R R Kabel: Wiring India's Growth Story and the FMEG Pivot

I. Introduction: The "Invisible" Megatrend

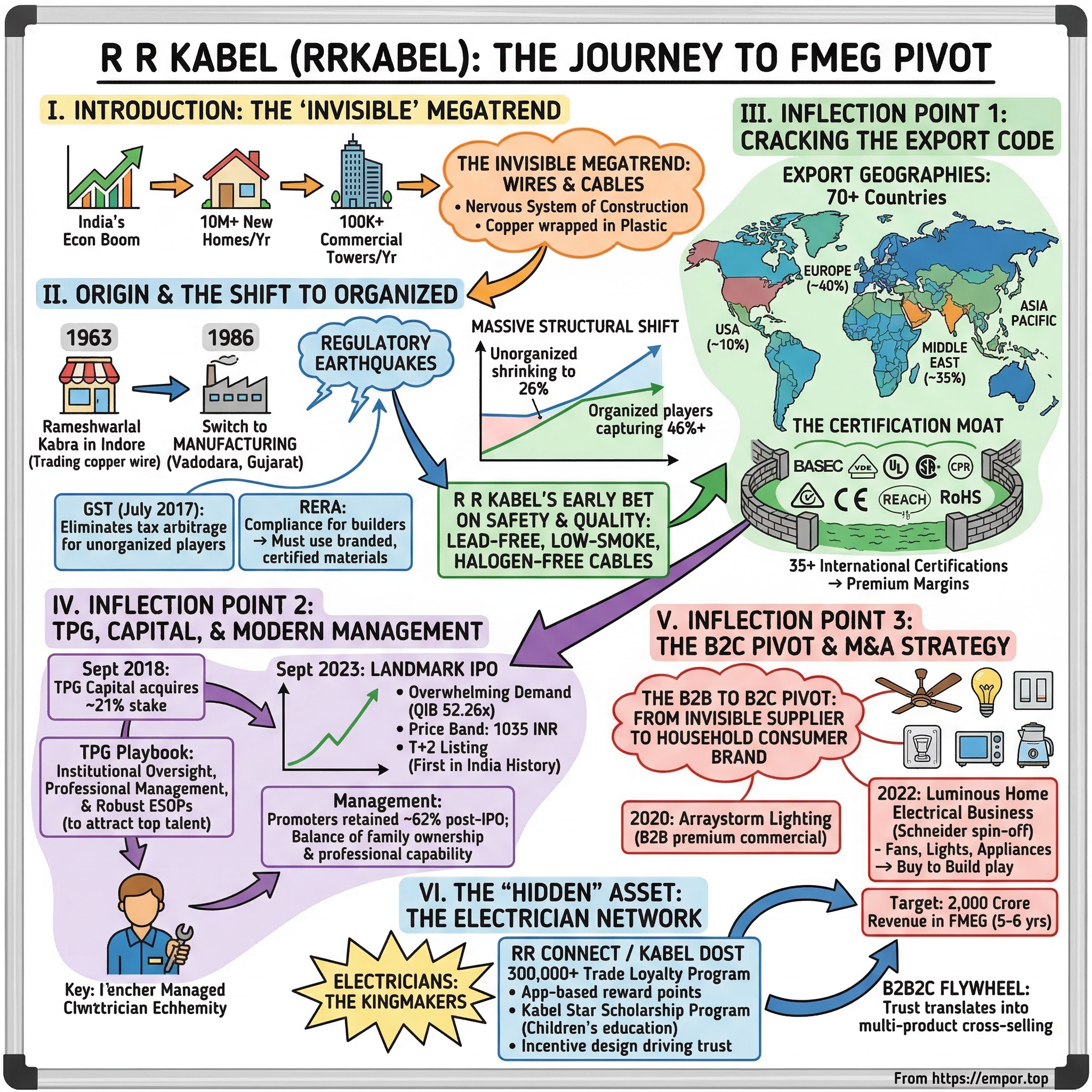

There is a peculiar paradox at the heart of India's economic boom. The nation builds more than ten million new homes each year, erects hundreds of thousands of commercial towers, lays millions of kilometers of power distribution lines, and yet almost nobody talks about the companies that supply the literal nervous system of all this construction: the wires and cables running through every wall, under every floor, and along every power corridor. It is copper wrapped in plastic. It is not glamorous. It does not trend on social media. And it has been one of the greatest wealth-creation categories in the Indian stock market over the past decade.

R R Kabel sits at the fascinating intersection of this invisible megatrend. The company is India's largest exporter of wires and cables, selling into more than seventy countries with a dizzying array of international safety certifications that most competitors cannot match. Domestically, it commands a roughly seven percent share of the organized wires and cables market—a market that itself has been growing at a compounded rate of approximately thirteen percent annually between FY19 and FY24. But here is what makes the R R Kabel story truly interesting for the long-term investor: the company is not content being a wire manufacturer. It is attempting one of the most difficult strategic pivots in Indian industry—the leap from being a trusted but invisible B2B supplier to becoming a household consumer brand in fast-moving electrical goods, or FMEG. Fans, lighting, switches, appliances. The stuff that sits in your living room, not behind your walls.

This is the story of a family that started trading copper wire from a small shop in Indore in 1963, built a manufacturing empire in Gujarat, attracted one of the world's most sophisticated private equity firms in TPG Capital, went public in a landmark IPO, and is now betting billions on a consumer transformation that will either catapult the company into the league of Havells and Polycab—or leave it stranded between two identities. The narrative arc here is not just about R R Kabel. It is about how traditional Indian family businesses evolve, how regulatory shifts can destroy entire swaths of unorganized industry overnight, and how the elusive "B2B to B2C" pivot actually gets executed in practice.

The numbers tell the story of a company in motion. Revenue grew from roughly twenty-seven billion rupees in FY21 to over seventy-six billion rupees in FY25—nearly tripling in four years. Net profit climbed from about 1.35 billion rupees to 3.1 billion rupees over the same period. The FMEG segment, while still small at roughly ten percent of revenue, has been growing at twenty-five to thirty-two percent annually. And all of this is happening against the backdrop of India's infrastructure supercycle, a housing boom propelled by regulation, and a once-in-a-generation shift from unorganized to organized manufacturing.

But before we get to the strategic chess moves and the financial engineering, we need to understand where this company came from. Because the origin story explains everything about how R R Kabel thinks about competition, quality, and the long game.

II. The Origin and the Shift to Organized

Picture Indore in 1963. A city in central India known for its textile mills and trading culture. Rameshwarlal Kabra, a man whose family had migrated from what is now Bangladesh through Nepal to India, opens a small retail shop selling copper winding wire. It is about as humble a beginning as you can imagine in Indian business. He is not an engineer. He is not backed by capital. He is a trader with an instinct for a product that every factory, every motor winder, and every electrician in India needs but nobody thinks much about.

For more than two decades, that is what the business was—trading. Rameshwarlal moved to Mumbai in 1965 and continued buying and selling winding wires and insulating materials. It was steady work. It put food on the table. But it was not transformative. The transformation came in 1986, when the family made the critical leap from trading to manufacturing, setting up their first winding wires manufacturing unit in Vadodara, Gujarat. This was a bet on India's industrial future. Gujarat, with its business-friendly policies and proximity to ports, would prove to be an inspired choice. By 1991, Ram Ratna International was launched as the export arm, and within a year it earned government recognition as an export house. Ram Ratna Wires Limited was formed and listed on the stock exchange in 1994. Then, in 1999, R R Kabel was launched with what the company described as the most advanced wire and cable manufacturing facility in India, located in Silvassa.

But here is the thing that investors need to understand about the Indian wires and cables market of the 1990s and 2000s: it was the Wild West. The market was overwhelmingly unorganized—small, local manufacturers operating out of sheds, producing cables with questionable copper purity, minimal safety testing, and virtually no quality certifications. These operators thrived because they could evade taxes, skip quality compliance, and undercut organized players on price. For a homeowner building a house, the difference between a branded cable and a local one was often thirty to forty percent in price. And since wires go inside walls where nobody sees them, the incentive to save money was enormous—even if the safety implications were terrifying.

Two regulatory earthquakes changed everything. The first was the Goods and Services Tax, implemented in July 2017. GST created a unified national tax structure that eliminated the tax arbitrage that unorganized players had relied upon for decades. Suddenly, the guy running a cable shop out of a shed in a small town had to register, file returns, and pay the same taxes as R R Kabel. The cost advantage of being unorganized shrank dramatically. The second earthquake was RERA—the Real Estate Regulation and Development Act—which imposed compliance requirements on builders and developers that effectively mandated the use of branded, certified building materials, including wires and cables. Builders who wanted RERA compliance could not afford to use uncertified cables from unknown manufacturers. They needed paper trails, quality certificates, and brand guarantees.

The impact was seismic. The unorganized sector, which had once dominated the Indian wires market, shrank to roughly twenty-six percent of total market share. Large listed players—Polycab, Havells, KEI, Finolex, and R R Kabel among them—collectively captured about forty-six percent. Other organized but unlisted players took another twenty-eight percent. This was not gradual erosion. This was a structural shift, a massive vacuum that branded players rushed to fill. And R R Kabel, with its three decades of manufacturing experience and an early investment in quality standards, was positioned to capture a disproportionate share of this shift.

The company had made a prescient bet on safety and quality that now paid off handsomely. R R Kabel was the first Indian company to introduce lead-free, low-smoke, halogen-free cables to the domestic market. Its Superex FR wire became India's first building wire to carry REACH and RoHS compliance—European safety standards that restrict over 245 harmful chemicals and ban hazardous substances like lead, mercury, and cadmium. For most Indian consumers, these certifications meant little. But for architects, builders, and institutional buyers who were increasingly conscious of safety liability, it meant everything. R R Kabel used "fire safety" as a branding tool in a market where house fires caused by faulty wiring were tragically common, and where trust in product quality was low. In a commoditized market, they found a way to differentiate on something that actually mattered.

The founder, Rameshwarlal Kabra, received the Padma Shri from the President of India in 2018 for his contributions to rural and tribal communities—a recognition that underscored the family's deep roots in Indian society and their understanding that business success in India requires more than just good products. It requires social embeddedness, community trust, and a reputation built over decades, not quarters. That reputation would become the foundation for everything that followed.

III. Inflection Point 1: Cracking the Export Code

While the domestic story of regulatory tailwinds and market share gains gets the headlines, the export business is where R R Kabel built something that might be genuinely durable—a competitive moat that is extremely difficult to replicate. And it is a business that most investors, even those who follow the company closely, tend to underappreciate.

Think about what it takes to sell electrical cables in Europe. Not in India, where enforcement has historically been patchy and brand trust does the heavy lifting. In Europe and the United Kingdom, where a single cable failure in a building can trigger lawsuits, regulatory investigations, and criminal liability. The barriers are not about having the cheapest copper or the fastest factory. They are about certifications—formal, audited, painstakingly acquired approvals from bodies that have no incentive to make the process easy.

R R Kabel spent the better part of the 2010s assembling a certification portfolio that reads like an alphabet soup of global safety standards. BASEC from the British Approvals Service for Cables. VDE from Germany. UL and CSA for the North American market. TUV for solar cables. ETL for sprinkler and irrigation cables. CPR—the Construction Products Regulation from the European Union. CE marking. And on top of all of that, the REACH and RoHS environmental compliance that the company had pioneered domestically. In total, the company accumulated over thirty-five international certifications. R R Kabel became the only Indian cable manufacturer to simultaneously offer building wire compliance with REACH, RoHS, CE, and CPR.

Why does this matter so much? Because each of these certifications takes years to acquire. The process involves factory audits, product testing, ongoing compliance monitoring, and significant financial investment. A competitor wanting to replicate R R Kabel's export capability would need to spend millions of dollars and half a decade just to get to the starting line. In the language of competitive strategy, this is a cornered resource—an intangible asset that cannot be easily bought, replicated, or substituted. It is the kind of moat that does not show up on a balance sheet but shows up very clearly in the income statement.

The results speak volumes. R R Kabel's products now sell in more than seventy-two countries across North America, Europe, Asia Pacific, and the Middle East. Export revenue accounts for approximately twenty-seven to thirty percent of total revenue—a diversification that most Indian wire manufacturers cannot match. The geographic breakdown of exports is telling: roughly forty percent goes to Europe, thirty-five percent to the Middle East, and about ten percent to the United States, with the remainder spread across other markets. The European and UK markets, in particular, generate premium margins because the certification barriers keep competition limited and pricing power intact.

The export business also serves as a natural hedge against domestic cyclicality. When Indian real estate hits a soft patch—as it periodically does—the export business provides a floor under revenue and margins. And because export contracts tend to be longer-term and more relationship-driven than domestic spot sales, they provide a degree of revenue visibility that pure domestic players do not enjoy.

There have been headwinds, of course. The Red Sea shipping crisis temporarily disrupted export logistics, and in August 2025, a twenty-five percent US tariff on Indian goods forced the company to redirect its American exports to other markets. But the US represented only about 2.5 percent of total revenue, so the tariff impact was manageable rather than existential. Management's response was pragmatic: rather than absorb the tariff cost, they redirected volume to markets where their certification portfolio gave them pricing power. This is the kind of strategic flexibility that a diversified export portfolio provides.

For investors tracking R R Kabel, the export business is the quiet engine. It does not generate the growth headlines that the FMEG pivot does, and it does not have the scale of the domestic wires business. But it generates premium margins, provides geographic diversification, and sits behind a certification moat that deepens with every passing year. Every new certification acquired, every new market entered, every new long-term supply relationship established adds another layer to a barrier that competitors will find increasingly expensive to breach. This is the hidden asset that the market may be underpricing.

IV. Inflection Point 2: TPG, Capital, and Modern Management

In September 2018, something happened that fundamentally altered the trajectory of R R Kabel. TPG Capital, one of the world's most sophisticated private equity firms—manager of over a hundred billion dollars in assets, with a reputation for identifying high-quality businesses in growth markets—acquired a roughly twenty-one percent minority stake in the company for approximately six hundred crore rupees, paying about 270 rupees per share. The investment valued R R Kabel at a fraction of what it would eventually be worth, but that is almost beside the point. What mattered was not the price TPG paid. What mattered was what TPG brought.

To understand the significance, you need to understand the typical lifecycle of a successful Indian family business. The founder builds something extraordinary through sheer grit, market knowledge, and personal relationships. The second generation inherits a thriving operation but faces a fundamentally different challenge: scaling it from a regional powerhouse to a national and international institution. This transition requires professional management, corporate governance, institutional processes, and capital market readiness—capabilities that family-run businesses often lack, not because the families are incompetent, but because these capabilities are simply different muscles than the ones used to build the business in the first place.

TPG's playbook with R R Kabel followed a pattern the firm had perfected across dozens of investments in Asia. They appointed two directors to the board—bringing institutional oversight and governance expectations that went far beyond what a family-run company typically operates under. They pushed for professionalization of management across every function. And critically, they helped design incentive structures that could attract top-tier talent from outside the family.

The introduction of robust Employee Stock Ownership Plans was a watershed moment. In traditional Indian manufacturing companies, non-family executives are well-compensated but rarely have meaningful equity upside. This creates a structural problem: the best talent in FMCG, consumer goods, and brand management gravitates toward companies where equity participation is standard. R R Kabel, under TPG's guidance, began offering ESOP pools that aligned non-family executives with margin expansion targets and, eventually, IPO milestones. This was a rarity in the Indian wire and cable industry, and it enabled the company to recruit leadership talent that would have been unattainable otherwise.

The Kabra family, to their credit, embraced the transition rather than resisting it. The family patriarch, Rameshwarlal Kabra, had built the foundation. His son Mahendrakumar Rameshwarlal Kabra, born in 1957, took on the role of Managing Director—bringing the credibility of family continuity while supporting the professionalization agenda. Shreegopal Kabra, another key family member, served as Group President of the broader RR Global conglomerate and held significant industry positions including Chairman of the International Copper Association's Wire and Cable Product Council and former President of IEEMA, the Indian Electrical and Electronics Manufacturers' Association. These were not honorary titles. They reflected a family that understood the value of industry-level engagement and was willing to lend the company's credibility to institutional processes.

The management team that emerged from this professionalization drive reflects the dual identity of the company. Rajesh Babu Jain runs the Wires and Cables business as Chief Operating Officer. Sanjay Narnarayan Taparia heads the International Business as CEO. Vivek Abrol, brought in as CEO of the Consumer Business—the FMEG Division—represents the kind of external hire that the ESOP program was designed to attract: a consumer-business professional tasked with building a brand, not just a manufacturing operation. Satishkumar Anandilal Agarwal serves as Chief Strategy Officer, and Shishir Sharma as Chief Marketing Officer—roles that simply did not exist in the company a decade earlier.

Then came the IPO. On September 13-15, 2023, R R Kabel went public with a price band of 983 to 1,035 rupees per share. The total issue size was approximately 1,964 crore rupees—comprising a small fresh issue of 180 crore rupees and a much larger offer for sale of 1,784 crore rupees, primarily driven by TPG trimming its stake. The offering was met with overwhelming demand: the overall subscription came in at 18.69 times, with qualified institutional buyers subscribing at a staggering 52.26 times. Anchor investors alone committed 585 crore rupees before the public offering even opened.

The listing on September 20, 2023, was notable for two reasons. First, R R Kabel shares opened at 1,180 rupees—a fourteen percent premium over the issue price—signaling strong market appetite for the India infrastructure and housing theme. Second, and more symbolically, this was the first T+2 listing in Indian stock market history, meaning shares were credited to investor accounts just two days after the IPO closed rather than the traditional six days. R R Kabel, in a sense, helped inaugurate a new era of capital market efficiency in India.

For TPG, the outcome was spectacular. Having invested at approximately 270 rupees per share in 2018, the firm sold down its stake at the IPO price of 1,035 rupees, reducing its holding from roughly seventeen percent to about six percent. Then, in May 2024, TPG sold its remaining five percent stake—approximately 56.33 lakh shares—through block deals worth about a thousand crore rupees. All told, TPG generated a roughly four-times return on its investment, translating to an internal rate of return of approximately thirty-one percent over five years. For a minority investment in a family-controlled Indian manufacturer, that is an exceptional outcome—and a case study in how private equity can catalyze value creation without needing operational control.

The promoter group—the Kabra family and associated entities—retained approximately sixty-two percent of the company post-IPO, ensuring that strategic decision-making remained firmly in family hands even as the management structure became increasingly institutional. This balance—family ownership providing long-term strategic continuity, professional management providing operational excellence, and public market listing providing capital access and transparency—is the institutional framework that R R Kabel carried into its most ambitious strategic bet: the pivot to consumer goods.

V. Inflection Point 3: The B2C Pivot and M&A Strategy

Every wire and cable company in India eventually arrives at the same strategic crossroads. The core business—manufacturing copper and aluminum conductors, wrapping them in insulation, and selling them through dealer networks—is fundamentally a good business. Capital requirements create barriers to entry. Regulatory shifts favor organized players. Infrastructure spending provides secular demand growth. But there is a ceiling. Wires and cables are perceived as commodities by end consumers, which means pricing power is limited, brand premiums are modest, and valuation multiples in the public market reflect these constraints.

Then there is the FMEG world—fast-moving electrical goods. Fans, lighting, switches, switchgears, water heaters, small appliances. These are products that consumers see, touch, choose, and develop brand loyalty toward. Havells built a consumer empire on the back of this insight, transforming from a switchgear manufacturer into one of India's most recognized household brands. Polycab has been aggressively expanding its FMEG portfolio. The economics are compelling: at scale, FMEG products command higher gross margins, generate greater brand equity, and earn significantly higher valuation multiples from the stock market. A pure wires and cables company might trade at fifteen to twenty times earnings. A diversified electricals company with a strong FMEG franchise can trade at forty to sixty times.

R R Kabel understood this math. The question was not whether to make the pivot, but how. Building an FMEG business from scratch—designing products, establishing manufacturing capacity, building brand awareness, creating distribution networks—takes years and costs hundreds of crores with no guarantee of success. The alternative was acquisition: buying an existing FMEG business that came with products, manufacturing, distribution, and brand recognition, even if the acquired business itself was not performing optimally.

On April 13, 2022, R R Kabel announced the acquisition that would define its FMEG strategy. The target was the Home Electrical Business of Luminous Power Technologies, which was being carved out and sold by its parent company, Schneider Electric of France. Schneider had acquired Luminous in stages—seventy-four percent in 2011 and the remaining twenty-six percent in 2017—but had decided to retain only the inverter and UPS business, divesting the fans, lights, and appliances division. The deal closed on May 30, 2022.

The specific financial terms were not publicly disclosed—both parties were unlisted at the time and chose not to reveal the valuation. What is known is that the Luminous Home Electrical Business had revenue of approximately three hundred crore rupees at the time of acquisition. Industry analysts estimated that R R Kabel paid in the vicinity of 225 crore rupees, which if accurate, represented roughly 0.75 times sales—a significant discount to the four to six times sales multiples that established FMEG players like Havells commanded in the public market.

Why the discount? Because the Luminous Home Electrical Business was not a crown jewel. Under Schneider's ownership, it had been a non-core division receiving limited strategic attention and investment. Margins were thin, the product portfolio needed refreshing, and the distribution network, while extensive, had not been optimized for standalone performance. This was not a business anyone was going to buy for its current profitability. It was a "buy to build" play—acquiring immediate access to manufacturing capacity, distribution networks, brand recognition, and product lines that would have taken R R Kabel five years or more to build organically.

The deal came with a critical asset: a four-year brand licensing agreement allowing R R Kabel to continue using the Luminous brand name for fans and lighting products. This was essentially a four-year runway to transition brand equity from Luminous to the R R Kabel brand while maintaining customer continuity. It was a clever structure—buying time to build brand awareness while leveraging an existing name that consumers already recognized.

Two years earlier, in 2020, R R Kabel had made a smaller but strategically complementary acquisition: Arraystorm Lighting Private Limited, a Bengaluru-based premium LED lighting company previously owned by Kores India. Arraystorm operated in the B2B commercial and institutional lighting space, supplying custom lighting solutions to clients including Google, Amazon, and Boston Consulting Group. The acquisition expanded R R Kabel's lighting capability from consumer-grade products into the premium commercial segment, where margins are higher and relationships are stickier.

The integration reality, however, has been exactly as messy as anyone who has studied M&A in Indian manufacturing would expect. The FMEG segment, while growing at an impressive twenty-five to thirty-two percent annually, remained a drag on consolidated margins in the first couple of years post-acquisition. When you are integrating manufacturing facilities, rationalizing product lines, building brand awareness, and investing in distribution—all simultaneously—profitability takes a backseat to market share. R R Kabel's FMEG margins lagged significantly behind peers like Havells, which had decades of consumer-brand-building experience and the scale economies that come with it.

But there were encouraging signs. By the second quarter of FY26, FMEG segment margins improved by 6.6 percentage points compared to the same quarter a year earlier. The business was generating quarterly revenue of around 230 crore rupees and growing at rates that suggested the flywheel was beginning to turn. Management set a target of reaching two thousand crore rupees in FMEG revenue within five to six years of the Luminous acquisition—a target that would require sustained thirty-plus percent growth but was not unreasonable given the trajectory.

The strategic logic of the FMEG pivot comes into sharp focus when you consider the company's existing distribution infrastructure. R R Kabel sells through a network of over a hundred thousand retailers across India. Every one of those retailers is a potential distribution point for fans, lighting, and switches. The marginal cost of adding an FMEG product to a retailer who already stocks R R Kabel wires is dramatically lower than building a new retail relationship from scratch. This is the cross-selling synergy that management repeatedly emphasized in investor presentations, and it is the single most important variable that will determine whether the FMEG pivot succeeds or fails. If R R Kabel can convert even a fraction of its wire-and-cable retail network into multi-product outlets, the economics of the FMEG business transform entirely.

VI. The "Hidden" Asset: The Electrician Network

Here is a question that most investors never think to ask about the wires and cables business: who actually decides which brand of wire goes into your home? The answer is not you. Even if you are building or renovating a house and obsessing over every detail—the tile color, the kitchen countertop, the bathroom fixtures—you almost certainly do not spend time evaluating wire brands. That decision is made by your electrician. In the Indian residential construction ecosystem, the electrician is the single most influential figure in determining which wires, cables, switches, and increasingly which fans and lights end up in a building. They are the kingmakers of the electrical products industry, and they do not show up on any organizational chart.

R R Kabel understood this dynamic earlier and more deeply than most competitors, and their response was to build one of the most sophisticated trade loyalty programs in Indian manufacturing: RR Connect, with registered members affectionately referred to as "Kabel Dost"—literally, "Cable Friend."

The program has enrolled more than three hundred thousand electricians and retailers across India. The mechanics are straightforward but thoughtfully designed. Electricians and retailers register on the RR Connect mobile app. Every purchase of eligible R R Kabel products earns reward points. These points are redeemable through direct bank account transfers or Paytm wallet credits—not through vouchers or catalog gifts that gather dust, but through actual cash equivalents that electricians can use immediately. The program operates on a tier-based structure: higher purchase volumes unlock higher reward rates and additional benefits. There are referral incentives for introducing other electricians to the program. Lucky draws provide engagement hooks. And at the end of each year, top performers receive gifts and trips based on their tier level.

But the program goes beyond transactional rewards. R R Kabel launched the Kabel Star Scholarship Program in 2021, providing scholarships to children of electricians who pass their tenth-grade examination on the first attempt. Now in its fourth season, the scholarship program creates an emotional bond that transcends commercial incentives. It signals to electricians that R R Kabel sees them not as a distribution channel to be exploited, but as a community to be invested in. In India's relationship-driven business culture, this distinction matters enormously.

The strategic genius of the electrician network becomes apparent when you think about the FMEG pivot. An electrician who has been recommending R R Kabel wires for years, who receives reward points on every purchase, whose child received a scholarship from the company, is naturally predisposed to recommend R R Kabel fans, lights, and switches when a homeowner asks. This is a B2B2C flywheel: the company sells to the trade (B2B), the trade influences the consumer (B2C), and the loyalty program ensures that the trade remains locked into the R R Kabel ecosystem. The homeowner never knows they are part of a flywheel. They just know their trusted electrician recommended a particular brand.

This dynamic is particularly powerful in India's tier-two and tier-three cities, where brand awareness for FMEG products is lower and electrician recommendations carry even more weight than they do in metropolitan areas. A homeowner in Mumbai might research fan brands online before buying. A homeowner in a smaller city is far more likely to simply ask their electrician, "Which brand should I get?" If R R Kabel has locked in that electrician's loyalty through years of rewards, relationships, and community investment, they have effectively pre-sold their FMEG products before the homeowner even walks into a store.

The network also generates valuable data. Three hundred thousand registered users generating purchase data across product categories, geographies, and time periods gives R R Kabel real-time visibility into demand patterns at a granularity that aggregate market research cannot provide. This data informs inventory management, production planning, and new product development. It is the kind of structural advantage that compounds over time and becomes more valuable as the FMEG product portfolio expands.

The risk, of course, is that competitors can build similar programs—and they have. Polycab, Havells, and others all run loyalty programs of various sophistication. But loyalty programs, like any relationship, are path-dependent. The electrician who has been earning points with R R Kabel for five years, whose child received a scholarship, who has a personal relationship with the local R R Kabel sales representative, is not going to switch to a competitor's app because it offers marginally better reward rates. Switching costs in relationship-driven loyalty programs are real, even if they do not show up on a balance sheet.

VII. Analytical Frameworks

To understand where R R Kabel stands competitively and where it is heading, it helps to examine the business through two established strategic frameworks. These are not academic exercises—they reveal the structural forces that will determine whether the company's ambitious strategy succeeds.

Hamilton's 7 Powers: Where Does R R Kabel Have Durable Advantage?

The first power worth examining is Scale Economies. R R Kabel operates four world-class manufacturing facilities and has announced a multi-year capex plan of approximately 1,450 crore rupees to add 42,000 metric tons of cable manufacturing capacity by 2028, with an additional 1,200 crore rupees planned over three years for value-added products including solar cables. Scale matters in this business for two reasons. First, copper and aluminum—the primary raw materials—are global commodities traded on the London Metal Exchange. A larger manufacturer has greater procurement leverage, can negotiate better terms with smelters, and can hedge commodity exposure more efficiently. Second, the fixed costs of running a cable factory—the extrusion lines, testing equipment, quality laboratories, and overhead—get spread over a larger revenue base as volumes grow. R R Kabel's revenue roughly tripled from FY21 to FY25, and this scale has driven meaningful operating leverage, with EBITDA margins expanding as capacity utilization improves.

The second power—and arguably the most distinctive—is what Hamilton Helmer would call a Cornered Resource, though in this case it is intangible. The portfolio of thirty-five-plus international certifications for the export business represents years of investment, hundreds of audits, and a level of compliance infrastructure that cannot be purchased or replicated quickly. A new entrant wanting to compete with R R Kabel in European or UK cable markets would need to spend years and millions of dollars acquiring these certifications—assuming they could pass the audits at all. This is not a patent that expires or a technology that can be reverse-engineered. It is an accumulated capability that deepens with every additional year of compliance history.

The third power is Brand, though here the analysis is more nuanced. In the trade channel—among electricians, contractors, and dealers—R R Kabel has strong brand equity built over decades. The Kabel Dost program and the safety-certification messaging have created genuine brand preference among professionals who specify and install cables. But in the consumer-facing FMEG market, R R Kabel's brand is nascent compared to Havells, which has spent decades building consumer awareness through advertising, retail presence, and product design. The FMEG pivot is essentially a bet that trade-channel brand equity can be converted into consumer brand equity over time—a transition that is underway but far from complete.

Notably absent from R R Kabel's power portfolio are Network Effects and Switching Costs in the traditional sense. Wires and cables are not platform businesses, and while the Kabel Dost program creates relationship-based switching costs among electricians, the end consumer faces no switching costs whatsoever. A homeowner renovating next year could easily choose a different brand of wire than they used last time. This absence of consumer-level switching costs is precisely why the FMEG pivot matters so much strategically—FMEG products, especially fans and lighting with smart features, have the potential to create brand preference and repeat purchase behavior that raw cables never will.

Porter's Five Forces: The Competitive Landscape

Competitive Rivalry is high and intensifying. R R Kabel competes directly with Polycab, the market leader with roughly eighteen percent share and a four-thousand-plus distributor network. Havells brings the strongest consumer brand and the most diversified product portfolio. KEI Industries is formidable in EPC projects and extra-high-voltage cables. Finolex Cables maintains a reputation for quality and healthy margins. And in February 2025, a new competitive threat emerged when UltraTech Cement—India's largest cement manufacturer—announced an 1,800 crore rupee capital expenditure plan to enter the wires and cables segment, with a plant near Bharuch, Gujarat, expected to be commissioned by December 2026. The announcement sent R R Kabel's stock down eleven percent in a single day, a visceral reminder that competitive threats can emerge from unexpected directions.

Supplier Power is high. Copper and aluminum are priced on global commodity exchanges, and no single cable manufacturer has meaningful pricing power over these inputs. Copper price volatility directly impacts margins unless manufacturers can pass through cost increases to customers quickly—and in a competitive market, pass-through is never instantaneous or complete. R R Kabel mitigates this partially through the higher margins in its export business and through operational efficiency improvements, but commodity exposure remains an irreducible risk in this industry.

Buyer Power is moderate. The dealer and distributor network has meaningful leverage in negotiations, particularly in price-sensitive domestic markets. However, R R Kabel's loyalty programs, brand reputation, and broad product portfolio help mitigate dealer power by creating reasons beyond price for dealers to stock and recommend the brand.

The Threat of Substitutes is low. Despite periodic excitement about wireless power transmission and advanced building technologies, copper wiring remains the fundamental technology for electrical distribution in buildings and infrastructure. No commercially viable substitute exists at scale, and none is likely to emerge in the foreseeable future. This gives the entire wires and cables industry a level of demand durability that many other manufacturing sectors lack.

The Threat of New Entrants is moderate and rising. Historically, the capital intensity of cable manufacturing, the importance of brand trust in a safety-critical product, and the regulatory compliance requirements created substantial barriers to entry. These barriers remain real, but the UltraTech announcement demonstrated that well-capitalized companies from adjacent industries can cross these barriers when the market opportunity is large enough. UltraTech's existing relationships with builders and construction companies give it a natural distribution channel into the same end market that R R Kabel serves. The organized wires and cables market, once a relatively cozy oligopoly, may be entering a more contested era.

VIII. Bear vs. Bull Case

The Bear Case: Where the Story Could Unravel

The most important question bears ask about R R Kabel is simple and devastating: can a "wires company" actually win in consumer appliances? The FMEG pivot is strategically logical but operationally brutal. Havells has spent decades and billions of rupees building consumer brand equity in fans, lighting, and switches. It has dedicated consumer marketing teams, retail store networks, product design capabilities, and the kind of brand recall that makes consumers ask for products by name. R R Kabel is attempting to compress decades of brand-building into a few years, and history is littered with B2B companies that failed to make the consumer transition. The Luminous brand licensing agreement provides a four-year window, but that window is finite. If R R Kabel cannot build sufficient consumer brand awareness under its own name by the time the license expires, it faces a cliff.

The second bear concern is cyclicality. Despite the structural tailwinds from formalization and infrastructure spending, R R Kabel's core wires and cables business remains tethered to India's real estate cycle. When construction activity slows—as it inevitably does in periodic cycles—R R Kabel's domestic revenue decelerates. The export business provides some diversification, but at thirty percent of revenue, it is not large enough to fully offset a domestic downturn. And the FMEG business, at roughly ten percent of revenue, is too small to move the needle in a downturn scenario.

Third, commodity risk is ever-present. Copper prices are set by global supply and demand dynamics that R R Kabel has no ability to influence. A sharp rise in copper prices compresses margins unless the company can pass through costs to customers—a process that involves time lag and competitive friction. In the short term, copper volatility can cause significant earnings swings that obscure the underlying business trajectory and test investor patience.

Fourth, the competitive landscape is intensifying. The entry of UltraTech Cement into wires and cables adds a well-capitalized competitor with deep builder relationships and no shortage of ambition. If other large industrial conglomerates follow UltraTech's lead, the organized market could face margin pressure even as it grows in absolute terms.

The Bull Case: Why the Upside Could Be Significant

Bulls point first to operating leverage. R R Kabel's FMEG business has been margin-dilutive because it is still scaling. The investments in manufacturing capacity, brand building, distribution expansion, and product development create a substantial fixed-cost base that has not yet been fully absorbed by revenue. But as the FMEG business scales past its breakeven point—which management expects within the next couple of years—the margin trajectory should inflect sharply. Each incremental rupee of FMEG revenue will drop through at a much higher rate than the first rupee did, because the cost structure is already in place. The 6.6 percentage point improvement in FMEG segment margins in Q2 FY26 suggests this inflection may have already begun.

Second, India's infrastructure spending cycle appears to be in its early-to-middle innings rather than its late innings. Government capital expenditure on roads, railways, power transmission, urban infrastructure, and smart cities continues to accelerate. The real estate sector, buoyed by RERA-driven formalization and rising urbanization, shows no signs of structural slowdown. And the renewable energy push—India's ambitious solar capacity targets—is creating an entirely new demand category for specialized solar cables, which R R Kabel is actively investing in with dedicated manufacturing capacity.

Third, the China Plus One dynamic is a genuine tailwind for the export business. Global manufacturers and infrastructure developers who historically sourced cables from China are actively diversifying their supply chains. India, with its English-speaking workforce, strong engineering talent, competitive labor costs, and a company like R R Kabel that already holds the requisite international certifications, is a natural beneficiary. The company's recent commissioning of a 10.2 megawatt hybrid wind-solar captive power project in Gujarat also helps reduce energy costs and appeal to international buyers with ESG mandates.

Fourth, the financial trajectory is compelling. Q3 FY26 saw revenue growth of 42.3 percent year-over-year, with net profit growing 72.5 percent. These are not incremental improvements—they suggest a business that is hitting its stride operationally. Analysts estimate a revenue CAGR of approximately nineteen percent for FY25-FY27, driven by infrastructure spending, housing demand, renewable energy, and electrification tailwinds. If margins expand simultaneously—as operating leverage from both the wires and FMEG businesses kicks in—earnings growth could significantly outpace revenue growth.

The KPIs That Matter

For investors tracking R R Kabel's ongoing performance, three key performance indicators deserve close attention above all others.

The first is FMEG revenue as a percentage of total revenue. This single metric captures the progress of the company's most important strategic initiative. Currently at roughly ten percent, this number needs to move meaningfully higher—toward fifteen to twenty percent—for the FMEG pivot to be considered successful. Quarterly trajectory matters more than absolute level; consistent quarter-over-quarter improvement signals that the cross-selling flywheel is working.

The second is consolidated EBITDA margin. As of H1 FY26, EBITDA margin was approximately eight percent, with improvement driven by both scale in the wires business and margin expansion in FMEG. Sustained margin expansion would confirm that operating leverage is materializing and that the company is successfully transitioning from growth-at-all-costs to profitable growth. Margin compression, conversely, would signal competitive pressure or integration challenges.

The third is export revenue growth rate. The export business is the highest-quality segment in terms of moat durability and margin profile. Sustained double-digit export growth would confirm that the certification moat is translating into market share gains and that the China Plus One opportunity is being captured. A slowdown would warrant investigation into whether competitive dynamics or geopolitical factors are eroding the company's positioning.

IX. Epilogue: The Playbook

The R R Kabel story, stripped to its essence, offers three strategic lessons that extend far beyond the wires and cables industry.

The first lesson is about the catalytic power of private equity in family businesses. TPG's investment in R R Kabel in 2018 was not just a capital infusion—it was a transformation catalyst. The private equity firm brought governance standards, incentive design, management professionalization, and capital market preparation capabilities that the Kabra family might have eventually developed on its own, but almost certainly not as quickly or as effectively. The four-times return that TPG generated was not charity; it was earned through the value created by forcing a decades-old family business to operate like a modern institution. For investors evaluating family-run Indian companies, the presence of a reputable PE investor on the cap table is often a signal that the governance and professionalization journey is underway—and that signal has predictive value.

The second lesson is about the strategic use of M&A to buy time. The Luminous acquisition was not about buying a great business. It was about buying five years of distribution build-out, manufacturing capacity creation, and brand development at a discount to what it would have cost to build from scratch. The price paid—reportedly close to one times sales for a business that was generating thin margins—reflected the current state of the business, not its potential. R R Kabel was essentially paying for optionality: the option to turn a struggling standalone division into a thriving category within a larger, better-resourced platform. This "buy to build" approach is fundamentally different from the "buy to harvest" approach that characterizes most acquisitions, and understanding the distinction is critical for evaluating whether the acquisition premium was justified.

The third lesson is about incentive design driving organizational transformation. The introduction of ESOPs at R R Kabel was not a routine HR initiative. It was a strategic weapon. By offering meaningful equity upside to non-family executives, the company gained access to a talent pool that would otherwise have been unavailable—experienced consumer goods leaders, brand marketers, and category managers who could credibly compete with the talent pools at Havells and Polycab. In a business where the quality of execution matters as much as the quality of strategy, the ability to attract and retain top talent is not a nice-to-have. It is a competitive necessity. R R Kabel's willingness to dilute family equity in exchange for management capability reflects a level of strategic maturity that is still uncommon in Indian family businesses.

As of March 2026, R R Kabel stands at a fascinating inflection point. The wires and cables business is firing on all cylinders, with domestic formalization and export diversification providing dual growth engines. The FMEG pivot is past the chaotic early integration phase and showing signs of operational traction. The balance sheet is clean enough to fund continued capital expenditure. And the management team—a blend of family continuity and professional capability—has the institutional backing of public market accountability.

The question that hangs over R R Kabel is the same question that hangs over every ambitious Indian manufacturer attempting the B2B-to-B2C transition: can a company that built its reputation behind the wall—literally, inside the walls of Indian homes—build an equally compelling reputation in front of it? The Kabra family has spent sixty years proving that they understand copper, quality, and the Indian building ecosystem. The next decade will determine whether they can extend that understanding to the products that homeowners actually see.

X. Further Reading and References

For those who want to go deeper into the R R Kabel story and the broader Indian electricals ecosystem, here are the essential sources.

The R R Kabel Draft Red Herring Prospectus, filed with SEBI ahead of the September 2023 IPO, remains the single most comprehensive document on the company's unit economics, segment-level financials, TPG's restructuring impact, and management's strategic vision. It is dense but indispensable for serious investors.

Industry reports from Ambit Capital and Marcellus Investment Managers on the Indian FMEG and building materials sector provide the competitive context needed to evaluate R R Kabel's positioning relative to Polycab, Havells, KEI, and Finolex. These reports are particularly valuable for understanding the formalization thesis and the structural shift from unorganized to organized.

Saurabh Mukherjea's "The Joys of Compounding" offers broader context on how Indian building material franchises are built through distribution moats—a framework directly applicable to understanding R R Kabel's electrician network and retail distribution strategy.

Industry primers on RERA and its impact on organized versus unorganized building materials—available from CRISIL, ICRA, and various brokerage houses—provide the regulatory backstory that makes the formalization tailwind comprehensible.

Finally, case studies on the Schneider Electric and Luminous carve-out, available through business school databases and industry publications, illuminate the strategic logic behind divestitures and acquisitions in Indian manufacturing—the kind of deal-making that defined R R Kabel's FMEG entry.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube