SAREGAMA: The Story of India's Oldest Music Label's Digital Renaissance

I. Introduction & Episode Roadmap

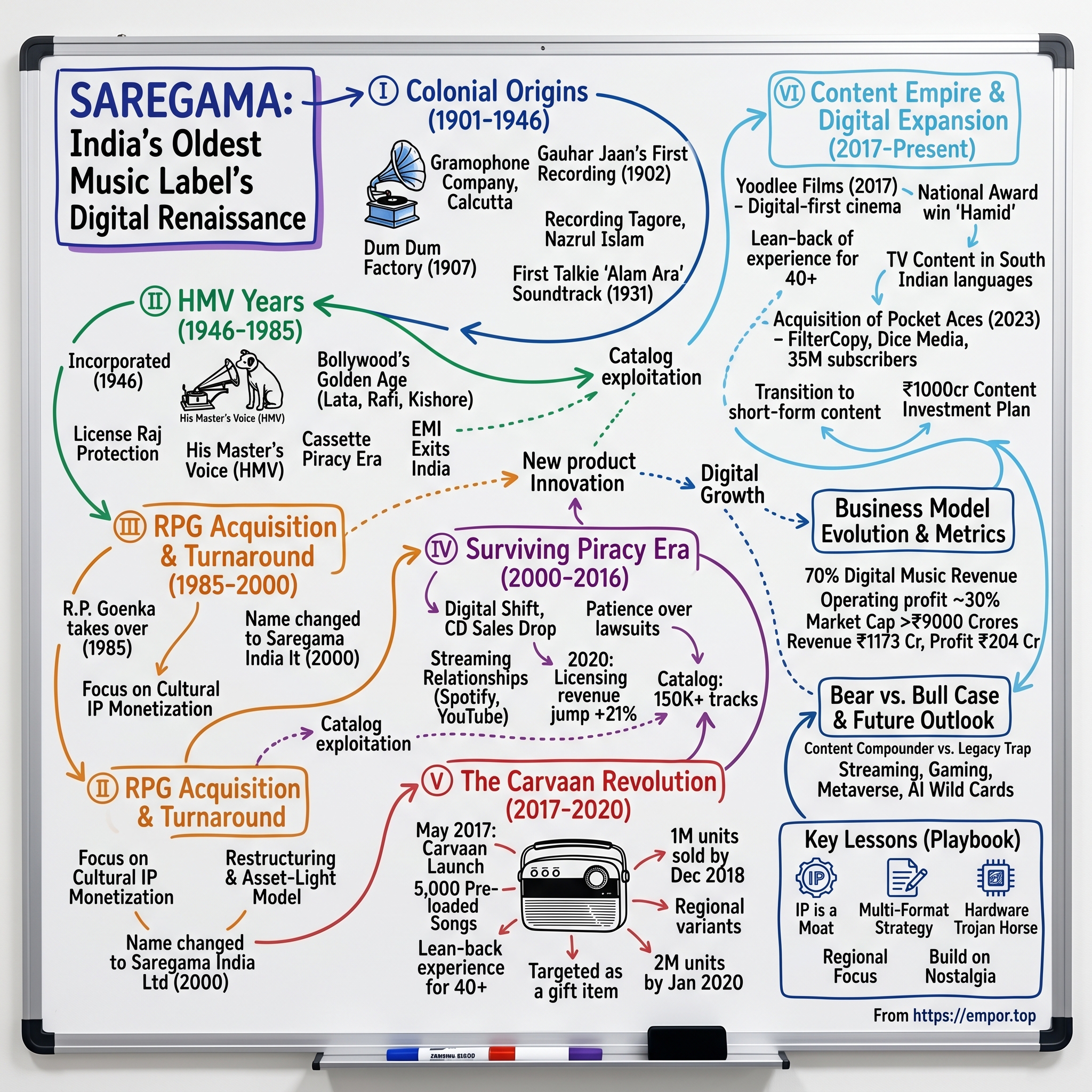

Picture this: It's 2017, and in the gleaming glass towers of Mumbai's business district, a 116-year-old company is about to launch a product that defies every rule of the digital age. No apps, no algorithms, no cloud connectivity. Just a wooden box with 5,000 pre-loaded Hindi songs and physical buttons your grandmother could operate with her eyes closed. The Saregama Carvaan would go on to sell over a million units in two years, turning a struggling music catalog company into one of India's most fascinating turnaround stories.

How did a company that started recording India's first gramophone records in 1902—when the British Raj still ruled and electricity was a luxury—transform itself into a digital content powerhouse worth over ₹9,000 crores today? How did the same company that once held a near-monopoly on Indian music through physical records navigate the piracy apocalypse of the 2000s, the streaming revolution, and emerge stronger on the other side?

This is the story of Saregama India—formerly The Gramophone Company of India, formerly HMV India—a company that has reinvented itself more times than Madonna. It's a story that spans from British colonial recording studios to Bollywood's golden age, from the collapse of physical media to the unexpected hardware renaissance of the Carvaan, from pure-play music licensing to becoming India's only entertainment company with IP across music, films, TV, and digital content.

The major themes we'll explore read like a playbook for heritage companies in the digital age: How do you monetize 120 years of cultural IP when your customers have moved from gramophones to Spotify? How do you disrupt yourself before others disrupt you? And perhaps most intriguingly—how do you use nostalgia not as a crutch but as a springboard for innovation?

We'll trace Saregama's journey through distinct eras: the colonial origins when recording an Indian voice was revolutionary; the HMV years when the company essentially soundtracked independent India's cultural awakening; the RPG acquisition that saved it from bankruptcy; the digital transition that nearly killed it; and the remarkable renaissance that followed. Along the way, we'll unpack the Carvaan phenomenon—a masterclass in product-market fit that Silicon Valley couldn't have predicted—and examine how a company that owns roughly 50% of all music ever recorded in India is positioning itself for the next century.

II. The Gramophone Era: British Roots & Colonial Beginnings (1901–1946)

The year was 1901, and in the bustling port city of Calcutta (now Kolkata), British entrepreneurs were setting up what would become India's first recording company. The Gramophone Company, headquartered in London, had already conquered Europe with its revolutionary technology—capturing human voices on wax cylinders and flat discs. But India, with its cacophony of languages, its classical music traditions stretching back millennia, and its vast untapped market of 300 million people, presented both an irresistible opportunity and a formidable challenge.

The company's first major breakthrough came in 1902 when they convinced Gauhar Jaan, one of India's most celebrated classical singers, to step into their makeshift recording studio. Gauhar Jaan was initially skeptical—the idea of capturing her voice in a machine seemed almost sacrilegious to traditional musicians. But when she finally agreed, she ended her three-minute performance with a declaration that would become legendary: "My name is Gauhar Jaan!" This wasn't vanity; it was practicality. In an era before album covers and liner notes, artists needed to identify themselves on the recording itself. What happened next was transformative for the Indian recording industry. In 1907, a record factory was started in Dum Dum in Calcutta, the first outside UK. This wasn't just a pressing plant—it was a statement. The Gramophone Company was betting big on India, establishing manufacturing capabilities that would make India self-sufficient in record production. The facility in Dum Dum would become legendary, not just for its output but for what it represented: India's entry into the modern industrial age through the medium of music. The company's technical capabilities continued to evolve through the 1920s. Saregama's recording studio, called Dum Dum studio, was built in 1928 in Calcutta. This wasn't just any recording facility—it would become one of the most storied studios in Southeast Asia. Nobel Laureate Rabindranath Tagore had recorded his songs and poems in his own voice at this studio. Rebel poet Kazi Nazrul Islam's voice was also recorded here. These weren't just commercial recordings; they were capturing the voice of India's cultural renaissance.

Then came 1931, a watershed moment not just for the company but for Indian cinema itself. The soundtrack of Alam Ara was released by Saregama and has a total of seven songs. Though the now-lost film didn't mention a composer or lyricist in its credits, later media reports and Saregama's website suggest that B. Irani and Feroz Shah Mistry were the composers. The film, India's first talkie, premiered on March 14, 1931, and created pandemonium. Police had to be called to control the crowds desperate to hear actors speak and sing on screen for the first time.

What made this period remarkable wasn't just the technological innovation but the cultural bridging the company achieved. The Gramophone Company was recording everything from classical Hindustani ragas to devotional bhajans, from Bengali folk songs to Tamil poetry. They were creating an audio archive of a civilization, capturing voices that would otherwise have been lost to time. By the 1940s, the company had established itself as the preeminent force in Indian recorded music.

The timing of their dominance was no accident. As India moved toward independence, there was a growing hunger for cultural expression, for Indian voices telling Indian stories. The Gramophone Company, despite its British ownership, had become fundamentally Indian in its soul. Its catalogs read like a who's who of Indian music—from the classical maestros to the emerging film music that would soon dominate popular culture.

By 1946, as the British prepared to leave India, the company faced its own transition. The colonial era was ending, but the foundation had been laid for something far greater—a music empire that would soundtrack independent India's journey into modernity.

III. The HMV Years: Independence to EMI Control (1946–1985)

On August 13, 1946—just two days before India's independence—The Gramophone Company was incorporated as The Gramophone Co. (India) Limited, a prescient move that would position it perfectly for the new nation's cultural explosion. On 13 August 1946, it was incorporated as a Private Limited company with the name of 'The Gramophone Co. It was converted into a public company on 28 October 1968 and consequently the name of the company was changed to 'The Gramophone Company of India Limited'.

The company, now part of the global EMI empire, wielded the most powerful brand in music: His Master's Voice, with its iconic logo of Nipper the dog listening to a gramophone. This wasn't just a trademark—it was a symbol of authenticity and quality that resonated deeply with Indian audiences. For nearly four decades, HMV would become synonymous with music itself in India. The 1950s and 1960s were HMV's golden age in India—a period when the company didn't just dominate the market but essentially was the market. From 1909 to 2003, the company retailed its music products—records, cassettes, and compact discs—under the His Master's Voice (HMV) brand, using the iconic logo of a dog named Nipper listening to a gramophone. During this era, if you bought music in India, you bought HMV.

The company's stranglehold on Bollywood music was particularly crucial. The great playback singers of the era—Lata Mangeshkar, Mohammed Rafi, Kishore Kumar, Asha Bhosle—all recorded for HMV. The legendary music directors like Naushad, S.D. Burman, and R.D. Burman created their masterpieces in HMV studios. The company wasn't just recording music; it was documenting the soundtrack of a nation finding its voice after independence.

What's remarkable about this period is how HMV operated with the efficiency of a monopoly but the soul of a cultural institution. They released everything from classical ragas to film songs, from devotional bhajans to regional folk music. The company's catalogs from this era read like an encyclopedia of Indian music—they were preserving culture while selling entertainment.

The business model was elegantly simple: control the recording, control the manufacturing, control the distribution. HMV owned pressing plants that churned out millions of records. They had exclusive contracts with virtually every major artist. Their distribution network reached from metropolitan cities to small towns. In an era before television became widespread, HMV records were how most Indians consumed entertainment at home.

But beneath this seemingly invincible empire, cracks were beginning to show. The License Raj—India's complex system of licenses and regulations—protected HMV from competition but also made it complacent. Innovation slowed. Costs ballooned. The company, cushioned by its monopoly, failed to anticipate the seismic shifts that would come with economic liberalization.

By the early 1980s, HMV was bleeding money. The advent of cassette tapes had democratized music piracy—suddenly, anyone with two cassette players could become a music distributor. The company's high cost structure, built for a monopoly era, couldn't compete with nimble pirates operating from Mumbai's back alleys. EMI, facing its own global challenges, decided it was time to cut its losses in India. The stage was set for one of the most dramatic corporate turnarounds in Indian business history.

IV. The RPG Acquisition: Turnaround Under Indian Ownership (1985–2000)

In 1985, when RPG Group took over the company from EMI when the company's financial health was poor, the acquisition seemed more like a rescue mission than a strategic investment. Rama Prasad Goenka, already known as India's "takeover tycoon," saw something in the struggling music company that others missed—not just a catalog of old songs, but a treasure trove of cultural IP waiting to be monetized in new ways.

Takes over Gramophone Company of India Ltd, now Saregama India in 1985, R.P. Goenka brought his characteristic turnaround expertise to bear. The company was hemorrhaging money, its manufacturing facilities were outdated, and cassette piracy was eating into legitimate sales. But Goenka understood that the real value lay not in the physical infrastructure but in the intellectual property—those hundreds of thousands of recordings that represented the musical memory of a nation.

The initial years under RPG ownership were about stabilization rather than transformation. Even after EMI sold the company to the RP-Sanjiv Goenka Group in 1985, Saregama continued to use the HMV name and symbol under a licensing agreement. This continuity was crucial—the HMV brand still commanded respect and nostalgia among Indian consumers, even as the business model underneath was being quietly revolutionized.

What Goenka brought to the table was a fundamentally different approach to the music business. Rather than seeing it as a manufacturing operation that happened to own content, he saw it as a content company that happened to do some manufacturing. This shift in perspective would prove prescient as the industry moved from physical to digital formats.

The RPG team began the unglamorous work of restructuring. They shuttered unprofitable retail stores, streamlined the distribution network, and most importantly, began to think creatively about how to monetize the vast catalog. They started licensing music for advertisements, supplied content to All India Radio, and explored new revenue streams that didn't depend on selling physical products.

Through the 1990s, as India liberalized its economy, the company found itself in an increasingly competitive landscape. New players like T-Series were aggressively acquiring film music rights, often outbidding the erstwhile monopolist. But rather than engage in expensive bidding wars for new content, RPG doubled down on exploiting their heritage catalog.

The masterstroke came on December 16, 2000, when the name of the company was changed from The Gramophone Company of India Limited to its current name, Saregama India Limited. This wasn't just a rebranding exercise—it was a declaration of independence from the colonial past and a signal that the company was ready for the digital age. "Saregama" referenced the first four notes of the Indian musical scale, immediately establishing the company's Indian identity while maintaining continuity with its heritage.

The timing of this transformation was critical. This arrangement ended in 2003, when EMI divested the rights to the HMV trademark to the British retailer of the same name. By then, Saregama had already established its own identity, making the loss of the HMV brand less traumatic than it might have been a decade earlier.

What the RPG era accomplished was remarkable: they took a company built for the gramophone age and prepared it for the internet era. They transformed a manufacturing-heavy operation into an asset-light licensing business. Most importantly, they recognized that in the content business, old doesn't mean obsolete—it means evergreen.

V. The Digital Transition: Surviving the Piracy Era (2000–2016)

The early 2000s were the music industry's darkest hour globally, and India was no exception. Napster had shown the world how to share music for free, and in India's chaotic markets, pirated CDs and MP3s were being sold for a fraction of legitimate prices. For Saregama, sitting on what was essentially a goldmine of content, this period could have been catastrophic.

The numbers were brutal. Physical sales, which had already been declining due to cassette piracy, fell off a cliff. The company watched helplessly as their songs—meticulously recorded over a century—were being distributed freely on peer-to-peer networks and burned onto counterfeit CDs sold at traffic signals for 20 rupees.

But Saregama had an advantage that Western music labels lacked: patience born from longevity. While Universal and Sony were suing teenagers for downloading music, Saregama quietly began building relationships with the very platforms that were disrupting them. They understood a fundamental truth: you can't fight technology; you have to embrace it.

The company's catalog, spanning film and non-film music, including Carnatic, Hindustani classical, devotional, folk, and other genres, in over 23 Indian languages, became their secret weapon. Streaming platforms needed content, especially local content that would differentiate them in the Indian market. Saregama had more of it than anyone else. The early streaming deals were not particularly lucrative—margins were thin and the platforms held most of the negotiating power. But Saregama played the long game. Its music is distributed on music streaming services including Spotify, Gaana, YouTube Music, Hungama, Apple Music, and others. Each platform needed authentic Indian content to differentiate itself, and Saregama had the deepest catalog in the country.

The Spotify saga perfectly encapsulates the dynamics of this era. In April 2019, shortly after Spotify's India launch, Saregama filed a copyright infringement case and Spotify had to remove over 100,000 Saregama-owned music tracks from its platform. A year later, in May 2020, they struck a licensing deal. This wasn't just business negotiation—it was Saregama demonstrating that its catalog was indispensable.

What's remarkable about this period is how Saregama transformed from a company fighting piracy to one that turned digital disruption into its primary growth engine. During the COVID year, the company's music licensing revenue—most of which comes from streaming services—jumped by a whopping 21% to Rs 236.1 cr. While hardware sales collapsed during lockdowns, streaming revenue soared as trapped-at-home Indians turned to music for comfort.

As of 2024, Saregama's catalogue includes over 150,000 tracks. The company that once sold physical records for 10 rupees was now earning fractions of pennies per stream—but with billions of streams across multiple platforms, those fractions added up. More importantly, the marginal cost of each additional stream was essentially zero. This was the beauty of the catalog business: create once, monetize forever.

The company also began exploring new licensing opportunities beyond traditional streaming. They started licensing music for social media platforms, for use in reels and stories. They provided music for advertisements, for films, for web series. Every new platform that emerged needed content, and Saregama was ready with a century's worth of it.

But by 2016, despite the streaming deals and diversified licensing, something was still missing. Revenue was growing but not explosively. The company needed a breakthrough product, something that would capture the imagination of consumers and investors alike. What they came up with would defy every trend in consumer technology.

VI. The Carvaan Revolution: Hardware in a Software World (2017–2020)

In May 2017, when Saregama launched Carvaan, nobody in the technology world understood it. Here was a company launching a wooden box with physical buttons and no touchscreen, no apps, no WiFi—just 5,000 pre-loaded Hindi songs and an FM radio. Tech reviewers called it "half a decade behind in technology." Silicon Valley would have laughed it out of the room.

But Vikram Mehra, Saregama's MD, understood something the tech world didn't: technology isn't always the answer. Launched in May this year, the product sold 90,000 units between July and September, and following that unexpected success, Saregama is, conservatively, targeting another 200,000 units in the next six months. The Carvaan would go on to become one of the most unlikely consumer electronics success stories of the decade.

The insight behind Carvaan was deceptively simple yet profound. "Our research showed that a majority of that age group had simply stopped listening to music and it was ironic because when this population was young, there was no social media. All they had was the radio but advancements in technology took that away from them," the company discovered. The 40-plus generation in India, who had grown up with Lata Mangeshkar and Kishore Kumar, had been left behind by Spotify's algorithms and YouTube's interface.

The unique proposition of this product is that even today in the times when digital music consumption is the order of the day, Carvaan attempts to give the older generation a lean-back, uncomplicated ala 70s Vividh Bharti music listening experience. Carvaan is a perfect blend of digital technology and retro form factor. No passwords, no subscriptions, no searching—just turn a knob and music plays.

But the real genius wasn't in the product design; it was in the go-to-market strategy. Carvaan is being positioned as a gifting item. As mentioned above, the buyer and the user are two different segments for Saregama Carvaan. The pitch—"Mummy Papa ke liye best gift"—targeted millennials looking for something to give their parents. The company understood that while the users might be tech-averse 60-year-olds, the buyers were their tech-savvy children wrestling with gift-giving guilt.

The numbers tell a story of explosive growth that caught everyone, including Saregama, by surprise. Music revenues for Saregama increased to Rs 73.20 crores for the quarter, up 134% year on year. 2018 was a breakthrough year for Saregama as it recorded 297K units sold in only the third quarter coinciding with Diwali shopping season. By December 2018, they had crossed the one million mark.

The company rapidly iterated on the success. Variants of Carvaan have been introduced in multiple regional languages, including Punjabi, Tamil, Bengali, and Marathi. They launched Carvaan Mini at Rs 2,490 for the more price-conscious segment. Carvaan Premium came with app connectivity for those wanting a bridge between old and new. By January 2020, they had sold two million units.

What Carvaan proved was revolutionary for consumer electronics: sometimes the best interface is no interface. Sometimes the most advanced technology is the technology that disappears. And sometimes, in a world racing toward the future, the biggest opportunity lies in serving those left behind.

The financial impact was transformative. The last five years have seen sales of over INR 2000 crores from Carvaan alone. But more importantly, Carvaan changed the perception of Saregama from a legacy music company to an innovative consumer brand. The stock market took notice—the company's valuation began its upward trajectory that would eventually take it past ₹9,000 crores.

VII. Content Empire: Films, TV & Digital Expansion (2017–Present)

While Carvaan was capturing headlines and flying off shelves, Saregama was quietly building something even more ambitious: a multi-format content empire that would position it as India's only entertainment company with IP across every medium. The year 2017 wasn't just about launching a retro music player; it was about recognizing that content was entering a golden age, and Saregama had the DNA to play across the entire spectrum. Yoodlee Films is the film production division of Saregama India, launched in 2017 and based in Mumbai. The studio focuses on content-driven cinema across languages and formats, with a strategy centred on digital-first releases. The timing was perfect—Netflix had just entered India, Amazon Prime Video was ramping up, and there was a desperate hunger for quality Indian content beyond the typical Bollywood formula.

Under the leadership of Siddharth Anand Kumar, Yoodlee positioned itself as the antithesis of mainstream Bollywood. Their films are shot at real locations with a maximum duration not more than 120 minutes. No vanity vans, no star tantrums, no 200-crore budgets. Just stories that needed to be told, efficiently produced and expertly distributed.

The results speak for themselves. Its film Hamid won two National Film Awards at the 66th National Film Awards, including Best Feature Film in Urdu and Best Child Artist for Talha Arshad Reshi. The film, about a Kashmiri boy trying to call God on his father's phone after his disappearance, showed that Yoodlee wasn't just making content—it was making cinema that mattered.

As of 2024, Yoodlee Films has produced 30 films, several of which have been released on platforms such as Netflix, JioHotstar, and ZEE5. We have 10 films on Netflix, 3 out of which are Netflix Originals, the company reported. This wasn't just about quantity; it was about creating a new model for Indian cinema—one where artistic integrity and commercial viability weren't mutually exclusive.

But films were just one piece of the content puzzle. Saregama produces content for TV channels in Tamil, Telugu, Kannada and Malayalam. The company understood that India's entertainment consumption wasn't monolithic—it was deeply regional, with each language market having its own stars, stories, and sensibilities. The real game-changer came in 2023. That same year, it acquired a majority stake in Pocket Aces Pictures Pvt. Ltd., a digital content and influencer marketing company behind brands like FilterCopy and Dice Media. The acquisition was valued at approximately INR 174 crores initially, with Saregama acquiring 51.8% and later increasing its stake to over 90%.

Pocket Aces wasn't just another acquisition—it was Saregama's bridge to the next generation. Pocket Aces has 35 million subscribers and clocks 700 million video views monthly across social media platforms with its channels FilterCopy (short fiction), Gobble (lifestyle), Nutshell (infotainment). This was the audience that had never bought a CD, never owned a cassette, and certainly never seen a gramophone. Yet they were the future of content consumption.

"We can see a change coming in content consumption with a marked preference for short-form over long-form, Pocket Aces is the secret sauce that will help us transition to this newer form of content," Saregama stated in its annual report. The synergies were obvious: Saregama had the music, Pocket Aces had the distribution and the cultural understanding of Gen Z.

In 2023, the company launched Saregama Talent, a vertical focused on artist management and promotion. This wasn't just about managing established artists but about creating the next generation of Indian music stars. The company that had recorded Lata Mangeshkar's first songs was now managing Instagram influencers with millions of followers.

The investment thesis was clear: Saregama also announced a plan to invest ₹1,000 crore over three years to acquire music content across multiple Indian languages. This wasn't defensive spending to protect market share—it was aggressive expansion to own the future of Indian entertainment.

What's remarkable about this content empire strategy is its comprehensiveness. Saregama is now India's only entertainment company with IP across all media channels—from century-old recordings to TikTok-style reels, from National Award-winning films to YouTube sketches, from devotional bhajans to web series on Netflix. They're not betting on one format or one platform; they're betting on the enduring power of storytelling, regardless of medium.

VIII. Business Model Evolution & Financial Performance

The transformation of Saregama's business model over the past two decades reads like a masterclass in corporate reinvention. From a company that made money by pressing vinyl records to one that generates revenue from billions of micro-transactions across streaming platforms, the evolution has been nothing short of remarkable. The numbers tell a story of remarkable transformation. Market Cap: 9,260 Crore, Revenue: 1,173 Cr, Profit: 204 Cr. But these headline figures mask the more interesting story of how the revenue is generated and where it's heading.

The shift in revenue composition has been dramatic. In the early 2000s, nearly 100% of revenue came from physical sales. Today, digital constitutes 70% of its music revenues. The company has essentially rebuilt itself from the ground up while maintaining profitability throughout the transition—a feat few legacy media companies globally have managed.

Music revenues increased to Rs 73.20 crores in Q2 FY18, up 134% YoY—this wasn't just growth; it was an explosion driven by the twin engines of streaming licensing and Carvaan sales. The beauty of the model is its diversification: when Carvaan sales slowed during COVID, streaming revenues soared. When physical events returned, live performance revenues kicked in.

The licensing business has become the crown jewel of the operation. With virtually zero marginal cost for each additional stream, every new platform, every new user, every new play translates almost directly to the bottom line. The company owns ~50% of all the music ever recorded in India—this isn't just a catalog; it's a toll booth on Indian cultural consumption.

The financial metrics reflect this asset-light transformation. Operating profit margins witnessed a fall and down at 30.1% in FY24 as against 30.0% in FY23—remarkably stable for a company undergoing such fundamental change. The company is debt-free, generating consistent cash flows, and reinvesting aggressively in content acquisition.

But there's a strategic shift happening that the numbers are just beginning to capture. Investments in content grew at 62% to touch Rs 316.0 crore, highest ever in its history, well on course to invest Rs 1,000 crore between FY25, FY26 and FY27. This isn't defensive spending; it's offensive. Saregama is transitioning from being primarily a catalog company to being a contemporary content creator.

The acquisition of Pocket Aces adds another dimension to the financial story. Revenue from Operations was Rs. 104 cr in FY23, growing at 34% CAGR over the last 4 years. More importantly, it brings a distribution network of 95 million young followers—an audience that Saregama's traditional business could never reach.

What's particularly impressive is the company's ability to maintain profitability while investing heavily in growth. Company has a low return on equity of 13.6% over last 3 years—this might seem concerning, but it reflects the massive cash position and the transitional nature of the business. As the new investments in content and acquisitions mature, these returns should improve significantly.

The market has noticed. From a low of around ₹100 in 2016, the stock has surged to over ₹500, with the market cap crossing ₹9,000 crores. But this might just be the beginning. With streaming still in its infancy in India, the shift to paid subscriptions just starting, and new content formats emerging constantly, Saregama's multiple revenue streams position it uniquely for the next decade.

IX. Playbook: Lessons in IP Monetization & Reinvention

If you were to write a business school case on how to transform a legacy company for the digital age, Saregama would be the textbook example. The playbook they've developed isn't just about survival—it's about thriving by understanding the timeless value of content and the ever-changing ways to deliver it.

Lesson 1: Heritage IP is a Moat, Not a Burden

Most legacy media companies see their old catalogs as dusty archives—nice to have but increasingly irrelevant. Saregama flipped this completely. They recognized that in a world of infinite content, curation becomes valuable. Their 150,000+ tracks aren't just songs; they're emotional touchpoints for billions of Indians. Every wedding needs "Din Shagna Da," every heartbreak has its Mukesh song, every celebration its Kishore Kumar anthem. This isn't content that ages; it's content that appreciates.

Lesson 2: Multi-Format Strategy Across Generations

Saregama doesn't have one customer; it has five generations of them. The 70-year-old listening to Lata Mangeshkar on Carvaan, the 45-year-old streaming Mohammed Rafi on Spotify during their commute, the 25-year-old discovering remixes on Instagram Reels, the teenager watching Yoodlee films on Netflix—each requires a different product, different marketing, different distribution. Saregama built capabilities for all of them.

Lesson 3: Hardware as a Trojan Horse

The Carvaan insight was profound: sometimes the best digital strategy is analog. By packaging digital content in a physical, familiar form factor, Saregama created a bridge product for the digital-resistant generation. But more cleverly, Carvaan became a subscription business in disguise—customers paid upfront for a lifetime of content access. No churn, no customer acquisition costs, no pricing pressure.

Lesson 4: Niche Marketing in Mass Markets

India isn't a market; it's 30 markets speaking different languages, consuming different content, celebrating different festivals. Saregama's regional strategy—Tamil Carvaan, Bengali content, Marathi films—recognizes this. They don't try to force-fit Hindi content everywhere. They create locally, market locally, but leverage their national infrastructure and capabilities.

Lesson 5: Timing and Cultural Insights

Every successful Saregama move has been about reading cultural shifts correctly. Launching Yoodlee when OTT platforms were hungry for content. Acquiring Pocket Aces when short-form video was exploding. Pushing into live events post-COVID when people were desperate for experiences. This isn't luck; it's pattern recognition born from being deeply embedded in Indian culture for over a century.

Lesson 6: Building on Nostalgia While Investing in the Future

The masterstroke is how Saregama uses its heritage as a launching pad, not a crutch. The cash flows from the old catalog fund new music acquisition. The brand trust from HMV days gives credibility to Yoodlee Films. The Carvaan customer database becomes a target for new products. It's a virtuous cycle where the past funds the future.

Lesson 7: Managing Brand Transitions

The shift from HMV to Saregama could have been traumatic. HMV had near-universal recognition; Saregama was unknown. But they managed it brilliantly—maintaining continuity where it mattered (the music), while signaling change where it was needed (the company's Indian identity). Today, few remember HMV, but everyone knows Saregama.

Lesson 8: The Platform Agnostic Approach

Saregama doesn't bet on platforms; it bets on content. When CDs died, they moved to digital. When downloads died, they moved to streaming. When streaming commoditized, they moved to social media. Tomorrow, if music moves to the metaverse or neural implants, Saregama will be there. The platform is just plumbing; content is the water.

Lesson 9: Vertical Integration Where It Matters

Unlike Western music companies that outsourced everything, Saregama kept critical capabilities in-house. They own their catalog, manage their artists, produce their content, and increasingly, control distribution through owned platforms. But they're not religious about it—they'll partner (Spotify), acquire (Pocket Aces), or build (Carvaan) depending on what makes sense.

Lesson 10: The Power of Patient Capital

Being part of the RP-Sanjiv Goenka Group gave Saregama something precious: time. They could afford to experiment with Carvaan, invest in films that might not work, acquire companies that need fixing. This patient capital, rare in today's quarterly-earnings-obsessed world, allowed for strategic moves that wouldn't pay off immediately but would compound over time.

The Saregama playbook isn't just about music or even media. It's about understanding that in the attention economy, content is currency, distribution is temporary, and the companies that win are those that can shape-shift while maintaining their core. It's about recognizing that technology changes everything except human nature—we still want stories, songs, and shared experiences. The medium changes; the need doesn't.

X. Competition & Market Dynamics

In the blood sport that is the Indian music industry, Saregama occupies a unique position—neither the biggest nor the loudest, but arguably the smartest player on the field. Understanding its competitive position requires understanding that this isn't one game but multiple games being played simultaneously.

The Catalog Wars

In the heritage music space, Saregama is the undisputed king. T-Series, despite being India's largest music label by revenue, started only in 1983. Sony Music India, while formidable, focuses primarily on contemporary content. Zee Music, launched in 2014, is practically an infant in comparison. When it comes to music from before 1990, Saregama owns the conversation. This isn't just about quantity—it's about owning the songs that defined generations.

The New Music Battle

Here, the dynamics flip completely. T-Series dominates with its stranglehold on Bollywood music, reportedly holding 35% market share in new releases. Sony Music and Zee Music aggressively bid for film music rights, often paying astronomical advances. Saregama's strategy has been surgical—acquiring music in regional languages where competition is less intense and economics more favorable. They're not trying to win every battle; they're choosing battles they can win profitably.

The Streaming Platform Dynamics

The power dynamic with streaming platforms is fascinating. Spotify, Amazon Music, and Apple Music need Saregama's catalog for credibility in India—imagine a music service without Kishore Kumar or Lata Mangeshkar. But Saregama needs these platforms for distribution. This mutual dependence creates a delicate balance. Saregama's advantage? As platforms proliferate—YouTube Music, Gaana, JioSaavn—its negotiating power increases.

The Creator Economy Threat and Opportunity

The biggest disruption isn't coming from traditional competitors but from individual creators. A kid with a laptop can now create, distribute, and monetize music without any label. Platforms like Instagram and YouTube have democratized music creation. Saregama's response has been clever: instead of fighting this trend, they're embracing it through Saregama Talent and the Pocket Aces acquisition. They're becoming the infrastructure for creators, not their competition.

Regional Market Dynamics

India's music market isn't monolithic—it's deeply fragmented by language. In Tamil music, Saregama competes with Think Music and Aditya Music. In Telugu, it's Aditya Music and Lahari Music. In Punjabi, it's Speed Records and White Hill Music. Each market has its own dynamics, star system, and consumer preferences. Saregama's national presence gives it economies of scale these regional players lack, while its local teams provide the cultural understanding national players miss.

The Unique Positioning

India's only entertainment company with IP across all media channels—this isn't marketing speak; it's a genuine differentiator. T-Series makes music and films but doesn't have Saregama's television production. Sony has music and television but lacks Saregama's heritage catalog. Zee has television and films but limited music presence. Netflix and Amazon have content but don't own IP. Saregama's diversification isn't just defensive—it creates synergies others can't replicate.

International Expansion Possibilities

The 30 million Indian diaspora represents a massive untapped opportunity. Currently, international revenues are minimal, but Indians in Silicon Valley, London, Dubai, and Toronto are hungry for cultural content. Saregama's challenge is distribution and marketing in these markets. The Carvaan has seen some success internationally, but the real opportunity lies in digital distribution tailored for NRIs who want both nostalgia and contemporary content.

The Platform vs. Content Debate

There's an ongoing battle between platforms (who have users) and content owners (who have IP). Globally, platforms have been winning—Spotify's market cap dwarfs any music label. But India might be different. With multiple competing platforms and relatively low subscription rates, content owners maintain leverage. Saregama's strategy of being platform-agnostic while building its own distribution (through Pocket Aces' 95 million followers) hedges both sides of this bet.

Competitive Advantages That Matter

Saregama's real moat isn't just its catalog—it's the combination of catalog depth, multi-format capabilities, patient capital, and cultural understanding built over 120 years. A new entrant can't replicate this overnight. Even deep-pocketed tech giants would struggle to acquire comparable content given how fragmented ownership is. The company's ability to operate across the value chain—from artist development to content creation to distribution—creates a flywheel effect competitors struggle to match.

The competitive landscape is evolving rapidly. Voice assistants are changing music discovery. Short-form video is redefining music consumption. Gaming is emerging as a new frontier for music monetization. AI might soon create music indistinguishable from human composition. In this chaos, Saregama's diversified approach—old and new, physical and digital, owned and licensed—positions it not to dominate any single battlefield but to profit from all of them.

XI. Bear vs. Bull Case & Future Outlook

Bull Case: The Content Compounder

The bulls see Saregama as India's answer to Universal Music Group—a content powerhouse perfectly positioned for India's digital explosion. Start with the macro: India's digital entertainment market is expected to grow from $30 billion to $100 billion by 2030. Music streaming penetration is still under 10%, compared to 30%+ in developed markets. As India's 600 million internet users mature and payment infrastructure improves, the shift from free to paid subscriptions is inevitable.

The catalog alone justifies optimism. Owning ~50% of all Indian music ever recorded is like owning beachfront property—they're not making any more of it. Every new platform, every new use case (gaming, metaverse, AI training), every new geography needs this content. The marginal cost of monetization is near zero, making this almost pure profit growth.

The Pocket Aces acquisition transforms Saregama from a music company to a content ecosystem. With 95 million young followers and expertise in short-form content, Saregama can now monetize across the entire content value chain. They can create music, produce videos, manage influencers, and distribute directly—a full-stack capability unique in India.

Management execution has been stellar. Every major move—Carvaan, Yoodlee, Pocket Aces—has worked. The ₹1,000 crore content investment plan shows ambition backed by capital. The company's ability to maintain 30%+ margins while investing aggressively demonstrates operational excellence.

The optionality is enormous. AI-powered music personalization, virtual concerts in the metaverse, music NFTs, expansion into global markets—each could be a billion-dollar opportunity. The company's proven ability to adapt (from gramophones to streaming) suggests they'll capture these opportunities as they emerge.

Bear Case: The Legacy Trap

The bears see structural challenges that financial engineering can't solve. Low ROE of 13.6% over last 3 years is a red flag—this is a business generating mediocre returns on shareholder capital. For a company trading at 45x P/E, these returns are concerning.

The dependence on the old catalog is problematic. Yes, it's valuable, but is "Lag Ja Gale" really going to drive growth for the next decade? Young Indians are increasingly consuming global content—K-pop, Latin music, English podcasts. Saregama's heritage catalog becomes less relevant with each generation.

New content creation remains subscale. Despite the ₹1,000 crore investment plan, Saregama is still a minor player in new music. T-Series, Sony, and Zee have deeper pockets and stronger relationships with Bollywood. In the winner-takes-all dynamics of hit content, being fourth or fifth is a recipe for mediocrity.

Streaming platform bargaining power is increasing. As Spotify and YouTube consolidate users, they'll squeeze music labels on rates. We've seen this globally—streaming saved the music industry but captured most of the value. India might follow the same pattern, leaving content owners with crumbs.

The hardware success of Carvaan may not be repeatable. It was a perfect product for a specific moment—that moment has passed. Attempts to replicate with Carvaan variants have seen diminishing returns. The company risks fighting the last war while missing the next one.

Competition is intensifying from unexpected quarters. ByteDance (TikTok's parent) is investing heavily in Indian music. Amazon and Netflix are backward-integrating into music production. Tech giants have infinitely deeper pockets and superior technology. Saregama risks being roadkill in the platform wars.

Future Bets: The Wild Cards

The future of Saregama might be determined by bets not yet visible in the numbers:

AI and Music Generation: AI will soon create music indistinguishable from human composition. This could destroy the value of music IP (why pay for songs when AI creates infinite music for free?) or enhance it (human-created music becomes premium, like handmade goods). Saregama's vast catalog could be training data for AI or could be made obsolete by it.

Short-form Content and Social Media: TikTok proved music can break through 15-second clips. Instagram Reels and YouTube Shorts are following suit. Pocket Aces gives Saregama capabilities here, but can a 120-year-old company really compete with digital natives in attention-hacking?

Gaming and Metaverse Opportunities: Gaming is becoming the largest entertainment medium globally. Virtual concerts in Fortnite generate millions. Indian gaming is exploding. Saregama has the IP but lacks gaming DNA. Partnerships or acquisitions might be necessary.

Global Indian Diaspora Market: 30 million overseas Indians are underserved by current offerings. They want premium Indian content but packaged for global sensibilities. Saregama could be the Disney of Indian content globally—or remain a domestic player.

The Synthesis View

The truth, as always, lies between extremes. Saregama is neither the next Spotify nor the next Blockbuster. It's a unique entity—a heritage company with startup energy, a content owner with platform ambitions, an Indian company with global potential.

The next five years will likely see continued strong performance driven by streaming growth and content investments. The bear concerns about ROE and competition are valid but manageable. The bull dreams of global domination are premature but not impossible.

For investors, Saregama represents a rare combination: exposure to India's digital transformation, ownership of irreplaceable assets, proven management execution, and multiple options for future growth. The risks are real—technological disruption, competitive pressure, execution challenges—but so are the opportunities.

XII. Epilogue & Reflections

From gramophone to algorithm—Saregama's 120-year journey reads like a meditation on permanence and change. This is a company that has survived two world wars, independence, partition, the License Raj, liberalization, the digital revolution, and a global pandemic. Each crisis became a catalyst for reinvention.

The Carvaan lesson is profound: sometimes going backward is the way forward. In our breathless rush toward digital everything, we forget that humans aren't upgrading as fast as our phones. The 60-year-old who grew up with radio doesn't want Spotify's infinite choice—she wants her 500 favorite songs available at the press of a button. Carvaan understood this. It's a reminder that great products solve human problems, not technological ones.

What Western music labels can learn from Saregama is humility and patience. Universal, Sony, and Warner fought digital transformation, sued their customers, and tried to preserve a dying business model. Saregama accepted reality and adapted. They didn't waste energy fighting piracy they couldn't stop; they found new ways to monetize. They didn't bet everything on one platform or format; they diversified across everything.

The future of music ownership and IP in India will be fascinating to watch. We're moving toward a world where music might be generated in real-time by AI, personalized to your mood, delivered directly to your brain. In this world, what's the value of owning "Dum Maro Dum"? Perhaps it becomes even more valuable—a marker of authenticity in an ocean of artificial content. Or perhaps it becomes worthless—a relic of when humans needed to create art.

For entrepreneurs and investors, Saregama offers several key takeaways:

First, heritage isn't a handicap—it's a moat if leveraged correctly. Your 100-year-old company has something the startup doesn't: trust, relationships, and assets that can't be replicated quickly.

Second, disruption doesn't always come from outside. Saregama disrupted itself with Carvaan before someone else could. The willingness to cannibalize your own business is painful but necessary.

Third, in content businesses, library value compounds. Every year, Saregama's catalog becomes more valuable—more platforms need it, more use cases emerge, more nostalgia accumulates. This is the opposite of most businesses where assets depreciate.

Fourth, India is not a market—it's a continent pretending to be a country. What works in Mumbai might fail in Chennai. What millennials want isn't what Gen X needs. One-size-fits-all is a recipe for fitting no one.

Finally, patience pays. Saregama's transformation took two decades. The Carvaan was conceived years before launch. Yoodlee Films took time to find its voice. In an era of quarterly capitalism, Saregama's long-term thinking is both anachronistic and essential.

As I write this, Saregama is trading at over ₹500, valued at more than ₹9,000 crores. The company that started by recording Gauhar Jaan on wax cylinders now streams billions of songs to smartphones. The same DNA that pressed vinyl records now produces Netflix originals. It's a testament to corporate evolution that Darwin would appreciate.

But perhaps the most profound reflection is this: Saregama isn't really in the music business or even the entertainment business. It's in the memory business. Every song in their catalog is someone's first dance, someone's wedding song, someone's memory of a parent now gone. In India, where family and tradition run deep, these aren't just songs—they're time machines.

The next time you hear "Ye Dosti" or "Kabhi Kabhie Mere Dil Mein," remember: you're not just listening to a song. You're experiencing the output of a 120-year-old algorithm for capturing and delivering human emotion. That algorithm has evolved from gramophone to AI, from Calcutta to the cloud, from the British Raj to the digital age.

And it's still playing.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube