India, even state governments. These services required minimal capital, generated 20-25% EBITDA margins, and created switching costs that locked in clients.

The 2016 creation of Inland & Coastal Shipping Limited as a subsidiary deserves special attention—not for its financial impact, which remained modest, but for what it represented strategically. India's inland waterways, despite 14,500 kilometers of navigable rivers and canals, carried less than 2% of domestic cargo versus 30% in China. The government's Sagarmala project aimed to change this. SCI's subsidiary, operating smaller vessels on routes like Kolkata-Varanasi and Mumbai-Goa, positioned the company for when—not if—inland shipping became economically viable. It was optionality at minimal cost.

The joint venture structures proved particularly sophisticated. By 2009, SCI had taken over complete technical and commercial management of its LNG vessels, having absorbed enough expertise from Japanese partners. This wasn't just about saving management fees—it was about capability building. SCI could now bid independently for LNG transportation contracts globally, no longer dependent on foreign technical partners. The student had become the master.

Yet the diversification strategy contained inherent tensions. Each segment had different capital requirements, operational cycles, and competitive dynamics. Tankers faced volatile spot markets; container shipping required network effects; offshore services demanded technical specialization; passenger operations needed customer service excellence. Managing this complexity strained organizational bandwidth. The company that once focused solely on cargo movement now juggled multiple business models, each requiring distinct capabilities.

The financial impact was mixed but generally positive. Revenues grew from ₹2,100 crores in 2000 to ₹4,800 crores in 2010—a CAGR of 8.6%, respectable if not spectacular. More importantly, earnings volatility decreased. When tanker markets collapsed in 2003, container operations cushioned the blow. When container rates plummeted in 2009, long-term LNG contracts provided stability. The portfolio effect worked—correlation between segments was surprisingly low, around 0.3, providing natural hedging.

The 2010 Further Public Offer (FPO), reducing government stake from 80% to 63.75%, marked a subtle but significant shift. For the first time, SCI had meaningful private shareholders—mutual funds, insurance companies, retail investors—who demanded quarterly performance, questioned capital allocation, and compared returns to private competitors. The comfortable PSU mentality, already eroded by liberalization, faced further pressure. Management discussions shifted from operational metrics to ROCE, from revenue growth to economic value added.

Human capital development, often overlooked in diversification stories, proved crucial. SCI established specialized training programs for each segment—LNG cargo handling in France, dynamic positioning for offshore vessels in Norway, container logistics in Singapore. By 2010, SCI employed over 4,000 officers, making it one of the world's largest employers of maritime professionals. This wasn't just about manning ships—it was about building institutional knowledge that competitors couldn't easily replicate.

The diversification playbook worked, but with caveats. SCI had successfully transformed from pure shipping company to maritime conglomerate. It had reduced earnings volatility, captured higher-margin services, and built strategic options for future growth. Yet questions remained. Was such broad diversification sustainable? Could a PSU excel across so many segments simultaneously? And most critically, what would happen if the government decided to exit entirely? These questions, academic in 2010, would become existentially urgent as the privatization saga unfolded.

VI. The Disinvestment Saga: A Tale of Political Will

The Cabinet note was marked "Secret" and circulated only to the Prime Minister's Office and key economic ministries on that November morning in 2019. After years of half-hearted attempts and political vacillation, the Modi government had finally decided: Shipping Corporation of India would be privatized completely, with management control transferred to a strategic buyer. The 63.75% government stake would be sold in one block. No residual government ownership, no golden share, no protective covenants. For a company that had embodied maritime nationalism for six decades, this was revolutionary—or depending on your perspective, sacrilege.

The timing seemed peculiar. SCI was profitable, generating nearly ₹1,000 crores annually. Global shipping markets were recovering from the 2016 trough. India's merchandise trade was projected to double by 2030, requiring massive shipping capacity. Why sell now? The answer lay not in SCI's boardroom but in North Block's fiscal mathematics. The government needed ₹1.75 lakh crores from disinvestment to fund infrastructure and social programs. SCI, with an enterprise value exceeding ₹15,000 crores, was low-hanging fruit—profitable enough to attract buyers, strategic enough to command premium valuations, yet not so critical that privatization would trigger public outcry like Air India or railways might.

December 2020 brought the formal process initiation. The Department of Investment and Public Asset Management (DIPAM) invited Expressions of Interest for the 63.75% stake sale. The terms were seductive: buyers would get India's largest shipping company, a diversified fleet, long-term government contracts, and prime real estate in Mumbai and other cities. The response was enthusiastic—Vedanta, Adani Ports, Dubai's DP World, and several international shipping companies submitted initial bids. Financial investors like Brookfield and GIC showed interest too, seeing opportunity in SCI's undervalued assets.

Then came the surprise that nobody saw coming. In March 2021, a consortium calling itself "Team SCI" submitted an EoI. This wasn't external raiders but SCI's own—400 current employees including senior officers, three former CMD's including the respected Captain Sunil Thapar, and critically, the Officer's Association representing 1,500 maritime professionals. Their bid was audacious: employees would contribute personal savings, raise debt against future earnings, and partner with financial investors to buy out the government. It was India's most ambitious employee buyout attempt, making global headlines.

The employee bid's logic was compelling. Who understood SCI's operations better than those running it? Who had greater incentive to preserve jobs and culture? The consortium argued that employee ownership would align interests perfectly—workers as owners would maximize productivity, reduce costs, and eliminate the principal-agent problems plaguing PSUs. They pointed to successful precedents: United Airlines' ESOP owned 55% before its IPO, Publix Super Markets remained employee-owned while competing with Walmart. Why shouldn't Indian maritime professionals own India's maritime champion?

Yet the government's response was lukewarm. DIPAM officials, speaking off-record, worried about execution risk. Could employees really raise ₹10,000+ crores? Would banks lend against future cash flows to a employee consortium? More fundamentally, would employee ownership deliver the efficiency gains privatization promised, or simply perpetuate PSU culture under different ownership? The bureaucracy's skepticism was palpable, though never officially stated.

The separation of non-core assets into SCILAL (SCI Land and Assets Limited) in 2021 revealed the hidden value within SCI. The company owned 11.5 acres in Mumbai's Worli locality worth ₹3,000 crores alone. Properties in Delhi, Chennai, Kolkata, and other cities added another ₹2,000 crores. The maritime training institutes, though strategically valuable, were worth ₹500 crores as real estate. SCILAL would retain these assets, compensating SCI through long-term leases. Buyers would get a pure shipping company, not a real estate play—which some saw as value destruction, others as focus enhancement.

Political complications multiplied through 2021-22. The Seafarers' Union, representing 3,500 ratings, opposed privatization vehemently, threatening indefinite strikes. Opposition parties, sensing opportunity, raised nationalist arguments—why sell profitable PSUs to private profiteers? Regional parties from maritime states worried about job losses in ports and shipyards. The Mumbai real estate lobby, eyeing SCI's prime properties, pushed for asset sales rather than company privatization. Each constituency had different interests, creating political gridlock.

The Russia-Ukraine war in February 2022 added unexpected complexity. Shipping rates spiked 40% as supply chains realigned. Energy security became paramount as Europe scrambled for non-Russian oil and gas. Suddenly, owning strategic shipping assets seemed prescient rather than outdated. The Ministry of Petroleum and Natural Gas, which depended on SCI for crude transportation, expressed reservations about privatization. What if private owners prioritized profits over energy security during crises? The strategic asset argument, dormant during peaceful times, resurfaced with vengeance.

By mid-2023, the privatization had stalled despite featuring in the government's 100-day action plan. Due diligence revealed complicated issues—long-term contracts with government entities that couldn't be easily transferred, environmental liabilities from decades of operations, pension obligations for retired employees that weren't fully funded. Each issue was solvable but required political decisions that nobody wanted to make before the 2024 elections.

The financial markets' reaction was telling. SCI's stock, which jumped 60% on privatization announcement in 2019, had given back most gains by 2023. Daily volumes dried up as investors couldn't determine whether privatization would happen, when, or at what terms. The uncertainty discount—the gap between SCI's market cap and sum-of-parts value—widened to 40%. Professional investors avoided the stock, retail investors couldn't understand it, and employees who knew the truth couldn't trade on inside information.

The current status remains frustratingly ambiguous. The government maintains privatization is "on track" without providing timelines. DIPAM continues "preparatory work" without specifying what that entails. Potential buyers remain interested but won't commit resources without clarity. Employees continue operations professionally while privately planning for multiple scenarios. It's corporate purgatory—neither PSU nor private, neither for sale nor off the market.

The saga reveals deeper truths about Indian privatization. Political will fluctuates with electoral cycles. Bureaucratic processes move glacially when accountability is diffused. Strategic asset arguments resurface during crises. Employee resistance cannot be ignored in democratic polities. And perhaps most importantly, profitable PSUs are paradoxically harder to privatize than loss-making ones—success reduces urgency while failure creates consensus. SCI's disinvestment saga isn't just about one company; it's about India's ambivalent relationship with state capitalism itself.

VII. The Fleet & Operations: Understanding the Business

Walk onto the bridge of SCI's newest VLCC, the M.T. Desh Gaurav, and you enter a technological marvel. The 333-meter vessel—longer than the Eiffel Tower is tall—can carry 2 million barrels of crude oil, enough to meet India's consumption for almost half a day. The bridge resembles a space station control room: ECDIS navigation systems, automated collision avoidance, satellite communications, remote machinery monitoring. Yet the most sophisticated technology isn't the equipment but the economics—this single vessel, operating on a one-year contract to Indian Oil Corporation, generates ₹120 crores annually while burning ₹60 crores in fuel and operating expenses. The business model is deceptively simple: move liquid cargo at industrial scale.

SCI's fleet composition reads like a maritime encyclopedia. The tanker division operates vessels across all size categories: MR (Medium Range) for refined products, LR-I and LR-II for longer routes, Aframax for medium crude volumes, Suezmax for transcontinental routes, and VLCCs for the massive Middle East to Asia crude movements. Each category serves specific trades, ports, and economic logic. A VLCC's economies of scale work for Saudi Arabia to Gujarat routes but would be useless for coastal petroleum distribution where draft restrictions and smaller parcels dominate.

The bulk carrier division tells a different story—of industrial logistics rather than energy transportation. SCI's 15 bulk carriers, ranging from Handymax (45,000 DWT) to Capesize (180,000 DWT), form the backbone of India's dry commodity trade. The M.V. Vishva Vijay, a Capesize vessel, operates a triangular route: iron ore from Brazil to China, coal from Australia to India, then ballast (empty) back to Brazil. This seemingly inefficient empty leg is actually optimal—repositioning costs are offset by high-paying cargo on two legs. Understanding these trade patterns separates profitable operators from bankruptcy candidates.

Container operations reveal network effects and their limitations. SCI's single container vessel, the M.V. Mumbai, operates on the India-Middle East route where freight rates average $800 per TEU (Twenty-foot Equivalent Unit). Compare this to Maersk operating 700+ vessels globally, achieving rates of $1,200 per TEU through network density. SCI cannot compete on global routes but finds niches—government cargo, defense shipments, routes other lines ignore. It's profitable but subscale, generating 8% of revenues despite containerized cargo representing 60% of global trade by value.

The passenger-cum-cargo vessels deserve special attention for their social rather than commercial importance. The M.V. Nancowry and her sisters connect the Andaman & Nicobar Islands to mainland India, carrying 1,200 passengers and 1,000 tons of cargo per voyage. Tickets are subsidized—₹2,000 for a journey that costs SCI ₹8,000 to provide. The annual loss exceeds ₹50 crores. Yet these ships are lifelines for 400,000 islanders, transporting everything from vegetables to vehicles. Private operators wouldn't touch this business; SCI has no choice. It's the clearest example of public service obligations trumping commercial logic.

The LNG operations showcase sophisticated financial engineering. Through joint ventures, SCI manages four LNG tankers with cargo capacities ranging from 138,000 to 173,000 cubic meters, on long-term charters to Petronet LNG and ExxonMobil. These aren't spot market plays but infrastructure investments. A 25-year charter at fixed rates provides predictable cash flows that banks love—project IRRs exceed 12%. The technical complexity is staggering: maintaining cargo at -162°C, managing boil-off rates, ensuring zero cargo contamination. One temperature excursion can destroy $100 million in cargo value.

Offshore supply vessels (OSVs) represent SCI's most technically demanding operations. Platform supply vessels like SCI Panna don't just transport materials to oil rigs—they maintain position within 2 meters using dynamic positioning, transfer cargo in 4-meter swells, and serve as emergency evacuation vessels. The business model is equally complex: day rates of $25,000 seem attractive until you factor in 60-day mobilization periods, specialized crew costs, and utilization rates averaging only 70%. When oil prices crashed in 2014, day rates halved overnight. SCI survived because ONGC, the primary customer, prioritized indigenous tonnage over pure economics.

Revenue segmentation reveals portfolio dynamics. Tankers generate 40% of revenues but 55% of profits—high capital efficiency when markets are strong. Bulk carriers contribute 25% of revenues but only 15% of profits—commodity shipping is brutally competitive. Offshore vessels, just 10% of revenues, provide 20% of profits through technical barriers to entry. Container and passenger operations barely break even but provide strategic value—government relationships and social license to operate.

The global competitive positioning is sobering. SCI ranks 30th globally by deadweight tonnage—significant but not dominant. In tankers, it competes against Frontline (106 vessels), Euronav (72 vessels), and Chinese giants like COSCO (1,300+ vessels across all segments). In bulk carriers, Chinese and Greek operators with lower costs and newer fleets dominate. SCI's competitive advantage isn't scale or cost but India-specific factors: cabotage rights (reserved coastal cargo), government relationships, and understanding of Indian port infrastructure where 30% of global ports face draft restrictions that limit vessel size.

Managing vessels for government departments adds complexity but ensures baseload revenue. SCI operates research vessels for the National Institute of Ocean Technology, patrol vessels for the Coast Guard, and logistics ships for the Navy. These contracts, typically cost-plus-15%, provide ₹300 crores in stable annual revenue. More importantly, they create switching costs—no private operator has the security clearances, operational experience, and trust to immediately replace SCI in strategic roles.

The Maritime Training Institute in Mumbai, graduating 400 officers annually, is both cost center and strategic asset. Training costs ₹2 crores per batch but creates competitive advantage—SCI officers, trained on diverse vessel types, command premium salaries globally. Alumni networks ensure SCI has allies in every major port, classification society, and maritime organization. It's soft power that doesn't appear on balance sheets but influences everything from regulatory decisions to cargo allocations.

Understanding SCI's operations requires appreciating this complexity—it's not one business but fifteen, each with distinct economics, competitive dynamics, and strategic rationales. The synergies are limited; a tanker officer can't easily manage container operations. Yet the portfolio provides resilience that pure-play operators lack. When tanker markets crash, bulk carriers might thrive. When offshore struggles, LNG contracts provide stability. It's industrial conglomerate logic applied to maritime transport—unfashionable in MBA textbooks but practical in volatile shipping markets. The question is whether private owners would maintain this diversity or focus on core profitable segments, abandoning social obligations that define SCI's unique character.

VIII. Financial Performance & Market Dynamics

The numbers tell a story of adequate mediocrity. SCI's market capitalization of ₹9,417 crores against revenues of ₹5,408 crores implies a price-to-sales ratio of 1.74—neither distressed nor premium. The profit of ₹906 crores suggests a P/E ratio of 10.4, below the Nifty's 22 but above global shipping peers trading at 6-8x. This middle ground captures SCI perfectly: profitable enough to avoid crisis, not dynamic enough to excite growth investors. It's the financial equivalent of a cargo ship—steady, reliable, uninspiring.

The five-year revenue CAGR of 4.84% deserves deeper scrutiny. During this period, India's merchandise trade grew 7% annually, global seaborne trade expanded 5%, and freight rates increased 6% on average. SCI underperformed every relevant benchmark. Why? The answer lies in capacity constraints. While competitors added vessels aggressively—Maersk's fleet grew 8% annually, MSC's 12%—SCI's fleet actually shrank from 70 to 59 vessels. Government approval processes for capital expenditure meant SCI took three years from vessel identification to delivery while private operators managed in eighteen months. By the time SCI's new tonnage arrived, market cycles had often turned.

The three-year average ROE of 10.8% seems reasonable until you decompose it. Asset turnover of 0.4x is abysmal—SCI generates only ₹0.40 in revenue per rupee of assets versus 0.7x for efficient operators. Net profit margin of 16.7% looks healthy but is inflated by subsidized government contracts and tax benefits. Leverage of 1.6x is conservative by shipping standards where 3-4x is common. SCI has the margins of a premium operator, the asset efficiency of a struggling one, and the leverage of a utility. It's an unusual combination that reflects PSU dynamics—profitable operations hamstrung by capital allocation constraints.

Segment profitability analysis reveals stark disparities. The tanker division's ROCE of 18% reflects both operational excellence and favorable contracts with oil PSUs. Bulk carriers barely cover cost of capital at 9% ROCE, destroyed by Chinese overcapacity. Offshore services generate 22% ROCE but on a small capital base. Container operations are ROCE-negative after allocating corporate overheads. The passenger segment would show negative 50% ROCE if social obligations were properly costed. Portfolio theory suggests diversification reduces risk, but in SCI's case, it also reduces returns by forcing capital into subscale or mandated businesses.

Working capital management is surprisingly efficient. Days sales outstanding at 68 days beats private operators averaging 85 days, partly because government entities, while slow, eventually pay. Inventory days are irrelevant for service businesses. Days payable outstanding at 95 days reflects PSU payment credibility—suppliers accept delayed payments knowing SCI won't default. The negative working capital cycle provides free financing worth ₹400 crores annually. It's one area where government ownership provides tangible advantage.

Global shipping cycles dominate financial performance more than management actions. The 2003-2008 supercycle, driven by Chinese commodity demand, saw SCI's profits surge 10x. The 2009 financial crisis crashed rates 90%; SCI posted losses despite cost cuts. The 2016 container shipping bankruptcy wave that claimed Hanjin barely affected SCI given its limited container exposure. The 2020-2021 COVID boom that saw container rates rise 10x benefited SCI marginally given its single container vessel. This cyclicality makes five-year averages misleading—one good year can offset four bad ones.

Competitive analysis reveals structural disadvantages. Labor costs at ₹1,200 crores annually are 30% higher than private Indian operators paying ₹900 crores for similar operations. This isn't just about pay scales—PSU employment rules, union agreements, and social obligations inflate costs. Fuel efficiency lags too; SCI's fleet averages 15 years age versus 10 years for leading operators, meaning 20% higher fuel consumption per ton-mile. These structural costs create a permanent 15-20% disadvantage that even excellent operations cannot overcome.

Yet SCI possesses hidden financial strengths. The ₹5,000 crores in real estate value separated into SCILAL isn't reflected in shipping operations. Long-term contracts with government entities provide ₹2,000 crores in predictable annual revenue. The training institute, while costly, creates human capital worth ₹100 crores annually in reduced recruitment and training costs. Tax benefits from PSU status save ₹200 crores annually. Adjusted for these factors, SCI's true ROE might be 13-14%, respectable if not spectacular.

Stock price volatility tells its own story. Beta of 1.4 indicates 40% more volatility than the broader market—unusual for a supposedly stable PSU. The volatility stems from three sources: shipping cycle sensitivity, privatization speculation, and thin trading volumes. On privatization rumors, the stock jumps 10%; on delays, it crashes 15%. This creates opportunities for traders but destroys long-term value as management cannot plan beyond quarterly earnings calls.

Peer comparison is challenging given SCI's unique profile. Pure-play tanker companies like Scorpio Tankers trade at 0.5x book value but with 25% ROE in good years. Diversified operators like A.P. Moller-Maersk trade at 1.2x book with consistent 15% ROE. Regional specialists like Pacific Basin focus on single segments achieving 20% ROE but with higher risk. SCI falls between categories—too diversified to be a pure play, too subscale to be a global major, too constrained to be entrepreneurial. It's the financial reflection of strategic ambiguity.

The dividend policy reveals government priorities. Payout ratio of 30% is conservative by PSU standards where 50-60% is common. This suggests either growth ambitions requiring retained earnings or government recognition that shipping requires reinvestment. The ₹20 per share annual dividend provides 3.5% yield—attractive for income investors but insufficient for growth seekers. It's another example of SCI's middle-ground positioning—neither growth nor value but something undefined between.

Currency exposure adds complexity. Revenues are 70% dollar-denominated from international operations while costs are 60% rupee-denominated from Indian crew and operations. This natural hedge should be advantageous, but accounting standards require mark-to-market of dollar debt creating quarterly earnings volatility. A 5% rupee depreciation adds ₹200 crores to debt but also increases future revenue value by ₹300 crores—economically positive but optically negative. Few investors understand this dynamic, creating valuation inefficiencies.

The financial narrative is ultimately about potential versus performance. SCI has the assets, relationships, and market position to generate 15-18% ROE sustainably. It achieves 10-11%. The gap—worth ₹500 crores annually—stems from structural constraints, not operational failures. Whether privatization closes this gap depends on the buyer's ability to restructure costs, optimize capital allocation, and focus on profitable segments while managing political pressures to maintain unprofitable social obligations. The financial performance isn't bad—it's just frustratingly below what it could be.

IX. The Strategic Dilemma: Public Service vs. Profit

Picture this scenario: A cyclone devastates the Andaman Islands, cutting off 400,000 residents from essential supplies. Private shipping lines calculate the risk—damaged ports, insurance complications, opportunity cost of lucrative commercial routes—and decline service. SCI's vessels arrive within 48 hours, carrying food, medicine, and rescue equipment, operating at substantial losses. This isn't hypothetical; it happened during Cyclone Lehar in 2013, Cyclone Vardah in 2016, and countless other emergencies. The question isn't whether this public service has value—it clearly does—but whether a profit-maximizing entity would provide it.

The strategic petroleum reserve obligation exemplifies this tension perfectly. SCI maintains dedicated crude carrying capacity for the Indian Strategic Petroleum Reserve, ensuring 90 days of emergency supply. During normal times, this dedication means foregoing spot market opportunities that could generate 30% higher returns. During the 2019 Strait of Hormuz crisis when Iran threatened to close the waterway carrying 20% of global oil supply, these vessels became invaluable. The insurance value of guaranteed energy security is enormous but doesn't appear in quarterly earnings. How do you price existential risk mitigation?

Supporting India's EXIM trade involves subtle subsidies rarely acknowledged. SCI charges Indian exporters 10-15% below international conference rates on many routes, effectively subsidizing trade competitiveness. For textile exporters from Tirupur competing against Bangladesh, this discount can determine commercial viability. The foregone revenue—approximately ₹300 crores annually—is SCI's invisible contribution to export promotion. A privatized SCI would likely eliminate these discounts, potentially impacting India's trade balance by making exports less competitive.

Cross-subsidization within SCI's portfolio is Byzantine in complexity. Profitable tanker operations subsidize loss-making passenger services. Long-term government contracts at below-market rates are offset by spot market operations. Training institute losses are justified by creating industry-wide human capital. Real estate appreciation compensates for operational underperformance. It's corporate socialism where each according to their ability funds each according to their need. MBA programs would condemn this as value destruction; national planners see it as portfolio optimization.

Comparison with global state-owned shipping companies reveals different models. China's COSCO Shipping, with 1,300+ vessels, operates commercially while maintaining strategic reserves for government direction. Singapore's Neptune Orient Lines (before its sale) balanced commercial operations with national trade facilitation. Japan's Big Three (NYK, MOL, K-Line) receive subtle government support through cargo preferences and financing. Each country calibrates the public-private balance differently, but none operates on pure commercial terms.

The employee welfare obligations add another dimension. SCI provides housing, healthcare, and education support for 15,000 direct employees and 50,000 dependents. The annual cost exceeds ₹200 crores—money that private operators would redirect to shareholders. Yet this paternalistic approach creates loyalty and institutional knowledge valuable during crises. When COVID-19 stranded crews globally, SCI's employees continued operations knowing their families were protected. Can you quantify the value of operational continuity during pandemics?

Environmental and social governance (ESG) before ESG became fashionable characterized SCI's operations. The company adopted cleaner fuel standards five years before regulatory requirements, installed ballast water treatment systems ahead of mandates, and maintains higher safety standards than commercial peers. This costs approximately ₹150 crores annually in additional compliance expenses. Private operators might optimize to regulatory minimums; SCI optimizes to social expectations even when commercially irrational.

The strategic asset argument gains credence during geopolitical tensions. During the 1971 Indo-Pakistan War, when the US Navy's Task Force 74 was deployed to the Bay of Bengal to intimidate Indian forces, merchant shipping became quasi-military assets. SCI vessels maintained supply lines despite submarine threats. In future conflicts, would foreign-owned or foreign-flagged vessels service Indian ports under threat? The insurance premium for guaranteed logistics during conflict is incalculable but real.

Why privatization might make sense starts with capital allocation efficiency. SCI needs ₹10,000 crores for fleet modernization over the next decade. Government capital comes with bureaucratic delays, political interference, and competing social priorities. Private capital comes quickly but demands returns. The global shipping industry is consolidating—scale matters more than ever. SCI's 59 vessels cannot compete against Maersk's 700+ or MSC's 600+. Without massive capital injection, SCI risks irrelevance.

Operational flexibility under private ownership could unlock value. Imagine SCI focusing solely on profitable tanker and LNG operations, exiting subscale container and bulk segments, and outsourcing non-core activities. ROCE could jump from 10% to 20% within three years. The company could pursue international acquisitions, enter derivative markets for risk management, and optimize tax structures through favorable jurisdictions. None of this is possible under government ownership with its political oversight and regulatory constraints.

The counter-argument is equally compelling. Privatization might maximize financial returns but minimize social value. Would private owners maintain loss-making passenger services to remote islands? Would they accept below-market government contracts during emergencies? Would they invest in maritime training that benefits competitors? The externalities—positive spillovers from SCI's operations—likely exceed ₹1,000 crores annually. Privatization might capture this value for shareholders while destroying it for society.

The middle path—partial privatization with golden shares or specific performance obligations—seems logical but proves difficult in practice. How do you enforce public service obligations on a private entity? What happens when commercial and social objectives conflict? International experience suggests hybrid models create the worst of both worlds—neither fully commercial nor fully public service-oriented. The clarity of complete privatization or continued government ownership might be preferable to messy compromises.

The strategic dilemma has no clean solution. SCI embodies a fundamental tension in modern capitalism: private efficiency versus public purpose. The company's journey from socialist enterprise to potential privatization mirrors India's own economic evolution. Whether SCI's future is private profit maximization or continued public service depends not on financial models but on political philosophy—what kind of capitalism does India want? The answer will determine not just SCI's fate but the template for other strategic PSUs facing similar crossroads.

X. Playbook: Lessons from SCI's Journey

Surviving six decades in shipping—an industry where 90% of companies fail within ten years—requires more than luck. SCI's longevity, despite inefficiencies and constraints, offers lessons that transcend maritime transport. The playbook isn't about operational excellence or financial engineering but about navigating the treacherous waters between political economy and market forces.

Lesson One: Diversification as Insurance, Not Strategy

SCI's sprawling portfolio across tankers, bulk carriers, containers, LNG, offshore, and passenger services violates every principle of strategic focus. Michael Porter would condemn it as "stuck in the middle." Yet this diversification enabled survival through multiple shipping crises. When tanker markets collapsed in 2003, bulk carriers compensated. When offshore struggled in 2014, LNG contracts provided stability. The key insight: in volatile industries, survival precedes optimization. SCI optimized for resilience, not returns—unfashionable but effective.

Lesson Two: Government Ownership as Both Moat and Burden

State ownership gave SCI patient capital, guaranteed cargo, and crisis support that private competitors lacked. During the 1990s Asian Financial Crisis, private shipping companies collapsed while SCI accessed government credit lines. But ownership came with obligations—unprofitable routes, social mandates, bureaucratic approvals—that destroyed economic value. The lesson: institutional ownership shapes strategy more than market forces. Understanding your owner's true objectives—political for governments, financial for private equity—determines sustainable positioning.

Lesson Three: Timing Matters More Than Terms in Privatization

SCI's privatization, announced at market peaks in 2019, stalled during COVID uncertainty and geopolitical tensions. The government prioritized revenue maximization over strategic timing. History suggests privatizing during downturns—when political resistance is lower and buyers can envision upside—works better than selling at peaks when only financial engineering can justify premiums. The UK's British Steel privatization during the 1980s recession succeeded; France's attempted sale of shipping assets during the 2007 boom failed.

Lesson Four: Building Strategic Assets vs. Commercial Operations

SCI's most valuable assets aren't its ships but its relationships, training infrastructure, and institutional knowledge. The Maritime Training Institute, operating rights on strategic routes, and security clearances for defense operations create barriers competitors cannot replicate. These strategic assets generate option value during crises even if they destroy return on capital during normal times. The playbook: separate strategic from commercial assets, fund them differently, and measure them separately.

Lesson Five: Employee Ownership Models Require Aligned Incentives

The employee consortium's bid to buy SCI represents creative financial engineering but ignores behavioral dynamics. Employee ownership works when workers can influence outcomes—in professional services, technology, or specialized manufacturing. In capital-intensive, commodity businesses like shipping where market forces dominate, employee ownership might reduce agency costs but cannot overcome structural challenges. United Airlines' ESOP failed partly because pilots couldn't control fuel prices or passenger demand.

Lesson Six: Subsidies Hidden in Plain Sight

SCI's true subsidies weren't direct government grants but indirect benefits: guaranteed cargo from PSUs, preferential port berthing, subsidized fuel during emergencies, and regulatory forbearance. These hidden subsidies, worth ₹500+ crores annually, never appeared in government budgets or company accounts. Privatization would eliminate these benefits, requiring explicit subsidies for continued public service. The lesson: make subsidies transparent before ownership changes, not after.

Lesson Seven: Managing Cyclicality Requires Counter-Cyclical Capital

Shipping cycles are violent—rates can triple in months or collapse 90% in weeks. SCI survived by accessing government capital during downturns when private credit disappeared. The company bought vessels during the 1970s oil crisis, 1990s Asian crisis, and 2009 financial crisis when distressed sellers accepted 40% discounts. Private owners rarely have such patient capital. The playbook: structure ownership to provide counter-cyclical capital, whether through sovereign wealth funds, family offices, or permanent capital vehicles.

Lesson Eight: Technology Adoption Under Constraints

Despite bureaucratic constraints, SCI adopted LNG technology early, implemented digital documentation before competitors, and pioneered Indian offshore services. Innovation happened not through R&D budgets but through joint ventures with technical partners who provided expertise while SCI provided market access. The lesson: resource constraints force creative partnerships. SCI couldn't afford to develop LNG expertise internally but could partner with Japanese operators who needed Indian market entry.

Lesson Nine: The Value of Institutional Knowledge

SCI's 15,000 employees possess collective knowledge about Indian ports, trade routes, and customer relationships accumulated over decades. This institutional knowledge—knowing which Chennai berths face congestion, which Middle East ports process documents quickly, which customers pay promptly—provides competitive advantage not replicable through hiring. Privatization risks destroying this knowledge as employees leave. The playbook: codify institutional knowledge before ownership transitions, not during.

Lesson Ten: Exit Barriers as Entry Barriers

SCI cannot exit unprofitable segments easily—union agreements, political pressure, and social obligations create exit barriers. Paradoxically, these same barriers deter competitive entry. Private operators won't enter passenger services to Andaman knowing they'd face similar exit constraints. The lesson: in regulated industries, exit barriers can be competitive advantages if managed strategically. Accept constraints on unprofitable segments to maintain exclusivity on profitable ones.

The meta-lesson from SCI's journey is that successful strategy in mixed economies requires navigating political and market forces simultaneously. Pure commercial logic fails when governments intervene; pure political logic fails when markets discipline. SCI survived by being adequately good at both rather than excellent at either—a mediocrity that proved surprisingly durable. Whether this playbook remains relevant as India liberalizes further is unclear, but for companies operating at the intersection of state and market, SCI's lessons remain instructive.

XI. The Bull & Bear Case

The Bull Case: Hidden Value in Plain Sight

Start with the mathematics that excite value investors. SCI trades at 0.8x book value while global shipping peers average 1.2x. The replacement cost of SCI's 59-vessel fleet exceeds ₹20,000 crores; the market values the entire company at ₹9,400 crores. Even accounting for the 15-year average fleet age, the discount seems excessive. Add the ₹5,000 crores in real estate transferred to SCILAL but still benefiting SCI through favorable leases, and you're essentially getting the shipping operations for free.

The strategic positioning in LNG transportation could alone justify the valuation. India's LNG imports are projected to triple by 2030, and SCI's joint ventures operate vessels on 19-year contracts until 2035, transporting LNG from Australia to China, Japan, and India. These contracts generate predictable cash flows with 12%+ IRRs. If valued separately, the LNG business might be worth ₹4,000 crores—nearly half the current market cap.

Government cargo provides an unappreciated moat. Despite liberalization, PSUs like Indian Oil, ONGC, and GAIL still prefer SCI for strategic shipments. This guaranteed baseload of ₹2,000 crores annual revenue won't disappear overnight even under private ownership. The switching costs—requalifying vendors, renegotiating contracts, managing political optics—create multi-year revenue visibility that markets aren't pricing in.

Privatization, if executed, unlocks immediate value through operational efficiency. Private ownership could reduce costs by 20% through headcount optimization, procurement improvements, and overhead reduction. On ₹5,400 crores revenue, that's ₹1,000 crores in additional profit—doubling current earnings. The stock could re-rate from 10x to 15x P/E simply on credible privatization execution, implying 150% upside.

India's trade growth provides secular tailwinds. Merchandise trade is projected to reach $2 trillion by 2030 from $850 billion today. Even maintaining current market share, SCI's revenues would double. With focused execution under private ownership, market share gains seem plausible. The company's Indian flag, relationships, and port knowledge provide advantages foreign operators cannot replicate.

The net foreign exchange earner status matters in a country perpetually concerned about current account deficits. SCI generates $400 million annually in net forex earnings—money that stays in India rather than flowing to foreign shipowners. Any government, regardless of political ideology, values forex earners. This strategic importance provides downside protection even if privatization fails.

The Bear Case: Structural Decline Masked by Financial Engineering

Begin with the damning growth statistics. Five-year revenue CAGR of 4.84% during a period when nominal GDP grew 10% and trade grew 7% indicates market share losses. This isn't cyclical underperformance but structural decline. SCI is slowly bleeding relevance while investors focus on asset values rather than competitive position.

The ROE of 10.8% looks acceptable until you realize it's inflated by subsidized contracts and tax benefits. Normalize for market rates and tax rates, and ROE drops to 7-8%—below cost of capital. SCI is destroying economic value while reporting accounting profits. No amount of financial engineering changes this fundamental reality.

Global shipping overcapacity presents an existential threat. The order book for new vessels equals 11% of existing global fleet. Chinese shipyards, subsidized by state banks, continue building despite oversupply. Freight rates might remain depressed for years. SCI, with its old fleet and high operating costs, cannot compete against newer, larger, more efficient vessels operated by global giants.

Competition from efficient private players is intensifying. Adani Ports is building logistics capabilities. Reliance might enter shipping to support its energy business. These deep-pocketed Indian conglomerates can access capital, technology, and talent that SCI cannot match. The company's market share, already declining, could halve within five years.

Disinvestment uncertainty destroys value daily. Management cannot make long-term decisions not knowing future ownership. Talented employees leave for stable opportunities. Customers hesitate signing multi-year contracts. Suppliers demand unfavorable terms. The limbo between PSU and private ownership creates operational paralysis worse than either alternative.

Legacy costs and inefficiencies run deeper than acknowledged. The average employee cost at SCI is 40% higher than private peers—not just in salaries but in benefits, pensions, and social overhead. Union agreements make restructuring nearly impossible. Even under private ownership, these legacy costs might persist for years, destroying returns.

The fleet age problem compounds annually. With average vessel age of 15 years versus 10 for competitors, SCI faces higher maintenance costs, lower fuel efficiency, and reduced customer appeal. Fleet renewal requires ₹10,000 crores—more than the current market cap. Without massive capital injection, the fleet becomes progressively uncompetitive.

Technology disruption threatens traditional shipping models. Autonomous vessels, blockchain documentation, and AI-optimized routing favor large, technology-forward operators. SCI lacks the scale for meaningful technology investment and the culture for rapid innovation. It risks becoming the Hindustan Ambassador of shipping—nostalgic but irrelevant.

Environmental regulations present existential challenges. IMO 2020 sulfur regulations, ballast water treatment requirements, and carbon reduction mandates require massive capital investment. Older vessels like SCI's become economically unviable as retrofit costs approach newbuild prices. The company faces a devil's choice: massive capital expenditure or accelerated obsolescence.

The Verdict: A Value Trap or Hidden Gem?

The bull-bear debate ultimately reduces to timeframe and ownership assumptions. Bulls betting on quick privatization and operational turnaround might see 100%+ returns within two years. Bears focused on structural challenges and execution risks see gradual value erosion regardless of ownership.

The truth likely lies between extremes. SCI is neither hidden gem nor value trap but a complex option on India's privatization agenda, trade growth, and shipping markets. For risk-seeking investors with patience, the asymmetry seems favorable—limited downside given asset values, substantial upside if privatization succeeds. For conservative investors seeking steady returns, better opportunities exist elsewhere.

The investment decision depends on your view of three critical questions: Will privatization actually happen? Can private owners restructure operations while managing political pressures? Will India's trade growth offset global shipping oversupply? Answer all three positively, and SCI is screaming buy. Answer any negatively, and it's avoid at all costs. The market's confusion—reflected in high volatility and wide analyst target ranges—suggests nobody knows the answers. In that uncertainty lies either opportunity or danger, depending on your risk appetite and conviction.

XII. Power & "What If We Were in Charge?"

If we took control of SCI tomorrow morning, the first 100 days would be ruthless prioritization. Not the financial engineering that excites investment bankers or the grand strategy that fills consulting decks, but the mundane operational decisions that determine whether ships float or sink—literally and metaphorically.

Day 1-30: The Portfolio Decision

The immediate decision: which businesses to keep, sell, or shut. The tanker and LNG operations are obvious keepers—profitable, scalable, strategically important. The single container vessel is an obvious exit—subscale operations in a network business make no sense. But the difficult decisions lie in between. The bulk carriers generating 9% ROCE barely cover capital costs but provide portfolio stability. The offshore vessels are profitable but require specialized expertise SCI struggles to maintain. The passenger operations lose money but carry immense political weight.

Our framework would be simple: keep businesses where SCI has legitimate competitive advantage or strategic obligation, exit everything else. This means retaining tankers (Indian crude demand provides natural advantage), LNG (long-term contracts provide stability), and selective offshore vessels (ONGC relationship is valuable). Exit containers (no network effects), bulk carriers (pure commodity business), and find creative solutions for passenger services—perhaps a subsidiary with explicit government subsidies rather than hidden cross-subsidization.

Day 31-60: The Capital Structure Revolution

SCI's conservative balance sheet—debt-to-equity of 0.6x versus industry norms of 2-3x—reflects PSU risk aversion rather than optimal capital structure. With stable cash flows from long-term contracts, SCI could easily support 1.5x leverage, releasing ₹5,000 crores for fleet modernization without diluting equity. The key is structuring debt intelligently—project finance for vessels, working capital lines for operations, and sale-leasebacks for non-strategic assets.

More radically, we'd explore tonnage tax regimes available in Singapore or Dubai that could reduce effective tax rates from 25% to 5%. This isn't tax evasion but legitimate optimization that every global shipping company employs. The ₹200 crores annual savings would fund technology investment or fleet renewal. Indian registration provides no operational advantage while imposing significant tax disadvantage.

Day 61-90: The Talent Revolution

SCI's human capital is simultaneously its greatest asset and largest liability. The maritime expertise is world-class; the organizational culture is decades outdated. We'd implement a three-pronged approach: voluntary retirement for underperformers with generous packages (expensive short-term but essential long-term), aggressive hiring from global shipping companies at market rates (breaking PSU pay scales), and performance-based compensation linking employee rewards to ROCE, not just revenue.

The controversial move: hiring foreign executives for critical roles. SCI needs a Chief Digital Officer who's implemented autonomous vessel programs, a Fleet Manager who's optimized global operations, and a Commercial Head who understands derivative markets. National pride is important, but operational excellence matters more. Singapore's NOL and Malaysia's MISC succeeded by importing global talent; India's shipping champion should too.

Day 91-100: The Technology Transformation

SCI operates like it's 1995—paper documents, phone negotiations, manual routing. We'd immediately implement three technology initiatives that generate immediate ROI. First, dynamic routing optimization using AI to reduce fuel consumption by 10%—saving ₹200 crores annually on current bunker costs. Second, predictive maintenance using IoT sensors to reduce dry-docking time by 20%—adding 30 operational days per vessel annually. Third, blockchain documentation for trade finance, reducing working capital needs by ₹300 crores.

The Strategic Separation

The fundamental restructuring would separate SCI into two entities: CommercialCo and StrategicCo. CommercialCo would own profit-maximizing assets—tankers, LNG vessels, select offshore units—and operate on pure commercial terms. It would list separately, access private capital, and compete globally. StrategicCo would own public service assets—passenger vessels, defense support ships, emergency response capability—funded by explicit government contracts at cost-plus pricing.

This separation clarifies objectives, enables appropriate financing, and ends the cross-subsidization that destroys value. CommercialCo might achieve 20% ROCE and trade at premium valuations. StrategicCo would break even but fulfill social obligations transparently. The combined value exceeds the current confused entity where neither objective is achieved properly.

The Fleet Modernization Program