RattanIndia Power: From Indiabulls Spinoff to Stressed Asset Turnaround

I. Introduction & Episode Roadmap

Picture this: In 2019, India's power sector was a graveyard of ambitions. Across the country, gleaming thermal power plants sat idle—monuments to $40 billion in stranded assets. Banks were bleeding red ink. Promoters were fleeing to bankruptcy courts. And yet, in a boardroom in Mumbai, executives from Goldman Sachs and Värde Partners were preparing to write one of the largest checks ever cut for a distressed Indian power asset. Their target? RattanIndia Power—a company that had just posted a staggering ₹27.9 billion loss.

This is the story of how RattanIndia Power, one of India's largest private thermal power generators with 2,700 MW capacity, navigated from conglomerate spinoff to near-collapse to remarkable turnaround. Born from the 2014 split of the Indiabulls empire, the company would pioneer India's first major power sector debt resolution outside bankruptcy courts—a template that would reshape how distressed infrastructure assets are rescued.

The central question isn't just how a power company survived India's worst infrastructure crisis. It's how Rajiv Rattan, an IIT Delhi engineer turned serial entrepreneur, convinced international investors to bet billions on coal-fired plants when the world was pivoting to renewables. The answer reveals profound lessons about timing, tenacity, and the art of the turnaround in emerging markets.

What makes RattanIndia's journey particularly fascinating is its counter-narrative arc. While peers rushed into captive coal blocks and got burned by Supreme Court cancellations, RattanIndia stayed clear. While others declared bankruptcy, it engineered a novel debt resolution. While the sector wrote obituaries for thermal power, it turned profitable. This isn't just a turnaround story—it's a masterclass in navigating systemic crisis through financial innovation and operational discipline.

II. The Indiabulls Origins: Building a Conglomerate (2000–2014)

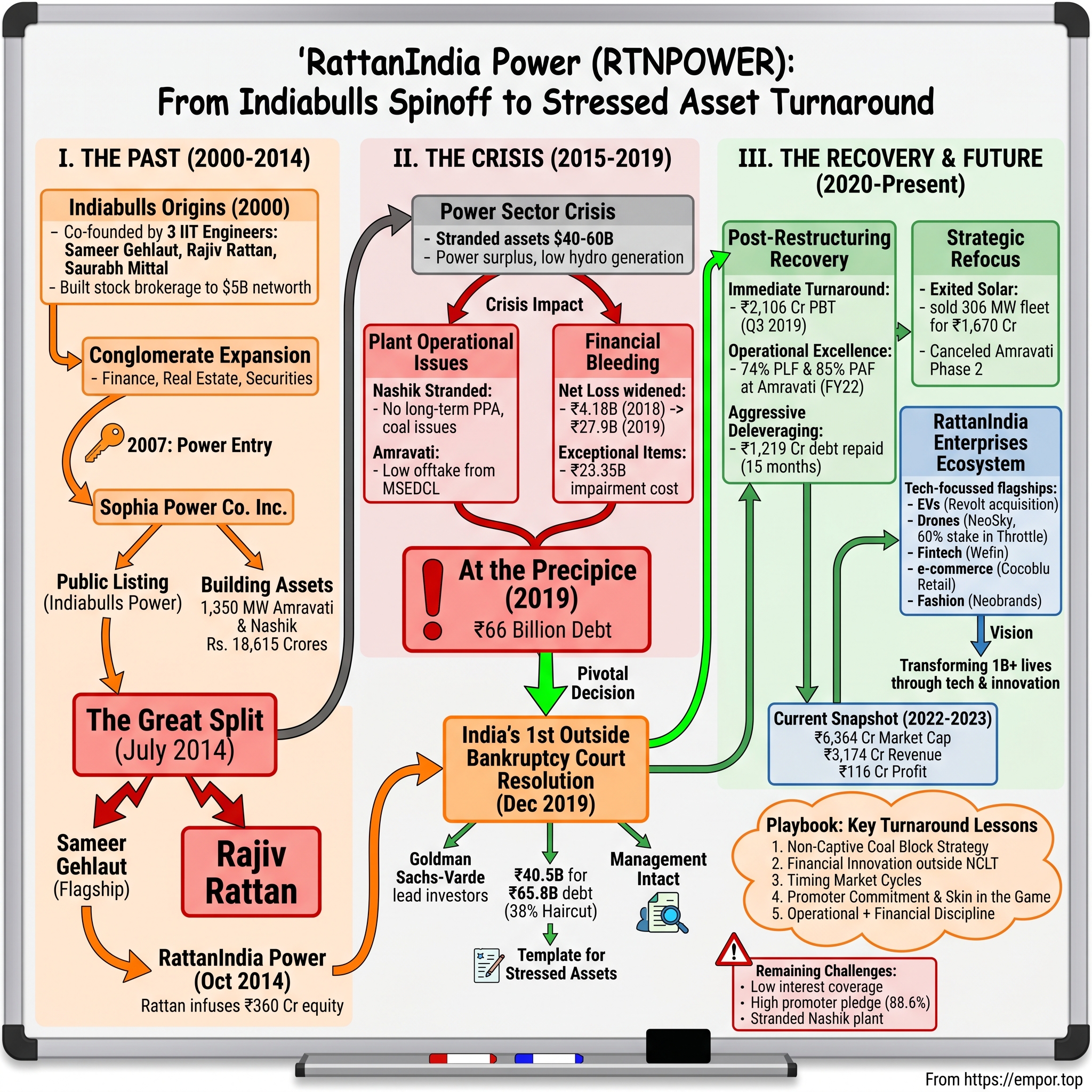

The millennium's dawn brought a new breed of Indian entrepreneurs—young engineers who saw opportunity where established players saw tradition. Indiabulls was started in 2000 with the establishment of Indiabulls Financial Services, a stockbroking firm co-founded by three IIT Delhi graduates–Sameer Gehlaut, Rajiv Rattan and Saurabh Mittal. An alumnus of IIT Delhi, Rajiv started his professional career with Schlumberger, one of the largest oilfield services company in the world. The three engineers, all in their mid-twenties, weren't content with safe corporate careers. They wanted to build something audacious.

Indiabulls Group started as India's first online stock trading brokerage which went on to become a large business conglomerate with businesses in Consumer Finance (2nd largest mortgage lender in India), Securities (largest stock brokerage in India), Real Estate and Power Generation with a combined networth of more than $5 billion. The timing was impeccable—India was just beginning its digital revolution, retail investing was nascent, and the financial services sector was ripe for disruption.

In October 1999, along with Rattan and Mittal, Gehlaut started Indiabulls after acquiring a Delhi brokerage. What began as a small acquisition quickly transformed into something far more ambitious. By 2004, the company had gone public, becoming one of India's fastest-growing financial services firms. The IPO was a watershed moment—suddenly, three engineers who'd started with borrowed capital were sitting atop a company worth hundreds of crores.

The conglomerate's expansion was breathtaking in both speed and scope. Indiabulls Financial Services subsequently set up subsidiaries in stockbroking, consumer finance, housing finance and real estate, among others. Indiabulls Real Estate was demerged from the company in 2006, and Indiabulls Securities in 2008. Each vertical wasn't just an add-on—it was a full-scale assault on established incumbents. The housing finance business would eventually become India's second-largest mortgage lender. The securities arm would handle more trades than firms that had existed for decades. But the move that would define Rajiv Rattan's legacy came in 2007, when the power sector beckoned. RattanIndia Power Limited was formerly incorporated in the name of Sophia Power Company Limited on October 8, 2007. On July 2009, the Company name was changed from Sophia Power Company Limited to Indiabulls Power Limited following its public listing. This wasn't just another vertical—it was a massive bet on India's infrastructure future, requiring capital commitments that dwarfed anything the group had done before.

The entry into power generation came at the peak of India's infrastructure euphoria. Private players were rushing to build capacity, state governments were doling out permits like candy, and everyone believed India's power demand would double every decade. The Indiabulls team saw an opportunity to leverage their financial engineering skills and access to capital markets to build world-class power assets from scratch. It was audacious—three finance guys with no power sector experience deciding to build multi-billion-dollar thermal plants.

By 2014, the conglomerate had grown into a sprawling empire worth over $5 billion in market value. But beneath the surface, tensions were brewing. Three founders, three visions, and increasingly divergent views on where to focus. The power business, in particular, had become a point of contention—it was capital-intensive, faced regulatory headwinds, and required a long-term commitment that not all partners shared. The stage was set for one of corporate India's most significant demergers.

III. The Great Split: Carving Out RattanIndia (2014)

July 2014 brought the thunderclap announcement. The three promoters of Indiabulls had split. Sameer Gehlaut would control the flagship companies like Indiabulls Housing Finance, Indiabulls Real Estate, Indiabulls Securities. Rajiv Rattan and Saurabh Mittal would control Indiabulls Power Ltd and Indiabulls Infrastructure and Power Ltd and would not be able to use the Indiabulls brand name after December 31. For outsiders, it seemed sudden. But insiders knew this had been brewing for months—divergent visions, different risk appetites, and fundamentally incompatible views on capital allocation.

The power business had become the focal point of disagreement. "It was imperative to ringfence" the retail brand from Indiabulls Power, an industrial company, as Housing Finance contributed 80 per cent to the group's profits. Gehlaut saw power as a capital sink that threatened the group's crown jewel—the housing finance business. Rattan saw it differently: an undervalued infrastructure play at the bottom of its cycle, ready for a turnaround.

Then came the September surprise. Rajiv Rattan, in a sudden move, took control of the group's two power companies after buying out Saurabh Mittal's stake in Indiabulls Infrastructure and Power. The acquisition came within two months of the promoters' split decision. Mittal would focus on the IT business while Rattan infused fresh equity of Rs 360 crore into Indiabulls Power. Rattan held 5 per cent directly, and through Indiabulls Infrastructure and Power (42 per cent stake), controlled 52 per cent of Indiabulls Power.

The timing wasn't coincidental. Rattan believed problems in the power business had reached "rock bottom". "In view of the proactive approach by the central government, the worst seems to be over," said Rattan who was the founding chairman. While others saw disaster, he saw opportunity. The Maharashtra regulator had just approved compensatory tariffs for imported coal usage—a game-changer for operational economics.

On October 30, 2014, the name officially changed from Indiabulls Power to RattanIndia Power with effect from the said date. Under the agreement, the power business would not use the Indiabulls brand name after December. It wasn't just a name change—it was a declaration of independence, a bet that one man's vision could salvage what a conglomerate had struggled to manage.

The split revealed a fundamental truth about Indian conglomerates: diversification can create value, but only until strategic visions diverge. Rattan was now alone at the helm of two massive thermal power projects, with construction still underway and the sector sliding into its worst crisis. The real test was about to begin.

IV. Building the Power Assets: Amravati & Nashik (2007–2015)

In 2007, when ground was broken on two massive thermal power projects in Maharashtra, India's power sector was riding high on promises of 9% GDP growth and insatiable energy demand. Amravati Thermal Power Plant in situated in Nandgaonpeth, 13 kilometers from Amravati city, Maharashtra in India. This coal based thermal power plant spread over an area of 1,350 acres at MIDC Industrial Area. NASIK THERMAL POWER PROJECT is being setup by Sinnar Thermal Power Ltd. (formerly known as RattanIndia Nasik Power Ltd.) – a subsidiary of RattanIndia Power Limited in 2,500 acre Multi-product SEZ at Sinnar, Nasik district, Maharashtra.

The scale of ambition was staggering. RattanIndia Power is one of Indias largest private power generation company, with installed capacity of 2,700 MW thermal power plants at Amravati and Nashik (1,350 MW at each location) in Maharashtra, India with investments of Rs. 18,615 Crores (US $2.5 Billion). Each plant would comprise five subcritical units of 270 MW—state-of-the-art BHEL equipment with no international risk for engineering and services. This wasn't just infrastructure; it was nation-building on an industrial scale.

The Amravati project moved with remarkable speed. By February 2015, the first units were ready. Then came a display of execution prowess that stunned the industry: RattanIndia has set a new benchmark in power plant construction and erection history of India by commissioning 3 units within a time span of 39 days at one site. Unit 3 and Unit 4 of Amravati power plant had earlier achieved COD on 03/02/2015 and 08/03/2015 respectively. By March 2015, all five units were operational—a 1,350 MW behemoth ready to power Maharashtra's growth.

The supporting infrastructure was equally impressive. Amravati Power Transmission Company Ltd. (APTCL), a wholly owned subsidiary of RattanIndia Power Ltd., has commissioned the transmission system for evacuation of power from Amravati power plant. The transmission system includes 104 km 400 KV D/C Quad Moose line from Amravati Project to Akola Substation. A dedicated railway line ensured coal supply from South Eastern Coalfields. Everything was engineered for maximum efficiency.

But Nashik told a different story—one that would haunt RattanIndia for years. In November 2014, it was reported that the full phase I of the Nashik plant was ready for commissioning but had not done so due to want of coal. The plant faced multiple challenges: land acquisition disputes, missing railway linkages, and crucially, no long-term power purchase agreements. While Amravati hummed with activity, Nashik stood largely idle—a ₹9,000 crore monument to the complexities of Indian infrastructure development.

The contrast between the two projects was stark. Amravati had secured a 25-year PPA with Maharashtra State Electricity Distribution Company Limited (MSEDCL) for 1,200 MW. Nashik had managed only fragmented agreements—650 MW with MSEDCL and hopes for another 300 MW with BEST Mumbai that never materialized. One plant was printing money; the other was bleeding it. The stage was set for one of Indian power sector's most dramatic crises.

V. The Power Sector Crisis Years (2015–2019)

By 2015, India's power sector had transformed from boom to bust. Excessive plant construction loans at 75% of overestimated costs on overrated plant capacities have led to stranded assets of US$40 to 60 billion. What began as ambitious capacity expansion had become a nightmare of idle plants, mounting debt, and vanishing demand. By the end of the calendar year 2015, despite poor hydroelectricity generation, India had become a power surplus nation with huge power generation capacity idling for want of demand.

For RattanIndia Power, the crisis hit particularly hard. The company had bet everything on Maharashtra's power demand continuing its upward trajectory. Instead, distribution companies began backing down power purchases, preferring cheaper renewable energy or simply reducing offtake to manage their own financial stress. As per the company, the suboptimal performance of its TPPs owing to lower offtake by MSEDCL led to financial stress. The Amravati plant, despite its operational excellence, was running well below capacity.

The Nashik plant became the poster child for everything wrong with India's power sector. RattanIndia has two thermal power plants: the first is the Nashik power plant that was reported stranded in 2020 due to no long-term purchase agreements. With no PPAs and coal supply issues, the plant sat largely idle—a ₹9,000 crore white elephant consuming maintenance costs while generating minimal revenue. The contrast with Amravati couldn't have been starker: one plant struggling with reduced offtake, the other essentially non-operational.

The financial hemorrhaging accelerated dramatically. The company's net loss also widened considerably from Rs 4.18 billion during 2017-18 to Rs 27.9 billion during 2018-19. The huge increase in the net loss is due to exceptional items, which primarily include Rs 23.35 billion on account of impairment cost. This wasn't just an operational loss—it was an acknowledgment that billions in invested capital might never generate returns.

What saved RattanIndia from complete disaster was a strategic decision made years earlier. Indiabulls Power was the only listed company in the power space that would not be impacted by the deallocation of coal blocks because it did not have any captive blocks. While peers scrambled after the Supreme Court's coal block cancellation, RattanIndia's reliance on Coal India linkages proved prescient. It was a small mercy in an ocean of troubles.

The broader context was equally grim. Tim Buckley, lead author of the report and director of energy finance studies with IEEFA, says stranded assets in the Indian thermal sector are not limited to the 34 projects highlighted by the Standing Committee on NPAs. "THE ISSUE IS DEEPER, AND THE FUTURE PIPELINE FACES SIMILAR RISKS," says Buckley. Banks were drowning in power sector NPAs, refusing new loans, and demanding resolution.

By 2019, RattanIndia Power stood at the precipice. With nearly ₹66 billion in debt, mounting losses, and one plant essentially stranded, the company needed a miracle. The entire sector was looking at insolvency courts as the only solution. But Rajiv Rattan had other plans—ones that would require convincing some of the world's most sophisticated investors to bet on Indian thermal power at its darkest hour.

VI. The Goldman Sachs Rescue: India's First Major Power Debt Resolution (2019–2020)

December 2019 marked a watershed moment not just for RattanIndia Power, but for India's entire distressed asset resolution framework. A Goldman Sachs- and Varde Partners-led coalition of investors have agreed to acquire all of the outstanding debt of India-based power generation company RattanIndia Power from the company's 12 existing lenders for INR40.5 billion (USD566 million). The face value of the portfolio is INR65.8 billion (USD919 million). This wasn't just a bailout—it was a sophisticated financial engineering solution that would become a template for the entire sector.

The deal structure was innovative and complex. Under the OTS transaction, the consortium of lenders led by PFC and SBI assigned RattanIndia Power's existing principal debt of about Rs 65.74 billion to a set of new investors, led by Goldman Sachs and Värde Partners, through Aditya Birla ARC Limited for Rs 40.5 billion. The firm's consortium of 12 lenders led by Power Finance Corp. Ltd (PFC) agreed to take a 38% haircut against their exposure of ₹6,575 crore to RattanIndia Power. Banks took their losses, but avoided the protracted pain of bankruptcy courts.

What made this deal remarkable was what it wasn't. Notably, this is the first successful scheme to have been closed under the RBI's Prudential Framework for Resolution of Stressed Assets and the largest in terms of size outside the National Company Law Tribunal (NCLT) framework without any change in the existing management. While peers were being dragged through insolvency proceedings with promoters losing control, Rajiv Rattan had engineered a solution that kept him at the helm.

The transaction valued something the market had forgotten: operational excellence. As per the company, the transaction values the company's generation assets at Rs 30 million per MW as against a value of Rs 12 million-Rs 15 million per MW discovered under most deals resolved as per the NCLT framework. Goldman Sachs and Värde weren't just buying distressed debt—they were betting on the Amravati plant's proven ability to generate cash flow, its long-term PPA with MSEDCL, and critically, on management's ability to navigate India's complex power sector.

CEO Aman Singh captured the significance: "the first of its kind in the stressed power space with overseas investors investing in the Indian power sector. This deal will provide a template for more such foreign investments in stressed assets." It was a bold claim that would soon be tested by reality.

The immediate impact was dramatic. The company's balance sheet was transformed overnight—debt reduced by 38%, fresh capital infused, and critically, patient foreign investors replaced anxious Indian banks. Goldman Sachs and Värde brought more than money; they brought credibility and time—two commodities RattanIndia desperately needed. The stage was set for one of Indian power sector's most remarkable turnarounds.

VII. Post-Restructuring Recovery & Turnaround (2020–Present)

The transformation was immediate and dramatic. Rattan India Power turned around in the current quarter ending December, 2019 to report a profit before tax of Rs 2,106 crore. It had a loss of Rs 188 crore in the corresponding quarter of the previous financial year. The profit comes after conclusion of debt resolution for its 1,350 MW Amravati power project in Maharashtra. This wasn't just a quarterly improvement—it was validation of the entire restructuring strategy.

The operational turnaround was equally impressive. RPL has demonstrated excellent operating performance in current FY 2021-22 amidst COVID-19 and acute coal shortage in the country affecting coal based thermal power plants. Amravati Thermal Power Plant has achieved the Plant Load Factor (PLF) of 74 per cent and Plant Availability Factor (PAF) of 85 per cent up to Q3 in current fiscal and stands out as one of the best thermal power plants in Maharashtra in operating performance. While the entire sector struggled with pandemic disruptions and coal shortages, RattanIndia's Amravati plant hummed along at near-peak efficiency.

Financial discipline became the new mantra. RattanIndia Power Ltd on Monday said it has repaid Rs 1,219 crore debt in the last 15 months, including Rs 200 crore prepayment, despite the challenges posed by the COVID-19. "During the last 15 months, RPL has repaid the debt of Rs. 1,219 crore to lenders, including Rs 200 crores as prepayment, even in the face of challenges posed by the pandemic," the company said in a BSE filing. This aggressive deleveraging signaled to markets that management wasn't just surviving—they were preparing for the next phase of growth.

But pragmatism ruled strategic decisions. The company, however, has decided to not construct the envisaged second phase of the Amravati project, owing to lack of long-term power purchase agreements (PPAs) in the market. This wasn't retreat—it was prudent capital allocation. Why build capacity when the market wasn't ready to buy it?A pivotal strategic shift came in September 2020. RattanIndia Group sold off its entire solar power project fleet totalling 306 Mw to Global Infrastructure Partners (GIP), one of the largest private equity firms in the renewable energy and infrastructure space. The deal value is Rs 1,670 crore, RattanIndia said in a public statement. The company was also involved in solar energy but that component was sold to GIP for Rs 1067 crore in September 2020 and the company exited the solar business.

This wasn't a retreat from renewables—it was strategic focus. With this deal, RattanIndia now has only two power plants in its basket – Amaravati thermal power plant (1,350 MW) for which it concluded debt restructuring in December 2019 and Nashik thermal power plant (1,350 MW) which is a stressed asset. The solar sale provided crucial capital for debt reduction while allowing management to concentrate on maximizing value from their thermal assets.

By 2022, the turnaround was complete. RPL posted a net profit of Rs 104.44 crore during the third quarter of FY2021-22 (Q3FY22), as against net profit of Rs 33.44 crore during the corresponding period of FY21. The company's EBITDA stood at Rs 298.72 crore during Q3 of the current fiscal. Vibhav Agarwal, Managing Director, captured the transformation: "RPL is a turn-around story in the Indian power sector with superlative operating performance. The company has showcased how stressed thermal assets can be resolved efficiently and put to use in the service of the nation."

The company's financial metrics showed sustained improvement. Current valuation metrics: Market Cap of 6,364 Crore, Revenue of 3,174 Cr, Profit of 116 Cr. While profitability remained modest relative to invested capital, the trajectory was unmistakable—from massive losses to consistent profits, from debt crisis to systematic deleveraging.

However, challenges persist. Company has low interest coverage ratio. Promoters have pledged or encumbered 88.6% of their holding. The Nashik plant remains largely stranded, entering insolvency proceedings in 2022. But the Amravati success story proved that with the right structure, even distressed thermal assets could generate value. The turnaround wasn't complete, but the proof of concept was undeniable.

VIII. The Broader RattanIndia Ecosystem

While RattanIndia Power fought its battles in the thermal sector, Rajiv Rattan was quietly architecting a parallel transformation. RattanIndia Enterprises Limited emerged as the flagship company of Rattanindia Group comprising tech focussed new age businesses including e-commerce, electric vehicles, fashion brands, fintech and drones. This wasn't diversification for its own sake—it was a calculated pivot toward India's digital future.

The strategy crystallized with a bold acquisition. In October 2022, RattanIndia Enterprises announced acquisition of electric motorcycle company Revolt Motors. The transaction was completed in January 2023, marking RattanIndia's aggressive entry into electric mobility. Revolt wasn't just any EV company—it was founded by Rahul Sharma, the maverick behind Micromax, and had already established a cult following for its RV400 electric motorcycle. The acquisition brought immediate results. Following the acquisition, Revolt became a wholly-owned subsidiary of RattanIndia Enterprises with plans to significantly scale up Revolt's growth. More impressively, between February 20 and March 31, 2023, Revolt Motors produced a record-breaking 6,500 bikes within a 40-day period, surpassing its previous average of 1,500 bikes per month—a fourfold increase in production within just two months of takeover. The drone ambitions were equally bold. RattanIndia Enterprises acquired a 60% stake in Bengaluru-based drone manufacturing startup Throttle Aerospace Systems through NeoSky India Limited, its wholly-owned subsidiary engaged in the business of drones. Founded in 2016 by Nagendran Kandasamy, who formerly worked with Boeing, Throttle Aerospace claims to be India's first drone manufacturer approved by the DGCA and also has a licence from the Ministry of Defence to manufacture military drones.

The vision was transformative. "Drones are set to redefine the commerce landscape in India in the next few years," said Anjali Rattan Nashier, Business Chairperson. "We believe drones will be the new smartphones, we want to see 'Made In India' drones in every Indian house." This wasn't hyperbole—in March 2022, RattanIndia Enterprises announced making an investment of INR 100 Cr in NeoSky, which would focus on designing, manufacturing and selling consumer micro drones across India. Beyond EVs and drones, the ecosystem expanded into multiple verticals. RattanIndia Enterprises Limited comprises tech focussed new age businesses including e-commerce, electric vehicles, fintech and drones. Through its wholly owned subsidiary Cocoblu Retail Ltd., RattanIndia Enterprises is one of the largest online sellers in India across multiple product categories.

The fintech ambitions were equally ambitious. RattanIndia Enterprises Ltd is leading the charge in Fintech through Wefin, a digital lending marketplace offering instant personal loans, two-wheeler loans, and credit cards to customers in partnership with leading banks and NBFCs in India.

In April 2023, RattanIndia made another strategic move. RattanIndia Enterprises launched a wholly-owned subsidiary Neobrands, marking its entry into the fast-growing apparel fashion business. Neobrands will be a house of brands across multiple fashion categories, including everyday fashion, denim, athleisure and performance wear categories. Anjali Rattan explained the rationale: "The fashion industry in India is witnessing a remarkable growth trajectory, with a huge demand for trendy and premium quality brands. Our brands across multiple categories are poised to capture this market opportunity by offering fashionable, yet affordable clothing options for men and women".

The vision tying all these ventures together was profound. As the company states: "Transform lives of a billion plus aspiring Indians through innovation and technology". This wasn't just corporate diversification—it was a bet on India's demographic dividend, its digital transformation, and the convergence of technology with everyday life. From power generation to electric motorcycles, from drones to fashion brands, RattanIndia was positioning itself at the intersection of India's infrastructure past and its technology future.

IX. Playbook: Lessons in Distressed Asset Turnaround

The RattanIndia Power story offers a masterclass in navigating sector-wide crisis through financial innovation and operational discipline. The playbook that emerged from their journey provides crucial lessons for anyone dealing with distressed infrastructure assets in emerging markets.

Managing Through Sector-Wide Crisis: The first lesson is counter-intuitive: sometimes the best strategy during a crisis is to do what you didn't do before it. While peers rushed into captive coal blocks during the boom, RattanIndia stayed out—a decision that looked foolish then but proved prescient when the Supreme Court cancelled allocations. As management noted, they were "the only listed company in the power space that would not be impacted by the deallocation of coal blocks." Strategic restraint during euphoria often becomes strategic advantage during crisis.

Innovation in Debt Resolution Outside Bankruptcy Courts: The Goldman Sachs-Värde deal wasn't just about getting a haircut—it was about creating a new template for distressed asset resolution. By structuring the deal outside NCLT, RattanIndia achieved what dozens of power companies couldn't: debt resolution with promoter control intact, international investors on board, and a valuation that recognized operational value rather than distressed liquidation. The deal valued assets at Rs 30 million per MW versus Rs 12-15 million in NCLT resolutions—a 100% premium for avoiding bankruptcy.

Rajiv Rattan's Philosophy: Throughout the crisis, Rattan maintained a contrarian view: "problems in the power business had reached rock bottom" and "in view of the proactive approach by the central government, the worst seems to be over." This wasn't blind optimism—it was calculated timing. He understood that infrastructure cycles are long, government intervention is inevitable, and the ability to survive the trough determines who captures value in the recovery.

The Importance of Patient Foreign Capital: Goldman Sachs and Värde weren't typical distressed debt investors looking for quick exits. They understood that Indian power assets require patient capital—time for regulatory reforms, tariff adjustments, and demand recovery. Their involvement brought not just money but credibility, transforming RattanIndia from a distressed borrower to a turnaround story. The aggressive debt repayment of Rs 1,219 crore in 15 months, including prepayments during COVID, signaled this transformation to markets.

Timing Market Cycles in Infrastructure: Infrastructure investing is fundamentally about timing cycles measured in decades, not quarters. RattanIndia entered power during the 2007 boom, survived the 2015-2019 bust, and positioned for recovery post-2020. The decision to sell solar assets for Rs 1,067 crore in 2020 wasn't abandoning renewables—it was monetizing non-core assets at peak valuations to strengthen the core business. Similarly, not building Amravati Phase 2 despite having approvals showed discipline—why add capacity without PPAs?

Promoter Commitment vs. Exit Strategies: Perhaps the most crucial lesson is about skin in the game. While many promoters abandoned ship during the crisis, Rattan doubled down—buying out partners, infusing Rs 360 crore of fresh equity, and pledging 88.6% of his holding to support the business. This wasn't recklessness; it was conviction that surviving the crisis would create asymmetric upside. The post-restructuring profit of Rs 2,106 crore in Q3 2019 validated this conviction.

The playbook also reveals what not to do. The Nashik plant's struggles—no railway line, no long-term PPAs, land disputes—show that in infrastructure, execution without securing offtake is a recipe for disaster. Having the best technology and newest equipment means nothing if you can't sell your output. The contrast between Amravati (secured PPA, operational success) and Nashik (no PPA, largely stranded) is a textbook lesson in project development priorities.

Finally, the RattanIndia story demonstrates that distressed asset turnarounds require both financial engineering and operational excellence. The debt resolution created breathing room, but sustained recovery came from operational improvements—achieving 74% PLF and 85% PAF at Amravati during COVID and coal shortages. This combination of financial restructuring and operational discipline is what separates successful turnarounds from mere survival.

X. Analysis & Investment Case

The investment case for RattanIndia Power presents a study in contrasts—a company that has engineered one of India's most successful power sector turnarounds yet trades at valuations that suggest the market remains skeptical.

Current Valuation Metrics: With a market cap of Rs 6,364 crore against revenues of Rs 3,174 crore and profits of Rs 116 crore, RattanIndia Power trades at a P/E multiple that appears reasonable for a turnaround story. However, the devil lies in the details. The company's low interest coverage ratio and 88.6% promoter pledge indicate that while operationally improved, financial stress persists. The market is pricing in execution risk on the Nashik plant and concerns about thermal power's long-term viability.

Competitive Position in Maharashtra's Power Market: RattanIndia's Amravati plant has emerged as one of Maharashtra's best-performing thermal assets, achieving 74% PLF when the state average hovers around 55%. The 25-year PPA with MSEDCL provides revenue visibility, but also caps upside during power shortages. The company operates in a market where it's neither the lowest-cost producer (that's NTPC) nor the most flexible (that's gas-based plants), but occupies a crucial middle ground—reliable baseload power with proven operational excellence.

Future of Thermal Power in India's Energy Transition: This is the existential question. India added 2.4 GW of coal-based capacity in FY24 and plans another 80 GW by 2030, suggesting thermal isn't dead yet. RattanIndia benefits from being an established operator in a market where new thermal capacity faces massive regulatory and financing hurdles. The company's plants are young (commissioned in 2015), efficient, and strategically located in India's most industrialized state. They're not competing with solar at noon but providing power at 8 PM when solar doesn't work and batteries aren't yet economical at grid scale.

Bear Case: The bear case writes itself. Stranded assets define the sector—Nashik's 1,350 MW sits largely idle with over Rs 9,000 crore invested. Renewable energy costs continue falling, making thermal PPAs increasingly uncompetitive. The 88.6% promoter pledge suggests limited financial flexibility, while ESG concerns make thermal power uninvestable for many institutional investors. Carbon pricing, if implemented, could destroy whatever economics remain. The company's current profitability might be peak earnings if renewable penetration accelerates or industrial demand shifts to captive green power.

Bull Case: The bull case rests on pragmatism trumping ideology. India's power demand is growing 7-8% annually, and someone needs to provide power when the sun doesn't shine and wind doesn't blow. RattanIndia has already taken its medicine—debt restructured, losses recognized, inefficient assets written down. The Amravati plant generates consistent cash flows, debt is being rapidly reduced, and the Goldman Sachs involvement provides credibility for future financing needs. If Nashik finds even partial resolution—say 650 MW of contracted capacity—it could add Rs 50-100 per share in value. The company trades at replacement cost despite having proven its ability to survive the worst sectoral crisis in Indian power history.

The Broader Ecosystem Play: The real option value might lie beyond RattanIndia Power itself. The broader RattanIndia Enterprises ecosystem—Revolt Motors, NeoSky drones, Neobrands fashion, Wefin fintech—represents a portfolio of new economy bets funded partly by old economy cash flows. If any of these ventures achieve scale, the value creation could dwarf the power business. Revolt Motors alone, if it captures even 5% of India's electric two-wheeler market, could be worth more than the entire current market cap.

Risk-Reward Assessment: RattanIndia Power is not for the faint-hearted. It's a leveraged bet on India's energy transition being messier and more prolonged than consensus expects. The company has proven it can survive existential crisis and generate profits, but whether it can generate returns above its cost of capital remains uncertain. For contrarian investors, it offers exposure to India's power sector recovery with management that has skin in the game and a track record of navigating crisis. For conservative investors, the promoter pledge, single-asset concentration risk, and thermal power's uncertain future make it uninvestable.

The investment case ultimately hinges on timeframe and conviction. Over 3-5 years, thermal power will likely remain crucial for India's grid stability, favoring established operators like RattanIndia. Over 10-15 years, the energy transition could render thermal assets stranded regardless of operational excellence. The company's current valuation suggests the market is pricing in the longer-term risk while potentially undervaluing near-term cash generation. For those who believe India's energy transition will be evolutionary rather than revolutionary, RattanIndia Power offers an interesting risk-reward proposition.

XI. Conclusion: The Art of the Infrastructure Turnaround

The RattanIndia Power saga represents more than just a corporate turnaround—it's a meditation on value creation in the most challenging circumstances. When Rajiv Rattan stood alone in 2014, taking control of two massive thermal power projects as the sector headed into its darkest period, conventional wisdom suggested he was catching a falling knife. Nearly a decade later, RattanIndia Power has not only survived but pioneered a new model for distressed infrastructure resolution in India.

The transformation from a ₹27.9 billion loss in FY19 to profitability by Q3 FY20 wasn't achieved through financial engineering alone. It required a rare combination of strategic patience, operational excellence, and the ability to convince sophisticated global investors that Indian thermal power, despite all its challenges, still had value to unlock. The Goldman Sachs-Värde transaction created a template that dozens of stressed power assets would attempt to follow, though few would match RattanIndia's execution.

What makes this story particularly instructive is its timing. RattanIndia navigated its crisis and recovery just as India's energy landscape began its most fundamental transformation—the shift toward renewables. Lesser management teams might have fought this transition, lobbying for thermal protection or doubling down on coal. Instead, RattanIndia accepted the new reality: maximize value from existing thermal assets while pivoting the broader group toward new economy opportunities. The sale of solar assets, the decision not to build Amravati Phase 2, and the aggressive diversification into EVs, drones, and fintech all reflect this pragmatic adaptation.

The lessons extend beyond the power sector. Infrastructure assets, by their nature, experience cycles measured in decades. Those who enter during booms often face busts; those who survive busts can capture extraordinary value in recoveries. RattanIndia's journey demonstrates that in infrastructure, the ability to endure determines ultimate returns more than initial positioning or even operational efficiency. The company that emerged from the crisis—delevered, focused, with patient international capital—bears little resemblance to the leveraged subsidiary that entered it.

Yet challenges persist. The Nashik plant remains largely stranded, a ₹9,000 crore reminder that even the best turnaround stories have incomplete chapters. The 88.6% promoter pledge suggests financial flexibility remains limited. The fundamental question about thermal power's role in India's energy future remains unanswered. These aren't just RattanIndia's challenges—they reflect the broader tensions in India's energy transition, where aspirations for renewable transformation meet the reality of baseload power needs.

The broader RattanIndia ecosystem—spanning from thermal power to electric motorcycles, from industrial drones to fashion brands—represents a fascinating experiment in portfolio transformation. Can cash flows from old economy infrastructure fund new economy ventures? Can the operational discipline learned in thermal power translate to consumer technology? The jury remains out, but the ambition is unmistakable: transform from an infrastructure company that survived crisis to a technology conglomerate that shapes India's future.

For students of distressed investing, RattanIndia Power offers crucial insights. First, in infrastructure distress, operational assets with proven cash flows can command significant premiums to stranded assets, even within the same company. Second, the ability to execute outside traditional bankruptcy frameworks can preserve enormous value for all stakeholders. Third, international capital, when properly structured, can transform not just balance sheets but credibility and governance. Fourth, management with skin in the game—even if highly leveraged through pledges—often outperforms professional managers in crisis situations.

Looking forward, RattanIndia Power stands at another inflection point. The successful turnaround has been achieved, but the next phase of value creation remains undefined. Will it become a cash cow funding new economy ventures? Will Nashik find resolution, unlocking billions in trapped value? Will carbon pricing and renewable acceleration strand even performing thermal assets? These questions don't have clear answers, which is precisely why the opportunity—or risk—exists.

The RattanIndia story ultimately validates an old infrastructure investing truth: in sectors with high capital intensity and long cycles, survivors inherit the earth. Those who entered Indian power during the 2007-2010 boom mostly failed or fled. Those who survived the 2015-2019 crisis, like RattanIndia, now operate in a market with massive barriers to new thermal capacity, growing power demand, and the operational expertise that only comes from navigating crisis. Whether this positions them for another decade of value creation or merely delays an inevitable transition to stranded assets remains the central question.

In the end, RattanIndia Power's journey from Indiabulls spinoff to stressed asset to turnaround story isn't just about one company's resilience. It's about how value can be created, destroyed, and recreated in infrastructure sectors undergoing fundamental transformation. It's about the importance of patient capital, operational excellence, and strategic flexibility in navigating multi-decade investment cycles. Most importantly, it's about recognizing that in infrastructure, the greatest opportunities often emerge from the deepest crises—for those with the vision to see them and the tenacity to capture them.

The art of the infrastructure turnaround, as RattanIndia demonstrates, isn't just about fixing what's broken. It's about reimagining what's possible when conventional wisdom says the game is over. For Rajiv Rattan and RattanIndia Power, the game has just begun.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube