Sammaan Capital: The Phoenix of Indian Shadow Banking

I. Introduction & Episode Roadmap

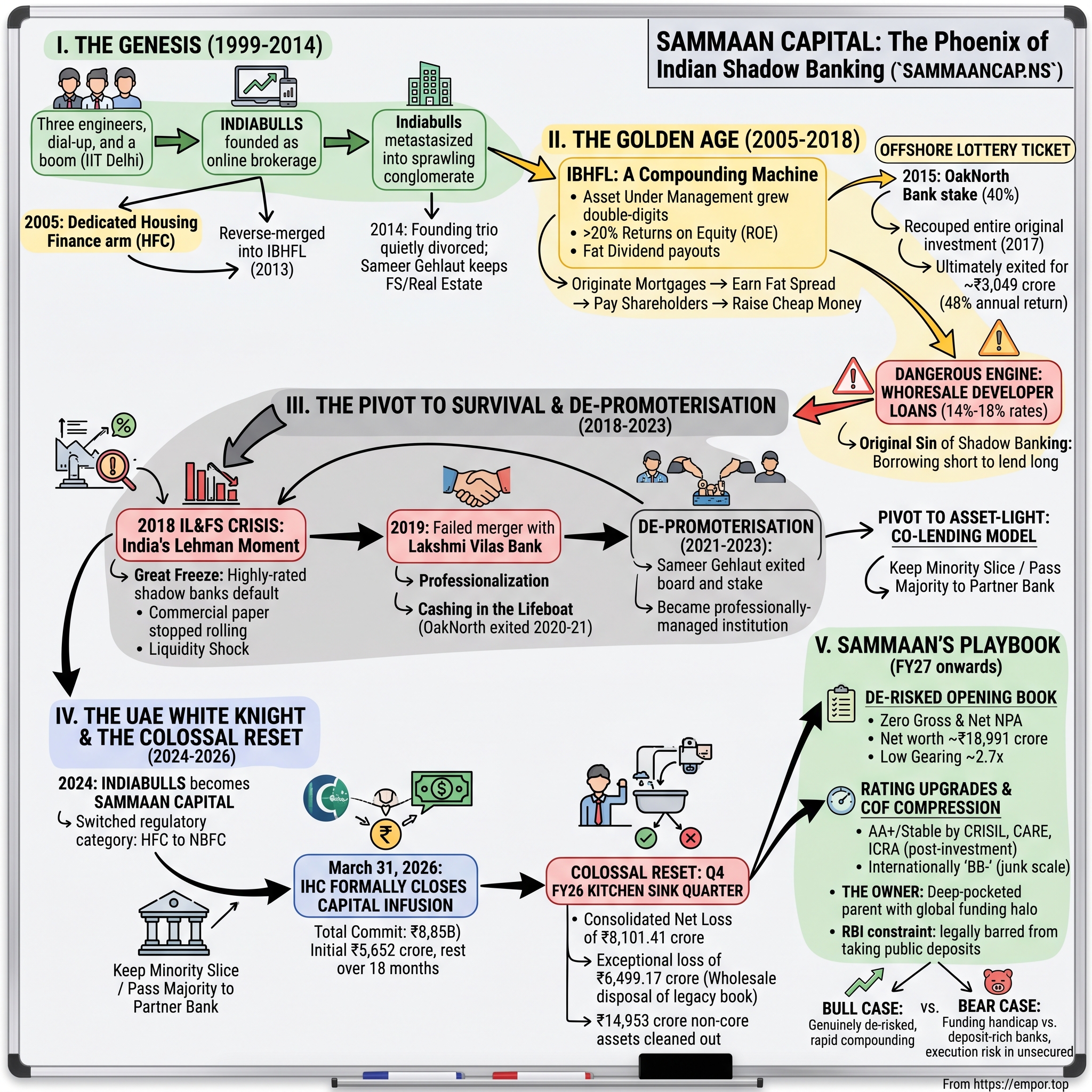

On the evening of May 20, 2026, a group of analysts dialed into a conference call that, on paper, should have been a wake. The company on the other end of the line had just reported one of the largest quarterly losses in the history of Indian non-bank finance: a consolidated net loss of ₹8,101 crore for the three months ended March 31, 2026 — roughly a billion dollars of red ink, printed by a lender that had earned a quarterly profit of ₹324 crore in the very same quarter a year earlier.1 And yet the stock did not collapse. In the sessions around the results it rose, at one point climbing double digits.2

That paradox is the whole story. Because the same March 31 on which Sammaan Capital Limited (SAMMAANCAP.NS) detonated its balance sheet was the day Abu Dhabi's International Holding Company (IHC) — the most valuable listed holding company in the Middle East, with a market capitalization of roughly $233 billion — formally closed a capital infusion that would eventually total ₹8,850 crore (about $1 billion) and make it the company's new promoter.34 The loss was not an accident of the quarter. It was a deliberate act: a "kitchen sink" purge, timed to the exact moment a sovereign-scale investor arrived with a fresh capital cushion to absorb the pain. Management wanted FY27 to open on a clean sheet, and it was willing to book a decade's worth of legacy sins in a single quarter to get there.

Rewind two decades and this same entity was Indiabulls Housing Finance Limited — a promoter-built, high-flying mortgage machine that was, at its peak, among India's largest private housing financiers, throwing off returns on equity north of 20% and ranking among the country's most generous dividend payers. How did that company shed its founder, its famous "Indiabulls" name, its wholesale developer loan book, and its very license category — and re-emerge as a professionally-managed, AA+ rated (domestically), Abu Dhabi-owned multi-product lender called Sammaan Capital?56

This is a survival story, but it is not a redemption fairy tale, and Empor is not the company's investor-relations desk. The independent question worth holding through all ten chapters is this: can an asset-light lender that is legally barred from taking public deposits, that funds itself through wholesale bond markets and co-lending partnerships, and whose international credit rating still sits below investment grade, actually out-compete deposit-rich giants like HDFC Bank, State Bank of India, and Bajaj Finance in the businesses it now wants to enter? Management says yes, and it has a $1 billion cushion and a genuinely cleaned-up book to back the claim. But the same management once promised discipline and then nearly drowned in its own leverage. We will test the new story against the old one — because the most useful thing a listener can do with a phoenix narrative is ask whether the bird has actually stopped catching fire.

We start where every good origin story does: with three engineers, a dial-up connection, and a boom.

II. The Genesis: Sameer Gehlaut & The Indian Brokerage Boom (1999–2005)

Picture Delhi at the turn of the millennium. India had opened its economy less than a decade earlier, the National Stock Exchange had just dragged share trading out of the paper-and-shouting era and onto electronic screens, and dematerialized shares — stocks held as digital entries rather than physical certificates — were suddenly making it possible for an ordinary person to buy equities from a computer. Into this opening walked Sameer Gehlaut, a mechanical engineer from IIT Delhi who had done a stint on offshore oil rigs before deciding that the real gusher was in Indian finance. In 1999, together with fellow IIT Delhi alumni Rajiv Rattan and Saurabh Mittal, he founded Indiabulls as an online stock brokerage — one of the first to try to bring internet-era trading to Indian retail investors.

The brokerage was the seed, but Gehlaut's ambition was a forest. Over the following years Indiabulls metastasized into a sprawling conglomerate — brokerage, real estate, power generation, infrastructure, and consumer finance — bound together by an aggressive sales culture, comfort with heavy leverage, and a taste for speed that would define the group for its entire life. The animating belief was simple and, for a while, spectacularly correct: India was urbanizing and formalizing, credit penetration was minuscule, and whoever could shovel capital into housing and property fastest would win.

The pivotal move for our story came in 2005, when the group established a dedicated housing finance arm to ride India's structural mortgage boom. This was not a niche side bet. Home ownership in India was — and remains — a deeply aspirational, under-financed market; a housing finance company (HFC) that could originate mortgages at scale was effectively selling picks and shovels to an entire nation's middle-class dream. The regulatory architecture helped: HFCs were then supervised by the National Housing Bank, enjoyed certain funding and tax advantages, and could grow a mortgage book far faster than a deposit-taking bank hemmed in by branch economics.

By 2013, the group tidied its plumbing. Indiabulls Financial Services Limited, the older listed financial-services entity, was reverse-merged into its own housing finance subsidiary, and the combined vehicle emerged as Indiabulls Housing Finance Limited (IBHFL) — a single, highly liquid, listed financial-services stock. The logic was clean: one balance sheet, one investor story, one regulatory identity centered on mortgages, and a share that institutional investors could actually build a position in.

Then, in 2014, the founding trio quietly divorced. In a mutual split of the sprawling empire, Rajiv Rattan and Saurabh Mittal took the infrastructure and power assets — later rebranded under the RattanIndia banner — while Gehlaut kept the crown jewels: financial services and real estate, with IBHFL at the center. It was an amicable carve-up of a conglomerate that had grown too unwieldy to steer as one, and it left Gehlaut as the undisputed sovereign of a fast-growing mortgage lender in the fastest-growing large economy on earth.

For investors, the lesson of the genesis era is about DNA. The traits that would later nearly kill the company — leverage tolerance, breakneck growth, and a promoter accustomed to absolute control — were not bugs bolted on during the good times. They were encoded at the founding. That DNA powered a decade of extraordinary returns before it powered a near-death experience. We turn to the returns first.

III. The Golden Age of Shadow Banking & The Real Estate Bets (2005–2018)

For roughly a decade, IBHFL was one of the great compounding machines of the Indian market — the kind of stock that turned a mortgage lender into a momentum darling. It grew its assets under management at a double-digit clip year after year and delivered returns on equity that consistently sat above 20%, a level that let it pay out generous dividends while still expanding. To the market, it looked like a virtuous flywheel: originate mortgages, earn a fat spread, pay shareholders handsomely, raise cheap money on the strength of the stock, originate more.

But underneath the respectable retail-mortgage veneer sat a second, far more powerful and far more dangerous engine. Alongside home loans, IBHFL lent aggressively to real estate developers — "wholesale" builder loans, extended at rich interest rates in the 14%–18% range against half-built residential and commercial projects. These loans were enormously profitable while property prices rose. The catch was in how they were funded. IBHFL financed long-dated, illiquid developer projects with short-dated, flighty money: commercial paper and wholesale mutual-fund debt that had to be rolled over every few months. This is the original sin of shadow banking — borrowing short to lend long — and it works beautifully right up until the short money stops showing up. Hold that thought; it becomes the hinge of the entire story.

The most instructive episode of the golden age had nothing to do with Indian mortgages at all. In November 2015, IBHFL deployed roughly ₹663 crore for a 40% stake in a newly launched British digital challenger bank, OakNorth Bank, which specialized in lending to small and mid-sized UK businesses.7 It was an odd, opportunistic bet for an Indian home lender — and it turned out to be the single best capital-allocation decision the company ever made. In November 2017, IBHFL sold roughly a quarter of its holding to Singapore's sovereign investor GIC for about ₹770 crore, in one stroke recouping more than its entire original investment while still keeping the bulk of the stake.7 Over the following years, through successive secondary sales, the company ultimately exited OakNorth entirely for roughly ₹3,049 crore — an annualized return on the order of 48% over about six years.8 Remember that this offshore lottery ticket exists; when the storm came, it would help keep the lights on.

What management did with all the golden-age profit is where the independent lens sharpens. Rather than hoard capital, IBHFL ran an aggressive shareholder-return policy, becoming one of the market's notable dividend payers. That thrilled retail holders and flattered the stock. But high payouts are the enemy of retained-earnings buffers, and a wholesale-funded lender's buffer is the only thing standing between it and a liquidity shock. The company was, in effect, distributing its umbrella just as the monsoon clouds gathered. In hindsight, the golden age was not evidence of a durable moat; it was evidence of a cyclical business enjoying the up-leg of a credit cycle while quietly running down its margin of safety. In September 2018, the down-leg arrived all at once.

IV. The Great Freeze: The 2018 IL&FS Crisis & The Failed Banking Dream (2018–2020)

Every financial system has its Lehman moment, and India's arrived in September 2018 when Infrastructure Leasing & Financial Services — IL&FS, a giant, supposedly rock-solid infrastructure financier — began defaulting on its debt. The shock was less about IL&FS itself than about what its collapse revealed: that highly-rated shadow banks could go from "AAA" to default with almost no warning. Mutual funds, which had been the willing suppliers of cheap short-term money to the entire non-bank sector, slammed the window shut. Commercial paper stopped rolling. And every lender that had funded long-term assets with short-term money — IBHFL foremost among them — was suddenly staring at an asset-liability mismatch it could not paper over.

This is worth translating out of jargon. Imagine you own a house you paid for with a credit card you have to fully repay every 30 days, betting you can always open a new card to cover the old one. The asset (the house) is fine and rising in value. But the day no bank will issue you a new card, you are insolvent on a cash-flow basis even though you are rich on a net-worth basis. That, in miniature, was the terror facing IBHFL. Its developer loans were long, illiquid, and — as it turned out — of uneven quality; its funding was short and had just evaporated.

Management's response was strategically logical and, in the end, futile. If the fatal flaw was the absence of a stable, low-cost deposit base, then the solution was to become a bank. In April 2019, IBHFL announced a merger with Lakshmi Vilas Bank (LVB), a small, troubled south Indian lender, in a bid to acquire a banking license and, with it, access to sticky retail deposits.9 It was an elegant idea on a whiteboard and a doomed one in practice. The Reserve Bank of India, via a letter dated October 9, 2019, declined to approve the amalgamation.9 The regulator's discomfort was not hard to read: a real-estate-heavy promoter group taking control of a public deposit-taking bank was precisely the kind of concentration the RBI had spent years trying to prevent, and the proposal was dogged by public-interest litigation alleging fund diversion. LVB itself was collapsing under bad loans and would soon be forced into a rescue merger of its own. The banking dream was dead.

Then 2020 turned a crisis into an existential threat. The near-collapse of Yes Bank and the outright failure of mortgage lender DHFL — another wholesale-funded HFC that imploded amid fraud allegations — poisoned investor sentiment toward any lender with a developer book. COVID-19 froze property sales and raised the specter of mass builder defaults. And the global rating agencies moved: successive downgrades pushed IBHFL's cost of capital toward levels that made profitable lending nearly impossible. A company that had spent a decade as a market darling now traded like a distressed credit, and the question was no longer how fast it could grow but whether it would survive at all.

For investors, this chapter is the permanent asterisk on the Sammaan story. The business very nearly died, and it nearly died not from a single bad loan but from a structural funding model that looked like genius in fair weather and a death trap in foul. Everything that follows — the professionalization, the asset-light pivot, the sovereign rescue — is an attempt to engineer that structural flaw out of the company. Whether it has truly been engineered out, rather than merely papered over with someone else's capital, is the question the rest of this story exists to answer.

V. The Pivot to Survival: Professionalization, Co-Lending, & "De-Promoterisation" (2020–2023)

Survival began, fittingly, by cashing in the one great decision of the good years. Between 2020 and 2021, IBHFL systematically sold down its OakNorth stake, converting that fortunate British bet into hundreds of crores of hard equity capital at the precise moment it needed to reassure lenders and repay maturing bonds without a stumble.8 There is a real lesson here for allocators: a non-core investment, made almost on a whim, turned out to be the liquidity lifeboat that a core business could climb into during its darkest year. Optionality is worth paying for precisely because you cannot predict which asset will save you.

The deeper problem, though, was not capital — it was trust, and trust had a name. As long as Sameer Gehlaut sat atop the company, regulators, rating agencies, and lenders would associate it with the promoter-led, real-estate-entangled, control-obsessed model that the entire post-IL&FS regime was designed to stamp out. So Gehlaut engineered his own removal in what the company openly called "de-promoterisation." In December 2021 he sold roughly half of his holding — about 11.9% of the company — to a set of institutional investors including affiliates of Blackstone, in a deal valued near $184 million, and signaled his intent to leave the board.10 He resigned his board seat in March 2022 and completed the exit of his residual stake by early 2023, leaving IBHFL as something genuinely new in its history: a board-run, professionally-managed institution with no controlling promoter at all.10

Into the operating vacuum stepped Managing Director and CEO Gagan Banga, a company lifer with more than two decades in the group, who now had to answer a brutal question: how do you grow a lender that can no longer fund itself cheaply and can no longer take deposits? His answer was to stop being a balance-sheet hog and start being an origination engine. Under the co-lending and loan-assignment model, Sammaan would source and underwrite a retail home loan or small-business loan, keep a minority slice on its own books, and pass the majority to a partner bank that supplied the low-cost capital. The company earns origination and servicing fees; the partner bank gets priced, ready-made retail assets it would struggle to source on its own. It is capital-light by design — you grow the loans you touch without proportionally growing the debt you owe.

It is worth being precise here, because the company's own numbers are more modest than the slogan. Rather than a blanket "keep 20%, pass 80%," Sammaan has guided that roughly 30% of incremental disbursements flow through the asset-light co-lending and direct-assignment route, executed across a network it says spans two dozen bank and financial-institution relationships and plugged together with fintech rails such as Yubi and Knight Fintech for API-driven integration.1112 The point is directional, not total: the model reduces balance-sheet intensity at the margin, it does not eliminate it. Alongside this, management drew a hard line down the middle of the company, formally separating a "growth book" of new-franchise retail mortgages and small-business loans from a "legacy book" of old developer and wholesale exposures earmarked to be run down, provisioned, or sold to asset reconstruction companies.

By 2023, then, the outline of the modern company was visible: no promoter, a professional board, a capital-light growth strategy, and a legacy book quarantined for disposal. What it still lacked was the one thing a sub-investment-grade wholesale borrower most needs — a deep-pocketed, high-credibility owner who could vouch for it to the funding markets. That owner was about to arrive from the Persian Gulf.

VI. The White Knight from Abu Dhabi: Enter International Holding Company (IHC) (2024–2026)

The first visible act of the new era was symbolic: the name went. In July 2024, Indiabulls Housing Finance Limited formally became Sammaan Capital Limited — "sammaan" meaning respect or dignity — and simultaneously converted its regulatory identity, exiting the housing-finance-company category to register with the RBI as a Non-Banking Financial Company (Investment and Credit Company).56 This was not mere rebranding vanity. Shedding "Indiabulls" severed the last public tie to the promoter era, and moving from an HFC to a broad NBFC license legally widened the product menu from pure mortgages to the full spectrum of retail and business credit the company now wanted to sell. The old identity was a liability; management chose to bury it.

Then came the capital. Abu Dhabi's International Holding Company is not an ordinary strategic investor. It is a sovereign-linked colossus — chaired within the orbit of Abu Dhabi's ruling family, spanning more than 1,300 subsidiaries across technology, infrastructure, financial services, and consumer sectors, with a market capitalization around $233 billion and a portfolio that includes stakes in the Adani group, Haldiram's, and a roster of global technology names.4 Through its affiliate Avenir Investment RSC Ltd, IHC agreed to inject capital into Sammaan via a preferential allotment of equity shares and warrants.3 On March 31, 2026, the transaction closed: Sammaan received an initial tranche of ₹5,652 crore (about $592 million) against equity and an upfront payment on warrants, with a further ₹3,198 crore (about $335 million) to arrive over roughly 18 months as those warrants convert — a total commitment of ₹8,850 crore, one of the largest foreign direct investments ever made into an Indian non-bank lender.34

The ownership arithmetic is more nuanced than a single headline number, and the nuance matters. On closing, Avenir held about 28.5% of Sammaan's equity; management has guided that this rises to roughly 43.5% once the warrants fully convert, with a mandatory open offer to public shareholders (announced at ₹139 per share) potentially lifting IHC's stake as high as 63.3% if fully taken up.313 IHC was classified as the promoter and installed nominee directors — including IHC group CFO Alwyn Crasta — onto a board already chaired by former RBI Deputy Governor Subhash Sheoratan Mundra, with the transaction cleared by the Competition Commission of India and approved by the RBI.131415 The company would sit inside IHC's newly created global financial-services platform, Judan Financial, as its India anchor.3

But the RBI's approval carried a catch that defines the company's entire future, and it deserves to be stated plainly rather than buried in triumphalism. The central bank sanctioned the deal on the explicit condition that Sammaan Capital cannot accept public deposits.15 For a lender whose original near-death experience was caused precisely by its inability to fund itself with sticky retail deposits, this is not a footnote — it is a permanent structural constraint. IHC's billion dollars buys a credibility halo and a capital cushion, and, as the company is quick to note, the chance to piggyback on the UAE's sovereign credit standing.3 What it does not buy is a deposit franchise. Sammaan will remain, by regulatory design, dependent on wholesale bond markets and co-lending partners for every rupee it lends. The new owner solved the trust problem. It did not, and legally could not, solve the funding-model problem. Which brings us to the spectacular way management chose to open the IHC era.

VII. The Colossal Reset: The ₹8,100 Crore "Kitchen Sink" Quarter (Q4 FY26)

There is an old trick in corporate turnarounds known as the "big bath" or "kitchen sink" quarter: when new ownership or new management arrives, throw every conceivable loss, write-down, and provision into a single reporting period, so that the past is buried in one grave and every future quarter can be compared against a cleansed baseline. Sammaan executed one of the most dramatic big baths Indian finance has seen — and it timed it to the day the new owner's money landed.

The numbers are stark. For Q4 FY26, Sammaan reported a consolidated net loss of ₹8,101.41 crore, against a ₹324.04 crore profit in the same quarter a year earlier; for the full year, the loss came to ₹7,144.56 crore.1 Two items did the damage. First, an exceptional loss of ₹6,499.17 crore, representing the mark-downs and wholesale disposal of remaining non-core developer and wholesale assets — the legacy book being dragged out and shot.1 Second, an impairment charge on financial instruments of ₹2,958 crore in the quarter (₹3,627.94 crore for the year), swollen by an additional ₹1,850 crore management-overlay provision layered on under the expected-credit-loss framework.111 In total, the company said it reclassified and cleaned out on the order of ₹14,953 crore of non-core loan assets and investments as part of the transformation.11 A deferred-tax credit of nearly ₹2,000 crore softened the after-tax blow only modestly.1

Here is the analytical crux, and it cuts both ways. The bull reading — which is management's reading — is that Sammaan entered FY27 with a genuinely de-risked, unified opening book of roughly ₹53,160 crore carrying, by the company's disclosure, zero gross and net non-performing assets, a net worth of about ₹18,991 crore, and low gearing of around 2.7 times.11 On the earnings call, Banga framed it as the end of a chapter: the mortgage-anchored book, he stressed, now shows zero net and gross NPAs, freeing management's bandwidth to chase growth rather than firefight the past.1216 If those figures hold, this is a lender that has, in a single violent quarter, converted a decade of buried problems into a clean slate — paid for, conveniently, by IHC's capital arriving the same day.

The skeptic's reading is equally grounded in the disclosures. A "zero NPA" book is not the same as a zero-risk book: the ₹53,160 crore opening AUM still contains roughly ₹10,346 crore of commercial real estate, project, and loan-against-property exposure yielding 12%–17% — the very category of lending that caused the original catastrophe — now heavily provisioned and slated to be co-originated down, but not gone.11 "Zero NPA" here reflects aggressive provisioning and write-offs, not the disappearance of underlying credit. And a ₹1,850 crore discretionary management overlay is, by definition, a judgment call about future losses that management itself controls — exactly the kind of accounting flexibility a skeptical analyst should watch. The kitchen sink cleans the kitchen; it does not prove the house will never flood again. What can be said fairly is that the reset was real, large, and independently visible in the audited statements — and that the credit-rating agencies, at least, believed it, as the next chapter's competitive analysis shows.

VIII. Sammaan's Playbook: Strategic Moats, Competitive Dynamics, & Hamilton Helmer's 7 Powers

Strip away the drama and ask the cold question every long-term investor must ask: once the balance sheet is clean and the sovereign owner is installed, what actually stops the next competitor from doing everything Sammaan does? To answer it, run the business through Hamilton Helmer's 7 Powers and Michael Porter's five forces, because the honest verdict is mixed — and the honesty is the point.

Start with the power management leans on hardest: process power. Sammaan's pitch is that it has built deep, proprietary, API-level integration with partner banks — automated co-lending pipes that let it originate a retail loan and place a slice onto a partner bank's books with a 90%-plus reimbursement turnaround inside roughly a fortnight.12 There is something real here: banks are institutionally slow at sourcing small-ticket, semi-urban retail loans, and Sammaan is fast, so a genuine symbiosis exists. But process power in Helmer's sense requires an advantage that competitors cannot easily copy even if they try, and lending plumbing built on third-party fintech rails like Yubi and Knight Fintech is available to any well-capitalized NBFC willing to build the same connections.11 This is a real operational capability; it is a weak moat.

Scale economies are, at best, medium. Sammaan's distribution reaches into tier-2 and tier-3 India, and the company plans to expand from around 200 branches toward 1,500-plus by FY29 while growing headcount from roughly 4,000 toward 20,000 by FY30.317 Physical density in under-banked geographies is a genuine barrier — it is expensive and slow to replicate. But in mortgages specifically, Sammaan is a minnow beside SBI, HDFC Bank, LIC Housing Finance, and Bajaj Finance, so it does not enjoy the funding-cost scale economics that actually decide who wins prime lending. Switching costs are low: a borrower with a good credit record can refinance a mortgage elsewhere the moment a rival offers 25 basis points less. And network effects are essentially absent — retail lending is a commoditized utility, not a platform that gets better as more people use it.

Porter's forces sharpen the discomfort. The bargaining power of borrowers is high; prime customers have endless, cheaper options. The threat of new entrants is moderated only by the capital and licensing cost of building a real NBFC-plus-branch footprint, which digital-first fintechs are steadily eroding. And the single most important force — the bargaining power of suppliers of capital — is stacked against Sammaan by regulatory design, because a lender banned from deposits is wholly dependent on bond markets and co-lending partners pricing it fairly. This is where IHC's arrival genuinely moved the needle: within roughly 50 days of the investment, all three domestic agencies upgraded Sammaan to AA+/Stable — CRISIL on April 9, CARE on May 12, and ICRA on May 20, 2026 — the company's first domestic upgrade in nearly a decade, and its bond yields reportedly tightened by around 100 basis points.1819

The genuinely durable edge, in other words, is not process or scale — it is the owner. IHC is a source of cheap, credible capital and a global funding halo that competitors cannot simply replicate, and that is the closest thing Sammaan has to Helmer's "cornered resource." The tell is in the ratings hierarchy itself: even after the upgrade wave, S&P Global Ratings lifted Sammaan only to 'BB-' on the international scale in June 2026 — still below investment grade.20 Domestically AA+, internationally junk. The moat, for now, is a rich parent, and a rich parent is a relationship, not a fortress. That distinction is the spine of the investment debate.

IX. The Investment Thesis: Bull vs. Bear Case, Risks, & KPIs

Imagine two investors on opposite sides of the same table, both staring at the same cleaned-up balance sheet and the same billion dollars. Their disagreement is the whole thesis.

The activist skeptic speaks first. Her central attack is the cost-of-capital handicap, and it is not theoretical. Management's own FY27 guidance projects a cost of funds around 9.3% and a net interest margin of just 3.5%, rising only gradually thereafter.17 On the earnings call, analysts pressed exactly this point, and management conceded that the decline in funding costs would be slow, because much of the existing debt is fixed-rate, non-callable paper that cannot be repriced simply because the rating improved.16 So how, she asks, does a lender paying 9%-plus for money win prime mortgages against banks funding themselves with 4%-cost deposits? The honest answer is that it cannot win on price in prime — which is precisely why management is pushing into higher-yielding gold loans, unsecured personal loans, and small-business credit yielding 11%–16%.1117 But that pivot walks Sammaan straight into the guns of Muthoot Finance in gold and Bajaj Finance in unsecured retail — seasoned specialists with decade-plus underwriting data — and unsecured lending carries delinquency risk an order of magnitude above prime home loans. Diversification into higher margin is also diversification into higher loss, executed by a team whose historical competence is mortgages.

She has two more darts. Concentration risk: if even one or two large co-lending partners retrench for their own balance-sheet or regulatory reasons, Sammaan's asset-light origination volume can drop overnight, because it does not own the funding. And the accountability question: this is the same management franchise that presided over the near-death of 2018–2020, and its FY30 targets — roughly ₹1,94,000 crore of AUM, ₹5,600 crore of profit, and an 18.7% return on equity, versus an FY27 starting ROE of just 6.8% — require nearly tripling the balance sheet and quadrupling profitability in four years.17 A skeptic reads that as the same growth-at-all-costs ambition that caused the original crisis, now underwritten by someone else's money.

The bull answers, and his case is not weak. The balance sheet is, right now, cleaner than it has been in the company's entire modern history — zero reported NPAs on a unified book, gearing near 2.7x against a self-imposed ceiling of 3.5x–4x, and capital adequacy management pledges to hold above 20%.1117 IHC's backing is not a slogan: it produced a real, agency-validated rating upgrade and a measurable ~100 bps of bond-yield compression, both of which directly lower the cost handicap the skeptic fears.1819 The asset-light model, if it holds to its ~30%-of-disbursals design, lets Sammaan grow AUM without proportionally ballooning debt — high operating leverage over a fixed origination platform.11 And there is genuine optionality in being IHC's India financial-services anchor inside the Judan platform: access to global capital, technology, and potentially inorganic deals that a standalone NBFC could never reach.3

So what should a fundamental investor actually watch — not compute, but monitor over the coming years? Three KPIs cut through the noise:

- Growth-book AUM and disbursement momentum. The FY27 plan calls for ₹30,100 crore of disbursals and AUM climbing toward ₹70,700 crore; growth AUM was roughly ₹44,038 crore, about 70% of the book, at the transition.1217 If sourcing volumes miss, the entire compounding story stalls at the first step.

- Cost of funds versus net interest margin. This is the crux of the whole handicap. Watch whether the rating-driven yield compression actually flows into a falling blended cost of funds and an expanding NIM — or whether, as management admitted, legacy fixed-rate debt keeps margins pinned for years.1617

- Asset quality in the new, higher-yield segments. As unsecured, gold, and MSME lending scale, the honest test is whether credit costs stay contained or whether the reach for yield reproduces, in miniature, the loss experience the company just spent ₹8,101 crore burying.11

The bull and bear do not actually disagree about the facts. They disagree about whether a rich owner and a clean slate are enough to overcome a permanent funding disadvantage in businesses full of incumbents. That is a question only execution, quarter by quarter, can settle.

X. Conclusion & Lessons for Founders

Stand back from the ledgers and the sovereign-wealth theatrics, and Sammaan Capital leaves behind a few durable lessons — the kind that outlast any single quarter's headline loss.

The first is about the price of survival, and who pays it. Sameer Gehlaut built a mortgage empire and then had to erase himself from it — board seat, shares, and famous name — because in the post-IL&FS world his continued control was the single biggest obstacle to the cheap funding and regulatory goodwill the company needed to live. For a founder, that is the hardest lesson of all: sometimes the most valuable thing you can do for the institution you built is to leave it entirely. De-promoterisation was not a defeat inflicted on the company; it was, arguably, its salvation.

The second is about capital allocation and the value of optionality. The OakNorth investment — a strange, non-core punt on a British digital bank — returned roughly 48% a year and became the liquidity lifeboat that helped the company survive its worst years.8 You cannot predict which bet will save you, which is exactly why disciplined, opportunistic optionality is worth carrying. The flip side is the cautionary tale of the golden-age dividends: distributing capital aggressively while running a wholesale-funded balance sheet left the company with no cushion when the short money vanished. Generosity in fair weather bought fragility in foul.

And the third is the open question the company now embodies. Sammaan Capital enters its next chapter as something genuinely novel in global finance: a shadow bank that is legally forbidden from taking public deposits, owned by an Abu Dhabi sovereign-linked conglomerate, run by professional managers, and operating in large part as an outsourced origination engine for other people's balance sheets. Management's own targets are unambiguous — a top-three NBFC position by FY29, high-teens returns on equity by FY30, a fifteen-product full-suite lender.317 Those are aspirations backed by a real capital cushion and a real cleanup, not fantasies. But they are aspirations set by a team that has promised discipline before, and the permanent handicap of a banned deposit franchise has not gone anywhere.

The phoenix, in the myth, rises from its own ashes reborn and immortal. Sammaan Capital has certainly burned — ₹8,101 crore of its own past, in a single deliberate quarter, to clear the ground for a new beginning. Whether what rises is a durable compounding machine or simply a better-funded version of the same cyclical, funding-constrained lender is not something any narrative can settle in advance. It is something the next several years of disbursements, funding costs, and credit losses will decide — and it is exactly what a serious long-term investor should be watching for.

References

-

Consolidated Income Statement, Q4 & FY26 Investor Presentation — Sammaan Capital, 2026-05-20 ↩↩↩↩↩

-

Sammaan Capital Q4 FY26 results: Rs 8,101 crore loss, stock rises 7% on balance sheet cleanup — Business Upturn, 2026-05-21 ↩

-

Sammaan Capital Becomes an IHC Group Company (Press Release) — Sammaan Capital, 2026-03-31 ↩↩↩↩↩↩↩↩↩

-

About IHC — A Permanent Strategic Partner, Q4 & FY26 Investor Presentation — Sammaan Capital, 2026-05-20 ↩↩↩

-

Indiabulls Housing Finance changes name to Sammaan Capital — BestMediaInfo, 2024-07 ↩↩

-

Indiabulls Housing Rebrands as Sammaan Capital — SMEStreet, 2024-07 ↩↩

-

Indiabulls Housing raises Rs 1,205 cr via QIP, stake sale in OakNorth — Business Standard, 2020-09-14 ↩↩

-

Indiabulls Housing Finance exits OakNorth Holdings — Outlook India, 2021 ↩↩↩

-

RBI rejects proposed merger of Indiabulls and Lakshmi Vilas Bank — ThePrint, 2019-10-09 ↩↩

-

Indiabulls Housing: Sameer Gehlaut Sells Half His Stake, Plans on Exiting the Board by Fiscal End — The Wire, 2021-12 ↩↩

-

Fully De-risked Book, Portfolio Guardrails & Product Portfolio, Q4 & FY26 Investor Presentation — Sammaan Capital, 2026-05-20 ↩↩↩↩↩↩↩↩↩↩

-

Sammaan Capital Q4 FY26 Earnings Call Highlights — Investing.com / GuruFocus, 2026-05-20 ↩↩↩↩

-

Shareholding Pattern & Transaction Update, Q4 & FY26 Investor Presentation — Sammaan Capital, 2026-05-20 ↩↩

-

CCI approves the acquisition of certain shareholding of Sammaan Capital Limited by Avenir Investment RSC Ltd — Press Information Bureau, Government of India ↩

-

RBI Approves Avenir Investment's Sammaan Capital Stake With Conditions — Whalesbook, 2026-03 ↩↩

-

Sammaan Capital Ltd Q4 2026 Earnings Call: Negative Points & Analyst Concerns — Investing.com / GuruFocus, 2026-05-20 ↩↩↩

-

Business Projections FY27–FY30 & FY30 Targets, Q4 & FY26 Investor Presentation — Sammaan Capital, 2026-05-20 ↩↩↩↩↩↩↩↩

-

Rating Upgrade & CoF Compression, Q4 & FY26 Investor Presentation — Sammaan Capital, 2026-05-20 ↩↩

-

CRISIL upgrades Shriram Finance to AAA, Sammaan Capital to AA+ rating — Business Standard, 2026-04-10 ↩↩

-

Sammaan Capital Upgraded To 'BB-/B' On Likely Improvement — S&P Global Ratings, 2026-06-02 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube