Reliance Industries: The Empire That Digitized India

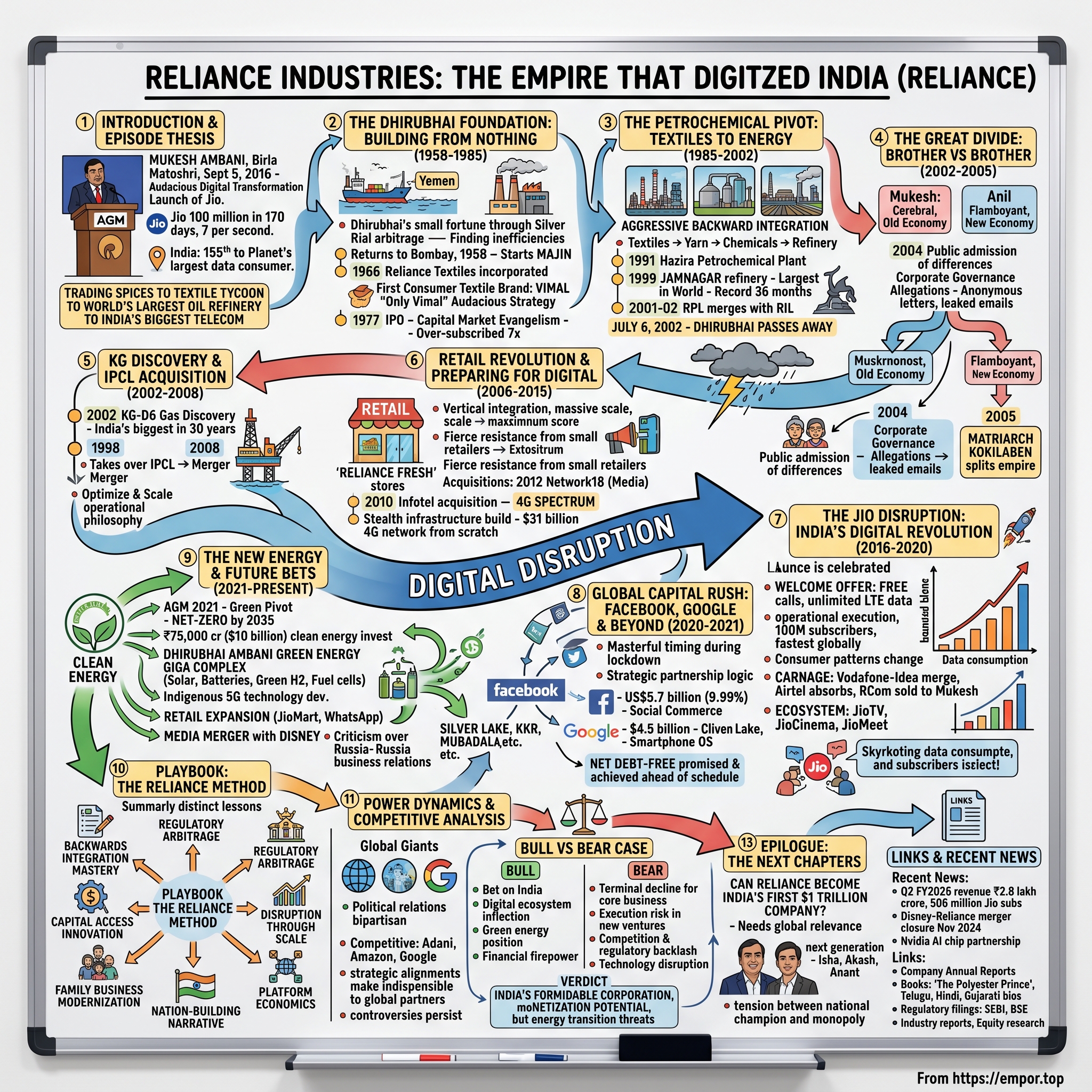

I. Introduction & Episode Thesis

Picture this: September 5, 2016. The Reliance Annual General Meeting at Mumbai's Birla Matoshri Sabhagar auditorium. Mukesh Ambani, India's richest man, steps up to the podium and makes an announcement that would fundamentally alter the trajectory of 1.3 billion lives. Jio's commercial rollout—with free voice calls and unlimited LTE data until December 31, 2016—wasn't just another telecom launch. It was the opening salvo in what would become the most audacious digital transformation of any nation in modern history.

The numbers tell a story of breathtaking velocity. Within 170 days, Jio crossed the 100-million customer mark on its 4G LTE network, adding nearly seven customers on its network every second, every day. India, which ranked 155th in the world for mobile broadband internet access, would catapult to become the planet's largest consumer of mobile data within a year. But this is merely the final chapter of a much grander narrative.

How does a company that began trading spices in a 350-square-foot Bombay office transform into India's largest public company by market capitalization and revenue, accounting for 7% of India's total merchandise exports? How does a textile trader's son from a village in Gujarat build an empire that today spans from the world's largest oil refinery to India's biggest telecom network?

The answer lies not in a single strategic masterstroke but in a six-decade playbook of vertical integration, regulatory navigation, and an almost mystical ability to align corporate ambition with national aspiration. This is the story of Reliance Industries—a company that didn't just adapt to India's economic liberalization; it helped write the script. A company that turned the burden of infrastructure building into a moat so wide that competitors drowned trying to cross it. A company that understood, perhaps better than any other, that in a nation of a billion aspirations, the real power lay not in serving the elite but in democratizing access to everything from polyester to pixels.

As we trace this journey from yarn to broadband, from Dhirubhai's legendary capital market innovations to Mukesh's digital revolution, we'll uncover the DNA of what might be the most consequential business story of the Asian century. Because Reliance isn't just a company—it's a thesis on how emerging markets create their own rules, their own capital structures, and ultimately, their own destinies.

II. The Dhirubhai Foundation: Building from Nothing (1958-1985)

The monsoon of 1958 brought more than rain to Bombay. It brought Dhirubhai Ambani back from Yemen, carrying with him ₹50,000 he had earned at Aden and a vision that would reshape Indian capitalism. The young man who had spent nearly a decade working his way up from gas station attendant to trading floor operator at A. Besse & Co. in Aden had observed something profound in the dusty ports of Yemen—something that would become the cornerstone of the Reliance empire.

In those early Yemen years, Dhirubhai had pulled off what might be history's most elegant currency arbitrage. Treasury officials in Yemen noticed their country's currency, the solid silver rial, was mysteriously vanishing from circulation. The trail led them to Aden, where they discovered young Dhirubhai had placed an open order for as many rials as he could obtain. He realized that the silver content of the rial was worth more than its exchange value, so he began purchasing rials, melting them down, and selling the silver ingots to bullion dealers in London. Despite small margins, it was profitable, and Dhirubhai amassed a small fortune.

This wasn't just clever trading—it was a masterclass in seeing value where others saw only currency. It was this lens—finding inefficiencies and arbitraging them relentlessly—that Dhirubhai would bring to every business he touched.

Ambani returned to India and started "Majin" in partnership with Champaklal Damani, his second cousin. Majin was to import polyester yarn and export spices to Yemen. But partnerships, Dhirubhai would learn, could constrain ambition. By 1965, the partnership dissolved, and Dhirubhai continued alone with what would become Reliance Commercial Corporation, set up in 1958 as a small venture firm trading commodities, especially spices and polyester yarn.

The real transformation began in 1966. Reliance Textiles Industries Pvt. Ltd. was incorporated in Maharashtra. It established a synthetic fabrics mill in the same year at Naroda in Gujarat. This wasn't just another textile mill in a country already crowded with them. Dhirubhai understood something his competitors didn't: in a nation where clothing was still largely unbranded, where textile traders operated in the shadows of wholesale markets, there was an opportunity to create India's first true consumer textile brand.

Enter Vimal—named after Dhirubhai's nephew. Named after his nephew, Vimal Ambani (Ramnikbhai's son), Dhirubhai established this clothing venture in the late 1960s, marking the beginning of Reliance Textiles Industries Limited in Naroda, Gujarat. What Dhirubhai did with Vimal was revolutionary for its time. Vimal, one of the earliest brands under Reliance's consumer-facing textile portfolio, dates back to the 1970s. Known for its popular tagline "Only Vimal," the brand holds a strong legacy in the Indian menswear and suiting market.

The Vimal strategy was audacious. Owing to its superior quality, Dhirubhai had priced Vimal higher than other brands. Initially, the textiles were not readily accepted by wholesalers in Ahmedabad and Bombay. The warehouse piled up with unsold stocks built up over four months. These stocks were then sold directly to retailers, bypassing wholesalers, in some cases by Dhirubhai himself. The retailers, impressed by the Reliance team's efforts, put all their efforts into Reliance products.

But Dhirubhai's true genius lay not in textiles but in understanding capital markets in a way that no Indian industrialist had before. The company held its initial public offering in 1977. The issue was over-subscribed by seven times. This wasn't just capital raising—it was capital market evangelism. Dhirubhai didn't just want institutional investors; he wanted the aam aadmi, the common man. He would hold shareholder meetings in stadiums, personally addressing thousands of small investors who had never before owned a piece of corporate India.

The 1980 polyester revolution marked another inflection point. The company expanded its polyester yarn business by setting up a Polyester Filament Yarn Plant in Patalganga, Raigad, Maharashtra with financial and technical collaboration with E. I. du Pont de Nemours & Co. This wasn't just about adding capacity—it was about backward integration, a strategy that would become Reliance's signature move. Control your supply chain, control your destiny.

By 1985, as the company prepared to change its name from Reliance Textiles Industries Ltd. to Reliance Industries Ltd., Dhirubhai had built something unprecedented: a company that was simultaneously a manufacturing powerhouse, a consumer brand, and a mass movement. The boy from Chorwad who had started with ₹50,000 had created a blueprint for how businesses could be built in the unique context of post-independence India—navigating the license raj, mobilizing retail capital, and most importantly, making every Indian feel like they could own a piece of the India growth story.

III. The Petrochemical Pivot: From Textiles to Energy (1985-2002)

The year 1985 marked more than a name change for Reliance. The company changed its name from Reliance Textiles Industries Ltd. to Reliance Industries Ltd—a signal that Dhirubhai's ambitions had outgrown the textile mills of Naroda. What followed was perhaps the most aggressive backward integration strategy ever executed by an Indian corporation, a move so bold that it would transform not just Reliance but the entire structure of Indian industry.

The logic was deceptively simple yet revolutionary in execution. If you made textiles, why not make the yarn? If you made the yarn, why not make the chemicals that created it? And if you made the chemicals, why not refine the oil from which those chemicals derived? Each step backward in the supply chain was a step toward complete control, toward margins that compounded at every level of production.

The Hazira petrochemical plant was commissioned in 1991-92, marking Reliance's entry into the petrochemicals business at scale. But the real moonshot came in 1999. The years 1998-2000 saw the construction of the integrated petrochemical complex at Jamnagar in Gujarat, the largest refinery in the world. Built in a record 36 months, the Jamnagar refinery wasn't just large—it was a statement of intent. While global oil majors took five to seven years to build refineries half its size, Reliance had created a 27-million-tonne behemoth that could process the heaviest, cheapest crudes that others couldn't touch.

The numbers from this period tell a story of breathtaking expansion. During 1985 to 1992, the company expanded its installed capacity for producing polyester yarn by over 145,000 tonnes per annum. By 2001, Reliance Industries Ltd. and Reliance Petroleum Ltd. became India's two largest companies in terms of all major financial parameters. In 2001-02, Reliance Petroleum was merged with Reliance Industries, creating an integrated giant that controlled the entire value chain from oil to textiles.

Yet this period of extraordinary growth was overshadowed by what was coming. On July 6, 2002, at Mumbai's Breach Candy Hospital, the lights dimmed on one of India's greatest entrepreneurial stories. Dhirubhai suffered from a major stroke on June 24th, 2002 and was admitted to Breach Candy Hospital, breathing his last shortly after on July 6th 2002. The patriarch who had built Reliance from nothing left behind not just a business empire but a succession crisis that would tear apart India's most powerful business family.

The founder's death exposed what had been simmering beneath the surface for years. Mukesh, the elder son, cerebral and strategic, had been driving the petrochemicals and refining expansion. Anil, younger and more flamboyant, had been the face of Reliance's capital markets operations and newer ventures. Dhirubhai passed away in 2002 and did not leave a will. Mukesh became chairman and managing director, while Anil became vice-chairman. Everything looked fine, but a storm was brewing beneath the surface.

What should have been a period of consolidation after the patriarch's death instead became a very public unraveling. The seeds of destruction had been sown in the very success that Dhirubhai had created—an empire so vast that two ambitious sons couldn't share it, a legacy so powerful that dividing it would reshape Indian business forever.

IV. The Great Divide: Brother vs Brother (2002-2005)

The mahogany boardroom on the 16th floor of Maker Chambers IV had seen many battles—with competitors, with regulators, with market forces. But nothing had prepared it for the war that erupted between its two vice-chairmen in the months following Dhirubhai's death. What began as strategic differences over capital allocation morphed into something far more primal: a struggle for the soul of India's largest private enterprise.

In November 2004, Mukesh in an interview admitted to having differences with Anil over ownership issues. He also said that the differences "are in the private domain". The CNBC-TV18 interview was a watershed moment—the first public acknowledgment that all was not well in the house that Dhirubhai built. For a family that had always presented a united front, where business disputes were settled in the prayer room of Sea Wind, their Cuffe Parade residence, this admission was seismic.

The specifics of the dispute read like a Shakespearean tragedy wrapped in a corporate thriller. Mukesh believed in the old economy—petrochemicals, refining, the heavy industries that generated predictable cash flows. Anil championed the new—telecommunications, financial services, entertainment. Mukesh saw capital as something to be preserved and deployed carefully. Anil saw it as fuel for aggressive expansion into sunrise sectors. These weren't just business disagreements; they were fundamentally different visions of what Reliance should become in the 21st century.

The corporate governance allegations that surfaced during this period pulled back the curtain on how the empire actually operated. Anonymous letters to regulators, leaked emails to financial newspapers, board meetings that descended into shouting matches—the spectacle transfixed corporate India. Here was the country's most powerful business family destroying itself in full public view, each faction using the media as a weapon, each brother marshaling loyal executives like generals positioning troops.

By early 2005, the situation had become untenable. Independent directors threatened to resign. Institutional investors, particularly foreign funds that had poured billions into Reliance, demanded clarity. The stock price, which had been the family's report card to the nation, gyrated wildly with each new revelation. Something had to give.

Enter Kokilaben, the matriarch who had stood beside Dhirubhai through his journey from yarn trader to tycoon. On June 18, 2005, she did what boards, lawyers, and mediators couldn't: she divided an empire. After a massive feud, their mother Kokilaben inked a deal to split Reliance Industries into two parts. Reliance Industries including petrochemicals, oil & gas exploration, refining and textiles went to Mukesh Ambani.

The split, valued at ₹99,000 crore at the time, was surgical in its precision. Mukesh retained the original Reliance Industries Ltd.—the petrochemicals, oil and gas, refining, and textiles businesses that generated the bulk of the revenues. Anil received Reliance Communications (telecom), Reliance Capital (financial services), Reliance Energy (power), and Reliance Natural Resources. It was a division that reflected not just assets but aspirations: Mukesh got the foundation, Anil got the future—or so it seemed.

Critically, the brothers signed a non-compete agreement that would prevent either from entering the other's domain. This clause, intended to prevent further conflict, would become a ticking time bomb that would explode a decade later with devastating consequences for one brother.

The post-split period revealed the true cost of the division. Reliance, which had operated as an integrated ecosystem where each business supported the other, was now two separate entities competing for capital, talent, and market position. Vendors who had dealt with one Reliance now had to choose sides. Employees who had spent careers building the empire watched as offices were divided, letterheads changed, and colleagues became competitors.

Yet in this destruction lay the seeds of transformation. Freed from the burden of consensus, Mukesh could now execute his vision without compromise. The conservative older brother, as the world would soon discover, had been harboring ambitions that would make his father's boldest moves look tentative. The stage was set for the next act: turning an old-economy giant into the architect of India's digital revolution.

V. The Krishna Godavari Discovery & IPCL Acquisition (2002-2008)

Even as the Ambani family was tearing itself apart in Mumbai's boardrooms, 1,500 kilometers away in the Bay of Bengal, drilling platforms were probing depths that would reshape India's energy security forever. In 2002, just months after Dhirubhai's death, Reliance announced India's biggest gas discovery in nearly three decades at the Krishna Godavari basin—one of the largest gas discoveries in the world during 2002. The KG-D6 block, with reserves estimated at 7 trillion cubic feet, wasn't just a gas field; it was validation of Mukesh's vision of Reliance as an integrated energy giant.

The timing was poetic. While brothers fought over who would inherit the empire, the empire itself was literally striking gold—or in this case, natural gas—beneath the ocean floor. The discovery came after years of expensive exploration, with many writing off Reliance's upstream ambitions as costly folly. The company had bid aggressively for exploration blocks during the New Exploration Licensing Policy rounds, committing billions to what many saw as speculative ventures. The KG-D6 discovery vindicated this strategy spectacularly.

But Mukesh understood that controlling energy resources meant nothing without the ability to process them. In 1998, Reliance took over Indian Petrochemicals Corporation Limited during privatization of public sector enterprises. The IPCL acquisition, formally completed through merger in 2008, wasn't just about adding capacity. This was about acquiring technology, talent, and most importantly, legitimacy in the petrochemicals space. IPCL brought with it decades of research, established customer relationships, and a network of production facilities that would have taken Reliance years to build organically.

The integration of IPCL revealed Mukesh's operational philosophy: acquire, optimize, and scale. Where IPCL had operated with public sector inefficiencies, Reliance brought private sector urgency. Plants that had run at 70% capacity were pushed to 95%. Product lines that had remained static for decades were upgraded with new polymer technologies. The workforce, initially resistant to the aggressive Reliance culture, was won over through a combination of performance incentives and the promise of being part of something transformational.

By 2008, Reliance's energy and petrochemicals businesses weren't just large—they were systemically important to India. The company was refining 1.24 million barrels of oil per day, producing polymers that went into everything from packaging to automotive parts, and sitting on gas reserves that could power Indian homes and factories for decades. Revenue had crossed $45 billion, making Reliance India's largest private sector company by a considerable margin.

The non-compete agreement with Anil, signed during the 2005 split, began to chafe during this period. Anil's Reliance Natural Resources claimed rights to gas from KG-D6 at prices far below market rates, based on a pre-split understanding. Mukesh refused, arguing that post-split agreements superseded earlier arrangements. The dispute, which would drag through courts for years, was more than a commercial disagreement—it was a continuation of the fraternal war by other means.

Yet these disputes, dramatic as they were, couldn't obscure a larger truth: Mukesh was methodically positioning Reliance for a future that went beyond hydrocarbons. The 2010 acquisition of Infotel Broadband Services Limited, the only company to win pan-India 4G spectrum in government auctions, initially puzzled observers. Why would an oil and petrochemicals giant want broadband spectrum? The answer would become clear soon enough, but first, there was an empire to build in the physical world.

VI. Retail Revolution & Preparing for Digital (2006-2015)

The year 2006 marked an inflection point that few recognized at the time. Reliance entered the organised retail market in India with the launch of its retail store format under the brand name of 'Reliance Fresh'. By the end of 2008, Reliance Retail had close to 600 stores across 57 cities. To outside observers, this looked like diversification for its own sake—an oil company selling vegetables. But Mukesh was playing a longer game, one that wouldn't become apparent for another decade.

The retail entry was vintage Reliance: massive scale from day one, vertical integration wherever possible, and a willingness to lose money for years to build market position. Reliance Fresh stores sprouted across urban India with remarkable speed. The company built its own supply chain, partnering directly with farmers, cutting out the medieval system of middlemen that had inflated food prices for generations. Cold chains, warehouses, logistics networks—infrastructure that should have taken decades to build appeared in years.

The resistance was fierce. Small retailers, who saw extinction in Reliance's arrival, organized protests. Several states, under pressure from trading communities that formed powerful vote banks, banned or restricted Reliance Retail's operations. Stores were vandalized, supply trucks burned, employees threatened. The company that had conquered complex industries like petrochemicals found itself struggling to sell tomatoes and onions.

But Mukesh's team persisted, adapting the model, learning from failures, and most importantly, building capabilities that transcended retail itself. They were creating India's most sophisticated supply chain network, developing technology systems that could track millions of SKUs, and perhaps most crucially, understanding the Indian consumer at a granular level that no company had attempted before.

In parallel, strange acquisitions were being made that seemed disconnected from the core business. In 2012, Reliance acquired Network18, giving it control of television channels like CNN-IBN, CNBC-TV18, and numerous digital properties. Critics called it vanity—a billionaire buying media influence. But Mukesh's team saw content as another form of infrastructure, as essential to the digital age as pipelines were to the petroleum age.

The masterstroke came in 2010. Reliance entered the broadband services market with acquisition of Infotel Broadband Services Limited, which was the only successful bidder for pan-India fourth-generation (4G) spectrum auction. The acquisition, made through a ₹4,800 crore deal just minutes after Infotel won the spectrum, raised eyebrows. Why would a petrochemicals and retail company want 4G spectrum that even established telecom players had avoided due to lack of ecosystem readiness?

What followed was one of the greatest stealth infrastructure builds in corporate history. While Anil's Reliance Communications struggled with debt and declining market share, Mukesh was secretly investing what would eventually amount to $31 billion in building a 4G network from scratch. No 2G legacy infrastructure to upgrade, no 3G investments to protect—just a pure 4G network designed for the data age.

The non-compete agreement with Anil was formally scrapped in 2010, freeing Mukesh to enter telecommunications. The timing was crucial. Smartphone prices were dropping, data consumption was beginning to spike globally, and India's young population was increasingly digital-native but still largely offline due to high data costs. The pieces of a massive disruption were falling into place.

Teams were hired from global telecom companies, often at multiples of their existing salaries. Towers were erected across the country—over 100,000 of them—in an infrastructure rollout that dwarfed even government programs. Fiber optic cables were laid—250,000 kilometers worth—creating a backbone that could handle the data explosion Mukesh's team was planning to trigger. Testing began in December 2015 with employees and partners, who couldn't quite believe what they were experiencing: speeds that matched global benchmarks at prices that seemed like accounting errors.

In 2010, Reliance and BP announced a partnership in the oil and gas business. BP took a 30 per cent stake in 23 oil and gas production sharing contracts for $7.2 billion. Reliance also formed a 50:50 joint venture with BP for sourcing and marketing gas in India. The BP deal provided not just capital but validation—one of the global oil majors was betting big on Reliance's energy future, providing the financial flexibility to fund the massive telecom investment.

By early 2016, the preparations were complete. Reliance had spent six years and over $30 billion building a network that didn't have a single commercial customer. The retail operations had created physical touchpoints across India. The media acquisitions had built a content library. The spectrum was secured, the network was tested, and the applications were ready.

The stage was set for what would become the most disruptive product launch in Indian corporate history. The boy from Chorwad's son was about to change how 1.3 billion people connected to the world.

VII. The Jio Disruption: India's Digital Revolution (2016-2020)

The Birla Matoshri auditorium was packed beyond capacity on September 1, 2016. Shareholders had queued since dawn, many traveling hundreds of kilometers to hear what Mukesh Ambani would announce at Reliance's 42nd Annual General Meeting. The speculation had been building for months. Test users had been leaking screenshots of impossible data speeds at unbelievable prices. Competitors had been scrambling to raise capital, sensing a storm approaching. When Mukesh finally took the stage and uttered the words "Jio Welcome Offer," he unleashed forces that would transform not just India's telecom industry but the entire trajectory of the nation's digital economy.

Domestic voice calls to any network across the country would be free for Jio subscribers even beyond the Welcome Offer. Roaming services would be absolutely free, across India and at any time. In an industry where voice revenues still constituted the majority of operator earnings, where roaming charges were a meaningful profit center, Jio had just announced that the core product was now free. Forever.

But free voice was just the appetizer. Reliance offered customers an irresistible deal—4GB of data a day for free until December 31, 2016. In a country where only 24.3% of Indians accessed mobile web and average usage was 400MB per month, Jio was offering 120GB per month at zero cost. The math didn't just break industry economics—it shattered them.

The operational execution of the launch was as audacious as the pricing. Long queues formed outside Reliance Digital stores nationwide as millions scrambled to get a Jio SIM card. The company activated 1.6 million subscribers in the first month. By day 83, it had crossed 50 million. Within 170 days, Jio crossed 100 million subscribers, becoming the fastest telecom operator in the world to reach this milestone.

The transformation in consumption patterns was immediate and staggering. Jio users consumed more than 100 crore GB of data per month—more than 3.3 crore GB a day. Jio carried nearly 5.5 crore hours of video daily on its network. India, which had been a footnote in global data consumption statistics, was suddenly the world's largest consumer of mobile data within a year.

The industry carnage was swift and merciless. Vodafone India and Idea Cellular decided to merge to form a new entity, creating what briefly became India's largest telecom operator by subscriber count—a defensive consolidation that spoke to the existential threat Jio posed. Bharti Airtel absorbed Tata Teleservices' consumer mobile business, another forced consolidation in the face of the Jio onslaught.

But perhaps no casualty was more poignant than that of Anil Ambani's Reliance Communications. Within six months of Jio's launch, younger brother Anil ended up selling his telecom firm Reliance Communications to Mukesh. The company that had once been India's most valuable telecom operator, that had pioneered CDMA technology in India, was essentially worthless in the face of Jio's assault. The younger brother who had dreamed of building his own empire was forced to surrender to the elder he had once fought so bitterly.

Jio wasn't just offering cheap data—it was building an ecosystem. JioTV brought live television to mobile phones. JioCinema offered Bollywood and regional content. JioSaavn, acquired for $104 million, provided music streaming. JioMeet, launched during the pandemic, attempted to challenge Zoom and Google Meet. Each app was free for Jio subscribers, creating switching costs that went beyond just network effects.

The infrastructure investment continued even after launch. By 2019, Jio had deployed over 350,000 base stations, more than any other operator globally had built in such a short time. The company was adding 10 million subscribers every month, each generating data traffic that would have crashed networks built for the voice era. Yet Jio's network, built from scratch for the data age, handled the load with remarkable stability.

By 2019, Jio had overtaken Airtel and Vodafone-Idea to become India's largest telecom operator. In just three years, a company that didn't exist commercially had captured over 35% market share in one of the world's most competitive telecom markets. The speed of conquest was unprecedented in global telecom history.

The strategic implications went far beyond market share. Jio had fundamentally changed how Indians viewed data—from a luxury to be rationed to an abundant resource to be consumed freely. This shift enabled everything from digital payments adoption to video streaming to e-commerce growth. Companies like Google, Facebook, and Amazon, which had struggled to reach beyond urban India, suddenly found hundreds of millions of new users coming online, fundamentally altering their global growth trajectories.

By early 2020, as the pandemic began to spread globally, Jio had over 380 million subscribers. The network that Mukesh had spent six years secretly building was about to become critical infrastructure for a nation that would soon be forced entirely online. But first, there was capital to be raised and partnerships to be forged that would value this digital transformation at scales that would have seemed fantastical just years earlier.

VIII. The Global Capital Rush: Facebook, Google & Beyond (2020-2021)

April 22, 2020. The world was in lockdown, equity markets were in freefall, and most corporations were hoarding cash. It was precisely at this moment that Mark Zuckerberg and Mukesh Ambani announced a deal that would redefine how global tech giants approached emerging markets. Facebook acquired a 9.99% stake in Jio Platforms for ₹43,574 crore (US$5.7 billion). This wasn't just an investment—it was Silicon Valley's admission that the future of the internet would be written in markets like India, and that local partners like Reliance were essential to that future.

The timing of the Facebook deal was masterful. Just weeks earlier, on March 23, 2020, India had announced one of the world's strictest lockdowns. Digital services went from convenience to necessity overnight. Students needed broadband for online classes. Office workers needed stable connections for video calls. Small businesses needed digital payment systems to survive. Jio, with its 388 million subscribers and integrated digital ecosystem, wasn't just a telecom operator—it was the rails on which locked-down India ran.

The Facebook investment valued Jio Platforms at approximately $66 billion, making it one of the largest foreign direct investments in India's history. But the strategic logic went beyond financial returns. Facebook's WhatsApp had over 400 million users in India but no clear monetization path. Reliance had millions of retail touchpoints through its stores but needed digital capabilities to compete with Amazon and Flipkart. Together, they envisioned JioMart orders placed through WhatsApp, connecting India's 30 million kirana (neighborhood) stores to digital commerce—a vision that could fundamentally restructure Indian retail.

What followed was one of the most remarkable fundraising runs in corporate history. In May 2020, private equity firm Silver Lake obtained a 1.15% stake with a ₹5,650 crore investment. Days later, Silver Lake doubled down, investing another ₹4,547 crore. General Atlantic announced it would invest ₹6,598.38 crore for a 1.34% stake. KKR acquired a 2.32% stake for ₹11,367 crore.

The parade of investors read like a who's who of global finance. Mubadala acquired a 1.85% stake for ₹9,093.60 crore. Abu Dhabi Investment Authority bought a 1.16% stake for ₹5,683.50 crore. TPG took a 0.93% stake worth ₹4,546.80 crore. L Catterton made an investment of ₹1,894.50 crore for a 0.39% stake.

Then came Google. On July 15, 2020, Sundar Pichai and Mukesh Ambani announced Google's $4.5 billion investment in Jio Platforms. Beyond the capital, the partnership involved jointly developing an affordable Android-based smartphone operating system, custom-built for India's unique needs. This wasn't just about building phones—it was about ensuring that the next 500 million Indians coming online would do so through a Jio-Google ecosystem.

Reliance raised more than $20 billion for Jio Platforms from global giants. This funding validated Jio's vision of becoming a digital ecosystem, not just a telecom operator. In just 12 weeks, during a global pandemic, Mukesh had raised over $20 billion, selling approximately 33% of Jio Platforms while maintaining firm control. The velocity was breathtaking—sometimes multiple deals were announced in the same week.

The capital wasn't just about the money, though the money was important. Each investor brought something strategic. Facebook brought social commerce expertise. Google brought technology capabilities. Silver Lake brought experience scaling technology companies. KKR and other financial investors brought global networks and operational expertise. This wasn't just fundraising—it was strategic alliance building on a massive scale.

Crucially, this capital raising fulfilled a promise Mukesh had made at the 2019 AGM: to make Reliance net debt-free by March 2021. Through the Jio Platforms stake sales, combined with a ₹53,125 crore rights issue (India's largest ever) and the sale of 49% stake in Reliance's fuel retail business to Rosneft for ₹7,000 crore, Reliance achieved net debt-free status ahead of schedule. The company that had been criticized for aggressive borrowing to fund Jio's buildout had engineered one of corporate history's great deleveraging acts.

The implications extended beyond Reliance. The Jio Platforms fundraising demonstrated that Indian technology companies could attract valuations comparable to their global peers. It showed that despite geopolitical tensions and economic uncertainty, global capital still saw India as the most attractive long-term growth market. And perhaps most importantly, it validated a new model for emerging market technology companies—one that combined local infrastructure and relationships with global technology and capital.

By the end of 2020, Jio Platforms had transformed from a telecom operator into something unprecedented: a technology platform valued at over $100 billion, backed by the world's leading technology companies and financial investors, with ambitions that spanned from connecting rural India to competing with global technology giants. The son of the polyester prince had built a digital empire that his father, for all his vision, could never have imagined.

IX. The New Energy & Future Bets (2021-Present)

June 24, 2021. At Reliance's 44th Annual General Meeting—held virtually, a sign of the times—Mukesh Ambani made an announcement that would have seemed heretical coming from the chairman of India's largest fossil fuel company: Reliance would achieve net-zero carbon emissions by 2035, and would invest ₹75,000 crore ($10 billion) in clean energy over three years. The company that had built its fortune on petrochemicals and oil refining was pivoting toward green hydrogen, solar manufacturing, and energy storage. The transformation wasn't just ambitious—it was existential.

The Dhirubhai Ambani Green Energy Giga Complex, announced for Jamnagar, would span 5,000 acres and house four giga factories: solar photovoltaic modules, energy storage batteries, electrolyzers for green hydrogen, and fuel cells. The scale matched Mukesh's traditional playbook—go big or go home—but the technology pivot represented something new. For the first time, Reliance was betting on technologies where it had no incumbent advantage, where Chinese companies dominated global supply chains, and where the economics remained uncertain.

The green hydrogen ambition was particularly audacious. Reliance announced plans to bring green hydrogen costs down to $1 per kilogram by 2030—a price point that would make it competitive with fossil fuels. The company partnered with Denmark's Stiesdal to develop hydrogen electrolyzers, with Ambri for grid-scale battery systems, and continued acquiring companies with complementary technologies. This wasn't just about manufacturing solar panels—it was about reimagining Reliance for a post-carbon future.

Meanwhile, the 5G rollout that began in October 2022 demonstrated that the core telecom business hadn't lost momentum. Jio launched standalone 5G services across major Indian cities, promising pan-India coverage by the end of 2023. True to form, the rollout velocity was staggering. While competitors struggled with the economics of 5G deployment, Jio leveraged its dense fiber network and existing tower infrastructure to achieve coverage at a fraction of typical costs.

The 5G strategy revealed another ambition: indigenous technology development. Unlike the 4G network that relied heavily on Samsung and other foreign vendors, Jio announced it was building an indigenous 5G solution in collaboration with global partners. The goal wasn't just to deploy 5G but to export it—to position Reliance as a global telecommunications equipment vendor competing with Huawei, Ericsson, and Nokia.

The retail and technology ventures continued expanding in parallel. Jio expanded its presence in fixed broadband and digital commerce through JioFiber and JioMart. By 2024, JioMart had integrated with WhatsApp, allowing customers to order groceries through the messaging app—the vision articulated during the Facebook investment finally becoming reality. The retail business, now run by Mukesh's daughter Isha Ambani, generated over ₹2.6 lakh crore in revenue annually, making it India's largest retailer by a considerable margin.

The succession planning, always a sensitive topic given Reliance's history, proceeded smoothly. Isha Ambani runs the retail leg, Akash Ambani heads Reliance Jio, and Anant Ambani is in charge of the new green energy business. Each child controlled a distinct vertical, avoiding the overlap that had caused fraternal conflict in the previous generation.

Recent developments have maintained the momentum. In February 2024, Reliance and BharatGPT Group announced they would launch Hanuman AI, a large language model working in 11 local languages across health, governance, financial services, and education. Reliance and Disney announced a deal to merge their streaming and television assets, closed in November 2024 with a reported value of $8.5 billion. In October 2024, Reliance entered into an agreement with Nvidia to procure Blackwell chips for its planned data center in Jamnagar.

But challenges loom. Reliance has faced criticism for maintaining business relations with Russia despite sanctions. The company has been listed on Leave Russia platform for remaining active in the Russian market. In December 2024, Reliance entered into a contract with Rosneft to procure 500,000 barrels of oil per day for 10 years, worth around $13 billion annually. The reputational risk of these relationships in an increasingly polarized geopolitical environment cannot be ignored.

As of September 2024, Reliance Jio has crossed the 500 million subscriber milestone, cementing its position as one of the world's largest telecom operators. The company that didn't exist commercially a decade ago now serves more subscribers than the entire population of the United States and European Union combined.

The new energy investments, while promising, face execution risks. Solar manufacturing confronts Chinese dominance and overcapacity. Green hydrogen economics remain unproven at scale. The battery storage market is fiercely competitive. Whether Reliance can replicate its telecom disruption in clean energy remains the defining question of Mukesh's final act as chairman.

X. Playbook: The Reliance Method

After six decades of evolution from a spice trading firm to a $220 billion conglomerate, certain patterns emerge that constitute what might be called the "Reliance Method"—a distinctly Indian approach to building and scaling businesses that has lessons for emerging market companies worldwide.

Backwards Integration Mastery

The Reliance playbook begins with a simple insight: in markets with weak infrastructure and unreliable suppliers, controlling your supply chain isn't just an advantage—it's survival. Dhirubhai didn't just make textiles; he made the yarn that went into them, then the chemicals that made the yarn, then refined the oil that made the chemicals. This backwards integration created compound margins that competitors couldn't match. When Mukesh built Jio, he didn't just operate a network—he laid his own fiber, built his own towers, and even designed his own devices. Control the stack, control your destiny.

Regulatory Arbitrage as Core Competency

While critics called it crony capitalism, Reliance's ability to navigate—and shape—India's regulatory environment was a legitimate competitive advantage. The company didn't just comply with regulations; it anticipated them, influenced them, and built businesses around regulatory windows that others missed. The 2010 Infotel acquisition minutes after winning 4G spectrum wasn't luck—it was preparation meeting opportunity. Every major Reliance business was built on a regulatory insight, from the decontrol of polyester licensing in the 1980s to the spectrum auctions of 2010.

Capital Access Innovation

Dhirubhai revolutionized Indian capital markets by making ordinary Indians shareholders. The 1977 IPO wasn't just oversubscribed—it created an equity cult that persists today. Mukesh took this further, accessing global capital at crucial moments. The 2020 Jio Platforms fundraising during a pandemic wasn't just about the $20 billion raised—it was about validating the business model through the endorsement of global tech giants. Each generation of Reliance leadership has pioneered new forms of capital access that others later copied.

Disruption Through Scale

Reliance never entered a business to be a marginal player. When it built refineries, it built the world's largest. When it launched telecom services, it gave away free data until competitors buckled. This wasn't recklessness—it was recognition that in capital-intensive industries with network effects, half-measures don't work. Go big, go fast, and make the market conform to your economics rather than the reverse.

Family Business Modernization

Despite the 2005 split, Reliance solved a challenge that destroys most Asian family businesses: professionalizing management while maintaining family control. The company recruited global talent, paid competitive salaries, and gave professional managers real authority—while ensuring the family remained the ultimate decision-makers. The current generation's smooth succession planning, with each child running distinct verticals, shows learning from past mistakes.

Nation-Building Narrative

Perhaps most importantly, Reliance positioned every major business initiative as serving national interest. Textiles would clothe India. Petrochemicals would industrialize India. Jio would digitize India. Green energy would decarbonize India. This wasn't just marketing—it was a worldview that aligned corporate expansion with national development, making opposition to Reliance seem like opposition to progress itself. Critics might call it cynical, but the consistency with which Reliance has executed this positioning across decades suggests genuine belief.

Platform Economics in an Analog World

Long before "platform" became a Silicon Valley buzzword, Reliance was building them. The textile business created a distribution platform. Retail created a physical platform. Jio created a digital platform. Each business became infrastructure for the next, creating cumulative advantages that pure-play competitors couldn't replicate. When Jio launched, it could leverage Reliance Retail stores for distribution, Reliance Capital for device financing, and Network18 for content—ecosystem advantages that no amount of capital could quickly replicate.

The Reliance Method isn't universally applicable—it requires patient capital, regulatory relationships, and scale that few companies can muster. It's also not without controversy, with critics pointing to market dominance, regulatory capture, and the societal costs of such concentration of power. But as a case study in how emerging market companies can build global-scale businesses despite infrastructure deficits, capital constraints, and institutional weaknesses, it remains unmatched.

XI. Power Dynamics & Competitive Analysis

The Reliance boardroom on the 16th floor of Maker Chambers IV isn't just a corporate headquarters—it's arguably the second most powerful address in India after the Prime Minister's Office. The company's influence extends through every corridor of power, transcending political parties, surviving regime changes, and growing stronger with each transition. Understanding Reliance means understanding how power actually works in the world's largest democracy.

The political relationships are remarkably bipartisan. Dhirubhai cultivated connections across the political spectrum, from Indira Gandhi's Congress to the BJP's early leaders. Mukesh has maintained this tradition, appearing equally comfortable with Narendra Modi as he was with Manmohan Singh. This isn't just about donations or lobbying—it's about positioning Reliance as essential to India's economic architecture, making it too big to fail and too important to antagonize.

The competitive landscape has shifted dramatically. Where once Reliance competed with the Birlas and Tatas in textiles, today it faces Gautam Adani in infrastructure, Amazon in retail, and Google in technology. In August 2024, Mukesh was surpassed as the wealthiest Indian by Gautam Adani, though such rankings fluctuate with stock prices. The Adani Group's aggressive expansion into airports, ports, and green energy directly challenges Reliance's ambitions, creating a rivalry that echoes the great business battles of the License Raj era.

The international partnerships reveal sophisticated power dynamics. The BP partnership in oil and gas, Facebook and Google investments in Jio, and the recent Disney merger aren't just business deals—they're strategic alignments that make Reliance indispensable to global corporations' India strategies. When Facebook needs to monetize WhatsApp in India, it needs Reliance. When Disney wants to compete with Netflix in India, it needs Reliance. This positioning as the essential local partner for global giants is perhaps Mukesh's greatest strategic achievement.

Yet controversies persist. The company has attracted controversy for reports of political corruption, cronyism, fraud, financial manipulation, and exploitation of its customers, Indian citizens, and natural resources. Its chairman, Mukesh Ambani, has been described as a plutocrat. The gas pricing dispute with the government, the allegations of spectrum allocation favoritism, and the concerns about market dominance in telecom have all reinforced perceptions of Reliance as a company that bends rules to its advantage.

The succession dynamics are being carefully managed. Unlike the chaos that followed Dhirubhai's death, Mukesh has clearly delineated responsibilities among his three children while he remains active. Akash running Jio, Isha leading retail, and Anant heading new energy ventures creates clear domains while maintaining family unity. The children have been gradually introduced to public roles, speaking at investor meetings and leading strategic initiatives, preparing them for eventual leadership.

The market power across verticals is staggering. In telecom, Jio serves over 500 million subscribers. In retail, Reliance is India's largest player with over ₹2.6 lakh crore in revenue. In refining, the Jamnagar complex remains among the world's largest. In petrochemicals, it's India's dominant player. This diversification creates resilience—when oil prices crash, telecom compensates; when telecom competition intensifies, retail provides stability.

Global comparisons are instructive. Reliance resembles Korea's chaebols like Samsung—family-controlled conglomerates that dominate multiple industries. It echoes the Japanese zaibatsu of the pre-war era—vertically integrated industrial giants with close government ties. Yet it's uniquely Indian in its retail investor base, its alignment with national development goals, and its ability to straddle both old and new economies simultaneously.

The regulatory capture concerns are real but complex. Reliance's influence on policy is undeniable—from polyester decontrol in the 1980s to spectrum allocation in 2010 to recent e-commerce regulations. Yet this influence isn't unidirectional. The government has also used Reliance to achieve policy goals, from industrialization in the 1980s to digital inclusion through Jio. It's a symbiotic relationship where both parties benefit, though consumers and competitors often bear the costs.

Looking ahead, the power dynamics face new challenges. Rising inequality has made concentrated wealth politically sensitive. Global ESG concerns make fossil fuel businesses increasingly problematic. Technology regulation worldwide is trending toward breaking up, not enabling, corporate giants. Whether Reliance can navigate these headwinds while maintaining its influence remains to be seen.

XII. Bull vs Bear Case

The Bull Case: Proxy for India's Inevitable Rise

The optimistic view of Reliance isn't just about the company—it's about betting on India itself. With 1.4 billion people, a median age of 28, and GDP growth consistently above 6%, India represents the last great growth market. Reliance, touching every aspect of Indian life from the fuel in vehicles to the data on phones, is the purest play on this growth story.

The digital ecosystem is reaching inflection points everywhere. Jio's 500 million users generate massive data that can be monetized through advertising, commerce, and financial services. The retail footprint of 18,000+ stores creates an omnichannel advantage that pure-play e-commerce companies can't match. The integration possibilities—ordering through WhatsApp, paying through JioMoney, delivering through Reliance Retail—create winner-take-all dynamics in multiple verticals.

The energy transition, paradoxically, strengthens Reliance's position. The company's petrochemical products are essential for solar panels, wind turbine blades, and electric vehicle components. The $10 billion green energy investment positions it to dominate India's renewable sector just as it dominated telecom. The existing Jamnagar infrastructure can be repurposed for green hydrogen production, turning a potential stranded asset into a competitive advantage.

Strategic partnerships de-risk execution. Facebook and Google's investments weren't just capital—they were technology transfer agreements. BP's partnership brings deep-water drilling expertise. The Disney merger creates content advantages. These aren't passive investors but active partners with incentives to ensure Reliance's success.

The financial firepower is unprecedented for an emerging market company. With operational cash flows exceeding ₹100,000 crore annually and a net debt-free status, Reliance can invest through cycles, absorb competitive attacks, and pursue opportunities that smaller players can't contemplate. The ability to spend $31 billion building Jio before earning a rupee of revenue won't be replicated by competitors.

The Bear Case: Icarus Flying Too Close to the Sun

The pessimistic view sees multiple structural challenges converging. The core petrochemicals and refining businesses face terminal decline as the world shifts to renewables. Demand for petroleum products has likely peaked in developed markets and will peak in India within a decade. The Jamnagar refineries, however efficient, risk becoming stranded assets in a decarbonizing world.

Execution risk in new ventures is material. Reliance has never manufactured solar panels at scale, where Chinese companies have 90%+ market share and massive cost advantages. Green hydrogen remains economically unviable without massive subsidies. The company's track record in new industries—remember Reliance Power under Anil—isn't uniformly successful.

Regulatory backlash is building. The dominance in telecom has triggered concerns about monopolistic behavior. E-commerce regulations targeting preferential treatment for select sellers affect JioMart's model. Data localization and privacy laws constrain the monetization of Jio's user base. The political winds that once favored large conglomerates are shifting toward populist suspicion of concentrated wealth.

Competition is intensifying everywhere. In telecom, Airtel has stabilized and is matching Jio's 5G rollout. In retail, Quick Commerce players like Blinkit and Zepto are redefining consumer expectations. In energy, Adani Green Energy is executing faster. The era of entering industries late and winning through scale is ending as markets mature and competitors wise up to Reliance's playbook.

The governance concerns persist despite professionalization. The family controls 50.3% of shares, making minority shareholders essentially silent partners. Related party transactions, while legal, create conflicts of interest. The concentration of power in one individual—Mukesh as Chairman and Managing Director—lacks the checks and balances modern governance demands.

Technology disruption cuts both ways. While Reliance disrupted telecom with Jio, it could itself be disrupted by satellite internet from Starlink or Amazon's Kuiper. The massive infrastructure investments in towers and fiber could become liabilities if satellite technology achieves cost parity. Similarly, the retail footprint could become an albatross if e-commerce adoption accelerates beyond projections.

The Verdict

The truth, as always, lies between extremes. Reliance remains India's most formidable corporation, with capabilities, capital, and connections that ensure relevance for decades. The digital transformation through Jio has created a platform with enormous monetization potential. The succession planning appears smoother than the previous generation.

Yet the challenges are real. The energy transition threatens the cash cow businesses. The execution risk in new ventures is substantial. The regulatory and competitive environment is less favorable than in Dhirubhai's era. The stock market valuation—at over ₹19 lakh crore market cap—prices in perfect execution across multiple ambitious ventures.

XIII. Epilogue: The Next Chapters

Standing in his father's office, surrounded by black-and-white photographs of textile mills and polyester plants, Mukesh Ambani must sometimes wonder what Dhirubhai would make of today's Reliance. The company that began with trading spices in 350 square feet now operates from a headquarters that occupies an entire building in Mumbai's business district. The firm that went public to raise ₹2.8 crore in 1977 now has a market capitalization exceeding ₹19 lakh crore. The founder who celebrated selling fabric to retailers would marvel at algorithms selling data plans to half a billion Indians.

Yet in fundamental ways, nothing has changed. The ambition to build at nation-scale remains. The ability to see around corners—from textile demand in the 1970s to data consumption in the 2010s—persists. The conviction that Reliance's success and India's progress are intertwined continues to drive strategy. Dhirubhai would recognize his son's Reliance not in its businesses but in its behavior: the audacious bets, the vertical integration, the capital market innovation, the political navigation.

The question of whether Reliance can become India's first $1 trillion company isn't just about financial metrics. At current growth rates, assuming successful execution of new energy ventures and continued digital monetization, the arithmetic works. But trillion-dollar valuations require more than growth—they require global relevance. Apple and Microsoft achieved these valuations by creating products the entire world uses. Saudi Aramco got there through resources the world needs. Can Reliance transcend its India-centric model to achieve global scale?

The early indicators are mixed. The company's attempts at international expansion—from the Yemen refinery project to overseas retail ventures—have been modest. The indigenous 5G technology remains unproven for export. The green hydrogen ambitions, while impressive, face global competition from companies with decades of experience. Yet the sheer scale of the Indian market might be enough. If India becomes a $10 trillion economy by 2035, as projected, Reliance's domestic dominance alone could justify trillion-dollar valuations.

The key metrics to watch tell the story of transformation. Jio's Average Revenue Per User (ARPU), currently around ₹195, needs to reach ₹300+ to justify infrastructure investments. Retail revenue per square foot must improve as e-commerce integration deepens. Green hydrogen production costs must achieve the promised $1 per kilogram to make the energy transition viable. The success or failure of these metrics will determine whether Mukesh's final act matches his father's original.

The ultimate question—whether Reliance is a national champion or monopolistic concern—doesn't have a clean answer. It's both. The company has undeniably accelerated India's development, from industrialization through petrochemicals to digitization through Jio. Yet this progress has come with costs: competitor destruction, regulatory capture, and wealth concentration that raises uncomfortable questions about corporate power in a democracy.

India needs companies like Reliance—entities with the scale, capability, and ambition to build infrastructure, compete globally, and drive development. Yet India also needs competition, innovation from startups, and distributed prosperity. The tension between these needs will define not just Reliance's future but India's economic model in the coming decades.

As the next generation—Isha, Akash, and Anant—prepare to take charge, they inherit not just a business empire but a social contract. Their grandfather built Reliance by democratizing capital. Their father built it by democratizing data. What they choose to democratize—or whether they choose concentration over democratization—will determine whether the Reliance story continues for another generation or becomes a cautionary tale about the limits of corporate power.

The boy from Chorwad who started with ₹15,000 created something that transcended business—he created an institution that embodies India's post-independence journey from scarcity to abundance, from isolation to integration, from potential to power. Whether his successors can navigate an India that's increasingly questioning such concentration of power while demanding even more ambitious transformation remains the question that will define Indian capitalism in the 21st century.

XIV. Links & Recent News

Recent News Section:

The latest developments at Reliance Industries continue to reinforce its position at the center of India's economic transformation. Q2 FY2025 consolidated revenue reached ₹2,83,548 crore, with EBITDA of ₹50,367 crore and PAT of ₹22,092 crore, while Jio's subscriber base stood at 506 million with capital expenditure of ₹40,010 crore.

The company's market capitalization tells a story of sustained value creation. Reliance Industries Limited reported a market capitalization of over 20 trillion Indian rupees in fiscal year 2024, making it not just India's most valuable company but a global giant ranked among the world's top 100 corporations by market value.

Strategic partnerships continue to evolve. The November 2024 closure of the Disney-Reliance media merger creates an $8.5 billion entertainment behemoth that will reshape India's content landscape. The Nvidia partnership for AI chips and data center development positions Reliance at the forefront of India's artificial intelligence infrastructure. Meanwhile, the controversial Rosneft oil deal highlights the complex geopolitical balancing act the company must maintain.

The green energy investments are progressing, with the Dhirubhai Ambani Green Energy Giga Complex taking shape in Jamnagar. Early production from solar module manufacturing has begun, though the ambitious targets for cost reduction in green hydrogen remain to be proven at scale.

Links Section:

For investors and analysts seeking deeper insights into Reliance Industries, primary sources remain essential. The company's annual reports, available on the RIL website, provide comprehensive financial and operational data. The quarterly investor presentations offer updated metrics on everything from Jio's ARPU to retail store additions to refining margins.

Books capturing the Reliance story include Hamish McDonald's "The Polyester Prince" (though banned in India, available internationally) and its updated version "Ambani & Sons," which chronicles the family split and its aftermath. Indian authors have produced numerous Telugu, Hindi, and Gujarati biographies of Dhirubhai that capture cultural nuances often missed in English-language accounts.

Regulatory filings with SEBI and the Bombay Stock Exchange provide real-time updates on shareholding patterns, related party transactions, and corporate actions. The Competition Commission of India's orders regarding Reliance's various businesses offer insights into market dominance concerns. Telecom Regulatory Authority of India (TRAI) data helps contextualize Jio's market position and pricing impact.

Industry reports from consultancies like McKinsey, BCG, and Bain frequently feature Reliance as a case study in digital transformation and emerging market strategy. Equity research reports from JM Financial, Morgan Stanley, and Goldman Sachs provide professional investor perspectives on valuation and growth prospects.

Historical interviews, particularly Dhirubhai's rare media appearances and Mukesh's annual AGM speeches, remain valuable for understanding the company's strategic evolution. The 2016 Jio launch speech and the 2021 green energy announcement stand out as defining moments in recent corporate history.

For those interested in the broader context, documentaries on Indian economic liberalization, the telecom revolution, and the rise of Indian conglomerates provide essential background. The Reliance story cannot be understood in isolation—it's inseparable from India's post-independence economic journey, and resources covering that broader narrative add crucial perspective to the company's trajectory.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube