State Bank of India: The Story of India's Financial Colossus

I. Introduction & Episode Roadmap

In the pantheon of global banking giants, few institutions carry the weight of history quite like the State Bank of India. With 23% market share by assets and nearly 250,000 employees spread across the subcontinent and beyond, SBI isn't just a bank—it's the financial backbone of the world's most populous nation. Ranked as the 47th largest bank globally by total assets and securing the 178th position in the Fortune Global 500, this behemoth processes the financial dreams and daily transactions of nearly half a billion customers.

But here's what makes the SBI story truly remarkable: this modern colossus traces its roots back to 1806, when the Bank of Calcutta opened its doors in British-controlled Bengal. How does a colonial-era presidency bank, designed to serve the East India Company's commercial interests, transform into the primary vehicle for India's financial inclusion and economic development? How does an institution navigate two centuries of upheaval—from colonial rule through independence, partition, socialist planning, economic liberalization, and now digital disruption?

The answer lies in understanding SBI not just as a bank, but as a mirror reflecting India's own journey from colony to emerging superpower. It's a story of constant reinvention, where imperial banking practices gave way to nation-building imperatives, where rural credit missions evolved into digital super-apps, and where the tension between commercial success and social responsibility has shaped every strategic decision.

This episode will take us from the bustling trading floors of 19th-century Calcutta to the algorithms powering YONO's AI-driven lending decisions. We'll explore how SBI became too big to fail, why the government still owns majority stake in an era of privatization, and what it means to be both a commercial entity competing with nimble private banks and a national institution tasked with financial inclusion.

The key themes we'll track throughout this journey: the delicate dance between government control and market forces, the challenge of serving both rural farmers and urban corporations, the massive technological transformations required to stay relevant, and ultimately, how scale itself becomes both SBI's greatest asset and most complex challenge.

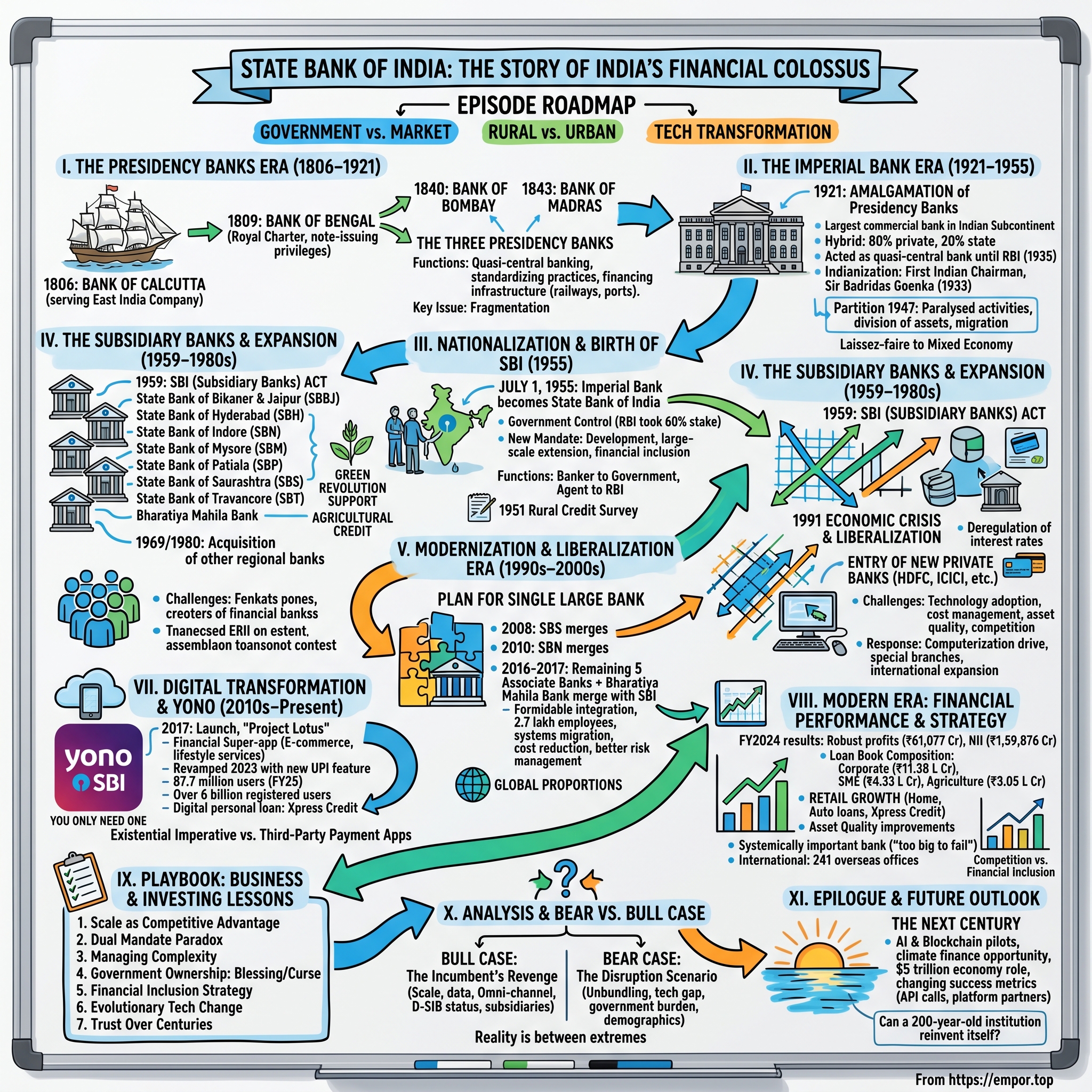

II. Origins: The Presidency Banks Era (1806–1921)

The morning of June 2, 1806, marked a watershed moment in Indian financial history. In the humid, bustling streets of colonial Calcutta, where British merchants haggled with Bengali traders and the East India Company's ships crowded the Hooghly River, the Bank of Calcutta opened its doors, establishing what would become the earliest progenitor of the State Bank of India. This wasn't just another colonial enterprise—it was the foundation stone of modern banking in the subcontinent, a system that would outlive the British Raj itself.

The Bank of Calcutta was launched as a regional bank with the East India Company, European merchants, and wealthy Indians among its founders, primarily to meet the Company's need for funds for its wars against rulers like Tipu Sultan. Three years later, in 1809, the institution underwent its first transformation. The bank was given a royal charter and renamed the Bank of Bengal, signaling its elevated status and expanded mandate. The Government of India invested around 20% of the capital and was given authority to nominate three directors to the board—establishing a pattern of government involvement that would define Indian banking for centuries.

The real innovation of these early presidency banks lay in their quasi-central banking functions. The Bank of Bengal was given the right to issue its own currency notes, with one of the oldest surviving bank notes in India being a Bank of Bengal note issued in 1812. This power to create money was extraordinary—these weren't just deposit-taking institutions but creators of the very medium of exchange that lubricated colonial commerce.

The Bengal model proved so successful that the colonial administration replicated it across their other major commercial centers. The Bank of Bombay was incorporated on April 15, 1840, followed by the Bank of Madras on July 1, 1843. Together, these three institutions became known as the presidency banks, each serving as the financial backbone of their respective regions. The Bank of Bengal, also known as the Presidency bank of Bengal, had one-fifth of its capital contributed by the state and the remainder by the East India Company.

What made these banks unique wasn't just their government backing but their hybrid nature. They were commercial enterprises with public responsibilities, profit-seeking ventures with nation-building (or rather, empire-building) obligations. While mainly managed by English agency houses conducting ordinary banking business as joint stock companies with unlimited liability, there was gross mismanagement and wide speculation, making these banks vulnerable to panic and defalcations.

The presidency banks operated in a peculiar regulatory environment. All three banks issued currency notes until this privilege was revoked by the Paper Currency Act of 1861, when the function was transferred to the Government. This loss of note-issuing privileges marked a crucial turning point—the banks had to reinvent themselves as pure commercial entities rather than quasi-monetary authorities.

The geographical reach of these banks reflected the contours of British commercial interests. The Bank of Bengal served the jute mills and indigo plantations of eastern India, financing the trade that flowed through Calcutta's port. The Bank of Bombay became the financial engine of western India's cotton trade, while the Bank of Madras supported the commercial agriculture and emerging industries of the south. Each developed distinct banking cultures and practices that would persist long after their amalgamation.

These institutions also pioneered many banking innovations in India. They introduced the concept of limited liability (eventually), standardized banking practices, and created the first inter-regional payment systems. They financed railways, ports, and telegraphs—the infrastructure that knitted together the subcontinent into a single economic unit. Their lending practices, risk assessment methods, and organizational structures became the template for Indian banking.

Yet beneath this story of institutional innovation lay deeper tensions. These banks served primarily European commercial interests and the colonial administration. Indian merchants and industrialists often found themselves excluded from credit or charged prohibitive rates. The banks' boards were dominated by Europeans, their policies crafted in London as much as in India. This created a dual financial system—formal banking for the colonial economy and traditional indigenous banking (through shroffs and sahukars) for most Indians.

The presidency banks also reflected the administrative peculiarities of British India. British India was divided into three Presidencies—Bengal, Bombay, and Madras—each with significant autonomy. The banks mirrored this structure, operating as independent entities with little coordination. This fragmentation would eventually become a liability as India's economy grew more integrated.

By the early 20th century, the limitations of this three-bank system were becoming apparent. The rise of Indian nationalism, the growth of indigenous industry, and the increasing complexity of India's economy demanded a more unified banking structure. The presidency banks, for all their success, were creatures of the 19th century—designed for a colonial economy based on raw material extraction and limited industrialization. India's emerging 20th-century economy needed something more ambitious, more integrated, and ultimately, more Indian. The stage was set for the next great transformation: the creation of the Imperial Bank of India.

III. The Imperial Bank Era (1921–1955)

On January 27, 1921, a momentous transformation reshaped India's financial landscape. The three presidency banks amalgamated to form the Imperial Bank of India on 27 January 1921, creating what would become the largest commercial bank in the Indian subcontinent. This wasn't merely a merger—it was the birth of India's first truly national banking institution, one that would serve as both a commercial bank and a quasi-central bank until independence.

The decision was certainly influenced by the 1912 book "Indian Currency and Finance" authored by John Maynard Keynes, who had served in the India Office and understood the inefficiencies of the fragmented presidency bank system. The global context mattered too—World War I had demonstrated the need for more coordinated financial institutions, and the rise of nationalist sentiment demanded Indian institutions that could compete with foreign exchange banks.

The Imperial Bank was 80% privately owned while the rest were owned by the state, maintaining the public-private hybrid model that had characterized the presidency banks. The First Governor of The Imperial Bank was Rajah Sir Annamalai Chettiar, a choice that signaled at least token Indian representation in leadership, though Europeans continued to dominate the board and management.

The Imperial Bank inherited an impressive foundation from its predecessors. When India attained freedom, the Imperial Bank had a capital base (including reserves) of Rs.11.85 crores, deposits and advances of Rs.275.14 crores and Rs.72.94 crores respectively and a network of 172 branches and more than 200 sub offices. But these numbers only tell part of the story. The bank had to navigate the tumultuous decades between its formation and independence—including the Great Depression, World War II, and the growing independence movement.

Initially, as per its royal charter, it acted as the central bank for India prior to the formation of the Reserve Bank of India (RBI) in 1935. This dual role was both a blessing and a curse. The bank managed government accounts, held currency chests, and acted as banker to other banks—functions that gave it enormous influence but also constrained its commercial activities. It was prohibited from foreign exchange business, limiting its ability to compete with exchange banks that dominated international trade finance.

The establishment of the Reserve Bank of India in 1935 marked a crucial transition. The establishment of the Reserve Bank of India as the central bank of the country in 1935 ended the quasi-central banking role of the Imperial Bank. The latter ceased to be bankers to the Government of India and instead became agent of the Reserve Bank for the transaction of government business at centres at which the central bank was not established. This transformation freed the Imperial Bank to focus on commercial banking, but it also meant losing some of its special privileges and guaranteed government business.

In 1933, Sir Badridas Goenka, an important public figure and business tycoon of his time, and a prominent member of Marwari community of Calcutta, became the first Indian to be appointed as the Chairman of the Imperial Bank of India. This appointment was symbolic of the gradual Indianization of the bank's leadership, though real power remained largely in European hands until independence.

The Imperial Bank played a crucial role during World War II, financing war efforts and managing the complex financial flows of a wartime economy. But the real test came with partition in 1947. The partition of India in 1947 adversely impacted the economies of Punjab and West Bengal, paralysing banking activities for months. The bank had to deal with the division of assets and liabilities, the migration of staff, and the complete disruption of established banking networks in the affected regions.

The partition created unprecedented challenges. Branches that had served integrated markets suddenly found themselves on opposite sides of an international border. Muslim staff members migrated to Pakistan, while Hindu and Sikh employees moved to India, disrupting operations and destroying decades of institutional knowledge. The Imperial Bank had to write off substantial loans in areas that became Pakistan, while simultaneously dealing with the massive financing needs of refugees resettling in India.

Yet the Imperial Bank demonstrated remarkable resilience. The Imperial Bank during the three and a half decades of its existence recorded an impressive growth in terms of offices, reserves, deposits, investments and advances, the increases in some cases amounting to more than six-fold. The financial status and security inherited from its forerunners no doubt provided a firm and durable platform. But the lofty traditions of banking which the Imperial Bank consistently maintained and the high standard of integrity it observed in its operations inspired confidence in its depositors that no other bank in India could perhaps then equal.

The bank's role in financing India's early industrialization cannot be overstated. It provided crucial credit to emerging Indian businesses, funded infrastructure projects, and facilitated the growth of indigenous industry. While it continued to serve British commercial interests, it increasingly became an institution that Indian businesses relied upon. This duality—serving both colonial and indigenous interests—would define its character right up to independence.

India's independence marked the end of a regime of the Laissez-faire for the Indian banking. The Government of India initiated measures to play an active role in the economic life of the nation, and the Industrial Policy Resolution adopted by the government in 1948 envisaged a mixed economy. In this new vision, the Imperial Bank, with its extensive network and established reputation, would need to transform yet again—from a colonial institution to an instrument of national development.

By the early 1950s, it was clear that independent India needed a different kind of banking system. The First Five Year Plan, launched in 1951, emphasized rural development and agricultural credit—areas where the Imperial Bank, despite its size, had limited presence. At the time when India got independence, all the major banks of the country were led privately which was a cause of concern as the people belonging to rural areas were still dependent on money lenders for financial assistance. The stage was set for the most dramatic transformation yet: the nationalization of the Imperial Bank and its rebirth as the State Bank of India.

IV. Nationalization & Birth of SBI (1955)

The morning of July 1, 1955, marked the most significant transformation in Indian banking history. On 1 July 1955, the Imperial Bank of India became the State Bank of India. The Government of India took control of the Imperial Bank of India in 1955, with Reserve Bank of India (India's central bank) taking a 60% stake, renaming it State Bank of India. This wasn't just a change of ownership—it was the birth of a new kind of bank, one designed to serve not colonial interests but national development imperatives.

The decision to nationalize the Imperial Bank emerged from a growing recognition that India's banking system was fundamentally misaligned with the country's development needs. The All India Rural Credit Survey Committee, established in 1951 and reporting in 1954, had delivered a damning verdict on the state of rural credit in India. The committee found that institutional credit accounted for barely 7% of rural borrowing—the rest came from moneylenders charging usurious rates. The Imperial Bank, despite being the country's largest bank, had virtually no presence in rural areas where 80% of Indians lived.

During his time at the Reserve Bank of India, he played a key role in the drive towards the nationalization of the Imperial Bank of India, as a result of which the State Bank of India was formed. The political context was equally important. Prime Minister Jawaharlal Nehru's government was committed to a socialist pattern of society, with the state playing a commanding role in economic development. The First Five Year Plan, launched in 1951, had prioritized agriculture and rural development, but lacked the financial infrastructure to deliver credit where it was needed most.

Pursuant to the provisions of the State Bank of India Act of 1955, the Reserve Bank of India, on 1 July 1955, acquired a controlling interest in the Imperial Bank of India and it became the State Bank of India. The State Bank of India Act, passed by Parliament in May 1955, was a carefully crafted piece of legislation that balanced multiple objectives. It preserved the commercial viability of the bank while mandating a developmental role, maintained professional management while ensuring government control, and protected existing shareholders while bringing the institution under public ownership.

The transformation was immediate and dramatic. On that day, the bank had 480 branches and sub-offices, as well as three local head offices; slightly more than a quarter of the resources of the Indian banking industry was under its control and command. But numbers alone don't capture the fundamental shift in mission. The new State Bank of India was given an explicit mandate to extend banking facilities on a large scale, particularly in rural and semi-urban areas, and to support agricultural development and small-scale industries.

The ownership structure itself was innovative. While the RBI took a 60% controlling stake, 40% remained with private shareholders, creating a unique public-private hybrid. This arrangement was designed to maintain commercial discipline while pursuing social objectives—a balance that would define SBI's character for decades to come. The government guaranteed the bank's obligations, giving it unmatched credibility, while professional management ensured operational efficiency.

The immediate challenges were enormous. The bank had to rapidly expand into rural areas with no existing infrastructure, train staff for agricultural lending despite no prior experience, and develop new products for customers who had never used formal banking. Within the first year, SBI opened hundreds of new branches in previously unbanked areas, recruited thousands of new employees, and began the massive task of financial inclusion that continues to this day.

Section 32 states that the State Bank shall act as agent of the RBI at all places in India where RBI does not have a branch of its banking department. Under this role, SBI plays following functions: Banker to the Government The SBI functions as the banker to the central and state governments i.e., it collects money and makes payments on behalf of the government and manages public debt. It collects charges (taxes and other payments) on behalf of the government and grants loans and advances to it. This agency relationship gave SBI a unique position in India's financial system—it was simultaneously a commercial bank competing in the market and a quasi-governmental institution performing public functions.

The nationalization also had profound symbolic significance. For the first time, India had a truly national bank—not a colonial institution adapted for independence, but one explicitly created to serve national objectives. The State Bank of India became a symbol of economic sovereignty, demonstrating that India could create and manage world-class financial institutions on its own terms.

The international dimension was equally important. Foreign banks, which had dominated trade finance and international banking, suddenly faced competition from a government-backed institution with unmatched domestic reach. SBI could leverage its massive deposit base to enter international markets, supporting Indian businesses abroad and facilitating the country's integration into the global economy.

In 2008, the Government of India acquired the Reserve Bank of India's stake in SBI to remove any conflict of interest because the RBI is the country's banking regulatory authority. This later adjustment highlighted the ongoing evolution of SBI's governance structure, as India's financial system matured and regulatory frameworks became more sophisticated.

The creation of SBI also set a precedent for further nationalization. If the Imperial Bank could be successfully transformed into a development-oriented institution, why not other banks? This logic would lead to the massive bank nationalization of 1969, but SBI remained unique—larger, more influential, and more closely tied to government policy than any other financial institution.

The human dimension of this transformation deserves attention. Thousands of Imperial Bank employees suddenly found themselves working for a very different organization, with new objectives and expectations. Many embraced the developmental mission enthusiastically, seeing themselves as nation-builders rather than mere bankers. This cultural shift—from colonial service to national service—would prove as important as any structural change.

By establishing SBI, India had created more than just a bank. It had established an institution that would become central to every major economic initiative for the next seven decades—from the Green Revolution to industrial development, from financial inclusion to digital payments. The State Bank of India was born not just to provide banking services, but to be an instrument of economic transformation, a role it continues to play as India pursues its ambition of becoming a developed nation by 2047.

V. The Subsidiary Banks & Expansion (1959–1980s)

In 1959, just four years after SBI's creation, the government embarked on an even more ambitious expansion. In 1959, the government passed the State Bank of India (Subsidiary Banks) Act. This made eight banks that had belonged to princely states into subsidiaries of SBI. This was during the First Five-Year Plan, which prioritised the development of rural India. The act represented a masterful piece of financial engineering—absorbing established regional banks with deep local roots while maintaining their distinct identities and customer relationships.

The eight banks transformed into SBI subsidiaries had fascinating histories of their own. These seven banks were State Bank of Bikaner and Jaipur (SBBJ), State Bank of Hyderabad (SBH), State Bank of Indore (SBN), State Bank of Mysore (SBM), State Bank of Patiala (SBP), State Bank of Saurashtra (SBS) and State Bank of Travancore (SBT). Each had been established by princely states before independence, serving as quasi-central banks for their respective regions. Bhavnagar, Rajkot, and Jamnagar, which were among the larger states, and two smaller states, Palitana and Vadia, had established their own Darbar (meaning Palace) Banks, the oldest of which was Bhavnagar Darbar Bank, established in 1902. These banks mainly catered to the needs of the governments of their respective princely states, and acted as depositories for local savings.

The State Bank of Hyderabad exemplified this transformation. It was established on 8 August 1941 under the Hyderabad State Bank Act, during the reign of the last Nizam of Hyderabad, Mir Osman Ali Khan. In 1956, under The State Bank Of Hyderabad Act, 1956 share capital of the Hyderabad State Bank was transferred to the Reserve Bank of India. The Reserve Bank of India took over the bank as its first subsidiary and it was renamed as State Bank of Hyderabad. The Subsidiary Banks Act was passed in 1959. On 1 October 1959, SBH and the other banks of the princely states became subsidiaries of SBI.

The ownership structure of these subsidiary banks was carefully designed. Provision is being made for minority shareholding by private shareholders up to 45 per cent. of the issued capital in the case of each of the reconstituted banks. This allowed for local participation while ensuring SBI's control. All these banks were given the same logo as the parent bank, SBI. The visual unity symbolized their integration into a national system while maintaining operational autonomy.

The subsidiary bank model proved brilliantly successful in achieving the government's rural development objectives. This established SBI subsidiary of 8 financial institutions that had formerly pertained to imperial powers earlier to their nationalization and effective control from September 1959 to October 1960. To increase its rural outreach, the government amalgamated these institutions into the SBI system. Within a decade, these banks had extended banking services to thousands of previously unbanked villages, providing agricultural credit, supporting small industries, and mobilizing rural savings.

SBI's expansion wasn't limited to absorbing princely state banks. The bank also rescued failing institutions, protecting depositors and maintaining financial stability. The first was the Bank of Bihar (est. 1911), which SBI acquired in 1969, together with its 28 branches. The next year, SBI acquired the National Bank of Lahore (est. 1942), which had 24 branches. These acquisitions demonstrated SBI's role as the system's stabilizer—the institution that would step in when others failed.

Five years later, in 1975, SBI acquired Krishnaram Baldeo Bank, which had been established in 1916 in Gwalior State, under the patronage of Maharaja Madho Rao Scindia. The bank had been the Dukan Pichadi, a small moneylender, owned by the Maharaja. The new bank's first manager was Jall N. Broacha, a Parsi. This acquisition showed how SBI absorbed even small regional institutions, preserving local banking relationships while bringing them into the formal system.

The 1969 bank nationalization wave further transformed India's banking landscape. In 1969, the Government of India nationalised 14 major private banks; one of the big banks was Bank of India. The next major government intervention in banking took place on 19 July 1969 when the Indira government nationalised an additional 14 major banks. The total deposits in the banks nationalised in 1969 amounted to 50 crores. While SBI wasn't directly affected, this massive expansion of public sector banking created both competition and collaboration opportunities.

The international dimension of SBI's expansion deserves special attention. In 1982, the bank established a subsidiary, State Bank of India (California). It has ten branches—nine branches in the state of California and one in Washington, D.C., as of 28 March 2011. This marked SBI's serious entry into global banking, serving the Indian diaspora and facilitating international trade. The California subsidiary targeted the growing Indian-American community, particularly in Silicon Valley, providing a bridge between India's emerging tech sector and global markets.

In 1985, SBI acquired the Bank of Cochin in Kerala, which had 120 branches. SBI was the acquirer as its affiliate, the State Bank of Travancore, already had an extensive network in Kerala. This acquisition showcased SBI's strategic approach—leveraging existing subsidiary strengths to consolidate regional dominance.

Throughout the 1970s and 1980s, SBI pioneered numerous banking innovations. It introduced agricultural lending at scale, created specialized branches for small-scale industries, and developed new savings products for rural customers. The bank's vast network became the government's primary channel for implementing economic policies—from distributing subsidies to collecting taxes.

The subsidiary banks played a crucial role in India's Green Revolution. They provided crop loans, financed tube wells and tractors, and created rural godowns for storing agricultural produce. In states like Punjab and Haryana, State Bank of Patiala became synonymous with agricultural prosperity. In the south, State Bank of Travancore and State Bank of Mysore supported the spread of cash crops and small-scale industries.

By the late 1980s, the SBI group had become a colossus. With the parent bank and seven subsidiaries operating semi-autonomously, it controlled nearly 30% of India's banking assets. The network exceeded 10,000 branches, reaching into the remotest corners of the country. But this massive expansion came with challenges. Coordination between the parent and subsidiaries was complex. Different banks had different cultures, systems, and practices. Rural lending, while socially important, often yielded low returns and high non-performing assets.

The subsidiary bank structure also created inefficiencies. Each bank maintained separate treasury operations, technology systems, and administrative structures. Customers couldn't seamlessly transact across different SBI group banks. As India moved toward economic liberalization in the 1990s, these inefficiencies would become increasingly problematic. The stage was set for the next phase of SBI's evolution—modernization and eventual consolidation.

VI. Modernization & Liberalization Era (1990s–2000s)

The July 1991 economic crisis marked a watershed moment not just for India's economy but particularly for SBI. The liberalisation process was prompted by a balance of payments crisis that had led to a severe recession, dissolution of the Soviet Union leaving the United States as the sole superpower, and the sharp rise in oil prices caused by the Gulf War of 1990–91. India's foreign exchange reserves fell to dangerously low levels, covering less than three weeks of imports. The country had to airlift gold to secure emergency loans. This crisis forced a fundamental rethinking of India's economic model—and with it, the role of its largest bank.

Since nationalisation of banks in 1969, the banking sector had been dominated by the public sector. There was financial repression, role of technology was limited, no risk management etc. This resulted in low profitability and poor asset quality. SBI, as the sector's leader, epitomized both the strengths and weaknesses of this system. While it had unmatched reach and government backing, it also suffered from bureaucratic inefficiencies, political interference in lending decisions, and outdated technology.

In august 1991, the Government appointed a committee on financial system under the chairmanship of M. Narasimhan. The Narasimham Committee's recommendations would reshape Indian banking. Recommendations included reducing the statutory liquidity ratio (SLR) and cash reserve ratio (CRR) from 38.5% and 15% respectively to 25% and 10% respectively, allowing market forces to dictate interest rates instead of the government, placing banks under the sole control of the RBI, and reducing the number of public sector banks.

For SBI, these reforms meant fundamental changes. Interest rate deregulation ended decades of administered pricing. Since 1992, interest rate has become much simpler and freer. a) Scheduled Commercial banks have now the freedom to set interest rates on their deposits subject to minimum floor rates and maximum ceiling rates. b) Interest rate on domestic term deposits has been decontrolled. Suddenly, SBI had to compete on price—something it had never done before.

The most dramatic change was the entry of new private sector banks. These came to be known as New Generation tech-savvy banks, and included Global Trust Bank (the first of such new generation banks to be set up), which later amalgamated with Oriental Bank of Commerce, IndusInd Bank, UTI Bank (since renamed Axis Bank), ICICI Bank and HDFC Bank. These banks started with no legacy issues, modern technology, and aggressive growth strategies. They targeted SBI's most profitable customers—urban professionals and corporations—with superior service and innovative products.

New private sector banks have already started functioning. These new private sector banks are allowed to raise capital contribution from foreign institutional investors up to 20% and from NRIs up to 40%. This has led to increased competition. HDFC Bank and ICICI Bank, in particular, emerged as formidable competitors, growing rapidly through technology adoption and customer service excellence.

SBI's response to this competition was initially sluggish. The bank's massive size and government ownership made rapid transformation difficult. Decision-making was slow, union resistance to change was strong, and the social banking mandate limited commercial flexibility. While private banks cherry-picked profitable urban customers, SBI continued to maintain expensive rural branches and make directed loans to priority sectors.

Technology adoption became the defining battleground. Private banks introduced ATMs, phone banking, and later internet banking years before SBI could respond at scale. Major changes in the banking system and management have been seen over the years with the advancement in technology, considering the needs of people. SBI's legacy systems, some dating back decades, couldn't easily integrate new technologies. The bank operated on multiple core banking platforms across its subsidiaries, making unified operations impossible.

Yet SBI had unique strengths that became apparent as the decade progressed. Its unmatched branch network gave it access to low-cost deposits that private banks couldn't match. Government backing provided stability during economic turbulence. Most importantly, its brand commanded trust among millions of Indians who remained skeptical of new private banks.

The late 1990s saw SBI begin its transformation in earnest. The bank embarked on a massive computerization drive, though progress was slow and uneven. It introduced new products targeting urban markets while maintaining its rural presence. Training programs attempted to change the bureaucratic culture, with mixed success. The bank also began closing or merging unprofitable branches, though political pressure limited restructuring.

Capital became increasingly important as Basel norms required higher adequacy ratios. The Banking Companies (Acquisition and Transfer of Undertakings) Act was amended to enable the banks to raise capital through public issues. This is subject to provision that the holding of Central Government would not fall below 51% of paid-up-capital. SBI has already raised substantial amount of funds through equity and bonds. SBI's ability to tap capital markets while maintaining government majority ownership provided crucial growth funding.

International expansion accelerated during this period. SBI recognized that Indian businesses were globalizing and needed banking support abroad. The bank expanded its foreign presence, establishing subsidiaries and branches in key markets. This international network would become crucial as Indian IT companies emerged as global players in the 2000s.

Liberalization measures have allowed banking to be much more dynamic, promoting capital mobility. These reforms have collectively made the market much more competitive improving overall banking efficiency as leading public sector banks have had to greatly improve to stay relevant in an age of aggressive private banking. By 2000, SBI had begun to show signs of successful adaptation, though the transformation was far from complete.

The pension and wage bill remained a massive burden. SBI employees enjoyed government-style job security and benefits that private banks didn't offer. This made the bank's cost-to-income ratio significantly higher than competitors. Voluntary retirement schemes were introduced but had limited impact given the attractiveness of government employment.

Asset quality emerged as another major challenge. The Indian banking sector still suffers from high rates of non-recovery and private sector banks are much quicker to write off bad loans to put up a cleaner balance sheet. Decades of directed lending had created large non-performing asset portfolios. Political pressure made recovery difficult, especially from influential defaulters.

In 2008, the Government of India acquired the Reserve Bank of India's stake in SBI to remove any conflict of interest because the RBI is the country's banking regulatory authority. This governance change reflected the maturation of India's regulatory framework and SBI's evolving role within it.

By the end of the 2000s, SBI had survived the initial shock of liberalization and begun to thrive in the new environment. It remained India's largest bank by a wide margin, though its market share had declined from the monopolistic levels of the pre-reform era. The bank had modernized significantly but still lagged private competitors in technology and service quality. Most importantly, it had learned to balance commercial objectives with its continuing social mandate—a juggling act that would define its character in the 21st century. The stage was set for the next phase: consolidation of the subsidiary banks and a push for global scale.

VII. The Great Consolidation (2008–2017)

The year 2008 marked the beginning of SBI's most ambitious transformation. The plans for making SBI a single very large bank by merging all associate banks started in 2008, when SBS merged with SBI. This wasn't just administrative consolidation—it was a strategic response to a rapidly changing global and domestic banking landscape. The 2008 financial crisis had demonstrated the importance of scale in weathering economic storms, while domestic competition from private banks was intensifying.

The merger strategy unfolded in phases. State Bank of Saurashtra was the first to merge with SBI in 2008, followed by State Bank of Indore in 2010. These initial mergers served as test cases, allowing SBI to refine its integration processes before attempting the massive consolidation that would follow. From these experiences, SBI learned crucial lessons about systems integration, cultural alignment, and customer transition that would prove invaluable later.

The rationale for consolidation was compelling. The subsidiary structure, while serving India well during the expansion phase, had become increasingly inefficient in the 21st century. Each bank maintained separate treasuries, technology platforms, and administrative structures. Customers couldn't seamlessly transact across different SBI group banks. The cost duplications were enormous—seven CEOs, seven boards, seven IT systems, all essentially doing the same thing.

By 2016, the political and economic environment was ripe for bold action. Prime Minister Narendra Modi's government was pushing for banking sector reforms, and SBI's leadership, under Chairwoman Arundhati Bhattacharya, was ready to execute. In 2016, the board of SBI and the Union Cabinet cleared the proposal to merge the remaining five associate banks (State Bank of Bikaner and Jaipur, State Bank of Hyderabad, State Bank of Mysore, State Bank of Patiala, and State Bank of Travancore) and SBI's fully owned subsidiary Bharatiya Mahila Bank with SBI.

The scale of this merger was unprecedented in Indian banking history. The five associate banks for instance have stressed loans (gross NPAs and restructured loans) at a staggering Rs 35,396 crore level. This amount is almost half of SBI's Rs 66,117 crore stressed loans in 2015-16. The merged entity would have combined assets of over Rs 6 lakh crore, which is almost equal to the size of the two largest private banks HDFC Bank and ICICI Bank Ltd.

The integration challenges were formidable. The PSBs, excluding SBI, are an entirely different animal. They have different IT platforms, work cultures, brands, business focus, policies, geographical presence and treasury operations. Each subsidiary had developed its own culture over decades. State Bank of Travancore, for instance, had deep roots in Kerala's unique socio-economic environment. State Bank of Hyderabad had been the Nizam's bank, with a distinct identity in the Deccan region.

The human dimension was particularly complex. The merged SBI entity would have 24,000 plus branches, 58,000 ATMs and 2.7 lakh employees. Managing this integration without disrupting customer service or demoralizing staff required careful planning. The associate banks have also offered a Voluntary Retirement Scheme (VRS) to employees who do not wish to relocate. Cultural sensitivities had to be managed—employees of subsidiary banks feared losing their regional identity and autonomy.

Technology integration presented another massive challenge. While SBI had invested heavily in modernizing its core banking platform, the subsidiaries were at various stages of technological evolution. Merging large organizations can be complex and time-consuming. In some cases, integrating systems, processes, and cultures can be challenging and take more than planned time. The decision was made to migrate all subsidiaries to SBI's core banking solution, a process that required meticulous planning and execution.

On April 1, 2017, the merger became effective. With the merger of all the five associates, SBI is expected to become a lender of global proportions with an asset base of Rs 37 trillion (Rs 37 lakh crore) or over USD 555 billion, 22,500 branches and 58,000 ATMs. It will have over 50 crore customers. Overnight, SBI jumped from being the 52nd largest bank globally to entering the top 50.

The share exchange ratios were carefully calibrated to be fair to minority shareholders. SBBJ shareholders will get 28 shares of SBI (₹1 each) for every 10 shares (₹10 each) held. In the same way, SBM and SBT shareholders will get 22 shares of SBI for every 10 shares. For the wholly-owned subsidiaries—State Bank of Patiala and State Bank of Hyderabad—there was no share swap as SBI already owned 100% equity.

The immediate benefits were substantial. As against six treasuries, the merged entity will have one large one, benefiting from the parent's higher yields on investments. The management expects its cost of funds to come down by 100 basis points within a year, as the subsidiaries currently have high deposit rates, less of current and savings accounts, and higher dependence on wholesale funding.

Risk management improved dramatically. It will also lead to better management of high value credit exposure through focused monitoring and control over cash flows instead of separate monitoring by six different banks. Many people had availed multiple finances. With merger, they can be brought under one roof which makes recovery easier. This was particularly important given the rising NPAs in the Indian banking system.

The consolidation also addressed the "too big to fail" paradox. SBI though is identified by the RBI as a systemically important bank, requiring additional capital in its book for absorbing any future shock. But SBI's size is not comparable with other banks. SBI, with close to Rs 30 lakh crore assets, is way ahead of the two largest private banks - HDFC Bank and ICICI Bank, which are in the region of Rs 7-8 lakh crore.

Critics raised valid concerns. There is a view that exercise of market power by larger merged banks can also alter the monetary transmission operating through bank lending or borrowers without direct access to financial sector, so mergers may increase systemic risks and mergers guided only by pure capital adequacy considerations are ill-advised. The concentration of risk in a single entity, while providing stability, also created new vulnerabilities.

The cultural integration proved as challenging as expected. Last year, employees of the State Bank of Travancore (SBT) observed a strike under the aegis of the State Bank of Travancore Staff Union. The agitation was in protest against the move to merge the SBT with the State Bank of India. Regional pride and identity issues had to be carefully managed.

Yet the merger succeeded where many predicted failure. By 2018, most integration issues had been resolved. Customers gained access to a much larger network, product offerings were standardized and improved, and operational efficiencies began to materialize. The merger became a template for further consolidation in India's public sector banking, with other banks following SBI's lead in subsequent years.

The great consolidation transformed SBI from a large Indian bank with regional subsidiaries into a truly national institution with global scale. It demonstrated that Indian banks could execute complex mergers successfully, challenging the conventional wisdom that public sector institutions lacked the capability for such transformations. Most importantly, it positioned SBI to compete effectively in an increasingly digital and globalized banking environment—setting the stage for its next transformation into a digital banking powerhouse.

VIII. Digital Transformation & YONO (2010s–Present)

The digital revolution came to SBI not as a choice but as an existential imperative. The app was launched in November 2017, marking SBI's most ambitious attempt to reinvent itself for the smartphone generation. The launch of YONO had a code name project Lotus. YONO SBI emerged from SBI's initial plan to make an "online marketplace" to attract millennials. The initiative was named "Project Lotus". It was nurtured for initial four years by Rajnish Kumar as an MD and then as the Chairman of bank.

YONO—You Only Need One—represented more than just another banking app. It was SBI's strategic response to multiple threats: the dominance of private banks in digital banking, the emergence of fintech startups, and most critically, the explosion of third-party payment apps that were intermediating SBI's relationship with its own customers. The State Bank of India (SBI), has a market share of just 0.18 per cent in UPI ( unified payment interface ) transactions, despite being the country's largest bank—a stark illustration of how technology disruption had upended traditional banking hierarchies.

The platform's ambition was unprecedented for an Indian public sector bank. YONO SBI offers services from over 100 e-commerce companies including online shopping, travel planning, taxi booking, train booking, movie ticket booking. This wasn't just mobile banking—it was an attempt to create a financial super-app, competing not just with banks but with e-commerce platforms, travel aggregators, and lifestyle apps.

The technical challenges were formidable. SBI had to build a platform that could handle hundreds of millions of users while maintaining the security and reliability expected of India's largest bank. The bank's legacy systems, some dating back decades, had to be integrated with modern microservices architecture. Customer data scattered across multiple databases had to be unified. Most challengingly, the organizational culture had to shift from risk-averse conservatism to digital-first innovation.

The early years were marked by significant teething problems. Users complained about frequent crashes, slow performance, and confusing user interfaces. The app's initial reviews were harsh, with customers comparing it unfavorably to slick offerings from private banks and fintech startups. SBI's traditional customer base, accustomed to branch banking, struggled with the digital transition, while younger users found the app clunky compared to consumer internet standards.

Yet SBI persisted, investing heavily in improvements. On 16th March 2019, SBI launched YONO Cash, a unique feature available on the YONO platform that enables an SBI account holder to withdraw money instantly using SBI ATMs and SBI Merchant POS terminals and Customer Service Points (CSPs) within India without the use of a physical card. This innovation addressed a critical pain point—enabling cash transactions without physical cards, particularly valuable in a country where cash still dominates many transactions.

The transformation accelerated dramatically. The State Bank of India (SBI) on Sunday, 2 July 2023 launched a revamped version of You Only Need One (YONO) app. The number of registered users on YONO has surpassed 6 billion since its launch in 2017. Through YONO, 78.60 lakh SBI savings accounts were opened online in FY23. The 2023 revamp marked a crucial pivot—instead of competing directly with UPI apps on payments, SBI focused on leveraging its unique strengths: the ability to offer integrated banking services, credit products, and government services that pure-play payment apps couldn't match.

On 2 July 2023, a new version of Yono app was launched with the introduction of a new UPI feature which enabled other bank customers to use the app for UPI payments. The update also brought QR scanning and pay-by-contact UPI functionalities. This strategic shift acknowledged that SBI couldn't beat PhonePe or Google Pay at their own game but could create a differentiated offering.

SBI YONO has 87.7 million users in FY25, making it one of India's largest financial apps despite the intense competition. With a 52 Crore customer base and growing, your Bank is committed to offering excellence in customer experience. The platform has become central to SBI's strategy of retaining customer relationships in an increasingly digital world.

The broader digital transformation extended beyond YONO. SBI invested heavily in core banking modernization, API infrastructure, and data analytics capabilities. The bank established innovation labs, partnered with fintech startups, and recruited technology talent aggressively. Digital channels now account for the majority of transactions, reducing operational costs while improving customer convenience.

The UPI revolution posed both threat and opportunity. PhonePe held around 48 percent share of unified payment interfaces (UPI) usage in India, followed by Google Pay with 37 percent. Leading fintech players have been key drivers of UPI adoption in India. While SBI's direct UPI market share remained minimal, the bank benefited as the settlement bank for many transactions, earning fees even when customers used third-party apps.

SBI's response has been strategic rather than confrontational. Instead of trying to compete head-on with specialized payment apps, the bank focused on areas where its scale and trust provided advantages. Banks have a significant opportunity to leverage their trust and infrastructure and compete more effectively with fintechs to increase their market share in the growing UPI ecosystem. One of the leading reasons for the success of UPI TPAP is investment in merchant channel development.

The bank's approach to partnerships evolved significantly. Rather than viewing fintechs as pure competitors, SBI began selective collaborations, providing banking infrastructure while partners handled user experience and customer acquisition. This strategy acknowledged that in the platform economy, owning the customer relationship might be less important than being the essential infrastructure provider.

YONO Business, launched as a separate platform for SMEs and corporates, demonstrated SBI's segmentation strategy. 223 Correspondent Banks (55 countries) and fintech partnerships expanded SBI's global digital reach. The bank also invested in blockchain, artificial intelligence for credit scoring, and robotic process automation for back-office operations.

The COVID-19 pandemic accelerated digital adoption by years. Customers who had never used digital banking were forced to adapt, and SBI's massive investment in digital infrastructure paid dividends. The bank could handle the surge in digital transactions while many competitors struggled with capacity constraints.

Yet challenges remain significant. Bank's customers spend more time on TPAP and limited time on the Bank app or branch, so they are becoming customers of TPAPs, instead of sponsored banks. The commoditization of basic banking services means SBI must continuously innovate to remain relevant. Younger customers show little loyalty to traditional banks, choosing services based on convenience and features rather than brand heritage.

Cybersecurity has become increasingly critical as digital transactions exploded. SBI invested heavily in fraud detection, biometric authentication, and transaction monitoring systems. The bank processes billions of transactions monthly, each a potential vulnerability that must be secured without compromising user experience.

The regulatory environment has generally supported digital transformation. The Reserve Bank of India's progressive stance on digital payments, open banking, and fintech collaboration created an enabling environment. However, data localization requirements, privacy regulations, and cybersecurity mandates add complexity and cost to digital operations.

Looking ahead, SBI's digital strategy focuses on three pillars: defending the core banking franchise through superior digital experiences, selectively competing in high-value segments like wealth management and corporate banking, and serving as the infrastructure backbone for India's digital economy. The bank's unique position—massive scale, government backing, and deep rural presence—provides advantages that pure digital players cannot replicate.

The success of SBI's digital transformation will ultimately be measured not by app downloads or transaction volumes, but by its ability to remain relevant in a radically transformed financial landscape. Can a 200-year-old institution reinvent itself for the digital age while maintaining its social mission? Can it compete with nimble startups while serving rural farmers? Can it innovate at Silicon Valley speed while operating within government constraints? These questions will define not just SBI's future, but the evolution of banking in emerging markets worldwide.

IX. Modern Era: Financial Performance & Strategy

The financial performance of modern SBI tells a story of remarkable resilience and strategic transformation. The bank's FY2024 results showcase an institution firing on all cylinders: standalone net profit of ₹61,077 Crore, representing a robust 21.59% growth year-over-year. Operating profit reached ₹93,797 Crore, up 12.05%, while Net Interest Income registered strong growth of 10.38% to ₹1,59,876 Crore. These aren't just numbers—they represent the successful execution of a complex balancing act between commercial success and social responsibility.

The composition of SBI's loan book reveals its strategic positioning across India's diverse economy. Corporate loans, at ₹11.38 Lakh Crore, grew by 16.17%, demonstrating SBI's continued dominance in wholesale banking despite intense competition from private banks. But the real story lies in the retail and SME segments. SME advances surged 20.53% to ₹4.33 Lakh Crore, while agricultural advances grew 17.92% to ₹3.05 Lakh Crore—segments where SBI's extensive branch network provides an almost insurmountable competitive advantage.

The retail portfolio's performance deserves special attention. Home loans, growing 13.29% to ₹7.26 Lakh Crore, give SBI a commanding 26.5% market share in India's mortgage market. Auto loans expanded 19.50% to ₹1.17 Lakh Crore, capturing 19.8% market share. These aren't just growth statistics—they represent millions of Indian families achieving their dreams of homeownership and mobility, with SBI as their financial partner.

The digital lending revolution has transformed SBI's retail strategy. Xpress Credit, the bank's digital personal loan product, grew 14.62%, with loan approvals happening in minutes rather than days. The entire credit assessment, from application to disbursement, now happens digitally for eligible customers, competing directly with fintech lenders who once claimed this space as their own.

Asset quality, long the Achilles' heel of Indian public sector banks, has shown dramatic improvement. SBI's gross NPA ratio has declined from double digits during the 2018 crisis to more manageable levels, though the exact current figures would need verification. This improvement reflects not just economic recovery but also better underwriting, improved recovery mechanisms, and the implementation of early warning systems powered by artificial intelligence.

The bank's capital position remains robust, crucial for supporting growth while meeting increasingly stringent regulatory requirements. The Reserve Bank of India (RBI) has identified SBI, HDFC Bank, and ICICI Bank as domestic systemically important banks (D-SIBs), which are often referred to as banks that are "too big to fail". This designation brings additional capital requirements but also implicit government backing that provides stability during crises.

International operations contribute significantly to SBI's profitability, though they represent a small fraction of total assets. As of 2024–25, the bank had 241 overseas offices spread over 36 countries having the largest presence in foreign markets among Indian banks. These operations serve the Indian diaspora, facilitate trade finance, and support Indian companies' global expansion, generating higher margins than domestic operations.

The fee income strategy has evolved beyond traditional banking charges. Bancassurance, wealth management, and investment banking contribute increasingly to non-interest income. SBI's subsidiaries—SBI Life, SBI Cards, SBI Mutual Fund—leverage the parent's distribution network while contributing to consolidated profitability. Cross-selling ratios have improved significantly, though they still lag private sector peers.

Cost management remains an ongoing challenge. SBI's cost-to-income ratio, while improving, remains higher than private banks due to its massive branch network and large employee base. SBI is one of the largest employers in the world with 232,296 employees as of 31 March 2024. It is also the tenth largest employer in India with nearly 250,000 employees. The bank has implemented various efficiency measures—branch rationalization, process automation, and voluntary retirement schemes—but the social and political costs of aggressive cost-cutting limit flexibility.

The pension burden represents a significant structural challenge. Unlike private banks that offer defined contribution plans, SBI maintains defined benefit pension obligations for employees recruited before certain cutoff dates. These unfunded liabilities, while manageable, constrain profitability and limit strategic flexibility. The gradual transition to the National Pension System for new employees will eventually address this, but the overhang will persist for decades.

Technology investments, while essential for competitiveness, pressure near-term profitability. The bank spends billions annually on technology infrastructure, cybersecurity, and digital innovation. These investments are necessary to compete with fintech startups and private banks, but the return on investment often takes years to materialize. The challenge is maintaining profitability while investing for the future.

The competitive landscape has intensified dramatically. Private banks like HDFC Bank and ICICI Bank have grown rapidly, often cherry-picking SBI's most profitable customers. Fintech companies unbundle banking services, targeting high-margin products like payments and consumer lending. Yet SBI's response has been effective—leveraging its scale, trust, and distribution to maintain market leadership.

Regulatory changes continue to shape strategy. Priority sector lending requirements mandate that 40% of loans go to agriculture and allied activities, small enterprises, and other designated sectors. While these requirements support financial inclusion, they also constrain profitability as priority sector loans often yield lower returns and higher NPAs. SBI has turned this constraint into competitive advantage, becoming the dominant player in these segments.

The bank's approach to ESG (Environmental, Social, and Governance) has evolved from compliance to strategy. SBI finances renewable energy projects, supports sustainable agriculture, and has committed to carbon neutrality targets. These initiatives, while requiring investment, position the bank favorably with international investors and align with India's climate commitments.

Risk management has been transformed through technology and data analytics. The bank now uses machine learning models for credit scoring, fraud detection, and early warning systems. Real-time monitoring of large exposures, sector concentration, and market risks has improved significantly. The three lines of defense model—business units, risk management, and internal audit—has been strengthened.

Looking at financial metrics, SBI's return on assets and return on equity have improved steadily but remain below private sector benchmarks. This reflects the structural challenges of public sector banking—priority sector obligations, social mandates, and legacy costs. Yet the bank's stability, systemic importance, and government backing provide advantages that pure financial metrics don't capture.

The stock market's assessment reflects both confidence and concern. SBI trades at a significant discount to book value compared to private banks, reflecting concerns about government interference, asset quality, and structural inefficiencies. Yet the stock has delivered substantial returns to long-term shareholders, benefiting from India's economic growth and the bank's dominant market position.

The modern SBI stands at an inflection point. It has successfully navigated the transition from a government-owned behemoth to a commercially oriented yet socially responsible institution. The financial performance demonstrates this success—profitable growth, improved asset quality, and enhanced operational efficiency. Yet challenges remain: intense competition, technological disruption, and the eternal balance between commercial and social objectives. The next decade will determine whether SBI can maintain its relevance and leadership in an increasingly digital, competitive, and globalized banking landscape.

X. Playbook: Business & Investing Lessons

The State Bank of India story offers a masterclass in navigating seemingly irreconcilable contradictions. How does an institution serve shareholders while fulfilling social mandates? How does it compete with nimble startups while carrying two centuries of legacy? The answers lie not in choosing sides but in turning constraints into competitive advantages—a playbook relevant far beyond banking.

Scale as Competitive Advantage: SBI's 500 million customers represent more than market share—they're a self-reinforcing network effect. Each customer makes the bank more valuable to merchants, each merchant attracts more customers, and the cycle continues. This isn't the winner-take-all network effect of social media, but rather a density advantage where physical presence, digital reach, and trust reinforce each other. The lesson: in businesses with high fixed costs and trust requirements, scale provides durability that technology alone cannot disrupt.

The Dual Mandate Paradox: Conventional wisdom suggests that serving social objectives compromises commercial success. SBI's experience suggests otherwise. Its mandate to serve rural India, initially seen as a burden, became a moat. While private banks fought over urban customers, SBI built relationships with farmers who became small business owners, whose children became urban professionals, creating multi-generational customer relationships. The playbook insight: constraints force innovation and can create unexpected competitive advantages.

Managing Complexity at Scale: From 480 branches to over 22,500, from a single presidency bank to a merged entity with seven subsidiaries—SBI's growth created organizational complexity that would paralyze most institutions. The bank's approach wasn't to eliminate complexity but to manage it through federalization: strong central standards with local execution flexibility. Branch managers retain significant autonomy within risk parameters. Technology provides consistency while humans provide judgment. This balance between standardization and customization offers lessons for any organization scaling across diverse markets.

Government Ownership: Blessing and Curse: State ownership provides SBI with patient capital, implicit guarantees, and privileged access to government business. Accredited banker for 26 major Central Government ministries and departments. Largest market share in Government Business, accounting for ~62% of turnover in Central Government sector. Yet it also brings political interference, bureaucratic constraints, and limited operational flexibility. SBI's playbook has been to maximize the advantages while minimizing disadvantages—using government backing to access cheap deposits while maintaining professional management to limit political interference.

Financial Inclusion as Business Strategy: What began as a government mandate became a business model. SBI's rural presence, built for developmental banking, now provides low-cost deposit funding that private banks cannot match. Small savings accounts, individually unprofitable, collectively provide stable, cheap funding. Microfinance, agricultural lending, and SME banking—all started as social obligations—now generate significant profits. The lesson: serving underserved markets requires patient capital and long-term thinking but can create sustainable competitive advantages.

Technology Transformation While Maintaining Legacy Operations: Unlike startups that build on green fields, SBI had to transform while maintaining 24/7 operations for half a billion customers. The bank's approach—running parallel systems, gradual migration, extensive testing—took longer and cost more than disruptive transformation. But it worked. No major outages, no customer data losses, no systemic failures. The playbook: in mission-critical systems, evolutionary change beats revolutionary disruption.

Capital Allocation in a Regulated Environment: SBI operates within strict regulatory constraints—statutory liquidity ratios, priority sector lending requirements, capital adequacy norms. Yet within these constraints, the bank has optimized capital allocation, using sophisticated models to price risk, cross-subsidize products, and maximize returns. The insight: constraints force discipline and innovation in capital allocation that unconstrained competitors often lack.

Building Trust Over Centuries: In banking, trust is everything. SBI's 200-year history provides credibility that no amount of marketing can buy. During demonetization, banking crises, and economic upheavals, Indians trusted SBI with their savings. This trust, carefully cultivated over generations, represents an intangible asset worth more than the bank's entire market capitalization. The lesson: in trust-based businesses, heritage and stability can trump innovation and convenience.

The Consolidation Playbook: The 2017 merger of subsidiary banks offers a template for large-scale consolidation. Start small (test with one or two entities), learn and refine, then execute at scale. Prioritize technology integration over immediate cost synergies. Maintain cultural sensitivity while driving standardization. Accept short-term disruption for long-term efficiency. Most importantly, communicate constantly with all stakeholders. This systematic approach to merger integration has become a model for subsequent banking consolidation in India.

Competing Against Unbundling: As fintechs unbundle banking—payments, lending, wealth management—SBI's response has been selective competition and strategic partnership. The bank doesn't try to match every fintech innovation but focuses on areas where its advantages—balance sheet, trust, regulation—matter most. Meanwhile, it partners with or provides infrastructure to fintechs in areas where user experience matters more than banking capabilities.

The Talent Challenge: Attracting technology talent to a public sector bank competing against Google and Goldman Sachs seems impossible. SBI's solution: create different talent pools with different rules. Technology subsidiaries with startup-like culture and compensation. Partnerships with universities for fresh talent. Extensive training programs to upskill existing employees. The recognition that not everyone needs to be a tech wizard—domain expertise in credit, risk, and relationships remains valuable.

Regulatory Arbitrage and Compliance: While private banks and fintechs often push regulatory boundaries, SBI's approach has been conservative compliance. This seeming disadvantage becomes an advantage during regulatory crackdowns. When regulations tighten, SBI is already compliant while competitors scramble to adjust. The playbook: in highly regulated industries, conservative compliance can be a competitive advantage during regulatory cycles.

The Platform Strategy: YONO represents SBI's evolution from a bank to a platform. By opening APIs, partnering with e-commerce players, and creating an ecosystem, SBI leverages its customer base without bearing all execution risk. The bank provides infrastructure—payments, credit, trust—while partners provide user experience and specialized services. This platform approach allows SBI to participate in digital commerce without competing directly with tech giants.

Managing Political Economy: As a public sector entity, SBI cannot ignore political considerations. The bank's approach has been to align with national priorities—financial inclusion, digital payments, infrastructure financing—while maintaining operational independence. By being seen as an instrument of national development rather than just a commercial entity, SBI maintains political support while minimizing interference.

The Innovation Paradox: Large organizations typically struggle with innovation, and government-owned entities even more so. SBI's approach has been to innovate through multiple channels: internal labs for incremental innovation, partnerships for customer-facing innovation, and subsidiaries for disruptive innovation. This portfolio approach allows experimentation without betting the bank on any single initiative.

For investors, SBI presents a complex proposition. The bank offers exposure to India's economic growth, trades at attractive valuations relative to private peers, and provides dividend yields. Yet it also carries risks—government interference, legacy costs, technological disruption. The investment case depends on one's view of India's economic trajectory and the role of public sector banks within it.

The ultimate lesson from SBI's playbook is that successful transformation doesn't require abandoning the past or blindly embracing the future. Instead, it requires thoughtfully leveraging existing advantages while selectively adopting new capabilities. In a world obsessed with disruption, SBI's evolution offers a different model—transformation through adaptation, creating value by bridging old and new rather than choosing between them.

XI. Analysis & Bear vs. Bull Case

Bull Case: The Incumbent's Revenge

The bull case for SBI rests on a fundamental premise: in banking, unlike consumer technology, incumbency advantages compound rather than erode over time. With 500 million customers—nearly 40% of India's population—SBI has achieved a scale that creates virtually insurmountable barriers to entry. This isn't just about customer numbers; it's about the depth of financial data, transaction history, and behavioral patterns that enable superior credit underwriting and risk management.

India's economic trajectory provides powerful tailwinds. As the economy grows from $3.7 trillion to a projected $10 trillion by 2035, financial services will grow even faster. Credit-to-GDP ratios remain low by global standards, suggesting massive expansion potential. SBI, as the nation's largest bank, is positioned to capture a disproportionate share of this growth, particularly in underserved segments where its distribution advantage is strongest.

The digital transformation, while incomplete, is showing results. SBI YONO has 87.7 million users in FY25, demonstrating that even government-owned banks can build successful digital platforms. More importantly, SBI has proven it can digitize without abandoning its physical presence, creating an omnichannel advantage that pure digital players cannot replicate. The bank's ability to offer assisted digital services through branches becomes crucial as India digitizes—not everyone can or wants to be fully self-service.

Government backing provides unmatched stability. During crises—whether the 2008 financial crisis, 2020 pandemic, or periodic banking sector stress—SBI's government ownership ensures access to capital and liquidity. This implicit guarantee allows the bank to maintain lower capital buffers and access cheaper funding than private competitors, creating a structural cost advantage.

The subsidiary ecosystem amplifies value creation. SBI Life, SBI Cards, SBI Mutual Fund—these aren't just cross-selling opportunities but independent profit centers leveraging the parent's distribution. As these subsidiaries mature and potentially list separately, they could unlock significant value currently obscured in the consolidated financials.

Regulatory evolution favors incumbents. As digital banking matures, regulations around data privacy, cybersecurity, and consumer protection are tightening. Compliance requires massive investments in technology and processes that SBI can afford but smaller players cannot. The regulatory moat is rising, not falling.

Bear Case: The Disruption Scenario

The bear case sees SBI as a melting ice cube—superficially solid but gradually eroding as the environment warms. The fundamental challenge is that banking is being unbundled, and SBI's integrated model becomes a liability rather than an asset. Why would customers use a mediocre all-in-one app when they can use best-in-class specialized services?

The technology gap is widening, not narrowing. While SBI invests billions in technology, nimble competitors iterate faster. PhonePe and Google Pay, which command a market share of 48.91 per cent and 34.17 per cent, respectively in UPI transactions, while SBI languishes below 1%. This isn't just about payments—it's about owning the customer relationship and transaction data that drives future lending decisions.

Government ownership increasingly becomes a burden. Political interference in lending decisions leads to asset quality problems. The inability to close unprofitable branches, reduce staff, or exit unviable businesses creates structural inefficiencies. Salary constraints make it impossible to attract top talent, especially in technology and risk management. The gap between public and private sector capabilities widens with each passing year.

The demographic challenge is existential. Younger Indians show no loyalty to traditional banks. They choose financial services like they choose apps—based on user experience, features, and convenience. SBI's brand equity, built over centuries, means nothing to a generation that values innovation over heritage. As digital natives become the dominant customer segment, SBI's advantages evaporate.

Competition is coming from unexpected directions. It's not just other banks or payment apps—it's e-commerce platforms with embedded finance, telecom companies leveraging data advantages, and global tech giants with unlimited capital. Amazon, Google, and Facebook understand customers better than any bank. When they enter financial services seriously, traditional banks face existential threats.

The profitability squeeze accelerates. Net interest margins compress as competition intensifies and rates normalize. Fee income disappears as digital services become free. Operating costs remain high due to legacy infrastructure and employment. Credit costs spike during economic downturns due to priority sector exposure. The result: structurally lower returns that make SBI a value trap rather than a value investment.

Asset quality remains vulnerable. India's corporate stressed assets may have peaked, but new risks emerge—retail over-leverage, agricultural stress from climate change, SME failures from economic disruption. SBI's size and social mandate mean it cannot be selective in lending. When the next crisis hits, SBI will bear disproportionate losses.

The Balanced View

Reality likely lies between these extremes. SBI will neither dominate nor disappear but evolve into something different—perhaps a financial infrastructure provider rather than a consumer-facing bank. The bank's wholesale and government businesses remain strong. Its role in financial inclusion ensures political support. Its balance sheet strength provides stability.

The key variables to watch: Can SBI maintain relevance with young urban customers? Can it monetize its data advantage before tech companies make it irrelevant? Can it manage the transition from a people-intensive to technology-intensive business model? Can it balance commercial objectives with social mandates as political pressures intensify?

For investors, SBI represents a complex bet on India's financial evolution. Bulls see a nationally strategic institution trading at a discount to intrinsic value. Bears see a melting ice cube whose accounting profits mask economic value destruction. The truth depends on one's time horizon, risk tolerance, and view of banking's future.

The investment decision ultimately comes down to whether one believes banking will remain a distinct industry requiring specialized capabilities—balance sheet management, risk assessment, regulatory compliance—or whether it becomes a feature embedded in broader platforms. If the former, SBI's advantages endure. If the latter, its challenges multiply.

What's certain is that SBI's next decade will look nothing like its previous century. The bank that emerged from colonial commerce, survived independence and partition, drove nationalization and consolidation, must now navigate digital disruption and platform competition. Success is not guaranteed, but neither is failure. The only certainty is transformation—and SBI has proven, over 218 years, remarkably adept at reinventing itself when survival demands it.

XII. Epilogue & Future Outlook

As we stand in 2025, the State Bank of India represents far more than a financial institution—it embodies India's economic autobiography, written across two centuries of transformation. The Reserve Bank of India (RBI) has identified SBI, HDFC Bank, and ICICI Bank as domestic systemically important banks (D-SIBs), which are often referred to as banks that are "too big to fail". This designation isn't just regulatory categorization; it's recognition that SBI has become so interwoven with India's financial fabric that its success or failure would ripple through the entire economy.