Reliance Infrastructure: The Rise, Fall, and Resurrection of India's Infrastructure Conglomerate

I. Cold Open & Thesis

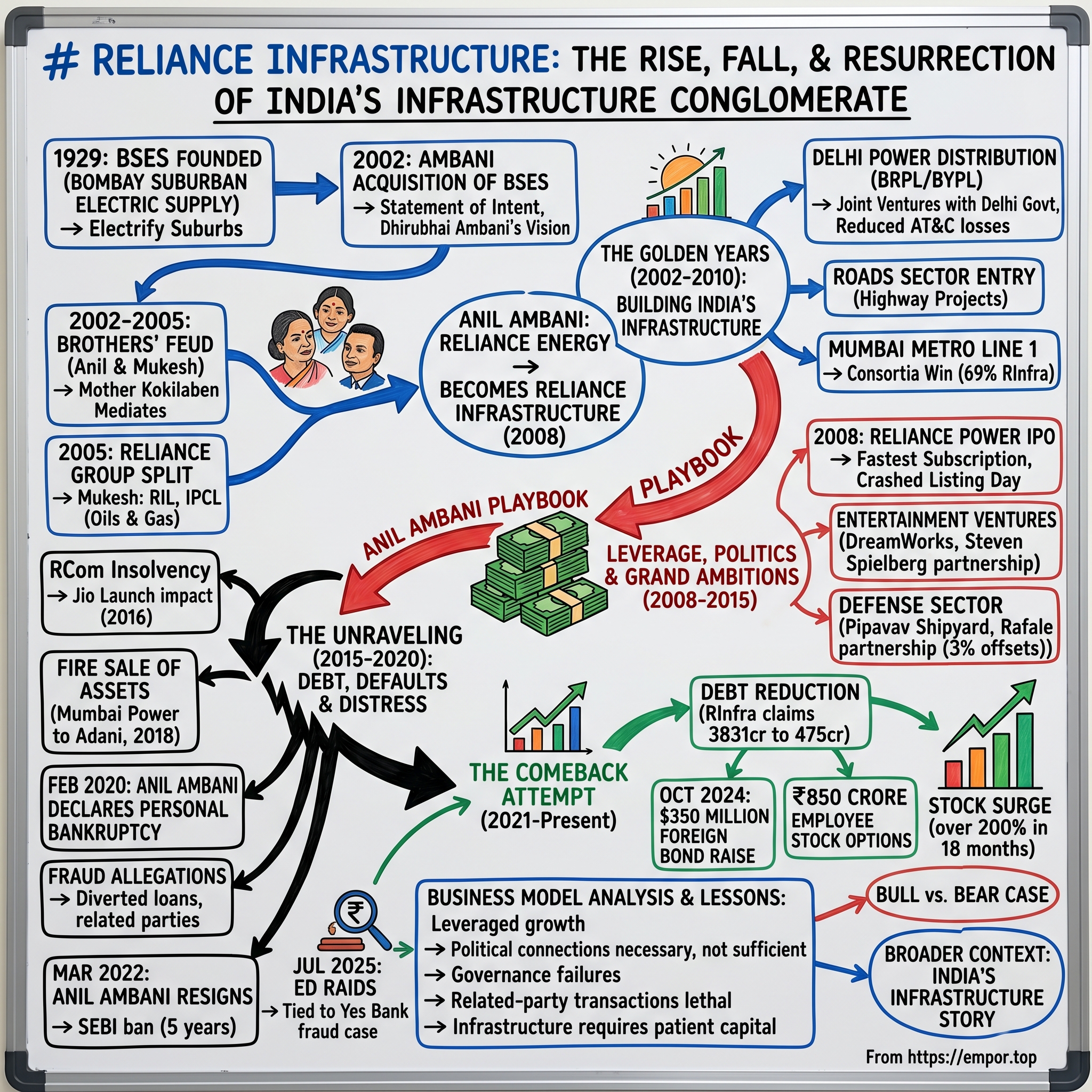

Picture this: February 2020, London's High Court. Anil Ambani, once India's sixth richest man with a fortune exceeding $42 billion, stands before a British judge and declares personal bankruptcy. His assets? Zero. His liabilities? Astronomical. The man who once controlled Mumbai's electricity grid, built gleaming metro lines, and commanded a business empire worth ₹1.7 lakh crore was now claiming he couldn't pay his debts.

Fast forward to October 2024. The same Reliance Infrastructure that seemed destined for liquidation announces a $350 million foreign bond raise. Its stock, written off by most investors, has surged over 200% in eighteen months. The company unveils an ₹850 crore employee stock option plan—a move typically reserved for growth companies, not those emerging from near-death experiences.

This is the paradox of Reliance Infrastructure: a company that refuses to die, yet struggles to truly live. It's a story that encapsulates everything magnificent and maddening about Indian capitalism—where political connections matter as much as profit margins, where bankruptcy doesn't necessarily mean the end, and where the line between resurrection and mirage remains perpetually blurred.

The question isn't just how a company that owned critical infrastructure across India's largest cities ended up in courts fighting for survival. It's how the same company, despite regulatory bans, fraud allegations, and credibility crises, continues to operate essential services and attract fresh capital. Is this the greatest comeback story in Indian corporate history, or the longest-running corporate zombie show?

What you're about to discover goes beyond one company's trajectory. This is the story of India's infrastructure dreams and nightmares, the perils of leveraged growth, and the extraordinary resilience—or stubbornness—of Indian promoters. It's about how essential services become political footballs, how debt can both build and destroy empires, and why in India, even bankruptcy comes with a sequel.

II. The BSES Foundation & Pre-Split Era

The monsoon of 1929 had been particularly harsh on Bombay. The city's primitive electrical infrastructure, a patchwork of private generators and unreliable municipal supply, had collapsed yet again. It was against this backdrop that a group of Parsi industrialists and British engineers came together in October to form the Bombay Suburban Electric Supply Company—BSES. Their mandate was audacious for the time: electrify the suburbs of what would become the world's most populous city.

For seven decades, BSES operated as the quintessential government undertaking—steady, inefficient, but indispensable. By the late 1990s, it supplied power to millions but hemorrhaged money with the reliability of Mumbai's local trains. The company's 83-year journey from colonial enterprise to socialist relic would have continued unremarkably, except for one development: Dhirubhai Ambani's sons were eyeing it.

The Ambani acquisition of BSES in 2002 wasn't just another corporate takeover—it was a statement of intent. Dhirubhai, who had passed away just months earlier, had built Reliance from a yarn trading operation into India's largest private company. His empire spanned petrochemicals, oil & gas, and telecommunications. But Dhirubhai understood something his competitors didn't: in a rapidly growing economy, whoever controlled the infrastructure controlled the future. The brothers' feud that erupted after Dhirubhai's death in July 2002 wasn't just a family squabble—it was a boardroom war that threatened to tear apart India's largest business empire. After the death of Dhirubhai Ambani in 2002, the management of the company was taken up by both the brothers. After bickering between Anil and his brother Mukesh, their mother Kokilaben mediated and split the family-owned businesses between the two brothers. For three years, Mukesh and Anil engaged in corporate warfare that played out in boardrooms, media leaks, and increasingly acrimonious public statements.

In October 2005, the split of Reliance Group was formalised. Mukesh Ambani got Reliance Industries and IPCL. Younger brother Anil Ambani received telecom, power, entertainment, and financial services business of the group. The younger Ambani, armed with an MBA from Wharton, inherited what many considered the sexier, higher-growth businesses—including the crown jewel that was Reliance Energy, which he would transform into Reliance Infrastructure in April 2008.

The split wasn't just about dividing assets; it was about diverging philosophies. Mukesh believed in the steady, capital-intensive business of petrochemicals and oil refining. Anil saw the future in infrastructure, telecommunications, and financial services—businesses that required massive leverage but promised outsized returns in a rapidly modernizing India. One brother chose the boring but profitable path of molecules; the other bet on electrons, concrete, and dreams.

What Anil inherited wasn't just a collection of assets—it was a platform to prove he could outshine his elder brother. And for a brief, shining moment, it seemed he might.

III. The Golden Years: Building India's Infrastructure (2002-2010)

The transformation of Delhi's power distribution system in 2002 was nothing short of revolutionary. When Reliance Energy took over BSES Rajdhani Power Limited (BRPL) and BSES Yamuna Power Limited (BYPL) as 51:49 joint ventures with the Delhi government, they inherited a disaster. Power theft was rampant—nearly 50% of electricity generated simply vanished into illegal connections. Bill collection rates hovered around 60%. The infrastructure was so decrepit that transformers regularly exploded during summer peak loads, plunging entire neighborhoods into darkness.

Anil Ambani's team approached this challenge with the precision of management consultants and the aggression of private equity operators. They installed tamper-proof meters, deployed flying squads to catch power thieves, and implemented GIS mapping to track every connection. Within five years, AT&C (Aggregate Technical & Commercial) losses dropped from 50% to under 30%. BRPL, serving 19 lakh consumers across South and West Delhi, became a case study at business schools. BYPL, with its 30 lakh consumers in East and Central Delhi, demonstrated that privatization could work even in politically sensitive essential services.

The numbers were staggering: 49 lakh consumers across India's capital now depended on Reliance for their electricity. This wasn't just a business—it was a stranglehold on Delhi's economic lifeline. Every mall, every factory, every middle-class home in vast swathes of the capital paid their power bills to Anil Ambani's companies. The monthly cash flow was predictable, regulated, and seemingly eternal.

But power distribution was just the beginning. In 2006, Reliance Infrastructure entered the roads sector, winning highway projects in Tamil Nadu. The logic was elegant: India needed $1 trillion in infrastructure investment over the next decade. The government had neither the money nor the expertise. Private players who could navigate the complex web of land acquisition, environmental clearances, and political negotiations would mint money.

The crown jewel of this expansion came with the Mumbai Metro Line 1 consortium win—a ₹23.56 billion project that would connect the eastern and western suburbs of India's commercial capital. This wasn't just about laying tracks; it was about transforming how millions of Mumbaikars commuted. The 11.4-kilometer Versova-Andheri-Ghatkopar corridor would carry 600,000 passengers daily, generating toll revenues for decades. The Mumbai Metro contract structure revealed Anil's strategic brilliance: MMOPL was promoted as a public–private partnership with equity participation from Reliance Infrastructure (69%), the Mumbai Metropolitan Region Development Authority (MMRDA) (26%), and Veolia Transport (5%). Later, RATP Dev Transdev Asia sold its 5% stake to MMOPL, resulting in Reliance Infrastructure increasing its shareholding to 74%. The project operated on a Build-Operate-Transfer basis, where the consortium will collect revenue for 35 years and then hand over the infrastructure to the government.

By 2010, Reliance Infrastructure wasn't just another infrastructure company—it was becoming India's infrastructure company. The company controlled power distribution networks serving millions, operated the country's first modern metro line, and was building highways across multiple states. Anil Ambani had successfully positioned himself as the face of India's infrastructure modernization.

The beauty of these businesses lay in their predictability. Power distribution generated steady cash flows—people always paid their electricity bills. Metro operations provided daily revenue streams from millions of commuters. Toll roads collected money 24/7. These weren't sexy tech businesses, but they were monopolies or near-monopolies in essential services. For an investor in 2010, Reliance Infrastructure looked like the perfect bet on India's growth story.

IV. The Anil Ambani Playbook: Leverage, Politics & Grand Ambitions (2008-2015)

The scene at the Bombay Stock Exchange on January 15, 2008, was unlike anything India's capital markets had witnessed. At 10 AM, when Reliance Power's IPO opened for subscription, the servers crashed within seconds. The IPO was subscribed in less than 60 seconds, the fastest in the history of Indian capital markets to date. By the time the three-day window closed, the issue was oversubscribed 73 times, with bids worth ₹7.5 lakh crore—nearly 10% of India's GDP at the time.

The ₹11,700 crore raised made it India's largest IPO ever. Anil Ambani had sold a dream—not just of power plants, but of powering India's future. The IPO prospectus promised 13,000 MW of generation capacity across multiple ultra-mega power projects. Retail investors mortgaged homes to subscribe. The grey market premium soared to ₹300 per share.

Then came the listing day—February 11, 2008. The stock opened at ₹430, below its issue price of ₹450, and promptly crashed to ₹372. Within hours, ₹60,000 crore of market value evaporated. The "disastrous listing" became a case study in market euphoria meeting reality. Investors who had borrowed to invest were wiped out. The media, which had breathlessly covered the IPO's success, now turned savage.

But Anil Ambani wasn't deterred. If anything, the Reliance Power IPO taught him a valuable lesson: in Indian markets, the story mattered more than the substance, at least initially. Between 2008 and 2015, he would apply this lesson repeatedly, raising capital against increasingly ambitious projections while leveraging political connections to win contracts. The entertainment ventures were particularly audacious. In 2005 Ambani made his debut in the entertainment industry with an acquisition of a majority stake in Adlabs Films, a company with interests in film processing, production, exhibition and digital cinema. The company was renamed Reliance MediaWorks in 2009. But the real coup came with Hollywood. In 2008 a joint venture worth US$1.2 billion with Steven Spielberg's production company DreamWorks cast Ambani's entertainment business on to a global platform.

The Spielberg deal wasn't just about money—it was about legitimacy. Here was an Indian businessman partnering with Hollywood royalty, financing films that would be watched globally. He has contributed to the production of several Spielberg films, including the Academy Award-winning Lincoln. For a brief moment, Anil Ambani wasn't just competing with his brother; he was playing on a global stage that Mukesh hadn't yet entered.

The infrastructure-politics nexus became increasingly evident during this period. Contracts for highways, airports, and power projects required not just capital but connections. Anil cultivated relationships across party lines—a necessity in India's fractious political landscape. He served in the Rajya Sabha, the upper house of the Parliament of India from Uttar Pradesh, as an Independent MP between 2004 and 2006. This wasn't vanity; it was strategic positioning.

By 2015, at the peak of his powers, Anil Ambani's empire was valued at ₹1.7 lakh crore. The group claimed to have "a customer base of over 100 million, the largest in India" across telecommunications, power, and infrastructure. The numbers were staggering, the ambition unlimited. But beneath the glossy annual reports and breathless media coverage, a dangerous reality was emerging: almost every expansion had been funded by debt.

The leverage that had turbocharged growth was becoming a noose. Interest payments were consuming cash flows. New projects required even more debt. The music would continue as long as asset values kept rising and banks kept lending. But in India's infrastructure sector, both assumptions were about to be severely tested.

V. The Unraveling: Debt, Defaults & Distress (2015-2020)

The first cracks appeared in Reliance Communications. Once India's second-largest telecom operator, RCom had borrowed heavily to fund spectrum purchases and network expansion. Then Mukesh Ambani launched Jio in September 2016 with free voice and data. Within months, the telecom industry's economics imploded. RCom's revenues collapsed from ₹20,000 crore to near zero. By 2017, the company was in insolvency proceedings.

But the real shock came with the Mumbai power sale. In August 2018, Anil announced he was selling Reliance Infrastructure's crown jewel—the Mumbai power transmission and distribution business—to Adani Transmission for ₹18,800 crore. This wasn't expansion or strategic repositioning; this was a fire sale. The business that generated predictable cash flows, that served millions of Mumbai's residents, was being sold to pay down debt.

The sale price itself told a story. Just five years earlier, the Mumbai power business had been valued at over ₹30,000 crore. Anil was selling at a 40% discount to pay creditors who were circling like vultures. The proceeds didn't go toward new investments or shareholder returns—they went straight to lenders who were threatening to pull the plug on the entire empire. The bankruptcy declaration in February 2020 was both shocking and predictable. In February 2020, Ambani was locked in a legal battle with three Chinese banks. He was asked to set aside US$100 million by the court which led him to make the statement that his net worth is currently zero after considering his liabilities. The man who once controlled billions claimed before a UK court that he couldn't pay his legal fees. His lawyers argued he was "a wealthy businessman and now he is not as a result of a 'disastrous turn of events' in the telecom market in India".

The fraud allegations added another layer to the collapse. In 2020, investigations revealed that loans worth ₹17,000 crore to RCom, Reliance Capital Finance Limited (RCFL), and Reliance Home Finance Limited (RHFL) showed signs of fraud. Money had allegedly been diverted to related parties, used for purposes other than stated in loan documents, and in some cases, simply disappeared into shell companies. The final humiliation came in March 2022. Anil Ambani stepped down from the boards of Reliance Infrastructure and Reliance Power, forced out by a SEBI order that restrained him from associating with any listed company. The man who had once commanded boardrooms across India was now legally barred from even serving as a director.

The regulatory crackdown revealed the extent of the rot. Investigations showed a pattern of related-party transactions, circular lending, and fund diversions that had kept the empire afloat long after its business model had failed. Banks that had eagerly lent during the boom years now classified the loans as fraud. Rating agencies that had maintained investment grades until the bitter end suddenly discovered what everyone else already knew—the emperor had no clothes.

By 2020, the Anil Ambani empire had effectively collapsed. From a peak market capitalization of ₹1.7 lakh crore, the listed entities were worth less than ₹5,000 crore. Shareholders who had invested in the Reliance Power IPO had lost 95% of their money. Banks wrote off tens of thousands of crores. Employees lost jobs. Vendors went unpaid. It was one of the most spectacular corporate collapses in Indian history.

Yet even in this devastation, the Delhi power distribution business continued to operate, generating cash, serving customers—a reminder that beneath the financial engineering and failed ambitions, there had been real assets, real businesses that might have thrived under different management.

VI. The Delhi Power Story: Crown Jewel or Albatross?

The morning of July 30, 2012, should have been Anil Ambani's vindication moment. Half of India—670 million people—had lost power in the world's largest blackout. But in Delhi, in the areas served by BSES Rajdhani Power Limited and BSES Yamuna Power Limited, the lights stayed on. While the national grid collapsed, Reliance's distribution network held firm, a testament to the operational improvements implemented over a decade.

The Delhi power story had begun in 2002 when the Delhi government unbundled the loss-making Delhi Vidyut Board (DVB). Three distribution companies emerged: BRPL and BYPL went to Reliance, while Tata Power took the third. It was India's largest power privatization experiment, and everyone was watching.

What Reliance inherited was a disaster masquerading as a utility. Power theft wasn't just common—it was culturally embedded. In areas like Seemapuri and Najafgarh, entire neighborhoods ran on illegal connections. Political parties actively protected power thieves, seeing them as vote banks. Collection rates in some areas were below 40%. The previous government utility had given up even trying to collect in certain neighborhoods.

The transformation strategy was part MBA case study, part street warfare. Reliance deployed technology—smart meters, aerial bunched cables that were harder to tap, GIS mapping of every connection. But technology alone wouldn't work in Delhi's complex social fabric. The company hired locals who knew the neighborhoods, who could negotiate with residents, who understood which battles to fight and which to postpone.

The numbers tell the story: AT&C losses dropped from 53% in 2002 to under 15% by 2015. The MMOPL earned a total revenue of ₹136 crore, and incurred losses of ₹191 crore. The revenues include ₹13.1 crore earned through leasing station space to 52 stalls across its 12 stations. The MMOPL said that it incurred an expenditure of ₹55 lakh per day to maintain the system and car depot. Collection efficiency improved from 60% to over 95%. The companies installed over 2 million electronic meters, upgraded thousands of transformers, and built new substations.

But success in operations didn't translate to financial success. The Delhi Electricity Regulatory Commission (DERC), under political pressure, refused to allow tariff increases that would cover costs. Regulatory assets—essentially IOUs from the government for under-recoveries—ballooned to over ₹20,000 crore. The companies were operationally profitable but financially strangled. In 2020, a potential exit appeared. NTPC Limited has appointed consulting firm EY as an advisor for acquiring Reliance Infrastructure Limited's Delhi electricity distribution businesses. In May 2020, NTPC had evinced interest to buy Reliance Infrastructure Limited's 51 per cent stake each in BSES Rajdhani Power Limited (BRPL) and BSES Yamuna Power Limited (BYPL). The state-owned power giant saw an opportunity to enter distribution, and Anil desperately needed cash.

But the deal collapsed. Reports suggest that NTPC backed out of the proposal as the bidding was not being conducted by Delhi Electricity Regulatory Commission (DERC). The regulatory commission, as further learnt, was not keen on overseeing the bidding process. The reality was more complex—NTPC discovered what every potential buyer discovered: the regulatory assets were essentially worthless without government guarantee, the political risk was enormous, and the operational challenges were daunting.

The current status reveals the fundamental paradox of these assets. Both the companies are joint ventures with the Delhi government. ADAG holds 51 per cent stake each in BYPL and BRPL, while the Government of NCT (National Capital Territory) of Delhi holds the remaining 49 per cent. They serve 4.4 million customers, generate steady cash flows, and have transformed from basket cases to functional utilities. Yet they remain unsellable at any reasonable valuation.

The political economy of Delhi power is Byzantine. Electricity tariffs are a political issue, decided not by economics but by electoral calculations. The AAP government, which came to power promising reduced electricity bills, cannot be seen allowing tariff increases. The result is a business that works operationally but is financially engineered to fail—profits are theoretical, cash is consumed by working capital, and value creation is impossible.

For Reliance Infrastructure, these distribution companies became both lifeline and millstone. They generate enough cash to keep the parent afloat but not enough to service its debts. They're too valuable to abandon but impossible to monetize. They represent everything that went right with Anil Ambani's operational strategy and everything that went wrong with his financial engineering.

VII. Defense, Airports & Other Adventures

The Rafale controversy of 2018 should have been Anil Ambani's moment of vindication in the defense sector. Here was Dassault, one of the world's premier defense contractors, choosing Reliance Defence as its Indian partner for the ₹58,000 crore fighter jet deal. But instead of triumph, it became another controversy, with opposition parties alleging crony capitalism and questioning why a company with no experience in aerospace was chosen over Hindustan Aeronautics Limited.

Reliance Defence, established in 2015, was Anil's most ambitious diversification. The company quickly assembled 11 subsidiaries spanning naval shipbuilding, aerospace, and land systems. The crown jewel was the acquisition of Pipavav Shipyard in 2016 for ₹819 crore—India's largest shipyard by dry dock capacity. The Dhirubhai Ambani Aerospace Park in Nagpur, spread across 289 acres, promised to become India's aerospace manufacturing hub.

The strategy seemed brilliant on paper. India planned to spend $250 billion on defense modernization over a decade. The government's "Make in India" push meant 30-50% of this would go to domestic manufacturers. Foreign defense companies needed Indian partners for offset obligations. Reliance Defence positioned itself as the perfect partner—it had infrastructure, political connections, and access to capital markets.

But defense is not infrastructure. The sales cycles span decades, not quarters. Technology transfer is complex and restricted. Manufacturing tolerances are measured in microns, not millimeters. Most critically, defense contracts require massive upfront investments with payments coming years later—exactly the wrong business model for a debt-laden conglomerate.

The Rafale partnership, instead of providing credibility, became a political football. In factual terms, Reliance Defence stood to get just over 3 per cent of the ₹30,000 crore Dassault Aviation offsets contract, contrary to the impression that it was to be the biggest beneficiary. But perception had already overtaken reality. No major defense contractor wanted to be seen partnering with a company under political scrutiny.

The airport ventures followed a similar trajectory. In March 2019, the company received a contract from the Airports Authority of India (AAI) worth ₹648 crores for the construction of Rajkot Greenfield Airport. But the Maharashtra airports saga was more telling. Reliance Infrastructure with its subsidiary company, Reliance Airport Developers Limited (RADL) operated five minor brownfield airports in various small towns of Maharashtra. In March 2015, the Government of Maharashtra was looking at cancelling the agreements and taking back control of the airports due to slow progress.

The pattern was consistent: win contracts through aggressive bidding and political connections, promise transformation, struggle with execution due to lack of capital, face regulatory and political backlash, either exit or operate at subsistence level. Each new venture was supposed to be the one that would turn things around. Each became another weight dragging down the empire.

VIII. The Comeback Attempt (2021-Present)

The stock charts from early 2024 defied all logic. Reliance Infrastructure, which had touched ₹5 in March 2020, surged past ₹300. Reliance Power, written off as worthless, jumped from ₹2 to ₹45. In trading rooms across Mumbai, the same question echoed: was this the greatest comeback in Indian corporate history or the last gasp of a dying conglomerate? In October 2024, Reliance Infrastructure board has approved raising of $350 million (Rs 2,930 crore) through ultra-low cost 10-year maturity unsecured foreign currency convertible bonds (FCCBs). The board also approved the employees stock option scheme (ESOPs), which will provide a grant of up to 26 million equity shares of value of over Rs 850 crore. For a company that had been written off, these were extraordinary developments.

The FCCB structure was telling. A 5% coupon for 10-year unsecured bonds from a company with Reliance Infrastructure's history should have been impossible. Yet VFSI Holdings Pte Limited, an affiliate of Varde Investment Partners, was willing to bet $350 million. Were they seeing value others missed, or were they the greater fools in a market bubble? Reality check arrived in July 2025. In a dramatic turn of events, the Enforcement Directorate (ED) launched raids on July 24, 2025, targeting over 35 premises linked to Anil Ambani's Reliance Group, just as the conglomerate was poised for a significant fundraising push. The raids, tied to an alleged ₹3,000 crore bank loan fraud and money laundering case involving Yes Bank and group entities like Reliance Communications (RCOM) and Reliance Home Finance (RHFL), have raised eyebrows due to their timing and the questionable relevance of decade-old allegations.

The investigations revealed patterns that had been suspected but never proven. According to investigators, the fraud occurred during the period between 2017 and 2019, when Yes Bank sanctioned loans to RAAGA companies. Just before the disbursement of loans, ED has found, "the Yes Bank promoters received money in their concerns," suggesting a suspected quid pro quo. Shell companies, circular transactions, evergreening of loans—the playbook was familiar to anyone who had followed Indian corporate scandals. The August 2024 SEBI order was devastating. SEBI has imposed a penalty of Rs 25 crore on Ambani and restrained him from being associated with the securities market including as a director or Key Managerial Personnel (KMP) in any listed company, or any intermediary registered with the market regulator, for a period of five years. The 222-page order detailed a fraudulent scheme where funds from Reliance Home Finance were siphoned off through loans to credit-unworthy entities linked to the promoter group.

Yet even after the ban, the stock prices continued their rally. The market seemed to be betting that Anil Ambani, like a phoenix, would rise again. The ₹850 crore ESOP scheme announced alongside the FCCB raise suggested confidence—or desperation. Why would employees want stock options in companies run by a man banned from the securities market?

The answer might lie in the peculiar dynamics of Indian markets. Retail investors, burned repeatedly, still believed in the Reliance name. Day traders saw volatility as opportunity. And perhaps most importantly, the assets—especially the Delhi power distribution business—still had value, regardless of who controlled them.

IX. Business Model Analysis & Lessons

The infrastructure conglomerate model that Anil Ambani pursued wasn't inherently flawed—it was the execution that killed it. Infrastructure businesses require three things: patient capital, operational excellence, and political navigation skills. Anil had the third in abundance, achieved the second in pockets, but catastrophically failed at the first.

The capital intensity of infrastructure is brutal. A power plant takes 5-7 years to build and 20 years to pay back. A metro line requires billions upfront with revenues trickling in over decades. Roads and airports follow similar patterns. This model works when you have either deep pockets (like the Adanis post-2014) or access to cheap, long-term capital (like Chinese infrastructure companies). Anil had neither.

Instead, he relied on financial engineering. Short-term loans funded long-term projects. Corporate guarantees backed special purpose vehicles. Complex cross-holdings obscured true leverage. For a while, rising asset values and India's growth story kept the music playing. But infrastructure businesses don't forgive leverage—one delayed project, one regulatory change, one economic downturn, and the entire edifice collapses.

The regulatory risk in essential services compounds the challenge. When you run Delhi's power distribution, you're not just a businessman—you're a public servant who happens to be in the private sector. Tariffs are politically determined. Service standards are publicly scrutinized. Every power cut becomes a political issue. The business model assumes rational regulation, but Indian politics rarely provides it.

What went wrong was a toxic combination of over-leverage, poor timing, and governance failures. The leverage is obvious—debt-to-equity ratios that would make private equity firms blush. The timing was unfortunate—Anil expanded aggressively just as India entered a decade-long investment slowdown post-2011. But the governance failures were unforgivable. Related-party transactions, fund diversions, and regulatory violations weren't accidents—they were choices.

The dangers of related-party transactions deserve special mention. When RHFL lent to shell companies that funneled money to other group entities, it wasn't just illegal—it was destroying the very foundation of the business. Trust, once broken in financial services, is almost impossible to rebuild. Every related-party transaction is a withdrawal from the bank of credibility, and Anil's companies made too many withdrawals.

What's working now is instructive. The Delhi distribution business continues to function because electricity distribution, despite all its challenges, generates predictable cash flows. The asset-light pivot—focusing on EPC and operations rather than ownership—makes sense but comes too late. The financial engineering capabilities that got them into trouble might, ironically, help them restructure their way out.

The lesson for investors is clear: in infrastructure, leverage is poison, governance is everything, and political connections are necessary but not sufficient. The best infrastructure investors—whether Brookfield, Macquarie, or successful Indian players like L&T—understand that infrastructure is ultimately a boring business that should generate boring returns. The moment it becomes exciting, you're probably doing it wrong.

X. Bull vs. Bear Case

The Bull Case starts with the assets. Despite everything, Reliance Infrastructure still controls valuable infrastructure. The Delhi power distribution business serves millions and generates steady cash flows. The company claims to have reduced debt from ₹3,831 crore to ₹475 crore. If true, this deleveraging changes everything. An infrastructure company without crushing debt can actually create value.

India's infrastructure boom is real and accelerating. The government plans to spend ₹100 lakh crore on infrastructure by 2030. Private players with execution capabilities and existing assets will benefit disproportionately. Reliance Infrastructure, despite its troubles, has operational expertise. They know how to run power distribution, build roads, and operate metros. In infrastructure, experience matters.

Management's financial engineering skills, for all their past misuse, could be valuable in restructuring. The FCCB raise at 5% for a company with Reliance Infrastructure's history shows either incredible salesmanship or hidden value. The stock price surge suggests the market sees something beyond the obvious troubles.

Political connections and relationships still matter in Indian infrastructure. Despite the controversies, the Reliance name still opens doors. In a sector where government is the biggest customer and regulator, relationships are assets—intangible but real.

The Bear Case is equally compelling. The governance and credibility issues are possibly irreparable. When SEBI bans your chairman for five years, when ED raids your offices, when banks classify your loans as fraud, the reputational damage is permanent. No serious institutional investor will touch these stocks. No reputable partner will join ventures. No talented executive will stake their career on a turnaround.

The regulatory overhang is massive. The SEBI ban runs until 2029. ED investigations continue. Multiple cases are in various courts. Any positive development gets overshadowed by the next regulatory action. This isn't a cloud that will pass—it's a permanent weather system.

Competition from better-capitalized players is intense. The Adanis have unlimited access to capital. Tata Power has credibility. New players like Brookfield and Singapore's GIC are entering Indian infrastructure with clean balance sheets and global expertise. Why would anyone choose Reliance Infrastructure as a partner?

The track record of value destruction is undeniable. From ₹1.7 lakh crore market cap to under ₹10,000 crore. From India's largest IPO to penny stock status. From infrastructure champion to cautionary tale. Past performance doesn't guarantee future results, but it certainly suggests them.

The most likely scenario lies between these extremes. The company will probably survive—infrastructure assets are too valuable and essential services too critical for complete collapse. But thriving seems impossible given the governance overhang. It's likely to remain a zombie company—alive but not really living, generating enough cash to service restructured debt but never enough to create real value.

XI. The Broader Context: India's Infrastructure Story

The Reliance Infrastructure saga can't be understood without understanding India's infrastructure journey. Post-1991 liberalization, India faced a choice: continue with public sector monopolies that were inefficient but accountable, or privatize and risk regulatory capture. It chose a messy middle path—public-private partnerships that combined the worst of both worlds.

The privatization model assumed that private efficiency would overcome public inefficiency. In some cases—telecom, airlines, banking—this worked. But infrastructure is different. The assets are immovable, the services essential, the politics unavoidable. When Delhi's power was privatized, it wasn't really privatized—it became a regulated private monopoly, which is an oxymoron that captures everything wrong with the model.

Reliance Infrastructure is both a product and a victim of this confusion. It assumed privatization meant freedom to operate commercially. The government assumed it meant private capital would fund public services. The result was a business model that satisfied neither profit requirements nor public service obligations.

The role of promoter-driven conglomerates adds another layer. In developed markets, infrastructure is dominated by focused specialists—Vinci in construction, National Grid in power transmission, Macquarie in infrastructure finance. In India, conglomerates do everything, leveraging relationships and capital across unrelated businesses. This works until it doesn't.

Regulatory capture versus public interest is the eternal tension. When infrastructure companies get too close to regulators, public interest suffers. When regulators strangle companies, investment dries up. Reliance Infrastructure managed to achieve both—too close to power when it suited them, abandoned when it didn't.

The global comparison is instructive. China built world-class infrastructure through state-owned enterprises with unlimited capital and no accountability. America built its infrastructure through regulated utilities with stable returns and strong governance. India tried to build infrastructure through leveraged conglomerates with political connections and weak governance. The results speak for themselves.

XII. Closing Thoughts & Key Takeaways

The resilience of Indian promoters is extraordinary, bordering on the pathological. Anil Ambani declared bankruptcy, was banned from capital markets, had his companies raided, yet still announces new ventures and stock options. This isn't resilience—it's denial of reality. Or perhaps it's the ultimate expression of Indian entrepreneurship: the refusal to accept defeat even when defeated.

Infrastructure as a political business is the central lesson. You can't separate infrastructure from politics because infrastructure is politics made concrete. Every road connects constituencies. Every power line carries votes. Every metro station is a political statement. Reliance Infrastructure understood this but thought political connections were sufficient. They weren't.

The importance of capital allocation cannot be overstated. Anil Ambani had access to more capital than almost any Indian entrepreneur—through inheritance, IPOs, and debt. He destroyed nearly all of it through poor allocation. Building infrastructure with short-term debt is like building a house on sand—it might stand for a while, but the first storm will destroy it.

Corporate governance in emerging markets remains the achilles heel. The concentration of power in promoters, the weakness of independent directors, the malleability of auditors—these aren't bugs but features of the system. Reliance Infrastructure exploited every weakness until the weaknesses destroyed them.

What this means for India's infrastructure future is sobering. India needs $1.5 trillion in infrastructure investment this decade. If the Reliance Infrastructure model is what private participation looks like—leveraged, politically connected, governance-challenged—then India needs a different model. Perhaps the future is sovereign funds and global infrastructure specialists. Perhaps it's a return to public sector dominance. Perhaps it's something new entirely.

The Reliance Infrastructure story isn't over. Companies this entangled in essential services don't simply disappear. They lumber on, zombie-like, generating enough cash to survive but not enough to thrive. For investors, the lesson is clear: in infrastructure, boring is beautiful, leverage is lethal, and governance is everything.

For India, the lesson is more complex. The country needs infrastructure, but it also needs to decide what kind of capitalism it wants. The Reliance Infrastructure model—politically connected conglomerates using public markets to fund private ambitions—has failed. What replaces it will determine not just India's infrastructure future but the nature of Indian capitalism itself.

The final irony is that Anil Ambani might still prove everyone wrong. Stranger resurrections have happened in Indian business. But even if he does, the cost has been too high—thousands of crores destroyed, millions of shareholders impoverished, and trust in Indian infrastructure companies permanently damaged. Some victories aren't worth winning. Some resurrections aren't worth celebrating.

This is the tragedy of Reliance Infrastructure: a company that could have been India's infrastructure champion became its cautionary tale. In trying to build everything, it built nothing lasting. In trying to be everywhere, it ended up nowhere. In trying to create an empire, it created ruins.

The empire may yet be rebuilt. The stock prices suggest some believe it will be. But empires built on weak foundations collapse, and those rebuilt on the same foundations collapse again. That's not pessimism—that's physics. And physics, unlike stock prices, doesn't lie.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube