SBI Life Insurance: Building India's Insurance Giant

I. Introduction & Episode Roadmap

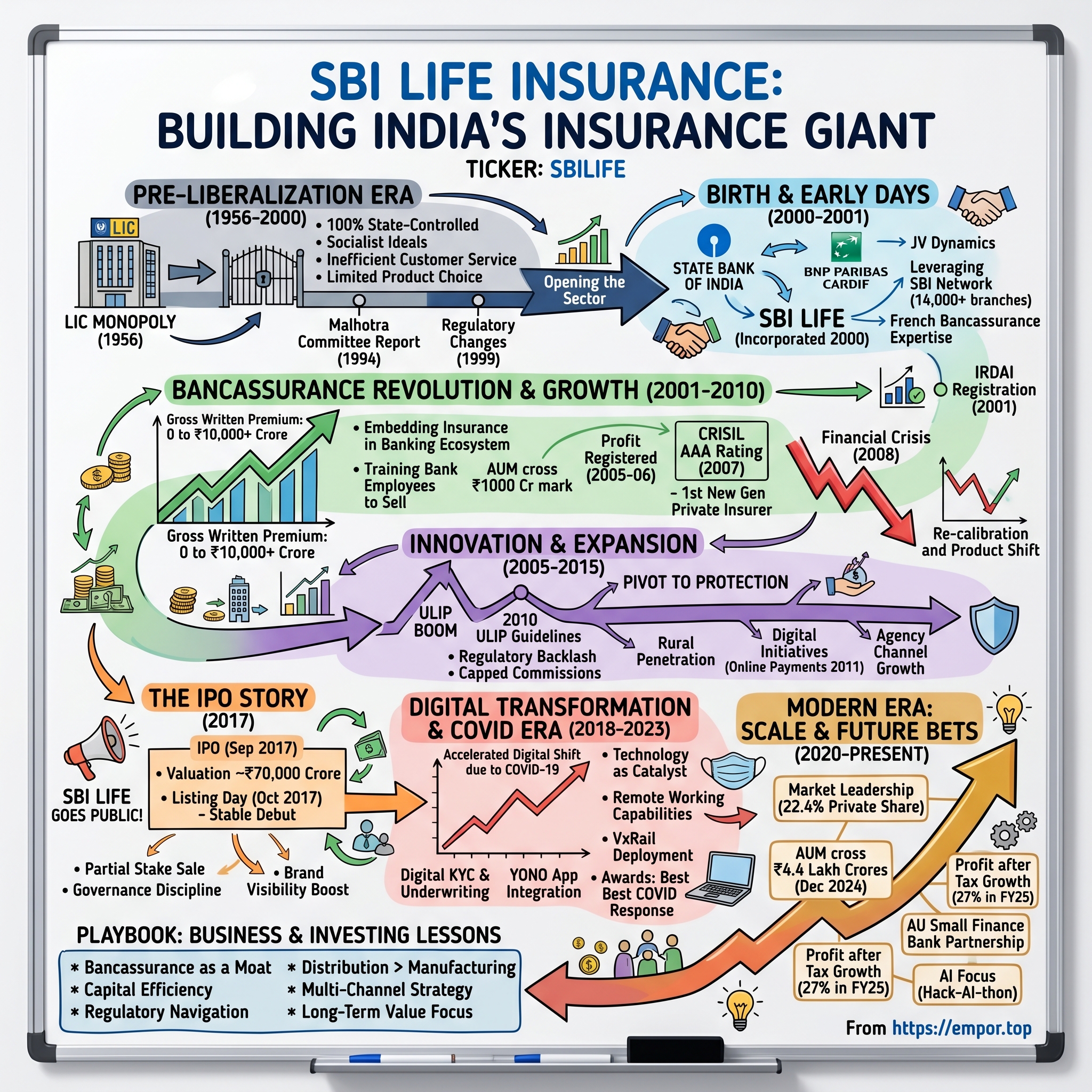

The story of SBI Life Insurance is fundamentally a story about transformation—how India's financial services sector evolved from state monopoly to competitive dynamism, and how one company rode that wave to become a Rs 1,81,195 crore behemoth. When you walk into any State Bank of India branch today, the insurance desk is as prominent as the traditional banking counters, a visual representation of how deeply SBI Life has embedded itself into India's financial fabric.

This isn't just another corporate success story. It's a masterclass in joint venture dynamics, regulatory navigation, and distribution leverage. SBI Life emerged from the marriage of India's largest public sector bank—State Bank of India—with French insurance expertise from BNP Paribas Cardif, creating a hybrid that would challenge the decades-old monopoly of Life Insurance Corporation of India.

The numbers tell a compelling story: from zero to becoming one of India's top three private life insurers, managing assets worth over Rs 3.7 trillion, serving millions of policyholders through a network that spans urban metros to rural villages. But the real story lies in the strategic choices, the timing of market entry, and the relentless focus on distribution that turned a late entrant into an industry leader.

What makes SBI Life particularly fascinating is how it solved the classic chicken-and-egg problem of insurance distribution in India. While competitors struggled to build agent networks from scratch or relied heavily on expensive direct sales forces, SBI Life had an ace up its sleeve—access to over 22,000 SBI branches and their captive customer base. This bancassurance model, relatively novel in India at the time, would become the company's defining competitive advantage.

The journey from incorporation in 2000 to public listing in 2017 and beyond reveals crucial lessons about building financial services businesses in emerging markets. It's about understanding regulatory cycles, riding product innovation waves, surviving crises, and constantly reinventing distribution strategies. As we dive deep into this story, we'll explore how a company that started when most Indians didn't understand life insurance beyond LIC policies became a digital-first insurer processing claims in minutes and selling policies through mobile apps.

This analysis will take us through the pre-liberalization insurance landscape dominated by LIC's socialist-era monopoly, the political battles that opened up the sector, the early days of building credibility against an entrenched incumbent, the ULIP boom and bust, the digital transformation accelerated by COVID-19, and the current battles being fought on technology platforms and customer experience. We'll examine the playbook that made SBI Life successful and debate whether those advantages remain defensible in an era of insurtech disruption and changing consumer preferences.

II. Pre-Liberalization Context & The LIC Monopoly

To understand SBI Life's emergence, we must first comprehend the insurance landscape it entered—a world utterly dominated by the Life Insurance Corporation of India. The year was 1956 when the Indian government, driven by socialist ideals and a desire to channel household savings into nation-building projects, nationalized the entire life insurance sector. In one sweeping move, 245 private insurance companies were merged to create LIC, establishing what would become one of the world's largest state-controlled monopolies.

This wasn't just a business consolidation; it was an ideological statement. Prime Minister Jawaharlal Nehru's government believed that insurance, like banking and heavy industry, was too important to be left to private enterprise. The monopoly would ensure that insurance premiums, instead of enriching private shareholders, would fund five-year plans, infrastructure projects, and industrial development. For the next 44 years, LIC would be synonymous with life insurance in India.

The monopoly created a peculiar market dynamic. On one hand, LIC built extraordinary reach—its agents became fixtures in middle-class neighborhoods, its policies funded daughters' weddings and children's education. The LIC agent, typically a respected community member who sold policies part-time, became a cultural institution. By the 1990s, LIC had over 600,000 agents and controlled assets worth hundreds of billions of rupees. Its market share wasn't just dominant; it was absolute—100%.

But monopolies breed inefficiencies. Customer service was notoriously poor—claim settlements took months, policy documents were incomprehensible, and innovation was non-existent. Products remained unchanged for decades. The traditional endowment policy, combining minimal insurance with forced savings, was virtually the only option available. Returns were paltry, often below inflation, but Indians had no alternatives. Insurance penetration remained abysmally low—less than 2% of GDP compared to global averages of 7-8%.

The economic crisis of 1991 changed everything. As India liberalized its economy under Prime Minister P.V. Narasimha Rao and Finance Minister Manmohan Singh, every sector came under scrutiny. Banking was partially privatized, capital markets were reformed, and foreign investment was welcomed. But insurance remained untouched initially—the political resistance was too strong. LIC employees' unions were powerful, and the fear of foreign companies "exploiting" Indian savings ran deep.

Enter the Malhotra Committee in 1993. Headed by former RBI Governor R.N. Malhotra, this committee was tasked with examining the insurance sector and recommending reforms. The committee's report in 1994 was revolutionary. It recommended ending LIC's monopoly, allowing private players, permitting foreign partnerships, and establishing an independent regulator. The logic was compelling—competition would improve service, increase penetration, bring innovation, and mobilize more savings for economic development.

But translating recommendations into policy took six years of political battles. The BJP, then in opposition, opposed "selling insurance to foreigners." The Left parties warned of "imperialism through insurance." LIC unions threatened nationwide strikes. The debate wasn't just economic but deeply emotional—insurance touched every Indian family, and LIC was seen as a national institution, not just a company.

The breakthrough came with the establishment of the Insurance Regulatory and Development Authority (IRDA) in 1999. This wasn't just about creating a regulator; it was about building an entire framework for a competitive insurance market from scratch. IRDA had to define capital requirements, solvency margins, investment guidelines, agent training standards, and consumer protection measures. They were essentially creating rules for a game that hadn't been played in India for over four decades.

When the sector finally opened in 2000, the structure was carefully calibrated to balance competing interests. Foreign ownership was capped at 26%—enough to bring expertise but not enough to control. This forced joint venture model would define the industry's evolution. Every foreign insurer needed an Indian partner, creating interesting dynamics of knowledge transfer, cultural adaptation, and strategic alignment.

The opportunity was massive but the challenges were daunting. New entrants would compete against LIC's 245-year combined institutional memory (counting all predecessor companies), its massive agent network, unmatched brand trust, and deep government connections. LIC policies were sold in post offices, its advertisements were cultural events, and its bonus declarations made newspaper headlines. How do you compete with that?

The answer, as companies like SBI Life would demonstrate, was not to compete head-on but to find gaps in LIC's armor. These gaps were numerous—urban educated customers wanting better service, corporations needing employee benefits, high-net-worth individuals seeking investment products, and young professionals comfortable with technology. The liberalization didn't just open a market; it revealed multiple markets that LIC had either ignored or underserved.

The timing was fortuitous. India's GDP was growing at 6-7% annually, creating a new middle class. IT services were booming, creating young professionals with disposable income. Nuclear families were replacing joint families, increasing the need for financial protection. Financial literacy was improving, and insurance was evolving from a tax-saving tool to a financial planning instrument.

The regulatory framework IRDAI created was surprisingly progressive. While protectionist in foreign ownership, it was liberal in product innovation, distribution models, and operational flexibility. New insurers could experiment with unit-linked products, online sales, and bancassurance—channels LIC had ignored. The regulator mandated rural and social sector obligations but gave flexibility in how to meet them.

By 2000, the stage was set for transformation. The first licenses were issued to ICICI Prudential and HDFC Standard Life, both bank-led joint ventures. But the most interesting entrant would be SBI Life—a joint venture between India's largest public sector bank and a French insurance giant. This wasn't just another private insurer; it was the public sector's answer to private competition, combining government DNA with foreign expertise.

III. The Birth of SBI Life: State Bank Meets French Expertise (2000-2001)

The boardrooms of State Bank of India in Mumbai must have been buzzing with unusual energy in early 2000. For an institution that traced its roots back to 1806 as the Bank of Calcutta, entering the insurance business represented both a massive opportunity and an existential question about identity. The decision to form SBI Life wasn't just about launching a new product line—it was about leveraging the most powerful distribution network in Indian banking to crack open a market that had been sealed for four decades.

SBI Life Insurance Company was incorporated as a public limited company in Mumbai on October 11, 2000, and registered with IRDAI in March 2001. The timing was deliberate and strategic. SBI's leadership had watched ICICI and HDFC—private sector banks that were fractions of SBI's size—move first into insurance. But SBI had something neither competitor possessed: 14,000 branches, 100,000 employees, and relationships with one in every three Indian households.

The partner selection process reveals much about SBI's strategic thinking. While ICICI chose Prudential for its Asian expertise and HDFC selected Standard Life for its conservative approach, SBI partnered with BNP Paribas Cardif, the life and property & casualty insurance arm of BNP Paribas. This wasn't the most obvious choice—BNP Paribas Cardif wasn't the largest global insurer, nor did it have significant Asian presence. But it offered something crucial: expertise in bancassurance, the model of selling insurance through bank branches, which was relatively underdeveloped in Asia but dominant in Europe.

The French had essentially invented modern bancassurance. In France, over 60% of life insurance was sold through banks, compared to less than 10% in most Asian markets. BNP Paribas Cardif brought systematic processes, training methodologies, and most importantly, a philosophy that insurance wasn't a separate business but an integral part of a bank's relationship with its customers. This aligned perfectly with SBI's vision—they didn't want to build a standalone insurance company but to embed insurance into their banking ecosystem.

The initial shareholding structure was telling: SBI held 74% (later increased to 76%) while BNP Paribas Cardif held 26% (later adjusted to 24%). This wasn't just about regulatory compliance with foreign ownership limits. SBI wanted clear control while ensuring enough stake for BNP Paribas to remain committed. The French brought not just capital—the initial paid-up capital was Rs 1,000 crore, substantial for a new insurer—but also technical expertise, product development capabilities, and critically, actuarial skills that India severely lacked.

The cultural amalgamation was fascinating. SBI, with its public sector ethos, bureaucratic processes, and social obligations, had to mesh with French efficiency, private sector aggression, and profit focus. Early employees describe surreal situations—French executives trying to understand why loan recovery in rural India followed harvest cycles, Indian managers explaining why policies needed to be available in 14 languages, and both sides debating whether a two-page policy document (French preference) or a 20-page one (Indian regulatory requirement) made more sense.

The first CEO, Sunil Behari Mathur, was a careful choice—an SBI veteran who understood the bank's culture but had also worked in international postings, bridging both worlds. The initial team was deliberately hybrid: senior positions split between SBI nominees who knew the distribution network and BNP Paribas executives who understood insurance economics. The first appointed actuary, a critical position in any insurance company, came from BNP Paribas, while the sales head was inevitably from SBI.

Product development in those early days was an exercise in adaptation. BNP Paribas Cardif's successful European products—mostly simple term and credit life insurance—needed complete reimagination for India. Indians didn't buy pure insurance; they wanted "money back." The French were puzzled by customers who asked, "What happens to my money if I don't die?" This led to the creation of endowment products that were essentially savings vehicles with minimal insurance coverage—economically inefficient but culturally necessary.

In its initial stage, business was mainly from the bancassurance channel. The strategy was clear: start with SBI's existing customers. Every home loan buyer was offered credit life insurance. Fixed deposit customers were pitched retirement plans. Savings account holders were introduced to child education policies. The bank's branch managers, initially resistant to "becoming insurance agents," were incentivized through commissions that often exceeded their monthly salaries.

The regulatory navigation required finesse. IRDAI was still finding its feet, regulations were being written in real-time, and precedents were being set daily. SBI Life's regulatory team, staffed with former LIC executives who understood insurance law and SBI veterans who knew banking regulations, became experts at threading the needle between banking and insurance compliance. They pioneered the concept of "bank referral arrangements," creating legal structures for banks to sell insurance without violating regulations that separated banking and insurance businesses.

Technology infrastructure was a massive challenge. SBI's core banking system, still being modernized in 2001, had to interface with a new insurance platform. BNP Paribas brought modern insurance software, but it assumed reliable internet connectivity—a luxury in India where many SBI branches still used dial-up connections. The solution was ingenious: a hybrid system where policies could be sold offline in branches and synchronized daily with central servers, combining First World insurance technology with Third World infrastructure realities.

The competitive dynamics were intriguing. LIC initially dismissed private insurers as "five-star" companies serving only the urban rich. ICICI Prudential and HDFC Life, the other early entrants, focused on metros and mini-metros, building agency forces and targeting high-net-worth individuals. SBI Life chose a different path—leveraging SBI's unmatched rural presence to go where others couldn't or wouldn't. By the end of 2001, SBI Life was selling policies in places where the nearest LIC office was 50 kilometers away.

Training was perhaps the biggest challenge. SBI had 100,000 employees, but none knew how to sell insurance. BNP Paribas Cardif's training modules, designed for French bank employees, had to be completely rewritten. The challenge wasn't just language but context—explaining actuarial concepts to branch managers who had never encountered probability theory, teaching insurance sales to employees whose entire careers had been about deposit mobilization.

The early metrics were modest but promising. In the first year of operations (2001-02), SBI Life collected premiums of Rs 95 crore—tiny compared to LIC's Rs 50,000 crore but impressive for a startup. More importantly, the loss ratio was controlled, claims were settled promptly, and customer complaints were minimal. The French emphasis on process and the Indian understanding of customer psychology created an unexpectedly effective combination.

By March 2002, SBI Life had established proof of concept. Insurance could be sold through bank branches. Public sector banks could compete with private sector efficiency. French insurance expertise could be adapted to Indian market realities. Joint ventures, despite cultural differences, could work. The foundation was laid for what would become one of India's most successful financial services companies.

The strategic masterstroke was recognizing that SBI Life wasn't really competing with LIC initially—it was creating a new market. LIC's agents targeted middle-aged, middle-class males who understood insurance. SBI Life reached young salary account holders who had never been approached for insurance. LIC sold through agents who visited homes; SBI Life sold to customers who walked into branches. LIC's policies were bought; SBI Life's policies were bundled with loans and deposits.

IV. The Bancassurance Revolution: Leveraging SBI's Network (2001-2010)

The numbers tell only part of the story: from virtually zero in 2001 to crossing Rs 10,000 crore in gross written premium by 2010, but the real revolution was happening at ground level in SBI branches across India. The bancassurance model that SBI Life pioneered wasn't just about selling insurance through banks—it was about fundamentally reimagining how financial products could be distributed in a country where most people had never bought insurance beyond what their employers provided.

Walking into an SBI branch in 2003 was a markedly different experience from 2001. Where once stood only traditional banking counters, now there were insurance desks, promotional materials, and most importantly, trained staff who could explain complex products in simple terms. The transformation didn't happen overnight—it required overcoming massive institutional inertia and changing mindsets that had been set in stone for decades.

The resistance from within SBI was substantial initially. Branch managers, already overwhelmed with banking targets, viewed insurance as an unwelcome distraction. The breakthrough came when SBI Life introduced a commission structure that made branch managers realize insurance could significantly boost their income. A branch manager in a mid-sized town could earn Rs 20,000-30,000 monthly in insurance commissions—often exceeding their regular salary. This economic incentive transformed skeptics into evangelists.

During financial year 2004-05 the company's assets under management (AUM) crossed Rs 1000 crore mark and in January 2005 it launched unit-linked product. In 2005-06 it became the first new generation private life insurance company registering profit. This early profitability—achieving it in just six years while competitors were still burning cash—validated the bancassurance model's efficiency.

The product innovation during this period was crucial. First new generation Private Life Insurance Company to make profit: PAT for the year is Rs 2.03 crores in 2005-06, a milestone that demonstrated the model's viability. The launch of unit-linked insurance plans (ULIPs) in January 2005 marked a pivotal moment. ULIPs combined insurance with market-linked investments, appealing to India's growing investor class who wanted both protection and wealth creation.

The ULIP revolution was perfectly timed. The Indian stock market was in a bull run, the Sensex had crossed 10,000, and retail investors were eager for market exposure. SBI Life's ULIPs offered something LIC's traditional endowment policies couldn't—transparency in charges, choice of funds, and potential for higher returns. The product flew off the shelves, with branches reporting customers queuing up to buy policies during market upswings.

But the real innovation was in distribution mechanics. SBI Life created a "hub and spoke" model where each SBI regional office had a dedicated insurance team that supported multiple branches. These teams conducted training, handled complex cases, and ensured compliance. The model scaled efficiently—instead of placing insurance experts in all 14,000 branches, they created 500 hubs supporting 25-30 branches each.

The training infrastructure was unprecedented. SBI Life established residential training centers where bank employees underwent intensive insurance education. The curriculum wasn't just about products but about changing mindsets—from thinking like bankers to thinking like financial advisors. Role-playing exercises simulated customer conversations, addressing common objections like "I already have LIC policy" or "Insurance is for old people."

By 2006, it became the sole private-sector life insurance company in India to announce profits, demonstrating its financial strength and customer trust. This achievement, barely six years after inception, was remarkable in an industry where most players expected to break even only after a decade.

The cross-selling strategy was sophisticated. Data analytics, primitive by today's standards but revolutionary then, identified customer segments most likely to buy insurance. Home loan customers were pitched mortgage protection. Parents opening children's education accounts were offered education insurance. Senior citizens renewing fixed deposits were introduced to pension plans. The conversion rates were multiples higher than cold calling or door-to-door sales.

Technology integration accelerated throughout this period. By 2007, SBI Life had connected most SBI branches to its central insurance platform. Policies could be issued instantly, premiums collected through existing bank accounts, and claims processed without customers visiting insurance offices. This seamless integration was years ahead of competitors who still required separate documentation and payment processes.

The rural penetration strategy leveraged SBI's unique strength—its presence in India's hinterlands. While private banks and their insurance partners focused on urban markets, SBI Life was selling policies in villages where the nearest LIC office might be 50 kilometers away. The products were simplified, documentation minimized, and processes adapted to rural realities—premium collections aligned with harvest cycles, claims settled through bank accounts when rural customers lacked standard address proofs.

Competition during this period was intensifying but differentiated. ICICI Prudential built a massive agency force, recruiting aggressively and training extensively. HDFC Life focused on high-net-worth individuals and corporate clients. Bajaj Allianz leveraged its general insurance distribution. But none had SBI's branch network advantage. By 2008, SBI Life was processing over 50,000 policies monthly, with 70% originating from bank branches.

The 2007 CRISIL AAA rating was a watershed moment, providing external validation of SBI Life's financial strength and operational excellence. This rating, the highest possible for an Indian financial institution, was particularly significant for a company less than seven years old. It enhanced credibility with corporate clients, facilitated better reinsurance terms, and most importantly, gave customers confidence that their long-term policies were secure.

Channel diversification began in earnest by 2008. While bancassurance remained dominant, SBI Life started building alternative channels. The agency channel grew to over 20,000 agents by 2009, carefully selected and trained to complement rather than compete with bank distribution. Corporate agency tie-ups were established with other banks, credit societies, and NBFCs. Direct sales teams targeted high-value customers in metros.

The financial crisis of 2008 tested the model severely. ULIPs, which had driven growth, suddenly became toxic as markets crashed. Customers who had bought policies expecting 20% returns faced negative values. Surrender requests flooded in. SBI Life's response was measured—extensive customer communication explaining market cycles, flexible premium payment options, and most critically, branch staff trained to handle distressed customers with empathy rather than sales pressure.

The crisis also triggered strategic recalibration. The product mix shifted toward traditional policies with guaranteed returns. The focus moved from aggressive growth to sustainable profitability. Risk management was strengthened with stricter underwriting standards and better claims investigation. The company learned that in insurance, unlike banking, problems could take years to surface but last for decades.

By 2010, crossing Rs 10,000 crore in gross written premium, SBI Life had definitively proven the bancassurance model. The company had 300 offices, 50,000 agents and advisors, and most importantly, over 8 million policies in force. The foundation was built not just for growth but for dominance. The cultural transformation was complete—insurance was no longer an appendage to SBI's banking business but an integral part of its financial services ecosystem.

The operational excellence achieved during this period was remarkable. Policy issuance time reduced from days to hours. Claim settlement ratios exceeded 95%, among the best in the industry. Customer complaints were minimal—less than 0.1% of policies resulted in escalations to IRDAI. The Net Promoter Score, while not formally measured then, would have been among the industry's highest based on renewal rates exceeding 80%.

The human capital development was equally impressive. SBI Life created an entire cadre of insurance professionals within SBI's banking ranks. Branch managers became insurance advisors, cashiers became policy processors, and relationship managers became financial planners. This transformation created career opportunities, additional income streams, and most importantly, a sense of ownership in insurance business success.

Looking back, the 2001-2010 period was when SBI Life built its moat. The bancassurance model, once established, became almost impossible to replicate. Competitors could tie up with other banks, but none had SBI's reach, trust, and customer base. The first-mover advantage in bancassurance, combined with superior execution, created a competitive advantage that persists today.

V. Product Innovation & Market Expansion (2005-2015)

The period from 2005 to 2015 was defined by extreme volatility—both in markets and regulations—that tested SBI Life's adaptability and strategic vision. This decade witnessed the ULIP boom and bust, regulatory overhauls that rewrote industry economics, and a fundamental shift in how insurance was perceived, sold, and regulated in India.

The unit-linked revolution began innocuously enough. When SBI Life launched its first ULIP product "Horizon" in January 2005, the timing couldn't have been better. The Sensex was soaring, real estate was booming, and Indians were discovering equity investing. ULIPs offered a perfect narrative—insurance plus investment, protection plus wealth creation. For middle-class Indians conditioned to view insurance as forced savings, ULIPs were revelatory.

The product design was ingenious in its simplicity. Customers paid premiums, a portion went toward life insurance coverage, and the rest was invested in equity or debt funds of their choice. Daily NAV calculations showed portfolio values, creating an addictive engagement loop. Customers who had never looked at traditional policy statements were now checking ULIP values daily, discussing fund performance at office water coolers.

SBI Life's ULIP distribution through bank branches created a perfect storm. Bank relationship managers, armed with historical return charts showing 20-30% annual gains, found ULIPs easier to sell than fixed deposits. The commissions were extraordinary—first-year commissions could reach 40% of premium, making a single ULIP sale worth months of salary for a bank employee. This incentive structure would later prove problematic, but in 2005-2008, it drove phenomenal growth.

The numbers were staggering. From virtually zero in 2005, ULIPs grew to constitute over 70% of SBI Life's new business premium by 2008. The company's AUM exploded from Rs 1,000 crore in 2004-05 to over Rs 10,000 crore by 2009. Branch managers who exceeded ULIP targets received foreign trips, cash bonuses, and rapid promotions. SBI Life became the fastest-growing among bank-promoted insurers.

But success bred excess. The focus shifted from insurance to investment returns. Sales pitches emphasized market performance, not mortality protection. Customers were shown illustrations with 15-20% projected returns, though regulations required showing 6% and 10% scenarios. The insurance component became token—just enough to qualify as insurance for tax benefits. Some ULIPs had insurance coverage as low as 5 times annual premium, making them mutual funds masquerading as insurance.

The 2008 financial crisis exposed the model's fragility. As markets crashed, ULIP values plummeted. Customers who had invested believing in guaranteed returns faced 30-40% losses. SBI branches were flooded with angry customers demanding their money back. The situation was particularly acute because many customers were retirees who had moved fixed deposits to ULIPs based on aggressive sales pitches.

SBI Life's response revealed organizational maturity. Instead of deflecting blame, they launched "Project Reassurance"—a massive customer outreach program. Branch staff were trained to explain market volatility, long-term investment horizons, and rupee-cost averaging. Flexible premium payment options were introduced. Partial withdrawal rules were relaxed. Most importantly, the sales force was retrained to set realistic expectations.

The regulatory backlash was swift and severe. The Indian life insurance sector saw a series of regulatory changes in September 2010, with IRDA finally deciding to clamp down on the mis-selling of ULIPs as investment products designed for regulatory arbitrage, and not as insurance products. The major steps taken by the regulator included increasing the mortality risk cover to 10 times the annual premium, thereby, increasing the insurance content and reducing the investment content, significantly reducing the commissions, increasing the lock-in period from 3 to 5 years and imposing a ceiling on ULIP charges.

The 2010 ULIP guidelines were a watershed moment. The above modifications will come into effect from 1st July 2010. All life insurers are advised that only the Unit Linked Insurance Products which conform to these revised guidelines shall be permitted to be offered for sale from 1st July 2010. These changes fundamentally altered product economics. Commissions were capped, charges were regulated, and minimum insurance coverage was mandated. The gold rush was over.

These new ULIP guidelines have resulted in new business premiums reducing by 21% in the last six months of financial year 2010-11 (October 2010 – March 2011) for life insurers as compared to the previous financial year 2009-10. For SBI Life, this meant reimagining its entire product strategy. The company had to pivot from high-margin ULIPs to traditional products with lower margins but more predictable economics.

The transformation wasn't just about products but about culture. The sales force, accustomed to easy ULIP sales with high commissions, had to learn to sell traditional products requiring more explanation and offering lower incentives. Many top performers left for other industries. Branch managers, seeing reduced insurance incentives, deprioritized insurance sales.

But crisis created opportunity. While competitors struggled with the transition, SBI Life leveraged its bancassurance strength to pivot toward protection products. Term insurance, previously ignored due to low commissions, became a focus area. The pitch changed from wealth creation to family protection. Marketing emphasized emotional security over financial returns.

Product innovation accelerated post-2010. SBI Life launched guarantee products offering assured returns, addressing customer skepticism about market-linked products. Pension products were redesigned to focus on retirement security rather than investment growth. Child education plans emphasized goal-based saving rather than market performance. Each product was carefully calibrated to meet regulatory requirements while remaining attractive to customers.

The agency channel expansion during this period was strategic. While bancassurance remained dominant, SBI Life recognized the need for distribution diversification. The number of agents grew from 20,000 in 2010 to over 70,000 by 2015. Unlike the earlier random recruitment, this was selective—focusing on professionals, women, and educated youth who could explain complex products and build long-term relationships.

Digital initiatives, still nascent, began taking shape. Online premium payments were introduced in 2011, revolutionary for customers accustomed to queuing in branches. Policy documents were digitized, claims tracking went online, and mobile apps were launched. These seemed minor then but laid the foundation for the digital transformation that would accelerate later.

Rural expansion continued steadily. SBI Life leveraged SBI's rural and semi-urban presence to reach markets other insurers ignored. Products were simplified—three-page brochures instead of thirty-page documents. Premium collection was aligned with agricultural cycles. Local language communication became standard. By 2015, over 30% of new policies came from rural and semi-urban areas.

The micro-insurance initiative deserves special mention. Working with SBI's financial inclusion programs, SBI Life offered insurance coverage to below-poverty-line families. Premiums were as low as Rs 100 annually, claims were settled in 48 hours, and documentation was minimal. While commercially unviable, these programs built enormous goodwill and fulfilled social obligations.

Corporate partnerships expanded beyond SBI. Tie-ups with regional rural banks, cooperative banks, and NBFCs broadened distribution. Each partnership required customization—products, processes, and training adapted to partner needs. The ability to manage multiple partnerships while maintaining service quality became a core competency.

The period also saw operational excellence initiatives. Claim settlement ratios improved from 90% to over 96%. Policy issuance time reduced to same-day in metros. Customer service moved from reactive to proactive—calling customers before renewal dates, sending birthday wishes, conducting financial planning camps. These soft touches built loyalty in a commoditized market.

Regulatory compliance became increasingly complex. New regulations on product design, distribution practices, customer protection, and financial reporting emerged regularly. SBI Life built a robust compliance infrastructure—dedicated teams, regular audits, mystery shopping, and whistleblower mechanisms. The investment in compliance, while expensive, prevented regulatory actions that plagued competitors.

The talent development during this period was remarkable. SBI Life created industry-leading training programs—actuarial training for mathematics graduates, leadership development for high performers, and specialized programs for different distribution channels. The SBI Life Insurance Academy, established in 2012, became an industry benchmark for professional development.

By 2015, SBI Life had successfully navigated the industry's most turbulent period. From ULIP dependence to product diversification, from commission-driven sales to customer-centric advisory, from urban focus to rural penetration—the transformation was comprehensive. The company that entered 2015 was fundamentally different from the one that had entered 2005, yet the core strength—SBI's distribution network—remained the bedrock of competitive advantage.

The financial performance reflected this transformation. Despite regulatory headwinds, premium income grew at 15% CAGR from 2010-2015. More importantly, the business mix shifted toward sustainable products. Protection products grew from 5% to 15% of new business. Persistency ratios improved from 60% to 75%. Customer satisfaction scores increased steadily.

Looking back, the 2005-2015 decade taught invaluable lessons. Product innovation without customer centricity was unsustainable. Regulatory arbitrage invited regulatory backlash. Distribution strength needed to be complemented by service excellence. Short-term profit maximization could damage long-term franchise value. These lessons would prove crucial as SBI Life prepared for its next phase—going public and competing in an increasingly digital world.

VI. The IPO Story: Going Public (2017)

The decision to go public in 2017 represented far more than a capital-raising exercise—it was a coming-of-age moment for SBI Life, a declaration that the company had matured from a joint venture experiment to a standalone financial powerhouse worthy of public ownership. The backstory of this IPO reveals intricate negotiations, strategic positioning, and careful timing that would set the stage for SBI Life's next phase of growth.

The push for an IPO had been building since 2015. BNP Paribas Cardif, having achieved substantial returns on its initial investment, was seeking partial liquidity. SBI, while content with the partnership, recognized that public listing would provide currency for acquisitions, enhance brand visibility, and create employee wealth through stock options. The regulatory environment was also favorable—SEBI had streamlined IPO processes, and investor appetite for financial services stocks was strong.

The preparation began in earnest in early 2016. Investment bankers from eight leading firms—including SBI Capital Markets, Axis Capital, BNP Paribas, Citigroup, Deutsche Bank, ICICI Securities, JM Financial, and Kotak Mahindra Capital—were appointed as book running lead managers, an unusually large syndicate reflecting the IPO's complexity and size. Each bank brought specific strengths: SBI Caps for regulatory navigation, international banks for foreign institutional investor access, and domestic banks for retail distribution.

The valuation exercise was particularly challenging. Insurance companies are notoriously difficult to value—traditional P/E ratios don't capture embedded value, future premium growth, or mortality assumptions. The bankers used multiple methodologies: embedded value multiples, price-to-book ratios, and comparisons with listed peers like HDFC Life and ICICI Prudential Life. The challenge was balancing attractive pricing for investors with maximizing proceeds for selling shareholders.

The timing decision was crucial. The September 2017 IPO window was chosen after careful analysis. The equity markets were buoyant—the Sensex had crossed 32,000. ICICI Lombard's successful IPO earlier that month had demonstrated investor appetite for insurance stocks. The festive season was approaching, traditionally a positive period for markets. Most importantly, SBI Life's FY17 results showed strong growth, with new business premium increasing at a CAGR of 35.45% between FY15-17, the highest among top five private insurers.

The structure of the offering was pure secondary sale—no fresh capital raise. The IPO involved sale of 120,000,000 equity shares, representing 12% of post-offer equity. SBI would sell 8% while BNP Paribas Cardif would offload 4%, carefully calibrated to maintain SBI's majority control while giving BNP Paribas desired liquidity. This structure sent a clear signal—the company didn't need capital; this was about providing liquidity and price discovery.

The price band was set at Rs 685-700 per share, valuing the company at approximately Rs 70,000 crore at the upper band. This represented a P/EV (Price to Embedded Value) multiple of about 2.7x, premium to the 2.2x at which HDFC Life was trading but justified by SBI Life's superior growth trajectory and distribution advantage. The pricing sparked debate—some analysts called it aggressive, others saw it as fair given the franchise value.

The roadshow was a masterclass in storytelling. Management, led by CEO Arijit Basu, presented a compelling narrative: SBI Life wasn't just an insurance company but a play on India's under-penetrated insurance market, riding on SBI's unmatched distribution and trust. The pitch emphasized multiple growth drivers: rising insurance awareness, increasing disposable incomes, favorable demographics, and regulatory push for financial inclusion.

The investor education process was intensive. Over three weeks, management conducted over 100 one-on-one meetings with institutional investors across Mumbai, Singapore, Hong Kong, London, and New York. The key messages were consistent: sustainable competitive advantages through bancassurance, improving product mix toward protection, technology investments for future growth, and experienced management team with proven execution track record.

The retail marketing campaign was unprecedented for an insurance IPO. Full-page newspaper advertisements, digital marketing campaigns, and investor awareness programs were launched. SBI branches displayed promotional materials, relationship managers called high-net-worth customers, and special IPO application camps were organized. The messaging was simple: "Own a piece of India's insurance growth story backed by SBI's trust."

When the IPO opened on September 20, 2017, the response was measured but positive. The institutional book built steadily, with quality long-only funds showing interest. Retail participation was strong, driven by SBI's customer base and the relatively affordable lot size of 21 shares (Rs 14,700 investment). The QIB portion was subscribed 5.72 times, retail 1.93 times, and HNI 0.78 times, resulting in overall subscription of 3.25 times.

The allocation strategy was carefully managed. Long-term institutional investors received priority over hedge funds. Retail allocation was maximized to create a stable shareholder base. The relatively modest oversubscription, compared to some tech IPOs, was actually welcomed—it suggested realistic pricing rather than hype.

Listed at ₹708.00 against issue price of ₹700.00, showing listing day gain of 1.14% on October 3, 2017. While the listing gains were modest, disappointing some retail investors expecting quick profits, the stable debut indicated institutional support. More importantly, it avoided the volatility that plagued some heavily hyped IPOs.

The post-IPO ownership structure was telling. SBI held 62.1%, BNP Paribas Cardif retained 22%, with 15.9% public float. Marquee investors included Government of Singapore, Aberdeen, Franklin Templeton, and several domestic mutual funds. This institutional ownership provided stability and validation of the business model.

The governance changes post-IPO were significant. Independent directors with insurance, banking, and technology expertise were inducted. Quarterly earnings calls became rigorous affairs with detailed disclosures. Management compensation was linked to stock performance through ESOPs. The company, always professionally run, now had the additional discipline of quarterly market scrutiny.

The strategic implications of going public were profound. Access to capital markets meant SBI Life could pursue acquisitions if opportunities arose. Stock currency enabled better talent retention through equity compensation. Public visibility enhanced brand recognition, important in a trust-based business like insurance. The listing also provided daily market validation of strategy and execution.

The IPO proceeds utilization, while going to selling shareholders rather than the company, had indirect benefits. SBI's partial stake sale demonstrated confidence in professional management without founder dependence. BNP Paribas's continued significant holding signaled long-term commitment to the partnership. The successful IPO also strengthened SBI Life's position in negotiations with bancassurance partners and reinsurers.

Employee morale received a significant boost. The ESOP program, launched pre-IPO, created wealth for hundreds of employees as stock prices appreciated. The public listing enhanced pride and professional identity—working for a listed company carried prestige. Recruitment became easier as SBI Life could offer equity compensation comparable to other listed insurers.

The market discipline imposed by public listing drove operational improvements. Cost ratios were scrutinized, growth quality was emphasized over quantity, and capital allocation became more rigorous. The quarterly reporting cycle, while adding pressure, created rhythm and urgency in execution. Management thinking evolved from annual planning to quarterly milestones.

The media coverage surrounding the IPO elevated SBI Life's profile substantially. From being known primarily as "SBI's insurance arm," it became recognized as an independent entity with its own identity, strategy, and growth story. This enhanced visibility helped in customer acquisition, partnership negotiations, and regulatory engagement.

The IPO also marked a generational transition. The founding team that had built SBI Life from scratch began planning succession. The next generation of leaders, many groomed internally, started taking larger responsibilities. The public listing provided a natural inflection point for this leadership evolution, ensuring continuity while bringing fresh perspectives.

Looking back, the 2017 IPO was executed near-perfectly. The timing caught the market upswing, pricing balanced all stakeholder interests, and execution was flawless. While listing gains were modest, the long-term value creation was substantial—the stock would double within three years, validating the IPO pricing and investment thesis.

The successful IPO established a template for other bank-sponsored insurance companies contemplating public listings. It demonstrated that insurance companies could access public markets independently of their parent banks, that investors would value distribution advantages appropriately, and that the Indian capital markets had matured to understand complex financial services businesses.

VII. Digital Transformation & COVID Era (2018-2023)

The period from 2018 to 2023 would test every assumption about the insurance business. What began as a steady digital evolution accelerated into a complete reimagination of how insurance could be sold, serviced, and delivered. The COVID-19 pandemic, rather than being just a crisis to survive, became a catalyst that compressed a decade of digital transformation into two years.

SBI Life is committed to enhance digital experiences for its customers, distributors and employees alike. This commitment, stated simply, masked an enormous transformation. When the company embarked on its digital journey in 2018, the insurance industry was still largely paper-based. Policy applications required physical signatures, medical examinations needed in-person visits, and claim settlements involved bundles of documents. The vision was to digitize not just customer interfaces but the entire value chain.

The initial digital initiatives seemed incremental but laid crucial groundwork. Online premium payments, which had been possible since 2011, were enhanced with multiple payment gateways, e-wallets, and UPI integration. The customer portal was redesigned for mobile-first experience. Video KYC was piloted for policy issuance. These seemed like small steps then but would prove invaluable when the pandemic struck.

While the engagement began as a future-proofing mechanism to enhance the remote working capabilities of the workforce in 2019, it soon became apparent that it was the ideal solution to handle the disruption caused by the pandemic in March 2020. The prescient investment in Dell Technologies' VxRail infrastructure, initiated in 2019, exemplified this forward-thinking approach. What was planned as a gradual digital upgrade became mission-critical overnight.

When India went into lockdown on March 24, 2020, SBI Life faced an existential challenge. Insurance is sold, not bought—it requires persuasion, explanation, trust-building. How do you sell life insurance when you can't meet customers? How do you conduct medical examinations during a health crisis? How do you process claims when offices are closed? The answer required complete operational reinvention.

With the deployment of the new VxRail solution from Dell Technologies, SBI Life was able to offer a robust and reliable platform that was instrumental in enabling the workforce to continue working productively during the remote working phase, amid the nationwide lockdown in March 2020. The solution ensured secure and containerized access to corporate users who handled confidential and sensitive data. It supported the existing VPN system that was used by another set of employees for business applications on company-provided assets. Additionally, the deployment also helped SBI Life with faster onboarding of employees, ease in end-point device management, and reduced time to reach the market. It offered the company optimal utilization of their workforce, seamless connectivity and increased efficiency of processes, at a time when remote working was crucial while keeping in mind their safety and well-being.

The technology transformation was just the foundation. The real challenge was behavioral change. Agents accustomed to face-to-face selling had to learn video conferencing. Underwriters who insisted on physical documents had to trust digital verification. Customers skeptical of online transactions had to be convinced about security. This required massive retraining, constant communication, and gradual trust-building.

The product innovation during COVID was remarkable. Recognizing customer anxiety about hospital visits, SBI Life launched tele-medical underwriting. Customers could complete medical requirements through video consultations and home sample collections. The turnaround time for policy issuance, which typically took 7-10 days, was reduced to 24 hours for standard cases. Some simple term policies could be bought entirely online in under 10 minutes.

The mortality impact of COVID created unprecedented challenges. Death claims spiked dramatically—some months saw 10x normal claim volumes. The traditional claim settlement process, requiring multiple documents and verifications, would have collapsed under this pressure. SBI Life simplified documentation requirements, accepted digital submissions, and fast-tracked COVID-related claims. Despite the surge, claim settlement ratios were maintained above 95%.

The 'new normal' propelled the significance of a safety net, with health, pension and protection solutions becoming cardinal to every investment portfolio. At SBI Life, we offer a bouquet of products catering to the evolving needs of our invaluable stakeholders. Digitalisation has become a business imperative, enabling seamless operations and ease of service. We have achieved many industry firsts and created remarkable synergy, which powers our abilities to deliver sustained value to all our stakeholders. Through our 'customer first' approach and increasing national presence, we have made insurance accessible to all, maintaining world-class services and providing hassle-free claims settlement experiences.

The distribution transformation was equally dramatic. With bank branches operating at limited capacity, the traditional bancassurance model was disrupted. SBI Life rapidly scaled digital lead generation—customers could express interest online, and agents would call to complete sales. The integration with SBI's YONO app, which had 50 million users, became a game-changer. Customers could buy simple products directly through the app without any human intervention.

The outbreak of the pandemic in the country and the imposition of immediate lockdown was a challenging phase for us, as we had to ensure that all our critical business functions were made operational for all our stakeholders, within the shortest possible time. While we were already in the process of building a future proof mechanism, the pandemic induced action just accelerated our progression. Our IT team immediately assessed the situation and after careful consideration, we successfully deployed the required platform, through collaboration with Dell Technologies. The VxRail solution helped us enable secure remote working for corporate end-users without compromising on user-experience.

The agent enablement during this period was transformative. Digital tools that were optional became mandatory. The Smart Advisor app provided agents with customer analytics, product recommendations, and digital proposal forms. Training moved entirely online—weekly webinars replaced physical meetings. Top performers shared best practices through video. The agent productivity, after an initial dip, actually exceeded pre-COVID levels by late 2020.

Customer behavior shifted fundamentally during the pandemic. The crisis made mortality salient—people who had postponed insurance decisions for years suddenly wanted coverage. Term insurance inquiries increased 300%. But customers also became more research-oriented, comparing products online before engaging with agents. The sales process evolved from push to pull, from product-selling to consultative advisory.

The partnerships ecosystem expanded beyond traditional channels. E-commerce platforms, digital payment apps, and even food delivery services became insurance distribution partners. These digital-native partnerships required API-based integration, real-time data exchange, and innovative products. Bite-sized insurance products—travel insurance for a single trip, COVID insurance for 3 months—were created for these channels.

SBI Life Insurance has won the Insurer of the Year - Life Category at the FICCI Insurance Industry Awards 2021 and SBI Life Insurance has won the award for 'Best Covid Response- Towards Customers, Towards Employees, Towards Communities' category at ASSOCHAM 13th Global E-Summit & Awards 2020. These recognitions validated the company's pandemic response strategy.

The post-pandemic period (2021-2023) saw consolidation of digital gains. Hybrid models emerged—customers might research online but prefer buying through agents. Digital became the default for service requests, but complex queries still needed human intervention. The omnichannel experience, seamlessly blending digital and physical touchpoints, became the new standard.

Artificial intelligence and analytics adoption accelerated. Chatbots handled routine queries, freeing customer service representatives for complex issues. Predictive analytics identified customers likely to lapse, enabling proactive retention. Automated underwriting, using medical history and lifestyle data, approved 60% of applications without human intervention. Claims assessment used image analytics to verify documents and detect fraud.

SBI Life Insurance, one of India's most trusted private life insurers, launched the 1st edition of 'Hack-AI-thon'; a nationwide innovation initiative encouraging bright minds to leverage AI for transforming the future of life insurance. The initiative offers a unique platform for tech students, across India, to co-create solutions for business-critical challenges in insurance, with a sharp focus on transforming customer experience, product accessibility and fraud prevention. This recent initiative shows the continued focus on innovation and engaging with the broader ecosystem.

The cybersecurity challenges multiplied with digitalization. As more customers transacted online and employees worked remotely, attack surfaces expanded. SBI Life invested heavily in security infrastructure—multi-factor authentication, encryption, regular security audits, and employee training. A Security Operations Center monitored threats 24/7. Despite millions of digital transactions, no major security breach occurred.

Regulatory adaptation was crucial. IRDAI progressively relaxed physical documentation requirements, allowed video KYC, and permitted digital policy issuance. SBI Life worked closely with regulators, sharing learnings and suggesting framework improvements. The company became a test bed for regulatory sandboxes, piloting innovative products and processes that would later become industry standards.

The financial performance during this period reflected successful transformation. Despite pandemic disruptions, premium growth remained robust. More importantly, the cost-to-income ratio improved as digital processes reduced operational expenses. Customer acquisition costs decreased as digital leads were cheaper than traditional agent-sourced business. The persistency ratio improved as digital engagement kept customers connected.

These glorious years of togetherness have led us to stand strong, in terms of profit maximisation, as well as customer and employee satisfaction quotients, even in the face of the pandemic woes. Employee experience transformed dramatically. Remote working, initially a pandemic necessity, became a permanent option for many roles. Digital collaboration tools enabled productivity regardless of location. The hiring process went completely digital—from recruitment to onboarding. Employee wellness programs, delivered digitally, addressed pandemic-related stress and anxiety.

The period also saw significant sustainability initiatives. Our key focus areas include energy efficiency, water conservation, waste management, driving paperless ways of working, embracing digital applications and solutions and reducing the use of plastic, among others. Digital transformation naturally aligned with environmental goals—less paper, reduced travel, lower carbon footprint.

Looking back, the 2018-2023 period transformed SBI Life from a traditional insurer with digital capabilities to a digital-first company with physical presence. The pandemic, rather than being just a crisis, became an opportunity to leapfrog competition and reimagine insurance. The company that emerged from this period was fundamentally different—more agile, more innovative, more customer-centric, and better prepared for future disruptions.

VIII. Modern Era: Scale, Technology & Future Bets (2020-Present)

The modern era of SBI Life represents the culmination of two decades of evolution—from a joint venture experiment to India's insurance powerhouse. The numbers tell a compelling story: SBI Life's AUM also continued to grow at 19% to Rs.4,41,678 crores as on December 31, 2024 from Rs. 3,71,410 crores as on December 31, 2023, with the debt-equity mix of 61:39. But beyond the financial metrics lies a more profound transformation—a company that has mastered the art of balancing scale with innovation, tradition with disruption, and growth with sustainability.

The scale achieved is staggering. The company has a diversified distribution network of 309,590 trained insurance professionals and wide presence with 1,086 offices across the country, comprising of strong bancassurance channel, agency channel and others comprising of corporate agents, brokers, Point of sale persons (POS), insurance marketing firms, web aggregators and direct business. This isn't just expansion—it's the creation of India's most comprehensive insurance distribution ecosystem.

SBI Life Insurance, one of the leading life insurers in the country registered a New Business Premium of Rs.26,256 crores for the period ended on 31st December, 2024 vis-a-vis Rs.26,000 crores for the period ended December 31, 2023. Regular premium has increased by 12% over the corresponding period ended on 31st December, 2023. This steady growth in a mature market demonstrates the strength of the franchise and execution capabilities.

The strategic focus has shifted decisively toward protection products. Establishing a clear focus on protection, SBI Life's protection new business premium stood at Rs.2,792 crores for the period ended December 31, 2024. Protection Individual new business premium stands at Rs.519 crores for the period ended December 31, 2024. This pivot from savings to protection represents both higher margins and genuine insurance value creation.

The most recent annual figures paint an even more impressive picture. Individual New Business Premium stands at Rs. 26,360 crores with 11% growth over previous year ended on 31st March, 2024. SBI Life's profit after tax stands at Rs. 2,413 crores for the year ended March 31, 2025 with a growth of 27% over previous year. The 27% profit growth significantly exceeding premium growth indicates improving operational efficiency and product mix optimization.

Financial strength remains robust. The company's solvency ratio continues to remain robust at 2.04 as on December 31, 2024 as against the regulatory requirement of 1.50. This capital buffer provides flexibility for growth investments while maintaining regulatory compliance. 94% of the debt investments are in AAA and Sovereign instruments, reflecting conservative investment philosophy appropriate for a life insurer.

The distribution evolution continues with partnership expansion. SBI Life strives to make insurance accessible to all, with its extensive presence across the country through its 1,086 offices, 25,949 employees, a large and productive network of about 241,251 agents, 77 corporate agents and 14 bancassurance partners with more than 41,000 partner branches, 144 brokers and other insurance marketing firms. The multi-channel approach ensures no customer segment is underserved.

Technology integration has moved from enabler to differentiator. The recent launch of AI initiatives demonstrates forward-thinking. SBI Life Insurance, one of India's most trusted private life insurers, launched the 1st edition of 'Hack-AI-thon'; a nationwide innovation initiative encouraging bright minds to leverage AI for transforming the future of life insurance. The initiative offers a unique platform for tech students, across India, to co-create solutions for business-critical challenges in insurance, with a sharp focus on transforming customer experience, product accessibility and fraud prevention.

The regional rounds of SBI Life's Hack-AI-thon saw an overwhelming response with over 7,500 registrations from tech students across India. This engagement with the broader ecosystem shows SBI Life isn't just adopting technology but actively shaping its development for insurance applications.

The market position remains dominant. Private Market leadership in New Business Premium of Rs.26,256 crores with 22.4% market share. This market share, maintained despite intense competition from both traditional players and new-age insurtechs, validates the business model's resilience.

Asset management has become a significant value driver. SBI Life's AUM also continued to grow at 15% to Rs. 4,48,039 crores as on March 31, 2025 from Rs. 3,88,923 crores as on March 31, 2024, with the debt-equity mix of 61:39. The AUM growth creates a virtuous cycle—higher assets generate more fee income, improving profitability without additional risk.

The focus on protection is yielding results. Establishing a clear focus on protection, SBI Life's protection new business premium stood at Rs. 4,095 crores for the year ended March 31, 2025. Protection Individual new business premium stands at Rs. 793 crores for the year ended March 31, 2025. Protection products, while smaller in premium, offer higher margins and lower capital requirements.

Corporate social responsibility has become integral to operations. SBI Life strongly encourages a culture of giving back to the society and has made substantial contribution in the areas of child education, healthcare, disaster relief and environmental upgrade. In 2024-25, the Company touched over 50,000 direct beneficiaries through various CSR interventions.

The quarterly performance shows consistency. SBI Life Insurance, the largest private sector life insurer, reported a 39 per cent year-on-year (YoY) rise in net profit to Rs 529.42 crore in July-September quarter of financial year 2025 (Q2FY25) from Rs 380.19 crore in the corresponding period a year ago. In April-September period (H1FY25), its net profit stood at Rs 1,049 crore, up 38 per cent YoY, compared to Rs 760 crore in H1FY24.

The value metrics are improving. Value of new business (VNB) -- present value of the future profits that are expected to come from new policies sold during a given year -- of the insurer dropped by 2.5 per cent YoY to Rs 1,450 crore in Q2 against Rs 1,487.4 crore in the year-ago period. In H1FY25, VNB of the insurer stood at Rs 2,420 crore, up 2 per cent from Rs 2,360 crore in the year ago period. While VNB growth has moderated, this reflects strategic choices to prioritize quality over quantity.

Partnership expansion continues strategically. SBI Life Insurance, among India's most trusted life insurers, has entered a strategic corporate agency partnership with AU Small Finance Bank, the country's largest Small Finance Bank. This collaboration aims to enhance access to comprehensive insurance solutions nationwide, supporting the government's 'Insurance for All by 2047' mission by extending financial protection to underserved and emerging markets across India.

Innovation remains a priority. Ravindra Sharma, Chief of Brand, Corporate Communication and CSR, SBI Life Insurance, said, "Innovation flourishes when diverse minds collaborate outside conventional boundaries. By inviting young talent to solve real life challenges—such as cybersecurity, personalization, and fraud prevention— SBI Life's Hack-AI-thon encourages future-ready solutions that are deeply aligned with the evolving needs of the insurance industry. This initiative reinforces our commitment to a collaborative, technology-led approach for enhancing customer experience."

The employee base has grown substantially. SBI Life strives to make insurance accessible to all, with its extensive presence across the country through its 1,110 offices, 26,355 employees, a large and productive network of about 240,304 agents, 60 corporate agents and 13 bancassurance partners with more than 41,000 partner branches, 141 brokers and other insurance marketing firms. This human capital, combined with technology, creates a formidable competitive advantage.

Looking at market valuation, Market Cap ₹ 1,80,042 Cr, SBI Life trades at substantial premium to book value, reflecting market confidence in future growth prospects. The consistent delivery of results has built investor trust.

The capital position provides strategic flexibility. Listed on the Bombay Stock Exchange ('BSE') and the National Stock Exchange ('NSE'), the company has an authorized capital of Rs. 20.0 billion and a paid-up capital of Rs. 10.0 billion. This capital base, combined with strong cash generation, enables both organic growth and potential acquisitions.

Risk management has evolved to address emerging challenges. Climate risk, cyber threats, and demographic shifts are being proactively managed. The conservative investment philosophy—94% in AAA-rated instruments—provides buffer against market volatility while generating stable returns.

The competitive landscape is intensifying. New-age insurtech players are targeting specific segments with innovative products. Traditional competitors are modernizing rapidly. International insurers are seeking greater market access. Yet SBI Life's comprehensive moat—distribution reach, brand trust, operational scale, and technological capabilities—remains defensible.

Regulatory changes continue shaping the industry. New guidelines on product design, distribution practices, and customer protection require constant adaptation. SBI Life's compliance infrastructure and regulatory relationships enable it to navigate these changes while maintaining business momentum.

The demographic dividend remains India's insurance opportunity. With insurance penetration still below 4% of GDP compared to global averages of 7%, the growth runway extends decades. Rising incomes, increasing awareness, and government push for financial inclusion create sustained demand for insurance products.

Environmental, Social, and Governance (ESG) considerations are becoming central. Beyond CSR activities, SBI Life is embedding sustainability in operations—paperless processes, green buildings, responsible investing. These initiatives resonate with younger customers and employees while reducing operational costs.

The future strategy balances multiple priorities. Geographic expansion into underserved markets continues. Product innovation focuses on simplified, transparent offerings. Distribution diversification reduces dependence on any single channel. Technology investments enhance both customer experience and operational efficiency.

International expansion possibilities are being explored. While currently India-focused, SBI Life's expertise in emerging market insurance could translate to other geographies. The large Indian diaspora provides natural entry points for international markets.

Partnership ecosystems are expanding beyond traditional financial services. Collaborations with healthcare providers, wellness platforms, and technology companies create new value propositions. These partnerships enable SBI Life to participate in customers' broader life journey, not just financial protection.

The leadership transition planning ensures continuity. With founding team members gradually retiring, next-generation leaders groomed internally are taking charge. This succession planning, rare in Indian companies, ensures strategic continuity while bringing fresh perspectives.

Employee engagement remains high despite industry challenges. Investment in training, career development, and work-life balance creates positive workplace culture. The ability to attract and retain talent in competitive market validates organizational health.

Customer-centricity drives operational decisions. From product design to claim settlement, customer needs take precedence. This focus, while sometimes sacrificing short-term profitability, builds long-term franchise value.

As SBI Life enters its 25th year, the company stands at an inflection point. The foundation is solid—market leadership, financial strength, operational excellence. The opportunities are massive—under-penetrated market, digital transformation, evolving customer needs. The execution capabilities are proven—consistent delivery across market cycles.

The modern era isn't just about maintaining success but reimagining possibilities. Can SBI Life become not just India's largest private insurer but a global insurance major? Can it transform from product manufacturer to comprehensive financial wellness provider? Can it balance shareholder returns with social impact? These questions will define the next chapter of SBI Life's journey.

IX. Playbook: Business & Investing Lessons

The SBI Life story offers a masterclass in building financial services businesses in emerging markets. The playbook that emerges from their journey contains lessons that transcend insurance, offering insights into joint ventures, distribution leverage, regulatory navigation, and long-term value creation. These aren't theoretical frameworks but battle-tested strategies that have survived market cycles, regulatory upheavals, and competitive onslaughts.

Lesson 1: Joint Venture Dynamics - The Art of Cultural Fusion

The SBI-BNP Paribas Cardif partnership demonstrates that successful joint ventures require more than complementary capabilities—they need cultural synthesis. SBI brought distribution and local market understanding; BNP Paribas brought technical expertise and global best practices. But the real success came from creating a third culture—neither purely public sector nor entirely private, neither completely Indian nor wholly French, but something unique that leveraged the best of both worlds.

The key was maintaining clear boundaries while enabling collaboration. BNP Paribas led product development and actuarial functions where technical expertise mattered most. SBI controlled distribution and customer relationships where local knowledge was crucial. Decision-making protocols were established upfront—strategic decisions required consensus, operational decisions followed functional leadership. This clarity prevented the paralysis that kills many joint ventures.

The equity structure—SBI maintaining majority control—wasn't just about regulatory compliance but about signaling. Customers trusted SBI Life because SBI's name came first and its stake was largest. But BNP Paribas's significant minority stake (22-24%) ensured their continued engagement. This balance—majority control with meaningful minority participation—became the template for successful bank-insurance joint ventures in India.

Lesson 2: Bancassurance as Competitive Moat

SBI Life proved that in financial services, distribution is destiny. The ability to reach customers cost-effectively at scale is the ultimate competitive advantage. While competitors spent thousands of rupees acquiring customers through agents or digital marketing, SBI Life accessed pre-qualified, trusting customers at near-zero acquisition cost through bank branches.

But bancassurance isn't just about access—it's about integration. SBI Life embedded insurance into the banking customer journey. Home loan applicants were offered mortgage protection before loan approval, making insurance feel like loan facilitation rather than cross-selling. Savings account holders received pre-approved insurance offers based on their transaction history. This contextual selling achieved conversion rates multiples higher than cold calling.

The moat deepened over time through data integration. SBI Life could underwrite risks better using banking transaction data. Premium collections through bank accounts reduced lapses. Claims could be settled directly into bank accounts. This operational integration created switching costs—customers found it convenient to keep insurance where they banked.

The network effects were powerful. Every new SBI branch became an SBI Life distribution point. Every new SBI customer became an SBI Life prospect. Every SBI relationship manager became an SBI Life advisor. This automatic scaling meant distribution costs as percentage of premium consistently declined, improving unit economics over time.

Lesson 3: Capital Efficiency in Insurance

Insurance is paradoxical—it's capital-intensive to start but capital-generative at scale. SBI Life mastered this transition. Initial capital was used judiciously—technology infrastructure over fancy offices, training over advertising, selective expansion over ubiquitous presence. This capital discipline meant achieving break-even faster than competitors who spent lavishly on customer acquisition.

The focus on regular premium products over single premium created recurring revenue streams with lower capital requirements. Protection products, while smaller in absolute premium, required minimal reserves and generated higher returns on capital. The product mix evolution—from capital-intensive savings products to capital-light protection products—improved capital efficiency without sacrificing growth.

Float management became a core competency. Insurance companies essentially get free leverage—premiums are collected upfront, claims paid later. SBI Life's conservative investment approach—94% in AAA-rated securities—might seem suboptimal but provided stable returns without risk of capital erosion. In insurance, avoiding losses matters more than maximizing gains.

The virtuous cycle of capital generation enabled self-funded growth. Unlike businesses that need constant capital infusion for expansion, SBI Life generated more capital than it could deploy, leading to consistent dividend payments. This capital efficiency made the business attractive to investors—growth without dilution.

Lesson 4: Distribution vs Manufacturing Paradigm

SBI Life's success challenges the conventional wisdom that manufacturing (product creation) drives value in financial services. Instead, distribution—the ability to reach and serve customers—proved more valuable. Products in insurance are largely commoditized; everyone offers term insurance, endowment plans, ULIPs. But not everyone can distribute them effectively.

The company structured itself as a distribution company that happens to manufacture insurance. The largest investments went into distribution infrastructure—branch network, agent training, digital platforms. Product development, while important, was standardized and efficient. This focus meant SBI Life could sell any product the market demanded rather than pushing products the company wanted to sell.

Distribution diversification became strategic imperative. While bancassurance remained dominant, agency, digital, and partnership channels were developed simultaneously. Each channel served different customer segments with tailored products and service models. This multi-channel approach reduced concentration risk and captured maximum market opportunity.

The distribution-first mindset influenced everything. Technology investments prioritized distributor enablement over product features. Marketing emphasized channel partner success over brand building. Incentive structures rewarded distribution productivity over product profitability. This alignment ensured organizational focus on what truly drove value.

Lesson 5: Regulatory Arbitrage and Compliance Excellence

Operating in a heavily regulated industry, SBI Life turned compliance from burden to advantage. By maintaining higher standards than required, the company built regulatory goodwill that provided flexibility during critical moments. When regulations changed—like the 2010 ULIP guidelines—SBI Life adapted faster because their practices already exceeded minimum requirements.