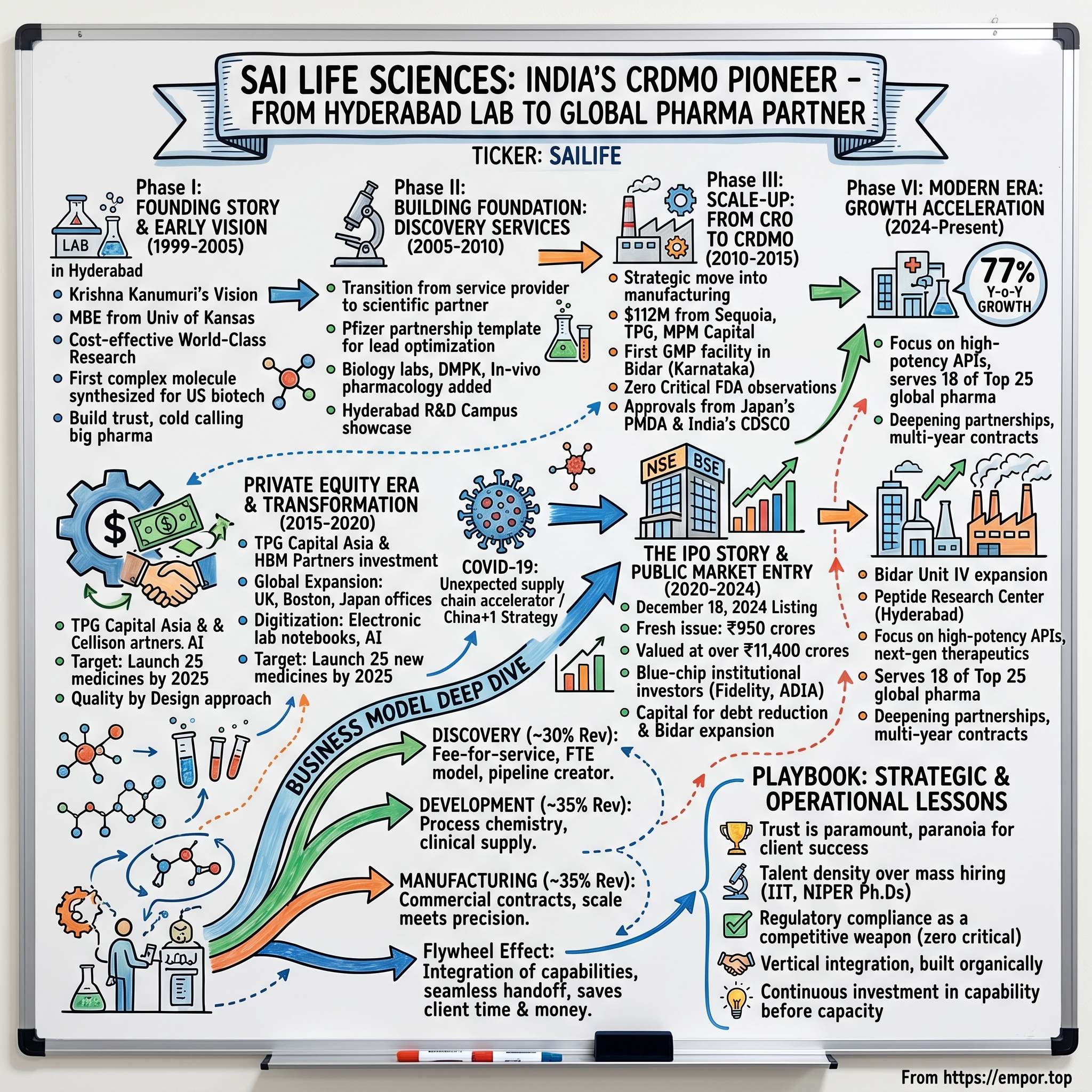

Sai Life Sciences: India's CRDMO Pioneer - From Hyderabad Lab to Global Pharma Partner

I. Introduction & Episode Setup

Picture this: It's December 18, 2024, and the trading floors at the National Stock Exchange are buzzing with unusual energy. A new pharma services company has just listed—Sai Life Sciences—and within minutes of opening, the stock jumps 6% above its IPO price of ₹549. Not the typical tech unicorn fanfare, but for those who understand the pharmaceutical services industry, this moment represents something far more significant: the public market debut of India's fastest-growing contract research, development, and manufacturing organization (CRDMO).

Here's the thing that makes this story remarkable: In an industry dominated by century-old Western giants and newer Chinese competitors, a company that started in a modest Hyderabad lab in 1999 now counts 17 of the world's top 20 pharmaceutical companies as clients. They've touched the development of over 200 drug discovery programs, with 40+ advancing to human trials. Their Q1 FY26 numbers? Revenue of ₹496 crores—a staggering 77% year-over-year growth that would make even software companies jealous.

But this isn't just another outsourcing success story. This is about how Krishna Kanumuri and his team built something that pharmaceutical giants trust with their most precious assets: their drug pipelines. In an industry where a single contamination can destroy billions in value, where regulatory missteps can shut down operations for years, Sai Life Sciences has maintained zero critical FDA observations across multiple inspections.

The question we're exploring today isn't just how they did it—it's why now? Why is a 25-year-old company suddenly growing at startup-like rates? What changed in the global pharmaceutical supply chain that turned regional players into strategic partners? And perhaps most intriguingly: Is this the beginning of India's emergence as the world's medicine chest, not just for generic drugs but for cutting-edge innovation?

As we unpack this story, we'll journey from the post-liberalization optimism of 1999 India through the private equity transformations of the 2010s, into today's geopolitically-charged pharmaceutical landscape where "China+1" isn't just a strategy—it's survival. Along the way, we'll decode the unit economics of drug development, understand why Big Pharma increasingly outsources its R&D, and examine whether Sai Life Sciences represents the vanguard of a new Indian pharmaceutical renaissance or simply caught a favorable wave at the right time.

II. The Founding Story & Early Vision (1999-2005)

The year was 1999. Y2K fears gripped the tech world, the dot-com bubble was reaching its frothy peak, and in Hyderabad—a city just beginning its transformation into "Cyberabad"—Krishna Kanumuri was contemplating a different kind of venture. While his peers chased software riches, Kanumuri saw opportunity in test tubes and chemical compounds. Kanumuri wasn't your typical pharma entrepreneur. With an MBA from the University of Kansas Graduate School of Business (1993-1995), he'd spent years understanding the pharmaceutical value chain from various angles. What he saw in 1999 was a perfect storm of opportunity: India's patent laws were about to change, global pharmaceutical companies were under pressure to reduce R&D costs, and Hyderabad was emerging as a biotech hub with government support and available scientific talent.

The founding of Sai Life Sciences in January 1999 wasn't accompanied by fanfare or venture capital millions. It started with a simple premise: Indian scientists could deliver world-class pharmaceutical research at a fraction of Western costs. But here's what made Kanumuri's approach different—he didn't want to build just another cost-arbitrage play. From day one, the vision was to become an integrated partner across the entire drug development lifecycle.

Consider the India that Kanumuri was operating in. The 1991 economic liberalization was less than a decade old. The pharmaceutical industry was dominated by reverse-engineering generic drugs—brilliant chemistry, but not original innovation. The concept of Indian companies doing cutting-edge drug discovery for Western pharma giants seemed almost absurd. Yet that's exactly what Kanumuri set out to build.

The early days were brutal. Picture a small team in a rented facility in Hyderabad, cold-calling pharmaceutical companies in New Jersey and Basel, trying to convince them that a startup in India could handle their precious drug discovery programs. The trust deficit was enormous. Western pharmaceutical companies had horror stories about intellectual property theft, quality issues, and communication barriers with offshore partners.

Kanumuri's strategy was methodical. Start small—take on discrete chemistry projects where failure wouldn't be catastrophic for clients. Deliver flawlessly. Build relationships. Then gradually expand the scope. The first breakthrough came when they successfully synthesized a complex molecule for a mid-sized US biotech—completing in six weeks what their in-house team estimated would take three months.

By 2003, Sai Life Sciences had established its initial foothold in synthetic and medicinal chemistry services. They weren't competing on price alone—they were competing on speed and technical complexity. When a Boston biotech needed 15 analogs of a lead compound synthesized and characterized, Sai delivered in 10 days. When a European pharma company struggled with a particularly challenging stereochemistry problem, Sai's chemists cracked it.

The company's early culture was shaped by what employees called "the 2 AM test"—if a client in San Diego had a question at 2 AM India time, someone would answer. This wasn't just about time zone coverage; it was about demonstrating a level of commitment that transcended the typical vendor-client relationship.

By 2005, Sai Life Sciences had completed projects for over 20 pharmaceutical companies, established a dedicated R&D facility in Hyderabad, and begun building capabilities beyond basic chemistry. The foundation was set, but the real test was ahead: could they move from being a reliable service provider to becoming a strategic partner in drug discovery?

III. Building the Foundation: Discovery Services Era (2005-2010)

The conference room at Pfizer's Connecticut research facility fell silent. It was 2006, and the pharmaceutical giant's discovery team had just heard a proposal that seemed almost too ambitious: an Indian company wanted to take ownership of an entire lead optimization program for a novel oncology target. Not just synthesize compounds, but design them, test them, iterate on them—essentially run a mini-drug discovery unit 8,000 miles away.

This was the moment Sai Life Sciences transitioned from service provider to scientific partner. The Pfizer team's skepticism was understandable. Drug discovery isn't just chemistry—it's an intricate dance of biology, pharmacology, and intuition developed over decades. Could a seven-year-old company from Hyderabad really deliver?

The answer came nine months later when Sai's integrated team delivered not just one, but three lead compounds with sub-nanomolar potency and favorable ADME properties. One of those compounds would eventually enter clinical trials. The project became a template for what Sai Life Sciences could offer: not just hands, but brains.

During this period, Sai made a critical strategic decision that would define its trajectory. Rather than remaining a pure chemistry shop, they began building integrated discovery capabilities. In interviews, Krishna spoke about building the company for the future, and that future required moving up the value chain.

The buildout was systematic. First came the biology labs—cell culture facilities, biochemical assay capabilities, and high-throughput screening infrastructure. Then DMPK (drug metabolism and pharmacokinetics)—understanding not just whether a compound binds to its target, but how it behaves in living systems. By 2008, they'd added in-vivo pharmacology and safety pharmacology capabilities.

Each capability addition was a bet. Setting up a biology lab meant competing for talent with established pharma companies. Building DMPK expertise required expensive instrumentation—LC-MS/MS systems that cost more than most Indian startups' entire seed rounds. But Kanumuri understood something fundamental: pharmaceutical companies don't want to manage ten different vendors for one drug discovery program. They want integration.

The numbers tell the story. In 2005, Sai Life Sciences had 150 scientists and generated roughly $10 million in revenue. By 2010, they'd grown to over 600 scientists and crossed $40 million in revenue. But more importantly, the nature of their engagements had transformed. Instead of discrete "make this molecule" projects, they were running integrated discovery programs worth millions of dollars each.

The 2008 financial crisis became an unexpected accelerator. As Big Pharma slashed R&D budgets and shuttered research sites, they needed partners who could do more with less. Sai Life Sciences was perfectly positioned—they could run a full discovery program at 30-40% of the cost of doing it in-house in the US or Europe, with comparable timelines and quality.

One project from this era illustrates the value proposition. A European pharmaceutical company needed to explore a novel target for inflammatory diseases. Instead of building an internal team, they engaged Sai Life Sciences. Over 18 months, Sai's integrated team synthesized over 300 compounds, tested them across multiple assays, optimized for potency and selectivity, and delivered two development candidates. The entire program cost less than what the company would have spent on salaries alone for an equivalent in-house team.

The Hyderabad R&D campus became a showcase. When clients visited, they didn't see a low-cost back office—they saw state-of-the-art laboratories that could rival any Western pharmaceutical company. The campus eventually expanded to over 2000 scientists working across 270,000 square feet of laboratory space. It wasn't just about scale; it was about creating an environment where world-class science could happen.

By 2010, Sai Life Sciences had established itself as one of India's premier drug discovery partners. They'd completed over 50 integrated discovery programs, filed numerous patent applications on behalf of clients, and most importantly, proven that innovation could happen anywhere—even in a country better known for generic drugs than novel drug discovery.

IV. The Scale-Up Journey: From CRO to CRDMO (2010-2015)

The email arrived on a humid Hyderabad morning in 2011. A US biotech client had a problem: their lead compound was showing promising Phase II results, but their CMO (contract manufacturing organization) had just informed them of a six-month delay in producing the Phase III clinical supply. Could Sai help?

This request would have been impossible for Sai to fulfill just a year earlier. They were a discovery company—test tubes and milligrams, not reactors and kilograms. But Kanumuri had been preparing for exactly this moment. The decision to expand from CRO to CRDMO wasn't reactive; it was strategic chess playing out over years.

The logic was compelling. Sai had helped clients discover and optimize dozens of drug candidates. They knew the molecules intimately—every synthetic route, every impurity, every polymorph. Yet when these molecules advanced to clinical trials, clients had to transfer them to separate manufacturing organizations, losing months and institutional knowledge in the process. What if Sai could shepherd molecules from conception through commercialization?

Building manufacturing capabilities meant entering an entirely different league. Discovery is about creativity and speed; manufacturing is about reproducibility and compliance. The investment required was staggering. While a discovery lab might need $100,000 in equipment, a GMP manufacturing facility required tens of millions in infrastructure, validation, and regulatory approvals. The funding came at a critical moment. Sai Life Sciences raised $112 million from investors including Sequoia Capital, TPG, and MPM Capital, providing the war chest needed for this ambitious expansion. But money alone wouldn't solve the challenge. Building a GMP facility meant navigating the labyrinthine world of pharmaceutical regulations.

The first manufacturing facility came online in 2012 at their Bidar site in Karnataka. It wasn't just any facility—it was designed from the ground up to meet the most stringent global standards. Every pipe, every valve, every air handling unit was specified to pharmaceutical grade. The validation documentation alone ran to thousands of pages.

Then came the regulatory gauntlet. Getting USFDA approval for a manufacturing facility isn't like getting a business license. FDA inspectors spend days, sometimes weeks, examining every aspect of operations. They review batch records, interview operators, test cleaning procedures, verify analytical methods. One critical observation can shut down operations for months.

Sai's first FDA inspection in 2013 was a nail-biter. The inspection team had prepared for months, running mock inspections, drilling standard operating procedures, ensuring every document was perfect. When the FDA inspectors arrived, they found... nothing major. Zero critical observations. For a first-time inspection of an Indian facility, this was almost unheard of.

The successful FDA approval opened floodgates. Suddenly, clients who'd been hesitant about manufacturing in India were interested. A US biotech that had been struggling with their existing CMO moved their entire Phase II supply to Sai. A European pharmaceutical company engaged them for commercial manufacturing of an oncology drug.

By 2014, Sai had also received approvals from Japan's PMDA (Pharmaceuticals and Medical Devices Agency) and India's CDSCO (Central Drugs Standard Control Organisation). The Japanese approval was particularly significant—Japanese regulators are notoriously stringent, and few Indian companies had successfully navigated their requirements.

The integration of discovery and manufacturing capabilities created a powerful flywheel effect. When Sai's discovery team developed a new synthetic route that reduced costs by 40%, the manufacturing team could immediately implement it. When the manufacturing team identified a scalability issue with a client's process, the discovery team could redesign the chemistry. This seamless handoff saved clients months and millions.

One project exemplified the integrated model's value. A San Francisco biotech had a promising kinase inhibitor entering Phase I trials. Sai had done the lead optimization work, so they knew every nuance of the molecule. When the client needed clinical supply, Sai manufactured it in weeks rather than the months it would have taken with a new CMO. When unexpected metabolites appeared in early trials, Sai's discovery team quickly synthesized reference standards. When the client needed to explore new salt forms for better bioavailability, Sai screened dozens of options while maintaining the clinical supply chain.

The numbers reflected the transformation. Revenue grew from $40 million in 2010 to over $100 million by 2015. More importantly, the revenue mix had shifted. Manufacturing now contributed nearly 40% of revenues, with higher margins than pure discovery services. Client retention rates exceeded 90%, with many clients expanding their engagements year over year.

By 2015, Sai Life Sciences had evolved from a discovery CRO to a true CRDMO, one of the few globally that could take a molecule from concept to commercial supply under one roof. But the transformation was far from complete. The next phase would require even bigger bets and deeper partnerships.

V. The Private Equity Era & Transformation (2015-2020)

The boardroom at Sai Life Sciences' Hyderabad headquarters was unusually crowded in July 2018. TPG Capital Asia had just acquired a significant minority stake from Tata Capital, marking a pivotal moment in the company's evolution. The deal wasn't just about capital—it was about ambition. "Contract development and manufacturing companies have started to gain market share as pharma innovators search for more cost effective, efficient, and comprehensive solutions," said Puneet Bhatia, Co-Managing Partner of TPG Capital Asia.

What followed was one of the most aggressive expansion phases in Indian pharmaceutical services history. Between 2016 and 2020, Sai Life Sciences quadrupled its capacity—a transformation that CEO Krishna Kanumuri described as fundamental to becoming "the partner of choice for large pharma and small biotechs".

The transformation wasn't just about adding square footage. It was about reimagining what an Indian CRDMO could be. While competitors focused on either discovery or manufacturing, Sai doubled down on integration. They built specialized units for high-potency APIs, established controlled substance handling capabilities, and created dedicated facilities for different stages of clinical development.

Backed by committed investors TPG Capital and HBM Partners, the company had the firepower to execute on an audacious vision: supporting the launch of 25 new medicines by 2025. This wasn't marketing fluff—it was a quantifiable commitment that would require fundamental operational changes.

The global expansion strategy unfolded methodically. In 2016, they established a presence in the UK, not through acquisition but by building relationships with Cambridge's biotech cluster. By 2017, they'd opened a business development office in Boston, putting them at the heart of the world's largest concentration of biotech companies. The Japan office came next, recognizing that Japanese pharmaceutical companies, traditionally insular, were beginning to embrace outsourcing.

Each geographic expansion served a strategic purpose. The UK presence gave them credibility with European biotechs. The Boston office provided proximity to decision-makers at companies that might never have considered an Indian partner. The Japan office offered entry into a market where relationships and trust matter more than cost.

Technology transformation paralleled geographic expansion. By 2018, Sai had implemented electronic lab notebooks across all discovery operations, digitized their manufacturing batch records, and begun using predictive analytics for process optimization. This wasn't digitization for its own sake—it was about creating seamless information flow from discovery through manufacturing.

The R&D expansion during this period was particularly strategic. Instead of trying to be everything to everyone, Sai focused on specific therapeutic areas where they could build deep expertise: oncology, central nervous system disorders, inflammation, and antivirals. Within these areas, they didn't just execute projects—they built knowledge platforms that made each subsequent project faster and more efficient.

Consider their oncology platform. By 2019, they'd worked on over 50 oncology programs, building expertise in kinase inhibitors, PROTACs, and antibody-drug conjugates. When a client came with a new oncology target, Sai could leverage this accumulated knowledge to accelerate timelines. They knew which assays were most predictive, which ADME properties mattered most, which synthetic routes scaled best.

The manufacturing expansion was equally targeted. The new Bidar Unit IV wasn't just additional capacity—it was designed specifically for complex, multi-step syntheses required for modern pharmaceuticals. The facility could handle everything from milligram-scale for early clinical trials to multi-ton commercial production, all while maintaining the flexibility to switch between products quickly.

Quality systems underwent a complete overhaul. By 2019, Sai had achieved a remarkable milestone: zero critical observations across multiple FDA inspections. This wasn't luck—it was the result of embedding quality thinking into every process, from how they designed experiments to how they cleaned reactors. They instituted a "Quality by Design" approach that anticipated problems rather than reacting to them.

The human capital investment was perhaps most crucial. Sai didn't just hire more people; they hired differently. They brought in former Big Pharma executives who understood client needs intimately. They recruited young PhDs from top Indian institutes and sent them for training at client sites. They created an internal university that provided continuous education on everything from regulatory changes to new synthetic methodologies.

By early 2020, just as the transformation was bearing fruit, the world changed. COVID-19 struck, global supply chains shattered, and pharmaceutical companies suddenly realized the risks of geographic concentration. For Sai Life Sciences, positioned as a reliable alternative to Chinese suppliers with Western-standard quality systems, the pandemic would prove to be an unexpected accelerator.

The PE-backed transformation had positioned them perfectly. They had the capacity, the capabilities, and the credibility to capture the coming wave of supply chain diversification. As one board member remarked in late 2019, not knowing what was coming: "We've built the infrastructure for the next decade of growth." They had no idea how prescient those words would prove to be.

VI. The IPO Story & Public Market Entry (2020-2024)

March 2020. While the world grappled with lockdowns and Sai's laboratories operated with skeleton crews in biosecure bubbles, another kind of preparation was underway in the company's finance department. The IPO machine, quietly humming since 2019, had shifted into high gear. The pandemic, rather than derailing plans, had crystallized the investment thesis: pharmaceutical supply chain resilience was no longer optional.

The path to public markets was anything but straightforward. The company needed to transform from a privately-held, PE-backed entity into a structure that public market investors could understand and value. This meant untangling complex shareholder agreements, standardizing accounting practices across geographies, and creating the governance infrastructure that public companies require. The numbers that emerged were impressive: ₹3,042.62 crores total issue size, comprising a fresh issue of ₹950 crores and an offer for sale of ₹2,092.62 crores. The price band was set at ₹522 to ₹549 per share, valuing the company at over ₹11,400 crores.

The roadshow circuit was grueling. Krishna Kanumuri and his team crisscrossed from Mumbai to Singapore, London to New York, telling the Sai story to institutional investors. The pitch was compelling: fastest-growing Indian CRDMO, 77% revenue growth in recent quarters, relationships with 18 of the top 25 global pharmaceutical companies, and a clear beneficiary of the "China+1" strategy that every pharma company was now pursuing.

The anchor book response was overwhelming—₹912.79 crores raised from anchor investors on December 10, 2024. This wasn't just oversubscription; it was validation from sophisticated institutional investors who understood the pharmaceutical services sector deeply.

The retail response during the public subscription period from December 11-13, 2024, was more measured but still positive. The issue was subscribed 10.26 times overall, with the QIB portion subscribed 30.93 times—a clear signal that institutional investors saw long-term value.

December 18, 2024, listing day, arrived with the kind of nervous energy that only IPO debuts bring. The shares listed on both BSE and NSE, opening at ₹650—an 18.4% premium to the issue price. While not the spectacular "pops" seen in tech IPOs, for a manufacturing-heavy CRDMO, this was solid validation.

The post-IPO structure revealed interesting dynamics. The promoter group retained significant skin in the game, while TPG and other PE investors partially exited, crystallizing returns on their patient capital. The fresh capital raised—₹950 crores—would be deployed for debt reduction and capacity expansion, particularly the ambitious Bidar Unit IV that would add 91 kiloliters of reactor capacity.

What made this IPO particularly notable wasn't just the successful execution but the timing. The pharmaceutical services sector was experiencing a renaissance. Global pharma companies, burned by supply chain vulnerabilities during COVID, were actively diversifying away from China. India, with its established pharmaceutical ecosystem, English-speaking scientific talent, and robust regulatory framework, was the obvious beneficiary.

The use of proceeds told its own story about ambition. While ₹650 crores would go toward debt repayment—cleaning up the balance sheet for public market scrutiny—the remainder would fund aggressive capacity expansion. The company wasn't going public to cash out; it was going public to accelerate.

Market analysts noted something interesting: unlike typical Indian IPOs dominated by retail enthusiasm, Sai Life Sciences attracted serious institutional money. Fidelity, ADIA, and other blue-chip funds participated, seeing in Sai not just an Indian outsourcing play but a critical piece of global pharmaceutical infrastructure.

The IPO also marked a cultural shift within the company. Quarterly earnings calls, investor relations, and public market scrutiny would replace the relative privacy of PE ownership. For a company built on long-term relationships and patient capital investment, adapting to quarterly capitalism would require careful navigation.

As 2024 closed, Sai Life Sciences had successfully transitioned from private to public, raising capital, achieving liquidity for early investors, and most importantly, gaining a currency—publicly traded stock—that would be crucial for future acquisitions and talent retention. The IPO wasn't the end goal; it was fuel for the next phase of growth.

VII. The Business Model Deep Dive

Imagine pharmaceutical development as a relay race where a single dropped baton costs billions. That's the game Sai Life Sciences plays—except they're not just one runner; they're the entire relay team. Their business model represents one of the most sophisticated value propositions in pharmaceutical services: true end-to-end integration from the first sketch of a molecule to commercial-scale manufacturing.

Here's the elegant simplicity underlying the complexity: pharmaceutical companies spend roughly $2.6 billion and 10-15 years to bring a single drug to market. About 70% of that spending goes toward activities that can be outsourced—discovery research, process development, clinical trial material, commercial manufacturing. Sai Life Sciences positioned itself to capture value across this entire chain, not just pieces of it.

The revenue model breaks down into three interconnected streams, each with distinct economics. Discovery services, contributing roughly 30% of revenues, operate on a fee-for-service or FTE (full-time equivalent) basis. A typical integrated discovery program might involve 20-30 scientists for 18-24 months, generating $3-5 million in revenue with EBITDA margins around 25-30%. The beauty of discovery isn't just the margins—it's the pipeline it creates for downstream services.

Development services, representing about 35% of revenue, involve taking discovered molecules through the regulatory maze toward human trials. This includes process chemistry, analytical development, and preparing regulatory documentation. A development project for a Phase II/III clinical supply might generate $5-10 million over 12-18 months, with margins slightly higher than discovery due to the specialized expertise required.

Manufacturing, the remaining 35% of revenue, is where scale meets precision. Commercial manufacturing contracts can span 5-7 years, generating $10-50 million annually per product, with EBITDA margins that can exceed 35% once volumes stabilize. The capital intensity is highest here—a single reactor might cost $5 million—but so is customer stickiness. Switching manufacturing partners for an approved drug is regulatory nightmare that companies avoid unless absolutely necessary.

The numbers tell a story of deliberate portfolio construction. Sai's CDMO portfolio features over 170 innovator pharmaceutical products, with 38 supporting the manufacturing of 28 commercial drugs. This isn't random accumulation—it's careful selection of molecules with blockbuster potential, complex chemistry that creates barriers to entry, and long commercial lifecycles.

Customer concentration, often viewed as risk, is actually strategic moat-building. Serving 18 of the top 25 global pharmaceutical companies means Sai has passed the most stringent quality audits, understands Big Pharma's decision-making processes, and has proven they can handle mission-critical projects. When Pfizer or Novartis has a new molecule, they don't Google "CRO services"—they call partners who've delivered before.

The unit economics reveal why this business model works. A discovery program might start with $100,000 in preliminary chemistry work. If successful, it escalates to a $3 million lead optimization program. If that molecule advances to clinical trials, Sai manufactures the clinical supply—another $5 million. If the drug gets approved, commercial manufacturing could generate $20 million annually for a decade. From a $100,000 seed, a $200 million relationship tree can grow.

This "molecule lifecycle" approach creates powerful lock-in effects. Having completed over 200 discovery programs with 40+ advancing to clinical phases, Sai has institutional knowledge about these molecules that no competitor can replicate. They know the synthetic challenges, the impurity profiles, the stability issues. For a pharmaceutical company to switch vendors mid-development would mean starting this learning curve over—costly in both time and risk.

The competitive moat deepens with scale. Each successful project generates data, relationships, and expertise that make the next project more likely to succeed. When a client needs a CDK4/6 inhibitor developed, Sai can leverage learnings from previous kinase programs. When someone needs a complex macrocycle manufactured, Sai's team has seen similar challenges before.

Geographic and therapeutic diversification provides resilience. While 60% of revenue comes from North American clients, the company also serves European, Japanese, and emerging market companies. Therapeutic focus on oncology, CNS, inflammation, and antivirals—areas with high unmet medical need and robust pipelines—ensures steady demand regardless of individual drug failures.

The model's true genius lies in its capital efficiency evolution. Early-stage discovery requires minimal capital—essentially lab space and brilliant minds. As molecules progress toward commercialization, capital requirements increase, but so do contract values and margins. By the time Sai needs to invest millions in manufacturing infrastructure, they have signed contracts and deep client relationships that de-risk the investment.

Pricing power comes from switching costs, not negotiation leverage. Once Sai is embedded in a drug's development, the cost of switching—regulatory refilings, technology transfer, potential delays—far exceeds any pricing premium Sai might charge. This doesn't mean gouging clients; it means earning fair returns for critical services where failure isn't an option.

The operational metrics that matter: capacity utilization (currently running at 75-80%), client retention (over 90%), project success rates (above industry averages), and regulatory inspection outcomes (zero critical observations). These aren't just KPIs—they're the vital signs of a business where trust and execution determine survival.

Revenue per employee, approaching $200,000, sits well above Indian IT services but below Western CROs—exactly where Sai wants to be. High enough to attract and retain top talent, competitive enough to win deals against Western competitors, profitable enough to fund continuous investment in capabilities.

The model isn't without challenges. Success depends on continued R&D spending by pharmaceutical companies, regulatory approval rates, and Sai's ability to maintain quality while scaling. But with global pharmaceutical R&D spending exceeding $200 billion annually and outsourcing penetration still below 50%, the runway for growth extends far into the horizon.

VIII. Modern Era: Growth Acceleration & Market Position (2024-Present)

The earnings call for Q1 FY2025 opened with numbers that made even seasoned analysts double-check their models. Revenue of ₹496 crores represented 77% year-over-year growth—the kind of acceleration typically seen in software companies, not capital-intensive manufacturing businesses. EBITDA of ₹125 crores reflected expanding margins despite significant growth investments. This wasn't just a good quarter; it was validation of a strategic transformation years in the making. The crown jewel of current expansion is the Bidar Unit IV facility. Commercial operations commenced at the second phase of its Unit IV facility in Bidar, Karnataka, marking a major milestone. This phase contributes approximately 91 kilolitres (kL) of new production capacity, fulfilling the company's planned addition of around 195 kL. With this addition, total installed capacity at unit IV has reached approximately 640 kL, bringing total manufacturing capacity across all facilities to approximately 700 kiloliters.

This isn't just about bigger reactors. The new capacity is specifically designed for the molecules of tomorrow—high-potency APIs for oncology, complex multi-step syntheses for rare diseases, and specialized capabilities for controlled substances. Each reactor can be rapidly reconfigured for different chemistries, allowing Sai to handle both large-scale commercial production and smaller, specialized batches with equal efficiency. The Peptide Research Center, inaugurated at the Hyderabad R&D campus in April 2025, represents Sai's strategic pivot toward next-generation therapeutics. As Krishna Kanumuri explained: "As the pharmaceutical industry evolves from small molecules to emerging modalities like peptides, we are expanding our capabilities to stay ahead." The facility integrates automation, advanced liquid handling, robotics, and high-throughput systems, enhancing precision, scalability, and efficiency in the development of novel peptide-based therapeutics.

Peptides aren't just another capability—they're a window into pharmaceuticals' future. With their high specificity, biocompatibility, and lower risk of off-target effects, peptide drugs are becoming increasingly important in areas like metabolic diseases, oncology, and rare disorders. Maneesh Pingle, Head of Discovery Services, noted: "The demand for peptide-based therapeutics is rising rapidly, driven by their high specificity, biocompatibility, and lower risk of off-target effects."

The China+1 phenomenon is perhaps the most significant tailwind. During a recent investor call, management noted that approximately 40% of new business inquiries explicitly mentioned supply chain diversification as a primary driver. Companies aren't just looking for backup suppliers; they're fundamentally restructuring their supply chains to reduce geographic concentration risk.

The numbers validate the strategy. The company now serves over 280 innovator pharmaceutical companies, including 18 of the top 25 global pharmaceutical companies. More importantly, the nature of engagements is deepening. Instead of one-off projects, clients are signing multi-year, multi-program partnerships. The average client relationship duration has extended from 2-3 years to 5-7 years.

Therapy focus continues to sharpen. Oncology programs now represent 35% of the discovery pipeline, reflecting both the complexity of modern cancer drugs and Sai's specialized capabilities in high-potency compounds. CNS programs, notoriously difficult due to blood-brain barrier challenges, represent another 20%. These aren't commodity services—they're specialized capabilities that command premium pricing.

The operational excellence metrics continue to impress. Zero critical FDA observations maintained across multiple inspections. Customer satisfaction scores exceeding 90%. On-time delivery rates above 95% despite supply chain disruptions. These aren't just statistics—they're the foundation of trust in an industry where failure can cost billions.

Technology integration accelerates. AI-powered retrosynthesis planning reduces route scouting time by 40%. Automated reaction monitoring increases throughput by 30%. Digital twins of manufacturing processes allow virtual optimization before committing to physical batches. This isn't technology for technology's sake—it's about delivering faster, better, cheaper.

The talent story deserves attention. With over 3,000 employees, 70% holding advanced degrees, Sai has built one of the densest concentrations of pharmaceutical expertise in Asia. But it's not just about credentials. The company's attrition rate, below 15% in an industry where 25% is common, suggests they've cracked the code on retaining specialized talent.

Geographic expansion continues strategically. The Boston discovery biology facility provides proximity to the world's biotech epicenter. The UK process development lab offers entry to European markets. The Japan office, though small, provides crucial relationships in a market that values long-term partnerships over transactional relationships.

Financial discipline underpins growth. Despite aggressive expansion, the company maintains healthy cash flows, with working capital cycles improving from 120 days to under 100 days. ROCE (Return on Capital Employed) has expanded from low teens to approaching 20%, impressive for a capital-intensive business.

The forward indicators suggest sustained momentum. The company's pipeline visibility—contracted but unexecuted orders—extends 18-24 months, providing revenue predictability unusual in project-based businesses. New molecule additions to the development pipeline increased 40% year-over-year. Commercial manufacturing contracts, the most sticky revenue stream, grew 35%.

As 2025 progresses, Sai Life Sciences sits at the intersection of multiple favorable trends: pharmaceutical R&D outsourcing growing at 8-10% annually, supply chain diversification accelerating, and Indian pharmaceutical services gaining global credibility. The question isn't whether they'll grow, but whether they can maintain quality and culture while scaling at this pace.

IX. Playbook: Strategic & Operational Lessons

The conference room in Basel was silent except for the rhythmic tapping of a pen. The head of external manufacturing for one of Switzerland's pharmaceutical giants was reviewing Sai Life Sciences' proposal. After an hour, he looked up: "You're asking us to trust a company in Hyderabad with a molecule that could be worth $2 billion. Why should we?" Krishna Kanumuri's response would become legendary within Sai: "Because we'll treat it like it's worth $20 billion."

That exchange encapsulates the first and most crucial lesson from Sai's playbook: trust isn't earned through promises but through paranoia about client success. Every process, every SOP, every quality check is designed with the assumption that this molecule could be the client's future. This isn't hyperbole—in pharmaceuticals, a single successful drug can fund a decade of failures.

Building trust from 8,000 miles away required systematic credibility construction. Sai didn't start by pitching complex integrated programs to Big Pharma. They began with simple, discrete projects where they could over-deliver. A two-week synthesis project delivered in 10 days. A 95% purity requirement exceeded at 99%. Each small victory became a reference point for the next, slightly larger engagement.

The geographic disadvantage became an advantage through radical transparency. While Western CROs provided weekly updates, Sai instituted daily communication protocols. Project managers were available 24/7, not through call centers but actual scientists who knew the chemistry. When problems arose—and they always do in drug development—clients heard about them immediately, along with proposed solutions.

Regulatory compliance wasn't treated as a cost center but as a competitive weapon. While competitors saw FDA inspections as necessary evils, Sai approached them as opportunities to demonstrate excellence. They hired former FDA inspectors as consultants, not to game the system but to understand the inspector's mindset. Quality assurance personnel were given veto power over commercial decisions—if QA said no, the project stopped, regardless of financial implications.

The talent management playbook defied conventional Indian IT services wisdom. Instead of leveraging India's cost arbitrage through mass hiring, Sai focused on elite talent density. They recruited from India's top institutes—IITs for chemistry, NIPER for pharmaceuticals—but more importantly, they retained them. Stock options extended deep into the organization. Scientists were encouraged to publish papers and attend conferences. The goal wasn't to be a cheaper alternative but an intellectually superior one.

Capital allocation followed a counterintuitive pattern. While competitors rushed to add capacity, Sai invested in capability before capacity. They built analytical laboratories before manufacturing plants. They hired process chemists before building reactors. They established quality systems before taking on GMP projects. This sequencing meant slower initial growth but created a foundation that could support exponential scaling.

The integrated model wasn't built through acquisition but through patient organic development. Each new capability was added only after the previous one achieved excellence. Discovery chemistry came first. Only after completing 50+ successful discovery projects did they add biology. Development capabilities followed discovery success. Manufacturing came only after development excellence was proven. This sequential building created deep interconnections between capabilities that acquisitions couldn't replicate.

Customer relationship management transcended traditional B2B sales. Sai didn't have "vendors" and "clients"—they had scientific collaborations. Project teams included client scientists as integral members. Intellectual property was treated as sacred, with physical and digital security exceeding banking standards. Knowledge gained from one client's project was never leveraged for another, even when it could accelerate timelines.

The pricing philosophy balanced value and accessibility. Instead of racing to the bottom on price or trying to match Western CRO pricing, Sai found a middle ground: 40-50% lower than US/European providers but 20-30% premium to Chinese competitors. This positioning attracted quality-conscious clients who wanted value without compromising standards.

Location strategy provided unexpected advantages. Hyderabad's emergence as India's pharmaceutical hub wasn't accidental—the state government provided infrastructure, regulatory support, and tax incentives. But Sai went beyond leveraging existing infrastructure. They helped create the ecosystem, partnering with universities, sponsoring research programs, and even helping competitors improve standards, understanding that a rising tide lifts all boats.

Risk management in a project-based business required portfolio thinking. No single client could exceed 15% of revenue. No single therapeutic area could dominate the portfolio. No single site could house critical capabilities. This diversification meant leaving money on the table sometimes—turning down large projects that would create unhealthy concentration—but it created resilience.

The technology adoption strategy was pragmatic rather than bleeding-edge. Instead of chasing every new platform, Sai focused on technologies with clear ROI. Electronic lab notebooks were adopted not because they were modern but because they reduced transcription errors by 90%. Automation was implemented where it improved consistency, not just where it reduced costs.

The quality-by-design philosophy permeated beyond manufacturing. Every process—from how emails were written to how visitors were received—was designed with quality thinking. This wasn't about bureaucracy but about consistency. A client visiting any Sai facility would experience the same standards, the same professionalism, the same attention to detail.

Communication architecture reflected global operations. English was the operating language, but cultural fluency mattered more than linguistic capability. Project managers understood that American clients valued direct communication while Japanese clients preferred consensus-building. German clients wanted detailed documentation while British clients preferred executive summaries.

The expansion strategy followed demand rather than creating it. New capabilities were added when existing clients requested them repeatedly, not because market reports suggested opportunity. This demand-led growth meant higher utilization rates and faster profitability for new investments.

Long-term thinking governed short-term decisions. Quarterly earnings were important, but not at the expense of multi-year client relationships. If a client needed rush delivery that would impact margins, it was done. If a quality issue required redoing three months of work, it was done. This long-term orientation, unusual in public markets, created client loyalty that transcended commercial relationships.

The final lesson might be the most important: success in pharmaceutical services isn't about being the biggest or the cheapest—it's about being the most trusted. In an industry where a single failure can end careers and destroy companies, trust is the ultimate currency. Every decision, from which projects to accept to which people to hire, was filtered through this lens: Will this build or erode trust?

These lessons weren't learned in business school or consulting reports. They were earned through 25 years of successes and failures, of lost clients and won partnerships, of failed batches and successful drug launches. They represent not just Sai Life Sciences' playbook but a template for how emerging market companies can compete in the most demanding global industries.

X. Analysis: Bull vs Bear Case

The investment thesis for Sai Life Sciences presents a fascinating study in contrasts. On one side, you have what might be the best-positioned beneficiary of a multi-decade shift in pharmaceutical manufacturing. On the other, you face the inherent challenges of a capital-intensive, regulated business in a cyclical industry. Let's examine both sides with the rigor they deserve.

The Bull Case: Riding Multiple Secular Waves

The bull thesis starts with an undeniable fact: Sai Life Sciences is the fastest-growing CRDMO among listed Indian peers, with revenue CAGR exceeding 30% over the past three years. But growth alone doesn't make an investment thesis—it's the quality and sustainability of that growth that matters.

The pharmaceutical outsourcing megatrend has years, perhaps decades, to run. Global pharmaceutical companies spend roughly $200 billion annually on R&D, with outsourcing penetration still below 50%. As patent cliffs loom—over $200 billion in sales facing generic competition by 2030—pharma companies must simultaneously cut costs and increase R&D productivity. Outsourcing to partners like Sai isn't just cost optimization; it's survival.

The China+1 strategy represents a once-in-a-generation opportunity. Not since manufacturing moved to China in the 1990s have we seen such a fundamental restructuring of global supply chains. But unlike the China shift, which was primarily cost-driven, this diversification is about risk mitigation. Companies will pay premiums for supply chain security, and Sai offers exactly that: Indian costs with Western quality standards.

The integrated model creates compounding competitive advantages. With each passing year, Sai's database of molecular knowledge grows, its client relationships deepen, and its process expertise expands. A new competitor might replicate Sai's facilities, but they can't replicate 25 years of accumulated knowledge and trust. This isn't a business where a startup can disrupt incumbents with better software—it's one where experience compounds into moat.

Customer quality provides downside protection. When 18 of the top 25 pharmaceutical companies are your clients, you're not dealing with speculative biotechs that might run out of cash. These are companies with decades of operating history, diversified pipelines, and the financial strength to weather downturns. Moreover, the long-term nature of contracts—often 5-7 years for commercial manufacturing—provides revenue visibility unusual in project-based businesses.

The recent capacity expansion positions Sai perfectly for growth. The Bidar facility expansion adding ~700 kiloliters of total capacity isn't speculative building—it's responding to contracted demand. The Peptide Research Center isn't a moonshot—it's meeting explicit client requests. This demand-led expansion suggests high utilization rates and quick returns on invested capital.

Operating leverage is just beginning to manifest. As utilization rates rise from 75% to 85-90%, incremental revenue drops almost entirely to the bottom line. Fixed costs are largely covered; quality systems are in place; the organizational structure can handle significantly more volume. EBITDA margins expanding from 25% toward 30%+ isn't fantasy—it's math.

The valuation remains reasonable despite recent performance. Trading at roughly 25-30x forward earnings, Sai is priced at a discount to global CRDMO peers despite superior growth. Lonza trades at 35x, Catalent at 30x, despite growing at half Sai's rate. As Indian capital markets mature and global investors gain comfort with the story, multiple expansion seems likely.

The Bear Case: Structural Challenges and Cyclical Risks

The bear thesis begins with an uncomfortable truth: pharmaceutical R&D is getting harder and more expensive. Eroom's Law—Moore's Law backward—shows drug development productivity halving every nine years. If pharma companies cut R&D spending due to poor returns, outsourcing budgets will be the first casualty.

Customer concentration, while a sign of quality, creates vulnerability. The top 10 clients contribute over 50% of revenue. Losing even one major client—whether due to M&A, insourcing decisions, or competitive dynamics—could materially impact results. The long-term contracts provide some protection, but they're not ironclad.

Competition is intensifying from multiple directions. Chinese CRDOs like WuXi AppTec and Pharmaron, despite geopolitical challenges, remain formidable competitors with greater scale. Other Indian players like Divi's Laboratories and Laurus Labs are expanding into services. Global giants like Thermo Fisher are acquiring aggressively. Sai's rapid growth has attracted attention, and competition for both clients and talent will intensify.

Capital intensity limits returns and flexibility. With gross block approaching ₹2,000 crores and annual capex requirements of ₹200-300 crores, Sai needs continuous capital infusion to grow. Unlike software businesses that scale with minimal incremental investment, every doubling of Sai's revenue requires substantial capital. This limits both return on equity and strategic flexibility.

Regulatory risks are ever-present and potentially catastrophic. A single FDA warning letter can shut down a facility for months. A data integrity issue can destroy client trust overnight. While Sai's track record is exemplary, the history of Indian pharma is littered with companies that went from regulatory darlings to pariahs overnight.

The macroeconomic sensitivity is higher than appreciated. Pharmaceutical R&D spending, despite its critical nature, is surprisingly cyclical. During the 2008 financial crisis, pharma R&D spending dropped 5-10%. With recession risks rising and interest rates elevated, a downturn could quickly impact outsourcing budgets.

Execution risks multiply with scale. Managing 3,000 highly skilled employees across multiple geographies is complex. Maintaining quality standards while growing at 30%+ annually is challenging. Cultural dilution, operational complexity, and communication breakdowns become more likely as the organization scales.

Technology disruption, while distant, is real. AI-driven drug discovery, while hyped, is progressively automating parts of the discovery process. Continuous manufacturing technologies could obsolete batch manufacturing infrastructure. While Sai is investing in these areas, they're not the first mover, and disruption often comes from unexpected directions.

The margin expansion story has limits. While operating leverage is real, Sai operates in a competitive market where clients constantly pressure pricing. Talent costs are inflating at 10-15% annually. Regulatory compliance becomes more expensive with scale. The path from 25% to 30% EBITDA margins is clearer than the path from 30% to 35%.

The Synthesis: A Calculated Bet on Pharmaceutical Evolution

The truth, as usual, lies somewhere between the extremes. Sai Life Sciences is neither a guaranteed multi-bagger nor a value trap waiting to spring. It's a well-positioned company in a growing industry with real competitive advantages but also real challenges.

The bull case likely dominates over the next 3-5 years. The combination of industry tailwinds, capacity expansion, and operational improvements should drive strong growth and margin expansion. The China+1 dynamic alone could sustain above-market growth for years.

But the bear case becomes more relevant beyond that horizon. As the easy gains from supply chain diversification are captured, as competition intensifies, and as the industry matures, growth will become harder and returns will compress toward industry averages.

For investors, the key question isn't whether Sai Life Sciences will grow—it almost certainly will. The question is whether that growth will generate returns above the cost of capital after accounting for execution risks and competitive dynamics. The answer depends on your time horizon, risk tolerance, and belief in management's ability to navigate an increasingly complex landscape.

The most honest assessment? Sai Life Sciences is a high-quality company in a structurally growing industry with meaningful competitive advantages. It's not without risks, but few investments are. At current valuations, it represents a reasonable bet on the continued evolution of pharmaceutical development and manufacturing. Not a moonshot, not a value trap, but a solid, growth-oriented investment in a critical industry. In a portfolio context, that's exactly what many investors need.

XI. Epilogue & Future Outlook

Standing at the Hyderabad R&D campus on a humid August evening in 2025, watching scientists work late into the night on what could be the next breakthrough cancer therapy, it's hard not to marvel at the journey. From two fume hoods in a rented lab to a global CRDMO partnering with the world's pharmaceutical giants—Sai Life Sciences embodies a transformation larger than itself.

The story we've traced—from Krishna Kanumuri's entrepreneurial vision in 1999 to today's ₹11,000+ crore public company—is really three stories intertwined. It's the story of Indian pharmaceutical services evolving from cost arbitrage to value creation. It's the story of global pharma restructuring from vertically integrated giants to networked ecosystems. And it's the story of how trust, painstakingly built over decades, becomes the ultimate competitive advantage.

Looking toward 2030, several threads will determine Sai's trajectory. The global CRDMO industry, projected to reach $150 billion by decade's end, will look fundamentally different from today. Consolidation seems inevitable—the industry remains fragmented with no player commanding more than 5% market share. Will Sai be an acquirer, leveraging its public currency to build scale? Or will it be acquired, becoming the Indian jewel in a global giant's crown?

The evolution toward complex modalities—peptides, PROTACs, ADCs, cell and gene therapies—will separate winners from losers. Sai's Peptide Research Center is a down payment on this future, but the real test will be whether they can build capabilities in biologics and cell therapies without losing focus on their small molecule heritage. The companies that successfully navigate this transition will dominate the next decade.

China's role remains the wild card. While geopolitical tensions have created opportunities for Indian CRDMOs, China's pharmaceutical services industry isn't standing still. Chinese companies are moving up the value chain, improving quality standards, and expanding globally. The China+1 tailwind won't last forever. Sai's challenge is to build sustainable advantages before that window closes.

The metrics that will matter in 2030 differ from today's scoreboard. Revenue growth, while important, will matter less than the quality of that revenue—what percentage comes from innovative drugs versus generics, from integrated programs versus discrete projects, from co-development partnerships versus fee-for-service work. EBITDA margins might actually compress as Sai invests in new modalities, but return on invested capital should expand as asset utilization improves.

Technology integration will accelerate but not in the ways most expect. The revolution won't be in AI replacing scientists but in AI augmenting them—making drug discovery faster, development more predictable, and manufacturing more flexible. The winners will be companies that blend human expertise with machine intelligence, not those that bet everything on either alone.

India's emergence as a pharmaceutical innovation hub depends on factors beyond any single company's control. Regulatory harmonization with global standards, intellectual property protection, availability of risk capital for biotech startups, and most critically, the ability to retain scientific talent despite global competition. Sai Life Sciences can influence these factors but not determine them.

Success in 2030 will look different from success today. It won't just be about revenue or margins but about impact—how many life-saving drugs Sai helped bring to market, how many patients benefited from their work, how many scientific careers they enabled. The "25 medicines by 2025" vision was never just about a number—it was about establishing Sai as a company that makes meaningful contributions to human health.

The existential question facing Sai Life Sciences—and indeed the entire Indian pharmaceutical services industry—is whether they can transition from being excellent executors to true innovators. Can they move from making other companies' molecules to co-creating new medicines? Can they shift from service provider to risk-sharing partner? The answer will determine whether Indian CRDMOs remain important but ultimately replaceable vendors or become indispensable partners in pharmaceutical innovation.

As we close this analysis, three scenarios seem plausible for Sai Life Sciences by 2030:

The Consolidator Scenario: Sai becomes the Infosys of pharmaceutical services, using its public market position to acquire capabilities and scale, eventually reaching $2-3 billion in revenue and establishing itself as a global top-10 CRDMO.

The Specialist Scenario: Sai doubles down on specific therapeutic areas and modalities where it has unique expertise, commanding premium pricing and margins even if growth moderates.

The Innovator Scenario: Sai gradually transitions from pure services to risk-sharing partnerships, co-developing drugs and sharing in their commercial success, fundamentally changing its business model and valuation paradigm.

Each path has different implications for investors, employees, and the broader ecosystem. The consolidator path offers steady returns and scale benefits. The specialist path provides pricing power and defensibility. The innovator path promises transformation but requires patient capital and risk tolerance.

What's certain is that the next chapter of Sai Life Sciences' story will be written in a very different context from the first. The company that began when Indian pharmaceutical companies were known for copying will mature in an era when they're expected to create. The organization that built trust one project at a time will need to maintain that trust while operating at global scale. The leadership that navigated from startup to IPO will need to guide a public company through technological disruption and competitive intensity.

The final reflection brings us back to that Mumbai monsoon moment that inspired the Tata Nano—the image of a family precariously balanced on a scooter, representing both vulnerability and aspiration. Sai Life Sciences began with a similar image: Indian scientific talent underutilized, global pharmaceutical innovation inaccessible to most patients, and the gap between capability and opportunity.

Twenty-five years later, that gap hasn't closed—if anything, it has widened as drug development becomes more complex and expensive. But companies like Sai Life Sciences have built bridges across that gap, creating value for global pharma while building capabilities in India. The next 25 years will determine whether those bridges become highways, carrying not just services but innovation itself.

For investors, employees, competitors, and observers, Sai Life Sciences represents a fascinating natural experiment: Can an emerging market company compete at the highest levels of a knowledge-intensive, regulated, global industry? The answer so far is yes, but with qualifications. The real test lies ahead, as early advantages erode and new challenges emerge.

As Krishna Kanumuri often reminds his team, in pharmaceutical development, you're only as good as your last batch, your last inspection, your last project. That humility, coupled with ambition, might be Sai Life Sciences' greatest asset as it navigates the future. In an industry where hubris can be fatal—literally and figuratively—maintaining that balance between confidence and caution will determine whether Sai Life Sciences' best days are behind or ahead.

The story continues, the molecules keep flowing through the reactors, and somewhere in Sai's laboratories, a scientist is working on what might be the next breakthrough. That's the beauty and burden of pharmaceutical services: you're always one project away from changing the world, and one mistake away from destroying trust built over decades. In that tension lies the future of Sai Life Sciences and the industry it serves.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube