Rashi Peripherals: The Hardware Backbone of India's Digital and AI Surge

I. Introduction & Episode Roadmap

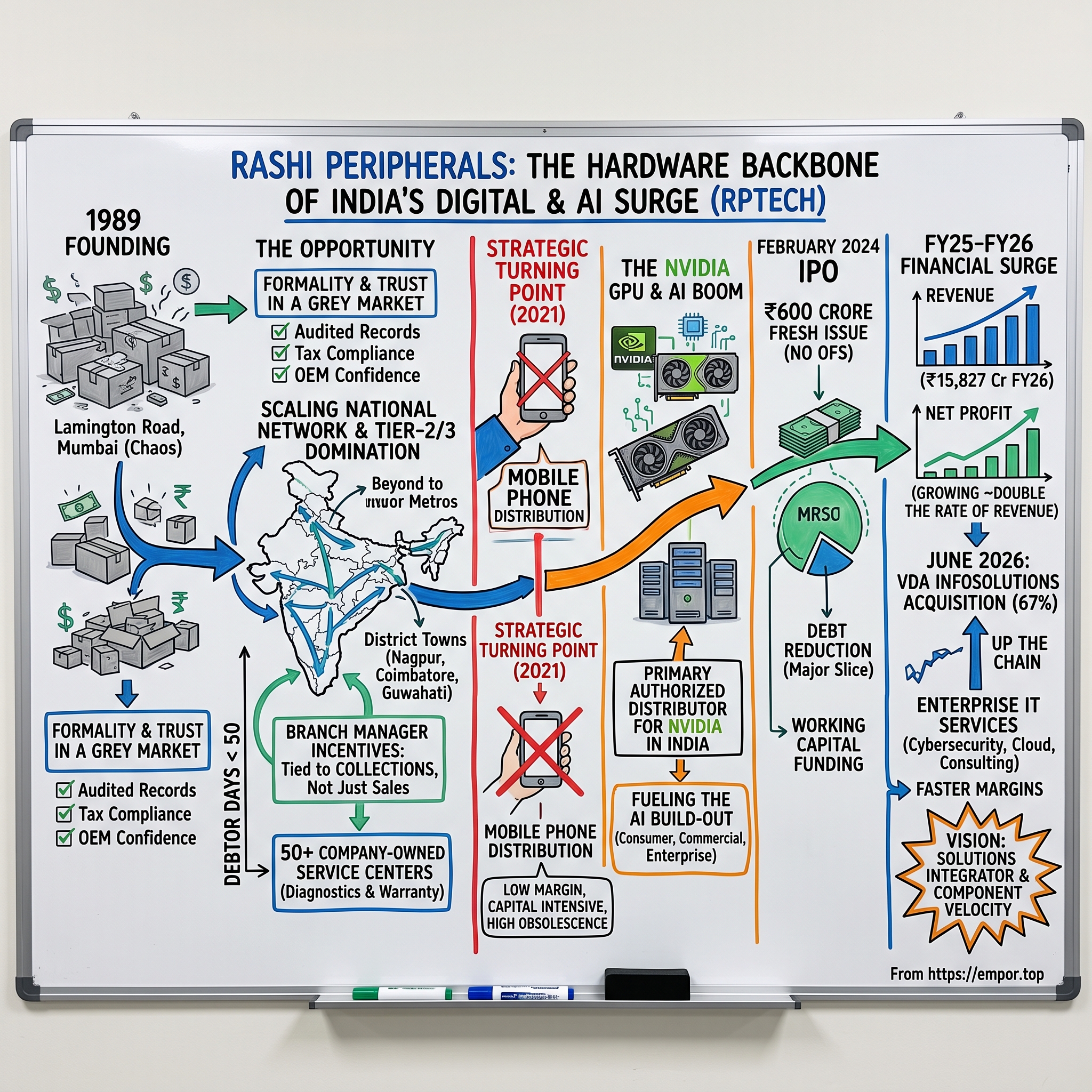

Picture a narrow lane in Mumbai's Lamington Road in the early 1990s — the beating, chaotic heart of India's electronics grey market. Shopkeepers hawk motherboards pulled from cardboard boxes with no warranty and no paperwork. Prices are scrawled on scraps of paper and change by the hour. Somewhere in that din, a memory chip that entered the country through a suitcase sits next to one that arrived through a customs bill, and to the buyer they look identical. This is the world into which Rashi Peripherals was born in 1989 — and the disorder of that world is precisely the thing the company would spend the next three and a half decades organizing, one invoice and one service center at a time.[^1]

Here is the puzzle worth sitting with. How does a small computer-component shop grow into a national technology distribution giant that, in the fiscal year ended March 2026, moved roughly ₹15,827 crore — nearly $1.9 billion — of hardware through the Indian channel?6 And how does it do that while earning a net profit margin that hovers below two percent — a razor-thin sliver that would make most business-school students recoil?6 The answer is that distribution is not really a margin business. It is a velocity business, a trust business, and above all a working-capital business. The company that manages cash conversion best, not the one that charges the most, tends to win.

Rashi Peripherals Limited trades on the NSE and BSE under the ticker RPTECH.4 It is, in its own description, a national ICT distributor partnering with more than 80 global technology brands — a roster that includes NVIDIA, Intel, AMD, HP, ASUS, Lenovo and dozens more — reaching more than 10,000 channel partners across hundreds of Indian towns and cities, and backed by a network of company-owned service centers that is unusual for the trade.[^1]1 Those are the company's figures, and we should treat them as claims to be examined rather than settled truths, but the shape of the business is clear: Rashi sits in the middle of the pipe that connects Silicon Valley's silicon to India's desktops, gaming rigs, offices and, increasingly, its data centers.

The thesis of this episode is not that Rashi is a great business — distribution rarely produces "great" businesses in the Buffett sense. The thesis is that Rashi is a revealing one. It is a case study in how you build durability in a structurally low-margin trade: through localized execution, disciplined product selection (including the counterintuitive decision to walk away from a huge revenue stream), and careful balance-sheet engineering. And it sits, almost by accident of its product mix, on top of two of the most powerful demand waves in modern computing — the enthusiast gaming boom and the enterprise AI build-out — because it happens to be NVIDIA's primary distribution partner in the world's most populous country.[^1]

Where we are headed over the next two and a half hours:

- The 1989 Mumbai founding and the grey-market chaos of India's PC revolution.

- The geographic masterstroke of bypassing the metros to dominate Tier-2 and Tier-3 India.

- The 2021 exit from mobile phone distribution, and the NVIDIA GPU and AI boom that followed.

- The February 2024 IPO and the balance-sheet re-engineering it funded.

- The June 2026 acquisition of VDA Infosolutions and the move up the value chain.

- Porter's Five Forces, Hamilton Helmer's Seven Powers, and an honest bull-versus-bear debate.

Let's begin where every distribution story begins — not with a product, but with a problem of trust.

II. Founding & Context: The Fragmented 1990s and the "PC DIY" Boom

To understand why two men decided to build a distribution company in 1989, you have to understand what a personal computer was in India at that moment: a luxury import, taxed to the sky, assembled by hand, and sold with a handshake you could not enforce. India had not yet had its 1991 moment — the balance-of-payments crisis that forced the country to dismantle the License Raj and open its economy. Import tariffs on finished electronics were punishing, foreign exchange was rationed, and the fastest way to get a graphics card or a hard disk was often to know a man who knew a man at the docks.

Into this world stepped Sureshkumar Pansari and Krishna Kumar Choudhary, who incorporated Rashi Peripherals in Mumbai in 1989.[^1] They were not building a brand consumers would recognize; they were building plumbing. The insight — and it is the founding insight of the entire company — was that the grey market's disorder was itself a business opportunity. When everything is informal, the party that chooses to be formal earns a scarce and valuable thing: the confidence of a global manufacturer who cannot otherwise trust anyone in the market.

Think about the problem from the point of view of an American or Taiwanese components maker in the mid-1990s eyeing India. The demand was obviously there — a middle class was forming, offices were computerizing, and the "assemble your own PC" culture was exploding because a locally built machine was far cheaper than an imported branded one. This was the DIY era, when a computer was a bag of parts — a motherboard, a processor, sticks of memory, a monitor, a floppy drive — sourced from different suppliers and screwed together on a shop counter. But how does a manufacturer collect payment, honor warranties, or protect its brand in a market where most sellers keep no books? The manufacturer needs a partner who pays taxes, holds inventory legitimately, keeps records, and can be audited. That partner becomes the authorized on-ramp to an entire country.

Rashi's early bet was to be exactly that partner: the organized, tax-compliant, white-market distributor in a grey-market trade. It is not a glamorous positioning. It is a credibility positioning, and credibility, once earned with a manufacturer, is sticky — because switching distributors means re-underwriting all that trust from scratch. Over the 1990s the company accumulated national distribution relationships with global names, laying down the physical logistics — warehouses, transport, credit lines to dealers — that would carry components from the ports to the shop counters of a rapidly modernizing country.[^1]

What should an investor take from the origin story? Two things. First, the company's core asset was never a product; it was a set of relationships and a reputation for straight dealing, both of which are real but also intangible and, crucially, non-exclusive — a manufacturer can appoint a second distributor tomorrow. Second, the business was born inside a specific structural gap in the Indian economy. As that gap narrowed — as the market formalized, GST arrived, and organized retail grew — the nature of Rashi's edge would have to evolve from "we are the legitimate ones" to "we are the most efficient and best-distributed ones." Holding that thought, let's watch how the company built the physical network that would become its most defensible advantage.

III. Scaling the National Network and Tier-2/3 Domination

Every distribution executive in India in the 2000s could recite the same conventional wisdom: the money is in the metros. Mumbai, Delhi, Bengaluru, Chennai — that is where the corporate buyers, the big system integrators, and the concentrated demand lived. The large players built their businesses around that gravity, and for good reason. It is operationally simpler to serve a hundred big accounts in six cities than ten thousand small dealers scattered across a subcontinent.

Rashi's most consequential structural decision was to zag where the industry zigged. Rather than crowd into the metros where the giants were strongest, the company pushed aggressively into Tier-2 and Tier-3 India — the district towns and smaller cities where a computer dealer in, say, Nagpur or Coimbatore or Guwahati struggled to get reliable supply, credit, and after-sales support from a distant metro warehouse. The result was a revenue mix weighted far more toward non-metro geographies than the industry norm, a deliberate inversion of the standard playbook.[^1] This is a form of what strategists call counter-positioning: the incumbents' entire cost structure and org chart were built for metro corporate sales, so matching Rashi's small-town, high-touch model would have meant partially cannibalizing their own approach.

But geography alone is not a strategy; it is a target. The engine that made the target reachable was organizational. Rashi built out a network of branches — more than fifty of them, reaching a fifty-second branch in Srinagar in FY25 — and ran them not as passive warehouses but as semi-independent profit-and-loss centers.3 This is the operational heart of the company, so it is worth slowing down on.

Consider the failure mode of a centralized distributor. Head office sets sales targets. Branch managers, paid mostly on volume, push product out the door to hit those targets — extending generous credit to dealers, letting inventory pile up in the channel, booking the "sale" the moment goods leave the warehouse. The revenue looks great until the dealer cannot sell through, cannot pay, and the receivable curdles into a bad debt. The industry has a name for this disease: channel stuffing. It is the single most common way distribution businesses destroy themselves.

Rashi's answer was to align the incentive with the risk. Branch managers' variable pay was tied not just to sales but to collections and local cash conversion — meaning a manager who shipped aggressively but could not collect saw it in their own compensation.[^1] Each branch functioned as a mini-warehouse and a local decision-maker, close enough to its dealers to judge who was good for the money and who was not. In a country where credit information on a small-town computer dealer is thin, that local knowledge is genuinely hard to replicate from a head office spreadsheet. It is also the mechanism behind one of the company's most-watched metrics: a debtor-days figure it has kept in the mid-40s, roughly 46 days in the first half of FY26, which is tight for a trade built on extending credit.8

The second pillar of the network was service. Traditional distributors move boxes and hand the warranty headache — the returns, the repairs, the RMA paperwork — back to the manufacturer or the end customer. Rashi instead built out more than fifty company-owned after-sales service centers, taking on diagnostics and warranty management itself.[^1]1 Why volunteer for that cost and complexity? Because it does two things at once. For the global brand, it means Rashi is not just a logistics vendor but the local face of the product, absorbing service infrastructure the manufacturer would otherwise have to build — which deepens the relationship. For the dealer, it means faster resolution and less friction, which earns loyalty. The service network converts a commodity function (moving boxes) into something closer to a relationship.

The honest counterpoint: none of this is a true moat in the economic sense. A competitor with enough capital could build branches and service centers too. What Rashi has is a lead — a decade-plus head start in specific towns, with specific dealers, and specific local managers — that is expensive and slow, though not impossible, to catch. For investors, the network is best understood as a durable operating advantage rather than an unbreachable wall, and its value shows up in the working-capital metrics more than in the margin line. With the rails built, the next question was what to run over them — and here the company made a decision that defined the modern business.

IV. Strategic Turning Point: Exiting Mobility (2021) & The NVIDIA GPU/AI Boom

Every distributor faces the same seductive temptation, and it is the temptation of the big number. Somewhere around the late 2010s, the biggest number in Indian technology distribution was the smartphone. Phones were selling by the tens of millions; the revenue you could book by distributing them was enormous. The nearest large comparable to Rashi, Redington, grew into a multi-billion-dollar giant partly on the back of mobile distribution, including marquee brands. If you measured success by revenue, mobile was the obvious place to be.

Rashi looked at that big number and, in 2021, walked away from it.[^1] The company exited mobile phone distribution — a deliberate decision to shrink a revenue line that many peers were racing to grow. To appreciate how counterintuitive that is, you have to understand the economics of a smartphone in the channel. Margins on phone distribution are brutally thin, often thinner than on IT components. Prices fall almost the moment a model launches, which means inventory you are holding is a depreciating asset measured in weeks. And the working capital required to hold and finance that fast-moving, fast-depreciating stock is immense. In other words, smartphones consume a great deal of a distributor's most precious resource — cash tied up in inventory and receivables — in exchange for very little profit and considerable obsolescence risk.

The strategic logic was capital reallocation. By exiting mobile, Rashi freed up working capital and management attention to concentrate on higher-value IT components and enthusiast hardware — categories with better margins, more durable pricing, and, as it turned out, a demand tailwind that was about to become a gale. This is the "anti-conglomerate" instinct: the discipline to judge a business not by the revenue it generates but by the return it earns on the capital it consumes. Whether it proves to be the right call over a full cycle is something an investor should keep testing, but the reasoning is coherent and, importantly, consistent with how management says it thinks about the business.

Which brings us to the graphics card. To a non-technical listener, a GPU — a graphics processing unit — began life as the chip that draws the images in a video game. NVIDIA's GeForce cards became the object of desire for a generation of Indian gamers and content creators, and Rashi became NVIDIA's primary authorized consumer and enterprise distributor in India — the channel through which those cards reach the market.[^1] The company describes commanding a dominant share of the organized Indian channel in graphics cards and a similarly high share in CPUs from Intel and AMD.[^1] Treat the precise share figures as management's characterization rather than an audited fact, but the direction is not in dispute: Rashi is the primary organized pipe for the components that enthusiasts crave.

Here is where the story gets interesting, because the very same chip architecture that draws a dragon in a video game turns out to be extraordinarily good at the mathematics behind artificial intelligence. A GPU is, at heart, a machine for doing thousands of simple calculations in parallel — and training and running an AI model is essentially thousands of simple calculations in parallel. That coincidence transformed NVIDIA from a gaming company into the arms dealer of the AI era, and it transformed Rashi's position from "the company that supplies gamers" into "the company that could supply India's AI build-out." On its FY26 earnings call, management leaned into exactly this framing, positioning Rashi as an AI solutions provider across consumer, commercial, and enterprise segments and pointing to demand in components and storage as growth drivers.6

The prize, if it materializes, is enterprise AI hardware — the servers, accelerated-computing systems, and data-center gear that Indian companies and cloud providers will need as they build AI capability. The margins there can be richer than in consumer components, and the logistics and financing complexity is exactly the kind of thing a distributor with a national footprint and a strong balance sheet can provide. But the skeptic should note two things. First, this is still a distribution opportunity — Rashi carries and moves the hardware; it does not own the intellectual property that makes it valuable. Second, its position rests heavily on a single supplier relationship. If NVIDIA reorganizes its Indian channel, the same concentration that is a tailwind today becomes a risk tomorrow. That tension between opportunity and dependence runs through the rest of this story. First, though, the company had to fix its balance sheet — and for that, it went public.

V. The IPO (Feb 2024) and Balance Sheet Re-engineering

An IPO is a mirror. It forces a private, founder-run company to explain itself to strangers, submit to disclosure, and — most revealingly — decide who gets the money. On that last question, Rashi's February 2024 offering told you something important about the founders before you read a single financial statement.

The company opened its public offering in early February 2024 and listed on the NSE and BSE on February 14, 2024.4 The structure was the tell. The roughly ₹600 crore raised was entirely a fresh issue of new shares — with no offer-for-sale component, meaning the promoters sold none of their own stock and took no money off the table.[^1] Every rupee raised flowed into the company itself rather than into founders' pockets. In a market where plenty of IPOs are exit vehicles dressed up as growth stories — existing owners cashing out while retail investors buy in at the top — a zero-OFS structure is a signal of alignment. The founders were putting the proceeds to work in the business they continued to own, not selling into the enthusiasm.

Where did the money go? Overwhelmingly, to fixing the liability side of the balance sheet. Of the net proceeds, the largest slice — a little over ₹320 crore — was earmarked to prepay or repay outstanding borrowings, with a further roughly ₹220 crore directed to funding working capital and the balance to general corporate purposes.[^1] To understand why paying down debt matters so much for a business like this, return to the core economics. A distributor lives on borrowed working capital: it buys inventory and extends credit to dealers, financing the gap with short-term debt, and it pays interest on that debt every single day. In a sub-2% net-margin business, interest expense is not a footnote — it is one of the largest forces standing between gross profit and net profit. Cut the debt, and you cut the interest drag; cut the interest drag, and more of each thin margin survives to the bottom line.

The effect on the company's financial durability was structural rather than cosmetic. Post-IPO, the balance sheet was materially de-levered, interest coverage improved, and net debt relative to equity fell to a conservative level before rising modestly again in FY25 as the company funded rapid growth.[^1]2 That last detail is worth dwelling on, because it captures the permanent tension of the business: de-leveraging buys you a cleaner balance sheet, but growth in a working-capital-hungry trade re-consumes that headroom. Every incremental rupee of revenue requires incremental inventory and receivables, which require incremental financing. The IPO did not solve that treadmill — nothing does — but it reset the company's starting position on it, giving Rashi the balance-sheet room to absorb a growth surge without immediately drowning in finance costs.

For investors, the IPO reads as a credibility-building exercise as much as a fundraising one. The signals — fresh issue only, proceeds to debt reduction and working capital, no founder cash-out — are the signals of owners behaving like owners. That does not guarantee good outcomes; alignment is necessary, not sufficient. But it earns management the benefit of the doubt going into the period that would test them: a two-year stretch in which revenue climbed sharply and the company made its boldest strategic move yet. That is where we turn next.

VI. The FY25-FY26 Financial Surge & The VDA Infosolutions Acquisition

Numbers can either illuminate a business or bury it, so let's take the recent financial history slowly and translate as we go, because the trajectory tells a genuine story about operating leverage in a thin-margin trade.

Start with the top line, which grew in a way that would flatter almost any company. Revenue rose from roughly ₹11,095 crore in FY24 to about ₹13,773 crore in FY25 — a jump of around 24% — and then to approximately ₹15,827 crore in FY26, another mid-teens gain.36 Growth of that pace over two years, in a mature-sounding business like hardware distribution, is not what you would naively expect. It reflects the demand tailwinds we have discussed — components, storage, the GPU cycle, Tier-2 channel stocking — and it reflects share gains in the organized channel.6

Now watch what happens beneath the top line, because this is where the operating leverage lives. In FY25, revenue grew about 24% but net profit grew roughly 46%, rising to around ₹210 crore from about ₹144 crore the year before.3 Profit growing at roughly double the rate of revenue is the signature of a business with high fixed-ish costs and thin margins: once you cover the cost of the network and the interest bill, incremental gross profit falls disproportionately to the bottom line. The pattern repeated into FY26, where the company reported net profit rising by roughly a third even as margins stayed in their familiar band, and the fourth quarter was especially strong, with revenue up around 51% and profit up around 65% year on year.56 The net margin itself barely moved — from roughly 1.3% in FY24 to somewhere in the 1.5–1.8% range more recently — which is the whole point about distribution: you do not win by expanding margins, you win by growing volume while holding margins and, above all, controlling the cash cycle.26

The revenue splits across two reported segments. Personal Computing and Enterprise Solutions (PES) — the larger share, around 58% of revenue — covers laptops, servers, enterprise hardware, and cloud infrastructure. Lifestyle and IT Essentials (LIT) — roughly the remaining 42% — houses the higher-excitement categories: GPUs, CPUs, motherboards, storage, networking, and gaming accessories.6 The distinction matters because it maps onto two different demand drivers — enterprise IT refresh cycles on one side, enthusiast and consumer upgrade cycles on the other — which do not always move together, giving the company a measure of diversification within a single trade.

Then came the move that reframed the whole investment case. On June 23, 2026, Rashi announced it had entered agreements to acquire a 67% controlling stake in VDA Infosolutions, a Mumbai-based enterprise IT solutions company founded in 2010, for ₹368.5 crore in cash, with the remaining 33% to be bought in three equal annual tranches through August 2029, implying a total enterprise valuation in the region of ₹550 crore.[^8] Structurally, this echoes the IPO discipline: a staggered acquisition that keeps the founders of VDA invested and incentivized through the transition, spreads the cash outflow over years, and reduces the shock of integration. Notably, the company disclosed the deal was not with a related party — a clean-governance detail that matters in a founder-controlled Indian firm.[^8]

Why VDA, and why does it change the story? VDA is not a box-mover; it specializes in the higher-value end of enterprise technology — cybersecurity, cloud infrastructure, virtualization, data protection, and IT consulting and services.[^8] Those are businesses that earn meaningfully fatter margins than hardware distribution, because they sell expertise and integration rather than shipping product. VDA was projected to post a turnover of roughly ₹850 crore in FY26 with a net worth above ₹230 crore.[^8] If, as reported, its profitability runs in the mid-single-digit-percent range on that revenue, VDA earns several times the net margin that Rashi's core distribution business does. Buying control of it is, in effect, buying a on-ramp into higher-margin systems integration and grafting it onto Rashi's much larger distribution trunk.

Is the price sensible? On the reported figures — roughly ₹550 crore of total value against ₹850 crore of turnover — Rashi paid well under one times sales, a modest multiple for a services business growing into an AI-driven IT-spending wave, and an earnings multiple in the mid-teens depending on where VDA's profit actually lands.[^8]7 For context, Rashi's own shares traded around an 18x earnings multiple in mid-2026 on a market capitalization in the vicinity of ₹5,000 crore, which means, at least on a headline basis, the acquisition was struck at a valuation broadly in line with or below Rashi's own — a transaction that is not obviously dilutive and could be accretive if the integration works.7 The prudent caveat is that VDA's FY26 numbers were provisional and unaudited when the deal was struck, and services acquisitions live or die on the retention of people and clients, not on the spreadsheet. The strategic direction, though, is unambiguous: Rashi is trying to climb from the low-margin floor of physical distribution toward the higher-margin ceiling of enterprise IT services, precisely as Indian corporates start spending on AI-ready infrastructure. Whether that climb succeeds is the central open question of the investment — and to frame it properly, we need to war-game the competitive landscape.

VII. Porter's Five Forces & Hamilton Helmer's Seven Powers

Strip away the AI excitement and the growth headlines, and you are left with a deceptively simple question: what, if anything, protects this business from being competed into oblivion? Distribution is the classic middleman trade, and middlemen are forever at risk of being squeezed from both sides. Let's run Rashi through two frameworks — Helmer's Seven Powers and Porter's Five Forces — and be honest about where the advantages are real and where they are thin.

Hamilton Helmer's Seven Powers. Of Helmer's seven, three are worth taking seriously for Rashi, and it is telling that none of them is airtight.

Scale economies are the strongest. A national footprint of dozens of branches, warehouses, and service centers, combined with high procurement volumes across 80-plus brands, gives Rashi purchasing terms, logistics density, and fixed-cost absorption that a regional or sub-scale competitor genuinely cannot match.[^1]1 In a business where you win on cost-to-serve and cash efficiency rather than price, scale is the advantage that most directly translates into survival. The limit is that Rashi is not the only company at scale — Redington and Ingram Micro are as large or larger — so scale here is a barrier against the small, not against the giants.

Switching costs are real but moderate. For a small-town dealer or a corporate system integrator, Rashi is embedded in daily operations through the credit it extends, the local inventory it holds, and the service it provides. Ripping that out and rebuilding it around another distributor is friction-heavy. But it is operational switching cost, not contractual lock-in — and a dealer can, and often does, buy from more than one distributor at once, which caps the power.

Counter-positioning is the most interesting. Rashi's decentralized, collections-linked, Tier-2/3-oriented model is genuinely awkward for a metro-centric incumbent to imitate without disrupting its own structure and incentives. That is a real edge in the specific geographies where Rashi is entrenched. But it is a regional advantage, not a national one, and it erodes as the whole market formalizes.

Notably absent from Rashi's arsenal are the powers that produce truly great businesses: it has no network economies, no meaningful brand pricing power (it sells other companies' brands), no cornered resource beyond revocable distribution agreements, and no proprietary process that rivals cannot learn. That absence is not a knock on management; it is the nature of the trade. It is also the reason the VDA move matters — services can generate switching costs and expertise-based advantages that pure distribution cannot.

Porter's Five Forces. The five forces sharpen the picture and explain why margins sit where they do.

Bargaining power of suppliers is very high. The global OEMs — NVIDIA, Intel, AMD, HP and the rest — set the prices, control the allocations of scarce product, and dictate the gross margin available to the channel.[^1] When a supplier is this powerful, the distributor is a price-taker on the most important variable in its business. This is the single biggest structural constraint on Rashi.

Bargaining power of buyers is medium-high. Channel partners can and do cross-shop between Rashi, Redington, and Savex Technologies, which keeps a lid on the markups Rashi can charge. The offset is the service network and local availability, which reduce the temptation to churn over a fractional price difference — but they do not eliminate it.

Threat of new entrants is very low. This is Rashi's best-defended flank. To enter national ICT distribution you need enormous working capital, the credit-risk machinery to manage thousands of dealers, a warehousing footprint spanning the country, and — hardest of all — authorized-distributor agreements from OEMs who have little reason to appoint an untested newcomer. Those requirements are a formidable barrier.

Threat of substitutes is low but non-zero. The cloud is the substitute to watch: as computing shifts to hyperscale data centers, some on-premise hardware demand evaporates. But cloud infrastructure is itself built from physical servers, GPUs, and networking gear that someone must distribute, and endpoints — laptops, components, edge devices — still need to be physically moved. The substitution reshapes demand more than it destroys it.

Competitive rivalry is high. Rashi, Redington, Ingram Micro, and Savex compete hard on price and terms, which is exactly why EBIT margins across the industry are pinned in a narrow band of roughly 2.5–3.5% and why net margins are thinner still.2 Nobody in this trade escapes the gravity of low pricing power.

Put the two frameworks together and the verdict is measured, not triumphant. Rashi has durable operating advantages — scale, entrenchment, service — that make it hard to dislodge in its niches, sitting inside an industry structure that permanently caps profitability. That is a business that can compound through volume and capital discipline, not one that will earn abnormal margins. Which is why who is running it, and how they behave with capital, matters enormously — and that is where we go next.

VIII. Current Management, Governance, and Localized Incentives

There is a moment in the life of every founder-built company when the question shifts from "can they build it?" to "can the next generation run it?" For Rashi, the person carrying that question is Kapal Suresh Pansari, the managing director and the second-generation leader who has become the operational architect of the modern company.

Kapal Pansari's fingerprints are on the three defining moves of the past half-decade: the 2021 decision to exit mobile distribution, the February 2024 IPO, and the June 2026 VDA acquisition.[^1][^8] Read as a sequence, those three moves share a common signature — a willingness to trade the comfort of a big revenue number for the discipline of better returns and a cleaner balance sheet. Exiting mobile shrank the top line to protect capital efficiency. The IPO raised money without the founders selling a share. The acquisition reached for margin rather than volume. Whether or not each proves correct, they are internally consistent, and consistency of strategy across years is one of the more reliable signals of a management team that actually has a philosophy rather than a series of reactions. On the FY25 call, the company also pointed to unglamorous execution details — a fifty-second branch opened in Srinagar, a CRM rollout to hundreds of users, entries into adjacent verticals like surveillance and quick-commerce fulfillment — the kind of operational granularity that suggests attention to the machine, not just the strategy.3

On governance, the headline number is promoter shareholding, reported around 64% as of early 2026, with — importantly — no promoter shares pledged.10 Both details matter for a minority investor. High promoter ownership means the founding family's wealth rises and falls with the same share price the public holds, which aligns incentives; the absence of share pledging means the promoters have not borrowed against their stake, removing a common source of hidden fragility in Indian family-controlled companies, where a falling stock can trigger forced selling by lenders. Combined with the zero-OFS IPO, the governance signals point in a consistent direction: owners who are staying in, not cashing out.

The skeptic's checklist should still be run, because founder control cuts both ways. High promoter ownership also concentrates decision-making power, limits the influence of minority shareholders, and makes related-party dealings a standing area to watch — which is exactly why the explicit disclosure that the VDA deal was not a related-party transaction is reassuring rather than incidental.[^8] An activist investor's questions here would be about capital allocation discipline as the company grows more acquisitive, board independence, and whether the family's control is exercised in the interest of all shareholders. Nothing in the record so far suggests it is not; the point is that these are the right questions to keep asking, not that there are red flags today.

The deepest governance feature, though, is not at the top of the org chart — it is at the branch level, in the incentive design we met earlier. Tying local managers' variable pay to collections and cash conversion rather than pure sales is, in effect, a governance mechanism embedded in the operating model. It pushes credit discipline down to the people closest to the customer, where the information is best, and it structurally discourages the channel-stuffing that wrecks distributors. The proof shows up in the numbers management is willing to be judged on: debtor days held around the mid-40s even while the company grew at a rapid clip and competed in a cut-throat market.8 That is the sort of result that is hard to fake over multiple years, and it is the strongest available evidence that the incentive system does what management says it does. With the people and the machine understood, we can finally weigh the case for and against the stock.

IX. The Investment-Story Spine: Bull vs. Bear Case

Here is where we war-game the whole thing — not to reach a verdict, but to lay both cases out honestly and identify what evidence would settle the argument in either direction.

The Bull Case: The High-Performance Computing Engine

The bull case rests on Rashi sitting at the confluence of three forces, each of which independently supports the story.

First, the AI and GPU supercycle. As NVIDIA's primary Indian distribution partner, Rashi is a toll booth on the road that AI and high-performance computing hardware travels to reach Indian buyers — from GeForce cards in gaming rigs to accelerated-computing systems in enterprise data centers.[^1] If Indian AI infrastructure spending inflects the way management and the broader market anticipate, Rashi does not need to invent anything or take technology risk; it simply needs to keep moving the hardware and financing the channel, which is exactly what it is built to do. The demand it has already seen in components and storage is early evidence that the wave is real, not merely hoped for.6

Second, margin accretion through the value chain. The VDA acquisition is the mechanism by which Rashi tries to escape the gravity of sub-2% distribution margins. Folding a cybersecurity, cloud, and integration business earning mid-single-digit margins into the enterprise segment lifts the blended profitability of the whole and, more importantly, changes what kind of company Rashi is — from a pure logistics provider toward a solutions integrator.[^8] If the integration works, the re-rating potential is not just about more profit; it is about a market willing to pay a higher multiple for a higher-quality earnings stream.

Third, capital efficiency and operating leverage. The de-leveraging funded by the IPO, combined with the structural operating leverage we saw in FY25 and FY26 — profit growing at roughly double the pace of revenue — is the engine pushing return on equity upward from the low-teens toward management's stated ambition of 15%-plus.[^1]2 In a thin-margin business, ROE is the truest scorecard, because it captures whether the company is generating real returns on the mountain of working capital it deploys.

The Bear Case: The Working Capital Trap

The bear case does not require anything to go dramatically wrong. It only requires the business to be what it structurally is.

First, the working-capital bleed. Growth in this trade is not free — it is the most expensive thing the company does. Every 15–20% of additional revenue demands a proportional slug of additional inventory and receivables, funded by short-term borrowing. If the cash conversion cycle — around 61 days recently — drifts wider, Rashi must borrow more, and finance costs eat directly into the thin profit. The FY26 finance bill running to tens of crores over nine months is a reminder that interest is a first-order expense here, not a rounding error.8 The cruel irony of the model is that success (growth) intensifies the very cash strain that most threatens it.

Second, supplier concentration. The flip side of the NVIDIA and Intel relationships that power the bull case is dependence on a handful of OEMs who hold the whip hand on pricing and allocation.[^1] If a major supplier renegotiated terms, appointed an additional national distributor to sit alongside Rashi, or pushed more corporate volume through direct channels, Rashi's economics would take an immediate hit it could do little to prevent. Concentration is a tailwind until the day it becomes a single point of failure.

Third, the structural margin ceiling. At its core, Rashi remains a price-taking distributor with limited pricing power, exposed to freight-cost inflation, currency swings on imported goods, and the demand cyclicality of PCs and components. The VDA move is precisely an attempt to raise that ceiling — but VDA is small relative to the distribution trunk, and it will be years before services materially change the blended margin, if they ever do. Until then, the ceiling is the ceiling.

The activist's stress test ties the two cases together: a skeptic would press on whether the company can keep the cash cycle disciplined while growing rapidly and integrating acquisitions, whether the NVIDIA dependence is being diversified, and whether an increasingly acquisitive posture stays as disciplined as the debut deal appeared to be. Those are the fault lines along which the story will be won or lost. Which points us to the handful of numbers that will actually tell us which way it is breaking.

X. Epilogue, Playbook Lessons, and Key KPIs

Step back from the details and Rashi's story resolves into a set of playbook lessons that generalize well beyond Indian technology distribution.

The first is the anti-conglomerate pivot — the discipline to walk away from a large but value-destructive revenue stream. The 2021 mobile exit is the cleanest example: it took conviction to shrink the top line in service of return on capital, in defiance of the industry's instinct that bigger revenue is always better.[^1] The lesson is that in a working-capital-intensive business, the revenue you decline can matter as much as the revenue you win, because bad revenue does not just earn thin margins — it consumes the cash that good revenue needs.

The second is aligning incentives with risk. By paying branch managers on collections and cash conversion rather than sales alone, Rashi pushed accountability to the point of best information and inoculated itself against the channel-stuffing that hollows out so many distributors.[^1] The generalizable insight: incentive design is risk management. In any business where local actors control credit and inventory, the compensation formula is a governance decision.

The third is strategic M&A done with discipline. The staggered VDA structure — 67% upfront, the rest over three years, at a modest multiple, with founders kept invested — is a template for buying capability without buying integration risk all at once.[^8] It is the same temperament visible in the zero-OFS IPO: a preference for moves that build the business and align interests over moves that maximize a near-term number.

None of this makes Rashi a sure thing. It remains a thin-margin, supplier-dependent, cyclically exposed distributor whose best structural advantages are durable operating leads rather than unbreachable moats. What it has going for it is a coherent strategy, an aligned and disciplined ownership group, and a fortunate seat on top of the two demand waves — enthusiast computing and enterprise AI — that will define the next decade of hardware. Whether it converts that seat into durable, higher-quality earnings is the open question the VDA acquisition was designed to answer.

For an investor tracking this company over time, three KPIs cut through the noise:

1. The cash conversion cycle (working-capital days). This is the master metric of the entire investment. As long as it stays disciplined — in the neighborhood of the mid-to-high 50s — growth is being funded efficiently and the balance sheet is healthy. If it drifts wider, it is the earliest warning that growth is turning into a debt-and-interest problem, and everything else in the story bends around it.

2. Blended segment margins, especially the enterprise/VDA mix. The whole bull case for a re-rating hinges on Rashi moving up the value chain. Watching whether the combined enterprise-plus-services margin actually rises — and whether VDA grows and retains its profitability inside Rashi — is how you verify the "escaping the margin floor" thesis with evidence rather than hope.

3. Revenue growth versus the market. In a scale-economies business, volume is not vanity — it is the source of purchasing power and supplier standing. Sustained mid-teens-plus growth that outpaces the broader ICT channel confirms Rashi is gaining share and feeding the flywheel; a slowdown toward market rates would suggest the operating edge is narrowing.6

Track those three, and you will know how the bull-versus-bear debate is actually resolving, long before it shows up in the headline profit figure.

XI. Outro

Rashi Peripherals began as an attempt to bring order to a chaotic grey market, and in a sense that remains its entire enterprise — imposing organization, credit discipline, and service on the messy business of getting hardware from the world's chip makers to India's dealers, offices, and data centers. It has done so without the luxury of pricing power, on margins so thin that the discipline itself becomes the product. Now it is reaching for something harder: to climb from the floor of commodity distribution toward the higher ground of enterprise solutions, just as India's AI build-out gathers pace. The rails are laid, the balance sheet is cleaner than it has ever been, and the founders' money is still on the table. What remains unproven is whether a middleman, however well run, can turn a fortunate position at the center of a supercycle into something more durable than volume. That is the story still being written — and the working-capital line, quarter by quarter, will narrate it.

References

-

Rashi Peripherals Ltd — Financials, Ratios & Consolidated Data, Screener.in ↩↩↩↩

-

Rashi Peripherals Limited — Q4 & FY25 Investor Presentation and Results, 2025-05-28 ↩↩↩↩

-

Company Page & Filing Archive: Rashi Peripherals Ltd (544119) — BSE India ↩↩

-

Rashi Peripherals Limited — Q4 FY26 and FY26 Earnings Release, 2026-05-25 ↩

-

Rashi Peripherals Reports Strong FY26 Revenue of INR 158,273 Mn as Q4 Revenue Jumps 51% YoY — Digital Terminal, 2026-05 ↩↩↩↩↩↩↩↩↩↩

-

Rashi Peripherals Ltd — Stock Quote & Valuation, Moneycontrol ↩↩

-

Rashi Peripherals Limited — 9M FY26 Financial Statement and Investor Update, 2026-02-12 ↩↩↩

-

Company Profile & Stock Tracker: Rashi Peripherals Limited (RPTECH) — NSE India ↩

-

Rashi Peripherals Limited — Annual Report 2024-2025, 2025-08-15 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube