Sammaan Capital: From India's Online Trading Pioneer to Housing Finance Transformation

I. Introduction & Episode Setup

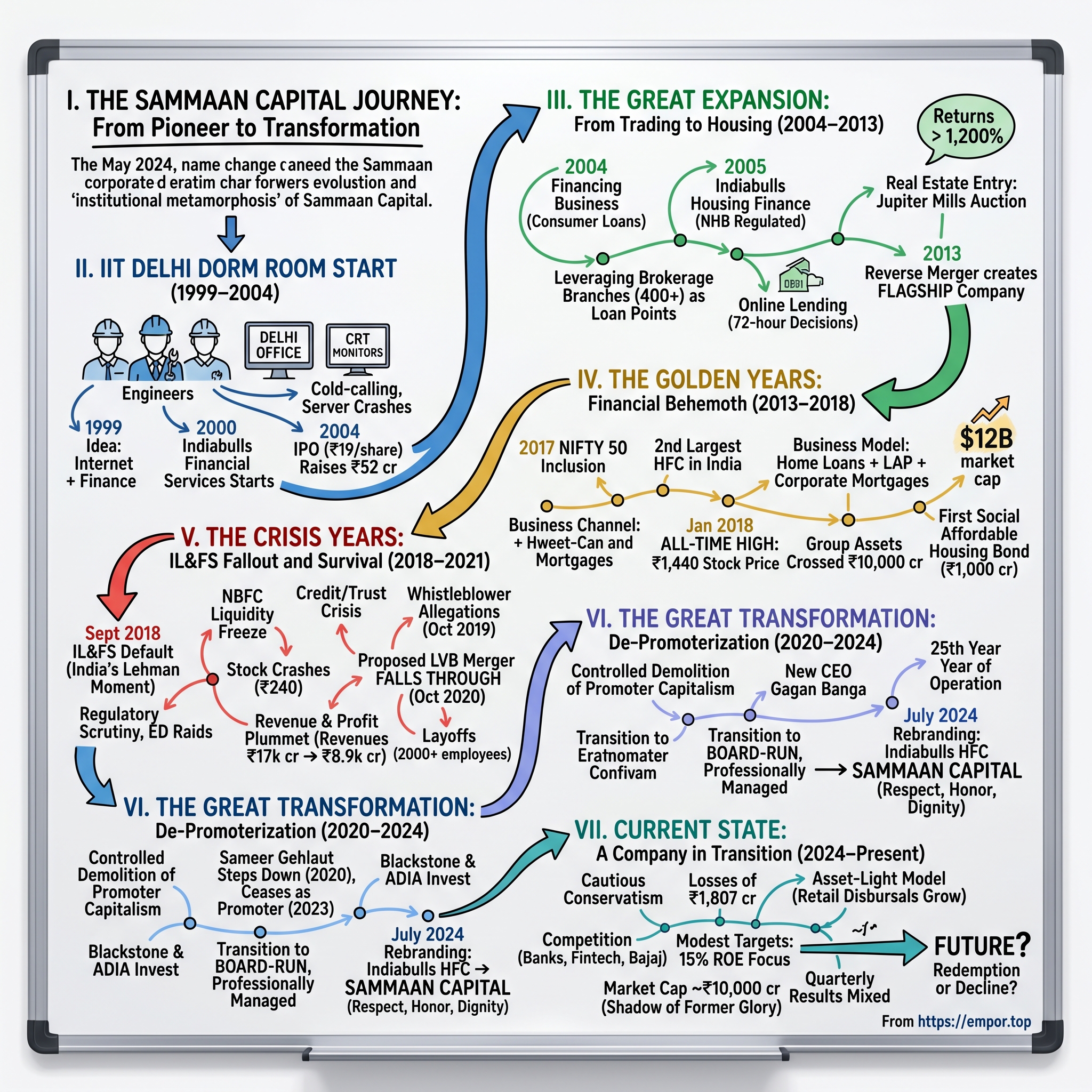

Picture this: It's May 2024, and one of India's most controversial financial services companies quietly changes its name from Indiabulls Housing Finance to Sammaan Capital. No fanfare, no grand announcements—just a simple regulatory filing that marks the end of an era. The company that once commanded a $12 billion market cap, whose stock delivered 1,200% returns in four years, whose founder graced magazine covers as India's youngest billionaire, has shed its old skin entirely.

Today, Sammaan Capital trades at ₹9,907 crore market cap, a shadow of its former glory. Revenue stands at ₹8,623 crore with losses of ₹1,807 crore. The stock has fallen 23% in the past year alone. But this isn't just another story of corporate decline—it's something far more fascinating: a complete institutional metamorphosis, from promoter-driven aggression to board-run conservatism, from boom-time darling to crisis survivor.

The central question we're exploring isn't just how a dot-com era online brokerage became India's second-largest housing finance company, then nearly collapsed, then transformed itself completely. It's about what this journey tells us about Indian capitalism itself—the interplay of ambition and regulation, the cycles of credit and crisis, the evolution from founder-led enterprises to institutional ownership.

This is a story of reinvention at its most extreme. Three IIT Delhi graduates who started trading stocks from a small Delhi office in 1999 would build an empire that touched everything from real estate to consumer finance. They would ride India's greatest economic boom, survive its worst financial crisis since independence, face fraud allegations, attempt failed mergers, and ultimately exit their own creation entirely. What remains today—Sammaan Capital—is both a continuation and a complete break from that history.

The company remains registered with and regulated by the National Housing Bank, still originating home loans, still managing a vast portfolio of mortgages. But everything else has changed: the ownership, the management, the strategy, even the name itself. As we'll see, this transformation raises profound questions about value creation, institutional evolution, and whether a company can truly escape its past by changing everything about its present.

II. The IIT Delhi Dorm Room Start (1999–2004)

The year is 1999. The Kargil War has just ended, the BJP-led NDA government is pushing economic reforms, and India's internet penetration stands at a mere 0.5%. In this environment, three mechanical engineering graduates from IIT Delhi—barely five years out of college—are huddled in a small office in Delhi, staring at bulky CRT monitors displaying stock prices. Sameer Gehlaut, born in 1974 to a Jat family in Rohtak, Haryana, is the driving force. His co-founders, Rajiv Rattan and Saurabh Mittal, share his background: middle-class families, top-tier engineering education, and most importantly, a burning ambition to build something massive.

The timing seems insane in retrospect. India's stock market has fewer than 10 million investors. Most trading happens through physical share certificates. The internet, where it exists, crawls at 56 kbps on dial-up modems that cost more per hour than most Indians earn in a day. Yet Gehlaut sees what others don't: the intersection of India's financial liberalization and the coming digital revolution. "We weren't trying to build a brokerage," he would later recall. "We were building the infrastructure for how Indians would interact with capital markets in the future."

Indiabulls Financial Services begins operations in January 2000, just as the dot-com bubble reaches its peak globally. The founders pool together ₹10 lakh in capital—borrowed from family, scraped from savings. Their first office is a 400-square-foot space in Hauz Khas, Delhi. They hire five employees, install three computers, and begin cold-calling potential clients. The pitch is revolutionary for its time: trade stocks online, get real-time prices, eliminate the middleman broker who might front-run your trades.

The early days are brutal. Server crashes during market hours. Clients who don't trust putting money into "computer systems." Established brokers who see them as upstarts to be crushed. But something remarkable happens: they start winning clients, particularly among India's emerging class of young professionals who understand technology. By December 2000, they have 500 active trading accounts. By 2001, despite the global dot-com crash, they have 5,000.What's remarkable is the speed of expansion. Since listing on the stock exchanges in September 2004 at a price of Rs 25, Indiabulls has appreciated some 60 times—but we're getting ahead of ourselves. The real story of 2000-2004 is about building infrastructure at breakneck speed while the market was still skeptical.

In late 2000, Indiabulls Securities, a subsidiary of Indiabulls Financial Services started offering online brokerage services and simultaneously opened physical offices across India. By 2003, Indiabulls securities had established a strong pan India presence and client base through its offices and on the internet. This dual approach—online for the tech-savvy, physical for the traditional—proves prescient. Within three years, they've built a network of more than 75 branches across 55 cities, becoming one of India's leading online brokerages.

The angel funding story deserves special attention. Sameer Gehlaut and Saurabh Mittal, two of the co-founders of Indian stock broking upstart Indiabulls Financial Services Ltd (IBFSL), are in the last lap of negotiations for angel funding from steel baron Lakshmi N. The numbers—an investment of $1 million at Rs 5 per share—are agreed upon telephonically. The deal is signed in London. This early backing from Lakshmi Mittal proves transformative—not just for the capital, but for the credibility it brings.

The IPO in 2004 marks the transition from startup to serious player. In 2004, Indiabulls Financial Services became a publicly-listed company after its initial public offering. In September 2004, Indiabulls Financial Services went public with an IPO at Rs 19 a share. The company raises ₹52 crore, enough capital to begin its next phase: the move into lending that would define its future.

III. The Great Expansion: From Trading to Housing (2004–2013)

The boardroom at Indiabulls headquarters in 2004 must have been electric with possibility. Fresh off their IPO success, the founders face a classic entrepreneur's dilemma: stick with what works (brokering) or bet everything on a bigger vision. They choose the latter. In late 2004, Indiabulls Financial Services started its financing business with consumer loans. It's a natural evolution—they have customer data, cash flow visibility, and most importantly, they understand risk pricing in ways traditional lenders don't.

But the real transformation comes in 2005. India's housing finance market is dominated by sleepy public sector banks and a few established players like HDFC. Mortgage penetration stands at just 3% of GDP versus 60% in developed markets. The opportunity is massive, but so are the barriers: you need licenses, capital, distribution, and most critically, trust. Who's going to take a home loan from a five-year-old company that started as an online broker?

Indiabulls Financial Services subsequently set up subsidiaries in stockbroking, consumer finance, housing finance and real estate, among others. The housing finance subsidiary—Indiabulls Housing Finance Limited—is incorporated in 2005, registered with and regulated by the National Housing Bank. This isn't just adding another vertical; it's a complete reimagining of what the company could become.

The genius of their approach lies in leveraging their existing infrastructure. Those 400+ brokering branches across India? They become loan origination points. The technology platform built for stock trading? It's repurposed for loan processing. By 2008, they've pioneered online lending in India—customers can apply for home loans through the internet, upload documents digitally, track approvals in real-time. In an industry where getting a home loan typically takes 45-60 days of paperwork hell, Indiabulls promises decisions in 72 hours. The numbers tell the story better than any narrative could: In 2008, IBFSL loan assets crossed Rs.10,000 crore. Think about that—from zero to ₹10,000 crore in loan assets in just four years. The stock market rewards this growth spectacularly. Since listing on the stock exchanges in September 2004 at a price of Rs 25, Indiabulls has appreciated some 60 times. By 2008, the company's shares had delivered investors returns of more than 1,200 percent.

The real estate connection deserves special mention. In March 2005, Indiabulls Properties Private Ltd, a subsidiary of Indiabulls Financial Services, participates in a government auction of Jupiter Mills, a defunct 11-acre textile mill in Lower Parel, Mumbai. They win the auction, marking their entry into real estate development. It's a synergistic move—property developers need construction finance, home buyers need mortgages, and Indiabulls can serve both sides of the transaction.

By 2006, the group's profit after tax crosses ₹100 crore, net worth crosses ₹1,000 crore. Indiabulls Real Estate is demerged from the parent company in 2006, Indiabulls Securities in 2008—each becoming a separate listed entity. The group is no longer just a financial services company; it's becoming a conglomerate touching multiple aspects of India's economic growth story.

The 2011 milestone crystallizes their transformation: IBREL purchased Indiabulls Blu from National Textile Corporation for ₹1,505 crore and the group profit after tax crossed ₹1,000 crore. But the crown jewel remains housing finance. In 2013, a critical corporate restructuring takes place: Indiabulls Financial Services reverse merged with its wholly owned subsidiary, Indiabulls Housing Finance, to form the flagship company of the group. This isn't just a technical merger—it's a statement that housing finance, not brokering or real estate development, is now the core of the empire.

IV. The Golden Years: Becoming a Financial Behemoth (2013–2018)

The scene is the Bombay Stock Exchange on a humid September morning in 2017. As the opening bell rings, something historic happens: Indiabulls Housing Finance enters the NIFTY 50 index, joining India's most elite companies. The three engineers from IIT Delhi who started with borrowed money and dial-up modems have built something that now sits alongside HDFC, Reliance, and Infosys in the country's benchmark index.

By 2017, Indiabulls Housing Finance had become the second-largest housing finance company in India and was included in the NIFTY 50 benchmark index. The journey to this moment has been nothing short of spectacular. Under Sameer Gehlaut's leadership, Indiabulls Housing Finance became India's third-largest housing finance company, providing over $35 billion in total lending to more than 500,000 customers and paying $1.8 billion in dividends to shareholders.

The business model during these golden years is a masterclass in financial engineering. The company offers home loans in the affordable housing segment with loan amounts ranging from Rs. 15-30 lakh and interest rates between 9.75% and 11.50% with an average tenure of 15 years, available to both salaried and self-employed customers. But this is just the base of the pyramid. The real profits come from loan-against-property (LAP) products and corporate mortgages, where margins are fatter and ticket sizes larger. The stock market tells the story of these golden years with brutal clarity. The all-time high or the highest price that Indiabulls Housing Finance stocks have ever touched was ₹1,440.00 and this occurred on Jan 2018. The highest closing price at which Indiabulls Housing Finance stocks have ever closed was ₹1,390.95 recorded on Jan 2018. Indiabulls Housing Finance, ever since hit a high of 1400 in August 2018 (four times it hit this level, Oct 2017, January 2018, April 2018) has been seeking lower levels. Think about that trajectory: from ₹25 at IPO in 2004 to ₹1,440 in January 2018—a 57-fold increase.

The operational metrics during this period are equally impressive. The company operates through a network of 217 branches and more than 8,000 channel partners. It has disbursed loans exceeding ₹3 lakh crore. The loan book stands at over ₹54,000 crore. They're servicing over 1.4 million homeowners. In December 2017, IBHFL announces the issuance of India's first Social Affordable Housing Bond of ₹1,000 crore with Yes Bank being the sole arranger and subscriber—a sign of their financial innovation and market credibility.

Sameer Gehlaut, at the peak of his power, oversees an empire valued at $12 billion in market capitalization. During his 20-year tenure from 2000-2020 as Executive Chairman, he secured $2 billion in equity investments and delivered a 26% compounded annual growth return to shareholders. The three IIT engineers have built something that rivals established players who've been in the business for decades.

But there are warning signs for those who care to look. The aggressive growth is funded by wholesale borrowing—commercial papers, bonds, bank loans. The asset-liability mismatch is growing. The company is increasingly dependent on short-term funding for long-term assets. Competition is intensifying, with banks entering the affordable housing segment aggressively. And most critically, the entire NBFC sector is skating on thin ice, dependent on continued liquidity and market confidence.

The party, as we'll see, is about to end spectacularly.

V. The Crisis Years: IL&FS Fallout and Survival (2018–2021)

September 2018. The Infrastructure Leasing & Financial Services (IL&FS) Group, a behemoth with ₹91,000 crore in debt, defaults on its commercial papers. It's India's Lehman moment. Within days, the entire NBFC sector freezes. Mutual funds stop lending to NBFCs. Banks pull back credit lines. The commercial paper market—the lifeblood of wholesale-funded NBFCs—simply vanishes. For Indiabulls Housing Finance, sitting at the peak of its powers with a stock price above ₹1,200, the timing couldn't be worse.

However, between late 2018 and 2019, its shares and bonds experienced a sharp decline in value due to a credit market crisis triggered by the collapse of IL&FS, the company's shrinking balance sheet, allegations of fraud by group promoters, and a proposed merger with the beleaguered Lakshmi Vilas Bank, which fell through. The IL&FS default isn't just a credit event—it's a trust crisis. Suddenly, every NBFC is suspect. Every aggressive lender is potentially the next domino to fall.

It gave Death Cross signal in Sept 2018, coinciding with the NBFC crisis gripping the market. The technical indicators are screaming danger, but the fundamental deterioration is even worse. The company's asset-liability management comes under severe stress. They can't roll over commercial papers. Banks that were eager to lend six months ago now won't return calls. The cost of borrowing spikes from 7-8% to 11-12% almost overnight.

Then come the allegations. In October 2019, a whistleblower complaint to the RBI and other regulators alleges that Indiabulls Housing Finance has siphoned off funds through shell companies. The allegations are explosive: round-tripping of funds, loans to connected parties, misuse of public money. The company vehemently denies everything, but the damage is done. Foreign investors start dumping the stock. Rating agencies put the company on watch.

The proposed merger with Lakshmi Vilas Bank—announced in April 2019—is supposed to be the escape route. The idea is elegant: merge with a bank, get access to low-cost deposits, solve the ALM problem permanently. But Lakshmi Vilas itself is dying, bleeding deposits and facing its own crisis. The RBI sits on the merger application for months, neither approving nor rejecting. Finally, in October 2020, the merger is called off. A month later, Lakshmi Vilas Bank is placed under moratorium and merged with DBS Bank India. Indiabulls' escape route has collapsed. The numbers are staggering in their brutality. Ever since 2019, the company's revenues have continuously fallen from Rs. 17,019 cr. to Rs. 8983 cr. in 2022. Their net profit also shows a similar sign falling from Rs. 4057 cr. to Rs. 1177 cr. The stock price tells an even more dramatic story. The stock crashed 37.8% and touched an intraday low as well as fresh 52-week low of Rs 240.10 when the Lakshmi Vilas Bank merger concerns intensified in September 2019.

The human cost is equally severe. Indiabulls Group has asked over 2,000, of its total of 26,000 employees, to leave as an outcome of performance review at the end of financial year 2019-20. Scores of employees took to social media to express disappointment and said they were asked to resign over WhatsApp calls. The company that once symbolized opportunity and growth is now synonymous with layoffs and despair.

The regulatory scrutiny intensifies through this period. Several public interest litigations (PILs) and first incident reports were filed against the company back in 2019, alleging irregularities, siphoning of funds, and other violations committed by the promoters of the company. Based on those allegations, the market regulator's corporate finance investigation department had started an investigation against the company in early 2020. In March 2022, the Enforcement Directorate (ED) conducted raid at Indiabulls Finance Centre in Mumbai. The case was registered on the basis of an FIR filed in Palghar which said that Indiabulls Housing Finance siphoned money and invested it in its own shares for increasing the prices. The complainant mentioned the real estate companies which had taken loans from Indiabulls Housing Finance and routed money back into its shares in the FIR.

Through all of this, the company maintains its innocence. However, the watchdog has not found any wrongdoing on part of the company with respect to the specific allegations made against it in the various public interest litigations and the complaints. But in markets, perception is reality. The damage to reputation is irreversible. Trust, once broken, is almost impossible to rebuild in financial services.

VI. The Great Transformation: De-Promoterization (2020–2024)

The boardroom at Indiabulls headquarters in early 2020 must have felt like a wake. The stock that once traded at ₹1,400 is now below ₹200. The founder who built this empire from nothing is about to do something almost unheard of in Indian corporate history: voluntarily give up control without a fight. Sameer Gehlaut stepped down as the chairman of Indiabulls Housing Finance in 2020 and ceased to be its promoter in 2023.

This isn't a hostile takeover or a bankruptcy proceeding. It's something far more interesting: a controlled demolition of promoter capitalism, replaced brick by brick with institutional ownership. Gehlaut's exit is methodical, almost surgical. First, he steps down from operational roles. Then he begins selling his stake—not in panic, but strategically. Gehlaut has sold half of his stake in the company amounting to 11.9% to several funds which include the likes of Blackstone Group Inc. and Abu Dhabi Investment Authority.

The timing of his complete exit from the board—March 31, 2022—marks the end of an era. The company that was synonymous with Sameer Gehlaut for two decades is now orphaned, searching for a new identity. The other co-founders had already moved on years earlier, with Rajiv Rattan and Saurabh Mittal managing other group businesses after the 2014 split.

What follows is a fascinating experiment in corporate governance. Can a company built on the vision and drive of a single promoter survive—even thrive—without him? The new management, led by professional executives and overseen by institutional investors, begins the slow process of transformation. They cut costs, reduce the loan book, focus on asset quality over growth. It's the opposite of everything Indiabulls stood for in its glory days.

The institutional investors who now control the company bring a different philosophy. Where Gehlaut was aggressive, they are conservative. Where he took risks, they seek safety. The company begins to look more like a traditional financial institution and less like the entrepreneurial dynamo it once was. This isn't necessarily bad—it's just different. The culmination of this transformation comes in July 2024 with the most visible change of all: In July 2024, Indiabulls Housing Finance was renamed as Sammaan Capital. The name change is far more than cosmetic. 'Sammaan' in Indian languages means "respect," "honor," "courtesy," and "dignity". The Company intends its brand, and the meaning of the word 'Sammaan' in the Indian context, to emphasise and convey to its stakeholders, a customer-centric approach, a sense of pride in buying a house or owning a business, propriety and dignified business conduct.

The rebranding statement reads like a manifesto of the new order: "Sammaan Capital Limited, in its first two decades of existence, was a promoter-led and promoter-driven lender. Over the last five years, the Company has transformed into a board-run, professionally managed, diversely held financial institution." The change in name is merely the latest milestone in the Company's continuing larger journey towards best-in-class corporate governance.

Gagan Banga, the new CEO, represents this new era perfectly—a professional manager, not a founder-entrepreneur. His statement captures the essence of the transformation: "Our new identity underscores our respect for our customers and all other stakeholders, our commitment to treating them with dignity and honour, and our pledge to conduct our business in a dignified and trustworthy manner."

This year also marks the Company's 25th year of operation—the erstwhile Indiabulls Financial Services Limited, from which the Company originates, was incorporated in the year 2000. From online stock trading startup to housing finance giant to whatever Sammaan Capital will become—it's been quite a journey.

VII. Current State: A Company in Transition (2024–Present)

Walk into any Sammaan Capital branch today—if you can find one, as many have been shuttered—and you'll see a company caught between its past and future. The aggressive sales culture that once defined Indiabulls has been replaced by cautious conservatism. The loan officers who once competed to disburse the most loans now focus on recovery and asset quality. The energy is different—less electric, more procedural.

The financial numbers tell the story of this transition with brutal clarity. Revenue stands at ₹8,623 crore, with losses of ₹1,807 crore. The company has delivered a poor sales growth of -8.19% over past five years. Company has a low return on equity of 0.95% over last 3 years. The company has low interest coverage ratio—a key metric for financial institutions that shows how easily they can service their debt. The recent quarterly results provide a mixed picture. Sammaan Capital Ltd's revenue fell -5.44% since last year same period to ₹2,132.45Cr in the Q4 2024-2025, while net profit jumped 1.44% since last year same period to ₹324.04Cr. The company reported a profit after tax of INR 303 crores for Q3 FY 2024, up from INR 291 crores in the same quarter last year. Net interest margin remained stable at 4.9%, and ROA increased marginally to 1.6% from 1.5%.

The stock market's verdict on Sammaan Capital is harsh. Sammaan Capital Ltd share price moved down by 19.65% on BSE over the last 12 months. The current market cap stands at around ₹10,000-11,000 crore—less than 20% of what it was at peak. SAMMAANCAP stock has fallen by −8.83% compared to the previous week, the month change is a −12.57% fall, over the last year SAMMAAN CAPITAL LTD has showed a −22.84% decrease.

The business model has fundamentally shifted toward an asset-light approach. Retail disbursals under the asset-light model grew to INR 7,200 crores in 9 months, with cumulative disbursals of over INR 18,000 crores in the last 2 years. This means the company is increasingly originating loans for other banks and financial institutions rather than keeping them on its own books—a safer but less profitable strategy.

The competition landscape has also transformed dramatically. Where Indiabulls once competed with HDFC and a handful of other housing finance companies, today it faces competition from universal banks (who have aggressively entered affordable housing), fintech startups (who have digitized the entire loan process), and other NBFCs who survived the crisis better. Bajaj Finance, with its superior technology and customer acquisition, has become what Indiabulls once aspired to be. HDFC's merger with HDFC Bank has created a behemoth that dwarfs everyone else.

Management's targets for the future seem modest compared to the past. The company is targeting a 15% ROE, which factors in everything including write-backs. This is respectable but far from the 25%+ ROEs of the glory days. The focus is clearly on survival and stability rather than aggressive growth.

VIII. Playbook: Lessons from the Transformation

Every epic business story contains lessons, and Sammaan Capital's journey from startup to giant to near-collapse to reinvention offers a masterclass in several critical areas. These aren't just academic observations—they're battle-tested insights from one of Indian finance's most dramatic transformations.

Building in Boom Times vs. Surviving in Crisis

The Indiabulls story demonstrates that companies built during boom times often carry structural weaknesses that only become apparent during crises. The aggressive growth from 2004-2018 was enabled by abundant liquidity, rising asset prices, and investor optimism. The business model—borrow short, lend long, grow fast—worked brilliantly until it didn't. When the IL&FS crisis hit, the company's dependence on wholesale funding became its Achilles heel. The lesson: business models that work in good times must be stress-tested for bad times. Companies need to ask not "how fast can we grow?" but "how will we survive when liquidity disappears?"

The Perils of Aggressive Growth in Cyclical Businesses

Housing finance is inherently cyclical, tied to real estate prices, interest rates, and economic growth. Indiabulls' strategy of aggressive expansion during the up-cycle maximized returns but also maximized risk. When you're growing at 40-50% annually in a business that historically grows at 15-20%, you're either a genius or heading for trouble. The company's loan book grew from zero to ₹54,000 crore in 13 years—spectacular, but ultimately unsustainable. The playbook insight: in cyclical businesses, the goal isn't to maximize growth during good times but to optimize for the full cycle.

Promoter-Driven vs. Institution-Driven Governance Models

The transformation from Sameer Gehlaut's Indiabulls to today's Sammaan Capital represents a fundamental shift in governance philosophy. Promoter-driven companies can move fast, take risks, and pivot quickly—advantages that helped Indiabulls grow rapidly. But they're also vulnerable to key-person risk, regulatory scrutiny, and governance concerns. The institutional model brings stability, credibility, and professional management, but often at the cost of entrepreneurial dynamism. Neither model is inherently superior; the key is matching the governance model to the company's stage and market environment.

Managing Regulatory Relationships in Financial Services

Indiabulls' relationship with regulators went from supportive to adversarial over time. Early on, regulators welcomed new players who brought innovation and competition. But as the company grew larger and more systemically important, regulatory scrutiny intensified. The failed Lakshmi Vilas Bank merger showed how regulatory approval can make or break strategic moves. The lesson: in financial services, managing regulatory relationships is as important as managing customer relationships. Trust with regulators must be built over years and can be destroyed in days.

Capital Allocation During Transformation

The decision to raise ₹7,500 crore through a rights issue (which was over 2x subscribed) shows how capital allocation priorities change during transformation. The old Indiabulls would have used this capital for aggressive growth. The new Sammaan is using it to strengthen the balance sheet, provide for bad loans, and build credibility. This conservative approach may disappoint growth investors but is essential for survival. The playbook teaches that capital allocation must match corporate strategy—and both must adapt to changing circumstances.

The Importance of Timing in Financial Cycles

Timing, as they say, is everything. Indiabulls' entry into housing finance in 2005 was perfectly timed to catch India's real estate boom. But the company failed to recognize when the cycle was turning in 2018. The stock hit ₹1,440 in January 2018—if investors had sold then, they'd be hailed as geniuses. Six months later, the IL&FS crisis began, and the stock never recovered. The lesson: in financial services, recognizing cycle turns is more important than riding the cycle.

Brand Reinvention Strategies in Regulated Industries

The rebranding from Indiabulls to Sammaan Capital isn't just cosmetic—it's an attempt to signal a complete break from the past. But in regulated industries with long memories, can you really escape your history with a name change? The jury is still out. What's clear is that rebranding must be accompanied by genuine operational and cultural change. Sammaan can't just be Indiabulls with a different name; it must be a fundamentally different company.

IX. Bear vs. Bull Case Analysis

Bear Case: The Weight of History

The pessimists have compelling arguments. Start with the declining financial metrics: revenue down 8.19% over five years, ROE at 0.95%, interest coverage ratios that would make any analyst nervous. These aren't temporary blips—they're trends that have persisted for half a decade. The company that once grew at 40% annually is now shrinking.

Legacy asset quality remains a massive concern. The company may have ₹7,000 crore in provisions, but in India's challenging legal environment, recovering bad loans can take decades. The retail loan book, especially loans given during 2015-2018 at the height of the real estate bubble, likely contains hidden stress that hasn't fully surfaced. Every quarter could bring new nasty surprises.

The competitive landscape has fundamentally shifted against Sammaan. Banks have aggressively entered affordable housing with lower costs of funds. Fintech players like Home First Finance have digitized the entire customer journey. Bajaj Finance has shown what modern NBFC excellence looks like. Where does Sammaan fit in this new world? It lacks the low cost of funds of banks, the technology edge of fintechs, and the execution excellence of Bajaj.

Regulatory overhang persists despite the name change. The Supreme Court directive for both the Enforcement Directorate (ED) and the Reserve Bank of India (RBI) to report back on the progress of investigations into suspected financial impropriety shows that legal challenges haven't disappeared. Every few months brings new PILs, new investigations, new headlines that remind everyone of the company's troubled past.

Most critically, there's a lack of clear strategic differentiation. What is Sammaan Capital's unique value proposition? Why would a customer choose them over HDFC, SBI, or Bajaj? The company talks about focusing on affordable housing and MSMEs, but so is everyone else. Without a clear competitive advantage, Sammaan risks becoming a zombie company—not dead, but not really alive either.

Bull Case: The Phoenix Scenario

The optimists see opportunity where others see disaster. India's housing finance opportunity remains massive, with mortgage penetration still below 11% of GDP compared to 60%+ in developed markets. As India urbanizes and incomes rise, millions will need home loans. The market is big enough for multiple players, and Sammaan's established infrastructure—200+ branches, 8,500+ channel partners—provides a foundation for growth.

The de-promoterization, while painful, has created a clean slate. The old aggressive culture is gone, replaced by professional management focused on sustainable growth. Institutional ownership by Blackstone and ADIA brings not just capital but credibility. The company no longer has the overhang of promoter-related controversies.

The governance improvements under new management are real and substantial. The board is now truly independent. Risk management has been overhauled. The asset-light model reduces balance sheet risk. These aren't cosmetic changes—they're fundamental improvements that position the company for long-term stability.

Despite all challenges, the brand recognition remains strong. Millions of Indians know the Indiabulls name, even if it's being phased out. This recognition can be leveraged as Sammaan builds its new identity. The company isn't starting from zero—it has relationships, data, and experience that new entrants lack.

There's also potential for operational turnaround under new management. The current numbers are terrible, but they're also off a low base. If management can deliver even modest growth while maintaining asset quality, the stock could re-rate significantly. At current valuations, the market is pricing in continued decline—any positive surprise could lead to sharp gains.

The Verdict

Both cases have merit, but the bear case feels stronger in the near term. The company faces structural challenges that won't disappear quickly. The housing finance industry has fundamentally changed, and Sammaan hasn't yet articulated a compelling vision for its place in this new world. The financial metrics suggest a company that's still struggling to find its footing.

However, the bull case shouldn't be dismissed entirely. Indian financial services have seen spectacular turnarounds before. If management can execute on their modest targets—15% ROE, stable asset quality, measured growth—the stock could deliver reasonable returns from current depressed levels. But this isn't a story of returning to past glory; it's about building something sustainable, if less spectacular.

X. Epilogue: The Future of Sammaan Capital

As we stand in 2024, looking at what Sammaan Capital has become and imagining what it might yet be, several strategic imperatives emerge for the new management. These aren't optional nice-to-haves—they're existential necessities for a company trying to write a successful second act.

First, digital transformation isn't just about having an app or website—it's about fundamentally reimagining the lending business for the digital age. Sammaan needs to move beyond the branch-based model that Indiabulls perfected in the 2000s. The future is about straight-through processing, AI-based credit decisions, and digital customer acquisition. The company that pioneered online stock trading in 2000 needs to pioneer something in 2025.

Second, strategic clarity is essential. Sammaan can't be all things to all people. Should it focus on affordable housing where margins are thin but volumes are large? Or on MSMEs where risks are higher but so are returns? The current strategy of doing both feels unfocused. The company needs to pick a lane and excel in it.

Third, cultural transformation must continue. The aggressive sales culture of Indiabulls is gone, but what replaces it? Sammaan needs to build a performance culture that balances growth with risk, ambition with prudence. This isn't easy—culture change never is—but it's essential for long-term success.

The M&A scenarios are intriguing. Could Sammaan be acquired by a bank looking for a ready-made housing finance platform? Could it merge with another struggling NBFC to gain scale? Or could it acquire smaller players to consolidate the fragmented affordable housing market? All options should be on the table.

India's housing market outlook remains broadly positive despite near-term challenges. The government's push for affordable housing, the demographic dividend of a young population, and rising income levels all support long-term growth. But the market is also becoming more competitive, regulated, and demanding. Success will require excellence, not just participation.

Can Sammaan write a successful second act? The honest answer is: we don't know. The company has survived an existential crisis, transformed its ownership and governance, and stabilized its operations. That's no small achievement. But survival isn't success. The next chapter—whether Sammaan becomes a sustainable, profitable lender or remains a cautionary tale of fallen giants—is still being written.

The key metrics to watch going forward are clear: asset quality trends (are NPAs really under control?), growth in the asset-light book (can they scale without taking balance sheet risk?), ROE improvement (can they reach the promised 15%?), and market share in chosen segments (are they winning or just participating?). These numbers will tell us whether Sammaan Capital is truly transforming or merely managing decline.

As we close this epic saga—from three IIT graduates with ₹10 lakh in capital to a ₹10,000 crore market cap company—we're reminded that in business, as in life, nothing is permanent. Companies rise and fall, fortunes are made and lost, reputations are built and destroyed. The Indiabulls story—now the Sammaan story—is far from over. Whether it ends in triumph or tragedy, redemption or further decline, remains to be seen. What's certain is that it will continue to offer lessons for students of Indian business for years to come.

The three engineers who started trading stocks from a small Delhi office in 1999 probably never imagined their creation would undergo such a dramatic transformation. Sameer Gehlaut, Rajiv Rattan, and Saurabh Mittal built something remarkable, watched it nearly collapse, and then stepped aside for others to rebuild. That takes a special kind of courage—or perhaps resignation. Either way, their story reminds us that in the end, no company is bigger than the market forces that shape it.

Sammaan Capital stands today at an inflection point. It has shed its past, quite literally, but hasn't yet defined its future. It has survived the crisis but hasn't yet proven it can thrive. It has new management but not yet a new strategy that inspires confidence. For investors, employees, and other stakeholders, the wait continues. The next few years will determine whether Sammaan Capital becomes a case study in successful corporate transformation or another footnote in India's corporate history. The stage is set, the actors are in place, and the second act is about to begin.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube