Reliance Jio: The Greatest Startup Pivot in History?

I. Introduction: The $100 Billion Bet

On the evening of September 1, 2016, inside a cavernous hall at the Reliance Corporate Park in Navi Mumbai, a silver-haired man in a white kurta walked onto a stage under the gaze of roughly 3,500 shareholders. Mukesh Ambani, the world's then-eighth richest person, held a black-and-blue SIM card between his thumb and forefinger the way a magician holds a coin before a trick. The cameras zoomed in. He smiled, barely. And then he said the words that would, within forty-five minutes, erase nearly a trillion rupees of market capitalization from the Indian telecom sector: "Voice calls on Jio will be absolutely free. Forever."

It was the kind of sentence that nobody in the industry thought a grown-up CEO could say. Voice had been the lifeblood of Indian telecom since Sunil Mittal's Airtel pioneered the market in the 1990s. Free voice didn't just discount a product; it implied that the product itself, the thing an entire industry had been built around, was now worth nothing. And Mukesh said it with the calm of a man who had spent six years and $30 billion building a weapon specifically designed to make his competitors' revenue streams obsolete.

This is the story of how a petrochemical conglomerate, a business whose biggest assets were oil refineries the size of small cities, pivoted into one of the largest and most consequential digital platform plays on planet Earth. Jio is not a telecom company. It never was. Telecom was merely the on-ramp. Reliance Jio is a "digital life" ecosystem that took the cash flows from the world's largest single-site oil refinery at Jamnagar and converted them, at industrial scale, into 4G spectrum, fiber-optic cable, low-cost smartphones, data centers, and eventually into boardroom seats alongside Facebook, Google, and NVIDIA.

The thesis of this episode is simple, even if the execution was not. Mukesh Ambani looked at India in 2010 and saw a country of 1.2 billion people about to experience the greatest compression of time in human economic history, the collapse of a twenty-year technology adoption curve into roughly forty-eight months. He decided not to catch the wave. He decided to manufacture it. He would build the pipes, then ride the data that flowed through those pipes into every other business that had ever depended on distribution.

Over the next three hours of this deep dive, the narrative will travel through four distinct acts. There is the family drama, a literal Mahabharata of the Ambani brothers, with a non-compete clause at its center that kept Mukesh out of telecom for nearly a decade. There is the stealth phase, the longest and most expensive period of corporate silence in Indian industrial history, when Reliance Industries laid a quarter of a million miles of optical fiber without selling a single consumer contract. There is the Big Bang of September 2016, which remains, even a decade later, the most extraordinary customer acquisition event ever recorded outside of the generative AI era. And finally, there is what happened after the conquest: the summer of 2020, when Silicon Valley came to Mumbai to buy a piece of Jio's future.

What makes Jio so fascinating, and what puts it in genuine contention for the greatest startup pivot in history, is not the scale, though the scale is staggering. It is the identity shift. This is a ninety-year-old polyester trader turned petrochemical giant that, inside of a single decade, rewrote itself into a consumer technology platform holding company. Pivots of that magnitude, executed at that size, with that much capital at stake, simply do not exist. The story that follows is how that happened, who made it happen, and what it now means for the next twenty years of Indian capitalism.

II. The Origins: A Family Split and a Non-Compete

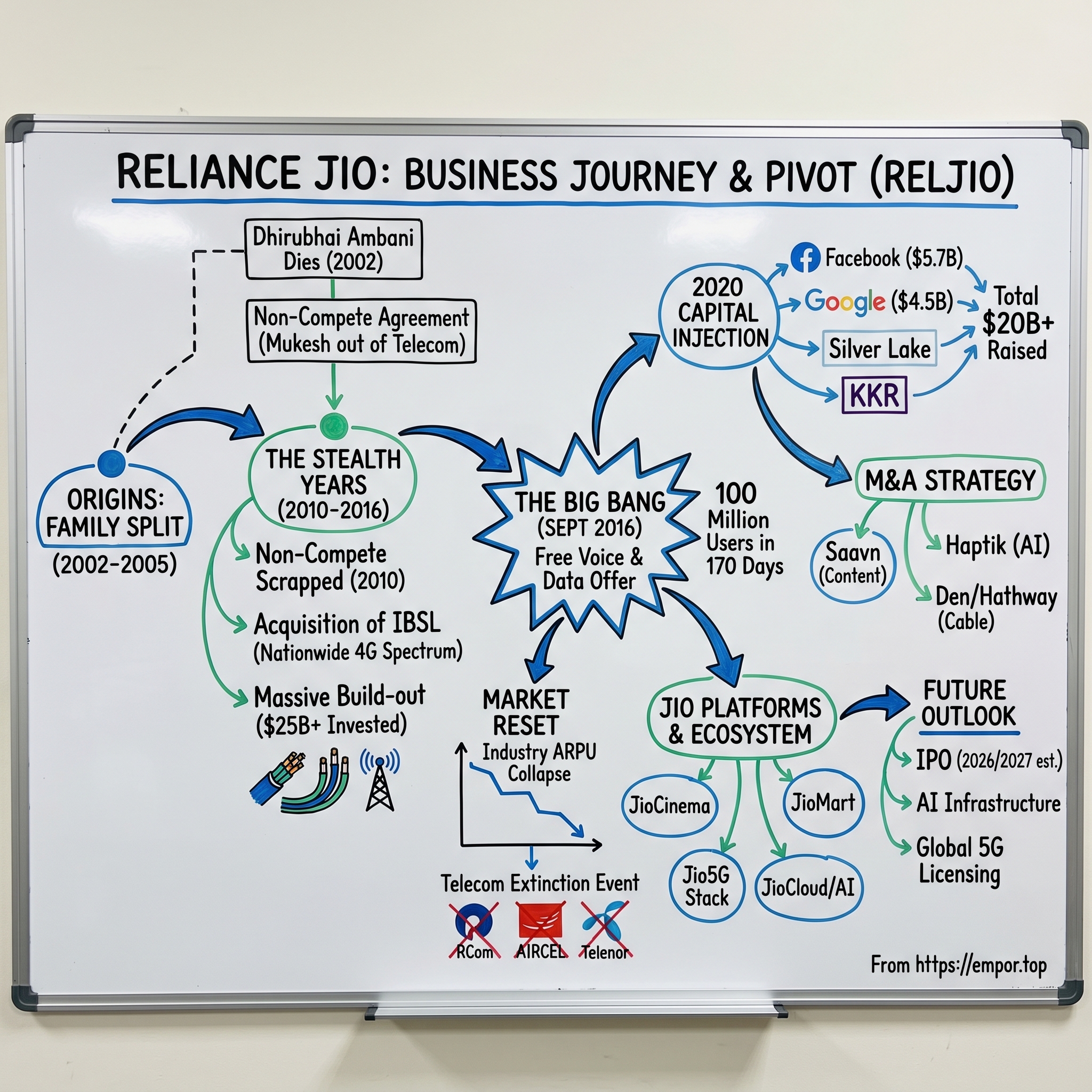

Every founding myth has a wound at its center. For Reliance, the wound is personal. On July 6, 2002, Dhirubhai Ambani died of a stroke in a Mumbai hospital, leaving behind no written will and two sons whose rivalry would eventually be mediated by their mother, Kokilaben, and a flotilla of merchant bankers. Mukesh, the elder, was the engineer, the Stanford-trained operator, the man who had commissioned the Jamnagar refinery. Anil, the younger, was the showman, the financier, the one with the Bollywood charm. Dhirubhai had let them compete inside the empire for years, believing friction sharpened both. But with the patriarch gone, friction became fracture.

In June 2005, Kokilaben announced the settlement. The sprawling house of Reliance would be cleaved in two. Mukesh would take the oil, gas, and petrochemicals, the slow-burn industrial cash machines. Anil would take the newer, sexier businesses, telecommunications, power generation, financial services, and entertainment. Reliance Communications, or RCom, was Anil's flagship. And critically, tucked into the settlement was a non-compete agreement. Mukesh could not enter telecom. Anil could not enter refining. The brothers would not pour kerosene on each other's fires.

For five years, that clause held. Anil pushed RCom into a CDMA-led mass market play, flooding India with one-rupee-per-minute tariffs and the now-iconic Reliance handsets. For a fleeting moment, he was the telecom king. Then the debt caught up with him. The global financial crisis, a stalled IPO for Reliance Power, mounting spectrum auction costs, and a generally deteriorating consumer telecom business began to unravel what had looked like a winning hand. By 2009, RCom was losing market share to Airtel, Vodafone, and Idea. Anil's empire was starting to bleed.

Then came the inflection. On May 23, 2010, the non-compete clause was mutually scrapped. For the first time, Mukesh had the legal right to enter telecom. The story goes, and it has been told and retold by Reliance lifers, that Mukesh did not wait a day. Within hours of the non-compete being dissolved, Manoj Modi, Mukesh's closest lieutenant and the man sometimes called the Reliance Chanakya, was on a call finalizing the acquisition of Infotel Broadband Services Limited. IBSL was a tiny, obscure company that had, just eleven days earlier, won something nobody else had understood the value of: the only nationwide pan-India block of Broadband Wireless Access spectrum in the 2300 MHz band.

This is the moment where the story separates from the rest of the industry. In 2010, nobody was thinking about 4G. There were no 4G handsets sold in India. There were barely any 4G handsets anywhere. The whole world was still rolling out 3G. Airtel, Vodafone, and every other incumbent had bid hard in the 3G auction, which was the auction everyone cared about. They treated the BWA auction as an afterthought. Infotel, a company most telecom reporters had never heard of, bid $2.7 billion and walked away with spectrum in all twenty-two telecom circles of India. Within hours of winning, Infotel was sold to Reliance Industries for roughly $1 billion in equity plus the spectrum liability. The world barely noticed.

Why 4G, and why then? The insight was that India would skip the desktop internet revolution entirely. Most Indians would never own a PC. Their first computer would be a smartphone, and their first connection would not be DSL, it would be a cellular data pipe. If that was the future, then owning the only nationwide 4G spectrum was owning the bedrock of the next twenty years of Indian digital life. Everyone else was optimizing for voice, for 3G, for the present. Mukesh was buying the future at distressed prices because no one else had shown up to the auction. And then he went dark for six years.

III. The Stealth Years: Building the Data Pipe

For most of 2011, 2012, 2013, 2014, and 2015, Reliance Jio, as it was eventually called, was the biggest business in India that nobody could see. Analysts covering Reliance Industries wrote earnings notes that routinely featured the phrase "the telecom venture continues to be in pre-operational stage." Capex ballooned quarter after quarter. No revenue. No customers. No launch date. The financial press, sharpening its claws, called it the "Jio black hole." Several foreign hedge funds shorted Reliance on the thesis that Mukesh had gone senile and was building a white elephant of Soviet proportions.

The scale of the build-out was unlike anything the Indian private sector had ever undertaken. By the time Jio formally launched, Reliance had poured somewhere between $25 billion and $30 billion into the network, a figure larger than the GDP of roughly seventy countries. But the critical detail is where that money went. It did not go into the usual telecom playbook of renting tower space and buying bulk bandwidth from third parties. It went into the ground. Literally into the ground.

While incumbents like Airtel and Vodafone had built their networks on leased tower infrastructure and leased backhaul from companies like Bharti Infratel and Indus Towers, Jio decided to own the backhaul itself. The company laid roughly 250,000 route-miles of optical fiber across India, enough cable to circle the earth ten times. It buried fiber to villages with fewer than a thousand residents. It spliced fiber into the basements of every major Indian metropolitan tower. The fiber was the moat, because the fiber determined the marginal cost of delivering a gigabyte of data, and that marginal cost was going to be the basis of everything that followed.

The second part of the moat was the decision to go all-IP, all the time. In plain English, this meant that Jio's network had no legacy voice infrastructure whatsoever. Every call, every message, every video stream travelled as internet data packets across the same pipes. Traditional telecom networks, built in the 2G and 3G era, ran voice on a separate circuit-switched layer that cost real money to operate, maintain, and license. By going pure IP, Jio was able to offer voice at essentially zero marginal cost. This was the engineering reality that underpinned the "free voice forever" announcement years later. The pricing was not a marketing stunt. It was a cost structure weaponized as marketing.

There is a phrase Mukesh started using around 2013 at internal town halls, a phrase that has since been memorialized in roughly every annual report Reliance has published. "Data is the new oil." It sounded like a line from a management consulting deck. But in the Reliance context, it was literal. Oil, the business Mukesh knew in his bones, was not really about the crude. It was about the refinery, the distribution, the pipelines, the retail outlets. Oil is useless without a refinery. And data, Mukesh argued, was exactly the same. Raw data, raw bandwidth, was a commodity. But a platform that refined that data into commerce, entertainment, communication, and financial services, that platform could be worth as much as Saudi Aramco.

What Jio was building during the stealth years was the refinery. And by 2016, the refinery was finished, the tanks were full, and the only question remaining was how the market would react when Mukesh opened the taps. The answer, it would turn out, involved one of the most violent pricing shocks in the history of modern consumer markets.

IV. The Big Bang: September 5, 2016

Consider the Indian mobile consumer on September 4, 2016. A typical prepaid user paid roughly 250 rupees per gigabyte of 2G or 3G data. Voice calls cost between 50 paise and 1.5 rupees per minute depending on the operator and the time of day. A heavy user might spend 1,500 rupees a month, roughly 2% of the median household income. Data was a luxury good, metered and rationed, something young people used sparingly and older people avoided entirely. India had roughly 350 million internet users, mostly concentrated in metros, mostly consuming text, not video.

Then came September 5. At the annual general meeting, Mukesh Ambani announced that Jio's Welcome Offer would give every new subscriber free voice, free SMS, and free unlimited 4G data until December 31, 2016. Four months of free everything. No credit card. No subscription. Just walk into a Reliance Digital store, show your Aadhaar card, and walk out with a SIM. In a country where data cost what it cost, this was not a discount. It was an expropriation of the industry's entire business model.

The result was not a marketing success. It was a stampede. By the end of the first month, Jio had 16 million subscribers. By the 170th day, that number had crossed 100 million. For context, that was faster than Facebook, faster than WhatsApp, faster than every pre-ChatGPT consumer technology product ever launched, and it was happening in a country where roughly half the population lived on less than four dollars a day. Rural India, which the telecom incumbents had written off as a low-ARPU swamp, turned out to be a data-hungry tiger once the price dropped to zero. Trucks would park outside villages and hand out SIM cards. Stores ran out of stock within hours of opening. Airtel's chairman Sunil Mittal publicly called the pricing "irrational." It was not. It was existential.

Because here is the thing about free. Free, in a network business, is not a price point. It is a gravity well. Once Jio dragged 100 million Indians into the well, the rest of the market followed, because no incumbent could afford to let those customers churn elsewhere. Airtel and Vodafone had to match. Matching meant their average revenue per user, the lifeblood of any telecom operator, collapsed. Indian ARPUs, which had been in the 150 to 200 rupee range, plunged toward 70. And that is where the carnage began.

In the three years following Jio's launch, the Indian telecom sector experienced what can only be described as an extinction event. Reliance Communications, Anil's flagship, filed for bankruptcy in 2019. Aircel collapsed. Tata Teleservices sold its consumer business to Airtel for effectively zero. Telenor exited India. Videocon, Sistema Shyam, MTS, all gone. Vodafone India and Idea Cellular, two of the largest incumbents, were forced into a defensive merger in 2018 to form Vodafone Idea, a company that to this day still trades as a going concern only because of repeated government relief packages. The Indian telecom market, which in 2015 had twelve meaningful operators, was by 2019 effectively a three-horse race between Jio, Airtel, and a wounded Vodafone Idea.

The analyst community initially called this a price war. That framing is wrong. A price war implies two combatants voluntarily agreeing to shrink margins. What happened in India was an industry-wide business model reset, imposed unilaterally by an operator whose parent company could subsidize it with petrochemical cash flows for as long as necessary. Jio was not competing in the telecom market. Jio was rewriting it. And once the rewrite was finished, the only remaining question was what would be written next, on top of the network that Jio now dominated.

V. Management: The Rise of Akash Ambani and the Professional Class

The transition of power inside Reliance is one of the most quietly consequential stories of the 2020s in Indian business. For a long time, Mukesh Ambani was the sun around which Reliance orbited. He was, and in many ways still is, the architect. But sometime in the late 2010s, a generational rotation began, and it began at Jio.

Akash Ambani, Mukesh's elder son, was born in 1991. He studied at the Dhirubhai Ambani International School, then went to Brown University in Rhode Island, where he studied economics. Friends from those years describe him as quiet, intensely focused on product, and almost uncharacteristically low-profile for an Ambani. Where his father was the deal maker, Akash became the product manager. He was appointed to the Jio board in 2014, while still in his early twenties, and spent the next eight years operating as an internal consumer champion, pushing Jio's leadership to think less like a telco and more like a platform.

On June 27, 2022, Mukesh stepped down as chairman of Reliance Jio Infocomm, the operating telecom subsidiary, and Akash was named chairman in his place. It was Reliance's first public succession signal and it was deliberate. Mukesh retained his role as chairman of Reliance Industries, the parent conglomerate, but the day-to-day steward of the telecom-and-digital engine was now his son. Akash's fingerprints are all over the post-2020 pivot from pipes to platforms. The aggressive push into JioCinema. The bet on a domestically built 5G stack. The move toward retail-commerce integration with JioMart. These are not the instincts of a telecom operator. They are the instincts of someone who grew up inside the mobile-first internet.

Around Akash sits a professional class that has no parallel in Indian family conglomerates. Manoj Modi, often described as the most powerful man in Indian business that nobody has heard of, has been Mukesh's consigliere for more than four decades. He rarely appears in public and almost never gives interviews. Inside Reliance, he is the man who negotiated the 2020 funding round against Mark Zuckerberg, Sundar Pichai, and the partners at KKR and Silver Lake. Kiran Thomas, a software engineer who joined Reliance in the late 1990s, runs the digital services side, including the Jio apps portfolio and the AI initiatives. Anshuman Thakur, Jatin Mehta, and a roster of senior executives handle strategy, treasury, and investor relations with an institutional polish that feels more Silicon Valley than Malabar Hill.

The question that hovers over every family conglomerate is the question of incentives. How do you get a professional manager at a Reliance subsidiary to behave like a founder when the family trust controls the equity? The answer, as far as it can be observed from the outside, is a combination of treasury shares, long-dated performance units tied to the eventual IPO of Jio Platforms, and what one former executive described as "a culture where Manoj Modi rings at midnight and you answer." The alignment is less about equity participation and more about access and status inside the highest levels of Indian industry. Whether that is sustainable through a genuine public listing and the scrutiny that comes with it is one of the most important open questions about the Jio story in 2026.

For investors, the management watchpoint is whether Akash's product-first instincts can survive the gravitational pull of a family-run balance sheet that will always, eventually, want to harvest cash for the next big industrial project. So far, the signals have been consistent. The platform pivot is deepening, not shallowing. The capital deployment is getting more sophisticated, not less. But the IPO, when it comes, will be the true test of whether the Jio management class is truly independent or simply a talented extension of the family office.

VI. M&A and Capital Deployment: Buy vs. Build

The summer of 2020 will be remembered by Indian capital markets historians the way Americans remember the summer of 1995. It was the summer when the world came to invest in Jio. Between April 22 and July 15, 2020, across a span of roughly eighty-five days, Reliance Industries raised approximately $20 billion from thirteen global investors in exchange for minority stakes in the newly carved-out Jio Platforms Limited. This was not a funding round. It was a coronation.

The first call came from Menlo Park. On April 22, 2020, Facebook announced a $5.7 billion investment for a 9.99% stake in Jio Platforms, the largest minority investment ever made by the company outside the United States. For Mark Zuckerberg, the strategic logic was elegant. WhatsApp had 400 million users in India and no obvious path to monetization because India had blocked Facebook's Free Basics program in 2016. Jio, with its merchant payments ambitions and its small-store retail network through JioMart, gave WhatsApp an on-ramp to Indian commerce. For Mukesh, the deal was even more elegant. It anchored Jio at a pre-money valuation of roughly $66 billion, and once the price was set, every other global investor wanted in.

The floodgates opened. Silver Lake followed within days. Vista Equity Partners came next. General Atlantic. KKR. Mubadala. ADIA. TPG. L Catterton. Then, in July, Google announced a $4.5 billion investment for a 7.7% stake, bringing its Android and cloud relationships into the orbit. In less than three months, Jio Platforms went from a wholly-owned subsidiary of Reliance Industries to a company with thirteen blue-chip minority investors and a valuation north of $65 billion. The velocity of capital deployment was unprecedented in Indian corporate history, and it permanently changed the way global technology investors thought about the Indian market.

What did Jio do with the money, and what did it do with the capability that the money represented? The answer is a string of strategic acquisitions that reveal a very specific deployment philosophy. In April 2019, even before the 2020 fundraising, Jio had merged with Saavn, the Indian music streaming service, in a transaction that valued the combined entity at roughly $1 billion. On a pure subscriber-basis, that was expensive. Spotify, which entered India a few months earlier, was trading at a similar per-user valuation. But Jio was not buying Saavn for streaming economics. It was buying a localized content engine that could be bundled into telecom plans at essentially zero marginal cost. The "integration value" was enormous.

The pattern repeats itself. Haptik, a conversational AI and chatbot company, was acquired in April 2019 for roughly $100 million. On its own, Haptik was a small enterprise software business. Inside Jio, it became the layer that would eventually power customer service across the entire Jio app stack. Radisys, a 5G software company based in the United States, was acquired in June 2018 for $74 million. On its own, a mid-size network equipment firm. Inside Jio, it became the foundation of the domestically built 5G radio access network stack, a piece of intellectual property that allows Reliance to sell its 5G solution to other telecom operators globally without paying Ericsson or Nokia a cent in royalties.

And then there is cable. The acquisition of Den Networks and Hathway Cable, completed in October 2018 for a combined enterprise value of roughly $1 billion, gave Jio access to 27 million cable television homes and, more importantly, the physical last-mile connection into urban apartment buildings that would dramatically accelerate the rollout of JioFiber. Traditional fiber-to-the-home deployments take years of trenching and permitting. By acquiring existing cable operators, Jio collapsed that timeline by a decade in India's largest cities. This is what "platform premium" looks like in practice. You do not buy a business for its current EBITDA. You buy it for the integration value it unlocks across the rest of the stack.

VII. The Hidden Businesses and Segment Data

If you only read the financial statements of Reliance Industries, Jio looks like a big, well-performing telecom company with a hundred and fifty billion dollars of gross assets, a rising ARPU, and a mid-teens EBITDA margin expansion story. That view is correct but incomplete. What the financial statements do not fully capture is that Jio Platforms Limited is, increasingly, a holding company for five separate businesses, each of which has its own strategic logic, competitive dynamics, and long-term profit pool.

The first is the core connectivity business. This is the "utility" layer, the 4G and increasingly 5G wireless network plus the JioFiber home broadband service. By the end of 2025, Jio had crossed 490 million wireless subscribers and roughly 18 million home broadband customers, making it the largest connectivity provider in India by a significant margin. ARPUs have climbed from roughly 130 rupees in 2019 to roughly 210 rupees in early 2026, and the market is now in what analysts call a tariff repair cycle, with periodic price increases being passed through by all three remaining carriers. This is the cash-flow engine of the group.

The second business is JioCinema, which has quietly become the most aggressive content and streaming play in India. In 2022, the Viacom18 joint venture, in which Reliance holds a controlling stake alongside James Murdoch's Bodhi Tree Systems and Paramount Global, paid roughly $2.9 billion for the digital streaming rights to the Indian Premier League for five years. The IPL is, for Indian consumers, the NFL Super Bowl, the English Premier League, and the World Cup rolled into a seven-week annual pilgrimage. Putting it on JioCinema for free during the 2023 and 2024 seasons, and then transitioning to a hybrid advertising and subscription model, has delivered peak concurrency numbers that at times exceeded 60 million viewers, higher than any live-streamed event anywhere in the world at the time. In early 2024, Reliance announced the merger of its media assets with Disney's India business, creating a combined streaming and broadcasting behemoth with more than 750 television channels and two major streaming services. The content arm is no longer a bundle sweetener. It is a profit pool in formation.

The third business is JioMart and the broader commerce integration with Reliance Retail. This is the online-to-offline play, leveraging more than 18,000 physical Reliance Retail stores, three million kirana merchants onboarded through WhatsApp-enabled order flow, and the JioMart app for digital order fulfillment. The thesis is that e-commerce in India will not look like Amazon. It will look like a hybrid of corner shops, small merchants, and last-mile aggregators, all stitched together through software. JioMart is the spine of that stitching.

The fourth business, and the one that gets the least attention in sell-side research but may matter most to long-term investors, is the Jio 5G stack itself. Most of the world's telcos buy their 5G radio and core infrastructure from Ericsson, Nokia, Huawei, or Samsung. Jio, thanks to the Radisys acquisition and years of in-house engineering, built its own. By 2024, Jio was signaling that it planned to license that stack to other operators globally, particularly in markets where Chinese vendors had been restricted for security reasons. This is the software-as-a-service optionality embedded inside the telecom business, and if even a handful of international operators adopt the Jio stack, it becomes a genuinely high-margin revenue stream with platform-like economics.

The fifth is JioCloud and the broader AI initiative. In October 2024, Reliance announced a strategic partnership with NVIDIA to build AI infrastructure in India, including a one-gigawatt data center in Jamnagar powered by Reliance's own renewable energy assets. The strategic logic is to ensure that when Indian enterprises and consumers adopt AI services at scale, the underlying compute is Indian, not routed through US or European data centers. For a country that in 2026 had roughly 900 million internet users, the sovereignty argument is powerful, and it positions Jio as the default AI infrastructure layer for the Indian digital economy.

As these five businesses scale, the blended margin profile of Jio Platforms is shifting. A pure telco typically operates at EBITDA margins in the mid-thirties to low-forties. A digital platform business with content, commerce, and cloud mix can support margins in the mid-fifties or higher. The segment mix, and how quickly the non-telco segments grow, is the single most important driver of the eventual IPO valuation.

VIII. The Playbook: 7 Powers and 5 Forces

To understand why Jio is not just a successful telecom operator but a genuinely durable competitive position, it helps to run the business through the two analytical frameworks that long-term investors use to evaluate moats. The first is Hamilton Helmer's 7 Powers framework, which classifies the sources of sustainable advantage. The second is Michael Porter's Five Forces analysis, which classifies the structural pressures on a market. Jio scores remarkably well on both.

Start with scale economies, the first of the 7 Powers. Scale economies exist where per-unit cost declines as volume grows. In telecom, the fixed costs of spectrum, towers, and fiber backhaul are enormous, and the marginal cost of carrying an additional gigabyte of data is essentially zero. Jio, with its fully-owned fiber backbone, its all-IP network, and its 490 million subscribers, has the lowest cost per gigabyte in the world. Some estimates put it at roughly one-eighth of the equivalent cost for a US carrier. That cost advantage is structural and widening, because every additional subscriber spreads the fixed cost base across a larger denominator.

Switching costs are the second power, and Jio has been building them deliberately. The strategy has been to bundle the core connectivity product with every adjacent digital service the company can stitch in. A typical Jio household in 2026 might have a wireless plan, a JioFiber home broadband plan, a JioCinema subscription, a JioCloud storage account, a JioPay wallet, and a Jio set-top box for television. Each layer of the bundle raises the cost of switching, because leaving Jio now means disrupting not one service but six, and each service is subsidized by the others.

The third power, cornered resource, is where Jio's advantage is perhaps most unique. The nationwide 4G and 5G spectrum that Jio holds is finite and, under Indian regulatory frameworks, nearly impossible for a new entrant to replicate. The rights-of-way for 250,000 miles of fiber, negotiated over a decade with thousands of state and municipal authorities, are effectively non-replicable. And the Ambani industrial relationships, built over fifty years of oil, retail, and political access, are a form of capital that does not show up on any balance sheet but absolutely exists in practice.

Network effects, the fourth power, are less obvious in the core connectivity business but are central to the payments and commerce layers. Every additional merchant accepting JioPay makes the consumer side more valuable. Every additional consumer using JioPay makes it more worthwhile for merchants to adopt. The WhatsApp integration through the Facebook investment amplifies this loop, since India has more WhatsApp users than any country on earth. The network effect is still early, but it is structurally in motion.

Now flip to Porter's Five Forces. Rivalry in Indian telecom is low by global standards. After the extinction event, the market consolidated into a three-player oligopoly, with Jio at roughly 40% revenue market share, Airtel at roughly 35%, and Vodafone Idea at a diminished and still deteriorating 15%. The barriers to entry are effectively infinite. No rational investor is going to put $50 billion into a greenfield Indian telecom operator in 2026. Supplier power is limited, because Jio owns its own 5G stack and negotiates fiber, tower, and energy costs at massive scale. Buyer power is individually low, though the regulator, TRAI, acts as a collective buyer proxy and does exert periodic pressure on tariffs. Substitutes, in the form of satellite internet from Starlink or proposed sovereign wireless alternatives, exist but face their own regulatory and economic hurdles in India.

The overall picture is a business whose competitive position is, in structural terms, among the strongest of any consumer platform in the world. Whether that structural strength translates into durable earnings power for shareholders depends, as always, on execution, regulation, and the willingness of the family to let the listed entity optimize for its own shareholders rather than the broader conglomerate.

IX. Analysis: The Bear vs. Bull Case

At some point every great investment story narrows to two competing narratives, and Jio is no exception. The bull case and the bear case for the eventual Jio Platforms IPO are both articulable, both internally consistent, and both supportable with current data. Working through them carefully is the best way to understand what long-term investors are actually underwriting.

The bull case starts with the simple observation that India in 2026 has roughly 900 million internet users, 550 million smartphone owners, and a young demographic profile that will continue to add digital consumers for at least the next fifteen years. Inside that market, Jio has the largest subscriber base, the lowest unit costs, the most integrated product bundle, and a growing content and commerce stack that extracts value from the connectivity relationship well beyond the monthly recurring revenue line. If the platform roadmap continues to execute, Jio becomes something like the WeChat of India, a single application layer through which hundreds of millions of people conduct their communication, commerce, media consumption, and financial transactions. When the IPO prices, which most observers expect in 2026 or 2027, the conservative bull case models value Jio Platforms at somewhere between $120 billion and $180 billion, which would make it the largest offering in Indian history by a wide margin.

On top of the consumer platform thesis, the bull case layers in the 5G-as-a-service optionality, the NVIDIA-partnered AI infrastructure story, and the eventual monetization of the enterprise and government digital stack. There is also the balance sheet dimension. Reliance Industries, the parent, has spent the past three years aggressively deleveraging the group and simplifying the corporate structure, which sets up Jio for a cleaner spin or listing. The global blue-chip investor base anchored in 2020 provides a floor of institutional support and a pre-set group of cornerstone IPO buyers.

The bear case is not that any of this is wrong. The bear case is that a lot of it is already priced. At a pre-IPO marked-to-market implied valuation north of $100 billion, Jio is not trading at a discount to its future. It is trading at an aggressive premium. Indian regulators, particularly TRAI and the Competition Commission of India, have shown increasing willingness to scrutinize dominant market positions. Any meaningful anti-trust action, whether on telecom tariffs, on retail integration, or on content market power following the Disney deal, could reset the growth trajectory.

There is also the governance question. Reliance Industries, as a conglomerate, carries what global investors call a "conglomerate discount," the idea that the sum of the parts trades at less than their unaggregated value because of cross-subsidization, opaque capital allocation, and family control dynamics. If Jio Platforms is listed but Reliance Industries retains majority control, some of that discount simply migrates to the new listed entity. The spin mechanics matter enormously. A clean spin where Jio has independent governance, independent capital allocation, and alignment with minority shareholders is very different from a controlled listing where Jio remains a captive of the parent's broader capital needs.

Layered on top, there is execution risk. The content arm is betting enormous sums on premium sports rights whose inflation curve has been steep. The AI infrastructure build-out is capital-intensive and depends on adoption curves that are, in 2026, still early. The payments and commerce segments face entrenched competition from PhonePe, Paytm, Google Pay, and Amazon. None of these risks are fatal. But collectively, they mean that the path from today's implied valuation to the bull case requires the kind of execution that is easy to describe and genuinely hard to deliver.

The key performance indicators that matter most for tracking Jio from here are relatively few. First, blended ARPU trend, because this captures both the pricing power of the core business and the success of the bundle strategy. Second, non-connectivity revenue mix as a percentage of Jio Platforms total revenue, because this is the single best proxy for the platform transition. Third, EBITDA margin trajectory, because the shift from telco-low to platform-high margins is the earnings power lever that drives any credible IPO valuation. Track those three. Most of the noise resolves itself.

X. Epilogue and Final Reflections

In the end, the Jio story is not a telecom story. It is a story about what happens when a legacy industrial empire, sitting on a mountain of petrochemical cash and staring into the face of a technology transition it did not invent, decides to fund its own reinvention at a scale that no startup could ever command. The lesson, for anyone watching industrial dynasties navigate their own generational shifts, is that disruption from within is possible, but only when the incumbent is willing to cannibalize its own mental model. Mukesh Ambani did not enter telecom to win market share from Airtel. He entered telecom to change what the telecom business actually was. You cannot disrupt a market by being ten percent better. You have to change the unit of value from minutes to ecosystems.

Where Jio now sits in the pantheon of great companies is a question that will look different in five years than it does in 2026. If the platform thesis plays out and the IPO delivers, Jio will be remembered alongside Tencent, Alibaba, and Meta as one of the defining consumer platform companies of the early twenty-first century. If the conglomerate discount swallows the story, Jio will still be remembered as one of the boldest industrial pivots in history, but its equity returns will look more like a very good telecom investment than a transformative technology holding. Either way, the scale of what was built, at the speed at which it was built, in a country at the specific developmental moment in which it was built, is something that business historians will write about for decades.

The monsoon cliché that opens so many Indian business stories is worn thin, but it applies here. The rain fell, the wires went underground, the signal went up, and by the time the weather cleared, a billion people were online on a network that had not existed a decade earlier. The Ambani brothers split the empire in 2005. In 2026, only one side of that split is still standing, and it is standing taller than the original ever did.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube