Ramkrishna Forgings: The Forging Dynasty That Conquered Global Auto Supply Chains

I. Introduction & Cold Open

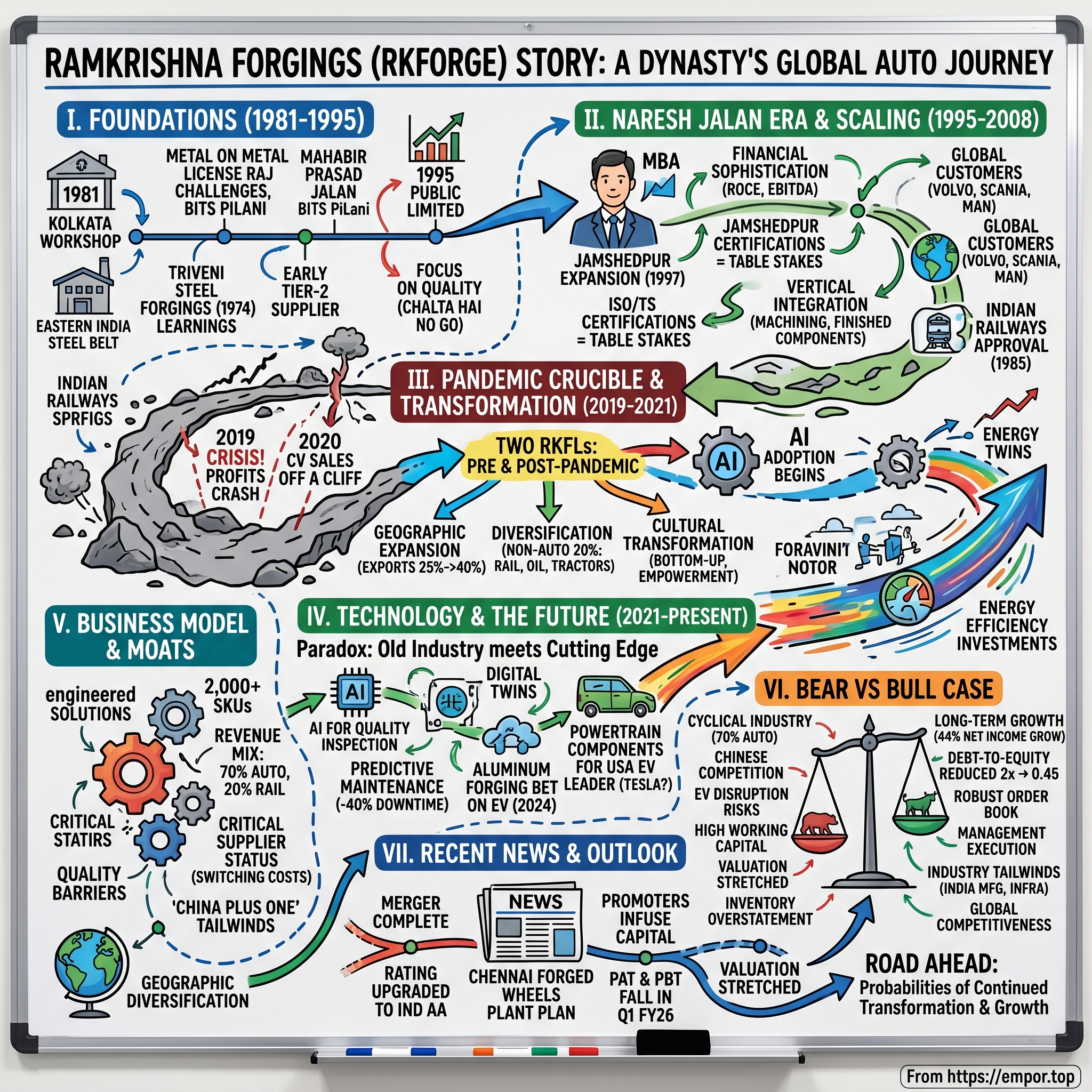

Picture this: A small forging workshop in Kolkata, 1981. The clang of metal on metal echoes through the humid air as workers shape hot steel into automotive components. Fast forward four decades—that workshop has transformed into a ₹10,000+ crore market cap powerhouse, supplying critical safety components to Mercedes, Volvo, and Scania across four continents. This is the story of Ramkrishna Forgings Limited, India's second-largest forging company, and how the Jalan family built an industrial empire that would become indispensable to the global automotive supply chain.

Today, RKFORGE generates over ₹4,000 crore in annual revenue, operates massive facilities across India, and exports 40% of its production to Europe, North America, and Asia. But the real story isn't just about scale—it's about survival, transformation, and the audacious bet that a traditional Indian manufacturing company could compete with global giants on quality, not just cost.

The forging industry is unsexy. It's hot, heavy, and hidden—most people never think about the critical components that connect their car's engine to its wheels, or the massive forgings that keep railway bogies from catastrophic failure. Yet these invisible parts are the backbone of modern transportation. And in this overlooked corner of manufacturing, Ramkrishna Forgings has quietly built one of India's most remarkable industrial success stories.

What makes this tale particularly compelling is timing. As global supply chains fracture and reorganize post-COVID, as the auto industry undergoes its greatest transformation in a century with electrification, and as India positions itself as the "China Plus One" manufacturing alternative, RKFORGE sits at the intersection of multiple secular trends. The question isn't whether they rode these waves—it's how they positioned themselves to catch them in the first place.

This is a story in three acts: First, the foundation years under patriarch Mahabir Prasad Jalan, who built credibility in India's License Raj era. Second, the aggressive expansion under his son Naresh, who transformed a domestic supplier into a global player. And third, the pandemic crucible that nearly broke the company but ultimately forged (pun intended) a leaner, technology-driven enterprise ready for the next phase of growth.

Along the way, we'll explore how a company from Kolkata convinced German automotive engineers to trust them with safety-critical components, why they chose to vertically integrate when competitors stayed asset-light, and how artificial intelligence is transforming one of humanity's oldest manufacturing processes. We'll also examine the bear case—because in cyclical industries with Chinese competition and EV disruption, nothing is guaranteed.

II. Origins & The Jalan Family Story (1981-1995)

The year was 1981, and India was a different country. Indira Gandhi was Prime Minister, the economy was shackled by the License Raj, and getting permission to expand manufacturing capacity required navigating byzantine bureaucracy. It was in this environment that Mahabir Prasad Jalan, a mechanical engineer from the prestigious Birla Institute of Technology and Science (BITS) Pilani, decided to start Ramkrishna Forgings.

But Mahabir wasn't a starry-eyed entrepreneur. With over 45 years of experience in the forging industry, he had already tasted both success and the harsh realities of Indian manufacturing. Seven years earlier, in 1974, he had founded Tribeni Steel Forgings, learning firsthand the challenges of building a forging business in socialist India. That venture served as his training ground—teaching him about metal properties, customer relationships, and most importantly, the critical importance of quality in an industry where component failure could mean catastrophic accidents. On November 12, 1981, Ramkrishna Forgings was incorporated as a Private Limited Company, founded on what Mahabir would later describe as "a bed of integrity, fuelled by burning ambition". The name itself—Ramkrishna—reflected the deep spiritual roots that would guide the company's ethical framework, even as it operated in an industry notorious for kickbacks and quality compromises.

The timing was both terrible and perfect. Terrible because India's economy was growing at the "Hindu rate of growth"—a measly 3.5% annually. Perfect because the commercial vehicle industry was about to explode as India slowly liberalized its economy. Every truck, bus, and tractor needed forgings—connecting rods, crankshafts, steering knuckles, axle beams. These weren't glamorous products, but they were essential. And in a country where overloaded trucks routinely plied potholed roads, quality literally meant the difference between life and death.

Mahabir's earlier venture, Tribeni Steel Forgings founded in 1974, served as his training ground before he launched Ramkrishna Forgings in 1981. This wasn't a Silicon Valley-style pivot—it was methodical empire building. Through Tribeni, Mahabir had built relationships with Tata Motors and Ashok Leyland, India's commercial vehicle giants. He understood their quality requirements, their payment cycles, and most importantly, their growth ambitions.

The early years were about survival and credibility. Operating from Kolkata—far from India's automotive hubs in Chennai and Pune—Ramkrishna had geographic disadvantages. But Mahabir turned this into a strength. Lower land costs meant better margins. Proximity to Eastern India's steel belt meant raw material advantages. And being away from competitors meant less poaching of skilled workers.

By the late 1980s, Ramkrishna had established itself as a reliable tier-2 supplier. Not the biggest, not the most advanced, but dependable. In an era when Indian manufacturing was synonymous with "chalta hai" (it'll do) mediocrity, Mahabir insisted on quality that matched global standards. This obsession would pay dividends when India opened its economy in 1991.

The watershed moment came in May 25, 1995, when the company converted into a Public Limited Company. This wasn't just about raising capital—it was a statement of intent. The Jalan family was ready to play on a bigger stage. And crucially, this was when the second generation entered the picture.

III. The Naresh Jalan Era Begins (1995-2008)

Naresh Jalan took an active plunge into Ramkrishna Forgings Limited in 1995, bringing an MBA in Finance and Marketing to complement his father's engineering background. This wasn't your typical second-generation story of reluctant succession. Naresh had spent years preparing for this moment, understanding that Indian manufacturing was at an inflection point.

The contrast between father and son was striking. Where Mahabir was the quintessential engineer—methodical, quality-obsessed, conservative—Naresh brought financial sophistication and marketing savvy. He spoke the language of return on capital employed (ROCE) and earnings before interest, taxes, depreciation, and amortization (EBITDA) at a time when most Indian forging companies still thought in terms of tonnage and production volumes.

His dynamic leadership saw RKFL invest significantly in state-of-the-art facilities employing best-in-class technologies, expanding the range of products both in size and criticality. But this wasn't blind expansion. Naresh understood that the global auto industry was consolidating, and suppliers needed scale to survive.

The late 1990s and early 2000s were transformative for Indian automotive. Global OEMs were setting up shop—Hyundai in Chennai, Honda in Greater Noida, Volkswagen scouting locations. Each brought their tier-1 suppliers, but they all needed local tier-2 and tier-3 vendors for cost competitiveness. Naresh positioned Ramkrishna perfectly for this opportunity. The Jamshedpur decision was pivotal. In 1997, the company undertook major expansion, whereby they increased their forging & die making capacity at Jamshedpur. Why Jamshedpur? It wasn't just about proximity to Tata Steel's raw materials. Jamshedpur represented India's manufacturing heritage—a city built by the Tatas where industrial discipline was embedded in the culture. Here, Naresh could find the skilled workers and engineering talent needed for his ambitious plans.

But expansion required more than just capacity. The global auto industry demanded certifications—ISO/TS 16949 for automotive, API for oil and gas, AAR M-1003 for railways. Each certification was a months-long process of documentation, process improvement, and audits. Naresh drove these initiatives personally, understanding that certifications were table stakes for global business.

They purchased a unit at Liluah Industrial Area, Howrah, which had a machine shop for the rough machining of components. During the year 2004-05, the company installed two double acting ram type drop hammers of 6 ton and 3 ton capacity. This wasn't random expansion—it was strategic vertical integration. By adding machining capabilities to their forging operations, Ramkrishna could supply finished components rather than just raw forgings, capturing more value and building switching costs.

The customer acquisition story during this period reads like a who's who of global automotive. Volvo, Iveco, Scania, MAN, UD Trucks—each win represented months of supplier audits, sample approvals, and price negotiations. But here's what's remarkable: Ramkrishna wasn't winning on price alone. They were competing on quality and reliability against established suppliers like Bharat Forge, which had a decades-long head start.

In 1985, they were approved by Indian Railways (RDSO) as a Critical Safety item Supplier for items like Hanger for Bolster suspension, Screw Coupling, Draw Gear Arrangement for passenger coach application. This early railway certification would prove prescient—it opened up a non-automotive revenue stream that would provide stability during auto industry downturns.

By 2008, Naresh had transformed his father's reliable tier-2 supplier into something more ambitious—a company ready to compete globally. Revenue had grown from tens of crores to hundreds of crores. The company had moved from simple drop forgings to complex machined components. Most importantly, they had built credibility with global OEMs who were notoriously reluctant to trust new suppliers with safety-critical parts.

IV. Scaling Up & Going Global (2008-2019)

The 2008 global financial crisis should have been a disaster for Ramkrishna Forgings. Auto sales crashed worldwide, credit markets froze, and suppliers went bankrupt by the dozens. But Naresh Jalan saw opportunity where others saw catastrophe. "When everyone is fearful," he would later tell investors, "that's when you build for the future."

While competitors retrenched, Ramkrishna accelerated its capital expenditure program. During the year 2008-09, the company augmented their Machining Facilities by procuring the CNC Gear Hobbing Machines, CNC Gear Shaving Machine and CNC Gear Shapping Machine from Mitsubishi Heavy Industries Ltd. These weren't just equipment purchases—they were capability acquisitions. Gear manufacturing is among the most precise operations in automotive, with tolerances measured in microns. By mastering this, Ramkrishna could bid for higher-value transmission components.

The diversification strategy during this period was deliberate and methodical. Beyond automotive, the company expanded into railways, bearings, oil & gas, power, construction, earth moving and mining. Each sector had different cycles, different payment terms, different quality requirements. Managing this complexity required sophistication that most Indian forging companies lacked. The capital raising journey tells the story of Ramkrishna's ambitions. Its first funding round was on Dec 11, 2012. Its latest funding round was a Post IPO round on Feb 25, 2013 for $9.25M. The investors included IFC (International Finance Corporation), Ascent Capital, and India Capital Growth—institutional names that brought credibility beyond just capital.

During the year 2010-11, the company increased their billet cutting facilities by importing fully automatic horizontal bandsaw machine from Amada Machine Tools, Japan. They augmented their machining facilities by procuring CNC Gear Hobbing Machines from Mitsubishi Heavy Industries Ltd, Japan and Premier Ltd, High Performance CNC Turning Centers and CNC Vertical Machining Centers from Doosan, Korea. During the year, the company added 50 new products in the Turing section, 22 new products in the Gear section and 12 new products in HMC/ VMC section. In January 2011, the company increased the installed capacity of the forgings section by 3600 tons with the installation of Maxi-Press at its Plant I at Jamshedpur.

This wasn't just capacity expansion—it was capability building. Each new machine opened up new product categories. The Maxi-Press allowed them to forge larger components for mining and construction equipment. The CNC gear machines enabled precision transmission parts. The strategy was clear: move up the value chain from simple forgings to complex, machined assemblies.

During the year 2012-13, the Company acquired and subscribed to equity shares representing 72.82% of the Paid up Share Capital of Globe Forex and Travels Limited and resultant Globe Forex and Travels Limited became the subsidiary of Company effective from January 10, 2013. This seemingly odd acquisition of a forex and travel company would later prove strategic for managing foreign exchange risks as exports grew.

The export story during this period was remarkable. From being a purely domestic supplier in the 1990s, Ramkrishna had built relationships with global tier-1 suppliers like Meritor. Each export order required meeting stringent quality standards, managing currency risks, and competing with established global suppliers. But the payoff was significant—export realizations were 20-30% higher than domestic sales.

During the Financial Year 2017-18, the Company raised Rs 199.99 Crore through a Qualified Institutional Placement (QIP) for the purpose of capital expenditure for ongoing and future expansion of projects, acquisition, working capital, repayment of loans and for general corporate purposes. In addition, it issued and allotted 39,21,568 equity shares to Qualified Institutional Buyers at a price of Rs 510 each on 20th July 2017.

But success came with a cost. The aggressive expansion was funded primarily through debt. By 2019, the company's debt had ballooned, and interest costs were eating into profitability. The automotive industry was slowing globally, and Ramkrishna seemed overextended. Critics pointed to the company's high debt-to-equity ratio and questioned whether the Jalans had expanded too aggressively.

Then came 2019, and everything changed.

V. The Pandemic Crucible & Transformation (2019-2021)

The numbers were brutal. Profits crashed from ₹120 crore in FY19 to just ₹9.7 crore in FY20. For a company that had been on a decade-long expansion spree, this was an existential crisis. Auto production globally came to a standstill. Export orders were cancelled. Domestic commercial vehicle sales—Ramkrishna's bread and butter—fell off a cliff.

But Naresh Jalan saw this differently. In investor calls during the pandemic, he would repeatedly say there were "two RKFLs - pre-pandemic and post-pandemic." This wasn't corporate speak—it was a fundamental reimagining of the business. The transformation had three pillars. First, geographic expansion. While competitors pulled back from international markets, Ramkrishna doubled down. "There are two RKFLs actually—one pre-pandemic and the other one post-pandemic. RKFL had a different kind of working style post the pandemic," says Naresh Jalan, 47, Managing Director of RKFL. The company expanded aggressively into Europe, Southeast Asia, North America, South America, and Turkey. Export contribution grew from 25% pre-pandemic to 40% by 2021.

Second, diversification beyond automotive. The company also took a strategic decision of getting into non-auto segments like railways, tractors and oil & gas, among other sectors. "These are the sectors where we were not prevalent pre-pandemic. Post-pandemic, almost 20% of our business comes from the non-auto sector". This wasn't opportunistic diversification—it was strategic de-risking. Each sector had different demand cycles, providing natural hedging against automotive volatility.

The third pillar was perhaps the most radical—cultural transformation. Ramkrishna had always been a promoter-driven company with top-down decision making. During the pandemic, Naresh flipped this model. He empowered plant managers, gave autonomy to sales teams, and created a bottom-up innovation culture. The message was clear: survival required everyone to think like an owner.

Castings and forgings is not exactly viewed as a new-age sector and is known to rely heavily on old methods and technologies but RKFL boasts of artificial intelligence (AI) adoption in a big way. The company uses automation and AI in various verticals, including production, quality checks, documentation and even in the overall accounting standards. "From having fully loaded paperwork in the system, we are trying to get into a system wherein we work on a paperless method and work more towards becoming an automated set-up with 24X7 operating standards".

The financial engineering during this period was equally impressive. Despite the profit collapse, Ramkrishna managed to reduce debt significantly. They renegotiated payment terms with suppliers, accelerated collections from customers, and most importantly, convinced lenders to restructure loans without classifying them as stressed assets. This wasn't financial manipulation—it was survival through relationship capital built over decades.

But the real test came when demand started recovering in late 2020. Global supply chains were in chaos. Chinese suppliers faced lockdowns. European forging companies had laid off skilled workers. Suddenly, global OEMs needed reliable suppliers who could ramp up quickly. And Ramkrishna, having maintained capacity and workforce through the crisis, was perfectly positioned.

The company commissioned a hollow spindle line, a press line with annual installed capacities of 10,200 tonnes & 17,000 tonnes respectively in 2020. In 2021, it commissioned a warm forging line with annual installed capacities of 9,900 T and a fabrication facility. While others were still assessing damage, Ramkrishna was adding capacity.

VI. The Technology & AI Revolution in Forgings (2021-Present)

Walk into Ramkrishna's Jamshedpur facility today, and you'll witness a paradox—one of humanity's oldest manufacturing processes transformed by cutting-edge artificial intelligence. Forging has remained fundamentally unchanged since the Bronze Age: heat metal, apply force, shape it. But how that process is controlled, optimized, and quality-checked has been revolutionized.

The AI adoption wasn't a Silicon Valley-style disruption play. It started with a simple problem: quality inspection. Traditional forging quality control involved manual inspection of samples—time-consuming, error-prone, and impossible to scale. Ramkrishna deployed computer vision systems that could inspect 100% of production in real-time, catching defects that human inspectors might miss after hours of monotonous checking. But the real breakthrough came with predictive maintenance. Using sensors and machine learning, Ramkrishna could predict equipment failures before they happened. In an industry where a single forge hammer breakdown could cost millions in lost production, this was revolutionary. Downtime reduced by 40%, maintenance costs fell by 30%, and most importantly, product quality improved dramatically.

The aluminum forging investment announced in 2024 represents the company's bet on the EV future. With a total installed capacity of 3,000 tons annually, the plant will primarily serve the electric vehicle segment and will require an investment of Rs 57.5 crore from the company. It is anticipated to be put into service by the second quarter of the fiscal year 2025–2026. According to a senior corporate executive, the project is expected to produce additional revenue of Rs 175 crore annually when it is operating at full capacity.

This wasn't just about adding capacity—it was about capabilities. Aluminum forging requires completely different technology than steel forging. The temperatures are different, the metallurgy is different, the quality control is different. But for EVs, aluminum is essential for lightweighting. This move aligns with Ramkrishna Forgings' commitment to vehicle lightweighting, a crucial factor in enhancing performance, improving fuel efficiency, and reducing the environmental impact of modern vehicles.

The company also made headlines in 2024 when it received approval to supply powertrain components to the USA's largest electric passenger vehicle producer. While the company didn't disclose the name, sources hint that it might be Tesla. This announcement coincides with tech billionaire Elon Musk's upcoming visit to India, where he is set to meet with the Indian Prime Minister Narendra Modi.

Meanwhile, the company invested ₹50 crore in energy efficiency and carbon reduction initiatives in 2023. This included solar installations, waste heat recovery systems, and process optimization that reduced energy consumption per ton of forgings by 15%. In an energy-intensive industry facing increasing ESG scrutiny, these investments were both defensive and strategic.

The technology transformation extended to the shop floor culture. Workers who had spent decades manually operating forge hammers were now monitoring screens, analyzing data, interpreting AI recommendations. This required massive retraining programs. But rather than resistance, Naresh found enthusiasm—workers saw technology as elevating their roles from manual laborers to skilled technicians.

By 2024, Ramkrishna had achieved something remarkable—they had taken one of the world's oldest manufacturing processes and made it cutting-edge. The company could now offer "digital twins" of components to customers, allowing virtual testing before physical production. They could guarantee quality levels that were unthinkable a decade ago. And they could do it all at costs competitive with Chinese manufacturers.

VII. Financial Engineering & Capital Structure

The financial transformation of Ramkrishna Forgings between 2019 and 2024 reads like a masterclass in capital allocation. From a debt-heavy, cyclical manufacturer to a lean, profitable growth story—the numbers tell a remarkable tale of discipline and strategic financial management. The headline achievement: debt-to-equity ratio fell from over 2x in 2019 to 0.45 by 2024—a transformation that seemed impossible during the pandemic depths. Focus on deleveraging b/s with target of being near net debt free by FY25E became the management mantra. This wasn't achieved through equity dilution but through operational excellence and disciplined capital allocation.

Revenue growth was spectacular: from ₹1,216 crore in FY20 to ₹4,034 crore in FY24—a 3.3x increase in just four years. But what's more impressive is how this growth was achieved. Rather than chasing volume at any cost, Ramkrishna focused on value-added products. The share of machined components increased from 30% to over 50% of sales, dramatically improving margins.

The working capital management story deserves special attention. In the forging industry, working capital cycles can stretch to 120+ days—raw material inventory, work-in-progress, finished goods, and then extended credit to OEMs. Ramkrishna brought this down to under 90 days through a combination of just-in-time manufacturing, better demand forecasting, and tough negotiations with both suppliers and customers.

The ownership structure evolution tells its own story. Strong Balance Sheet: Robust debt-to-equity ratio of 0.45. While promoter holding remained steady at around 43%, the quality of institutional investors improved dramatically. FIIs increased their stake to 24.47%, with names like Franklin Templeton and Aberdeen Standard taking positions. This wasn't just passive investment—these institutions brought governance improvements and global best practices.

But the real financial engineering came in capital allocation. During FY23-24E company planned to add ~56,000 ton cold & warm forging press line which is technologically advanced and different from its existing lines. This wasn't funded through debt but through internal accruals—a testament to the cash generation capabilities built post-pandemic.

The dividend policy reflected this confidence. In 2023, Ramkrishna Forgings has declared dividend 3 times (on 30 Oct 2023, 09 May 2023, 31 Jan 2023), amounting to total of ₹ 2 per share. While the payout ratio remained conservative at around 10%, this was deliberate—the company preferred reinvesting in high-return projects rather than distributing cash.

The September 2023 QIP raise of up to ₹1,000 crore was strategic timing. With the stock near all-time highs and institutional interest strong, this was opportunistic financing that would fund the next phase of growth without stretching the balance sheet. The funds were earmarked for technology upgrades, EV transition investments, and potential acquisitions.

What's remarkable is how Ramkrishna managed this transformation while maintaining operational performance. EBITDA margins stayed above 20% throughout, return on capital employed improved to mid-teens, and cash flow from operations consistently exceeded net profit—signs of a quality business.

VIII. Business Model & Competitive Moats

Understanding Ramkrishna Forgings' business model requires appreciating the complexity of modern automotive supply chains. The company doesn't just forge metal—it provides engineered solutions that are critical to vehicle safety and performance. This distinction is crucial for understanding their competitive moats.

The product portfolio spans over 2,000 SKUs, from simple connecting rods weighing a few kilograms to massive mining equipment forgings exceeding 100 kilograms. But breadth alone isn't the moat—it's the ability to produce these at consistent quality, meeting specifications measured in microns, with failure rates below 50 parts per million.

The revenue mix tells the strategic story: Automotive contributes 70%, Railways 20%, and Engineering/Others 10%. Within automotive, the split is equally strategic—60% commercial vehicles, 30% passenger vehicles, 10% two/three-wheelers. This isn't accidental diversification but calculated risk management. When commercial vehicle cycles turn down, passenger vehicles often compensate. When domestic markets slow, exports (now 40% of revenue) provide cushion.

The critical supplier status is perhaps the strongest moat. Once approved as a supplier for safety-critical components like steering knuckles or axle beams, switching costs become prohibitive for OEMs. It's not just about finding another supplier—it's about months of testing, certification, field trials, and the risk of catastrophic failure if something goes wrong. Ramkrishna supplies components where failure could mean loss of life, creating switching costs that go beyond economics.

Quality certifications read like an alphabet soup—ISO/TS 16949, API, AAR M-1003, IRIS—but each represents years of process improvement and substantial barriers to entry. A new entrant would need 3-5 years just to obtain these certifications, assuming they had the technical capabilities to meet the standards.

The geographic diversification adds another layer to the moat. With 20% of products going to North America, significant presence in Europe, and growing Asian exports, Ramkrishna has de-risked from any single market. But more importantly, succeeding in developed markets—with their stringent quality requirements and litigious environments—creates credibility that opens doors globally.

The "China Plus One" strategy adopted by global manufacturers post-COVID has been a massive tailwind. As companies seek to diversify supply chains away from China, India emerges as the obvious alternative. But within India, only a handful of companies have the scale, quality, and certifications to serve global OEMs. Ramkrishna is one of them.

The vertical integration strategy, controversial when implemented, now looks prescient. From forging to machining to heat treatment to assembly—controlling the entire value chain means better quality control, faster delivery times, and most importantly, higher margins. Competitors who outsource machining operations can't match Ramkrishna's turnaround times or quality consistency. The recent $220 million North American contract announced in February 2024 exemplifies the strength of these moats. This contract spans over a decade and marks the company's foray into a new vertical within the forging sector, focusing on supplying Tier 1 customers in the Light Vehicle segment across North America. This isn't just a purchase order—it's a decade-long partnership worth ₹1,800 crore, representing validation of Ramkrishna's capabilities by the world's most demanding automotive market.

The technology moat is evolving rapidly. While traditional forging companies focus on tonnage and basic quality, Ramkrishna has invested in simulation software, finite element analysis, and digital twins. They can now simulate the entire forging process before making a single part, predicting stress points, optimizing material usage, and guaranteeing performance characteristics that competitors can't match.

Labor productivity tells another story. With 2,300 employees generating ₹4,000+ crore in revenue, the revenue per employee exceeds ₹1.7 crore—among the highest in Indian manufacturing. This isn't about automation replacing workers but about technology amplifying human capabilities.

The customer concentration risk, often cited as a weakness, is actually more nuanced. While top 10 customers contribute significant revenue, these aren't single relationships but multiple programs across different vehicle platforms. Losing a customer would mean losing specific programs, not the entire relationship—a crucial distinction that reduces risk significantly.

IX. Strategic Analysis & Industry Dynamics

The forging industry sits at a fascinating intersection of old-world manufacturing and new-age disruption. On one hand, the basic process—heating metal and hammering it into shape—hasn't changed since the Iron Age. On the other, the precision required, the materials used, and the applications served are evolving at breakneck speed.

Globally, the forging industry is worth approximately $100 billion, with automotive accounting for 60% of demand. Within this, India represents just 3% of global production despite being the world's third-largest auto market. This gap represents both opportunity and challenge—opportunity because there's room to grow, challenge because global competitors aren't standing still.

The competitive landscape in India is dominated by Bharat Forge, with revenues exceeding ₹12,000 crore—three times Ramkrishna's size. But size alone doesn't tell the story. Bharat Forge focuses heavily on passenger vehicles and developed markets, while Ramkrishna has carved niches in commercial vehicles and emerging markets. The strategies are complementary rather than directly competitive.

Other competitors like Mahindra CIE, MM Forgings, and Happy Forgings operate in specific segments. What distinguishes Ramkrishna is its breadth—from 1kg to 125kg forgings, from two-wheelers to mining equipment, from India to North America. This diversification, initially seen as lack of focus, now provides resilience that focused players lack.

The China factor looms large. Chinese forging companies, backed by state subsidies and massive scale, can undercut on price. But post-COVID supply chain disruptions have exposed the risks of over-dependence on China. Global OEMs are actively diversifying suppliers, and India—with its democratic governance, English-speaking workforce, and established auto industry—is the natural beneficiary.

The EV transition presents both threats and opportunities. Traditional powertrain components—crankshafts, connecting rods, camshafts—will eventually disappear. But EVs still need suspension components, steering systems, and structural parts. In fact, the heavier battery packs in EVs require stronger suspension components, potentially increasing content per vehicle for forging companies.

Railway modernization in India represents a massive opportunity. With the government's push for Vande Bharat trains, metro expansions, and freight corridor development, demand for railway forgings is set to explode. Ramkrishna's early positioning in this segment—they've been supplying critical safety items since 1985—provides first-mover advantages.

Management's vision to "almost more than double in the next five years" seems aggressive but achievable. With current capacity utilization around 70%, there's room to grow without major capex. The aluminum forging facility adds new capabilities for EV components. Geographic expansion provides new markets. And operational leverage means margins should expand with scale.

The strategic partnership with McKinsey, announced recently, signals ambition beyond organic growth. While details remain confidential, such engagements typically focus on operational excellence, digital transformation, or inorganic expansion. Given Ramkrishna's strong balance sheet and proven integration capabilities, acquisitions could accelerate growth.

Industry consolidation seems inevitable. Smaller forging companies lack the scale to meet global OEM requirements or invest in necessary technology. Ramkrishna, with its strong balance sheet and operational expertise, is well-positioned to be a consolidator rather than consolidated.

X. Bear Case vs Bull Case

The Bear Case:

The recent numbers should worry investors. PAT down 88.2% QoQ, PBT down 47.8% in Q1 FY26—these aren't minor fluctuations but dramatic reversals. For a company that had been posting consistent growth, this sudden deterioration raises questions about execution and market dynamics.

The cyclical nature of the automotive industry remains Ramkrishna's Achilles heel. Despite diversification efforts, 70% of revenue still comes from automotive. When commercial vehicle cycles turn—and they always do—the impact on profitability can be severe. The company's fixed cost base means operating leverage works both ways.

Chinese competition isn't going away. While "China Plus One" provides tailwinds today, Chinese manufacturers are establishing facilities in Mexico, Vietnam, and other low-cost countries. They're also moving up the value chain, investing in technology and quality. The cost advantage that Indian manufacturers enjoy is shrinking.

The EV disruption timeline remains uncertain but the direction is clear. While Ramkrishna has invested in aluminum forging for EV components, this requires different capabilities, customer relationships, and competitive dynamics. Success in traditional forgings doesn't guarantee success in EV components.

Company has low interest coverage ratio—a concerning sign for a cyclical business. While debt has reduced from peak levels, it's still substantial. In a downturn, servicing this debt while maintaining operations could strain cash flows.

Customer concentration remains high. Losing a major OEM relationship—whether due to insourcing, technology changes, or competitive dynamics—could materially impact revenues. The decade-long contracts provide some protection but aren't ironclad.

Valuation looks stretched. Stock is trading at 3.51 times its book value—premium valuations for a cyclical manufacturer. The market seems to be pricing in perfect execution and continued growth, leaving little room for disappointment.

The Bull Case:

The long-term growth trajectory remains intact. Looking at Ramkrishna Forgings' exceptional 44% five-year net income growth in particular, we are definitely impressed. This isn't a one-year wonder but sustained outperformance across cycles.

The balance sheet transformation is real and sustainable. Strong Balance Sheet: Robust debt-to-equity ratio of 0.45 provides the financial flexibility to weather downturns and invest in growth. This is a fundamentally different company than pre-pandemic.

Geographic and product diversification is working. Exports at 40%, non-auto at 20%, and growing—these aren't just metrics but fundamental de-risking of the business model. Each new geography and sector reduces dependence on any single market.

The $220 million North American contract validates the global competitiveness. This isn't low-value commodity business but sophisticated components for developed markets. It proves Ramkrishna can compete on quality and technology, not just cost.

Management execution has been exceptional. From pandemic survival to technology adoption to financial transformation—the Jalan family has consistently delivered. Their skin in the game (43% ownership) aligns interests with minority shareholders.

Industry tailwinds are strengthening. India's manufacturing renaissance, infrastructure spending, railway modernization, "China Plus One" sourcing—multiple secular trends favor Ramkrishna's positioning.

The technology investments are bearing fruit. AI-driven quality control, predictive maintenance, digital twins—these aren't buzzwords but real operational improvements driving margins and customer satisfaction.

Valuation in context looks reasonable. Yes, the P/B is elevated, but for a company generating mid-teen ROEs with strong growth prospects, premium valuations are justified. Compared to global auto suppliers, Ramkrishna still trades at a discount.

The optionality value is underappreciated. Aluminum forging for EVs, potential acquisitions, new geographic markets, adjacent sectors—multiple growth vectors provide upside that isn't fully priced in.

XI. Recent News

The latest quarterly results paint a mixed picture. Ramkrishna Forgings Ltd's net profit fell -78.46% since last year same period to ₹11.79Cr in the Q1 2025-2026. On a quarterly growth basis, Ramkrishna Forgings Ltd has generated -94.1% fall in its net profits since last 3-months. However, revenue jumped 5.02% since last year same period to ₹1,018.88Cr in the Q1 2025-2026. On a quarterly growth basis, Ramkrishna Forgings Ltd has generated 6.28% jump in its revenue since last 3-months.

Looking at the full year FY25 performance provides better context. For the full year, net profit rose 42.52% to Rs 415.03 crore in the year ended March 2025 as against Rs 291.21 crore during the previous year ended March 2024. Sales rose 8.90% to Rs 4034.11 crore in the year ended March 2025 as against Rs 3704.54 crore during the previous year ended March 2024.

Major operational developments include significant capacity expansion. Cold forging capacity of 25,000 tons and hot/warm forging capacity of 14,250 tons commissioned. The company successfully commissioned new cold, hot, and warm forging capacities, increasing total capacity to 268,400 metric tons.

The order book remains robust. Ramkrishna Forgings Ltd (BOM:532527) reported new order wins worth INR 4,600 crores during FY25, diversified across geographies and industries. This provides strong revenue visibility for the coming years.

A significant strategic development is the merger completion. The merger of ACIL into the parent entity was approved, simplifying the business structure and expected to enhance operational efficiency.

Financial credibility continues to improve. India Ratings upgraded the company's long-term bank loan rating to IND AA with a stable outlook, reflecting improved financial stability. This upgrade should reduce borrowing costs and improve access to capital.

Looking forward, the company has announced ambitious expansion plans. Ramkrishna Forgings plans to invest Rs 2,000 crore in a new Chennai plant for forged wheels, aiming for production to begin in FY27. This represents a significant bet on the growing demand for specialized automotive components.

However, recent corporate governance concerns have emerged. A joint report confirmed a ₹220.52 crore inventory overstatement at Ramkrishna Forgings, adversely impacting net worth by approximately 7%. The company plans to address the discrepancies and mitigate potential losses. In response, Ramkrishna Forgings' promoters will infuse fresh capital through warrants priced at nearly three times the market value to reassure minority shareholders after inventory discrepancies.

The stock market reaction has been negative. The stock is down significantly from its peaks, trading near ₹600-650 levels compared to highs above ₹1,000 in 2024. This presents either a buying opportunity for believers in the long-term story or a warning sign of deeper issues.

XII. Conclusion: The Road Ahead

Ramkrishna Forgings stands at a critical juncture. The transformation from a small Kolkata workshop to a ₹10,000+ crore global supplier is remarkable, but past performance doesn't guarantee future success. The company faces both extraordinary opportunities and existential challenges.

The investment case ultimately boils down to whether you believe traditional manufacturing can successfully navigate technological disruption. Ramkrishna's track record suggests it can—from surviving License Raj to thriving post-liberalization, from weathering the 2008 crisis to emerging stronger post-pandemic. Each challenge has made the company more resilient.

The bear case concerns are real and shouldn't be dismissed. Inventory overstatements, profit volatility, and EV disruption are material risks. But the bull case—built on management execution, industry positioning, and financial strength—appears stronger. The company has consistently proven skeptics wrong.

For long-term investors, Ramkrishna Forgings represents a bet on India's manufacturing renaissance, the global automotive industry's evolution, and most importantly, on a management team that has navigated every crisis thrown at them. The recent stock price weakness, while concerning, may present an opportunity for patient capital.

The story of Ramkrishna Forgings is far from over. As Naresh Jalan said, there are two RKFLs—pre-pandemic and post-pandemic. Perhaps we're witnessing the emergence of a third RKFL—one that combines traditional manufacturing excellence with digital capabilities, global reach with local expertise, and financial discipline with growth ambition.

In the end, investing is about probabilities, not certainties. The probability that Ramkrishna Forgings continues its transformation journey, captures new opportunities, and creates shareholder value appears higher than the probability of failure. But as always in investing, only time will tell if this forging dynasty can continue conquering global auto supply chains in an era of unprecedented change.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube