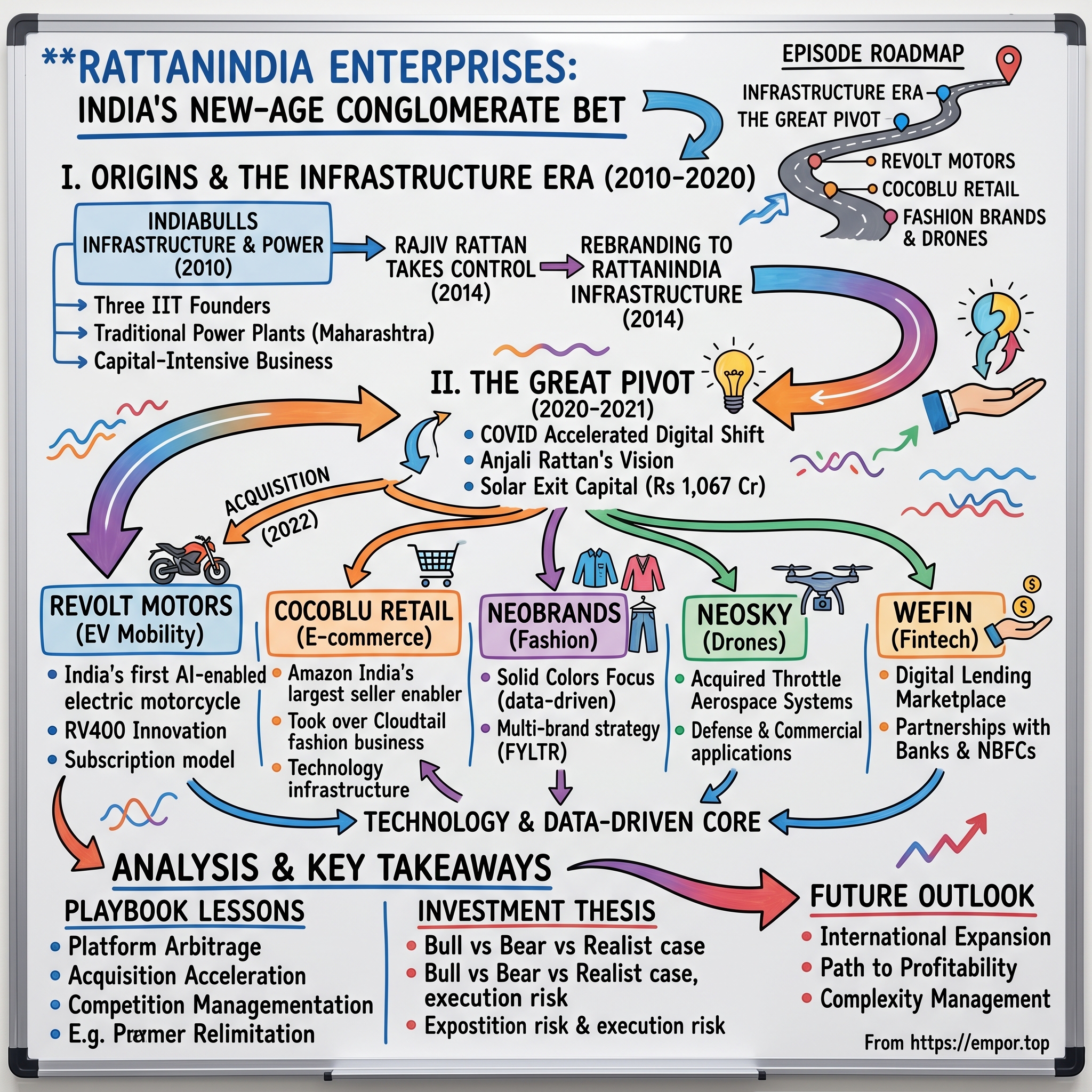

RattanIndia Enterprises: India's New-Age Conglomerate Bet

I. Introduction & Episode Roadmap

Picture this: It's March 2021, and while the world is still reeling from COVID-19, a Delhi-based infrastructure company quietly changes its name. RattanIndia Infrastructure becomes RattanIndia Enterprises. No press fanfare. No grand announcements. Just a subtle shift in paperwork that would signal one of the most audacious pivots in Indian corporate history.

The transformation is staggering in scope. A company that once traded power and built infrastructure projects is now manufacturing electric motorcycles, selling fashion brands online, flying drones, and running one of India's largest e-commerce operations. Market cap today? ₹6,997 crore. Revenue? ₹6,866 crore. But the real story isn't in these numbers—it's in the sheer ambition of trying to build India's answer to a modern tech conglomerate while the paint is still drying on the business model.

Here's the fundamental question we're exploring: How does a traditional infrastructure company transform itself into a new-age technology conglomerate? And more importantly, can this model actually work in India's hyper-competitive digital economy?

The answer matters because RattanIndia isn't just betting on one trend. They're placing simultaneous bets on electric vehicles through Revolt Motors, e-commerce through Cocoblu, fashion through Neobrands, drones through Neosky, and fintech through WeFin. It's either brilliant portfolio theory or dangerous overextension—and we're going to figure out which.

What makes this story particularly fascinating is the timing. While Reliance was building Jio and transforming into a tech giant from the top down, RattanIndia was attempting something arguably more difficult: acquiring and building multiple tech businesses from scratch, all while managing the complexity of a conglomerate structure that most modern companies actively avoid.

This isn't just another Indian business transformation story. It's a case study in how emerging market companies are rewriting the playbook for conglomerate building in the digital age. The old model—think Tata or Birla groups—was built on licenses, land, and relationships. The new model that RattanIndia is pioneering? It's built on technology, consumer brands, and the belief that India's digital transformation creates room for multiple winners.

Over the next several hours, we'll dissect every major decision, analyze each business vertical, and ultimately answer whether RattanIndia Enterprises represents the future of Indian conglomerates or a cautionary tale about the perils of trying to be everything to everyone. The journey takes us from power plants to electric bikes, from wholesale trading to direct-to-consumer fashion, from traditional infrastructure to cutting-edge drone technology.

Buckle up. This is the story of how one company decided to bet everything on India's digital future—and what that bet actually looks like when you open the hood.

II. Origins & The Infrastructure Era (2010-2020)

The Mumbai monsoon of 2010 was particularly brutal. Infrastructure projects across Maharashtra were drowning in debt, coal linkages were becoming political footballs, and the power sector was entering what would become India's darkest period of stranded assets. It was precisely this moment when a company called Indiabulls Infrastructure & Power was born—incorporated on November 9, 2010, in the heart of New Delhi.

But the real story begins earlier, in the glass towers of Gurgaon where three IIT Delhi graduates had built Indiabulls into one of India's most aggressive financial conglomerates. Sameer Gehlaut, Rajiv Rattan, and Saurabh Mittal had co-founded Indiabulls in 2000 as India's first online stock trading brokerage, riding the dot-com wave before most Indians even knew what online trading meant. By 2010, they'd built an empire spanning housing finance, real estate, and securities. The group had become a large business conglomerate with the second-largest mortgage lender in India, the largest stock brokerage, and a combined net worth of more than $5 billion.

The power business wasn't supposed to be complicated. In November 2011, the Power Business Undertaking of Indiabulls Real Estate got demerged into the new entity, bringing with it ambitious plans for thermal power generation. The vision was straightforward: build large-scale power plants in Maharashtra, secure coal linkages, sign power purchase agreements with state utilities, and ride India's infrastructure boom. Classic infrastructure playbook, circa 2010.

Rajiv Rattan, the quieter of the three founders, took charge of this infrastructure venture. An alumnus of IIT Delhi who started his professional career with Schlumberger, one of the largest oilfield services companies in the world, Rattan brought an engineer's precision to what was essentially a bet on India's power deficit. The company quickly moved to establish two massive thermal power plants—one in Amravati with 1,350 MW capacity and another in Nashik with 1,350 MW capacity. Combined, these 2,700 MW projects represented one of the largest private sector power generation capacities in Maharashtra.

The Amravati plant, in particular, became the crown jewel. Commissioned in 2015, it was designed to supply electricity to Maharashtra's perpetually power-starved grid. The company secured coal from South Coalfields Limited and Mahanadi Coalfields Limited, navigating the byzantine world of Coal India allocations that would later become the sector's Achilles heel.

But 2014 marked a seismic shift—not in the power sector, but in the promoter structure itself. RattanIndia was the outcome of the split of Indiabulls where the energy component was renamed RattanIndia in 2014. The three musketeers who had built Indiabulls decided to go their separate ways. In September 2014, Rajiv Rattan took control of the group's two power companies after buying out Saurabh Mittal's stake, a move that came within two months of the three original promoters deciding to recast their holdings.

The timing of Rattan's takeover was either brilliant or foolhardy, depending on your perspective. It coincided with Indiabulls Power being allowed a Rs 1.55 per unit compensatory tariff for using imported coal, granted by the Maharashtra Electricity Regulatory Commission. This regulatory win gave Rattan confidence that the worst was behind them. Speaking to media, Rattan said problems in the power business had reached "rock bottom" and that "the worst seems to be over and things are looking up for the sector".

The rebranding from Indiabulls Infrastructure to RattanIndia Infrastructure in November 2014 wasn't just cosmetic. It signaled a complete separation from the Indiabulls brand and the beginning of Rattan's independent journey. Under the separation agreement, the power business would stop using the Indiabulls brand name after December.

What followed were six grueling years of managing a capital-intensive infrastructure business in one of India's most challenging sectors. The Nashik plant faced its own demons—reported stranded in 2020 due to no long-term purchase agreements and conflicts on land acquisition. The promised infrastructure boom turned into a bust. Coal linkages became political nightmares. State electricity boards delayed payments. Environmental clearances became moving targets.

Yet Rattan persisted, even expanding into renewable energy. His wife Anjali founded RattanIndia Solar in 2014, scaling it to a 306 MW portfolio within three years, with projects spread across Maharashtra, Karnataka, Madhya Pradesh, and other states. The solar business attracted serious institutional money, counting General Electric Energy Financial Services as an investor.

But by 2020, the writing was on the wall. The traditional infrastructure model was dying. In September 2020, the company sold its solar business to GIP for Rs 1,067 crore and exited completely. This wasn't retreat—it was strategic repositioning. The capital from the solar exit would fund something far more ambitious: a complete transformation from infrastructure to technology.

The decade from 2010 to 2020 taught Rattan invaluable lessons. He'd learned how to manage massive capital deployments, navigate regulatory mazes, handle institutional investors, and most importantly, when to pivot. The infrastructure era hadn't been a failure—the Amravati plant continued generating power and cash. But it was clear that the next decade belonged to a different kind of infrastructure: digital platforms, electric vehicles, and e-commerce logistics.

As 2020 ended and COVID-19 accelerated India's digital transformation, RattanIndia Infrastructure was sitting on a war chest, operational power assets generating steady cash, and most importantly, a founder who had spent a decade learning how to build at scale. The stage was set for one of Indian corporate history's most audacious pivots.

III. The Great Pivot: From Infrastructure to Tech (2020-2021)

The pandemic changed everything. While the world locked down in March 2020, Rajiv and Anjali Rattan saw opportunity where others saw chaos. India's digital adoption, which might have taken a decade, compressed into months. E-commerce penetration jumped from 3% to 8%. Electric vehicle conversations shifted from "someday" to "now." Drone deliveries went from science fiction to government priority. The Rattans realized their infrastructure company was perfectly positioned to become something entirely different—a technology conglomerate for the new India.

The transformation began quietly in late 2020, accelerated through early 2021, and culminated in March 2021 with the official name change from RattanIndia Infrastructure Limited to RattanIndia Enterprises Limited. This wasn't just rebranding—it was a complete reimagining of what the company could be.

In 2020, RattanIndia Enterprises made a strategic shift towards electric mobility and renewable energy. This decision was in line with India's push for sustainable development and reduction of carbon emissions. The timing was deliberate. The government had just announced massive incentives for electric vehicles, drone manufacturing was being liberalized, and e-commerce was experiencing unprecedented growth.

The intellectual foundation for this pivot came from Anjali Rattan, who emerged as the driving force behind the transformation. Mrs. Anjali Rattan Nashier studied Electrical Engineering at Kurukshetra University. In addition to that, she is a law graduate. She is an alumnus of Judge Business School, University of Cambridge. She has also studied HR strategy at London Business School. She is currently pursuing OPM (Owner's President's Management Programme) at Harvard Business School, Boston. Her experience building and selling RattanIndia Solar for over Rs 1,000 crore had taught her how to identify, scale, and exit new businesses—exactly the playbook needed for this transformation.

The vision was audacious yet clear. As Anjali articulated it: "Single biggest quality of an entrepreneur is optimism. I am eternally optimistic on India. Favorable demographics, our talented people and a stable democratic system make up for a very strong foundation for our economic progress. I do not have an iota of doubt that our 1.35 billion aspiring Indians will propel the growth of the country towards top 3 economies in the world. Digital ecosystems and technology will make India the beacon of economic progress in the world."

The strategic framework they developed was elegant in its simplicity. Digital ecosystems are driving the next generation change in the country and technology will play a vital role in solving India scale problems. RattanIndia Enterprises Limited will be at the forefront of this change with businesses with large addressable markets and potential to solve fundamental problems of the country.

But vision without execution is hallucination. The Rattans needed world-class talent to execute this transformation. They brought in Arun Duggal as Chairman—a heavyweight with credentials that read like a who's who of global finance. Mr. Arun Duggal is Chairman of ICRA (A Subsidiary of Moody's USA), He is on the Boards of Directors of ITC Limited and Jubilant Pharma Limited, Singapore. He is an experienced international Banker and has advised companies and financial institutions on Financial Strategy, M & A and Capital Raising. Mr. Duggal had a 26 years' career with Bank of America, mostly in the U.S., Hong Kong and Japan. His last assignment was as Chief Executive of Bank of America in India. Mr. Duggal has vast international experience and has been Chairman and on the Board of Directors of the companies in Korea, Australia, Singapore, London and South Africa. A Mechanical Engineer from the prestigious Indian Institute of Technology, Delhi (recipient of Distinguished Alumni Service Award) Mr. Duggal holds an MBA from the Indian Institute of Management, Ahmedabad (recipient of Distinguished Alumnus Award).

The first major business to launch was e-commerce. Cocoblu Retail Limited, a subsidiary of the company, is engaged in the E-commerce business since 2021. This wasn't about competing with Amazon or Flipkart directly. Instead, Cocoblu positioned itself as an enabler—helping brands scale on these platforms. The logic was brilliant: why fight the platforms when you can become their largest seller?

The drone business followed a different path—acquisition rather than organic build. In August, RattanIndia announced a strategic investment in Matternet, a US-based urban drone logistics platform. The venture has operations across many countries worldwide, and was among the first companies to do drone delivery for COVID-19 vaccines in the US.

Anjali explained the rationale with characteristic clarity: "So rather than spending another eight years in India, it's better to partner with a company and get all the technology and software here quickly." The timing was perfect—The Ministry of Civil Aviation (MoCA) recently announced liberalised and updated the Drone Rules 2021, which has made it easier for companies to carry out drone operations. The government also recently announced a Production Linked Incentive (PLI) Scheme for the drone industry to enhance India's manufacturing capabilities.

The financial engineering behind this transformation was equally sophisticated. The solar exit had provided capital, but more importantly, it had provided credibility. Here was a management team that could build and exit businesses successfully. The power generation business, while no longer the focus, continued generating steady cash flow—about Rs 3,000-4,000 crore in annual revenue—providing the foundation for these new ventures.

By mid-2021, the transformation was in full swing. The company had identified five core verticals: electric mobility, e-commerce, fashion brands, fintech, and drones. Each vertical had its own leadership, its own P&L, but all were united under the RattanIndia Enterprises umbrella. The holding company structure allowed for different risk profiles, different capital structures, and crucially, different exit strategies for each business.

The market initially didn't know what to make of this transformation. Was this diversification or lack of focus? Was it visionary or reckless? The stock price reflected this confusion, trading sideways through most of 2021. But the Rattans weren't building for the stock market—they were building for the next decade of India's growth.

What made this pivot particularly remarkable was its timing. While established conglomerates like Reliance were leveraging existing assets and relationships to move into technology, RattanIndia was attempting something far more difficult—building multiple technology businesses from a standing start. No existing customer base to leverage. No technology infrastructure to build upon. Just capital, vision, and the belief that India's digital transformation would create room for multiple winners.

The stage was set. The team was in place. The capital was allocated. Now came the hard part—execution. And the first major test would come through the acquisition of a struggling electric motorcycle company founded by one of India's most controversial entrepreneurs. The Revolt Motors story would either validate the entire transformation strategy or expose it as expensive ambition without substance.

IV. The Revolt Motors Acquisition: Betting on Electric Mobility

Rahul Sharma's journey reads like a Bollywood script—complete with meteoric rise, crushing fall, and an attempted comeback that would become someone else's triumph. In 2017, at the peak of Micromax's decline, when Chinese smartphones had decimated his mobile empire, Sharma did what entrepreneurs do when cornered: he pivoted to something completely different. He founded Revolt Intellicorp, marking his entry into the electric vehicle sector with India's first AI-enabled electric motorcycle.

The parallels to Micromax were uncanny. Armed with a degree in Mechanical Engineering and a Bachelor's in Commerce, he ventured into the entrepreneurial world, driven by a passion for technology and innovation. In 2000, Rahul Sharma, with Rajesh Aggarwal, Vikas Jain, and Sumeet Arora, launched Micromax Informatics. Initially targeting low-end tech products, the company gained a significant boost after partnering with Nokia in 2001. Inspired by a 2007 visit to rural Bihar, Sharma developed phones with long-lasting batteries to tackle the problem of unreliable power supply in remote areas. Micromax quickly became a household name in India, known for its innovative features like long battery life and dual SIM capabilities.

But by 2018, the company reported a 26% decline in revenues and a 76% drop in profits, highlighting the tough market conditions it faced. The mobile phone warrior had been bloodied. Yet Sharma saw opportunity where others saw saturation. In the last 20 years, there has been no major disruption in the two-wheeler space. The new-age consumer hates making compromises, and this became our first point of consideration while conceptualising our products. After going through the available options in the market, we decided to create a motorcycle using an alternate source of energy, without compromising on form factor or performance.

Rahul Sharma has reportedly invested Rs. 400-500 crore into the company, which is headquartered in Gurgaon. The company also has a production facility in Manesar which has a capacity of 1,20,000 bikes commissioned for the first phase. This wasn't a half-hearted attempt—Sharma was betting everything on electric mobility.

The RV400, unveiled in June 2019, was a masterclass in understanding Indian consumers. The bike didn't look like a science experiment; it looked like a proper motorcycle. Powering the Revolt RV400 is a 3kW motor, which produces 5kW of peak power. The motor is mated to a 3.7kWh battery that offers a maximum range of 150km in Eco mode. The bike comes equipped with three modes – Eco, Normal and Sport – and the range varies as per the riding modes. The Revolt RV400's top speed is 85kmph in the Sports mode.

But the real innovation wasn't in the specs—it was in solving Indian problems. It also gets an app that can be used to start up the motorcycle, set up a geofence, and also get notified if the battery charge is low. Apart from that, the Revolt is offering the RV400 with an onboard charger and a portable battery charger and will soon set up battery swapping stations, to be known as Switch Stations. The swappable battery system addressed range anxiety head-on. Can't find a charging station? Just swap your battery. Living in an apartment without charging infrastructure? Take the 18kg battery home and charge it there.

The artificial engine sounds—generated through speakers—might seem gimmicky, but they solved a real psychological barrier. Indian riders associated silence with powerlessness. Revolt has also equipped the RV400 with speakers to produce faux exhaust notes. Sharma understood that adoption wasn't just about technology; it was about emotion.

By 2022, Revolt had gained traction but was burning cash. The company had expanded to retail stores in various cities including Jaipur, Surat, Bengaluru, Delhi, Pune, Ahmedabad, Kolkata, Noida, Hyderabad and Chennai, among others. Revolt further claims that in the last year, it has expanded its presence across India by opening 29 dealership stores in the country. It also asserted that its electric bikes have covered over 100 Mn Kms on Indian roads to date.

Enter RattanIndia. The timing was perfect—Revolt needed capital and distribution muscle, while RattanIndia needed a ready-made electric vehicle business. RattanIndia had earlier acquired 33.84% shares in Revolt along with an option of increasing its shareholdings in the startup. This wasn't a sudden decision; it was calculated courtship.

In October 2022, RattanIndia announced the full acquisition. "Revolt is currently by far the best EV bike in the world. With this acquisition of 100% shareholding in Revolt Motors, we are doubling down on our belief that EV revolution in the country is coming faster than we anticipate. I do not have any doubt that what is good for the environment and the country makes for a great business," said Anjali Rattan, business chairperson of RattanIndia Enterprises.

For Rahul Sharma, it was bittersweet. "It is a proud moment for me as we pass on the baton for the next phase of Revolt's growth trajectory. I am very proud of what we have created with Revolt. Revolters love their Revolts and there is a huge demand for our bikes. I am sure the Revolt revolution has just begun," said Rahul Sharma, managing director and founder of Revolt.

The acquisition brought immediate changes. RattanIndia's capital infusion allowed Revolt to expand aggressively. Revolt has made significant strides in expanding its dealership network, demonstrating aggressive growth over the past year. The number of dealer stores increased to 115, marking a fourfold increase year-over-year in 2024. The company also launched new variants, including the RV400 BRZ with its 150km operational range, available in five colors.

The product itself had evolved significantly. The latest RV400 came with a 3.24 Kwh battery, offering a range of 150 km/charge. The ARAI claimed range of Revolt RV400 is 80-150 km/charge. The three riding modes—Eco, Normal, and Sport—allowed riders to optimize between performance and range, with the Sport mode delivering that crucial 85 kmph top speed that made highway riding viable.

But the masterstroke was the business model innovation. Rather than selling bikes outright, Revolt introduced subscription plans that made the economics irresistible. For less than the monthly fuel cost of a 125cc bike, customers could ride electric. The battery-as-a-service model meant lower upfront costs and eliminated battery degradation concerns—Revolt would handle replacements.

The manufacturing story was equally strategic. Revolt has worked with Chinese brand Super Soco TS to make the RV400, and will work closely with them for its "platform development." This wasn't about reinventing the wheel; it was about localizing proven technology for Indian conditions—the same playbook Sharma had used at Micromax.

By 2024, Revolt Motors had become the crown jewel of RattanIndia's transformation. The company claimed to be the market leader in electric motorcycles in India, with more than 100 dealership stores across 65 cities. The international expansion had begun too, with Sri Lanka as the first market and Nepal following soon after.

The numbers told the story of vindication. From a standing start in 2019 to market leadership in 2024, Revolt had proven that Indians were ready for electric motorcycles—if you gave them the right product at the right price with the right emotion. The RV400 wasn't just competing with electric vehicles; it was competing with 125cc petrol bikes and winning.

For RattanIndia, Revolt validated the entire transformation thesis. They'd taken a struggling startup, infused capital and operational expertise, and created a category leader. The playbook was proven. Now it was time to replicate it across e-commerce, fashion, and drones. The transformation was no longer theoretical—it was generating revenue, creating jobs, and most importantly, changing how Indians thought about mobility.

V. Cocoblu Retail: The E-commerce Play

The timing couldn't have been more perfect—or more audacious. In October 2021, just as Amazon was being forced to shut down Cloudtail, its largest seller in India due to regulatory pressure, a company nobody had heard of was quietly incorporating in Delhi. Cocoblu Retail Limited is a Public company incorporated on 21 October 2021. Within months, it would become one of the most controversial and successful players in Indian e-commerce.

The masterstroke came in January 2022. RattanIndia Enterprises, on 11 January 2022, operationalized its e-commerce foray by approving an investment of Rs 350 crore in its wholly-owned subsidiary Cocoblu Retail to build and undertake the business of online retail on e-commerce platforms. This wasn't just capital injection—it was a declaration of intent to dominate Indian e-commerce through a completely different playbook.

The strategy was brilliantly counterintuitive. While everyone else was trying to build their own e-commerce platforms to compete with Amazon and Flipkart, Cocoblu decided to become the biggest seller ON these platforms. Cocoblu will be partnering with several big and small brands in India to bring them onto leading online platforms in the country. Cocoblu is committed to scale up local micro, small and medium manufacturers and help them build their brands and reach their true potential through digital channels.

By February 2022, Cocoblu was operational. RattanIndia Enterprises Limited's 100% owned subsidiary, Cocoblu Retail Limited has started sales on Amazon India platform today and revenue generation has started in the company. The speed of execution was breathtaking—from incorporation to revenue generation in just four months.

But the real coup came in April 2022. Cocoblu Retail will take over the fashion, apparel and accessories business of Cloudtail who is the Amazon's largest seller in India. The reports claim Cloudtail has communicated that Cocoblu Retail will handle the fashion business from April. Suddenly, Cocoblu wasn't just another seller—it was inheriting the crown jewel of Amazon India's marketplace.

The technology infrastructure Cocoblu built was the secret weapon. Cocoblu Retail has invested heavily in technology and has developed cutting edge retail systems with deep integrations with existing ecommerce platforms in record time. This enables the company to utilize the full potential of online retail eco-system in the country. This wasn't about selling products; it was about building a technology layer that could manage thousands of SKUs, optimize pricing in real-time, and predict demand patterns across categories.

The market opportunity was massive. E-retail is a key driver of our economy with sales of Rs. 2.8 lac crore in FY-21. The sector is growing at an annualized rate of 25-30% and is estimated to reach sales of approximately Rs. 9 lac crore by FY 2026. India is home to second largest internet enabled population and third largest E-commerce consumer base in the country with e-commerce penetration of less than 5%, leaving tremendous headroom for growth in the sector.

The human capital story was equally impressive. Deep expertise comes from our passionate team of almost 200 e-com natives, who are adept with big data technology and well-versed with product category dynamics. The leadership team read like an all-star roster of Indian e-commerce—professionals with decades of experience from Amazon, Flipkart, and major FMCG companies.

The business model was elegant in its simplicity. Cocoblu Retail with its digital first approach is focused on online retail on E-commerce platforms in India. This provides a great opportunity to scale up its retail offerings in India without the complexities and capex of physical retail. No warehouses to build. No last-mile delivery to manage. Just pure technology and category expertise.

But success bred controversy. By 2023, small sellers on Amazon were in revolt (no pun intended). Forum discussions revealed the anxiety: "all apperal category sale is highjacked by Cocoblue" "After investigation i found that all brand is taken by COCOBLUE and all sale allocate to this Company.. i want to know is COCOBLUE is legal entity as per Indian Ecommerce Laws?"

The dominance was real. You are right Amazon gives 50% sale in apparel category to Cocoblu Retail. Seems Amazon is not charging commission from Cocoblu that's why they can sell at very low price. Some sellers speculated about special relationships: "They have partnership similar to Appario collaboration with Amazon in the electronics category. they have collaborations with senior management at Amazon and high investments."

The regulatory questions were valid but ultimately irrelevant. Cocoblu had structured itself perfectly—it wasn't owned by Amazon, it wasn't violating FDI norms, and it was operating as an independent seller. The fact that it had taken over Cloudtail's business and dominated certain categories was just good business, not illegal practice.

Anjali Rattan's vision for Cocoblu was clear from the start: "Cocoblu will be well-positioned to provide value to salient brand-owners and sellers in India's ever-expanding e-commerce landscape. Our investment of Rs 350 crore is intended to give fillip towards creation of an all-digital approach to selling lifestyle offerings via leading e-commerce platforms."

The infrastructure capabilities were staggering. A pan-India infrastructure harmonises all four ingredients flawlessly, across all 26 states. So whichever one of India's 19,000 pin codes your customer calls home, they can get speedy, delightful delivery every single time. This wasn't built—it was leveraged through partnerships with Amazon's fulfillment network. Cocoblu has tied up with ~136 Amazon Fulfillment Centers.

The category expansion was relentless. Starting with fashion and apparel from the Cloudtail acquisition, Cocoblu quickly expanded into electronics, home goods, and FMCG. Each category brought new challenges but also new data, new relationships, and new economies of scale.

By 2024, Cocoblu had become exactly what RattanIndia envisioned—not an e-commerce company, but an e-commerce enabler. It wasn't competing with Amazon; it was Amazon's best partner. It wasn't fighting brands; it was making them successful online. The business model was so successful that competitors started copying it, but Cocoblu's first-mover advantage and technology moat proved difficult to overcome.

The financial performance validated the strategy. While specific revenue numbers for Cocoblu weren't disclosed separately, the growth in RattanIndia's overall e-commerce segment told the story. From zero revenue in 2021 to becoming a major contributor to the company's Rs 6,866 crore topline by 2024, Cocoblu had become the quiet giant of Indian e-commerce.

What made Cocoblu particularly brilliant was how it solved a real problem for both platforms and brands. Platforms needed large, reliable sellers who could handle volume and maintain service levels. Brands needed partners who understood e-commerce intricacies but didn't want to build capabilities themselves. Cocoblu sat perfectly in the middle, taking a margin but creating value for everyone.

The Cocoblu story proved that in the platform economy, you don't need to own the platform to win. Sometimes, being the biggest player on someone else's platform is an even better business. As RattanIndia looked to replicate this success in fashion and other verticals, the Cocoblu playbook would become the template—find a fragmented market, add technology and capital, and dominate through execution.

VI. The Fashion Brands & Other Ventures

The fashion story began in April 2023 with a simple observation: Indians love solid colors. RattanIndia Enterprises on Tuesday launched a wholly-owned subsidiary Neobrands, marking its entry into the fast-growing apparel fashion business. But this wasn't just another fashion label launch—it was the beginning of a multi-brand strategy designed to capture India's $100 billion apparel market through technology and data.

Neobrands Limited, wholly owned subsidiary of RattanIndia Enterprises Limited, is a house of brands across multiple fashion categories including everyday fashion, denims, athleisure and performance wear categories. The direct-to-consumer brands are aimed at capturing the fast-growing fashion and apparel market in India. The ambition was clear from day one—build multiple brands, each targeting specific consumer segments, all powered by shared backend infrastructure.

The first brand to launch was FYLTR in April 2023. FYLTR is offering casual clothing for men and women in over 200 styles and solid colours on e-commerce platform Amazon. The brand conducted research that revealed the increasing popularity of solid colors in India. This wasn't guesswork—it was data-driven product development based on Cocoblu's massive e-commerce sales data.

"We are committed to providing our customers with the latest fashion trends through FYLTR, and our colour stories are carefully crafted to reflect consumers' unique tastes and preferences," said Anjali Rattan, business chairperson, RattanIndia Enterprises Ltd. The product range includes a variety of apparel such as t-shirts, shirts, tops, polo t-shirts, shorts and khakis.

The technology story behind FYLTR was fascinating. Plus, its anti-odour feature keeps the wearer fresh & feeling confident all day long. These T-shirts also offer UV protection, safeguarding the skin from harmful UV rays. The Stretchies Khaki trousers are extremely soft to wear. With their breathable cotton fabric, these khakis are perfect for summers as they'll keep the wearer cool and comfortable even on the hottest days.

By November 2023, FYLTR was expanding into winter wear. Neobrands, a 100 per cent wholly-owned subsidiary of RattanIndia, is excited to introduce its casual fashion brand, FYLTR's lightweight winter collection which is now available online through its brand store on Amazon. From cozy sweatshirts, trendy hoodies to snug puffer jackets, FYLTR sets a new standard for comfort-infused style.

The market response was immediate. RattanIndia Enterprises share price: The stock soared 20 per cent to hit a 52-week high of Rs 77.65. Today's sharp jump in the share price came after the company's subsidiary, Neobrands, launched its casual fashion brand. Investors understood what many missed—this wasn't just about selling clothes; it was about building a fashion technology platform.

Meanwhile, the drone business was taking flight through an entirely different approach. RattanIndia Enterprises has forayed into the drone business in the country through its wholly-owned subsidiary NeoSky and expects the commercial rollout of products in the first quarter of 2023. The company has earmarked an initial investment of Rs 100 crore in NeoSky.

NeoSky India Ltd, a wholly owned subsidiary of RattanIndia Enterprises Ltd. is leading the way in drone industry in India with its 360° Drone-as-a-Product and Drone-as-a-Service portfolio. The strategy was comprehensive—don't just build drones, build an entire ecosystem including training, services, and software.

The acquisition of Throttle Aerospace Systems (TAS) in 2022 accelerated the drone ambitions. TAS, a subsidiary of NeoSky India is a market leader in enterprise, defence & delivery drones in India and currently counts marquee organisations as its clients. This wasn't organic growth—it was strategic acquisition of proven technology and customer relationships.

The regulatory wins validated the strategy. "Throttle Aerospace Systems (TAS) received Type-Certification for its drone product, DOPO, from the Directorate General of Civil Aviation (DGCA)," the company stated in an exchange filing. TAS designs, develops and manufactures drones in India as part of the 'Atmanirbhar Bharat' initiative. The parent company NeoSky has a DGCA license for a Drone Remote Pilot Training Organization (RPTO).

The drone applications were diverse and practical. NeoSky drones reduce the risks associated with mining activities by detecting hot spots in coal stockpiles and any potential risk of spontaneous combustion. We offer durable and lightweight construction drones that makes them perfect for last mile deliveries. NeoSky's Automated drones provide top-of-the-line security for oil & gas facilities, surveillance, and infrastructure inspection.

The defense angle was particularly promising. As a Ministry of Defence (MoD) licensed company (TAS), we understand the importance of this defence drones. We have state of the art drones for Surveillance, Logistics and Anti-Drones which are built to last across different terrains. The Defender is an indigenously built anti-drone platform to actively track rouge drones via vision-based techniques & neutralize rouge drones using net (non – lethal).

The fintech venture, WeFin (initially called BankSe), took yet another approach. RattanIndia Enterprises Ltd is leading the charge in Fintech through Wefin, a digital lending marketplace offering instant personal loans, two-wheeler loans, and credit cards to customers in partnership with leading banks and NBFCs in India. This wasn't about becoming a lender—it was about becoming the technology layer between lenders and borrowers.

Wefin is positioned as India's premier, all-digital, one-stop financial solutions provider bringing together lending institutions on a real-time platform to fulfil customer requirements instantly. It has tied up with 30 leading banks, NBFCs (Non-Banking Financial Companies) and FinTechs and has more than 250,000 registered customers on its portal.

The strategic investment in Matternet added international credibility. RattanIndia Enterprises Ltd. has made strategic investment in Matternet, US based market leader in urban drone logistics. Drones systems are set to positively impact the core sectors of the economy and will prove to be extremely transformative by providing cost effective business solutions for developing countries like India.

The capital allocation told the story of priorities. "We have committed Rs 3,000 crore in RattanIndia Enterprises in total for investment in four businesses," Nashier added. Fashion got attention but drones got serious money. E-commerce got the most capital but fintech had the highest margins. Each vertical had its own logic, its own timeline, its own success metrics.

What united all these ventures was the underlying technology philosophy. Whether it was FYLTR using e-commerce data to design products, NeoSky using AI for autonomous flight, or WeFin using algorithms for instant credit decisions, technology wasn't an add-on—it was the core competency.

The market opportunity across these verticals was staggering. Indian drone industry is expected to grow from $360 mn in 2020 to $10 bn in 2025 and $37 bn by 2030. The fashion industry in India is witnessing remarkable growth, with an increasing demand for trendy and premium quality apparel. Fintech India is a $612 bn retail credit market.

By 2024, these "other ventures" were no longer other—they were becoming significant contributors to RattanIndia's identity. The company that started as a power generator had successfully built positions in five completely different industries. Each venture validated the transformation thesis: India's digital economy had room for new players who could combine capital, technology, and execution.

The portfolio approach also provided strategic flexibility. When e-commerce margins compressed, drones could compensate. When fashion inventory built up, fintech's asset-light model balanced the books. When regulatory challenges hit fintech, fashion provided stability. This wasn't diversification for its own sake—it was intelligent risk management wrapped in growth ambition.

VII. Financial Performance & Market Position

The numbers tell a story of aggressive growth, strategic losses, and a market that can't quite decide if RattanIndia is a visionary play or an expensive experiment. The company reported a consolidated net loss of Rs 170.43 crore in Q3 FY25 as against net profit of Rs 187.35 crore in Q3 FY24. Revenue from operations rose 2.2% year-on-year to Rs 1,921.49 crore in Q3 December 2024.

In 2024, RattanIndia Enterprises's revenue was 68.66 billion, an increase of 22.40% compared to the previous year's 56.10 billion. Earnings were 844.35 million, a decrease of -80.19%. This dramatic earnings decline while revenue grew tells the classic story of a company in heavy investment mode—revenues are scaling but profitability is being sacrificed for growth.

The market valuation reflects this uncertainty. The 52-week high of Rattanindia Enterprises Ltd (RTNINDIA) is ₹92.10 and the 52-week low is ₹37.42. The P/E (price-to-earnings) ratio of Rattanindia Enterprises Ltd (RTNINDIA) is 84.34. The P/B (price-to-book) ratio is 8.43. These valuations—a P/E of 84 and P/B of 8.43—scream either "expensive" or "high growth expectations," depending on your perspective.

The quarterly performance trajectory reveals the volatility inherent in building multiple new businesses simultaneously. The company's consolidated net loss widened to Rs 355.89 crore in Q4 FY25 as compared with net loss of Rs 81.29 crore in Q4 FY24. Net sales jumped 16.2% YoY to Rs 1,504.56 crore in Q4 FY25. The pattern is consistent—revenue growth accompanied by widening losses.

Breaking down the revenue composition reveals the transformation in action. While specific segment-wise data isn't fully disclosed, the shift from infrastructure to new-age businesses is dramatic. Cocoblu Retail Limited, a subsidiary of the company, is engaged in the E-commerce business since 2021, and has quickly become a major revenue contributor. The electric vehicle business through Revolt Motors is generating meaningful revenue but at significant losses as it scales manufacturing and distribution.

The capital structure story is equally revealing. Promoter Holding: 74.8%—this high promoter stake provides stability but also concentration risk. The promoters' continued commitment, evidenced by the Rs 350 crore investment in Cocoblu and Rs 100 crore in NeoSky, signals confidence but also raises questions about capital allocation.

Comparative analysis with listed peers is challenging because RattanIndia's unique conglomerate structure has few direct comparables. Unlike Reliance, which transformed from petrochemicals to retail and telecom using massive cash flows from its core business, RattanIndia is attempting transformation while its legacy power business provides limited cash generation. Unlike pure-play EV companies like Ola Electric, RattanIndia can't be valued solely on EV metrics.

The working capital dynamics have shifted dramatically with the business transformation. Working capital days have increased from 2.59 days to 68.3 days, reflecting the shift from infrastructure to consumer-facing businesses that require inventory and receivables management. This isn't necessarily negative—it's the natural consequence of moving from B2B power generation to B2C retail and manufacturing.

Debt management has been a bright spot. Company has reduced debt, which is remarkable given the capital-intensive nature of the new ventures. This suggests careful financial engineering, possibly using equity capital for new ventures while paying down legacy debt from cash flows.

The return metrics paint a sobering picture. Company has a low return on equity of -1.22% over last 3 years. For a company trading at 8.4 times book value, negative ROE is concerning. However, this needs context—the company is essentially in startup mode across multiple businesses, where negative returns are expected before scale is achieved.

Market sentiment has been volatile but generally positive about the long-term story. Mkt Cap: 6,997 Crore (down -36.1% in 1 year). The 36% decline over one year suggests market skepticism about near-term profitability, but the absolute market cap of nearly Rs 7,000 crore indicates belief in the transformation thesis.

The dividend policy—or lack thereof—is telling. Though the company is reporting repeated profits, it is not paying out dividend. This is actually from an earlier period when the company had profits, but the message is clear: cash is being retained for growth investment, not returned to shareholders.

Segment-wise performance reveals the challenge of multi-business execution. The e-commerce business (Cocoblu) is likely the largest revenue contributor but operates at thin margins typical of the sector. The EV business (Revolt) is scaling but burning cash on manufacturing and distribution expansion. The fashion business (Neobrands) is too nascent to contribute meaningfully. The drone and fintech businesses are still in investment phase.

The cash flow situation is critical to understand. While the company reports losses, the actual cash burn might be different due to non-cash charges, working capital movements, and inter-segment transfers. The ability to fund multiple cash-burning businesses simultaneously while servicing legacy debt requires sophisticated treasury management.

International comparison provides perspective. In the US, Amazon took nearly 20 years to become consistently profitable while building multiple businesses. In China, companies like Xiaomi successfully expanded from phones to dozens of categories while remaining unprofitable for years. RattanIndia is attempting a similar playbook but in a much shorter timeframe and with less capital.

The valuation debate centers on whether to value RattanIndia as a sum-of-parts (where each business is valued separately) or as an integrated conglomerate. Sum-of-parts might yield: Revolt Motors at 2-3x revenues (EV comparable), Cocoblu at 0.5-1x revenues (e-commerce comparable), Neobrands at 3-4x revenues (D2C fashion comparable), NeoSky at 5-10x revenues (deep tech comparable), and the power business at book value. This could justify valuations significantly higher than current levels, but execution risk remains paramount.

The key financial metrics to watch going forward are: revenue growth rate (needs to stay above 20% to justify valuations), gross margin expansion (critical for path to profitability), cash burn rate (sustainability of current investment levels), and segment-wise EBITDA progression (which businesses will turn profitable first).

The path to profitability likely requires one of the new businesses to achieve significant scale and positive unit economics within the next 12-18 months. Cocoblu, with its asset-light model and established operations, is the most likely candidate. Revolt needs to achieve 50,000+ unit annual sales to reach EBITDA breakeven. The fashion and drone businesses are likely 2-3 years from meaningful contribution.

The financial performance ultimately reflects a company in transition—no longer a boring infrastructure player, not yet a profitable technology conglomerate. The numbers show aggressive investment, rapid revenue scaling, and a race against time to achieve profitability before capital markets lose patience. It's a high-wire act that could result in either spectacular success or expensive failure.

VIII. India's Digital & EV Transformation Context

India in 2024 isn't just another emerging market—it's ground zero for the most ambitious economic transformation in human history. Electric vehicle sales in India have reached a historic milestone this year, crossing the 2 million mark for the first time. In 2023, total EV sales were ~1.6 million units; Excitingly, in 2024 that figure surged to over 2 million units, marking a growth of 24%, reflecting an increase in consumer demand. Consequently, the penetration of EVs in India's overall vehicle market increased to approximately 8%, up from 6.8% the previous year.

But these numbers only tell part of the story. Currently, India's EV market is relatively small, accounting for about 2.5% of all cars sold in 2024, with high prices and a limited charging network deterring potential buyers. However, we anticipate rapid expansion driven by more affordable EVs, an extensive charging infrastructure, and a shrinking price gap between traditional vehicles and EVs. The disconnect between overall EV adoption (8%) and car-specific adoption (2.5%) reveals the real story—India's EV revolution isn't happening in cars; it's happening on two wheels.

The two-wheeler segment dominates India's electric vehicle market, commanding approximately 92% market share in 2024. This dominance is driven by increasing consumer adoption of electric scooters and motorcycles. The segment's leadership can be attributed to factors such as affordability, convenience in navigating congested urban areas, and lower operating costs compared to conventional vehicles.

This two-wheeler dominance makes perfect sense when you understand India. This isn't California where Tesla defines the EV narrative. This is a country where 75% of households own a two-wheeler but only 8% own a car. The median Indian household income is around $3,000 per year. An electric scooter at $1,000 is achievable; a $25,000 electric car is fantasy. RattanIndia understood this, which is why Revolt Motors focused on motorcycles, not cars.

The government's ambitions are breathtaking in scope. India has established an objective to elevate the proportion of Electric Vehicle (EV) sales to 30% in private cars, 70% in commercial vehicles, 40% in buses, and 80% in two-wheelers and three-wheelers by the year 2030. This equates to an ambitious objective of 80 million EVs on Indian roads by 2030. These aren't incremental targets—they're revolutionary.

The infrastructure challenge is equally massive. A recent Confederation of Indian Industry (CII) report emphasized the necessity of establishing at least 1.32 million charging stations in India by 2030 to facilitate the rapid growth of electric vehicles, requiring over 4,00,000 installations annually. In FY25, India had 26,367 public EV charging stations, according to the Bureau of Energy Efficiency. That's a 50x increase needed in five years.

India's electric vehicle (EV) performance in 2024 was spearheaded by a handful of states, with Uttar Pradesh leading EV sales, contributing 19% of the national total, followed by Maharashtra (12%) and Karnataka (9%). These three states accounted for 40% of all EV sales in the country. On the infrastructure front, Karnataka led with the largest public charging network (5,765 stations), accounting for 23% of the national total. Maharashtra (3,728) and Uttar Pradesh (1,989) followed, reflecting strong alignment between sales and infrastructure growth.

The competitive landscape is transforming rapidly. Tata Motors maintained its dominance in the e-car segment with a market share of ~62%,followed by MG Motor India at 22%. Despite its strong position, Tata Motors had a ~7% YoY fall in sales. But the real action is in two-wheelers where dozens of startups are competing with established players, creating a Cambrian explosion of innovation.

Policy support has been critical but inconsistent. The second iteration of India's EV demand promotion policy, the Faster Adoption and Manufacturing of Electric Vehicles in India II (FAME II) concluded in March 2024, after being in force for 5 years. According to the research by ICCT, 69% of the ₹11,500 crore earmarked under the scheme was utilized by the end. The launch of the ₹10,900 crore PM E-DRIVE scheme in October 2024 further bolstered India's EV transition.

The e-commerce transformation provides equally important context for RattanIndia's strategy. India's 750 million internet users represent the world's second-largest online population, but e-commerce penetration remains below 5%. This isn't saturation—it's opportunity. Every percentage point of penetration increase represents $15 billion in market size.

The quick commerce revolution has been even more dramatic. Companies like Blinkit, Swiggy Instamart, and Zepto are delivering groceries in 10 minutes, fundamentally changing consumer expectations. This creates opportunities for players like Cocoblu who can leverage these platforms for distribution without building their own last-mile infrastructure.

Digital payments have removed a major friction point. UPI (Unified Payments Interface) processed 131 billion transactions in 2024, more than the combined total of all other countries' real-time payment systems. When a roadside vendor accepts digital payments, e-commerce becomes truly democratized.

The demographic dividend is real but time-bound. India has 600 million people under age 25—digital natives who think shopping without an app is weird. But this demographic window closes by 2040 when India starts aging. Companies have 15 years to capture this generation's lifetime value.

The India electric vehicle market size was valued at USD 8.49 billion in 2024 and is projected to grow at a CAGR of 40.7% from 2025 to 2030. At this growth rate, the market will be worth $50 billion by 2030. But this likely understates the opportunity because it doesn't account for the ecosystem effects—charging infrastructure, battery swapping, financing, insurance, and services.

The China factor looms large over everything. In 2024, electric car sales in Brazil more than doubled, with over 85% of new electric cars coming from China. A key factor behind this impressive growth was electric cars being exempt from import duties of 35%, though this exemption started to be gradually removed in 2024 and is set to end by the middle of 2026. India is watching Brazil's experience closely—how to benefit from Chinese technology while protecting domestic industry.

Another notable trend from 2024 was the numerous manufacturing announcements from Chinese OEMs in countries such as Brazil, Thailand, Indonesia and Malaysia, where temporary exemptions from import tariffs for electric cars are coming to an end. Chinese companies are increasingly looking to manufacture in India rather than export to India—a trend that benefits players like Revolt who have local manufacturing but use Chinese technology partnerships.

The broader mobility transformation goes beyond just vehicles. Shared mobility, autonomous vehicles, and mobility-as-a-service are all emerging simultaneously. An Indian consumer might use Ola for rides, Bounce for scooter rental, and Revolt for ownership—creating a complex, multi-modal transportation ecosystem that didn't exist five years ago.

Climate commitments add urgency. India's transport sector accounts for 14% of national energy-related CO₂ emissions. The record growth in 2024 strengthens India's pathway to meeting its Paris Agreement goals and net-zero commitments by 2070. But unlike developed markets where climate action is primarily about reducing consumption, in India it's about enabling sustainable growth for a population that's still increasing consumption.

The investment landscape is frothy but selective. The automobile sector received a cumulative equity FDI inflow of about Rs. 2,48,682.50 crore (US$ 29.07 billion) between April 2000–March 2025. But most of this is going to established players or proven models. Companies like RattanIndia that are building multiple bets simultaneously are rare.

What makes India's transformation unique is its compressed timeline. The US took 100 years to go from horses to cars to EVs. China took 40 years. India is attempting the same journey in 20 years, while simultaneously building the digital infrastructure, financial systems, and consumer behaviors to support it.

For RattanIndia, this context is everything. They're not just building businesses; they're surfing multiple tsunamis simultaneously—electrification, digitalization, and democratization. Each of their ventures—Revolt, Cocoblu, Neobrands, NeoSky, WeFin—is positioned at the intersection of these megatrends.

The risk is that these trends could reverse. EV adoption could stall if battery costs don't decline. E-commerce growth could slow if logistics costs don't improve. Digital payments could face regulatory challenges. But the opposite is equally possible—these trends could accelerate beyond anyone's imagination.

India's transformation is best understood not as a single story but as thousands of experiments happening simultaneously. Some will fail spectacularly. Others will create trillion-dollar outcomes. RattanIndia has placed chips on multiple tables, understanding that in a transformation this profound, diversification isn't just about risk management—it's about maximizing the probability of catching a rocket ship.

The next five years will determine whether India becomes the world's third-largest economy or remains stuck in the middle-income trap. Whether EVs become mainstream or remain niche. Whether e-commerce penetration reaches 15% or stalls at 7%. For companies like RattanIndia, these aren't abstract questions—they're existential ones. The transformation context isn't background; it's the main event.

IX. Playbook: Strategy & Execution Lessons

The RattanIndia playbook reads like a masterclass in contrarian thinking. While everyone else was building focused, pure-play businesses, they went full conglomerate. While others raised venture capital, they used internal capital. While competitors built brands, they bought them. Every decision seems to violate conventional wisdom, yet there's method to this madness.

Lesson 1: The Platform Arbitrage Play

The genius of Cocoblu wasn't in competing with Amazon—it was in becoming Amazon's largest partner in categories Amazon couldn't or wouldn't dominate directly. This is platform arbitrage at its finest. You don't need to own the platform if you can own the relationship between the platform and its suppliers. Cocoblu sits in the middle, taking margin from both sides while adding genuine value through technology, working capital, and scale.

The same logic applies to WeFin. Instead of becoming a lender (capital intensive, regulated, risky), they became the technology layer between lenders and borrowers. They own the customer acquisition and credit decisioning technology while banks provide the capital. It's a beautiful model—asset-light for RattanIndia but asset-heavy for partners who need the distribution.

Lesson 2: The Acquisition Acceleration Model

Revolt Motors validates a critical insight: in fast-moving markets, buying time is more valuable than saving money. Rahul Sharma spent five years and Rs 400-500 crore building Revolt. RattanIndia acquired it at a valuation that wasn't disclosed but was likely reasonable given Revolt's cash burn. They instantly got technology, manufacturing capability, brand recognition, and most importantly, five years of learning compressed into a single transaction.

This acquisition acceleration model extends beyond just buying companies. When Cocoblu took over Cloudtail's fashion business, they weren't just buying revenue—they were buying relationships, data, and operational knowledge that would have taken years to build organically. The question isn't "build vs buy" but "what's the value of time?"

Lesson 3: The Capital Allocation Paradox

RattanIndia's capital allocation seems schizophrenic until you understand the underlying logic. They put Rs 350 crore into Cocoblu (asset-light, working capital intensive), Rs 100 crore into NeoSky (R&D intensive, long payback), and an undisclosed amount into Revolt (manufacturing intensive, negative gross margins initially). This isn't random—it's portfolio theory applied to corporate strategy.

Each business has different risk profiles, capital requirements, and return timelines. Cocoblu could be profitable quickly but has limited moat. Revolt has strong moat but requires massive capital to scale. NeoSky is a long-term option on drone delivery. By funding all three simultaneously, they're creating a natural hedge. When one business struggles, others can compensate.

Lesson 4: The Talent Arbitrage Strategy

Look at the leadership hires—Arun Duggal (ex-Bank of America), advisory board members from IIT/IIM, and operational leaders from Amazon/Flipkart. This isn't just hiring senior people; it's importing institutional knowledge from world-class organizations into a company that was, until recently, running power plants.

The talent arbitrage goes deeper. By positioning itself as a "tech company" rather than an infrastructure company, RattanIndia can attract talent that would never join a traditional power company. The equity upside story, the multiple business units offering varied experiences, and the transformation narrative all make RattanIndia an attractive destination for ambitious professionals.

Lesson 5: The Regulatory Navigation Framework

Every RattanIndia business operates in a regulatory grey zone or rapidly evolving regulatory environment. E-commerce faces FDI restrictions and platform regulations. EVs depend on subsidies and safety standards. Drones require aviation clearances. Fintech needs lending licenses. This isn't coincidence—it's strategy.

Regulatory complexity creates moats. If it were easy to navigate these regulations, everyone would do it. RattanIndia's experience dealing with power sector regulations—arguably India's most complex regulatory environment—gives them an edge. They understand how to work with government, when to push boundaries, and when to wait for clarity.

Lesson 6: The Brand Architecture Decision

RattanIndia made a crucial decision: keep the corporate brand separate from product brands. Consumers buy Revolt motorcycles, not RattanIndia motorcycles. They shop FYLTR fashion, not RattanIndia fashion. This brand architecture provides flexibility—brands can be sold, partnerships can be formed, and failures can be contained without contaminating the parent brand.

This contrasts sharply with Reliance's approach where Jio became synonymous with Reliance, or Tata's approach where the Tata brand is on everything from salt to software. RattanIndia's approach is more similar to Alphabet or Procter & Gamble—the corporate entity is unknown to consumers but powerful in financial markets.

Lesson 7: The Ecosystem Play

Each RattanIndia business strengthens others in non-obvious ways. Cocoblu's e-commerce data informs Neobrands' product development. Revolt's customer base is a natural target for WeFin's lending products. NeoSky's drones could eventually deliver Cocoblu's products. This isn't synergy in the traditional sense—it's ecosystem building where the whole becomes greater than the sum of parts.

The ecosystem extends beyond just internal businesses. The investment in Matternet provides technology for NeoSky. The relationship with Amazon through Cocoblu could eventually benefit all businesses. The banking relationships from WeFin could provide working capital for other ventures. Every relationship is leveraged multiple times.

Lesson 8: The Patient Capital Advantage

With 74.8% promoter holding, RattanIndia has something most startups lack—patient capital. They don't need to show profitability in 18 months to raise the next round. They don't have venture capitalists pushing for exits. They can make ten-year bets that would be impossible for venture-backed competitors.

This patient capital advantage is most visible in the drone business. NeoSky won't generate meaningful revenue for years, but RattanIndia can afford to wait. They're building capabilities, getting certifications, and establishing relationships while competitors burn through venture capital trying to show rapid growth.

Lesson 9: The Complexity Management System

Running multiple businesses simultaneously requires sophisticated management systems. RattanIndia appears to have adopted a federal structure—each business has its own CEO and P&L responsibility, but shares certain corporate resources like finance, legal, and strategy. This provides autonomy for speed while maintaining control for governance.

The complexity management extends to reporting and metrics. Each business likely has different KPIs—Cocoblu focuses on GMV and take rate, Revolt on units sold and gross margin, NeoSky on R&D milestones. Managing this complexity without losing focus requires discipline that most conglomerates lack.

Lesson 10: The Transformation Narrative Power

Perhaps the most underappreciated aspect of RattanIndia's playbook is the power of the transformation narrative itself. By positioning themselves as a "digital transformation story," they've created a compelling narrative for investors, employees, and partners. Everyone wants to be part of a transformation story; nobody wants to join a dying infrastructure company.

This narrative power extends to valuation. A power company trades at 0.5-1x book value. A technology conglomerate can trade at 5-10x book value. Same assets, same cash flows, but different story equals different multiple. RattanIndia understood that in modern markets, narrative is as important as numbers.

The Meta-Lesson: Violating Rules Intelligently

The overarching lesson from RattanIndia's playbook is that you can violate conventional wisdom if you do it intelligently and systematically. Conglomerates are out of fashion? Build one anyway but with modern governance. Venture capital is abundant? Use internal capital for control. Specialization is key? Diversify but with underlying thesis consistency.

Every rule RattanIndia breaks, they break for a reason. Every unconventional decision has conventional logic behind it. This isn't recklessness—it's calculated contrarianism. In a market where everyone is following the same playbook, doing something different isn't just brave; it might be the only way to win.

The execution remains the challenge. Having a good playbook and running it successfully are different things. RattanIndia's playbook is sound, but the game is far from over. The next few years will determine whether this playbook produces a championship or becomes a cautionary tale about the perils of complexity.

X. Analysis & Investment Thesis

The investment case for RattanIndia is essentially a bet on execution in the face of staggering complexity. At 84x earnings and 8.4x book value, the market is pricing in successful transformation but not flawless execution. This creates an interesting risk-reward dynamic that deserves careful analysis.

The Bull Case: India's Berkshire Hathaway in the Making

The optimistic view sees RattanIndia as early Berkshire Hathaway—a capital allocation machine run by skilled operators who can compound value across multiple businesses. The 74.8% promoter holding ensures alignment, patient capital enables long-term thinking, and the multi-business model provides diversification.

The market opportunity is undeniable. If India's e-commerce grows from $100 billion to $500 billion by 2030, Cocoblu could 5x just by maintaining share. If EV adoption reaches even half the government targets, Revolt could be selling 200,000 units annually. If drone delivery becomes reality, NeoSky could be worth more than all other businesses combined.

The platform positioning is particularly powerful. Unlike pure-play competitors who need to build everything themselves, RattanIndia can leverage existing platforms (Amazon for Cocoblu, banks for WeFin) while capturing significant value. This asset-light approach means higher returns on capital once scale is achieved.

The optionality value is enormous. Each business is essentially a call option on a massive trend. Even if only one or two succeed spectacularly, the returns could justify the entire investment. This is venture capital math applied to a public company—multiple shots on goal with asymmetric payoffs.

The Bear Case: Complexity Collapse in Progress

The pessimistic view sees a company drowning in complexity, burning cash across multiple fronts without achieving dominance in any. The losses are real and widening—Rs 355 crore in Q4 FY25 versus Rs 81 crore in Q4 FY24. At this burn rate, even patient capital has limits.

The competitive intensity is brutal. In e-commerce, Cocoblu faces not just Amazon and Flipkart but hundreds of other sellers. In EVs, Ola Electric raised $500 million and is still struggling. In drones, global giants like DJI have massive technological advantages. Being subscale in multiple difficult businesses is a recipe for perpetual losses.

The execution risk is multiplicative, not additive. Running one startup is hard; running five simultaneously is nearly impossible. Each business requires different skills, different talent, different strategies. The probability of succeeding in all is minuscule. More likely, management attention gets diluted and all businesses underperform.

The valuation assumes perfection. At current multiples, RattanIndia needs to grow revenue 30% annually while reaching profitability within 2-3 years. Any disappointment—a failed product launch, regulatory setback, competitive loss—could trigger multiple compression. The stock could easily fall 50% and still be expensive on traditional metrics.

The Realist Case: Measured Transformation with Volatile Path

The realistic view acknowledges both opportunity and challenge. RattanIndia will likely succeed in some ventures and fail in others. The question is whether the successes will be large enough to offset the failures and justify the current valuation.

Cocoblu has the clearest path to profitability. The business model is proven, the infrastructure is built, and the scale is emerging. If they can reach Rs 5,000 crore in GMV at a 10% take rate with 5% EBITDA margins, that's Rs 25 crore in EBITDA—not huge but proof of concept.

Revolt needs to reach 50,000 units annually to break even. The current run rate of ~15,000 units suggests this is achievable by 2026. The bigger question is whether they can reach 100,000+ units to generate meaningful profits. The brand is strong, the product is improving, but competition is intensifying.

NeoSky and WeFin are longer-term options. Neither will contribute meaningfully to revenue or profits in the next 2-3 years. They're valuable as strategic hedges and learning platforms but shouldn't be counted in near-term valuation.

Valuation Framework: Sum-of-Parts Reality Check

A sum-of-parts valuation provides perspective:

- Cocoblu: At 1x GMV (e-commerce comparable), worth Rs 2,000 crore

- Revolt: At 2x revenue (EV comparable), worth Rs 1,000 crore

- Neobrands: At 3x revenue (D2C comparable), worth Rs 300 crore

- NeoSky: At 10x revenue (deep tech comparable), worth Rs 200 crore

- WeFin: At 2x book value (fintech comparable), worth Rs 100 crore

- Power Business: At book value, worth Rs 1,000 crore

- Net Debt: Negative Rs 500 crore

Total sum-of-parts: Rs 4,100 crore versus current market cap of Rs 6,997 crore

This suggests 40% overvaluation on current metrics but doesn't account for growth potential. If each business doubles in three years—aggressive but possible—the sum-of-parts reaches Rs 8,200 crore, implying 17% upside.

Key Monitorables for Investors

The investment thesis hinges on specific, measurable milestones:

- Cocoblu reaching Rs 5,000 crore GMV (validates e-commerce execution)

- Revolt achieving 50,000 unit annual run rate (proves manufacturing scale)

- Consolidated EBITDA turning positive (shows business model viability)

- Cash burn reducing below Rs 100 crore quarterly (ensures sustainability)

- One new business reaching Rs 500 crore revenue (demonstrates replication ability)

Risk-Reward Assessment

The risk-reward is asymmetric but not clearly favorable. Downside could be 40-50% if execution falters. Upside could be 100-200% if multiple businesses succeed. For growth investors comfortable with volatility, this might be attractive. For value investors seeking safety, this is probably a pass.

The investment timeline matters enormously. Over 1-2 years, the stock could be extremely volatile as quarterly results disappoint or surprise. Over 5-7 years, if even two businesses succeed, returns could be exceptional. This is not a trade; it's a long-term commitment to India's transformation.

The Investment Decision

RattanIndia represents a fascinating but complex investment opportunity. It's simultaneously overvalued on current metrics and potentially undervalued on future potential. It's both a risky conglomerate and a diversified growth portfolio. It's either brilliant capital allocation or dangerous complexity.

For investors who believe in India's digital transformation, have patience for multi-year execution, and can stomach significant volatility, RattanIndia offers exposure to multiple megatrends through a single stock. For investors seeking predictability, profitability, or simple business models, this is the wrong investment.

The ultimate question isn't whether RattanIndia is a good investment—it's whether it's the right investment for your specific goals, timeline, and risk tolerance. In a market full of simple stories, RattanIndia offers something different: complexity with potential, ambition with execution risk, transformation with uncertainty. Sometimes the most interesting investments are the hardest to understand. RattanIndia is definitely that.

XI. Future Outlook & Key Questions

The next 24 months will determine whether RattanIndia becomes a case study in successful transformation or expensive ambition. Three critical developments are already in motion that will shape the company's trajectory.

International Expansion: The Revolt Goes Global

Sri Lanka was the test. Following a successful launch in Sri Lanka last year, Nepal is set to be the next key international market, with further expansion plans in the pipeline. But the real prize is Southeast Asia—Thailand, Indonesia, Vietnam—markets where two-wheeler culture dominates and Chinese brands haven't yet established monopolies.

The international strategy for Revolt is fascinating. Instead of competing in developed markets against established brands, they're targeting emerging markets where the transition from petrol to electric is just beginning. These markets have similar characteristics to India—price-sensitive consumers, two-wheeler dominance, growing environmental awareness, and government support for electrification.

The challenge is localization. Each market has different regulations, consumer preferences, and competitive dynamics. What works in Delhi might fail in Dhaka. The question is whether RattanIndia can replicate Revolt's India playbook internationally or needs entirely new strategies for each market.

The Next Acquisition Target: Following the Breadcrumbs

RattanIndia's acquisition strategy follows a clear pattern—buy struggling but technologically advanced companies at reasonable valuations. The next target is likely in one of three areas:

A direct-to-consumer brand with strong technology but weak finances would fit perfectly into the Neobrands portfolio. India has dozens of D2C brands that raised venture capital in 2021-2022 but are now struggling with profitability. RattanIndia could acquire 2-3 brands for the price they paid for Revolt.

A fintech platform with lending licenses but capital constraints would accelerate WeFin's growth. Many NBFCs are struggling with funding costs and regulatory requirements. RattanIndia's patient capital and corporate backing could provide stability while gaining instant lending capabilities.

A logistics technology company would complete the ecosystem. If you're selling online (Cocoblu), manufacturing vehicles (Revolt), and flying drones (NeoSky), controlling last-mile delivery becomes strategic. A small logistics tech acquisition could provide the foundation for an integrated delivery network.

Path to Profitability: The Clock is Ticking

The market's patience isn't infinite. RattanIndia needs at least one business to achieve EBITDA profitability by FY26 to maintain credibility. The most likely candidate is Cocoblu, which has scale, established operations, and improving unit economics.

The profitability path requires careful sequencing. First, Cocoblu reaches EBITDA breakeven through scale and operational efficiency. This provides confidence and some cash flow. Second, Revolt achieves gross margin positivity through volume and cost reduction. Third, the fashion brands reach contribution margin positivity. The drone and fintech businesses can remain in investment mode if the core businesses stabilize.

But profitability can't come at the expense of growth. The market is valuing RattanIndia on growth potential, not current earnings. Slowing growth to achieve profitability would likely trigger multiple compression—the worst of both worlds.

The Consolidation Question: When to Simplify

At some point, RattanIndia will need to simplify its structure. The current complexity—multiple subsidiaries, various business models, different stages of development—makes it difficult for investors to value and understand the company. The question is when and how to consolidate.

One approach is vertical integration within ecosystems. Merge Cocoblu and Neobrands into a single e-commerce entity. Combine NeoSky and its subsidiaries into one drone company. This maintains diversification while reducing complexity.

Another approach is to spin off mature businesses. Once Revolt reaches scale and profitability, it could be listed separately, unlocking value and providing growth capital. This worked well for Reliance with Jio and Retail.

The timing is crucial. Consolidate too early and you lose flexibility. Wait too long and complexity becomes unmanageable. The optimal window is probably 2026-2027, after businesses prove viability but before they need massive growth capital.

The Technology Platform Question

RattanIndia talks about technology but hasn't built a unified technology platform. Each business has its own tech stack, data systems, and development teams. This is expensive and inefficient. The question is whether to build a shared technology platform that all businesses can leverage.