Sai Parenterals: The Indo-Australian Pharma Gamble

I. Introduction & Episode Roadmap

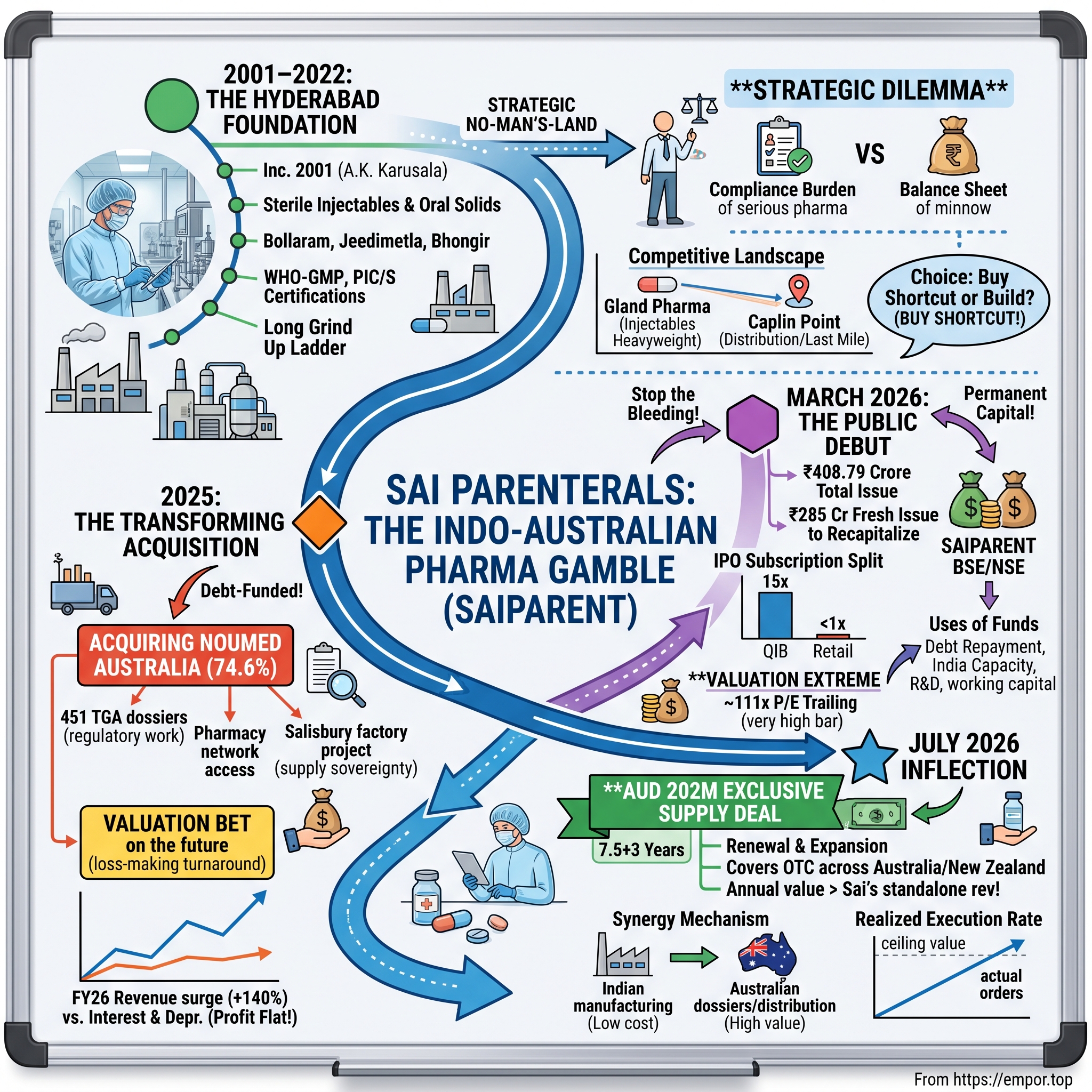

Picture a mid-sized industrial shed in Jeedimetla, on the grimy northern edge of Hyderabad, where the air smells of solvent and the fluorescent lights never quite go off. Inside, gowned technicians move through airlocks into cleanrooms held at higher pressure than the corridor outside, filling glass vials with sterile liquid that must be free of a single stray particle or a trace of bacterial endotoxin. For nearly a quarter of a century, this was the entire universe of Sai Parenterals — a diligent, unglamorous contract maker of injectable medicines, the kind of company that supplies government hospitals and quietly compounds antibiotics for brands whose names you actually recognize.

Then, over roughly eighteen months, this obscure small-cap did something that companies ten times its size rarely attempt. With standalone revenue of just ₹163 crore — under $20 million — it reached across the Indian Ocean and bought a controlling stake in an Australian pharmaceutical distributor for about ₹125 crore.15 It funded that leap with expensive short-term debt, watched its interest bill swell and flatten its profits, then rushed to the public markets in March 2026 to raise fresh capital and pay the debt down.89 And in July 2026, just weeks after listing, its new Australian arm signed an exclusive over-the-counter supply contract worth AUD 202 million — roughly ₹1,300 crore — whose annual run-rate alone exceeds everything the parent company earned in a year.67

That is the hook of this story, and it deserves skepticism as much as admiration. Because the interesting question is not whether Sai Parenterals pulled off a dramatic transformation — it plainly attempted one — but whether the transformation is the durable creation of value it is being sold as, or a leveraged bet whose bill has simply been deferred.

The paradigm shift here is worth naming precisely. The conventional Indian pharma playbook is patient and organic: a contract manufacturer slowly climbs the value chain, files its own dossiers in regulated markets, earns approvals over a decade, and gradually captures more of the margin. Sai Parenterals chose the opposite. Rather than build its way into a premium regulated market, it decided to buy the last mile — the regulatory registrations and the retail distribution relationships that are the scarce assets in global generics. Manufacturing, in this worldview, is the commodity; the dossier and the shelf space are the moat.

Here is the roadmap for how we will interrogate that thesis:

- The Hyderabad Foundation (2001–2022): How a sterile-injectables capability got built in India's pharma capital, and why that discipline matters.

- The Competitive Jungle: Benchmarking Sai against Gland Pharma and Caplin Point Laboratories to locate its real position.

- The Transforming M&A (2025): The acquisition of Adelaide-based Noumed Pharmaceuticals, and whether the price was strategic or reckless.

- The Public Listing & Deleveraging (2026): Going public at an eye-watering multiple to unwind the acquisition debt.

- The July 2026 Validation: Deconstructing the AUD 202 million supply contract and its economics.

- The Playbook & Analysis: Porter's Five Forces, Hamilton Helmer's Seven Powers, and an honest bull-versus-bear ledger.

Let us begin where every sterile-injectables story in India seems to begin — in Hyderabad.

II. The Hyderabad Hub & Founding Context (2001–2022)

There is a reason so many of India's drug stories are set in and around Hyderabad, and it is not romantic. In the 1980s and 1990s, the erstwhile state of Andhra Pradesh made a deliberate industrial bet on bulk drugs — the active pharmaceutical ingredients that are the raw chemistry of medicine — clustering them in industrial estates like Jeedimetla and Bollaram on the city's outskirts. Over time, an ecosystem thickened around that base: fermentation and synthesis expertise, a labor pool of chemists and microbiologists trained at local universities, proximity to solvents and intermediates, and later the marketing of "Genome Valley" as a life-sciences corridor. If you wanted to manufacture medicine in India cheaply and at scale, Hyderabad was the obvious address.

There is a second, quieter reason Hyderabad matters to a story like this one. India's rise as the "pharmacy of the world" — the source of a large share of the generic medicines consumed across Africa, Latin America, and the West — was built on a specific arbitrage: world-class chemistry and manufacturing discipline at a fraction of Western labor and capital cost. Hyderabad sat at the center of that arbitrage. A company incubated there inherited not just cheap production but a labor market fluent in the grammar of international regulatory audits, a network of contract testing labs, and a cultural expectation that the ambitious end game was always export — selling into the regulated markets of the US, Europe, and Australia, where the same pill fetches many times its domestic price. Sai Parenterals was, from birth, a company whose geography pointed it outward.

Into that ecosystem, in January 2001, Anil Kumar Karusala incorporated Sai Parenterals as a private limited formulations company.15 The name itself signals the ambition — parenteral refers to medicine delivered by injection, bypassing the digestive tract — and it hints at a founder who chose the hard road from the start. Anyone can, with enough capital, press tablets. Making sterile injectables is a different discipline entirely.

Consider what the word "sterile" actually demands. An oral tablet that carries a few microbes will usually be neutralized by stomach acid. A vial of injectable liquid, pushed directly into a patient's bloodstream, has no such backstop; a single contaminant can kill. So sterile manufacturing means aseptic filling rooms held under positive pressure, HEPA-filtered air, rigorous gowning protocols, validated sterilization cycles, and obsessive control of two invisible enemies — particulate matter and bacterial endotoxins, the fever-inducing debris that dead bacteria leave behind. The machinery is precise and expensive, the batch-failure rates unforgiving, and the regulatory scrutiny relentless. This is the "extreme cleanroom discipline" that separates injectables from the rest of generic pharma, and it is the source of whatever structural advantage Sai possesses.

A useful analogy for the non-specialist: an oral-solids plant is like a bakery, where cleanliness matters but the oven's heat forgives many sins. A sterile-injectables plant is closer to a semiconductor fab, where a single particle of dust in the wrong place ruins the product, where the environment itself is the product, and where the difference between a passing and a failing batch can be invisible to the naked eye. That is why the machines cost what they cost, why the people must be trained the way they are trained, and why a regulator's inspection is less a checklist than an audit of an entire culture. It is also why, once a company has genuinely mastered aseptic processing, the mastery is not easily copied — you cannot buy it at a trade show or hire it away in a quarter. The flip side, which the bulls tend to skip past, is that this same discipline is a permanent tax: the cost of maintaining sterility never goes away, and an idle sterile line still burns money keeping its cleanrooms qualified.

The company's climb, by its own telling, was a long grind up a ladder of certifications. It moved from basic domestic Good Manufacturing Practice toward the WHO-GMP standard that opens up institutional and export tenders, and eventually to the demanding PIC/S regime — the Pharmaceutical Inspection Co-operation Scheme — whose approval is a passport into stringently regulated markets.3 Each rung took years and capital, because a certification is not a plaque on the wall; it is a state of continuous compliance that an inspector can revoke.

In January 2022, Sai Parenterals converted from a private to a public limited company.15 On paper this is a dry administrative step. In practice it is the moment a founder-run shop begins dressing for institutional capital — cleaning up its governance, formalizing its board, and setting the stage for the liquidity event that would eventually arrive four years later. The timing is telling. A company that spent two decades as a quiet private manufacturer does not restructure itself for public markets on a whim; the 2022 conversion signals that, well before the Noumed deal was conceived, the founders had already decided the next chapter would require outside capital and public currency. In hindsight, it reads as the first move in a longer sequence — convert, acquire, list — executed with more strategic patience than the frenetic 2025–2026 headlines might suggest.

That the whole sequence traced back to one man is both the company's strength and its central governance question. Anil Kumar Karusala had spent more than three decades in pharmaceuticals before Sai's transformation, and the business bears the marks of a founder-operator rather than a professional-manager committee: concentrated ownership, decisive and unhedged bets, and a willingness to lever the balance sheet in pursuit of a vision that a more risk-averse board might have vetoed.2 Founders of this type — the ones who make a single, career-defining wager — are precisely the people who build outsized businesses and precisely the people who occasionally sink them. There is no diversification of judgment to fall back on; the company is, in a real sense, a leveraged bet on one person's reading of the global generics market. For minority investors, that is the deal on offer, and it should be accepted or declined with clear eyes rather than pretended away.

The people running it remained tightly held. Anil Kumar Karusala serves as Chairman and Managing Director, and the company credits him with more than three decades in the industry.2 He is supported by Whole-time Director Vijitha Gorrepati, whose remit centers on procurement and technical operations, and by Non-Executive Director Karusala Aruna — the three of them the named promoters of the business.29 Before the IPO diluted them, the promoter group held roughly 61.23% of the equity, an unusually concentrated stake for a listing-stage company.

That concentration cuts both ways, and an honest investor should hold both edges at once. High promoter ownership means genuine skin in the game — the family's wealth rises and falls with minority shareholders', which is precisely the alignment you want. But it also means that the audacious capital-allocation decisions to come — the debt-funded foreign acquisition, the aggressive guidance — flowed from a very small circle with very little external check. When founders own most of the company and also make every big call, the quality of the business becomes almost entirely a bet on the quality of their judgment. Which is exactly why the next question — what, precisely, does this company make and sell? — matters so much.

III. The Core Business: Branded Generics vs. CDMO Services

Walk the floor of a Sai Parenterals plant and you are really looking at two businesses wearing the same uniform. The first is a branded generics operation that sells finished medicines into India's vast public and private healthcare system. The second is a contract development and manufacturing organization — a CDMO — that makes batches to order for other pharmaceutical brands, domestic and global. The company's own framing is that it produces "injectables, tablets, capsules, syrups, and ointments for India and export markets," split across those two revenue streams.16

The branded-generics side supplies central and state government procurement agencies, hospitals, and pharmacies, concentrated in bread-and-butter therapeutic areas: cardiovascular drugs, neuropsychiatry, anti-diabetics, and anti-infectives. It is high in volume and vital to public health — and, as we will see, structurally low in margin, because selling into government tenders means competing largely on price against a crowd of equally certified rivals. To understand why this business is such a grind, picture the mechanics of a government drug tender: a procurement agency publishes a requirement for, say, several million vials of a common antibiotic; a dozen certified manufacturers bid; the lowest compliant price usually wins; payment then arrives on the government's own unhurried schedule, sometimes many months later. The manufacturer funds the raw materials and production up front and waits to be paid — which is why this business is described, accurately, as working-capital-intensive. It keeps the plant busy and the brand visible, but it ties up cash and earns thin margins. It is the definition of revenue that is easy to grow and hard to profit from.

The CDMO side is the more interesting strategic asset, because it embeds Sai in the supply chains of larger brands that prefer to outsource the capital-intensive, compliance-heavy work of sterile filling. When a branded pharmaceutical company does not want to build and maintain its own aseptic lines — or wants surge capacity, or a lower-cost source — it contracts a partner like Sai to make batches to its specification. The value here is stickier than in tender supply: qualifying a contract manufacturer is a lengthy, audited process, so once a brand has approved a partner's line for a given product, it is reluctant to re-qualify a new one for a marginal price saving. That reluctance is a modest form of switching cost, and it is the seed of whatever pricing power Sai's manufacturing enjoys. There is early evidence the export ambition is real rather than aspirational: the group has secured overseas institutional business, including a reported anti-tuberculosis supply order worth around ₹104.5 crore from the Philippines — a reminder that even before the Australian gambit, Sai was reaching for regulated and semi-regulated export markets rather than resigning itself to domestic tenders.7

The physical footprint tells the story of specialization. Unit I, in Jeedimetla, handles sterile non-beta-lactam injectables — the vials, ampoules, and pre-filled syringes that are the technical heart of the company.3 Unit II, also in Jeedimetla, is dedicated to sterile penicillin dry-powder injectables, physically segregated because beta-lactam antibiotics like penicillin can cross-contaminate and trigger dangerous allergic reactions if they mingle with other drugs. Unit III, in Bhongir on the Hyderabad–Warangal highway, makes oral solids, liquids, and ointments — and crucially, it carries the TGA (Australia) and PIC/S approvals that would later become the linchpin of the entire international strategy.3 Unit IV, in Bollaram, produces cephalosporin formulations, another antibiotic class that demands its own dedicated line. And through a subsidiary, Revat Laboratories in Ongole, Andhra Pradesh, the group runs high-volume generic oral solids. In all, five facilities with a combined installed capacity reported at 1,160 million units a year on a single-shift basis as of March 2025.16

Now, the moat argument — and it deserves to be stated fairly, then tested. The bull case is that sterile injectables are structurally superior to oral solids because the barriers to entry are so much higher. Anyone can build a tablet line; almost no one can build and maintain a sterile injectable line that passes a US FDA or TGA inspection. Sterility assurance, endotoxin limits, particulate control — these require heavy, ongoing capital and a culture of discipline that takes years to instill and one bad audit to destroy. Where that discipline exists, pricing power follows, because the customer is buying reliability as much as the molecule.

The role of the Revat Laboratories subsidiary in Ongole is instructive on this point. Adding a dedicated high-volume oral-solids facility to a group whose distinctive edge is sterile injectables is a choice worth questioning. Oral solids are the commoditized end of the business — exactly the segment where scale players win on cost and a sub-scale entrant earns thin returns. A skeptic would ask whether that capital might have been better concentrated on the sterile lines where Sai actually has a defensible position, rather than spread across the very dosage forms where it does not. It is a small but revealing example of the build-everything instinct that recurs throughout this company's history.

Here is where an independent lens has to push back. Possessing the certifications is necessary but not sufficient; the harder question is utilization. A plant approved for 1,160 million units that runs well below capacity is not a moat — it is a fixed-cost anchor. And Sai's numbers point in exactly that direction. In FY25, the standalone business generated an EBITDA margin of about 24% and a strikingly high return on capital employed near 29%, which suggests the sterile assets, when running, are genuinely productive.16 But the domestic institutional business — the government-tender volume — is admitted even by sympathetic analysts to be low-margin and working-capital-hungry, the kind of revenue that keeps the lines busy without generating much cash. The evidence check, then, is mixed: real technical capability, real certifications, but a revenue mix still tilted toward the least profitable end of what those capabilities could earn.

Which frames the central tension of the whole story. A company with a genuine but under-monetized manufacturing edge, stuck selling too much of its output into commoditized domestic tenders, has two choices. It can slowly, organically earn its way into premium regulated markets — or it can try to buy a shortcut. To understand why management chose the shortcut, we have to look at the competitive jungle it was trapped in.

IV. The Strategic Dilemma & The Competitive Landscape

Every small pharmaceutical company in India eventually runs into the same wall, and it has a shape. Below a certain size — call it the ₹200-crore-revenue frontier — a firm is caught in a strategic no-man's-land. It is too small to command the scale economies, the multinational relationships, or the regulatory bandwidth of the global champions. Yet it is large enough, and certified enough, to attract the full weight of regulatory scrutiny, without the margins to comfortably absorb it. You get the compliance burden of a serious pharma company with the balance sheet of a minnow. That, in a sentence, was Sai Parenterals' dilemma.

To feel the gap, war-game Sai against the two companies it is most often measured against. The first is Gland Pharma — the undisputed heavyweight of Indian injectables. Gland is a different order of animal: FY25 operating revenue of roughly ₹5,616 crore, an EBITDA margin around 26%, and a spotless track record with the US FDA that anchors deep, long-run relationships with multinational pharma.16 Gland's game is a business-to-business injectables engine built on massive scale and regulatory credibility — the "shortest path to market" for global partners who want a reliable Indian factory. Sai, at roughly one-thirtieth of Gland's revenue, simply cannot meet Gland on that battlefield. There is no version of a head-to-head capacity war that Sai wins.

There is a subtler point buried in the Gland comparison that is easy to miss. Gland's return on capital employed in FY25 was in the mid-teens, while Sai's standalone ROCE was reportedly close to 29%.16 At first glance that flatters Sai — it appears to earn far more per rupee of capital than the giant. But the honest reading is more nuanced: high ROCE on a tiny capital base is common and fragile, and Sai's entire strategy from here involves deploying much more capital — into Indian capacity, an R&D center, and an Australian plant. The relevant question is not what Sai earned on its small historical asset base, but what it will earn on the vastly larger one it is now building. Scaling a business almost always compresses those glittering small-company returns; the test is how far.

The second benchmark is more instructive, because it points to the strategy Sai actually chose. Caplin Point Laboratories built a highly profitable empire — revenue well past ₹1,500 crore — not by fighting the giants in the most regulated markets, but by avoiding them. Caplin's insight was that in generics, the scarce asset is often not manufacturing but distribution. It went to markets that global players ignored — Latin America, Francophone Africa — and there it did not merely sell drugs; it owned the last mile, controlling the registrations and the on-the-ground distribution that let it capture the full margin from factory to pharmacy shelf. Caplin proved that a mid-sized Indian company could earn premium economics if it controlled who the customer buys from, not just what gets made.

It is worth dwelling on why distribution, and not manufacturing, became the prize — because it is counterintuitive to anyone raised on the idea that "making things" is where value lives. In a mature generic market, dozens of factories can make the same molecule to the same standard. What they cannot easily do is place that molecule on a pharmacy shelf under a trusted label with a registration already in hand. The pharmacy chain does not want to manage forty supplier relationships and forty regulatory files; it wants one reliable partner who handles the registration, the quality, the recalls, and the logistics, and who shows up on time every time. Whoever becomes that partner captures a durable position that the manufacturers upstream can only supply into, never bypass. Caplin understood this a decade early. Sai's leadership, studying the same map, decided the Australian version of that position was for sale — and that buying it beat building it.

That is the lens through which the entire Noumed gamble makes sense. Sai's management looked at these two models and, implicitly, chose Caplin's over Gland's. It concluded that grinding out more low-margin domestic tenders was a dead end, and that the prize lay in the highly regulated, premium-priced markets — Australia and New Zealand first, with Europe and the US as distant ambitions — where a molecule that sells for a rupee in an Indian government tender can sell for a multiple of that on a Western pharmacy shelf.

The obstacle was time. Organically entering the Australian market means filing dossiers with the Therapeutic Goods Administration, waiting out review queues, building relationships with pharmacy buyers who have no reason to trust a new Indian supplier, and doing all of it over the better part of a decade. Sai's leadership decided it did not have a decade. Rather than earn its way into the last mile, it would buy it — acquiring, in one transaction, a portfolio of Australian registrations and an existing seat at the table with the pharmacy networks.

It is a genuinely bold reading of the competitive map, and it is also where the risk begins. Buying the last mile is only value-creating if you do not overpay for it, and if the asset you buy is actually the moat it appears to be. So the question that hangs over the rest of this story is simple and unsentimental: did Sai Parenterals buy a shortcut, or a liability? To answer it, we have to open up the deal itself.

V. The Transforming Gamble: Acquiring Noumed Australia (2025)

In November 2025, a company most Australian pharmacists had never heard of quietly changed hands. Sai Parenterals, operating through a newly minted Singapore holding vehicle called Sai Parenterals Pte Ltd, acquired a controlling 74.6% stake in Noumed Pharmaceuticals Pty Ltd of Adelaide.57 The reported price was about ₹125 crore — roughly $13.9 million — funded through a mix of equity and, more consequentially, a large slug of high-cost short-term debt.5

So who, exactly, was Noumed, and why would a Hyderabad injectables maker want it? Noumed traced its lineage to the UK's Noumed Life Sciences, and had grown into a commercial platform for generic and over-the-counter medicines across Australia and New Zealand — a supplier of private-label OTC products to the pharmacy chains that dominate the Antipodean drug retail landscape. Its chief executive, Mark Thulborne, would later frame the business in the language of relationships rather than products, emphasizing Noumed's record of building "lasting customer relationships" and delivering "quality products on time" — the vocabulary of a distributor whose real asset is trust, not a molecule.6 On its own, that is a modestly interesting distribution business. What made it strategically valuable were two assets that money normally cannot buy quickly.

The first was a portfolio of 451 established product dossiers — the completed regulatory registrations that permit a specific medicine to be sold in Australia. Each dossier represents years of filing, testing, and TGA review that Sai would otherwise have had to replicate one molecule at a time. Buying 451 of them at once was, in effect, buying a decade of regulatory work off the shelf. The second asset was a bet on the future: Noumed was building a state-of-the-art manufacturing facility at Salisbury, in Adelaide's north, with a reported investment of around AUD 53 million — a plant explicitly positioned to serve Australia's growing appetite for "domestic supply sovereignty," the post-pandemic political preference for medicines made locally rather than imported.6

The "domestic supply sovereignty" angle deserves a moment, because it is more than marketing. The COVID-19 pandemic taught every developed country an uncomfortable lesson about how much of its essential medicine supply depended on a handful of factories in India and China, and how quickly export bans and freight chaos could turn a supply chain into a national-security problem. Australia, an affluent country at the far end of most supply lines, felt this acutely. Governments across the developed world began to prize local pharmaceutical manufacturing — even at a cost premium — as a form of resilience. A plant physically located in Adelaide, making medicines on Australian soil, is therefore worth more than its unit economics alone would suggest: it can win preference in government and pharmacy procurement precisely because it is local. Noumed's Salisbury project was a bet on that political tailwind, and in acquiring it, Sai was buying a call option on it too.

That combination — established registrations, existing pharmacy relationships, and a soon-to-be-local factory — is the "last mile" Sai could not build organically. On the logic of the Caplin playbook, it is a coherent purchase.

But a coherent strategy can still be a bad deal, and here the independent lens has to bear down. Noumed was loss-making at the time of the acquisition, weighed down by high overheads and the enormous capital expenditure of building the Salisbury plant. Sai did not buy a cash cow; it bought a cash-consuming turnaround with strategic optionality attached. And it paid for that turnaround with borrowings that immediately began to bite.

The financial arithmetic of FY26 is where the gamble's cost shows up in stark relief. As Noumed was partially consolidated into the group, reported revenue surged roughly 140% to about ₹381 crore.8 On the surface, spectacular growth. But look one line down. Interest expense climbed to roughly ₹18 crore and depreciation to about ₹17 crore — the twin costs of a debt-funded acquisition of an asset-heavy, loss-making business.8 The result was that consolidated net profit stayed essentially flat: around ₹14 crore in FY26 against about ₹14 crore in FY25.8 The company more than doubled its revenue and earned no additional profit for shareholders.

So did they overpay? The honest answer is that "overpay" is the wrong frame for an asset like this, and getting the frame right is the whole discipline. ₹125 crore for a loss-making distributor with a half-built plant looks expensive if you value Noumed as a standalone earnings stream — because there were no earnings, only losses. It looks cheap if you value what Sai actually bought: 451 ready-made TGA registrations, an incumbent relationship with a dominant pharmacy network, and a locally-built manufacturing option in a country prizing supply sovereignty. The trouble is that the second valuation is almost entirely a judgment about the future, not a multiple of the past. There is no clean market price for "a decade of regulatory work plus a seat at the table," which means the deal cannot be proven fair or foolish on the day it closed — only in hindsight, as the acquired assets either throw off the cash that justifies the price or fail to. What can be said with confidence is that Sai paid a real, cash-and-debt price today for a bundle of optionality that will only be worth something tomorrow, and it financed that bet in a way that left no room for the optionality to disappoint on schedule.

This is the moment that separates the bulls from the bears. To a skeptic, FY26 is the very picture of value-destructive empire-building: a small company borrowed aggressively to buy a bigger, loss-making foreign business, inflated its top line, and delivered zero incremental profit while loading the balance sheet with risk. To a bull, FY26 is simply the trough of a deliberate transformation — the year the costs of the leap all land before any of the benefits arrive. Both readings fit the same numbers. What neither can escape is that, as of the acquisition, Sai had converted a modestly profitable domestic manufacturer into a leveraged, loss-absorbing, cross-border group whose survival now depended on quickly refinancing that debt. And there was really only one way to do that at speed — sell shares to the public.

VI. The Public Debut: March 2026 IPO & Deleveraging Strategy

The timing was not a coincidence; it was the plan. Having taken on expensive debt to swallow Noumed, Sai Parenterals needed a source of cheaper, permanent capital to stop the bleeding — and it needed it fast. The public markets were the exit valve. The company filed its draft red herring prospectus on October 1, 2025, with Arihant Capital Markets as book-running lead manager, and moved to its public offering the following spring.9

The mechanics were straightforward. The IPO carried a price band of ₹372 to ₹392 per share, and the total issue came to about ₹408.79 crore — a fresh issue of ₹285 crore plus an offer-for-sale of ₹123.79 crore.16 One detail in that split deserves emphasis, because it is a genuine governance positive that the promotional narrative tends to blur: the offer-for-sale was shares sold by non-promoter investors cashing out, not by the founding family.16 The promoters did not use the listing to reduce their own control or take money off the table — they diluted only through the fresh issue, from roughly 61% pre-IPO toward about 51% afterward.8 Founders who hold their stake through a listing rather than selling into it are, at minimum, behaving consistently with the "skin in the game" they advertise.

The subscription told a more sober story than the headline transformation suggested. The issue was subscribed only about 2.05 times overall — a tepid result by the standards of a hot Indian primary market, where genuinely coveted small-cap issues routinely clear dozens of times over.11 The composition of that demand is revealing. Qualified institutional buyers — the mutual funds and professional investors who are supposed to do the deepest diligence — bid nearly 15 times their allotment, a strong vote of confidence from the smart-money end of the room. Retail investors, by contrast, did not even fill their reserved portion, and the non-institutional (high-net-worth) category was barely covered.11 Read together, that split says something specific: the professionals who understood the cross-border thesis were willing to underwrite it, while the broader public — often drawn to IPOs by grey-market froth and listing-pop expectations — stayed away from a stock that offered little obvious short-term upside at its demanding price. The shares listed on the BSE (scrip code 544742) and NSE under the ticker SAIPARENT on April 2, 2026, opening at a modest premium of only two to three percent over the issue price.410 For a company selling a dramatic international growth story, the market's shrug at listing was itself a data point — the crowd was not paying up for the narrative.

The reason for that caution sits in the valuation, and it is the sharpest edge of the bear case. At the offer price, Sai was asking investors to pay an implied price-to-earnings multiple of roughly 111 times — annualized off its first-half FY26 numbers.16 Put that beside Gland Pharma, the sector's blue-chip, trading at around 45 times earnings, and the gap is jarring.16 Investors were being asked to pay more than twice the multiple of a company thirty times Sai's size, with a flawless regulatory record and vastly greater scale, to own a small-cap whose net margins had just been flattened by acquisition debt. On any conventional yardstick, that is an expensive stock priced for a transformation that had not yet been proven.

One should also be fair about the counter-argument to that bearishness, because valuation on trailing earnings can genuinely mislead for a company in the middle of a step-change. If the FY26 profit was artificially suppressed by one-time-in-nature acquisition costs — the interest on debt about to be repaid, the depreciation on a plant not yet earning — then the trailing P/E is measuring the stock against a deliberately depressed denominator. Bulls would argue the honest multiple is the forward one, computed against the earnings the deleveraged, contract-fed business can produce. That is a legitimate frame. It is also, notably, an act of faith in numbers that did not yet exist at listing — which is precisely why a disciplined investor treats a 100-times trailing multiple not as a death sentence but as a very high bar the company must clear, quarter by quarter, to justify the price already paid.

What the fresh capital was for, however, was defensible on its own terms — because the primary object of the offer was, bluntly, to undo the mess the acquisition had created. Debt repayment was an explicit use of proceeds, aimed at retiring the high-cost borrowings that were burning through the income statement.9 The disclosed split of the fresh issue is worth reading closely, because it reveals management's real priorities: roughly ₹110.8 crore for capacity expansion and manufacturing upgrades, about ₹18 crore for a research-and-development center, around ₹33 crore for working capital, roughly ₹20 crore for debt repayment, and a tranche of about ₹36 crore channeled through the Singapore subsidiary to fund the Noumed investment.9 Notice the shape of that allocation. The single largest use is not deleveraging at all — it is more capacity. For a company whose existing plants were already reportedly under-utilized, and whose interest burden was the acute problem, choosing to spend more on new bricks than on paying down debt is a statement of temperament. It tells you this is a management team wired to build and expand, not to consolidate — a disposition that is thrilling if the demand materializes and dangerous if it does not. Management's pitch, in essence, was that the IPO was a recapitalization plus a war chest — a reset button on the debt, and fuel for the next leg of growth.

That pitch rested entirely on one assumption: that Noumed would deliver enough real, profitable business to justify the debt taken on to buy it. For most of FY26, that assumption was an act of faith. Then, in the first week of July 2026, it stopped being faith and became a signed contract.

VII. The July 2026 Inflection: The AUD 202M Exclusive Supply Deal

On July 1, 2026, Noumed Pharmaceuticals put out the announcement that reframed the entire investment case. It had secured an exclusive over-the-counter medicine supply agreement with one of Australia's leading pharmacy networks, running for an initial term of seven and a half years, with an option to extend by a further three.67 The total contract value was AUD 202 million — approximately ₹1,300 crore.6 Notably, this was not a cold-start win but a renewal and expansion of an existing Noumed supply relationship, now struck at a materially higher value and broader product scope — a detail that matters, because a renewal is a customer voting to deepen a relationship they already know.14 The market's reaction was immediate: the stock jumped sharply on the news.1213

To grasp why this single contract mattered so much, you have to size it against the company that won it. Spread over seven and a half years, AUD 202 million works out to an average annual run-rate of roughly AUD 27 million — about ₹173 crore a year.6 Now hold that figure next to Sai Parenterals' entire standalone revenue for FY25: ₹163.11 crore.16 In other words, the annual run-rate of this one Australian contract exceeds the whole of what the parent company sold in a year before the acquisition. It is rare to see a piece of new business that is, by itself, larger than the acquirer's pre-deal top line. That is the definition of a material, trajectory-altering event.

There is a further detail that strengthens the case, and it should be given its due. This was not a first date; it was a wedding after a long courtship. The July 2026 agreement was a renewal and expansion of an existing supply relationship between Noumed and the pharmacy network, struck at a materially higher value and a broader product scope than before.14 In diligence terms, that matters enormously. A brand-new customer signing a large first contract is a bet on an unproven supplier; an existing customer choosing to deepen and lengthen the relationship is revealing something they have learned from experience — that the supplier delivers. Anil Kumar Karusala framed the renewal in exactly those terms, describing it as reflecting "the confidence Australian pharmacy groups place in Noumed."6 Management framing should always be discounted, but here the structure of the deal — a renewal, not a debut — corroborates the claim rather than merely asserting it.

The economics of the deal reveal why management believed the Noumed thesis in the first place. Under the agreement, Noumed is responsible for the entire end-to-end supply chain: securing TGA registrations, sourcing active ingredients, managing manufacturing, assuring quality, and distributing nationwide across Australia.6 Crucially, some of that manufacturing can be back-integrated to Sai's low-cost Indian lines — the very sterile and oral-formulation plants in Hyderabad that were previously stuck making thin-margin domestic tenders. This is the mechanism by which the group hopes to convert a distribution contract into a manufacturing-plus-distribution margin: instead of Noumed buying finished OTC products from third parties and clipping a thin reseller's spread, it can source them from its own parent's Indian lines at cost, and keep the difference. The contract also comes with a built-in growth ramp: a commitment to add roughly 12 new OTC products every year, so the revenue base is designed to widen over the life of the deal rather than merely tick along.6 Over a seven-and-a-half-year term, a steady annual drip of new registrations compounds into a materially broader product shelf — which is why the headline figure understates the strategic optionality if the cadence is actually met.

This is the synergy that, on paper, justifies the whole gamble — and it is worth spelling out plainly, because it is the crux of the "why win" case. India makes the medicine cheaply; Australia sells it dearly. Sai manufactures high-quality sterile liquids and oral formulations in Hyderabad at a fraction of Western cost. Noumed registers those formulations with the TGA and sells them directly to Australian pharmacies under long-term, premium-priced contracts. In the old model, the margin between the Indian factory gate and the Australian pharmacy shelf was captured by a chain of third-party distributors and importers. By owning both ends, the combined group aims to keep that entire spread for itself. That is the "dossier and distribution arbitrage" in action, and if it works at scale, it is a genuinely differentiated position.

But an independent read cannot stop at the press release, because a headline contract value is a ceiling, not a floor. AUD 202 million is a total potential value over ten years including the extension, not a guaranteed cheque. It depends on volumes that must actually be ordered, on the 12-products-a-year cadence being met, and — most importantly — on Noumed's ability to fulfil orders profitably rather than merely reliably. High-overhead retail distribution can quietly erode the very margin the arbitrage is supposed to capture. And every rupee of that Indian-made supply now runs through Sai's Hyderabad plants, which means the contract is only as secure as those plants' regulatory standing. The deal transforms the scale of the opportunity; whether it transforms the quality of the earnings is the question the next several years will answer. That distinction — scale won versus value proven — is exactly what the investing lessons of this story turn on.

VIII. Playbook: Business & Investing Lessons

Step back from the ticker and the deal points, and Sai Parenterals offers three lessons that generalize well beyond one Hyderabad pharma company.

Lesson 1: The dossier-and-distribution arbitrage. The deepest lesson here is a claim about where value actually lives in global generic pharma — and it inverts most people's intuition. We tend to assume the hard, valuable part is making the medicine. Increasingly, it is not. Manufacturing capacity for standard generics has become abundant and, therefore, commoditized; factories in India, China, and elsewhere compete the margin out of the physical act of production. What stays scarce are two things: the regulatory approvals that grant the right to sell a drug in a rich, tightly controlled market, and the distribution relationships that grant access to the shelf. Those are slow to build, hard to replicate, and — critically — transferable in an acquisition. By buying Noumed, Sai acquired 451 registrations and a seat at the table with major pharmacy networks in a single stroke, converting itself overnight from a maker-of-things into an owner-of-access. Whether it paid the right price is a separate question; the strategic logic is sound, and it is the same logic Caplin Point used to build a far larger business.

Lesson 2: Surviving the "valley of death" in transformational M&A. When a small company acquires a larger, loss-making foreign business, it enters a dangerous stretch where the costs of the deal all arrive before any of the benefits — the interest expense, the integration overhead, the depreciation on a half-built plant — while the revenue synergies remain promises. That is the valley of death, and it is where most transformational small-cap acquisitions quietly bleed out. Sai's survival mechanism was timing: it used a public listing as a recapitalization tool, raising equity to retire acquisition debt at almost precisely the moment the acquired business landed a marquee contract. The lesson is not "leverage up and hope." It is that if you are going to attempt a transformation you cannot fund from cash flow, you had better have a credible, pre-planned path to permanent capital — and the discipline to use it to deleverage rather than to chase the next deal.

Lesson 3: The cost of capital as the price of speed. Everything Sai did can be read as a single trade: it exchanged a temporary hit to margins and balance-sheet safety for years of saved time. Organically earning TGA approvals and pharmacy relationships would have taken the better part of a decade; buying them cost ₹125 crore and a punishing interest bill.58 For a long-term investor, the honest way to frame this is not "was the margin hit bad?" — of course it was, in the short run — but "was the time it bought worth the price paid?" That depends entirely on whether the acquired moat proves durable. Speed is only valuable if what you race toward is still standing when you arrive.

There is a fourth lesson worth naming, quieter than the others but arguably the most durable: the discipline of how you finance a leap often matters more than the leap itself. Sai's decision to route the acquisition through a Singapore holding company was not merely tax-efficiency theater; it created a clean, ring-fenced structure through which foreign investment and foreign-currency contracts could flow without entangling the Indian listed entity in every operational risk. And the sequencing — debt first, then a rapid equity raise to term it out — is a textbook, if nerve-wracking, use of the capital structure: short-term debt is the fastest money to deploy, equity is the cheapest money to hold, and the art is in not getting caught between the two if markets close. Sai executed that pivot in a window that stayed open. Had the IPO market soured in early 2026, the same short-term debt that enabled the deal could have become the noose that ended it. That the maneuver worked should not be mistaken for proof that it was safe.

A brief myth-versus-reality check is warranted here, because the consensus retelling of this story has already begun to smooth over its edges. Myth: a scrappy small-cap pulled off a brilliant acquisition and instantly transformed itself into a global player. Reality: a small-cap took on expensive debt to buy a loss-making foreign business, delivered zero incremental profit in the year that followed, listed at a valuation the broad market declined to chase, and has since signed one large contract — a renewal of an existing relationship — whose profitability is not yet demonstrated in reported results. Both descriptions are true. The gap between them is exactly the space where an independent investor earns their keep, by refusing to let a clean narrative substitute for delivered cash flow.

Notice that all these lessons share a hinge: they are conditional. The arbitrage works if the margin survives contact with reality. The valley-of-death crossing succeeds if the deleveraging holds and no fresh debt is raised. The speed premium pays off if the moat is real. A disciplined investor does not accept these conditions on management's word. So the remainder of this story is devoted to stress-testing them — starting with what management is now promising, and what could break those promises.

IX. Current Strategy, Risk Radar, and Activist Stress Test

Management is not being timid about the future, and the boldness of its guidance is itself something to weigh. Leadership has publicly targeted FY27 consolidated revenue of around ₹750 crore — roughly double the ₹381 crore of FY26 — at an EBITDA margin near 17%. That is a striking claim, and it hangs almost entirely on two things going right: the smooth rollout of the July 2026 OTC supply contract, and the commercialization of the Salisbury plant. When a company's forward guidance depends on assets and contracts that have not yet produced a full year of results, the guidance is best treated as a statement of ambition, not a forecast — and management's credibility will be measured, over the coming quarters, by how tightly actual results track it. This is the first real test of whether this team sets targets it can hit.

A note on how to assess that credibility, since Sai has only a short public track record and no long archive of earnings calls to mine for consistency. In the absence of years of guidance-versus-delivery history, an investor has to lean on behavioral tells, and Sai offers a few worth holding in tension. On the reassuring side: the promoters did not sell into their own IPO, the offer-for-sale came from other investors, and the founding family diluted only through the fresh issue — behavior consistent with people who intend to be around for the outcome.168 On the cautionary side: the company overpromises structurally, in the sense that its stated FY27 revenue target embeds a near-doubling that depends on assets not yet proven, and it chose to allocate more IPO capital to new capacity than to extinguishing the debt that had just flattened its earnings.9 Neither pattern is damning on its own; together they sketch a management team that is genuinely committed and genuinely aggressive — a combination that can compound value or destroy it depending on execution. The single most valuable thing investors can do is stop parsing the rhetoric and start scoring the results against the targets, call by call, as the public record finally begins to accumulate.

The risk radar. Three exposures stand out as genuinely material, and they are worth understanding mechanically rather than as a checklist.

The first, and most acute, is regulatory compliance risk at the source. Because the Australian supply chain is meant to be partly back-integrated to Sai's Indian plants, the entire Noumed contract sits atop the compliance status of Unit I, Unit III, and their sister facilities. A single adverse event — a WHO-GMP audit failure, a TGA warning letter, an import alert — would not merely dent one product line; it could sever the supply feeding a ₹1,300-crore contract. The concentration of dependency is the danger: the more the company routes premium Australian revenue through specific Hyderabad lines, the more a localized regulatory problem becomes a group-wide one.

The second is execution risk at Salisbury. The Adelaide facility was slated to begin commercial operations around the fourth quarter of 2026. Until it does, its capital costs and overheads sit on the income statement as depreciation and expense without generating offsetting revenue — the classic drag of a plant that is built but not yet earning.6 Any cost overrun or commissioning delay keeps that drag in place longer and pushes out the margin recovery the whole thesis depends on.

The third is API supply dependency. Like much of the Indian formulations industry, Sai remains heavily reliant on third-party active pharmaceutical ingredients, a significant share of them sourced from China. That exposes the company to raw-material price swings and to geopolitical or logistical shocks in the API supply chain — a vulnerability shared across the sector but sharpened here by the thin margins on the domestic book.

The activist stress test. Now imagine a skeptical long/short investor or an activist studying this company. Where would they press? The pressure point is capital efficiency. They would ask, pointedly, why a company sitting on 1,160 million units of installed capacity — reportedly running at less-than-full utilization — is simultaneously raising capital to build more capacity, both in India and at Salisbury.16 Why add asset intensity to a business that has not yet demonstrated it can fill the assets it already owns? Their demands would be predictable and, frankly, hard to rebut: stop chasing low-margin domestic government tenders that consume working capital and return little; aggressively outsource non-sterile oral-solid production to third parties rather than building it in-house; and concentrate every rupee of internal capital on the high-margin sterile injectable and export lines where the company's genuine edge lies. That is the disciplined version of Sai's own strategy — and the gap between it and management's build-everything ambition is precisely the governance question a concentrated, founder-controlled board invites. Whether one reads that gap as visionary conviction or as undisciplined empire-building is, in the end, the whole bull-versus-bear debate.

X. Bull vs. Bear Case & Key KPIs to Track

Let us lay the two cases side by side without a thumb on the scale, and then run the company through the two frameworks that best expose the durability of an advantage.

The bull case. The optimistic path is clean and self-reinforcing. The ₹285 crore of fresh IPO proceeds retire the high-cost acquisition debt, which switches off the roughly ₹18 crore annual interest burn and lets profit finally track revenue rather than lag it.98 The AUD 202 million Australian contract scales smoothly, adding high-margin, recurring, hard-currency cash flow with a built-in 12-products-a-year growth ramp.6 The Salisbury plant comes online in late 2026, satisfying Australia's local-supply preference and positioning Noumed as a domestic manufacturer rather than a mere importer — a status that can command both political goodwill and pricing. As earnings scale into the elevated valuation, the frightening 100-plus price-to-earnings multiple compresses naturally, and SAIPARENT re-rates as a differentiated cross-border pharma play. In this world, FY26 was simply the cost of admission.

The bear case. The pessimistic path uses the same facts and reaches the opposite destination. Noumed's retail-distribution model turns out to carry high enough overhead that consolidated operating margins never reach the guided 17%, and the celebrated arbitrage is quietly eaten by the cost of running an Australian last-mile business. A regulatory problem at a Hyderabad plant disrupts shipments and triggers penalty clauses in the very contract that anchors the story. The working-capital intensity of servicing a large, long-dated OTC contract forces fresh borrowing, and the interest drag the IPO was meant to end simply returns under a new name. And if earnings growth disappoints even modestly, a stock priced at more than 100 times earnings has a very long way to fall, because there is no valuation support beneath it.16 In this world, FY26 was not the trough but a preview.

Before scoring the frameworks, it helps to state plainly what each is for. Porter's Five Forces is a map of industry structure — it tells you whether the neighborhood a company operates in is inherently profitable or inherently brutal, regardless of how clever any single firm is. Helmer's Seven Powers is the complementary question — it asks whether a particular company has built something that lets it earn more than its rivals in a durable, defensible way. A business can sit in a tough industry (bad Porter) yet still own real power (good Helmer), or vice versa. Running Sai through both, rather than one, is the way to separate "is this a good business to be in?" from "does this company have an edge worth paying for?"

Porter's Five Forces, applied honestly, lands Sai in a middling-to-tough neighborhood. Rivalry is intense: Indian formulations and injectables are crowded with certified competitors, and even the export markets host scaled players like Gland. Buyer power is high and asymmetric — government tender agencies squeeze price mercilessly, and even a marquee customer like a dominant Australian pharmacy network holds real leverage over a supplier for whom the contract is existential. Supplier power is meaningful given the dependence on Chinese APIs. Threat of substitutes is low in the sense that people will always need these medicines, but any specific generic molecule is endlessly substitutable. Barriers to entry are the one force working in Sai's favor — sterile-injectable certification and TGA dossiers are genuinely hard to obtain — but note that Sai chose to buy past that barrier rather than defend a position behind it, which tells you the barrier protects the market more than it protects any one incumbent.

Hamilton Helmer's Seven Powers is the more revealing lens, because it forces the question: does Sai own any durable power, or just a good position? Scale economies — no; Sai is sub-scale, which was the entire problem. Network economies — not applicable. Branding — weak; generics and private-label OTC are, by definition, not brand-led. Switching costs — here there is a real, if modest, kernel: once Sai's formulations are registered under Noumed's dossiers and embedded in a pharmacy network's private-label range, swapping suppliers means re-registration and re-qualification, which is friction that protects the relationship. Cornered resource — this is the strongest claim: the 451 TGA dossiers and the exclusive pharmacy contract are genuinely scarce, hard-to-replicate assets, and owning them is the closest thing Sai has to real power. Counter-positioning — arguably present, in that the low-cost Indian-manufacture-plus-Australian-distribution model is awkward for pure distributors and pure manufacturers alike to copy. Process power — the sterile-manufacturing discipline, if sustained, qualifies modestly. The honest verdict: Sai's advantage rests mainly on a cornered resource (the dossiers and the contract) reinforced by switching costs — and cornered resources are powerful but not permanent. Dossiers can be replicated by a determined competitor over time, and a contract, however long, eventually comes up for renewal. This is a defensible position, not an impregnable one.

The KPIs that actually matter. Ignore the noise and watch three numbers over the coming years.

- Consolidated EBITDA margin, against the ~17% FY27 target. This is the single cleanest test of whether the company is genuinely transitioning from low-margin domestic volume to high-margin export value, or merely getting bigger. Margin, not revenue, is where this thesis is won or lost.

- The Salisbury facility's commissioning date and ramp. Whether the Adelaide plant goes live on schedule and fills up — or becomes an asset-heavy white elephant absorbing depreciation for years — will tell you whether management can execute capital projects, not just sign contracts.

- The Noumed contract's realized execution rate. Track the quarterly revenue actually flowing from the AUD 202 million agreement against the roughly ₹173 crore annual run-rate it implies. A signed ceiling is not delivered revenue; the gap between the two is the truest measure of whether the July 2026 inflection was real.

Watch those three, and the bull-bear debate largely resolves itself over time — which brings us back to the larger arc.

XI. Epilogue

The distance Sai Parenterals has traveled is genuinely remarkable to state plainly: a regional maker of injectable generics in Telangana and Andhra Pradesh, incorporated in a Hyderabad industrial estate at the turn of the millennium, reconstituted itself in the span of a year and a half into an integrated, multinational group with manufacturing in India, distribution in Australia, and a holding structure routed through Singapore. Companies far larger try transformations like this and fail. Sai, at least, got the pieces onto the board.

But the point of this story is not to celebrate the reinvention — it is to hold it up to the light. What Sai Parenterals demonstrates is that true business scale is not achieved merely by manufacturing more of the same thing; it can be pursued by taking bold, leveraged bets on the parts of the value chain — regulatory access and distribution — that others cannot easily replicate. That is the lesson. It is also, in the same breath, the risk. The very leverage and boldness that make the strategy interesting are what make it fragile, and the difference between a visionary cross-border pharma play and an over-extended small-cap that flew too close to the sun will be settled not by the ambition of the plan but by the discipline of its execution.

It is worth being clear-eyed about how much of this story is still a promise rather than a proof. As of the middle of 2026, the transformation exists mostly in the future tense. The contract's revenue has not yet flowed through a full year of results. The Salisbury plant has not yet made a commercial batch. The deleveraging has begun but is not complete. The elevated valuation has not yet been either vindicated by earnings or punished by their absence. Every element of the bull case is plausible; not one of them is yet demonstrated. That is not a criticism — it is simply the honest state of the evidence, and it is why the responsible posture toward Sai Parenterals today is neither the breathless enthusiasm of the transformation narrative nor the reflexive contempt of the "value-destructive small-cap" dismissal, but patient attention to a small set of numbers that will, over the next several years, quietly settle the argument.

For now, the contract is signed, the debt is being paid down, and the plant is nearly built. A regional injectables maker has, through sheer nerve and a favorable market window, given itself a shot at a far larger and more defensible business than the one it started with. Whether it converts that shot is the only question that ultimately matters — and the answer will be written not in press releases but in margins, in the fill rate of that Adelaide plant, and in the cash that either does or does not arrive from Australia. What remains unproven is precisely the thing the whole thesis rests on: whether the moat Sai bought is as durable as the price it paid.

References

-

Sai Parenterals Ltd (544742) Stock Quote — Bombay Stock Exchange ↩

-

India's SAI Parenterals acquires Australia-based Noumed Pharma for Rs 125 Cr — BioSpectrum Asia ↩↩↩↩

-

Sai Parenterals' Noumed Signs AUD 202 Mn Australia OTC Supply Deal — Hybiz TV, 2026-07-01 ↩↩↩↩↩↩↩↩↩↩↩

-

Sai Parenterals Subsidiary Noumed Bags ₹1,300 Cr OTC Supply Deal in Australia — Sahi.com, 2026-07-01 ↩↩↩↩

-

Sai Parenterals Ltd — Consolidated Financials and Shareholding — Screener.in ↩↩↩↩↩↩↩↩

-

Sai Parenterals Files DRHP for ₹285 Cr Fresh Issue & OFS — HDFC Sky ↩↩↩↩↩↩↩

-

Sai Parenteral IPO Listing at 2.04% Premium at ₹400 per Share — Univest, 2026-04-02 ↩

-

Sai Parenteral's IPO Date, Price, GMP, Review, Details — Chittorgarh ↩↩

-

Pharma Stock Skyrockets 15% After Securing ₹1,300 Cr Australian OTC Supply Deal — Trade Brains, 2026-07-01 ↩

-

Sai Parenterals subsidiary wins AUD 202 Mn OTC order — ScanX ↩

-

Noumed Pharmaceuticals Renews its Exclusive OTC Supply Agreement with Australia's Leading Pharmacy Networks — EquityBulls, 2026-07-01 ↩↩

-

SAI PARENTERAL'S LIMITED — Company Registration Details — ZaubaCorp ↩↩

-

Sai Parenteral's IPO Review, GMP, Valuation, Risks — INDmoney ↩↩↩↩↩↩↩↩↩↩↩↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube